Liquidity Sweep Breakout - LSBLiquidity Sweep Breakout - LSB

A professional session-based breakout system designed for OANDA:USDJPY and other JPY pairs.

Not guesswork, but precision - built on detailed observation of institutional moves to capture clear trade direction daily.

Master the Market’s Daily Bank Flow.

---

Strategy Detail:

I discovered this strategy after carefully studying how Japanese banks influence the forex market during their daily settlement period. Banks are some of the biggest players in the financial world, and when they adjust or settle their accounts in the morning, it often creates a push in the market. From years of observation, I noticed a consistent pattern, once banks finish their settlements, the market usually continues moving in the same direction that was formed right after those actions. This daily banking flow often sets the tone for the entire trading session, especially for JPY pairs like USDJPY.

To capture this move, I built the indicator so that it follows the bank-driven trend with clear rules for entries, stop-loss (SL), and take-profit (TP). The system is designed with professional risk management in mind. By default, it assumes a $10,000 account size, risks only 1% of that balance per trade, and targets a 1:1.5 reward-to-risk ratio. This means for every $100 risked, the potential profit is $150. Such controlled risk makes the system safer and more sustainable for long-term traders. At the same time, users are not limited to this setup, they can adjust the account balance in the settings, and the indicator will automatically recalculate the lot size and risk levels based on their own capital. This ensures the strategy works for small accounts and larger accounts alike.

🌍 Why It Works

Fundamentally driven: Based on **daily Japanese banking settlement flows**.

Session-specific precision: Targets the exact window when USDJPY liquidity reshapes.

Risk-managed: Always calculates lot size based on account and risk preferences.

Automatable: With webhook + MT5 EA, it can be fully hands-free.

---

✅ Recommended

Pair: USDJPY (best observed behavior).

Timeframe: 3-Minute chart.

Platform: TradingView Premium (for webhooks).

Execution: MT5 via EA.

---

🔎 Strategy Concept

The Tokyo Magic Breakout (TMB) is built on years of session observation and the unique daily rhythm of the Japanese banking system.

Every morning between 5:50 AM – 6:10 AM PKT (09:50 – 10:10 JST), Japanese banks perform daily reconciliation and settlement. This often sets the tone for the USDJPY direction of the day.

This strategy isolates that critical moment of liquidity adjustment and waits for a clean breakout confirmation. Instead of chasing noise, it executes only when price action is aligned with the Tokyo market’s hidden flows.

---

🕒 Timing Logic

Session Start: 5:00 AM PKT (Tokyo market open range).

Magic Candle: The 5:54 AM PKT candle is marked as the reference “breakout selector.”

Checkpoints: First confirmation at 6:30 AM PKT, then every 15 minutes until 8:30 AM PKT.

* If price stays inside the magic range → wait.

* If a breakout happens but the candle wick touches the range → wait for the next checkpoint.

* If by 8:30 AM PKT no clean breakout occurs → the day is marked as No Trade Day (NTD).

👉 Recommended timeframe: 3-Minute chart (3M) for precise signals.

---

📈 Trade Execution

Entry: Clean break above/below the magic candle’s range.

Stop-Loss: Opposite side of the Tokyo session high/low.

Take-Profit: Calculated by Reward\:Risk ratio (default 1.5:1).

Lot Size: Auto-calculated based on your risk model:

* Fixed Dollar

* % of Equity

* Conservative (minimum of both).

Visuals include:

✅ Entry/SL/TP lines

✅ Shaded risk (red) and reward (green) zones

✅ Trade labels (Buy/Sell with lot size & levels)

✅ TP/SL hit markers

---

🔔 Alerts & Automation (AutoTMB)

This strategy is fully automation-ready with EA + MT5:

1. Enable alerts in TMB settings.

2. Insert your PineConnector License Key.

3. Configure your risk management preferences.

4. Create a TradingView alert → in the message box simply type:

Pine Script®

{{alert_message}}

and set the EA webhook.

Now, every breakout trade (with exact entry, SL, TP, and lot size) is sent instantly.

👉 On your MT5:

* Install the EA.

* Use the same license key.

* Run it on a VPS or local MT5 terminal.

You now have a hands-free trading system: AutoTMB.

Cerca negli script per "liquidity"

Liquidity strategy tester [Influxum]This tool is based on the concept of liquidity. It includes 10 methods for identifying liquidity in the market. Although this tool is presented as a strategy, we see it more as a data-gathering instrument.

Warning: This indicator/strategy is not intended to generate profitable strategies. It is designed to identify potential market advantages and help with identifying effective entry points to capitalize on those advantages.

Once again, we have advanced the methods of effectively searching for liquidity in the market. With strategies, defined by various entry methods and risk management, you can find your edge in the market. This tool is backed by thorough testing and development, and we plan to continue improving it.

In its current form, it can also be used to test well-known ICT or Smart Money concepts. Using various methods, you can define market structure and identify areas where liquidity is located.

Fair Value Gaps - one of the entry signal options is fair value gaps, where an imbalance between buyers and sellers in the market can be expected.

Time and Price Theory - you can test this by setting liquidity from a specific session and testing entries as that liquidity is grabbed

Judas Swing - can be tested as a market reversal after a breakout during the first hours of trading.

Power of Three - accumulation can be observed as the market moving within a certain range, identified as cluster liquidity in our tool, manipulation occurs with the break of liquidity, and distribution is the direction of the entry.

🟪 Methods of Identifying Liquidity

Pivot Liquidity

This refers to liquidity formed by local extremes – the highest or lowest prices reached in the market over a certain period. The period is defined by a pivot number and determines how many candles before and after the high/low were higher/lower. Simply put, the pivot number represents the number of adjacent candles to the left and right, with a lower high for a pivot high and a higher low for a pivot low. The higher the number, the more significant the high/low is. Behind these local market extremes, we expect to find orders waiting for breakout as well as stop-losses.

Gann Swing

Similar to pivot liquidity, Gann swing identifies significant market points. However, instead of candle highs and lows, it focuses on the closing prices. A Gann swing is formed when a candle closes above (or below) several previous closes (the number is again defined by a strength parameter).

Percentage Change

Apart from ticks, percentages are also a key unit of market movement. In the search for liquidity, we monitor when a local high or low is formed. For liquidity defined by percentage change, a high must be a certain percentage higher than the last low to confirm a significant high. Similarly, a low must be a defined percentage away from the last significant high to confirm a new low. With the right percentage settings, you can eliminate market noise.

Session Range (3x)

Session range is a popular concept for finding liquidity, especially in smart money concepts (SMC). You can set up liquidity visualization for the Asian, London, or New York sessions – or even all three at once. This tool allows you to work with up to three sessions, so you can easily track how and if the market reacts to liquidity grabs during these sessions.

Tip for traders: If you want to see the reaction to liquidity grab during a specific session at a certain time (e.g., the well-known killzone), you can set the Trading session in this tool to the exact time where you want to look for potential entries.

Unfinished Auction

Based on order flow theory, an unfinished auction occurs when the market reverses sharply without filling all pending orders. In price action terms, this can be seen as two candles at a local high or low with very similar or identical highs/lows. The maximum difference between these values is defined as Tolerance, with the default setting being 3 ticks. This setting is particularly useful for filtering out noise during slower market periods, like the Asian session.

Double Tops and Bottoms

A very popular concept not only from smart money concepts but also among price pattern traders is the double bottom and double top. This occurs when the market stops and reverses at a certain price twice in a row. In the tool, you can set how many candles apart these bottoms/tops can be by adjusting the Length parameter. According to some theories, double bottoms are more effective when there is a significant peak between the two bottoms. You can set this in the tool as the Swing value, which defines how large the movement (expressed in ticks) must be between the two peaks/bottoms. The final parameter you can adjust is Tolerance, which defines the possible price difference between the two peaks/bottoms, also expressed in ticks.

Range or Cluster Liquidity

When the market stays within a certain price range, there’s a chance that breakout orders and stop-losses are accumulating outside of this range. Our tool defines ranges in two ways:

Candle balance calculates the average price within a candle (open, high, low, and close), and it defines consolidation when the centers of candles are within a certain distance from each other.

Overlap confirms consolidation when a candle overlaps with the previous one by a set percentage.

Daily, Weekly, and Monthly Highs or Lows

These options simply define liquidity as the previous day’s, week’s, or month’s highs or lows.

Visual Settings

You can easily adjust how liquidity is displayed on the chart, choosing line style, color, and thickness. To display only uncollected liquidity, select "Delete grabbed liquidity."

Liquidity Duration

This setting allows you to control how long liquidity areas remain valid. You can cancel liquidity at the end of the day, the second day, or after a specific number of candles.

