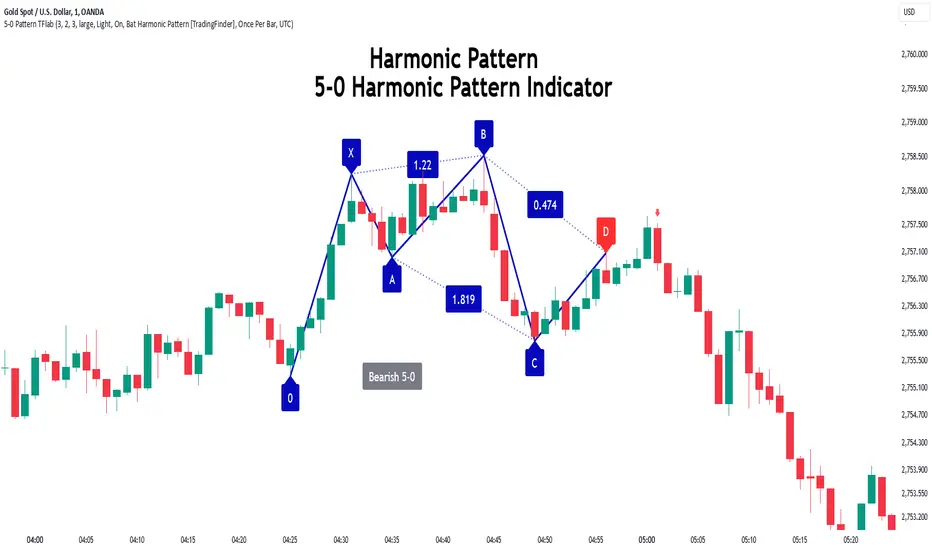

5-0 Harmonic Pattern [TradingFinder] 0XABCD 50 Harmonic Detector🔵 Introduction

Harmonic patterns are a powerful tool in technical analysis, widely used to detect reversal points and trend changes. Among these, the 5-0 Harmonic Pattern stands out due to its reliance on specific Fibonacci ratios—1.13, 1.618, 2.24, and 0.45 to 0.55—anchored at points 0, X, A, B, C, and D. This pattern provides a structured approach for identifying critical buy and sell points, helping traders achieve optimal entry and exit levels in volatile markets.

This 5-0 Harmonic Pattern indicator automatically detects and marks bullish and bearish formations on the chart, offering precise trading signals based on established harmonic ratios. With its dynamic signals, the 5-0 pattern enables traders to anticipate market movements and capitalize on favorable price trends.

Especially in fast-moving markets, harmonic patterns, particularly the 5-0 Harmonic Pattern, equip traders with an essential framework for identifying reversal opportunities and refining their trading strategies.

Bullish 5-0 Pattern :

Bearish 5-0 Pattern :

🔵 How to Use

The 5-0 Harmonic Pattern indicator is designed to automatically mark the key levels of the harmonic structure: 0, X, A, B, C, and D. By doing so, it detects both bullish and bearish patterns and helps traders recognize optimal entry and exit points.

Formed through specific Fibonacci levels, this pattern signals potential shifts in trend direction, giving traders critical insights for managing entries and exits effectively. The tool proves valuable in high-volatility settings, enabling traders to leverage these signals for refined decision-making.

🟣 Bullish 5-0 Pattern

A bullish 5-0 pattern materializes when Fibonacci levels indicate a potential price reversal to the upside. With points 0, X, A, B, C, and D in alignment, the indicator highlights this upward momentum by displaying a green arrow as a buy signal on the chart. This marking provides a clear entry point, indicating that prices are likely to rise, making it a prime moment for traders to enter long positions.

Additionally, the bullish 5-0 pattern is equipped with tools for traders to set stop-loss and take-profit points based on harmonic lines within the pattern, which represent support and resistance levels. Using these dynamic points, traders can create a more effective risk-reward setup while following the bullish signals in a standalone harmonic strategy.

🟣 Bearish 5-0 Pattern

The bearish 5-0 pattern functions similarly but signals a likely downturn. This pattern emerges when Fibonacci ratios align at points 0, X, A, B, C, and D, predicting a reversal downward. The indicator generates a sell signal, marked by a red arrow, prompting traders to exit long positions or initiate short trades to capitalize on falling prices.

Traders can utilize this bearish pattern for defining exit strategies and setting key levels for stop-loss and take-profit orders. The bearish 5-0 pattern enhances traders’ abilities to gauge critical price levels and manage trade risk effectively, especially in volatile markets. For traders focused on profiting from downward trends, this indicator serves as a powerful tool for timely entries and exits.

🔵 Setting

🟣 Logical Setting

ZigZag Pivot Period : You can adjust the period so that the harmonic patterns are adjusted according to the pivot period you want. This factor is the most important parameter in pattern recognition.

Show Valid Forma t: If this parameter is on "On" mode, only patterns will be displayed that they have exact format and no noise can be seen in them. If "Off" is, the patterns displayed that maybe are noisy and do not exactly correspond to the original pattern.

Show Formation Last Pivot Confirm : if Turned on, you can see this ability of patterns when their last pivot is formed. If this feature is off, it will see the patterns as soon as they are formed. The advantage of this option being clear is less formation of fielded patterns, and it is accompanied by the latest pattern seeing and a sharp reduction in reward to risk.

Period of Formation Last Pivot : Using this parameter you can determine that the last pivot is based on Pivot period.

🟣 Genaral Setting

Show : Enter "On" to display the template and "Off" to not display the template.

Color : Enter the desired color to draw the pattern in this parameter.

LineWidth : You can enter the number 1 or numbers higher than one to adjust the thickness of the drawing lines. This number must be an integer and increases with increasing thickness.

LabelSize : You can adjust the size of the labels by using the "size.auto", "size.tiny", "size.smal", "size.normal", "size.large" or "size.huge" entries.

🟣 Alert Setting

Alert : On / Off

Message Frequency : This string parameter defines the announcement frequency. Choices include: "All" (activates the alert every time the function is called), "Once Per Bar" (activates the alert only on the first call within the bar), and "Once Per Bar Close" (the alert is activated only by a call at the last script execution of the real-time bar upon closing). The default setting is "Once per Bar".

Show Alert Time by Time Zone : The date, hour, and minute you receive in alert messages can be based on any time zone you choose. For example, if you want New York time, you should enter "UTC-4". This input is set to the time zone "UTC" by default.

Conclusion

The 5-0 Harmonic Pattern indicator serves as a robust solution for technical analysts and traders looking to pinpoint market reversal points. By automatically recognizing 5-0 patterns and generating buy and sell signals based on Fibonacci ratios, this tool supports precise trend analysis and entry/exit timing. The indicator’s adjustable alerts, color themes, and pattern toggles allow for comprehensive customization, ensuring alignment with individual trading strategies.

Harmonic patterns, especially the 5-0 Harmonic Pattern, guide traders in identifying high-accuracy entry and exit points, thus aiding in more informed trading decisions. By combining Fibonacci ratio analysis with real-time signal updates, this indicator provides a well-rounded approach for risk management and capitalizing on trading opportunities. Professional traders can harness this tool to enhance technical analysis precision and capitalize on price trends effectively, maximizing profitability in both bullish and bearish markets.

Cerca negli script per "profit"

Advanced Position Management [Mr_Rakun]Advanced Position Management

This Pine Script code is for a strategy titled "Advanced Position Management," aimed at effective trade execution and management using multiple take profit levels, trailing stop loss, and dynamic position sizing.

Take Profit Levels: It defines up to three take profit (TP) levels, allowing partial position exits at different price thresholds. The take profit levels and their respective quantities are adjustable using inputs.

Stop Loss and Trailing Stop: The script implements an initial stop loss based on a percentage from the entry price. Additionally, it features a trailing stop that moves based on either a percentage or previous TP levels, dynamically adjusting to maximize gains while protecting profits.

Position Size: The position size is customizable and based on USD value, allowing the trader to manage risk more effectively.

Advantages:

Flexibility: Multiple take profit levels and a dynamic stop loss system allow traders to lock in profits while keeping the position open for further gains.

Risk Management: The initial stop loss and trailing stop help to limit losses and protect profits as the trade moves in the desired direction.

Automation: Once the strategy is deployed, it automatically handles entry, exit, and stop management, reducing the need for constant monitoring.

------ TR ------

Gelişmiş Pozisyon Yönetimi

Bu Pine Script kodu, Gelişmiş Pozisyon Yönetimi için kendi stratejilerinize kolayca entegre edeceğiniz bir risk yönetimidir. Çoklu kâr al seviyeleri, takip eden stop-loss ve dinamik pozisyon büyüklüğü kullanarak işlem yürütme ve yönetiminde etkilidir.

