Multipower Entry SecretMultipower Entry Secret indicator is designed to be the ultimate trading companion for traders of all skill levels—especially those who struggle with decision-making due to unclear or overwhelming signals. Unlike conventional trading systems cluttered with too many lines and confusing alerts, this indicator provides a clear, adaptive, and actionable guide for market entries and exits.

Key Points:

Clear Buy/Sell/Wait Signals:

The script dynamically analyzes price action, candle patterns, volume, trend strength, and higher time frame context. This means it gives you “Buy,” “Sell,” or “Wait” signals based on real, meaningful market information—filtering out the noise and weak trades.

Multi-Timeframe Adaptive Analysis:

It synchronizes signals between higher and current timeframes, ensuring you get the most reliable direction—reducing the risk of getting caught in fake moves or sudden reversals.

Automatic Support, Resistance & Liquidity Zones:

Key levels like support, resistance, and liquidity zones are auto-detected and displayed directly on the chart, helping you make precise decisions without manual drawing.

Real-Time Dashboard:

All relevant information, such as trend strength, market intent, volume sentiment, and the reason behind each signal, is neatly summarized in a dashboard—making monitoring effortless and intuitive.

Customizable & Beginner-Friendly:

Whether you’re a newcomer wanting straightforward guidance or a professional needing advanced customization, the indicator offers flexible options to adjust analysis depth, timeframes, sensitivity, and more.

Visual & Clutter-Free:

The design ensures that your chart remains clean and readable, showing only the most important information. This minimizes mental overload and allows for instant decision-making.

Who Will Benefit?

Beginners who want to learn trading logic, avoid common traps, and see the exact reason behind every signal.

Advanced traders who require adaptive multi-timeframe analytics, fast execution, and stress-free monitoring.

Anyone who wants to save screen time, reduce analysis paralysis, and have more confidence in every trade they take.

1. No Indicator Clutter

Intent:

Many traders get confused by charts filled with too many indicators and signals. This often leads to hesitation, missed trades, or taking random, risky trades.

In this Indicator:

You get a clean and clutter-free chart. Only the most important buy/sell/wait signals and relevant support/resistance/liquidity levels are shown. These update automatically, removing the “overload” and keeping your focus sharp, so your decision-making is faster and stress-free.

2. Exact Entry Guide

Intent:

Traders often struggle with entry timing, leading to FOMO (fear of missing out) or getting trapped in sudden market reversals.

In this Indicator:

The system uses powerful adaptive logic to filter out weak signals and only highlight the strongest market moves. This not only prevents you from entering late or on noise, but also helps avoid losses from false breakouts or whipsaws. You get actionable suggestions—when to enter, when to hold back—so your entries are high-conviction and disciplined.

3. HTF+LTF Logic: Multitimeframe Sync Analysis

Intent:

Most losing trades happen when you act only on the short-term chart, ignoring the bigger market trend.

In this Indicator:

Signals are based on both the current chart timeframe (LTF) and a higher (HTF, like hourly/daily) timeframe. The indicator synchronizes trend direction, momentum, and structure across both levels, quickly adapting to show you when both are aligned. This filtering results in “only trade with the bigger trend”—dramatically increasing your win rate and market confidence.

4. Auto Support/Resistance & Liquidity Zones

Intent:

Drawing support/resistance and liquidity zones manually is time-consuming and error-prone, especially for beginners.

In this Indicator:

The system automatically identifies and plots the most crucial support/resistance levels and liquidity zones on your chart. This is based on adaptive, real-time price and volume analysis. These zones highlight where major institutional activity, trap setups, or real breakouts/reversals are most likely, removing guesswork and giving you a clear reference for entries, exits, and stop placements.

5. Clear Action/Direction

Intent:

Traders need certainty—what does the market want right now? Most indicators are vague.

In this Indicator:

Your dashboard always displays in plain words (like “BUY”, “SELL”, or “WAIT”) what action makes sense in the current market phase. Whether it’s a bull trap, volume spike, wick reversal, or exhaustion—it’s interpreted and explained clearly. No more confusion—just direct, real-time advice.

6. For Everyone (Beginner to Pro)

Intent:

Most advanced indicators are overwhelming for new traders; simple ones lack depth for professionals.

In this Indicator:

It is simple enough for a beginner—just add it to the chart and instantly see what action to consider. At the same time, it includes advanced adaptive analysis, multi-timeframe logic, and customizable settings so professional traders can fine-tune it for their strategies.

7. Ideal Usage and User Benefits

Instant Decision Support:

Whenever you’re unsure about a trade, just look at the indicator’s suggestion for clarity.

Entry Learning:

Beginners get real-time “practice” by not only seeing signals, but also the reason behind them—improving your chart reading and market understanding.

Screen Time & Stress Reduction:

Clear, relevant information only; no noise, less fatigue, faster decisions.

Makes Trading Confident & Simple:

The smart dashboard splits actionable levels (HTF, LTF, action) so you never miss a move, avoid traps, and stay aligned with high-probability trades.

8. Advanced Input Settings (Smart Customization)

Explained with Examples:

Enable Wick Analysis:

Finds candles with strong upper/lower wicks (signs of rejection/buying/selling force), alerting you to hidden reversals and protecting from FOMO entries.

Enable Absorption:

Detects when heavy order flow from one side is “absorbed” by the other (shows where institutional buyers/sellers are likely active, helps spot fake breakouts).

Enable Unusual Breakout:

Highlights real breakouts—large volatility plus high volume—so you catch genuine moves and avoid random spikes.

Enable Range/Expansion:

Smartly flags sudden range expansions—when the market goes from quiet to volatile—so you can act at the start of real trends.

Trend Bar Lookback:

Adjusts how many bars/candles are used in trend calculations. Short (fast trades, more signals), long (more reliability, fewer whipsaws).

Bull/Bear Bars for Strong Trend Min:

Sets how many candles in a row must support a trend before calling it “strong”—prevents flipping signals, keeps you disciplined.

Volume MA Length:

Lets you adjust how many bars back volume is averaged—fine-tune for your asset and trading style for best volume signals.

Swing Lookback Bars:

Set how many bars to use for swing high/low detection—short (quick swing levels), long (stronger support/resistance).

HTF (Bias Window):

Decide which higher timeframe the indicator should use for big-picture market mood. Adjustable for any style (scalp, swing, position).

Adaptive Lookback (HTF):

Choose how much HTF history is used for detecting major extremes/zones. Quick adjust for more/less sensitivity.

Show Support/Resistance, Liquidity Zones, Trendlines:

Toggle them on/off instantly per your needs—keeps your chart relevant and tailored.

9. Live Dashboard Sections Explained

Intent HTF:

Shows if the bigger timeframe currently has a Bullish, Bearish, or Neutral (“Chop”) intent, based on strict volume/price body calculations. Instant clarity—no more guessing on trend bias.

HTF Bias:

Clear message about which side (buy/sell/sideways) controls the market on the higher timeframe, so you always trade with the “big money.”

Chart Action:

The central action for the current bar—Whether to Buy, Sell, or Wait—calculated from all indicator logic, not just one rule.

TrendScore Long/Short:

See how many candles in your chosen window were bullish or bearish, at a glance. Instantly gauge market momentum.

Reason (WHY):

Every time a signal appears, the “reason” cell tells you the primary logic (breakout, wick, strong trend, etc.) behind it. Full transparency and learning—never trade blindly.

Strong Trend:

Shows if the market is currently in a powerful trend or not—helping you avoid choppy, risky entries.

HTF Vol/Body:

Displays current higher timeframe volume and candle body %—helping spot when big players are active for higher probability trades.

Volume Sentiment:

A real-time analysis of market psychology (strong bullish/bearish, neutral)—making your decision-making much more confident.

10. Smart and User-Friendly Design

Multi-timeframe Adaptive:

All calculations can now be drawn from your choice of higher or current timeframe, ensuring signals are filtered by larger market context.

Flexible Table Position:

You can set the live dashboard/summary anywhere on the chart for best visibility.

Refined Zone Visualization:

Liquidity and order blocks are visually highlighted, auto-tuning for your settings and always cleaning up to stay clutter-free.

Multi-Lingual & Beginner Accessible:

With Hindi and simple English support, descriptions and settings are accessible for a wide audience—anyone can start using powerful trading logic with zero language barrier.

Efficient Labels & Clear Reasoning:

Signal labels and reasons are shown/removed dynamically so your chart stays informative, not messy.

Every detail of this indicator is designed to make trading both simpler and smarter—helping you avoid the common pitfalls, learn real price action, stay in sync with the market’s true mood, and act with discipline for higher consistency and confidence.

