Full Regime Engine – Trend / Mean Revert / No-Trade🚀 Full Regime Engine Strategy: Trend / Mean Revert / No-Trade

This comprehensive strategy, named the Full Regime Engine, is designed to adapt its trading logic based on prevailing market conditions, classifying the market into three distinct regimes: Trend, Mean Reversion (MR), and No-Trade. It uses a combination of Average True Range (ATR) volatility ratio and the Average Directional Index (ADX) to determine the current regime, ensuring the appropriate entry and exit logic is applied.

⚙️ How the Regime Engine Works

The strategy uses two core indicators to define the market regime:

Volatility Ratio (ATR / SMA of ATR):

High Volatility Ratio (above highVolThr) suggests an active, potentially trending market.

Low Volatility Ratio (below lowVolThr) suggests a calmer, mean-reverting environment.

Average Directional Index (ADX):

High ADX (above adxTrendMin) confirms the strength of a potential trend.

Low ADX (below adxChopMax) confirms a weak, non-directional, or choppy market suitable for mean reversion.

The regimes are defined as follows:

🟢 Trend Regime: High Volatility Ratio AND High ADX.

🔵 Mean Reversion (MR) Regime: Low Volatility Ratio AND Low ADX.

⚫ No-Trade Regime: Any other condition, including outside of the defined session/time filters.

🎯 Entry and Exit Logic by Regime

The strategy employs a different entry and exit approach for each active regime:

1. Trend Regime (Pullback Entries)

Definition: The trend is established using a cross of Fast and Slow EMAs (emaFastLen and emaSlowLen).

Entry Signal: A pullback entry, where the price momentarily touches the Fast EMA and then closes back in the direction of the trend.

Long: low <= Fast EMA and close > Fast EMA (during a bullish trend).

Short: high >= Fast EMA and close < Fast EMA (during a bearish trend).

Risk Management: Uses a wider Stop Loss (slTrend) and Take Profit (tpTrend) based on ATR multiples, reflecting the expectation of larger moves in a trending market.

2. Mean Reversion Regime (VWAP Deviation Fades)

Definition: Trades the fade of extreme price movements back towards the Volume-Weighted Average Price (VWAP).

Entry Signal: Price is significantly deviated from VWAP (measured in ATR multiples mrDevATR) and shows a reversal candle.

Long (Fade Short): Price is far below VWAP (devZ < -mrDevATR) and the current candle is bullish (close > open).

Short (Fade Long): Price is far above VWAP (devZ > mrDevATR) and the current candle is bearish (close < open).

Risk Management: Uses a tighter Stop Loss (slMR) and Take Profit (tpMR) based on ATR multiples, suitable for capturing smaller moves near the mean.

⏱️ Time-Based Filters

The strategy includes robust time filters to only trade during periods with higher liquidity and predictable activity:

RTH Session Filter: Trades only within the defined "Regular Trading Hours" session (sessionStr).

Midday Filter: Optionally avoids the typically slow and choppy midday trading hours (11:00–13:00).

📊 Visuals & Customization

Background Colors: The chart background automatically colors to display the current regime: Green for Trend, Blue for Mean Revert, and Gray for No-Trade.

Plot Shapes: Distinct shapes and labels mark the raw entry signals for both Trend (Triangles) and Mean Reversion (Circles).

ATR Exits: Plots the dynamically calculated Stop Loss (Red) and Take Profit (Green) lines based on the trade's entry mode (Trend or MR).

💡 Note: This is a comprehensive engine that requires careful optimization of the input parameters for your specific instrument and timeframe. Start with the default settings and adjust the regime thresholds (ATR Ratio and ADX) and the risk/reward multiples (SL/TP) to suit your trading style.

Cerca negli script per "ema"

Alpha SignalsThis strategy is designed to highlight potential short-term market setups using a fast and slow EMA crossover system on a 5-minute chart. It provides visual signals directly on the chart to help traders observe trend changes and potential entry points.

Key Features:

EMA Crossover Entries – The strategy enters long trades when the fast EMA crosses above the slow EMA and short trades when the fast EMA crosses below the slow EMA.

Time-Based Exits – Trades are automatically closed after a configurable number of bars to manage exposure.

Visual Alerts – Buy and sell signals are displayed as labels directly on the chart for easy interpretation.

Configurable Settings – Users can adjust fast and slow EMA lengths as well as the exit bar count to suit their trading preferences.

Usage:

Suitable for short-term traders focusing on the NQ1 futures contract or other instruments with similar volatility.

Can be used for observation, back testing, or as a confirmation tool alongside other strategies.

Does not guarantee profitability; intended for educational purposes and strategy testing only.

KDJ – Long Only v3.0 (TradingView Strategy)

Overview|概覽

EN

A research strategy that automates long-only entries using a KDJ-centric core with multi-layer confirmations and volatility-aware exits. Default preset targets ETH 5m; other symbols/timeframes can be tuned.

中文

研究用策略,透過 KDJ 核心與多層確認來自動化只做多進場,並以隨波動調整的出場邏輯運作。預設為 ETH 5 分鐘;其他商品/週期可自行調參。

Backtest (hypothetical) example: ETHUSDT.P, 5m, 2024-09-18→2025-09-18, fee 0.05%, slippage 1 tick.(僅示意,屬假設性回測)

What it does|做什麼

EN

Signals are organized into channels:

A KDJ trend core

B OB/FVG touch pullback

CP Double-bottom (buffered neckline)

SR Support/Resistance bounce with rejection/zone checks

D EMA pullback (long EMA length)

E VWAP reclaim (lower-band pierce & recapture)

F Prior-low sweep & reclaim

中文

訊號分成多通道:

A KDJ 順勢核心

B OB/FVG 回踩觸價

CP 雙底(頸線含緩衝)

SR 支撐/阻力觸價不破(含拒絕與區域檢查)

D EMA 回踩(長週期 EMA)

E VWAP 收復(下緣穿越後收回)

F 前低掃回

High-level logic|高層級原理

HTF/Mid-TF context:內建 5/15/1H 或 15/60/4H 組合;以簡化趨勢線/區域提供觸價參考

Trend & structure:本階 EMA(8/21/200) 結構;Structure Breakout(近期高低點 ±ATR 緩衝)/EMA8/21 回踩

Momentum/volume:MACD、KDJ 金叉與低區偵測、量能驗證

Regime:ADX 閘(趨勢/盤整門檻)、EMA 帶寬過濾震盪、Peak Guard 避免過度延伸

No look-ahead:入場不使用前視;樞紐/趨勢線僅作情境參考

Inputs & Features|參數與功能

Market Preset:Generic / ETH(ETH 預設收緊若干門檻,開箱即用)

Entry Mode:KDJ_Core / CandleOnly / KDJ_and_Candle

Session Filter:最多三段交易時窗

Lite Filters:過度延伸、實體大小、DI 差距

S/R 模組:拒絕條件、KDJ 覆核、區域要求、即時 R:R 檢核

OrderBlock/FVG:近棒位移掃描

Chart Pattern:雙底 W,ATR 容差與頸線緩衝

Plotting:EMA200、通道字母標記、可選 TP/SL 標籤

Automation via Alerts(generic)|快訊自動化(通用)

EN

On entries/exits the strategy emits JSON through alert_message. Create alerts with “Any alert() function call” and route them to your own webhook/bridge. Symbol mapping, sizing mode, and user info are configurable in inputs.

中文

進出場時透過 alert_message 輸出 JSON。建立快訊時選 “Any alert() function call”,再由你的 webhook/橋接服務轉單;輸入面板可設定商品代碼、下單型式與使用者資訊。

提示:調整參數後,請重建快訊,並將訊息欄設為 {{strategy.order.alert_message}}。

Position sizing|部位大小

base / quote / percent_local / percent(percent_local 以本地 USD 估值計算)

可選「按數量模式」以便與本地部位同步(position_size sync)

Risk & Exits|風險與出場

SL:ATR / Swing / ATR_or_Swing;TP Cap 以 ATR 或 % 限制上限

Breakeven & Trailing:達指定 R:R 啟動保本;之後以 最高價回看 − ATR×k 追蹤

Same-bar exits:可允許/禁止同根觸發 TP/SL

Pyramiding:pyramiding=2,最多兩筆多單可同時存在(淨倉交易所請留意整體倉位的平倉行為)

Suggested workflow|建議流程

回測目標市場/週期 → 設定時段/濾網與門檻 → 微調 TP/SL 與部位大小 → 建立快訊({{strategy.order.alert_message}})→ 監看執行日誌

Notes & Disclaimer|注意與免責

回測結果仰賴時間框解析與成交規則;棒內路徑與實盤可能不同

僅供研究/教育;非投資建議

本頁無廣告、無外部連結或聯絡資訊

Release Notes|版本說明

2025-09-19

新增:One-shot Force Flat(一鍵清倉僅一次)— 於下一根收盤執行,完成後自動失效

Webhook:進/出場皆輸出 JSON;提醒更新參數後重建快訊

行為澄清:pyramiding=2,允許同圖表最多兩筆多單並存;同棒出場可設定

2025-09-18

Netted venue 說明:在淨倉模式下,出場會影響同商品的整體淨多倉;請留意手動單與策略單的互動

2025-08-28

修正小數顯示;預設優化(ETH/5m);保留隨波動的 RR/SL 邏輯

Nirvana True Duel전략 이름

열반의 진검승부 (영문: Nirvana True Duel)

컨셉과 철학

“열반의 진검승부”는 시장 소음은 무시하고, 확실할 때만 진입하는 전략입니다.

EMA 리본으로 추세 방향을 확인하고, 볼린저 밴드 수축/확장으로 변동성 돌파를 포착하며, OBV로 거래량 확인을 통해 가짜 돌파를 필터링합니다.

