Put/Call RatioPut/Call Ratio Indicator

This indicator visualizes the Put/Call Ratio for various market symbols, helping traders assess market sentiment and potential reversals. It offers a dropdown menu to select from a range of Put/Call Ratios, including broad equities (CBOE), major indices (SPX, QQQ, IWM, VIX), and individual stocks (TSLA, GOOG, META, AMZN, MSFT, INTC).

The indicator plots the Put/Call Ratio with adjustable moving averages and standard deviation bands to highlight overbought or oversold conditions. A short-term moving average (default: 10 periods) is displayed with trend-based coloring, while longer-term moving averages (defaults: 30 and 200 periods) are calculated but hidden by default. Bands at 1, 1.5, and 2 standard deviations provide context for extreme readings.

Key Overbought/Oversold Signals:

Short-Term Extremes: The 10-day moving average moves beyond 1 standard deviation from the 200-day moving average, signaling potential overbought (above) or oversold (below) conditions. This will be highlighted by red or green background color.

Ratio Extremes: The Put/Call Ratio line itself crosses outside 2 standard deviations from the 200-day moving average, indicating stronger overbought or oversold zones.

Conditional coloring of the ratio line reflects its position relative to the bands, and background shading highlights when the short-term moving average crosses key levels.

Key Features:

Selectable Put/Call Ratio symbols.

Trend-colored moving averages.

Standard deviation bands for volatility analysis.

Dynamic line and background coloring for quick insights.

Usage:

Use this indicator to gauge market sentiment—high ratios may suggest bearish sentiment or oversold conditions, while low ratios may indicate bullish sentiment or overbought conditions. Combine with price action or other tools for confirmation.

Cerca negli script per "spx"

[GOG] Risk-Appetite IndicatorOverall tradfi risk appetite indicator. Plotting ARKK/SPX and ARKW/SPX. Look for divergences to your risk assets to look for entries and exits. Also generally useful to compare to past peaks to spot euphoria.

ChillLax Relative Strength Line with NewHigh NewLow Blue DotThis is similar to the IBD MarketSurge (MarketSmith) Blue Dot:

This plots the Relative Strength line vs. an index (default index is SPX), with a Dot when the RS line is hitting a New High.

If the RS hits a New High over the past X bars (default is 50), it shows a Light Blue (user definable) Dot on the RS line, if RS hits New High before the instrument hits New High, it shows a bigger/darker Blue Dot. Reverse for New Lows (orange for RS NL, Red for RS NL before Price NL)

This Dot is similar to the IBD Marketsurge RS New High Blue Dot, this indicator shows all the previous dots (MarketSurge shows only the last one). This on, unlike IBD, also shows RS New Lows. This one distinguishes RS NH before Price NH, and RS NL before Price NL. Lastly, IBD's lookback period is 52 week, here it is default to 50 days, but it is changeable.

Relative Performance SuiteOverview

The Relative Performance Suite (RPS) is a versatile and comprehensive indicator designed to evaluate an asset's performance relative to a benchmark. By offering multiple methods to measure performance, including Relative Performance, Alpha, and Price Ratio, this tool helps traders and investors assess asset strength, resilience, and overall behavior in different market conditions.

Key Features:

✅ Multiple Performance Measures:

Choose from various relative performance calculations, including:

Relative Performance:

Measures how much an asset has outperformed or underperformed its benchmark over a given period.

Relative Performance (Proportional):

A proportional version of relative performance,

factoring in scaling effects.

Relative Performance (MA Based):

Uses moving averages to smooth performance fluctuations.

Alpha:

A measure of an asset’s performance relative to what would be expected based on its beta and the benchmark’s return. It represents the excess return above the risk-free rate after adjusting for market risk.

Price Ratio:

Compares asset prices directly to determine relative value over time.

✅ Customizable Moving Averages:

Apply different moving average types (SMA, EMA, SMMA, WMA, VWMA) to smooth price inputs and refine calculations.

✅ Beta Calculation:

Includes a Beta measure used in Alpha calculation, which users can toggle the visibility of helping users understand an asset's sensitivity to market movements.

✅ Risk-Free Rate Adjustment:

Incorporate risk-free rates (e.g., US Treasury yields, Fed Funds Rate) for a more accurate calculation of Alpha.

✅ Logarithmic Returns Option:

Users can switch between standard returns and log returns for more refined performance analysis.

✅ Dynamic Color Coding:

Identify outperformance or underperformance with intuitive color coding.

Option to color bars based on relative strength, making chart analysis easier.

✅ Customizable Tables for Data Display:

Overview table summarizing key metrics.

Explanation table offering insights into how values are derived.

How to Use:

Select a Benchmark: Choose a comparison symbol (e.g., TOTAL or SPX ).

Pick a Performance Metric: Use different modes to analyze relative performance.

Customize Calculation Methods: Adjust moving averages, timeframes, and log returns based on preference.

Interpret the Colors & Tables: Utilize the dynamic coloring and tables to quickly assess market conditions.

Ideal For:

Traders looking to compare individual asset performance against an index or benchmark.

Investors analyzing Alpha & Beta to understand risk-adjusted returns.

Market analysts who want a visually intuitive and data-rich performance tracking tool.

This indicator provides a powerful and flexible way to track relative asset strength, helping users make more informed trading decisions.

SPY/TLT Strategy█ STRATEGY OVERVIEW

The "SPY/TLT Strategy" is a trend-following crossover strategy designed to trade the relationship between TLT and its Simple Moving Average (SMA). The default configuration uses TLT (iShares 20+ Year Treasury Bond ETF) with a 20-period SMA, entering long positions on bullish crossovers and exiting on bearish crossunders. **This strategy is NOT optimized and performs best in trending markets.**

█ KEY FEATURES

SMA Crossover System: Uses price/SMA relationship for signal generation (Default: 20-period)

Dynamic Time Window: Configurable backtesting period (Default: 2014-2099)

Equity-Based Position Sizing: Default 100% equity allocation per trade

Real-Time Visual Feedback: Price/SMA plot with trend-state background coloring

Event-Driven Execution: Processes orders at bar close for accurate backtesting

█ SIGNAL GENERATION

1. LONG ENTRY CONDITION

TLT closing price crosses ABOVE SMA

Occurs within specified time window

Generates market order at next bar open

2. EXIT CONDITION

TLT closing price crosses BELOW SMA

Closes all open positions immediately

█ ADDITIONAL SETTINGS

SMA Period: Simple Moving Average length (Default: 20)

Start Time and End Time: The time window for trade execution (Default: 1 Jan 2014 - 1 Jan 2099)

Security Symbol: Ticker for analysis (Default: TLT)

█ PERFORMANCE OVERVIEW

Ideal Market Conditions: Strong trending environments

Potential Drawbacks: Whipsaws in range-bound markets

Backtesting results should be analyzed to optimize the MA Period and EMA Filter settings for specific instruments

BTC-SPX Momentum Gauge + EMA SignalHere's an explanation of the market dynamics and signal benefits of this script:

Momentum and Sentiment Indicator:

The script uses the momentum of the S&P 500 to change the chart's background color, providing a quick visual cue of market sentiment. Green indicates potential bullish momentum in the broader market, while red suggests bearish momentum. This can help traders gauge overall market direction at a glance.

Bitcoin Trend Analysis:

By plotting the scaled TEMA of Bitcoin (BTC), traders can see how Bitcoin's trend correlates or diverges from the current asset being analyzed. Since Bitcoin is often viewed as a hedge against traditional financial systems or inflation, its trend can signal broader economic shifts or investor sentiment towards alternative investments.

Dual Trend Confirmation:

The script offers two trend lines: one for Bitcoin and one for the current ticker. When these lines move in tandem, it might indicate a strong market trend across both traditional and crypto markets. Divergence between these lines can highlight potential market anomalies or opportunities for arbitrage or hedging.

Smoothness vs. Reactivity:

The use of TEMA for Bitcoin provides a smoother signal than a simple moving average, reducing lag while still reacting to price changes. This can be particularly useful for identifying longer-term trends in Bitcoin's volatile market. The 20-period EMA for the current ticker, on the other hand, gives a quicker response to price changes in the asset you're directly trading.

Cross-Asset Correlation:

By overlaying Bitcoin's trend on another asset's chart, traders can analyze how these markets might influence each other. For instance, if Bitcoin is in an uptrend while a traditional asset is declining, it might suggest capital rotation into cryptocurrencies.

