Engulfing & Pin Bar Breakout StrategyOverview

This strategy automates a classic, powerful trading methodology based on identifying key candlestick reversal patterns and trading the subsequent price breakout. It is designed to be a complete, "set-and-go" system with built-in risk and position size management.

The core logic operates on the 1-Hour timeframe, scanning for four distinct high-probability reversal signals: two bullish and two bearish. An entry is only triggered when the market confirms the signal by breaking a key price level, aiming to capture momentum following a potential shift in market sentiment.

The Strategy Logic

The system is composed of two distinct modules: Bullish (Long) and Bearish (Short).

🐂 Bullish (Long) Setup

The script initiates a long trade based on the following strict criteria:

Signal: Identifies either a Hammer or a Bullish Engulfing pattern. These patterns often indicate that sellers are losing control and buyers are stepping in.

Confirmation: Waits for the very next candle after the signal.

Entry Trigger: A long position is automatically opened as soon as the price breaks above the high of the signal candle.

Stop Loss: Immediately set just below the low of the signal candle.

Take Profit: A fixed target is placed at a 1:5 Risk/Reward Ratio.

🐻 Bearish (Short) Setup

The script initiates a short trade based on the following strict criteria:

Signal: Identifies either a Shooting Star or a Bearish Engulfing pattern. These patterns suggest buying pressure is fading and sellers are taking over.

Confirmation: Waits for the very next candle after the signal.

Entry Trigger: A short position is automatically opened as soon as the price breaks below the low of the signal candle.

Stop Loss: Immediately set just above the high of the signal candle.

Take Profit: A fixed target is placed at a 1:4 Risk/Reward Ratio.

Key Feature: Automated Risk Management

This strategy is designed for disciplined trading. You do not need to calculate position sizes manually.

Fixed Risk: The script automatically calculates the correct position size to risk exactly 2% of your total account equity on every single trade.

Dynamic Sizing: The position size will adjust based on the distance between your entry price and your stop loss for each specific setup, ensuring a consistent risk profile.

How To Use

Apply the script to your chosen chart (e.g., BTC/USD).

Crucially, set your chart's timeframe to 1-Hour (H1). The strategy is specifically calibrated for this interval.

Navigate to the "Strategy Tester" tab below your chart to view backtest results, including net profit, win rate, and individual trades.

Disclaimer: This script is provided for educational and informational purposes only. It is not financial advice. All trading involves substantial risk, and past performance is not indicative of future results. Please use this tool responsibly and at your own risk.

Cerca negli script per "profit"

Mutanabby_AI | Fresh Algo V24Mutanabby_AI | Fresh Algo V24: Advanced Multi-Mode Trading System

Overview

The Mutanabby_AI Fresh Algo V24 represents a sophisticated evolution of multi-component trading systems that adapts to various market conditions through advanced operational configurations and enhanced analytical capabilities. This comprehensive indicator provides traders with multiple signal generation approaches, specialized assistant functions, and dynamic risk management tools designed for professional market analysis across diverse trading environments.

Primary Signal Generation Framework

The Fresh Algo V24 operates through two fundamental signal generation approaches that accommodate different market perspectives and trading philosophies. The Trending Signals Mode serves as the primary trend-following mechanism, combining Wave Trend Oscillator analysis with Supertrend directional signals and Squeeze Momentum breakout detection. This mode incorporates ADX filtering that requires values exceeding 20 to ensure sufficient trend strength exists before signal activation, making it particularly effective during sustained directional market movements where momentum persistence creates profitable trading opportunities.

The Contrarian Signals Mode provides an alternative approach targeting reversal opportunities through extreme market condition identification. This mode activates when the Wave Trend Oscillator reaches critical threshold levels, specifically when readings surpass 65 indicating potential bearish reversal conditions or drop below 35 suggesting bullish reversal opportunities. This methodology proves valuable during overextended market phases where mean reversion becomes statistically probable.

Advanced Filtering Mechanisms

The system incorporates multiple sophisticated filtering mechanisms designed to enhance signal quality and reduce false positive occurrences. The High Volume Filter requires volume expansion confirmation before signal activation, utilizing exponential moving average calculations to ensure institutional participation accompanies price movements. This filter substantially improves signal reliability by eliminating low-conviction breakouts that lack adequate volume support from professional market participants.

The Strong Filter provides additional trend confirmation through 200-period exponential moving average analysis. Long position signals require price action above this benchmark level, while short position signals necessitate price action below it. This ensures strategic alignment with longer-term trend direction and reduces the probability of trading against major market movements that could invalidate shorter-term signals.

Cloud Filter Configuration System

The Fresh Algo V24 offers four distinct cloud filter configurations, each optimized for specific trading timeframes and market approaches. The Smooth Cloud Filter utilizes the mathematical relationship between 150-period and 250-period exponential moving averages, providing stable trend identification suitable for position trading strategies. This configuration generates signals exclusively when price action aligns with cloud direction, creating a more deliberate but highly reliable signal generation process.

The Swing Cloud Filter employs modified Supertrend calculations with parameters specifically optimized for swing trading timeframes. This filter achieves optimal balance between responsiveness and stability, adapting effectively to medium-term price movements while filtering excessive market noise that typically affects shorter-term analytical systems.

For active intraday traders, the Scalping Cloud Filter utilizes accelerated Supertrend calculations designed to capture rapid trend changes effectively. This configuration provides enhanced signal generation frequency suitable for compressed timeframe strategies. The advanced Scalping+ Cloud Filter incorporates Hull Moving Average confirmation, delivering maximum responsiveness for ultra-short-term trading while maintaining signal quality through additional momentum validation processes.

Specialized Assistant Functionality

The system includes two distinct assistant modes that provide supplementary market analysis capabilities. The Trend Assistant Mode activates advanced cloud analysis overlays that display dynamic support and resistance zones calculated through adaptive volatility algorithms. These levels automatically adjust to current market conditions, providing visual guidance for identifying trend continuation patterns and potential reversal areas with mathematical precision.

The Trend Tracker Mode concentrates on long-term trend identification by displaying major exponential moving averages with color-coded fill areas that clarify directional bias. This mode maintains visual simplicity while providing comprehensive trend context evaluation, enabling traders to quickly assess broader market direction and align shorter-term strategies accordingly.

Dynamic Risk Management System

The integrated risk management system automatically adapts across all operational modes, calculating stop loss and take profit targets using Average True Range multiples that adjust to current market volatility. This approach ensures consistent risk parameters regardless of selected operational mode while maintaining relevance to prevailing market conditions.

Stop loss placement occurs at dynamically calculated distances from entry points, while three progressive take profit targets establish at customizable ATR multiples respectively. The system automatically updates these levels upon trend direction changes, ensuring current market volatility influences all risk calculations and maintains appropriate risk-reward ratios throughout trade management.

Comprehensive Market Analysis Dashboard

The sophisticated dashboard provides real-time market analysis including volatility measurements, institutional activity assessment, and multi-timeframe trend evaluation across five-minute through four-hour periods. This comprehensive market context assists traders in selecting appropriate operational modes based on current market characteristics rather than relying exclusively on historical performance data.

The multi-timeframe analysis ensures mode selection considers broader market context beyond the primary trading timeframe, improving overall strategic alignment and reducing conflicts between different temporal market perspectives. The dashboard displays market state classification, volatility percentages, institutional activity levels, current trading session information, and trend pressure indicators with professional formatting and clear visual hierarchy.

Enhanced Trading Assistants

The Fresh Algo V24 includes specialized trading assistant features that complement the primary signal generation system. The Reversal Dot functionality identifies potential reversal points through Wave Trend Oscillator analysis, displaying visual indicators when crossover conditions occur at extreme levels. These reversal indicators provide early warning signals for potential trend changes before they appear in the primary signal system.

The Dynamic Take Profit Labels feature automatically identifies optimal profit-taking opportunities through RSI threshold analysis, marking potential exit points at multiple levels for long positions and corresponding levels for short positions. This automated profit management system helps traders optimize exit timing without requiring constant manual monitoring of technical indicators.

Advanced Alert System

The comprehensive alert system accommodates all operational modes while providing granular notification control for various signal types and risk management events. Traders can configure separate alerts for normal buy signals, strong buy signals, normal sell signals, strong sell signals, stop loss triggers, and individual take profit target achievements.

