SMA + RSI + Volume + ATR StrategySMA + RSI + Volume + ATR Strategy

1. Indicators Used:

SMA (Simple Moving Average): This is a trend-following indicator that calculates the average price of a security over a specified period (50 periods in this case). It's used to identify the overall trend of the market.

RSI (Relative Strength Index): This measures the speed and change of price movements. It tells us if the market is overbought (too high) or oversold (too low). Overbought is above 70 and oversold is below 30.

Volume: This is the amount of trading activity. A higher volume often indicates strong interest in a particular price move.

ATR (Average True Range): This measures volatility, or how much the price is moving in a given period. It helps us adjust stop losses and take profits based on market volatility.

2. Conditions for Entering Trades:

Buy Signal (Green Up Arrow):

Price is above the 50-period SMA (indicating an uptrend).

RSI is below 30 (indicating the market might be oversold or undervalued, signaling a potential reversal).

Current volume is higher than average volume (indicating strong interest in the move).

ATR is increasing (indicating higher volatility, suggesting that the market might be ready for a move).

Sell Signal (Red Down Arrow):

Price is below the 50-period SMA (indicating a downtrend).

RSI is above 70 (indicating the market might be overbought or overvalued, signaling a potential reversal).

Current volume is higher than average volume (indicating strong interest in the move).

ATR is increasing (indicating higher volatility, suggesting that the market might be ready for a move).

3. Take Profit & Stop Loss:

Take Profit: When a trade is made, the strategy will set a target price at a certain percentage above or below the entry price (1.5% in this case) to automatically exit the trade once that target is hit.

Stop Loss: If the price goes against the position, a stop loss is set at a percentage below or above the entry price (0.5% in this case) to limit losses.

4. Execution of Trades:

When the buy condition is met, the strategy will enter a long position (buying).

When the sell condition is met, the strategy will enter a short position (selling).

5. Visual Representation:

Green Up Arrow: Appears on the chart when the buy condition is met.

Red Down Arrow: Appears on the chart when the sell condition is met.

These arrows help you see at a glance when the strategy suggests you should buy or sell.

In Summary:

This strategy uses a combination of trend-following (SMA), momentum (RSI), volume, and volatility (ATR) to decide when to buy or sell a stock. It looks for opportunities when the market is either oversold (buy signal) or overbought (sell signal) and makes sure there’s enough volume and volatility to back up the move. It also includes take-profit and stop-loss levels to manage risk.

Cerca negli script per "profit"

Bollinger Bands Reversal Strategy Analyzer█ OVERVIEW

The Bollinger Bands Reversal Overlay is a versatile trading tool designed to help traders identify potential reversal opportunities using Bollinger Bands. It provides visual signals, performance metrics, and a detailed table to analyze the effectiveness of reversal-based strategies over a user-defined lookback period.

█ KEY FEATURES

Bollinger Bands Calculation

The indicator calculates the standard Bollinger Bands, consisting of:

A middle band (basis) as the Simple Moving Average (SMA) of the closing price.

An upper band as the basis plus a multiple of the standard deviation.

A lower band as the basis minus a multiple of the standard deviation.

Users can customize the length of the Bollinger Bands and the multiplier for the standard deviation.

Reversal Signals

The indicator identifies potential reversal signals based on the interaction between the price and the Bollinger Bands.

Two entry strategies are available:

Revert Cross: Waits for the price to close back above the lower band (for longs) or below the upper band (for shorts) after crossing it.

Cross Threshold: Triggers a signal as soon as the price crosses the lower band (for longs) or the upper band (for shorts).

Trade Direction

Users can select a trade bias:

Long: Focuses on bullish reversal signals.

Short: Focuses on bearish reversal signals.

Performance Metrics

The indicator calculates and displays the performance of trades over a user-defined lookback period ( barLookback ).

Metrics include:

Win Rate: The percentage of trades that were profitable.

Mean Return: The average return across all trades.

Median Return: The median return across all trades.

These metrics are calculated for each bar in the lookback period, providing insights into the strategy's performance over time.

Visual Signals

The indicator plots buy and sell signals on the chart:

Buy Signals: Displayed as green triangles below the price bars.

Sell Signals: Displayed as red triangles above the price bars.

Performance Table

A customizable table is displayed on the chart, showing the performance metrics for each bar in the lookback period.

The table includes:

Win Rate: Highlighted with gradient colors (green for high win rates, red for low win rates).

Mean Return: Colored based on profitability (green for positive returns, red for negative returns).

Median Return: Colored similarly to the mean return.

Time Filtering

Users can define a specific time window for the indicator to analyze trades, ensuring that performance metrics are calculated only for the desired period.

Customizable Display

The table's font size can be adjusted to suit the user's preference, with options for "Auto," "Small," "Normal," and "Large."

█ PURPOSE

The Bollinger Bands Reversal Overlay is designed to:

Help traders identify high-probability reversal opportunities using Bollinger Bands.

Provide actionable insights into the performance of reversal-based strategies.

Enable users to backtest and optimize their trading strategies by analyzing historical performance metrics.

█ IDEAL USERS

Swing Traders: Looking for reversal opportunities within a trend.

Mean Reversion Traders: Interested in trading price reversals to the mean.

Strategy Developers: Seeking to backtest and refine Bollinger Bands-based strategies.

Performance Analysts: Wanting to evaluate the effectiveness of reversal signals over time.

ATR-Based Suitability CheckerPurpose:

This indicator helps traders identify the most suitable timeframe for trading by comparing fees to market volatility (ATR). Instead of filtering out specific assets or strategies, it focuses on finding optimal trading conditions for the selected timeframe. It is designed to adapt dynamically, ensuring that traders can align their approach with the current market environment.

Key Features:

Dynamic ATR Analysis: Measures volatility using the Average True Range (ATR) and evaluates how fees impact potential profitability across timeframes.

Fee-to-ATR Ratio: Calculates the proportion of fees to ATR, highlighting conditions where fees are too large relative to price movements.

Visual Feedback: **Red Background:** Indicates unsuitable trading conditions where fees dominate. **Green Background:** Highlights suitable conditions for trading efficiency. Markers provide quick visual identification of suitability.

Custom Transparency: Enables users to adjust the background’s transparency for better chart visibility.

How to Use:

Timeframe Optimization: When volatility rises, price movements become larger, making shorter timeframes more suitable for trading. Conversely, during periods of low volatility, longer timeframes are preferable to avoid overtrading within a narrow price range.

Spot & Leverage Trading: For spot trading, this tool identifies conditions where fees (e.g., 0.25%-0.3%) might excessively impact profitability. For instance, if ATR is comparable to fees, the trading environment may not be ideal. In leveraged trading, the indicator helps assess whether the current volatility supports your chosen leverage level, ensuring that leverage does not amplify undue risks.

Efficiency Focus: The indicator emphasizes finding a balance between market conditions and your trading strategy. Not all timeframes need to be "suitable" at all times; instead, it highlights the best opportunities based on current market dynamics. Utilize the suitability ratio across different timeframes to guide and adjust your trading strategies effectively.

Input Parameters:

ATR Length: Defines the period for ATR calculation (default: 14).

Fee Percentage (%): Trading fee as a percentage of the closing price (default: 0.1%).

Unsuitable Threshold (% of 1 ATR): Sets the maximum acceptable fee-to-ATR ratio for suitable conditions (default: 20%).

Background Transparency (0-100): Adjusts the opacity of the background highlight (default: 80).

Who Should Use This:

This tool is ideal for traders seeking to align their strategy with market conditions by finding the most suitable timeframe. It applies to both spot and leveraged markets, helping optimize efficiency while managing fees and volatility.

Notes:

The ATR-Based Suitability Checker is a supplementary tool. Combine it with other forms of analysis for comprehensive decision-making.

Regularly adjust the parameters to match your trading preferences and market conditions.

MMXM ICT [TradingFinder] Market Maker Model PO3 CHoCH/CSID + FVG🔵 Introduction

The MMXM Smart Money Reversal leverages key metrics such as SMT Divergence, Liquidity Sweep, HTF PD Array, Market Structure Shift (MSS) or (ChoCh), CISD, and Fair Value Gap (FVG) to identify critical turning points in the market. Designed for traders aiming to analyze the behavior of major market participants, this setup pinpoints strategic areas for making informed trading decisions.

