The Golden Ratio MultiplierBy Philip Swift

As Bitcoin continues to progress on its adoption journey, we learn more about its growth trajectory.

Rather than Bitcoin price action behaving like a traditional stock market share price, we see it act more like a technology being adopted at an exponential rate.

This is because Bitcoin is a network being adopted by society, and because it is decentralised money with limited supply, its price is a direct representation of that adoption process.

There are a number of regression analysis tools and stock to flow ratio studies that are helping us to understand the direction of Bitcoin’s adoption curve.

The new tool outlined in this paper brings an alternative degree of precision to understanding Bitcoin’s price action over time. It will demonstrate that Bitcoin’s adoption is not only following a broad growth curve but appears to be following established mathematical structures.

In doing so, it also:

Accurately and consistently highlights intracycle highs and lows for Bitcoin’s price.

Picks out every market cycle top in Bitcoin’s history.

Forecasts when Bitcoin will top out in the coming market cycle.

To begin, we will use the 350 day moving average of Bitcoin’s price. It has historically been an important moving average because once price moves above it, a new bull run begins.

more ...

medium.com

All rights reserved to Philip Swift (@PositiveCrypto)

Cerca negli script per "curve"

VWMA + SMA BBollinger + RSI Strategy (ChartArt) mod by BiO618This is a script I remade from the original ChartArt's "CA_RSI_Bolling_Strat".

I added a VWMA following the SMA basis curve.

BBand was made with the SMA curve, +2DS.

The point of adding VWMA to the script is to get a fast correlation between price change and volume change.

How to interpret it:

Since 3-Intervals-VWMA = (P1*V1 + P2*V2 + P3*V3) / (V1+V2+V3)

As the volume grows, VWMA get smaller.

If the price goes to the upper band, and the VWMA follows it, Price grew more than Volume, and a correction would happen soon.

If the price goes to the lower band, and the VWMA follows it, Price dipped with a lot of Volume, and a continuation of trend would be expected.

If the price goes to the upper band, and the VWMA stays close to SMA, Price grew with a correspondient Volume, and the continuation of trend would be expected.

If the price goes to the lower band, and the VWMA stays close to SMA, Price dipped with low Volume, a correction would happen soon.

Remember that NO INDICATOR is flawless, support your interpretation with other indicators like RSI and MACD.

Hope you enjoy it!

φ!

RSI Donchian R1 Alerts by JustUncleLThis study is based on an idea by presented by RicardoSantos and JayRogers of using Donchian Channel (DC) on the RSI curve. The idea being that when RSI passes through the DC centre and touches the Highest/Lowest DC then price action tends to follow in the same direction and stay there until the RSI crosses DC centre line again.

This script expands on the original idea by including alert and exit signals based on the above rules. These alerts are also filtered by the rule: they must be within the Oversold and Overbought boundaries of the RSI.

There is also the option of applying MA smoothing to the RSI curve, the HullMA (8) is recommended (default).

Each Entry and Exit signal creates an Alertcondition that can be picked up by the TradingView Alarm system.

TIP: Remember this type of Trading technique only works well in a trending market. Do not try to trade this technique in a ranging/flat market.

Adaptive Trend Mapper-ATM [Arjo]Adaptive Trend Mapper (ATM) is a directional pressure indicator designed to visualize how buying and selling commitment evolves during market trends.

Instead of focusing on price direction alone, ATM maps who is exerting stronger pressure —buyers or sellers—and how that pressure expands, weakens, or compresses over time.

Idea

ATM is built around a single concept:

Directional pressure is best understood by weighting trend strength against directional imbalance .

To achieve this, the indicator transforms trend strength into two opposing pressure measures:

Bull Pressure Index

Bear Pressure Index

These indices expand, contract, and converge based on how strongly buyers or sellers are committing, rather than simply tracking momentum or price changes.

How It Works

1. Bull & Bear Pressure Indices

ATM derives two pressure curves by weighting trend strength against directional imbalance:

The Bull Pressure Index increases when upward pressure strengthens.

The Bear Pressure Index increases when downward pressure strengthens.

Both indices operate on a 0–100 scale and are designed to diverge during strong trends and converge during non-directional or compressed phases.

Optional smoothing can be applied to reduce noise and improve readability.

2. Compression / Squeeze Detection

When:

Trend strength weakens,

Bull and Bear pressure converge,

And convergence continues over time,

ATM highlights a compression zone, signaling reduced directional conviction.

These zones often precede directional expansion once pressure rebuilds.

3. Adaptive Trend Context

An adaptive smoothed price curve is displayed on the chart to provide trend context.

Color changes reflect short-term directional shifts, helping align pressure signals with price structure.

This component is contextual only and does not generate signals by itself.

4. Optional Trend Bias Reference

An optional EMA-50 can be enabled to help identify broader directional bias and align pressure behavior with the prevailing trend.

5. Step-Based Visualization

The pressure indices can be optionally step-compressed, improving clarity on fast or noisy charts by reducing minor fluctuations.

How to Use ATM

Rising Bull Pressure → strengthening buyer commitment

Rising Bear Pressure → strengthening seller commitment

Wide separation between indices → strong directional trend

Convergence with compression highlight → range or pre-breakout environment

Notes

ATM uses widely known market concepts such as trend strength, directional imbalance, and adaptive smoothing as conceptual inputs.

All calculations, pressure mapping logic, and compression detection are original implementations developed specifically for this script.

ATM is effective when used to assess participation quality, not as a standalone signal generator.

Disclaimer

This indicator is intended for analysis and educational purposes only.

It does not generate buy or sell signals.

Always apply proper risk management.

Happy Trading.

Breakeven LECAPs BONCAPsEN

Breakeven LECAPs & BONCAPs (ARS → USD) + Futures Curve

This indicator plots the breakeven USD/ARS exchange rate for Argentine fixed-rate Treasury instruments LECAPs (S tickers) and BONCAPs (T tickers), showing the USD/ARS level at each maturity where holding the peso instrument would match the performance of holding dollars.

What you get

• Breakeven labels at (Maturity Date, Breakeven Dollar)

• Automatic FX benchmarks:

• Dólar MEP: BCBA:AL30 / BCBA:AL30D

• Dólar Cable (CCL): BCBA:AL30 / BCBA:AL30C

• Optional Custom Dollar input (1000–10000 ARS)

• Optional MatbaRofex USD futures labels at their expiry dates

• Optional polynomial regression curves for LECAPs, BONCAPs, and Futures (degree 1–4), with independent toggles, colors, and smoothness points

Core calculations

• Direct Return = (Maturity Price / Last Price) - 1

• TNA (Annualized Rate) = Direct Return × 365 / Days to Maturity

• Breakeven Dollar = Current Dollar × (1 + Direct Return)

Tooltip (hover labels)

Ticker/type, maturity date, days to maturity, current price, maturity price (px_finish), direct return, TNA, and breakeven value.

⸻

ES

Breakeven LECAPs & BONCAPs (ARS → USD) + Curva de Futuros

Este indicador grafica el tipo de cambio USD/ARS de equilibrio (breakeven) para instrumentos de tasa fija del Tesoro argentino LECAPs (tickers S) y BONCAPs (tickers T). Te muestra a qué nivel de dólar, en cada vencimiento, una inversión en pesos igualaría el rendimiento de quedarse en dólares.

Qué muestra

• Etiquetas de breakeven en (Fecha de vencimiento, Dólar breakeven)

• Referencias automáticas de tipo de cambio:

• Dólar MEP: BCBA:AL30 / BCBA:AL30D

• Dólar Cable (CCL): BCBA:AL30 / BCBA:AL30C

• Opción de Dólar Custom (1000–10000 ARS)

• Opción de mostrar futuros de USD MatbaRofex en sus vencimientos

• Curvas de regresión polinómica opcionales para LECAPs, BONCAPs y Futuros (grado 1–4), con toggle, color y suavizado configurables por separado

Cálculos principales

• Retorno Directo = (Precio de vencimiento / Último precio) - 1

• TNA = Retorno Directo × 365 / Días al vencimiento

• Dólar Breakeven = Dólar actual × (1 + Retorno Directo)

Tooltip (pasar el mouse por las etiquetas)

Ticker/tipo, fecha de vencimiento, días restantes, precio actual, precio de vencimiento (px_finish), retorno directo, TNA y valor de breakeven.

==================== DISCLAIMER / AVISO LEGAL ====================

This indicator is for informational and educational purposes only.

Eco Valores S.A. does NOT provide investment advice or recommendations.

Consult a qualified financial advisor before making investment decisions.

Este indicador es solo para fines informativos y educativos.

Eco Valores S.A. NO brinda asesoramiento ni recomendaciones de inversion.