🟪 Strategy

Now we come to the part of working with strategies.

Max # of bars after liquidity grab – This parameter allows you to define how many candles you can search for entry signals from the moment liquidity is grabbed. If you are using engulfing as an entry signal, which consists of 2 candles, keep in mind that this number must be at least 2. In general, if you want to test a quick and sharp reaction, set this number as low as possible. If you want to wait for a structural change after the liquidity grab, which may require more candles, set the number a bit higher.

🟪 Strategy - entries

In this section, we define the signals or situations where we can enter the market after liquidity has been taken out.

Liquidity grab - This setup triggers a trade immediately after liquidity is grabbed, meaning the trade opens as the next candle forms.

Close below, close above - This refers to situations where the price closes below liquidity, but then reverses and closes above liquidity again, suggesting the liquidity grab was a false breakout.

Over bar - This occurs when the entire candle (high and low) passes beyond the liquidity level but then experiences a pullback.

Engulfing - A popular price action pattern that is included in this tool.

2HL - weak, medium, strong - A variation of a popular candlestick pattern.

Strong bar - A strong reactionary candle that forms after a liquidity grab. If liquidity is grabbed at a low, this would be a strong long candle that closes near its high and is significantly larger compared to typical volatility.

Naked bar - A candlestick pattern we’ve tested that serves as a good confirmation of market movement.

FVG (Fair Value Gap) - A currently popular concept. This is the only signal with additional settings. “Pending FVG order valid” means if a fair value gap forms after a liquidity grab, a limit order is placed, which remains valid for a set number of candles. “FVG minimal tick size” allows you to filter based on the gap size, measured in ticks. “GAP entry model” lets you decide whether to place the limit order at the gap close or its edge.

🟪 Strategy - General

Long, short - You can choose whether to focus on long or short trades. It’s interesting to see how long and short trades yield different results across various markets.

Pyramiding - By default, the tool opens only one trade at a time. If a new signal arises while a trade is open, it won’t enter another position unless the pyramiding box is checked. You also need to set the maximum number of open trades in the Properties.

Position size - Simply set the size of the traded position.

🟪 Strategy - Time

In this section, you can set time parameters for the strategy being tested.

Test since year - As the name implies, you can limit the testing to start from a specific year.

Trading session - Define the trading session during which you want to test entries. You can also visualize the background (BG) for confirmation.

Exclude session - You can set a session period during which you prefer not to search for trades. For example, when the New York session opens, volatility can sharply increase, potentially reducing the long-term success rate of the tested setup.

🟪 Strategy - Exits

This section lets you define risk management rules.

PT & SL - Set the profit target (PT) and stop loss (SL) here.

Lowest/highest since grab - This option sets the stop loss at the lowest point after a liquidity grab at a low or at the highest point after a liquidity grab at a high. Since markets usually overshoot during liquidity grabs, it’s good practice to place the stop loss at the furthest point after the grab. You can also set your risk-reward ratio (RRR) here. A value of 1 sets an RRR of 1:1, 2 means 2:1, and so on.

Lowest/highest last # bars - Similar to the previous option, but instead of finding the extreme after a liquidity grab, it identifies the furthest point within the last number of candles. You can set how far back to look using the # bars field (for an engulfing pattern, 2 is optimal since it’s made of two candles, and the stop loss can be placed at the edge of the engulfing pattern). The RRR setting works the same way as in the previous option.

Other side liquidity grab - If this option is checked, the trade will exit when liquidity is grabbed on the opposite side (i.e., if you entered on a liquidity grab at a low, the trade will exit when liquidity is grabbed at a high).

Exit after # bars - A popular exit strategy where you close the position after a set number of candles.

Exit after # bars in profit - This option exits the trade once the position is profitable for a certain number of consecutive candles. For example, if set to 5, the position will close when 5 consecutive candles are profitable. You can also set a maximum number of candles (in the max field), ensuring the trade is closed after a certain time even if the profit condition hasn’t been met.

🟪 Alerts

Alerts are a key tool for traders to ensure they don’t miss trading opportunities. They also allow traders to manage their time effectively. Who would want to sit in front of the computer all day waiting for a trading opportunity when they could be attending to other matters? In our tool, you currently have two options for receiving alerts:

Liquidity grabs alert – if you enable this feature and set an alert, the alert will be triggered every time a candle on the current timeframe closes and intersects with the displayed liquidity line.

Entry signals alert – this feature triggers an alert when a signal for entry is generated based on the option you’ve selected in the Entry type. It’s an ideal way to be notified only when a trading opportunity appears according to your predefined rules.

Liquidity Trading Algorithm (LTA)

The Liquidity Trading Algorithm is an algorithm designed to provide trade signals based on

liquidity conditions in the market. The underlying algorithm is based on the Liquidity

Dependent Price Movement (LDPM) metric and the Liquidity Dependent Price Stability (LDPS)

algorithm.

Together, LDPM and LDPS demonstrate statistically significant forecasting capabilities for price-

action on equities, cryptocurrencies, and futures. LTA takes these liquidity measurements and

translates them into actionable insights by way of entering or exiting a position based

on the future outlooks, as measured by the current liquidity status.

The benefit of LTA is that it can incorporate these powerful liquidity measurements into

actionable insights with several features designed to help you tailor LTA's behavior and

measurements to your desired vantage point. These customizable features come by the way of determining LTA's assessment style, and additional monitoring systems for avoiding bear and bull traps, along with various other quality of life features, discussed in more detail below.

First, a few quick facts:

- LTA is compatible on a wide array of instruments, including Equities, Futures, Cryptocurrencies, and Forex.

- LTA is compatible on most intervals in so long as the data can be calculated appropriately,

(be sure to do a backtest on timescales less than 1-minue to ensure the data can be computed).

- LTA only measures liquidity at the end of the interval of the chart chosen, and does not respond to conditions during the candle interval, unless specified (such as with `Stops`).

- LTA is interval-dependent, this means it will measure and behave differently on different

intervals as the underlying algorithms are dependent on the interval chosen.

- LTA can utilize fractional share sizing for cryptocurrencies.

- LTA can be restricted to either bullish or bearish indications.

- Additional Monitoring Systems are available for additional risk mitigation.

In short, LTA is a widely applicable, unique algorithm designed to translate liquidity measurements into liquidity insights.

Before getting more into the details, here is a quick list of the main features and settings

available for customization:

- Backtesting Start Date: Manual selection of the start date for the algorithm during backtesting.

- Assessment Style: adjust how LDPM and LDPS measure and respond to changes in liquidity.

- Impose Wait: force LTA to wait before entering or exiting a position to ensure conditions have remained conducive.

- Trade Direction Allowance: Restrict LTA to only long or only short, if desired.

- Position Sizing Method: determine how LTA calculates position sizing.

- Fractional Share Sizing: allow LTA to calculate fractional share sizes for cryptocurrencies

- Max Size Limit: Impose a maximum size on LTA's positions.

- Initial Capital: Indicate how much capital LTA should stat with.

- Portfolio Allotment: Indicate to LTA how much (in percentages) of the available balance should be considered when calculating position size.

- Enact Additional Monitoring Systems: Indicate if LTA should impose additional safety criteria when monitoring liquidity.

- Configure Take Profit, Stop-Loss, Trailing Stop Loss

- Display Information tables on the current position, overall strategy performance, along

with a text output showing LTA's processes.

- Real-time text output and updates on LTA's inner workings.

Let's get into some more of the details.

LTA's Assessment Style

LTA's assessment style determines how LTA collects and responds to changing data. In traditional terms, this is akin to (but not quite exactly the same as) the sensitivity versus specificity spectrum, whereby on one end (the sensitive end), an algorithm responds to changes in data in a reactive manner (which tends to lower its specificity, or how often it is correct in its indications), and on the other end, the opposite one, the algorithm foresakes quick changes for longevity of outlook.

While this is in part true, it is not a full view of the underlying mechanisms that changing the assessment style augments. A better analogy would be that the sensitive end of the spectrum (`Aggressive`) is in a state such that the algorithm wants to changing its outlooks, and as such, with changes in data, the algorithm has to be convinced as to why that is not a good idea to change outlooks, whereas the the more specific states (`Conservative`, `Diamond`) must be convinced that their view is no longer valid and that it needs to be changed.

This means the `Aggressive` and the `Diamond` settings fundamentally differ not just in their

data collection, but also in the data processing such that the `Aggressive` decision tree has to

be convinced that the data is the same (as its defualt is that it has changed),

and the `Diamond` decision tree has to be convinced that the data is not the same, and as such, the outlook need changed.

From there, the algorithm cooks through the data and determines to what the outlook should be changed to, given the current state of liquidity.