The document introduces the MMXM model, a trading strategy that identifies market maker activity to predict price movements. The model operates across five distinct stages: original consolidation, price run, smart money reversal, accumulation/distribution, and completion. This systematic approach allows traders to differentiate between buyside and sellside curves, offering a structured framework for interpreting price action.

Market makers play a pivotal role in facilitating these movements by bridging liquidity gaps. They continuously quote bid (buy) and ask (sell) prices for assets, ensuring smooth trading conditions.

By maintaining liquidity, market makers prevent scenarios where buyers are left without sellers and vice versa, making their activity a cornerstone of the MMXM strategy.

SMT Divergence serves as the first signal of a potential trend reversal, arising from discrepancies between the movements of related assets or indices. This divergence is detected when two or more highly correlated assets or indices move in opposite directions, signaling a likely shift in market trends.

Liquidity Sweep occurs when the market targets liquidity in specific zones through false price movements. This process allows major market participants to execute their orders efficiently by collecting the necessary liquidity to enter or exit positions.

The HTF PD Array refers to premium and discount zones on higher timeframes. These zones highlight price levels where the market is in a premium (ideal for selling) or discount (ideal for buying). These areas are identified based on higher timeframe market behavior and guide traders toward lucrative opportunities.

Market Structure Shift (MSS), also referred to as ChoCh, indicates a change in market structure, often marked by breaking key support or resistance levels. This shift confirms the directional movement of the market, signaling the start of a new trend.

CISD (Change in State of Delivery) reflects a transition in price delivery mechanisms. Typically occurring after MSS, CISD confirms the continuation of price movement in the new direction.

Fair Value Gap (FVG) represents zones where price imbalance exists between buyers and sellers. These gaps often act as price targets for filling, offering traders opportunities for entry or exit.

By combining all these metrics, the Smart Money Reversal provides a comprehensive tool for analyzing market behavior and identifying key trading opportunities. It enables traders to anticipate the actions of major players and align their strategies accordingly.

MMBM :

MMSM :

🔵 How to Use

The Smart Money Reversal operates in two primary states: MMBM (Market Maker Buy Model) and MMSM (Market Maker Sell Model). Each state highlights critical structural changes in market trends, focusing on liquidity behavior and price reactions at key levels to offer precise and effective trading opportunities.

The MMXM model expands on this by identifying five distinct stages of market behavior: original consolidation, price run, smart money reversal, accumulation/distribution, and completion. These stages provide traders with a detailed roadmap for interpreting price action and anticipating market maker activity.

🟣 Market Maker Buy Model

In the MMBM state, the market transitions from a bearish trend to a bullish trend. Initially, SMT Divergence between related assets or indices reveals weaknesses in the bearish trend. Subsequently, a Liquidity Sweep collects liquidity from lower levels through false breakouts.

After this, the price reacts to discount zones identified in the HTF PD Array, where major market participants often execute buy orders. The market confirms the bullish trend with a Market Structure Shift (MSS) and a change in price delivery state (CISD). During this phase, an FVG emerges as a key trading opportunity. Traders can open long positions upon a pullback to this FVG zone, capitalizing on the bullish continuation.

🟣 Market Maker Sell Model

In the MMSM state, the market shifts from a bullish trend to a bearish trend. Here, SMT Divergence highlights weaknesses in the bullish trend. A Liquidity Sweep then gathers liquidity from higher levels.

The price reacts to premium zones identified in the HTF PD Array, where major sellers enter the market and reverse the price direction. A Market Structure Shift (MSS) and a change in delivery state (CISD) confirm the bearish trend. The FVG then acts as a target for the price. Traders can initiate short positions upon a pullback to this FVG zone, profiting from the bearish continuation.

Market makers actively bridge liquidity gaps throughout these stages, quoting continuous bid and ask prices for assets. This ensures that trades are executed seamlessly, even during periods of low market participation, and supports the structured progression of the MMXM model.

The price’s reaction to FVG zones in both states provides traders with opportunities to reduce risk and enhance precision. These pullbacks to FVG zones not only represent optimal entry points but also create avenues for maximizing returns with minimal risk.

🔵 Settings

Higher TimeFrame PD Array : Selects the timeframe for identifying premium/discount arrays on higher timeframes.

PD Array Period : Specifies the number of candles for identifying key swing points.

ATR Coefficient Threshold : Defines the threshold for acceptable volatility based on ATR.

Max Swing Back Method : Choose between analyzing all swings ("All") or a fixed number ("Custom").

Max Swing Back : Sets the maximum number of candles to consider for swing analysis (if "Custom" is selected).

Second Symbol for SMT : Specifies the second asset or index for detecting SMT divergence.

SMT Fractal Periods : Sets the number of candles required to identify SMT fractals.

FVG Validity Period : Defines the validity duration for FVG zones.

MSS Validity Period : Sets the validity duration for MSS zones.

FVG Filter : Activates filtering for FVG zones based on width.

FVG Filter Type : Selects the filtering level from "Very Aggressive" to "Very Defensive."

Mitigation Level FVG : Determines the level within the FVG zone (proximal, 50%, or distal) that price reacts to.

Demand FVG : Enables the display of demand FVG zones.

Supply FVG : Enables the display of supply FVG zones.

Zone Colors : Allows customization of colors for demand and supply FVG zones.

Bottom Line & Label : Enables or disables the SMT divergence line and label from the bottom.

Top Line & Label : Enables or disables the SMT divergence line and label from the top.

Show All HTF Levels : Displays all premium/discount levels on higher timeframes.

High/Low Levels : Activates the display of high/low levels.

Color Options : Customizes the colors for high/low lines and labels.

Show All MSS Levels : Enables display of all MSS zones.

High/Low MSS Levels : Activates the display of high/low MSS levels.

Color Options : Customizes the colors for MSS lines and labels.

🔵 Conclusion

The Smart Money Reversal model represents one of the most advanced tools for technical analysis, enabling traders to identify critical market turning points. By leveraging metrics such as SMT Divergence, Liquidity Sweep, HTF PD Array, MSS, CISD, and FVG, traders can predict future price movements with precision.

The price’s interaction with key zones such as PD Array and FVG, combined with pullbacks to imbalance areas, offers exceptional opportunities with favorable risk-to-reward ratios. This approach empowers traders to analyze the behavior of major market participants and adopt professional strategies for entry and exit.

By employing this analytical framework, traders can reduce errors, make more informed decisions, and capitalize on profitable opportunities. The Smart Money Reversal focuses on liquidity behavior and structural changes, making it an indispensable tool for financial market success.

On-Chain Analysis [LuxAlgo]The On-Chain Analysis tool offers a comprehensive overview of essential on-chain metrics, enabling traders and investors to grasp the underlying activity and sentiment within the cryptocurrency market. By integrating metrics like wallet profitability, exchange flows, on-chain volume, social sentiment, and more into your charts, users can gain valuable insights into cryptocurrency network behavior, spot emerging trends, and better manage risk in the cryptocurrency market.

🔶 USAGE

🔹 On-Chain Analysis

When analyzing cryptocurrencies, several fundamental metrics are crucial for assessing the value and potential of a digital asset. This indicator is designed to help traders and analysts evaluate the markets by utilizing various data gathered directly from the blockchain. The gathered on-chain data includes wallet profitability, exchange flows, miner flows, on-chain volume, large buyers/sellers, market capitalization, market dominance, active addresses, total value locked (TVL), market value to realized value (MVRV), developer activity, social sentiment, holder behavior, and balance types.

Use wallet profitability and social sentiment metrics to gauge the overall mood of the market, helping to anticipate potential buying or selling pressure.

On-chain volume and active addresses provide insights into how actively a cryptocurrency is being used, indicating network health and adoption levels.

By tracking exchange flows and holder balance types, you can identify significant moves by whales or institutions, which may signal upcoming price shifts.

Market capitalization and miner flows give you an understanding of the supply side of the market, aiding in evaluating whether an asset is overvalued or undervalued.

The distribution of holdings among retail investors, whales, and institutional groups can greatly influence market dynamics. A large concentration of holdings by whales may indicate the potential for significant price swings, given their capacity to execute substantial trades. A higher proportion of institutional investors often suggests confidence in the asset's long-term potential, as these entities typically conduct thorough research before investing. While retail participation indicates broader adoption, it also introduces higher volatility, as these investors tend to be more reactive to market fluctuations.

Understanding the balance and behavior of short-term traders, mid-term cruisers, and long-term hodlers helps traders and analysts predict market trends and assess the underlying confidence in a particular cryptocurrency.

