VB Finviz-style MTF Screener📊 VB Multi-Timeframe Stock Screener (Daily + 4H + 1H)

A structured, high-signal stock screener that blends Daily fundamentals, 4H trend confirmation, and 1H entry timing to surface strong trading opportunities with institutional discipline.

🟦 1. Daily Screener — Core Stock Selection

All fundamental and structural filters run strictly on Daily data for maximum stability and signal quality.

Daily filters include:

📈 Average Volume & Relative Volume

💲 Minimum Price Threshold

📊 Beta vs SPY

🏢 Market Cap (Billions)

🔥 ATR Liquidity Filter

🧱 Float Requirements

📘 Price Above Daily SMA50

🚀 Minimum Gap-Up Condition

This layer acts like a Finviz-style engine, identifying stocks worth trading before momentum or timing is considered.

🟩 2. 4H Trend Confirmation — Momentum Check

Once a stock passes the Daily screen, the 4-hour timeframe validates trend strength:

🔼 Price above 4H MA

📈 MA pointing upward

This removes structurally good stocks that are not in a healthy trend.

🟧 3. 1H Entry Alignment — Timing Layer

The Hourly timeframe refines near-term timing:

🔼 Price above 1H MA

📉 Short-term upward movement detected

This step ensures the stock isn’t just good on paper—it’s moving now.

🧪 MTF Debug Table (Your Transparency Engine)

A live diagnostic table shows:

All Daily values

All 4H checks

All 1H checks

Exact PASS/FAIL per condition

Perfect for tuning thresholds or understanding why a ticker qualifies or fails.

🎯 Who This Screener Is For

Swing traders

Momentum/trend traders

Systematic and rules-based traders

Traders who want clean, multi-timeframe alignment

By combining Daily fundamentals, 4H trend structure, and 1H momentum, this screener filters the market down to the stocks that are strong, aligned, and ready.

Cerca negli script per "spy"

Adaptive Trend Navigator [ATH Filter & Risk Engine]Description:

This strategy implements a systematic Trend Following approach designed to capture major moves while actively protecting capital during severe bear markets. It combines a classic Moving Average "Fan" logic with two advanced risk management layers: a 4-Stage Dynamic Stop Loss and a macro-economic "Circuit Breaker" filter.

Core Concepts:

1. Trend Identification (Entry Logic) The script uses a cascade of Simple Moving Averages (SMA 25, 50, 100, 200) to identify the maturity of a trend.

Entries are triggered by specific crossovers (e.g., SMA 25 crossing SMA 50) or by breaking above the previous trade's high ("High-Water Mark" Re-Entry).

2. The "Circuit Breaker" (Crash Protection) To prevent trading during historical market collapses (like 2000 or 2008), the strategy monitors the Nasdaq 100 (QQQ) as a global benchmark:

Normal Regime: If the market is within 20% of its All-Time High, the strategy operates normally.

Crisis Regime: If the QQQ falls more than 20% from its ATH, the "Circuit Breaker" activates (Visualized by a Red Background).

Recovery Rule: In a Crisis Regime, new long positions are blocked unless the QQQ reclaims its SMA 200. This filters out "bull traps" in secular bear markets.

3. 4-Stage Risk Engine (Exit Logic) Once in a trade, the risk management adapts to the position's performance:

Stage 1: Fixed initial Stop Loss (default 10%) for breathing room.

Stage 2: Moves to Break-Even area once the price rises 12%.

Stage 3: Tightens to a trailing stop (8%) after 25% profit.

Stage 4: Maximizes gains with a tight trailing stop (5%) during parabolic moves (>40% profit).

Visual Guide:

SMAs: 25/50/100/200 period lines for trend visualization.

Red Background: Indicates the "Crisis Regime" where trading is halted due to broad market weakness.

Blue Background: Indicates a "Recovery Phase" (Crisis is active, but market is above SMA 200).

Red Line: Shows the dynamic Stop Loss level for active positions.

Settings: All parameters (SMA lengths, Drawdown threshold, Risk Stages) are fully customizable. The QQQ benchmark ticker can also be changed to SPY or other indices depending on the asset class traded.

MA200 Deviation Percentile200-Day MA Deviation with Dynamic Thresholds

OVERVIEW

This indicator measures price deviation from the 200-day moving average as a percentage, with dynamically calculated overbought/oversold thresholds based on historical percentiles.

Best suited for broad market indices (SPY, QQQ, IWM, etc.) where the 200-day MA serves as a reliable long-term trend indicator. Individual stocks may exhibit more erratic behavior around this level.

CALCULATION

Deviation (%) = (Close - 200MA) / 200MA x 100

Dynamic thresholds are derived from actual historical distribution rather than assuming normal distribution:

- Overbought threshold = 97.5th percentile of historical deviations

- Oversold threshold = 2.5th percentile of historical deviations

SETTINGS

MA Length (default: 200)

Moving average period.

Lookback Period (default: 1260)

Historical window for threshold calculation. 1260 bars approximates 5 years of daily data.

