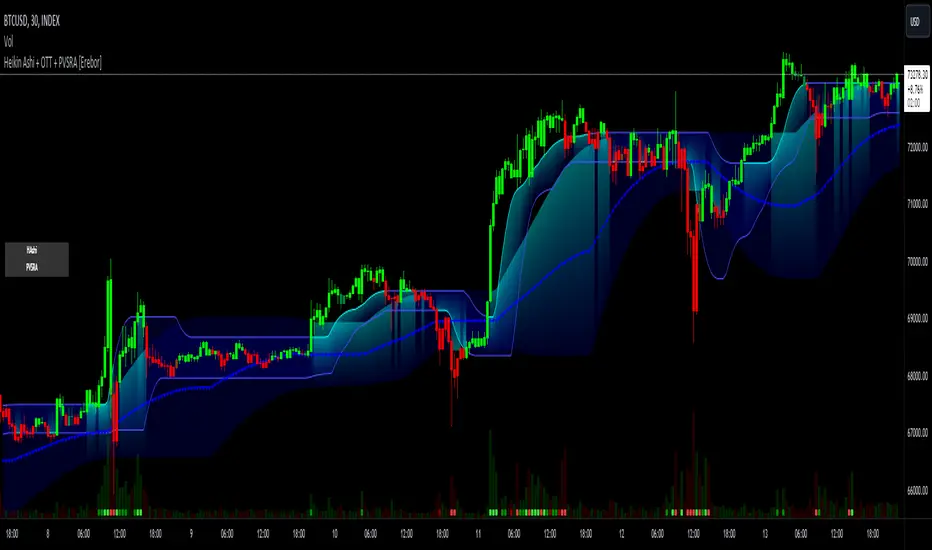

Heikin Ashi and Optimized Trend Tracker and PVSRA [Erebor]Heikin Ashi Candles

Let's consider a modification to the traditional “Heikin Ashi Candles” where we introduce a new parameter: the period of calculation. The traditional HA candles are derived from the open , high low , and close prices of the underlying asset.

Now, let's introduce a new parameter, period, which will determine how many periods are considered in the calculation of the HA candles. This period parameter will affect the smoothing and responsiveness of the resulting candles.

In this modification, instead of considering just the current period, we're averaging or aggregating the prices over a specified number of periods . This will result in candles that reflect a longer-term trend or sentiment, depending on the chosen period value.

For example, if period is set to 1, it would essentially be the same as traditional Heikin Ashi candles. However, if period is set to a higher value, say 5, each candle will represent the average price movement over the last 5 periods, providing a smoother representation of the trend but potentially with delayed signals compared to lower period values.

Traders can adjust the period parameter based on their trading style, the timeframe they're analyzing, and the level of smoothing or responsiveness they prefer in their candlestick patterns.

Optimized Trend Tracker

The "Optimized Trend Tracker" is a proprietary trading indicator developed by TradingView user ANIL ÖZEKŞİ. It is designed to identify and track trends in financial markets efficiently. The indicator attempts to smooth out price fluctuations and provide clear signals for trend direction.

The Optimized Trend Tracker uses a combination of moving averages and adaptive filters to detect trends. It aims to reduce lag and noise typically associated with traditional moving averages, thereby providing more timely and accurate signals.

Some of the key features and applications of the OTT include:

• Trend Identification: The indicator helps traders identify the direction of the prevailing trend in a market. It distinguishes between uptrends, downtrends, and sideways consolidations.

• Entry and Exit Signals: The OTT generates buy and sell signals based on crossovers and direction changes of the trend. Traders can use these signals to time their entries and exits in the market.

• Trend Strength: It also provides insights into the strength of the trend by analyzing the slope and momentum of price movements. This information can help traders assess the conviction behind the trend and adjust their trading strategies accordingly.

• Filter Noise: By employing adaptive filters, the indicator aims to filter out market noise and false signals, thereby enhancing the reliability of trend identification.

• Customization: Traders can customize the parameters of the OTT to suit their specific trading preferences and market conditions. This flexibility allows for adaptation to different timeframes and asset classes.

Overall, the OTT can be a valuable tool for traders seeking to capitalize on trending market conditions while minimizing false signals and noise. However, like any trading indicator, it is essential to combine its signals with other forms of analysis and risk management strategies for optimal results. Additionally, traders should thoroughly back-test the indicator and practice using it in a demo environment before applying it to live trading.

PVSRA (Price, Volume, S&R Analysis)

“PVSRA” (Price, Volume, S&R Analysis) is a trading methodology and indicator that combines the analysis of price action, volume, and support/resistance levels to identify potential trading opportunities in financial markets. It is based on the idea that price movements are influenced by the interplay between supply and demand, and analyzing these factors together can provide valuable insights into market dynamics.

Here's a breakdown of the components of PVSRA:

• Price Action Analysis: PVSRA focuses on analyzing price movements and patterns on price charts, such as candlestick patterns, trendlines, chart patterns (like head and shoulders, triangles, etc.), and other price-based indicators. Traders using PVSRA pay close attention to how price behaves at key support and resistance levels and look for patterns that indicate potential shifts in market sentiment.

• Volume Analysis: Volume is an essential component of PVSRA. Traders monitor changes in trading volume to gauge the strength or weakness of price movements. An increase in volume during a price move suggests strong participation and conviction from market participants, reinforcing the validity of the price action. Conversely, low volume during price moves may indicate lack of conviction and potential reversals.

• Support and Resistance (S&R) Analysis: PVSRA incorporates the identification and analysis of support and resistance levels on price charts. Support levels represent areas where buying interest is expected to be strong enough to prevent further price declines, while resistance levels represent areas where selling interest may prevent further price advances. These levels are often identified using historical price data, trendlines, moving averages, pivot points, and other technical analysis tools.

The PVSRA methodology combines these three elements to generate trading signals and make trading decisions. Traders using PVSRA typically look for confluence between price action, volume, and support/resistance levels to confirm trade entries and exits. For example, a bullish reversal signal may be considered stronger if it occurs at a significant support level with increasing volume.

It's important to note that PVSRA is more of a trading approach or methodology rather than a specific indicator with predefined rules. Traders may customize their analysis based on their preferences and trading style, incorporating additional technical indicators or filters as needed. As with any trading strategy, risk management and proper trade execution are essential components of successful trading with PVSRA.

The following types of moving average have been included: "SMA", "EMA", "SMMA (RMA)", "WMA", "VWMA", "HMA", "KAMA", "LSMA", "TRAMA", "VAR", "DEMA", "ZLEMA", "TSF", "WWMA". Thanks to the authors.

Thank you for your indicator “Optimized Trend Tracker”. © kivancozbilgic

Thank you for your indicator “PVSRA Volume Suite”. © creengrack

Thank you for your programming language, indicators and strategies. © TradingView

Kind regards.

© Erebor_GIT

Cerca negli script per "kama"

Adaptive Fisherized Z-scoreHello Fellas,

It's time for a new adaptive fisherized indicator of me, where I apply adaptive length and more on a classic indicator.

Today, I chose the Z-score, also called standard score, as indicator of interest.

Special Features

Advanced Smoothing: JMA, T3, Hann Window and Super Smoother

Adaptive Length Algorithms: In-Phase Quadrature, Homodyne Discriminator, Median and Hilbert Transform

Inverse Fisher Transform (IFT)

Signals: Enter Long, Enter Short, Exit Long and Exit Short

Bar Coloring: Presents the trade state as bar colors

Band Levels: Changes the band levels

Decision Making

When you create such a mod you need to think about which concepts are the best to conclude. I decided to take Inverse Fisher Transform instead of normalization to make a version which fits to a fixed scale to avoid the usual distortion created by normalization.

