Luxy BIG beautiful Dynamic ORBThis is an advanced Opening Range Breakout (ORB) indicator that tracks price breakouts from the first 5, 15, 30, and 60 minutes of the trading session. It provides complete trade management including entry signals, stop-loss placement, take-profit targets, and position sizing calculations.

The ORB strategy is based on the concept that the opening range of a trading session often acts as support/resistance, and breakouts from this range tend to lead to significant moves.

What Makes This Different?

Most ORB indicators simply draw horizontal lines and leave you to figure out the rest. This indicator goes several steps further:

Multi-Stage Tracking

Instead of just one ORB timeframe, this tracks FOUR simultaneously (5min, 15min, 30min, 60min). Each stage builds on the previous one, giving you multiple trading opportunities throughout the session.

Active Trade Management

When a breakout occurs, the indicator automatically calculates and displays entry price, stop-loss, and multiple take-profit targets. These lines extend forward and update in real-time until the trade completes.

Cycle Detection

Unlike indicators that only show the first breakout, this tracks the complete cycle: Breakout → Retest → Re-breakout. You can see when price returns to test the ORB level after breaking out (potential re-entry).

Failed Breakout Warning

If price breaks out but quickly returns inside the range (within a few bars), the label changes to "FAILED BREAK" - warning you to exit or avoid the trade.

Position Sizing Calculator

Built-in risk management that tells you exactly how many shares to buy based on your account size and risk tolerance. No more guessing or manual calculations.

Advanced Filtering

Optional filters for volume confirmation, trend alignment, and Fair Value Gaps (FVG) to reduce false signals and improve win rate.

Core Features Explained

### 1. Multi-Stage ORB Levels

The indicator builds four separate Opening Range levels:

ORB 5 - First 5 minutes (fastest signals, most volatile)

ORB 15 - First 15 minutes (balanced, most popular)

ORB 30 - First 30 minutes (slower, more reliable)

ORB 60 - First 60 minutes (slowest, most confirmed)

Each level is drawn as a horizontal range on your chart. As time progresses, the ranges expand to include more price action. You can enable or disable any stage and assign custom colors to each.

How it works: During the opening minutes, the indicator tracks the highest high and lowest low. Once the time period completes, those levels become your ORB high and low for that stage.

### 2. Breakout Detection

When price closes outside the ORB range, a label appears:

BREAK UP (green label above price) - Price closed above ORB High

BREAK DOWN (red label below price) - Price closed below ORB Low

The label shows which ORB stage triggered (ORB5, ORB15, etc.) and the cycle number if tracking multiple breakouts.

Important: Signals appear on bar close only - no repainting. What you see is what you get.

### 3. Retest Detection

After price breaks out and moves away, if it returns to test the ORB level, a "RETEST" label appears (orange). This indicates:

The original breakout level is now acting as support/resistance

Potential re-entry opportunity if you missed the first breakout

Confirmation that the level is significant

The indicator requires price to move a minimum distance away before considering it a valid retest (configurable in settings).

### 4. Failed Breakout Detection

If price breaks out but returns inside the ORB range within a few bars (before the breakout is "committed"), the original label changes to "FAILED BREAK" in orange.

This warns you:

The breakout lacked conviction

Consider exiting if already in the trade

Wait for better setup

Committed Breakout: The indicator tracks how many bars price stays outside the range. Only after staying outside for the minimum number of bars does it become a committed breakout that can be retested.

### 5. TP/SL Lines (Trade Management)

When a breakout occurs, colored horizontal lines appear showing:

Entry Line (cyan for long, orange for short) - Your entry price (the ORB level)

Stop Loss Line (red) - Where to exit if trade goes against you

TP1, TP2, TP3 Lines (same color as entry) - Profit targets at 1R, 2R, 3R

These lines extend forward as new bars form, making it easy to track your trade. When a target is hit, the line turns green and the label shows a checkmark.

Lines freeze (stop updating) when:

Stop loss is hit

The final enabled take-profit is hit

End of trading session (optional setting)

### 6. Position Sizing Dashboard

The dashboard (bottom-left corner by default) shows real-time information:

Current ORB stage and range size

Breakout status (Inside Range / Break Up / Break Down)

Volume confirmation (if filter enabled)

Trend alignment (if filter enabled)

Entry and Stop Loss prices

All enabled Take Profit levels with percentages

Risk/Reward ratio

Position sizing: Max shares to buy and total risk amount

Position Sizing Example:

If your account is $25,000 and you risk 1% per trade ($250), and the distance from entry to stop loss is $0.50, the calculator shows you can buy 500 shares (250 / 0.50 = 500).

### 7. FVG Filter (Fair Value Gap)

Fair Value Gaps are price inefficiencies - gaps left by strong momentum where one candle's high doesn't overlap with a previous candle's low (or vice versa).

When enabled, this filter:

Detects bullish and bearish FVGs

Draws semi-transparent boxes around these gaps

Only allows breakout signals if there's an FVG near the breakout level

Why this helps: FVGs indicate institutional activity. Breakouts through FVGs tend to be stronger and more reliable.

Proximity setting: Controls how close the FVG must be to the ORB level. 2.0x means the breakout can be within 2 times the FVG size - a reasonable default.

### 8. Volume & Trend Filters

Volume Filter:

Requires current volume to be above average (customizable multiplier). High volume breakouts are more likely to sustain.

Set minimum multiplier (e.g., 1.5x = 50% above average)

Set "strong volume" multiplier (e.g., 2.5x) that bypasses other filters

Dashboard shows current volume ratio

Trend Filter:

Only shows breakouts aligned with a higher timeframe trend. Choose from:

VWAP - Price above/below volume-weighted average

EMA - Price above/below exponential moving average

SuperTrend - ATR-based trend indicator

Combined modes (VWAP+EMA, VWAP+SuperTrend) for stricter filtering

### 9. Pullback Filter (Advanced)

Purpose:

Waits for price to pull back slightly after initial breakout before confirming the signal.

This reduces false breakouts from immediate reversals.

How it works:

- After breakout is detected, indicator waits for a small pullback (default 2%)

- Once pullback occurs AND price breaks out again, signal is confirmed

- If no pullback within timeout period (5 bars), signal is issued anyway

Settings:

Enable Pullback Filter: Turn this filter on/off

Pullback %: How much price must pull back (2% is balanced)

Timeout (bars): Max bars to wait for pullback (5 is standard)

When to use:

- Choppy markets with many fake breakouts

- When you want higher quality signals

- Combine with Volume filter for maximum confirmation

Trade-off:

- Better signal quality

- May miss some valid fast moves

- Slight entry delay

How to Use This Indicator

### For Beginners - Simple Setup

Add the indicator to your chart (5-minute or 15-minute timeframe recommended)

Leave all default settings - they work well for most stocks

Watch for BREAK UP or BREAK DOWN labels to appear

Check the dashboard for entry, stop loss, and targets

Use the position sizing to determine how many shares to buy

Basic Trading Plan:

Wait for a clear breakout label

Enter at the ORB level (or next candle open if you're late)

Place stop loss where the red line indicates

Take profit at TP1 (50% of position) and TP2 (remaining 50%)

### For Advanced Traders - Customized Setup

Choose which ORB stages to track (you might only want ORB15 and ORB30)

Enable filters: Volume (stocks) or Trend (trending markets)

Enable FVG filter for institutional confirmation

Set "Track Cycles" mode to catch retests and re-breakouts

Customize stop loss method (ATR for volatile stocks, ORB% for stable ones)

Adjust risk per trade and account size for accurate position sizing

Advanced Strategy Example:

Enable ORB15 only (disable others for cleaner chart)

Turn on Volume filter at 1.5x with Strong at 2.5x

Enable Trend filter using VWAP

Set Signal Mode to "Track Cycles" with Max 3 cycles

Wait for aligned breakouts (Volume + Trend + Direction)

Enter on retest if you missed the initial break

### Timeframe Recommendations

5-minute chart: Scalping, very active trading, crypto

15-minute chart: Day trading, balanced approach (most popular)

30-minute chart: Swing entries, less screen time

60-minute chart: Position trading, longer holds

The indicator works on any intraday timeframe, but ORB is fundamentally a day trading strategy. Daily charts don't make sense for ORB.

