Liquidity_Zone by SebasVentuLiquidity_Zone by SebasVentu It is a strategy that shows the liquidity zones and also has a simulator

Es una estrategia que muestra las zonas de liquidez y ademas cuenta con un simulador

Cerca negli script per "liquidity"

US/SPY- Financial Regime Index Swing Strategy Credits: concept inspired by EdgeTools Bloomberg Financial Conditions Index (Proxy)

Improvements: eight component basket, inverse volatility weights, winsorization option( statistical technique used to limit the influence of outliers in a dataset by replacing extreme values with less extreme ones, rather than removing them entirely), slope and price gates, exit guards, table and gradients.

Summary in one paragraph

A macro regime swing strategy for index ETFs, futures, FX majors, and large cap equities on daily calculation with optional lower time execution. It acts only when a composite Financial Conditions proxy plus slope and an optional price filter align. Originality comes from an eight component macro basket with inverse volatility weights and winsorized return z scores that produce a portable yardstick.

Scope and intent

Markets: SPY and peers, ES futures, ACWI, liquid FX majors, BTC, large cap equities.

Timeframes: calculation daily by default, trade on any chart.

Default demo: SPY on Daily.

Purpose: convert broad financial conditions into clear swing bias and exits.

Originality and usefulness

Unique fusion: return z scores for eight liquid proxies with inverse volatility weighting and optional winsorization, then slope and price gates.

Failure mode addressed: false starts in chop and early shorts during easy liquidity.

Testability: all knobs are inputs and the table shows components and weights.

Portable yardstick: z scores center at zero so thresholds transfer across symbols.

Method overview in plain language

Base measures

Return basis: natural log return over a configurable window, standardized to a z score. Winsorization optional to cap extremes.

Components

EQ US and EQ GLB measure equity tone.

CREDIT uses LQD over HYG. Higher credit quality outperformance is risk off so sign is flipped after z score.

RATES2Y uses two year yield, sign flipped.

SLOPE uses ten minus two year yield spread.

USD uses DXY, sign flipped.

VOL uses VIX, sign flipped.

LIQ uses BIL over SPY, sign flipped.

Each component is smoothed by the composite EMA.

Fusion rule

Weighted sum where weights are equal or inverse volatility with exponent gamma, normalized to percent so they sum to one.

Signal rule

Long when composite crosses up the long threshold and its slope is positive and price is above the SMA filter, or when composite is above the configured always long floor.

Short when composite crosses down the short threshold and its slope is negative and price is below the SMA filter.

Long exit on cross down of the long exit line or on a fresh short signal.

Short exit on cross up of the short exit line or on a fresh long signal, or when composite falls below the force short exit guard.

What you will see on the chart

Markers on suggestion bars: L for long, S for short, LX and SX for exits.

Reference lines at zero and soft regime bands at plus one and minus one.

Optional background gradient by regime intensity.

Compact table with component z, weight percent, and composite readout.

Table fields and quick reading guide

Component: EQ US, EQ GLB, CREDIT, RATES2Y, SLOPE, USD, VOL, LIQ.

Z: current standardized value, green for positive risk tone where applicable.

Weight: contribution percent after normalization.

Composite: current index value.

Reading tip: a broadly green Z column with slope positive often precedes better long context.

Inputs with guidance

Setup

Calc timeframe: default Daily. Leave blank to inherit chart.

Lookback: 50 to 1500. Larger length stabilizes regimes and delays turns.

EMA smoothing: 1 to 200. Higher smooths noise and delays signals.

Normalization

Winsorize z at ±3: caps extremes to reduce one off shocks.

Return window for equities: 5 to 260. Shorter reacts faster.

Weighting

Weight lookback: 20 to 520.

Weight mode: Equal or InvVol.

InvVol exponent gamma: 0.1 to 3. Higher compresses noisy components more.

Signals

Trade side: Long Short or Both.

Entry threshold long and short: portable z thresholds.

Exit line long and short: soft exits that give back less.

Slope lookback bars: 1 to 20.

Always long floor bfci ≥ X: macro easy mode keep long.