Moreover, I chose JMA, T3, Hann Window and Super Smoother, because JMA and T3 are the bleeding-edge MA's at the moment with the best balance of lag and responsiveness. Additionally, I chose Hann Window and Super Smoother because of their extraordinary smoothing capabilities and because Ehlers favours them.

Furthermore, I decided to choose the half length of the dominant cycle instead of the full dominant cycle to make the indicator more responsive which is very important for a signal emitter like Z-score. Signal emitters always need to be faster or have the same speed as the filters they are combined with.

Usage

The Z-score is a low timeframe scalper which works best during choppy/ranging phases. The direction you should trade is determined by the last trend change. E.g. when the last trend change was from bearish market to bullish market and you are now in a choppy/ranging phase confirmed by e.g. Chop Zone or KAMA slope you want to do long trades.

Interpretation

The Z-score indicator is a momentum indicator which shows the number of standard deviations by which the value of a raw score (price/source) is above or below the mean value of what is being observed or measured. Easily explained, it is almost the same as Bollinger Bands with another visual representation form.

Signals

B -> Buy -> Z-score crosses above lower band

S -> Short -> Z-score crosses below upper band

BE -> Buy Exit -> Z-score crosses above 0

SE -> Sell Exit -> Z-score crosses below 0

If you were reading till here, thank you already. Now, follows a bunch of knowledge for people who don't know the concepts I talk about.

T3

The T3 moving average, short for "Tim Tillson's Triple Exponential Moving Average," is a technical indicator used in financial markets and technical analysis to smooth out price data over a specific period. It was developed by Tim Tillson, a software project manager at Hewlett-Packard, with expertise in Mathematics and Computer Science.

The T3 moving average is an enhancement of the traditional Exponential Moving Average (EMA) and aims to overcome some of its limitations. The primary goal of the T3 moving average is to provide a smoother representation of price trends while minimizing lag compared to other moving averages like Simple Moving Average (SMA), Weighted Moving Average (WMA), or EMA.

To compute the T3 moving average, it involves a triple smoothing process using exponential moving averages. Here's how it works:

Calculate the first exponential moving average (EMA1) of the price data over a specific period 'n.'

Calculate the second exponential moving average (EMA2) of EMA1 using the same period 'n.'

Calculate the third exponential moving average (EMA3) of EMA2 using the same period 'n.'

The formula for the T3 moving average is as follows:

T3 = 3 * (EMA1) - 3 * (EMA2) + (EMA3)

By applying this triple smoothing process, the T3 moving average is intended to offer reduced noise and improved responsiveness to price trends. It achieves this by incorporating multiple time frames of the exponential moving averages, resulting in a more accurate representation of the underlying price action.

JMA

The Jurik Moving Average (JMA) is a technical indicator used in trading to predict price direction. Developed by Mark Jurik, it’s a type of weighted moving average that gives more weight to recent market data rather than past historical data.

JMA is known for its superior noise elimination. It’s a causal, nonlinear, and adaptive filter, meaning it responds to changes in price action without introducing unnecessary lag. This makes JMA a world-class moving average that tracks and smooths price charts or any market-related time series with surprising agility.

In comparison to other moving averages, such as the Exponential Moving Average (EMA), JMA is known to track fast price movement more accurately. This allows traders to apply their strategies to a more accurate picture of price action.

Inverse Fisher Transform

The Inverse Fisher Transform is a transform used in DSP to alter the Probability Distribution Function (PDF) of a signal or in our case of indicators.

The result of using the Inverse Fisher Transform is that the output has a very high probability of being either +1 or –1. This bipolar probability distribution makes the Inverse Fisher Transform ideal for generating an indicator that provides clear buy and sell signals.

Hann Window

The Hann function (aka Hann Window) is named after the Austrian meteorologist Julius von Hann. It is a window function used to perform Hann smoothing.

Super Smoother

The Super Smoother uses a special mathematical process for the smoothing of data points.

The Super Smoother is a technical analysis indicator designed to be smoother and with less lag than a traditional moving average.

Adaptive Length

Length based on the dominant cycle length measured by a "dominant cycle measurement" algorithm.

Happy Trading!

Best regards,

simwai

---

Credits to

@cheatcountry

@everget

@loxx

@DasanC

@blackcat1402

TASC 2024.01 Gap Momentum System█ OVERVIEW

TASC's January 2024 edition of Traders' Tips features an article titled “Gap Momentum” by Perry J. Kaufman. The article discusses how a trader might create a momentum strategy based on opening gap data. This script implements the Gap Momentum system presented therein.

█ CONCEPTS

In the article, Perry J. Kaufman introduces Gap Momentum as a cumulative series constructed in the same way as On-Balance Volume (OBV) , but using gap openings (today’s open minus yesterday’s close).

To smoothen the resulting time series (i.e., obtain the " signal line "), the author applies a simple moving average . Subsequently, he proposes the following two trading rules for a long-only trading system:

• Enter a long position when the signal line is moving higher.

• Exit when the signal line is moving lower.

█ CALCULATIONS

The calculation of Gap Momentum involves the following steps:

1. Calculate the ratio of the sum of positive gaps over the past N days to the sum of negative gaps (absolute values) over the same time period.

2. Add the resulting gap ratio to the cumulative time series. This time series is the Gap Momentum.

3. Keep moving forward, as in an N-day moving average.

Kaufman Efficiency Ratio (KER)The Kaufman Efficiency Ratio (also known as the Efficiency Ratio or ER) is a technical indicator used in technical analysis to measure the efficiency of a financial instrument's price movement. It was developed by Perry J. Kaufman and is designed to help traders and analysts identify the trendiness or choppiness of a market.

The Kaufman Efficiency Ratio is calculated using the following formula:

ER = (Change in Price over N periods) / (Sum of the absolute price changes over N periods)

Here's how the formula works:

"Change in Price over N periods" is the net price change over a specified number of periods (usually days or bars). It's calculated by subtracting the closing price of N periods ago from the current closing price.

"Sum of the absolute price changes over N periods" is the sum of the absolute values of price changes (i.e., ignoring the direction) over the same N periods.

The resulting Efficiency Ratio (ER) value will fall within the range of 0 to 1, with 1 indicating a perfectly trending market and 0 indicating a perfectly choppy or range-bound market. In other words, the closer the ER is to 1, the stronger and more efficient the trend is perceived to be.

[AIO] Multi Collection Moving Averages 140 MA TypesAll In One Multi Collection Moving Averages.

Since signing up 2 years ago, I have been collecting various Сollections.

I decided to get it into a decent shape and make it one of the biggest collections on TV, and maybe the entire internet.

And now I'm sharing my collection with you.

