ChronoFlow## ChronoFlow Sentinel

ChronoFlow Sentinel is a regime console that blends normalized fast/mid/slow regression slopes, phases them against a dual-speed EMA spread, and grades alignment so you instantly know whether the time stack is trending, rotating, or fighting itself.

HOW IT WORKS

Multi-Timeframe Slopes – Linear regression slopes are fetched via request.security() for your chosen fast, mid, and slow frames.

Normalized Weighting – User weights are rescaled so the composite chrono score is always on a consistent scale, regardless of configuration.

Phase Differential – The indicator subtracts a slow EMA from a fast EMA to detect whether price impulse confirms the slope mix.

Alignment Score – Signs of the three slopes are compared to compute a 0-1 alignment metric; backgrounds and alerts use this to signal confidence vs. chop.

Diagnostics Console – A bottom-right table streams each slope, the blended score, and which timeframe currently dominates.

HOW TO USE IT

Trend Qualification : Only push multi-contract positions when chrono score is positive, phase is positive, and alignment stays above your alert threshold (default 0.66).

Chop Defense : When alignment dips and conflict markers appear, immediately switch into mean-reversion tactics or sit flat.

Swing + Intraday Bridge : Pair ChronoFlow with other structure tools; require both aligned backgrounds and price confirmation before committing to swing entries.

CRYPTOCAP:SOL | CRYPTOCAP:XRP side by side view with ChronoFlow

VISUAL FEATURES

Optional flow curves: Enable Plot Raw Flows to audit each timeframe's slope when troubleshooting a signal.

Background intensity: Opacity auto-adjusts with alignment, so weak trends look faded while strong regimes glow vividly.

Signal/Conflict toggles: Long/short and chop markers are opt-in, keeping the panel pristine until you need annotations.

Conflict alerts: Built-in alert condition fires whenever alignment falls below your threshold, warning execution layers to scale down risk.

PARAMETERS

Fast Frame (default: 30): Fast timeframe for regression slope calculation.

Mid Frame (default: 120): Mid timeframe for regression slope calculation.

Slow Frame (default: D): Slow timeframe for regression slope calculation.

Fast Regression (default: 21): Regression length for fast timeframe.

Mid Regression (default: 34): Regression length for mid timeframe.

Slow Regression (default: 55): Regression length for slow timeframe.

Phase Length (default: 13): EMA period for phase differential calculation.

Fast Weight (default: 0.45): Influence of the fast timeframe in the composite score.

Mid Weight (default: 0.35): Influence of the mid timeframe in the composite score.

Slow Weight (default: 0.20): Influence of the slow timeframe in the composite score.

Plot Raw Flows (default: disabled): Enable to audit each timeframe's slope when troubleshooting.

Show Signal Labels (default: disabled): Toggle long/short signal markers.

Show Conflict Labels (default: disabled): Toggle conflict/chop markers.

Conflict Alert Level (default: 0.66): Set the alignment threshold that should trigger reduced size or flat positioning.

ALERTS

The indicator includes three alert conditions:

ChronoFlow Bullish: Detected a bullish regime shift

ChronoFlow Bearish: Detected a bearish regime shift

ChronoFlow Conflict: Flagged a low-alignment regime

LIMITATIONS

This indicator requires access to multiple timeframes via request.security() , which may consume additional resources. The alignment score is a simplified metric—real market conditions are more complex than a 0-1 scale can capture. The phase differential calculation assumes EMA spreads are meaningful proxies for momentum, which may not hold in all market regimes. Users should test parameter combinations on their specific instruments and timeframes, as default values are optimized for typical index futures trading.

---

Cerca negli script per "bear"

Volumetric Inverse Fair Value Gap (IFVG) [Kodexius]The Volumetric Inverse Fair Value Gap (IFVG) indicator detects and visualizes inverse fair value gaps (IFVGs) zones where previous inefficiencies in price (fair value gaps) are later invalidated or “inverted.”

Unlike traditional FVG indicators, this tool integrates volume-based analysis to quantify the bullish, bearish, and overall strength of each inversion. It visually represents these metrics within a dynamically updating box on the chart, giving traders deeper insight into market reactions when liquidity imbalances are filled and reversed.

Features

Inverse fair value gap detection

The script identifies bullish and bearish fair value gaps, stores them as pending zones, and turns them into inverse fair value gaps when price trades back through the gap in the opposite direction. Each valid inversion becomes an active IFVG zone on the chart.

Sensitivity control with ATR filter and strict mode

A minimum gap size based on ATR is used to filter out small and noisy gaps. Strict mode can be enabled so that any wick contact between the relevant candles prevents the gap from being accepted as a fair value gap. This lets you decide how clean and selective the zones should be.

Show Last N Boxes control

The indicator can keep only the most recent N IFVG zones visible. Older zones are removed from the chart once the number of active objects exceeds the user setting. This prevents clutter on higher timeframes or long histories and keeps attention on the most relevant recent zones.

Ghost box for the original gap

When the ghost option is enabled, the script draws a faint box that marks the original fair value gap from which the inverse zone came. This makes it easy to see where the initial imbalance appeared and how price later inverted that area.

Volumetric bull, bear and strength metrics

For each IFVG, the script estimates how much of the bar volume is associated with buying and how much with selling, then computes bull percentage, bear percentage and a strength score that uses a percentile rank of volume. These values are stored with the IFVG object and drive the visualization inside the zone.

Three band visual layout inside each IFVG

Each active IFVG is drawn as a container with three horizontal sections. The top band represents the bull percentage, the middle band the bear percentage and the bottom band the strength metric. The width of each bar reflects its respective value so you can read the structure of the zone at a glance.

Customizable colors and label text

Colors for bull, bear, strength, the empty background area, the ghost box and label text can be adjusted in the inputs. This allows you to match the indicator to different chart themes or highlight specific aspects such as strength or direction.

Automatic invalidation and cleanup

When price clearly closes beyond the IFVG in a way that breaks the logic of that zone, the script marks it as inactive and deletes all boxes and labels linked to it. Only valid and active IFVGs remain on the chart, which keeps the display clean and focused.

Calculations

1. Detecting Fair Value Gaps (FVGs)

A fair value gap is identified when price action leaves an imbalance between candle wicks. Depending on the mode:

Bullish FVG: When low > high

Bearish FVG: When high < low

Optionally, the strict mode ensures wicks do not touch.

The gap’s significance is filtered using the ATR multiplier input to exclude minor noise.

Once detected, FVGs are stored as pending zones until inverted by opposite movement (price crossing through).

bool bull_cond = strict_mode ? (low > high ) : (close > high )

bool bear_cond = strict_mode ? (high < low ) : (close < low )

float gap_size = 0.0

if bull_cond and close > open

gap_size := low - high

if bear_cond and close < open

gap_size := low - high

2. Creating IFVGs (Inversions)

When price later moves through a previous FVG in the opposite direction, an Inverse FVG (IFVG) is created.

For example:

A previous bearish FVG becomes bullish IFVG if price moves upward through it.

A previous bullish FVG becomes bearish IFVG if price moves downward through it.

The IFVG is initialized with structural boundaries (top, bottom) and timestamp metadata to anchor visualization.

if not p.is_bull_gap and close > p.top

inverted := true

to_bull := true

if p.is_bull_gap and close < p.btm

inverted := true

to_bull := false

3. Volume Metrics (Bull, Bear, Strength)

Each IFVG calculates buy and sell volumes from the current bar’s price spread and total volume.

Bull % = proportion of upward (buy) volume

Bear % = proportion of downward (sell) volume

Strength % = normalized percentile rank of total volume

These are obtained through a custom function that estimates directional volume contribution:

calc_metrics(float o, float h, float l, float c, float v) =>

float rng = h - l

float buy_v = 0.0

if rng == 0

buy_v := v * 0.5

else

if c >= o

buy_v := v * ((math.abs(c - o) + (math.min(o, c) - l)) / rng)

else

buy_v := v * ((h - math.max(o, c)) / rng)

float sell_v = v - buy_v

float total = buy_v + sell_v

float p_bull = total > 0 ? buy_v / total : 0

float p_bear = total > 0 ? sell_v / total : 0

float p_str = ta.percentrank(v, 100) / 100.0

Strategy: HMA 50 + Supertrend SniperHMA 50 + Supertrend Confluence Strategy (Trend Following with Noise Filtering)

Description:

Introduction and Concept This strategy is designed to solve a common problem in trend-following trading: Lag vs. False Signals. Standard Moving Averages often lag too much, while price action indicators can generate false signals during choppy markets. This script combines the speed of the Hull Moving Average (HMA) with the volatility-based filtering of the Supertrend indicator to create a robust "Confluence System."

The primary goal of this script is not just to overlay two indicators, but to enforce a strict rule where a trade is only taken when Momentum (HMA) and Volatility Direction (Supertrend) are in perfect agreement.