Force short exit when bfci < Y: macro stress guard.

Confirm

Use price trend filter and Price SMA length.

View

Glow line and Show component table.

Symbols

SPY ACWI HYG LQD VIX DXY US02Y US10Y BIL are defaults and can be changed.

Realism and responsible publication

No performance claims. Past is not future.

Shapes can move intrabar and settle on close.

Execution is on standard candles only.

Honest limitations and failure modes

Major economic releases and illiquid sessions can break assumptions.

Very quiet regimes reduce contrast. Use longer windows or higher thresholds.

Component proxies are ETFs and indexes and cannot match a proprietary FCI exactly.

Strategy notice

Orders are simulated on standard candles. All security calls use lookahead off. Nonstandard chart types are not supported for strategies.

Entries and exits

Long rule: bfci cross above long threshold with positive slope and optional price filter OR bfci above the always long floor.

Short rule: bfci cross below short threshold with negative slope and optional price filter.

Exit rules: long exit on bfci cross below long exit or on a short signal. Short exit on bfci cross above short exit or on a long signal or on force close guard.

Position sizing

Percent of equity by default. Keep target risk per trade low. One percent is a sensible starting point. For this example we used 3% of the total capital

Commisions

We used a 0.05% comission and 5 tick slippage

Legal

Education and research only. Not investment advice. Test in simulation first. Use realistic costs.

Gold 15m: Trend + S/R + Liquidity Sweep (RR 1:2)This strategy is designed for short-term trading on XAUUSD (Gold) using the 15-minute timeframe. It combines trend direction, support/resistance pivots, liquidity sweep detection, and momentum confirmation to identify high-probability reversal setups in line with the dominant market trend.

⚙️ Core Logic:

Trend Filter (EMA 200):

The strategy only takes long positions when price is above the 200 EMA and short positions when price is below it.

Support/Resistance via Pivots:

Dynamic swing highs and lows are identified using pivot points. These act as local supply and demand levels where liquidity is likely to accumulate.

Liquidity Sweep Detection:

A bullish liquidity sweep occurs when price briefly breaks below the last pivot low (grabbing liquidity) and then closes back above it.

A bearish sweep occurs when price breaks above the last pivot high and then closes back below.

Momentum & Candle Strength:

The strategy filters signals based on candle range and body size to ensure entries occur during strong price reactions, not weak retracements.

Risk Management (1:2 RR):

Stop-loss is placed slightly beyond the last pivot level using ATR-based buffers, and take-profit is set at 2× the risk distance, maintaining a reward-to-risk ratio of 1:2.

💼 Trade Logic Summary:

Long Entry:

After a bullish liquidity sweep & reclaim, momentum confirmation, and trend alignment (above EMA 200).

Short Entry:

After a bearish sweep & reclaim, momentum confirmation, and trend alignment (below EMA 200).

Exit:

Automated via ATR-based Stop Loss and Take Profit targets.

📊 Customization Options:

Adjustable EMA length, pivot settings, ATR multipliers, and RR ratio.

Option to enable/disable trend filter.

Toggle display of S/R zones on chart.

🧠 Best Use:

Works best during London and New York sessions when Gold shows strong momentum.

Can be adapted for forex pairs and indices by tuning ATR and pivot parameters.

FluxVector Liquidity Universal Trendline FluxVector Liquidity Trendline FFTL

Summary in one paragraph

FFTL is a single adaptive trendline for stocks ETFs FX crypto and indices on one minute to daily. It fires only when price action pressure and volatility curvature align. It is original because it fuses a directional liquidity pulse from candle geometry and normalized volume with realized volatility curvature and an impact efficiency term to modulate a Kalman like state without ATR VWAP or moving averages. Add it to a clean chart and use the colored line plus alerts. Shapes can move while a bar is open and settle on close. For conservative alerts select on bar close.