전략 로직

매수 조건 (롱)

20EMA > 50EMA (상승 추세)

밴드폭 수축 후 확장 시작

종가가 상단 밴드 돌파

OBV 상승 흐름 유지

매도 조건 (숏)

20EMA < 50EMA (하락 추세)

밴드폭 수축 후 확장 시작

종가가 하단 밴드 이탈

OBV 하락 흐름 유지

진입·청산

손절: ATR × 1.5 배수

익절: 손절폭의 1.5~2배에서 부분 청산

시간 청산: 설정한 최대 보유 봉수 초과 시 강제 청산

장점

✅ 추세·변동성·거래량 3중 필터 → 노이즈 최소화

✅ 백테스트·알람 지원 → 기계적 매매 가능

✅ 5분/15분 차트에 적합 → 단타/스윙 트레이딩 활용 가능

주의점

⚠ 횡보장에서는 신호가 적거나 실패 가능

⚠ 수수료·슬리피지 고려 필요

📜 Nirvana True Duel — Strategy Description (English)

Name:

Nirvana True Duel (a.k.a. Nirvana Cross)

Concept & Philosophy

The “Nirvana True Duel” strategy focuses on trading only meaningful breakouts and avoiding unnecessary noise.

Nirvana: A calm, patient state — waiting for the right opportunity without emotional trading.

True Duel: When the signal appears, enter decisively and let the market reveal the outcome.

In short: “Ignore market noise, trade only high-probability breakouts.”

🧩 Strategy Components

Trend Filter (EMA Ribbon): Stay aligned with the main market trend.

Volatility Squeeze (Bollinger Band): Detect volatility contraction & expansion to catch explosive moves early.

Volume Confirmation (OBV): Filter out false breakouts by confirming with volume flow.

⚔️ Entry & Exit Conditions

Long Setup:

20 EMA > 50 EMA (uptrend)

BB width breaks out from recent squeeze

Close > Upper Bollinger Band

OBV shows positive flow

Short Setup:

20 EMA < 50 EMA (downtrend)

BB width breaks out from recent squeeze

Close < Lower Bollinger Band

OBV shows negative flow

Risk Management:

Stop Loss: ATR × 1.5 below/above entry

Take Profit: 1.5–2× stop distance, partial take-profit allowed

Time Stop: Automatically closes after max bars held (e.g. 8h on 5m chart)

✅ Strengths

Triple Filtering: Trend + Volatility + Volume → fewer false signals

Mechanical & Backtestable: Ideal for objective trading & performance validation

Adaptable: Works well on Bitcoin, Nasdaq futures, and other high-volatility markets (5m/15m)

⚠️ Things to Note

Low signal frequency or higher failure rate in sideways/range markets

Commission & slippage should be factored in, especially on lower timeframes

ATR multiplier and R:R ratio should be optimized per asset

CoinGpt NQ策略# CoinGpt NQ 策略(MACD·多因子·可金字塔)

## 概述

**CoinGpt NQ策略**是一套面向 **纳指期货 NQ(建议:`CME_MINI:NQ1!`)30 分钟** 的可运行交易策略。

核心以 **MACD 趋势动量** 为骨架,叠加 **EMA 趋势过滤**、**可选金字塔加仓**、**三种出场模式(固定 TP/SL、追踪、追踪+TP)** 与 **风控上限**,提供三套一键预设(Balanced / Trend / Scalper),满足不同市场状态与风险偏好。

> 适配:期货/连续合约;仅做多(本脚本版本)。

> 时间框架:**30m**(可在“仅在 30m 生效”开关控制)。

---

## 进场逻辑

* **信号触发**:`MACD 上穿 Signal`(并要求直方图连续上升 2 根)。

* **趋势过滤**:价格位于 `EMA(p_emaLen)` 上方,且 `MACD>0 & Signal>0`(可关闭)。

* **时间框架限制**:默认仅在 30m 有效(可关闭)。

## 出场逻辑

* **固定 TP/SL**:按百分比计算限价止盈与止损。

* **追踪止盈**:默认以 **ATR 偏移** 跟踪;

* **追踪 + TP**:在拖尾的同时设置上沿 TP。

* **反向保护**:`MACD 下穿 Signal` 时市价平仓。

> 出场模式在输入项 **「出场模式」** 选择:

> `Auto(by preset) / Fixed TP/SL / Trailing / Trailing + TP`

---

## 金字塔加仓(可选)

* 仅在已有多单且不利回撤达到阈值时触发;

* 最多 `p_maxAdds` 层;每层在 **上次加仓价** 基础上按 `p_addStep%` 回撤触发;

* 目的:**拉低均价、提高持仓性价比**;采用小步长、有限层数控制回撤风险。

---

## 风险管理

* **当日最大亏损**:`strategy.risk.max_intraday_loss(p_maxDailyDD, %权益)`

* **单笔头寸上限**:`strategy.risk.max_position_size(p_posCapPct)`

* **订单量**(策略属性):默认 **90% 权益**。

* 实盘更建议:Balanced≈**40%**、Trend≈**35%**、Scalper≈**30%**(在“策略属性 → 订单大小”中调整)。

---

## 三套预设(参数一键生效)

| 预设 | MACD(fast/slow/signal) | 趋势EMA | 金字塔 | 加仓步长 | 固定TP/SL(%) | 追踪(ATR倍数) | 单笔上限 | 当日亏损 |

| ---------------- | ---------------------- | ----- | --- | ----- | ----------------- | --------- | ---- | ---- |

| **Balanced(默认)** | 8 / 21 / 5 | 233 | 2 层 | 0.12% | TP 0.22 / SL 0.15 | 1.2× | 50% | 1.5% |

| **Trend** | 10 / 24 / 7 | 200 | 3 层 | 0.10% | TP 0.25 / SL 0.18 | 1.6× | 45% | 1.2% |

| **Scalper** | 6 / 19 / 4 | 100 | 关闭 | —— | TP 0.18 / SL 0.12 | 1.3× | 35% | 1.0% |

> 说明:

>

> * Balanced:均衡型,适合多数时期;

> * Trend:顺势拉伸,持仓更久、盈亏比更高;

> * Scalper:快进快出、高胜率、不过度叠仓。

---

## 使用建议

1. **品种/周期**:`CME_MINI:NQ1!`(或当季主力合约),**30m**。

2. **手续费**:本策略默认 **1 USD/合约**(在“策略属性”可按实盘成本调整)。

3. **成交精度**:建议在“策略属性 → 高级设置”勾选 **Bar Magnifier**,提升限价/拖尾成交模拟精度。

4. **仓位**:策略默认 90% 仅为展示;回测与实盘更建议 **30%\~40% 权益**。

5. **风险**:金字塔仅做轻量、有限层数;若市场极端震荡,适当降低单笔上限与当日亏损阈值。

---

## 输入项(TradingView 右侧面板)

* **参数预设**:`Balanced / Trend / Scalper`

* **仅在 30m 周期生效**:开/关

* **出场模式**:`Auto(by preset) / Fixed TP/SL / Trailing / Trailing + TP`

> 其余细节参数由预设自动注入,无需手动繁杂调整,**开箱即用**。

---

## 注意事项

* 本脚本为研究与教育用途,不构成投资建议。期货与杠杆交易风险高,请在可承受范围内使用。

* 预设适配历史统计特征,未来表现不保证;建议结合自身风控与账户规模,先小仓/纸面验证。

* 仅做多版本;若需要双向(多空)或加入 RTH(美股盘中)/HTF(更高周期确认)等扩展,请在评论区留言。

---

**作者注**:

* 本策略在 Pine v6 编写,避免了常见的 v6 语法踩坑(如 `strategy.risk.max_position_size()` 仅 1 参、`plot` 标题需常量、追踪需成对参数 `trail_price + trail_offset` 等)。

* 欢迎在评论区反馈你的回测截图(区间、手续费、订单量),我会根据数据给出更贴合你的参数档。

# CoinGpt NQ Strategy (MACD · Multi-Factor · Optional Pyramiding)

## Overview

**CoinGpt NQ Strategy** is a ready-to-trade system for **Nasdaq-100 futures (NQ; recommended: `CME_MINI:NQ1!`) on the 30-minute timeframe**.

It uses **MACD momentum** as the backbone, adds an **EMA trend filter**, optional **pyramiding**, and **three exit modes** (Fixed TP/SL, Trailing, Trailing+TP) with built-in risk caps. Three one-click presets—**Balanced / Trend / Scalper**—cover different regimes and risk appetites.

> Instruments: futures / continuous contract

> Direction: **Long-only** (this script version)

> Timeframe: **30m** (toggleable)

---

## Entry

* **Trigger:** `MACD` line crossing **above** `Signal`.

* **Trend filter (optional):** price above `EMA(p_emaLen)` and `MACD > 0 & Signal > 0`.

* **Timeframe guard:** by default, signals are valid on **30m** only.

## Exit

* **Fixed TP/SL:** percentage-based limit and stop.

* **Trailing:** ATR-based trailing offset (or percent).

* **Trailing + TP:** trailing stop **and** a take-profit cap.

* **Protective flip:** when `MACD` crosses **below** `Signal`, close the long.

> Choose exit mode in **Inputs → “Exit Mode”**:

> `Auto(by preset) / Fixed TP/SL / Trailing / Trailing + TP`.

---

## Pyramiding (optional)

* Adds only **against adverse pullbacks** from the last add price.

* Up to `p_maxAdds` layers; each layer triggers at `p_addStep%` pullback from the **previous add**.

* Goal: **improve average price** with **small steps & limited layers** to keep drawdowns controlled.

---

## Risk Management

* **Daily loss cap:** `strategy.risk.max_intraday_loss(p_maxDailyDD, % of equity)`.

* **Per-trade size cap:** `strategy.risk.max_position_size(p_posCapPct)`.

* **Order size (strategy properties):** default **90% of equity** (for display).

* Practical suggestion: Balanced ≈ **40%**, Trend ≈ **35%**, Scalper ≈ **30%** (set in Strategy Properties → Order size).