Why this combination? (The Logic Behind the Mashup)

Hull Moving Average (HMA 50): We use the HMA because it significantly reduces lag compared to SMA or EMA by using weighted calculations. It acts as our primary Trend Direction detector. However, HMA can be too sensitive and "whipsaw" during sideways markets.

Supertrend (ATR-based): We use the Supertrend (Factor 3.0, Period 10) as our Volatility Filter. It uses Average True Range (ATR) to determine the significant trend boundary.

How it Works (Methodology) The strategy uses a boolean logic system to filter out low-quality trades:

Bullish Confluence: The HMA must be rising (Slope > 0) AND the Close Price must be above the Supertrend line (Uptrend).

Bearish Confluence: The HMA must be falling (Slope < 0) AND the Close Price must be below the Supertrend line (Downtrend).

The "Choppy Zone" (Noise Filter): This is a unique feature of this script. If the HMA indicates one direction (e.g., Rising) but the Supertrend indicates the opposite (e.g., Downtrend), the market is considered "Choppy" or indecisive. In this state, the script paints the candles or HMA line Gray and exits all positions (optional setting) to preserve capital.

Visual Guide & Signals To make the script easy to interpret for traders who do not read Pine Script, I have implemented specific visual cues:

Green Cross (+): Indicates a LONG entry signal. Both HMA and Supertrend align bullishly.

Red Cross (X): Indicates a SHORT entry signal. Both HMA and Supertrend align bearishly.

Thick Line (HMA): The main line changes color based on the trend.

Green: Bullish Confluence.

Red: Bearish Confluence.

Gray: Divergence/Choppy (No Trade Zone).

Thin Step Line: This is the Supertrend line, serving as your dynamic Trailing Stop Loss.

Strategy Settings

HMA Length: Default is 50 (Mid-term trend).

ATR Factor/Period: Default is 3.0/10 (Standard for trend catching).

Exit on Choppy: A toggle switch allowing users to decide whether to hold through noise or exit immediately when indicators disagree.

Risk Warning This strategy performs best in trending markets (Forex, Crypto, Indices). Like all trend-following systems, it may experience drawdown during prolonged accumulation/distribution phases. Please backtest with your specific asset before using it with real capital.

Bollinger Bands Delta Matrix Analytics [BDMA] Bollinger Bands Delta Matrix Analytics (BDMA) v7.0

Deep Kinetic Engine – 5x8 Volatility & Delta Decision Matrix

1. Introduction & Concept

Bollinger Bands Delta Matrix Analytics (BDMA) v7.0 is an analytical framework that merges:

- Spatial analysis via Bollinger Bands (%B location),

- with a 4-factor Deep Kinetic Engine based on:

• Total Volume

• Buy Volume

• Sell Volume

• Delta (Buy – Sell) Z-Scores

and converts them into an expanded 5×8 decision matrix that continuously tracks where price is trading and how the underlying orderflow is behaving.

BDMA is not a trading system or strategy. It does not generate entry/exit signals.

Instead, it provides a structured contextual map of volatility, volume, and delta so traders can:

- identify climactic extensions vs. fakeouts,

- distinguish strong initiative moves vs. passive absorption,

- and detect squeezes, traps, and liquidity voids with a unified visual dashboard.

2. Spatial Engine – Bollinger S-States (S1–S5)

The spatial dimension of BDMA comes from classic Bollinger Bands.

Price location is expressed as Percent B (%B) and mapped into 5 spatial states (S-States):

S1 – Hyper Extension (Above Upper Band)

Price has pushed beyond the upper Bollinger Band.

Often associated with parabolic or blow-off behavior, late-stage momentum, and elevated reversal risk.

S2 – Resistance Test (Upper Zone)

Price trades in the upper Bollinger region but remains inside the bands.

Represents a sustained test of resistance, typically within an established or emerging uptrend.

S3 – Neutral Zone (Middle)

Price hovers around the mid-band.

This is the mean reversion gravity field where the market often consolidates or transitions between regimes.

S4 – Support Test (Lower Zone)

Price trades in the lower Bollinger region but inside the bands.

Represents a sustained test of support within range or downtrend structures.

S5 – Hyper Drop (Below Lower Band)

Price extends below the lower Bollinger Band.

Often aligned with panic, forced liquidations, or capitulation-type behavior, with increased snap-back risk.

These 5 S-States define the vertical axis (rows) of the BDMA matrix.

3. Deep Kinetic Engine – 4-Factor Z-Score & D-States (D1–D8)

The Deep Kinetic Engine transforms raw volume and delta into standardized Z-Scores to measure how abnormal current activity is relative to its recent history.

For each bar:

- Raw Buy Volume is estimated from the candle’s position within its range

- Raw Sell Volume is complementary to buy volume

- Raw Delta = Buy Volume – Sell Volume

- Total Volume = Buy Volume + Sell Volume

These 4 series are then normalized using a unified Z-Score lookback to produce:

1. Z_Vol_Total – overall activity and liquidity intensity

2. Z_Vol_Buy – aggression from buyers (attack)

3. Z_Vol_Sell – aggression from sellers (defense or attack)

4. Z_Delta – net victory of one side over the other

Thresholds for Extreme, Significant, and Neutral Z-Score levels are fully configurable, allowing you to tune the sensitivity of the kinetic states.

Using Z_Vol_Total and Z_Delta (plus threshold logic), BDMA assigns one of 8 Deep Kinetic states (D-States):

D1 – Climax Buy

Extreme Total Volume + Extreme Positive Delta → Buying climax or blow-off behavior.

D2 – Strong Buy

High Volume + High Positive Delta → Confirmed bullish initiative activity.

D3 – Weak Buy / Fakeout

Low Volume + High Positive Delta → Bullish delta without commitment, low-liquidity breakout risk.

D4 – Absorption / Conflict

High Volume + Neutral Delta → Aggressive two-way trade, strong absorption, war zone behavior.

D5 – Neutral

Low Volume + Neutral Delta → Low-energy environment with low conviction.

D6 – Weak Sell / Fakeout

Low Volume + High Negative Delta → Bearish delta without commitment, low-liquidity breakdown risk.

D7 – Strong Sell

High Volume + High Negative Delta → Confirmed bearish initiative activity.

D8 – Capitulation

Extreme Volume + Extreme Negative Delta → Panic selling or capitulation regime.

These 8 D-States define the horizontal axis (columns) of the BDMA matrix.

4. The 5×8 BDMA Decision Matrix

The core of BDMA is a 5×8 matrix where:

- Rows (1–5) = Spatial S-States (S1…S5)

- Columns (1–8) = Kinetic D-States (D1…D8)

Each of the 40 possible combinations (SxDy) is pre-computed and mapped to:

- a Status or Regime Title (for example: Climax Breakout, Bear Trap Spring, Capitulation Breakdown),

- a Bias (Climactic Bull, Neutral, Strong Bear, Conflict or Reversal Risk, and similar labels),

- and a Strategic Signal or Consideration (for example: High reversal risk, Wait for confirmation, Low probability zone – avoid).

Internally, BDMA resolves all 40 regimes so the current state can be displayed on the dashboard without performance overhead.

5. Key Regime Families (How to Read the Matrix)

5.1. Breakouts and Breakdowns

Climax Breakout (Top-side)

Spatial S1 with Kinetic D1 or D2

Bias: Explosive or Extreme Bull

Signal:

- Strong or climactic upside extension with abnormal bullish orderflow.

- Trend continuation is possible, but reversal risk is extremely high after blow-off phases.

Low-Conviction Breakout (Fakeout Risk)

S1 with D3 (Weak Buy, low liquidity)

Bias: Weak Bull – Caution

Signal:

- Breakout not supported by volume.

- Elevated risk of failed auction or bull trap.

Capitulation Breakdown (Bottom-side)

Spatial S5 with Kinetic D8

Bias: Climactic Bear (panic)

Signal:

- Capitulation-type selling or forced liquidations.

- Trend can still proceed, but snap-back or violent short-covering risk is high.

Initiative Breakdown vs. Weak Breakdown

- Strong, high-volume breakdown typically corresponds to D7 (Strong Sell).

- Low-volume breakdown often corresponds to D6 (Weak Sell or Fakeout) with potential for failure.

5.2. Absorption, Traps and Springs

Absorption at Resistance (Top-side conflict)

S1 or S2 with D4 (Absorption or Conflict)

Bias: Conflict – Extreme Tension

Signal:

- Heavy two-way trade near resistance.

- Potential distribution or reversal if sellers begin to dominate.

Bull Trap or Failed Auction

Typically S1 with D6 (Weak Sell breakdown behavior after a top-side attempt)

Indicates a breakout attempt that fails and reverses, often after poor liquidity structure.