DEFAULT CONFIGURATION

ON by Default:

• All 4 ORB stages (5/15/30/60)

• Breakout Detection

• Retest Labels

• All TP levels (1/1.5/2/3)

• TP/SL Lines (Detailed mode)

• Dashboard (Bottom Left, Dark theme)

• Position Size Calculator

OFF by Default (Optional Filters):

• FVG Filter

• Pullback Filter

• Volume Filter

• Trend Filter

• HTF Bias Check

• Alerts

Recommended for Beginners:

• Leave all defaults

• Session Mode: Auto-Detect

• Signal Mode: Track Cycles

• Stop Method: ATR

• Add Volume Filter if trading stocks

Recommended for Advanced:

• Enable ORB15 + ORB30 only (disable 5 & 60)

• Enable: Volume + Trend + FVG

• Signal Mode: Track Cycles, Max 3

• Stop Method: ATR or Safer

• Enable HTF Daily bias check

## Settings Guide

The settings are organized into logical groups. Here's what each section controls:

### ORB COLORS Section

Show Edge Labels: Display "ORB 5", "ORB 15" labels at the right edge of the levels

Background: Fill the area between ORB high/low with color

Transparency: How see-through the background is (95% is nearly invisible)

Enable ORB 5/15/30/60: Turn each stage on or off individually

Colors: Assign colors to each ORB stage for easy identification

### SESSION SETTINGS Section

Session Mode: Choose trading session (Auto-Detect works for most instruments)

Custom Session Hours: Define your own hours if needed (format: HHMM-HHMM)

Auto-Detect uses the instrument's natural hours (stocks use exchange hours, crypto uses 24/7).

### BREAKOUT DETECTION Section

Enable Breakout Detection: Master switch for signals

Show Retest Labels: Display retest signals

Label Size: Visual size for all labels (Small recommended)

Enable FVG Filter: Require Fair Value Gap confirmation

Show FVG Boxes: Display the gap boxes on chart

Signal Mode: "First Only" = one signal per direction per day, "Track Cycles" = multiple signals

Max Cycles: How many breakout-retest cycles to track (6 is balanced)

Breakout Buffer: Extra distance required beyond ORB level (0.1-0.2% recommended)

Min Distance for Retest: How far price must move away before retest is valid (2% recommended)

Min Bars Outside ORB: Bars price must stay outside for committed breakout (2 is balanced)

### TARGETS & RISK Section

Enable Targets & Stop-Loss: Calculate and show trade management

TP1/TP2/TP3 checkboxes: Select which profit targets to display

Stop Method: How to calculate stop loss placement

- ATR: Based on volatility (best for most cases)

- ORB %: Fixed % of ORB range

- Swing: Recent swing high/low

- Safer: Widest of all methods

ATR Length & Multiplier: Controls ATR stop distance (14 period, 1.5x is standard)

ORB Stop %: Percentage beyond ORB for stop (20% is balanced)

Swing Bars: Lookback period for swing high/low (3 is recent)

### TP/SL LINES Section

Show TP/SL Lines: Display horizontal lines on chart

Label Format: "Short" = minimal text, "Detailed" = shows prices

Freeze Lines at EOD: Stop extending lines at session close

### DASHBOARD Section

Show Info Panel: Display the metrics dashboard

Theme: Dark or Light colors

Position: Where to place dashboard on chart

Toggle rows: Show/hide specific information rows

Calculate Position Size: Enable the position sizing calculator

Risk Mode: Risk fixed $ amount or % of account

Account Size: Your total trading capital

Risk %: Percentage to risk per trade (0.5-1% recommended)

### VOLUME FILTER Section

Enable Volume Filter: Require volume confirmation

MA Length: Average period (20 is standard)

Min Volume: Required multiplier (1.5x = 50% above average)

Strong Volume: Multiplier that bypasses other filters (2.5x)

### TREND FILTER Section

Enable Trend Filter: Require trend alignment

Trend Mode: Method to determine trend (VWAP is simple and effective)

Custom EMA Length: If using EMA mode (50 for swing, 20 for day trading)

SuperTrend settings: Period and Multiplier if using SuperTrend mode

### HIGHER TIMEFRAME Section

Check Daily Trend: Display higher timeframe bias in dashboard

Timeframe: What TF to check (D = daily, recommended)

Method: Price vs MA (stable) or Candle Direction (reactive)

MA Period: EMA length for Price vs MA method (20 is balanced)

Min Strength %: Minimum strength threshold for HTF bias to be considered

- For "Price vs MA": Minimum distance (%) from moving average

- For "Candle Direction": Minimum candle body size (%)

- 0.5% is balanced - increase for stricter filtering

- Lower values = more signals, higher values = only strong trends

### ALERTS Section

Enable Alerts: Master switch (must be ON to use any alerts)

Breakout Alerts: Notify on ORB breakouts

Retest Alerts: Notify when price retests after breakout

Failed Break Alerts: Notify on failed breakouts

Stage Complete Alerts: Notify when each ORB stage finishes forming

After enabling desired alert types, click "Create Alert" button, select this indicator, choose "Any alert() function call".

## Tips & Best Practices

### General Trading Tips

ORB works best on liquid instruments (stocks with good volume, major crypto pairs)

First hour of the session is most important - that's when ORB is forming

Breakouts WITH the trend have higher success rates - use the trend filter

Failed breakouts are common - use the "Min Bars Outside" setting to filter weak moves

Not every day produces good ORB setups - be patient and selective

### Position Sizing Best Practices

Never risk more than 1-2% of your account on a single trade

Use the built-in calculator - don't guess your position size

Update your account size monthly as it grows

Smaller accounts: use $ Amount mode for simplicity

Larger accounts: use % of Account mode for scaling

### Take Profit Strategy

Most traders use: 50% at TP1, 50% at TP2

Aggressive: Hold through TP1 for TP2 or TP3

Conservative: Full exit at TP1 (1:1 risk/reward)

After TP1 hits, consider moving stop to breakeven

TP3 rarely hits - only on strong trending days

### Filter Combinations

Maximum Quality: Volume + Trend + FVG (fewest signals, highest quality)

Balanced: Volume + Trend (good quality, reasonable frequency)

Active Trading: No filters or Volume only (many signals, lower quality)

Trending Markets: Trend filter essential (indices, crypto)

Range-Bound: Volume + FVG (avoid trend filter)

### Common Mistakes to Avoid

Chasing breakouts - wait for the bar to close, don't FOMO into wicks

Ignoring the stop loss - always use it, move it manually if needed

Over-leveraging - the calculator shows MAX shares, you can buy less

Trading every signal - quality > quantity, use filters

Not tracking results - keep a journal to see what works for YOU

## Pros and Cons

### Advantages

Complete all-in-one solution - from signal to position sizing

Multiple timeframes tracked simultaneously

Visual clarity - easy to see what's happening

Cycle tracking catches opportunities others miss

Built-in risk management eliminates guesswork

Customizable filters for different trading styles

No repainting - what you see is locked in

Works across multiple markets (stocks, forex, crypto)

### Limitations

Intraday strategy only - doesn't work on daily charts

Requires active monitoring during first 1-2 hours of session

Not suitable for after-hours or extended sessions by default

Can produce many signals in choppy markets (use filters)

Dashboard can be overwhelming for complete beginners

Performance depends on market conditions (trends vs ranges)

Requires understanding of risk management concepts

### Best For

Day traders who can watch the first 1-2 hours of market open

Traders who want systematic entry/exit rules

Those learning proper position sizing and risk management

Active traders comfortable with multiple signals per day

Anyone trading liquid instruments with clear sessions

### Not Ideal For

Swing traders holding multi-day positions

Set-and-forget / passive investors

Traders who can't watch market open

Complete beginners unfamiliar with trading concepts

Low volume / illiquid instruments

## Frequently Asked Questions

Q: Why are no signals appearing?

A: Check that you're on an intraday timeframe (5min, 15min, etc.) and that the current time is within your session hours. Also verify that "Enable Breakout Detection" is ON and at least one ORB stage is enabled. If using filters, they might be blocking signals - try disabling them temporarily.

Q: What's the best ORB stage to use?

A: ORB15 (15 minutes) is most popular and balanced. ORB5 gives faster signals but more noise. ORB30 and ORB60 are slower but more reliable. Many traders use ORB15 + ORB30 together.

Q: Should I enable all the filters?

A: Start with no filters to see all signals. If too many false signals, add Volume filter first (stocks) or Trend filter (trending markets). FVG filter is most restrictive - use for maximum quality but fewer signals.

Q: How do I know which stop loss method to use?

A: ATR works for most cases - it adapts to volatility. Use ORB% if you want predictable stop placement. Swing is for respecting chart structure. Safer gives you the most room but largest risk.

Q: Can I use this for swing trading?

A: Not really - ORB is fundamentally an intraday strategy. The ranges reset each day. For swing trading, look at weekly support/resistance or moving averages instead.

Q: Why do TP/SL lines disappear sometimes?

A: Lines freeze (stop extending) when: stop loss is hit, the last enabled take-profit is hit, or end of session arrives (if "Freeze at EOD" is enabled). This is intentional - the trade is complete.

Q: What's the difference between "First Only" and "Track Cycles"?

A: "First Only" shows one breakout UP and one DOWN per day maximum - clean but might miss opportunities. "Track Cycles" shows breakout-retest-rebreak sequences - more signals but busier chart.

Q: Is position sizing accurate for options/forex?