140 Different Types of Moving Averages are waiting for you.

Specifically :

"

AARMA | Adaptive Autonomous Recursive Moving Average

ADMA | Adjusted Moving Average

ADXMA | Average Directional Moving Average

ADXVMA | Average Directional Volatility Moving Average

AHMA | Ahrens Moving Average

ALF | Ehler Adaptive Laguerre Filter

ALMA | Arnaud Legoux Moving Average

ALSMA | Adaptive Least Squares

ALXMA | Alexander Moving Average

AMA | Adaptive Moving Average

ARI | Unknown

ARSI | Adaptive RSI Moving Average

AUF | Auto Filter

AUTL | Auto-Line

BAMA | Bryant Adaptive Moving Average

BFMA | Blackman Filter Moving Average

CMA | Corrected Moving Average

CORMA | Correlation Moving Average

COVEMA | Coefficient of Variation Weighted Exponential Moving Average

COVNA | Coefficient of Variation Weighted Moving Average

CTI | Coral Trend Indicator

DEC | Ehlers Simple Decycler

DEMA | Double EMA Moving Average

DEVS | Ehlers - Deviation Scaled Moving Average

DONEMA | Donchian Extremum Moving Average

DONMA | Donchian Moving Average

DSEMA | Double Smoothed Exponential Moving Average

DSWF | Damped Sine Wave Weighted Filter

DWMA | Double Weighted Moving Average

E2PBF | Ehlers 2-Pole Butterworth Filter

E2SSF | Ehlers 2-Pole Super Smoother Filter

E3PBF | Ehlers 3-Pole Butterworth Filter

E3SSF | Ehlers 3-Pole Super Smoother Filter

EDMA | Exponentially Deviating Moving Average (MZ EDMA)

EDSMA | Ehlers Dynamic Smoothed Moving Average

EEO | Ehlers Modified Elliptic Filter Optimum

EFRAMA | Ehlers Modified Fractal Adaptive Moving Average

EHMA | Exponential Hull Moving Average

EIT | Ehlers Instantaneous Trendline

ELF | Ehler Laguerre filter

EMA | Exponential Moving Average

EMARSI | EMARSI

EPF | Edge Preserving Filter

EPMA | End Point Moving Average

EREA | Ehlers Reverse Exponential Moving Average

ESSF | Ehlers Super Smoother Filter 2-pole

ETMA | Exponential Triangular Moving Average

EVMA | Elastic Volume Weighted Moving Average

FAMA | Following Adaptive Moving Average

FEMA | Fast Exponential Moving Average

FIBWMA | Fibonacci Weighted Moving Average

FLSMA | Fisher Least Squares Moving Average

FRAMA | Ehlers - Fractal Adaptive Moving Average

FX | Fibonacci X Level

GAUS | Ehlers - Gaussian Filter

GHL | Gann High Low

GMA | Gaussian Moving Average

GMMA | Geometric Mean Moving Average

HCF | Hybrid Convolution Filter

HEMA | Holt Exponential Moving Average

HKAMA | Hilbert based Kaufman Adaptive Moving Average

HMA | Harmonic Moving Average

HSMA | Hirashima Sugita Moving Average

HULL | Hull Moving Average

HULLT | Hull Triple Moving Average

HWMA | Henderson Weighted Moving Average

IE2 | Early T3 by Tim Tilson

IIRF | Infinite Impulse Response Filter

ILRS | Integral of Linear Regression Slope

JMA | Jurik Moving Average

KA | Unknown

KAMA | Kaufman Adaptive Moving Average & Apirine Adaptive MA

KIJUN | KIJUN

KIJUN2 | Kijun v2

LAG | Ehlers - Laguerre Filter

LCLSMA | 1LC-LSMA (1 line code lsma with 3 functions)

LEMA | Leader Exponential Moving Average

LLMA | Low-Lag Moving Average

LMA | Leo Moving Average

LP | Unknown

LRL | Linear Regression Line

LSMA | Least Squares Moving Average / Linear Regression Curve

LTB | Unknown

LWMA | Linear Weighted Moving Average

MAMA | MAMA - MESA Adaptive Moving Average

MAVW | Mavilim Weighted Moving Average

MCGD | McGinley Dynamic Moving Average

MF | Modular Filter

MID | Median Moving Average / Percentile Nearest Rank

MNMA | McNicholl Moving Average

MTMA | Unknown

MVSMA | Minimum Variance SMA

NLMA | Non-lag Moving Average

NWMA | Dürschner 3rd Generation Moving Average (New WMA)

PKF | Parametric Kalman Filter

PWMA | Parabolic Weighted Moving Average

QEMA | Quadruple Exponential Moving Average

QMA | Quick Moving Average

REMA | Regularized Exponential Moving Average

REPMA | Repulsion Moving Average

RGEMA | Range Exponential Moving Average

RMA | Welles Wilders Smoothing Moving Average

RMF | Recursive Median Filter

RMTA | Recursive Moving Trend Average

RSMA | Relative Strength Moving Average - based on RSI

RSRMA | Right Sided Ricker MA

RWMA | Regressively Weighted Moving Average

SAMA | Slope Adaptive Moving Average

SFMA | Smoother Filter Moving Average

SMA | Simple Moving Average

SSB | Senkou Span B

SSF | Ehlers - Super Smoother Filter P2

SSMA | Super Smooth Moving Average

STMA | Unknown

SWMA | Self-Weighted Moving Average

SW_MA | Sine-Weighted Moving Average

TEMA | Triple Exponential Moving Average

THMA | Triple Exponential Hull Moving Average

TL | Unknown

TMA | Triangular Moving Average

TPBF | Three-pole Ehlers Butterworth

TRAMA | Trend Regularity Adaptive Moving Average

TSF | True Strength Force

TT3 | Tilson (3rd Degree) Moving Average

VAMA | Volatility Adjusted Moving Average

VAMAF | Volume Adjusted Moving Average Function

VAR | Vector Autoregression Moving Average

VBMA | Variable Moving Average

VHMA | Vertical Horizontal Moving Average

VIDYA | Variable Index Dynamic Average

VMA | Volume Moving Average

VSO | Unknown

VWMA | Volume Weighted Moving Average

WCD | Unknown

WMA | Weighted Moving Average

XEMA | Optimized Exponential Moving Average

ZEMA | Zero Lag Moving Average

ZLDEMA | Zero-Lag Double Exponential Moving Average

ZLEMA | Ehlers - Zero Lag Exponential Moving Average

ZLTEMA | Zero-Lag Triple Exponential Moving Average

ZSMA | Zero-Lag Simple Moving Average

"

Don't forget that you can use any Moving Average not only for the chart but also for any of your indicators without affecting the code as in my example.

But remember that some MAs are not designed to work with anything other than a chart.

All MA and Code lists are sorted strictly alphabetically by short name (A-Z).

Each MA has its own number (ID) by which you can display the Moving Average you need.

Next to the ID selection there are tooltips with short names and their numbers. Use them.

The panel below will help you to read the Name of the selected MA.

Because of the size of the collection I think this is the optimal and most convenient use. Correct me if this is not the case.

Unknown - Some MAs I collected so long ago that I lost the full real name and couldn't find the authors. If you recognize them, please let me know.

I have deliberately simplified all MAs to input just Source and Length.

Because the collection is so large, it would be quite inconvenient and difficult to customize all MA functions (multipliers, offset, etc.).

If you need or like any MA you will still have to take it from my collection for your code.

I tried to leave the basic MA settings inside function in first strings.

I have tried to list most of the authors, but since the bulk of the collection was created a long time ago and was not intended for public publication I could not find all of them.

Some of the features were created from scratch or may have been slightly modified, so please be careful.

If you would like to improve this collection, please write to me in PM.

Also Credits, Likes, Awards, Loves and Thanks to :

@alexgrover

@allanster

@andre_007

@auroagwei

@blackcat1402

@bsharpe

@cheatcountry

@CrackingCryptocurrency

@Duyck

@ErwinBeckers

@everget

@glaz

@gotbeatz26107

@HPotter

@io72signals

@JacobAmos

@JoshuaMcGowan

@KivancOzbilgic

@LazyBear

@loxx

@LuxAlgo

@MightyZinger

@nemozny

@NGBaltic

@peacefulLizard50262

@RicardoSantos

@StalexBot

@ThiagoSchmitz

@TradingView

— 𝐀𝐧𝐝 𝐎𝐭𝐡𝐞𝐫𝐬 !

So just a Big Thank You to everyone who has ever and anywhere shared their codes.