`Balanced` lies in the middle of this balance, attempting to balance being open to new ideas while not removing the wisdom of the past, as it were.

On a scale of most `sensitive` to most `specific`, it is as follows: `Aggressive`, `Balanced`,

`Conservative`, `Diamond`.

Functionally, these different modes can help in different liquidity environments, as certain

environments are more conducive to an eager approach (such as found near `Aggressive`) or are more conducive to a more conservative approach, where sudden changes in liquidity are known to be short-lived and unremarkable (such as many previously identified bull or bear traps).

For instance, on low interval views, it can often-times be beneficial to keep the algorithm towards the `Sensitive` end, since on the lower-timeframes, the crosswinds can change quite dramatically; whereas on the longer intervals, it may be useful to maintain a more `Specific` algorithm (such as found near `Diamond` mode) setting since longer intervals typically lend themselves to longer time-horizons, which themselves typically lend themselves to "weathering the storm", as it were.

LTA's Assessment Style is also supported by the Additional Monitoring Systems which works

to add sensitivity without sacrificing specificity by enacting a separate monitoring system, as described below.

Additional Monitoring Systems

The Additional Monitoring System (AMS) attempts to add more context to any changes in liquidity conditions as measured, such that LTA as a whole will have an expanded view into any rapidly changing liquidity conditions before these changes manifest in the traditional data streams. The ideal is that this allows for early exits or early entrances to positions "a head of time".

The traditional use of this system is to indicate when liquidity is suggestive of the end of a particular run (be it a bear run or a bull run), so an early exit can be initiated (and thus,

downside averted) even before the data officially showcase such changes. In such cases (when AMS becomes activated), the algorithm will signal to exit any open positions, and will restrict the opening of any new positions.

When a position is exited because of AMS, it is denoted as an `Early Exit` and if a position is prevented from being entered, the text output will display `AM prevented entry...` to indicate that conditions are not meeting AMS' additional standards.

The algorithm will wait to make any actions while `AMS` is `active` and will only enter into a new position once `AMS` has been `deactivated` and overall liquidity conditions are appropriate.

Functionally, the benefits of AMS translate to:

- Toggeling AMS on will typically see a net reduction in overall profitability, but

- AMS will typically (almost always) reduce max drawdown,

an increases in max runup, and increase return-over-maxdrawdown, and

- AMS can provide benefit for equities that experience a lot of "traps" by navigating early

entrance and early exits.

So in short, AMS is way of adding an additional level of liquidity monitoring that attempts to

exit positions if conditions look to be deteriorating, and to enter conditions if they look to be

improving. The cost of this additional monitoring, however, is a greater number of trades indicated, and a lower overall profitability.

Impose Wait

Note: `Impose Wait` will not force Take Profit, Stop Loss, or Trailing Stop Loss to

wait.

LTA can be indicated to `wait` before entering or exiting a position if desired. This means that if conditions change, whereas without a `wait` imposed, the algorithm would immediately indicate this change via a signal to alter the strategy's position, with a `wait` imposed, the algorithm will `wait` the indicated number of bars, and then re-check conditions before proceeding.

If, while waiting, conditions change to a state that is no longer compatible with the "order-in-

waiting", then the order-in-waiting is removed, and the counts reset (i.e.: conditions must remain favorable to the intended positional change throughout the wait period).

Since LTA works at the end-of-intervals, there is an inherently "built-in" wait of 1 bar when

switching directly from long to short (i.e.: if a full switch is indicated, then it is indicated as

conditions change -> exit new position -> wait until -> check conditions ->

enter new position as indicated). Thus, to impose a wait of `1 bar` would be to effectively have a total of two candles' ends prior to the entrance of the new position).

There are two main styles of `Impose Wait` that you can utilize:

- `Wait` : this mode will cause LTA to `wait` when both entering and exiting a position (in so long as it is not an exit signaled via a Take Profit, Stop Loss or Trailing Stop Loss).

- `Exit-Wait` : This mode will >not< cause LTA to `wait` if conditions require the closing of a position, but will force LTA to wait before entering into a position.

Position:

In addition to the availability to restrict LTA to either a long-only or short-only strategy, LTA

also comprises additional flexibility when deciding on how it should navigate the markets with

regards to sizing. Notably, this flexibility benefits several aspects of LTA's existence, namely the ability to determine the `Sizing Method`, or if `Fractional Share Sizing` should be employed, and more, as discussed below.

Position Sizing Method

There are two main ways LTA can determine the size of a position. Either via the `Fixed-Share` choice, or the `Fixed-Percentage` choice.

- `Fixed-Share` will use the amount indicated in the `Max Sizing Limit` field as the position size, always.

Note: With `Fixed-Share` sizing, LTA will >not< check if the balance is sufficient

prior to signaling an entrance.

- `Fixed-Percentage` will use the percentage amount indicated in the `Portfolio Allotment` field as the percentage of available funds to use when calculating the position size. Additionally, with the `Fixed-Percentage` choice, you can set the `Max Sizing Limit` if desired, which will ensure that no position will be entered greater than the amount indicated in the field.

Fractional Share Sizing

If the underlying instrument supports it (typically only cryptocurrencies), share sizing can be

fractionalized. If this is done, the resulting positin size is rounded to `4 digits`. This means any

position with a size less than `0.00005` will be rounded to `0.0000`

Note: Ensure that the underlying instrument supports fractional share sizing prior

to initiating.

Max Sizing Limit

As discussed above, the `Max Sizing Limit` will determine:

- The position size for every position, if `Sizing Method : Fixed-Share` is utilized, or

- The maximum allowed size, regardless of available capital, if `Sizing Method : Fixed-Percentage` is utilized.

Note: There is an internal maximum of 100,000 units.

Initial Capital

Note: There are 2 `Initial Capital` settings; one in LTA's settings and one in the

`Properties` tab. Ensure these two are the same when doing backtesting.

The initial capital field will be used to determine the starting balanace of the strategy, and

is used to calculate the internal data reporting (the data tables).

Portfolio Allotment

You can specify how much of the total available balance should be used when calculating the share size. The default is 100%.

Stops

Note: Stops over-ride `AMS` and `Impose Wait`, and are not restricted to only the

end-of-candle and will occur instantaneously upon their activation. Neither `AMS` nor `Impose Wait` can over-ride a signal from a `Take-Profit`, `Stop-Loss`, or a `Trailing-Stop Loss`.

LTA enhouses three stops that can be configured, a `Take-Profit`, a `Stop-Loss` and a `Trailing-Stop Loss`. The configurations can be set in the settings in percent terms. These exit signals will always over-ride AMS or any other restrictions on position exit.

Their configuration is rather standard; set the percentages you want the signal to be sent at and so it will be done.

Some quick notes on the `Trailing-Stop Loss`:

- The activation percentage must be reached (in profits) prior to the `Traililng-Stop Loss`

from activating the downside protection. For example, if the `Activation Percentage` is 10%, then unless the position reaches (at any point) a 10% profit, then it will not signal any exits on the downside, should it occur.

- The downside price-point is continuously updated and is calculated from the maximum profit reached in the given position and the loss percentage placed in the appropriate field.

Data Tables and Data Output

LTA provides real-time data output through a variety of mechanisms:

- `Position Table`

The `Position Table` displays information about the current position, including:

> Position Duration : how long the position has been open for.

> Indicates if the side is Long or Short, depending on if it is long or short.

> Entry Price: the price the position was entered at.

> Current Price (% Dif): the current price of the underlying and the %-difference between the entry price and the current price.

> Max Profit ($/%): the maximum profit reached in $ and % terms.

> Current PnL ($/%) : the current PnL for the open position.

- `Performance Table`

The `Performance Table` displays information regarding the overall performance of the algorithm since its `Start Date`. These data include:

> Initial Equity ($): The initial equity the algorithm started with.

> Current Equity ($): The current total equity of the account (including open positions)

> Net Profits ($|%) : The overall net profit in $ and % terms.

> Long / Short Trade Counts: The respective trade counts for the positions entered.

> Total Closed Trades: The running sum of the number of trades closed.

> Profitability: The calculation of the number of profitable trades over the total number of

trades.

> Avg. Profit / Trade: The calculation of the average profit per trade in both $ and % terms.

> Avg. Loss / Trade: The calculation of the average loss per trade in both $ and % terms.

> Max Run-Up: The maximum run-up the algorithm has seen in both $ and % terms.

> Max Drawdown: The maximum draw-down the algorithm has seen in both $ and % terms.

> Return-Over-Max-Drawdown: the ratio of the maximum drawdown against the current net profits.