A: The calculator is designed for shares (stocks). For options, ignore the share count and use the risk amount. For forex, you'll need to adapt the lot size calculation manually.

Q: How much capital do I need to use this?

A: The indicator works for any account size, but practical day trading typically requires $25,000 in the US due to Pattern Day Trader rules. Adjust the "Account Size" setting to match your capital.

Q: Can I backtest this strategy?

A: This is an indicator, not a strategy script, so it doesn't have built-in backtesting. You can visually review historical signals or code a strategy script using similar logic.

Q: Why does the dashboard show different entry price than the breakout label?

A: If you're looking at an old breakout, the ORB levels may have changed when the next stage completed. The dashboard always shows the CURRENT active range and trade setup.

Q: What's a good win rate to expect?

A: ORB strategies typically see 40-60% win rate depending on market conditions and filters used. The strategy relies on positive risk/reward ratios (2:1 or better) to be profitable even with moderate win rates.

Q: Does this work on crypto?

A: Yes, but crypto trades 24/7 so you need to define what "session start" means. Use Session Mode = Custom and set your preferred daily reset time (e.g., 0000-2359 UTC).

## Credits & Transparency

### Development

This indicator was developed with the assistance of AI technology to implement complex ORB trading logic.

The strategy concept, feature specifications, and trading logic were designed by the publisher. The implementation leverages modern development tools to ensure:

Clean, efficient, and maintainable code

Comprehensive error handling and input validation

Detailed documentation and user guidance

Performance optimization

### Trading Concepts

This indicator implements several public domain trading concepts:

Opening Range Breakout (ORB): Trading strategy popularized by Toby Crabel, Mark Fisher and many more talanted traders.

Fair Value Gap (FVG): Price imbalance concept from ICT methodology

SuperTrend: ATR-based trend indicator using public formula

Risk/Reward Ratio: Standard risk management principle

All mathematical formulas and technical concepts used are in the public domain.

### Pine Script

Uses standard TradingView built-in functions:

ta.ema(), ta.atr(), ta.vwap(), ta.highest(), ta.lowest(), request.security()

No external libraries or proprietary code from other authors.

## Disclaimer

This indicator is provided for educational and informational purposes only. It is not financial advice.

Trading involves substantial risk of loss and is not suitable for every investor. Past performance shown in examples is not indicative of future results.

The indicator provides signals and calculations, but trading decisions are solely your responsibility. Always:

Test strategies on paper before using real money

Never risk more than you can afford to lose

Understand that all trading involves risk

Consider seeking advice from a licensed financial advisor

The publisher makes no guarantees regarding accuracy, profitability, or performance. Use at your own risk.

---

Version: 3.0

Pine Script Version: v6

Last Updated: October 2024

For support, questions, or suggestions, please comment below or send a private message.

---

Happy trading, and remember: consistent risk management beats perfect entry timing every time.

Cerca negli script per "profit"

Adaptive Trend 1m ### Overview

The "Adaptive Trend Impulse Parallel SL/TP 1m Realistic" strategy is a sophisticated trading system designed specifically for high-volatility markets like cryptocurrencies on 1-minute timeframes. It combines trend-following with momentum filters and adaptive parameters to dynamically adjust to market conditions, ensuring more reliable entries and risk management. This strategy uses SuperTrend for primary trend detection, enhanced by MACD, RSI, Bollinger Bands, and optional volume spikes. It incorporates parallel stop-loss (SL) and multiple take-profit (TP) levels based on ATR, with options for breakeven and trailing stops after the first TP. Optimized for realistic backtesting on short timeframes, it avoids over-optimization by adapting indicators to market speed and efficiency.

### Principles of Operation

The strategy operates on the principle of adaptive impulse trading, where entry signals are generated only when multiple conditions align to confirm a strong trend reversal or continuation:

1. **Trend Detection (SuperTrend)**: The core signal comes from an adaptive SuperTrend indicator. It calculates upper and lower bands using ATR (Average True Range) with dynamic periods and multipliers. A buy signal occurs when the price crosses above the lower band (from a downtrend), and a sell signal when it crosses below the upper band (from an uptrend). Adaptation is based on Rate of Change (ROC) to measure market speed, shortening periods in fast markets for quicker responses.

2. **Momentum and Trend Filters**:

- **MACD**: Uses adaptive fast and slow lengths. In "Trend Filter" mode (default when "Use MACD Cross" is false), it checks if the MACD line is above/below the signal for long/short. In cross mode, it requires a crossover/crossunder.

- **RSI**: Adaptive period RSI must be above 50 for longs and below 50 for shorts, confirming overbought/oversold conditions dynamically.

- **Bollinger Bands (BB)**: Depending on the mode ("Midline" by default), it requires the price to be above/below the BB midline for longs/shorts, or a breakout in "Breakout" mode. Deviation adapts to market efficiency.

- **Volume Spike Filter** (optional): Entries require volume to exceed an adaptive multiple of its SMA, signaling strong impulse.

3. **Volatility Filter**: Entries are only allowed if current ATR percentage exceeds a historical minimum (adaptive), preventing trades in low-volatility ranges.

4. **Risk Management (Parallel SL/TP)**:

- **Stop-Loss**: Set at an adaptive ATR multiple below/above entry for long/short.

- **Take-Profits**: Three levels at adaptive ATR multiples, with partial position closures (e.g., 51% at TP1, 25% at TP2, remainder at TP3).

- **Post-TP1 Features**: Optional breakeven moves SL to entry after TP1. Trailing SL uses BB midline as a dynamic trail.

- All levels are calculated per trade using the ATR at entry, making them "realistic" for 1m charts by widening SL and tightening initial TPs.

The strategy enters long on buy signals with all filters met, and short on sell signals. It uses pyramid margin (100% long/short) for full position sizing.

Adaptation is driven by:

- **Market Speed (normSpeed)**: Based on ROC, tightens multipliers in volatile periods.

- **Efficiency Ratio (ER)**: Measures trend strength, adjusting periods for trending vs. ranging markets.

This ensures the strategy "adapts" without manual tweaks, reducing false signals in varying conditions.

### Main Advantages

- **Adaptability**: Unlike static strategies, parameters dynamically adjust to market volatility and trend strength, improving performance across ranging and trending phases without over-optimization.

- **Realistic Risk Management for 1m**: Wider SL and tiered TPs prevent premature stops in noisy short-term charts, while partial profits lock in gains early. Breakeven/trailing options protect profits in extended moves.

- **Multi-Filter Confirmation**: Combines trend, momentum, and volume for high-probability entries, reducing whipsaws. The volatility filter avoids flat markets.

- **Debug Visualization**: Built-in plots for signals, levels, and component checks (when "Show Debug" is enabled) help users verify logic on charts.

- **Efficiency**: Low computational load, suitable for real-time trading on TradingView with alerts.

Backtesting shows robust results on volatile assets, with a focus on sustainable risk (e.g., SL at 3x ATR avoids excessive drawdowns).

### Uniqueness

What sets this strategy apart is its **fully adaptive framework** integrating multiple indicators with real-time market metrics (ROC for speed, ER for efficiency). Most trend strategies use fixed parameters, leading to poor adaptation; here, every key input (periods, multipliers, deviations) scales dynamically within bounds, creating a "self-tuning" system. The "parallel SL/TP with 1m realism" adds custom handling for micro-timeframes: tightened initial TPs for quick wins and adaptive min-ATR filter to skip low-vol bars. Unlike generic mashups, it justifies the combination—SuperTrend for trend, MACD/RSI/BB for impulse confirmation, volume for conviction—working synergistically to capture "trend impulses" while filtering noise. The post-TP1 breakeven/trailing tied to BB adds a unique profit-locking mechanism not common in open-source scripts.

### Recommended Settings

These settings are optimized and recommended for trading ASTER/USDT on Bybit, with 1-minute chart, x10 leverage, and cross margin mode. They provide a balanced risk-reward for this volatile pair:

- **Base Inputs**:

- Base ATR Period: 10

- Base SuperTrend ATR Multiplier: 2.5

- Base MACD Fast: 8

- Base MACD Slow: 17

- Base MACD Signal: 6

- Base RSI Period: 9

- Base Bollinger Period: 12

- Bollinger Deviation: 1.8

- Base Volume SMA Period: 19

- Base Volume Spike Multiplier: 1.8

- Adaptation Window: 54

- ROC Length: 10

- **TP/SL Settings**:

- Use Stop Loss: True

- Base SL Multiplier (ATR): 3

- Use Take Profits: True

- Base TP1 Multiplier (ATR): 5.5

- Base TP2 Multiplier (ATR): 10.5

- Base TP3 Multiplier (ATR): 19

- TP1 % Position: 51

- TP2 % Position: 25

- Breakeven after TP1: False

- Trailing SL after TP1: False

- Base Min ATR Filter: 0.001

- Use Volume Spike Filter: True

- BB Condition: Midline

- Use MACD Cross (false=Trend Filter): True

- Show Debug: True

For backtesting, use initial capital of 30 USD, base currency USDT, order size 100 USDT, pyramiding 1, commission 0.1%, slippage 0 ticks, long/short margin 0%.