Gelişmiş Pozisyon Yönetimi

Kâr Alma Seviyeleri;

Kod, pozisyonların farklı fiyat seviyelerinde kısmi kapatılmasını sağlayan üç farklı kâr alma (TP) seviyesini tanımlar. Bu kâr alma seviyeleri ve ilgili miktarları, girişlerle ayarlanabilir.

Stop Loss ve Takip Eden Stop;

Koda, giriş fiyatından bir yüzdeye dayalı olarak başlangıçta stop-loss uygulanır. Ayrıca, fiyat hareketine göre kendini ayarlayan takip eden bir stop-loss sistemi bulunur. Ayrıca TP seviyelerini takip eden stop loss özelliğide vardır.

Avantajları:

Esneklik;

Çoklu kâr alma seviyeleri ve dinamik stop-loss sistemi, trader'ların kazançlarını kilitleyip aynı zamanda pozisyonu açık tutmalarına olanak tanır.

Risk Yönetimi;

Başlangıç stop-loss ve takip eden stop, zararı sınırlamaya ve kazançları korumaya yardımcı olur.

Otomasyon;

Strateji bir kez devreye alındığında, giriş, çıkış ve stop yönetimi otomatik olarak gerçekleştirilir, bu da sürekli takip ihtiyacını azaltır.

$TUBR: Stop Loss IndicatorATR-Based Stop Loss Indicator for TradingView by The Ultimate Bull Run Community: TUBR

**Overview**

The ATR-Based Stop Loss Indicator is a custom tool designed for traders using TradingView. It helps you determine optimal stop loss levels by leveraging the Average True Range (ATR), a popular measure of market volatility. By adapting to current market conditions, this indicator aims to minimize premature stop-outs and enhance your risk management strategy.

---

**Key Features**

- **Dynamic Stop Loss Levels**: Calculates stop loss prices based on the ATR, providing both long and short stop loss suggestions.

- **Customizable Parameters**: Adjust the ATR period, multiplier, and smoothing method to suit your trading style and the specific instrument you're trading.

- **Visual Aids**: Plots stop loss lines directly on your chart for easy visualization.

- **Alerts and Notifications** (Optional): Set up alerts to notify you when the price approaches or hits your stop loss levels.

---

**Understanding the Indicator**

1. **Average True Range (ATR)**:

- **What It Is**: ATR measures market volatility by calculating the average range between high and low prices over a specified period.

- **Why It's Useful**: A higher ATR indicates higher volatility, which can help you set stop losses that accommodate market fluctuations.

2. **ATR Multiplier**:

- **Purpose**: Determines how far your stop loss is placed from the current price based on the ATR.

- **Example**: An ATR multiplier of 1.5 means the stop loss is set at 1.5 times the ATR away from the current price.

3. **Smoothing Methods**:

- **Options**: Choose from RMA (default), SMA, EMA, WMA, or Hull MA.

- **Effect**: Different smoothing methods can make the ATR more responsive or smoother, affecting where the stop loss is placed.

---

**How the Indicator Works**

- **Long Stop Loss Calculation**:

- **Formula**: `Long Stop Loss = Close Price - (ATR * ATR Multiplier)`

- **Purpose**: For long positions, the stop loss is set below the current price to protect against downside risk.

- **Short Stop Loss Calculation**:

- **Formula**: `Short Stop Loss = Close Price + (ATR * ATR Multiplier)`

- **Purpose**: For short positions, the stop loss is set above the current price to protect against upside risk.

- **Plotting on the Chart**:

- **Green Line**: Represents the suggested stop loss level for long positions.

- **Red Line**: Represents the suggested stop loss level for short positions.

---

**How to Use the Indicator**

1. **Adding the Indicator to Your Chart**:

- **Step 1**: Copy the PineScript code of the indicator.

- **Step 2**: In TradingView, click on **Pine Editor** at the bottom of the platform.

- **Step 3**: Paste the code into the editor and click **Add to Chart**.

- **Step 4**: The indicator will appear on your chart with the default settings.

2. **Adjusting the Settings**:

- **ATR Period**:

- **Definition**: Number of periods over which the ATR is calculated.

- **Adjustment**: Increase for a smoother ATR; decrease for a more responsive ATR.

- **ATR Multiplier**:

- **Definition**: Factor by which the ATR is multiplied to set the stop loss distance.

- **Adjustment**: Increase to widen the stop loss (less likely to be hit); decrease to tighten the stop loss.

- **Smoothing Method**:

- **Options**: RMA, SMA, EMA, WMA, Hull MA.

- **Adjustment**: Experiment to see which method aligns best with your trading strategy.

- **Display Options**:

- **Show Long Stop Loss**: Toggle to display or hide the long stop loss line.

- **Show Short Stop Loss**: Toggle to display or hide the short stop loss line.

3. **Interpreting the Indicator**:

- **Long Positions**:

- **Action**: Set your stop loss at the value indicated by the green line when entering a long trade.

- **Short Positions**:

- **Action**: Set your stop loss at the value indicated by the red line when entering a short trade.

- **Adjusting Stop Losses**:

- **Trailing Stops**: You may choose to adjust your stop loss over time, moving it in the direction of your trade as the ATR-based stop loss levels change.

4. **Implementing in Your Trading Strategy**:

- **Risk Management**:

- **Position Sizing**: Use the stop loss distance to calculate your position size based on your risk tolerance.

- **Consistency**: Apply the same settings consistently to maintain discipline.

- **Combining with Other Indicators**:

- **Enhance Decision-Making**: Use in conjunction with trend indicators, support and resistance levels, or other technical analysis tools.

- **Alerts Setup** (If included in the code):

- **Purpose**: Receive notifications when the price approaches or hits your stop loss level.

- **Configuration**: Set up alerts in TradingView based on the alert conditions defined in the indicator.

---

**Benefits of Using This Indicator**

- **Adaptive Risk Management**: By accounting for current market volatility, the indicator helps prevent setting stop losses that are too tight or too wide.

- **Minimize Premature Stop-Outs**: Reduces the likelihood of being stopped out due to normal price fluctuations.

- **Flexibility**: Customizable settings allow you to tailor the indicator to different trading instruments and timeframes.

- **Visualization**: Clear visual representation of stop loss levels aids in quick decision-making.

---

**Things to Consider**

- **Market Conditions**:

- **High Volatility**: Be cautious as ATR values—and thus stop loss distances—can widen, increasing potential losses.

- **Low Volatility**: Tighter stop losses may increase the chance of being stopped out by minor price movements.

- **Backtesting and Optimization**:

- **Historical Analysis**: Test the indicator on past data to evaluate its effectiveness and adjust settings accordingly.

- **Continuous Improvement**: Regularly reassess and fine-tune the parameters to adapt to changing market conditions.

- **Risk Per Trade**:

- **Alignment with Risk Tolerance**: Ensure the stop loss level keeps potential losses within your acceptable risk per trade (e.g., 1-2% of your trading capital).

- **Emotional Discipline**:

- **Stick to Your Plan**: Avoid making impulsive changes to your stop loss levels based on emotions rather than analysis.

---

**Example Usage Scenario**

1. **Setting Up a Long Trade**:

- **Entry Price**: $100

- **ATR Value**: $2

- **ATR Multiplier**: 1.5

- **Calculated Stop Loss**: $100 - ($2 * 1.5) = $97

- **Action**: Place a stop loss order at $97.

2. **During the Trade**:

- **Price Increases to $105**

- **ATR Remains at $2**

- **New Stop Loss Level**: $105 - ($2 * 1.5) = $102

- **Action**: Move your stop loss up to $102 to lock in profits.

---

**Final Tips**

- **Documentation**: Keep a trading journal to record your trades, stop loss levels, and observations for future reference.

- **Education**: Continuously educate yourself on risk management and technical analysis to enhance your trading skills.

- **Support**: Engage with trading communities or seek professional advice if you're unsure about implementing the indicator effectively.

---

**Conclusion**

The ATR-Based Stop Loss Indicator is a valuable tool for traders looking to enhance their risk management by setting stop losses that adapt to market volatility. By integrating this indicator into your trading routine, you can improve your ability to protect capital and potentially increase profitability. Remember to use it as part of a comprehensive trading strategy, and always adhere to sound risk management principles.

---

**How to Access the Indicator**

To start using the ATR-Based Stop Loss Indicator, follow these steps:

1. **Obtain the Code**: Copy the PineScript code provided for the indicator.

2. **Create a New Indicator in TradingView**:

- Open TradingView and navigate to the **Pine Editor**.

- Paste the code into the editor.

- Click **Save** and give your indicator a name.

3. **Add to Chart**: Click **Add to Chart** to apply the indicator to your current chart.