Cloud crossover alerts notify traders when trend direction changes occur, providing early indication of potential strategy adjustments. The alert system includes detailed trade setup information, timeframe data, and relevant entry and exit levels, ensuring traders receive complete context for informed decision-making without requiring constant chart monitoring.

Technical Foundation Architecture

The Fresh Algo V24 combines multiple proven technical analysis components including Wave Trend Oscillator for momentum assessment, Supertrend for directional bias determination, Squeeze Momentum for volatility analysis, and various exponential moving averages for trend confirmation. Each component contributes specific market insights while the unified system provides comprehensive market evaluation through their mathematical integration.

The multi-component approach reduces dependency on individual indicator limitations while leveraging the analytical strengths of each technical tool. This creates a robust analytical framework capable of adapting to diverse market conditions through appropriate mode selection and parameter optimization, ensuring consistent performance across varying market environments.

Market State Classification

The indicator incorporates advanced market state classification through ADX analysis, distinguishing between trending, ranging, and transitional market conditions. This classification system automatically adjusts signal sensitivity and filtering parameters based on current market characteristics, optimizing performance for prevailing conditions rather than applying static analytical approaches.

The volatility measurement system calculates current market activity levels as percentages, providing quantitative assessment of market energy and helping traders select appropriate operational modes. Institutional activity detection through volume analysis ensures signal generation aligns with professional market participation patterns.

Implementation Strategy Considerations

Successful implementation requires careful matching of operational modes to prevailing market conditions and individual trading objectives. Trending modes demonstrate optimal performance during directional markets with sustained momentum characteristics, while contrarian modes excel during range-bound or overextended market conditions where reversal probability increases.

The cloud filter configurations provide varying degrees of confirmation strength, with smoother settings reducing false signal occurrence at the expense of some responsiveness to price changes. Traders must balance signal quality against signal frequency based on their risk tolerance and available trading time, utilizing the comprehensive customization options to optimize performance for their specific requirements.

Multi-Timeframe Integration

The system provides seamless multi-timeframe analysis through the integrated dashboard, displaying trend alignment across multiple time horizons from five-minute through four-hour periods. This analysis helps traders understand broader market context and avoid conflicts between different temporal perspectives that could compromise trade outcomes.

Session analysis identifies current trading session characteristics, providing context for expected market behavior patterns and helping traders adjust their approach based on typical session volatility and participation levels. This geographic market awareness enhances strategic decision-making and improves timing for trade execution.

Advanced Visualization Features

The indicator includes sophisticated visualization capabilities through gradient candle coloring based on MACD analysis, providing immediate visual feedback on momentum strength and direction. This enhancement allows rapid market assessment without requiring detailed indicator analysis, improving efficiency for traders managing multiple instruments simultaneously.

The cloud visualization system uses color-coded fill areas to clearly indicate trend direction and strength, with automatic adaptation to selected operational modes. This visual clarity reduces analytical complexity while maintaining comprehensive market information display through professional chart presentation.

Performance Optimization Framework

The Fresh Algo V24 incorporates performance optimization features including signal strength classification, automatic parameter adjustment based on market conditions, and dynamic filtering that adapts to current volatility levels. These optimizations ensure consistent performance across varying market environments while maintaining signal quality standards.

The system automatically adjusts sensitivity levels based on selected operational modes, ensuring appropriate responsiveness for different trading approaches. This adaptive framework reduces the need for manual parameter adjustments while maintaining optimal performance characteristics for each operational configuration.

Conclusion

The Mutanabby_AI Fresh Algo V24 represents a comprehensive solution for professional trading analysis, combining multiple analytical approaches with advanced visualization and risk management capabilities. The system's strength lies in its adaptive multi-mode design and sophisticated filtering mechanisms, providing traders with versatile tools for various market conditions and trading styles.

Success with this system requires understanding the relationship between different operational modes and their optimal application scenarios. The comprehensive dashboard and alert system provide essential market context and trade management support, enabling systematic approach to market analysis while maintaining flexibility for individual trading preferences.

The indicator's sophisticated architecture and extensive customization options make it suitable for traders at all experience levels, from those seeking systematic signal generation to advanced practitioners requiring comprehensive market analysis tools. The multi-timeframe integration and adaptive filtering ensure consistent performance across diverse market conditions while providing clear guidelines for strategic implementation.

ai quant oculusAI QUANT OCULUS

Version 1.0 | Pine Script v6

Purpose & Innovation

AI QUANT OCULUS integrates four distinct technical concepts—exponential trend filtering, adaptive smoothing, momentum oscillation, and Gaussian smoothing—into a single, cohesive system that delivers clear, objective buy and sell signals along with automatically plotted stop-loss and three profit-target levels. This mash-up goes beyond a simple EMA crossover or standalone TRIX oscillator by requiring confluence across trend, adaptive moving averages, momentum direction, and smoothed price action, reducing false triggers and focusing on high‐probability turning points.

How It Works & Why Its Components Matter

Trend Filter: EMA vs. Adaptive MA

EMA (20) measures the prevailing trend with fixed sensitivity.

Adaptive MA (also EMA-based, length 10) approximates a faster-responding moving average, standing in for a KAMA-style filter.

Bullish bias requires AMA > EMA; bearish bias requires AMA < EMA. This ensures signals align with both the underlying trend and a more nimble view of recent price action.

Momentum Confirmation: TRIX

Calculates a triple-smoothed EMA of price over TRIX Length (15), then converts it to a percentage rate-of-change oscillator.

Positive TRIX reinforces bullish entries; negative TRIX reinforces bearish entries. Using TRIX helps filter whipsaws by focusing on sustained momentum shifts.

Gaussian Price Smoother

Applies two back-to-back 5-period EMAs to the price (“gaussian” smoothing) to remove short-term noise.

Price above the smoothed line confirms strength for longs; below confirms weakness for shorts. This layer avoids entries on erratic spikes.

Confluence Signals

Buy Signal (isBull) fires only when:

AMA > EMA (trend alignment)

TRIX > 0 (momentum support)

Close > Gaussian (price strength)

Sell Signal (isBear) fires under the inverse conditions.

Requiring all three conditions simultaneously sharply reduces false triggers common to single-indicator systems.

Automatic Risk & Reward Plotting

On each new buy or sell signal (edge detection via not isBull or not isBear ), the script:

Stores entryPrice at the signal bar’s close.

Draws a stop-loss line at entry minus ATR(14) × Stop Multiplier (1.5) by default.

Plots three profit-target lines at entry plus ATR × Target Multiplier (1×, 1.5×, and 2×).

All previous labels and lines are deleted on each new signal, keeping the chart uncluttered and focusing only on the current trade.

Inputs & Customization

Input Description Default

EMA Length Period for the main trend EMA 20

Adaptive MA Length Period for the faster adaptive EM A substitute 10

TRIX Length Period for the triple-smoothed momentum oscillator 15

Dominant Cycle Length (Reserved) 40

Stop Multiplier ATR multiple for stop-loss distance 1.5

Target Multiplier ATR multiple for first profit target 1.5

Show Buy/Sell Signals Toggle on-chart labels for entry signals On

How to Use

Apply to Chart: Best on 15 m–1 h timeframes for swing entries or 5 m for agile scalps.

Wait for Full Confluence:

Look for the AMA to cross above/below the EMA and verify TRIX and Gaussian conditions on the same bar.

A bright “LONG” or “SHORT” label marks your entry.

Manage the Trade:

Place your stop where the red or green SL line appears.

Scale or exit at the three yellow TP1/TP2/TP3 lines, automatically drawn by volatility.

Repeat Cleanly: Each new signal clears prior annotations, ensuring you only track the active setup.

Why This Script Stands Out

Multi-Layer Confluence: Trend, momentum, and noise-reduction must all align, addressing the weaknesses of single-indicator strategies.

Automated Trade Management: No manual plotting—stop and target lines appear seamlessly with each signal.

Transparent & Customizable: All logic is open, adjustable, and clearly documented, allowing traders to tweak lengths and multipliers to suit different instruments.

Disclaimer

No indicator guarantees profit. Always backtest AI QUANT OCULUS extensively, combine its signals with your own analysis and risk controls, and practice sound money management before trading live.

Options Strategy V2.0📈 Options Strategy V2.0 – Intraday Reversal-Resilient Momentum System

Overview:

This strategy is designed specifically for intraday SPY, TSLA, MSFT, etc. options trading (0DTE or 1DTE), using high-probability signals derived from a confluence of technical indicators: EMA crossovers, RSI thresholds, ATR-based risk control, and volume spikes. The strategy aims to capture strong directional moves while avoiding overtrading, thanks to a built-in cooldown logic and optional time/session filters.