Always backtest on your platform and use risk management—risk no more than 1-2% per trade. This is not financial advice; trade at your own risk.

🚀 Ultimate Trading Tool + Strat Method🚀 Ultimate Trading Tool + Strat Method - Complete Breakdown

Let me give you a comprehensive overview of this powerful indicator!

🎯 What This Indicator Does:

This is a professional-grade, all-in-one trading system that combines two proven methodologies:

1️⃣ Technical Analysis System (Original)

Advanced trend detection using multiple EMAs

Momentum analysis with MACD

RSI multi-timeframe analysis

Volume surge detection

Automated trendline drawing

2️⃣ Strat Method (Pattern Recognition)

Inside bars, outside bars, directional bars

Classic patterns: 2-2, 1-2-2

Advanced patterns: 3-1-2, 2-1-2, F2→3

Timeframe continuity filters

📊 How It Generates Signals:

Technical Analysis Signals (Green/Red Triangles):

Buy Signal Triggers When:

✅ Price above EMA 21 & 50 (uptrend)

✅ MACD histogram rising (momentum)

✅ RSI between 30-70 (not overbought/oversold)

✅ Volume surge above 20-period average

✅ Price breaks above resistance trendline

Scoring System:

Trend alignment: +1 point

Momentum: +1 point

RSI favorable: +1 point

Trendline breakout: +2 points

Minimum score required based on sensitivity setting

Strat Method Signals (Blue/Orange Labels):

Pattern Recognition:

2-2 Setup: Down bar → Up bar (or reverse)

1-2-2 Setup: Inside bar → Down bar → Up bar

3-1-2 Setup: Outside bar → Inside bar → Up bar

2-1-2 Setup: Down bar → Inside bar → Up bar

F2→3 Setup: Failed directional bar becomes outside bar

Confirmation Required:

Must break previous bar's high (buy) or low (sell)

Optional timeframe continuity (daily & weekly aligned)

💰 Risk Management Features:

Dynamic Stop Loss & Take Profit:

ATR-Based: Adapts to market volatility

Stop Loss: Entry - (ATR × 1.5) by default

Take Profit: Entry + (ATR × 3.0) by default

Risk:Reward: Customizable 1:2 to 1:5 ratios

Visual Risk Zones:

Colored boxes show risk/reward area

Dark, bold lines for easy identification

Clear entry, stop, and target levels

🎨 What You See On Screen:

Main Signals:

🟢 Green Triangle "BUY" - Technical analysis long signal

🔴 Red Triangle "SELL" - Technical analysis short signal

🎯 Blue Label "STRAT" - Strat method long signal

🎯 Orange Label "STRAT" - Strat method short signal

Trendlines:

Green lines - Support trendlines (bullish)

Red lines - Resistance trendlines (bearish)

Automatically drawn from pivot points

Extended forward to predict future levels

Stop/Target Levels:

Bold crosses at stop loss levels (red color)

Bold crosses at take profit levels (green color)

Line width = 3 for maximum visibility

Trade Zones:

Light green boxes - Long trade risk/reward zone

Light red boxes - Short trade risk/reward zone

Shows potential profit vs risk visually

📊 Information Dashboard (Top Right):

Shows real-time market conditions:

Main Signal: Current technical signal status

Strat Method: Active Strat pattern

Trend: Bullish/Bearish/Neutral

Momentum: Strong/Weak based on MACD

Volume: High/Normal compared to average

TF Continuity: Daily/Weekly alignment

RSI: Current RSI value with color coding

Support/Resistance: Current trendline levels

🔔 Alert System:

Entry Alerts:

Technical Signals:

🚀 BUY SIGNAL TRIGGERED!

Type: Technical Analysis

Entry: 45.23

Stop: 43.87

Target: 48.95

```

**Strat Signals:**

```

🎯 STRAT BUY TRIGGER!

Pattern: 3-1-2

Entry: 45.23

Trigger Level: 44.56

Exit Alerts:

Target hit notifications

Stop loss hit warnings

Helps maintain discipline

⚙️ Customization Options:

Signal Settings:

Sensitivity: High/Medium/Low (controls how many signals)

Volume Filter: Require volume surge or not

Momentum Filter: Require momentum confirmation

Strat Settings:

TF Continuity: Require daily/weekly alignment

Pattern Selection: Enable/disable specific patterns

Confirmation Mode: Show only confirmed triggers

Risk Settings:

ATR Multiplier: Adjust stop/target distance

Risk:Reward: Set preferred ratio

Visual Elements: Show/hide any component

Visual Settings:

Colors: Customize all signal colors

Display Options: Toggle signals, levels, zones

Trendline Length: Adjust pivot detection period

🎯 Best Use Cases:

Day Trading:

Use low sensitivity setting

Enable all Strat patterns

Watch for high volume signals

Quick in/out trades

Swing Trading:

Use medium sensitivity

Require timeframe continuity

Focus on trendline breakouts

Hold for target levels

Position Trading:

Use high sensitivity (fewer signals)

Require strong momentum

Focus on weekly/daily alignment

Larger ATR multipliers

💡 Trading Strategy Tips:

High-Probability Setups:

Double Confirmation: Technical + Strat signal together

Trend Alignment: All timeframes agree

Volume Surge: Institutional participation

Trendline Break: Clear level breakout

Risk Management:

Always use stops - System provides them

Position sizing - Risk 1-2% per trade

Don't chase - Wait for signal confirmation

Take profits - System provides targets

What Makes Signals Strong:

✅ Both technical AND Strat signals fire together

✅ Timeframe continuity (daily & weekly aligned)

✅ Volume surge confirms institutional interest

✅ Multiple indicators align (trend + momentum + RSI)

✅ Clean trendline breakout with no resistance above (or support below)

⚠️ Common Mistakes to Avoid:

Don't ignore stops - System calculates them for a reason

Don't overtrade - Wait for quality setups

Don't disable volume filter - Unless you know what you're doing

Don't use max sensitivity - You'll get too many signals

Don't ignore timeframe continuity - It filters bad trades

🚀 Why This Indicator is Powerful:

Combines Multiple Edge Sources:

Technical analysis (trend, momentum, volume)

Pattern recognition (Strat method)

Risk management (dynamic stops/targets)

Market structure (trendlines, support/resistance)

Professional Features:

No repainting - signals are final when bar closes

Clear risk/reward before entry

Multiple confirmation layers

Adaptable to any market or timeframe

Beginner Friendly:

Clear visual signals

Automatic calculations

Built-in risk management

Comprehensive dashboard

This indicator essentially gives you everything a professional trader uses - trend analysis, momentum, patterns, volume, risk management - all in one clean package!

Any specific aspect you'd like me to explain in more detail? 🎯RetryClaude can make mistakes. Please double-check responses. Sonnet 4.5

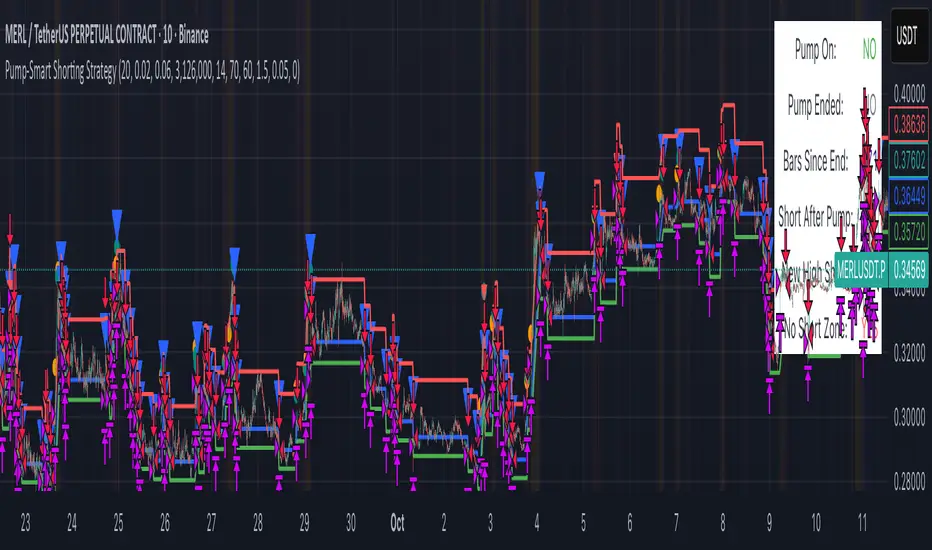

Pump-Smart Shorting StrategyThis strategy is built to keep your portfolio hedged as much as possible while maximizing profitability. Shorts are opened after pumps cool off and on new highs (when safe), and closed quickly during strong upward moves or if stop loss/profit targets are hit. It uses visual overlays to clearly show when hedging is on, off, or blocked due to momentum, ensuring you’re protected in most market conditions but never short against the pump. Fast re-entry keeps the hedge active with minimal downtime.