Consulte con un asesor financiero calificado antes de invertir.

===================================================================

Power RSI Segment Runner [CHE] Power RSI Segment Runner — Tracks RSI momentum across higher timeframe segments to detect directional switches for trend confirmation.

Summary

This indicator calculates a running Relative Strength Index adapted to segments defined by changes in a higher timeframe, such as daily closes, providing a smoothed view of momentum within each period. It distinguishes between completed segments, which fix the final RSI value, and ongoing ones, which update in real time with an exponential moving average filter. Directional switches between bullish and bearish momentum trigger visual alerts, including overlay lines and emojis, while a compact table displays current trend strength as a progress bar. This segmented approach reduces noise from intra-period fluctuations, offering clearer signals for trend persistence compared to standard RSI on lower timeframes.

Motivation: Why this design?

Standard RSI often generates erratic signals in choppy markets due to constant recalculation over fixed lookback periods, leading to false reversals that mislead traders during range-bound or volatile phases. By resetting the RSI accumulation at higher timeframe boundaries, this indicator aligns momentum assessment with broader market cycles, capturing sustained directional bias more reliably. It addresses the gap between short-term noise and long-term trends, helping users filter entries without over-relying on absolute overbought or oversold thresholds.

What’s different vs. standard approaches?

- Baseline Reference: Diverges from the classic Wilder RSI, which uses a fixed-length exponential moving average of gains and losses across all bars.

- Architecture Differences:

- Segments momentum resets at higher timeframe changes, isolating calculations per period instead of continuous history.

- Employs persistent sums for ups and downs within segments, with on-the-fly RSI derivation and EMA smoothing.

- Integrates switch detection logic that clears prior visuals on reversal, preventing clutter from outdated alerts.

- Adds overlay projections like horizontal price lines and dynamic percent change trackers for immediate trade context.

- Practical Effect: Charts show discrete RSI endpoints for past segments alongside a curved running trace, making momentum evolution visually intuitive. Switches appear as clean, extendable overlays, reducing alert fatigue and highlighting only confirmed directional shifts, which aids in avoiding whipsaws during minor pullbacks.

How it works (technical)

The indicator begins by detecting changes in the specified higher timeframe, such as a new daily bar, to define segment boundaries. At each boundary, it finalizes the prior segment's RSI by summing positive and negative price changes over that period and derives the value from the ratio of those sums, then applies an exponential moving average for smoothing. Within the active segment, it accumulates ongoing ups and downs from price changes relative to the source, recalculating the running RSI similarly and smoothing it with the same EMA length.

Points for the running RSI are collected into an array starting from the segment's onset, forming a curved polyline once sufficient bars accumulate. Comparisons between the running RSI and the last completed segment's value determine the current direction as long, short, or neutral, with switches triggering deletions of old visuals and creation of new ones: a label at the RSI pane, a vertical dashed line across the RSI range, an emoji positioned via ATR offset on the price chart, a solid horizontal line at the switch price, a dashed line tracking current close, and a midpoint label for percent change from the switch.

Initialization occurs on the first bar by resetting accumulators, and visualization gates behind a minimum bar count since the segment start to avoid early instability. The trend strength table builds vertically with filled cells proportional to the rounded RSI value, colored by direction. All drawing objects update or extend on subsequent bars to reflect live progress.

Parameter Guide

EMA Length — Controls the smoothing applied to the running RSI; higher values increase lag but reduce noise. Default: 10. Trade-offs: Shorter settings heighten sensitivity for fast markets but risk more false switches; longer ones suit trending conditions for stability.

Source — Selects the price data for change calculations, typically close for standard momentum. Default: close. Trade-offs: Open or high/low may emphasize gaps, altering segment intensity.

Segment Timeframe — Defines the higher timeframe for segment resets, like daily for intraday charts. Default: D. Trade-offs: Shorter frames create more frequent but shorter segments; longer ones align with major cycles but delay resets.

Overbought Level — Sets the upper threshold for potential overbought conditions (currently unused in visuals). Default: 70. Trade-offs: Adjust for asset volatility; higher values delay bearish warnings.

Oversold Level — Sets the lower threshold for potential oversold conditions (currently unused in visuals). Default: 30. Trade-offs: Lower values permit deeper dips before signaling bullish potential.

Show Completed Label — Toggles labels at segment ends displaying final RSI. Default: true. Trade-offs: Enables historical review but can crowd charts on dense timeframes.

Plot Running Segment — Enables the curved polyline for live RSI trace. Default: true. Trade-offs: Visualizes intra-segment flow; disable for cleaner panes.

Running RSI as Label — Displays current running RSI as a forward-projected label on the last bar. Default: false. Trade-offs: Useful for quick reads; may overlap in tight scales.

Show Switch Label — Activates RSI pane labels on directional switches. Default: true. Trade-offs: Provides context; omit to minimize pane clutter.

Show Switch Line (RSI) — Draws vertical dashed lines across the RSI range at switches. Default: true. Trade-offs: Marks reversal bars clearly; extends both ways for reference.

Show Solid Overlay Line — Projects a horizontal line from switch price forward. Default: true. Trade-offs: Acts as dynamic support/resistance; wider lines enhance visibility.

Show Dashed Overlay Line — Tracks a dashed line from switch to current close. Default: true. Trade-offs: Shows price deviation; thinner for subtlety.

Show Percent Change Label — Midpoint label tracking percent move from switch. Default: true. Trade-offs: Quantifies progress; centers dynamically.

Show Trend Strength Table — Displays right-side table with direction header and RSI bar. Default: true. Trade-offs: Instant strength gauge; fixed position avoids overlap.

Activate Visualization After N Bars — Delays signals until this many bars into a segment. Default: 3. Trade-offs: Filters immature readings; higher values miss early momentum.

Segment End Label — Color for completed RSI labels. Default: 7E57C2. Trade-offs: Purple tones for finality.

Running RSI — Color for polyline and running elements. Default: yellow. Trade-offs: Bright for live tracking.

Long — Color for bullish switch visuals. Default: green. Trade-offs: Standard for uptrends.

Short — Color for bearish switch visuals. Default: red. Trade-offs: Standard for downtrends.

Solid Line Width — Thickness of horizontal overlay line. Default: 2. Trade-offs: Bolder for emphasis on key levels.

Dashed Line Width — Thickness of tracking and vertical lines. Default: 1. Trade-offs: Finer to avoid dominance.

Reading & Interpretation

Completed segment RSIs appear as static points or labels in purple, indicating the fixed momentum at period close—values drifting toward the upper half suggest building strength, while lower half implies weakness. The yellow curved polyline traces the live smoothed RSI within the current segment, rising for accumulating gains and falling for losses. Directional labels and lines in green or red flag switches: green for running momentum exceeding the prior segment's, signaling potential uptrend continuation; red for the opposite.

The right table's header colors green for long, red for short, or gray for neutral/wait, with filled purple bars scaling from bottom (low RSI) to top (high), topped by the numeric value. Overlay elements project from switch bars: the solid green/red line as a price anchor, dashed tracker showing pullback extent, and percent label quantifying deviation—positive for alignment with direction, negative for counter-moves. Emojis (up arrow for long, down for short) float above/below price via ATR spacing for quick chart scans.

Practical Workflows & Combinations

- Trend Following: Enter long on green switch confirmation after a higher high in structure; filter with table strength above midpoint for conviction. Pair with volume surge for added weight.

- Exits/Stops: Trail stops to the solid overlay line on pullbacks; exit if percent change reverses beyond 2 percent against direction. Use wait bars to confirm without chasing.

- Multi-Asset/Multi-TF: Defaults suit forex/stocks on 1H-4H with daily segments; for crypto, shorten EMA to 5 for volatility. Scale segment TF to weekly for daily charts across indices.

- Combinations: Overlay on EMA clouds for confluence—switch aligning with cloud break strengthens signal. Add volatility filters like ATR bands to debounce in low-volume regimes.

Behavior, Constraints & Performance

Signals confirm on bar close within segments, with running polyline updating live but gated by minimum bars to prevent flicker. Higher timeframe changes may introduce minor repaints on timeframe switches, mitigated by relying on confirmed HTF closes rather than intrabar peeks. Resource limits cap at 500 labels/lines and 50 polylines, pruning old objects on switches to stay efficient; no explicit loops, but array growth ties to segment length—suitable for up to 500-bar histories without lag.

Known limits include delayed visualization in short segments and insensitivity to overbought/oversold levels, as thresholds are inputted but not actively visualized. Gaps in source data reset accumulators prematurely, potentially skewing early RSI.