Trading Signals:

Crossovers or divergences between the TEMA of Bitcoin and the EMA of the current ticker could be used as signals for entry or exit points. For example, if the BTC TEMA crosses above the current ticker's EMA, it might suggest a shift towards crypto assets.

Risk Management:

The visual cues from the background color and moving averages can aid in risk management. For example, trading in the direction of the momentum indicated by the background color might be seen as going with the market flow, potentially reducing risk.

Macro-Economic Insights:

The relationship between Bitcoin and traditional markets can offer insights into macroeconomic conditions, particularly related to inflation, monetary policy, and investor sentiment towards fiat currencies.

Headwind and tailwind:

Currently BTC correlated trade instruments experience headwind or tailwind from the broader market. This indicator lets the user see it to help their trade decision process.

Additional Statement:

As the market realizes the dangers of the fiat that its construct is built upon and evolves and migrates into stable money, incorruptible by inflation, this indicator will reveal the external influence of that corruptible and the internal influence of the incorruptible; having diminishing returns as the rise of stable money overtakes the treasuries of the fiat construct.

SuperTrend Heikin AshiSupertrend Heikin Ashi is an indicator based on the standard calculation of the Supertrend with the difference of using the Open and Close value of the Heikin Ashi candles instead of the normal Candle Sticks.

In this way the main characteristic of the HA candles is exploited, thus filtering movements that could generate false signals.

I recommend using SPY, SPX, QQQ to be aware of the market situation, not operating (or paying great attention) long on stocks when the indicator is red and the price is below the drawn line.

Price Action Health CheckThis is a price action indicator that measures market health by comparing EMAs, adapting automatically to different timeframes (Weekly/Daily more reliable) and providing context-aware health status.

Key features:

Automatically adjusts EMA periods based on timeframe

Measures price action health through EMA separation and historical context

Provides visual health status with clear improvement/deterioration signals

Projects a 13-period trend line for directional context

Trading applications:

Identify shifts in market health before major trend changes

Validate trend strength by comparing current readings to historical averages

Time entries/exits based on health status transitions

Filter trades using timeframe-specific health readings

I like to use it to keep SPX in check before deciding the market is going down.

Note: For optimal analysis, use primarily on Weekly and Daily timeframes where price action patterns are more significant.

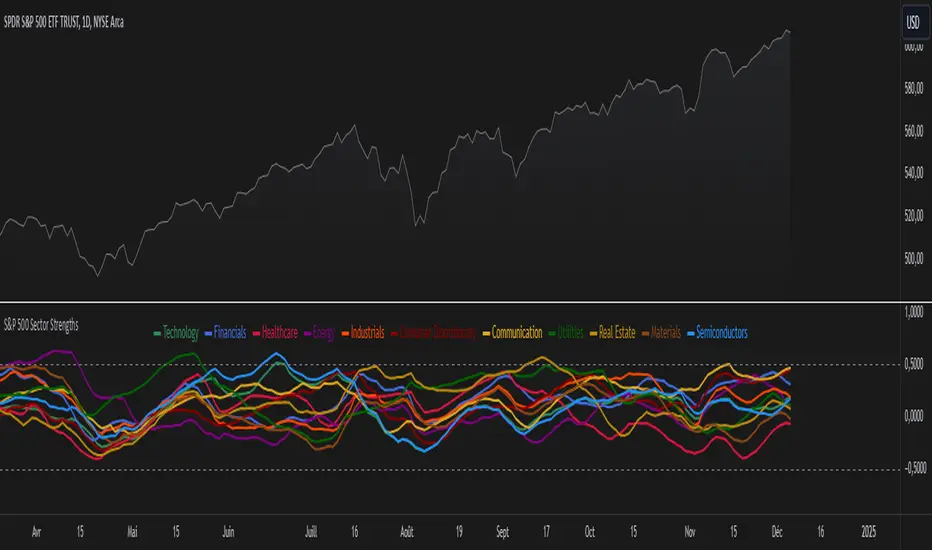

S&P 500 Sector StrengthsThe "S&P 500 Sector Strengths" indicator is a sophisticated tool designed to provide traders and investors with a comprehensive view of the relative performance of various sectors within the S&P 500 index. This indicator utilizes the True Strength Index (TSI) to measure and compare the strength of different sectors, offering valuable insights into market trends and sector rotations.

At its core, the indicator calculates the TSI for each sector using price data obtained through the request.security() function. The TSI, a momentum oscillator, is computed using a user-defined smoothing period, allowing for customization based on individual preferences and trading styles. The resulting TSI values for each sector are then plotted on the chart, creating a visual representation of sector strengths.

To use this indicator effectively, traders should focus on comparing the movements of different sector lines. Sectors with lines moving higher are showing increasing strength, while those with descending lines are exhibiting weakness. This comparative analysis can help identify potential investment opportunities and sector rotations. Additionally, when multiple sector lines move in tandem, it may signal a broader market trend.

The indicator includes dashed lines at 0.5 and -0.5, serving as reference points for overbought and oversold conditions. Sectors with TSI values above 0.5 might be considered overbought, suggesting caution, while those below -0.5 could be viewed as oversold, potentially indicating buying opportunities.

One of the key advantages of this indicator is its flexibility. Users can toggle the visibility of individual sectors and customize their colors, allowing for a tailored analysis experience. This feature is particularly useful when focusing on specific sectors or reducing chart clutter for clearer visualization.

The indicator's ability to provide a comprehensive overview of all major S&P 500 sectors in a single chart is a significant benefit. This consolidated view enables quick comparisons and helps in identifying relative strengths and weaknesses across sectors. Such insights can be invaluable for portfolio allocation decisions and in spotting emerging market trends.

Moreover, the dynamic legend feature enhances the indicator's usability. It automatically updates to display only the visible sectors, improving chart readability and interpretation.

By leveraging this indicator, market participants can gain a deeper understanding of sector dynamics within the S&P 500. This enhanced perspective can lead to more informed decision-making in sector allocation strategies and individual stock selection. The indicator's ability to potentially detect early trends by comparing sector strengths adds another layer of value, allowing users to position themselves ahead of broader market movements.

In conclusion, the "S&P 500 Sector Strengths" indicator is a powerful tool that combines technical analysis with sector comparison. Its user-friendly interface, customizable features, and comprehensive sector coverage make it an valuable asset for traders and investors seeking to navigate the complexities of the S&P 500 market with greater confidence and insight.

IV Rank/Percentile with Williams VIX FixDisplay IV Rank / IV Percentile

This indicator is based on William's VixFix, which replicates the VIX—a measure of the implied volatility of the S&P 500 Index (SPX). The key advantage of the VixFix is that it can be applied to any security, not just the SPX.

IV Rank is calculated by identifying the highest and lowest implied volatility (IV) values over a selected number of past periods. It then determines where the current IV lies as a percentage between these two extremes. For example, if over the past five periods the highest IV was 30%, the lowest was 10%, and the current IV is 20%, the IV Rank would be 50%, since 20% is halfway between 10% and 30%.

IV Percentile, on the other hand, considers all past IV values—not just the highest and lowest—and calculates the percentage of these values that are below the current IV. For instance, if the past five IV values were 30%, 10%, 11%, 15%, and 17%, and the current IV is 20%, the IV Rank remains at 50%. However, the IV Percentile is 80% because 4 out of the 5 past values (80%) are below the current IV of 20%.