Pump Detection:

RSI (Relative Strength Index): Calculated over a custom period (default 14 bars). If RSI rises above a threshold (default 70), the strategy considers the market to be in a pump (strong upward momentum).

Volume Spike: The current volume is compared to a 20-bar simple moving average of volume. If it exceeds the average by 1.5× and price increases at least 5% in one bar, pump conditions are triggered.

Price Jump: Measured by (close - close ) / close . A single-bar change > 5% helps confirm rapid momentum.

Pump Zone (No Short): If any of these conditions is true, an orange or red background is shown and shorts are blocked.

Cooldown and Re-Entry:

Cooldown Detection: After the pump ends, RSI must fall below a set value (default ≤ 60), and either volume returns towards average or price momentum is less than half the original spike (oneBarUp <= pctUp/2).

barsWait Parameter: You can specify a waiting period after cooldown before a short is allowed.

Short Entry After Pump/Cooldown: When these cooldown conditions are met, and no short is active, a blue background is shown and a short position is opened at the next signal.

New High Entry:

Lookback New High: If the current high is greater than the highest high in the last N bars (default 20), and pump is NOT active, a short can be opened.

Take Profit (TP) & Stop Loss (SL):

Take Profit: Short is closed if price falls to a threshold below the entry (minProfitPerc, default 2%).

Stop Loss: Short is closed if price rises to a threshold above the entry (stopLossPerc, default 6%).

Preemptive Exit:

Any time a pump is detected while a short position is open, the strategy closes the short immediately to avoid losses.

Visual Feedback:

Orange Background: Market is pumping, do not short.

Red Background: Other conditions block shorts (cooldown or waiting).

Blue Background: Shorts allowed.

Triangles/Circles: Mark entries, pump start/end, for clear trading signals.

GRG/RGR Signal, MA, Ranges and PivotsThis indicator is a combination of several indicators.

It is a combination of two of my indicators which I solely use for trading

1. EMA 10-20-50-200, Pivots and Previous Day/Week/Month range

2. 3/4-Bar GRG / RGR Pattern (Conditional 4th Candle)

You can use them individually if you already have some of them or just use this one. Belive me when I say, this is all you need, along with market structure knowlege and even if you don’t have that, this indicator has been doing wonders for me. This is all I use. I do not use anything else.

**Note - Do checkout the indicators individually as I have added valuable information in the comment section.

It contains the following,

1. 10 EMA/SMA - configurable

2. 20 EMA/SMA - configurable

3. 50 EMA/SMA - configurable

4. 200 EMA/SMA - configurable

5. Previous Day's Range - configurable

6. Previous Week's Range - configurable

7. Previous Month's Range - configurable

8. Pivots - configurable

9. Buy Sell Signal - configurable

The Moving Averages

It is a very important combination and using it correctly with price action will strengthen your entries and exits.

The ema's or sma's added are the most powerful ones and they do definitely act as support and resistance.

The Daily/Weekly/Monthly Ranges

The Daily/Weekly/Monthly ranges are extremely important for any trader and should be used for targets and reversals.

Pivots

Pivots can provide support and resistance level. R5 and S5 can be used to check for over stretched conditions. You can customise them however you like. It is a full pivot indicator.

It is defaulted to show R5 and S5 only to reduce noise in the chart but it can be customised.

The 3/4 RGR or GRG Signal Generator

Combined with a 3/4 RGR or GRG setup can be all a trader needs.

You don't need complex strategies and SMC concepts to trade. Simple EMAs, ranges and RGR/GRG setup is the most winning combination.

This indicator can be used to identify the Green-Red-Green or Red-Green-Red pattern.

It is a price action indicator where a price action which identifies the defeat of buyers and sellers.

If the buyers comprehensively defeat the sellers then the price moves up and if the sellers defeat the buyers then the price moves down.

In my trading experience this is what defines the price movement.

It is a 3 or 4 candle pattern, beyond that i.e, 5 or more candles could mean a very sideways market and unnecessary signal generation.

How does it work?

Upside/Green signal

1. Say candle 1 is Green, which means buyers stepped in, then candle 2 is Red or a Doji, that means sellers brought the price down. Then if candle 3 is forming to be Green and breaks the closing of the 1st candle and opening of the 2nd candle, then a green arrow will appear and that is the place where you want to take your trade.

2. Here the buyers defeated the sellers.

3. Sometimes candle 3 falls short but candle 4 breaks candle 1's closing and candle 2's opening price. We can enter on candle 4.

4. Important - We need to enter the trade as soon as the price moves above the candle 1 and 2's body and should not wait for the 3rd or 4th candle to close. Ignore wicks.

5. But for a more optimised entry I have added an option to use candle’s highs and lows instead of open and close. This reduces lot of noise and provides us with more precise entry. This setting is turned on by default.

6. I have restricted it to 4 candles and that is all that is needed. More than that is a longer sideways market.

7. I call it the +-+ or GRG pattern or Green-Red-Green or Buyer-Seller-Buyer or Seller defeated or just Buyer pattern.

8. Stop loss can be candle 2's mid for safe traders (that includes me) or candle 2's body low for risky traders.

9. Back testing suggests that body low will be useless and result in more points in loss because for the bigger move this point will not be touched, so why not get out faster.

Downside/Red signal

1. Say candle 1 is Red, which means sellers stepped in, then candle 2 is Green or a Doji, that means buyers took the price up. Then if candle 3 is forming to be Red and breaks the closing of the 1st candle and opening of the 2nd candle then a Red arrow will appear and that is the place where you want to take your trade.

2. Sometimes candle 3 falls short but candle 4 breaks candle 1's closing and candle 2's opening price. We can enter on candle 4.

3. We need to enter the trade as soon as the price moves below the candle 1 and 2's body and should not wait for the 3rd or 4th candle to close.

4. But for a more optimised entry I have added an option to use candle’s highs and lows instead of open and close. This reduces lot of noise and provides us with more precise entry. This setting is turned on by default.

5. I have restricted it to 4 candles and that is all that is needed. More than that is a longer sideways market.

6. I call it the -+- or RGR pattern or Red-Green-Red or Seller-Buyer-Seller or Buyer defeated or just Seller pattern.

7. Stop loss can be candle 2's mid for safe traders ( that includes me) or candle 2's body high for risky traders.

8. Back testing suggests that body high will be useless and result in more points in loss because for the bigger move this point will not be touched, so why not get out faster.

Combining Indicators and Signal

Combining these indicators with GRG/RGR signal can be very powerful and can provide big moves.

1. MA crossover and Signal - This is very powerful and provides a very big move. Trades can be held for longer. If after taking the trade we notice that the MA crossover has happened then trades can be held for higher targets.

2. Pivots and Signal - Pivots and add a support or resistance point. Take profits on these points. R5/S5 are over streched conditions so we can start looking for reversal signals and ignore other signals

3. Intraday Range - first 1, 5, 15 min of the day - Sideways days is when price will stay in these ranges. You can take profits at these ranges or if the range is broken and we get a signal, then it can mean that the direction will be sustained.

4. Previous Day/Week/Month Ranges - These can be used as Take Profit points if the price is moving towards them after getting the signal. If the range is broken and we get a signal then it can be a strong signal. They can also be used as reversal points if a strong signal is generated.

Important Settings

1. Include 4th Candle Confirmation - You can enable or disable the 4th candle signal to avoid the noise, but at times I have noticed that the 4th candle gives a very strong signal or I can say that the strong signal falls on the 4th candle. This is mostly a coincidence.

2. Bars to check (default 10) - You can also configure how many previous bars should the signal be generated for. 10 to 30 is good enough. To backtest increase it to 2000 or 5000 for example.

3. Use Candle High/Low for confirmation instead of Candle Open/Close - More optimized entry and noise reduction. This option is now defaulted to false.

4. Show Green-Red-Green (bull) signals - Show only bull entries. Useful when I have a predefined view i.e, I know market is going to go up today.

5. Show Red-Green-Red (bear) signals - Show only bear entries. Useful when I have a predefined view i.e, I know market is going to go down today.

6. 3rd candle should be a Strong candle before considering 4th candle - This will enforce additional logic in 4 candle setup that the 3rd candle is the candle in our direction of breakout. This means something like GRGG is mandatory, which is still the default behaviour. If disabled, the 3rd candle can be any candle and 4th candle will act as our breakout candle. This behaviour has led to breakouts and breakdowns as times, hence I added this as a separate feature. Vice-versa for a RGGR.

For a 4 candle setup till now we were expecting GRGG or RGRR but we can let the system ignore the 3rd candle completely if needed.