- `Text Output`

LTA will output, if desired, signals to the text output field every time it analysis or performs and action. These messages can include information such as:

"

08:00:00 >> AM Protocol activated ... exiting position ...

08:00:00 >> Exit Order Created for qty: 2, profit: 380 (4.34%)

...

09:30:00 >> Checking conditions ...

09:30:00 >> AM protocol prevented entry ... waiting ...

"

This way, you can keep an eye out on what is happening "under the hood", as it were.

LTA will produce a message at the end of its assessment at the end of each candle interval, as well as when a position is exited due to a `Stop` or due to `AMS` being activated.

Additionally, the `Text Output` includes a initial message, but for space-constraints, this

can be toggled off with the `Blank Text Output` option within LTA's configurations.

For additional information, please refer to the Author's Instructions below.

Liquidity Sweep Filter Strategy [AlgoAlpha X PineIndicators]This strategy is based on the Liquidity Sweep Filter developed by AlgoAlpha. Full credit for the concept and original indicator goes to AlgoAlpha.

The Liquidity Sweep Filter Strategy is a non-repainting trading system designed to identify liquidity sweeps, trend shifts, and high-impact price levels. It incorporates volume-based liquidation analysis, trend confirmation, and dynamic support/resistance detection to optimize trade entries and exits.

This strategy helps traders:

Detect liquidity sweeps where major market participants trigger stop losses and liquidations.

Identify trend shifts using a volatility-based moving average system.

Analyze volume distribution with a built-in volume profile visualization.

Filter noise by differentiating between major and minor liquidity sweeps.

How the Liquidity Sweep Filter Strategy Works

1. Trend Detection Using Volatility-Based Filtering

The strategy applies a volatility-adjusted moving average system to determine trend direction:

A central trend line is calculated using an EMA smoothed over a user-defined length.

Upper and lower deviation bands are created based on the average price deviation over multiple periods.

If price closes above the upper band, the strategy signals an uptrend.

If price closes below the lower band, the strategy signals a downtrend.

This approach ensures that trend shifts are confirmed only when price significantly moves beyond normal market fluctuations.

2. Liquidity Sweep Detection

Liquidity sweeps occur when price temporarily breaks key levels, triggering stop-loss liquidations or margin call events. The strategy tracks swing highs and lows, marking potential liquidity grabs:

Bearish Liquidity Sweeps – Price breaks a recent high, then reverses downward.

Bullish Liquidity Sweeps – Price breaks a recent low, then reverses upward.

Volume Integration – The strategy analyzes trading volume at each sweep to differentiate between major and minor sweeps.

Key levels where liquidity sweeps occur are plotted as color-coded horizontal lines:

Red lines indicate bearish liquidity sweeps.

Green lines indicate bullish liquidity sweeps.

Labels are displayed at each sweep, showing the volume of liquidated positions at that level.

3. Volume Profile Analysis

The strategy includes an optional volume profile visualization, displaying how trading volume is distributed across different price levels.

Features of the volume profile:

Point of Control (POC) – The price level with the highest traded volume is marked as a key area of interest.

Bounding Box – The profile is enclosed within a transparent box, helping traders visualize the price range of high trading activity.

Customizable Resolution & Scale – Traders can adjust the granularity of the profile to match their preferred time frame.

The volume profile helps identify zones of strong support and resistance, making it easier to anticipate price reactions at key levels.

Trade Entry & Exit Conditions

The strategy allows traders to configure trade direction:

Long Only – Only takes long trades.

Short Only – Only takes short trades.

Long & Short – Trades in both directions.

Entry Conditions

Long Entry:

A bullish trend shift is confirmed.

A bullish liquidity sweep occurs (price sweeps below a key level and reverses).

The trade direction setting allows long trades.

Short Entry:

A bearish trend shift is confirmed.

A bearish liquidity sweep occurs (price sweeps above a key level and reverses).

The trade direction setting allows short trades.

Exit Conditions

Closing a Long Position:

A bearish trend shift occurs.

The position is liquidated at a predefined liquidity sweep level.

Closing a Short Position:

A bullish trend shift occurs.

The position is liquidated at a predefined liquidity sweep level.

Customization Options

The strategy offers multiple adjustable settings:

Trade Mode: Choose between Long Only, Short Only, or Long & Short.

Trend Calculation Length & Multiplier: Adjust how trend signals are calculated.

Liquidity Sweep Sensitivity: Customize how aggressively the strategy identifies sweeps.

Volume Profile Display: Enable or disable the volume profile visualization.

Bounding Box & Scaling: Control the size and position of the volume profile.

Color Customization: Adjust colors for bullish and bearish signals.

Considerations & Limitations

Liquidity sweeps do not always result in reversals. Some price sweeps may continue in the same direction.

Works best in volatile markets. In low-volatility environments, liquidity sweeps may be less reliable.

Trend confirmation adds a slight delay. The strategy ensures valid signals, but this may result in slightly later entries.

Large volume imbalances may distort the volume profile. Adjusting the scale settings can help improve visualization.

Conclusion

The Liquidity Sweep Filter Strategy is a volume-integrated trading system that combines liquidity sweeps, trend analysis, and volume profile data to optimize trade execution.

By identifying key price levels where liquidations occur, this strategy provides valuable insight into market behavior, helping traders make better-informed trading decisions.

Key use cases for this strategy:

Liquidity-Based Trading – Capturing moves triggered by stop hunts and liquidations.

Volume Analysis – Using volume profile data to confirm high-activity price zones.

Trend Following – Entering trades based on confirmed trend shifts.

Support & Resistance Trading – Using liquidity sweep levels as dynamic price zones.

This strategy is fully customizable, allowing traders to adapt it to different market conditions, timeframes, and risk preferences.

Full credit for the original concept and indicator goes to AlgoAlpha.

Liquidity Breakout - Strategy [presentTrading]- Introduction and How It Is Different

The Liquidity Breakout Strategy is a unique trading strategy that focuses on identifying and leveraging patterns in market price data. This strategy, mainly inspired by the script "Master Pattern" by LuxAlgo, takes a different approach from many traditional strategies that rely on technical indicators or fundamental analysis. Instead, the Liquidity Breakout is based on the concept of contraction detection and liquidity levels. This approach allows traders to identify potential trading opportunities that other strategies might miss.

BTCUSDT 6h

The strategy is different from other trading strategies because it uses a unique combination of pattern detection, liquidity levels, and user-defined trading direction. This combination allows the strategy to adapt to various market conditions and trading styles, making it a versatile tool for traders.

- Strategy: How It Works

1. Contraction Detection: The strategy uses a lookback period defined by the user (default is 10 bars) to identify contractions in the market. A contraction is a period where the market is consolidating, often followed by a significant price movement. The strategy identifies contractions by finding pivot highs and pivot lows within the lookback period. If a pivot high is lower than the previous pivot high and a pivot low is higher than the previous pivot low, a contraction is detected.

2. liquidity Levels:

What are Liquidity levels? Liquidity levels, also known as liquidity pools or zones, are price levels at which there is a significant amount of trading activity. They are often areas where large institutional traders (like banks or hedge funds) have placed orders. These levels are important because they can act as support or resistance levels, and price often reacts at these levels.

In the context of this strategy, liquidity levels are used to identify potential entry and exit points for trades. When the price reaches a liquidity level, it could indicate a potential trading opportunity. For example, if the price breaks through a liquidity level, it could signal the start of a new trend. On the other hand, if the price approaches a liquidity level and then reverses, it could signal a potential reversal.

The strategy uses these two elements to identify potential trading opportunities. When a contraction is detected, the strategy will look for a breakout in the direction of the trend. If the breakout occurs at a liquidity level, the strategy will execute a trade.

The strategy also allows traders to set their stop loss based on either the Average True Range (ATR) or a fixed percentage. This flexibility allows traders to manage their risk according to their personal risk tolerance and trading style.

- Trade Direction

One of the unique features of the Master Pattern Strategy is the ability to choose the trading direction. Traders can choose to trade in the "Long" direction, the "Short" direction, or "Both". This feature allows traders to adapt the strategy to their personal trading style and market outlook.

For example, if a trader believes that the market is in an uptrend, they can choose to trade only in the "Long" direction. Conversely, if the market is in a downtrend, they can choose to trade only in the "Short" direction. If the trader believes that the market is volatile and there are opportunities in both directions, they can choose to trade in "Both" directions.

- Usage

To use the strategy, traders need to input their preferred settings, including the contraction detection lookback period, liquidity levels, stop loss type, and trading direction. Once these settings are input, the strategy will automatically detect potential trading opportunities and execute trades according to the defined parameters.