Sensible Defaults & Quick Tuning

Start with EMA length 10, daily segments, and 3-bar wait for balanced responsiveness on hourly charts. For excessive switches in ranging markets, increase wait bars to 5 or EMA to 14 to dampen noise. If signals lag in trends, drop EMA to 5 and use 1H segments. For stable assets like indices, widen to weekly segments; tune colors for dark/light themes without altering logic.

What this indicator is—and isn’t

This tool serves as a momentum visualization and switch detector layered over price action, aiding trend identification and confirmation in segmented contexts. It is not a standalone trading system, predictive model, or risk calculator—always integrate with broader analysis, position sizing, and stop-loss discipline. View it as an enhancement for discretionary setups, not automated alerts without validation.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

HermesHERMES STRATEGY - TRADINGVIEW DESCRIPTION

OVERVIEW

Hermes is an adaptive trend-following strategy that uses dual ALMA (Arnaud Legoux Moving Average) filters to identify high-quality entry and exit points. It's designed for swing and position traders who want smooth, low-lag signals with minimal whipsaws.

Unlike traditional moving averages that operate on price, Hermes analyzes price returns (percentage changes) to create signals that work consistently across any asset class and price range.

HOW IT WORKS

DUAL ALMA SYSTEM

The strategy uses two ALMA lines applied to price returns:

• Fast ALMA (Blue Line): Short-term trend signal (default: 80 periods)

• Slow ALMA (Black Line): Long-term baseline trend (default: 250 periods)

ALMA is superior to simple or exponential moving averages because it provides:

• Smoother curves with less noise

• Significantly reduced lag

• Natural resistance to outliers and flash crashes

TRADING LOGIC

BUY SIGNAL:

• Fast ALMA crosses above Slow ALMA (bullish regime)

• Price makes new N-bar high (momentum confirmation)

• Optional: Price above 200 EMA (macro trend filter)

• Optional: ALMA lines sufficiently separated (strength filter)

SELL SIGNAL:

• Fast ALMA crosses below Slow ALMA (bearish regime)

• Optional: Price makes new N-bar low (momentum confirmation)

The strategy stays in position during the entire bullish regime, allowing you to ride trends for weeks or months.

VISUAL INDICATORS

LINES:

• Blue Line: Fast ALMA (short-term signal)

• Black Line: Slow ALMA (long-term baseline)

TRADE MARKERS:

• Green Triangle Up: Buy executed

• Red Triangle Down: Sell executed

• Orange "M": Buy blocked by momentum filter

• Purple "W": Buy blocked by weak crossover strength

KEY PARAMETERS

ALMA SETTINGS:

• Short Period (default: 30) - Fast signal responsiveness

• Long Period (default: 250) - Baseline stability

• ALMA Offset (default: 0.90) - Balance between lag and smoothness

• ALMA Sigma (default: 7.5) - Gaussian curve width

ENTRY/EXIT FILTERS:

• Buy Lookback (default: 7) - Bars for momentum confirmation (required)

• Sell Lookback (default: 0) - Exit momentum bars (0 = disabled for faster exits)

• Min Crossover Strength (default: 0.0) - Required ALMA separation (0 = disabled)

• Use Macro Filter (default: true) - Only enter above 200 EMA

BEST PRACTICES

RECOMMENDED ASSETS - Works well on:

• Cryptocurrencies (Bitcoin, Ethereum, etc.)

• Major indices (S&P 500, Nasdaq)

• Large-cap stocks

• Commodities (Gold, Oil)

RECOMMENDED TIMEFRAMES:

• Daily: Primary timeframe for swing trading

• 4-Hour: More active trading (increase trade frequency)

• Weekly: Long-term position trading

PARAMETER TUNING:

• More trades: Lower Short Period (60-80)

• Fewer trades: Raise Short Period (100-120)

• Faster exits: Set Sell Lookback = 0

• Safer entries: Enable Macro Filter (Use Macro Filter = true)

STRATEGY ADVANTAGES

1. Low Lag - ALMA provides faster signals than traditional moving averages

2. Smooth Signals - Minimal whipsaws compared to crossover strategies

3. Asset Agnostic - Same parameters work across different markets

4. Trend Capture - Stays positioned during entire bullish regimes

5. Risk Management - Multiple filters prevent poor entries

6. Visual Clarity - Easy to interpret regime and filter states

WHEN TO USE HERMES

BEST FOR:

• Trending markets (crypto bull runs, equity uptrends)

• Swing trading (hold days to weeks)

• Position trading (hold weeks to months)

• Clear trend identification

• Risk-managed exposure

NOT SUITABLE FOR:

• Ranging/sideways markets

• Scalping or day trading

• High-frequency trading

• Mean reversion strategies

RISK DISCLAIMER

This indicator is for educational purposes only. Past performance does not guarantee future results. Always use proper position sizing and risk management. Test thoroughly on historical data before live trading.

CREDITS

Inspired by Giovanni Santostasi's Power Law Volatility Indicator, generalized for universal application across all assets using adaptive ALMA filtering.

Strategy by Hermes Trading Systems

QUICK START

1. Add indicator to chart

2. Use on daily timeframe for best results

3. Look for green buy signals when blue line crosses above black line

4. Exit on red sell signals when blue line crosses below black line

5. Adjust parameters based on your trading style:

• Conservative: Enable Macro Filter, increase Buy Lookback to 10

• Aggressive: Disable Macro Filter, lower Short Period to 60

• Default settings work well for most assets

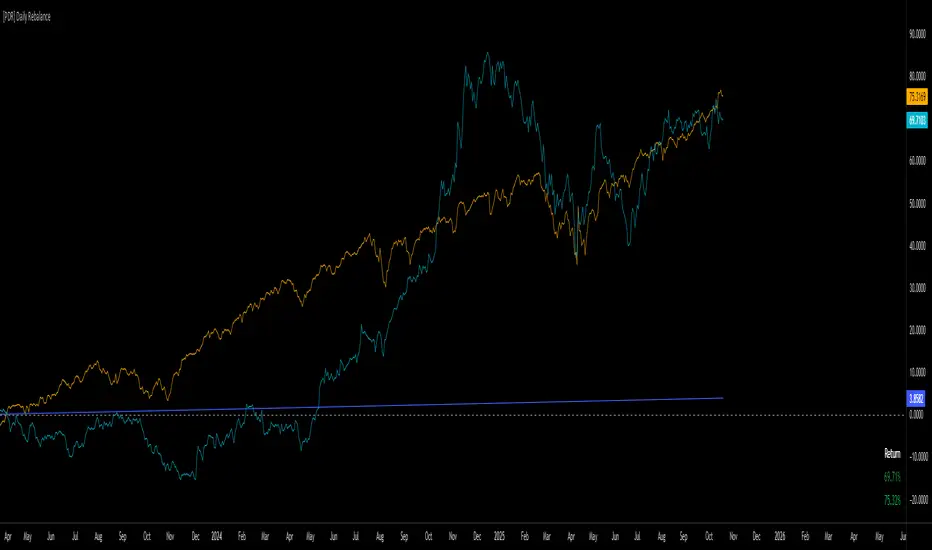

[PDR] Daily Rebalance█ OVERVIEW

This indicator is a powerful portfolio backtesting tool designed to simulate the performance of a static-weight, daily rebalancing strategy. It allows you to define a portfolio of up to 10 assets, set their target weights, and track its cumulative return against a user-defined benchmark and a risk-free rate.

The core of the script is its daily rebalancing logic, which calculates and logs every trade needed to bring the portfolio back to its target allocations at the close of each day. This provides a transparent and detailed view of how a static portfolio would have performed historically, including the impact of trading costs.

█ KEY FEATURES

Daily Rebalancing: Simulates a portfolio that is rebalanced at the close of every day to maintain target asset allocations.

Customizable Portfolio: Configure up to 10 different assets with specific weights. If all weights are left at 0, the script automatically creates an equal-weight portfolio from the selected assets.

Performance Comparison: Plots the portfolio's equity curve against a user-defined benchmark (e.g., SET:SET50 ) and a risk-free return, allowing for easy relative performance analysis.

Realistic Simulation: Accounts for trading costs like broker commission and minimum lot sizes for more accurate and grounded backtesting results.

Detailed Performance Metrics: An on-chart table displays real-time statistics, including Current Drawdown, Max Drawdown, and Total Return for both your portfolio and the benchmark.

Trade-by-Trade Logs: For full transparency, every rebalancing trade (BUY/SELL), including shares, price, notional value, and fees, is logged in the Pine Logs panel.

█ HOW TO USE

**Apply to a Daily Chart:** This script is designed to work exclusively on the daily ( 1D ) timeframe. Applying it to any other timeframe will result in a runtime error.

**Configure Settings:** Open the indicator's settings. Set your `Initial Capital`, `Start Time`, and the `Benchmark` symbol you wish to compare against.