⚙️ Core Concept

The strategy executes trades only in the direction of the prevailing trend, determined by short- and long-term Exponential Moving Averages (EMA). Entry signals are generated when the Relative Strength Index (RSI) confirms momentum in the direction of the trend, and volume spikes suggest institutional activity.

To increase adaptability and user control, it includes a highly customizable parameter set for both long and short entries independently.

📌 Key Features

✅ Trend-Following Logic

Long entries are only allowed when EMA(short) > EMA(long)

Short entries are only allowed when EMA(short) < EMA(long)

✅ RSI Confirmation

Long: Requires RSI crossover above a configurable threshold

Short: Requires RSI crossunder below a configurable threshold

Optional rejection filters: Entry blocked above/below specific RSI extremes

✅ Volume Spike Filter

Confirms institutional participation by comparing current volume to an average multiplied by a user-defined factor.

✅ ATR-Based Risk Management

Both Stop Loss (SL) and Take Profit (TP) are dynamically calculated using ATR × a multiplier.

TP/SL ratio is fully configurable.

✅ Cooldown Control

After every trade, the system waits for a set number of bars before allowing new entries.

This prevents overtrading and increases signal quality.

Optionally, cooldown is ignored for reversal trades, ensuring the system can react immediately to a confirmed trend change.

✅ Candle Body Filter (Noise Control)

Avoids trades on candles with too small bodies relative to wicks (often noise or indecision candles).

✅ VWAP Confirmation (Optional)

Ensures price is trading above VWAP for long entries, or below for short entries.

✅ Time & Session Filters

Trades only during regular market hours (09:30–16:00 EST).

No-trade zone (e.g., 14:15–15:45 EST) to avoid low-liquidity traps or late-day whipsaws.

✅ End-of-Day Auto Close

All open positions are force-closed at 15:55 EST, protecting against overnight risk (especially relevant for 0DTE options).

📊 Visual Aids

EMA plots show trend direction

VWAP line provides real-time mean-reversion context

Stop Loss and Take Profit lines appear dynamically with each trade

Alerts notify of entry signals and exit triggers

🔧 Customization Panel

Nearly every element of the strategy can be tailored:

EMA lengths (short and long, for both sides)

RSI thresholds and length

ATR length, SL multiplier, and TP/SL ratio

Volume spike sensitivity

Minimum EMA distance filter

Candle body ratio filter

Session restrictions

Cooldown logic (duration + reversal exception)

This makes the strategy extremely versatile, allowing both conservative and aggressive configurations depending on the trader’s profile and the market context.

📌 Example Use Case: SPY Options (0DTE or 1DTE)

This system was designed and tested specifically for SPY and other intraday options trading, where:

Delta is around 0.50 or higher

Trades are short-lived (often 1–5 candles)

You aim to trade 1–3 signals per day, filtering out weak entries

🚫 Important Notes

It is not a scalping strategy; it relies on confirmed breakouts with trend support

No pyramiding or re-entries without cooldown to preserve risk integrity

Should be used with real-time alerts and manual broker execution

📈 Alerts Included

📈 Long Entry Signal

📉 Short Entry Signal

⚠️ Auto-closed all positions at 15:55 EST

✅ Proven Settings – Real Trades + Backtest Results

The current version of the strategy includes the optimal settings I’ve arrived at through extensive backtesting, as well as 3 months of real trading with consistent profitability. These results reflect real-world execution under live market conditions using 0DTE SPY options, with disciplined trade management and risk control.

🧠 Final Thoughts

Options Strategy V2.0 is a robust, highly tunable intraday strategy that blends momentum, trend-following, and volume confirmation. It is ideal for disciplined traders focused on SPY or other 0DTE/1DTE options, and it includes guardrails to reduce false signals and improve execution timing.

Perfect for those who seek precision, flexibility, and risk-defined setups—not blind automation.

RISK MANAGEMENT CALCULATOR V3📊 RISK MANAGEMENT CALCULATOR – Lot Size, Profit & R:R Tool

This script is designed to help traders instantly calculate lot size, expected profit, and risk/reward ratio based on their trade plan.

✅ Features:

Input your Risk Amount ($), Entry, Stop Loss, and up to 3 Take Profits

Calculates:

✅ Lot Size based on risk

✅ Split profits per TP level (equally weighted)

✅ Total Profit & Risk/Reward (R:R)

Displays everything in a clean bottom-right table

Optimized for both:

🖥️ Desktop mode (larger layout)

📱 Mobile mode (toggle compact view)

💡 How to Use:

Enter your planned Entry, Stop Loss, and Risk Amount

Set any TP1, TP2, or TP3 prices (set TP to 0 if not used)

The system will auto-compute your ideal lot size and show estimated profits

🔧 Parameters:

Risk Amount ($) – how much you’re willing to lose

Entry Price – your trade entry

Stop Loss Price – your SL level

Take Profit 1/2/3 – optional TP targets

Pip Value – profit/loss per point for 1 standard lot

📱 Mobile Mode – compact the table for small screens

🔐 Notes:

No trades are executed – this is a risk planning tool only

Designed for all markets (forex, gold, indices, crypto)

TP profits are equally split (e.g. 2 TP = 50% / 50%)

RISK MANAGEMENT CALCULATOR📊 RISK MANAGEMENT CALCULATOR – Lot Size, Profit & R:R Tool

This script is designed to help traders instantly calculate lot size, expected profit, and risk/reward ratio based on their trade plan.

✅ Features:

Input your Risk Amount ($), Entry, Stop Loss, and up to 3 Take Profits

Calculates:

✅ Lot Size based on risk

✅ Split profits per TP level (equally weighted)

✅ Total Profit & Risk/Reward (R:R)

Displays everything in a clean bottom-right table

Optimized for both:

🖥️ Desktop mode (larger layout)

📱 Mobile mode (toggle compact view)

💡 How to Use:

Enter your planned Entry, Stop Loss, and Risk Amount

Set any TP1, TP2, or TP3 prices (set TP to 0 if not used)

The system will auto-compute your ideal lot size and show estimated profits

🔧 Parameters:

Risk Amount ($) – how much you’re willing to lose

Entry Price – your trade entry

Stop Loss Price – your SL level

Take Profit 1/2/3 – optional TP targets

Pip Value – profit/loss per point for 1 standard lot

📱 Mobile Mode – compact the table for small screens

🔐 Notes:

No trades are executed – this is a risk planning tool only

Designed for all markets (forex, gold, indices, crypto)

TP profits are equally split (e.g. 2 TP = 50% / 50%)

Modular Range-Trading Strategy (V9.2)# 模块化震荡行情策略 (V9.2)

# Modular Range-Trading Strategy (V9.2)

## 策略简介 | Strategy Overview

该策略基于布林带 (Bollinger Bands)、RSI、MACD、ADX 等经典指标的组合,通过多逻辑模块化结构识别震荡区间的价格反转机会,支持多空双向操作,并在相同逻辑下允许智能加仓,适用于震荡市场的回测和研究。

This strategy combines classic indicators such as Bollinger Bands, RSI, MACD, and ADX to identify price reversal opportunities within ranging markets. It features a modular multi-logic structure, allowing both long and short trades with intelligent pyramiding under the same logic. It is designed for backtesting and research in range-bound conditions.

---

## 功能特点 | Key Features

- **多逻辑结构**:支持多套震荡逻辑(动能确认均值回归、布林带极限反转等)。

- **加仓与仓位互斥**:同逻辑下可智能加仓,不同逻辑间自动互斥,避免冲突。

- **回测可调时间范围**:可自定义回测起止时间,精准评估策略表现。

- **指标可视化**:布林带、RSI、MACD 及动态 ATR 止损线实时绘图。

- **K线收盘确认信号**:通过 `barstate.isconfirmed` 控制信号,避免未收盘的虚假信号。

- **Multi-logic structure**: Supports multiple range-trading logics (e.g., momentum-based mean reversion, Bollinger Band reversals).

- **Pyramiding with mutual exclusion**: Allows intelligent pyramiding within the same logic while preventing conflicts between different logics.

- **Adjustable backtesting range**: Customizable start and end dates for accurate performance evaluation.

- **Visual indicators**: Real-time plotting of Bollinger Bands, RSI, MACD, and dynamic ATR stop lines.