🔶 DETAILS

This script includes some of the most significant and insightful metrics in the crypto space, designed to evaluate and enhance trading decisions by assessing the value and growth potential of cryptocurrencies. The introduced metrics are:

🔹 Wallet Profitability

Definition: Represents the percentage distribution of addresses by profitability at the current price.

Importance: Indicates potential selling pressure or reduced selling pressure based on whether addresses are in profit or loss.

🔹 Exchange Flow

Definition: The total amount of a cryptocurrency moving in and out of exchanges.

Importance: Large inflows to exchanges can indicate potential selling pressure, while large outflows might suggest accumulation or long-term holding.

🔹 Miner Flow

Definition: Tracks the inflow and outflow of funds by miners.

Importance: High inflows could indicate selling pressure, whereas low inflows or outflows might reflect miner confidence.

🔹 On-Chain Volume

Definition: The total value of transactions conducted on a blockchain within a specific period.

Importance: On-chain volume reflects actual usage of the network, indicating how actively a cryptocurrency is being utilized for transactions.

🔹 Large Buyers/Sellers

Definition: Tracks the number of large buyers (bulls) and sellers (bears) based on transaction volume.

Importance: Comparing the number of large buyers (bulls) to large sellers (bears) helps gauge market trends and sentiment.

🔹 Market Capitalization

Definition: The total value of a cryptocurrency's circulating supply, calculated by multiplying the current price by the total supply.

Importance: Market cap is a key indicator of a cryptocurrency’s size and market dominance. It helps compare the relative size of different cryptocurrencies.

🔹 Market Dominance

Definition: Market dominance represents a cryptocurrency’s share of the total market capitalization of all cryptocurrencies. It is calculated by dividing the market cap of the cryptocurrency by the total market cap of the cryptocurrency market.

Importance: Market dominance is a crucial indicator of a cryptocurrency's influence and relative position in the market. It helps assess the strength of a cryptocurrency compared to others and provides insights into its market presence and potential influence.

Special Consideration: Since BTC and ETH dominance is relatively high compared to other cryptocurrencies, specific adjustments are made during the presentation of values and charts. When analyzing BTC, the total market capitalization is used. For ETH analysis, BTC is excluded from the total market cap. For any other cryptocurrency besides BTC and ETH, both BTC and ETH are excluded from the total market cap to provide a more accurate view.

🔹 Active Addresses

Definition: The number of unique addresses involved in transactions within a specific period.

Importance: A higher number of active addresses suggests greater network activity and user adoption, which can be a sign of a healthy ecosystem.

🔹 Total Value Locked (TVL)

Definition: The total value of assets locked in a decentralized finance (DeFi) protocol.

Importance: TVL is a key metric for DeFi platforms, indicating the level of trust and the amount of liquidity in a protocol.

🔹 Market Value to Realized Value (MVRV)

Definition: A ratio comparing the market cap to realized cap.

Importance: A high ratio may indicate overvaluation (potential selling), while a low ratio could signal undervaluation (potential buying).

🔹 Developer Activity

Definition: The level of activity on a cryptocurrency’s public repositories (e.g., GitHub).

Importance: Strong developer activity is a sign of ongoing innovation, updates, and a healthy project.

🔹 Social Sentiment

Definition: The general sentiment or mood of the community and investors as expressed on social media and forums.

Importance: Positive sentiment often correlates with price increases, while negative sentiment can signal potential downtrends.

🔹 Holder Balance (Behavior)

Definition: Distribution of addresses by holding behavior: Traders (short-term), Cruisers (mid-term), and Hodlers (long-term).

Importance: Helps predict market behavior based on different holder types.

🔹 Holder Balance (Type)

Definition: Distribution of cryptocurrency holdings among Retail (small holders), Whales (large holders), and Investors (institutional players).

Importance: Assesses the potential impact of different user groups on the market. A more decentralized distribution is generally viewed as positive, reducing the risk of price manipulation by large holders.

These metrics provide a comprehensive view of a cryptocurrency’s health, adoption, and potential for growth, making them essential for fundamental analysis in the crypto space.

🔶 SETTINGS

The script offers a range of customizable settings to tailor the analysis to your trading needs.

🔹 On-Chain Analysis

On-Chain Data: Choose the specific on-chain metric from the drop-down menu. Options include Wallet Profitability, Exchange Flow, Miner Flow, On-Chain Volume, Large Buyers/Sellers (Volume), Market Capitalization, Market Dominance, Active Addresses, Total Value Locked, Market Value to Realized Value, Developer Activity, Social Sentiment, Holder Balance (Behavior), and Holder Balance (Type).

Smoothing: Set the smoothing level to refine the displayed data. This can help in filtering out noise and getting a clearer view of trends.

Signal Line: Choose a signal line type (SMA, EMA, RMA, or None) and the length of the moving average for signal line calculation.

🔹 On-Chain Dashboard

On-Chain Stats: Toggle the display of the on-chain statistics.

Dashboard Size, Position, and Colors: Customize the size, position, and colors of the on-chain dashboard on the chart.

🔶 LIMITATIONS

Availability of on-chain data may vary and may not be accessible for all crypto assets.

🔶 RELATED SCRIPTS

Market-Sentiment-Technicals

Bullish Reversal Bar Strategy [Skyrexio]Overview

Bullish Reversal Bar Strategy leverages the combination of candlestick pattern Bullish Reversal Bar (description in Methodology and Justification of Methodology), Williams Alligator indicator and Williams Fractals to create the high probability setups. Candlestick pattern is used for the entering into trade, while the combination of Williams Alligator and Fractals is used for the trend approximation as close condition. Strategy uses only long trades.

Unique Features

No fixed stop-loss and take profit: Instead of fixed stop-loss level strategy utilizes technical condition obtained by Fractals and Alligator or the candlestick pattern invalidation to identify when current uptrend is likely to be over (more information in "Methodology" and "Justification of Methodology" paragraphs)

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Trend Trade Filter: strategy uses Alligator and Fractal combination as high probability trend filter.

Methodology

The strategy opens long trade when the following price met the conditions:

1.Current candle's high shall be below the Williams Alligator's lines (Jaw, Lips, Teeth)(all details in "Justification of Methodology" paragraph)

2.Price shall create the candlestick pattern "Bullish Reversal Bar". Optionally if MFI and AO filters are enabled current candle shall have the decreasing AO and at least one of three recent bars shall have the squat state on the MFI (all details in "Justification of Methodology" paragraph)

3.If price breaks through the high of the candle marked as the "Bullish Reversal Bar" the long trade is open at the price one tick above the candle's high

4.Initial stop loss is placed at the Bullish Reversal Bar's candle's low

5.If price hit the Bullish Reversal Bar's low before hitting the entry price potential trade is cancelled

6.If trade is active and initial stop loss has not been hit, trade is closed when the combination of Alligator and Williams Fractals shall consider current trend change from upward to downward.

Strategy settings

In the inputs window user can setup strategy setting:

Enable MFI (if true trades are filtered using Market Facilitation Index (MFI) condition all details in "Justification of Methodology" paragraph), by default = false)

Enable AO (if true trades are filtered using Awesome Oscillator (AO) condition all details in "Justification of Methodology" paragraph), by default = false)

Justification of Methodology

Let's explore the key concepts of this strategy and understand how they work together. The first and key concept is the Bullish Reversal Bar candlestick pattern. This is just the single bar pattern. The rules are simple:

Candle shall be closed in it's upper half

High of this candle shall be below all three Alligator's lines (Jaw, Lips, Teeth)

Next, let’s discuss the short-term trend filter, which combines the Williams Alligator and Williams Fractals. Williams Alligator

Developed by Bill Williams, the Alligator is a technical indicator that identifies trends and potential market reversals. It consists of three smoothed moving averages:

Jaw (Blue Line): The slowest of the three, based on a 13-period smoothed moving average shifted 8 bars ahead.

Teeth (Red Line): The medium-speed line, derived from an 8-period smoothed moving average shifted 5 bars forward.

Lips (Green Line): The fastest line, calculated using a 5-period smoothed moving average shifted 3 bars forward.

When the lines diverge and align in order, the "Alligator" is "awake," signaling a strong trend. When the lines overlap or intertwine, the "Alligator" is "asleep," indicating a range-bound or sideways market. This indicator helps traders determine when to enter or avoid trades.