Absorption at Support and Bear Trap (Spring)

S4 or S5 with D4 or D3

Bias: Conflict or Weak Bear – Reversal Risk

Signal:

- Aggressive buying into lows (spring or shakeout behavior).

- Potential bear trap if price reclaims lost territory.

5.3. Trend Phases

Strong Uptrend Phases

Typically seen when S2–S3 combine with strong bullish kinetic behavior.

Bias: Strong or Extreme Bull

Signal:

- Pullbacks into S3 or S4 with supportive kinetic states often act as trend continuation zones.

Strong Downtrend Phases

Typically seen when S3–S4 combine with strong bearish kinetic behavior.

Bias: Strong or Extreme Bear

Signal:

- Rallies into resistance with strong bearish kinetic backing may act as continuation sell zones.

5.4. Neutral, Exhaustion and Squeeze

Exhaustion or Liquidity Void

S1 or S5 with D5 (Neutral kinetics)

Bias: Neutral or Exhaustion

Signal:

- Spatial extremes without kinetic confirmation.

- Often marks the end of a move, with poor follow-through.

Choppy, Low-Activity Range

S3 with D5

Bias: Neutral

Signal:

- Low volume, low conviction market.

- Typically a low-probability environment where standing aside can be logical.

Squeeze or High-Tension Zone

S3 with D4 or tightly clustered kinetic values

Bias: Conflict or High Tension

Signal:

- Hidden battle inside a volatility contraction.

- Often precedes large directionally-biased moves.

6. Dashboard Layout & Reading Guide

When Show Dashboard is enabled, BDMA displays:

1. Title and Status Line

Name of the current regime (for example: Climax Breakout, Bear Trap Spring, Mean Reversion).

2. Bias Line

Plain-language summary of directional context such as Climactic Bull, Strong Bear, Neutral, or Conflict and Reversal Risk.

3. Signal or Strategic Notes

Concise guidance focused on risk and context, not entries. For example:

- High reversal risk – aggressive traders only

- Wait for confirmation (break or rejection)

- Low probability zone – avoid taking new positions

4. Kinetic Profile (4-Factor Z-Score)

Shows the current Z-Scores for Total Volume (Activity), Buy Volume (Attack), Sell Volume (Defense), and Delta (Net Result).

5. Matrix Heatmap (5×8)

Visual representation of S-State vs. D-State with color coding:

- Bullish clusters in a green spectrum

- Bearish clusters in a red spectrum

- Conflict or exhaustion zones in yellow, amber, or neutral tones

The dashboard can be repositioned (top right, middle right, or bottom right) and its size can be adjusted (Tiny, Small, Normal, or Large) to fit different layouts.

7. Inputs & Customization

7.1. Core Parameters (Bollinger and Z-Score)

- Bollinger Length and Standard Deviation define the spatial engine.

- Z-Score Lookback (All Factors) defines how many bars are used to normalize volume and delta.

7.2. Deep Kinetic Thresholds

- Extreme Threshold defines what is considered climactic (D1 or D8).

- Significant Threshold distinguishes strong initiative vs. weak or fakeout behavior.

- Neutral Threshold is the band within which delta is treated as neutral.

These thresholds allow you to tune the sensitivity of the kinetic classification to fit different timeframes or instruments.

7.3. Calculation Method (Volume Delta)

Geometry (Approx)

- Fast, non-repainting approach based on candle geometry.

- Suitable for most users and real-time decision-making.

Intrabar (Precise)

- Uses lower-timeframe data for more precise volume delta estimation.

- Intrabar mode can repaint and requires compatible data and plan support on the platform.

- Best used for post-analysis or research, not blind automation.

7.4. Visuals and Interface

- Toggle Bollinger Bands visibility on or off.

- Switch between Dark and Light color themes.

- Configure dashboard visibility, matrix heatmap display, position, and size.

8. Multi-Language Semantic Engine (Asia and Middle East Focus)

BDMA v7.0 includes a fully integrated multi-language layer, targeting a wide geographic user base.

Supported Languages:

English, Türkçe, Русский, 简体中文, हिन्दी, العربية, فارسی, עברית

All dashboard labels, regime titles, bias descriptions, and signal texts are dynamically translated via an internal dictionary, while semantic meaning is kept consistent across languages.

This makes BDMA suitable for multi-language communities, study groups, and educational content across different regions.

However, due to the heavy computational load of the Deep Kinetic Engine and TradingView’s strict Pine Script execution limits, it was not possible to expand support to additional languages. Adding more translation layers would significantly increase memory usage and exceed runtime constraints. For this reason, the current language set represents the maximum optimized configuration achievable without compromising performance or stability.

9. Practical Usage Notes

BDMA is most powerful when used as a contextual overlay on top of market structure (HH, HL, LH, LL), higher-timeframe trend, key levels, and your own execution framework.

Recommended usage:

- Identify the current regime (Status and Bias).

- Check whether price location (S-State) and kinetic behavior (D-State) agree with your trade idea.

- Be especially cautious in climactic and absorption or conflict zones, where volatility and risk can be elevated.

Avoid treating BDMA as an automatic green equals buy, red equals sell tool.

The real edge comes from understanding where you are in the volatility or kinetic spectrum, not from forcing signals out of the matrix.

10. Limitations & Important Warnings

BDMA does not predict the future.

It organizes current and recent data into a structured context.

Volume data quality depends on the underlying symbol, exchange, and broker feed.

Forex, crypto, indices, and stocks may all behave differently.

Intrabar mode can repaint and is sensitive to lower-timeframe data availability and your plan type.

Use it with extra caution and primarily for research.

No indicator can remove the need for clear trading rules, disciplined risk management, and psychological control.

11. Disclaimer

This script is provided strictly for educational and analytical purposes.

It is not a trading system, signal service, financial product, or investment advice.

Nothing in this indicator or its description should be interpreted as a recommendation to buy or sell any asset.

Past behavior of any indicator or market pattern does not guarantee future results.

Trading and investing involve significant risk, including the risk of losing more than your initial capital in leveraged products.

You are solely responsible for your own decisions, risk management, and results.

By using this script, you acknowledge that you understand these risks and agree that the author or authors and publisher or publishers are not liable for any loss or damage arising from its use.

Smart Money Concepts [Modern Neon V2]This is a visually overhauled version of the popular Smart Money Concepts (SMC) indicator, designed specifically for traders who prefer Dark Mode, High Contrast, and Maximum Visibility.

While the underlying logic preserves the robust structure detection of the original LuxAlgo script, the visual presentation has been completely modernized. The default "dull" colors have been replaced with a vibrant Cyberpunk Neon palette, and text labels have been significantly upscaled to ensure market structure is readable at a glance, even on high-resolution monitors.

🎨 Visual & Style Enhancements:

Neon Palette:

Bullish: Electric Cyan (#00F5FF)

Bearish: Neon Hot Pink (#FF007F)

Neutral/Levels: Bright Gold (#FFD700)

High Visibility Text: Market Structure labels (BOS, CHoCH, HH/LL) have been upgraded from "Tiny" to Normal size. Key Swing Points (Strong High/Low) are set to Large.

Modern "Solid" Blocks: Order Blocks and FVGs feature reduced transparency (60%) for a bolder, solid look that doesn't get washed out on dark backgrounds.

Decluttered: Removed unnecessary "Small" elements and dotted lines to focus on price action.

🛠 Key Features:

Real-Time Structure: Automatic detection of Internal and Swing structure (BOS & CHoCH) with trend coloring.

Order Blocks: Highlights Bullish and Bearish Order Blocks with new mitigation logic.

Fair Value Gaps (FVG): Auto-threshold detection for high-probability gaps.

Premium & Discount Zones: Automatically plots equilibrium zones for better entry targeting.

Multi-Timeframe Levels: Display Daily, Weekly, and Monthly highs/lows.

Trend Dashboard: (If you added the dashboard code) A clean panel displaying the current Internal and Swing trend bias.

CREDITS & LICENSE: This script is a modification of the "Smart Money Concepts " indicator.

Original Author: © LuxAlgo

License: Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0)

creativecommons.org

Relative Strength Heatmap [BackQuant]Relative Strength Heatmap

A multi-horizon RSI matrix that compresses 20 different lookbacks into a single panel, turning raw momentum into a visual “pressure gauge” for overbought and oversold clustering, trend exhaustion, and breadth of participation across time horizons.

What this is

This indicator builds a strip-style heatmap of 20 RSIs, each with a different length, and stacks them vertically as colored tiles in a single pane. Every tile is colored by its RSI value using your chosen palette, so you can see at a glance:

How many “fast” versus “slow” RSIs are overbought or oversold.

Whether momentum is concentrated in the short lookbacks or spread across the whole curve.

When momentum extremes cluster, signalling strong market pressure or exhaustion.

On top of the tiles, the script plots two simple breadth lines:

A white line that counts how many RSIs are above 70 (overbought cluster).