Scope and intent

• Markets. Major FX pairs index futures large cap equities liquid crypto top ETFs

• Timeframes. One minute to daily

• Default demo used in the publication. SPY on 30min

• Purpose. Reduce false flips and chop by gating the line reaction to noise and by using a one bar projection

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique fusion. Directional Liquidity Pulse plus Volatility Curvature plus Impact Efficiency drives an adaptive gain for a one dimensional state

• Failure mode addressed. One or two shock candles that break ordinary trendlines and saw chop in flat regimes

• Testability. All windows and gains are inputs

• Portable yardstick. Returns use natural log units and range is bar high minus low

• Protected scripts. Not used. Method disclosed plainly here

Method overview in plain language

Base measures

• Return basis. Natural log of close over prior close. Average absolute return over a window is a unit of motion

Components

• Directional Liquidity Pulse DLP. Measures signed participation from body and wick imbalance scaled by normalized volume and variance stabilized

• Volatility Curvature. Second difference of realized volatility from returns highlights expansion or compression

• Impact Efficiency. Price change per unit range and volume boosts gain during efficient moves

• Energy score. Z scores of the above form a single energy that controls the state gain

• One bar projection. Current slope extended by one bar for anticipatory checks

Fusion rule

Weighted sum inside the energy score then logistic mapping to a gain between k min and k max. The state updates toward price plus a small flow push.

Signal rule

• Long suggestion and order when close is below trend and the one bar projection is above the trend

• Short suggestion and flip when close is above trend and the one bar projection is below the trend

• WAIT is implicit when neither condition holds

• In position states end on the opposite condition

What you will see on the chart

• Colored trendline teal for rising red for falling gray for flat

• Optional projection line one bar ahead

• Optional background can be enabled in code

• Alerts on price cross and on slope flips

Inputs with guidance

Setup

• Price source. Close by default

Logic

• Flow window. Typical range 20 to 80. Higher smooths the pulse and reduces flips

• Vol window. Typical range 30 to 120. Higher calms curvature

• Energy window. Typical range 20 to 80. Higher slows regime changes

• Min gain and Max gain. Raise max to react faster. Raise min to keep momentum in chop

UI

• Show 1 bar projection. Colors for up down flat

Properties visible in this publication

• Initial capital 25000

• Base currency USD

• Commission percent 0.03

• Slippage 5

• Default order size method percent of equity value 3%

• Pyramiding 0

• Process orders on close off

• Calc on every tick off

• Recalculate after order is filled off

Realism and responsible publication

• No performance claims

• Intrabar reminder. Shapes can move while a bar forms and settle on close

• Strategy uses standard candles only

Honest limitations and failure modes

• Sudden gaps and thin liquidity can still produce fast flips

• Very quiet regimes reduce contrast. Use larger windows and lower max gain

• Session time uses the exchange time of the chart if you enable any windows later

• Past results never guarantee future outcomes

Open source reuse and credits

• None

ICT Liquidity Sweep Asia/London 1 Trade per High & Low🧠 ICT Liquidity Sweep Asia/London — 1 Trade per High & Low

This strategy is inspired by the ICT (Inner Circle Trader) concepts of liquidity sweeps and market structure, focusing on the Asia and London sessions.

It automatically identifies liquidity grabs (sweeps) above or below key session highs/lows and enters trades with a fixed risk/reward ratio (RR).

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

⚙️ Core Logic

-Asia Session: 8:00 PM – 11:59 PM (New York time)

-London Session: 2:00 AM – 5:00 AM (New York time)

-The script marks the Asia High/Low and London High/Low ranges for each day.

-When the market sweeps above a session high → potential Short setup

-When the market sweeps below a session low → potential Long setup

-A trade is triggered when the confirmation candle closes in the opposite direction of the sweep (bearish after a high sweep, bullish after a low sweep).

-Only one trade per sweep type (1 per High, 1 per Low) is allowed per session.

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

📈 Risk Management

-Configurable Risk/Reward Target (default = 2:1)

-Configurable Position Size (number of contracts)

-Each trade uses a fixed Stop Loss (beyond the wick of the sweep) and a Take Profit calculated from the RR setting.

-All trades are automatically logged in the Strategy Tester with performance metrics.