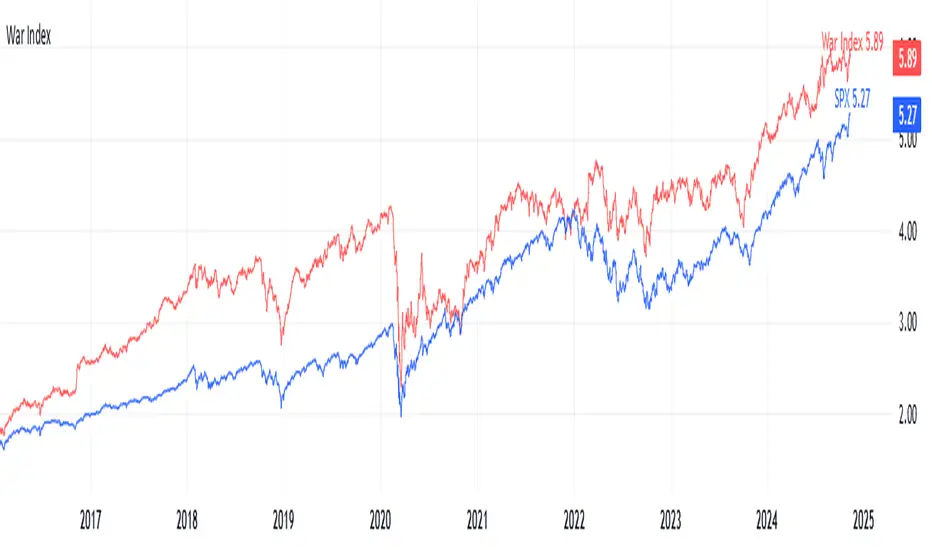

War IndexIntroduction

Welcome to the War Index! This project aims to provide traders, investors, and analysts with a specialized financial indicator that tracks the performance of key defense and aerospace companies. By aggregating the percentage changes of selected stocks, the War Index offers insights into the defense sector's dynamics and its relationship with the broader market.

What is the War Index?

The War Index is a custom financial indicator designed to approximate the collective performance of major defense and aerospace companies. It aggregates the daily percentage changes of selected stocks within the defense sector to provide a singular metric that reflects the overall health and trends of this industry. Additionally, the index is compared against the S&P 500 (SPX) to contextualize its performance relative to the broader market.

Index Components

The War Index comprises the following 16 stocks, each representing a significant player in the defense and aerospace industries:

Lockheed Martin Corporation ( NYSE:LMT )

Northrop Grumman Corporation ( NYSE:NOC )

Boeing Company ( NYSE:BA )

Raytheon Technologies Corporation ( NYSE:RTX )

General Dynamics Corporation ( NYSE:GD )

BAE Systems plc ( OTC:BAESY )

L3Harris Technologies, Inc. ( NYSE:LHX )

Textron Inc. ( NYSE:TXT )

Huntington Ingalls Industries, Inc. ( NYSE:HII )

Oshkosh Corporation ( NYSE:OSK )

Leidos Holdings, Inc. ( NYSE:LDOS )

Kratos Defense & Security Solutions, Inc. ( NASDAQ:KTOS )

Spirit AeroSystems Holdings, Inc. ( NYSE:SPR )

Parsons Corporation ( NYSE:PSN )

CACI International Inc ( NYSE:CACI )

ViaSat, Inc. ( NASDAQ:VSAT )

Purpose of the War Index

The War Index serves several key purposes:

Sector Performance Tracking : By aggregating the performance of major defense and aerospace companies, the index provides a clear picture of the sector's overall health.

Investment Analysis : Investors can use the index to identify trends, evaluate sector strength, and make informed decisions regarding their portfolios.

Comparative Benchmarking : Comparing the War Index with broader market indices like the S&P 500 helps in understanding how the defense sector performs relative to the general market.

Disclaimer: This War Index is an approximated indicator intended for informational purposes only. It should not be construed as investment advice. Always conduct your own research or consult with a financial advisor before making investment decisions.

SP500 RatiosThe "SP500 Ratios" indicator is a powerful tool developed for the TradingView platform, allowing users to access a variety of financial ratios and inflation-adjusted data related to the S&P 500 index. This indicator integrates with Nasdaq Data Link (formerly known as Quandl) to retrieve historical data, providing a comprehensive overview of key financial metrics associated with the S&P 500.

Key Features

Price to Sales Ratio: Quarterly ratio of price to sales (revenue) for the S&P 500.

Dividend Yield: Monthly dividend yield based on 12-month dividend per share.

Price Earnings Ratio (PE Ratio): Monthly price-to-earnings ratio based on trailing twelve-month reported earnings.

CAPE Ratio (Shiller PE Ratio): Monthly cyclically adjusted PE ratio, based on average inflation-adjusted earnings over the past ten years.

Earnings Yield: Monthly earnings yield, the inverse of the PE ratio.

Price to Book Ratio: Quarterly ratio of price to book value.

Inflation Adjusted S&P 500: Monthly S&P 500 level adjusted for inflation.

Revenue Per Share: Quarterly trailing twelve-month sales per share, not adjusted for inflation.

Earnings Per Share: Monthly real earnings per share, adjusted for inflation.

User Configuration

The indicator offers flexibility through user-configurable options. You can choose to display or hide each metric according to your analysis needs. Users can also adjust the line width for better visibility on the chart.

Visualization

The selected data is plotted on the chart with distinct colors for each metric, facilitating visual analysis. A dynamic legend table is also generated in the top-right corner of the chart, listing the currently displayed metrics with their associated colors.

This indicator is ideal for traders and analysts seeking detailed insights into the financial performance and valuations of the S&P 500, while benefiting from the customization flexibility offered by TradingView.

VIX Percentile Rank HistogramVIX Percentile Rank Histogram

The VIX Percentile Rank Histogram provides a visual representation of the CBOE Volatility Index (VIX) percentile rank over a customizable lookback period, helping traders gauge market sentiment and make informed trading decisions.

Overview:

This indicator calculates the percentile rank of the VIX over a specified lookback period and displays it as a histogram. The histogram helps traders understand whether the current VIX level is relatively high or low compared to its recent history. This information is particularly useful for timing entries and exits in the S&P 500 or related ETFs and Mega Caps.

How It Works:

VIX Data Integration: The script fetches daily VIX close prices, regardless of the chart you are viewing, to analyze market volatility.

Percentile Rank Calculation: The indicator calculates the rank percentile of the VIX over the chosen lookback period.

Histogram Visualization: The histogram plots the difference between the flipped VIX percentile rank and 50, showing green bars for ranks below 50 (indicating lower market volatility) and red bars for ranks above 50 (indicating higher market volatility).

Usage:

This indicator is most effective when trading the S&P 500 (SPX, SPY, ES1!) or ETFs and Mega Caps that closely follow the S&P 500. It provides insight into market sentiment, helping traders make more informed decisions.

Timing Entries and Exits: Green histogram readings suggest it's a good time to enter or hold long positions, while red readings suggest considering exits or short positions.

Market Sentiment: A high VIX percentile rank (red bars) indicates market fear and uncertainty, while a low percentile rank (green bars) suggests investor confidence and reduced volatility.

Key Features:

Customizable Lookback Period: The default lookback period is set to 20 days, but can be adjusted based on the trader's average trade duration. For example, if your trades typically last 20 days, a 20-day lookback period helps contextualize the VIX level relative to its recent history.

Histogram Visualization: The histogram provides a clear visual representation of market volatility.

Green Bars: Indicate a lower-than-median VIX percentile rank, suggesting reduced market volatility.

Red Bars: Indicate a higher-than-median VIX percentile rank, suggesting increased market volatility.

Threshold Line: A dashed gray line at the 0 level serves as a visual reference for the median VIX rank.

Important Note:

This indicator always shows readings from the VIX, regardless of the chart you are viewing. For example, if you are looking at Natural Gas futures, this indicator will provide no relevant data. It works best when trading the S&P 500 or related ETFs and Mega Caps.

Mateo's Time of Day Analysis LEThis strategy takes a trade every day at a specified time and then closes it at a specified time.

The purpose of this strategy is to help determine if there are better times to day to buy or sell.

I was originally inspired to write this when a YouTuber stated that SPX had been up during the last 30 minutes of the day over 80% of the time the past year. No matter who says it, test it, and in my opinion, TradingView is one of the easiest placed to do that! Unfortunately, that particular claim did not turn out to be accurate, but this tool remains for those who want to optimize timing their entries and exits at specific times of day.

Breadth Indicators NYSE Percent Above Moving AverageBreadth Indicators NYSE - transmits the processed data from the Barchart provider

NYSE - Breadth Indicators

S&P 500 - Breadth Indicators

DOW - Breadth Indicators

RUSSEL 1000 - Breadth Indicators

RUSSEL 2000 - Breadth Indicators

RUSSEL 3000 - Breadth Indicators

Moving Average - 5, 20, 50, 100, 150, 200

The "Percentage above 50-day SMA" indicator measures the percentage of stocks in the index trading above their 50-day moving average. It is a useful tool for assessing the general state of the market and identifying overbought and oversold conditions.

One way to use the "Percentage above 50-day SMA" indicator in a trading strategy is to combine it with a long-term moving average to determine whether the trend is bullish or bearish. Another way to use it is to combine it with a short-term moving average to identify pullbacks and rebounds within the overall trend.