A black line that counts how many RSIs are below 30 (oversold cluster).

This turns a single symbol’s RSI ladder into a compact “market pressure gauge” that shows not only whether RSI is overbought or oversold, but how many different horizons agree at the same time.

Core idea

A single RSI looks at one length and one timescale. Markets, however, are driven by flows that operate on multiple horizons at once. By computing RSI over a ladder of lengths, you approximate a “term structure” of strength:

Short lengths react to immediate swings and very recent impulses.

Medium lengths reflect swing behaviour and local trends.

Long lengths reflect structural bias and higher timeframe regime.

When many lengths agree, for example 10 or more RSIs all above 70, it suggests broad participation and strong directional pressure. When only a few fast lengths stretch to extremes while longer ones stay neutral, the move is more fragile and more likely to mean-revert.

This script makes that structure visible as a heatmap instead of forcing you to run many separate RSI panes.

How it works

1) Generating RSI lengths

You control three parameters in the calculation settings:

RS Period – the base RSI length used for the shortest strip.

RSI Step – the amount added to each successive RSI length.

RSI Multiplier – a global scaling factor applied after the step.

Each of the 20 RSIs uses:

RSI length = round((base_length + step × index) × multiplier) , where the index goes from 0 to 19.

That means:

RSI 1 uses (len + step × 0) × mult.

RSI 2 uses (len + step × 1) × mult.

…

RSI 20 uses (len + step × 19) × mult.

You can keep the ladder dense (small step and multiplier) or stretch it across much longer horizons.

2) Heatmap layout and grouping

Each RSI is plotted as an “area” strip at a fixed vertical level using histbase to stack them:

RSI 1–5 form Group 1.

RSI 6–10 form Group 2.

RSI 11–15 form Group 3.

RSI 16–20 form Group 4.

Each group has a toggle:

Show only Group 1 and 2 if you care mainly about fast and medium horizons.

Show all groups for a full spectrum from very short to very long.

Hide any group that feels redundant for your workflow.

The actual numeric RSI values are not plotted as lines. Instead, each strip is drawn as a horizontal band whose fill color represents the current RSI regime.

3) Palette-based coloring

Each tile’s color is driven by the RSI value and your chosen palette. The script includes several palettes:

Viridis – smooth green to yellow, good for subtle reading.

Jet – strong blue to red sequence with high contrast.

Plasma – purple through orange to yellow.

Custom Heat – cool blues to neutral grey to hot reds.

Gray – grayscale from white to black for minimalistic layouts.

Cividis, Inferno, Magma, Turbo, Rainbow – additional scientific and rainbow-style maps.

Internally, RSI values are bucketed into ranges (for example, below 10, 10–20, …, 90–100). Each bucket maps to a unique colour for that palette. In all schemes, low RSI values are mapped to the “cold” or darker side and high RSI values to the “hot” or brighter side.

The result is a true momentum heatmap:

Cold or dark tiles show low RSI and oversold or compressed conditions.

Mid tones show neutral or mid-range RSI.

Warm or bright tiles show high RSI and overbought or stretched conditions.

4) Bull and bear breadth counts

All 20 RSI values are collected into an array each bar. Two counters are then calculated:

Bull count – how many RSIs are above 70.

Bear count – how many RSIs are below 30.

These are plotted as:

A white line (“RSI > 70 Count”) for the overbought cluster.

A black line (“RSI < 30 Count”) for the oversold cluster.

If you enable the “Show Bull and Bear Count” option, you get an immediate reading of how many of the 20 horizons are stretched at any moment.

5) Cluster alerts and background tagging

Two alert conditions monitor “strong cluster” regimes:

RSI Heatmap Strong Bull – triggers when at least 10 RSIs are above 70.

RSI Heatmap Strong Bear – triggers when at least 10 RSIs are below 30.

When one of these conditions is true, the indicator can tint the background of the chart using a soft version of the current palette. This visually marks stretches where momentum is extreme across many lengths at once, not just on a single RSI.

What it plots

In one oscillator window, the indicator provides:

Up to 20 horizontal RSI strips, each representing a different RSI length.

Color-coded tiles reflecting the current RSI value for each length.

Group toggles to show or hide each block of five RSIs.

An optional white line that counts how many RSIs are above 70.

An optional black line that counts how many RSIs are below 30.

Optional background highlights when the number of overbought or oversold RSIs passes the strong-cluster threshold.

How it measures breadth and pressure

Single-symbol breadth

Breadth is usually defined across a basket of symbols, such as how many stocks advance versus decline. This indicator uses the same concept across time horizons for a single symbol. The question becomes:

“How many different RSI lengths are stretched in the same direction at once?”

Examples:

If only 2 or 3 of the shortest RSIs are above 70, bull count stays low. The move is fast and local, but not yet broadly supported.

If 12 or more RSIs across short, medium and long lengths are above 70, the bull count spikes. The move has broad momentum and strong upside pressure.

If 10 or more RSIs are below 30, bear count spikes and you are in a broad oversold regime.

This is breadth of momentum within one market.

Market pressure gauge

The combination of heatmap tiles and breadth lines acts as a pressure gauge:

High bull count with warm colors across most strips indicates strong upside pressure and crowded long positioning.

High bear count with cold colors across most strips indicates strong downside pressure and capitulation or forced selling.

Low counts with a mixed heatmap indicate neutral pressure, fragmented flows, or range-bound conditions.

You can treat the strong-cluster alerts as “extreme pressure” signals. When they fire, the market is heavily skewed in one direction across many horizons.

How to read the heatmap

Horizontal patterns (through time)

Look along the time axis and watch how the colors evolve:

Persistent hot tiles across many strips show sustained bullish pressure and trend strength.

Persistent cold tiles across many strips show sustained bearish pressure and weak demand.

Frequent flipping between hot and cold colours indicates a choppy or mean-reverting environment.

Vertical structure (across lengths at one bar)

Focus on a single bar and read the column of tiles from top to bottom:

Short RSIs hot, long RSIs neutral or cool: early trend or short-term fomo. Price has moved fast, longer horizons have not caught up.

Short and long RSIs all hot: mature, entrenched uptrend. Broad participation, high pressure, greater risk of blow-off or late-entry vulnerability.

Short RSIs cold but long RSIs mid to high: pullback in a higher timeframe uptrend. Dip-buy and continuation setups are often found here.

Short RSIs high but long RSIs low: countertrend rallies within a broader downtrend. Good hunting ground for fades and short entries after a bounce.

Bull and bear breadth lines

Use the two lines as simple, numeric breadth indicators:

A rising white line shows more RSIs pushing above 70, so bullish pressure is expanding in breadth.

A rising black line shows more RSIs pushing below 30, so bearish pressure is expanding in breadth.

When both lines are low and flat, few horizons are extreme and the market is in mid-range territory.

Cluster zones

When either count crosses the strong threshold (for example 10 out of 20 RSIs in extreme territory):

A strong bull cluster marks a broadly overbought regime. Trend followers may see this as confirmation. Mean-reversion traders may see it as a late-stage or blow-off context.

A strong bear cluster marks a broadly oversold regime. Downtrend traders see strong pressure, but the risk of sharp short-covering bounces also increases.

Trading applications

Trend confirmation

Use the heatmap and breadth lines as a trend filter:

Prefer long setups when the heatmap shows mostly mid to high RSIs and the bull count is rising.

Avoid fresh shorts when there is a strong bull cluster, unless you are specifically trading exhaustion.

Prefer short setups when the heatmap is mostly low RSIs and the bear count is rising.

Avoid aggressive longs when a strong bear cluster is active, unless you are trading reflexive bounces.

Mean-reversion timing

Treat cluster extremes as exhaustion zones:

Look for reversal patterns, failed breakouts, or order flow shifts when bull count is very high and price starts to stall or diverge.

Look for reflexive bounce potential when bear count is very high and price stops making new lows or shows absorption at the lows.

Use the palette and counts together: hot tiles plus a peaking white line can mark blow-off conditions, cold tiles plus a peaking black line can mark capitulation.

Regime detection and risk toggling

Use the overall shape of the ladder over time:

If upper strips stay warm and lower strips stay neutral or warm for extended periods, the market is in an uptrend regime. You can justify higher risk for long-biased strategies.

If upper strips stay cold and lower strips stay neutral or cold, the market is in a downtrend regime. You can justify higher risk for short-biased strategies or defensive positioning.

If colours and counts flip frequently, you are likely in a range or choppy regime. Consider reducing size or using more tactical, short-term strategies.

Multi-horizon synchronization

You can think of each RSI length as a proxy for a different “speed” of the same market:

When only fast RSIs are stretched, the move is local and less robust.

When fast, medium and slow RSIs align, the move has multi-horizon confirmation.

You can require a minimum bull or bear count before allowing your main strategy to engage.