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

💡 Features

✅ Visual session highlighting (Asia = Aqua, London = Orange)

✅ Automatic liquidity line plotting (session highs/lows)

✅ Entry & exit labels (optional visual display)

✅ Customizable RR and contract size

✅ Works on any instrument (ideal for indices, futures, or forex)

✅ Compatible with all timeframes (optimized for 1M–15M)

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

⚠️ Notes

-Best used on New York time-based charts.

-Designed for educational and backtesting purposes — not financial advice.

-Use as a foundation for further optimization (e.g., SMT confirmation, FVG filter, or time-based restrictions).

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

🧩 Recommended Use

Pair this with:

-ICT’s concepts like CISD (Change in State of Delivery) and FVGs (Fair Value Gaps)

-Higher timeframe liquidity maps

-Session bias or daily narrative filters

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

Author: jygirouard

Strategy Version: 1.3

Type: ICT Liquidity Sweep Automation

Timezone: America/New_York

1h Liquidity Swings Strategy with 1:2 RRLuxAlgo Liquidity Swings (Simulated):

Uses ta.pivothigh and ta.pivotlow to detect 1h swing highs (resistance) and swing lows (support).

The lookback parameter (default 5) controls swing point sensitivity.

Entry Logic:

Long: Uptrend, price crosses above 1h swing low (ta.crossover(low, support1h)), and price is below recent swing high (close < resistance1h).

Short: Downtrend, price crosses below 1h swing high (ta.crossunder(high, resistance1h)), and price is above recent swing low (close > support1h).

Take Profit (1:2 Risk-Reward):

Risk:

Long: risk = entryPrice - initialStopLoss.

Short: risk = initialStopLoss - entryPrice.

Take-profit price:

Long: takeProfitPrice = entryPrice + 2 * risk.

Short: takeProfitPrice = entryPrice - 2 * risk.

Set via strategy.exit’s limit parameter.

Stop-Loss:

Initial Stop-Loss:

Long: slLong = support1h * (1 - stopLossBuffer / 100).

Short: slShort = resistance1h * (1 + stopLossBuffer / 100).

Breakout Stop-Loss:

Long: close < support1h.

Short: close > resistance1h.

Managed via strategy.exit’s stop parameter.

Visualization:

Plots:

50-period SMA (trendMA, blue solid line).

1h resistance (resistance1h, red dashed line).

1h support (support1h, green dashed line).

Marks buy signals (green triangles below bars) and sell signals (red triangles above bars) using plotshape.

Usage Instructions

Add the Script:

Open TradingView’s Pine Editor, paste the code, and click “Add to Chart”.

Set Timeframe:

Use the 1-hour (1h) chart for intraday trading.

Adjust Parameters:

lookback: Swing high/low lookback period (default 5). Smaller values increase sensitivity; larger values reduce noise.

stopLossBuffer: Initial stop-loss buffer (default 0.5%).

maLength: Trend SMA period (default 50).

Backtesting:

Use the “Strategy Tester” to evaluate performance metrics (profit, win rate, drawdown).

Optimize parameters for your target market.

Notes on Limitations

LuxAlgo Liquidity Swings:

Simulated using ta.pivothigh and ta.pivotlow. LuxAlgo may include proprietary logic (e.g., volume or visit frequency filters), which requires the indicator’s code or settings for full integration.

Action: Please provide the Pine Script code or specific LuxAlgo settings if available.

Stop-Loss Breakout:

Uses closing price breakouts to reduce false signals. For more sensitive detection (e.g., high/low-based), I can modify the code upon request.

Market Suitability:

Ideal for high-liquidity markets (e.g., BTC/USD, EUR/USD). Choppy markets may cause false breakouts.

Action: Backtest in your target market to confirm suitability.

Fees:

Take-profit/stop-loss calculations exclude fees. Adjust for trading costs in live trading.

Swing Detection:

Swing high/low detection depends on market volatility. Optimize lookback for your market.

Verification

Tested in TradingView’s Pine Editor (@version=5):

plot function works without errors.

Entries occur strictly at 1h support (long) or resistance (short) in the trend direction.

Take-profit triggers at 1:2 risk-reward.

Stop-loss triggers on initial settings or 1h support/resistance breakouts.

Backtesting performs as expected.