Fractals, another tool by Bill Williams, help identify potential reversal points on a price chart. A fractal forms over at least five consecutive bars, with the middle bar showing either:

Up Fractal: Occurs when the middle bar has a higher high than the two preceding and two following bars, suggesting a potential downward reversal.

Down Fractal: Happens when the middle bar shows a lower low than the surrounding two bars, hinting at a possible upward reversal.

Traders often use fractals alongside other indicators to confirm trends or reversals, enhancing decision-making accuracy.

How do these tools work together in this strategy? Let’s consider an example of an uptrend.

When the price breaks above an up fractal, it signals a potential bullish trend. This occurs because the up fractal represents a shift in market behavior, where a temporary high was formed due to selling pressure. If the price revisits this level and breaks through, it suggests the market sentiment has turned bullish.

The breakout must occur above the Alligator’s teeth line to confirm the trend. A breakout below the teeth is considered invalid, and the downtrend might still persist. Conversely, in a downtrend, the same logic applies with down fractals.

How we can use all these indicators in this strategy? This strategy is a counter trend one. Candle's high shall be below all Alligator's lines. During this market stage the bullish reversal bar candlestick pattern shall be printed. This bar during the downtrend is a high probability setup for the potential reversal to the upside: bulls were able to close the price in the upper half of a candle. The breaking of its high is a high probability signal that trend change is confirmed and script opens long trade. If market continues going down and break down the bullish reversal bar's low potential trend change has been invalidated and strategy close long trade.

If market really reversed and started moving to the upside strategy waits for the trend change form the downtrend to the uptrend according to approximation of Alligator and Fractals combination. If this change happens strategy close the trade. This approach helps to stay in the long trade while the uptrend continuation is likely and close it if there is a high probability of the uptrend finish.

Optionally users can enable MFI and AO filters. First of all, let's briefly explain what are these two indicators. The Awesome Oscillator (AO), created by Bill Williams, is a momentum-based indicator that evaluates market momentum by comparing recent price activity to a broader historical context. It assists traders in identifying potential trend reversals and gauging trend strength.

AO = SMA5(Median Price) − SMA34(Median Price)

where:

Median Price = (High + Low) / 2

SMA5 = 5-period Simple Moving Average of the Median Price

SMA 34 = 34-period Simple Moving Average of the Median Price

This indicator is filtering signals in the following way: if current AO bar is decreasing this candle can be interpreted as a bullish reversal bar. This logic is applicable because initially this strategy is a trend reversal, it is searching for the high probability setup against the current trend. Decreasing AO is the additional high probability filter of a downtrend.

Let's briefly look what is MFI. The Market Facilitation Index (MFI) is a technical indicator that measures the price movement per unit of volume, helping traders gauge the efficiency of price movement in relation to trading volume. Here's how you can calculate it:

MFI = (High−Low)/Volume

MFI can be used in combination with volume, so we can divide 4 states. Bill Williams introduced these to help traders interpret the interaction between volume and price movement. Here’s a quick summary:

Green Window (Increased MFI & Increased Volume): Indicates strong momentum with both price and volume increasing. Often a sign of trend continuation, as both buying and selling interest are rising.

Fake Window (Increased MFI & Decreased Volume): Shows that price is moving but with lower volume, suggesting weak support for the trend. This can signal a potential end of the current trend.

Squat Window (Decreased MFI & Increased Volume): Shows high volume but little price movement, indicating a tug-of-war between buyers and sellers. This often precedes a breakout as the pressure builds.

Fade Window (Decreased MFI & Decreased Volume): Indicates a lack of interest from both buyers and sellers, leading to lower momentum. This typically happens in range-bound markets and may signal consolidation before a new move.

For our purposes we are interested in squat bars. This is the sign that volume cannot move the price easily. This type of bar increases the probability of trend reversal. In this indicator we added to enable the MFI filter of reversal bars. If potential reversal bar or two preceding bars have squat state this bar can be interpret as a reversal one.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2024.12.31. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 50%

Maximum Single Position Loss: -5.29%

Maximum Single Profit: +29.99%

Net Profit: +5472.66 USDT (+54.73%)

Total Trades: 103 (33.98% win rate)

Profit Factor: 1.634

Maximum Accumulated Loss: 1231.15 USDT (-8.32%)

Average Profit per Trade: 53.13 USDT (+0.94%)

Average Trade Duration: 76 hours

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 4h ETH/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

Financials Score All Description of the "Financials Score All" Script

This Pine Script calculates a financial score for a specific stock, based on various financial metrics. The purpose is to provide a comprehensive numerical score that reflects the financial health of the stock. The score is calculated using multiple financial indicators, including profitability, valuation, debt management, and liquidity. Here’s a breakdown of what each part of the script does:

period = input.string('FQ', 'Period', options= )

FQ refers to Quarterly financial data.

FY refers to Fiscal Year financial data.

Financial Metrics:

The script uses various financial metrics to calculate the score. These are obtained via request.financial, which retrieves financial data for the stock from TradingView's database. Below are the metrics used:

opmar (Operating Margin): Measures the company's profitability as a percentage of revenue.

eps (Earnings Per Share): Represents the portion of a company's profit allocated to each outstanding share.

eps_ttm (Earnings Per Share – Trailing Twelve Months): EPS over the most recent 12 months.

pe_ratio (Price-to-Earnings Ratio): A measure of the price investors are willing to pay for a stock relative to its earnings.

pb_ratio (Price-to-Book Ratio): A valuation ratio comparing a company’s market value to its book value.

de_ratio (Debt-to-Equity Ratio): A measure of the company’s financial leverage, showing how much debt it has compared to shareholders' equity.

roe_pb (Return on Equity Adjusted to Book): Measures the company's profitability relative to its book value.

fcf_per_share (Free Cash Flow per Share): Represents the free cash flow available for dividends, debt reduction, or reinvestment, per share.

pfcf_ratio (Price-to-Free-Cash-Flow Ratio): A measure comparing a company’s market value to its free cash flow.

current_ratio (Current Ratio): A liquidity ratio that measures a company's ability to pay short-term obligations with its current assets.

RSI Calculation:

The script calculates the Relative Strength Index (RSI) for the stock using an 8-period lookback:

rsi = ta.rsi(close, 8)

Score Calculation:

The script calculates a total score by adding points based on the values of the financial metrics. Each metric is checked against a condition, and if the condition is met, the score is incremented:

If the Operating Margin (opmar) is greater than 20, the score is incremented by 20 points.

If Earnings Per Share (EPS) is positive, 10 points are added.

If the P/E ratio is between 0 and 20, 10 points are added.

If the P/B ratio is less than 3, 10 points are added.

If the Debt-to-Equity ratio is less than 0.8, 10 points are added.

If the Return on Equity Adjusted to Book is greater than 10, 10 points are added.

If the P/FCF ratio is between 0 and 15, 10 points are added.

If the Current Ratio is greater than 1.61, 10 points are added.

If the RSI is less than 35, 10 points are added.

The score is accumulated based on these conditions and stored in the total_score variable.

Displaying the Total Score:

Finally, the total score is plotted on the chart:

Summary of How It Works:

This script calculates a financial score for a stock using a variety of financial indicators. Each metric has a threshold, and when the stock meets certain criteria (for example, a good operating margin, a healthy debt-to-equity ratio, or a low P/E ratio), points are added to the overall score. The result is a single numerical value that reflects the financial health of the stock.

This score can help traders or investors identify companies with strong financials, or serve as a comparison tool between different stocks based on their financial health.

Generally >60 is the best stocks for med and long term trades

Omega_galskyThe strategy uses three Exponential Moving Averages (EMAs) — EMA8, EMA21, and EMA89 — to decide when to open buy or sell trades. It also includes a mechanism to move the Stop Loss (SL) to the Break-Even (BE) point, which is the entry price, once the price reaches a Risk-to-Reward (R2R) ratio of 1:1.

Key Steps:

Calculating EMAs: The script computes the EMA values for the specified periods. These help identify market trends and potential entry points.

Buy Conditions:

EMA8 crosses above EMA21.

The candle that causes the crossover is green (closing price is higher than the opening price).

The closing price is above EMA89.

If all conditions are met, a buy order is executed.

Sell Conditions:

EMA8 crosses below EMA21.

The candle that causes the crossover is red (closing price is lower than the opening price).

The closing price is below EMA89.

If all conditions are met, a sell order is executed.

Stop Loss and Take Profit:

Initial Stop Loss and Take Profit levels are calculated based on the entry price and a percentage defined by the user.