4. **Customize Settings**: Adjust the input parameters to suit your preferences and start integrating the indicator into your trading strategy.

---

**Disclaimer**

Trading involves significant risk, and it's possible to lose all your capital. The ATR-Based Stop Loss Indicator is a tool to aid in decision-making but does not guarantee profits or prevent losses. Always conduct your own analysis and consider seeking advice from a financial professional before making trading decisions.

Varanormal Mac N Cheez Strategy v1Mac N Cheez Strategy (Set a $200 Take profit Manually)

It's super cheesy. Strategy does the following:

Here's a detailed explanation of what the entire script does, including its key components, functionality, and purpose.

1. Strategy Setup and Input Parameters:

Strategy Name: The script is named "NQ Futures $200/day Strategy" and is set as an overlay, meaning all elements (like moving averages and signals) are plotted on the price chart.

Input Parameters:

fastLength: This sets the length of the fast moving average. The user can adjust this value, and it defaults to 9.

slowLength: This sets the length of the slow moving average. The user can adjust this value, and it defaults to 21.

dailyTarget: The daily profit target, which defaults to $200. If set to 0, this disables the daily profit target.

stopLossAmount: The fixed stop-loss amount per trade, defaulting to $100. This value is used to calculate how much you're willing to lose on a single trade.

trailOffset: This value sets the distance for a trailing stop. It helps protect profits by automatically adjusting the stop-loss as the price moves in your favor.

2. Calculating the Moving Averages:

fastMA: The fast moving average is calculated using the ta.sma() function on the close price with a period length of fastLength. The ta.sma() function calculates the simple moving average.

slowMA: The slow moving average is also calculated using ta.sma() but with the slowLength period.

These moving averages are used to determine trend direction and identify entry points.

3. Buy and Sell Signal Conditions:

longCondition: This is the buy condition. It occurs when the fast moving average crosses above the slow moving average. The script uses ta.crossover() to detect this crossover event.

shortCondition: This is the sell condition. It occurs when the fast moving average crosses below the slow moving average. The script uses ta.crossunder() to detect this crossunder event.

4. Executing Buy and Sell Orders:

Buy Orders: When the longCondition is true (i.e., fast MA crosses above slow MA), the script enters a long position using strategy.entry("Buy", strategy.long).

Sell Orders: When the shortCondition is true (i.e., fast MA crosses below slow MA), the script enters a short position using strategy.entry("Sell", strategy.short).

5. Setting Stop Loss and Trailing Stop:

Stop-Loss for Long Positions: The stop-loss is calculated as the entry price minus the stopLossAmount. If the price falls below this level, the trade is exited automatically.

Stop-Loss for Short Positions: The stop-loss is calculated as the entry price plus the stopLossAmount. If the price rises above this level, the short trade is exited.

Trailing Stop: The trail_offset dynamically adjusts the stop-loss as the price moves in favor of the trade, locking in profits while still allowing room for market fluctuations.

6. Conditional Daily Profit Target:

The script includes a daily profit target that automatically closes all trades once the total profit for the day reaches or exceeds the dailyTarget.

Conditional Logic:

If the dailyTarget is greater than 0, the strategy checks whether the strategy.netprofit (total profit for the day) has reached or exceeded the target.

If the strategy.netprofit >= dailyTarget, the script calls strategy.close_all(), closing all open trades for the day and stopping further trading.

If dailyTarget is set to 0, this logic is skipped, and the script continues trading without a daily profit target.

7. Plotting Moving Averages:

plot(fastMA): This plots the fast moving average as a blue line on the price chart.

plot(slowMA): This plots the slow moving average as a red line on the price chart. These help visualize the crossover points and the trend direction on the chart.

8. Plotting Buy and Sell Signals:

plotshape(): The script uses plotshape() to add visual markers when buy or sell conditions are met:

"Long Signal": When a buy condition (longCondition) is met, a green marker is plotted below the price bar with the label "Long".

"Short Signal": When a sell condition (shortCondition) is met, a red marker is plotted above the price bar with the label "Short".

These markers help traders quickly see when buy or sell signals occurred on the chart.

In addition, triangle markers are plotted:

Green Triangle: Indicates where a buy entry occurred.

Red Triangle: Indicates where a sell entry occurred.

Summary of What the Script Does:

Inputs: The script allows the user to adjust moving average lengths, daily profit targets, stop-loss amounts, and trailing stop offsets.

Signals: It generates buy and sell signals based on the crossovers of the fast and slow moving averages.

Order Execution: It executes long positions on buy signals and short positions on sell signals.

Stop-Loss and Trailing Stop: It sets dynamic stop-losses and uses a trailing stop to protect profits.

Daily Profit Target: The strategy stops trading for the day once the net profit reaches the daily target (unless the target is disabled by setting it to 0).

Visual Markers: It plots moving averages and buy/sell signals directly on the main price chart to aid in visual analysis.

This script is designed to trade based on moving average crossovers, with robust risk management features like stop-loss and trailing stops, along with an optional daily profit target to limit daily trading activity. Let me know if you need further clarification or want to adjust any specific part of the script!

Trailing Stop ProTrailing Stop Pro is a sophisticated TradingView indicator designed to enhance your trading strategy by dynamically managing trailing stops based on market volatility. This tool leverages the Average True Range (ATR) to adjust stop levels, providing traders with a robust mechanism to protect profits and minimize losses.

Key Features:

Dynamic Trailing Stops: Automatically adjusts stop levels using ATR, allowing for responsive and adaptive risk management.

Customizable Inputs: Tailor the indicator to your trading style with adjustable parameters such as ATR Length, ATR Multiplier, and Source Vector.

Visual Clarity: Distinct color settings for long and short stops, with adjustable line thickness and transparency, ensuring clear visualization on your charts.

Professional Grade: The "Pro" designation signifies advanced features suitable for both novice and experienced traders seeking reliable and efficient stop management.

How It Works:

To set up the indicator, begin by defining the Chrono Point, which specifies the exact time you want the trailing stop mechanism to activate. This allows for precise control over when your stops begin to trail. Next, set the Credit Unit as the initial entry price for your trade, serving as the baseline from which the trailing stops will adjust.

The indicator uses ATR-based adjustments to determine stop levels. Customize the sensitivity of the trailing stop by adjusting the ATR Length (default is 14) and ATR Multiplier (default is 0.5). A longer ATR length smooths out volatility, while a higher multiplier increases the distance of the stop from the price.

Select your Source Vector from "High/Low," "Close," or "Open" prices as the basis for stop calculation. This flexibility allows you to align the indicator with your preferred trading strategy. The indicator plots trailing stops directly on the chart, with color-coded lines indicating long (teal) and short (red) positions. You can adjust the line thickness and transparency for optimal visibility.

The Mission Status feature automatically detects whether the trade is long or short and adjusts the trailing stop accordingly. If the price hits the trailing stop, the trade is considered exited, and the indicator calculates the profit or loss percentage.

Benefits:

Risk Management: Protect your trades from adverse market movements while locking in profits as prices move favorably.

Automation: Reduce manual intervention with automatic stop adjustments, allowing you to focus on strategic decision-making.

User-Friendly Interface: Intuitive settings and clear visual cues make it easy to integrate into your existing trading workflow.

Conclusion:

Trailing Stop Pro is an essential tool for traders looking to enhance their risk management strategies with precision and ease. By automating the trailing stop process and providing clear visual feedback, this indicator empowers you to navigate the markets with confidence. Whether you're a seasoned trader or just starting, Trailing Stop Pro offers the functionality and flexibility needed to optimize your trading performance.

The Trailing Stop Pro indicator is a tool designed to assist traders in managing risk and optimizing their trading strategies. However, it should not be considered as financial advice or a guarantee of profitability. Trading involves significant risk, and it is possible to lose more than your initial investment. Users are encouraged to thoroughly test the indicator in a demo environment and consider their own financial situation and risk tolerance before using it in live trading. Past performance is not indicative of future results, and users should seek advice from a qualified financial advisor if needed.

AB_Bnf_Selling_5minThe Mathematical Level Reversal Strategy is designed to identify potential reversal points in the market using mathematical levels combined with price action on a 5-minute chart. This strategy is particularly effective for intraday traders who seek to capitalize on precise entry and exit points based on calculated levels rather than traditional indicators like moving averages or Bollinger Bands.

Creators' Mathematical Levels Explanation

Mathematical levels are predetermined price points calculated based on various factors such as previous high/low points, Fibonacci retracements, or other arithmetic calculations. These levels are used to anticipate areas where the price might reverse or experience significant support or resistance.

higher threshold: A predefined level where the price is expected to experience resistance, leading to a potential reversal downward.