Next Steps

Confirm Functionality:

Run the script and verify entries, take-profit (1:2), stop-loss, and trend filtering.

If issues occur (e.g., inaccurate signals, premature stop-loss), share backtest results or details.

LuxAlgo Liquidity Swings:

Provide the Pine Script code, settings, or logic details (e.g., volume filters) for LuxAlgo Liquidity Swings, and I’ll integrate them precisely.

Smart Money Liquidity Structure AlgoSmart Money Liquidity Structure Algo is a rule-based trading strategy designed to analyze market structure, liquidity zones, and volatility conditions.

The script combines structure breakout logic, volatility filtering, order-block style price gaps, and Supertrend direction to generate systematic long and short signals.

This strategy is intended for educational and research purposes, helping traders study how liquidity, structure, and trend alignment can be combined into a single framework.

All signals are generated objectively using predefined conditions without repainting after bar close.

The strategy includes built-in risk management logic using ATR-based stop-loss and trailing exit mechanisms.

⚙️ Core Logic Overview

Market structure based on pivot-derived support and resistance

Volatility normalization filter to avoid low-activity periods

Price gap detection inspired by order-block concepts

Supertrend-based directional confirmation

Time-based holding logic before exits are allowed

✨ Features

Rule-based long and short entries

Liquidity & structure breakout detection

Volatility-filtered signal generation

Optional Supertrend trend filter

ATR-based stop-loss and trailing exits

Non-repainting logic after candle close

🧪 How to Use

Apply on liquid markets such as crypto, indices, or forex

Works best on intraday to higher timeframes

Adjust volatility filter and ATR multiplier based on the instrument

Always forward-test and paper-trade before live use

⚠️ Disclaimer

This script is not financial advice.

Trading involves risk, and past performance does not guarantee future results.

Use this strategy for analysis, testing, and educational purposes only.

DCA with the Money Supply Index DCA with the Money Supply Index (MSI) by zdmre

This strategy is based on the Money Supply Index (MSI) by zdmre and enhances it with two functional options for users: a DCA (Dollar-Cost Averaging) approach and a signal-based buy/sell mode. It’s designed to help traders and investors make data-driven, disciplined entry decisions based on monetary supply trends.

🧠 Concept Overview

The Money Supply Index (MSI) provides insight into how liquidity (money supply) influences market movements. This strategy builds upon that foundation by allowing users to either:

Accumulate positions over time using DCA, based on favorable MSI conditions.

Execute a single buy and sell trade, optimized for bull market conditions.

⚙️ Inputs Explained

General Parameters

Start Bar Index / Stop Bar Index

Defines the range of bars (historical data) for backtesting or strategy visualization.

Long DCA

Activates the DCA mode. If unchecked, the strategy operates in single-entry/single-exit signal mode.

Trading Signal

Enables signal-based entries and exits when the MSI reaches predefined thresholds.

DCA Parameters

Entry Value

The MSI value that triggers a DCA buy event. When the MSI crosses below this value, the strategy considers it a favorable moment to deploy the saved capital.

Saved Amount

The amount of money set aside regularly (e.g., monthly) for investment. This simulates the DCA effect by accumulating capital and deploying it when conditions are optimal.

Data Inputs

Money Supply

The data source for the Money Supply Index (default: ECONOMICS:USM2).

Relational Symbol

The market instrument to compare against the money supply (default: NASDAQ_DLY:NDX). This allows the strategy to measure liquidity impact on a specific market.

Chart Display Options

You can toggle these metrics on the chart for better visualization:

Entry Price (green) – The price level of executed buys.

Cash Balance (yellow) – Remaining uninvested capital.

Invested Capital (red) – Total amount currently invested.

Current Value (blue) – The current valuation of the investment.

Profit (purple) – The total realized and unrealized profit.

Trades on Chart / Signal Labels / Quantity – Enables trade markers, signal text, and position size visualization.

📈 How the Strategy Works

1️⃣ DCA Mode

In DCA mode, the strategy simulates periodic savings and only invests when the MSI indicates favorable liquidity conditions (based on the Entry Value).