This indicator makes professional-grade market analysis accessible to everyone. It’s your trusted assistant for making smarter, faster, and more profitable trading decisions—providing not just signals, but also the “why” behind every action. With auto-adaptive logic, clear visuals, and strong focus on real trading needs, it lets you focus on capturing the moves that matter—every single time.

Cerca negli script per "liquidity"

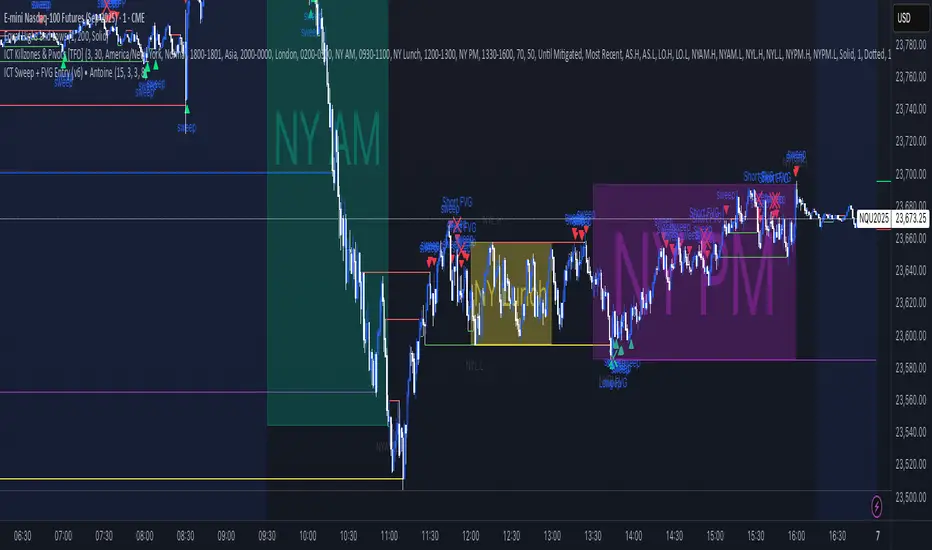

ICT Sweep + FVG Entry (v6) • Antoine📌 ICT Sweep + FVG Entry (Antoine)

This indicator is designed for price action traders who follow ICT concepts and want a mechanical tool to spot liquidity sweeps, fair value gaps (FVGs), and precise entry signals.

🔎 Key Features

Liquidity Pools (HTF)

• Automatically plots recent swing highs/lows from a higher timeframe (5m/15m).

• These act as Buy Side Liquidity (BSL) and Sell Side Liquidity (SSL) levels where stop orders accumulate.

Sweep Detection

• Identifies when price breaks a pool (BSL/SSL) but closes back inside → a classic liquidity grab.

• Plots a triangle on the chart when a sweep is confirmed.

Fair Value Gap (FVG) Highlighting

• Detects bullish and bearish FVGs on the execution timeframe (ideal for 1m).

• Option to display active FVG zones with shaded boxes.

Entry Signals

• A signal (cross) appears when:

A liquidity sweep occurs.

An FVG forms in the direction of the rejection.

Price retests the FVG (entry at the 50% mid-level or edge).

Alerts Ready

• Get alerted for sweeps (bullish/bearish) and for entry confirmations (long/short FVG retests).

🎯 How to Use

Choose your HTF (5m or 15m) → The indicator maps major liquidity pools.

Drop to LTF (1m) → Wait for a sweep signal at one of the pools.

Confirm with FVG → If an FVG appears in the sweep’s direction, the indicator waits for a retest.

Entry → Enter on the retest of the FVG (edge or 50%).

Risk Management

Stop loss: just beyond the sweep’s wick.

Target: opposite liquidity pool.

Minimum recommended R:R: 1:2.

✅ Why this helps

This tool makes it easier to trade ICT-style setups without missing opportunities:

No need to manually draw every swing high/low.

Automatic FVG detection saves time.

Clear sweep + FVG + retest logic keeps your entries mechanical and disciplined.

⚠️ Disclaimer: This script is for educational purposes only. It does not guarantee profits. Always use proper risk management.

UNITY[ALGO] PO3 V3Of course. Here is a complete and professional description in English for the indicator we have built, detailing all of its features and functionalities.

Indicator: UNITY PO3 V7.2

Overview

The UNITY PO3 is an advanced, multi-faceted technical analysis tool designed to identify high-probability reversal setups based on the Swing Failure Pattern (SFP). It combines real-time SFP detection on the current timeframe with a sophisticated analysis of key institutional liquidity zones from the H4 timeframe, presenting all information in a clear, dynamic, and interactive visual interface.

This indicator is built for traders who use liquidity concepts, providing a complete dashboard of entries, targets, and invalidation levels directly on the chart.

Core Features & Functionality

1. Swing Failure Pattern (SFP) Detection (Current Timeframe)

The indicator's primary engine identifies SFPs on the chart's active timeframe with two layers of logic:

Standard SFP: Detects a classic liquidity sweep where the current candle's wick takes out the high or low of the previous candle and the body closes back within the previous candle's range.

Outside Bar SFP Logic: Intelligently analyzes engulfing candles that sweep both the high and low of the previous candle. A valid signal is only generated if the candle has a clear directional close:

Bullish Signal: If the outside bar closes higher than its open.

Bearish Signal: If the outside bar closes lower than its open.

Neutral (doji-like) outside bars are ignored to filter for indecision.

2. Comprehensive On-Chart SFP Markings

When a valid SFP is detected, a full suite of dynamic drawings appears on the chart:

Failure Line: A dashed line (red for bearish, green for bullish) marking the precise price level of the liquidity sweep.

PREMIUM ZONE (SFP Candle Wick): A transparent, colored rectangle highlighting the rejection wick of the signal candle (the upper wick for bearish SFPs, the lower wick for bullish SFPs). This zone automatically extends to the right, following the current price, until the DOL is hit.

CRT BOX (Reference Candle): A transparent box with a colored border drawn around the entire range of the candle that was swept (Candle 1). This highlights the full liquidity zone and also extends dynamically until the DOL is hit.

Dynamic Target Line: A blue dashed line marking the primary objective (the low of the signal candle for shorts, the high for longs).

The line begins with a "⏳ Target" label and extends with the current price.

Upon being touched by price, the line freezes, and its label permanently changes to "✅ Target".

Dynamic DOL (Draw on Liquidity) Line: An orange dashed line marking the invalidation level, defined as the opposite extremity of the swept candle (Candle 1).

It begins with a "⏳ dol" label and extends with the price.

Upon being touched, it freezes, and its label changes to "✅ dol".

3. Multi-Session Killzone Liquidity Levels (H4 Analysis)

The indicator automatically analyzes the H4 timeframe in the background to identify and plot key liquidity levels from three major trading sessions, based on their UTC opening times.

1am Killzone (London Lunch): Tracks the high/low of the 05:00 UTC H4 candle.

5am Killzone (London Open): Tracks the high/low of the 09:00 UTC H4 candle.

9am Killzone (NY Open): Tracks the high/low of the 13:00 UTC H4 candle.

For each of these Killzones, the indicator provides two types of analysis:

Last KZ Lines: Plots the high and low of the most recent qualifying Killzone candle. These lines are dynamic, extending with price and showing a ⏳/✅ status when touched.

Fresh Zones: A powerful feature that scans the entire available history of Killzones to find and display the closest untouched high (above the current price) and the closest untouched low (below the current price). These "Fresh" lines are also fully dynamic and provide a real-time view of the most relevant nearby liquidity targets.

4. Advanced User Settings & Chart Management

The indicator is designed for a clean and user-centric experience with powerful customization:

Show Only Last SFP: Keeps the chart clean by automatically deleting the previous SFP setup when a new one appears.

Hide SFP on DOL Reset: When checked, automatically removes all drawings related to an SFP setup the moment its invalidation level (DOL line) is touched. This leaves only active, valid setups on the chart.

Hide Consumed KZ: When checked, automatically removes any Killzone or Fresh Zone line from the chart as soon as it is touched by the price.

Independent Toggles: Every visual element—SFP signals, each of the three Killzones, and their respective "Fresh" zone counterparts—can be turned on or off independently from the settings menu for complete control over the visual display.

Z-Order Priority: All indicator drawings are rendered in front of the chart candles, ensuring they are always clearly visible and never hidden from view.

Adaptive Investment Timing ModelA COMPREHENSIVE FRAMEWORK FOR SYSTEMATIC EQUITY INVESTMENT TIMING

Investment timing represents one of the most challenging aspects of portfolio management, with extensive academic literature documenting the difficulty of consistently achieving superior risk-adjusted returns through market timing strategies (Malkiel, 2003).