---

## Presets (one-click)

| Preset | MACD (fast/slow/signal) | Trend EMA | Pyramiding | Add Step | Fixed TP/SL (%) | Trailing (ATR) | Pos Cap | Daily DD |

| ---------------------- | ----------------------- | --------- | ---------- | -------- | ------------------------- | -------------- | ------- | -------- |

| **Balanced (default)** | 8 / 21 / 5 | 233 | 2 layers | 0.12% | TP **0.22** / SL **0.15** | **1.2×** | **50%** | **1.5%** |

| **Trend** | 10 / 24 / 7 | 200 | 3 layers | 0.10% | TP **0.25** / SL **0.18** | **1.6×** | **45%** | **1.2%** |

| **Scalper** | 6 / 19 / 4 | 100 | Off | — | TP **0.18** / SL **0.12** | **1.3×** | **35%** | **1.0%** |

> **Balanced:** all-weather, stable.

> **Trend:** holds longer and targets higher R multiples.

> **Scalper:** quick in/out, higher hit-rate, no stacking.

---

## Usage Tips

1. **Symbol/TF:** `CME_MINI:NQ1!`, **30m**.

2. **Fees:** default **\$1 per contract** (adjust to your broker in Strategy Properties).

3. **Execution realism:** enable **Bar Magnifier** (Strategy Properties → Advanced) for more accurate limit/trailing fills.

4. **Sizing:** the script defaults to 90% only to showcase behavior—use **30–40%** in realistic tests.

5. **Pyramiding:** keep layers small & capped. In choppy regimes, reduce `p_posCapPct` and `p_maxDailyDD`.

---

## Inputs (right-panel)

* **Param Preset:** `Balanced / Trend / Scalper`

* **30m-only:** on/off

* **Exit Mode:** `Auto(by preset) / Fixed TP/SL / Trailing / Trailing + TP`

> All other parameters are pre-wired by the chosen preset for **plug-and-play** operation.

---

## Notes & Disclaimer

* Educational use only—**not** financial advice. Futures and leverage carry substantial risk.

* Presets reflect historical characteristics; **future performance is not guaranteed**. Start small or paper trade first.

* This version is **long-only**; if you need a two-sided (long & short) variant or extras (RTH/HTF filters), leave a comment.

---

**Author Notes**

* Written in **Pine v6** with common pitfalls avoided (e.g., `strategy.risk.max_position_size()` takes **one** arg, `plot` titles are **const strings**, trailing requires `trail_price + trail_offset`).

* Share your backtest screenshots (period, fees, order size) and I can suggest **tighter, data-driven knobs** for your setup.

Trend MasterOverview

The Strategy is a trend-following trading system designed for forex, stocks, or other markets on TradingView. It uses pivot points to identify support and resistance levels, combined with a 200-period Exponential Moving Average (EMA) to filter trades. The strategy enters long or short positions based on trend reversals during specific trading sessions (London or New York). It incorporates robust risk management, including position sizing based on risk percentage or fixed amount, trailing stop-losses, breakeven moves, and weekly/monthly profit/loss limits to prevent overtrading.

This script is ideal for traders who want a semi-automated approach with visual aids like colored session backgrounds, support/resistance lines, and a performance dashboard. It supports backtesting from a custom start date and can limit trades to one per session for discipline. Alerts are built-in for entries, exits, and stop-loss adjustments, making it compatible with automated trading bots.

Key Benefits:

Trend Reversal Detection: Spots higher highs/lows and lower highs/lows to confirm trend changes.

Session Filtering: Trades only during high-liquidity sessions to avoid choppy markets.

Risk Control: Automatically calculates position sizes to risk only a set percentage or dollar amount per trade.

Performance Tracking: Displays a table of weekly or monthly P&L (profit and loss) with color-coded heatmaps for easy review.

Customizable: Adjust trade direction, risk levels, take-profit ratios, and more via inputs.

The strategy uses a 1:1.2 risk-reward ratio by default but can be tweaked.

How It Works

Trend Identification:

The script calculates pivot highs and lows using left (4) and right (2) bars to detect swing points.

It identifies patterns like Higher Highs (HH), Higher Lows (HL), Lower Highs (LH), and Lower Lows (LL) to determine the trend direction (uptrend if above resistance, downtrend if below support).

Support (green dotted lines) and resistance (red dotted lines) are drawn dynamically and update on trend changes.

Bars are colored blue (uptrend) or black (downtrend) for visual clarity.

Entry Signals:

Long Entry: Price closes above the 200 EMA, trend shifts from down to up (e.g., breaking resistance), during an active session (London or NY), and no trade has been taken that session (if enabled).

Short Entry: Price closes below the 200 EMA, trend shifts from up to down (e.g., breaking support), during an active session, and no prior trade that session.

Trades can be restricted to "Long Only," "Short Only," or "Both."

Entries are filtered by a start date (e.g., from January 2022) and optional month-specific testing.

Position Sizing and Risk:

Risk per trade: Either a fixed dollar amount (e.g., $500) or percentage of equity (e.g., 1%).

Quantity is calculated as: Risk Amount / (Entry Price - Stop-Loss Price).

This ensures you never risk more than intended, regardless of market volatility.

Stop-Loss (SL) and Take-Profit (TP):

SL for Longs: Set below the recent support level, adjustable by a "reduce value" (e.g., tighten by 0-90%) and gap (e.g., add a buffer).

SL for Shorts: Set above the recent resistance level, with similar adjustments.

TP: Based on risk-reward ratio (default 1.2:1), so if SL is 100 pips away, TP is 120 pips in profit.

Visual boxes show SL (red) and TP (green) on the chart for the next 4 bars after entry.

Trade Management:

Trailing SL: Automatically moves SL to the new support (longs) or resistance (shorts) if it tightens the stop without increasing risk.

Breakeven Move: If enabled, SL moves to entry price once profit reaches a set ratio of initial risk (default 1:1). For example, if risk was 1%, SL moves to breakeven at 1% profit.

One Trade Per Session: Prevents multiple entries in the same London or NY session to avoid overtrading.

Sessions include optional weekend inclusion and are highlighted (blue for London, green for NY).

Risk Limits (Weekly/Monthly):

Monitors P&L for the current week or month.

Stops trading if losses hit a limit (e.g., -3%) or profits reach a target (e.g., +7%).

Resets at the start of each new week/month.

Alerts notify when limits are hit.

Exits:

Trades exit at TP, SL, or manually via alerts.

No time-based exits; relies on price action.

Performance Dashboard:

A customizable table (position, size, colors) shows P&L percentages for each week/month in a grid.

Rows = Years, Columns = Weeks (1-52) or Months (1-12).

Color scaling: Green for profits (darker for bigger wins), red for losses (darker for bigger losses).

Yearly totals in the last column.

Helps visualize strategy performance over time without manual calculations.

Input Parameters Explained

Here's a breakdown of the main inputs for easy customization:

Trade Direction: "Both" (default), "Long Only," or "Short Only" – Controls allowed trade types.

Test Only Selected Month: If true, backtests only the specified month from the start year.

Start Year/Month: Sets the backtest start date (default: Jan 2022).

Include Weekends: If true, sessions can include weekends (rarely useful for forex).

Only One Trade Per Session: Limits to one entry per London/NY session (default: true).

Risk Management Time Frame: "Weekly" or "Monthly" – For P&L limits.

Enable Limits: Toggle weekly/monthly stop trading on loss/profit thresholds.

Loss Limit (%)/Profit Target (%): Stops trading if P&L hits these (e.g., -3% loss or +7% profit).

London/New York Session: Enable/disable, with time ranges (e.g., London: 0800-1300 UTC).

Left/Right Bars: For pivot detection (default: 4 left, 2 right) – Higher values smooth signals.

Support/Resistance: Toggle lines, colors, style, width.

Change Bar Color: Colors bars based on trend.

TP RR: Take-profit risk-reward (default: 1.2).

Stoploss Reduce Value: Tightens SL (negative values widen it, 0-0.9 range).

Stoploss Gap: Adds a buffer to SL (e.g., 0.1% away from support).

Move to Breakeven: Enables SL move to entry at a profit ratio (default: true, 1:1).

Use Risk Amount $: If true, risks fixed $ (e.g., 500); else, % of equity (default: 1%).

EMA 3: The slow EMA period (default: 200) for trend filter.

Performance Display: Toggle table, location (e.g., Bottom Right), size, colors, scaling for heatmaps.

Setup and Usage Tips

Add to Chart: Copy the script into TradingView's Pine Editor, compile, and add to your chart.

Backtesting: Use the Strategy Tester tab. Adjust inputs and test on historical data.

Live Trading: Connect alerts to a broker or bot (e.g., via webhook). The script sends JSON-formatted alerts for entry, exit, SL moves, and limits.

Best Markets: Works well on crypto pairs like SOLUSD or RUNEUSD on 4H timeframes.

Risk Warning: This is not financial advice. Always use demo accounts first. Past performance doesn't guarantee future results. Commission is set to 0.05% by default – adjust for your broker.

Customization: Experiment with EMA length or RR ratio for your style.