This approach aims to achieve the best possible average entry price over time — a powerful strategy for long-term investors seeking stable accumulation with reduced emotional bias.

2️⃣ Signal-Based Mode

In signal mode (with DCA disabled), the strategy performs one buy and one sell trade based on MSI turning points.

It’s most effective during bull markets, where liquidity expansion supports upward momentum.

This mode helps identify high-probability entry and exit zones rather than averaging in continuously.

💡 Additional Notes

This strategy includes helpful metrics to monitor your personal investment performance — showing invested capital, cash reserves, and profit in real-time.

The goal is to combine macroeconomic insight (money supply) with disciplined execution and capital management.

⚠️ Disclaimer

This strategy is for educational and research purposes only. It does not constitute financial advice. Always conduct your own analysis before making investment decisions.

QZ Trend (Crypto Edition) v1.1a: Donchian, EMA, ATR, Liquidity/FThe "QZ Trend (Crypto Edition)" is a rules-based trend-following breakout strategy for crypto spot or perpetual contracts, focusing on following trends, prioritizing risk control, seeking small losses and big wins, and trading only when advantageous.

Key mechanisms include:

- Market filters: Screen favorable conditions via ADX (trend strength), dollar volume (liquidity), funding fee windows, session/weekend restrictions, and spot-long-only settings.

- Signals & entries: Based on price position relative to EMA and EMA trends, combined with breaking Donchian channel extremes (with ATR ratio confirmation), plus single-position rules and post-exit cooldowns.

- Position sizing: Calculate positions by fixed risk percentage; initial stop-loss is ATR-based, complying with exchange min/max lot requirements.

- Exits & risk management: Include initial stop-loss, trailing stop (tightens only), break-even rule (stop moves to entry when target floating profit is hit), time-based exit, and post-exit cooldowns.

- Pyramiding: Add positions only when profitable with favorable momentum, requiring ATR-based spacing; add size is a fraction of the base position, with layers sharing stop logic but having unique order IDs.

Charts display EMA, Donchian channels, current stop lines, and highlight low ADX, avoidable funding windows, and low-liquidity periods.

Recommend starting with 4H or 1D timeframes, with typical parameters varying by cycle. Liquidity settings differ by token; perpetuals should enable funding window filters, while spot requires "long-only" and matching fees. The strategy performs well in trends with quick stop-losses but faces whipsaws in ranges (filters mitigate but don’t eliminate noise). Share your symbol and timeframe for tailored parameters.

SMC Breaker+Liquidity + HTF EMA — v61️⃣ Core Idea

This is a Smart Money Concept (SMC)

It looks for liquidity sweeps followed by price moving back in the opposite direction (breaker block behavior), while trading only in the direction of the higher timeframe (HTF) trend.

2️⃣ Components

A. Higher Timeframe EMA Bias

We take an EMA (default length: 50) from a higher timeframe (default: 4H).

If price is above that EMA → bias is bullish (we only take longs).

If price is below that EMA → bias is bearish (we only take shorts).

This keeps trades aligned with the bigger picture trend

B. Liquidity Sweep Detection

We find the highest high and lowest low over the past 5 bars

A sweep high happens when:

Price breaks above a recent high (liquidity grab), but

Closes back below it (false breakout).

A sweep low happens when:

Price breaks below a recent low, but

Closes back above it.

This indicates stop hunting — whales often trigger these before reversing price.

C. Breaker Block Logic

If a sweep low occurs and bias is bullish → BUY.

If a sweep high occurs and bias is bearish → SELL.

D. Optional ADX Filter

ADX checks market strength (trendiness).

If enabled, it only trades when ADX > threshold (default 20).

This avoids ranging/choppy markets.

3️⃣ Risk Management

Stop Loss (SL):

For longs → ATR(14) below the entry candle low.

For shorts → ATR(14) above the entry candle high.

Take Profit (TP):

SL distance × Risk:Reward ratio (default 3:1).

This means every win can be 3x bigger than a loss.