The purpose of using the "Percentage above 50-day SMA" indicator is to participate in a larger trend with a better risk-reward ratio. By using this indicator to identify pullbacks and bounces, you can reduce the risk of entering trades at the wrong time.

Bull Signal Recap:

150-day EMA of $SPXA50R crosses above 52.5 and remains above 47.50 to set the bullish tone.

5-day EMA of $SPXA50R moves below 40 to signal a pullback

5-day EMA of $SPXA50R moves above 50 to signal an upturn

Bear Signal Recap:

150-day EMA of $SPXA50R crosses below 47.50 and remains below 52.50 to set the bearish tone.

5-day EMA of $SPXA50R moves above 60 to signal a bounce

5-day EMA of $SPXA50R moves below 50 to signal a downturn

Tweaking

There are numerous ways to tweak a trading system, but chartists should avoid over-optimizing the indicator settings. In other words, don't attempt to find the perfect moving average period or crossover level. Perfection is unattainable when developing a system or trading the markets. It is important to keep the system logical and focus tweaks on other aspects, such as the actual price chart of the underlying security.

What do levels above and below 50% signify in the long-term moving average?

A move above 52.5% is deemed bullish, and below 47.5% is deemed bearish. These levels help to reduce whipsaws by using buffers for bullish and bearish thresholds.

How does the short-term moving average work to identify pullbacks or bounces?

When using a 5-day EMA, a move below 40 signals a pullback, and a move above 60 signals a bounce.

How is the reversal of pullback or bounce identified?

A move back above 50 after a pullback or below 50 after a bounce signals that the respective trend may be resuming.

How can you ensure that the uptrend has resumed?

It’s important to wait for the surge above 50 to ensure the uptrend has resumed, signaling improved breadth.

Can the system be tweaked to optimize indicator settings?

While there are various ways to tweak the system, seeking perfection through over-optimizing settings is advised against. It's crucial to keep the system logical and focus tweaks on the price chart of the underlying security.

RUSSIAN \ Русская версия.

Индикатор "Процент выше 50-дневной скользящей средней" измеряет процент акций, торгующихся в индексе выше их 50-дневной скользящей средней. Это полезный инструмент для оценки общего состояния рынка и выявления условий перекупленности и перепроданности.

Один из способов использования индикатора "Процент выше 50-дневной скользящей средней" в торговой стратегии - это объединить его с долгосрочной скользящей средней, чтобы определить, является ли тренд бычьим или медвежьим. Другой способ использовать его - объединить с краткосрочной скользящей средней, чтобы выявить откаты и отскоки в рамках общего тренда.

Цель использования индикатора "Процент выше 50-дневной скользящей средней" - участвовать в более широком тренде с лучшим соотношением риска и прибыли. Используя этот индикатор для выявления откатов и отскоков, вы можете снизить риск входа в сделки в неподходящее время.

Краткое описание бычьего сигнала:

150-дневная ЕМА на уровне $SPXA50R пересекает отметку 52,5 и остается выше 47,50, что задает бычий настрой.

5-дневная ЕМА на уровне $SPXA50R опускается ниже 40, сигнализируя об откате

5-дневная ЕМА на уровне $SPXA50R поднимается выше 50, сигнализируя о росте

Обзор медвежьих сигналов:

150-дневная ЕМА на уровне $SPXA50R пересекает уровень ниже 47,50 и остается ниже 52,50, что указывает на медвежий настрой.

5-дневная ЕМА на уровне $SPXA50R поднимается выше 60, сигнализируя о отскоке

5-дневная ЕМА на уровне $SPXA50 опускается ниже 50, что сигнализирует о спаде

Корректировка

Существует множество способов настроить торговую систему, но графологам следует избегать чрезмерной оптимизации настроек индикатора. Другими словами, не пытайтесь найти идеальный период скользящей средней или уровень пересечения. Совершенство недостижимо при разработке системы или торговле на рынках. Важно поддерживать логику системы и уделять особое внимание другим аспектам, таким как график фактической цены базовой ценной бумаги.

Что означают уровни выше и ниже 50% в долгосрочной скользящей средней?

Движение выше 52,5% считается бычьим, а ниже 47,5% - медвежьим. Эти уровни помогают снизить риски, используя буферы для бычьих и медвежьих порогов.

Как краткосрочная скользящая средняя помогает идентифицировать откаты или отскоки?

При использовании 5-дневной ЕМА движение ниже 40 указывает на откат, а движение выше 60 указывает на отскок.

Как определяется разворот отката или отскока?

Движение выше 50 после отката или ниже 50 после отскока сигнализирует о возможном возобновлении соответствующего тренда.

Как вы можете гарантировать, что восходящий тренд возобновился?

Важно дождаться скачка выше 50, чтобы убедиться в возобновлении восходящего тренда, сигнализирующего о расширении диапазона.

Можно ли настроить систему для оптимизации настроек индикатора?

Хотя существуют различные способы настройки системы, не рекомендуется стремиться к совершенству с помощью чрезмерной оптимизации настроек. Крайне важно сохранить логичность системы и сфокусировать изменения на ценовом графике базовой ценной бумаги.

[BT] NedDavis Series: CPI Minus 5-Year Moving Average🟧 GENERAL

The script works on the Monthly Timeframe and has 2 main settings (explained in FEATURES ). It uses the US CPI data, reported by the Bureau of Labour Statistics.

🔹Functionality 1: The main idea is to plot the distance between the CPI line and the 5 year moving average of the CPI line. This technique in mathematics is called "deviation from the moving average". This technique is used to analyse how has CPI previously acted and can give clues at what it might do in the future. Economic historians use such analysis, together with specific period analysis to predict potential risks in the future (see an example of such analysis in HOW TO USE section. The mathematical technique is a simple subtraction between 2 points (CPI - 5yr SMA of CPI).

▶︎Interpretation for deviation from a moving average:

Positive Deviation: When the line is above its moving average, it indicates that the current value is higher than the average, suggesting potential strength or bullish sentiment.

Negative Deviation: Conversely, when the line falls below its moving average, it suggests weakness or bearish sentiment as the current value is lower than the average.

▶︎Applications:

Trend Identification: Deviations from moving averages can help identify trends, with sustained deviations indicating strong trends.

Reversal Signals: Significant deviations from moving averages may signal potential trend reversals, especially when combined with other technical indicators.

Volatility Measurement: Monitoring the magnitude of deviations can provide insights into market volatility and price movements.

Remember the indicator is applying this only for the US CPI - not the ticker you apply the indicator on!

🔹Functionality 2: It plots on a new pane below information about the Consumer Price Index. You can also find the information by plotting the ticker symbol USACPIALLMINMEI on TradingView, which is a Monthly economic data by the OECD for the CPI in the US. The only addition you would get from the indicator is the plot of the 5 year Simple Moving Average.

🔹What is the US Consumer Price Index?

Measures the change in the price of goods and services purchased by consumers;

Traders care about the CPI because consumer prices account for a majority of overall inflation. Inflation is important to currency valuation because rising prices lead the central bank to raise interest rates out of respect for their inflation containment mandate;

It is measured as the average price of various goods and services are sampled and then compared to the previous sampling.

Source: Bureau of Labor Statistics;

FEATURES OF INDICATOR

1) The US Consumer Price Index Minus the Five Year Moving Average of the same.

As shown on the picture above and explained in previous section. Here a more detailed view.

2) The actual US Consumer Price Index (Annual Rate of change) and the Five year average of the US Consumer Price Index. Explained above and shown below:

To activate 2) go into settings and toggle the check box.

HOW TO USE

It can be used for a fundamental analysis on the relationship between the stock market, the economy and the Feds decisions to hike or cut rates, whose main mandate is to control inflation over time.

I have created this indicator to show my analysis in this idea:

What does a First Fed Rate cut really mean?

CREDITS

I have seen such idea in the past posted by the institutional grade research of NedDavis and have recreated it for the TradingView platform, open-source for the community.

Mag7 IndexThis is an indicator index based on cumulative market value of the Magnificent 7 (AAPL, MSFT, NVDA, TSLA, META, AMZN, GOOG). Such an indicator for the famous Mag 7, against which your main security can be benchmarked, was missing from the TradingView user library.