CE - 42MACRO Equity Factor Table This is Part 1 of 2 from the 42MACRO Recreation Series

The CE - 42MACRO Equity Factor Table is a whole toolbox packaged in a single indicator.

It aims to provide a probabilistic insight into the market realized GRID Macro Regime, use a multiplex of important Assets and Indices to form a high probability Implied Correlation expectation and allows to derive extra market insights by showing the most important aggregates and their performance over multiple timeframes... and what that might mean for the whole market direction, as well as the underlying asset.

WARNING

By the nature of the macro regimes, the outcomes are more accurate over longer Chart Timeframes (Week to Months).

However, it is also a valuable tool to form a proper,

market realized, short to medium term bias.

NOTE

This Indicator is intended to be used alongside the 2nd part "CE - 42MACRO Yield and Macro"

for a more wholistic approach and higher accuracy.

Due to coding limitations they can not be merged into one Indicator.

Methodology:

The Equity Factor Table tracks specifically chosen Assets to identify their performance and add the combined performances together to visualize 42MACRO's GRID Equity Model.

For this it uses the below Assets, with more to come:

Dividend Compounders ( AMEX:SPHD )

Mid Caps ( AMEX:VO )

Emerging Markets ( AMEX:EEM )

Small Caps ( AMEX:IWM )

Mega Cap Growth ( NASDAQ:QQQ )

Brazil ( AMEX:EWZ )

United Kingdom ( AMEX:EWU )

Growth ( AMEX:IWF )

United States ( AMEX:SPY )

Japan ( AMEX:DXJ )

Momentum ( AMEX:MTUM )

China ( AMEX:FXI )

Low Beta ( AMEX:SPLV )

International ex-US ( NASDAQ:ACWX )

India ( AMEX:INDA )

Eurozone ( AMEX:EZU )

Quality ( AMEX:QUAL )

Size ( AMEX:OEF )

Functionalities:

1. Correlations

Takes a measure of Cross Market Correlations

2. Implied Trend

Calculates the trend for each Asset and uses the Correlation to obtain the Implied Trend for the underlying Asset

There are multiple functionalities to enhance Signal Speed and precision...

Reading a signal only over a certain threshold, otherwise being colored in gray to signal noise or unclear market behavior

Normalization of Signal

Double Normalization of Signal for more Speed... ideal for the Crypto Market

Using an additional Hull Moving Average to enhance Signal Speed

Additional simple Background coloring to get a Signal from the HMA

Barcoloring based on the Implied Correlation

3. Equity Factor Table

Shows market realized Asset performance

Provides the approximate realized GRID market regimes

Informs about "Risk ON" and "Risk OFF" market states

Now into the juicy stuff...

Visuals:

There is a variety of options to change visual settings of what is plotted and where

+ additional considerations.

Everything that is relevant in the underlying logic which can improve comprehension can be visualized with these options.

More to come

Market Correlation:

The Market Correlation Table takes the Correlation of all the Assets to the Asset on the Chart,

it furthermore uses the Normalized KAMA Oscillator by IkkeOmar to analyse the current trend of every single Asset.

(To enhance the Signal you can apply the mentioned Indicator on the relevant Assets to find your target Asset movements that you intend to capture...

and then change the length of the Indicator in here)

It then Implies a Correlation based on the Trend and the Correlation to give a probabilistically adjusted expectation for the future Chart Asset Movement.

This is strengthened by taking the average of all Implied Trends.

Thus the Correlation Table provides valuable insights about probabilistically likely Movement of the Asset over the defined time duration,

providing alpha for Traders and Investors alike.

Equity Factors:

The table provides valuable information about the current market environment (whether it's risk on or risk off),

the rough GRID models from 42MACRO and the actual market performance.

This allows you to obtain a deeper understanding of how the market works and makes it simple to identify the actual market direction,

makes it possible to derive overall market Health and shows market strength or weakness.

Utility:

The Equity Factor Table is divided in 4 Sections which are the GRID regimes:

Economic Growth:

Goldilocks

Reflation

Economic Contraction:

Inflation

Deflation

Top 5 Equity Factors:

Are the values green for a specific Column?

If so then the market reflects the corresponding GRID behavior.

Bottom 5 Equity Factors:

Are the values red for a specific Column?

If so then the market reflects the corresponding GRID behavior.

So if we have Goldilocks as current regime we would see green values in the Top 5 Goldilocks Cells and red values in the Bottom 5 Goldilocks Cells.

You will find that Reflation will look similar, as it is also a sign of Economic Growth.

Same is the case for the two Contraction regimes.

This whole Indicator, as well as the second part, is based to a majority on 42MACRO's models.

I only brought them into TV and added things on top of it.

If you have questions or need a more in-depth guide DM me.

Will make a guide to all functionalities if necessity becomes apparent.

GM

Auto-Length Adaptive ChannelsIntroduction

The key innovation of the ALAC is the implementation of dynamic length identification, which allows the indicator to adjust to the "market beat" or dominant cycle in real-time.

The Auto-Length Adaptive Channels (ALAC) is a flexible technical analysis tool that combines the benefits of five different approaches to market band and price deviation calculations.

Traders often tend to overthink of what length their indicators should use, and this is the main idea behind this script. It automatically calculates length based on pivot points, averaging the distance that is in between of current market highs and lows.

This approach is very helpful to identify market deviations, because deviations are always calculated and compared to previous market behavior.

How it works

The indicator uses a Detrended Rhythm Oscillator (DRO) to identify the dominant cycle in the market. This length information is then used to calculate different market bands and price deviations. The ALAC combines five different methodologies to compute these bands:

1 - Bollinger Bands

2 - Keltner Channels

3 - Envelope

4 - Average True Range Channels

5 - Donchian Channels

By averaging these calculations, the ALAC produces an overall market band that generalizes the approaches of these five methods into a single, adaptive channel.

How to Use

When the price is at the upper band, this might suggest that the asset is overbought and may be due for a price correction. Conversely, when the price is at the lower band, the asset may be oversold and due for a price increase.

The space between the bands represents the market's volatility. Wider bands indicate higher volatility, while narrower bands suggest lower volatility.

Indicator Settings

The settings of the ALAC allow for customization to suit different trading strategies:

Use Autolength?: This allows the indicator to automatically adjust the length of the dominant cycle.

Usual Length: If "Use Autolength?" is disabled, this setting allows the user to manually specify the length of the cycle.

Moving Average Type: This selects the type of moving average to be used in the calculations. Options include SMA, EMA, ALMA, DEMA, JMA, KAMA, SMMA, TMA, TSF, VMA, VAMA, VWMA, WMA, and ZLEMA.

Channel Multiplier: This adjusts the distance between the bands.

Channel Multiplier Step: This changes the step size of the channel multiplier. Each next market band will be multiplied by a previous one. You can potentially use values below 1, which will plot bands inside the first, main channel.

Use DPO instead of source data?: This setting uses the DPO for calculations instead of the source data. Basically, this is how you can add or eliminate trend from calculation of an average leg-up / leg-down move.

Fast: This adjusts the fast length of the DPO.

Slow: This adjusts the slow length of the DPO.

Zig-zag Period: This adjusts the period of the zig-zag pattern used in the DPO.

(!) For more information about DPO visit official TradingView description here: link

Also, I want to say thanks to @StockMarketCycles for initial idea of Detrended Rhythm Oscillator (DRO) that I use in this script.

The Adaptive Average Channel is a powerful and versatile indicator that combines the strengths of multiple technical analysis methods.

In summary, with the ALAC, you can:

1 - Dynamically adapt to any asset and price action with automatic calculation of dominant cycle lengths.