These levels help protect against large losses and lock in profits.

Break-Even Logic:

When the price moves favorably to reach a 1:1 R2R ratio:

For a buy trade, the Stop Loss is moved to the entry price if the price increases sufficiently.

For a sell trade, the Stop Loss is moved to the entry price if the price decreases sufficiently.

This ensures the trade is risk-free after the price reaches the predefined level.

Visual Representation:

The EMAs are plotted on the chart for easy visualization of trends and crossovers.

Entry and exit points are also marked on the chart to track trades.

Purpose:

The strategy is designed to capitalize on EMA crossovers while minimizing risks using Break-Even logic and predefined Stop Loss/Take Profit levels. It automates decision-making for trend-following traders and ensures disciplined risk management.

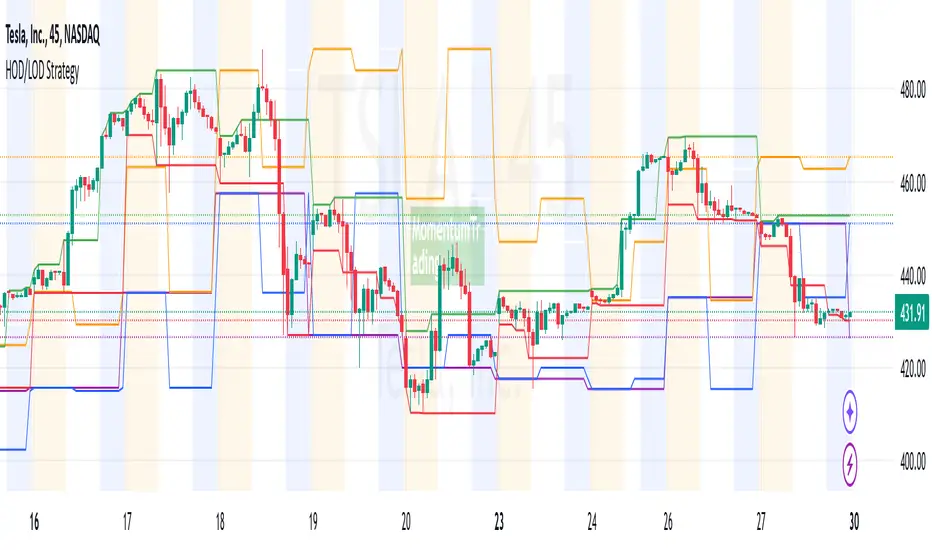

HOD/LOD/PMH/PML/PDH/PDL Strategy by @tradingbauhaus This script is a trading strategy @tradingbauhaus designed to trade based on key price levels, such as the High of Day (HOD), Low of Day (LOD), Premarket High (PMH), Premarket Low (PML), Previous Day High (PDH), and Previous Day Low (PDL). Below, I’ll explain in detail what the script does:

Core Functionality of the Script:

Calculates Key Price Levels:

HOD (High of Day): The highest price of the current day.

LOD (Low of Day): The lowest price of the current day.

PMH (Premarket High): The highest price during the premarket session (before the market opens).

PML (Premarket Low): The lowest price during the premarket session.

PDH (Previous Day High): The highest price of the previous day.

PDL (Previous Day Low): The lowest price of the previous day.

Draws Horizontal Lines on the Chart:

Plots horizontal lines on the chart for each key level (HOD, LOD, PMH, PML, PDH, PDL) with specific colors for easy visual identification.

Defines Entry and Exit Rules:

Long Entry (Buy): If the price crosses above the PMH (Premarket High) or the PDH (Previous Day High).

Short Entry (Sell): If the price crosses below the PML (Premarket Low) or the PDL (Previous Day Low).

Long Exit: If the price reaches the HOD (High of Day) during a long position.

Short Exit: If the price reaches the LOD (Low of Day) during a short position.

How the Script Works Step by Step:

Calculates Key Levels:

Uses the request.security function to fetch the HOD and LOD of the current day, as well as the highs and lows of the previous day (PDH and PDL).

Calculates the PMH and PML during the premarket session (before 9:30 AM).

Plots Levels on the Chart:

Uses the plot function to draw horizontal lines on the chart representing the key levels (HOD, LOD, PMH, PML, PDH, PDL).

Each level has a specific color for easy identification:

HOD: White.

LOD: Purple.

PDH: Orange.

PDL: Blue.

PMH: Green.

PML: Red.

Defines Trading Rules:

Uses conditions with ta.crossover and ta.crossunder to detect when the price crosses key levels.

Long Entry: If the price crosses above the PMH or PDH, a long position (buy) is opened.

Short Entry: If the price crosses below the PML or PDL, a short position (sell) is opened.

Long Exit: If the price reaches the HOD during a long position, the position is closed.

Short Exit: If the price reaches the LOD during a short position, the position is closed.

Executes Orders Automatically:

Uses the strategy.entry and strategy.close functions to open and close positions automatically based on the defined rules.

Advantages of This Strategy:

Based on Key Levels: Uses important price levels that often act as support and resistance.

Easy to Visualize: Horizontal lines on the chart make it easy to identify levels.

Automated: Entries and exits are executed automatically based on the defined rules.

Limitations of This Strategy:

Dependent on Volatility: Works best in markets with significant price movements.

False Crosses: There may be false crosses that generate incorrect signals.

No Advanced Risk Management: Does not include dynamic stop-loss or take-profit mechanisms.

How to Improve the Strategy:

Add Stop-Loss and Take-Profit: To limit losses and lock in profits.

Filter Signals with Indicators: Use RSI, MACD, or other indicators to confirm signals.

Optimize Levels: Adjust key levels based on the asset’s behavior.

In summary, this script is a trading strategy that operates based on key price levels, such as HOD, LOD, PMH, PML, PDH, and PDL. It is useful for traders who want to trade based on significant support and resistance levels.

Ultra Trade JournalThe Ultra Trade Journal is a powerful TradingView indicator designed to help traders meticulously document and analyze their trades. Whether you're a novice or an experienced trader, this tool offers a clear and organized way to visualize your trading strategy, monitor performance, and make informed decisions based on detailed trade metrics.

Detailed Description

The Ultra Trade Journal indicator allows users to input and visualize critical trade information directly on their TradingView charts.

.........

User Inputs

Traders can specify entry and exit prices , stop loss levels, and up to four take profit targets.

.....

Dynamic Plotting

Once the input values are set, the indicator automatically plots horizontal lines for entry, exit, stop loss, and each take profit level on the chart. These lines are visually distinct, using different colors and styles (solid, dashed, dotted) to represent each element clearly.

.....

Live Position Tracking

If enabled, the indicator can adjust the exit price in real-time based on the current market price, allowing traders to monitor live positions effectively.

.....

Tick Calculations

The script calculates the number of ticks between the entry price and each exit point (stop loss and take profits). This helps in understanding the movement required for each target and assessing the potential risk and reward.

.....

Risk-Reward Ratios

For each take profit level, the indicator computes the risk-reward (RR) ratio by comparing the ticks at each target against the stop loss ticks. This provides a quick view of the potential profitability versus the risk taken.

.....

Comprehensive Table Display

A customizable table is displayed on the chart, summarizing all key trade details. This includes the entry and exit prices, stop loss and take profit levels, tick counts, and their respective RR ratios.

Users can adjust the table's Position and text color to suit their preferences.

.....

Visual Enhancements

The indicator uses adjustable background shading between entry and stop loss/take profit lines to visually represent potential trade outcomes. This shading adjusts based on whether the trade is long or short, providing an intuitive understanding of trade performance.

.........

Overall, the Ultra Trade Journal combines visual clarity with detailed analytics, enabling traders to keep a well-organized record of their trades and enhance their trading strategies through insightful data.

Smart DCA Strategy (Public)INSPIRATION

While Dollar Cost Averaging (DCA) is a popular and stress-free investment approach, I noticed an opportunity for enhancement. Standard DCA involves buying consistently, regardless of market conditions, which can sometimes mean missing out on optimal investment opportunities. This led me to develop the Smart DCA Strategy – a 'set and forget' method like traditional DCA, but with an intelligent twist to boost its effectiveness.

The goal was to build something more profitable than a standard DCA strategy so it was equally important that this indicator could backtest its own results in an A/B test manner against the regular DCA strategy.

WHY IS IT SMART?