- Default Settings

The default settings for the Master Pattern Strategy are as follows:

Contraction Detection Lookback: 10

Liquidity Levels: 20

Stop Loss Type: ATR

ATR Length: 20

ATR Multiplier: 3.0

Fixed Percentage: 0.01

Trading Direction: Both

These settings can be adjusted according to the trader's personal preferences and market conditions. It's recommended that traders experiment with different settings to find the ones that work best for their trading style and goals.

Titan EMA Liquidity [Stansbooth]

🔥 Precision EMA + FVG Liquidity Sweep System

Advanced Buy/Sell Signal Engine for High-Probability Trade Entries

Unlock a new level of precision with this all-in-one market structure indicator built for traders who demand accuracy, clarity, and confidence.

This tool combines EMA trend filtration , Fair Value Gap (FVG) detection , and liquidity sweep analysis to deliver powerful buy and sell signals that align with institutional price behavior.

✅ Key Features

Dynamic EMA Trend Filter:

Identifies true trend direction and filters out low-quality trades. Signals only trigger when momentum aligns with higher-timeframe directional bias.

Smart FVG Detection:

Automatically highlights bullish and bearish Fair Value Gaps, helping you spot premium/discount zones where institutional traders seek entries.

Liquidity Sweep Identification:

Detects equal highs/lows, stop hunts, and engineered liquidity grabs—then confirms reversals when price sweeps liquidity and returns inside structure.

High-Accuracy Signal Engine:

Buy/Sell alerts trigger only when three layers agree:

1. EMA trend alignment

2. FVG confirmation

3. Liquidity sweep completion

This results in cleaner signals , fewer false entries, and strong trend continuation setups.

Optimized for All Market Conditions:

Works for scalping, day trading, and swing trading across Forex, Crypto, Indices, and Stocks.

What This Indicator Helps You Achieve

Capture smart-money style entries with reduced drawdown

Enter after liquidity grabs instead of before them

Avoid chop with EMA-filtered market direction

Spot precision premium/discount zones using automatic FVG mapping

Obtain high-confidence Buy/Sell signals based on institutional concept

Why Traders Love It

This system isn’t just another signal generator—it’s a market-structure aware model that reads the chart the same way professional traders do.

Every signal is based on probability stacking , giving you the clarity and confidence to take the best setups while ignoring noise.

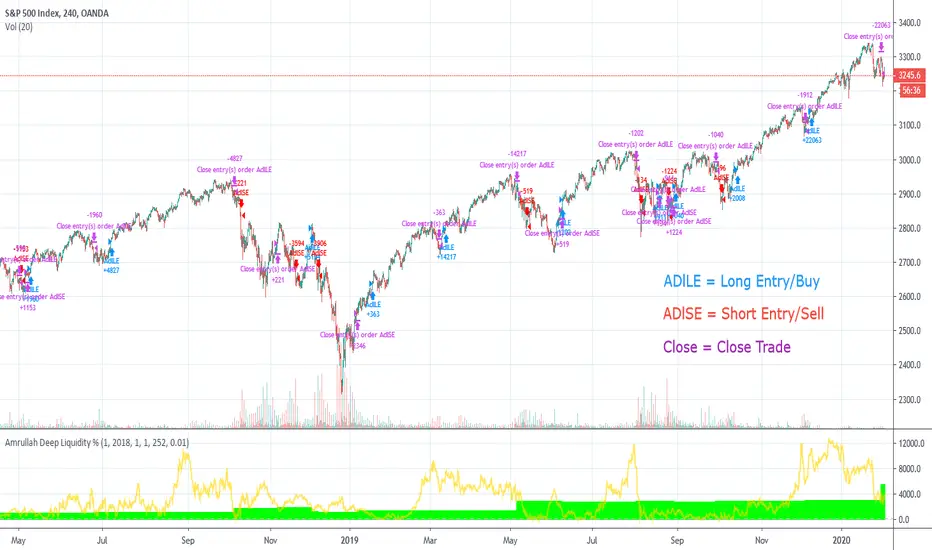

Amrullah Deep Liquidity for S&P 500Amrullah Deep Liquidity (ADL)

Amrullah Deep Liquidity (ADL) is a high profit factor strategy based on models designed by Muhd Amrullah.

Choosing your trading pair that you are planning to backtest

Check that you have been given access to Amrullah Deep Liquidity (ADL). Select SPX500USD with the default 4H time frame. Once done, open Indicators > Invite-Only Scripts > Amrullah Deep Liquidity %.

Choosing your initial capital that you want to begin backtesting

Go to Settings > Properties > Initial Capital and type in the amount of capital you're starting with. For the SPX500USD trading pair, the initial capital is denominated in USD.

Adjusting your equity at risk until the trades match your risk profile and comfort level

Go to Inputs > Equity Risk and adjust the value you are comfortable with. To analyse performance, you also want to choose the Start Year, Start Month and Start Date. Select lower equity risk for trades that you intend to take without the use of leverage. You can select an equity risk from 0.001 to 0.05 or all the way to 1.

Finding the time frame with the highest profit factor

Profit factor is defined as the gross profit a strategy makes across a defined period of time divided by its gross loss. You may choose to scroll through other time frames to find better models. You can select a different time frame from 1 min to 1H or all the way to 1M. Once you find the model you desire, you are encouraged to check that the model has a backtested profit factor of >3.5. You can then begin looking through the Performance Summary to find other detailed statistics.

Analysing the equity curve from the Amrullah Deep Liquidity (ADL) strategy

A green equity curve indicates that the trades are accumulating profits. A red equity curve indicates that the trades are accumulating losses. A healthy equity curve is one that is green and grows steadily to the right and upward direction.

Analysing the display arrows on the chart

Amrullah Deep Liquidity (ADL) tells you when to take a trade and how much to put in a trade. ADL can do this as the model identifies inventory risk in traders and market makers in the chosen market. On your Tradingview chart, ADL will display an arrow that tells you when to enter a trade. You can also see the amount to trade beside the arrow.

Opting for a trial

Yes you may opt for a trial which has limited availability.

The author's background and experience

My career in software and deep learning development spans across more than 5 years. At work, I lead a team to solve core computer vision tasks for large companies. I continually read all kinds of computer science books and papers, and follows progress on tools used in financial markets.

Amrullah Deep Liquidity for ETHUSDAmrullah Deep Liquidity (ADL)

Amrullah Deep Liquidity (ADL) is a high profit factor strategy based on models designed by Muhd Amrullah.

Choosing your trading pair that you are planning to backtest

Check that you have been given access to Amrullah Deep Liquidity (ADL). Select ETHUSD with the default 4H time frame. Once done, open Indicators > Invite-Only Scripts > Amrullah Deep Liquidity %.

Choosing your initial capital that you want to begin backtesting

Go to Settings > Properties > Initial Capital and type in the amount of capital you're starting with. For the ETHUSD trading pair, the initial capital is denominated in USD.

Adjusting your equity at risk until the trades match your risk profile and comfort level

Go to Inputs > Equity Risk and adjust the value you are comfortable with. To analyse performance, you also want to choose the Start Year, Start Month and Start Date. Select lower equity risk for trades that you intend to take without the use of leverage. You can select an equity risk from 0.001 to 0.05 or all the way to 1.

Finding the time frame with the highest profit factor

Profit factor is defined as the gross profit a strategy makes across a defined period of time divided by its gross loss. You may choose to scroll through other time frames to find better models. You can select a different time frame from 1 min to 1H or all the way to 1M. Once you find the model you desire, you are encouraged to check that the model has a backtested profit factor of >3.5. You can then begin looking through the Performance Summary to find other detailed statistics.

Analysing the equity curve from the Amrullah Deep Liquidity (ADL) strategy

A green equity curve indicates that the trades are accumulating profits. A red equity curve indicates that the trades are accumulating losses. A healthy equity curve is one that is green and grows steadily to the right and upward direction.

Analysing the display arrows on the chart

Amrullah Deep Liquidity (ADL) tells you when to take a trade and how much to put in a trade. ADL can do this as the model identifies inventory risk in traders and market makers in the chosen market. On your Tradingview chart, ADL will display an arrow that tells you when to enter a trade. You can also see the amount to trade beside the arrow.

Opting for a trial

Yes you may opt for a trial which has limited availability.

The author's background and experience

My career in software and deep learning development spans across more than 5 years. At work, I lead a team to solve core computer vision tasks for large companies. I continually read all kinds of computer science books and papers, and follows progress on tools used in financial markets.

Amrullah Deep Liquidity for BTCUSDAmrullah Deep Liquidity (ADL)

Amrullah Deep Liquidity (ADL) is a high profit factor strategy based on models designed by Muhd Amrullah.