2 - Identify potential overbought and oversold conditions with the adaptive market bands.

3 - Customize your analysis with various settings, including moving average type and channel multiplier.

4 - Enhance your trading strategy by using the indicator in conjunction with other forms of analysis.

CE - Market Performance TableThe 𝓜𝓪𝓻𝓴𝓮𝓽 𝓟𝓮𝓻𝓯𝓸𝓻𝓶𝓪𝓷𝓬𝓮 𝓣𝓪𝓫𝓵𝓮 is a sophisticated market tool designed to provide valuable insights into the current market trends and the approximate current position in the Macroeconomic Regime.

Furthermore the 𝓜𝓪𝓻𝓴𝓮𝓽 𝓟𝓮𝓻𝓯𝓸𝓻𝓶𝓪𝓷𝓬𝓮 𝓣𝓪𝓫𝓵𝓮 provides the Correlation Implied Trend for the Asset on the Chart. Lastly it provides information about current "RISK ON" or "RISK OFF" periods.

Methodology:

𝓜𝓪𝓻𝓴𝓮𝓽 𝓟𝓮𝓻𝓯𝓸𝓻𝓶𝓪𝓷𝓬𝓮 𝓣𝓪𝓫𝓵𝓮 tracks the 15 underlying Stock ETF's to identify their performance and puts the combined performances together to visualize 42MACRO's GRID Equity Model.

For this it uses the below ETF's:

Dividends (SPHD)

Low Beta (SPLV)

Quality (QUAL)

Defensives (DEF)

Growth (IWF)

High Beta (SPHB)

Cyclicals (IYT, IWN)

Value (IWD)

Small Caps (IWM)

Mid Caps (IWR)

Mega Cap Growth (MGK)

Size (OEF)

Momentum (MTUM)

Large Caps (IWB)

Overall Settings:

The main time values you want to change are:

Correlation Length

- Defines the time horizon for the Correlation Table

ROC Period

- Defines the time horizon for the Performance Table

Normalization lookback

- Defines the time horizon for the Trend calculation of the ETF's

- For longer term Trends over weeks or months a length of 50 is usually pretty accurate

Visuals:

There is a variety of options to change the visual settings of what is being plotted and the two table positions and additional considerations.

Everything that is relevant in the underlying logic that can help comprehension can be visualized with these options.

Market Correlation:

The Market Correlation Table takes the Correlation of the above ETF's to the Asset on the Chart, it furthermore uses the Normalized KAMA Oscillator by IkkeOmar to analyse the current trend of every single ETF.

It then Implies a Correlation based on the Trend and the Correlation to give a probabilistically adjusted expectation for the future Chart Asset Movement. This is strengthened by taking the average of all Implied Trends.

With this the Correlation Table provides valuable insights about probabilistically likely Movement of the Asset, for Traders and Investors alike, over the defined time duration.

Market Performance:

𝓜𝓪𝓻𝓴𝓮𝓽 𝓟𝓮𝓻𝓯𝓸𝓻𝓶𝓪𝓷𝓬𝓮 𝓣𝓪𝓫𝓵𝓮 is the actual valuable part of this Indicator.

It provides valuable information about the current market environment (whether it's risk on or risk off), the rough GRID models from 42MACRO and the actual market performance.

This allows you to obtain a deeper understanding of how the market works and makes it simple to identify the actual market direction.

Utility:

The 𝓜𝓪𝓻𝓴𝓮𝓽 𝓟𝓮𝓻𝓯𝓸𝓻𝓶𝓪𝓷𝓬𝓮 𝓣𝓪𝓫𝓵𝓮 is divided in 4 Sections which are the GRID regimes:

Economic Growth:

Goldilocks

Reflation

Economic Contraction:

Inflation

Deflation

Top 5 Equity Style Factors:

Are the values green for a specific Column? If so then the market reflects the corresponding GRID behavior.

Bottom 5 Equity Style Factors:

Are the values red for a specific Column? If so then the market reflects the corresponding GRID behavior.

So if we have Goldilocks as current regime we would see green values in the Top 5 Goldilocks Cells and red values in the Bottom 5 Goldilocks Cells.

You will find that Reflation will look similar, as it is also a sign of Economic Growth.

Same is the case for the two Contraction regimes.

Price Action (ValueRay)With this indicator, you gain access to up to 5 moving averages from a selection of 15 different types. This flexibility allows you to customize your trading strategy based on your preferences and market conditions. Whether you're a fan of simple moving averages, exponential moving averages, or weighted moving averages, our indicator has got you covered! Additionally, all the MAs are Multi-Time-Frame!

The indicator also provides trading signals. By analyzing market trends and price movements, it generates accurate buy and sell signals, providing you with clear entry and exit points. You can choose between Fast, Mid, and Slow signal speeds.

Trendlines are another crucial aspect of effective trading, and our indicator seamlessly integrates them, helping you visualize the market's direction.

Furthermore, the indicator empowers you with recent highs and lows. By highlighting these key levels, it becomes easier than ever to spot support and resistance areas, aiding you in making well-informed trading choices.

Additionally, you can switch the ADR% (Average Daily Range as a Percentage) on and off. This number instantly provides you with information on how much the stock usually moves per day as a percentage.

Key Features:

Up to 5 Moving Averages, each with its own timeframe.

SMA, EMA, WMA, RMA, Triangular, Volume Weighted, Elastic Volume Weighted, Least Squares, ZLEMA, Hull, Double EMA, Triple EMA, T3, ALMA, KAMA (more to come in future versions).

Recent High and Low Pivot Points acting as support/resistance.

Trendline indicating the current trend.

Buy/Sell Signals (recommended for use as exit points, stop loss, or take profit levels).

Signals can have three different speeds: Fast, Mid, and Slow. You can switch them anytime depending on how quickly or slowly you want to exit a trade.

The predefined colors are best suited for a dark background, and the predefined settings provide a solid starting point that many traders use in their daily work.

Unlock the full potential of your trading strategy with our comprehensive indicator and start making informed trading decisions today!

Cong Adaptive Moving AverageDr. Scott Cong's new adaptation of an adaptive moving average (AMA), featured in TASC March 2023.

It adjusts its parameters automatically according to the volatility of market, tracking price closely in trending movement, staying flat in congestion areas.

Perry Kaufman’s adaptive moving average, first described in his 1995 book Smarter Trading, is a great example of how an AMA can self-adjust to adapt to changing environments. This indicator presents a new scheme for an adaptive moving average that is responsive, smooth, and robust.

Another New Adaptive Moving Average [CC]The New Adaptive Moving Average was created by Scott Cong (Stocks and Commodities Mar 2023) and this is a companion indicator to my previous script . This indicator still works off of the same concept as before with effort vs results but this indicator takes a slightly different approach and instead defines results as the absolute difference between the closing price and a closing price x bars ago. As you can see in my chart example, this indicator works great to stay with the current trend and provides either a stop loss or take profit target depending on which direction you are going in. As always, I use darker colors to show stronger signals and lighter colors to show normal signals. Buy when the line turns green and sell when it turns red.

Let me know if there are any other indicator scripts you would like to see me publish!

A New Adaptive Moving Average [CC]The New Adaptive Moving Average was created by Scott Cong (Stocks and Commodities Mar 2023) and his idea was to focus on the Adaptive Moving Average created by Perry Kaufman and to try to improve it by introducing a concept of effort vs results. In this case the effort would be the total range of the underlying price action since each bar is essentially a war of the bulls vs the bears. The result would be the total range of the close so we are looking for the highest close and lowest close in that same time period. This gives us an alpha that we can use to plug into the Kaufman Adaptive Moving Average algorithm which gives us a brand new indicator that can hug the price just enough to allow us to ride the stock up or down. I have color coded it to be darker colors when it is a strong signal and lighter colors when it is a normal signal. Buy when the line turns green and sell when it turns red.