This will result in additional signals.

7. Three intraday ranges added for index and stock traders - 1 min, 5 min and 15 min ranges will be displayed. These are disabled by default except 15 min. These are very important ranges and in sideways days the price will usually move within the 15 min. A breakout of this range and a positive signal can be a very powerful setup.

Safe traders can avoid taking a trade in this range as it can lead to fakeouts.

The line style, width, color and opacity are configurable.

Pointers/Golden Rules

1. If after taking the trade, the next candle moves in your direction and closes strong bullish or bearish, then move SL to break even and after that you can trail it.

2. If a upside trade hits SL and immediately a down side trade signal is generated on the next candle then take it. Vice versa is true.

3. Trades need to be taken on previous 2 candle's body high or low combined and not the wicks.

4. The most losses a trader takes is on a sideways day and because in our strategy the stop loss is so small that even on a sideways day we'll get out with a little profit or worst break even.

5. Hold trades for longer targets and don't panic.

6. If last 3-4 days have been sideways then there is a good probability that today will be trending so we can hold our trade for longer targets. Inverse is true when the market has been trending for 2-3 days then volatility followed by sideways is coming (DOW theory). Target to hold the trade for whole day and not exit till the day closes.

7. In general avoid trading in the middle of the day for index and stocks. Divide the day into 3 parts and avoid the middle.

8. Use Support/Resistance, 10, 20, 50, 200 EMA/SMA, Gaps, Whole/Round numbers(very imp) for identifying targets.

9. Trail your SL.

10. For indexes I would use 5 min and 15 min timeframe and at times 10 mins.

11. For commodities and crypto we can use higher timeframe as well. Look for signals during volatile time durations and avoid trading the whole day. Signal usually gives good targets on those times.

12. If a GRG or RGR pattern appears on a daily timeframe then this is our time to go big.

13. Minimum Risk to Reward should be 1:2 and for longer targets can be 1:4 to 1:10.

14. Trade with small lot size. Money management will happen automatically.

15. With small lot size and correct Risk-Reward we can be very profitable. Don't trade with big lot size.

16. Stay in the market for longer and collect points not money.

17. Very imp - Watch market and learn to generate a market view.

18. Very imp - Only 3 type of candles are needed in trading -

Strong Bullish (Big Green candle), Strong Bearish (Big Red candle),

Hammer (it is Strong Bullish), Inverse Hammer (it is Strong Bearish)

and Doji (indecision or confusion).

If on daily timeframe I see Strong Bullish candle previous day then I am biased to the upside the next day, if I see Strong Bearish candle the previous day then I am biased to the downside the next day, if I see Doji on the previous day then I am cautious the next day, if there are back to back Dojis forming in daily or weekly then I am preparing for big move so time to go big once I get the signal.

19. Most Important Candlestick pattern - Bullish and Bearish Engulfing

20. The only Chart patterns I need -

a) Falling Wedge/Channel Bullish Pattern Uptrend or Bull Flag - Buying - Forming over a couple days for intraday and forming over a couple of weeks for swing

b) Falling Wedge/Channel Bullish Pattern Downtrend or Falling Channel - Buying

c) Rising Wedge Bearish Pattern Uptrend or Rising Channel - Selling

d) Rising Wedge Bearish Pattern Downtrend or Bear flag - Selling

e) Head and Shoulder - Over a longer period not for intraday. In 15 min takes few days and for swing 1hr or 4h or daily can take few days

f) M and W pattern - Reversal Patterns - They form within the above 4 patterns, usually resulting in the break of trend line

21. How Gaps work -

a) Small Gap up in Uptrend - Market can fill the gap and reverse. The perception is that people are buying. If previous day candle was Strong Bullish then market view is up.

b) Big Gap up in Uptrend - Not news driven - Profit booking will come but may not fill the entire gap

c) Big Gap up in Uptrend - News driven, war related, tax, interest rate - Market can keep going up without stopping.

c) Flat opening in Uptrend - Big chance of market going up. If previous day candle was Strong Bullish then view is upwards, if it was Doji then still upwards.

d) Gap down in Uptrend - Market is surprised. After going down initially it can go up

e) Small Gap down in Downtrend - Market can fill the gap and keep moving down. If previous day candle was Strong Bearish then view is still down.

f) Flat opening in Downtrend - View is down, short today.

g) Big Gap down in Downtrend - Profit booking and foolish buying will come but market view is still down.

h) Gap down with News - Volatility, sideways then down.

i) Gap Up in Downtrend - Can move up - Price can move up during 2/3rd of the day and End of the day revert and close in red.

22. Go big on bearish days for option traders. Puts are better bought and Calls are better sold.

23. Cluster of green signals can lead to bigger move on the upside and vice versa for red signals.

24. Most of this is what I learned from successful traders (from the top 2%) only the indicator is mine.

BOCS Channel Scalper Strategy - Automated Mean Reversion System# BOCS Channel Scalper Strategy - Automated Mean Reversion System

## WHAT THIS STRATEGY DOES:

This is an automated mean reversion trading strategy that identifies consolidation channels through volatility analysis and executes scalp trades when price enters entry zones near channel boundaries. Unlike breakout strategies, this system assumes price will revert to the channel mean, taking profits as price bounces back from extremes. Position sizing is fully customizable with three methods: fixed contracts, percentage of equity, or fixed dollar amount. Stop losses are placed just outside channel boundaries with take profits calculated either as fixed points or as a percentage of channel range.

## KEY DIFFERENCE FROM ORIGINAL BOCS:

**This strategy is designed for traders seeking higher trade frequency.** The original BOCS indicator trades breakouts OUTSIDE channels, waiting for price to escape consolidation before entering. This scalper version trades mean reversion INSIDE channels, entering when price reaches channel extremes and betting on a bounce back to center. The result is significantly more trading opportunities:

- **Original BOCS**: 1-3 signals per channel (only on breakout)

- **Scalper Version**: 5-15+ signals per channel (every touch of entry zones)

- **Trade Style**: Mean reversion vs trend following

- **Hold Time**: Seconds to minutes vs minutes to hours

- **Best Markets**: Ranging/choppy conditions vs trending breakouts

This makes the scalper ideal for active day traders who want continuous opportunities within consolidation zones rather than waiting for breakout confirmation. However, increased trade frequency also means higher commission costs and requires tighter risk management.

## TECHNICAL METHODOLOGY:

### Price Normalization Process:

The strategy normalizes price data to create consistent volatility measurements across different instruments and price levels. It calculates the highest high and lowest low over a user-defined lookback period (default 100 bars). Current close price is normalized using: (close - lowest_low) / (highest_high - lowest_low), producing values between 0 and 1 for standardized volatility analysis.

### Volatility Detection:

A 14-period standard deviation is applied to the normalized price series to measure price deviation from the mean. Higher standard deviation values indicate volatility expansion; lower values indicate consolidation. The strategy uses ta.highestbars() and ta.lowestbars() to identify when volatility peaks and troughs occur over the detection period (default 14 bars).

### Channel Formation Logic:

When volatility crosses from a high level to a low level (ta.crossover(upper, lower)), a consolidation phase begins. The strategy tracks the highest and lowest prices during this period, which become the channel boundaries. Minimum duration of 10+ bars is required to filter out brief volatility spikes. Channels are rendered as box objects with defined upper and lower boundaries, with colored zones indicating entry areas.

### Entry Signal Generation:

The strategy uses immediate touch-based entry logic. Entry zones are defined as a percentage from channel edges (default 20%):

- **Long Entry Zone**: Bottom 20% of channel (bottomBound + channelRange × 0.2)

- **Short Entry Zone**: Top 20% of channel (topBound - channelRange × 0.2)

Long signals trigger when candle low touches or enters the long entry zone. Short signals trigger when candle high touches or enters the short entry zone. This captures mean reversion opportunities as price reaches channel extremes.

### Cooldown Filter:

An optional cooldown period (measured in bars) prevents signal spam by enforcing minimum spacing between consecutive signals. If cooldown is set to 3 bars, no new long signal will fire until 3 bars after the previous long signal. Long and short cooldowns are tracked independently, allowing both directions to signal within the same period.

### ATR Volatility Filter:

The strategy includes a multi-timeframe ATR filter to avoid trading during low-volatility conditions. Using request.security(), it fetches ATR values from a specified timeframe (e.g., 1-minute ATR while trading on 5-minute charts). The filter compares current ATR to a user-defined minimum threshold:

- If ATR ≥ threshold: Trading enabled

- If ATR < threshold: No signals fire

This prevents entries during dead zones where mean reversion is unreliable due to insufficient price movement.

### Take Profit Calculation:

Two TP methods are available:

**Fixed Points Mode**:

- Long TP = Entry + (TP_Ticks × syminfo.mintick)

- Short TP = Entry - (TP_Ticks × syminfo.mintick)

**Channel Percentage Mode**:

- Long TP = Entry + (ChannelRange × TP_Percent)

- Short TP = Entry - (ChannelRange × TP_Percent)

Default 50% targets the channel midline, a natural mean reversion target. Larger percentages aim for opposite channel edge.