**Define Your Assets:** In the 'Assets' group, check the box to enable each asset you want to include, select the symbol, and define its target `Weight (%)`.

**Set Trading Costs:** Adjust the `Broker Commission (%)` and `Minimal Buyable Lot` to match your expected trading conditions.

**Analyze the Results:** The performance curves are plotted in the indicator pane below your main chart. The key metrics table is displayed on the bottom-right of your chart.

**View Rebalancing Trades:** This is a crucial step for understanding the simulation. To see the detailed daily trades, you **must** open the **Pine Logs**. You can find this panel at the bottom of your TradingView window, next to the "Pine Editor" and "Strategy Tester" tabs. The logs provide a complete breakdown of every rebalancing action.

█ DISCLAIMER

This is a backtesting and simulation tool, not a trading signal generator. Its purpose is for research and performance analysis. Past performance is not indicative of future results. Always conduct your own research before making any investment decisions.

Lorentzian Harmonic Flow - Temporal Market Dynamic Lorentzian Harmonic Flow - Temporal Market Dynamic (⚡LHF)

By: DskyzInvestments

What this is

LHF Pro is a research‑grade analytical instrument that models market time as a compressible medium , extracts directional flow in curved time using heavy‑tailed kernels, and consults a history‑based memory bank for context before synthesizing a final, bounded probabilistic score . It is not a mashup; each subsystem is mathematically coupled to a single clock (time dilation via gamma) and a single lens (Lorentzian heavy‑tailed weighting). This script is dense in logic (and therefore heavy) because it prioritizes rigor, interpretability, and visual clarity.

Intended use

Education and research. This tool expresses state recognition and regime context—not guarantees. It does not place orders. It is fully functional as published and contains no placeholders. Nothing herein is financial advice.

Why this is original and useful

Curved time: Markets do not move at a constant pace. LHF Pro computes a Lorentz‑style gamma (γ) from relative speed so its analytical windows contract when the tape accelerates and relax when it slows.

Heavy‑tailed lens: Lorentzian kernels weight information with fat tails to respect rare but consequential extremes (unlike Gaussian decay).

Memory of regimes: A K‑nearest‑neighbors engine works in a multi‑feature space using Lorentz kernels per dimension and exponential age fade , returning a memory bias (directional expectation) and assurance (confidence mass).

One ecosystem: Squeeze, TCI, flow, acceleration, and memory live on the same clock and blend into a single final_score —visualized and documented on the dashboard.

Cognitive map: A 2D heat map projects memory resonance by age and flow regime, making “where the past is speaking” visible.

Shadow portfolio metaphor: Neighbor outcomes act like tiny hypothetical positions whose weighted average forms an educational pressure gauge (no execution, purely didactic).

Mathematical framework (full transparency)

1) Returns, volatility, and speed‑of‑market

Log return: rₜ = ln(closeₜ / closeₜ₋₁)

Realized vol: rv = stdev(r, vol_len); vol‑of‑vol: burst = |rv − rv |

Speed‑of‑market (analog to c): c = c_multiplier × (EMA(rv) + 0.5 × EMA(burst) + ε)

2) Trend velocity and Lorentz gamma (time dilation)

Trend velocity: v = |close − close | / (vel_len × ATR)

Relative speed: v_rel = v / c

Gamma: γ = 1 / √(1 − v_rel²), stabilized by caps (e.g., ≤10)

Interpretation: γ > 1 compresses market time → use shorter effective windows.

3) Adaptive temporal scale

Adaptive length: L = base_len / γ^power (bounded for safety)

Harmonic horizons: Lₛ = L × short_ratio, Lₘ = L × mid_ratio, Lₗ = L × long_ratio

4) Lorentzian smoothing and Harmonic Flow

Kernel weight per lag i: wᵢ = 1 / (1 + (d/γ)²), d = i/L

Horizon baselines: lw_h = Σ wᵢ·price / Σ wᵢ

Z‑deviation: z_h = (close − lw_h)/ATR

Harmonic Flow (HFL): HFL = (w_short·zₛ + w_mid·zₘ + w_long·zₗ) / (w_short + w_mid + w_long)

5) Flow kinematics

Velocity: HFL_vel = HFL − HFL

Acceleration (curvature): HFL_acc = HFL − 2·HFL + HFL

6) Squeeze and temporal compression

Bollinger width vs Keltner width using L

Squeeze: BB_width < KC_width × squeeze_mult

Temporal Compression Index: TCI = base_len / L; TCI > 1 ⇒ compressed time

7) Entropy (regime complexity)

Shannon‑inspired proxy on |log returns| with numerical safeguards and smoothing. Higher entropy → more chaotic regime.

8) Memory bank and Lorentzian k‑NN

Feature vector (5D):

Outcomes stored: forward returns at H5, H13, H34

Per‑dimension similarity: k(Δ) = 1 / (1 + Δ²), weighted by user’s feature weights

Age fading: weight_age = mem_fade^age_bars

Neighbor score: sᵢ = similarityᵢ × weight_ageᵢ

Memory bias: mem_bias = Σ sᵢ·outcomeᵢ / Σ sᵢ

Assurance: mem_assurance = Σ sᵢ (confidence mass)

Normalization: mem_bias normalized by ATR and clamped into band

Shadow portfolio metaphor: neighbors behave like micro‑positions; their weighted net forward return becomes a continuous, adaptive expectation.

9) Blended score and breakout proxy

Blend factor: α_mem = 0.45 + 0.15 × (γ − 1)

Final score: final_score = (1−α_mem)·tanh(HFL / (flow_thr·1.5)) + α_mem·tanh(mem_bias_norm)

Breakout probability (bounded): energy = cap(TCI−1) + |HFL_acc|×k + cap(γ−1)×k + cap(mem_assurance)×k; breakout_prob = sigmoid(energy). Caps avoid runaway “100%” readings.

Inputs — every control, purpose, mechanics, and tuning

🔮 Lorentz Core

Auto‑Adapt (Vol/Entropy): On = L responds to γ and entropy (breathes with regime), Off = static testing.

Base Length: Calm‑market anchor horizon. Lower (21–28) for fast tapes; higher (55–89+) for slow.

Velocity Window (vel_len): Bars used in v. Shorter = more reactive γ; longer = steadier.

Volatility Window (vol_len): Bars used for rv/burst (c). Shorter = more sensitive c.

Speed‑of‑Market Multiplier (c_multiplier): Raises/lowers c. Lower values → easier γ spikes (more adaptation). Aim for strong trends to peak around γ ≈ 2–4.

Gamma Compression Power: Exponent of γ in L. <1 softens; >1 amplifies adaptation swings.

Max Kernel Span: Upper bound on smoothing loop (quality vs CPU).

🎼 Harmonic Flow

Short/Mid/Long Horizon Ratios: Partition L into fast/medium/slow views. Smaller short_ratio → faster reaction; larger long_ratio → sturdier bias.

Weights (w_short/w_mid/w_long): Governs HFL blend. Higher w_short → nimble; higher w_long → stable.

📈 Signals

Squeeze Strictness: Threshold for BB1 = compressed (coiled spring); <1 = dilated.

v/c: Relative speed; near 1 denotes extreme pacing. Diagnostic only.

Entropy: Regime complexity; high entropy suggests caution, smaller size, or waiting for order to return.

HFL: Curved‑time directional flow; sign and magnitude are the instantaneous bias.

HFL_acc: Curvature; spikes often accompany regime ignition post‑squeeze.

Mem Bias: Directional expectation from historical analogs (ATR‑normalized, bounded). Aligns or conflicts with HFL.

Assurance: Confidence mass from neighbors; higher → more reliable memory bias.

Squeeze: ON/RELEASE/OFF from BB

Savitzky-Golay Hampel Filter | AlphaNattSavitzky-Golay Hampel Filter | AlphaNatt

A revolutionary indicator combining NASA's satellite data processing algorithms with robust statistical outlier detection to create the most scientifically advanced trend filter available on TradingView.