Choosing your trading pair that you are planning to backtest

Check that you have been given access to Amrullah Deep Liquidity (ADL). Select BTCUSD with the default 4H time frame. Once done, open Indicators > Invite-Only Scripts > Amrullah Deep Liquidity %.

Choosing your initial capital that you want to begin backtesting

Go to Settings > Properties > Initial Capital and type in the amount of capital you're starting with. For the BTCUSD trading pair, the initial capital is denominated in USD.

Adjusting your equity at risk until the trades match your risk profile and comfort level

Go to Inputs > Equity Risk and adjust the value you are comfortable with. To analyse performance, you also want to choose the Start Year, Start Month and Start Date. Select lower equity risk for trades that you intend to take without the use of leverage. You can select an equity risk from 0.001 to 0.05 or all the way to 1.

Finding the time frame with the highest profit factor

Profit factor is defined as the gross profit a strategy makes across a defined period of time divided by its gross loss. You may choose to scroll through other time frames to find better models. You can select a different time frame from 1 min to 1H or all the way to 1M. Once you find the model you desire, you are encouraged to check that the model has a backtested profit factor of >3.5. You can then begin looking through the Performance Summary to find other detailed statistics.

Analysing the equity curve from the Amrullah Deep Liquidity (ADL) strategy

A green equity curve indicates that the trades are accumulating profits. A red equity curve indicates that the trades are accumulating losses. A healthy equity curve is one that is green and grows steadily to the right and upward direction.

Analysing the display arrows on the chart

Amrullah Deep Liquidity (ADL) tells you when to take a trade and how much to put in a trade. ADL can do this as the model identifies inventory risk in traders and market makers in the chosen market. On your Tradingview chart, ADL will display an arrow that tells you when to enter a trade. You can also see the amount to trade beside the arrow.

Opting for a trial

Yes you may opt for a trial which has limited availability.

The author's background and experience

My career in software and deep learning development spans across more than 5 years. At work, I lead a team to solve core computer vision tasks for large companies. I continually read all kinds of computer science books and papers, and follows progress on tools used in financial markets.

Amrullah Deep Liquidity for ETHBTCAmrullah Deep Liquidity (ADL)

Amrullah Deep Liquidity (ADL) is a high profit factor strategy based on models designed by Muhd Amrullah.

Choosing your trading pair that you are planning to backtest

Check that you have been given access to Amrullah Deep Liquidity (ADL). Select ETHBTC with the default 2H time frame. Once done, open Indicators > Invite-Only Scripts > Amrullah Deep Liquidity %.

Choosing your initial capital that you want to begin backtesting

Go to Settings > Properties > Initial Capital and type in the amount of capital you're starting with. For the ETHBTC trading pair, the initial capital is denominated in BTC.

Adjusting your equity at risk until the trades match your risk profile and comfort level

Go to Inputs > Equity Risk and adjust the value you are comfortable with. To analyse performance, you also want to choose the Start Year, Start Month and Start Date. Select lower equity risk for trades that you intend to take without the use of leverage. You can select an equity risk from 0.001 to 0.05 or all the way to 1.

Finding the time frame with the highest profit factor

Profit factor is defined as the gross profit a strategy makes across a defined period of time divided by its gross loss. You may choose to scroll through other time frames to find better models. You can select a different time frame from 1 min to 1H or all the way to 1M. Once you find the model you desire, you are encouraged to check that the model has a backtested profit factor of >3.5. You can then begin looking through the Performance Summary to find other detailed statistics.

Analysing the equity curve from the Amrullah Deep Liquidity (ADL) strategy

A green equity curve indicates that the trades are accumulating profits. A red equity curve indicates that the trades are accumulating losses. A healthy equity curve is one that is green and grows steadily to the right and upward direction.

Analysing the display arrows on the chart

Amrullah Deep Liquidity (ADL) tells you when to take a trade and how much to put in a trade. ADL can do this as the model identifies inventory risk in traders and market makers in the chosen market. On your Tradingview chart, ADL will display an arrow that tells you when to enter a trade. You can also see the amount to trade beside the arrow.

Opting for a trial

Yes you may opt for a trial which has limited availability.

The author's background and experience

My career in software and deep learning development spans across more than 5 years. At work, I lead a team to solve core computer vision tasks for large companies. I continually read all kinds of computer science books and papers, and follows progress on tools used in financial markets.

MACD Liquidity Tracker Strategy [Quant Trading]MACD Liquidity Tracker Strategy

Overview

The MACD Liquidity Tracker Strategy is an enhanced trading system that transforms the traditional MACD indicator into a comprehensive momentum-based strategy with advanced visual signals and risk management. This strategy builds upon the original MACD Liquidity Tracker System indicator by TheNeWSystemLqtyTrckr , converting it into a fully automated trading strategy with improved parameters and additional features.

What Makes This Strategy Original

This strategy significantly enhances the basic MACD approach by introducing:

Four distinct system types for different market conditions and trading styles

Advanced color-coded histogram visualization with four dynamic colors showing momentum strength and direction

Integrated trend filtering using 9 different moving average types

Comprehensive risk management with customizable stop-loss and take-profit levels

Multiple alert systems for entry signals, exits, and trend conditions

Flexible signal display options with customizable entry markers

How It Works

Core MACD Calculation

The strategy uses a fully customizable MACD configuration with traditional default parameters:

Fast MA : 12 periods (customizable, minimum 1, no maximum limit)

Slow MA : 26 periods (customizable, minimum 1, no maximum limit)

Signal Line : 9 periods (customizable, now properly implemented and used)

Cryptocurrency Optimization : The strategy's flexible parameter system allows for significant optimization across different crypto assets. Traditional MACD settings (12/26/9) often generate excessive noise and false signals in volatile crypto markets. By using slower, more smoothed parameters, traders can capture meaningful momentum shifts while filtering out market noise.

Example - DOGE Optimization (45/80/290 settings) :

• Performance : Optimized parameters yielding exceptional backtesting results with 29,800% PnL

• Why it works : DOGE's high volatility and social sentiment-driven price action benefits from heavily smoothed indicators

• Timeframes : Particularly effective on 30-minute and 4-hour charts for swing trading

• Logic : The very slow parameters filter out noise and capture only the most significant trend changes

Other Optimizable Cryptocurrencies : This parameter flexibility makes the strategy highly effective for major altcoins including SUI, SEI, LINK, Solana (SOL) , and many others. Each crypto asset can benefit from custom parameter tuning based on its unique volatility profile and trading characteristics.

Four Trading System Types

1. Normal System (Default)

Long signals : When MACD line is above the signal line

Short signals : When MACD line is below the signal line

Best for : Swing trading and capturing longer-term trends in stable markets

Logic : Traditional MACD crossover approach using the signal line

2. Fast System

Long signals : Bright Blue OR Dark Magenta (transparent) histogram colors

Short signals : Dark Blue (transparent) OR Bright Magenta histogram colors

Best for : Scalping and high-volatility markets (crypto, forex)

Logic : Leverages early momentum shifts based on histogram color changes

3. Safe System

Long signals : Only Bright Blue histogram color (strongest bullish momentum)

Short signals : All other colors (Dark Blue, Bright Magenta, Dark Magenta)

Best for : Risk-averse traders and choppy markets

Logic : Prioritizes only the strongest bullish signals while treating everything else as bearish

4. Crossover System

Long signals : MACD line crosses above signal line

Short signals : MACD line crosses below signal line

Best for : Precise timing entries with traditional MACD methodology

Logic : Pure crossover signals for more precise entry timing

Color-Coded Histogram Logic

The strategy uses four distinct colors to visualize momentum:

🔹 Bright Blue : MACD > 0 and rising (strong bullish momentum)

🔹 Dark Blue (Transparent) : MACD > 0 but falling (weakening bullish momentum)

🔹 Bright Magenta : MACD < 0 and falling (strong bearish momentum)

🔹 Dark Magenta (Transparent) : MACD < 0 but rising (weakening bearish momentum)

Trend Filter Integration

The strategy includes an advanced trend filter using 9 different moving average types:

SMA (Simple Moving Average)

EMA (Exponential Moving Average) - Default

WMA (Weighted Moving Average)

HMA (Hull Moving Average)

RMA (Running Moving Average)

LSMA (Least Squares Moving Average)

DEMA (Double Exponential Moving Average)

TEMA (Triple Exponential Moving Average)

VIDYA (Variable Index Dynamic Average)

Default Settings : 50-period EMA for trend identification

Visual Signal System

Entry Markers : Blue triangles (▲) below candles for long entries, Magenta triangles (▼) above candles for short entries

Candle Coloring : Price candles change color based on active signals (Blue = Long, Magenta = Short)