Enhanced Market Structure StrategyATR-Based Risk Management:

Stop Loss: 2 ATR from entry (configurable)

Take Profit: 3 ATR from entry (configurable)

Dynamic Position Sizing: Based on ATR stop distance and max risk percentage

Advanced Signal Filters:

RSI Filter:

Long trades: RSI < 70 and > 40 (avoiding overbought)

Short trades: RSI > 30 and < 60 (avoiding oversold)

Volume Filter:

Requires volume > 1.2x the 20-period moving average

Ensures institutional participation

MACD Filter (Optional):

Long: MACD line above signal line and rising

Short: MACD line below signal line and falling

EMA Trend Filter:

50-period EMA for trend confirmation

Long trades require price above rising EMA

Short trades require price below falling EMA

Higher Timeframe Filter:

Uses 4H/Daily EMA for multi-timeframe confluence

Enhanced Entry Logic:

Regular Entries: IDM + BOS + ALL filters must pass

Sweep Entries: Failed breakouts with tighter stops (1.6 ATR)

High-Probability Focus: Only trades when multiple confirmations align

Visual Improvements:

Detailed Entry Labels: Show entry, stop, target, and risk percentage

SL/TP Lines: Visual representation of risk/reward

Filter Status: Bar coloring shows when all filters align

Comprehensive Statistics: Real-time performance metrics

Key Strategy Parameters:

pinescript// Recommended Settings for Different Markets:

// Forex (4H-Daily):

// - CHoCH Period: 50-75

// - ATR SL: 2.0, ATR TP: 3.0

// - All filters enabled

// Crypto (1H-4H):

// - CHoCH Period: 30-50

// - ATR SL: 2.5, ATR TP: 4.0

// - Volume filter especially important

// Indices (4H-Daily):

// - CHoCH Period: 50-100

// - ATR SL: 1.8, ATR TP: 2.7

// - EMA and MACD filters crucial

Expected Performance Improvements:

Win Rate: 55-70% (improved filtering)

Profit Factor: 2.0-3.5+ (better risk/reward with ATR)

Reduced Drawdown: Stricter filters reduce false signals

Consistent Risk: ATR-based stops adapt to volatility

This enhanced version provides much more robust signal filtering while maintaining the core market structure edge, resulting in higher-probability trades with consistent risk management.

Outside Bar Strategy with Multiple Entry ModelsOutside Bar Strategy with Multiple Entry Models

This Pine Script strategy implements a versatile trading system based on the Outside Bar pattern, offering three distinct entry models: Close Entry, High/Low Entry, and Midpoint Entry. Designed for traders seeking flexibility, the strategy includes customizable risk/reward ratios, an optional EMA trend filter, and enhanced visualization with line fills.

Key Features:

Entry Models:

Close Entry: Enters a long position when the current candle closes above the high of the previous outside bullish bar . For short, it enters when the candle closes below the low of the previous outside bearish bar.

High/Low Entry: Enters a long position when the price crosses above the high of the previous outside bullish bar . For short, it enters when the price crosses below the low of the previous outside bearish bar .

Midpoint Entry: Places a limit order at the midpoint of the previous outside bar, entering when the price reaches this level.

EMA Trend Filter: Optionally filters signals based on the alignment of EMAs (7 > 25 > 99 > 200 for long, 7 < 25 < 99 < 200 for short). Can be toggled via the Use EMA Filter input.

Risk/Reward Management: Configurable risk/reward ratio (default 2.0) with stop-loss set at the low/high of the outside bar and take-profit calculated based on the bar's range multiplied by the ratio.

Visualization:

Lines for entry, stop-loss, and take-profit levels (dashed for active trades, solid for pending Midpoint Entry orders).

Line fills: Red between entry and stop-loss, green between entry and take-profit.

Previous lines and fills persist on the chart for historical reference (line deletion disabled).

Pending limit orders for Midpoint Entry extend dynamically to the right until triggered or canceled.

Information Table: Displays real-time trade details (entry model, RR ratio, open trade status, entry/stop/take-profit levels, profit/loss percentage) and strategy statistics (success rate, total trades). For Midpoint Entry, pending order details are shown.

Inputs:

Entry Model: Choose between Close Entry, High/Low Entry, or Midpoint Entry (default: Close Entry).

Risk/Reward Ratio: Set the RR ratio (default: 2.0, step: 0.5).

Use EMA Filter: Enable/disable the EMA trend filter (default: true).

Line Colors and Style: Customize colors for entry, stop-loss, and take-profit lines, and select line style (solid or dashed).

Table Settings: Adjust table text color, size (small/normal/large), and position (right top/middle/bottom).

Disclaimer: This strategy is for educational purposes only. Backtest thoroughly and use at your own risk. Past performance is not indicative of future results.

Dskyz (DAFE) MAtrix with ATR-Powered Precision Dskyz (DAFE) MAtrix with ATR-Powered Precision

This cutting‐edge futures trading strategy built to thrive in rapidly changing market conditions. Developed for high-frequency futures trading on instruments such as the CME Mini MNQ, this strategy leverages a matrix of sophisticated moving averages combined with ATR-based filters to pinpoint high-probability entries and exits. Its unique combination of adaptable technical indicators and multi-timeframe trend filtering sets it apart from standard strategies, providing enhanced precision and dynamic responsiveness.

imgur.com

Core Functional Components

1. Advanced Moving Averages

A distinguishing feature of the DAFE strategy is its robust, multi-choice moving averages (MAs). Clients can choose from a wide array of MAs—each with specific strengths—in order to fine-tune their trading signals. The code includes user-defined functions for the following MAs:

imgur.com

Hull Moving Average (HMA):

The hma(src, len) function calculates the HMA by using weighted moving averages (WMAs) to reduce lag considerably while smoothing price data. This function computes an intermediate WMA of half the specified length, then a full-length WMA, and finally applies a further WMA over the square root of the length. This design allows for rapid adaptation to price changes without the typical delays of traditional moving averages.

Triple Exponential Moving Average (TEMA):

Implemented via tema(src, len), TEMA uses three consecutive exponential moving averages (EMAs) to effectively cancel out lag and capture price momentum. The final formula—3 * (ema1 - ema2) + ema3—produces a highly responsive indicator that filters out short-term noise.

Double Exponential Moving Average (DEMA):

Through the dema(src, len) function, DEMA calculates an EMA and then a second EMA on top of it. Its simplified formula of 2 * ema1 - ema2 provides a smoother curve than a single EMA while maintaining enhanced responsiveness.

Volume Weighted Moving Average (VWMA):

With vwma(src, len), this MA accounts for trading volume by weighting the price, thereby offering a more contextual picture of market activity. This is crucial when volume spikes indicate significant moves.

Zero Lag EMA (ZLEMA):

The zlema(src, len) function applies a correction to reduce the inherent lag found in EMAs. By subtracting a calculated lag (based on half the moving average window), ZLEMA is exceptionally attuned to recent price movements.

Arnaud Legoux Moving Average (ALMA):

The alma(src, len, offset, sigma) function introduces ALMA—a type of moving average designed to be less affected by outliers. With parameters for offset and sigma, it allows customization of the degree to which the MA reacts to market noise.

Kaufman Adaptive Moving Average (KAMA):

The custom kama(src, len) function is noteworthy for its adaptive nature. It computes an efficiency ratio by comparing price change against volatility, then dynamically adjusts its smoothing constant. This results in an MA that quickly responds during trending periods while remaining smoothed during consolidation.

Each of these functions—integrated into the strategy—is selectable by the trader (via the fastMAType and slowMAType inputs). This flexibility permits the tailored application of the MA most suited to current market dynamics and individual risk management preferences.

2. ATR-Based Filters and Risk Controls

ATR Calculation and Volatility Filter:

The strategy computes the Average True Range (ATR) over a user-defined period (atrPeriod). ATR is then used to derive both:

Volatility Assessment: Expressed as a ratio of ATR to closing price, ensuring that trades are taken only when volatility remains within a safe, predefined threshold (volatilityThreshold).

ATR-Based Entry Filters: Implemented as atrFilterLong and atrFilterShort, these conditions ensure that for long entries the price is sufficiently above the slow MA and vice versa for shorts. This acts as an additional confirmation filter.

Dynamic Exit Management:

The exit logic employs a dual approach:

Fixed Stop and Profit Target: Stops and targets are set at multiples of ATR (fixedStopMultiplier and profitTargetATRMult), helping manage risk in volatile markets.

Trailing Stop Adjustments: A trailing stop is calculated using the ATR multiplied by a user-defined offset (trailOffset), which captures additional profits as the trade moves favorably while protecting against reversals.

3. Multi-Timeframe Trend Filtering

The strategy enhances its signal reliability by leveraging a secondary, higher timeframe analysis:

15-Minute Trend Analysis:

By retrieving 15-minute moving averages (fastMA15m and slowMA15m) via request.security, the strategy determines the broader market trend. This secondary filter (enabled or disabled through useTrendFilter) ensures that entries are aligned with the prevailing market direction, thereby reducing the incidence of false signals.

4. Signal and Execution Logic

Combined MA Alignment:

The entry conditions are based primarily on the alignment of the fast and slow MAs. A long condition is triggered when the current price is above both MAs and the fast MA is above the slow MA—complemented by the ATR filter and volume conditions. The reverse applies for a short condition.

Volume and Time Window Validation:

Trades are permitted only if the current volume exceeds a minimum (minVolume) and the current hour falls within the predefined trading window (tradingStartHour to tradingEndHour). An additional volume spike check (comparing current volume to a moving average of past volumes) further filters for optimal market conditions.

Comprehensive Order Execution:

The strategy utilizes flexible order execution functions that allow pyramiding (up to 10 positions), ensuring that it can scale into positions as favorable conditions persist. The use of both market entries and automated exits (with profit targets, stop-losses, and trailing stops) ensures that risk is managed at every step.

5. Integrated Dashboard and Metrics

For transparency and real-time analysis, the strategy includes:

On-Chart Visualizations:

Both fast and slow MAs are plotted on the chart, making it easy to see the market’s technical foundation.

Dynamic Metrics Dashboard:

A built-in table displays crucial performance statistics—including current profit/loss, equity, ATR (both raw and as a percentage), and the percentage gap between the moving averages. These metrics offer immediate insight into the health and performance of the strategy.

Input Parameters: Detailed Breakdown

Every input is meticulously designed to offer granular control:

Fast & Slow Lengths:

Determine the window size for the fast and slow moving averages. Smaller values yield more sensitivity, while larger values provide a smoother, delayed response.

Fast/Slow MA Types:

Choose the type of moving average for fast and slow signals. The versatility—from basic SMA and EMA to more complex ones like HMA, TEMA, ZLEMA, ALMA, and KAMA—allows customization to fit different market scenarios.