"This is the same mathematics that processes signals from the Hubble Space Telescope and analyzes data from the Large Hadron Collider - now applied to financial markets."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🚀 SCIENTIFIC PEDIGREE

Savitzky-Golay Filter Applications:

NASA: Satellite telemetry and space probe data processing

CERN: Particle physics data analysis at the LHC

Pharmaceutical: Chromatography and spectroscopy analysis

Astronomy: Processing signals from radio telescopes

Medical: ECG and EEG signal processing

Hampel Filter Usage:

Aerospace: Cleaning sensor data from aircraft and spacecraft

Manufacturing: Quality control in precision engineering

Seismology: Earthquake detection and analysis

Robotics: Sensor fusion and noise reduction

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🧬 THE MATHEMATICS

1. Savitzky-Golay Filter

The SG filter performs local polynomial regression on data points:

Fits a polynomial of degree n to a sliding window of data

Evaluates the polynomial at the center point

Preserves higher moments (peaks, valleys) unlike moving averages

Maintains derivative information for true momentum analysis

Originally published in Analytical Chemistry (1964)

Mathematical Properties:

Optimal smoothing in the least-squares sense

Preserves statistical moments up to polynomial order

Exact derivative calculation without additional lag

Superior frequency response vs traditional filters

2. Hampel Filter

A robust outlier detector based on Median Absolute Deviation (MAD):

Identifies outliers using robust statistics

Replaces spurious values with polynomial-fitted estimates

Resistant to up to 50% contaminated data

MAD is 1.4826 times more robust than standard deviation

Outlier Detection Formula:

|x - median| > k × 1.4826 × MAD

Where k is the threshold parameter (typically 3 for 99.7% confidence)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💎 WHY THIS IS SUPERIOR

vs Moving Averages:

Preserves peaks and valleys (critical for catching tops/bottoms)

No lag penalty for smoothness

Maintains derivative information

Polynomial fitting > simple averaging

vs Other Filters:

Outlier immunity (Hampel component)

Scientifically optimal smoothing

Preserves higher-order features

Used in billion-dollar research projects

Unique Advantages:

Feature Preservation: Maintains market structure while smoothing

Spike Immunity: Ignores false breakouts and stop hunts

Derivative Accuracy: True momentum without additional indicators

Scientific Validation: 60+ years of academic research

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚙️ PARAMETER OPTIMIZATION

1. Polynomial Order (2-5)

2 (Quadratic): Maximum smoothing, gentle curves

3 (Cubic): Balanced smoothing and responsiveness (recommended)

4-5 (Higher): More responsive, preserves more features

2. Window Size (7-51)

Must be odd number

Larger = smoother but more lag

Formula: 2×(desired smoothing period) + 1

Default 21 = analyzes 10 bars each side

3. Hampel Threshold (1.0-5.0)

1.0: Aggressive outlier removal (68% confidence)

2.0: Moderate outlier removal (95% confidence)

3.0: Conservative outlier removal (99.7% confidence) (default)

4.0+: Only extreme outliers removed

4. Final Smoothing (1-7)

Additional WMA smoothing after filtering

1 = No additional smoothing

3-5 = Recommended for most timeframes

7 = Ultra-smooth for position trading

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📊 TRADING STRATEGIES

Signal Recognition:

Cyan Line: Bullish trend with positive derivative

Pink Line: Bearish trend with negative derivative

Color Change: Trend reversal with polynomial confirmation

1. Trend Following Strategy

Enter when price crosses above cyan filter

Exit when filter turns pink

Use filter as dynamic stop loss

Best in trending markets

2. Mean Reversion Strategy

Enter long when price touches filter from below in uptrend

Enter short when price touches filter from above in downtrend

Exit at opposite band or filter color change

Excellent for range-bound markets

3. Derivative Strategy (Advanced)

The SG filter preserves derivative information

Acceleration = second derivative > 0

Enter on positive first derivative + positive acceleration

Exit on negative second derivative (momentum slowing)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📈 PERFORMANCE CHARACTERISTICS

Strengths:

Outlier Immunity: Ignores stop hunts and flash crashes

Feature Preservation: Catches tops/bottoms better than MAs

Smooth Output: Reduces whipsaws significantly

Scientific Basis: Not curve-fitted or optimized to markets

Considerations:

Slight lag in extreme volatility (all filters have this)

Requires odd window sizes (mathematical requirement)

More complex than simple moving averages

Best with liquid instruments

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🔬 SCIENTIFIC BACKGROUND

Savitzky-Golay Publication:

"Smoothing and Differentiation of Data by Simplified Least Squares Procedures"

- Abraham Savitzky & Marcel Golay

- Analytical Chemistry, Vol. 36, No. 8, 1964

Hampel Filter Origin:

"Robust Statistics: The Approach Based on Influence Functions"

- Frank Hampel et al., 1986

- Princeton University Press

These techniques have been validated in thousands of scientific papers and are standard tools in:

NASA's Jet Propulsion Laboratory

European Space Agency

CERN (Large Hadron Collider)

MIT Lincoln Laboratory

Max Planck Institutes

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💡 ADVANCED TIPS

News Trading: Lower Hampel threshold before major events to catch spikes

Scalping: Use Order=2 for maximum smoothness, Window=11 for responsiveness

Position Trading: Increase Window to 31+ for long-term trends

Combine with Volume: Strong trends need volume confirmation

Multiple Timeframes: Use daily for trend, hourly for entry

Watch the Derivative: Filter color changes when first derivative changes sign

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚠️ IMPORTANT NOTICES

Not financial advice - educational purposes only

Past performance does not guarantee future results

Always use proper risk management

Test settings on your specific instrument and timeframe

No indicator is perfect - part of complete trading system

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🏆 CONCLUSION

The Savitzky-Golay Hampel Filter represents the pinnacle of scientific signal processing applied to financial markets. By combining polynomial regression with robust outlier detection, traders gain access to the same mathematical tools that:

Guide spacecraft to other planets

Detect gravitational waves from black holes

Analyze particle collisions at near light-speed

Process signals from deep space

This isn't just another indicator - it's rocket science for trading .

"When NASA needs to separate signal from noise in billion-dollar missions, they use these exact algorithms. Now you can too."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Developed by AlphaNatt

Version: 1.0

Release: 2025

Pine Script: v6

"Where Space Technology Meets Market Analysis"

Not financial advice. Always DYOR

Global Bond Yields Monitor [MarktQuant]Global Bond Yields Monitor

The Global Bond Yields Monitor is designed to help users track and compare government bond yields across major economies. It provides an at-a-glance view of short- and long-term interest rates for multiple countries, enabling users to observe shifts in global fixed-income markets.

Key Features:

Multi-Country Coverage: Includes major advanced and emerging economies such as the United States, China, Japan, Germany, United Kingdom, Canada, Australia, and more.

Multiple Maturities: Displays yields for the 2-year, 5-year, 10-year, and 30-year maturities (20-year for Russia).

Dynamic Yield Data: Plots real-time yields for the selected country directly from TradingView’s data sources.

Weekly Change Tracking: Calculates and displays the yield change from one week ago ( ) for each maturity.

Table Visualization: Option to display a compact data table showing current yields and weekly changes, color-coded for easier interpretation.

Visual Yield Curve Comparison: Plots yield lines for short- and long-term maturities, with shaded areas between curves for visual clarity.

Customizable Display: Choose table placement and whether to show or hide the weekly change table.

Use Cases

This script is intended for analysts, traders, and investors who want to monitor shifts in sovereign bond markets. Changes in yields can reflect adjustments in monetary policy expectations, inflation outlook, or broader macroeconomic trends.

❗Important Note❗

This indicator is for market monitoring and educational purposes only. It does not generate trading signals, and it should not be interpreted as financial advice. All data is sourced from TradingView’s available market feeds, and accuracy may depend on the source data.

Lorentzian Theory Classifier🧮 Lorentzian Theory Classifier: An Observatory for Market Spacetime

Transcend the flat plane of traditional charting. Enter the curved, dynamic reality of market spacetime. The Lorentzian Theory Classifier (LTC) is not an indicator; it is a computational observatory. It is an instrument engineered to decode the geometry of market behavior, revealing the hidden curvatures and resonant frequencies that precede significant turning points.

We discard the outdated tools of Euclidean simplicity and embrace a more profound truth: financial markets, much like the cosmos described by general relativity, are governed by a fabric that is warped by the mass of participation and the energy of volatility. The LTC is your lens to perceive this fabric, to move beyond predicting lines on a chart and begin reading the very architecture of probability.

The Resonance Manifold: Standard Euclidean models search for historical analogues within a rigid sphere, missing the crucial outliers that define market extremes. The LTC's Lorentzian Resonance engine operates in a curved, non-Euclidean space, allowing it to connect with these "fat-tail" events—the true genesis points of major reversals.

🌌 THE THEORETICAL FRAMEWORK: A new Grand Unified Theory of Market Analysis

The LTC is built upon a revolutionary synthesis of concepts from special relativity, quantum mechanics, and information theory. It reframes market analysis not as a problem of forecasting, but as a problem of state recognition in a non-Euclidean manifold.

1. The Lorentzian Kernel: The Mathematics of Reality

Financial markets are not Gaussian. Their reality is one of "fat tails"—sudden, high-impact events that standard models dismiss as anomalies. The LTC acknowledges this reality by using the mathematically pure and robust Lorentzian kernel as its core engine:

Similarity(x, y) = 1 / (1 + (||x − y||² / γ²))

||x − y||²: The squared distance between the current market state (x) and a historical state (y) in our 8-dimensional feature space.