- **Close-bar confirmation**: Uses `barstate.isconfirmed` to avoid false signals before bar close.

---

## 使用说明 | Usage

1. 将该脚本添加到 TradingView 图表。

2. 在参数中设置回测时间段和指标参数。

3. 仅用于学习与策略研究,请勿直接用于实盘交易。

1. Add this script to your TradingView chart.

2. Configure backtesting dates and indicator parameters as needed.

3. For educational and research purposes only. **Not for live trading.**

---

## ⚠️ 免责声明 | Disclaimer

本策略仅供学习和研究使用,不构成任何形式的投资建议。

作者不参与任何实盘交易、资金管理或收益分成,也不保证策略盈利能力。

严禁将本脚本用于任何非法集资、私募募资或与虚拟货币相关的金融违法活动。

使用本策略即表示您自行承担所有风险与法律责任。

This strategy is for educational and research purposes only and does not constitute investment advice.

The author does not participate in live trading, asset management, or profit sharing, nor guarantee profitability.

The use of this script in illegal fundraising, private placements, or cryptocurrency-related financial activities is strictly prohibited.

By using this strategy, you accept all risks and legal responsibilities.

---

AI's Opinion Trading System V21. Complete Summary of the Indicator Script

AI’s Opinion Trading System V2 is an advanced, multi-factor trading tool designed for the TradingView platform. It combines several technical indicators (moving averages, RSI, MACD, ADX, ATR, and volume analysis) to generate buy, sell, and hold signals. The script features a customizable AI “consensus” engine that weighs multiple indicator signals, applies user-defined filters, and outputs actionable trade instructions with clear stop loss and take profit levels. The indicator also tracks sentiment, volume delta, and allows for advanced features like pyramiding (adding to positions), custom stop loss/take profit prices, and flexible signal confirmation logic. All key data and signals are displayed in a dynamic, color-coded table on the chart for easy review.

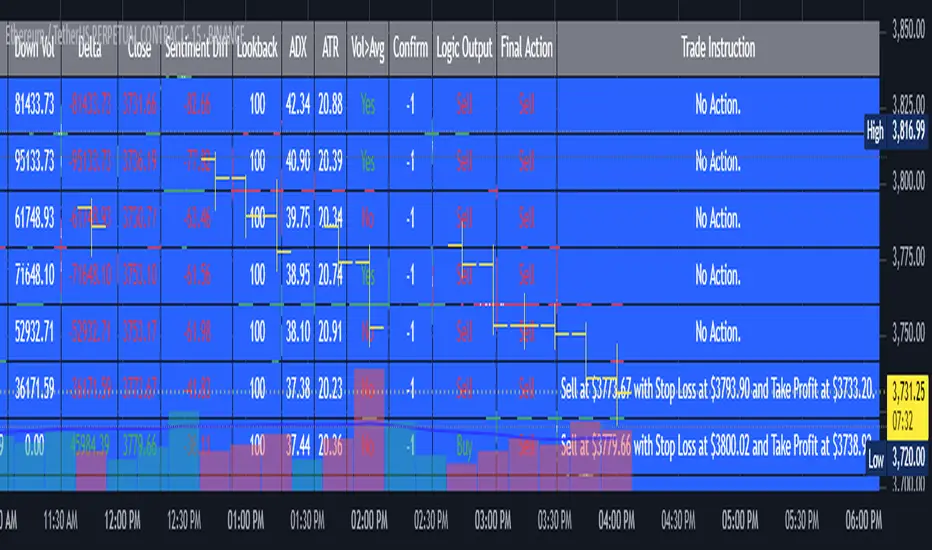

2. Full Explanation of the Table

The table is a real-time dashboard summarizing the indicator’s logic and recommendations for the most recent bars. It is color-coded for clarity and designed to help traders quickly understand market conditions and AI-driven trade signals.

Columns (from left to right):

Column Name What it Shows

Bar The time context: “Now” for the current bar, then “Bar -1”, “Bar -2”, etc. for previous bars.

Raw Consensus The raw AI consensus for each bar: “Buy”, “Sell”, or “-” (neutral).

Up Vol The amount of volume on up (rising) bars.

Down Vol The amount of volume on down (falling) bars.

Delta The difference between up and down volume. Green if positive, red if negative, gray if neutral.

Close The closing price for each bar, color-coded by price change.

Sentiment Diff The difference between the close and average sentiment price (a custom sentiment calculation).

Lookback The number of bars used for sentiment calculation (if enabled).

ADX The ADX value (trend strength).

ATR The ATR value (volatility measure).

Vol>Avg “Yes” (green) if volume is above average, “No” (red) otherwise.

Confirm Whether the AI signal is confirmed over the required bars.

Logic Output The AI’s interpreted signal after applying user-selected logic: “Buy”, “Sell”, or “-”.

Final Action The final signal after all filters: “Buy”, “Sell”, or “-”.

Trade Instruction A plain-English instruction: Buy/Sell/Add/Hold/No Action, with price, stop loss, and take profit.

Color Coding:

Green: Positive/bullish values or signals

Red: Negative/bearish values or signals

Gray: Neutral or inactive

Blue background: For all table cells, for visual clarity

White text: Default, except for color-coded cells

3. Full User Instructions for Every Input/Style Option

Below are plain-language instructions for every user-adjustable option in the indicator’s input and style pages:

Inputs

Table Location

What it does: Sets where the summary table appears on your chart.

How to use: Choose from 9 positions (Top Left, Top Center, Top Right, etc.) to avoid overlapping with other chart elements.

Decimal Places

What it does: Controls how many decimal places prices and values are displayed with.

How to use: Increase for assets with very small prices (e.g., SHIB), decrease for stocks or forex.

Show Sentiment Lookback?

What it does: Shows or hides the “Lookback” column in the table, which displays how many bars are used in the sentiment calculation.

How to use: Turn off if you want a simpler table.

AI View Mode

What it does: Selects the logic for how the AI combines signals from different indicators.

Majority: Follows the most common signal among all indicators.

Weighted: Uses custom weights for each type of signal.

Custom: Lets you define your own logic (see below).

How to use: Pick the logic style that matches your trading philosophy.

AI Consensus Weight / Vol Delta Weight / Sentiment Weight

What they do: When using “Weighted” AI View Mode, these let you set how much influence each factor (indicator consensus, volume delta, sentiment) has on the final signal.

How to use: Increase a weight to make that factor more important in the AI’s decision.

Custom AI View Logic

What it does: Lets advanced users write their own logic for when the AI should signal a trade (e.g., “ai==1 and delta>0 and sentiment>0”).

How to use: Only use if you understand basic boolean logic.

Use Custom Stop Loss/Take Profit Prices?

What it does: If enabled, you can enter your own fixed stop loss and take profit prices for buys and sells.

How to use: Turn on to override the auto-calculated SL/TP and enter your desired prices below.

Custom Buy/Sell Stop Loss/Take Profit Price

What they do: If custom SL/TP is enabled, these fields let you set exact prices for stop loss and take profit on both buy and sell trades.

How to use: Enter your preferred price, or leave at 0 for auto-calculation.

Sentiment Lookback

What it does: Sets how many bars the sentiment calculation should look back.

How to use: Increase to smooth out sentiment, decrease for faster reaction.

Max Pyramid Adds

What it does: Limits how many times you can add to an existing position (pyramiding).

How to use: Set to 1 for no adds, higher for more aggressive scaling in trends.

Signal Preset

What it does: Quick-sets a group of signal parameters (see below) for “Robust”, “Standard”, “Freedom”, or “Custom”.

How to use: Pick a preset, or select “Custom” to adjust everything manually.

Min Bars for Signal Confirmation

What it does: Sets how many bars a signal must persist before it’s considered valid.

How to use: Increase for more robust, less frequent signals; decrease for faster, but possibly less reliable, signals.

ADX Length

What it does: Sets the period for the ADX (trend strength) calculation.

How to use: Longer = smoother, shorter = more sensitive.

ADX Trend Threshold

What it does: Sets the minimum ADX value to consider a trend “strong.”

How to use: Raise for stricter trend confirmation, lower for more trades.

ATR Length

What it does: Sets the period for the ATR (volatility) calculation.

How to use: Longer = smoother volatility, shorter = more reactive.

Volume Confirmation Lookback

What it does: Sets how many bars are used to calculate the average volume.