Lower Threshold: A predefined level where the price might find support, leading to a potential upward reversal.

In this strategy, we focus on price movements around the upper mathematical level, where prices are likely to reverse downwards.

Strategy Logic

Setup:

The strategy is applied on a 5-minute chart.

Mathematical levels are calculated based on your preferred method, such as Fibonacci levels, pivot points, or custom calculations. For this strategy, let's assume we are using a specific predefined upper level.

Sell Signal Criteria:

A 5-minute candle must cross above the predefined upper mathematical level or close entirely above it (open and close both above the level).

The following candle must break below the low of the candle that crossed the upper level and close below that low. This confirms a bearish reversal.

Once these conditions are met, a sell signal is triggered.

Stop Loss:

The stop loss is placed at the high of the candle that crossed above the upper mathematical level.

This level represents the point where the trade setup would be invalidated.

Take Profit:

Target 1: The first take profit is set at a level that offers a 1:5 risk-to-reward ratio.

Target 2: An alternative take profit level is set at a 1:3 risk-to-reward ratio, providing flexibility based on market conditions.

Trade Management:

Once a trade is initiated, no new trades will be taken until the current trade hits either the stop loss or the first take profit level. This prevents overlapping signals and helps in managing risk effectively.

Originality and Usefulness

This strategy offers a unique approach by using mathematical levels instead of traditional indicators. It provides traders with a clear framework for identifying and executing high-probability reversal trades, particularly in intraday markets.

Originality:

The strategy's originality lies in its reliance on mathematical levels combined with a multi-candle confirmation pattern. This approach reduces the chances of false signals and offers a robust method for identifying potential reversals.

Usefulness:

The strategy is particularly useful for traders who prefer a more quantitative approach, relying on calculated price levels rather than indicators. The clear rules for entry, stop loss, and take profit make it easier to execute consistently.

The inclusion of both 1:5 and 1:3 risk-to-reward targets allows for flexibility depending on market conditions, ensuring that traders can adapt to varying levels of volatility.

Chart Signals and Examples

To demonstrate the effectiveness of this strategy, let's look at a few hypothetical examples on a 5-minute chart:

Example 1: Clear Reversal Signal

The price steadily rises and crosses above the predefined upper mathematical level. The next candle breaks below the low of this candle and closes lower, triggering a sell signal.

A red dotted line is drawn at the stop loss level (the high of the candle that crossed the upper level).

Two green dashed lines are drawn to indicate the first and second take profit levels.

Example 2: No Signal Due to Ongoing Trade

After an initial sell signal is triggered, the price fluctuates but does not hit either the stop loss or the first take profit target. During this period, the strategy refrains from issuing any new signals, adhering to the trade management rule.

Example 3: Trade Reaches Target 1

In another scenario, the price moves sharply in favor of the trade after the signal is triggered. The first take profit level is hit, securing a profit. The trade is then considered closed, and the strategy is ready to issue a new signal when conditions are met.

Monthly Day Long Strategy with VIX and Risk ManagementThis trading strategy is designed to open long positions on a specific day of the month, with the conditions for entry and exit based on the VIX index and additional risk management techniques. The strategy includes stop-loss and take-profit features to manage risk and lock in profits.

Inputs:

Entry Day of the Month (entry_day): Specifies which day of the month to consider for initiating a trade. The default value is the 27th.

Hold Duration (Days) (hold_duration_days): Defines how many days to hold the position after opening. The default value is 4 days.

VIX Threshold (vix_threshold): Sets the maximum acceptable value for the VIX index to consider an entry. If the VIX is below this threshold, it signals a potential trade. The default value is 20.0.

Stop Loss (%) (stop_loss_percentage): Determines the percentage below the entry price where the stop-loss will be triggered. The default value is 2.0%.

Take Profit (%) (take_profit_percentage): Sets the percentage above the entry price where the take-profit will be triggered. The default value is 5.0%.

Functions:

next_weekday(date): Adjusts the entry date to the next Monday if it falls on a weekend (Saturday or Sunday). This ensures trades do not occur on non-trading days.

Logic:

Entry Conditions:

Date Check: Opens a long position if the current date matches the adjusted entry date (the 27th or the next Monday if the 27th falls on a weekend).

VIX Filter: The VIX index value must be below the specified threshold (e.g., 20.0) to consider an entry.

Exit Conditions:

Time-Based Exit: Closes the position after the hold duration of 4 days.

Stop-Loss: Automatically closes the position if the price drops to a level that is a specified percentage below the entry price (e.g., 2.0%).

Take-Profit: Closes the position if the price rises to a level that is a specified percentage above the entry price (e.g., 5.0%).

Plots:

VIX Plot: Displays the VIX index on the chart for visual reference.

VIX Threshold Line: A horizontal line representing the VIX threshold value.

Summary:

The strategy aims to take advantage of specific entry days while filtering trades based on VIX levels to ensure market conditions are favorable. Risk management is enhanced through stop-loss and take-profit settings, which help in controlling potential losses and securing profits. The strategy ensures trades are only made on trading days and not on weekends, adjusting automatically to the next Monday if needed.

ChatGPT kann Fehler machen. Überprüfe wichtige Informationen.

Multi-Step Vegas SuperTrend - strategy [presentTrading]Long time no see! I am back : ) Please allow me to gain some warm-up.

█ Introduction and How it is Different

The "Vegas SuperTrend Strategy" is an enhanced trading strategy that leverages both the Vegas Channel and SuperTrend indicators to generate buy and sell signals.

What sets this strategy apart from others is its dynamic adjustment to market volatility and its multi-step take profit mechanism. Unlike traditional single-step profit-taking approaches, this strategy allows traders to systematically scale out of positions at predefined profit levels, thereby optimizing their risk-reward ratio and maximizing potential gains.

BTCUSD 6hr performance

█ Strategy, How it Works: Detailed Explanation

The Vegas SuperTrend Strategy combines the strengths of the Vegas Channel and SuperTrend indicators to identify market trends and generate trade signals. The following subsections delve into the details of how each component works and how they are integrated.

🔶 Vegas Channel Calculation

The Vegas Channel is based on a simple moving average (SMA) and the standard deviation (STD) of the closing prices over a specified period. The channel is defined by upper and lower bounds that are dynamically adjusted based on market volatility.

Simple Moving Average (SMA):

SMA_vegas = (1/N) * Σ(Close_i) for i = 0 to N-1

where N is the length of the Vegas Window.

Standard Deviation (STD):

STD_vegas = sqrt((1/N) * Σ(Close_i - SMA_vegas)^2) for i = 0 to N-1

Vegas Channel Upper and Lower Bounds:

VegasChannelUpper = SMA_vegas + STD_vegas

VegasChannelLower = SMA_vegas - STD_vegas

The details are here:

🔶 Trend Detection and Trade Signals

The strategy determines the current market trend based on the closing price relative to the SuperTrend bounds:

Market Trend:

MarketTrend = 1 if Close > SuperTrendPrevLower

-1 if Close < SuperTrendPrevUpper

Previous Trend otherwise

Trade signals are generated when there is a shift in the market trend:

Bullish Signal: When the market trend shifts from -1 to 1.

Bearish Signal: When the market trend shifts from 1 to -1.

🔶 Multi-Step Take Profit Mechanism

The strategy incorporates a multi-step take profit mechanism that allows for partial exits at predefined profit levels. This helps in locking in profits gradually and reducing exposure to market reversals.

Take Profit Levels:

The take profit levels are calculated as percentages of the entry price:

TakeProfitLevel_i = EntryPrice * (1 + TakeProfitPercent_i/100) for long positions

TakeProfitLevel_i = EntryPrice * (1 - TakeProfitPercent_i/100) for short positions

Multi-steps take profit local picture:

█ Trade Direction

The trade direction can be customized based on the user's preference:

Long: The strategy only takes long positions.

Short: The strategy only takes short positions.

Both: The strategy can take both long and short positions based on the market trend.

█ Usage

To use the Vegas SuperTrend Strategy, follow these steps:

Configure Input Settings:

- Set the ATR period, Vegas Window length, SuperTrend Multiplier, and Volatility Adjustment Factor.

- Choose the desired trade direction (Long, Short, Both).

- Enable or disable the take profit mechanism and set the take profit percentages and amounts for each step.

█ Default Settings

The default settings of the strategy are designed to provide a balanced approach to trading. Below is an explanation of each setting and its effect on the strategy's performance:

ATR Period (10): This setting determines the length of the ATR used in the SuperTrend calculation. A longer period smoothens the ATR, making the SuperTrend less sensitive to short-term volatility. A shorter period makes the SuperTrend more responsive to recent price movements.