Signal Text : Optional "Long" or "Short" text inside entry triangles (toggleable)

Trend MA : Gray line plotted on main chart for trend reference

Parameter Optimization Examples

DOGE Trading Success (Optimized Parameters) :

Using 45/80/290 MACD settings with 50-period EMA trend filter has shown exceptional results on DOGE:

Performance : Backtesting results showing 29,800% PnL demonstrate the power of proper parameter optimization

Reasoning : DOGE's meme-driven volatility and social sentiment spikes create significant noise with traditional MACD settings

Solution : Very slow parameters (45/80/290) filter out social media-driven price spikes while capturing only major momentum shifts

Optimal Timeframes : 30-minute and 4-hour charts for swing trading opportunities

Result : Exceptionally clean signals with minimal false entries during DOGE's characteristic pump-and-dump cycles

Multi-Crypto Adaptability :

The same optimization principles apply to other major cryptocurrencies:

SUI : Benefits from smoothed parameters due to newer coin volatility patterns

SEI : Requires adjustment for its unique DeFi-related price movements

LINK : Oracle news events create price spikes that benefit from noise filtering

Solana (SOL) : Network congestion events and ecosystem developments need smoothed detection

General Rule : Higher volatility coins typically benefit from very slow MACD parameters (40-50 / 70-90 / 250-300 ranges)

Key Input Parameters

System Type : Choose between Fast, Normal, Safe, or Crossover (Default: Normal)

MACD Fast MA : 12 periods default (no maximum limit, consider 40-50 for crypto optimization)

MACD Slow MA : 26 periods default (no maximum limit, consider 70-90 for crypto optimization)

MACD Signal MA : 9 periods default (now properly utilized, consider 250-300 for crypto optimization)

Trend MA Type : EMA default (9 options available)

Trend MA Length : 50 periods default (no maximum limit)

Signal Display : Both, Long Only, Short Only, or None

Show Signal Text : True/False toggle for entry marker text

Trading Applications

Recommended Use Cases

Momentum Trading : Capitalize on strong directional moves using the color-coded system

Trend Following : Combine MACD signals with trend MA filter for higher probability trades

Scalping : Use "Fast" system type for quick entries in volatile markets

Swing Trading : Use "Normal" or "Safe" system types for longer-term positions

Cryptocurrency Trading : Optimize parameters for individual crypto assets (e.g., 45/80/290 for DOGE, custom settings for SUI, SEI, LINK, SOL)

Market Suitability

Volatile Markets : Forex, crypto, indices (recommend "Fast" system or smoothed parameters)

Stable Markets : Stocks, ETFs (recommend "Normal" or "Safe" system)

All Timeframes : Effective from 1-minute charts to daily charts

Crypto Optimization : Each major cryptocurrency (DOGE, SUI, SEI, LINK, SOL, etc.) can benefit from custom parameter tuning. Consider slower MACD parameters for noise reduction in volatile crypto markets

Alert System

The strategy provides comprehensive alerts for:

Entry Signals : Long and short entry triangle appearances

Exit Signals : Position exit notifications

Color Changes : Individual histogram color alerts

Trend Conditions : Price above/below trend MA alerts

Strategy Parameters

Default Settings

Initial Capital : $1,000

Position Size : 100% of equity

Commission : 0.1%

Slippage : 3 points

Date Range : January 1, 2018 to December 31, 2069

Risk Management (Optional)

Stop Loss : Disabled by default (customizable percentage-based)

Take Profit : Disabled by default (customizable percentage-based)

Short Trades : Disabled by default (can be enabled)

Important Notes and Limitations

Backtesting Considerations

Uses realistic commission (0.1%) and slippage (3 points)

Default position sizing uses 100% equity - adjust based on risk tolerance

Stop-loss and take-profit are disabled by default to show raw strategy performance

Strategy does not use lookahead bias or future data

Risk Warnings

Past performance does not guarantee future results

MACD-based strategies may produce false signals in ranging markets

Consider combining with additional confluences like support/resistance levels

Test thoroughly on demo accounts before live trading

Adjust position sizing based on your risk management requirements

Technical Limitations

Strategy does not work on non-standard chart types (Heikin Ashi, Renko, etc.)

Signals are based on close prices and may not reflect intraday price action

Multiple rapid signals in volatile conditions may result in overtrading

Credits and Attribution

This strategy is based on the original "MACD Liquidity Tracker System" indicator created by TheNeWSystemLqtyTrckr . This strategy version includes significant enhancements:

Complete strategy implementation with entry/exit logic

Addition of the "Crossover" system type

Proper implementation and utilization of the MACD signal line

Enhanced risk management features

Improved parameter flexibility with no artificial maximum limits

Additional alert systems for comprehensive trade management

The original indicator's core color logic and visual system have been preserved while expanding functionality for automated trading applications.

Entropy, Liquidity, and Momentum - ELMoELMo is a momentum trading strategy based on two concepts: entropy and liquidity

The core concept behind the strategy is twofold: trade based on reversals in momentum based on the strength of a trend, and trade when market liquidity is beneficial to the position.

Entries and exits are determined by first calculating Shannon entropy for the time series and applying various moving averages. Separately, the Hui-Heubel Liquidity Ratio (lhh) is calculated and applied as a filter. Finally, additional conditionals such as RSI are applied to reduce false entries.

Entropy is defined as the amount of 'randomness' in a system and in this application can be thought of as a measure of the strength or weakness of a trend. The main moving averages and visible components in ELMo represent the normalized entropy score of the 'close' value (0 is series minimum, 1 is maximum). lhh will measure illiquid/fragile markets with low values and liquid/resilient markets with a high value. In general, the strategy will prefer to enter long when liquidity is high and short when liquidity is low, based off of cross events in the displayed entropy moving averages. I have published lhh as a separate indicator but it is not required for this strategy to function.

Several settings can be configured inside the strategy, including long/short bias, lookback window, MA band lengths, RSI boundaries, and more, but I have tried to choose sensible defaults that work for a large variety of situations and equities. My preferred time scales are 1m 1h 4h 1d 1w 1mo but others may work fine. Trailing stops are implemented using configurable ATR values. Additional settings are available to limit entry times (default is set to US options market open/close), and backtesting start date.

The long strategy is generally more accurate than short. Since Pinescript does not have a way to manage long/short exposure in a hedged fashion, I prefer to run two separate instances of ELMo in long-only and short-only modes for signaling. I prefer to trade this strategy with a long bias using the short signals as indications of windows of weakness where hedging could be prudent.

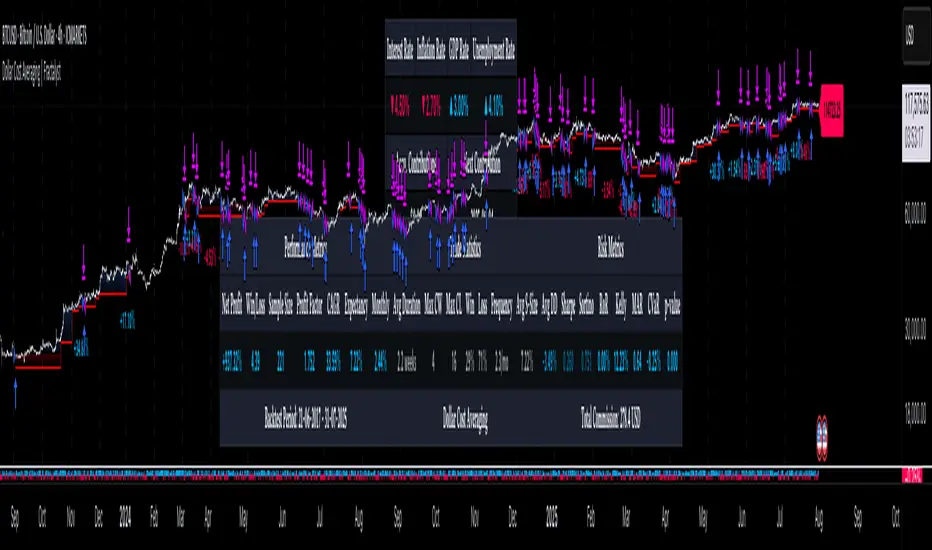

USD Liquidity Conditions Index Swing Stock Strategy Original credits goes to @ElDoggo22 www.tradingview.com

I looked in the post created by him, of USD liquidity and I have noticed that if you are going to apply a percentile top and bottom to it, can become an interesting swing strategy for US Stocks.

So in this case I decided to create a 99th percentile for top and 4th percentile for bot with a big length, preferably 100+ candles, for this example i took 150.