The key to this strategy is its dynamic approach: buying aggressively when the market shows signs of being oversold, and sitting on the sidelines when it's not. This approach aims to optimize entry points, enhancing the potential for better returns while maintaining the simplicity and low stress of DCA.

WHAT THIS STRATEGY IS, AND IS NOT

This is an investment style strategy. It is designed to improve upon the common standard DCA investment strategy. It is therefore NOT a day trading strategy. Feel free to experiment with various timeframes, but it was designed to be used on a daily timeframe and that's how I recommend it to be used.

You may also go months without any buy signals during bull markets, but remember that is exactly the point of the strategy - to keep your buying power on the sidelines until the markets have significantly pulled back. You need to be patient and trust in the historical backtesting you have performed.

HOW IT WORKS

The Smart DCA Strategy leverages a creative approach to using Moving Averages to identify the most opportune moments to buy. A trigger occurs when a daily candle, in its entirety including the high wick, closes below the threshold line or box plotted on the chart. The indicator is designed to facilitate both backtesting and live trading.

HOW TO USE

Settings:

The input parameters for tuning have been intentionally simplified in an effort to prevent users falling into the overfitting trap.

The main control is the Buying strictness scale setting. Setting this to a lower value will provide more buying days (less strict) while higher values mean less buying days (more strict). In my testing I've found level 9 to provide good all round results.

Validation days is a setting to prevent triggering entries until the asset has spent a given number of days (candles) in the overbought state. Increasing this makes entries stricter. I've found 0 to give the best results across most assets.

In the backtest settings you can also configure how much to buy for each day an entry triggers. Blind buy size is the amount you would buy every day in a standard DCA strategy. Smart buy size is the amount you would buy each day a Smart DCA entry is triggered.

You can also experiment with backtesting your strategy over different historical datasets by using the Start date and End date settings. The results table will not calculate for any trades outside what you've set in the date range settings.

Backtesting:

When backtesting you should use the results table on the top right to tune and optimise the results of your strategy. As with all backtests, be careful to avoid overfitting the parameters. It's better to have a setup which works well across many currencies and historical periods than a setup which is excellent on one dataset but bad on most others. This gives a much higher probability that it will be effective when you move to live trading.

The results table provides a clear visual representation as to which strategy, standard or smart, is more profitable for the given dataset. You will notice the columns are dynamically coloured red and green. Their colour changes based on which strategy is more profitable in the A/B style backtest - green wins, red loses. The key metrics to focus on are GOA (Gain on Account) and Avg Cost.

Live Trading:

After you've finished backtesting you can proceed with configuring your alerts for live trading.

But first, you need to estimate the amount you should buy on each Smart DCA entry. We can use the Total invested row in the results table to calculate this. Assuming we're looking to trade on

BTCUSD

Decide how much USD you would spend each day to buy BTC if you were using a standard DCA strategy. Lets say that is $5 per day

Enter that USD amount in the Blind buy size settings box

Check the Blind Buy column in the results table. If we set the backtest date range to the last 10 years, we would expect the amount spent on blind buys over 10 years to be $18,250 given $5 each day

Next we need to tweak the value of the Smart buy size parameter in setting to get it as close as we can to the Total Invested amount for Blind Buy

By following this approach it means we will invest roughly the same amount into our Smart DCA strategy as we would have into a standard DCA strategy over any given time period.

After you have calculated the Smart buy size, you can go ahead and set up alerts on Smart DCA buy triggers.

BOT AUTOMATION

In an effort to maintain the 'set and forget' stress-free benefits of a standard DCA strategy, I have set my personal Smart DCA Strategy up to be automated. The bot runs on AWS and I have a fully functional project for the bot on my GitHub account. Just reach out if you would like me to point you towards it. You can also hook this into any other 3rd party trade automation system of your choice using the pre-configured alerts within the indicator.

PLANNED FUTURE DEVELOPMENTS

Currently this is purely an accumulation strategy. It does not have any sell signals right now but I have ideas on how I will build upon it to incorporate an algorithm for selling. The strategy should gradually offload profits in bull markets which generates more USD which gives more buying power to rinse and repeat the same process in the next cycle only with a bigger starting capital. Watch this space!

MARKETS

Crypto:

This strategy has been specifically built to work on the crypto markets. It has been developed, backtested and tuned against crypto markets and I personally only run it on crypto markets to accumulate more of the coins I believe in for the long term. In the section below I will provide some backtest results from some of the top crypto assets.

Stocks:

I've found it is generally more profitable than a standard DCA strategy on the majority of stocks, however the results proved to be a lot more impressive on crypto. This is mainly due to the volatility and cycles found in crypto markets. The strategy makes its profits from capitalising on pullbacks in price. Good stocks on the other hand tend to move up and to the right with less significant pullbacks, therefore giving this strategy less opportunity to flourish.

Forex:

As this is an accumulation style investment strategy, I do not recommend that you use it to trade Forex.

For more info about this strategy including backtest results, please see the full description on the invite only version of this strategy named "Smart DCA Strategy"

IU Opening range Breakout StrategyIU Opening Range Breakout Strategy

This Pine Script strategy is designed to capitalize on the breakout of the opening range, which is a popular trading approach. The strategy identifies the high and low prices of the opening session and takes trades based on price crossing these levels, with built-in risk management and trade limits for intraday trading.

Key Features:

1. Risk Management:

- Risk-to-Reward Ratio (RTR):

Set a customizable risk-to-reward ratio to calculate target prices based on stop-loss levels.

Default: 2:1

- Max Trades in a Day:

Specify the maximum number of trades allowed per day to avoid overtrading.

Default: 2 trades in a day.

- End-of-Day Close:

Automatically closes all open positions at a user-defined session end time to ensure no overnight exposure.

Default: 3:15 PM

2. Opening Range Identification

- Opening Range High and Low:

The script detects the high and low of the first trading session using Pine Script's session functions.

These levels are plotted as visual guides on the chart:

- High: Lime-colored circles.

- Low: Red-colored circles.

3. Trade Entry Logic

- Long Entry:

A long trade is triggered when the price closes above the opening range high.

- Entry condition: Crossover of the price above the opening range high.

-Short Entry:

A short trade is triggered when the price closes below the opening range low.

- Entry condition: Crossunder of the price below the opening range low.

Both entries are conditional on the absence of an existing position.

4. Stop Loss and Take Profit

- Long Position:

- Stop Loss: Previous candle's low.

- Take Profit: Calculated based on the RTR.

- **Short Position:**

- **Stop Loss:** Previous candle's high.

- **Take Profit:** Calculated based on the RTR.

The strategy plots these levels for visual reference:

- Stop Loss: Red dashed lines.

- Take Profit: Green dashed lines.

5. Visual Enhancements

-Trade Level Highlighting:

The script dynamically shades the areas between the entry price and SL/TP levels:

- Red shading for the stop-loss region.

- Green shading for the take-profit region.

- Entry Price Line:

A silver-colored line marks the average entry price for active trades.

How to Use:

1.Input Configuration:

Adjust the Risk-to-Reward ratio, max trades per day, and session end time to suit your trading preferences.

2.Visual Cues:

Use the opening range high/low lines and shading to identify potential breakout opportunities.

3.Execution:

The strategy will automatically enter and exit trades based on the conditions. Review the plotted SL and TP levels to monitor the risk-reward setup.

Important Notes:

- This strategy is designed for intraday trading and works best in markets with high volatility during the opening session.

- Backtest the strategy on your preferred market and timeframe to ensure compatibility.

- Proper risk management and position sizing are essential when using this strategy in live markets.

Optimal MA FinderIntroduction to the "Optimal MA Finder" Indicator

The "Optimal MA Finder" is a powerful and versatile tool designed to help traders optimize their moving average strategies. This script combines flexibility, precision, and automation to identify the most effective moving average (MA) length for your trading approach. Whether you're aiming to improve your long-only strategy or implement a buy-and-sell methodology, the "Optimal MA Finder" is your go-to solution for enhanced decision-making.

What Does It Do?

The script evaluates a wide range of moving average lengths, from 10 to 500, to determine which one produces the best results based on historical data. By calculating critical metrics such as the total number of trades and the profit factor for each MA length, it identifies the one that maximizes profitability. It supports both simple moving averages (SMA) and exponential moving averages (EMA), allowing you to tailor the analysis to your preferred method.

The logic works by backtesting each MA length against the price data and assessing the performance under two strategies:

Buy & Sell: Includes both long and short trades.