Vegas Window Length (100): This setting defines the period for the Vegas Channel's moving average. A longer window provides a broader view of the market trend, while a shorter window makes the channel more responsive to recent price changes.

SuperTrend Multiplier (5): This base multiplier adjusts the sensitivity of the SuperTrend to the ATR. A higher multiplier makes the SuperTrend less sensitive, reducing the frequency of trade signals. A lower multiplier increases sensitivity, generating more signals.

Volatility Adjustment Factor (5): This factor dynamically adjusts the SuperTrend multiplier based on the width of the Vegas Channel. A higher factor increases the sensitivity of the SuperTrend to changes in market volatility, while a lower factor reduces it.

Take Profit Percentages (3.0%, 6.0%, 12.0%, 21.0%): These settings define the profit levels at which portions of the trade are exited. They help in locking in profits progressively as the trade moves in favor.

Take Profit Amounts (25%, 20%, 10%, 15%): These settings determine the percentage of the position to exit at each take profit level. They are distributed to ensure that significant portions of the trade are closed as the price reaches the set levels, reducing exposure to reversals.

Adjusting these settings can significantly impact the strategy's performance. For instance, increasing the ATR period or the SuperTrend multiplier can reduce the number of trades, potentially improving the win rate but also missing out on some profitable opportunities. Conversely, lowering these values can increase trade frequency, capturing more short-term movements but also increasing the risk of false signals.

Zero-lag TEMA Crosses Strategy[Pakun]Here's the adjusted strategy description in English, aligned with the house rules:

---

### Strategy Name: Zero-lag TEMA Cross Strategy

**Purpose:** This strategy aims to identify entry and exit points in the market using Zero-lag Triple Exponential Moving Averages (TEMA). It focuses on minimizing lag and improving the accuracy of trend-following signals.

### Uniqueness and Usefulness

**Uniqueness:** This strategy employs the less commonly used Zero-lag TEMA, compared to standard moving averages. This unique approach reduces lag and provides more timely signals.

**Usefulness:** This strategy is valuable for traders looking to capture trend reversals or continuations with reduced lag. It has the potential to enhance the profitability and accuracy of trades.

### Entry Conditions

**Long Entry:**

- **Condition:** A crossover occurs where the short-term Zero-lag TEMA surpasses the long-term Zero-lag TEMA.

- **Signal:** A buy signal is generated, indicating a potential uptrend.

**Short Entry:**

- **Condition:** A crossunder occurs where the short-term Zero-lag TEMA falls below the long-term Zero-lag TEMA.

- **Signal:** A sell signal is generated, indicating a potential downtrend.

### Exit Conditions

**Exit Strategy:**

- **Stop Loss:** Positions are closed if the price moves against the trade and hits the predefined stop loss level. The stop loss is set based on recent highs/lows.

- **Take Profit:** Positions are closed when the price reaches the profit target. The profit target is calculated as 1.5 times the distance between the entry price and the stop loss level.

### Risk Management

**Risk Management Rules:**

- This strategy incorporates a dynamic stop loss mechanism based on recent highs/lows over a specified period.

- The take profit level ensures a reward-to-risk ratio of 1.5 times the stop loss distance.

- These measures aim to manage risk and protect capital.

**Account Size:** ¥500,000

**Commissions and Slippage:** 94 pips per trade and 1 pip slippage

**Risk per Trade:** 1% of account equity

### Configurable Options

**Configurable Options:**

- Lookback Period: The number of bars to calculate recent highs/lows.

- Fast Period: Length of the short-term Zero-lag TEMA (69).

- Slow Period: Length of the long-term Zero-lag TEMA (130).

- Signal Display: Option to display buy/sell signals on the chart.

- Bar Color: Option to change bar colors based on trend direction.

### Adequate Sample Size

**Sample Size Justification:**

- To ensure the robustness and reliability of the strategy, it should be tested with a sufficiently long period of historical data.

- It is recommended to backtest across multiple market cycles to adapt to different market conditions.

- This strategy was backtested using 10 days of historical data, including 184 trades.

### Notes

**Additional Considerations:**

- This strategy is designed for educational purposes and should be thoroughly tested in a demo environment before live trading.

- Settings should be adjusted based on the asset being traded and current market conditions.

### Credits

**Acknowledgments:**

- The concept and implementation of Zero-lag TEMA are based on contributions from technical analysts and the trading community.

- Special thanks to John Doe for the TEMA concept.

- Thanks to Zero-lag TEMA Crosses .

- This strategy has been enhanced by adding new filtering algorithms and risk management rules to the original TEMA code.

### Clean Chart Description

**Chart Appearance:**

- This strategy provides a clean and informative chart by plotting Zero-lag TEMA lines and optional entry/exit signals.

- The display of signals and color bars can be toggled to declutter the chart, improving readability and analysis.

Bollinger Bands Enhanced StrategyOverview

The common practice of using Bollinger bands is to use it for building mean reversion or squeeze momentum strategies. In the current script Bollinger Bands Enhanced Strategy we are trying to combine the strengths of both strategies types. It utilizes Bollinger Bands indicator to buy the local dip and activates trailing profit system after reaching the user given number of Average True Ranges (ATR). Also it uses 200 period EMA to filter trades only in the direction of a trend. Strategy can execute only long trades.

Unique Features

Trailing Profit System: Strategy uses user given number of ATR to activate trailing take profit. If price has already reached the trailing profit activation level, scrip will close long trade if price closes below Bollinger Bands middle line.

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Major Trend Filter: Strategy utilizes 100 period EMA to take trades only in the direction of a trend.

Flexible Risk Management: Users can choose number of ATR as a stop loss (by default = 1.75) for trades. This is flexible approach because ATR is recalculated on every candle, therefore stop-loss readjusted to the current volatility.

Methodology

First of all, script checks if currently price is above the 200-period exponential moving average EMA. EMA is used to establish the current trend. Script will take long trades on if this filtering system showing us the uptrend. Then the strategy executes the long trade if candle’s low below the lower Bollinger band. To calculate the middle Bollinger line, we use the standard 20-period simple moving average (SMA), lower band is calculated by the substruction from middle line the standard deviation multiplied by user given value (by default = 2).

When long trade executed, script places stop-loss at the price level below the entry price by user defined number of ATR (by default = 1.75). This stop-loss level recalculates at every candle while trade is open according to the current candle ATR value. Also strategy set the trailing profit activation level at the price above the position average price by user given number of ATR (by default = 2.25). It is also recalculated every candle according to ATR value. When price hit this level script plotted the triangle with the label “Strong Uptrend” and start trail the price at the middle Bollinger line. It also started to be plotted as a green line.

When price close below this trailing level script closes the long trade and search for the next trade opportunity.

Risk Management

The strategy employs a combined and flexible approach to risk management:

It allows positions to ride the trend as long as the price continues to move favorably, aiming to capture significant price movements. It features a user-defined ATR stop loss parameter to mitigate risks based on individual risk tolerance. By default, this stop-loss is set to a 1.75*ATR drop from the entry point, but it can be adjusted according to the trader's preferences.

There is no fixed take profit, but strategy allows user to define user the ATR trailing profit activation parameter. By default, this stop-loss is set to a 2.25*ATR growth from the entry point, but it can be adjusted according to the trader's preferences.

Justification of Methodology

This strategy leverages Bollinger bangs indicator to open long trades in the local dips. If price reached the lower band there is a high probability of bounce. Here is an issue: during the strong downtrend price can constantly goes down without any significant correction. That’s why we decided to use 200-period EMA as a trend filter to increase the probability of opening long trades during major uptrend only.

Usually, Bollinger Bands indicator is using for mean reversion or breakout strategies. Both of them have the disadvantages. The mean reversion buys the dip, but closes on the return to some mean value. Therefore, it usually misses the major trend moves. The breakout strategies usually have the issue with too high buy price because to have the breakout confirmation price shall break some price level. Therefore, in such strategies traders need to set the large stop-loss, which decreases potential reward to risk ratio.

In this strategy we are trying to combine the best features of both types of strategies. Script utilizes ate ATR to setup the stop-loss and trailing profit activation levels. ATR takes into account the current volatility. Therefore, when we setup stop-loss with the user-given number of ATR we increase the probability to decrease the number of false stop outs. The trailing profit concept is trying to add the beat feature from breakout strategies and increase probability to stay in trade while uptrend is developing. When price hit the trailing profit activation level, script started to trail the price with middle line if Bollinger bands indicator. Only when candle closes below the middle line script closes the long trade.