ATR Parameters:

atrPeriod and atrMultiplier shape the volatility assessment, directly affecting entry filters and risk management through stop-loss and profit target levels.

Trend and Volume Filters:

Inputs such as useTrendFilter, minVolume, and the volume spike condition help confirm that a trade occurs in active, trending markets rather than during periods of low liquidity or market noise.

Trading Hours:

Restricting trade execution to specific hours (tradingStartHour and tradingEndHour) helps avoid illiquid or choppy markets outside of prime trading sessions.

Exit Strategies:

Parameters like trailOffset, profitTargetATRMult, and fixedStopMultiplier provide multiple layers of risk management and profit protection by tailoring how exits are generated relative to current market conditions.

Pyramiding and Fixed Trade Quantity:

The strategy supports multiple entries within a trend (up to 10 positions) and sets a predefined trade quantity (fixedQuantity) to maintain consistent exposure and risk per trade.

Dashboard Controls:

The resetDashboard input allows for on-the-fly resetting of performance metrics, keeping the strategy’s performance dashboard accurate and up-to-date.

Why This Strategy is Truly Exceptional

Multi-Faceted Adaptability:

The ability to switch seamlessly between various moving average types—each suited to particular market conditions—enables the strategy to adapt dynamically. This is a testament to the high level of coding sophistication and market insight infused within the system.

Robust Risk Management:

The integration of ATR-based stops, profit targets, and trailing stops ensures that every trade is executed with well-defined risk parameters. The system is designed to mitigate unexpected market swings while optimizing profit capture.

Comprehensive Market Filtering:

By combining moving average crossovers with volume analysis, volatility thresholds, and multi-timeframe trend filters, the strategy only enters trades under the most favorable conditions. This multi-layered filtering reduces noise and enhances signal quality.

-Final Thoughts-

The Dskyz Adaptive Futures Elite (DAFE) MAtrix with ATR-Powered Precision strategy is not just another trading algorithm—it is a multi-dimensional, fully customizable system built on advanced technical principles and sophisticated risk management techniques. Every function and input parameter has been carefully engineered to provide traders with a system that is both powerful and transparent.

For clients seeking a state-of-the-art trading solution that adapts dynamically to market conditions while maintaining strict discipline in risk management, this strategy truly stands in a class of its own.

****Please show support if you enjoyed this strategy. I'll have more coming out in the near future!!

-Dskyz

Caution

DAFE is experimental, not a profit guarantee. Futures trading risks significant losses due to leverage. Backtest, simulate, and monitor actively before live use. All trading decisions are your responsibility.

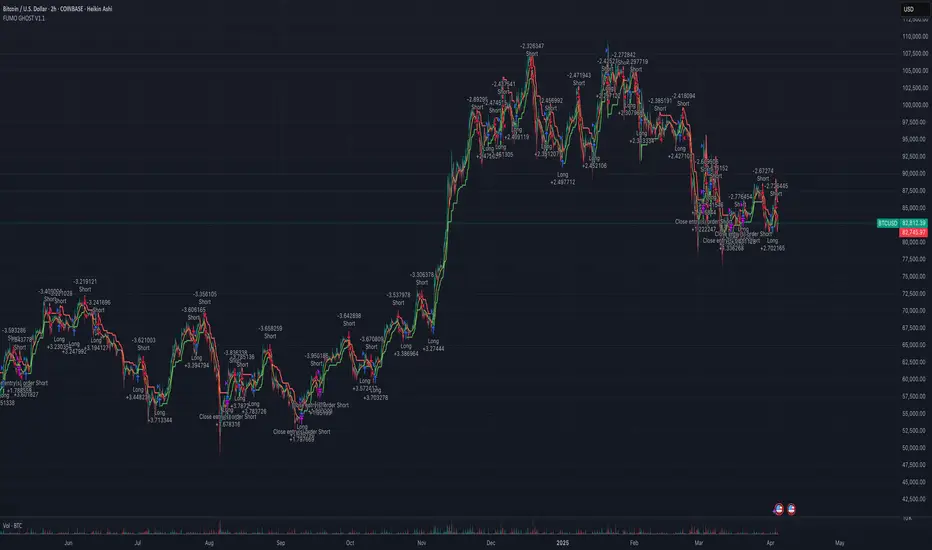

FUMO GHOST V1.1FUMO GHOST V1.0 is a high-precision trend-following strategy that identifies explosive price continuations using EMA + Supertrend logic, filtered through Heikin Ashi confirmation candles.

This strategy is designed to operate across timeframes — from scalping (1M) to swing trading (1H+) — using adaptive auto-settings for sensitivity.

It’s built to be minimal, efficient, and bold — just like the #FUMO mindset.

🔍 Core Logic:

Supertrend (ATR-based) defines trend direction

EMA is used as a momentum baseline

Heikin Ashi logic filters entries:

Long: price above EMA, trend up, HA candle strong (open == low)

Short: price below EMA, trend down, HA candle weak (open == high)

Exit: triggered automatically on Supertrend reversal

This system is designed to stay in the trend as long as it’s valid — no scalping in/out or rapid re-entries.

⚙ Strategy Settings:

Auto-adjusts EMA & ATR parameters by timeframe (1M to 1D)

Manual override available (use_custom = true)

“Silent Mode” hides all visuals for minimal charting

Uses internal Heikin Ashi logic, regardless of visible candles

🧪 Backtest Notes:

Backtest is powered by TradingView’s built-in strategy() engine

Default risk: 10% equity per trade

For accurate simulation, enable “Use standard OHLC” in strategy settings — this ensures reliable backtest when internal Heikin Ashi logic is used

🔒 Why is the code protected?

This script uses:

A unique combination of Supertrend + EMA + Heikin Ashi filters

Internal timeframe-aware parameter scaling

Logic tuned specifically for explosive trend continuations

While freely available for public use, the source code is closed to protect the inner mechanism and prevent reverse engineering.

FUMO GHOST V1.0 is built for clarity, conviction, and confidence.

Make your next trade bold.

Make Fuck U Money — 24/7.

Dual SuperTrend w VIX Filter - Strategy [presentTrading]Hey everyone! Haven't been here for a long time. Been so busy again in the past 2 months. I recently started working on analyzing the combination of trend strategy and VIX, but didn't get outstanding results after a few tries. Sharing this tool with all of you in case you have better insights.

█ Introduction and How it is Different

The Dual SuperTrend with VIX Filter Strategy combines traditional trend following with market volatility analysis. Unlike conventional SuperTrend strategies that focus solely on price action, this experimental system incorporates VIX (Volatility Index) as an adaptive filter to create a more context-aware trading approach. By analyzing where current volatility stands relative to historical norms, the strategy adjusts to different market environments rather than applying uniform logic across all conditions.

BTCUSD 6hr Long Short Performance

█ Strategy, How it Works: Detailed Explanation

🔶 Dual SuperTrend Core

The strategy uses two SuperTrend indicators with different sensitivity settings:

- SuperTrend 1: Length = 13, Multiplier = 3.5

- SuperTrend 2: Length = 8, Multiplier = 5.0

The SuperTrend calculation follows this process:

1. ATR = Average of max(High-Low, |High-PreviousClose|, |Low-PreviousClose|) over 'length' periods

2. UpperBand = (High+Low)/2 - (Multiplier * ATR)

3. LowerBand = (High+Low)/2 + (Multiplier * ATR)

Trend direction is determined by:

- If Close > previous LowerBand, Trend = Bullish (1)

- If Close < previous UpperBand, Trend = Bearish (-1)

- Otherwise, Trend = previous Trend

🔶 VIX Analysis Framework

The core innovation lies in the VIX analysis system:

1. Statistical Analysis:

- VIX Mean = SMA(VIX, 252)

- VIX Standard Deviation = StdDev(VIX, 252)

- VIX Z-Score = (Current VIX - VIX Mean) / VIX StdDev

2. **Volatility Bands:

- Upper Band 1 = VIX Mean + (2 * VIX StdDev)

- Upper Band 2 = VIX Mean + (3 * VIX StdDev)

- Lower Band 1 = VIX Mean - (2 * VIX StdDev)

- Lower Band 2 = VIX Mean - (3 * VIX StdDev)

3. Volatility Regimes:

- "Very Low Volatility": VIX < Lower Band 1

- "Low Volatility": Lower Band 1 ≤ VIX < Mean

- "Normal Volatility": Mean ≤ VIX < Upper Band 1

- "High Volatility": Upper Band 1 ≤ VIX < Upper Band 2

- "Extreme Volatility": VIX ≥ Upper Band 2

4. VIX Trend Detection:

- VIX EMA = EMA(VIX, 10)

- VIX Rising = VIX > VIX EMA

- VIX Falling = VIX < VIX EMA

Local performance:

🔶 Entry Logic Integration

The strategy combines trend signals with volatility filtering:

Long Entry Condition:

- Both SuperTrend 1 AND SuperTrend 2 must be bullish (trend = 1)

- AND selected VIX filter condition must be satisfied

Short Entry Condition:

- Both SuperTrend 1 AND SuperTrend 2 must be bearish (trend = -1)

- AND selected VIX filter condition must be satisfied

Available VIX filter rules include:

- "Below Mean + SD": VIX < Lower Band 1

- "Below Mean": VIX < VIX Mean

- "Above Mean": VIX > VIX Mean

- "Above Mean + SD": VIX > Upper Band 1

- "Falling VIX": VIX < VIX EMA

- "Rising VIX": VIX > VIX EMA

- "Any": No VIX filtering

█ Trade Direction

The strategy allows testing in three modes:

1. **Long Only:** Test volatility effects on uptrends only

2. **Short Only:** Examine volatility's impact on downtrends only

3. **Both (Default):** Compare how volatility affects both trend directions

This enables comparative analysis of how volatility regimes impact bullish versus bearish markets differently.