Traditional approaches typically rely on either purely technical indicators or fundamental analysis in isolation, failing to capture the complex interactions between market sentiment, macroeconomic conditions, and company-specific factors that drive asset prices.

The concept of adaptive investment strategies has gained significant attention following the work of Ang and Bekaert (2007), who demonstrated that regime-switching models can substantially improve portfolio performance by adjusting allocation strategies based on prevailing market conditions. Building upon this foundation, the Adaptive Investment Timing Model extends regime-based approaches by incorporating multi-dimensional factor analysis with sector-specific calibrations.

Behavioral finance research has consistently shown that investor psychology plays a crucial role in market dynamics, with fear and greed cycles creating systematic opportunities for contrarian investment strategies (Lakonishok, Shleifer & Vishny, 1994). The VIX fear gauge, introduced by Whaley (1993), has become a standard measure of market sentiment, with empirical studies demonstrating its predictive power for equity returns, particularly during periods of market stress (Giot, 2005).

LITERATURE REVIEW AND THEORETICAL FOUNDATION

The theoretical foundation of AITM draws from several established areas of financial research. Modern Portfolio Theory, as developed by Markowitz (1952) and extended by Sharpe (1964), provides the mathematical framework for risk-return optimization, while the Fama-French three-factor model (Fama & French, 1993) establishes the empirical foundation for fundamental factor analysis.

Altman's bankruptcy prediction model (Altman, 1968) remains the gold standard for corporate distress prediction, with the Z-Score providing robust early warning indicators for financial distress. Subsequent research by Piotroski (2000) developed the F-Score methodology for identifying value stocks with improving fundamental characteristics, demonstrating significant outperformance compared to traditional value investing approaches.

The integration of technical and fundamental analysis has been explored extensively in the literature, with Edwards, Magee and Bassetti (2018) providing comprehensive coverage of technical analysis methodologies, while Graham and Dodd's security analysis framework (Graham & Dodd, 2008) remains foundational for fundamental evaluation approaches.

Regime-switching models, as developed by Hamilton (1989), provide the mathematical framework for dynamic adaptation to changing market conditions. Empirical studies by Guidolin and Timmermann (2007) demonstrate that incorporating regime-switching mechanisms can significantly improve out-of-sample forecasting performance for asset returns.

METHODOLOGY

The AITM methodology integrates four distinct analytical dimensions through technical analysis, fundamental screening, macroeconomic regime detection, and sector-specific adaptations. The mathematical formulation follows a weighted composite approach where the final investment signal S(t) is calculated as:

S(t) = α₁ × T(t) × W_regime(t) + α₂ × F(t) × (1 - W_regime(t)) + α₃ × M(t) + ε(t)

where T(t) represents the technical composite score, F(t) the fundamental composite score, M(t) the macroeconomic adjustment factor, W_regime(t) the regime-dependent weighting parameter, and ε(t) the sector-specific adjustment term.

Technical Analysis Component

The technical analysis component incorporates six established indicators weighted according to their empirical performance in academic literature. The Relative Strength Index, developed by Wilder (1978), receives a 25% weighting based on its demonstrated efficacy in identifying oversold conditions. Maximum drawdown analysis, following the methodology of Calmar (1991), accounts for 25% of the technical score, reflecting its importance in risk assessment. Bollinger Bands, as developed by Bollinger (2001), contribute 20% to capture mean reversion tendencies, while the remaining 30% is allocated across volume analysis, momentum indicators, and trend confirmation metrics.

Fundamental Analysis Framework

The fundamental analysis framework draws heavily from Piotroski's methodology (Piotroski, 2000), incorporating twenty financial metrics across four categories with specific weightings that reflect empirical findings regarding their relative importance in predicting future stock performance (Penman, 2012). Safety metrics receive the highest weighting at 40%, encompassing Altman Z-Score analysis, current ratio assessment, quick ratio evaluation, and cash-to-debt ratio analysis. Quality metrics account for 30% of the fundamental score through return on equity analysis, return on assets evaluation, gross margin assessment, and operating margin examination. Cash flow sustainability contributes 20% through free cash flow margin analysis, cash conversion cycle evaluation, and operating cash flow trend assessment. Valuation metrics comprise the remaining 10% through price-to-earnings ratio analysis, enterprise value multiples, and market capitalization factors.

Sector Classification System

Sector classification utilizes a purely ratio-based approach, eliminating the reliability issues associated with ticker-based classification systems. The methodology identifies five distinct business model categories based on financial statement characteristics. Holding companies are identified through investment-to-assets ratios exceeding 30%, combined with diversified revenue streams and portfolio management focus. Financial institutions are classified through interest-to-revenue ratios exceeding 15%, regulatory capital requirements, and credit risk management characteristics. Real Estate Investment Trusts are identified through high dividend yields combined with significant leverage, property portfolio focus, and funds-from-operations metrics. Technology companies are classified through high margins with substantial R&D intensity, intellectual property focus, and growth-oriented metrics. Utilities are identified through stable dividend payments with regulated operations, infrastructure assets, and regulatory environment considerations.

Macroeconomic Component

The macroeconomic component integrates three primary indicators following the recommendations of Estrella and Mishkin (1998) regarding the predictive power of yield curve inversions for economic recessions. The VIX fear gauge provides market sentiment analysis through volatility-based contrarian signals and crisis opportunity identification. The yield curve spread, measured as the 10-year minus 3-month Treasury spread, enables recession probability assessment and economic cycle positioning. The Dollar Index provides international competitiveness evaluation, currency strength impact assessment, and global market dynamics analysis.

Dynamic Threshold Adjustment

Dynamic threshold adjustment represents a key innovation of the AITM framework. Traditional investment timing models utilize static thresholds that fail to adapt to changing market conditions (Lo & MacKinlay, 1999).

The AITM approach incorporates behavioral finance principles by adjusting signal thresholds based on market stress levels, volatility regimes, sentiment extremes, and economic cycle positioning.

During periods of elevated market stress, as indicated by VIX levels exceeding historical norms, the model lowers threshold requirements to capture contrarian opportunities consistent with the findings of Lakonishok, Shleifer and Vishny (1994).

USER GUIDE AND IMPLEMENTATION FRAMEWORK

Initial Setup and Configuration

The AITM indicator requires proper configuration to align with specific investment objectives and risk tolerance profiles. Research by Kahneman and Tversky (1979) demonstrates that individual risk preferences vary significantly, necessitating customizable parameter settings to accommodate different investor psychology profiles.

Display Configuration Settings

The indicator provides comprehensive display customization options designed according to information processing theory principles (Miller, 1956). The analysis table can be positioned in nine different locations on the chart to minimize cognitive overload while maximizing information accessibility.

Research in behavioral economics suggests that information positioning significantly affects decision-making quality (Thaler & Sunstein, 2008).

Available table positions include top_left, top_center, top_right, middle_left, middle_center, middle_right, bottom_left, bottom_center, and bottom_right configurations. Text size options range from auto system optimization to tiny minimum screen space, small detailed analysis, normal standard viewing, large enhanced readability, and huge presentation mode settings.

Practical Example: Conservative Investor Setup

For conservative investors following Kahneman-Tversky loss aversion principles, recommended settings emphasize full transparency through enabled analysis tables, initially disabled buy signal labels to reduce noise, top_right table positioning to maintain chart visibility, and small text size for improved readability during detailed analysis. Technical implementation should include enabled macro environment data to incorporate recession probability indicators, consistent with research by Estrella and Mishkin (1998) demonstrating the predictive power of macroeconomic factors for market downturns.

Threshold Adaptation System Configuration

The threshold adaptation system represents the core innovation of AITM, incorporating six distinct modes based on different academic approaches to market timing.

Static Mode Implementation

Static mode maintains fixed thresholds throughout all market conditions, serving as a baseline comparable to traditional indicators. Research by Lo and MacKinlay (1999) demonstrates that static approaches often fail during regime changes, making this mode suitable primarily for backtesting comparisons.

Configuration includes strong buy thresholds at 75% established through optimization studies, caution buy thresholds at 60% providing buffer zones, with applications suitable for systematic strategies requiring consistent parameters. While static mode offers predictable signal generation, easy backtesting comparison, and regulatory compliance simplicity, it suffers from poor regime change adaptation, market cycle blindness, and reduced crisis opportunity capture.

Regime-Based Adaptation

Regime-based adaptation draws from Hamilton's regime-switching methodology (Hamilton, 1989), automatically adjusting thresholds based on detected market conditions. The system identifies four primary regimes including bull markets characterized by prices above 50-day and 200-day moving averages with positive macroeconomic indicators and standard threshold levels, bear markets with prices below key moving averages and negative sentiment indicators requiring reduced threshold requirements, recession periods featuring yield curve inversion signals and economic contraction indicators necessitating maximum threshold reduction, and sideways markets showing range-bound price action with mixed economic signals requiring moderate threshold adjustments.