How to use: Longer = more stable volume baseline, shorter = more sensitive.

Volume Confirmation Multiplier

What it does: Sets how much current volume must exceed average volume to be considered “high.”

How to use: Increase for stricter volume filter.

RSI Flat Min / RSI Flat Max

What they do: Define the RSI range considered “flat” (i.e., not trending).

How to use: Widen to be stricter about requiring a trend, narrow for more trades.

Style Page

Most style settings (such as plot colors, label sizes, and shapes) are preset in the script for visual clarity.

You can adjust plot visibility and colors (for signals, stop loss, take profit) in the TradingView “Style” tab as with any indicator.

Buy Signal: Shows as a green triangle below the bar when a buy is triggered.

Sell Signal: Shows as a red triangle above the bar when a sell is triggered.

Stop Loss/Take Profit Lines: Red and green lines for SL/TP, visible when a trade is active.

SL/TP Labels: Small colored markers at the SL/TP levels for each trade.

How to use:

Toggle visibility or change colors in the Style tab if you wish to match your chart theme or preferences.

In Summary

This indicator is highly customizable—you can tune every aspect of the AI logic, risk management, signal filtering, and table display to suit your trading style.

The table gives you a real-time, comprehensive view of all relevant signals, filters, and trade instructions.

All inputs are designed to be intuitive—hover over them in TradingView for tooltips, or refer to the explanations above for details.

200 SMA (5%/-3% Buffer) for SPY & QQQ In my testing TQQQ is an absolute monster of an ETF that performs extremely well even from a buy and hold standpoint over long periods of time, its largest drawback is the massive drawdown exposure that it faces which can be easily sidestepped with this strategy.

This strategy is meant to basically abuse TQQQ's insane outperformance while augmenting the typical 200SMA strategy in a way that uses all of its strengths while avoiding getting whipsawed in sideways markets.

The strategy BUYS when price crosses 5% over the 200SMA and then SELLS when price drops 3% below the 200SMA. Between trades I'll be parking my entire account in SGOV.

So maximizing profit while minimizing risk.

You use the strategy based off of QQQ and then make the trades on TQQQ when it tells you to BUY/SELL.

Here are some reasons why I will be using this strategy:

Simple emotionless BUY and SELL signals where I don't care who the president is, what is happening in the world, who is bombing who, who the leadership team is, no attachment to individual companies and diversified across the NASDAQ.

~85% win percentage and when it does lose the loses are nothing compared to the wins and after a loss you're basically set up for a massive win in the next trade.

Max drawdown of around 53% when using TQQQ

You benefit massively when the market is doing well and when there is a recession you basically sit in SGOV for a year and then are set up for a monster recovery with a clear easy BUY signal. So as long as you're patient you win regardless of what happens.

The trades are often very long term resulting in you taking advantage of Long Term Capital Gains tax advantage which could mean saving up to 15-20% in taxes.

With only a few trades you can spend time doing other stuff and don't have to track or pay attention to anything that is happening.

Simple, easy, and massively profitable.

Refined MA + Engulfing (M5 + Confirmed Structure Break)I would like to start by saying that this strategy was put together using ChatGPT, some past trades from myself and some backtested trades, and from my time as a student in Wallstreet Academy under Cue Banks.

I am not profitable yet. I am too jumpy and blow accounts. I'm hoping this strategy (and it's indicator twin) can help me spend less time on the charts, so that I'm not tempted to press buttons as much.

It does fire quite a bit. But, the Strategy Tester tab shows a 30% win rate with our wins being significant to our losses. So, in theory, if you followed the rules of this strategy STRICTLY, you COULD BE profitable.

With that being said, there are times that this strategy has shown to trigger and I ask, "Why?".

I just want to help myself and others, and maybe make some decent\cool stuff along the way. Enjoy

KR

Gann Single Square Swing Trading System with Gann AnglesGann Single Square Swing Trading System

This script automatically detects "squares" - geometric patterns where price movement equals time movement. When price moves the same distance as the number of bars (time), it creates powerful support/resistance levels based on Gann theory.

Key Visual Elements

• Box: The detected square pattern

• Dark Blue Line (50%): Most important trading level

• Green Lines: Profit target levels (125%, 150%)

• Red Lines: Stop loss levels (-25%, -50%)

• Colored Angle Lines: Gann angles for trend direction

• Quality Score: Blue label showing setup strength (aim for 70%+)

Simple Trading Rules

LONG Trades (Green 🟢 Square)

1. Entry: Buy when price touches the dark blue 50% line from above

2. Stop Loss: Place below the red -25% line

3. Take Profit: Exit at green 125% line (first target) or 150% line (second target)

SHORT Trades (Red 🔴 Square)

1. Entry: Sell when price touches the dark blue 50% line from below

2. Stop Loss: Place above the red -25% line

3. Take Profit: Exit at green 125% line (first target) or 150% line (second target)

Entry Checklist

✅ Square quality score > 70%

✅ Price touches 50% level (dark blue line)

✅ Volume above average (if volume filter enabled)

✅ Clear square formation visible

Alerts

The script generates automatic alerts when price reaches the 50% trading level. Enable alerts in TradingView to get notified of setups.

Bottom Line: Wait for the alert → Check quality score → Enter at 50% level → Set stop at red line → Take profit at green line.

Candlestick Patterns Backtester [Optimized]Candlestick Patterns Backtester

What this is: This indicator is based on a really cool candlestick pattern backtester that I found (I'll update this later when I remember where I got it from or find the actual author). The original had this massive table showing win/loss ratios for a bunch of candlestick patterns, and according to the built-in backtester, it was actually profitable - which was pretty impressive.

The Problem: I played around with the original for a while but honestly wasn't really able to get it to work well at all for actual trading. It was still pretty cool to look at though! The main issues were:

It was just a big static table - hard to do anything useful with it

Couldn't send signals out to other strategies

The code was a monster - like 2,000+ lines of repetitive mess

What I Did: I completely refactored this thing and got it down from 2,000+ lines to just a few hundred lines. Much cleaner now! Here's what it does:

45+ Candlestick Patterns - All the classics are in there

Dynamic Filtering - Set your own requirements (minimum win rate, profit factor, total trades, etc.)

Flexible Logic - Choose AND/OR logic for your filters

Signal Generation - Creates actual buy/sell signals you can use with other strategies

Visual Badges - Shows pattern badges on chart when they meet your criteria

Active Patterns Table - Only shows patterns that are currently profitable based on your settings

Settings You Can Adjust:

Minimum win rate threshold

Minimum profit factor

Minimum number of trades required

Whether to use AND or OR logic for filtering

Colors, badge display, debug options

Reality Check: Trading these patterns really wasn't for me, but it was still a great learning experience. The backtesting results look good on paper, but as always, past performance doesn't guarantee future results. Use this as a research tool and educational resource more than anything else.

Credit: This is based on someone else's original work that I heavily modified and optimized. I'll update this description once I track down the original author to give proper credit where it's due.

This introduction captures your casual, honest tone while explaining the technical improvements you made and setting realistic expectations about the indicator's practical use.

Daily Performance Analysis [Mr_Rakun]The Daily Performance Analysis indicator is a comprehensive trading performance tracker that analyzes your strategy's success rate and profitability across different days of the week and month. This powerful tool provides detailed statistics to help traders identify patterns in their trading performance and optimize their strategies accordingly.

Weekly Performance Analysis:

Tracks wins/losses for each day of the week (Monday through Sunday)

Calculates net profit/loss for each trading day

Shows profit factor (gross profit ÷ gross loss) for each day

Displays win rate percentage for each day

Monthly Performance Analysis:

Monitors performance for each day of the month (1-31)

Provides the same detailed metrics as weekly analysis

Helps identify monthly patterns and trends

Add to Your Strategy:

Copy the performance analysis code and integrate it into your existing Pine Script strategy

Optimize Strategy: Use insights to refine entry/exit timing or avoid trading on poor-performing days

Pattern Recognition: Identify which days of the week/month work best for your strategy

Risk Management: Avoid trading on historically poor-performing days

Strategy Optimization: Fine-tune your approach based on empirical data

Performance Tracking: Monitor long-term trends in your trading success

Data-Driven Decisions: Make informed adjustments to your trading schedule

HSI First 30m Candle Strategy (5m Chart)## HSI First Candle Breakout Strategy

USE on 10m TF for max profit rate.