█ Usage

Use this strategy as an experimental framework:

1. Form a hypothesis about how volatility affects trend reliability

2. Configure VIX filters to test your specific hypothesis

3. Analyze performance across different volatility regimes

4. Compare results between uptrends and downtrends

5. Refine your volatility filtering approach based on results

6. Share your findings with the trading community

This framework allows you to investigate questions like:

- Are uptrends more reliable during rising or falling volatility?

- Do downtrends perform better when volatility is above or below its historical average?

- Should different volatility filters be applied to long vs. short positions?

█ Default Settings

The default settings serve as a starting point for exploration:

SuperTrend Parameters:

- SuperTrend 1 (Length=13, Multiplier=3.5): More responsive to trend changes

- SuperTrend 2 (Length=8, Multiplier=5.0): More selective filter requiring stronger trends

VIX Analysis Settings:

- Lookback Period = 252: Establishes a full market cycle for volatility context

- Standard Deviation Bands = 2 and 3 SD: Creates statistically significant regime boundaries

- VIX Trend Period = 10: Balances responsiveness with noise reduction

Default VIX Filter Selection:

- Long Entry: "Above Mean" - Tests if uptrends perform better during above-average volatility

- Short Entry: "Rising VIX" - Tests if downtrends accelerate when volatility is increasing

Feel Free to share your insight below!!!

TMA StrategyThe **TMA Strategy** is a trend-following strategy that leverages **Smoothed Moving Averages (SMMA)** and **candlestick patterns** to identify high-probability trading opportunities. It is designed for traders who want to capture strong trends while minimizing noise from short-term fluctuations.

**Key Features:**

✔ **Multiple Smoothed Moving Averages (SMMA):** Uses 21, 50, 100, and 200-period SMMAs to identify market trends and key support/resistance zones.

✔ **Candlestick Pattern Confirmation:** Incorporates **3-line strike** and **engulfing candle** patterns to confirm trade entries.

✔ **Dynamic Trend Filter:** A **2-period EMA** ensures that trades align with the dominant trend, reducing false signals.

✔ **Customizable Session Filter:** Allows users to enable/disable trading within specific market sessions (New York, London, Tokyo, etc.), ensuring trades are executed only during high-liquidity hours.

✔ **Risk Management:** Uses predefined exit conditions based on EMA/SMMA crossovers to lock in profits and minimize losses.

**Trading Logic:**

📌 **Long Entry:**

- Bullish Engulfing or 3-Line Strike pattern appears.

- Price is above the 200 SMMA.

- 2 EMA confirms an uptrend.

- Trade executes if session filter allows.

📌 **Short Entry:**

- Bearish Engulfing or 3-Line Strike pattern appears.

- Price is below the 200 SMMA.

- 2 EMA confirms a downtrend.

- Trade executes if session filter allows.

📌 **Exit Conditions:**

- Long trades exit when EMA(2) crosses **below** SMMA(200).

- Short trades exit when EMA(2) crosses **above** SMMA(200).

**Ideal Markets & Timeframes:**

✅ Best suited for **Forex, Stocks, and Crypto** markets.

✅ Works well on **higher timeframes (15m, 1H, 4H, Daily)** for stronger trend confirmation.

📢 **Disclaimer:**

This strategy is for educational purposes only. Backtest results do not guarantee future performance. Always use proper risk management and test in a demo account before live trading.

🚀 **Try the TMA Strategy now and enhance your trend-following approach!**

MACD Volume Strategy for XAUUSD (15m) [PineIndicators]The MACD Volume Strategy is a momentum-based trading system designed for XAUUSD on the 15-minute timeframe. It integrates two key market indicators: the Moving Average Convergence Divergence (MACD) and a volume-based oscillator to identify strong trend shifts and confirm trade opportunities. This strategy uses dynamic position sizing, incorporates leverage customization, and applies structured entry and exit conditions to improve risk management.

⚙️ Core Strategy Components

1️⃣ Volume-Based Momentum Calculation

The strategy includes a custom volume oscillator to filter trade signals based on market activity. The oscillator is derived from the difference between short-term and long-term volume trends using Exponential Moving Averages (EMAs)

Short EMA (default = 5) represents recent volume activity.

Long EMA (default = 8) captures broader volume trends.

Positive values indicate rising volume, supporting momentum-based trades.

Negative values suggest weak market activity, reducing signal reliability.

By requiring positive oscillator values, the strategy ensures momentum confirmation before entering trades.

2️⃣ MACD Trend Confirmation

The strategy uses the MACD indicator as a trend filter. The MACD is calculated as:

Fast EMA (16-period) detects short-term price trends.

Slow EMA (26-period) smooths out price fluctuations to define the overall trend.

Signal Line (9-period EMA) helps identify crossovers, signaling potential trend shifts.

Histogram (MACD – Signal) visualizes trend strength.

The system generates trade signals based on MACD crossovers around the zero line, confirming bullish or bearish trend shifts.

📌 Trade Logic & Conditions

🔹 Long Entry Conditions

A buy signal is triggered when all the following conditions are met:

✅ MACD crosses above 0, signaling bullish momentum.

✅ Volume oscillator is positive, confirming increased trading activity.

✅ Current volume is at least 50% of the previous candle’s volume, ensuring market participation.

🔻 Short Entry Conditions

A sell signal is generated when:

✅ MACD crosses below 0, indicating bearish momentum.

✅ Volume oscillator is positive, ensuring market activity is sufficient.

✅ Current volume is less than 50% of the previous candle’s volume, showing decreasing participation.

This multi-factor approach filters out weak or false signals, ensuring that trades align with both momentum and volume dynamics.

📏 Position Sizing & Leverage

Dynamic Position Calculation:

Qty = strategy.equity × leverage / close price

Leverage: Customizable (default = 1x), allowing traders to adjust risk exposure.

Adaptive Sizing: The strategy scales position sizes based on account equity and market price.

Slippage & Commission: Built-in slippage (2 points) and commission (0.01%) settings provide realistic backtesting results.

This ensures efficient capital allocation, preventing overexposure in volatile conditions.

🎯 Trade Management & Exits

Take Profit & Stop Loss Mechanism

Each position includes predefined profit and loss targets:

Take Profit: +10% of risk amount.

Stop Loss: Fixed at 10,100 points.

The risk-reward ratio remains balanced, aiming for controlled drawdowns while maximizing trade potential.

Visual Trade Tracking

To improve trade analysis, the strategy includes:

📌 Trade Markers:

"Buy" label when a long position opens.

"Close" label when a position exits.

📌 Trade History Boxes:

Green for profitable trades.

Red for losing trades.

📌 Horizontal Trade Lines:

Shows entry and exit prices.

Helps identify trend movements over multiple trades.

This structured visualization allows traders to analyze past performance directly on the chart.

⚡ How to Use This Strategy

1️⃣ Apply the script to a XAUUSD (Gold) 15m chart in TradingView.

2️⃣ Adjust leverage settings as needed.

3️⃣ Enable backtesting to assess past performance.

4️⃣ Monitor volume and MACD conditions to understand trade triggers.

5️⃣ Use the visual trade markers to review historical performance.

The MACD Volume Strategy is designed for short-term trading, aiming to capture momentum-driven opportunities while filtering out weak signals using volume confirmation.

[SHORT ONLY] ATR Sell the Rip Mean Reversion Strategy█ STRATEGY DESCRIPTION

The "ATR Sell the Rip Mean Reversion Strategy" is a contrarian system that targets overextended price moves on stocks and ETFs. It calculates an ATR‐based trigger level to identify shorting opportunities. When the current close exceeds this smoothed ATR trigger, and if the close is below a 200-period EMA (if enabled), the strategy initiates a short entry, aiming to profit from an anticipated corrective pullback.

█ HOW IS THE ATR SIGNAL BAND CALCULATED?

This strategy computes an ATR-based signal trigger as follows:

Calculate the ATR

The strategy computes the Average True Range (ATR) using a configurable period provided by the user:

atrValue = ta.atr(atrPeriod)

Determine the Threshold

Multiply the ATR by a predefined multiplier and add it to the current close:

atrThreshold = close + atrValue * atrMultInput

Smooth the Threshold

Apply a Simple Moving Average over a specified period to smooth out the threshold, reducing noise:

signalTrigger = ta.sma(atrThreshold, smoothPeriodInput)

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The current close is above the smoothed ATR signal trigger.

The trade occurs within the specified trading window (between Start Time and End Time).

If the EMA filter is enabled, the close must also be below the 200-period EMA.

2. EXIT CONDITION

An exit Signal is generated when the current close falls below the previous bar’s low (close < low ), indicating a potential bearish reversal and prompting the strategy to close its short position.

█ ADDITIONAL SETTINGS

ATR Period: The period used to calculate the ATR, allowing for adaptability to different volatility conditions (default is 20).

ATR Multiplier: The multiplier applied to the ATR to determine the raw threshold (default is 1.0).

Smoothing Period: The period over which the raw ATR threshold is smoothed using an SMA (default is 10).

Start Time and End Time: Defines the time window during which trades are allowed.

EMA Filter (Optional): When enabled, short entries are only executed if the current close is below the 200-period EMA, confirming a bearish trend.

█ PERFORMANCE OVERVIEW

This strategy is designed for use on the Daily timeframe, targeting stocks and ETFs by capitalizing on overextended price moves.

It utilizes a dynamic, ATR-based trigger to identify when prices have potentially peaked, setting the stage for a mean reversion short entry.

The optional EMA filter helps align trades with broader market trends, potentially reducing false signals.

Backtesting is recommended to fine-tune the ATR multiplier, smoothing period, and EMA settings to match the volatility and behavior of specific markets.

BullBear with Volume-Percentile TP - Strategy [presentTrading] Happy New Year, everyone! I hope we have a fantastic year ahead.

It's been a while since I published an open script, but it's time to return.