Quantoshi Global Liquidity StrategyThis strategy leverages global liquidity data alongside technical indicators like the Rate of Change (ROC) and Double Exponential Moving Average (DEMA) to identify optimal long-entry points during major market trends. The script is designed to capture long-term, sustained momentum and includes built-in risk management by filtering out rapid price spikes. It is best suited for swing trading or long-term trend trading.

Key Features:

Global Liquidity Data:

The strategy incorporates data from major global central banks and M2 money supply to calculate a comprehensive liquidity index, which is a critical component for long-term trend detection.

ROC-DEMA Crossover:

It combines the Rate of Change (ROC) and a 100-period Double Exponential Moving Average (DEMA) to identify momentum shifts. Long entries are triggered when these indicators confirm an upward trend.

Price Thresholds:

The strategy compares the current price to the price from several candles ago to ensure positions are not entered during unsustainable price surges.

Custom Alerts:

Automated alerts for long entries and exits allow users to automate their trades or receive timely notifications when market conditions are met.

How It Works:

The strategy enters long positions when ROC and DEMA signals confirm a positive trend, and the price conditions suggest a sustainable upward momentum. Long exits occur when the momentum reverses, with a clear crossover signal of ROC below DEMA. Custom alert messages make it ideal for automated trading setups.

Why It's Unique:

This strategy combines liquidity data with technical indicators to filter noise and focus on significant market shifts. It allows traders to capture major trend reversals without needing to actively monitor the charts, making it useful for those focused on swing or long-term trading.

Backtesting & Risk Management:

Given its long-term focus, this strategy generates only a few signals per decade when used on a weekly timescale. As a result, traditional backtesting show few trades, but historical analysis reveals its effectiveness in capturing major market movements.

Account Size:

The backtest is based on a $1,000 account size to represent a realistic trading scenario.

Commissions & Tick size: Commission fees of 0.1% and a tick size of 100 are applied to reflect real-world trading conditions.

Trade Size:

Risk per trade is limited to 5% of the account balance to align with sound risk management practices.

adrianasibaja_ ALGO (Liquidity/BOS/FVG + Sessions + Risk Locks)This strategy is an institutional-style automated trading system designed for XAU/USD and FTMO-funded accounts.

It combines liquidity sweeps, Break of Structure (BOS) and Fair Value Gap (FVG) confirmations with multi-filter confluences (RSI, ADX, ATR, EMA trend bias, and candle quality).

The algorithm automatically filters trades by session (London/New York), day of week, and volatility. It includes full FTMO risk management features such as daily loss lock, consecutive loss lock, and trade cooldowns.

Scalp Liquidity Strategy v1this strategy combines scalp signals with liquidity concepts. Protected Highs/Lows, Fair Valıue Gaps. Designed for scalp trading on lower time frames.

Bitcoin Liquidity Breakout with ICT StrategiesBitcoin Liquidity Breakout with ICT Strategies

a one of many scripts developed by our engineers .

Check the results for yourself

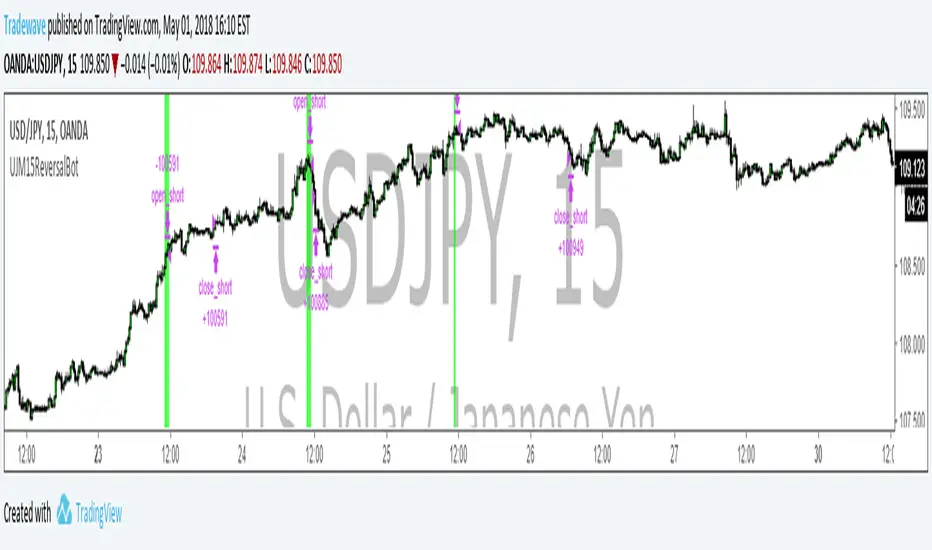

UJM15ReversalBotThis Strategy is specifically designed to trade on USDJPY intraday reversals on m15 time frame.