The index bar values are calculated by taking the weighted average of the 7 stocks, relative to their market cap. Explicitly, we are multiplying each bar period's total outstanding stock amount by the OHLC of that period for each stock and dividing that value by the combined sum of outstanding stock for the 7 corporations. OHLC is taken for the extended trading session.

The index dynamically adjusts with respect to the chosen main security and the bars/line visible in the chart window; that is, the first close value is normalized to the main security's first close value. It provides recalculation of the performance in that chart window as you scroll (this isn't apparent in the demo chart above this description).

It can be useful for checking market breadth, or benchmarking price performance of the individual stock components that comprise the Magnificent 7. I prefer comparing the indicator to the Nasdaq Composite Index (IXIC) or S&P500 (SPX), but of course you can make comparisons to any security or commodity.

Settings Input Options:

1) Bar vs. Line - view as OHLC colored bars or line chart. Line chart color based on close above or below the previous period close as green or red line respectively.

2) % vs Regular - the final value for the window period as % return for that window or index value

3) Turn on/off - bottom right tile displaying window-period performance

Inspired by the simpler NQ 7 Index script by @RaenonX but with normalization to main security at start of window and additional settings input options.

Please provide feedback for additional features, e.g., if a regular/extended session option is useful.

Danger Signals from The Trading MindwheelThe " Danger Signals " indicator, a collaborative creation from the minds at Amphibian Trading and MARA Wealth, serves as your vigilant lookout in the volatile world of stock trading. Drawing from the wisdom encapsulated in "The Trading Mindwheel" and the successful methodologies of legends like William O'Neil and Mark Minervini, this tool is engineered to safeguard your trading journey.

Core Features:

Real-Time Alerts: Identify critical danger signals as they emerge in the market. Whether it's a single day of heightened risk or a pattern forming, stay informed with specific danger signals and a tally of signals for comprehensive decision-making support. The indicator looks for over 30 different signals ranging from simple closing ranges to more complex signals like blow off action.

Tailored Insights with Portfolio Heat Integration: Pair with the "Portfolio Heat" indicator to customize danger signals based on your current positions, entry points, and stops. This personalized approach ensures that the insights are directly relevant to your trading strategy. Certain signals can have different meanings based on where your trade is at in its lifecycle. Blow off action at the beginning of a trend can be viewed as strength, while after an extended run could signal an opportunity to lock in profits.

Forward-Looking Analysis: Leverage the 'Potential Danger Signals' feature to assess future risks. Enter hypothetical price levels to understand potential market reactions before they unfold, enabling proactive trade management.

The indicator offers two different modes of 'Potential Danger Signals', Worst Case or Immediate. Worst Case allows the user to input any price and see what signals would fire based on price reaching that level, while the Immediate mode looks for potential Danger Signals that could happen on the next bar.

This is achieved by adding and subtracting the average daily range to the current bars close while also forecasting the next values of moving averages, vwaps, risk multiples and the relative strength line to see if a Danger Signal would trigger.

User Customization: Flexibility is at your fingertips with toggle options for each danger signal. Tailor the indicator to match your unique trading style and risk tolerance. No two traders are the same, that is why each signal is able to be turned on or off to match your trading personality.

Versatile Application: Ideal for growth stock traders, momentum swing traders, and adherents of the CANSLIM methodology. Whether you're a novice or a seasoned investor, this tool aligns with strategies influenced by trading giants.

Validation and Utility:

Inspired by the trade management principles of Michael Lamothe, the " Danger Signals " indicator is more than just a tool; it's a reflection of tested strategies that highlight the importance of risk management. Through rigorous validation, including the insights from "The Trading Mindwheel," this indicator helps traders navigate the complexities of the market with an informed, strategic approach.

Whether you're contemplating a new position or evaluating an existing one, the " Danger Signals " indicator is designed to provide the clarity needed to avoid potential pitfalls and capitalize on opportunities with confidence. Embrace a smarter way to trade, where awareness and preparation open the door to success.

Let's dive into each of the components of this indicator.

Volume: Volume refers to the number of shares or contracts traded in a security or an entire market during a given period. It is a measure of the total trading activity and liquidity, indicating the overall interest in a stock or market.

Price Action: the analysis of historical prices to inform trading decisions, without the use of technical indicators. It focuses on the movement of prices to identify patterns, trends, and potential reversal points in the market.

Relative Strength Line: The RS line is a popular tool used to compare the performance of a stock, typically calculated as the ratio of the stock's price to a benchmark index's price. It helps identify outperformers and underperformers relative to the market or a specific sector. The RS value is calculated by dividing the close price of the chosen stock by the close price of the comparative symbol (SPX by default).

Average True Range (ATR): ATR is a market volatility indicator used to show the average range prices swing over a specified period. It is calculated by taking the moving average of the true ranges of a stock for a specific period. The true range for a period is the greatest of the following three values:

The difference between the current high and the current low.

The absolute value of the current high minus the previous close.

The absolute value of the current low minus the previous close.

Average Daily Range (ADR): ADR is a measure used in trading to capture the average range between the high and low prices of an asset over a specified number of past trading days. Unlike the Average True Range (ATR), which accounts for gaps in the price from one day to the next, the Average Daily Range focuses solely on the trading range within each day and averages it out.

Anchored VWAP: AVWAP gives the average price of an asset, weighted by volume, starting from a specific anchor point. This provides traders with a dynamic average price considering both price and volume from a specific start point, offering insights into the market's direction and potential support or resistance levels.

Moving Averages: Moving Averages smooth out price data by creating a constantly updated average price over a specific period of time. It helps traders identify trends by flattening out the fluctuations in price data.

Stochastic: A stochastic oscillator is a momentum indicator used in technical analysis that compares a particular closing price of an asset to a range of its prices over a certain period of time. The theory behind the stochastic oscillator is that in a market trending upwards, prices will tend to close near their high, and in a market trending downwards, prices close near their low.

While each of these components offer unique insights into market behavior, providing sell signals under specific conditions, the power of combining these different signals lies in their ability to confirm each other's signals. This in turn reduces false positives and provides a more reliable basis for trading decisions

These signals can be recognized at any time, however the indicators power is in it's ability to take into account where a trade is in terms of your entry price and stop.

If a trade just started, it hasn’t earned much leeway. Kind of like a new employee that shows up late on the first day of work. It’s less forgivable than say the person who has been there for a while, has done well, is on time, and then one day comes in late.

Contextual Sensitivity:

For instance, a high volume sell-off coupled with a bearish price action pattern significantly strengthens the sell signal. When the price closes below an Anchored VWAP or a critical moving average in this context, it reaffirms the bearish sentiment, suggesting that the momentum is likely to continue downwards.

By considering the relative strength line (RS) alongside volume and price action, the indicator can differentiate between a normal retracement in a strong uptrend and a when a stock starts to become a laggard.

The integration of ATR and ADR provides a dynamic framework that adjusts to the market's volatility. A sudden increase in ATR or a character change detected through comparing short-term and long-term ADR can alert traders to emerging trends or reversals.

The "Danger Signals" indicator exemplifies the power of integrating diverse technical indicators to create a more sophisticated, responsive, and adaptable trading tool. This approach not only amplifies the individual strengths of each indicator but also mitigates their weaknesses.