Backtest Results

Operating window: Date range of backtests is 2020.10.01 - 2024.07.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 30%

Maximum Single Position Loss: -9.78%

Maximum Single Profit: +25.62%

Net Profit: +6778.11 USDT (+67.78%)

Total Trades: 111 (48.65% win rate)

Profit Factor: 2.065

Maximum Accumulated Loss: 853.56 USDT (-6.60%)

Average Profit per Trade: 61.06 USDT (+1.62%)

Average Trade Duration: 76 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 4h BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

BB Position CalculatorPosition Size Calculator Instructions

Overview

The Position Size Calculator is designed to help traders automatically determine the appropriate lot size based on the dollar amount they are willing to risk. It includes features for automatic lot sizing, fixed lot risk calculations, take profit calculations (both automatic and fixed), max run-up, and max drawdown. Calculated values are displayed in ticks, points, and USD.

Key Features

• Automatic Lot Sizing: Automatically calculates lot size based on the amount of money you are willing to risk.

• Fixed Lot Risk Calculations: Provides risk calculations for fixed lot sizes.

• Take Profit Calculations: Offers both automatic and fixed take profit calculations.

• Max Run-Up and Max Drawdown: Monitors and displays the maximum run-up and drawdown of your trade.

• Detailed Metrics: Displays all calculated values in ticks, points, and USD.

Setup Instructions

1. Add and Remove for Each Position: The calculator is designed to be added to your chart for each new position. Once your preferences are set the first time, save them as your default to retain your settings for future use.

2. Adding the Indicator to Favorites:

• Use the TradingView keyboard shortcut “/” then type “pos.”

• Use the arrow key to select the Position Size Calculator and press enter.

• Close the indicator selection pop-up.

3. Setting the Trigger Price:

• A blue pop-up labeled “SET TRIGGER PRICE” will appear at the bottom of the chart.

• Click on the chart at the price level where you want to enter the trade.

4. Setting the Stop Loss:

• The pop-up will change to “SET STOP LOSS.”

• Click on the chart at the price level where your stop loss will be set.

5. Setting the Take Profit:

• The pop-up will change to “SET TAKE PROFIT.”

• Click on the chart at the price level where you want to take profit. If you have selected the option to overwrite with a set risk/reward ratio (R:R), the calculation will use this price level.

6. Setting the Trade Window Start:

• The pop-up will change to “SET TRADE WINDOW START.”

• Click on the bar in time where you want the indicator to start monitoring for price to trigger the position.

7. Adjusting the Position:

• Clicking on any part of the indicator will display draggable lines, allowing you to fine-tune the position that was previously plotted by the first four chart clicks.

Additional Notes

• Compatibility: This calculator has only been tested with futures trading.

• Customization: Once your preferences are set, save them as your default to make setup quicker for future trades.

• Support: If you have any questions or feature requests, please feel free to reach out.

Position Size Calculator for ContractDescription:

Position Size Calculator is a versatile Pine Script tool designed to help traders manage their risk and position sizing effectively. This script calculates essential trading metrics and visualizes them directly on your chart, helping you make informed trading decisions.

Features:

- Account Size & Risk Management:

- Account Size: Input your total account balance to calculate position sizes.

- Maximum Risk: Define how much of your account you are willing to risk per trade in dollars.

- Pip Value: Set the value of a single pip for one contract, which is crucial for calculating risk

and position size.

Trade Setup Visualization:

- Entry Price: Specify the price at which you plan to enter the trade.

- Stop Loss: Define your stop loss level to manage your risk.

- Take Profit: Set your target profit level for the trade.

- Visualize the Entry, Stop Loss, and Take Profit levels on your chart with customizable line

colors and text sizes.

- View the distance in pips between the Entry, Stop Loss, and Take Profit levels.

Position Size Calculation:

- Calculates the number of contracts to open based on your risk tolerance and the pip value.

- Displays the maximum number of contracts you can open given your risk parameters.

Customizable Table Display:

- Table Position: Choose the position of the summary table on the chart (Top-Left, Top-Right,

Bottom-Left, Bottom-Right, etc.).

- Table Text Size: Adjust the text size for the summary table.

- Table Background Color: Set the background color for the summary table.

- Table Border Color: Customize the border color of the summary table.

How to Use:

1- Input your Account Size: Enter your current account balance.

2- Set Maximum Risk and Pip Value: Define how much you're willing to risk per trade and the

pip value for your contract.

3- Define Trade Levels: Input your desired Entry Price, Stop Loss, and Take Profit levels.

4- Customize Visuals: Adjust the line styles and table settings to fit your preferences.

5- View Calculations: The script will display the distance in pips and the calculated position

size directly on your chart.

Example Usage:

Example to calculate the value of 1 pips with 1 contract:

Inputs:

Account Size: Your total trading account balance.

Maximum Risk: Risk amount per trade in dollars.

Pip Value: Value of one pip for a single contract.

Entry Price: The price at which you plan to enter the trade.

Stop Loss: The level at which you will exit the trade to cut losses.

Take Profit: The target price to lock in profits.

Line Text Size: Size of the text for the Entry, Stop Loss, and Take Profit lines.

Line Extend: Option to extend the lines for visual clarity.

Table Position: Position of the summary table on the chart.

Table Text Size: Size of the text in the summary table.

Table Background Color: Background color of the summary table.

Table Border Color: Border color of the summary table.

Visuals:

Entry Price, Stop Loss, and Take Profit levels are clearly marked on the chart.

Summary Table with important trade metrics displayed.

MAC Investor V3.0 [VK]This indicator combines multiple functionalities to assist traders in making informed decisions. It primarily uses Heikin Ashi candles, Moving Averages, and a Price Action Channel (PAC) to provide signals for entering and exiting trades. Here's a detailed breakdown:

Inputs

MAC Length: Sets the length for the PAC calculation.

Use Heikin Ashi Candles: Option to use Heikin Ashi candles for calculations.

Show Coloured Bars around MAC: Option to color bars based on their relation to the PAC.

Show Long/Short Signals: Options to display long and short signals.

Show MAs? : Option to show moving averages on the chart.

Show MAs Trend at the Bottom?: Option to show trend signals at the bottom of the chart.

MA Lengths: Length settings for three different moving averages.

Change MA Color Based on Direction?: Option to change the color of moving averages based on trend direction.

MA Higher TimeFrame: Allows setting a higher timeframe for moving averages.

Show SL-TP Lines: Option to display Stop Loss and Take Profit lines.

SL/TP Percentages: Set the percentages for Stop Loss and three levels of Take Profit.

Calculations and Features

Heikin Ashi Candles: Calculations are based on Heikin Ashi candle data if selected.

Price Action Channel (PAC): Uses Exponential Moving Averages (EMA) of the high, low, and close to create a channel.

Bar Coloring: Colors the bars based on their position relative to the PAC.

Long and Short Signals: Uses crossovers of the close price and PAC upper/lower bands to generate signals.

Moving Averages (MA): Plots three moving averages and colors them based on their trend direction.

Overall Trend Indicators: Uses triangles at the bottom of the chart to show the overall trend of the MAs.

Stop Loss and Take Profit Levels: Calculates and plots these levels based on user-defined percentages from the entry price.

Alerts: Provides alerts for long and short signals.

Use Cases and How to Use

Identifying Trends: The PAC helps to identify the trend direction. If the closing price is above the PAC upper band, it suggests an uptrend; if below the lower band, it suggests a downtrend.

Entering Trades: Use the long and short signals to enter trades. A long signal is generated when the closing price crosses above the PAC upper band, and a short signal is generated when it crosses below the PAC lower band.

Exit Strategies: Utilize the Stop Loss (SL) and Take Profit (TP) levels to manage risk and lock in profits. These levels are automatically calculated based on the entry price and user-defined percentages.

Trend Confirmation with MAs: The moving averages provide additional confirmation of the trend. When all three MAs are trending in the same direction (e.g., all green for an uptrend), it adds confidence to the trade signal.

Overall Trend Indicators: The triangles at the bottom of the chart show the overall trend direction of the MAs:

Green Triangle: All three MAs are trending upwards, indicating a strong uptrend.

Red Triangle: All three MAs are trending downwards, indicating a strong downtrend.

Yellow Triangle: Mixed signals from the MAs, indicating no clear trend.

Bar Coloring for Quick Analysis: The colored bars give a quick visual cue about the market condition, aiding in faster decision-making.

Alerts: Set up alerts to get notified when a long or short signal is generated, allowing you to act promptly without constantly monitoring the chart.

Maximizing Profit

To maximize profit with this indicator:

Follow the Signals: Use the long and short signals to time your entries. Ensure you follow the trend indicated by the PAC and MAs.

Risk Management: Always set your Stop Loss and Take Profit levels to manage risk. This will help you cut losses early and secure profits.

Confirm with MAs: Look for confirmation from the moving averages. When all MAs align with the signal, it indicates a stronger trend.