Let me know if there are any other indicators you would like to see me publish!

ER-Adaptive ATR Limit Channels w/ States [Loxx]As simple as it gets, channels based on high, low and ATR distances, Shows possible short term support / resistance or can be used as a take profit/stop-loss in some trading systems. It does this by comparing high/low values of price to multiplied by a multiple of ATR to determine when the trend changes. States are included to change the sensitivity to trend changes. 1 is very sensitive, 3 is least sensitive.

This uses Loxx's Expanded Source Types. You can read about them here:

What is ER Adaptive ATR?

Average True Range (ATR) is widely used indicator in many occasions for technical analysis . It is calculated as the RMA of true range. This version adds a "twist": it uses Perry Kaufman's Efficiency Ratio to calculate adaptive true range

Adaptive Fisherized KSTIntroduction

Heyo guys, here is a new adaptive fisherized indicator of me.

I applied Inverse Fisher Transform, Ehlers dominant cycle analysis,

smoothing and divergence analysis on the Know Sure Thing (KST) indicator.

Moreover, the indicator doesn't repaint.

Usage

I didn't backtest the indicator, but I recommend the 5–15 min timeframe.

It can be also used on other timeframs, but I have no experience with that.

The indicator has no special filter system, so you need to find an own combo in order to build a trading system.

A trend filter like KAMA or my Adaptive Fisherized Trend Intensity Index could fit well.

If you find a good combo, let me know it in the comments pls.

Signals

Zero Line

KST crossover 0 => Enter Long

KST crossunder 0 => Enter Short

Cross

KST crossover KST MA => Enter Long

KST crossunder KST MA => Enter Short

Cross Filtered

KST crossover KST MA and KST above 0 => Enter Long

KST crossunder KST MA and KST under 0 => Enter Short

KST crossunder 0 => Exit Long

KST crossover 0 => Exit Short

More to read: KST Explanation

Enjoy and let me know your opinion!

--

Credits to

- @tista

- @blackcat1402

- @DasanC

- @cheatcountry

Intrabar Efficiency Ratio█ OVERVIEW

This indicator displays a directional variant of Perry Kaufman's Efficiency Ratio, designed to gauge the "efficiency" of intrabar price movement by comparing the sum of movements of the lower timeframe bars composing a chart bar with the respective bar's movement on an average basis.

█ CONCEPTS

Efficiency Ratio (ER)

Efficiency Ratio was first introduced by Perry Kaufman in his 1995 book, titled "Smarter Trading". It is the ratio of absolute price change to the sum of absolute changes on each bar over a period. This tells us how strong the period's trend is relative to the underlying noise. Simply put, it's a measure of price movement efficiency. This ratio is the modulator utilized in Kaufman's Adaptive Moving Average (KAMA), which is essentially an Exponential Moving Average (EMA) that adapts its responsiveness to movement efficiency.

ER's output is bounded between 0 and 1. A value of 0 indicates that the starting price equals the ending price for the period, which suggests that price movement was maximally inefficient. A value of 1 indicates that price had travelled no more than the distance between the starting price and the ending price for the period, which suggests that price movement was maximally efficient. A value between 0 and 1 indicates that price had travelled a distance greater than the distance between the starting price and the ending price for the period. In other words, some degree of noise was present which resulted in reduced efficiency over the period.

As an example, let's say that the price of an asset had moved from $15 to $14 by the end of a period, but the sum of absolute changes for each bar of data was $4. ER would be calculated like so:

ER = abs(14 - 15)/4 = 0.25

This suggests that the trend was only 25% efficient over the period, as the total distanced travelled by price was four times what was required to achieve the change over the period.

Intrabars

Intrabars are chart bars at a lower timeframe than the chart's. Each 1H chart bar of a 24x7 market will, for example, usually contain 60 intrabars at the LTF of 1min, provided there was market activity during each minute of the hour. Mining information from intrabars can be useful in that it offers traders visibility on the activity inside a chart bar.

Lower timeframes (LTFs)

A lower timeframe is a timeframe that is smaller than the chart's timeframe. This script determines which LTF to use by examining the chart's timeframe. The LTF determines how many intrabars are examined for each chart bar; the lower the timeframe, the more intrabars are analyzed, but fewer chart bars can display indicator information because there is a limit to the total number of intrabars that can be analyzed.

Intrabar precision

The precision of calculations increases with the number of intrabars analyzed for each chart bar. As there is a 100K limit to the number of intrabars that can be analyzed by a script, a trade-off occurs between the number of intrabars analyzed per chart bar and the chart bars for which calculations are possible.

Intrabar Efficiency Ratio (IER)

Intrabar Efficiency Ratio applies the concept of ER on an intrabar level. Rather than comparing the overall change to the sum of bar changes for the current chart's timeframe over a period, IER compares single bar changes for the current chart's timeframe to the sum of absolute intrabar changes, then applies smoothing to the result. This gives an indication of how efficient changes are on the current chart's timeframe for each bar of data relative to LTF bar changes on an average basis. Unlike the standard ER calculation, we've opted to preserve directional information by not taking the absolute value of overall change, thus allowing it to be utilized as a momentum oscillator. However, by taking the absolute value of this oscillator, it could potentially serve as a replacement for ER in the design of adaptive moving averages.

Since this indicator preserves directional information, IER can be regarded as similar to the Chande Momentum Oscillator (CMO) , which was presented in 1994 by Tushar Chande in "The New Technical Trader". Both CMO and ER essentially measure the same relationship between trend and noise. CMO simply differs in scale, and considers the direction of overall changes.

█ FEATURES

Display

Three different display types are included within the script:

• Line : Displays the middle length MA of the IER as a line .

Color for this display can be customized via the "Line" portion of the "Visuals" section in the script settings.

• Candles : Displays the non-smooth IER and two moving averages of different lengths as candles .

The `open` and `close` of the candle are the longest and shortest length MAs of the IER respectively.

The `high` and `low` of the candle are the max and min of the IER, longest length MA of the IER, and shortest length MA of the IER respectively.

Colors for this display can be customized via the "Candles" portion of the "Visuals" section in the script settings.

• Circles : Displays three MAs of the IER as circles .

The color of each plot depends on the percent rank of the respective MA over the previous 100 bars.

Different colors are triggered when ranks are below 10%, between 10% and 50%, between 50% and 90%, and above 90%.

Colors for this display can be customized via the "Circles" portion of the "Visuals" section in the script settings.

With either display type, an optional information box can be displayed. This box shows the LTF that the script is using, the average number of lower timeframe bars per chart bar, and the number of chart bars that contain LTF data.

Specifying intrabar precision

Ten options are included in the script to control the number of intrabars used per chart bar for calculations. The greater the number of intrabars per chart bar, the fewer chart bars can be analyzed.

The first five options allow users to specify the approximate amount of chart bars to be covered:

• Least Precise (Most chart bars) : Covers all chart bars by dividing the current timeframe by four.

This ensures the highest level of intrabar precision while achieving complete coverage for the dataset.

• Less Precise (Some chart bars) & More Precise (Less chart bars) : These options calculate a stepped LTF in relation to the current chart's timeframe.

• Very precise (2min intrabars) : Uses the second highest quantity of intrabars possible with the 2min LTF.

• Most precise (1min intrabars) : Uses the maximum quantity of intrabars possible with the 1min LTF.