γ (Gamma): A dynamic bandwidth parameter, our "Lorentz factor," which adapts to market entropy (chaos). In calm markets, gamma is small, demanding precise resonance. In chaotic markets, gamma expands, intelligently seeking broader patterns.

This heavy-tailed function is revolutionary. It correctly assigns profound significance to the rare, extreme events that truly define market structure, while gracefully tuning out the noise of mundane price action. It doesn't just calculate; it understands context.

2. The 8-Dimensional State Vector: The Market's Quantum Fingerprint

To achieve a holistic view, the LTC projects the market onto an 8-dimensional Hilbert space, where each dimension represents a critical "observable":

Momentum & Acceleration (f_rsi, f_roc): The market's velocity and its rate of change.

Cyclical Position (f_stoch, f_cci): The market's location within its recent oscillation cycles.

Energy & Participation (f_vol, f_cor): The force of capital flow and its harmony with price.

Chaos & Uncertainty (f_ent, f_mom): The degree of randomness and the standardized force of price changes.

These are not eight separate indicators. They are entangled properties of a single "market wavefunction." The LTC's genius lies in measuring the geometric distance between these complete quantum states.

3. The k-NN Oracle: A Council of Past Universes

The LTC employs a k-Nearest Neighbors algorithm, but in our curved Lorentzian spacetime. It poses a constant, profound question: " Which moments in history are most geometrically congruent to the present moment across all eight dimensions? "

It then summons a "council" of these historical neighbors. Each neighbor's future outcome (did price ascend or descend?) casts a vote, weighted by its resonant similarity. The result is a probabilistic forecast of stunning clarity:

Prognosis: The final weighted consensus on future direction.

Assurance: The degree of unanimity within the council—a direct measure of the prediction's confidence.

The Funnel of Conviction: The LTC's process is a rigorous distillation of information. Raw, chaotic market data is resolved into a clean 8-dimensional state vector. The Lorentzian Kernel filters these states for resonance, which are then passed to the k-NN Oracle for a vote. Noise is eliminated at each stage, resulting in a single, validated, high-conviction signal.

⚙️ THE COMMAND CONSOLE: A Guide to Calibrating Your Observatory

Mastering the LTC's inputs is to become an architect of your own analytical universe. Each parameter is a dial that tunes the observatory's focus, from galactic structures to subatomic fluctuations. The tooltips in-script—over 6,000 words of documentation—provide immediate reference; this guide provides the philosophy.

A summarized guide to the Core, Signal, Supreme, and Visual controls is included directly in the indicator's code and tooltips. We encourage all users to explore these settings to tune the LTC to their unique analytical style.

🏆 THE SUPREME DASHBOARD: Your Mission Control

The dashboard is not a data table; it is your command interface with market reality. It translates the intricate dance of probabilities and vectors into clear, actionable intelligence.

⚡ ORACLE STATUS

Prognosis: The primary directional vector. Its color, magnitude, and emoji (⚡) reveal the strength and conviction of the Oracle's forward guidance.

Assurance: A real-time gauge of prediction quality, from "LOW" (high uncertainty) to "ELITE" (overwhelming statistical consensus). Interpret this as your core risk metric: trade with conviction when Assurance is ELITE; trade with caution when it is LOW.

🔮 RESONANCE ANALYSIS

Chaos: A direct measurement of market entropy. "LOW CHAOS" signifies a predictable, orderly regime. "HIGH CHAOS" is a warning of randomness and unpredictability, where trend-following logic may fail.

Turbulence: A measure of raw volatility. When the market is "TURBULENT," expect wider price swings and increased risk. Use this metric to adjust stop-loss distances and profit targets dynamically.

🏆 PERFORMANCE & ⚔️ GUARD METRICS

These sections provide illustrative statistics on the script's recent historical behavior. Metrics like Yield Ratio and Guard Index offer a quick heuristic on the prevailing risk-reward environment. Crucially, these are for observational context only and are not a substitute for your own rigorous testing and analysis.

🎨 THE VISUAL MANIFESTATION: Charting the Unseen

The LTC's visuals are designed to transform your chart from a 2D price graph into a 4D informational battlespace.

The Dynamic Aura (Background Color): This is the ambient energy field of the market. A luminous green (Ascend) signifies a bullish resonance field; a deep red (Descend) indicates bearish pressure.

The Assurance Shroud (Blue Bands): A visualization of confidence. When the shroud is wide and expansive , the Oracle's vision is clear and its predictions are robust.

The Prognosis Arc (Curved Line): A geodesic projection of the market's most likely path, based on the current Prognosis.

The Turbulence Cloud (Orange Mist): A visual warning system for market chaos. When this entropic mist expands , it is a clear sign that you are navigating a nebula of high unpredictability.

Oracle Markers (▲▼): The final, validated signals. These are not merely pivot points. They are moments in spacetime where a structural pivot has been confirmed and then ratified by a high-conviction vote from the Lorentzian Oracle. They are the pinnacles of confluence.

The Analyst's Observatory: The LTC transforms your chart into a command center for market analysis, providing a complete, at-a-glance view of market state, risk, and probabilistic trajectory.

🔧 THE ARCHITECT'S VISION: From a Blank Slate to a New Cosmos

The LTC was not assembled; it was derived. It began not with code, but with first principles, asking: "If we were to build an instrument to measure the market today, unbound by the technical dogmas of the 20th century, what would it look like?" The answer was clear: it must be multi-dimensional, it must be adaptive, and it must be built on a mathematical framework that respects the "fat-tailed" nature of reality.

The decision to use a pure Lorentzian kernel was non-negotiable. It represented a commitment to intellectual honesty over computational ease. The development of the Supreme Dashboard was driven by the philosophy of the "glass cockpit"—a belief that a trader's greatest asset is not a black box signal, but a transparent and intuitive flow of high-quality information. This script is the result of that unwavering vision: to create not just another indicator, but a new lens through which to perceive the market.

⚠️ RISK DISCLOSURE & PHILOSOPHY OF USE

The Lorentzian Theory Classifier is an instrument of profound analytical power, intended for the serious, discerning trader. It does not generate infallible signals. It generates high-probability, data-driven hypotheses based on a rigorous and transparent methodology. All trading involves substantial risk, and the future is fundamentally unknowable. Past performance, whether real or simulated, is no guarantee of future results. Use this tool to augment your own skill, to confirm your own analysis, and to manage your own risk within a well-defined trading plan.

"The effort to understand the universe is one of the very few things that lifts human life a little above the level of farce, and gives it some of the grace of tragedy."

— Steven Weinberg, Nobel Laureate in Physics

Trade with rigor. Trade with perspective. Trade with enlightenment. Trade with insight. Trade with anticipation.

— Dskyz, for DAFE Trading Systems

RSI-Adaptive T3 [ChartPrime]The RSI-Adaptive T3 is a precision trend-following tool built around the legendary T3 smoothing algorithm developed by Tim Tillson , designed to enhance responsiveness while reducing lag compared to traditional moving averages. Current implementation takes it a step further by dynamically adapting the smoothing length based on real-time RSI conditions — allowing the T3 to “breathe” with market volatility. This dynamic length makes the curve faster in trending moves and smoother during consolidations.

To help traders visualize volatility and directional momentum, adaptive volatility bands are plotted around the T3 line, with visual crossover markers and a dynamic info panel on the chart. It’s ideal for identifying trend shifts, spotting momentum surges, and adapting strategy execution to the pace of the market.

HOIW IT WORKS

At its core, this indicator fuses two ideas:

The T3 Moving Average — a 6-stage recursively smoothed exponential average created by Tim Tillson , designed to reduce lag without sacrificing smoothness. It uses a volume factor to control curvature.

A Dynamic Length Engine — powered by the RSI. When RSI is low (market oversold), the T3 becomes shorter and more reactive. When RSI is high (overbought), the T3 becomes longer and smoother. This creates a feedback loop between price momentum and trend sensitivity.

// Step 1: Adaptive length via RSI

rsi = ta.rsi(src, rsiLen)

rsi_scale = 1 - rsi / 100

len = math.round(minLen + (maxLen - minLen) * rsi_scale)

pine_ema(src, length) =>

alpha = 2 / (length + 1)

sum = 0.0

sum := na(sum ) ? src : alpha * src + (1 - alpha) * nz(sum )

sum

// Step 2: T3 with adaptive length

e1 = pine_ema(src, len)

e2 = pine_ema(e1, len)

e3 = pine_ema(e2, len)

e4 = pine_ema(e3, len)

e5 = pine_ema(e4, len)

e6 = pine_ema(e5, len)

c1 = -v * v * v

c2 = 3 * v * v + 3 * v * v * v

c3 = -6 * v * v - 3 * v - 3 * v * v * v

c4 = 1 + 3 * v + v * v * v + 3 * v * v

t3 = c1 * e6 + c2 * e5 + c3 * e4 + c4 * e3

The result: an evolving trend line that adapts to market tempo in real-time.