Threshold Percentile (default: 5%)

Two-tailed threshold. 5% places overbought/oversold boundaries at the 97.5th and 2.5th percentiles respectively.

INTERPRETATION

Deviation Value

- Positive: Price trading above 200MA

- Negative: Price trading below 200MA

- Magnitude indicates extent of deviation

Percentile Ranking (0-100%)

- Shows where current deviation ranks historically

- Above 90%: Historically elevated

- Below 10%: Historically depressed

Dynamic Threshold Lines

- Red line: Upper boundary based on historical distribution

- Green line: Lower boundary based on historical distribution

- These adapt automatically to each asset's volatility characteristics

APPLICATION

Mean Reversion

Extreme deviations tend to normalize over time. When deviation exceeds dynamic thresholds, probability of mean reversion increases.

Trend Assessment

Sustained positive/negative deviation confirms trend direction. Zero-line crossovers may signal trend changes.

NOTES

- Optimized for daily timeframe on market indices

- Requires sufficient historical data (minimum equal to lookback period)

- Extreme readings do not guarantee immediate reversals

- Use in conjunction with other analysis methods

Mebane Faber GTAA 5In 2007, Mebane Faber published research that challenged the conventional wisdom of buy-and-hold investing. His paper, titled "A Quantitative Approach to Tactical Asset Allocation" and published in the Journal of Wealth Management, demonstrated that a simple timing mechanism could reduce portfolio volatility and drawdowns while maintaining competitive returns (Faber, 2007). This indicator implements his Global Tactical Asset Allocation strategy, known as GTAA5, following the original methodology.

The core insight of Faber's research stems from a century of market data. By analyzing asset class performance from 1901 onwards, Faber found that a ten-month simple moving average served as an effective trend filter across major asset classes. When an asset trades above its ten-month moving average, it tends to continue its upward trajectory; when it falls below, significant drawdowns often follow (Faber, 2007, pp. 12-16). This observation aligns with momentum research by Jegadeesh and Titman (1993), who documented that intermediate-term momentum persists across equity markets.

The GTAA5 strategy allocates capital equally across five diversified asset classes: domestic equities (SPY), international developed markets (EFA), aggregate bonds (AGG), commodities (DBC), and real estate investment trusts (VNQ). Each asset receives a twenty percent allocation when trading above its ten-month moving average. When an asset falls below this threshold, its allocation moves to short-term treasury bills (SHY), creating a dynamic cash position that scales with market risk (Cambria Investment Management, 2013).

The strategy's historical performance during market crises illustrates its function. During the 2008 financial crisis, traditional sixty-forty portfolios experienced drawdowns exceeding forty percent. The GTAA5 strategy limited losses to approximately twelve percent by reducing equity exposure as prices declined below their moving averages (Faber, 2013). This asymmetric return profile represents the strategy's primary characteristic.

This implementation uses monthly closing prices retrieved via request.security() to calculate the ten-month simple moving average. This distinction matters, as approximations using daily data (such as a 200-day moving average) can generate different signals during volatile periods. Monthly data ensures the indicator produces signals consistent with published academic research.

The indicator provides position monitoring, automatic rebalancing detection on either the first or last trading day of each month, and share calculations based on user-defined capital. A dashboard displays current trend status for each asset class, target versus actual weightings, and trade instructions for rebalancing. Performance metrics including annualized volatility and Sharpe ratio provide ongoing risk assessment.

Several limitations warrant acknowledgment. First, the strategy rebalances monthly, meaning it cannot respond to intra-month market crashes. Second, transaction costs and taxes from monthly rebalancing may reduce net returns for taxable accounts. Third, the ten-month lookback period, while historically robust, offers no guarantee of future effectiveness. As Ilmanen (2011) notes in "Expected Returns", all timing strategies face the risk of regime change, where historical relationships break down.

This indicator serves educational purposes and portfolio monitoring. It does not constitute financial advice.

References:

Cambria Investment Management (2013). Global Tactical Asset Allocation: An Introduction to the Approach. Research Report, Los Angeles.

Faber, M.T. (2007). A Quantitative Approach to Tactical Asset Allocation. Journal of Wealth Management, Spring 2007, pp. 9-79.

Faber, M.T. (2013). Global Asset Allocation: A Survey of the World's Top Asset Allocation Strategies. Cambria Investment Management, Los Angeles.

Ilmanen, A. (2011). Expected Returns: An Investor's Guide to Harvesting Market Rewards. John Wiley and Sons, Chichester.

Jegadeesh, N. and Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. Journal of Finance, 48(1), pp. 65-91.

Classic Wave: The Easy WayClassic Wave is a simple strategy with few rules and no over-optimization. Despite its simplicity, it is backed by a nearly century-long historical track record, delivering excellent returns on the weekly chart of the SPX (TVC).

I also recommend observing its strong performance on the SPY (weekly), which is the perfect instrument for executing this strategy with futures in the future.