Spotting hidden shifts

Sometimes price appears flat or drifting, but the heatmap quietly cools or warms:

If price is sideways while many hot tiles fade toward neutral, momentum is decaying under the surface and trend risk is increasing.

If price is sideways while many cold tiles climb back toward neutral, selling pressure is decaying and the tape is repairing itself.

Settings overview

Calculation Settings

RS Period – base RSI length for the shortest strip.

RSI Step – the increment added to each successive RSI length.

RSI Multiplier – scales all generated RSI lengths.

Calculation Source – the input series, such as close, hlc3 or others.

Plotting and Coloring Settings

Heatmap Color Palette – choose between Viridis, Jet, Plasma, Custom Heat, Gray, Cividis, Inferno, Magma, Turbo or Rainbow.

Show Group 1 – toggles RSI 1–5.

Show Group 2 – toggles RSI 6–10.

Show Group 3 – toggles RSI 11–15.

Show Group 4 – toggles RSI 16–20.

Show Bull and Bear Count – enables or disables the two breadth lines.

Alerts

RSI Heatmap Strong Bull – fires when the number of RSIs above 70 reaches or exceeds the configured threshold (default 10).

RSI Heatmap Strong Bear – fires when the number of RSIs below 30 reaches or exceeds the configured threshold (default 10).

Tuning guidance

Fast, tactical configurations

Use a small base RS Period, for example 2 to 5.

Use a small RSI Step, for tight clustering around the fast horizon.

Keep the multiplier near 1.0 to avoid extreme long lengths.

Focus on Group 1 and Group 2 for intraday and short-term trading.

Swing and position configurations

Use a mid-range RS Period, for example 7 to 14.

Use a moderate RSI Step to fan out into slower horizons.

Optionally use a multiplier slightly above 1.0.

Keep all four groups enabled for a full view from fast to slow.

Macro or higher timeframe configurations

Use a larger base RS Period.

Use a larger RSI Step so the top of the ladder reaches very slow lengths.

Focus on Group 3 and Group 4 to see structural momentum.

Treat clusters as regime markers rather than frequent trading signals.

Notes

This indicator is a contextual tool, not a standalone trading system. It does not model execution, spreads, slippage or fundamental drivers. Use it to:

Understand whether momentum is narrow or broad across horizons.

Confirm or filter existing signals from your primary strategy.

Identify environments where the market is crowded into one side.

Distinguish between isolated spikes and truly broad pressure moves.

The Relative Strength Heatmap is designed to answer a simple but powerful question:

“How many versions of RSI agree with what I am seeing on the chart?”

By compressing those answers into a single panel with clear colour coding and breadth lines, it becomes a practical, visual gauge of momentum breadth and market pressure that you can overlay on any trading framework.

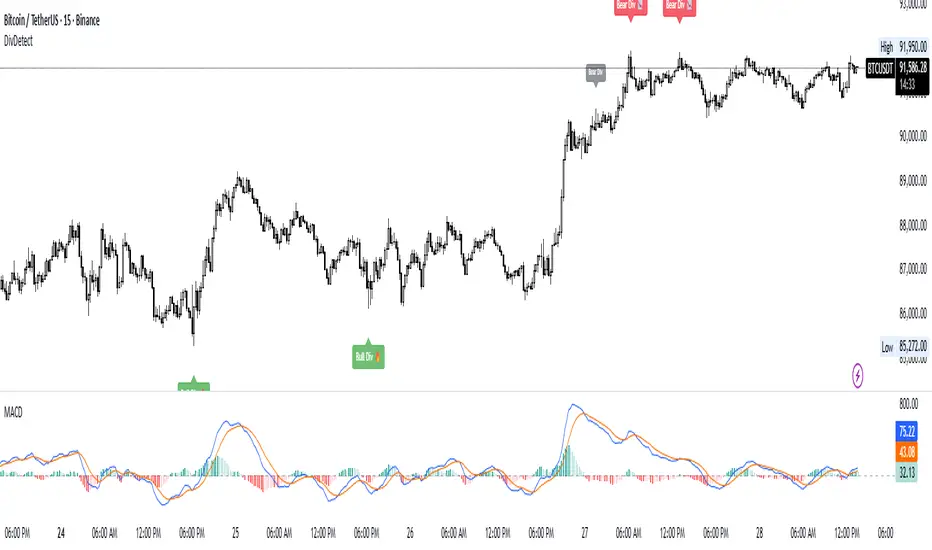

Divergence Detector (MACD + Volume)Divergence Detector (MACD + Volume Confirmation)

This indicator automatically detects bullish and bearish divergences between price and MACD, enhanced with volume confirmation to filter out weak signals.

🔹 Core Logic

Pivot Detection:

The script identifies swing highs and lows (pivots) using customizable left/right lookback values.

Bullish Divergence:

Occurs when price makes a lower low, but MACD makes a higher low.

A label "Bull Div" appears below the bar; if confirmed by high volume, it shows "Bull Div 🔥".

Bearish Divergence:

Occurs when price makes a higher high, but MACD makes a lower high.

A label "Bear Div" appears above the bar; if confirmed by high volume, it shows "Bear Div 📉".

Volume Confirmation:

The indicator checks whether the volume at the pivot bar is above the moving average of volume (customizable length).

This ensures that divergence signals are backed by strong market participation.

Inputs

MACD Fast/Slow/Signal Length – standard MACD parameters

Pivot Lookback Left/Right – defines the swing structure sensitivity

Volume MA Length – defines how volume strength is validated

Output

Labels:

🔹 Bull Div / Bull Div 🔥 → Bullish divergence (confirmed with volume)

🔹 Bear Div / Bear Div 📉 → Bearish divergence (confirmed with volume)

Tips

Works best on higher timeframes and trending markets.

Volume confirmation helps filter false divergences in low liquidity conditions.

Combine with trend or structure indicators for better trade setups.

----------------------------------------------------------------------------------------------

اندیکاتور شناسایی واگرایی MACD با تأیید حجم

این اندیکاتور بهصورت خودکار واگراییهای صعودی و نزولی بین قیمت و MACD را شناسایی کرده و با استفاده از تأیید حجم (Volume Confirmation) سیگنالهای ضعیف را فیلتر میکند.

🔹 منطق عملکرد

شناسایی پیوتها:

نقاط چرخش (سقف و کف) با استفاده از تعداد کندلهای قابل تنظیم در دو سمت شناسایی میشوند.

واگرایی صعودی (Bullish):

زمانی که قیمت کف پایینتر و MACD کف بالاتر میسازد.

برچسب "Bull Div" در زیر کندل نمایش داده میشود؛ اگر حجم بالا باشد، با علامت 🔥 مشخص میگردد.

واگرایی نزولی (Bearish):

زمانی که قیمت سقف بالاتر و MACD سقف پایینتر میسازد.

برچسب "Bear Div" در بالای کندل نمایش داده میشود؛ اگر حجم بالا باشد، با 📉 مشخص میگردد.

تأیید حجم:

اگر حجم در کندل پیوت بالاتر از میانگین متحرک حجم باشد، سیگنال معتبرتر در نظر گرفته میشود.

تنظیمات ورودی

تنظیمات MACD (Fast, Slow, Signal)

پارامترهای شناسایی پیوت (Left / Right)

طول میانگین متحرک حجم (Volume MA Length)

خروجیها

Bull Div 🔥 / Bear Div 📉 برای واگراییهای تأییدشده با حجم

Bull Div / Bear Div برای واگراییهای بدون تأیید حجم

نکات کاربردی

بهترین عملکرد در تایمفریمهای بالا و بازارهای دارای روند

تأیید حجم به حذف سیگنالهای اشتباه در شرایط حجم پایین کمک میکند

برای دقت بیشتر، آن را با اندیکاتورهای روند یا ساختار ترکیب کنید

⚠️ Disclaimer:

This script is provided for educational and informational purposes only.

It does not constitute financial advice, and the author is not responsible for any financial losses caused by its use.

Always confirm signals with your own analysis and other tools before making trading decisions.

⚠️ توجه:

این اسکریپت صرفاً جهت آموزش و اطلاعرسانی طراحی شده و توصیه مالی یا سرمایهگذاری محسوب نمیشود.

نویسنده مسئول هیچگونه ضرر یا زیان احتمالی ناشی از استفاده از آن نیست.

لطفاً پیش از هر تصمیم معاملاتی، تحلیل شخصی خود را انجام داده و از این ابزار در کنار سایر ابزارهای تحلیل و مدیریت ریسک استفاده کنید.

Volume Gaps & Imbalances (Zeiierman)█ Overview

Volume Gaps & Imbalances (Zeiierman) is an advanced market-structure and order-flow visualizer that maps where the market traded, where it did not, and how buyer-vs-seller pressure accumulated across the entire price range.