KEY FEATURES

⯁ RSI-Based Adaptive Smoothing

The length of the T3 calculation dynamically adjusts between a Min Length and Max Length , based on the current RSI.

When RSI is low → the T3 shortens, tracking reversals faster.

When RSI is high → the T3 stretches, filtering out noise during euphoria phases.

Displayed length is shown in a floating table, colored on a gradient between min/max values.

⯁ T3 Calculation (Tim Tillson Method)

The script uses a 6-stage EMA cascade with a customizable Volume Factor (v) , as designed by Tillson (1998) .

Formula:

T3 = c1 * e6 + c2 * e5 + c3 * e4 + c4 * e3

This technique gives smoother yet faster curves than EMAs or DEMA/Triple EMA.

⯁ Visual Trend Direction & Transitions

The T3 line changes color dynamically:

Color Up (default: blue) → bullish curvature

Color Down (default: orange) → bearish curvature

Plot fill between T3 and delayed T3 creates a gradient ribbon to show momentum expansion/contraction.

Directional shift markers (“🞛”) are plotted when T3 crosses its own delayed value — helping traders spot trend flips or pullback entries.

⯁ Adaptive Volatility Bands

Optional upper/lower bands are plotted around the T3 line using a user-defined volatility window (default: 100).

Bands widen when volatility rises, and contract during compression — similar to Bollinger logic but centered on the adaptive T3.

Shaded band zones help frame breakout setups or mean-reversion zones.

⯁ Dynamic Info Table

A live stats panel shows:

Current adaptive length

Maximum smoothing (▲ MaxLen)

Minimum smoothing (▼ MinLen)

All values update in real time and are color-coded to match trend direction.

HOW TO USE

Use T3 crossovers to detect trend transitions, especially during periods of volatility compression.

Watch for volatility contraction in the bands — breakouts from narrow band periods often precede trend bursts.

The adaptive smoothing length can also be used to assess current market tempo — tighter = faster; wider = slower.

CONCLUSION

RSI-Adaptive T3 modernizes one of the most elegant smoothing algorithms in technical analysis with intelligent RSI responsiveness and built-in volatility bands. It gives traders a cleaner read on trend health, directional shifts, and expansion dynamics — all in a visually efficient package. Perfect for scalpers, swing traders, and algorithmic modelers alike, it delivers advanced logic in a plug-and-play format.

Volumetric Tensegrity🧮 Volumetric Tensegrity unifies two of the Leading Indicator suite's critical engines — ZVOL ( volume anomaly detection ) and OBVX ( directional conviction ). Originally designed as a structural economizer for traders navigating strict indicator limits (e.g. < 10 slots per chart), it was forced to evolve beyond that constraint simply to fulfill it, albeit with a difference. The fatal flaw of traditional fusion, where two metrics are blended mathematically, is that they lose scale integrity (i.e. meaning). VTense encodes optical tensegrity to scale the amplitude of the ZVOL histogram and the slope of the OBVX spread independently, so that expansion and direction may coexist without either dominating the frame.

🧬 Tensegrity , by definition, is an intelligent design principle where elements in compression are suspended within a network of continuous tension, forming a stable, self-supporting structure . Originally conceived in esoteric biomorphology (c.f. Da Vinci, Snelson, Casteneda), tensegrity balances force through opposition, not rigidity. Applied to financial markets, Volumetric Tensegrity captures this same principle: price compresses, volume expands, conviction builds or fades — yet structure holds through the interplay. The result is not a prediction engine, but a pressure field — one that visualizes where structure might bend, break, or rebound based on how volume breathes.

🗜️ Rather than layering multiple indicators and consuming precious chart space, VTense frees up room for complementary overlays like momentum mapping, liquidity tiers, or volatility phase detection — making it ideal for modular traders operating in tight technical real estate.

🧠 Core Logic - VTense separates and preserves two essential structural forces:

• ZVOL Histogram : A Z-score-based expansion map that measures current volume deviation from its historical average. It reveals buildup zones, dormant stretches, and breakout pressure — regardless of price behavior.

• OBVX Spread : A directional conviction curve that tracks the difference between On-Balance Volume and its volume-weighted fast trend. It shows whether the crowd is leaning in (accumulation/distribution) or backing off.

🔊 ZVOL controls the amplitude of the histogram, while OBVX controls the curvature and slope of the spread. Without sacrificing breathing behavior or analytical depth, VTense provides a compact yet dynamic lens to track both expansion pressure and directional bias within a single footprint.

🌊 Volumetric Tensegrity forecasts breakout readiness, trend fatigue, and compression zones by measuring the volatility within volume . Unlike traditional tools that track volatility of price, this indicator reveals when effort becomes unstable — signaling inflection points before price reacts. Designed to decode rhythm shifts at the volume level, it operates as a pre-ignition scanner that thrives on low-timeframe charts (15m and under) while scaling effectively to 1H for validation.

🪖 From Generals to Scouts

👀 When used jointly, ZVOL + OBVX act as the general : deep-field analysts confirming stress, commitment, or exhaustion. VTense , by contrast, functions as a scout — capturing subtle buildup and alignment before structure fully reveals itself. The indicator aims to be a literal vanguard, establishing a position that can be confirmed or flexibly abandoned when the higher authority arrives to evaluate.

🥂 Use the ZVOL + OBVX pair when :

• You need independent axis control and manual dissection

• You’re building long-form confluence setups

• You have more indicator slots than you need

🔎 Use VTense when :

• You need compact clarity across multiple instruments

• You’re prioritizing confluence _detection_ over granular separation

• You’re building efficient multi-layered systems under slot constraints

🏗️ Structural Behavior and Interpretation

🫁 Z VOL Respiration Histogram : Structural Effort vs Baseline

🔵 Compression Coil – volume volatility is low and stable; the market is coiling

🟢 Steady Rhythm – volume is healthy but unremarkable; balanced participation

🟡 Passive/Absorbed Effort – expansion failing to manifest; watch for reversal

🟠 Clean Expansion – actionable volatility rise backed by structure

🔴 Volatile Blowout – chaos, climax; likely end-phase or fakeout

⚖️ ZVOL Respiration measures how hard the crowd is pressing — not just that volume is rising, but how statistically abnormal the surge is. Because it is rescaled proportionally to OBVX, the amplitude of the histogram reflects structural urgency without overwhelming the visual field.

🖐️ OBVX Spread : Real-Time Directional Conviction Behind Price Moves

🔑 The curvature of the spread reveals not just directional bias but crowd temp o: sharp slopes = urgent transitions; gradual slopes = building structural shifts. Curvature is key: sharp OBVX slope = urgency; gentle arcs = controlled drift or indecision.

• Green Rising : Accumulation — upward pressure from real buyers

• Red Falling : Distribution — sell pressure, downward slope

• Flat Curves : Transitional → uncertainty, microstructure digestion

🎭 Synchronized vs Divergent Behavior

⏱️ Synchronized (high-confluence) : often precedes structural breakouts, with internal conviction clearly visible before price resolves.

• ZVOL expands (yellow/orange/red) and OBVX climbs steeply green = strong bullish pressure

• ZVOL expands while OBVX steepens red = growing sell-side intent

🪤 Divergent (conflict tension) : flags potential traps, fakeouts, and liquidity sweeps.

• ZVOL expands sharply, but OBVX flattens or opposes → reactive expansion without crowd commitment

⛔️ Latent Drift + Structural Holding Patterns : tensegrity in action — the market holds tension without directional release.

• ZVOL compresses (blue) + OBVX meanders near zero → structure is resting, building up energy

• After prolonged drift, expect violent asymmetry when balance finally breaks

📚 Phase Interpretation: Dynamic Structural Read

• 1️⃣ Quiet Coil : Histogram flat, OBVX flat → no urgency

• 2️⃣ Initial Pulse : Yellow bars, OBVX slope builds → actionable tension

• 3️⃣ Structural Breath : Synchronized expansion and slope → directional commitment

• 4️⃣ Disagreement : Spike in ZVOL, flattening OBVX → exhaustion risk or false signal

💡 Suggested Use

• Run on 15m charts for breakout anticipation and 1H for validation

• Pair with ZVOL + OBVX to confirm crowd conviction behind the tension phase

• Use as a rhythm filter for the suite's trend indicators (e.g., RDI , SUPeR TReND 2.718 , et. al.)