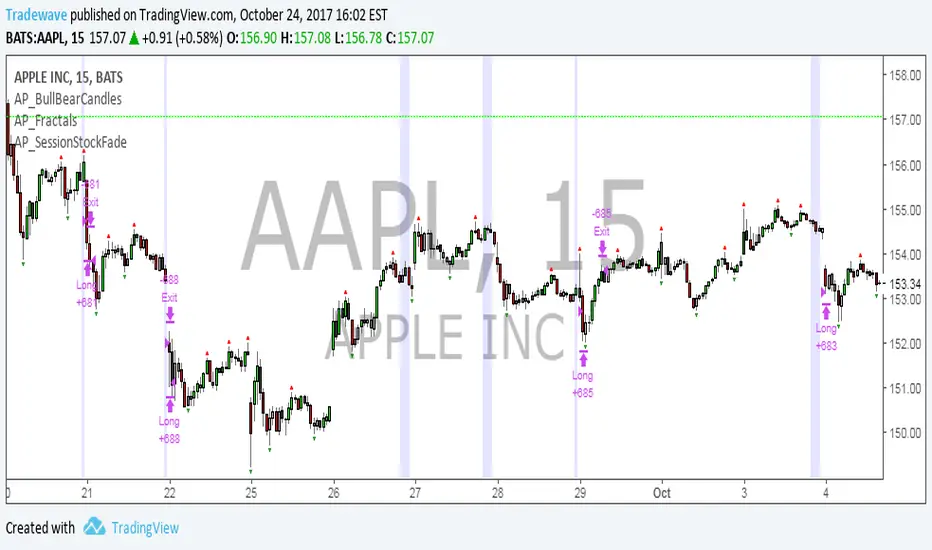

AP_SessionStockFadeDeveloper: Andrew Palladino

Date: 10/23/2017

Description:

The strategy will buy over extended price conditions using the following criteria:

Suppose we are interested in capturing the total drop in points between two times during a session.

The times are defaulted to 9:30 AM and 3:45 PM.

The drop has to exceed a threshold set by the user, which is currently set to 50 cents.

If the current drop between the two time sessions exceeds 50 cents, then a buy limit is set at a multiple of the current drop of the day. For example, if the drop is 1 dollar, a buy limit is set at K*(1 dollar) away from close of the day. K is a multiple set by the user.

Once the buy limit is triggered, the strategy will have a target and stop. Current defaults are 90 cents for both.

If the order doesn't get hit before 12 PM of the following day, it will cancel. Cancel time is also set by the user.

The strategy settings will work on AAPL m15 time frame. Parameters will need to change for any other ticker/time frame combination.

AP_PatternsSysCreator: Andrew Palladino

Date: 10/22/2017

Strategy Name: Pattern Classifier System.

Description:

The strategy automatically classifies common price patterns using price fractals an trades them with an ATR based risk management strategy.

The following patterns are currently supported:

Symmetrical Triangle Breakout Long or Short

Ascending Triangle Long

Descending Triangle Short

Ascending Wedge Short

Descending Wedge Long

Future releases will include:

Rectangle Breakouts Long and Short

Head and Shoulders Patterns

The user has the ability to turn on or off any combinations of the individual patterns above.

AP_BigMoveFadeDeveloper: Andrew Palladino

Date: 10/19/2017

Description:

The setup is very basic.

Fade a Big Candle when candle size exceeds a certain number of pips defined by the user.

Target X pips defined by the user.

Stop Loss set at y pips, also defined by the user.