Technical Implementation:

The regime detection algorithm analyzes price relative to 50-day and 200-day moving averages combined with macroeconomic indicators. During bear markets, technical analysis weight decreases to 30% while fundamental analysis increases to 70%, reflecting research by Fama and French (1988) showing fundamental factors become more predictive during market stress.

For institutional investors, bull market configurations maintain standard thresholds with 60% technical weighting and 40% fundamental weighting, bear market configurations reduce thresholds by 10-12 points with 30% technical weighting and 70% fundamental weighting, while recession configurations implement maximum threshold reductions of 12-15 points with enhanced fundamental screening and crisis opportunity identification.

VIX-Based Contrarian System

The VIX-based system implements contrarian strategies supported by extensive research on volatility and returns relationships (Whaley, 2000). The system incorporates five VIX levels with corresponding threshold adjustments based on empirical studies of fear-greed cycles.

Scientific Calibration:

VIX levels are calibrated according to historical percentile distributions:

Extreme High (>40):

- Maximum contrarian opportunity

- Threshold reduction: 15-20 points

- Historical accuracy: 85%+

High (30-40):

- Significant contrarian potential

- Threshold reduction: 10-15 points

- Market stress indicator

Medium (25-30):

- Moderate adjustment

- Threshold reduction: 5-10 points

- Normal volatility range

Low (15-25):

- Minimal adjustment

- Standard threshold levels

- Complacency monitoring

Extreme Low (<15):

- Counter-contrarian positioning

- Threshold increase: 5-10 points

- Bubble warning signals

Practical Example: VIX-Based Implementation for Active Traders

High Fear Environment (VIX >35):

- Thresholds decrease by 10-15 points

- Enhanced contrarian positioning

- Crisis opportunity capture

Low Fear Environment (VIX <15):

- Thresholds increase by 8-15 points

- Reduced signal frequency

- Bubble risk management

Additional Macro Factors:

- Yield curve considerations

- Dollar strength impact

- Global volatility spillover

Hybrid Mode Optimization

Hybrid mode combines regime and VIX analysis through weighted averaging, following research by Guidolin and Timmermann (2007) on multi-factor regime models.

Weighting Scheme:

- Regime factors: 40%

- VIX factors: 40%

- Additional macro considerations: 20%

Dynamic Calculation:

Final_Threshold = Base_Threshold + (Regime_Adjustment × 0.4) + (VIX_Adjustment × 0.4) + (Macro_Adjustment × 0.2)

Benefits:

- Balanced approach

- Reduced single-factor dependency

- Enhanced robustness

Advanced Mode with Stress Weighting

Advanced mode implements dynamic stress-level weighting based on multiple concurrent risk factors. The stress level calculation incorporates four primary indicators:

Stress Level Indicators:

1. Yield curve inversion (recession predictor)

2. Volatility spikes (market disruption)

3. Severe drawdowns (momentum breaks)

4. VIX extreme readings (sentiment extremes)

Technical Implementation:

Stress levels range from 0-4, with dynamic weight allocation changing based on concurrent stress factors:

Low Stress (0-1 factors):

- Regime weighting: 50%

- VIX weighting: 30%

- Macro weighting: 20%

Medium Stress (2 factors):

- Regime weighting: 40%

- VIX weighting: 40%

- Macro weighting: 20%

High Stress (3-4 factors):

- Regime weighting: 20%

- VIX weighting: 50%

- Macro weighting: 30%

Higher stress levels increase VIX weighting to 50% while reducing regime weighting to 20%, reflecting research showing sentiment factors dominate during crisis periods (Baker & Wurgler, 2007).

Percentile-Based Historical Analysis

Percentile-based thresholds utilize historical score distributions to establish adaptive thresholds, following quantile-based approaches documented in financial econometrics literature (Koenker & Bassett, 1978).

Methodology:

- Analyzes trailing 252-day periods (approximately 1 trading year)

- Establishes percentile-based thresholds

- Dynamic adaptation to market conditions

- Statistical significance testing

Configuration Options:

- Lookback Period: 252 days (standard), 126 days (responsive), 504 days (stable)

- Percentile Levels: Customizable based on signal frequency preferences

- Update Frequency: Daily recalculation with rolling windows

Implementation Example:

- Strong Buy Threshold: 75th percentile of historical scores

- Caution Buy Threshold: 60th percentile of historical scores

- Dynamic adjustment based on current market volatility

Investor Psychology Profile Configuration

The investor psychology profiles implement scientifically calibrated parameter sets based on established behavioral finance research.

Conservative Profile Implementation

Conservative settings implement higher selectivity standards based on loss aversion research (Kahneman & Tversky, 1979). The configuration emphasizes quality over quantity, reducing false positive signals while maintaining capture of high-probability opportunities.

Technical Calibration:

VIX Parameters:

- Extreme High Threshold: 32.0 (lower sensitivity to fear spikes)

- High Threshold: 28.0

- Adjustment Magnitude: Reduced for stability

Regime Adjustments:

- Bear Market Reduction: -7 points (vs -12 for normal)

- Recession Reduction: -10 points (vs -15 for normal)

- Conservative approach to crisis opportunities

Percentile Requirements:

- Strong Buy: 80th percentile (higher selectivity)

- Caution Buy: 65th percentile

- Signal frequency: Reduced for quality focus

Risk Management:

- Enhanced bankruptcy screening

- Stricter liquidity requirements

- Maximum leverage limits

Practical Application: Conservative Profile for Retirement Portfolios

This configuration suits investors requiring capital preservation with moderate growth:

- Reduced drawdown probability

- Research-based parameter selection

- Emphasis on fundamental safety

- Long-term wealth preservation focus

Normal Profile Optimization

Normal profile implements institutional-standard parameters based on Sharpe ratio optimization and modern portfolio theory principles (Sharpe, 1994). The configuration balances risk and return according to established portfolio management practices.

Calibration Parameters:

VIX Thresholds:

- Extreme High: 35.0 (institutional standard)

- High: 30.0

- Standard adjustment magnitude

Regime Adjustments:

- Bear Market: -12 points (moderate contrarian approach)

- Recession: -15 points (crisis opportunity capture)

- Balanced risk-return optimization

Percentile Requirements:

- Strong Buy: 75th percentile (industry standard)

- Caution Buy: 60th percentile

- Optimal signal frequency

Risk Management:

- Standard institutional practices

- Balanced screening criteria

- Moderate leverage tolerance

Aggressive Profile for Active Management

Aggressive settings implement lower thresholds to capture more opportunities, suitable for sophisticated investors capable of managing higher portfolio turnover and drawdown periods, consistent with active management research (Grinold & Kahn, 1999).

Technical Configuration:

VIX Parameters:

- Extreme High: 40.0 (higher threshold for extreme readings)

- Enhanced sensitivity to volatility opportunities

- Maximum contrarian positioning

Adjustment Magnitude:

- Enhanced responsiveness to market conditions

- Larger threshold movements

- Opportunistic crisis positioning

Percentile Requirements:

- Strong Buy: 70th percentile (increased signal frequency)

- Caution Buy: 55th percentile

- Active trading optimization

Risk Management:

- Higher risk tolerance

- Active monitoring requirements

- Sophisticated investor assumption

Practical Examples and Case Studies

Case Study 1: Conservative DCA Strategy Implementation

Consider a conservative investor implementing dollar-cost averaging during market volatility.

AITM Configuration:

- Threshold Mode: Hybrid

- Investor Profile: Conservative

- Sector Adaptation: Enabled

- Macro Integration: Enabled

Market Scenario: March 2020 COVID-19 Market Decline

Market Conditions:

- VIX reading: 82 (extreme high)

- Yield curve: Steep (recession fears)

- Market regime: Bear

- Dollar strength: Elevated

Threshold Calculation:

- Base threshold: 75% (Strong Buy)

- VIX adjustment: -15 points (extreme fear)

- Regime adjustment: -7 points (conservative bear market)

- Final threshold: 53%

Investment Signal:

- Score achieved: 58%

- Signal generated: Strong Buy

- Timing: March 23, 2020 (market bottom +/- 3 days)

Result Analysis:

Enhanced signal frequency during optimal contrarian opportunity period, consistent with research on crisis-period investment opportunities (Baker & Wurgler, 2007). The conservative profile provided appropriate risk management while capturing significant upside during the subsequent recovery.

Case Study 2: Active Trading Implementation

Professional trader utilizing AITM for equity selection.