The core of the indicator is a price-by-price volume profile built from Bullish and Bearish volume assignments. The script highlights:

True zero-volume voids (regions of no traded volume)

Bull/Bear imbalance rows (horizontal volume slices)

A multi-section Delta Panel, showing aggregated Buy–Sell pressure per vertical sector

A clean separation between profile structure, volume efficiency, and delta flows

Together, these components reveal market inefficiencies, displacement zones, and fair-value regions that price tends to revisit — making it an exceptional tool for structural trading, order-flow analysis, and contextual confluence.

Highlights

Identifies true volume voids (untraded price regions), more precisely than standard FVG tools

Plots Bull vs Bear volume at each price row for fine-grained imbalance reading

Includes a sector-based Delta Grid that aggregates Buy–Sell dominance

█ How It Works

⚪ Profile Construction

The indicator scans a user-defined Lookback window and divides the full high–low range into Rows. Each bar's volume is allocated into the correct price bucket:

Bullish volume when close > open

Bearish volume when close <= open

This produces three values per price level:

Bull Volume

Bear Volume

Total Volume & Imbalance Profile

Rows where no volume at all occurred are marked as volume gaps — signaling true untraded zones, often produced by impulsive imbalanced moves.

⚪ Zero-Volume Gaps (True Voids)

Unlike candle-based Fair Value Gaps (FVGs), volume gaps identify the deeper, structural inefficiency: Price moved so fast through a region that no trades occurred at those prices. These areas often attract revisits because liquidity never exchanged hands there.

⚪ Bull/Bear Volume Imbalance

Every price row is drawn using two colored horizontal segments:

Bull segment proportional to bullish volume

Bear segment proportional to bearish volume

This reveals where buyers or sellers dominated individual price levels.

⚪ Delta Panel

The full volume profile is cut into Summary Sections. For each block, the script computes: Δ = (Bull Volume − Bear Volume) ÷ Total Volume × 100%

█ How to Use

⚪ Spot True Voids & Inefficiencies

Zero-volume zones highlight where the price moved without trading. These areas often behave like:

Refill zones during retracements

Targets during displacement

Thin regions price slices through quickly

Ideal for both SMC-style trading and structural mapping.

⚪ Identify Bull/Bear Control at Each Price Level

Broad bullish segments show zones of buyer absorption, while wide bearish slices reveal seller control.

This helps you interpret:

Where buyers supported the price

Where sellers defended a level

Which price levels matter for continuation or reversal

⚪ Use Delta Sectors for Contextual Direction

The delta panel shows where market pressure is accumulating, revealing whether the profile is dominated by:

Bullish flow (positive delta)

Bearish flow (negative delta)

Neutral flow (balanced or minimal delta)

█ Settings

Lookback – Number of bars scanned to build the profile.

Rows – Vertical resolution of price bins.

Source – Price source used to assign volume into rows.

Summary Sections – Number of vertical delta sectors.

Summary Width – Horizontal size of the delta bar panel.

Gap From Profile – Distance between profile and delta grid.

Show Delta Text – Toggle Δ% labels.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

ULTIMATE ORDER FLOW SYSTEM🔥 ULTIMATE ORDER FLOW SYSTEM

Overview

This comprehensive order flow analysis tool combines **Volume Profile**, **Cumulative Delta**, and **Large Order Detection** to identify high-probability trading setups. The script analyzes institutional order flow patterns and volume distribution to pinpoint key levels where price is likely to react.

📊 Core Components & Methodology

🔥 ULTIMATE ORDER FLOW SYSTEM

Overview

This comprehensive order flow analysis tool combines Volume Profile, Cumulative Delta, and Large Order Detection to identify high-probability trading setups. The script analyzes institutional order flow patterns and volume distribution to pinpoint key levels where price is likely to react.

________________________________________

📊 Core Components & Methodology

1. Volume Profile Analysis

The script constructs a horizontal volume profile by:

• Dividing the price range into configurable rows (default: 20)

• Accumulating volume at each price level over a lookback period (default: 50 bars)

• Separating buy volume (green bars close > open) from sell volume (red bars)

• Identifying three critical levels:

o POC (Point of Control): Price level with highest traded volume - acts as a strong magnet

o VAH/VAL (Value Area High/Low): Contains 70% of total volume - defines fair value zone

o HVN (High Volume Nodes): Resistance zones where institutions accumulated positions

o LVN (Low Volume Nodes): Thin zones that price moves through quickly - ideal targets

Why This Matters: Institutional traders leave footprints through volume. HVN zones show where large players defended levels, making them reliable support/resistance.

________________________________________

2. Cumulative Delta (Order Flow)

Tracks the running total of buying vs selling pressure:

• Bar Delta: Difference between buy and sell volume per candle

• Cumulative Delta: Sum of all bar deltas - shows net directional pressure

• Delta Moving Average: Smoothed delta (20-period) to identify trend

• Delta Divergences:

o Bullish: Price makes lower low, but delta makes higher low (absorption at bottom)

o Bearish: Price makes higher high, but delta makes lower high (exhaustion at top)

How It Works: When cumulative delta trends up while price consolidates, it signals accumulation. Delta divergences reveal when smart money is positioned opposite to retail expectations.

________________________________________

3. Large Order Detection

Identifies institutional-sized orders in real-time:

• Compares current bar volume to 20-period moving average

• Flags orders exceeding 2.5x average volume (configurable multiplier)

• Distinguishes bullish (green circles below) vs bearish (red circles above) large orders

Rationale: Sudden volume spikes at key levels indicate institutional participation - the "fuel" needed for breakouts or reversals.

________________________________________

🎯 Trading Signal Logic

Combined Setup Criteria

The script generates SHORT and LONG signals when multiple conditions align:

SHORT Signal Requirements:

1. Price reaches an HVN resistance zone (within 0.2%)

2. Large sell order detected (volume spike + red candle)

3. Cumulative delta is bearish OR bearish divergence present

4. 10-bar cooldown between signals (prevents overtrading)

LONG Signal Requirements:

1. Price reaches an HVN support zone

2. Large buy order detected (volume spike + green candle)

3. Cumulative delta is bullish OR bullish divergence present

4. 10-bar cooldown enforced

________________________________________

🔧 Customization Options

Setting - Purpose - Recommendation

Volume Profile Rows - Granularity of level detection - 20 (balanced)

Lookback Period - Historical data analyzed - 50 bars (intraday), 200 (swing)

Large Order Multiplier - Sensitivity to volume spikes - 2.5x (standard), 3.5x (conservative)

HVN Threshold - Resistance zone detection - 1.3 (default)

LVN Threshold - Target zone identification - 0.6 (default)

Divergence Lookback - Pivot detection period - 5 bars (responsive)

________________________________________

📈 Dashboard Indicators

The real-time panel displays:

• POC: Current Point of Control price

• Location: Whether price is at HVN resistance

• Orders: Current large buy/sell activity

• Cumulative Δ: Net order flow value + trend direction

• Divergence: Active bullish/bearish divergences

• Bar Strength: % of candle volume that's directional (>65% = strong)

• SETUP: Current trade signal (LONG/SHORT/WAIT)

________________________________________

🎨 Visual System

• Yellow POC Line: Highest volume level - primary pivot

• Blue Value Area Box: Fair value zone (VAH to VAL)

• Red HVN Zones: Resistance/support from institutional accumulation

• Green LVN Zones: Low-liquidity targets for quick moves

• Volume Bars: Green (buy pressure) vs Red (sell pressure) distribution

• Triangles: LONG (green up) and SHORT (red down) entry signals

• Diamonds: Divergence warnings (cyan=bullish, fuchsia=bearish)

________________________________________

💡 How This Script Is Unique

Unlike standalone volume profile or delta indicators, this script:

1. Synthesizes three complementary methods - volume structure, order flow momentum, and liquidity detection

2. Requires multi-factor confirmation - signals only trigger when price, volume, and delta align at key zones

3. Adapts to market regime - delta filters ensure you're trading with the dominant order flow direction

4. Provides context, not just signals - the dashboard helps you understand why a setup is forming

________________________________________

⚙️ Best Practices

Timeframes:

• 5-15 min: Scalping (use 30-50 bar lookback)

• 1-4 hour: Swing trading (use 100-200 bar lookback)

Risk Management:

• Enter on signal candle close

• Stop loss: Beyond nearest HVN/LVN zone

• Target 1: Next LVN level

• Target 2: Opposite value area boundary

Filters:

• Avoid signals during major news events

• Require bar delta strength >65% for aggressive entries

• Wait for delta MA cross confirmation in ranging markets

________________________________________

🚨 Alerts Available

• Long Setup Trigger

• Short Setup Trigger

• Bullish/Bearish Divergence Detection

• Large Buy/Sell Order Execution

________________________________________

📚 Educational Context

This methodology is based on principles used by professional order flow traders:

• Market Profile Theory: Volume distribution reveals fair value

• Tape Reading: Large orders show institutional intent

• Auction Theory: Price seeks areas of liquidity imbalance (LVN zones)

The script automates pattern recognition that discretionary traders spend years learning to identify manually.