Overall Trend Indicators: Pay attention to the triangles at the bottom for overall trend confirmation. Only enter trades when the overall trend is in your favor.

Heikin Ashi for Smoothing: Use Heikin Ashi candles for smoother trends and fewer false signals.

Backtesting: Test the indicator on historical data to understand its performance and adjust settings as necessary.

Adapt to Market Conditions: Adjust the lengths of PAC and MAs based on the market's volatility and timeframe you are trading on.

How to Use the Indicator

Add to Chart: Add the indicator to your TradingView chart.

Configure Settings: Customize the input settings to fit your trading strategy and timeframe.

Monitor Signals: Watch for long and short signals and observe the trend direction with the PAC and MAs.

Check Overall Trend: Look at the triangles at the bottom of the chart to see the overall trend direction of the MAs.

Set Alerts: Configure alerts to get notified of new signals.

Manage Trades: Use the SL and TP levels to manage your trades effectively.

Grid TraderGrid Trader Indicator ( GTx ):

Overview

The Grid Trader Indicator is a tool that helps traders visualize key levels within a specified trading range. The indicator plots accumulation and distribution levels, an entry level, an exit level, and a midpoint. This guide will help you understand how to use the indicator and its features for effective grid trading.

Basics of Trading Range, Grid Buy, and Grid Sell

Trading Range

A trading range is the horizontal price movement between a defined upper ( resistance ) and lower ( support ) level over a period of time. When a security trades within a range, it repeatedly moves between these two levels without trending upwards or downwards significantly. Traders often use the trading range to identify potential buy and sell points:

Upper Level (Resistance): This is the price level at which selling pressure overcomes buying pressure, preventing the price from rising further.

Lower Level (Support): This is the price level at which buying pressure overcomes selling pressure, preventing the price from falling further.

Grid Trading Strategy

Grid trading is a type of trading strategy that involves placing buy and sell orders at predefined intervals around a set price. It aims to profit from the natural market volatility by buying low and selling high in a range-bound market. The strategy divides the trading range into several grid levels where orders are placed.

Grid Buy

Grid buy orders are placed at intervals below the current price . When the price drops to these levels, buy orders are triggered . This strategy ensures that the trader buys more as the price falls, potentially lowering the average purchase price .

Grid Sell

Grid sell orders are placed at intervals above the current price . When the price rises to these levels, sell orders are triggered . This ensures that the trader sells portions of their holdings as the price increases, potentially securing profits at higher levels .

Key Points of Grid Trading

Grid Size : The interval between each buy and sell order. This can be constant (e.g., $2 intervals) or variable based on certain conditions.

Accumulation Range : The lower part of the trading range where buy orders are placed.

Distribution Range : The upper part of the trading range where sell orders are placed.

Midpoint : The average price of the entry and exit levels, often used as a reference point for balance.

As the price moves up and down within this range, your buy orders will be triggered as the price drops and your sell orders will be triggered as the price rises. This allows you to accumulate more of the asset at lower prices and sell portions at higher prices, profiting from the price oscillations within the defined range. Grid trading can be particularly effective in a sideways market where there is no clear long-term trend. However, it requires careful monitoring and adjustment of grid levels based on market conditions to minimize risks and maximize returns .

Configuring the Indicator :

Once the indicator is added, you will see a settings icon next to it. Click on it to open the settings menu.

Adjust the Upper Level , Lower Level , Entry Level , and Exit Level to match your trading strategy and market conditions.

Set the Levels Visibility to control how many bars back the levels will be plotted.

Interpreting the Levels :

Accumulation Levels : These are plotted below the entry level and are potential buy zones. They are labeled as Accumulation Level 1, 2, and 3.

Distribution Levels : These are plotted above the exit level and are potential sell zones. They are labeled as Distribution Level 1, 2, and 3.

Upper Level : Marked in fuchsia, indicating the top boundary of the trading range.

Exit Level : Marked in yellow, indicating the level at which you plan to exit trades.

Midpoint : Marked in white, indicating the average of the entry and exit levels.

Entry Level : Marked in yellow, indicating the level at which you plan to enter trades.

Lower Level : Marked in aqua, indicating the bottom boundary of the trading range.

By visualizing key levels, you can make informed decisions on where to place buy and sell orders, potentially maximizing your trading profits through systematic grid trading.

Wolf DCA CalculatorThe Wolf DCA Calculator is a powerful and flexible indicator tailored for traders employing the Dollar Cost Averaging (DCA) strategy. This tool is invaluable for planning and visualizing multiple entry points for both long and short positions. It also provides a comprehensive analysis of potential profit and loss based on user-defined parameters, including leverage.

Features

Entry Price: Define the initial entry price for your trade.

Total Lot Size: Specify the total number of lots you intend to trade.

Percentage Difference: Set the fixed percentage difference between each DCA point.

Long Position: Toggle to switch between long and short positions.

Stop Loss Price: Set the price level at which you plan to exit the trade to minimize losses.

Take Profit Price: Set the price level at which you plan to exit the trade to secure profits.

Leverage: Apply leverage to your trade, which multiplies the potential profit and loss.

Number of DCA Points: Specify the number of DCA points to strategically plan your entries.

How to Use

1. Add the Indicator to Your Chart:

Search for "Wolf DCA Calculator" in the TradingView public library and add it to your chart.

2. Configure Inputs:

Entry Price: Set your initial trade entry price.

Total Lot Size: Enter the total number of lots you plan to trade.

Percentage Difference: Adjust this to set the interval between each DCA point.

Long Position: Use this toggle to choose between a long or short position.

Stop Loss Price: Input the price level at which you plan to exit the trade to minimize losses.

Take Profit Price: Input the price level at which you plan to exit the trade to secure profits.

Leverage: Set the leverage you are using for the trade.

Number of DCA Points: Specify the number of DCA points to plan your entries.

3. Analyze the Chart:

The indicator plots the DCA points on the chart using a stepline style for clear visualization.

It calculates the average entry point and displays the potential profit and loss based on the specified leverage.

Labels are added for each DCA point, showing the entry price and the lots allocated.

Horizontal lines mark the Stop Loss and Take Profit levels, with corresponding labels showing potential loss and profit.

Benefits

Visual Planning: Easily visualize multiple entry points and understand how they affect your average entry price.

Risk Management: Clearly see your Stop Loss and Take Profit levels and their impact on your trade.

Customizable: Adapt the indicator to your specific strategy with a wide range of customizable parameters.

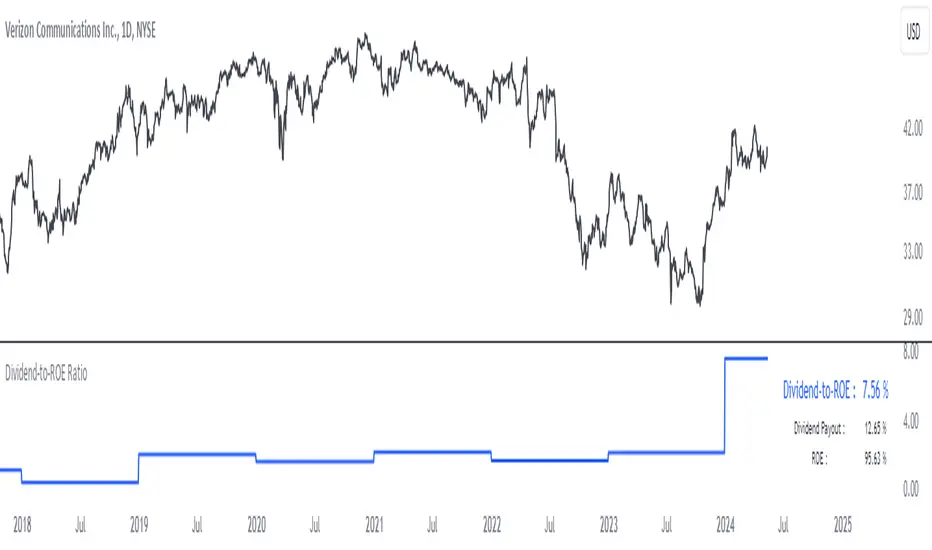

Dividend-to-ROE RatioDividend-to-ROE Ratio Indicator

The Dividend-to-ROE Ratio indicator offers valuable insights into a company's dividend distribution relative to its profitability, specifically comparing the Dividend Payout Ratio (proportion of earnings as dividends) to the Return on Equity (ROE), a measure of profitability from shareholder equity.

Interpretation:

1. Higher Ratio: A higher Dividend-to-ROE Ratio suggests a stable dividend policy, where a significant portion of earnings is returned to shareholders. This can indicate consistent dividend payments, often appealing to income-seeking investors.