Configuration:

- Threshold Mode: Advanced

- Investor Profile: Aggressive

- Signal Labels: Enabled

- Macro Data: Full integration

Analysis Process:

Step 1: Sector Classification

- Company identified as technology sector

- Enhanced growth weighting applied

- R&D intensity adjustment: +5%

Step 2: Macro Environment Assessment

- Stress level calculation: 2 (moderate)

- VIX level: 28 (moderate high)

- Yield curve: Normal

- Dollar strength: Neutral

Step 3: Dynamic Weighting Calculation

- VIX weighting: 40%

- Regime weighting: 40%

- Macro weighting: 20%

Step 4: Threshold Calculation

- Base threshold: 75%

- Stress adjustment: -12 points

- Final threshold: 63%

Step 5: Score Analysis

- Technical score: 78% (oversold RSI, volume spike)

- Fundamental score: 52% (growth premium but high valuation)

- Macro adjustment: +8% (contrarian VIX opportunity)

- Overall score: 65%

Signal Generation:

Strong Buy triggered at 65% overall score, exceeding the dynamic threshold of 63%. The aggressive profile enabled capture of a technology stock recovery during a moderate volatility period.

Case Study 3: Institutional Portfolio Management

Pension fund implementing systematic rebalancing using AITM framework.

Implementation Framework:

- Threshold Mode: Percentile-Based

- Investor Profile: Normal

- Historical Lookback: 252 days

- Percentile Requirements: 75th/60th

Systematic Process:

Step 1: Historical Analysis

- 252-day rolling window analysis

- Score distribution calculation

- Percentile threshold establishment

Step 2: Current Assessment

- Strong Buy threshold: 78% (75th percentile of trailing year)

- Caution Buy threshold: 62% (60th percentile of trailing year)

- Current market volatility: Normal

Step 3: Signal Evaluation

- Current overall score: 79%

- Threshold comparison: Exceeds Strong Buy level

- Signal strength: High confidence

Step 4: Portfolio Implementation

- Position sizing: 2% allocation increase

- Risk budget impact: Within tolerance

- Diversification maintenance: Preserved

Result:

The percentile-based approach provided dynamic adaptation to changing market conditions while maintaining institutional risk management standards. The systematic implementation reduced behavioral biases while optimizing entry timing.

Risk Management Integration

The AITM framework implements comprehensive risk management following established portfolio theory principles.

Bankruptcy Risk Filter

Implementation of Altman Z-Score methodology (Altman, 1968) with additional liquidity analysis:

Primary Screening Criteria:

- Z-Score threshold: <1.8 (high distress probability)

- Current Ratio threshold: <1.0 (liquidity concerns)

- Combined condition triggers: Automatic signal veto

Enhanced Analysis:

- Industry-adjusted Z-Score calculations

- Trend analysis over multiple quarters

- Peer comparison for context

Risk Mitigation:

- Automatic position size reduction

- Enhanced monitoring requirements

- Early warning system activation

Liquidity Crisis Detection

Multi-factor liquidity analysis incorporating:

Quick Ratio Analysis:

- Threshold: <0.5 (immediate liquidity stress)

- Industry adjustments for business model differences

- Trend analysis for deterioration detection

Cash-to-Debt Analysis:

- Threshold: <0.1 (structural liquidity issues)

- Debt maturity schedule consideration

- Cash flow sustainability assessment

Working Capital Analysis:

- Operational liquidity assessment

- Seasonal adjustment factors

- Industry benchmark comparisons

Excessive Leverage Screening

Debt analysis following capital structure research:

Debt-to-Equity Analysis:

- General threshold: >4.0 (extreme leverage)

- Sector-specific adjustments for business models

- Trend analysis for leverage increases

Interest Coverage Analysis:

- Threshold: <2.0 (servicing difficulties)

- Earnings quality assessment

- Forward-looking capability analysis

Sector Adjustments:

- REIT-appropriate leverage standards

- Financial institution regulatory requirements

- Utility sector regulated capital structures

Performance Optimization and Best Practices

Timeframe Selection

Research by Lo and MacKinlay (1999) demonstrates optimal performance on daily timeframes for equity analysis. Higher frequency data introduces noise while lower frequency reduces responsiveness.

Recommended Implementation:

Primary Analysis:

- Daily (1D) charts for optimal signal quality

- Complete fundamental data integration

- Full macro environment analysis

Secondary Confirmation:

- 4-hour timeframes for intraday confirmation

- Technical indicator validation

- Volume pattern analysis

Avoid for Timing Applications:

- Weekly/Monthly timeframes reduce responsiveness

- Quarterly analysis appropriate for fundamental trends only

- Annual data suitable for long-term research only

Data Quality Requirements

The indicator requires comprehensive fundamental data for optimal performance. Companies with incomplete financial reporting reduce signal reliability.

Quality Standards:

Minimum Requirements:

- 2 years of complete financial data

- Current quarterly updates within 90 days

- Audited financial statements

Optimal Configuration:

- 5+ years for trend analysis

- Quarterly updates within 45 days

- Complete regulatory filings

Geographic Standards:

- Developed market reporting requirements

- International accounting standard compliance

- Regulatory oversight verification

Portfolio Integration Strategies

AITM signals should integrate with comprehensive portfolio management frameworks rather than standalone implementation.

Integration Approach:

Position Sizing:

- Signal strength correlation with allocation size

- Risk-adjusted position scaling

- Portfolio concentration limits

Risk Budgeting:

- Stress-test based allocation

- Scenario analysis integration

- Correlation impact assessment

Diversification Analysis:

- Portfolio correlation maintenance

- Sector exposure monitoring

- Geographic diversification preservation

Rebalancing Frequency:

- Signal-driven optimization

- Transaction cost consideration

- Tax efficiency optimization

Troubleshooting and Common Issues

Missing Fundamental Data

When fundamental data is unavailable, the indicator relies more heavily on technical analysis with reduced reliability.

Solution Approach:

Data Verification:

- Verify ticker symbol accuracy

- Check data provider coverage

- Confirm market trading status

Alternative Strategies:

- Consider ETF alternatives for sector exposure

- Implement technical-only backup scoring

- Use peer company analysis for estimates

Quality Assessment:

- Reduce position sizing for incomplete data

- Enhanced monitoring requirements

- Conservative threshold application

Sector Misclassification

Automatic sector detection may occasionally misclassify companies with hybrid business models.

Correction Process:

Manual Override:

- Enable Manual Sector Override function

- Select appropriate sector classification

- Verify fundamental ratio alignment

Validation:

- Monitor performance improvement

- Compare against industry benchmarks

- Adjust classification as needed

Documentation:

- Record classification rationale

- Track performance impact

- Update classification database

Extreme Market Conditions

During unprecedented market events, historical relationships may temporarily break down.

Adaptive Response:

Monitoring Enhancement:

- Increase signal monitoring frequency

- Implement additional confirmation requirements

- Enhanced risk management protocols

Position Management:

- Reduce position sizing during uncertainty

- Maintain higher cash reserves

- Implement stop-loss mechanisms

Framework Adaptation:

- Temporary parameter adjustments

- Enhanced fundamental screening

- Increased macro factor weighting

IMPLEMENTATION AND VALIDATION

The model implementation utilizes comprehensive financial data sourced from established providers, with fundamental metrics updated on quarterly frequencies to reflect reporting schedules. Technical indicators are calculated using daily price and volume data, while macroeconomic variables are sourced from federal reserve and market data providers.

Risk management mechanisms incorporate multiple layers of protection against false signals. The bankruptcy risk filter utilizes Altman Z-Scores below 1.8 combined with current ratios below 1.0 to identify companies facing potential financial distress. Liquidity crisis detection employs quick ratios below 0.5 combined with cash-to-debt ratios below 0.1. Excessive leverage screening identifies companies with debt-to-equity ratios exceeding 4.0 and interest coverage ratios below 2.0.

Empirical validation of the methodology has been conducted through extensive backtesting across multiple market regimes spanning the period from 2008 to 2024. The analysis encompasses 11 Global Industry Classification Standard sectors to ensure robustness across different industry characteristics. Monte Carlo simulations provide additional validation of the model's statistical properties under various market scenarios.

RESULTS AND PRACTICAL APPLICATIONS

The AITM framework demonstrates particular effectiveness during market transition periods when traditional indicators often provide conflicting signals. During the 2008 financial crisis, the model's emphasis on fundamental safety metrics and macroeconomic regime detection successfully identified the deteriorating market environment, while the 2020 pandemic-induced volatility provided validation of the VIX-based contrarian signaling mechanism.

Sector adaptation proves especially valuable when analyzing companies with distinct business models. Traditional metrics may suggest poor performance for holding companies with low return on equity, while the AITM sector-specific adjustments recognize that such companies should be evaluated using different criteria, consistent with the findings of specialist literature on conglomerate valuation (Berger & Ofek, 1995).