### Stop Loss Placement:

Stop losses are placed just outside the channel boundary by a user-defined tick offset:

- Long SL = ChannelBottom - (SL_Offset_Ticks × syminfo.mintick)

- Short SL = ChannelTop + (SL_Offset_Ticks × syminfo.mintick)

This logic assumes channel breaks invalidate the mean reversion thesis. If price breaks through, the range is no longer valid and position exits.

### Trade Execution Logic:

When entry conditions are met (price in zone, cooldown satisfied, ATR filter passed, no existing position):

1. Calculate entry price at zone boundary

2. Calculate TP and SL based on selected method

3. Execute strategy.entry() with calculated position size

4. Place strategy.exit() with TP limit and SL stop orders

5. Update info table with active trade details

The strategy enforces one position at a time by checking strategy.position_size == 0 before entry.

### Channel Breakout Management:

Channels are removed when price closes more than 10 ticks outside boundaries. This tolerance prevents premature channel deletion from minor breaks or wicks, allowing the mean reversion setup to persist through small boundary violations.

### Position Sizing System:

Three methods calculate position size:

**Fixed Contracts**:

- Uses exact contract quantity specified in settings

- Best for futures traders (e.g., "trade 2 NQ contracts")

**Percentage of Equity**:

- position_size = (strategy.equity × equity_pct / 100) / close

- Dynamically scales with account growth

**Cash Amount**:

- position_size = cash_amount / close

- Maintains consistent dollar exposure regardless of price

## INPUT PARAMETERS:

### Position Sizing:

- **Position Size Type**: Choose Fixed Contracts, % of Equity, or Cash Amount

- **Number of Contracts**: Fixed quantity per trade (1-1000)

- **% of Equity**: Percentage of account to allocate (1-100%)

- **Cash Amount**: Dollar value per position ($100+)

### Channel Settings:

- **Nested Channels**: Allow multiple overlapping channels vs single channel

- **Normalization Length**: Lookback for high/low calculation (1-500, default 100)

- **Box Detection Length**: Period for volatility detection (1-100, default 14)

### Scalping Settings:

- **Enable Long Scalps**: Toggle long entries on/off

- **Enable Short Scalps**: Toggle short entries on/off

- **Entry Zone % from Edge**: Size of entry zone (5-50%, default 20%)

- **SL Offset (Ticks)**: Distance beyond channel for stop (1+, default 5)

- **Cooldown Period (Bars)**: Minimum spacing between signals (0 = no cooldown)

### ATR Filter:

- **Enable ATR Filter**: Toggle volatility filter on/off

- **ATR Timeframe**: Source timeframe for ATR (1, 5, 15, 60 min, etc.)

- **ATR Length**: Smoothing period (1-100, default 14)

- **Min ATR Value**: Threshold for trade enablement (0.1+, default 10.0)

### Take Profit Settings:

- **TP Method**: Choose Fixed Points or % of Channel

- **TP Fixed (Ticks)**: Static distance in ticks (1+, default 30)

- **TP % of Channel**: Dynamic target as channel percentage (10-100%, default 50%)

### Appearance:

- **Show Entry Zones**: Toggle zone labels on channels

- **Show Info Table**: Display real-time strategy status

- **Table Position**: Corner placement (Top Left/Right, Bottom Left/Right)

- **Color Settings**: Customize long/short/TP/SL colors

## VISUAL INDICATORS:

- **Channel boxes** with semi-transparent fill showing consolidation zones

- **Colored entry zones** labeled "LONG ZONE ▲" and "SHORT ZONE ▼"

- **Entry signal arrows** below/above bars marking long/short entries

- **Active TP/SL lines** with emoji labels (⊕ Entry, 🎯 TP, 🛑 SL)

- **Info table** showing position status, channel state, last signal, entry/TP/SL prices, and ATR status

## HOW TO USE:

### For 1-3 Minute Scalping (NQ/ES):

- ATR Timeframe: "1" (1-minute)

- ATR Min Value: 10.0 (for NQ), adjust per instrument

- Entry Zone %: 20-25%

- TP Method: Fixed Points, 20-40 ticks

- SL Offset: 5-10 ticks

- Cooldown: 2-3 bars

- Position Size: 1-2 contracts

### For 5-15 Minute Day Trading:

- ATR Timeframe: "5" or match chart

- ATR Min Value: Adjust to instrument (test 8-15 for NQ)

- Entry Zone %: 20-30%

- TP Method: % of Channel, 40-60%

- SL Offset: 5-10 ticks

- Cooldown: 3-5 bars

- Position Size: Fixed contracts or 5-10% equity

### For 30-60 Minute Swing Scalping:

- ATR Timeframe: "15" or "30"

- ATR Min Value: Lower threshold for broader market

- Entry Zone %: 25-35%

- TP Method: % of Channel, 50-70%

- SL Offset: 10-15 ticks

- Cooldown: 5+ bars or disable

- Position Size: % of equity recommended

## BACKTEST CONSIDERATIONS:

- Strategy performs best in ranging, mean-reverting markets

- Strong trending markets produce more stop losses as price breaks channels

- ATR filter significantly reduces trade count but improves quality during low volatility

- Cooldown period trades signal quantity for signal quality

- Commission and slippage materially impact sub-5-minute timeframe performance

- Shorter timeframes require tighter entry zones (15-20%) to catch quick reversions

- % of Channel TP adapts better to varying channel sizes than fixed points

- Fixed contract sizing recommended for consistent risk per trade in futures

**Backtesting Parameters Used**: This strategy was developed and tested using realistic commission and slippage values to provide accurate performance expectations. Recommended settings: Commission of $1.40 per side (typical for NQ futures through discount brokers), slippage of 2 ticks to account for execution delays on fast-moving scalp entries. These values reflect real-world trading costs that active scalpers will encounter. Backtest results without proper cost simulation will significantly overstate profitability.

## COMPATIBLE MARKETS:

Works on any instrument with price data including stock indices (NQ, ES, YM, RTY), individual stocks, forex pairs (EUR/USD, GBP/USD), cryptocurrency (BTC, ETH), and commodities. Volume-based features require data feed with volume information but are optional for core functionality.

## KNOWN LIMITATIONS:

- Immediate touch entry can fire multiple times in choppy zones without adequate cooldown

- Channel deletion at 10-tick breaks may be too aggressive or lenient depending on instrument tick size

- ATR filter from lower timeframes requires higher-tier TradingView subscription (request.security limitation)

- Mean reversion logic fails in strong breakout scenarios leading to stop loss hits

- Position sizing via % of equity or cash amount calculates based on close price, may differ from actual fill price

- No partial closing capability - full position exits at TP or SL only

- Strategy does not account for gap openings or overnight holds

## RISK DISCLOSURE:

Trading involves substantial risk of loss. Past performance does not guarantee future results. This strategy is for educational purposes and backtesting only. Mean reversion strategies can experience extended drawdowns during trending markets. Stop losses may not fill at intended levels during extreme volatility or gaps. Thoroughly test on historical data and paper trade before risking real capital. Use appropriate position sizing and never risk more than you can afford to lose. Consider consulting a licensed financial advisor before making trading decisions. Automated trading systems can malfunction - monitor all live positions actively.

## ACKNOWLEDGMENT & CREDITS:

This strategy is built upon the channel detection methodology created by **AlgoAlpha** in the "Smart Money Breakout Channels" indicator. Full credit and appreciation to AlgoAlpha for pioneering the normalized volatility approach to identifying consolidation patterns. The core channel formation logic using normalized price standard deviation is AlgoAlpha's original contribution to the TradingView community.

Enhancements to the original concept include: mean reversion entry logic (vs breakout), immediate touch-based signals, multi-timeframe ATR volatility filtering, flexible position sizing (fixed/percentage/cash), cooldown period filtering, dual TP methods (fixed points vs channel percentage), automated strategy execution with exit management, and real-time position monitoring table.

Katz Calypso Indicator (Refactored)Overview

The Katz Calypso Indicator is a comprehensive momentum oscillator designed to identify potential entry and exit points in the market. At its core, it uses the True Strength Index (TSI) to gauge the strength and direction of a trend. To enhance signal accuracy and reduce false positives, the indicator integrates several optional filters, including the Waddah Attar Explosion, an EMA filter, and an ATR filter. It also provides an optional RVGI-based exit signal system.

This tool is designed to provide a clear, visual representation of market momentum, with customizable filters to adapt to various trading styles and market conditions.

How to Use the Indicator

The indicator is displayed in a separate pane below the main price chart.

TSI Line (Blue): This is the main oscillator line. Its position relative to the zero line indicates the overall trend bias (above 0 is bullish, below is bearish).