This strategy introduces an indicator called Bull Bear Power, combined with an advanced take-profit system, which is the main innovative and educational aspect of this script. I hope all of you find some useful insights here. Welcome to engage in meaningful exchanges. This is a versatile tool suitable for both novice and experienced traders.

█ Introduction and How it is Different

Unlike traditional strategies that rely solely on price or volume indicators, this approach combines Bull Bear Power (BBP) with volume percentile analysis to identify optimal entry and exit points. It features a dynamic take-profit mechanism based on ATR (Average True Range) multipliers adjusted by volume and percentile factors, ensuring adaptability to diverse market conditions. This multifaceted strategy not only improves signal accuracy but also optimizes risk management, distinguishing it from conventional trading methods.

BTCUSD 6hr performance

Disable the visualization of Bull Bear Power (BBP) to clearly view the Z-Score.

█ Strategy, How it Works: Detailed Explanation

The BBP Strategy with Volume-Percentile TP utilizes several interconnected components to analyze market data and generate trading signals. Here's an overview with essential equations:

🔶 Core Indicators and Calculations

1. Exponential Moving Average (EMA):

- **Purpose:** Smoothens price data to identify trends.

- **Formula:**

EMA_t = (Close_t * (2 / (lengthInput + 1))) + (EMA_(t-1) * (1 - (2 / (lengthInput + 1))))

- Usage: Baseline for Bull and Bear Power.

2. Bull and Bear Power:

- Bull Power: `BullPower = High_t - EMA_t`

- Bear Power: `BearPower = Low_t - EMA_t`

- BBP:** `BBP = BullPower + BearPower`

- Interpretation: Positive BBP indicates bullish strength, negative indicates bearish.

3. Z-Score Calculation:

- Purpose: Normalizes BBP to assess deviation from the mean.

- Formula:

Z-Score = (BBP_t - bbp_mean) / bbp_std

- Components:

- `bbp_mean` = SMA of BBP over `zLength` periods.

- `bbp_std` = Standard deviation of BBP over `zLength` periods.

- Usage: Identifies overbought or oversold conditions based on thresholds.

🔶 Volume Analysis

1. Volume Moving Average (`vol_sma`):

vol_sma = (Volume_1 + Volume_2 + ... + Volume_vol_period) / vol_period

2. Volume Multiplier (`vol_mult`):

vol_mult = Current Volume / vol_sma

- Thresholds:

- High Volume: `vol_mult > 2.0`

- Medium Volume: `1.5 < vol_mult ≤ 2.0`

- Low Volume: `1.0 < vol_mult ≤ 1.5`

🔶 Percentile Analysis

1. Percentile Calculation (`calcPercentile`):

Percentile = (Number of values ≤ Current Value / perc_period) * 100

2. Thresholds:

- High Percentile: >90%

- Medium Percentile: >80%

- Low Percentile: >70%

🔶 Dynamic Take-Profit Mechanism

1. ATR-Based Targets:

TP1 Price = Entry Price ± (ATR * atrMult1 * TP_Factor)

TP2 Price = Entry Price ± (ATR * atrMult2 * TP_Factor)

TP3 Price = Entry Price ± (ATR * atrMult3 * TP_Factor)

- ATR Calculation:

ATR_t = (True Range_1 + True Range_2 + ... + True Range_baseAtrLength) / baseAtrLength

2. Adjustment Factors:

TP_Factor = (vol_score + price_score) / 2

- **vol_score** and **price_score** are based on current volume and price percentiles.

Local performance

🔶 Entry and Exit Logic

1. Long Entry: If Z-Score crosses above 1.618, then Enter Long.

2. Short Entry: If Z-Score crosses below -1.618, then Enter Short.

3. Exiting Positions:

If Long and Z-Score crosses below 0:

Exit Long

If Short and Z-Score crosses above 0:

Exit Short

4. Take-Profit Execution:

- Set multiple exit orders at dynamically calculated TP levels based on ATR and adjusted by `TP_Factor`.

█ Trade Direction

The strategy determines trade direction using the Z-Score from the BBP indicator:

- Long Positions:

- Condition: Z-Score crosses above 1.618.

- Short Positions:

- Condition: Z-Score crosses below -1.618.

- Exiting Trades:

- Long Exit: Z-Score drops below 0.

- Short Exit: Z-Score rises above 0.

This approach aligns trades with prevailing market trends, increasing the likelihood of successful outcomes.

█ Usage

Implementing the BBP Strategy with Volume-Percentile TP in TradingView involves:

1. Adding the Strategy:

- Copy the Pine Script code.

- Paste it into TradingView's Pine Editor.

- Save and apply the strategy to your chart.

2. Configuring Settings:

- Adjust parameters like EMA length, Z-Score thresholds, ATR multipliers, volume periods, and percentile settings to match your trading preferences and asset behavior.

3. Backtesting:

- Use TradingView’s backtesting tools to evaluate historical performance.

- Analyze metrics such as profit factor, drawdown, and win rate.

4. Optimization:

- Fine-tune parameters based on backtesting results.

- Test across different assets and timeframes to enhance adaptability.

5. Deployment:

- Apply the strategy in a live trading environment.

- Continuously monitor and adjust settings as market conditions change.

█ Default Settings

The BBP Strategy with Volume-Percentile TP includes default parameters designed for balanced performance across various markets. Understanding these settings and their impact is essential for optimizing strategy performance:

Bull Bear Power Settings:

- EMA Length (`lengthInput`): 21

- **Effect:** Balances sensitivity and trend identification; shorter lengths respond quicker but may generate false signals.

- Z-Score Length (`zLength`): 252

- **Effect:** Long period for stable mean and standard deviation, reducing false signals but less responsive to recent changes.

- Z-Score Threshold (`zThreshold`): 1.618

- **Effect:** Higher threshold filters out weaker signals, focusing on significant market moves.

Take Profit Settings:

- Use Take Profit (`useTP`): Enabled (`true`)

- **Effect:** Activates dynamic profit-taking, enhancing profitability and risk management.

- ATR Period (`baseAtrLength`): 20

- **Effect:** Shorter period for sensitive volatility measurement, allowing tighter profit targets.

- ATR Multipliers:

- **Effect:** Define conservative to aggressive profit targets based on volatility.

- Position Sizes:

- **Effect:** Diversifies profit-taking across multiple levels, balancing risk and reward.

Volume Analysis Settings:

- Volume MA Period (`vol_period`): 100

- **Effect:** Longer period for stable volume average, reducing the impact of short-term spikes.

- Volume Multipliers:

- **Effect:** Determines volume conditions affecting take-profit adjustments.

- Volume Factors:

- **Effect:** Adjusts ATR multipliers based on volume strength.

Percentile Analysis Settings:

- Percentile Period (`perc_period`): 100

- **Effect:** Balances historical context with responsiveness to recent data.

- Percentile Thresholds:

- **Effect:** Defines price and volume percentile levels influencing take-profit adjustments.

- Percentile Factors:

- **Effect:** Modulates ATR multipliers based on price percentile strength.

Impact on Performance:

- EMA Length: Shorter EMAs increase sensitivity but may cause more false signals; longer EMAs provide stability but react slower to market changes.

- Z-Score Parameters:*Longer Z-Score periods create more stable signals, while higher thresholds reduce trade frequency but increase signal reliability.

- ATR Multipliers and Position Sizes: Higher multipliers allow for larger profit targets with increased risk, while diversified position sizes help in securing profits at multiple levels.

- Volume and Percentile Settings: These adjustments ensure that take-profit targets adapt to current market conditions, enhancing flexibility and performance across different volatility environments.

- Commission and Slippage: Accurate settings prevent overestimation of profitability and ensure the strategy remains viable after accounting for trading costs.

Conclusion

The BBP Strategy with Volume-Percentile TP offers a robust framework by combining BBP indicators with volume and percentile analyses. Its dynamic take-profit mechanism, tailored through ATR adjustments, ensures that traders can effectively capture profits while managing risks in varying market conditions.

TradeShields Strategy Builder🛡 WHAT IS TRADESHIELDS?

This no-code strategy builder is designed for traders on TradingView, offering an intuitive platform to create, backtest, and automate trading strategies. While identifying signals is often straightforward, the real challenge in trading lies in managing risk and knowing when not to trade. It equips users with advanced tools to address this challenge, promoting disciplined decision-making and structured trading practices.

This is not just a collection of indicators but a comprehensive toolkit that helps identify high-quality opportunities while placing risk management at the core of every strategy. By integrating customizable filters, robust controls, and automation capabilities, it empowers traders to align their strategies with their unique objectives and risk tolerance.

_____________________________________

🛡 THE GOAL: SHIELD YOUR STRATEGY

The mission is simple: to shield your strategy from bad trades . Whether you're a seasoned trader or just starting, the hardest part of trading isn’t finding signals—it’s avoiding trades that can harm your account. This framework prioritizes quality over quantity , helping filter out suboptimal setups and encouraging disciplined execution.

With tools to manage risk, avoid overtrading, and adapt to changing market conditions, it protects your strategy against impulsive decisions and market volatility.

_____________________________________

🛡 HOW TO USE IT

1. Apply Higher Timeframe Filters

Begin by analyzing broader market trends using tools like the 200 EMA, Ichimoku Cloud, or Supertrend on higher timeframes (e.g., daily or 4-hour charts).

- Example: Ensure the price is above the 200 EMA on the daily chart for long trades or below it for short trades.

2. Identify the Appropriate Entry Signal

Choose an entry signal that aligns with your model and the asset you're trading. Options include:

Supertrend changes for trend reversals.

Bollinger Band touches for mean-reversion trades.

RSI strength/weakness for overbought or oversold conditions.

Breakouts of key levels (e.g., daily or weekly highs/lows) for momentum trades.

MACD and TSI flips.

3. Determine Take-Profit and Stop-Loss Levels

Set clear exit strategies to protect your capital and lock in profits:

Use single, dual, or triple take-profit levels based on percentages or price levels.

Choose a stop-loss type, such as fixed percentage, ATR-based, or trailing stops.