Long Only: Focuses solely on long positions for more conservative strategies.

Once the optimal MA length is identified, the script overlays it on the chart, highlighting periods when the price crosses over or under the optimal MA, helping traders identify potential entry and exit points.

Why Is It Useful?

This indicator stands out for its ability to automate a task that is often labor-intensive and subjective: finding the best MA length. By providing a clear, data-driven answer, it saves traders countless hours of manual testing while significantly enhancing the accuracy of their strategies. For example, instead of guessing whether a 50-period EMA is more effective than a 200-period SMA, the "Optimal MA Finder" will pinpoint the exact length and type of MA that has historically yielded the best results for your chosen strategy.

Key Benefits:

Precision: Identifies the MA length with the highest profit factor for maximum profitability.

Automation: Conducts thorough backtesting without manual effort.

Flexibility: Adapts to your preferred MA type (SMA or EMA) and trading strategy (Buy & Sell or Long Only).

Real-Time Feedback: Provides actionable insights by plotting the optimal MA directly on your chart and highlighting relevant trading periods.

Example of Use: Imagine you're trading a volatile stock and want to optimize your long-only strategy. By applying the "Optimal MA Finder," you discover that a 120-period EMA results in the highest profit factor. The indicator plots this EMA on your chart, showing you when to consider entering or exiting positions based on price movements relative to the EMA.

In short, the "Optimal MA Finder" empowers traders by delivering data-driven insights and improving the effectiveness of trading strategies. Its clear logic, combined with robust automation, makes it an invaluable tool for both novice and experienced traders seeking consistent results.

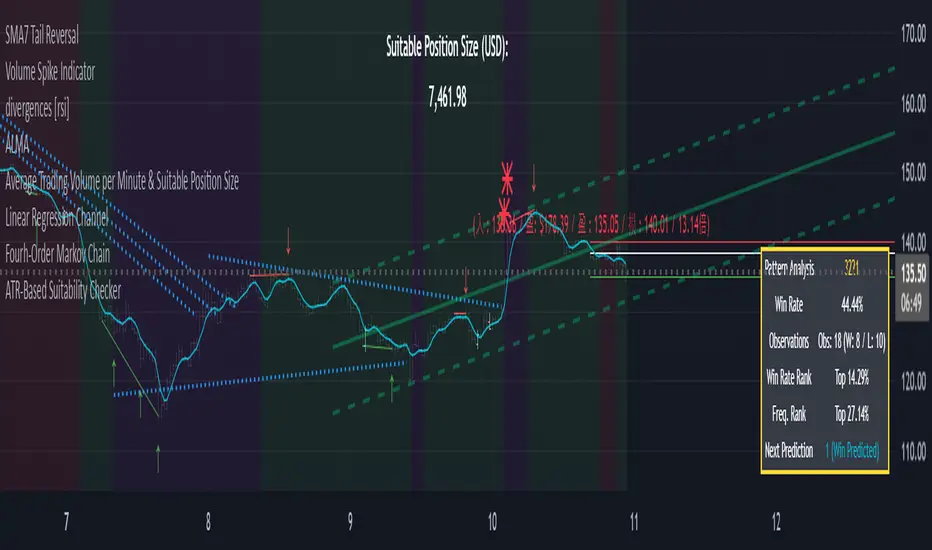

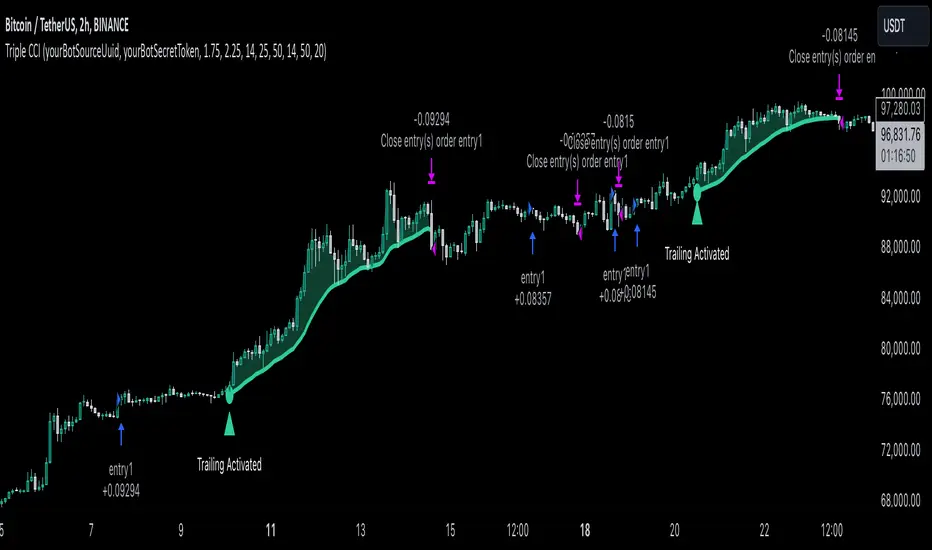

Triple CCI Strategy MFI Confirmed [Skyrexio]Overview

Triple CCI Strategy MFI Confirmed leverages 3 different periods Commodity Channel Index (CCI) indicator in conjunction Money Flow Index (MFI) and Exponential Moving Average (EMA) to obtain the high probability setups. Fast period CCI is used for having the high probability to enter in the direction of short term trend, middle and slow period CCI are used for confirmation, if market now likely in the mid and long-term uptrend. MFI is used to confirm trade with the money inflow/outflow with the high probability. EMA is used as an additional trend filter. Moreover, strategy uses exponential moving average (EMA) to trail the price when it reaches the specific level. More information in "Methodology" and "Justification of Methodology" paragraphs. The strategy opens only long trades.

Unique Features

Dynamic stop-loss system: Instead of fixed stop-loss level strategy utilizes average true range (ATR) multiplied by user given number subtracted from the position entry price as a dynamic stop loss level.

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Four layers trade filtering system: Strategy utilizes two different period CCI indicators, MFI and EMA indicators to confirm the signals produced by fast period CCI.

Trailing take profit level: After reaching the trailing profit activation level scrip activate the trailing of long trade using EMA. More information in methodology.

Methodology

The strategy opens long trade when the following price met the conditions:

Fast period CCI shall crossover the zero-line.

Slow and Middle period CCI shall be above zero-lines.

Price shall close above the EMA. Crossover is not obligatory

MFI shall be above 50

When long trade is executed, strategy set the stop-loss level at the price ATR multiplied by user-given value below the entry price. This level is recalculated on every next candle close, adjusting to the current market volatility.

At the same time strategy set up the trailing stop validation level. When the price crosses the level equals entry price plus ATR multiplied by user-given value script starts to trail the price with EMA. If price closes below EMA long trade is closed. When the trailing starts, script prints the label “Trailing Activated”.

Strategy settings

In the inputs window user can setup the following strategy settings:

ATR Stop Loss (by default = 1.75)

ATR Trailing Profit Activation Level (by default = 2.25)

CCI Fast Length (by default = 14, used for calculation short term period CCI)

CCI Middle Length (by default = 25, used for calculation short term period CCI)

CCI Slow Length (by default = 50, used for calculation long term period CCI)

MFI Length (by default = 14, used for calculation MFI

EMA Length (by default = 50, period of EMA, used for trend filtering EMA calculation)

Trailing EMA Length (by default = 20)

User can choose the optimal parameters during backtesting on certain price chart.

Justification of Methodology

Before understanding why this particular combination of indicator has been chosen let's briefly explain what is CCI, MFI and EMA.

The Commodity Channel Index (CCI) is a momentum-based technical indicator that measures the deviation of a security's price from its average price over a specific period. It helps traders identify overbought or oversold conditions and potential trend reversals.

The CCI formula is:

CCI = (Typical Price − SMA) / (0.015 × Mean Deviation)

Typical Price (TP): This is calculated as the average of the high, low, and closing prices for the period.

Simple Moving Average (SMA): This is the average of the Typical Prices over a specific number of periods.

Mean Deviation: This is the average of the absolute differences between the Typical Price and the SMA.

The result is a value that typically fluctuates between +100 and -100, though it is not bounded and can go higher or lower depending on the price movement.