• Ideal during low-volume regimes to detect pressure buildup before triggers

🧏🏻 Volumetric Tensegrity doesn’t signal. It breathes , and listens to pressure shifts before they speak in price. As a scout, it lets you see structural posture before signals align — helping you front-run resolution with clarity, not prediction.

Smart Adaptive MACDAn advanced MACD variant that dynamically adapts to market volatility using ATR-based scaling.

Key Features:

Volatility-sensitive MACD and Signal lengths

Optional smoothed MACD line

Dynamic histogram heatmap (strong vs. weak momentum)

Built-in Regular and Hidden Divergence detection

Clear visual signals via solid (regular) and dashed (hidden) divergence lines

What makes this different:

Unlike traditional MACD indicators with fixed-length settings, this version adapts in real time

to changing volatility conditions. It shortens during high-momentum environments for faster

reaction, and lengthens during low-volatility phases to reduce noise. This allows better

alignment with market behavior and cleaner momentum signals.

Divergence Detection – How It Works

The Smart Adaptive MACD detects both regular and hidden divergences by comparing price action with the smoothed MACD line. It uses recent pivot highs and lows to evaluate divergence and draws lines on the chart when conditions are met.

Regular Divergence Detection

This type of divergence signals potential reversals. It occurs when the price moves in one

direction while the MACD moves in the opposite.

Bullish Regular Divergence:

Price makes lower lows, but MACD makes higher lows.

Result: A solid green line is plotted beneath the MACD curve.

Bearish Regular Divergence:

Price makes higher highs, but MACD makes lower highs.

Result: A solid red line is plotted above the MACD curve.

Hidden Divergence Detection

This type of divergence signals trend continuation. It occurs when price pulls back slightly,

but the MACD shows deeper movement in the opposite direction.

Bullish Hidden Divergence:

Price makes higher lows, but MACD makes lower lows.

Result: A dashed green line is plotted below the MACD curve.

Bearish Hidden Divergence:

Price makes lower highs, but MACD makes higher highs.

Result: A dashed red line is plotted above the MACD curve.

How to Use:

This tool is best used alongside price structure, key support/resistance levels, or as a

secondary confirmation for your trend or reversal strategy. It is designed to enhance your

interpretation of market momentum and divergence without needing extra chart clutter.

Disclaimer:

This script is provided for educational and informational purposes only. It is not intended as

financial advice or a recommendation to buy or sell any asset. Always conduct your own

research and consult with a licensed financial advisor before making trading decisions. Use

at your own risk.

License:

This script is published under the Mozilla Public License 2.0 and is fully open-source.

Built by AresIQ | 2025

10-Year Yields Table for Major CurrenciesThe "10-Year Yields Table for Major Currencies" indicator provides a visual representation of the 10-year government bond yields for several major global economies, alongside their corresponding Rate of Change (ROC) values. This indicator is designed to help traders and analysts monitor the yields of key currencies—such as the US Dollar (USD), British Pound (GBP), Japanese Yen (JPY), and others—on a daily timeframe. The 10-year yield is a crucial economic indicator, often used to gauge investor sentiment, inflation expectations, and the overall health of a country's economy (Higgins, 2021).

Key Components:

10-Year Government Bond Yields: The indicator displays the daily closing values of 10-year government bond yields for major economies. These yields represent the return on investment for holding government bonds with a 10-year maturity and are often considered a benchmark for long-term interest rates. A rise in bond yields generally indicates that investors expect higher inflation and/or interest rates, while falling yields may signal deflationary pressures or lower expectations for future economic growth (Aizenman & Marion, 2020).

Rate of Change (ROC): The ROC for each bond yield is calculated using the formula:

ROC=Current Yield−Previous YieldPrevious Yield×100

ROC=Previous YieldCurrent Yield−Previous Yield×100

This percentage change over a one-day period helps to identify the momentum or trend of the bond yields. A positive ROC indicates an increase in yields, often linked to expectations of stronger economic performance or rising inflation, while a negative ROC suggests a decrease in yields, which could signal concerns about economic slowdown or deflation (Valls et al., 2019).

Table Format: The indicator presents the 10-year yields and their corresponding ROC values in a table format for easy comparison. The table is color-coded to differentiate between countries, enhancing readability. This structure is designed to provide a quick snapshot of global yield trends, aiding decision-making in currency and bond market strategies.

Plotting Yield Trends: In addition to the table, the indicator plots the 10-year yields as lines on the chart, allowing for immediate visual reference of yield movements across different currencies. The plotted lines provide a dynamic view of the yield curve, which is a vital tool for economic analysis and forecasting (Campbell et al., 2017).

Applications:

This indicator is particularly useful for currency traders, bond investors, and economic analysts who need to monitor the relationship between bond yields and currency strength. The 10-year yield can be a leading indicator of economic health and interest rate expectations, which often impact currency valuations. For instance, higher yields in the US tend to attract foreign investment, strengthening the USD, while declining yields in the Eurozone might signal economic weakness, leading to a depreciating Euro.

Conclusion:

The "10-Year Yields Table for Major Currencies" indicator combines essential economic data—10-year government bond yields and their rate of change—into a single, accessible tool. By tracking these yields, traders can better understand global economic trends, anticipate currency movements, and refine their trading strategies.

References:

Aizenman, J., & Marion, N. (2020). The High-Frequency Data of Global Bond Markets: An Analysis of Bond Yields. Journal of International Economics, 115, 26-45.

Campbell, J. Y., Lo, A. W., & MacKinlay, A. C. (2017). The Econometrics of Financial Markets. Princeton University Press.

Higgins, M. (2021). Macroeconomic Analysis: Bond Markets and Inflation. Harvard Business Review, 99(5), 45-60.

Valls, A., Ferreira, M., & Lopes, M. (2019). Understanding Yield Curves and Economic Indicators. Financial Markets Review, 32(4), 72-91.

True Amplitude Envelopes (TAE)The True Envelopes indicator is an adaptation of the True Amplitude Envelope (TAE) method, based on the research paper " Improved Estimation of the Amplitude Envelope of Time Domain Signals Using True Envelope Cepstral Smoothing " by Caetano and Rodet. This indicator aims to create an asymmetric price envelope with strong predictive power, closely following the methodology outlined in the paper.

Due to the inherent limitations of Pine Script, the indicator utilizes a Kernel Density Estimator (KDE) in place of the original Cepstral Smoothing technique described in the paper. While this approach was chosen out of necessity rather than superiority, the resulting method is designed to be as effective as possible within the constraints of the Pine environment.

This indicator is ideal for traders seeking an advanced tool to analyze price dynamics, offering insights into potential price movements while working within the practical constraints of Pine Script. Whether used in dynamic mode or with a static setting, the True Envelopes indicator helps in identifying key support and resistance levels, making it a valuable asset in any trading strategy.

Key Features:

Dynamic Mode: The indicator dynamically estimates the fundamental frequency of the price, optimizing the envelope generation process in real-time to capture critical price movements.

High-Pass Filtering: Uses a high-pass filtered signal to identify and smoothly interpolate price peaks, ensuring that the envelope accurately reflects significant price changes.

Kernel Density Estimation: Although implemented as a workaround, the KDE technique allows for flexible and adaptive smoothing of the envelope, aimed at achieving results comparable to the more sophisticated methods described in the original research.

Symmetric and Asymmetric Envelopes: Provides options to select between symmetric and asymmetric envelopes, accommodating various trading strategies and market conditions.

Smoothness Control: Features adjustable smoothness settings, enabling users to balance between responsiveness and the overall smoothness of the envelopes.

The True Envelopes indicator comes with a variety of input settings that allow traders to customize the behavior of the envelopes to match their specific trading needs and market conditions. Understanding each of these settings is crucial for optimizing the indicator's performance.

Main Settings

Source: This is the data series on which the indicator is applied, typically the closing price (close). You can select other price data like open, high, low, or a custom series to base the envelope calculations.

History: This setting determines how much historical data the indicator should consider when calculating the envelopes. A value of 0 will make the indicator process all available data, while a higher value restricts it to the most recent n bars. This can be useful for reducing the computational load or focusing the analysis on recent market behavior.

Iterations: This parameter controls the number of iterations used in the envelope generation algorithm. More iterations will typically result in a smoother envelope, but can also increase computation time. The optimal number of iterations depends on the desired balance between smoothness and responsiveness.

Kernel Style: The smoothing kernel used in the Kernel Density Estimator (KDE). Available options include Sinc, Gaussian, Epanechnikov, Logistic, and Triangular. Each kernel has different properties, affecting how the smoothing is applied. For example, Gaussian provides a smooth, bell-shaped curve, while Epanechnikov is more efficient computationally with a parabolic shape.