Optionally, set breakeven adjustments after hitting your first take-profit target.

4. Apply Risk Management Filters

Incorporate risk controls to ensure disciplined execution:

Limit the number of trades per day, week, or month to avoid overtrading.

Use time-based filters to trade during specific sessions or custom windows.

Avoid trading around high-impact news events with region-specific filters.

5. Automate and Execute

Leverage the advanced automation features to streamline execution. Alerts are tailored specifically for each supported platform, ensuring seamless integration with tools like PineConnector, 3Commas, Zapier, and more.

_____________________________________

🛡 CORE FOCUS: RISK MANAGEMENT, AUTOMATION, AND DISCIPLINED TRADING

This builder emphasizes quality over quantity, encouraging traders to approach markets with structure and control. Its innovative tools for risk management and automation help optimize performance while reducing effort, fostering consistency and long-term success.

_____________________________________

🛡 KEY FEATURES

General Settings

Theme Customization : Light and dark themes for a tailored interface.

Timezone Adjustment : Align session times and news schedules with your local timezone.

Position Sizing : Define lot sizes to manage risk effectively.

Directional Control : Choose between long-only, short-only, or both directions for trading.

Time Filters

Day-of-Week Selection : Enable or disable trading on specific days.

Session-Based Trading : Restrict trades to major market sessions (Asia, London, New York) or custom windows.

Custom Time Windows : Precisely control the timeframes for trade execution.

Risk Management Tools

Trade Limits : Maximum trades per day, week, or month to avoid overtrading.

Automatic Trade Closures : End-of-session, end-of-day, or end-of-week options.

Duration-Based Filters : Close trades if take-profit isn’t reached within a set timeframe or if they remain unprofitable beyond a specific duration.

Stop-Loss and Take-Profit Options : Fixed percentage or ATR-based stop-losses, single/dual/triple take-profit levels, and breakeven stop adjustments.

Economic News Filters

Region-Specific Filters : Exclude trades around major news events in regions like the USA, UK, Europe, Asia, or Oceania.

News Avoidance Windows : Pause trades before and after high-impact events or automatically close trades ahead of scheduled news releases.

Higher Timeframe Filters

Multi-Timeframe Tools : Leverage EMAs, Supertrend, or Ichimoku Cloud on higher timeframes (Daily, 4-hour, etc.) for trend alignment.

Chart Timeframe Filters

Precision Filtering : Apply EMA or ADX-based conditions to refine trade setups on current chart timeframes.

Entry Signals

Customizable Options : Choose from signals like Supertrend, Bollinger Bands, RSI, MACD, Ichimoku Cloud, or EMA pullbacks.

Indicator Parameter Overrides : Fine-tune default settings for specific signals.

Exit Settings

Flexible Take-Profit Targets : Single, dual, or triple targets. Exit at significant levels like daily/weekly highs or lows.

Stop-Loss Variability : Fixed, ATR-based, or trailing stop-loss options.

Alerts and Automation

Third-Party Integrations : Seamlessly connect with platforms like PineConnector, 3Commas, Zapier, and Capitalise.ai.

Precision-Formatted Alerts : Alerts are tailored specifically for each platform, ensuring seamless execution. For example:

- PineConnector alerts include risk-per-trade parameters.

- 3Commas alerts contain bot-specific configurations.

_____________________________________

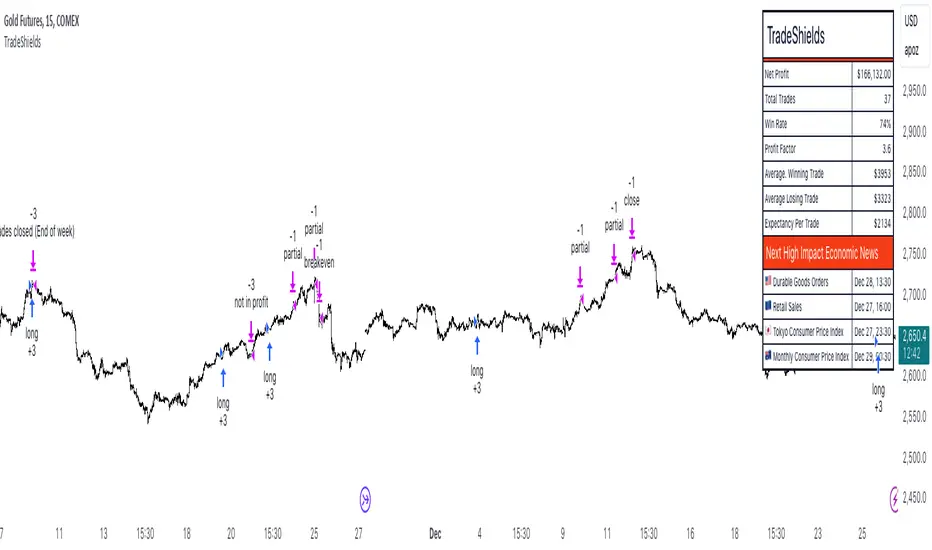

🛡 PUBLISHED CHART SETTINGS: 15m COMEX:GC1!

Time Filters : Trades are enabled from Tuesday to Friday, as Mondays often lack sufficient data coming off the weekend, and weekends are excluded due to market closures. Custom time sessions are turned off by default, allowing trades throughout the day.

Risk Filters : Risk is tightly controlled by limiting trades to a maximum of 2 per day and enabling a mechanism to close trades if they remain open too long and are unprofitable. Weekly trade closures ensure that no positions are carried over unnecessarily.

Economic News Filters : By default, trades are allowed during economic news periods, giving traders flexibility to decide how to handle volatility manually. It is recommended to enable these filters if you are creating strategies on lower timeframes.

Higher Timeframe Filters : The setup incorporates confluence from higher timeframe indicators. For example, the 200 EMA on the daily timeframe is used to establish trend direction, while the Ichimoku cloud on the 30-minute timeframe adds additional confirmation.

Entry Signals : The strategy triggers trades based on changes in the Supertrend indicator.

Exit Settings : Trades are configured to take partial profits at three levels (1%, 2%, and 3%) and use a fixed stop loss of 2%. Stops are moved to breakeven after reaching the first take profit level.

_____________________________________

🛡 WHY CHOOSE THIS STRATEGY BUILDER?

This tool transforms trading from reactive to proactive, focusing on risk management and automation as the foundation of every strategy. By helping users avoid unnecessary trades, implement robust controls, and automate execution, it fosters disciplined trading.

McClellan A-D Volume Integration ModelThe strategy integrates the McClellan A-D Oscillator with an adjustment based on the Advance/Decline (A-D) volume data. The McClellan Oscillator is calculated by taking the difference between the short-term and long-term exponential moving averages (EMAs) of the A-D line. This strategy introduces an enhancement where the A-D volume (the difference between the advancing and declining volume) is factored in to adjust the oscillator value.

Inputs:

• ema_short_length: The length for the short-term EMA of the A-D line.

• ema_long_length: The length for the long-term EMA of the A-D line.

• osc_threshold_long: The threshold below which the oscillator must drop for an entry signal to trigger.

• exit_periods: The number of periods after which the position is closed.

• Data Sources:

• ad_advance and ad_decline are the data sources for advancing and declining issues, respectively.

• vol_advance and vol_decline are the volume data for the advancing and declining issues. If volume data is unavailable, it defaults to na (Not Available), and the fallback logic ensures that the strategy continues to function.

McClellan Oscillator with Volume Adjustment:

• The A-D line is calculated by subtracting the declining issues from the advancing issues. Then, the volume difference is applied to this line, creating a “weighted” A-D line.

• The short and long EMAs are calculated for the weighted A-D line to generate the McClellan Oscillator.

Entry Condition:

• The strategy looks for a reversal signal, where the oscillator falls below the threshold and then rises above it again. The condition is designed to trigger a long position when this reversal happens.

Exit Condition:

• The position is closed after a set number of periods (exit_periods) have passed since the entry.

Plotting:

• The McClellan Oscillator and the threshold are plotted on the chart for visual reference.

• Entry and exit signals are highlighted with background colors to make the signals more visible.

Scientific Background:

The McClellan A-D Oscillator is a popular market breadth indicator developed by Sherman and Marian McClellan. It is used to gauge the underlying strength of a market by analyzing the difference between the number of advancing and declining stocks. The oscillator is typically calculated using exponential moving averages (EMAs) of the A-D line, with the idea being that crossovers of these EMAs indicate potential changes in the market’s direction.

The integration of A-D volume into this model adds another layer of analysis, as volume is often considered a leading indicator of price movement. By factoring in volume, the strategy becomes more sensitive to not just the number of advancing or declining stocks but also how significant those movements are based on trading volume, as discussed in Schwager, J. D. (1999). Technical Analysis of the Financial Markets. This enhanced version aims to capture stronger and more sustainable trends in the market, helping to filter out false signals.

Additionally, volume analysis is often used to confirm price movements, as described in Wyckoff, R. (1931). The Day Trading System. Therefore, incorporating the volume of advancing and declining stocks in the McClellan Oscillator offers a more robust signal for trading decisions.

Zero-Lag MA Trend FollowingScript Name: Zero-Lag MA Trend Following Auto-Trading

Purpose and Unique Features:

This script is designed to implement a trend-following auto-trading strategy by combining the Zero-Lag Moving Average (ZLMA), Exponential Moving Average (EMA), and ATR Bands. To differentiate it from similar scripts, the following key aspects are emphasized:

Zero-Lag MA (ZLMA):

Responds quickly to price changes, minimizing lag compared to EMA.

Detects crossovers with EMA and generates Diamond Signals to indicate trend reversals.

ATR Bands:

Measures market volatility to set stop-loss levels.

Helps optimize entry points and manage risk effectively.

Diamond Signals:

A vital visual cue indicating the early stages of trend reversals.

Green diamonds signal an uptrend, while red diamonds signal a downtrend.