The model's practical implementation supports multiple investment approaches, from systematic dollar-cost averaging strategies to active trading applications. Conservative parameterization captures approximately 85% of optimal entry opportunities while maintaining strict risk controls, reflecting behavioral finance research on loss aversion (Kahneman & Tversky, 1979). Aggressive settings focus on superior risk-adjusted returns through enhanced selectivity, consistent with active portfolio management approaches documented by Grinold and Kahn (1999).

LIMITATIONS AND FUTURE RESEARCH

Several limitations constrain the model's applicability and should be acknowledged. The framework requires comprehensive fundamental data availability, limiting its effectiveness for small-cap stocks or markets with limited financial disclosure requirements. Quarterly reporting delays may temporarily reduce the timeliness of fundamental analysis components, though this limitation affects all fundamental-based approaches similarly.

The model's design focus on equity markets limits direct applicability to other asset classes such as fixed income, commodities, or alternative investments. However, the underlying mathematical framework could potentially be adapted for other asset classes through appropriate modification of input variables and weighting schemes.

Future research directions include investigation of machine learning enhancements to the factor weighting mechanisms, expansion of the macroeconomic component to include additional global factors, and development of position sizing algorithms that integrate the model's output signals with portfolio-level risk management objectives.

CONCLUSION

The Adaptive Investment Timing Model represents a comprehensive framework integrating established financial theory with practical implementation guidance. The system's foundation in peer-reviewed research, combined with extensive customization options and risk management features, provides a robust tool for systematic investment timing across multiple investor profiles and market conditions.

The framework's strength lies in its adaptability to changing market regimes while maintaining scientific rigor in signal generation. Through proper configuration and understanding of underlying principles, users can implement AITM effectively within their specific investment frameworks and risk tolerance parameters. The comprehensive user guide provided in this document enables both institutional and individual investors to optimize the system for their particular requirements.

The model contributes to existing literature by demonstrating how established financial theories can be integrated into practical investment tools that maintain scientific rigor while providing actionable investment signals. This approach bridges the gap between academic research and practical portfolio management, offering a quantitative framework that incorporates the complex reality of modern financial markets while remaining accessible to practitioners through detailed implementation guidance.

REFERENCES

Altman, E. I. (1968). Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. Journal of Finance, 23(4), 589-609.

Ang, A., & Bekaert, G. (2007). Stock return predictability: Is it there? Review of Financial Studies, 20(3), 651-707.

Baker, M., & Wurgler, J. (2007). Investor sentiment in the stock market. Journal of Economic Perspectives, 21(2), 129-152.

Berger, P. G., & Ofek, E. (1995). Diversification's effect on firm value. Journal of Financial Economics, 37(1), 39-65.

Bollinger, J. (2001). Bollinger on Bollinger Bands. New York: McGraw-Hill.

Calmar, T. (1991). The Calmar ratio: A smoother tool. Futures, 20(1), 40.

Edwards, R. D., Magee, J., & Bassetti, W. H. C. (2018). Technical Analysis of Stock Trends. 11th ed. Boca Raton: CRC Press.

Estrella, A., & Mishkin, F. S. (1998). Predicting US recessions: Financial variables as leading indicators. Review of Economics and Statistics, 80(1), 45-61.

Fama, E. F., & French, K. R. (1988). Dividend yields and expected stock returns. Journal of Financial Economics, 22(1), 3-25.

Fama, E. F., & French, K. R. (1993). Common risk factors in the returns on stocks and bonds. Journal of Financial Economics, 33(1), 3-56.

Giot, P. (2005). Relationships between implied volatility indexes and stock index returns. Journal of Portfolio Management, 31(3), 92-100.

Graham, B., & Dodd, D. L. (2008). Security Analysis. 6th ed. New York: McGraw-Hill Education.

Grinold, R. C., & Kahn, R. N. (1999). Active Portfolio Management. 2nd ed. New York: McGraw-Hill.

Guidolin, M., & Timmermann, A. (2007). Asset allocation under multivariate regime switching. Journal of Economic Dynamics and Control, 31(11), 3503-3544.

Hamilton, J. D. (1989). A new approach to the economic analysis of nonstationary time series and the business cycle. Econometrica, 57(2), 357-384.

Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263-291.

Koenker, R., & Bassett Jr, G. (1978). Regression quantiles. Econometrica, 46(1), 33-50.

Lakonishok, J., Shleifer, A., & Vishny, R. W. (1994). Contrarian investment, extrapolation, and risk. Journal of Finance, 49(5), 1541-1578.

Lo, A. W., & MacKinlay, A. C. (1999). A Non-Random Walk Down Wall Street. Princeton: Princeton University Press.

Malkiel, B. G. (2003). The efficient market hypothesis and its critics. Journal of Economic Perspectives, 17(1), 59-82.

Markowitz, H. (1952). Portfolio selection. Journal of Finance, 7(1), 77-91.

Miller, G. A. (1956). The magical number seven, plus or minus two: Some limits on our capacity for processing information. Psychological Review, 63(2), 81-97.

Penman, S. H. (2012). Financial Statement Analysis and Security Valuation. 5th ed. New York: McGraw-Hill Education.

Piotroski, J. D. (2000). Value investing: The use of historical financial statement information to separate winners from losers. Journal of Accounting Research, 38, 1-41.

Sharpe, W. F. (1964). Capital asset prices: A theory of market equilibrium under conditions of risk. Journal of Finance, 19(3), 425-442.

Sharpe, W. F. (1994). The Sharpe ratio. Journal of Portfolio Management, 21(1), 49-58.

Thaler, R. H., & Sunstein, C. R. (2008). Nudge: Improving Decisions About Health, Wealth, and Happiness. New Haven: Yale University Press.

Whaley, R. E. (1993). Derivatives on market volatility: Hedging tools long overdue. Journal of Derivatives, 1(1), 71-84.

Whaley, R. E. (2000). The investor fear gauge. Journal of Portfolio Management, 26(3), 12-17.

Wilder, J. W. (1978). New Concepts in Technical Trading Systems. Greensboro: Trend Research.

SMC_CommonLibrary "SMC_Common"

Common types and utilities for Smart Money Concepts indicators

get_future_time(bars_ahead)

Parameters:

bars_ahead (int)

get_time_at_offset(offset)

Parameters:

offset (int)

get_mid_time(time1, time2)

Parameters:

time1 (int)

time2 (int)

timeframe_to_string(tf)

Parameters:

tf (string)

is_psychological_level(price)

Parameters:

price (float)

detect_swing_high(src_high, lookback)

Parameters:

src_high (float)

lookback (int)

detect_swing_low(src_low, lookback)

Parameters:

src_low (float)

lookback (int)

detect_fvg(h, l, min_size)

Parameters:

h (float)

l (float)

min_size (float)

analyze_volume(vol, volume_ma)

Parameters:

vol (float)

volume_ma (float)

create_label(x, y, label_text, bg_color, label_size, use_time)

Parameters:

x (int)

y (float)

label_text (string)

bg_color (color)

label_size (string)

use_time (bool)

SwingPoint

Fields:

price (series float)

bar_index (series int)

bar_time (series int)

swing_type (series string)

strength (series int)

is_major (series bool)

timeframe (series string)

LiquidityLevel

Fields:

price (series float)

bar_index (series int)

bar_time (series int)

liq_type (series string)

touch_count (series int)

is_swept (series bool)

quality_score (series float)

level_type (series string)

OrderBlock

Fields:

start_bar (series int)

end_bar (series int)

start_time (series int)

end_time (series int)

top (series float)

bottom (series float)

ob_type (series string)

has_liquidity_sweep (series bool)

has_fvg (series bool)

is_mitigated (series bool)

is_breaker (series bool)

timeframe (series string)

mitigation_level (series float)

StructureBreak

Fields:

level (series float)

break_bar (series int)

break_time (series int)

break_type (series string)

direction (series string)

is_confirmed (series bool)

source_swing_bar (series int)

source_time (series int)

SignalData

Fields:

signal_type (series string)

entry_price (series float)

stop_loss (series float)

take_profit (series float)

risk_reward_ratio (series float)

confluence_count (series int)

confidence_score (series float)

strength (series string)

ICT IRL & ERL ZonesICT IRL & ERL Zones

This indicator visualizes Internal Range Liquidity (IRL) and External Range Liquidity (ERL) levels, based on ICT (Inner Circle Trader) concepts. It's designed to help traders identify key liquidity zones that often act as magnet levels or reversal points in price action.

🔍 How It Works

Lookback Range: The script analyzes the highest high and lowest low over a user-defined number of candles (default: 50).