Portfolio Heat Indicator can be found by clicking on the image below

Danger Signals Included

Price Closes Near Low - Daily Closing Range of 30% or Less

Price Closes Near Weekly Low - Weekly Closing Range of 30% or Less

Price Closes Near Daily Low on Heavy Volume - Daily Closing Range of 30% or Less on Heaviest Volume of the Last 5 Days

Price Closes Near Weekly Low on Heavy Volume - Weekly Closing Range of 30% or Less on Heaviest Volume of the Last 5 Weeks

Price Closes Below Moving Average - Price Closes Below One of 5 Selected Moving Averages

Price Closes Below Swing Low - Price Closes Below Most Recent Swing Low

Price Closes Below 1.5 ATR - Price Closes Below Trailing ATR Stop Based on Highest High of Last 10 Days

Price Closes Below AVWAP - Price Closes Below Selected Anchored VWAP (Anchors include: High of base, Low of base, Highest volume of base, Custom date)

Price Shows Aggressive Selling - Current Bars High is Greater Than Previous Day's High and Closes Near the Lows on Heaviest Volume of the Last 5 Days

Outside Reversal Bar - Price Makes a New High and Closes Near the Lows, Lower Than the Previous Bar's Low

Price Shows Signs of Stalling - Heavy Volume with a Close of Less than 1%

3 Consecutive Days of Lower Lows - 3 Days of Lower Lows

Close Lower than 3 Previous Lows - Close is Less than 3 Previous Lows

Character Change - ADR of Last Shorter Length is Larger than ADR of Longer Length

Fast Stochastic Crosses Below Slow Stochastic - Fast Stochastic Crosses Below Slow Stochastic

Fast & Slow Stochastic Curved Down - Both Stochastic Lines Close Lower than Previous Day for 2 Consecutive Days

Lower Lows & Lower Highs Intraday - Lower High and Lower Low on 30 Minute Timeframe

Moving Average Crossunder - Selected MA Crosses Below Other Selected MA

RS Starts Curving Down - Relative Strength Line Closes Lower than Previous Day for 2 Consecutive Days

RS Turns Negative Short Term - RS Closes Below RS of 7 Days Ago

RS Underperforms Price - Relative Strength Line Not at Highs, While Price Is

Moving Average Begins to Flatten Out - First Day MA Doesn't Close Higher

Price Moves Higher on Lighter Volume - Price Makes a New High on Light Volume and 15 Day Average Volume is Less than 50 Day Average

Price Hits % Target - Price Moves Set % Higher from Entry Price

Price Hits R Multiple - Price hits (Entry - Stop Multiplied by Setting) and Added to Entry

Price Hits Overhead Resistance - Price Crosses a Swing High from a Monthly Timeframe Chart from at Least 1 Year Ago

Price Hits Fib Level - Price Crosses a Fib Extension Drawn From Base High to Low

Price Hits a Psychological Level - Price Crosses a Multiple of 0 or 5

Heavy Volume After Significant Move - Above Average and Heaviest Volume of the Last 5 Days 35 Bars or More from Breakout

Moving Averages Begin to Slope Downward - Moving Averages Fall for 2 Consecutive Days

Blow Off Action - Highest Volume, Largest Spread, Multiple Gaps in a Row 35 Bars or More Post Breakout

Late Buying Frenzy - ANTS 35 Bars or More Post Breakout

Exhaustion Gap - Gap Up 5% or Higher with Price 125% or More Above 200sma

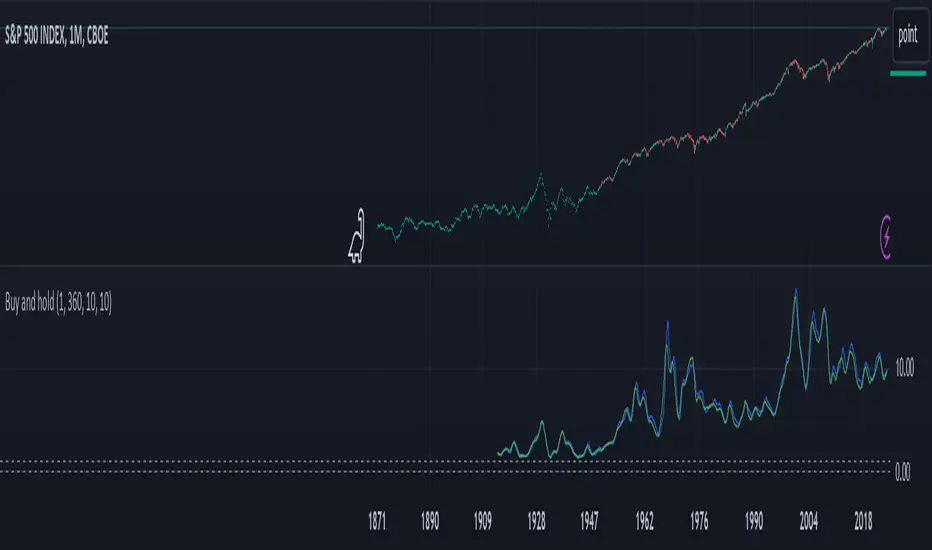

Buy and hold visualiserThis indicator shows the historical performance of a buy and hold portfolio. The purpose of the indicator is to show

1. the effect of the hold time (time between buying and selling a number of instruments) and

2. the effect of investing all capital at once (lump sum) versus dividing the investment over a number of months or years (cost averaging).

The indicator shows four lines:

- a dotted line at 0 (dollar or any other currency),

- a dotted line at the level of initial investment,

- a blue line that shows the amount of capital after selling at the end of the investment period after a lump sum investment,

- a green line that shows the amount of capital after selling at the end of the investment period after an investment that was done in chunks (cost averaging)

When 'chunks' is set to 1, the green line will match the blue line.

When 'investment' is set to 1, the blue and green lines will show the factor by which the initial investment was multiplied at the end of the investment period.

The effect of the hold time can be easily seen in the following example: Choose SPX (CBOE) as the active instrument, set 'chunks' to 1 and 'months' to 12. Depending on when you bought your portfolio, selling it a year later is like tossing a coin. Set 'months' to 360 and it becomes clear that it doesn't matter when you buy, the value of your portfolio will likely multiply considerably in 30 years, even if you bought everything all at once just before a bear market. It shows that with a long time horizon, you don't have to worry about timing the market.

Continue the example above and set 'chunks' to 12, thus spreading the initial investment over 12 months. The green line shows the cost averaging performance. The blue lump sum line is above the green line most of the time. Increase the chunks to 60 and the difference increases.

ARIMA Moving Average and Forecaster [SS]Finally releasing this. This took months, over 3 months to be precise, to figure out, code and troubleshoot! I honestly was going to give up on this project, but I finally got it to actually work fairly reliably. So hopefully you like it!

This is a very basic ARIMA modeler. It can do the following:

1. Provide you with an ARIMA based Moving Average;

2. Provide you with a standard error band;

3. Auto-select a lag length for assessment based on stationarity;

3. Provide you with the option of extending the error range by a user selected amount of standard deviations; and

4. Forecasting and plotting the forecast on the chart.

I will go over each function individually, but before I do, I think its important to talk a bit about what an ARIMA Model is and does:

ARIMA stands for AutoRegressive Integrated Moving Average and is an approach to modeling and time series forecasting. In simple terms, it combines autoregressive (AR) and moving average (MA) components to capture the underlying patterns in a time series data. The "AutoRegressive" part accounts for the relationship between an observation and its previous values, while the "Moving Average" part considers the relationship between an observation and a residual error from past observations. The "Integrated" component involves differencing the time series to make it stationary, which aids in stabilizing the model. ARIMA models help predict future values based on patterns observed in historical data, making them useful for forecasting in various fields such as economics, finance, and weather prediction.

The benefits to ARIMA is it will forecast based on the current trend, but it also provides for both the up and down scenario of the trend (i.e., if we are in a downtrend, what it would look like and what values we could expect if the trend reverses and vice versa). All of this is within the scope of this indicator, believe it or not!

If you would like more information on ARIMA, you can check out my educational post about it here:

Alrighty, now for the indicator functions.

ARIMA Moving Average and Standard Error Band

The ARIMA moving average is very simple, it takes the SMA of the current trend, lags it and plots out the lagged SMA. You can toggle the auto-select lag on, or you can pick your own lag manually. The above image is an auto-selected lag, but if we manually lag it by 5, this is what it looks like:

Its simply a lagged average of the 5 SMA (that is essentially how ARIMA works, by creating a moving average and lagging the moving average).

There are some implications to selecting a lag factor when it comes to forecasting, but I will cover this in the forecasting section. But I do want to make mention, you can use the ARIMA moving average in lieu of other moving averages. The advantage to doing this is it will be able to plot out the error bands. For example, if we wanted to get an ARIMA MA of the 200 SMA, we can toggle on the error bands and this is what we get:

Or the 50 MA:

NOTE: You ABSOLUTELY SHOULD NEVER use more than a lag of 4 or 5 for Forecasting (will be discussed later).

Auto-Select Lag

The indicator pulls the ARIMA modeler framework from my Forecasting library and pulls the stationarity assessment from my SPTS library. When you are doing an ARIMA model for forecasting, we need to ensure the data is stationary. Thus, if you want to forecast out the current trend, its highly recommended you select the "Auto Determine Lag Length" to find the most appropriate lag and forecast accordingly.

You can, however, chose your own lag order (model order), but this should never be above 4 or 5.

You should never select a lag of more than 5 because you are introducing too much "trendiness" into the equation, and you will get astronomical readings. ARIMA models never generally exceed a lag of 3 or 4 at most, as they are supposed be stationary and de-trended.

Extending by Standard Deviation

There is an option to select a standard deviation extension band. This is helpful for active day trading. Here is NIO extended by 2 standard deviations:

General suggestion is to only extend by 2 standard deviations and this is sufficient for most stocks.

Forecasting

The hallmark of an ARIMA model is the ability to use it for forecasting. Thus, the forecasting feature is a large portion of this indicator. You can see it displayed in the main chart above, but let's show some other examples:

NIO on the 1 hour:

TSLA on the 4 hour:

You can also display a forecasting table:

The result row shows the most likely, conservative, price at each time increment.

The Upper Confidence and Lower Confidence show what the trend would look like if it continued up or down at the current rate and the 95% confidence intervals show the values that the true source is likely to fall between at various increments in time with a 95% confidence (i.e. 95% probability that it should fall between these levels at period xyz assuming normal distribution).

The important levels, in my opinion, are the upper and lower confidence levels. These show you the current rate of decline or increase that the stock is expecting and what the trend would look like with a continuation or a reversal. This is ARIMA's biggest strength, as it has the ability to plot both outcomes assuming the current trend rate and time remains constant.

And that is the indicator! ARIMA is a bit of a complex process, but its a very powerful tool when used properly!

Troubleshooting:

One thing of note. Sometimes when autoselecting a length for forecasting, if there has been a heavy trend in one direction, you will not get the upper or lower confidence levels because of the lack of any up or down movement. In this case, manually select a lag of 3 to 5 to correct for this.

Let me know if you have any questions below and safe trades everyone!

Market Average TrendThis indicator aims to be complimentary to SPDR Tracker , but I've adjusted the name as I've been able to utilize the "INDEX" data provider to support essentially every US market.

This is a breadth market internal indicator that allows quick review of strength given the 5, 20, 50, 100, 150 and 200 simple moving averages. Each can be toggled to build whatever combinations are desired, I recommend reviewing classic combinations such as 5 & 20 as well as 50 & 200.

It's entirely possible that I've missed some markets that "INDEX" provides data for, if you find any feel free to drop a comment and I'll add support for them in an update.

Markets currently supported:

S&P 100

S&P 500

S&P ENERGIES

S&P INFO TECH

S&P MATERIALS

S&P UTILITIES

S&P FINANCIALS

S&P REAL ESTATE

S&P CON STAPLES

S&P HEALTH CARE

S&P INDUSTRIALS

S&P TELECOM SRVS

S&P CONSUMER DISC

S&P GROWTH

NAS 100

NAS COMP

DOW INDUSTRIAL

DOW COMP

DOW UTILITIES

DOW TRANSPORTATION

RUSSELL 1000

RUSSELL 2000

RUSSELL 3000

You can utilize this to watch stocks for dip buys or potential trend continuation entries, short entries, swing exits or numerous other portfolio management strategies.

If using it with stocks, it's advisable to ensure the stock often follows the index, otherwise obviously it's great to use with major indexes and determine holdings sentiment.

Important!

The "INDEX" data provider only supplies updates to all of the various data feeds at the end of day, I've noticed quite some delays even after market close and not taken time to review their actual update schedule (if even published). Therefore, it's strongly recommended to mostly ignore the last value in the series until it's the day after.

Only works on daily timeframes and above, please don't comment that it's not working if on other timeframes lower than daily :)

Feedback and suggestions are always welcome, enjoy!

chrono_utilsLibrary "chrono_utils"

Collection of objects and common functions that are related to datetime windows session days and time

ranges. The main purpose of this library is to handle time-related functionality and make it easy to reason about a

future bar and see if it is part of a predefined user session and/or inside a datetime window. All existing session

functions I found in the documentation e.g. "not na(time(timeframe, session, timezone))" are not suitable for

strategies, since the execution of the orders is delayed by one bar due to the execution happening at the bar close.

So a prediction for the next bar is necessary. Moreover, a history operator with a negative value is not allowed e.g.

`not na(time(timeframe, session, timezone) )` expression is not valid. Thus, I created this library to overcome

this small but very important limitation. In the meantime, I added useful functionality to handle session-based

behavior. An interesting utility that emerged from this development is data anomaly detection where a comparison

between the prediction and the actual value is happening. If those two values are different then a data inconsistency

happens between the prediction bar and the actual bar (probably due to a holiday or half session day etc..)

exTimezone(timezone)

exTimezone - Convert extended timezone to timezone string

Parameters:

timezone (simple string) : - The timezone or a special string

Returns: string representing the timezone

nameOfDay(day)

nameOfDay - Convert the day id into a short nameOfDay

Parameters:

day (int) : - The day id to convert

Returns: - The short name of the day

today()

today - Get the day id of this day

Returns: - The day id

nthDayAfter(day, n)

nthDayAfter - Get the day id of n days after the given day

Parameters:

day (int) : - The day id of the reference day

n (int) : - The number of days to go forward

Returns: - The day id of the day that is n days after the reference day

nextDayAfter(day)

nextDayAfter - Get the day id of next day after the given day

Parameters:

day (int) : - The day id of the reference day

Returns: - The day id of the next day after the reference day

nthDayBefore(day, n)

nthDayBefore - Get the day id of n days before the given day

Parameters:

day (int) : - The day id of the reference day

n (int) : - The number of days to go forward

Returns: - The day id of the day that is n days before the reference day

prevDayBefore(day)

prevDayBefore - Get the day id of previous day before the given day

Parameters:

day (int) : - The day id of the reference day

Returns: - The day id of the previous day before the reference day

tomorrow()

tomorrow - Get the day id of the next day

Returns: - The next day day id

normalize(num, min, max)

normalizeHour - Check if number is inthe range of

Parameters:

num (int)

min (int)

max (int)

Returns: - The normalized number

normalizeHour(hourInDay)

normalizeHour - Check if hour is valid and return a noralized hour range from

Parameters:

hourInDay (int)

Returns: - The normalized hour

normalizeMinute(minuteInHour)

normalizeMinute - Check if minute is valid and return a noralized minute from

Parameters:

minuteInHour (int)

Returns: - The normalized minute

monthInMilliseconds(mon)

monthInMilliseconds - Calculate the miliseconds in one bar of the timeframe

Parameters:

mon (int) : - The month of reference to get the miliseconds

Returns: - The number of milliseconds of the month

barInMilliseconds()

barInMilliseconds - Calculate the miliseconds in one bar of the timeframe

Returns: - The number of milliseconds in one bar

method init(this, fromDateTime, toDateTime)

init - Initialize the time window object from boolean values of each session day

Namespace types: DateTimeWindow

Parameters:

this (DateTimeWindow) : - The time window object that will hold the from and to datetimes

fromDateTime (int) : - The starting datetime of the time window

toDateTime (int) : - The ending datetime of the time window

Returns: - The time window object

method init(this, refTimezone, chTimezone, fromDateTime, toDateTime)

init - Initialize the time window object from boolean values of each session day

Namespace types: DateTimeWindow

Parameters:

this (DateTimeWindow) : - The time window object that will hold the from and to datetimes

refTimezone (simple string) : - The timezone of reference of the 'from' and 'to' dates

chTimezone (simple string) : - The target timezone to convert the 'from' and 'to' dates

fromDateTime (int) : - The starting datetime of the time window

toDateTime (int) : - The ending datetime of the time window

Returns: - The time window object

method init(this, sun, mon, tue, wed, thu, fri, sat)

init - Initialize the session days object from boolean values of each session day

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object that will hold the day selection

sun (bool) : - Is Sunday a trading day?

mon (bool) : - Is Monday a trading day?

tue (bool) : - Is Tuesday a trading day?

wed (bool) : - Is Wednesday a trading day?

thu (bool) : - Is Thursday a trading day?

fri (bool) : - Is Friday a trading day?

sat (bool) : - Is Saturday a trading day?

Returns: - The session days objectfrom_chart

method init(this, unixTime)

init - Initialize the object from the hour and minute of the session time in exchange timezone (syminfo.timezone)

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

unixTime (int) : - The unix time

Returns: - The session time object

method init(this, hourInDay, minuteInHour)

init - Initialize the object from the hour and minute of the session time in exchange timezone (syminfo.timezone)

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

hourInDay (int) : - The hour of the time

minuteInHour (int) : - The minute of the time

Returns: - The session time object

method init(this, hourInDay, minuteInHour, refTimezone)

init - Initialize the object from the hour and minute of the session time

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

hourInDay (int) : - The hour of the time

minuteInHour (int) : - The minute of the time

refTimezone (string) : - The timezone of reference of the 'hour' and 'minute'

Returns: - The session time object

method init(this, startTime, endTime)

init - Initialize the object from the start and end session time in exchange timezone (syminfo.timezone)

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object that will hold the start and end time of the daily session

startTime (SessionTime) : - The time the session begins

endTime (SessionTime) : - The time the session ends

Returns: - The session time range object

method init(this, startTimeHour, startTimeMinute, endTimeHour, endTimeMinute, refTimezone)

init - Initialize the object from the start and end session time

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object that will hold the start and end time of the daily session

startTimeHour (int) : - The time hour the session begins

startTimeMinute (int) : - The time minute the session begins

endTimeHour (int) : - The time hour the session ends

endTimeMinute (int) : - The time minute the session ends

refTimezone (string)

Returns: - The session time range object

method init(this, days, timeRanges)

init - Initialize the user session object from session days and time range

Namespace types: UserSession

Parameters:

this (UserSession) : - The user-defined session object that will hold the day and the time range selection

days (SessionDays) : - The session days object that defines the days the session is happening

timeRanges (SessionTimeRange ) : - The array of all the session time ranges during a session day

Returns: - The user session object

method to_string(this)

to_string - Formats the time window into a human-readable string

Namespace types: DateTimeWindow

Parameters:

this (DateTimeWindow) : - The time window object with the from and to datetimes

Returns: - The string of the time window

method to_string(this)

to_string - Formats the session days into a human-readable string with short day names

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object with the day selection

Returns: - The string of the session day short names

method to_string(this)

to_string - Formats the session time into a human-readable string

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

Returns: - The string of the session time

method to_string(this)

to_string - Formats the session time into a human-readable string

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object with the start and end time of the daily session

Returns: - The string of the session time

method to_string(this)

to_string - Formats the user session into a human-readable string

Namespace types: UserSession

Parameters:

this (UserSession) : - The user-defined session object with the day and the time range selection

Returns: - The string of the user session

method to_string(this)

to_string - Formats the bar into a human-readable string

Namespace types: Bar

Parameters:

this (Bar) : - The bar object with the open and close times

Returns: - The string of the bar times

method to_string(this)

to_string - Formats the chart session into a human-readable string

Namespace types: ChartSession

Parameters:

this (ChartSession) : - The chart session object that contains the days and the time range shown in the chart

Returns: - The string of the chart session

method get_size_in_secs(this)

get_size_in_secs - Count the seconds from start to end in the given timeframe

Namespace types: DateTimeWindow

Parameters:

this (DateTimeWindow) : - The time window object with the from and to datetimes

Returns: - The number of seconds inside the time widow for the given timeframe

method get_size_in_secs(this)

get_size_in_secs - Calculate the seconds inside the session

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object with the start and end time of the daily session

Returns: - The number of seconds inside the session

method get_size_in_bars(this)

get_size_in_bars - Count the bars from start to end in the given timeframe

Namespace types: DateTimeWindow

Parameters:

this (DateTimeWindow) : - The time window object with the from and to datetimes

Returns: - The number of bars inside the time widow for the given timeframe

method get_size_in_bars(this)

get_size_in_bars - Calculate the bars inside the session

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object with the start and end time of the daily session

Returns: - The number of bars inside the session for the given timeframe

method from_chart(this)

from_chart - Initialize the session days object from the chart

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object that will hold the day selection

Returns: - The user session object

method from_chart(this)

from_chart - Initialize the session time range object from the chart

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object that will hold the start and end time of the daily session

Returns: - The session time range object

method from_chart(this)

from_chart - Initialize the session object from the chart

Namespace types: ChartSession

Parameters:

this (ChartSession) : - The chart session object that will hold the days and the time range shown in the chart

Returns: - The chart session object

method to_sess_string(this)

to_sess_string - Formats the session days into a session string with day ids

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object

Returns: - The string of the session day ids

method to_sess_string(this)

to_sess_string - Formats the session time into a session string

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

Returns: - The string of the session time

method to_sess_string(this)

to_sess_string - Formats the session time into a session string

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object with the start and end time of the daily session

Returns: - The string of the session time

method to_sess_string(this)

to_sess_string - Formats the user session into a session string

Namespace types: UserSession

Parameters:

this (UserSession) : - The user-defined session object with the day and the time range selection

Returns: - The string of the user session

method to_sess_string(this)

to_sess_string - Formats the chart session into a session string

Namespace types: ChartSession

Parameters:

this (ChartSession) : - The chart session object that contains the days and the time range shown in the chart

Returns: - The string of the chart session

method from_sess_string(this, sess)

from_sess_string - Initialize the session days object from the session string

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object that will hold the day selection

sess (string) : - The session string part that represents the days

Returns: - The session days object

method from_sess_string(this, sess)

from_sess_string - Initialize the session time object from the session string in exchange timezone (syminfo.timezone)

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object that will hold the hour and minute of the time

sess (string) : - The session string part that represents the time HHmm

Returns: - The session time object

method from_sess_string(this, sess, refTimezone)

from_sess_string - Initialize the session time object from the session string

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object that will hold the hour and minute of the time

sess (string) : - The session string part that represents the time HHmm

refTimezone (simple string) : - The timezone of reference of the 'hour' and 'minute'

Returns: - The session time object

method from_sess_string(this, sess)

from_sess_string - Initialize the session time range object from the session string in exchange timezone (syminfo.timezone)

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object that will hold the start and end time of the daily session

sess (string) : - The session string part that represents the time range HHmm-HHmm

Returns: - The session time range object

method from_sess_string(this, sess, refTimezone)

from_sess_string - Initialize the session time range object from the session string

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object that will hold the start and end time of the daily session

sess (string) : - The session string part that represents the time range HHmm-HHmm

refTimezone (simple string) : - The timezone of reference of the time ranges

Returns: - The session time range object

method from_sess_string(this, sess)

from_sess_string - Initialize the user session object from the session string in exchange timezone (syminfo.timezone)

Namespace types: UserSession

Parameters:

this (UserSession) : - The user-defined session object that will hold the day and the time range selection

sess (string) : - The session string that represents the user session HHmm-HHmm,HHmm-HHmm:ddddddd

Returns: - The session time range object

method from_sess_string(this, sess, refTimezone)

from_sess_string - Initialize the user session object from the session string

Namespace types: UserSession

Parameters:

this (UserSession) : - The user-defined session object that will hold the day and the time range selection

sess (string) : - The session string that represents the user session HHmm-HHmm,HHmm-HHmm:ddddddd

refTimezone (simple string) : - The timezone of reference of the time ranges

Returns: - The session time range object

method nth_day_after(this, day, n)

nth_day_after - The nth day after the given day that is a session day (true) in the object

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object with the day selection

day (int) : - The day id of the reference day

n (int) : - The number of days after

Returns: - The day id of the nth session day of the week after the given day

method nth_day_before(this, day, n)

nth_day_before - The nth day before the given day that is a session day (true) in the object

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object with the day selection

day (int) : - The day id of the reference day

n (int) : - The number of days after

Returns: - The day id of the nth session day of the week before the given day

method next_day(this)

next_day - The next day that is a session day (true) in the object

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object with the day selection

Returns: - The day id of the next session day of the week

method previous_day(this)

previous_day - The previous day that is session day (true) in the object

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object with the day selection

Returns: - The day id of the previous session day of the week

method get_sec_in_day(this)

get_sec_in_day - Count the seconds since the start of the day this session time represents

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

Returns: - The number of seconds passed from the start of the day until that session time

method get_ms_in_day(this)

get_ms_in_day - Count the milliseconds since the start of the day this session time represents

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

Returns: - The number of milliseconds passed from the start of the day until that session time

method eq(this, other)

eq - Compare two bars

Namespace types: Bar

Parameters:

this (Bar) : - The bar object with the open and close times

other (Bar) : - The bar object to compare with

Returns: - Whether this bar is equal to the other one

method get_open_time(this)

get_open_time - The open time object

Namespace types: Bar

Parameters:

this (Bar) : - The bar object with the open and close times