The stepped lower timeframe for "Less Precise" and "More Precise" options is calculated from the current chart's timeframe as follows:

Chart Timeframe Lower Timeframe

Less Precise More Precise

< 1hr 1min 1min

< 1D 15min 1min

< 1W 2hr 30min

> 1W 1D 60min

The last five options allow users to specify an approximate fixed number of intrabars to analyze per chart bar. The available choices are 12, 24, 50, 100, and 250. The script will calculate the LTF which most closely approximates the specified number of intrabars per chart bar. Keep in mind that due to factors such as the length of a ticker's sessions and rounding of the LTF, it is not always possible to produce the exact number specified. However, the script will do its best to get as close to the value as possible.

Specifying MA type

Seven MA types are included in the script for different averaging effects:

• Simple

• Exponential

• Wilder (RMA)

• Weighted

• Volume-Weighted

• Arnaud Legoux with `offset` and `sigma` set to 0.85 and 6 respectively.

• Hull

Weighting

This script includes the option to weight IER values based on the percent rank of absolute price changes on the current chart's timeframe over a specified period, which can be enabled by checking the "Weigh using relative close changes" option in the script settings. This places reduced emphasis on IER values from smaller changes, which may help to reduce noise in the output.

█ FOR Pine Script™ CODERS

• This script imports the recently published lower_ltf library for calculating intrabar statistics and the optimal lower timeframe in relation to the current chart's timeframe.

• This script uses the recently released request.security_lower_tf() Pine Script™ function discussed in this blog post .

It works differently from the usual request.security() in that it can only be used on LTFs, and it returns an array containing one value per intrabar.

This makes it much easier for programmers to access intrabar information.

• This script implements a new recommended best practice for tables which works faster and reduces memory consumption.

Using this new method, tables are declared only once with var , as usual. Then, on the first bar only, we use table.cell() to populate the table.

Finally, table.set_*() functions are used to update attributes of table cells on the last bar of the dataset.

This greatly reduces the resources required to render tables.

Look first. Then leap.

QQE Student's T-Distribution Bollinger Bands Oscillator Credit to all of the developers on this project (aka all of the places I got the code from lol) @eylwithsteph @storma @Fractured @lejmer @AlexGrover @Montyjus @Jiehonglim @StephXAGs @peacefulLizard50262 @gorx1 @above-c-level

This script utilizes @above-c-level 's Student's T-Distribution script to give us a great estimation of volatility. I took this idea and apply it to the QQE filter! That being said I have added a boat load of features as to make this script as useful to as many people as possible. This is the Osc version

Included averages: 'TMA', 'ALMA', 'EMA', 'DEMA', 'TEMA', 'WMA', 'VWMA', 'SMA', 'SMMA', 'HMA', 'LSMA', 'JMA', 'VAMA', 'FRAMA', 'ZLEMA', 'KAMA', 'IDWMA', 'FLMSA', 'PEMA', 'HCF', 'TIF', 'MF', 'ARMA', 'DAF', 'WRMA', 'RMA', 'RAF', 'A2RMA', 'QQE 1', 'QQE 2','Centroid',"Harmonic Mean","Geometric Mean","Quadratic Mean","Median","Trimean","Midhinge","Midrange","VWAP"

Included Features: Smoothing, Additional Moving Average, Log Space, Mean Momentum via Derivative, Normalization, Convergence DIvergence, Candle View

Use this just like macd/rsi but instead this directly reflects the band version! It also shows really valid support and resistance. Use this in combination with the band version for more power.

QQE Student's T-Distribution Bollinger BandsCredit to all of the developers on this project (aka all of the places I got the code from lol) @eylwithsteph @storma @Fractured @lejmer @AlexGrover @Montyjus @Jiehonglim @StephXAGs @peacefulLizard50262 @gorx1 @above-c-level

This script utilizes @above-c-level 's Student's T-Distribution script to give us a great estimation of volatility. I took this idea and apply it to the QQE filter! That being said I have added a boat load of features as to make this script as useful to as many people as possible.

Included averages: 'TMA', 'ALMA', 'EMA', 'DEMA', 'TEMA', 'WMA', 'VWMA', 'SMA', 'SMMA', 'HMA', 'LSMA', 'JMA', 'VAMA', 'FRAMA', 'ZLEMA', 'KAMA', 'IDWMA', 'FLMSA', 'PEMA', 'HCF', 'TIF', 'MF', 'ARMA', 'DAF', 'WRMA', 'RMA', 'RAF', 'A2RMA', 'QQE 1', 'QQE 2','Centroid',"Harmonic Mean","Geometric Mean","Quadratic Mean","Median","Trimean","Midhinge","Midrange","VWAP"

Included Features: Smoothing, Additional Moving Average, Log Space, Mean Momentum via Derivative

Use this just like BB but instead (as long as you are on qqe) you get real prices that are stable! It also shows really valid support and resistance. Use this in combination with the osc version for more power.

Multi Trend Cross Strategy TemplateToday I am sharing with the community trend cross strategy template that incorporates any combination of over 20 built in indicators. Some of these indicators are in the Pine library, and some have been custom coded and contributed over time by the beloved Pine Coder community. Identifying a trend cross is a common trend following strategy and a common custom-code request from the community. Using this template, users can now select from over 400 different potential trend combinations and setup alerts without any custom coding required. This Multi-Trend cross template has a very inclusive library of trend calculations/indicators built-in, and will plot any of the 20+ indicators/trends that you can select in the settings.

How it works : Simple trend cross strategies go long when the fast trend crosses over the slow trend, and/or go short when the fast trend crosses under the slow trend. Options for either trend direction are built-in to this strategy template. The script is also coded in a way that allows you to enable/modify pyramid settings and scale into a position over time after a trend has crossed.

Use cases : These types of strategies can reduce the volatility of returns and can help avoid large market downswings. For instance, those running a longer term trend-cross strategy may have not realized half the down swing of the bear markets or crashes in 02', 08', 20', etc. However, in other years, they may have exited the market from time to time at unfavorable points that didn't end up being a down turn, or at times the market was ranging sideways. Some also use them to reduce volatility and then add leverage to attempt to beat buy/hold of the underlying asset within an acceptable drawdown threshold.

Special thanks to @Duyck, @everget, @KivancOzbilgic and @LazyBear for coding and contributing earlier versions of some of these custom indicators in Pine.

This script incorporates all of the following indicators. Each of them can be selected and modified from within the indicator settings:

ALMA - Arnaud Legoux Moving Average

DEMA - Double Exponential Moving Average

DSMA - Deviation Scaled Moving Average - Contributed by Everget

EMA - Exponential Moving Average

HMA - Hull Moving Average

JMA - Jurik Moving Average - Contributed by Everget

KAMA - Kaufman's Adaptive Moving Average - Contributed by Everget

LSMA - Linear Regression , Least Squares Moving Average

RMA - Relative Moving Average

SMA - Simple Moving Average

SMMA - Smoothed Moving Average

Price Source - Plotted based on source selection

TEMA - Triple Exponential Moving Average

TMA - Triangular Moving Average

VAMA - Volume Adjusted Moving Average - Contributed by Duyck

VIDYA - Variable Index Dynamic Average - Contributed by KivancOzbilgic

VMA - Variable Moving Average - Contributed by LazyBear

VWMA - Volume Weighted Moving Average

WMA - Weighted Moving Average

WWMA - Welles Wilder's Moving Average

ZLEMA - Zero Lag Exponential Moving Average - Contributed by KivancOzbilgic

Disclaimer : This is not financial advice. Open-source scripts I publish in the community are largely meant to spark ideas that can be used as building blocks for part of a more robust trade management strategy. If you would like to implement a version of any script, I would recommend making significant additions/modifications to the strategy & risk management functions. If you don’t know how to program in Pine, then hire a Pine-coder. We can help!