________________________________________

⚠️ Disclaimer

This indicator is a trading tool, not a trading system. It identifies high-probability setups based on order flow analysis but requires proper risk management, market context, and trader discretion. Past performance does not guarantee future results.

________________________________________

Version: 6 (Pine Script)

Type: Overlay + Separate Pane (Delta Panel)

Resource Usage: Moderate (500 bars history, 500 lines/boxes)

________________________________________

For questions or support, please comment below. If you find this script valuable, please boost and favorite! 🚀

1. Volume Profile Analysis

The script constructs a horizontal volume profile by:

- Dividing the price range into configurable rows (default: 20)

- Accumulating volume at each price level over a lookback period (default: 50 bars)

- Separating buy volume (green bars close > open) from sell volume (red bars)

- Identifying three critical levels:

- POC (Point of Control): Price level with highest traded volume - acts as a strong magnet

- VAH/VAL (Value Area High/Low): Contains 70% of total volume - defines fair value zone

- HVN (High Volume Nodes): Resistance zones where institutions accumulated positions

- LVN (Low Volume Nodes): Thin zones that price moves through quickly - ideal targets

Why This Matters: Institutional traders leave footprints through volume. HVN zones show where large players defended levels, making them reliable support/resistance.

---

2. Cumulative Delta (Order Flow)

Tracks the running total of buying vs selling pressure:

- **Bar Delta**: Difference between buy and sell volume per candle

- **Cumulative Delta**: Sum of all bar deltas - shows net directional pressure

- **Delta Moving Average**: Smoothed delta (20-period) to identify trend

- **Delta Divergences**:

- **Bullish**: Price makes lower low, but delta makes higher low (absorption at bottom)

- **Bearish**: Price makes higher high, but delta makes lower high (exhaustion at top)

**How It Works**: When cumulative delta trends up while price consolidates, it signals accumulation. Delta divergences reveal when smart money is positioned opposite to retail expectations.

---

### 3. **Large Order Detection**

Identifies **institutional-sized orders** in real-time:

- Compares current bar volume to 20-period moving average

- Flags orders exceeding 2.5x average volume (configurable multiplier)

- Distinguishes bullish (green circles below) vs bearish (red circles above) large orders

**Rationale**: Sudden volume spikes at key levels indicate institutional participation - the "fuel" needed for breakouts or reversals.

---

## 🎯 Trading Signal Logic

### Combined Setup Criteria

The script generates **SHORT** and **LONG** signals when multiple conditions align:

**SHORT Signal Requirements:**

1. Price reaches an HVN resistance zone (within 0.2%)

2. Large sell order detected (volume spike + red candle)

3. Cumulative delta is bearish OR bearish divergence present

4. 10-bar cooldown between signals (prevents overtrading)

**LONG Signal Requirements:**

1. Price reaches an HVN support zone

2. Large buy order detected (volume spike + green candle)

3. Cumulative delta is bullish OR bullish divergence present

4. 10-bar cooldown enforced

---

## 🔧 Customization Options

| Setting | Purpose | Recommendation |

|---------|---------|----------------|

| **Volume Profile Rows** | Granularity of level detection | 20 (balanced) |

| **Lookback Period** | Historical data analyzed | 50 bars (intraday), 200 (swing) |

| **Large Order Multiplier** | Sensitivity to volume spikes | 2.5x (standard), 3.5x (conservative) |

| **HVN Threshold** | Resistance zone detection | 1.3 (default) |

| **LVN Threshold** | Target zone identification | 0.6 (default) |

| **Divergence Lookback** | Pivot detection period | 5 bars (responsive) |

---

## 📈 Dashboard Indicators

The real-time panel displays:

- **POC**: Current Point of Control price

- **Location**: Whether price is at HVN resistance

- **Orders**: Current large buy/sell activity

- **Cumulative Δ**: Net order flow value + trend direction

- **Divergence**: Active bullish/bearish divergences

- **Bar Strength**: % of candle volume that's directional (>65% = strong)

- **SETUP**: Current trade signal (LONG/SHORT/WAIT)

---

## 🎨 Visual System

- **Yellow POC Line**: Highest volume level - primary pivot

- **Blue Value Area Box**: Fair value zone (VAH to VAL)

- **Red HVN Zones**: Resistance/support from institutional accumulation

- **Green LVN Zones**: Low-liquidity targets for quick moves

- **Volume Bars**: Green (buy pressure) vs Red (sell pressure) distribution

- **Triangles**: LONG (green up) and SHORT (red down) entry signals

- **Diamonds**: Divergence warnings (cyan=bullish, fuchsia=bearish)

---

## 💡 How This Script Is Unique

Unlike standalone volume profile or delta indicators, this script:

1. **Synthesizes three complementary methods** - volume structure, order flow momentum, and liquidity detection

2. **Requires multi-factor confirmation** - signals only trigger when price, volume, and delta align at key zones

3. **Adapts to market regime** - delta filters ensure you're trading with the dominant order flow direction

4. **Provides context, not just signals** - the dashboard helps you understand *why* a setup is forming

---

## ⚙️ Best Practices

**Timeframes:**

- 5-15 min: Scalping (use 30-50 bar lookback)

- 1-4 hour: Swing trading (use 100-200 bar lookback)

**Risk Management:**

- Enter on signal candle close

- Stop loss: Beyond nearest HVN/LVN zone

- Target 1: Next LVN level

- Target 2: Opposite value area boundary

**Filters:**

- Avoid signals during major news events

- Require bar delta strength >65% for aggressive entries

- Wait for delta MA cross confirmation in ranging markets

---

## 🚨 Alerts Available

- Long Setup Trigger

- Short Setup Trigger

- Bullish/Bearish Divergence Detection

- Large Buy/Sell Order Execution

---

## 📚 Educational Context

This methodology is based on principles used by professional order flow traders:

- **Market Profile Theory**: Volume distribution reveals fair value

- **Tape Reading**: Large orders show institutional intent

- **Auction Theory**: Price seeks areas of liquidity imbalance (LVN zones)

The script automates pattern recognition that discretionary traders spend years learning to identify manually.

---

## ⚠️ Disclaimer

This indicator is a **trading tool, not a trading system**. It identifies high-probability setups based on order flow analysis but requires proper risk management, market context, and trader discretion. Past performance does not guarantee future results.

---

**Version**: 6 (Pine Script)

**Type**: Overlay + Separate Pane (Delta Panel)

**Resource Usage**: Moderate (500 bars history, 500 lines/boxes)

---

*For questions or support, please comment below. If you find this script valuable, please boost and favorite!* 🚀

Ultimate Multi-Asset Correlation System by able eiei Ultimate Multi-Asset Correlation System - User Guide

Overview

This advanced TradingView indicator combines WaveTrend oscillator analysis with comprehensive multi-asset correlation tracking. It helps traders understand market relationships, identify regime changes, and spot high-probability trading opportunities across different asset classes.

Key Features

1. WaveTrend Oscillator

Main Signal Lines: WT1 (blue) and WT2 (red) plot momentum and its moving average

Overbought/Oversold Zones: Default levels at +60/-60

Cross Signals:

🟢 Bullish: WT1 crosses above WT2 in oversold territory

🔴 Bearish: WT1 crosses below WT2 in overbought territory

Higher Timeframe (HTF) Analysis: Shows WT1 from 4H, Daily, and Weekly timeframes for trend confirmation

2. Multi-Asset Correlation Tracking

Monitors relationships between:

Major Assets: Gold (XAUUSD), Dollar Index (DXY), US 10-Year Yield, S&P 500

Crypto Assets: Bitcoin, Ethereum, Solana, BNB

Cross-Asset Analysis: Correlation between traditional markets and crypto

3. Market Regime Detection

Automatically identifies market conditions:

Risk-On: High correlation + positive sentiment (🟢 Green background)

Risk-Off: High correlation + negative sentiment (🔴 Red background)

Crypto-Risk-On: Strong crypto correlations (🟠 Orange background)

Low-Correlation: Divergent market behavior (⚪ Gray background)

Neutral: Mixed signals (🟡 Yellow background)

How to Use

Basic Setup

Add to Chart: Apply the indicator to any chart (works on all timeframes)

Choose Display Mode (Display Options):

All: Shows everything (recommended for comprehensive analysis)

WaveTrend Only: Focus on momentum signals

Correlation Only: View market relationships

Heatmap Only: Simplified correlation view

Enable Asset Groups:

✅ Major Assets: Traditional markets (stocks, bonds, commodities)