2. Lower Ratio: Conversely, a lower ratio implies that the company retains more earnings for growth, potentially signaling a focus on reinvestment for future expansion rather than immediate dividend payouts.

3. Excessively High Ratio: An exceptionally high ratio may raise concerns. While it could reflect a generous dividend policy, excessively high ratios might indicate that a company is distributing more earnings than it can sustainably afford. This could potentially hinder the company's ability to reinvest in its operations, research, or navigate economic downturns effectively.

Utility and Applications:

The Dividend-to-ROE Ratio can be particularly useful in the following scenarios:

1. Income-Oriented Investors: For investors seeking consistent dividend income, a higher ratio signifies a company's commitment to distributing profits to shareholders, potentially aligning with income-oriented investment strategies.

2. Financial Health Assessment: Analysts and stakeholders can use this ratio to gauge a company's financial health and dividend sustainability. It provides insights into management's capital allocation decisions and strategic focus.

3. Comparative Analysis: When comparing companies within the same industry, this ratio helps in benchmarking dividend policies and identifying outliers with unusually high or low ratios.

Considerations:

1. Contextual Analysis: Interpretation should be contextualized within industry standards and the company's financial history. Comparing the ratio with peers in the same sector can provide meaningful insights.

2. Financial Health: It's crucial to evaluate this indicator alongside other financial metrics (like cash flow, debt levels, and profit margins) to grasp the company's overall financial health and sustainability of its dividend policy.

Disclaimer: This indicator is for informational purposes only and does not constitute financial advice. Investors should conduct thorough research and consult with financial professionals before making investment decisions based on this ratio.

PUELL - PUELL Top and Bottom Indicator for BTC [Logue]Puell Multiple Indicator (PUELL) - The Puell multiple is the ratio between the daily coin issuance in USD and its 365-day moving average. This multiple helps to measure miner profitability. The PUELL indicator smooths the Puell multiple using a 14-day simple moving average. When the PUELL goes to high values relative to historical values, it indicates the profitability of the miners is high and a top may be near. When the PUELL is low relative to historical values, it indicates the profitability of the minors is low and a bottom may be near. The default trigger values are PUELL values above 3.0 for a "top" and below 0.5 for a "bottom".

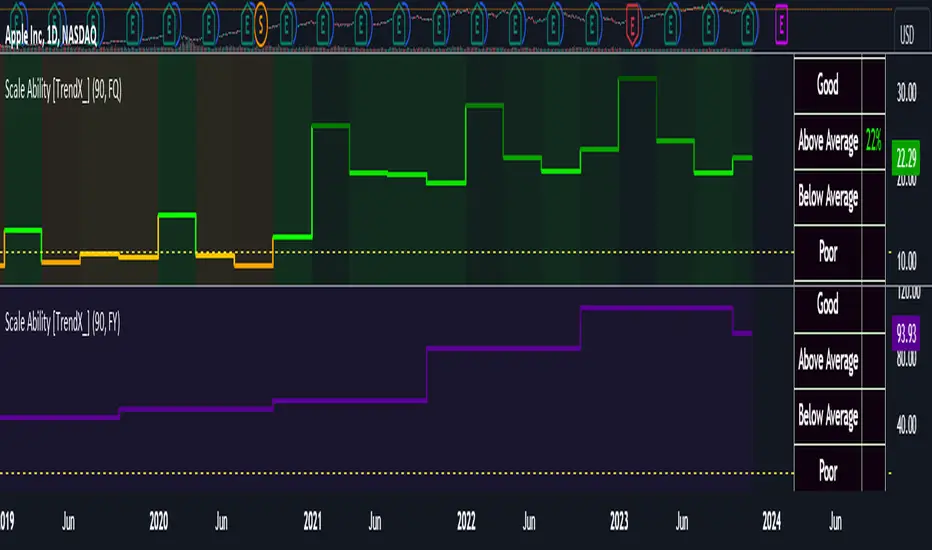

Scale Ability [TrendX_]Scale Ability indicator can indicate a company’s potential for future growth and profitability.

A scalable company is one that can increase its revenue and market share without increasing its costs proportionally, which can benefit from economies of scale. Therefore, the high-scale ability can generate more value for its shareholders - which is important for investment decisions.

Scale Ability indicator consists of 3 financial components:

Cash Flow from Investing Activities to Total Assets Ratio (CFIA / TA)

Net Income to Total Debt Ratio (NI / TD)

Earnings Before Interest, Taxes, Depreciation and Amortization to Equity Ratio (EBITDA / E)

These measures can help investors assess how efficiently and effectively a company uses its resources to generate revenue and profit.

Note:

This can be customizable between Fiscal Quarter (FQ) and Fiscal Year (Fy)

This is suitable for companies in fast-growing industries.

FUNCTION

CFIA / TA Ratio

A company with a net income to total debt of 9% could indicate that it is investing in its assets to keep up with the market demand and the technological changes which can create competitive advantages.

NI/ TD Ratio

A company with a net income to total debt of 9% could show that it is profitable and has a strong financial position, which can easily cover its debt payments.

EBITDA / E Ratio

A company with a net income to total debt of 14% illustrates that it is generating a high return on its equity.

USAGE

Scale index division:

> 43 : Excellent

32 - 43 : Good

12 - 31 : Above Average

= 11 : Average

8 - 10 : Below Average

5 - 7 : Poor

< 4 : Very Poor

DISCLAIMER

This is only a rough estimate, and the actual ratio may differ significantly depending on the stage of the business cycle and the company’s strategy, and the comparison of each company and its peers.

This indicator is not financial advice, it can only help traders make better decisions. There are many factors and uncertainties that can affect the outcome of any endeavor, and no one can guarantee or predict with certainty what will occur.

Therefore, one should always exercise caution and judgment when making decisions based on past performance.

RSI & Backed-Weighted MA StrategyRSI & MA Strategy :

INTRODUCTION :

This strategy is based on two well-known indicators that work best together: the Relative Strength Index (RSI) and the Moving Average (MA). We're going to use the RSI as a trend-follower indicator, rather than a reversal indicator as most are used to. To the signals sent by the RSI, we'll add a condition on the chart's MA, filtering out irrelevant signals and considerably increasing our winning rate. This is a medium/long-term strategy. There's also a money management method enabling us to reinvest part of the profits or reduce the size of orders in the event of substantial losses.

RSI :

The RSI is one of the best-known and most widely used indicators in trading. Its purpose is to warn traders when an asset is overbought or oversold. It was designed to send reversal signals, but we're going to use it as a trend indicator by increasing its length to 20. The RSI formula is as follows :

RSI (n) = 100 - (100 / (1 + (H (n)/L (n))))

With n the length of the RSI, H(n) the average of days closing above the open and L(n) the average of days closing below the open.

MA :

The Moving Average is also widely used in technical analysis, to smooth out variations in an asset. The SMA formula is as follows :

SMA (n) = (P1 + P2 + ... + Pn) / n

where n is the length of the MA.

However, an SMA does not weight any of its terms, which means that the price 10 days ago has the same importance as the price 2 days ago or today's price... That's why in this strategy we use a RWMA, i.e. a back-weighted moving average. It weights old prices more heavily than new ones. This will enable us to limit the impact of short-term variations and focus on the trend that was dominating. The RWMA used weights :

The 4 most recent terms by : 100 / (4+(n-4)*1.30)

The other oldest terms by : weight_4_first_term*1.30

So the older terms are weighted 1.30 more than the more recent ones. The moving average thus traces a trend that accentuates past values and limits the noise of short-term variations.

PARAMETERS :

RSI Length : Lenght of RSI. Default is 20.

MA Type : Choice between a SMA or a RWMA which permits to minimize the impact of short term reversal. Default is RWMA.

MA Length : Length of the selected MA. Default is 19.

RSI Long Signal : Minimum value of RSI to send a LONG signal. Default is 60.

RSI Short signal : Maximum value of RSI to send a SHORT signal. Default is 40.

ROC MA Long Signal : Maximum value of Rate of Change MA to send a LONG signal. Default is 0.

ROC MA Short signal : Minimum value of Rate of Change MA to send a SHORT signal. Default is 0.

TP activation in multiple of ATR : Threshold value to trigger trailing stop Take Profit. This threshold is calculated as multiple of the ATR (Average True Range). Default value is 5 meaning that to trigger the trailing TP the price need to move 5*ATR in the right direction.

Trailing TP in percentage : Percentage value of trailing Take Profit. This Trailing TP follows the profit if it increases, remaining selected percentage below it, but stops if the profit decreases. Default is 3%.

Fixed Ratio : This is the amount of gain or loss at which the order quantity is changed. Default is 400, which means that for each $400 gain or loss, the order size is increased or decreased by a user-selected amount.