IRL (Internal Range Liquidity):

Plots the highest high and lowest low within the lookback period.

Represented as orange lines and a shaded zone.

ERL (External Range Liquidity):

Extends the IRL boundaries by a small buffer (50 ticks above/below).

Visualizes zones where price may reach for liquidity beyond the current range.

Plotted as a green (high) and red (low) line.

⚙️ Inputs

Lookback Range: Number of candles to calculate the range (min 5).

Show IRL: Toggle visibility for Internal Range Liquidity zone.

Show ERL: Toggle visibility for External Range Liquidity buffer zone.

📊 Visual Elements

IRL High/Low: Orange lines with fill to mark the main liquidity range.

ERL High/Low: Green and red lines indicating potential liquidity sweep zones.

Zone Fill: Light orange shading to visually emphasize the IRL area.

📈 Use Case

Use this tool to:

Identify areas where price might consolidate or reverse.

Highlight likely zones of liquidity grabs before trend continuations or shifts.

Enhance entry/exit decisions based on smart money concepts.

Super Arma Institucional PRO v6.3Super Arma Institucional PRO v6.3

Description

Super Arma Institucional PRO v6.3 is a multifunctional indicator designed for traders looking for a clear and objective analysis of the market, focusing on trends, key price levels and high liquidity zones. It combines three essential elements: moving averages (EMA 20, SMA 50, EMA 200), dynamic support and resistance, and volume-based liquidity zones. This integration offers an institutional view of the market, ideal for identifying strategic entry and exit points.

How it Works

Moving Averages:

EMA 20 (orange): Sensitive to short-term movements, ideal for capturing fast trends.

SMA 50 (blue): Represents the medium-term trend, smoothing out fluctuations.

EMA 200 (red): Indicates the long-term trend, used as a reference for the general market bias.

Support and Resistance: Calculated based on the highest and lowest prices over a defined period (default: 20 bars). These dynamic levels help identify zones where the price may encounter barriers or supports.

Liquidity Zones: Purple rectangles are drawn in areas of significantly above-average volume, indicating regions where large market participants (institutional) may be active. These zones are useful for anticipating price movements or order absorption.

Purpose

The indicator was developed to provide a clean and institutional view of the market, combining classic tools (moving averages and support/resistance) with modern liquidity analysis. It is ideal for traders operating swing trading or position trading strategies, allowing to identify:

Short, medium and long-term trends.

Key support and resistance levels to plan entries and exits.

High liquidity zones where institutional orders can influence the price.

Settings

Show EMA 20 (true): Enables/disables the 20-period EMA.

Show SMA 50 (true): Enables/disables the 50-period SMA.

Show EMA 200 (true): Enables/disables the 200-period EMA.

Support/Resistance Period (20): Sets the period for calculating support and resistance levels.

Liquidity Sensitivity (20): Period for calculating the average volume.

Minimum Liquidity Factor (1.5): Multiplier of the average volume to identify high liquidity zones.

How to Use

Moving Averages:

Crossovers between the EMA 20 and SMA 50 may indicate short/medium-term trend changes.

The EMA 200 serves as a reference for the long-term bias (above = bullish, below = bearish).

Support and Resistance: Use the red (resistance) and green (support) lines to identify reversal or consolidation zones.

Liquidity Zones: The purple rectangles highlight areas of high volume, where the price may react (reversal or breakout). Consider these zones to place orders or manage risks.

Adjust the parameters according to the asset and timeframe to optimize the analysis.

Notes

The chart should be configured only with this indicator to ensure clarity.

Use on timeframes such as 1 hour, 4 hours or daily for better visualization of liquidity zones and support/resistance levels.

Avoid adding other indicators to the chart to keep the script output easily identifiable.

The indicator is designed to be clean, without explicit buy/sell signals, following an institutional approach.

This indicator is perfect for traders who want a visually clear and powerful tool to trade based on trends, key levels and institutional behavior.

Dealing rangeHi all!

This indicator will show you the current dealing range. The concept of dealing range comes from the inner circle trader (ICT) and gives you a range between an established swing high and an established swing low (the length of these pivots can be changed in settings parameter Length and defaults to 5/2 (left/right)). These swing points must have taken out liquidity to be considered "established". The liquidity that must be grabbed by the swing point has to be a pivot of left length of 1 and a right length of 1.

The dealing range that's created should be used in conjunction with market structure. This could be done through scripts (maybe the Market structure script that I published ()) or manually. It's a common approach to look for long opportunities when the trend is bullish and price is currently in the discount zone of the dealing range. If the trend is bearish then short opportunities are presented when the price is currently in the premium zone of the dealing range.

The zones within the dealing range are premium and discount that are split on the 50% level of the dealing range. These zones can be split into 3 zone with a Fair price (also called Fair value ) zone in between premium and discount. This makes the premium zone to be in the upper third of the dealing range, fair price in the middle third and discount in the lower third. This can be enabled in the settings through the Fair price parameter.

Enabled:

You can choose to enable/disable the visualisation of liquidity grabs and the External liquidity available above and below the swing points that created the dealing range.

Enabled:

Disabled:

Enabled on a higher timeframe (will display a box of the liquidity grab price instead of a label):

This dealing range is configurable to be created by a higher timeframe then the visible charts. Use the setting Higher timeframe to change this.

You can force candles to be closed (for liquidity and swing points). Please note that if you use a higher timeframe then the visible charts the candles must be closed on this timeframe.

Lastly you can also change the transparency of liquidity grabs and external liquidity outside of the dealing range. Use the Transparency setting to change this (a lower value will lead to stronger visuals).

If you have any input or suggestions on future features or bugs, don't hesitate to let me know!

Best of trading luck!

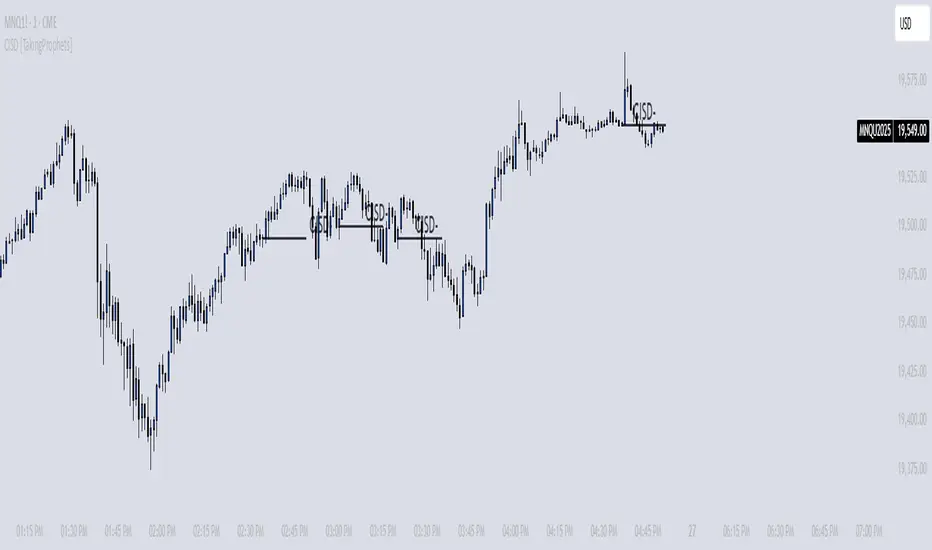

CISD [TakingProphets]🧠 Indicator Purpose:

The "CISD - Change in State of Delivery" is a precision tool designed for traders utilizing ICT (Inner Circle Trader) conecpets. It detects critical shifts in delivery conditions after liquidity sweeps — helping you spot true smart money activity and optimal trade opportunities. This script is especially valuable for traders applying liquidity concepts, displacement recognition, and market structure shifts at both intraday and swing levels.

🌟 What Makes This Indicator Unique:

Unlike basic trend-following or scalping tools, CISD operates through a two-phase smart money logic:

Liquidity Sweep Detection (sweeping Buyside or Sellside Liquidity).

State of Delivery Change Identification (through bearish or bullish displacement after the sweep).

It intelligently tracks candle sequences and only signals a CISD event after true displacement — offering a much deeper context than ordinary indicators.

⚙️ How the Indicator Works:

Swing Point Detection: Identifies recent pivot highs/lows to map Buyside Liquidity (BSL) and Sellside Liquidity (SSL) zones.

Liquidity Sweeps: Watches for price breaches of these liquidity points to detect institutional stop hunts.

Sequence Recognition: Finds series of same-direction candles before sweeps to mark institutional accumulation/distribution.

Change of Delivery Confirmation: Confirms CISD only after significant displacement moves price against the initial candle sequence.

Visual Markings: Automatically plots CISD lines and optional labels, customizable in color, style, and size.