SUPER MACD📈 MACD Indicator Update - Version 2

🔹 New Features and Improvements:

1️⃣ New MACD Calculation Options:

Users can now choose from various Moving Averages to calculate the MACD. The default options are SMA (Simple Moving Average) and EMA (Exponential Moving Average), but there are 14 other versions available to experiment with:

SMA (Simple Moving Average)

EMA (Exponential Moving Average)

WMA (Weighted Moving Average)

RMA (Smoothed Moving Average)

HMA (Hull Moving Average)

JMA (Jurik Moving Average)

DEMA (Double Exponential Moving Average)

TEMA (Triple Exponential Moving Average)

LSMA (Least Squares Moving Average)

VWMA (Volume-Weighted Moving Average)

SMMA (Smoothed Moving Average)

KAMA (Kaufman’s Adaptive Moving Average)

ALMA (Arnaud Legoux Moving Average)

FRAMA (Fractal Adaptive Moving Average)

VIDYA (Variable Index Dynamic Average)

2️⃣ Improved Input Visibility and Organization:

We’ve reorganized the inputs so that the most commonly used ones are now placed at the beginning for quicker and more convenient configuration.

3️⃣ Bug Fixes and Code Improvements:

Minor bugs have been fixed, and the code has been optimized for better stability and performance. The code is now cleaner and fully functional in version 6.

4️⃣ Cometreon Public Library Integration:

To lighten the code and improve its modularity, we’ve integrated the Cometreon public library. This makes the code more efficient and reduces the need to duplicate common functions.

☄️ With this update, the MACD indicator becomes even more versatile and user-friendly, offering a wide range of calculation methods and an improved interface!

Ultra Moving Average Rating Trend StrategyThis is a technical analysis strategy based initially on the rating strategy, but fully adapted and converted to moving average rating.

In this case we are using: Ichimoku, SMA, EMA, ALMA, SMMA, LSMA, VWMA, DEMA, HMA, KAMA FRAMA, VIDYA, JMA, TEMA, ZLEMA, TRIMA and T3 moving averages.

With all of them together I am making an index.

Rules for entry and exit:

If % percentage of all the moving averages is telling to go long , we go long or exit short. And viceversa for short.

If there are any questions, please let me know !

Moving Average Compendium RefurbishedThis is my effort to bring together in a single script the widest range of moving averages possible.

I aggregated the calculation of averages within a library.

For more information about the library follow the link:

Basically this indicator is the visual result of this library.

You can choose the moving average and the script updates the chart as per the type.

The unique parameters of certain moving averages remain at their default values.

To have a rainbow of moving averages I also made an indicator:

Available moving averages:

AARMA = 'Adaptive Autonomous Recursive Moving Average'

ADEMA = '* Alpha-Decreasing Exponential Moving Average'

AHMA = 'Ahrens Moving Average'

ALMA = 'Arnaud Legoux Moving Average'

ALSMA = 'Adaptive Least Squares'

AUTOL = 'Auto-Line'

CMA = 'Corrective Moving average'

CORMA = 'Correlation Moving Average Price'

COVWEMA = 'Coefficient of Variation Weighted Exponential Moving Average'

COVWMA = 'Coefficient of Variation Weighted Moving Average'

DEMA = 'Double Exponential Moving Average'

DONCHIAN = 'Donchian Middle Channel'

EDMA = 'Exponentially Deviating Moving Average'

EDSMA = 'Ehlers Dynamic Smoothed Moving Average'

EFRAMA = '* Ehlrs Modified Fractal Adaptive Moving Average'

EHMA = 'Exponential Hull Moving Average'

EMA = 'Exponential Moving Average'

EPMA = 'End Point Moving Average'

ETMA = 'Exponential Triangular Moving Average'

EVWMA = 'Elastic Volume Weighted Moving Average'

FAMA = 'Following Adaptive Moving Average'

FIBOWMA = 'Fibonacci Weighted Moving Average'

FISHLSMA = 'Fisher Least Squares Moving Average'

FRAMA = 'Fractal Adaptive Moving Average'

GMA = 'Geometric Moving Average'

HKAMA = 'Hilbert based Kaufman\'s Adaptive Moving Average'

HMA = 'Hull Moving Average'

JURIK = 'Jurik Moving Average'

KAMA = 'Kaufman\'s Adaptive Moving Average'

LC_LSMA = '1LC-LSMA (1 line code lsma with 3 functions)'

LEOMA = 'Leo Moving Average'

LINWMA = 'Linear Weighted Moving Average'

LSMA = 'Least Squares Moving Average'

MAMA = 'MESA Adaptive Moving Average'

MCMA = 'McNicholl Moving Average'

MEDIAN = 'Median'

REGMA = 'Regularized Exponential Moving Average'

REMA = 'Range EMA'

REPMA = 'Repulsion Moving Average'

RMA = 'Relative Moving Average'

RSIMA = 'RSI Moving average'

RVWAP = '* Rolling VWAP'

SMA = 'Simple Moving Average'

SMMA = 'Smoothed Moving Average'

SRWMA = 'Square Root Weighted Moving Average'

SW_MA = 'Sine-Weighted Moving Average'

SWMA = '* Symmetrically Weighted Moving Average'

TEMA = 'Triple Exponential Moving Average'

THMA = 'Triple Hull Moving Average'

TREMA = 'Triangular Exponential Moving Average'

TRSMA = 'Triangular Simple Moving Average'

TT3 = 'Tillson T3'

VAMA = 'Volatility Adjusted Moving Average'

VIDYA = 'Variable Index Dynamic Average'

VWAP = '* VWAP'

VWMA = 'Volume-weighted Moving Average'

WMA = 'Weighted Moving Average'

WWMA = 'Welles Wilder Moving Average'

XEMA = 'Optimized Exponential Moving Average'

ZEMA = 'Zero-Lag Exponential Moving Average'

ZSMA = 'Zero-Lag Simple Moving Average'

Adaptive Deviation [Loxx]Adaptive Deviation is an educational/conceptual indicator that is a new spin on the regular old standard deviation. By definition, the Standard Deviation (STD, also represented by the Greek letter sigma σ or the Latin letter s) is a measure that is used to quantify the amount of variation or dispersion of a set of data values. In technical analysis we usually use it to measure the level of current volatility.

Standard Deviation is based on Simple Moving Average calculation for mean value. This version of standard deviation uses the properties of EMA to calculate what can be called a new type of deviation, and since it is based on EMA, we can call it EMA deviation. And added to that, Perry Kaufman's efficiency ratio is used to make it adaptive (since all EMA type calculations are nearly perfect for adapting).

The difference when compared to standard is significant--not just because of EMA usage, but the efficiency ratio makes it a "bit more logical" in very volatile market conditions.

The green line is the Adaptive Deviation, the white line is regular Standard Deviation. This concept will be used in future indicators to further reduce noise and adapt to price volatility.

Included

Loxx's Expanded Source Types

[blackcat] L1 Linear Regression-Adjusted EMALevel 1

Background

Vitali Apirine proposed a new idea named "The Linear Regression-Adjusted Exponential Moving Average". Here it is the pine v4 impelementation of this idea.

Function

Linear Regression Adjusted Exponential Moving Average (LRAdj EMA) is used to combine a linear regression (linreg in tradingview) with an EMA. It can be used to define the trend reveral points while filtering price action. The LRAdj EMA can be used in combination with a traditional EMA of the same length to facilitate trend identification or it can serve as an important MA candicate in a trading system to potentially replace T3, JMA, KAMA or other MA functions.

Remarks

Feedbacks are appreciated.