**The HSI First Candle Breakout Strategy** is a systematic trading approach tailored for Hang Seng Index Futures during the main Hong Kong day session. The strategy is designed to capture early market momentum by reacting to the first significant move of the day.

### How It Works

- **Reference Candle:** At the start of each day session (09:00), the high and low of the first 15-minute candle are recorded.

- **Breakout Trigger:**

- A **buy (long) trade** is initiated if price breaks above the first candle’s high.

- A **sell (short) trade** is initiated if price breaks below the first candle’s low.

- **Stop Loss & Take Profit:**

- Stop-loss is placed on the opposite side of the reference candle.

- Take-profit target is set at a distance equal to the size of the reference candle (1R).

- **Filters:**

- Skip the day if the first candle’s range exceeds 200 index points.

- Only the first triggered direction is traded per session.

- All trades are closed before the market closes if neither target nor stop is hit.

- **Execution:** The strategy works best on intraday charts (5m or 15m) and is ideal for traders seeking disciplined, systematic intraday setups.

### Key Features

- Captures the day’s initial momentum burst.

- Strict risk management with predefined stops and targets.

- One trade per day, reducing overtrading and noise.

- Clear-cut, rule-based, and objective system—no discretion required.

**This strategy offers a transparent and robust framework for traders to systematically capture high-probability breakouts in the Hang Seng Index Futures market.**

🟡🔵🟢🔴Beginner's Assistant by carljchapman🟡🔵🟢🔴

Overview

This indicator dynamically marks highs and lows of the premarket (4:00am-9:30amEST) and opening range. It displays Fair Value Gaps, 9 and 21 period Exponential Moving Averages (EMA) and the Volume Weighted Average Price (VWAP). To really help beginners, it marks suggested entry points on the chart with green or red triangles, when a reasonable trend appears.

Features

Automatically draws blue lines for Premarket High and Low values

Dynamically marks the opening Range region

Visual entry signals for long and short opportunities

Primarily used for stocks/funds , but works with forex and crypto

Quick configuration settings to tailor details for your experience level

Mobile friendly mode

Supports alerts

How To Use

Open your chart, and select a 1 or 2 minute timeframe.

Watch for green triangles and red triangles, hinting at entries for long or short positions. Pay particular attention to the price action as it approaches the bounds of the opening range and the premarket levels. I suggest also using a MACD indicator for confirmation of the trend.

For scalping 0dte Options, switch frequently between the 1 ,2 and 5 minute or higher timeframes. Do this so you will not miss an entry opportunity or be unaware of the overall trend.

As a beginner, until you have refined your strategy and develop risk management, take profits as low as 10%. A small profit can quickly become a much larger loss. With 0dte options, time will devour your profits even when the price doesn’t budge.

What makes this indicator so beginner friendly?

Charts with too many lines and colors are are a nightmare for beginners! And empty charts do not tell the whole story. Simple checkboxes in the configuration settings let you turn on and off features to match your comfort level. As you become more familiar you might try turning off the suggested entries to see if you would have selected the same or better ones yourself. Just one example of how you will learn and verify your knowledge. You will quickly spot Opening Range Breakouts and more.

Why are the triangle pointers not simply above or below the bars?

As a beginner, I like to review charts to see how much the price changed, then estimate how much a contract would move based on its delta. A mouthful, I know. But what price does an arrow pointing up below a bar reflect? Would I have entered at the open or close, low or high? This indicator helps by putting the marker close to the price when indicated. It can even display the actual price on the bar. This is helpful for you to make fast calculations without a measuring tool.

I am an experienced trader. Can this help me make winning trades?

Sure. It can also help you make losing ones! Profit is not guaranteed with any indicator or strategy. This indicator is designed to assist you as you learn and while you trade. You won't see the words BUY or SELL. This is not a signal bot! It is merely a tool to assist you. You can learn a lot by spending time observing price movement using this indicator without ever making a single trade.

🟡🔵🟢🔴

ATR Trailing Stop with ATR Targets [v6]What the Indicator Does

This custom TradingView indicator is designed for active traders who want to automate and visualize their trailing stop management and target setting, using true market volatility. It combines the Average True Range (ATR) with dynamic market structure logic to:

Trail a stop-loss behind major swings in real time, using 2×ATR (adjustable) from the highest high in uptrends or the lowest low in downtrends.

Flip trading bias between bullish and bearish when the stop is breached.

Identify and plot three profit targets (at 1, 2, and 3 ATR from the breakout/flip point) after every stop-flip, helping traders scale out or set take-profits objectively.

Maintain a visible presence on your chart every bar to avoid indicator errors, with color and labeling for clear distinction between long/short phases.

How the Indicator Works

1. ATR Calculation

ATR Period and Multiplier: You select your preferred ATR length (default is 14 bars) and a multiplier (default is 2.0).

Volatility Adjustment: ATR measures the average "true" bar range, so the trailing stop and targets adapt to current volatility.

2. Trailing Stop Logic

Uptrend (bullish bias): The indicator tracks the highest high made since the last bearish-to-bullish flip and sets the stop at - .

The stop only raises (never lowers) during an uptrend, protecting gains in strong moves.

Downtrend (bearish bias): Tracks the lowest low made since the last bullish-to-bearish flip, with stop at + .

The stop only lowers (never raises) in a downtrend.

Flip Point: If price closes through the trailing stop, the current bias “flips,” and the logic reverses (bullish to bearish or vice versa). At the new close, flip price and bar index are stored for target calculation.

3. ATR Targets after Flip

After each stop flip:

Three targets—based on the new close price—are calculated and plotted:

Long flip (new bull bias): Target1 = close + 1×ATR, Target2 = close + 2×ATR, Target3 = close + 3×ATR.

Short flip (new bear bias): Target1 = close - 1×ATR, Target2 = close - 2×ATR, Target3 = close - 3×ATR.

These targets help with scaling out, partial profit-taking, or setting automated orders.

4. Visual Feedback

Trailing stop line: Green for long bias, red for short bias.

Targets: Distinct color-coded circles at 1, 2, 3 ATR levels from the most recent flip.

Flip Labels: Mark the bar and price where bias flipped (“Long Flip” or “Short Flip”) for quick pattern recognition.

Subtle background shading: Ensures TradingView's requirement for “indicator output every bar.”

How to Use This Indicator

Parameter Setup

ATR Period and Multiplier: Adjust to match the timeframe and volatility of your instrument.

Lower periods/multipliers for short-term/volatile trading.

Higher values for smoother signals or higher timeframes.

Starting Trend: Set to match the expected initial bias if the instrument has strong trend characteristics.

Trading Application

1. Daily Bias Approach

Establish your bias in line with your trading plan (e.g., only trade long if price is above the previous day's high, short below the previous day's low).

Only look for trades in the indicator's current bias direction, as expressed by the stop and background color.

2. Entry

Use the indicator as a real-time confirmation or trailing stop for your entries.

Breakout: Enter when price establishes the current bias, using the trailing stop as your risk level.

Reversal: Wait for a bias flip after an extended move; enter in the direction of the new bias.

VWAP Rebound: Combine with a VWAP bounce—enter only if the indicator bias supports your direction.

3. Exits/Targets

Trailing stop management: Move your stop according to the plotted line; exit if your stop is hit.

Profit-taking: Scale out or take profits as price approaches each ATR-based target.

Use the dynamic labeling to identify reversal flips and reset your plan if stopped or the bias changes.

4. Market Context

Filter and frame setups by watching correlated indicators (DXY, VIX, AUDJPY, put/call ratio) and upcoming news; trade only in the daily bias direction for best consistency.

5. Practical Tips

Combine this indicator with your custom watchlist and alert settings to get notified on flips or targets.

Review the last label ("Long Flip"/"Short Flip") and targets to plan partial exits.

Remember: ATR adapts to volatility, so the stop and targets stay proportionate even when price action shifts.

NY HIGH LOW BREAKNY HIGH LOW BREAK: A New York Session Breakout Strategy

The "NY HIGH LOW BREAK" indicator is a powerful TradingView script designed to identify and capitalize on breakout opportunities during the New York trading session. This strategy focuses on the initial price action of the New York market open, looking for clear breaches of the high or low established within the first 30 minutes. It's particularly suited for intraday traders who seek to capture momentum-driven moves.

Strategy Logic

The core of the "NY HIGH LOW BREAK" strategy revolves around these key components:

New York Session Opening Range Identification:

The script first identifies the opening range of the New York session. This is defined by the high and low prices established during the first 30 minutes of the New York trading session (from 7:01 AM GMT-4 to 7:31 AM GMT-4).