The Money Flow Index (MFI) is a technical indicator that measures the strength of money flowing into and out of a security. It combines price and volume data to assess buying and selling pressure and is often used to identify overbought or oversold conditions. The formula for MFI involves several steps:

1. Calculate the Typical Price (TP):

TP = (high + low + close) / 3

2. Calculate the Raw Money Flow (RMF):

Raw Money Flow = TP × Volume

3. Determine Positive and Negative Money Flow:

If the current TP is greater than the previous TP, it's Positive Money Flow.

If the current TP is less than the previous TP, it's Negative Money Flow.

4. Calculate the Money Flow Ratio (MFR):

Money Flow Ratio = Sum of Positive Money Flow (over n periods) / Sum of Negative Money Flow (over n periods)

5. Calculate the Money Flow Index (MFI):

MFI = 100 − (100 / (1 + Money Flow Ratio))

MFI above 80 can be considered as overbought, below 20 - oversold.

The Exponential Moving Average (EMA) is a type of moving average that places greater weight and significance on the most recent data points. It is widely used in technical analysis to smooth price data and identify trends more quickly than the Simple Moving Average (SMA).

Formula:

1. Calculate the multiplier

Multiplier = 2 / (n + 1) , Where n is the number of periods.

2. EMA Calculation

EMA = (Current Price) × Multiplier + (Previous EMA) × (1 − Multiplier)

This strategy leverages Fast period CCI, which shall break the zero line to the upside to say that probability of short term trend change to the upside increased. This zero line crossover shall be confirmed by the Middle and Slow periods CCI Indicators. At the moment of breakout these two CCIs shall be above 0, indicating that there is a high probability that price is in middle and long term uptrend. This approach increases chances to have a long trade setup in the direction of mid-term and long-term trends when the short-term trend starts to reverse to the upside.

Additionally strategy uses MFI to have a greater probability that fast CCI breakout is confirmed by this indicator. We consider the values of MFI above 50 as a higher probability that trend change from downtrend to the uptrend is real. Script opens long trades only if MFI is above 50. As you already know from the MFI description, it incorporates volume in its calculation, therefore we have another one confirmation factor.

Finally, strategy uses EMA an additional trend filter. It allows to open long trades only if price close above EMA (by default 50 period). It increases the probability of taking long trades only in the direction of the trend.

ATR is used to adjust the strategy risk management to the current market volatility. If volatility is low, we don’t need the large stop loss to understand the there is a high probability that we made a mistake opening the trade. User can setup the settings ATR Stop Loss and ATR Trailing Profit Activation Level to realize his own risk to reward preferences, but the unique feature of a strategy is that after reaching trailing profit activation level strategy is trying to follow the trend until it is likely to be finished instead of using fixed risk management settings. It allows sometimes to be involved in the large movements. It’s also important to make a note, that script uses another one EMA (by default = 20 period) as a trailing profit level.

Backtest Results

Operating window: Date range of backtests is 2022.04.01 - 2024.11.25. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 50%

Maximum Single Position Loss: -4.13%

Maximum Single Profit: +19.66%

Net Profit: +5421.21 USDT (+54.21%)

Total Trades: 108 (44.44% win rate)

Profit Factor: 2.006

Maximum Accumulated Loss: 777.40 USDT (-7.77%)

Average Profit per Trade: 50.20 USDT (+0.85%)

Average Trade Duration: 44 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 2h BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

Breaks and Retests - Free990Strategy Description: "Breaks and Retests - Free990"

The "Breaks and Retests - Free990" strategy is based on identifying breakout and retest opportunities for potential entries in both long and short trades. The idea is to detect price breakouts above resistance levels or below support levels, and subsequently identify retests that confirm the breakout levels. The strategy offers an automated approach to enter trades after a breakout followed by a retest, which serves as a confirmation of trend continuation.

Key Components:

Support and Resistance Detection:

The strategy calculates pivot levels based on historical price movements to define support and resistance areas. A lookback range is used to determine these key levels.

Breakouts and Retests:

The system identifies when a breakout occurs above a resistance level or below a support level.

It then waits for a retest of the previously broken level as confirmation, which is often a better entry opportunity.

Trade Direction Selection:

Users can choose between "Long Only," "Short Only," or "Both" directions for trading based on their market view.

Stop Loss and Trailing Stop:

An initial stop loss is placed at a defined percentage away from the entry.

The trailing stop loss is activated after the position gains a specified percentage in profit.

Long Entry:

A long entry is triggered if the price breaks above a resistance level and subsequently retests that level successfully.

The entry condition checks if the breakout was confirmed and if a retest was valid.

The long entry is only executed if the user-selected direction is either "Long Only" or "Both."

Short Entry:

A short entry is triggered if the price breaks below a support level and subsequently retests that level.

The short entry is only executed if the user-selected direction is either "Short Only" or "Both."

sell_condition checks whether the support has been broken and whether the retest condition is valid.

An initial stop loss is placed when the trade is opened to limit the risk if the trade moves against the position.

The stop loss is calculated based on a user-defined percentage (stop_loss_percent) of the entry price.

pinescript

Copy code

stop_loss_price := strategy.position_avg_price * (1 - stop_loss_percent / 100)

For long positions, the stop loss is placed below the entry price.

For short positions, the stop loss is placed above the entry price.

Trailing Stop:

When a position achieves a certain profit threshold (profit_threshold_percent), the trailing stop mechanism is activated.

For long positions, the trailing stop follows the highest price reached, ensuring that some profit is locked in if the price reverses.

For short positions, the trailing stop follows the lowest price reached.

Code Logic for Trailing Stop:

Exit Execution:

The strategy exits the position when the price hits the calculated stop loss level.

This includes both the initial stop loss and the trailing stop that adjusts as the trade progresses.

Code Logic for Exit:

Summary:

Breaks and Retests - Free990 uses support and resistance levels to identify breakouts, followed by retests for confirmation.

Entry Points: Triggered when a breakout is confirmed and a retest occurs, for both long and short trades.

Exit Points:

Initial Stop Loss: Limits risk for both long and short trades.

Trailing Stop Loss: Locks in profits as the price moves in favor of the position.

This strategy aims to capture the momentum after breakouts and minimize losses through effective use of stop loss and trailing stops. It gives the flexibility of selecting trade direction and ensures trades are taken with confirmation through the retest, which helps to reduce false breakouts.

Original Code by @HoanGhetti

ATR-based TP/SL with Dynamic RREnglish

This indicator combines the power of the Average True Range (ATR) with dynamic calculations for Take Profit (TP) and Stop Loss (SL) levels, offering a clear visualization of trading opportunities and their respective Risk-Reward Ratios (RRR).

Features:

Dynamic TP/SL Calculation:

TP and SL levels are derived using user-defined ATR multipliers for precise positioning.

Multipliers are flexible, allowing traders to adjust according to their strategies.

Risk-Reward Ratio (RRR):

Automatically calculates and displays the RRR for each trade signal.

Helps traders quickly assess if a trade aligns with their risk management plan.

Entry Conditions:

Buy signals occur when the closing price crosses above the 20-period Simple Moving Average (SMA).

Sell signals occur when the closing price crosses below the 20-period SMA.

Visual Aids:

Red and green lines indicate Stop Loss and Take Profit levels.

Blue and orange labels show the RRR for long and short trades, respectively.

How It Works:

The indicator uses the ATR to calculate TP and SL levels:

TP: Adjusted based on the desired Risk-Reward Ratio (RR).

SL: Proportional to the ATR multiplier.

Entry signals are plotted with "BUY" or "SELL" markers, while the respective TP/SL levels are drawn as horizontal lines.

Why Use This Indicator?

Perfect for traders who value precise risk management.

Helps identify trades with favorable RRR (e.g., greater than 1.5 or 2.0).

Ideal for swing traders, day traders, and scalpers looking to automate their decision-making process.

Customization:

ATR Length: Control the sensitivity of ATR-based calculations.

ATR Multipliers: Set the TP and SL distances relative to the ATR.

Desired RRR: Define the risk/reward ratio you aim to achieve.

Important Notes:

The indicator does not place trades automatically; it is for visual and analytical purposes.

Always backtest and combine it with additional analysis for best results.

French

Cet indicateur combine la puissance de l’Average True Range (ATR) avec des calculs dynamiques pour les niveaux de Take Profit (TP) et de Stop Loss (SL), tout en offrant une visualisation claire des opportunités de trading et de leurs Ratios Risque/Rendement (RRR).

Fonctionnalités :

Calcul Dynamique des TP/SL :

Les niveaux de TP et SL sont calculés à l'aide de multiplicateurs ATR définis par l’utilisateur pour une position précise.