Rules for entry :

Long : either bot or top lines are ascending

We exit long either the top line is descending, or we have sudden cross of the moving average with both top and bot within the same candle

Short: we enter short when we have a sudden cross down of the moving average with both top and bot within the same candle

We exit short when we have a cross over of the moving average with both top and bot within the same candle ( or we have a long entry condition)

If there are qny questions, please let me know !

Liquidity Sweep & FVG StrategyThis strategy combines higher-timeframe liquidity levels, stop-hunt (sweep) logic, Fair Value Gaps (FVGs) and structure-based take-profits into a single execution engine.

It is not a simple mash-up of indicators: every module (HTF levels, sweeps, FVGs, ZigZag, sessions) feeds the same entry/exit logic.

1. Core Idea

The script looks for situations where price:

Sweeps a higher-timeframe high/low (takes liquidity around obvious levels),

Then forms a displacement candle with a gap (FVG) in the opposite direction,

Then uses the edge of that FVG as a limit entry,

And manages exits using unswept structural levels (ZigZag swings or HTF levels) as targets.

The intent is to systematically trade failed breakouts / stop hunts with a defined structure and risk model.

It is a backtesting / study tool, not a signal service.

2. How the Logic Works (Conceptual)

a) Higher-Timeframe Liquidity Engine

Daily, Weekly and Monthly highs/lows are pulled via request.security() and stored as HTF liquidity levels.

Each level is drawn as a line with optional label (1D/1W/1M High/Low).

A level is marked as “swept” once price trades through it; swept levels may be removed or shortened depending on settings.

b) Sweep & Manipulation Filter

A low sweep occurs when the current low trades through a stored HTF low.

A high sweep occurs when the current high trades through a stored HTF high.

If both a high and a low are swept in the same bar, the script flags this as “manipulation” and blocks new entries around that noise.

The script also tracks the sweep wick, bar index and HTF timeframe for later use in SL placement and labels.

c) FVG Detection & Management

FVGs are defined using a 3-candle displacement model:

Bullish FVG: high < low

Bearish FVG: low > high

Only gaps larger than a minimum size (ATR-based if no manual value is set) are kept.

FVGs are stored in arrays as boxes with: top, bottom, mid (CE), direction, and state (filled / reclaimed).

Boxes are auto-extended and visually faded when price is far away, or deleted when filled.

d) Entry Conditions (Sweep + FVG)

For each recent sweep window:

After a low sweep, the script searches for the nearest bullish FVG below price and uses its top edge as a long limit entry.

After a high sweep, it searches for the nearest bearish FVG above price and uses its bottom edge as a short limit entry.

A “knife protection” check blocks trades where price is already trading through the proposed stop.

Only one entry per sweep is allowed; entries are only placed inside the configured NY trading sessions and only if no manipulation flag is active and EOD protection allows it.

e) Stop-Loss Placement (“Tick-Free” SL)

The stop is not placed directly on the HTF level; instead, the script scans a window around the sweep bar to find a local extreme:

Longs: lowest low in a configurable bar window around the sweep.

Shorts: highest high in that window.

This produces a structure-based SL that is generally outside the main sweep wick.

f) Take-Profit Logic (ZigZag + HTF Levels)

A lightweight ZigZag engine tracks swing highs/lows and removes levels that have already been broken.

For intraday timeframes (< 1h), TP candidates come from unswept ZigZag swings above/below the entry.

For higher timeframes (≥ 1h), TP candidates fall back to unswept HTF liquidity levels.

The script picks up to two targets:

TP1: nearest valid target in the trade direction (or a 2R fallback if none exists),

TP2: second target (or a 4R fallback if none exists).

A multi-TP model is used: typically 50% at TP1, remainder managed towards TP2 with breakeven plus offset once TP1 is hit.

g) Session & End-of-Day Filters

Three predefined NY sessions (Early, Open, Afternoon) are available; entries are only allowed inside active sessions.

An End-of-Day filter checks a user-defined NY close time and:

Blocks new entries close to the end of the day,

Optionally forces flat before the close.

3. Inputs Overview (Conceptual)

Liquidity settings: which HTF levels to track (1D/1W/1M), how many to show, and sweep priority (highest TF vs nearest vs any).

FVG settings: visibility radius, search window after a sweep, minimum FVG size.

ZigZag settings: swing length used for TP discovery.

Execution & protection: limit order timeout, breakeven offset, EOD protection.

Visuals: labels, sweep markers, manipulation warning, session highlighting, TP lines, etc.

For exact meaning of each input, please refer to the inline comments in the open-source code.

4. Strategy Properties & Backtesting Notes

Default strategy properties in this script:

Initial capital: 100,000

Order size: 10% of equity (strategy.percent_of_equity)

Commission: 0.01% per trade (adjust as needed for your broker/asset)

Slippage: must be set manually in the Strategy Tester (recommended: at least a few ticks on fast markets).

Even though the order size is 10% of equity, actual risk per trade depends on the SL distance and is typically much lower than 10% of the account. You should still adjust these values to keep risk within what you personally consider sustainable (e.g. somewhere in the 1–2% range per trade).

For more meaningful results:

Test on liquid instruments (e.g. major indices, FX, or liquid futures).

Use enough history to reach 100+ closed trades on your market/timeframe.

Always include realistic commission and slippage.

Do not assume that past performance will continue.

5. How to Use

Apply the strategy to your preferred symbol and timeframe.

Set broker-like commission and slippage in the Strategy Tester.

Adjust:

HTF levels (1D/1W/1M),

Sessions (NY windows),

FVG search window and minimum size,

ZigZag length and EOD filter.

Observe how entries only appear:

After a HTF sweep,

In the configured session,

At a FVG edge,

With TP lines anchored at unswept structure / liquidity.

Use this primarily as a research and backtesting tool to study how your own ICT / SMC ideas behave over a large sample of trades.

6. Disclaimer

This script is for educational and research purposes only.

It does not constitute financial advice, and it does not guarantee profitability. Always validate results with realistic assumptions and use your own judgment before trading live.

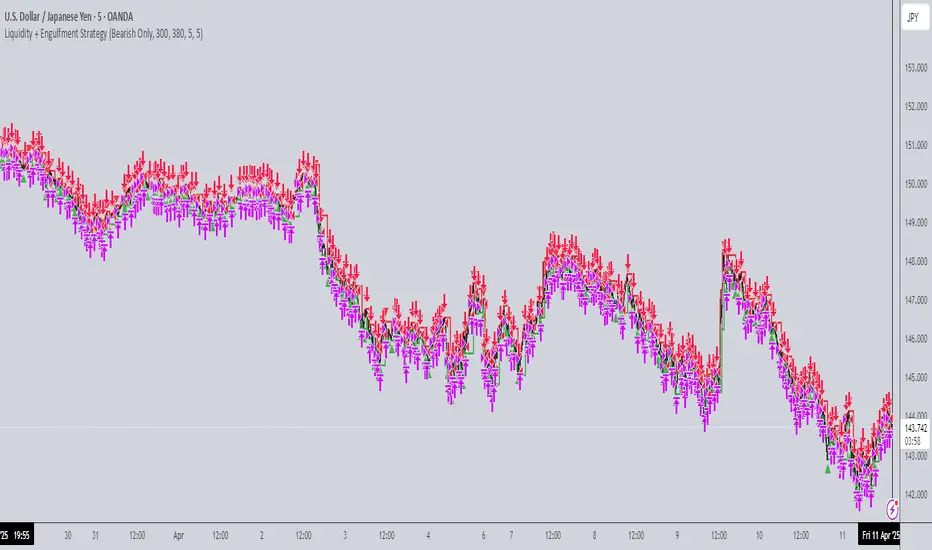

Liquidity Sweep + BOS Retest System — Prop Firm Edition🟦 Liquidity Sweep + BOS Retest System — Prop Firm Edition

A High-Probability Smart Money Strategy Built for NQ, ES, and Funding Accounts

🚀 Overview

The Liquidity Sweep + BOS Retest System (Prop Firm Edition) is a precision-engineered SMC strategy built specifically for prop firm traders. It mirrors institutional liquidity behavior and combines it with strict account-safe entry rules to help traders pass and maintain funding accounts with consistency.

Unlike typical indicators, this system waits for three confirmations — liquidity sweep, displacement, and a clean retest — before executing any trade. Every component is optimized for low drawdown, high R:R, and prop-firm-approved risk management.

Whether you’re trading Apex, TakeProfitTrader, FFF, or OneUp Trader, this system gives you a powerful mechanical framework that keeps you within rules while identifying the market’s highest-probability reversal zones.

🔥 Key Features

1. Liquidity Sweep Detection (Stop Hunt Logic)