✅ Crypto Assets: Digital currencies

Mix and match based on your trading focus

Reading the Charts

WaveTrend Section (Bottom Panel)

Above 0 = Bullish momentum

Below 0 = Bearish momentum

Above +60 = Overbought (potential reversal)

Below -60 = Oversold (potential bounce)

Lighter lines = Higher timeframe trends

Correlation Histogram (Colored Bars)

Blue bars: Major asset correlations

Orange bars: Crypto correlations

Purple bars: Cross-asset correlations

Bar height: Correlation strength (-50 to +50 scale)

Background Color

Intensity reflects correlation strength

Color shows market regime

Dashboard Elements

🎯 Market Regime Analysis (Top Left)

Current Regime: Overall market condition

Average Correlation: Strength of relationships (0-1 scale)

Risk Sentiment: -100% (risk-off) to +100% (risk-on)

HTF Alignment: Multi-timeframe trend agreement

Signal Quality: Confidence level for current signals

📊 Correlation Matrix (Top Right)

Shows correlation values between asset pairs:

1.00: Perfect positive correlation

0.75+: Strong correlation (🟢 Green)

0.50+: Medium correlation (🟡 Yellow)

0.25+: Weak correlation (🟠 Orange)

Below 0.25: Negative/no correlation (🔴 Red)

🔥 Correlation Heatmap (Bottom Right)

Visual matrix showing:

Gold vs. DXY, BTC, ETH

DXY vs. BTC, ETH

BTC vs. ETH

Color-coded strength

📈 Performance Tracker (Bottom Left)

Tracks individual asset momentum:

WT1 Values: Current momentum reading

Status: OB (overbought) / OS (oversold) / Normal

Trading Strategies

1. High-Probability Trend Following

✅ Entry Conditions:

WaveTrend bullish/bearish cross

HTF Alignment matches signal direction

Signal Quality > 70%

Correlation supports direction

2. Regime Change Trading

🎯 Watch for regime shifts:

Risk-Off → Risk-On = Consider long positions

High correlation → Low correlation = Reduce position size

Crypto-Risk-On = Focus on crypto longs

3. Divergence Trading

🔍 Look for:

Strong correlation breakdown = Potential volatility

Cross-asset correlation surge = Follow the leader

Volume-price correlation extremes = Trend confirmation

4. Overbought/Oversold Reversals

⚡ Trade reversals when:

WT crosses in extreme zones (-60/+60)

HTF alignment shows opposite trend weakening

Correlation confirms mean reversion setup

Customization Tips

Fine-Tuning Parameters

WaveTrend Core:

Channel Length (10): Lower = more sensitive, Higher = smoother

Average Length (21): Adjust for your timeframe

Correlation Settings:

Length (50): Longer = more stable, Shorter = more responsive

Smoothing (5): Reduce noise in correlation readings

Market Regime:

Risk-On Threshold (0.6): Lower = earlier regime signals

High Correlation Threshold (0.75): Adjust sensitivity

Custom Asset Selection

Replace default symbols with your preferred markets:

Major Assets: Any forex, indices, bonds

Crypto: Any digital currencies

Must use correct exchange prefix (e.g., BINANCE:BTCUSDT)

Alert System

Enable "Advanced Alerts" to receive notifications for:

✅ Market regime changes

✅ Correlation breakdowns/surges

✅ Strong signals with high correlation

✅ Extreme volume-price correlation

✅ Complete HTF alignment

Correlation Interpretation Guide

ValueMeaningTrading Implication+0.75 to +1.0Strong positiveAssets move together+0.5 to +0.75Moderate positiveGenerally aligned+0.25 to +0.5Weak positiveLoose relationship-0.25 to +0.25No correlationIndependent movements-0.5 to -0.25Weak negativeSlight inverse relationship-0.75 to -0.5Moderate negativeTend to move opposite-1.0 to -0.75Strong negativeStrongly inversely correlated

Best Practices

Use Multiple Timeframes: Check HTF alignment before trading

Confirm with Correlation: Strong signals work best with supportive correlations

Watch Regime Changes: Adjust strategy based on market conditions

Volume Matters: Enable volume-price correlation for confirmation

Quality Over Quantity: Trade only high-quality setups (>70% signal quality)

Common Patterns to Watch

🔵 Risk-On Environment:

Gold-BTC positive correlation

DXY negative correlation with risk assets

High crypto correlations

🔴 Risk-Off Environment:

Flight to safety (Gold up, stocks down)

DXY strength

Correlation breakdowns

🟡 Transition Periods:

Low correlation across assets

Mixed HTF signals

Use caution, reduce position sizes

Technical Notes

Calculation Period: Uses HLC3 (average of high, low, close)

Correlation Window: Rolling correlation over specified length

HTF Data: Accurately calculated using security() function

Performance: Optimized for real-time calculation on all timeframes

Support

For optimal performance:

Use on 15-minute to daily timeframes

Enable only needed asset groups

Adjust correlation length based on trading style

Combine with your existing strategy for confirmation

Enjoy comprehensive multi-asset analysis! 🚀

Day-Type Detector — Rejection / FNL / Outside / StopRun (Clean)Day-Type Detector — Rejection / FNL / Outside / Stop-Run (Clean Version)

This indicator identifies four high-impact candlestick day-types commonly used in professional price-action and auction-market trading: Rejection Days, Failed New Low (FNL) Days, Outside Days, and Stop-Run Days. These patterns often precede major directional moves, reversals, and absorption events, making them particularly valuable for swing traders, positional traders, and short-term discretionary traders.

The script is designed to work across all timeframes and is built around volatility-adjusted measurements using Average Daily Range (ADR) for accuracy and consistency.

What This Indicator Detects

1. Rejection Day (Bullish & Bearish)

A Rejection Day is a wide-range bar that rejects a previous extreme.

The indicator identifies rejection based on:

Range > ADR × threshold

Long lower wick (for bullish) or long upper wick (for bearish)

Close located in the strong zone of the day’s range

These conditions highlight areas where aggressive counter-orderflow entered the market.

2. Failed New Low (FNL) / Failed New High

An FNL day traps traders who attempted breakout selling or buying.

The indicator checks for:

A break beyond the previous session’s low or high

Immediate rejection back inside

Midpoint recapture conditions

ADR-normalized range requirements

These days often trigger powerful directional reversals.

3. Outside Day (Bullish & Bearish)

An Outside Day is a statistically significant expansion day that breaks both the previous high and low.

The script validates:

High > previous high and low < previous low

Range > ADR threshold

Close beyond prior session extreme to complete the rejection sequence

Outside Days often represent stop runs, shakeouts, or trend accelerations.

4. Stop-Run Day (Bullish & Bearish)

Stop-Run Days are aggressive volatility expansions and tend to be the largest ranges within short windows.

This detector identifies them using:

Range > ADR × multiplier

Close located near the extreme of the day (top for bullish, bottom for bearish)

Strong body relative to total range

Break above/below previous session extreme

These patterns indicate capitulation or forced liquidation and are often followed by continuation or sharp counter-rotation.

Key Features

✔ Historical Pattern Marking

All qualifying bars are marked on the chart using plotshape() in global scope, ensuring full historical visibility.

✔ Event Logging & Table Display

A table (top-right of the chart) displays the most recent pattern detections, including:

Timestamp

Pattern type

Bar index

This allows users to monitor and study past pattern occurrences without scanning the chart manually.

✔ ADR-Adjusted Detection

Volatility uncertainty is removed by anchoring all thresholds to ADR.

This ensures consistency across:

Different symbols

Different timeframes

Different market regimes

✔ Alerts Included

Alerts are preconfigured for:

Rejection Day Bull / Bear

FNL Bull / Bear

Outside Day Bull / Bear

Stop-Run Bull / Bear

This allows the user to receive real-time notifications when major day-type structures develop.

How to Use

Add the indicator to any timeframe chart.

Enable or disable:

Historical markers

History table

ADR diagnostics

Watch for shape markers or use alerts for real-time signals.

Use the history table to review recent occurrences.

Combine these day-types with:

Market structure levels

High/low volume nodes (LVNs)

Support/resistance zones

Trend context

These day-types are most effective when they occur near meaningful structural levels because they show where strong order-flow entered the market.

Best Practices

Use higher timeframes (1H–1D) for swing entries.

Confirm signals with market structure or volume profile.

Treat these day-types as context, not standalone signals.

Observe follow-through behavior in the next 1–3 bars after detection.

Credits

This script is based on concepts commonly seen in auction-market theory and professional price-action frameworks, such as Rejection Days, Failed New Lows, Outside Days, and Stop-Run behaviors.

All calculations and logic have been rebuilt from scratch to ensure clean, reliable, and optimized Pine Script v6 execution.

Luxy Super-Duper SuperTrend Predictor Engine and Buy/Sell signalA professional trend-following grading system that analyzes historical trend