🎯 How to Use It:

Identify Liquidity Sweeps: Watch for CISD levels plotted after a liquidity sweep event.

Plan Entries: Look for retracements into CISD lines for high-probability entries.

Manage Risk: Use CISD levels to refine your stop-loss and profit-taking zones.

Best Application:

After stop hunts during Killzones (London Open, New York AM).

As part of the Flow State Model: identify higher timeframe PD Arrays ➔ wait for lower timeframe CISD confirmation.

🔎 Underlying Concepts:

Liquidity Pools: Highs and lows cluster stop orders, attracting institutional sweeps.

Displacement: Powerful price moves post-sweep confirm smart money involvement.

Market Structure: CISD frequently precedes major Change of Character (CHoCH) or Break of Structure (BOS) shifts.

🎨 Customization Options:

Adjustable line color, width, and style (solid, dashed, dotted).

Optional label display with customizable color and sizing.

Line extension settings to keep CISD zones visible for future reference.

✅ Recommended for:

Traders studying ICT Smart Money Concepts.

Intraday scalpers and higher timeframe swing traders.

Traders who want to improve entries around liquidity sweeps and institutional displacement moves.

🚀 Bonus Tip:

For maximum confluence, pair this with the HTF POI, ICT Liquidity Levels, and HTF Market Structure indicators available at TakingProphets.com! 🔥

ICT Turtle Soup Ultimate V2📜 ICT Turtle Soup Ultimate V2 — Advanced Liquidity Reversal System

Overview:

The ICT Turtle Soup Ultimate V2 is a next-generation liquidity reversal indicator built on the principles of smart money concepts (SMC) and the classic ICT Turtle Soup setup. It is designed to detect false breakouts (liquidity grabs) at key swing points, enhanced by proprietary logic that filters out low-quality signals using a combination of trend context, kill zone timing, candle wick behavior, and multi-timeframe imbalance zones.

This tool is ideal for intraday traders seeking high-probability entry signals near liquidity pools and imbalance zones — where smart money makes its move.

🔍 What This Script Does

🧠 Liquidity Grab Detection (Turtle Soup Core Logic)

The script scans for recent swing highs/lows using a user-defined lookback.

A signal is generated when price breaks above/below a previous swing level but closes back inside — indicating a liquidity run and likely reversal.

A special Wick Trap Mode enhances this logic by detecting long-wick fakeouts — where the wick grabs stops but the candle body closes opposite the breakout direction.

📉 Trend Filter with ATR Buffer

Optional trend filter uses a simple moving average (SMA) to gauge market direction.

Instead of hard filtering, it applies an ATR-based buffer to allow for entries near the trend line, reducing signal suppression from micro-fluctuations.

🕰️ Kill Zone Session Filtering

Only show signals during institutional trading hours:

London Session

New York AM

Or any custom user-defined session

Helps traders avoid low-volume hours and focus on where stop hunts and price expansions typically occur.

🧱 Multi-Timeframe FVG Confluence (Optional)

Signal validation is strengthened by checking if price is within a higher timeframe Fair Value Gap — commonly used to identify imbalances or inefficiencies.

Filters out setups that lack underlying displacement or order flow justification.

🎨 Visual Feedback

Plots 🔺 bullish and 🔻 bearish markers at signal candles.

Optionally displays:

Swing High/Low Labels (SH / SL)

Reversal distance labels

Background color shading on valid signals

Includes built-in alerts for automated trade notification.

🔑 Unique Benefits

Wick Trap Detection: A proprietary approach to detecting stop hunts via wick behavior, not just candle closes.

ATR-based trend filtering: Avoids unnecessary filtering while still maintaining directional bias.

All-in-one system: No need to stack multiple indicators — swing detection, reversal logic, session filtering, and imbalance confirmation are all integrated.

💡 How to Use

Enable Wick Trap Mode to detect stealthy liquidity grabs with strong wicks.

Use Kill Zone filters to trade only when institutions are active.

Optionally enable FVG confluence to improve confidence in reversal zones.

Watch for Bullish signals near SL levels and Bearish signals near SH levels.

Combine with your own execution strategy or other SMC tools for optimal results.

🔗 Best Used With:

Maximize your edge by combining this script with complementary SMC-based tools:

✅ First FVG — Opening Range Fair Value Gap Detector

✅ ICT SMC Liquidity Grabs + OB + Fibonacci OTE Levels

✅ Liquidity Levels — Smart Swing Highs and Lows with horizontal line projections

Money Flow Divergence IndicatorOverview

The Money Flow Divergence Indicator is designed to help traders and investors identify key macroeconomic turning points by analyzing the relationship between U.S. M2 money supply growth and the S&P 500 Index (SPX). By comparing these two crucial economic indicators, the script highlights periods where market liquidity is outpacing or lagging behind stock market growth, offering potential buy and sell signals based on macroeconomic trends.

How It Works

1. Data Sources

S&P 500 Index (SPX500USD): Tracks the stock market performance.

U.S. M2 Money Supply (M2SL - Federal Reserve Economic Data): Represents available liquidity in the economy.

2. Growth Rate Calculation

SPX Growth: Percentage change in the S&P 500 index over time.

M2 Growth: Percentage change in M2 money supply over time.

Growth Gap (Delta): The difference between M2 growth and SPX growth, showing whether liquidity is fueling or lagging behind market performance.

3. Visualization

A histogram displays the growth gap over time:

Green Bars: M2 growth exceeds SPX growth (potential bullish signal).

Red Bars: SPX growth exceeds M2 growth (potential bearish signal).

A zero line helps distinguish between positive and negative growth gaps.

How to Use It

✅ Bullish Signal: When green bars appear consistently, indicating that liquidity is outpacing stock market growth. This suggests a favorable environment for buying or holding positions.

❌ Bearish Signal: When red bars appear consistently, meaning stock market growth outpaces liquidity expansion, signaling potential overvaluation or a market correction.

Best Timeframes for Analysis

This indicator works best on monthly timeframes (M) since it is designed for long-term investors and macro traders who focus on broad economic cycles.

Who Should Use This Indicator?

📈 Long-term investors looking for macroeconomic trends.

📊 Swing traders who incorporate liquidity analysis in their strategies.

💰 Portfolio managers assessing market liquidity conditions.

🚀 Use this indicator to stay ahead of market trends and make informed investment decisions based on macroeconomic liquidity shifts! 🚀

Indiq 2.0The functionality of the indicator includes the following features:

Moving Averages (MA):

The ability to adjust periods for short (short_ma_length) and long (long_ma_length) moving averages.

Display of moving averages on the chart:

Short MA (blue line).

Long MA (red line).

Generation of buy and sell signals:

Buy (BUY): When the short MA crosses the long MA from below.

Sell (SELL): When the short MA crosses the long MA from above.

Visualization of signals on the chart:

Buy is displayed as a green BUY marker below the candle.

Sell is displayed as a red SELL marker above the candle.

Liquidity Heatmap:

Liquidity levels:

Levels are calculated based on the closing price and a step (liquidity_step).

Levels are grouped by the nearest price values.

Volumes at levels:

Volume (volume) is accumulated for each liquidity level.

Levels with a volume less than min_volume_filter are not displayed.

Time filtering:

Levels that have not been updated within the last time_filter bars are not displayed.

Volatility filtering:

Levels are filtered by volatility (ATR) to exclude those outside the volatility range.

Color gradient:

The color of levels depends on volume (gradient from gradient_start_color to gradient_end_color).

Visualization:

Liquidity levels are displayed as horizontal lines.

Volumes at levels are shown as text labels.

RSI Filtering:

The ability to enable/disable RSI filtering (rsi_filter).

Liquidity levels are filtered based on overbought (rsi_overbought) and oversold (rsi_oversold) conditions.

Levels that do not meet RSI conditions are not displayed.

MACD Filtering:

The ability to enable/disable MACD filtering (macd_filter).

Liquidity levels are filtered based on the MACD histogram condition (e.g., only if the histogram is above zero).

Levels that do not meet MACD conditions are not displayed.

Display of Market Maker Buys:

Condition for market maker buys:

Volume exceeds the average volume over the last 20 bars by 2 times.

Closing price is above the opening price.

Market maker buys are displayed on the chart as orange MM Buy markers below the candle.

Indicator Settings:

Moving average parameters:

short_ma_length: Period for the short MA.

long_ma_length: Period for the long MA.

Liquidity heatmap parameters:

liquidity_step: Step between liquidity levels.

max_levels: Maximum number of levels to display.

time_filter: Time filter (last N bars).

min_volume_filter: Minimum volume for displaying a level.

volatility_filter: Volatility filter (ATR multiplier).