These crucial levels are then extended forward on the chart as horizontal lines, serving as potential support and resistance zones.

Breakout Signal Generation:

Long Signal: A buy signal is generated when the price breaks above the high of the New York opening range. Specifically, it looks for a candle whose open and close are both above the highLinePrice, and importantly, the previous candle's open was below and close was above the highLinePrice. This indicates a strong upward momentum confirming the breakout.

Short Signal: Conversely, a sell signal is generated when the price breaks below the low of the New York opening range. It looks for a candle whose open and close are both below the lowLinePrice, and the previous candle's open was above and close was below the lowLinePrice. This suggests strong downward momentum confirming the breakdown.

Supertrend Filter (Implicit/Future Enhancement):

While the supertrend and direction variables are present in the code, they are not actively used in the current signal generation logic. This suggests a potential future enhancement where the Supertrend indicator could be incorporated as a trend filter to confirm breakout directions, adding an extra layer of confluence to the signals. For example, only taking long breakouts when Supertrend indicates an uptrend, and short breakouts when Supertrend indicates a downtrend.

Second Candle Confirmation (Possible Future Enhancement):

The close_sec_candle function and openSEC, closeSEC variables indicate an attempt to capture the open and close of a "second candle" (30 minutes after the initial New York open). Currently, closeSEC is used in a specific condition for signal_way but not directly in the primary longSignal or shortSignal logic. This also suggests a potential future refinement where the price action of this second candle could be used for further confirmation or specific entry criteria.

Time-Based Filtering:

Signals are only considered valid within a specific trading window from 8:00 AM GMT-4 to 8:00 AM GMT-4 + 16 * 30 minutes (which is 480 minutes, or 8 hours) on 1-minute and 5-minute timeframes. This ensures that trades are taken during the most active and volatile periods of the New York session, avoiding late-session chop.

The script also highlights the New York session and lunch hours using background colors, providing visual context to the trading day.

Key Features

Automated New York Open Range Detection: The script automatically identifies and plots the high and low of the first 30 minutes of the New York trading session.

Clear Breakout Signals: Visually distinct "BUY" and "SELL" labels appear on the chart when a breakout occurs, making it easy to spot trading opportunities.

Timeframe Adaptability: While optimized for 1-minute and 5-minute timeframes for signal generation, the opening range lines can be displayed on various timeframes.

Customizable Risk-to-Reward (RR): The rr input allows users to define their preferred risk-to-reward ratio for potential trades, although it's not directly implemented in the current signal or trade management logic. This could be used by traders for manual trade management.

Visual Session and Lunch Highlights: The script colors the background to clearly delineate the New York trading session and the lunch break, helping traders understand the market context.

How to Use

Apply the Indicator: Add the "NY HIGH LOW BREAK" indicator to your chart on TradingView.

Select a Relevant Timeframe: For optimal signal generation, use 1-minute or 5-minute timeframes.

Observe the Opening Range: The green and red lines represent the high and low of the first 30 minutes of the New York session.

Look for Breakouts: Wait for price to decisively break above the green line (for a buy) or below the red line (for a sell).

Confirm Signals: The "BUY" or "SELL" labels will appear on the chart when the breakout conditions are met within the active trading window.

Implement Your Risk Management: Use your preferred risk management techniques, including stop-loss and take-profit levels, in conjunction with the signals generated. The rr input can guide your manual risk-to-reward calculations.

Potential Enhancements & Considerations

Supertrend Confirmation: Integrating the supertrend variable to filter signals would significantly enhance the strategy's robustness by aligning trades with the prevailing trend.

Stop-Loss and Take-Profit Automation: The rr input currently serves as a manual guide. Future versions could integrate automated stop-loss and take-profit placement based on this ratio, potentially using ATR for dynamic sizing.

Volume Confirmation: Adding a volume filter to confirm breakouts would ensure that only high-conviction moves are traded.

Backtesting and Optimization: Thorough backtesting across various assets and market conditions is crucial to determine the optimal settings and profitability of this strategy.

Session Times: The current session times are hardcoded. Making these user-definable inputs would allow for greater flexibility across different time zones and trading preferences.

The "NY HIGH LOW BREAK" is a straightforward yet effective strategy for capturing initial New York session momentum. By focusing on clear breakout levels, it aims to provide timely and actionable trading signals for intraday traders.

Pullback Pro Dow Strategy v7 (ADX Filter)

### **Strategy Description (For TradingView)**

#### **Title:** Pullback Pro: Dow Theory & ADX Strategy

---

#### **1. Summary**

This strategy is designed to identify and trade pullbacks within an established trend, based on the core principles of Dow Theory. It uses market structure (pivot highs and lows) to determine the trend direction and an Exponential Moving Average (EMA) to pinpoint pullback entry opportunities.

To enhance trade quality and avoid ranging markets, an ADX (Average Directional Index) filter is integrated to ensure that entries are only taken when the trend has sufficient momentum.

---

#### **2. Core Logic: How It Works**

The strategy's logic is broken down into three main steps:

**Step 1: Trend Determination (Dow Theory)**

* The primary trend is identified by analyzing recent pivot points.

* An **Uptrend** is confirmed when the script detects a pattern of higher highs and higher lows (HH/HL).

* A **Downtrend** is confirmed by a pattern of lower highs and lower lows (LH/LL).

* If neither pattern is present, the strategy considers the market to be in a range and will not seek trades.

**Step 2: Entry Signal (Pullback to EMA)**

* Once a clear trend is established, the strategy waits for a price correction.

* **Long Entry:** In a confirmed uptrend, a long position is initiated when the price pulls back and crosses *under* the specified EMA.

* **Short Entry:** In a confirmed downtrend, a short position is initiated when the price rallies and crosses *over* the EMA.

**Step 3: Confirmation & Risk Management**

* **ADX Filter:** To ensure the trend is strong enough to trade, an entry signal is only validated if the ADX value is above a user-defined threshold (e.g., 25). This helps filter out weak signals during choppy or consolidating markets.

* **Stop Loss:** The initial Stop Loss is automatically and logically placed at the last market structure point:

* For long trades, it's placed at the `lastPivotLow`.

* For short trades, it's placed at the `lastPivotHigh`.

* **Take Profit:** Two Take Profit levels are calculated based on user-defined Risk-to-Reward (R:R) ratios. The strategy allows for partial profit-taking at the first target (TP1), moving the remainder of the position to the second target (TP2).

---

#### **3. Input Settings Explained**

**① Dow Theory Settings**

* **Pivot Lookback Period:** Determines the sensitivity for detecting pivot highs and lows. A smaller number makes it more sensitive to recent price swings; a larger number focuses on more significant, longer-term pivots.

**② Entry Logic (Pullback)**

* **Pullback EMA Length:** Sets the period for the Exponential Moving Average used to identify pullback entries.

**③ Risk & Exit Management**

* **Take Profit 1 R:R:** Sets the Risk-to-Reward ratio for the first take-profit target.

* **Take Profit 1 (%):** The percentage of the position to be closed when TP1 is hit.

* **Take Profit 2 R:R:** Sets the Risk-to-Reward ratio for the final take-profit target.

**④ Filters**

* **Use ADX Trend Filter:** A master switch to enable or disable the ADX filter.

* **ADX Length:** The lookback period for the ADX calculation.

* **ADX Threshold:** The minimum ADX value required to confirm a trade signal. Trades will only be placed if the ADX is above this level.

---

#### **4. Best Practices & Recommendations**

* This is a trend-following system. It is designed to perform best in markets that exhibit clear, sustained trending behavior.

* It may underperform in choppy, sideways, or strongly ranging markets. The ADX filter is designed to help mitigate this, but no filter is perfect.

* **Crucially, you must backtest this strategy thoroughly** on your preferred financial instrument and timeframe before considering any live application.

* Experiment with the `Pivot Lookback Period`, `Pullback EMA Length`, and `ADX Threshold` to optimize performance for a specific market's characteristics.

---

#### **DISCLAIMER**

This script is provided for educational and informational purposes only. It does not constitute financial advice. All trading involves a high level of risk, and past performance is not indicative of future results. You are solely responsible for your own trading decisions. The author assumes no liability for any financial losses you may incur from using this strategy. Always conduct your own research and due diligence.

Rifle UnifiedThis script is designed for use on 30-second charts of Dow Jones-related symbols (YM, MYM, US30). It provides automated buy and sell signals using a combination of price action, RSI (Relative Strength Index), and volume analysis. The script is intended for both live trading signals and backtesting, with configurable risk management and debugging features.

Core Functionality

1. Signal Generation Logic

Trigger: The algorithm looks for a sharp price move (drop or rise) of a user-defined threshold (default: 80 points) within a specified lookback window (default: 20 minutes).

Levels: It monitors for price drops below specific numerical levels ending in 23, 43, or 73 (e.g., 42223, 42273).

RSI Condition: When price falls below one of these levels and the RSI is below 30, the setup is considered active.

Buy Signal: A buy is triggered if, after setup:

Price rises back above the level,

The RSI rate of change (ROC) indicates exhaustion of the drop,

The current bar shows positive momentum.

2. Trade Management

Stop Loss & Take Profit: Configurable fixed or trailing stop loss and take profit levels are plotted and managed automatically.

Exit Signals: The script signals exit based on price action relative to these risk management levels.

3. Filters & Enhancements

Parabolic Move Filter: Prevents entries during extreme price moves.

Dead Cat Bounce Filter: Avoids false signals after sharp reversals.

Volume Filter: Optionally requires volume conditions for trade entries (especially for shorts).

Multiple Confirmation Layers : Includes checks for 5-minute RSI, momentum, and price retracement.

User Inputs & Customization

Trade Direction: Toggle between LONG and SHORT signal generation.

Trigger Settings: Adjust thresholds for price moves, lookback windows, RSI ROC, and volume requirements.

Trade Settings: Set take profit, stop loss, and trailing stop behavior.

Debug & Visualization: Enable or disable various plots, labels, and debug tables for in-depth analysis.

Backtesting: Integrated backtester with summary and detailed statistics tables.

Technical Features

Uses External Libraries: Relies on RifleShooterLib for core logic and BackTestLib for backtesting and statistics.

Multi-timeframe Analysis: Incorporates both 30-second and 5-minute RSI calculations.

Chart Annotations: Plots entry/exit points, risk levels, and debug information directly on the chart.

Alert Conditions: Built-in alert triggers for key events (initial move, stall, entry).

Intended Use

Markets: Dow Jones symbols (YM, MYM, US30, or US30 CFD).

Timeframe: 30-second chart.

Purpose: Automated signal generation for discretionary or algorithmic trading, with robust risk management and backtesting support.

Notable Customization & Extension Points

Momentum Calculation: Plans to replace the current momentum measure with "sqz momentum".

Displacement Logic: Future update to use "FVG concept" for displacement.

High-Contrast RSI: Optional visual enhancements for RSI extremes.

Time-based Stop: Consideration for adding a time-based stop mechanism.

This script is highly modular, with extensive user controls, and is suitable for both live trading and historical analysis of Dow Jones index movements

Price Reaction Analysis by Day of WeekOverview

The "Price Reaction Analysis by Day of Week" indicator is a tool that enables traders to analyze historical price reaction patterns to technical indicator signals on a selected day of the week. It examines price behavior on a chosen candle (from 1 to 30) in the next day or subsequent days after a signal, depending on the timeframe, and provides success rate statistics to support data-driven trading decisions. The indicator is optimized for timeframes up to 1 day (e.g., 1D, 12H, 8H, 6H, 4H, 1H, 15M), as the analysis relies on day-of-week comparisons. Lower timeframes generate more signals due to the higher number of candles per day.

Key Features

1. Flexible Technical Indicator Selection

Users can choose one of four technical indicators: RSI, SMI, MA, or Bollinger Bands. Each indicator has configurable parameters, such as:

RSI length, oversold/overbought levels.

SMI length, %K and %D smoothing, signal levels.

MA length.

Bollinger Bands length and multiplier.

2. Day-of-Week Analysis

The indicator allows users to select a day of the week (Monday, Tuesday, Wednesday, Thursday, Friday) for generating signals. It analyzes price reactions on a selected candle (from 1 to 30) in the next day or subsequent days after the signal. Examples:

On a daily timeframe, a signal on Monday can be analyzed for the first, fourth, or later candle (up to 30) in subsequent days (e.g., Tuesday, Wednesday).

On timeframes lower than 1 day (e.g., 12H, 8H, 6H, 4H, 1H, 15M), the analysis targets the selected candle in the next day or subsequent days. For example, on a 4H timeframe, you can analyze the second Tuesday candle following a Monday signal. The maximum timeframe is 1 day to ensure consistent day-of-week analysis.

3. Visual Signals

Signals for the analysis period are marked with background highlights in real-time when the indicator’s conditions are met. The last highlighted candle of the selected day is always analyzed. Arrows are displayed on the chart at the candle specified by the “Candles to Compare” setting (e.g., the first candle if set to 1):

Green upward triangles (below the candle) for successful buy signals (the closing price of the selected candle is higher than the signal candle’s close).

Red downward triangles (above the candle) for successful sell signals (the closing price of the selected candle is lower than the signal candle’s close).

Gray “x” marks for unsuccessful signals (no price reversal in the expected direction). Arrow positions are intuitive: buy signals below the candle, sell signals above. Highlights and arrows do not require waiting for future signals but are essential for calculating statistics.

Note: The first candle of the next day may appear shifted on the chart due to timezone differences, which can affect the timing of signal appearance.

4. Signal Conditions (Highlights) for Each Indicator

RSI: The oscillator is in oversold (buy) or overbought (sell) zones.

SMI: SMI returns from oversold (buy) or overbought (sell) zones.

MA: Price crosses the MA (upward for buy, downward for sell).

Bollinger Bands: Price returns inside the bands (from below for buy, from above for sell).

5. Success Rate Statistics

A table in the top-right corner of the chart displays:

The number of buy and sell signals for the selected day of the week.

The percentage of cases where the price of the selected candle in the next day or subsequent days reversed as expected (e.g., rising after a buy signal). Statistics are based on comparing the closing price of the signal candle with the closing price of the selected candle (e.g., first, fourth) in the next day or subsequent days.

Important: Statistics do not account for price movements within the candle or after its close. The price on the selected candle (e.g., fourth) may be lower than earlier candles but still higher than the signal candle, counting as a positive buy signal, though it does not guarantee profit.

6. Date Range

Users can specify the analysis date range, enabling strategy testing on historical data from a chosen period. Ensure the start and end dates are set correctly.

Applications

The indicator is designed for traders who want to leverage historical patterns for position planning. Examples:

On a 4-hour timeframe: If a sell signal highlight appears on Monday and statistics show an 80% chance that the fourth Tuesday candle is bearish, traders may consider playing a correction at the open of that candle.

On a daily timeframe: If a highlight indicates market overheating, traders may consider entering a position at the open of the first candle after the signal (e.g., Tuesday), provided statistics suggest an edge. Users can analyze the signal on the first candle and check later candles to validate results, increasing confidence in consistent patterns.

Key Settings

Indicator Type: Choose between RSI, SMI, MA, or Bollinger Bands.

Selected Day: Monday, Tuesday, Wednesday, Thursday, or Friday.

Candles to Compare: The number of the candle in the next day or subsequent days (from 1 to 30).

Indicator Parameters: Lengths, levels (e.g., oversold/overbought for RSI).

Background Colors: Configurable highlights for buy and sell signals.

Notes

Timeframes: The indicator is optimized for timeframes up to 1 day (e.g., 1D, 12H, 8H, 6H, 4H, 1H, 15M), as the analysis relies on day-of-week patterns. Timeframes lower than 1 day generate more signals due to the higher number of candles per day.

Candle Shift: The first candle of the next day may appear shifted on the chart due to timezone differences, affecting the timing of signals across markets or platforms.

Statistical Limitations: Results are based on the closing prices of the selected candle, ignoring fluctuations in earlier candles, within the candle, or subsequent price movements. Traders must assess whether entering at the open or after the close of the selected candle is profitable.

Testing: Effectiveness depends on historical data and parameter settings. Testing different configurations across markets and timeframes is recommended.

Who Is It For?

Swing and position traders who base decisions on technical analysis and historical patterns.

Market analysts seeking patterns in price behavior by day of the week.

TradingView users of all experience levels, thanks to an intuitive interface and flexible settings.

GCM Bull Bear RiderGCM Bull Bear Rider (GCM BBR)

Your Ultimate Trend-Riding Companion