Signal Line (Red): A moving average of the TSI line. Crossovers between the TSI and Signal Line are the primary triggers for trade signals.

Zero Line: The centerline of the oscillator. A cross of the Zero Line can indicate a significant shift in momentum.

Overbought/Oversold Levels: These user-defined levels (defaulting to 65 and -65) help identify potential exhaustion points in a trend, which can be used for taking profits.

On-Chart Signals: The indicator plots shapes directly on the chart to make signals easy to spot:

Green Triangles (Up): Indicate long entry or continuation signals.

Red Triangles (Down): Indicate short entry or continuation signals.

Yellow Triangles: Suggest taking profits.

Maroon/Lime Triangles: Indicate an exit based on a signal cross (like RVGI or the Zero Line).

Trading Rules

Long Trade Rules

Entry: A long trade is signaled when ALL of the following conditions are met:

The blue TSI Line crosses above the red Signal Line.

The blue TSI Line is above the 0 Zero Line.

All enabled filters (Waddah Attar, EMA, ATR) confirm bullish conditions.

A green triangle labeled "Long" will appear below the price.

Exit (Take Profit): A take-profit signal for a long trade is generated when either of these occurs:

The TSI Line crosses below the Overbought level.

The TSI Line crosses back below the Signal Line while still above zero.

A yellow triangle labeled "TPL" (Take Profit Long) will appear above the price.

Exit (Stop/Reverse): A signal to exit a long trade is generated when either of these occurs:

The TSI Line crosses below the 0 Zero Line.

The RVGI Exit filter is enabled and generates a bearish crossover signal.

A maroon triangle labeled "Exit Long" will appear above the price.

Short Trade Rules

Entry: A short trade is signaled when ALL of the following conditions are met:

The blue TSI Line crosses below the red Signal Line.

The blue TSI Line is below the 0 Zero Line.

All enabled filters (Waddah Attar, EMA, ATR) confirm bearish conditions.

A red triangle labeled "Short" will appear above the price.

Exit (Take Profit): A take-profit signal for a short trade is generated when either of these occurs:

The TSI Line crosses above the Oversold level.

The TSI Line crosses back above the Signal Line while still below zero.

A yellow triangle labeled "TPS" (Take Profit Short) will appear below the price.

Exit (Stop/Reverse): A signal to exit a short trade is generated when either of these occurs:

The TSI Line crosses above the 0 Zero Line.

The RVGI Exit filter is enabled and generates a bullish crossover signal.

A lime green triangle labeled "Exit Short" will appear below the price.

Optional Filters

You can enable or disable these filters in the indicator's settings to fine-tune its sensitivity.

Waddah Attar Explosion Filter: This filter measures trend strength and volatility. When enabled, it ensures that entries are only taken during periods of strong, confirmed momentum, helping to avoid sideways or choppy markets.

EMA Price Filter: A classic trend filter. When enabled, it will only allow long entries if the price is above the specified Exponential Moving Average and short entries only if the price is below it.

ATR Filter: This acts as a volatility-based filter to prevent chasing a move. It helps ensure that you are not entering a long trade when the price has already moved too far above its EMA, or vice-versa for a short trade.

RVGI Exit Filter: The Relative Vigor Index (RVGI) is used here exclusively as an exit signal. When enabled, a crossover of the RVGI and its signal line can provide an earlier exit signal before the TSI crosses the zero line, potentially locking in profits sooner.

Disclaimer: This indicator is provided for educational and informational purposes only. It is not financial advice. Trading carries a high level of risk, and you can lose more than your initial investment. You should use this indicator at your own risk and discretion. Always conduct your own research and consider your risk tolerance before making any trading decisions.

Hilly's Advanced Crypto Scalping Strategy - 5 Min ChartTo determine the "best" input parameters for the Advanced Crypto Scalping Strategy on a 5-minute chart, we need to consider the goals of optimizing for profitability, minimizing false signals, and adapting to the volatile nature of cryptocurrencies. The default parameters in the script are a starting point, but the optimal values depend on the specific cryptocurrency pair, market conditions, and your risk tolerance. Below, I'll provide recommended input values based on common practices in crypto scalping, along with reasoning for each parameter. I’ll also suggest how to fine-tune them using TradingView’s backtesting and optimization tools.

Recommended Input Parameters

These values are tailored for a 5-minute chart for liquid cryptocurrencies like BTC/USD or ETH/USD on exchanges like Binance or Coinbase. They aim to balance signal frequency and accuracy for day trading.

Fast EMA Length (emaFastLen): 9

Reasoning: A 9-period EMA is commonly used in scalping to capture short-term price movements while remaining sensitive to recent price action. It reacts faster than the default 10, aligning with the 5-minute timeframe.

Slow EMA Length (emaSlowLen): 21

Reasoning: A 21-period EMA provides a good balance for identifying the broader trend on a 5-minute chart. It’s slightly longer than the default 20 to reduce noise while confirming the trend direction.

RSI Length (rsiLen): 14

Reasoning: The default 14-period RSI is a standard choice for momentum analysis. It works well for detecting overbought/oversold conditions without being too sensitive on short timeframes.

RSI Overbought (rsiOverbought): 75

Reasoning: Raising the overbought threshold to 75 (from 70) reduces false sell signals in strong bullish trends, which are common in crypto markets.

RSI Oversold (rsiOversold): 25

Reasoning: Lowering the oversold threshold to 25 (from 30) filters out weaker buy signals, ensuring entries occur during stronger reversals.

MACD Fast Length (macdFast): 12

Reasoning: The default 12-period fast EMA for MACD is effective for capturing short-term momentum shifts in crypto, aligning with scalping goals.

MACD Slow Length (macdSlow): 26

Reasoning: The default 26-period slow EMA is a standard setting that works well for confirming momentum trends without lagging too much.

MACD Signal Smoothing (macdSignal): 9

Reasoning: The default 9-period signal line is widely used and provides a good balance for smoothing MACD crossovers on a 5-minute chart.

Bollinger Bands Length (bbLen): 20

Reasoning: The default 20-period Bollinger Bands are effective for identifying volatility breakouts, which are key for scalping in crypto markets.

Bollinger Bands Multiplier (bbMult): 2.0

Reasoning: A 2.0 multiplier is standard and captures most price action within the bands. Increasing it to 2.5 could reduce signals but improve accuracy in highly volatile markets.

Stop Loss % (slPerc): 0.8%

Reasoning: A tighter stop loss of 0.8% (from 1.0%) suits the high volatility of crypto, helping to limit losses on false breakouts while keeping risk manageable.

Take Profit % (tpPerc): 1.5%

Reasoning: A 1.5% take-profit target (from 2.0%) aligns with scalping’s goal of capturing small, frequent gains. Crypto markets often see quick reversals, so a smaller target increases the likelihood of hitting profits.

Use Candlestick Patterns (useCandlePatterns): True

Reasoning: Enabling candlestick patterns (e.g., engulfing, hammer) adds confirmation to signals, reducing false entries in choppy markets.

Use Volume Filter (useVolumeFilter): True

Reasoning: The volume filter ensures signals occur during high-volume breakouts, which are more likely to sustain in crypto markets.

Signal Arrow Size (signalSize): 2.0

Reasoning: Increasing the arrow size to 2.0 (from 1.5) makes buy/sell signals more visible on the chart, especially on smaller screens or volatile price action.

Background Highlight Transparency (bgTransparency): 85

Reasoning: A slightly higher transparency (85 from 80) keeps the background highlights subtle but visible, avoiding chart clutter.

How to Apply These Parameters

Copy the Script: Use the Pine Script provided in the previous response.

Paste in TradingView: Open TradingView, go to the Pine Editor, paste the code, and click "Add to Chart."

Set Parameters: In the strategy settings, manually input the recommended values above or adjust them via the input fields.

Test on a 5-Minute Chart: Apply the strategy to a liquid crypto pair (e.g., BTC/USDT, ETH/USDT) on a 5-minute chart.

Fine-Tuning for Optimal Performance

To find the absolute best parameters for your specific trading pair and market conditions, use TradingView’s Strategy Tester and optimization features:

Backtesting:

Run the strategy on historical data for your chosen pair (e.g., BTC/USDT on Binance).

Check metrics like Net Profit, Profit Factor, Win Rate, and Max Drawdown in the Strategy Tester.

Focus on a sample period of at least 1–3 months to capture various market conditions (bull, bear, sideways).

Parameter Optimization:

In the Strategy Tester, click the settings gear next to the strategy name.

Enable optimization for key inputs like emaFastLen (test range: 7–12), emaSlowLen (15–25), slPerc (0.5–1.5), and tpPerc (1.0–3.0).

Run the optimization to find the combination with the highest net profit or best Sharpe ratio, but avoid over-optimization (curve-fitting) by testing on out-of-sample data.

Market-Specific Adjustments: