Market Sessions [odnac]

This indicator highlights the three main global market sessions (USA, Europe, Asia) and their overlaps directly on the chart.

It helps traders quickly identify active trading periods and potential high-liquidity overlaps.

Features:

Customizable start and end times for each session

Optional daily dividers with weekday labels

Session markers displayed as circles above the candles

Overlap sessions displayed in distinct colors

Adjustable opacity for better chart visibility

Option to hide weekends

Sessions included:

USA Market Session (default 13:30–20:00 UTC)

Europe Market Session (default 07:00–16:00 UTC)

Asia Market Session (default 00:00–09:00 UTC)

Overlaps: USA + Europe, USA + Asia, Europe + Asia

This tool is designed for intraday timeframes (1m–60m) and can be useful for scalping, day trading, or session-based strategies.

Cerca negli script per "session"

Named SessionsShows London, New York and Tokyo sessions (and optionally Sydney).

Beginner-friendly - shows names of sessions, not just colors

Marks low and high of session

Shows if session is currently open

Session names can be customized

Session label is placed above or below depending on price move during session, visually indicating the trend (also works during open session)

Is displayed only on timeframes below 4H

How it works

Session trend is calculated simply by subtracting the session's opening price from the session's closing price (or current price if session is open).

If there is a gap before the session, the previous close is used instead of the first candle's open price.

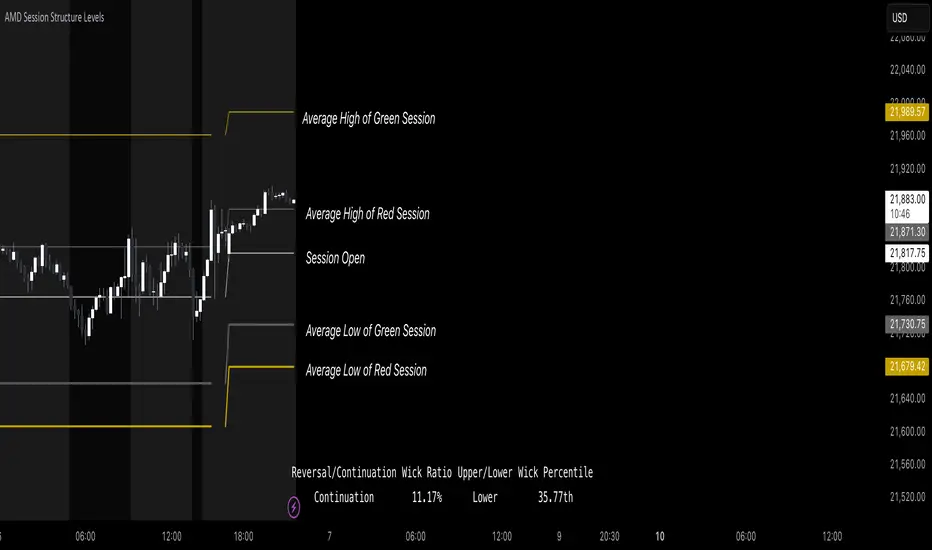

AMD Session Structure Levels# Market Structure & Manipulation Probability Indicator

## Overview

This advanced indicator is designed for traders who want a systematic approach to analyzing market structure, identifying manipulation, and assessing probability-based trade setups. It incorporates four core components:

### 1. Session Price Action Analysis

- Tracks **OHLC (Open, High, Low, Close)** within defined sessions.

- Implements a **dual tracking system**:

- **Official session levels** (fixed from the session open to close).

- **Real-time max/min tracking** to differentiate between temporary spikes and real price acceptance.

### 2. Market Manipulation Detection

- Identifies **manipulative price action** using the relationship between the open and close:

- If **price closes below open** → assumes **upward manipulation**, followed by **downward distribution**.

- If **price closes above open** → assumes **downward manipulation**, followed by **upward distribution**.

- Normalized using **ATR**, ensuring adaptability across different volatility conditions.

### 3. Probability Engine

- Tracks **historical wick ratios** to assess trend vs. reversal conditions.

- Calculates **conditional probabilities** for price moves.

- Uses a **special threshold system (0.45 and 0.03)** for reversal signals.

- Provides **real-time probability updates** to enhance trade decision-making.

### 4. Market Condition Classification

- Classifies market conditions using a **wick-to-body ratio**:

```pine

wick_to_body_ratio = open > close ? upper_wick / (high - low) : lower_wick / (high - low)

```

- **Low ratio (<0.25)** → Likely a **trend day**.

- **High ratio (>0.25)** → Likely a **range day**.

---

## Why This Indicator Stands Out

### ✅ Smarter Level Detection

- Uses **ATR-based dynamic levels** instead of static support/resistance.

- Differentiates **manipulation from distribution** for better decision-making.

- Updates probabilities **in real-time**.

### ✅ Memory-Efficient Design

- Implements **circular buffers** to maintain efficiency:

```pine

var float manipUp = array.new_float(lookbackPeriod, 0.0)

var float manipDown = array.new_float(lookbackPeriod, 0.0)

```

- Ensures **constant memory usage**, even over extended trading sessions.

### ✅ Advanced Probability Calculation

- Utilizes **conditional probabilities** instead of simple averages.

- Incorporates **market context** through wick analysis.

- Provides **actionable signals** via a probability table.

---

## Trading Strategy Guide

### **Best Entry Setups**

✅ Wait for **price to approach manipulation levels**.

✅ Confirm using the **probability table**.

✅ Check the **wick ratio for context**.

✅ Enter when **conditional probability aligns**.

### **Smart Exit Management**

✅ Use **distribution levels** as **profit targets**.

✅ Scale out **when probabilities shift**.

✅ Monitor **wick percentiles** for confirmation.

### **Risk Management**

✅ Size positions based on **probability readings**.

✅ Place stops at **manipulation levels**.

✅ Adjust position size based on **trend vs. range classification**.

---

## Configuration Tips

### **Session Settings**

```pine

sessionTime = input.session("0830-1500", "Session Hours")

weekDays = input.string("23456", "Active Days")

```

- Match these to your **primary trading session**.

- Adjust for different **market opens** if needed.

### **Analysis Parameters**

```pine

lookbackPeriod = input.int(50, "Lookback Period")

low_threshold = input.float(0.25, "Trend/Range Threshold")

```

- **50 periods** is a good starting point but can be optimized per instrument.

- The **0.25 threshold** is ideal for most markets but may need adjustments.

---

## Market Structure Breakdown

### **Trend/Continuation Days**

- **Characteristics:**

✅ Small **opposing wicks** (minimal counter-pressure).

✅ Clean, **directional price movement**.

- **Bullish Trend Day Example:**

✅ Small **lower wicks** (minimal downward pressure).

✅ Strong **closes near the highs** → **Buyers in control**.

- **Bearish Trend Day Example:**

✅ Small **upper wicks** (minimal upward pressure).

✅ Strong **closes near the lows** → **Sellers in control**.

### **Reversal Days**

- **Characteristics:**

✅ **Large opposing wicks** → Failed momentum in the initial direction.

- **Bullish Reversal Example:**

✅ **Large upper wick early**.

✅ **Strong close from the lows** → **Sellers failed to maintain control**.

- **Bearish Reversal Example:**

✅ **Large lower wick early**.

✅ **Weak close from the highs** → **Buyers failed to maintain control**.

---

## Summary

This indicator systematically quantifies market structure by measuring **manipulation, distribution, and probability-driven trade setups**. Unlike traditional indicators, it adapts dynamically using **ATR, historical probabilities, and real-time tracking** to offer a structured, data-driven approach to trading.

🚀 **Use this tool to enhance your decision-making and gain an objective edge in the market!**

TLA20 - Multi-Session Box and Level ToolTLA20 is a highly customizable indicator designed to enhance intraday analysis by marking predefined trading sessions, key levels, and midpoints directly on your charts. With its versatile features, TLA20 is ideal for traders looking to visualize multiple time zones, daily price ranges, and historical reference levels efficiently.

Key Features:

Session Visualization: Mark up to three custom trading sessions with distinct start and end times, adjustable for different time zones and weekend inclusions.

Dynamic Highlights: Automatically draw session highs, lows, midlines, and open prices with options to extend beyond session bounds.

Custom Styling: Configure border colors, styles, and fill options for each session box to match your chart preferences.

Historical Levels: Highlight previous daily highs/lows, weekly highs/lows, and monthly highs/lows for improved context in your trading.

Intuitive Adjustments: Enable or disable each feature and customize settings for precise alignment with your trading strategy.

Use Cases:

Track trading sessions across different markets and time zones.

Identify key price levels like session midpoints and opens for entry/exit strategies.

Overlay historical levels to recognize potential support and resistance areas.

This indicator does not provide direct trading signals but serves as a robust tool for enhancing technical analysis.

Disclaimer: The script is provided “as is” without warranties of any kind. Always test on a demo account before applying in live markets.

NY Killzone (Morning, Lunch, Afternoon)Indicator for New York session that splits Morning, Lunch and Afternoon part of the session.

Works on Time Frames of 30m and below.

GBPJPY Pro: 1H Trend + Prob + Sessions + Timer + Swings📊 GBPJPY – Table Explanation (High Volatility Control)

GBPJPY is fast and volatile.

The table is designed to protect you before profit.

🔹 Market Trend (1H)

The most important field for this pair.

Trading against the trend is very risky

👉 Always follow the 1H trend.

🔹 Session

Best trading times:

London

London–New York Overlap

👉 Avoid trading outside these sessions.

🔹 Candle Time Left

Extremely important for GBPJPY.

Entering before candle close can be dangerous

👉 Always wait for confirmation.

🔹 Buy / Sell Probability

50%+ can be acceptable due to strong moves

“READY” status is more important than the number

👉 Quality over quantity.

🔹 RSI / Volume

RSI moves fast

Strong volume often precedes sharp moves

⚠️ Result:

A defensive table that helps avoid late or emotional entries.

Multi-Session H/L - Sweep & Grab v5# Multi-Session High/Low Levels with Liquidity Sweep & Grab Detection

## Overview

This indicator automatically identifies and plots the High and Low levels of key trading sessions (Asia, London, New York AM, New York PM) and Previous Day levels. It features advanced **Liquidity Sweep** and **Liquidity Grab** detection based on ICT/SMC methodology.

## Key Features

### 📊 Multi-Session Tracking

- **Asia Session** - Captures the Asian trading range

- **London Session** - Tracks the London open volatility

- **New York AM Session** - Monitors the NY morning session

- **New York PM Session** - Follows the afternoon price action

- **Previous Day High/Low** - Key daily reference levels

### 💧 Liquidity Detection (ICT/SMC Concepts)

**Liquidity Grab:**

- Detected when price **wicks through** a level but **closes back** inside

- Single candle event with rejection

- Often signals a potential reversal

- Label shows: `"Session H/L (Grab)"`

**Liquidity Sweep:**

- Detected when price **closes beyond** the level

- Indicates liquidity has been fully taken

- Label shows: `"Session H/L (Swept)"`

### 🎯 Visual Features

- Lines automatically **stop at the candle** where liquidity was grabbed or swept

- Different line styles for Active / Grabbed / Swept levels

- Customizable colors for each session

- Optional session background highlighting

- Information table showing all levels and their status

### ⚙️ Customization Options

- Adjustable session times for any timezone (GMT+0 to GMT+5)

- Calculation timeframe selection

- Line width and style settings

- Label size options

- Toggle each session on/off

- "Stop Line on Grab" option

### 🔔 Alerts

- Separate alerts for **Liquidity Grab** events

- Separate alerts for **Liquidity Sweep** events

- Available for all sessions and Previous Day levels

## How to Use

1. **Identify Key Levels:** The indicator automatically marks session highs and lows

2. **Watch for Liquidity Events:** Monitor when price approaches these levels

3. **Grab = Potential Reversal:** A liquidity grab (wick rejection) often signals smart money has collected orders and price may reverse

4. **Sweep = Liquidity Taken:** A sweep (close beyond level) confirms the liquidity pool has been cleared

5. **Plan Your Trades:** Use these levels in confluence with other SMC concepts like Fair Value Gaps (FVG) and Order Blocks (OB)

## Status Colors in Table

- 🟢 **Green (Active)** - Level has not been touched

- 🟠 **Orange (Grab)** - Wick touched the level, potential reversal zone

- 🔴 **Red (Swept)** - Close beyond level, liquidity fully taken

## Settings Explained

| Setting | Description |

|---------|-------------|

| Calculation Timeframe | Timeframe used for session calculations |

| Timezone | Your broker's timezone (GMT+0 to GMT+5) |

| Extend Lines | Extend active lines into the future |

| Stop Line on Grab | If enabled, lines stop when grabbed (not just swept) |

| Swept/Grab Line Style | Visual differentiation for liquidity events |

## Notes

- Works on all markets (Forex, Crypto, Stocks, Indices, Commodities)

- Best used on timeframes from 1min to 1H

- Session times are fully customizable to match your time zone

- The indicator respects the ICT/SMC definition where a **Grab** is a single-candle wick rejection and a **Sweep** involves price closing beyond the level

Night Mode Session | ZeeZeeMon🇷🇺 Описание (Russian)

Night Mode Session Highlight

Night Mode Session Highlight — это визуальный индикатор, предназначенный для подсветки заданного временного диапазона на графике. Индикатор позволяет выделять ночную торговую сессию или любой другой временной интервал с помощью фоновой заливки, что упрощает анализ поведения цены в определённые часы.

Основные возможности

Подсветка выбранного временного диапазона на графике

Настройка времени сессии в формате HHMM–HHMM

Выбор таймзоны из выпадающего списка (IANA)

Настраиваемый цвет и прозрачность фоновой заливки

Корректная работа с интервалами, пересекающими полночь

Совместимость со всеми таймфреймами и инструментами

Параметры

Ночной режим (сессия) — временной интервал, который будет подсвечиваться (например, 0000-0800)

Таймзона — таймзона, относительно которой рассчитывается сессия

Цвет ночной подсветки — цвет и прозрачность фоновой заливки

Принцип работы

Индикатор проверяет, попадает ли текущий бар в заданную временную сессию с учётом выбранной таймзоны. Если условие выполняется, фон графика окрашивается выбранным цветом.

Назначение

Индикатор может использоваться для:

анализа ночной или азиатской сессии

визуального разделения торговых периодов

изучения волатильности и ликвидности в разные часы

вспомогательной визуальной фильтрации графика

Индикатор не генерирует торговых сигналов и не является торговой стратегией.

🇬🇧 Description (English)

Night Mode Session Highlight

Night Mode Session Highlight is a visual indicator designed to highlight a specific time range on the chart. It allows users to mark the night trading session or any custom time interval using background shading, making it easier to analyze price behavior during selected hours.

Key Features

Highlights a custom time session on the chart

Session time input in HHMM–HHMM format

Timezone selection via dropdown list (IANA)

Customizable background color and transparency

Correct handling of sessions crossing midnight

Works on all timeframes and instruments

Settings

Night Session — time range to be highlighted (e.g. 0000-0800)

Timezone — timezone used for session calculation

Night Background Color — background shading color and transparency

How It Works

The indicator checks whether the current bar belongs to the specified session using the selected timezone. If the condition is met, the chart background is filled with the chosen color.

Purpose

This indicator can be used for:

analyzing night or Asian trading sessions

visually separating trading periods

studying volatility and liquidity at different times

additional visual filtering of the chart

This indicator does not generate trading signals and is not a trading strategy.

Crypto Session Range 📄 INDICATOR DESCRIPTION (ENGLISH)

Crypto Session Range (Custom Timezone) is a lightweight and accurate session-based indicator designed specifically for cryptocurrency markets (24/7).

This indicator allows traders to define custom trading time windows using any global timezone, solving common issues found in traditional session indicators that are built for stock markets.

🔹 Key Features

Custom timezone support (e.g. America/Puerto_Rico, America/New_York, UTC)

Up to 3 configurable trading sessions

Visual background highlighting during active sessions

Automatic High & Low range tracking for each session

Optional range extension after the session ends

Works on all crypto pairs and timeframes

🔹 Who Is This For?

Crypto traders who want precise session control

Day traders, scalpers, and session-based strategies

Traders who operate during specific market windows (London / NY / custom)

🔹 Notes

This indicator is not restricted to exchange trading hours and is fully compatible with 24/7 markets like crypto, unlike many default session tools.

CVD Flow Labels for Sessions Ranges [AMT Edition]CVD Flow Labels for Session Ranges

Description:

This script provides a session-aware Cumulative Volume Delta (CVD) analysis designed to enhance the “Session Ranges ” framework by combining price extremes with detailed volume flow dynamics. Unlike generic trend or scalping indicators, this tool focuses on identifying aggressive buying and selling pressure, distinguishing between absorption (failed auctions where aggressive flows are rejected) and acceptance (confirmed continuation of flows).

How it works:

CVD Calculation: The script calculates delta for each bar using a choice of Total, Periodic, or EMA-based cumulative methods. Delta represents the net difference between estimated buying and selling volume per bar.

Normalization: By normalizing delta relative to recent volatility, it highlights extreme flows that are statistically significant, making large shifts in market sentiment easier to spot.

Session-Specific Analysis: The indicator separates Asia, London, and New York sessions to allow context-sensitive interpretation of price and volume interactions. Each session’s extremes are monitored, and flow labels are plotted relative to these extremes.

Flow Labels: Bullish and bearish absorption (“ABS”) and acceptance (“ACC WEAK/STRONG”) labels provide immediate visual cues about whether aggressive flows are being absorbed or accepted at key price levels.

Alerts: Configurable alerts trigger when absorption or acceptance occurs, supporting active trading or strategy automation.

Originality & Usefulness:

This script is original because it integrates volume-based auction theory with session-specific market structure, rather than simply showing trend or scalping signals. By combining CVD dynamics with session extreme levels from the “Session Ranges ” script, traders can:

Identify where price is likely to be accepted or rejected.

Confirm aggressive buying or selling flows before entering trades.

Time entries near session extremes with higher probability setups.

How to use:

Apply the “Session Ranges ” to see session highs, lows, and interaction lines.

Use this CVD Flow Labels script to visualize absorption and acceptance at these session levels.

Enter trades based on alignment of session extremes and flow signals:

Absorption at a session extreme may indicate a potential reversal.

Acceptance suggests continuation in the direction of the flow.

Alerts can help manage trades without constant screen monitoring.

This tool is designed to give traders a structured, session-based view of market auctions, providing actionable insights that go beyond typical trend-following or scalping methods. It emphasizes flow analysis and statistical extremes, enabling traders to make more informed decisions grounded in market microstructure.

Dual Session Range Boxes with FIB Lines█ OVERVIEW

The Dual Session Range Boxes with FIB Lines indicator is a powerful tool for identifying and visualizing Range Breakout or Inside Boxes Strategy setups with dual session tracking, customizable Fibonacci extensions, and trade zone levels. Perfect for traders who focus on session-based strategies across multiple markets.

█ FEATURES

◆ DUAL SESSION RANGES

- Range 1: Defines the Range (ORB) based on a specific time window

- Range 2: Extends the Range levels throughout a second session for trade management

- Both ranges can be independently configured with preset sessions or custom times

◆ SESSION PRESETS

- Tokyo Session (00:00 - 09:00)

- London Session (08:00 - 17:00)

- New York Session (14:00 - 21:00)

- Pre Market Session (10:00 - 15:30)

- Custom Time: Define your own session windows

◆ FIBONACCI EXTENSION LEVELS

- Automatically calculated from Range 1 High/Low

- Buy Side Levels: Projected above the range (green)

- Sell Side Levels: Projected below the range (red)

- 10 customizable Fib levels with individual on/off toggles:

- 23.6%, 38.2%, 50%, 61.8%, 78.6%, 100%, 127.2%, 161.8%, 200%, 261.8%

- Special color highlighting for key levels (50%, 100%, 200%)

- All percentage values are fully editable

◆ INSIDE TRADE ZONES

- Two horizontal lines drawn inside the Range 1 box

- Configurable percentage from High/Low (default: 10%)

- Helps identify premium/discount zones within the range

◆ LABELS & DISPLAY OPTIONS

- Show/hide price values on labels

- Show/hide percentage values on labels

- Adjustable label size (Tiny, Small, Normal, Large, Huge)

- Configurable label offset (distance above lines)

- Multiple rounding options for price display:

- 0.25 (quarter points - ideal for indices)

- 0.1 (tenth points)

- 0.01 (two decimals)

◆ STYLE CUSTOMIZATION

- Independent fill and border colors for both ranges

- Adjustable border width (1-5)

- Line style options: Solid, Dashed, Dotted

- Separate color settings for:

- Buy side Fibonacci levels

- Sell side Fibonacci levels

- Trade zone lines

- Special levels (50%, 100%, 200%)

◆ HISTORICAL DATA CONTROL

- Toggle to show/hide historical sessions

- Current session always remains visible

- Clean chart view when analyzing only the active session

█ HOW TO USE

1. Set your timezone in General settings

2. Configure Range 1 to capture your desired Opening Range period

3. Configure Range 2 to define how long levels should extend

4. Adjust Fibonacci levels based on your trading strategy

5. Use Trade Zones to identify key areas within the range

6. Toggle historical data on/off based on your analysis needs

█ USE CASES

- Opening Range Breakout (ORB) strategies

- Session-based trading (London, New York, Tokyo, Pre-Market)

- Fibonacci extension targets for breakout trades

- Identifying support/resistance from session ranges

- Multi-session analysis and confluence zones

█ NOTES

- Indicator works on timeframes lower than Daily

- All times are based on the selected timezone setting

- Range 2 only activates after Range 1 completes

- Fibonacci levels extend from Range 1 start to Range 2 end

Let me know if you like to have any enhancements.

Leave a like if you like it!

Range Deviations PRO | Trade SymmetryRange Deviations PRO — Extended Session Levels

An enhanced version of the original Range Deviations by @joshuuu, retaining the full core logic while adding a key upgrade:

🔹 All session ranges, midlines, and deviation levels now extend into the next trading session, giving seamless multi-session context.

Supports Asia, CBDR, Flout, ONS, and Custom Sessions — with options for half/full standard deviations, equilibrium, and range boxes exactly as in the original.

Extending these levels helps identify:

• Liquidity sweeps

• Trap moves / false breaks

• Daily high/low projections

• Premium–discount behavior across sessions

Ideal for traders using ICT concepts who want clearer continuation of session structure into the next day.

Credit: Original logic by @joshuuu — enhancements by TradeSymmetry.

Disclaimer: Educational use only. Not financial advice.

Asia & London Session Boxes (NY Time) + 4H SwingsAsia & London Session Boxes + 4H Swings

Description

A multi-timeframe session analysis tool designed for forex and futures traders operating on NY time. This indicator visualizes major trading sessions with automatic high/low range boxes while simultaneously tracking 4-hour swing levels, giving you a complete picture of institutional trading activity and key price levels.

How It Works

Session Boxes (NY Time Zone)

Asia Session (20:00 – 00:00 NY): Blue-shaded box marking the complete range from open to close

London Session (02:00 – 06:00 NY): Yellow-shaded box capturing the high-volatility London open

Each session box automatically records the highest high and lowest low during that timeframe, providing instant reference for session extremes and potential supply/demand zones.

4-Hour Swing Levels

Detects swing highs and lows on a 30-minute timeframe for ultra-responsive level identification

Red lines: Swing highs (resistance levels)

Green lines: Swing lows (support levels)

Lines extend to the right for continuous monitoring

Auto-removes touched levels: When price breaches a swing, it automatically deletes that level to keep your chart clean and focused on active levels

Key Features

Session-Based Trading Analysis: Identify which session created important price levels and ranges

Multi-Timeframe Architecture: Analyzes 30-minute swings while tracking 4-hour patterns on your current chart

Smart Level Cleanup: Touched swings automatically remove themselves, eliminating clutter

NY Time Conversion: All times automatically adjust to your NY timezone for consistency

Institutional Perspective: View exactly where institutions are trading during major session hours

Zero Lag Detection: Real-time identification of swing extremes

Ideal For

Forex traders (especially EUR/USD, GBP/USD) targeting session breakouts

Scalpers and swing traders needing precise support/resistance levels

Market structure traders analyzing institutional price action

Session traders looking to trade Asia/London opens

1-minute to 4-hour timeframe charts

Trading Applications

Trade Asia session breakouts into London

Identify liquidity zones from previous sessions

Detect swing extremes for entry/exit planning

Confirm trend direction using multi-session structure

Find support/resistance on intraday pullbacks

Default Settings Optimized For

NASDAQ futures and forex pairs

Scalping and short-term swing trading

NY timezone trading (automatically converts UTC-4)

30-minute swing detection for precise level identification

ALN Sessions Box — Auto- DSTDevoleper: Sheikh Rakib

What it does

Draws candle-synced high/low range boxes for the three major sessions—Asia (Dhaka view), London, and New York—on any timeframe. London and New York are DST-aware (times auto-shift on DST changes). Boxes update live with session high/low and close exactly on the session’s final bar.

Key features

Auto-DST: Uses Europe/London and America/New_York time zones, so session windows auto-adjust when DST turns on/off.

Asia (BDT) window: Default 06:00–15:00 Asia/Dhaka (no DST).

Candle-linked boxes: Top/bottom track session High/Low; right edge finalizes on the session end bar—clean breakout zones.

Clean UI: Optional labels, outline toggle, and three opacity presets (Dark/Medium/Light).

Plug & play: Drop in, customize colors/times, done.

Inputs you can tweak

Time Range (LOCAL) for each session

Defaults: Asia 06:00–15:00 (Asia/Dhaka), London 08:00–17:00 (Europe/London), New York 08:00–17:00 (America/New_York)

For equities, switch New York to 09:30–16:00—DST handling remains automatic.

Colour per session, Show Session Labels, Show Range Outline, Opacity Preset.

UTC Offset input is retained for compatibility but not used for session detection.

Quick BDT reference (for the default 08:00–17:00 local windows)

London → DST ON (BST): 13:00–22:00 BDT · DST OFF (GMT): 14:00–23:00 BDT

New York → DST ON (EDT): 18:00–03:00 BDT (next day) · DST OFF (EST): 19:00–04:00 BDT (next day)

Asia (Dhaka) → 06:00–15:00 BDT (no DST)

Tips

If you see dotted vertical lines, that’s TradingView Session breaks (Chart Settings → Appearance). Turn off if you prefer a cleaner view.

Some symbols don’t trade during parts of a session—adjust Time Range as needed.

Labels are placed inside the box; adjust opacity/colors to suit your theme.

A sharp, professional session map for spotting breakouts, reversals, and volatility windows at a glance.

AutoDay MA (Session-Normalized)📊 AutoDay MA (Session-Normalized Moving Average)

⚡ Daily power, intraday precision.

AutoDay MA automatically converts any N-day moving average into the exact equivalent on your current intraday timeframe.

💡 Concept inspired by Brian Shannon (Alphatrends) – mapping daily MAs onto intraday charts by normalizing session minutes.

🛠 How it works

Set Days (N) (e.g., 5, 10, 20).

Define Session Minutes per Day (⏱ 390 = US RTH, 🌍 1440 = 24h).

The indicator detects your chart’s timeframe and computes:

Length = (Days × SessionMinutes) / BarMinutes

Applies your chosen MA type (📐 SMA / EMA / RMA / WMA) with rounding (nearest, up, down).

Displays all details in a clear corner info panel.

✅ Why use it

Consistency 🔄: Same 5-day smoothing across all intraday charts.

Session-aware 🕒: Works for equities, futures, FX, crypto.

Transparency 🔍: Always shows the math & final MA length.

Alerts built-in 🔔: Cross up/down vs. price.

📈 Examples

5-Day on 1m → 1950-period MA

5-Day on 15m → 130-period MA

5-Day on 65m → 30-period MA

10-Day on 24h/15m (crypto) → 960-period MA

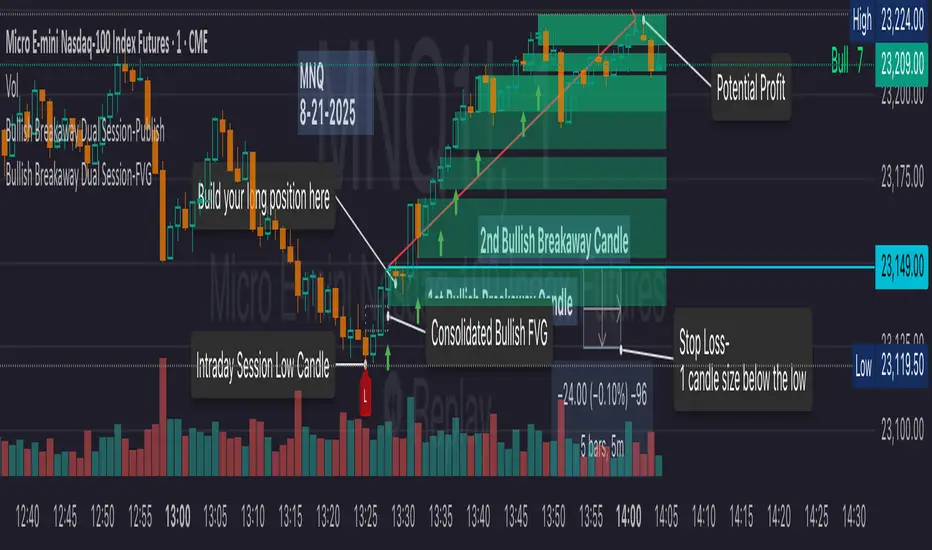

Bullish Breakaway Dual Session-Publish-Consolidated FVG

Inspired by the FVG Concept:

This indicator is built on the Fair Value Gap (FVG) concept, with a focus on Consolidated FVG. Unlike traditional FVGs, this version only works within a defined session (e.g., ETH 18:00–17:00 or RTH 09:30–16:00).

Bullish consolidated FVG & Bullish breakaway candle

Begins when a new intraday low is printed. After that, the indicator searches for the 1st bullish breakaway candle, which must have its low above the high of the intraday low candle. Any candles in between are part of the consolidated FVG zone. Once the 1st breakaway forms, the indicator will shades the candle’s range (high to low). Then it will use this candle as an anchor to search for the 2nd, 3rd, etc. breakaways until the session ends.

Session Reset: Occurs at session close.

Repaint Behavior:

If a new intraday (or intra-session) low forms, earlier breakaway patterns are wiped, and the system restarts from the new low.

Counter:

A session-based counter at the top of the chart displays how many bullish consolidated FVGs have formed.

Settings

• Session Setup:

Choose ETH, RTH, or custom session. The indicator is designed for CME futures in New York timezone, but can be adjusted for other markets.

If nothing appears on your chart, check if you loaded it during an inactive session (e.g., weekend/Friday night).

• Max Zones to Show:

Default = 3 (recommended). You can increase, but 3 zones are usually most useful.

• Timeframe:

Best on 1m, 5m, or 15m. (If session range is big, try higher time frame)

Usage

1. Avoid Trading in Wrong Direction

• No bullish breakaway = No long trade.

• Prevents the temptation to countertrade in strong downtrends.

2. Catch the Trend Reversal

• When a bullish breakaway appears after an intraday low, it signals a potential reversal.

• You will need adjust position sizing, watch out liquidity hunt, and place stop loss.

• Best entries of your preferred choices: (this is your own trading edge)

Retest

Breakout

Engulf

MA cross over

Whatever your favorite approach

• Reversal signal is the strongest when price stays within/above the breakaway candle’s

range. Weak if it breaks below.

3. Higher Timeframe Confirmation

• 1m can give false reversals if new lows keep forming.

• 5m often provides cleaner signals and avoids premature reversals.

Failed Trade Example:

This indicator will repaint if a new intraday session low is updated. So it is possible to have a failed trade. Here is an example from the same session in 1m chart. However, if you enter the trade later at another bullish breakaway candle signal. The loss can be mitigated by the profit.

Therefore you should use smaller position size for your 1st trade. You should also considering using 5m chart to avoid 1m bull trap. In this example, if you use 5m chart, you can totally avoid this failed trade.

If you enter the trade, you will see the intraday low is stop loss hunted. You can also see the 1st bullish breakaway candle is super weak. There are a lot of candles below the breakaway candle low, so it is very possible to fail.

In the next chart, you can see the failed traded get stop loss hunted. However you can enter another trade with huge profit to win back the loss from the 1st trade if you follow the rule.

Summary

This indicator offers 3 main advantages:

1. Prevents wrong-direction trades.

2. Confirms trend entry after reversal signals.

3. Filters false positives using higher timeframes.

How to sharp your edge:

1. ⏳Extreme patience⏳: Do not guess the bottom during a downtrend before a confirmed bullish breakaway candle. If you get caught, have the courage to cut loss. This is literally the most important usage of this indicator. Again, this is the most important rule of this indicator and actually the hardest rule to follow.

2. 🛎Better Entry🛎: After a confirmed bullish breakaway, you will always have a good opportunity to enter the trade using established trading technique. Your edge will come from the position size, draw down, stop loss placement, risk/reward ratio.

3. ✂Cut loss fast✂: If you enter a trade according to the rule, but you are still not making profit for a period of time, and the price is below the low of the breakaway candle. It is very likely you may hit stop loss soon (intraday session low). It won't be a bad idea to cut loss before stop loss hit.

4. 🔂Reentry with confidence after stop loss🔂: a stop loss will not invalidate the indicator. If you see a second chance to reenter, you should still follow the trade guide and rule.

5. 🕔Time frame matter🕔: try 1m, 3m, 5m, 10m, 15m time frame. Over time, you should know what time frame work best for you and the market. Higher time frame will reduce the noise of false positive trade, but it comes with a higher stop loss placement and less max profit, however it may come with a lower draw down. Time frame will matter depending on the range of the session. If the session range is small (<0.5%), lower time frame is good. If session range is big (>1%), 5m time frame is better. Remember to wait for candle to close, if you use higher time frame.

Last Mention:

The indicator is only used for bullish side trading.

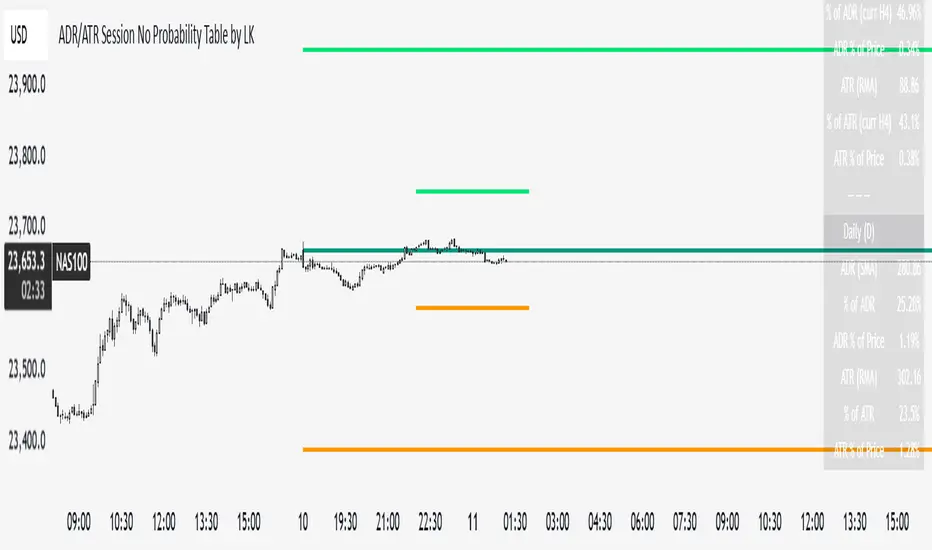

ADR/ATR Session No Probability Table by LKHere you go—clear, English docs you can drop into your script’s description or share with teammates.

ADR/ATR Session by LK — Overview

This indicator summarizes Average Daily Range (ADR) and Average True Range (ATR) for two horizons:

• Session H4 (e.g., 06:00–13:00 on a 4‑hour chart)

• Daily (D)

It shows:

• Current ADR/ATR values (using your chosen smoothing method)

• How much of ADR/ATR today/this bar has already been consumed (% of ADR/ATR)

• ADR/ATR as a percent of price

• Optional probability blocks: likelihood that %ADR will exceed user‑defined thresholds over a lookback window

• Optional on‑chart lines for the current H4 and Daily candles: Open, ADR High, ADR Low

⸻

What the metrics mean

• ADR (H4 / D): Moving average of the bar range (high - low).

• ATR (H4 / D): Moving average of True Range (max(hi-lo, |hi-close |, |lo-close |)).

• % of ADR (curr H4): (H4 range of the current H4 bar) / ADR(H4) × 100. Updates live even if the current time is outside the session.

• % of ADR (Daily): (today’s intra‑day range) / ADR(D) × 100.

• % of ATR (curr H4 / Daily): TR / ATR × 100 for that horizon.

• ADR % of Price / ATR % of Price: ADR or ATR divided by current price × 100 (a quick “volatility vs. price” gauge).

Session logic (H4): ADR/ATR(H4) only update on bars that fall inside the configured session window; outside the window the values hold steady (no recalculation “bleed”).

Daily range tracking: The indicator tracks today’s high/low in real‑time and resets at the day change.

⸻

Inputs (quick reference)

Core

• Length (ADR/ATR): smoothing length for ADR/ATR (default 21).

• Wait for Higher TF Bar Close: if true, updates ADR/ATR only after the higher‑TF bar closes when using request.security.

Timeframes

• Session Timeframe (H4): default 240.

• Daily Timeframe: default D.

Session time

• Session Timezone: “Chart” (default) or a fixed timezone.

• Session Start Hour, End Hour (minutes are fixed to 0 in this version).

Smoothing methods

• H4 ADR Method / H4 ATR Method: SMA/EMA/RMA/WMA.

• Daily ADR Method / Daily ATR Method: SMA/EMA/RMA/WMA.

Table appearance

• Table BG, Table Text, Table Font Size.

Lines (optional)

• Show current H4 segments, Show current Daily segments

• Line colors for Open / ADR High / ADR Low

• Line width

Probability

• H4 Probability Lookback (bars): number of H4 bars to examine (e.g., 300).

• Daily Probability Lookback (days): number of D bars (e.g., 180).

• ADR thresholds (%): CSV list of thresholds (e.g., 25,50,55,60,65,70,75,80,85,90,95,100,125,150).

The table will show the % of lookback bars where %ADR ≥ threshold.

Tip: If you want probabilities only for session H4 bars (not every H4 bar), ask and I can add a toggle to filter by inSess.

⸻

How to read the table

H4 block

• ADR (method) / ATR (method): the session‑aware averages.

• % of ADR (curr H4): live progress of this H4 bar toward the session ADR.

• ADR % of Price: ADR(H4) relative to price.

• % of ATR (curr H4) and ATR % of Price: same idea for ATR.

H4 Probability (lookback N bars)

• Rows like “≥ 80% ADR” show the fraction (in %) of the last N H4 bars that reached at least 80% of ADR(H4).

Daily block

• Mirrors the H4 block, but for Daily.

Daily Probability (lookback M days)

• Rows like “≥ 100% ADR” show the fraction of the last M daily bars whose daily range reached at least 100% of ADR(D).

⸻

Practical usage

• Use % of ADR (curr H4 / Daily) to judge exhaustion or room left in the day/session.

E.g., if Daily %ADR is already 95%, be cautious with momentum continuation trades.

• The probability tables give a quick historical context:

If “≥ 125% ADR” is ~18%, the market rarely stretches that far; your trade sizing/targets can reflect that.

• ADR/ATR % of Price helps normalize volatility between instruments.

⸻

Troubleshooting

• If probability rows are blank: ensure lookback windows are large enough (and that the chart has enough history).

• If ADR/ATR show … (NA): usually you don’t have enough bars for the chosen length/TF yet.

• If line segments are missing: verify you’re on a chart with visible current H4/D bars and the toggles are enabled.

⸻

Notes & customization ideas

• Add a toggle to count only session bars in H4 probability.

• Add separate thresholds for H4 vs Daily.

• Let users pick minutes for session start/end if needed.

• Add alerts when %ADR crosses specified thresholds.

If you want me to bundle any of the “ideas” above into the code, say the word and I’ll ship a clean patch.

ADR/ATR Session by LK## **Features**

1. **Custom ADR & ATR Calculation**

* Calculates **Average Daily Range (ADR)** and **Average True Range (ATR)** separately for:

* **Session timeframe** (default H4 / 06:00–13:00)

* **Daily timeframe**

* Independent smoothing method selection (**SMA, EMA, RMA, WMA**) for H4 ADR, H4 ATR, Daily ADR, and Daily ATR.

2. **Percentage Metrics**

* % of ADR / ATR covered by the **current H4 bar**.

* ADR / ATR expressed as a percentage of the **current price**.

* % of ADR already reached for the **current day**.

* % of Daily ATR vs current day’s True Range.

3. **Dynamic Chart Lines**

* Draws **3 lines for H4**: Session Open, ADR High, ADR Low.

* Draws **3 lines for Daily**: Daily Open, ADR High, ADR Low.

* Lines **extend to the right** so they stay visible across the chart.

* Colors and widths are fully customizable.

4. **Real-Time Data Table**

* Compact table displaying all ADR/ATR values and percentages.

* Adjustable table font size (**tiny, small, normal, large, huge**).

* Transparent background option for minimal chart obstruction.

5. **Flexible Session Settings**

* Select session start and end time in hours/minutes.

* Choose session timezone (chart timezone or major financial centers).

* Toggle H4 lines, Daily lines separately.

6. **Lookahead Control**

* Option to wait for higher-timeframe candle close before updating values (more accurate, less repainting).

---

## **How to Use**

### **1. Adding the Indicator**

* Copy and paste the Pine Script into TradingView’s Pine Editor.

* Click **“Add to chart”**.

* Make sure your chart supports the higher timeframes you choose (e.g., H4 and Daily).

### **2. Setting Your Session**

* **Session Start Hour** & **End Hour** → Defines the intraday session to measure ADR/ATR (default: 06:00–13:00).

* **Session Timezone** → Pick “Chart” or a major financial center (e.g., New York, London, Tokyo).

### **3. Choosing Smoothing Methods**

* For each ADR/ATR (H4 and Daily), choose:

* SMA (Simple)

* EMA (Exponential)

* RMA (Wilder’s smoothing)

* WMA (Weighted)

### **4. Adjusting Chart Display**

* **Show H4 Lines** → Displays session open and ADR High/Low for the current H4 session.

* **Show Daily Lines** → Displays daily open and ADR High/Low.

* Customize line colors and widths.

### **5. Reading the Table**

* **H4 Section**

* ADR / ATR values for the selected session.

* % of ADR/ATR covered by the **current H4 bar**.

* ADR/ATR as % of the current price.

* **Daily Section**

* ADR / ATR for the daily timeframe.

* % of ADR already covered by today’s range.

* ADR/ATR as % of price.

### **6. Pro Tips**

* Use **H4 ADR %** to gauge intraday exhaustion — if current range is near 100%, market may slow or reverse.

* Use **Daily ADR %** for swing trade context — if a day has moved beyond its ADR, expect lower continuation probability.

* Combine with support/resistance to identify high-probability reversal zones.

[Smith] VWAP Deviation + VWAP Deviation +

Short Description:

Advanced VWAP indicator with deviation bands, smart signal filtering, and session-based performance tracking. Features log-space scaling, RSI confirmation, volume filters, and market regime detection.

Full Description:

The VWAP Deviation + is a comprehensive trading indicator that combines Volume Weighted Average Price (VWAP) analysis with advanced signal filtering to identify high-probability trade opportunities. This indicator goes beyond basic VWAP by incorporating multiple confirmation layers and intelligent market analysis.

🎯 Key Features

Core VWAP Analysis:

- Custom volume-weighted mean calculation with deviation bands (2σ and 3σ)

- Optional log-space scaling for proportional price movements

- Real-time VWAP line with customizable visibility

Smart Signal Detection:

- RSI confirmation for all trade signals

- Volume filter requiring above-average trading activity

- Market regime detection (trending vs ranging markets)

- Optional RSI divergence analysis

Advanced Filtering:

- Multi-condition signal validation

- Session-based performance tracking (Asian, London, NY)

- Real-time win rate calculation

- Strong vs regular signal classification

Visual Features:

- Clean, professional interface with customizable colors

- Optional signal shapes and annotations

- Performance statistics table

- Filled deviation bands for easy visualization

📊 How It Works

The indicator identifies trade opportunities when:

1. Price touches VWAP deviation bands (2σ or 3σ)

2. RSI confirms oversold/overbought conditions

3. Volume exceeds the specified threshold

4. Market regime conditions are favorable

Signal Types:

- LONG : Price at lower bands + RSI oversold + volume confirmation

- SHORT : Price at upper bands + RSI overbought + volume confirmation

- STRONG : Same conditions but at 3σ bands for higher conviction trades

⚙️ Customization Options

Core Settings:

- VWAP length and source selection

- Adjustable deviation multipliers

- Log-space scaling toggle

Signal Filters:

- RSI length and threshold levels

- Volume filter with customizable multiplier

- Market type filtering options

Advanced Features:

- Session statistics tracking

- RSI divergence detection

- Market regime analysis

Visual Controls:

- Show/hide individual components

- Custom color schemes

- Signal display toggles

🔔 Alert System

Built-in alerts for:

- Long and short trade opportunities

- Strong signal confirmations

- RSI divergence signals

💡 Best Practices

- Use higher timeframes (15m+) for more reliable signals

- Combine with additional confirmation indicators

- Pay attention to session statistics for timing optimization

- Monitor market regime indicators for context

This indicator is suitable for day traders, swing traders, and anyone looking to improve their VWAP-based trading strategies with advanced filtering and market analysis.

Market Session Boxes with Volume Delta [algo_aakash]This script highlights four key forex trading sessions — Tokyo, London, New York, and Sydney — by drawing color-coded boxes directly on the chart. For each session, it shows:

High and low of the session

Total volume traded

Volume delta (bullish vs bearish pressure)

Optional extension of session highs/lows into future candles

Cleanly labeled time range and stats

Users can:

Select which sessions to display

Customize session times (in UTC+0)

Choose colors per session

Toggle session labels and extension lines

Use Case: Designed to help intraday and short-term traders visualize market rhythm, liquidity zones, and session-based volatility. The volume delta metric adds an extra layer of sentiment analysis.

This tool works best on intraday timeframes like 15m, 30m, or 1H.

Disclaimer:

This indicator is for educational and visual analysis purposes. It does not constitute trading advice or guarantee results. Always conduct your own analysis before making trading decisions.

ALN Sessions - for NQ2/24/25 - v1

This script does not calculate any stats.

It uses the sessions and stats from NQStats/ALNSessions

Option to draw boxes around the session times.

Options to adjust the table text/background colors/position.

The logic will determine how the Asia and London sessions interact.

Once the New York session starts (8am), it will then display the appropriate stats.

Script quirk...fyi. The script removes the stats table at 6PM.

That's just how it works. I used grok to assist with the code, and it got funky. It works, so I left it that way.

The appropriate stats table will then be displayed when the next New York session begins.

---

There is another table I used just for troubleshooting to show the values of the Asia/London session highs/lows. This can just be ignored.

3/3/25 - republished.

Opening Range with Breakouts & Targets [LuxAlgo]Opening Range with Breakouts & Targets is based on the long-standing Opening Range Breakout strategy popularized by traders such as Toby Crabel and Mark Fisher.

This indicator measures and displays the price range created from the first period within a new trading session, along with price breakouts from that range and targets associated with the range width.

🔶 USAGE

The Opening Range (OR) can be a powerful tool for making a clear distinction between ranging and trending trading days. Using a rigid structure for drawing a range, provides a consistent basis to make judgments and comparisons that will better assist the user in determining a hypothesis for the day's price action.

NOTE: During a suspected "Range Day", the Opening Range can be used for reversion strategies, typically targeting the opposite extreme of the range or the mean of the range. However, more commonly the Opening Range is used for breakouts on suspected "Trend Days", targeting further upward or downward market movement.

The common Opening Range Breakout Strategy (ORB) outlines a structure to enter and exit positions based on rigid points determined by the Opening Range. This methodology can be adjusted based on markets or trading styles.

Determine Opening Range High & Low: These are the high and low price within a chosen period of time after the market opens. This can be customized to the user's trading style and preference. Common Ranges are from 5-60 mins.

Watch for a Breakout with Volume: A Breakout occurs when price crosses the OR High (ORH) or OR Low (ORL), an increase in volume is typically desired when witnessing these breakouts to confirm a stronger movement.

Manage Risk: Based on user preference and the appropriately determined amount of risk, multiple ways can be determined to manage risk by using Opening Range.

For Example: A stop-loss could be set at OR Mean (ORM) or the opposite side of the range, while a profit target could optionally be set at the first price target generated by the script.

Alternatively, a user might want to use a Moving Average (MA) as an adaptive stop-loss and use price targets to scale out. These are just 2 examples of the possible options, both capable with this tool.

🔹 Signals

Signals will fire based on the break of the opening range, this is indicated by arrows above and below the range boundaries.

Optionally, a bias can be added to these signals to aid in mitigating false signals by using a directional filter based on the current day's OR relative to the previous day's OR.

Regardless of the signal bias being enabled, the Opening Range Zone will always be colored directionally according to this.

If the current day's OR is above the previous day's OR, the Zone will be Green.

If the current day's OR is below the previous day's OR, the Zone will be Red.

By enabling the signal bias, signals in the opposite direction of the daily bias will fire on the cross of the first target in that direction.

🔹 Targets

In this indicator, targets are not limited and will generate infinitely based on a % width of the Opening Range.

Additionally, there are 2 display methods for these targets.

Extended: Extends the targets to the current bar and displays all targets that have been crossed so far within the session.

Adaptive: Extends only the 2 closest targets surrounding price, allowing for a display consisting of fewer lines at one time.

🔶 DETAILS

🔹 Historical Display

This indicator can be utilized in multiple ways, for use in real-time, and for historical analysis to form methods. Because of this, the indicator has an option to display only the current day's data or the entire historical data. This can also help clean up the chart when it is in use.

🔹 Time Period

The specific time period to create the opening range is entirely up to each user's preference, by default it is set to 30 mins; however, this time period can be edited with full control if desired.

Simply toggle on the "Custom Range" and input a range of time to create the range.

🔹 Session Moving Average

The Session Moving Average is a common Moving Average, which resets at the beginning of a new session. This allows for an unbiased MA that was created entirely from the current session's price action.

Note: The start of the session is determined by the start of the Opening Range if using a custom range of time.

🔶 SETTINGS

Show Historical Data: Choose to display only the current session's data or the full history of data.

Opening Range Time Period: Select the time period to form the opening range from. This operates on Session Start, so it will change with the chart.

Custom Range: Opt for a custom Range by enabling this and inputting your range times as well as your needed timezone.

Breakout Signal Bias: Select if the Breakout Signals will use a Daily Directional Bias for firing.

Target % of Range: Sets the % of the Range width that will be used as an increment for the Targets to display in.

Target Cross Source: Choose to use the Close price or High/Low price as the crossing level for Target displays. When this source crosses a target it will generate more targets.

Target Display: Choose which style of display to use for targets.

Session Moving Average: Optionally enable a Moving average of your choice that resets at the beginning of each session (start of opening range).

Trade Session Tracker [theUltimator5]Trade Session Tracker is a unique indicator designed to isolate each discrete trading session on the US stock exchanges and display a cumulative running price for each session so you can visualize how each session performs over long periods of time.

This indicator allows you to unlock a potentially unique and powerful trading strategy that exploits returns during lower liquidity periods through trend analysis. Certain stocks tend to move in the same direction during specific windows in the day, and now you can find them yourself.

This indicator only works properly on the daily timeframe. Other timeframes are not supported.

The sessions that this indicator supports are:

Intraday (Market open to market close)

After Hours (Market close until 20:00 eastern)

Overnight (20:00 eastern through 04:00 eastern the next day)

Pre-market (04:00 eastern through market open)

Close-to-open (market close to the following market open)

There are two plot modes:

Cumulative — chained returns since chart start (synthetic continuous price line)

Daily Change — single-session return (refreshes each new trading day)

!IMPORTANT!

This indicator only supports symbols that trade on the overnight markets through the BOATS ATS. This includes hundreds of ticker symbols, but the majority of smaller cap stocks or non-equity symbols are not supported.

Some symbols offer dividends, and the "ADJ" button at the bottom right corner of the chart must be disabled for the data to display properly, or else you will get extremely skewed results. Notorious symbols for this are SPY and AAPL.

How it works:

Standard chart data only calculates sessions through open, close, and previous close and cannot isolate out pre-market and after hours price action.

With the addition of overnight data, we now have a separate set of open and close values which can be pulled.

To calculate after hours price action, we use the opening price of the overnight venue divided by the close price earlier that day.

To calculate the pre-market price action, we divide the open price by the previous overnight close price.

Overnight price is simply calculated by overnight close divided by overnight open.

There is a table that can be toggled off and repositioned that shows the current settings.

Here is an example of close-to-open and intraday

Here is an example of overnight returns