Strategy Rules and Parameters

When a bullish candle closes above the 20-period EMA, we place the stop-loss below the low of that candle and target a risk-reward ratio of 1:1.

A second, more profitable variant is to change the risk-reward ratio in the code to 2:1.

-Total capital: $10,000

-We use 10% of the total capital per trade.

-Commissions: 0.1% per trade.

The code construction is simple and very well detailed within the script itself.

Risk-Reward Ratio 2:1

Using a 2:1 risk-reward ratio reduces the win rate but significantly increases profitability.

Across the full historical data of the SPX index (weekly), the system would have generated 236 trades, with a win rate of 51.27% and a profit factor of 2.53.

From January 1, 2023, to November 28, 2025, the system would have generated 5 trades, with an 80% win rate and a profit factor of 9.244.

What makes this system so good?

-It takes advantage of the long-term bullish bias of U.S. stock indices and traditional markets.

-It filters out a lot of noise thanks to the weekly timeframe.

-It uses simple parameters with no over-optimization.

Final Notes:

This strategy has consistently outperformed the returns offered by most traditional funds over time, with fewer drawdowns and significantly less stress. I hope you like it.

Elite Correlation Matrix AIThe Elite Correlation Matrix AI indicator provides comprehensive real-time correlation analysis across multiple asset classes, displaying the interrelationships between equities, bonds, commodities, currencies, and volatility instruments.

The indicator calculates and displays correlation coefficients between a predefined set of major market indices and instruments, including:

• Major equity indices (SPY, QQQ, IWM)

• Long-term Treasury bonds (TLT)

• Gold (GLD)

• Crude oil (USO)

• Volatility (VIX)

• US Dollar Index (DXY)

• Bitcoin (BTCUSD)

Key features include:

• Rolling correlation calculations across user-defined periods to identify both short-term and longer-term relationships

• Visual correlation heat map showing the strength and direction of relationships between all tracked instruments

• Detection of correlation breakdowns, which often precede significant market regime shifts

• Dashboard display providing summary metrics of prevailing correlation patterns

The indicator enables users to monitor the current state of market relationships and identify when traditional correlations begin to break down, which frequently serves as an early warning of impending changes in market behavior. By tracking the degree of connectedness between different asset classes, the indicator provides insight into the current risk environment and the potential for diversification effectiveness.

This analysis is particularly valuable for understanding periods of market stress when asset relationships deviate from their normal patterns, as well as identifying environments where traditional correlations hold and where they are undergoing structural changes.

Trend Breakout & Ratchet Stop System [Market Filter]Description:

This strategy implements a robust trend-following system designed to capture momentum moves while strictly managing downside risk through a multi-stage "Ratchet" exit mechanism and broad market filters.

It is designed for swing traders who want to align individual stock entries with the overall market direction.

How it works:

1. Market Regime Filters (The "Safety Check") Before taking any position, the strategy checks the health of the broader market to avoid "catching falling knives."

Broad Market Filter: By default, it checks NASDAQ:QQQ (adjustable). If the benchmark is trading below its SMA 200, the strategy assumes a Bear Market and suppresses all new long entries.

Volatility Filter (VIX): Uses CBOE:VIX to gauge fear. If the VIX is above a specific threshold (Default: 32), entries are paused, and existing positions can optionally be closed to preserve capital.

2. Entry Logic Entries are based on Momentum and Trend confirmation. A position is opened if filters are clear AND one of the following occurs:

Golden Cross: SMA 25 crosses over SMA 50.

SMA Breakouts: A "Three-Bar-Break" logic confirms a breakout above the SMA 50, 100, or 200 (price must establish itself above the moving average).

3. The "Ratchet" Exit System The exit logic evolves as the trade progresses, tightening risk like a ratchet:

Stage 0 (Initial Risk): Starts with a standard percentage Stop Loss from the entry price.

Stage 1 (Breakeven/Lock): Once the price rises by Profit Step 1 (e.g., +10%), the Stop Loss jumps to a tighter level and locks there. This secures the initial move.

Stage 2 (Trailing Mode): If the price continues to rise to Profit Step 2 (e.g., +15%), the Stop Loss converts into a dynamic Trailing Stop relative to the Highest High. This allows the trade to run as long as the trend persists.

Additional Exits:

Dead Cross: Closes position if SMA 25 crosses under SMA 50.

VIX Panic: Emergency exit if volatility spikes above the threshold.

Settings & Customization:

SMAs: Adjustable lengths for all Moving Averages.

Filters: Toggle Market/VIX filters on/off and choose your benchmark ticker (e.g., SPY or QQQ).

Risk Management: Fully customizable percentages for the Ratchet steps (Initial SL, Stage 1 Trigger, Trailing distance).

stock-vs-industry using NQUSB benchmark idexesOriginal idea from Stock versus Industry by Tr33man .

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

═══ PRIMARY IMPROVEMENT: NQUSB Hierarchical Index Benchmarks ═══

The KEY improvement: Multi-Level Industry Granularity with Drill-Down/Drill-Up Navigation

From: Simple ETF Comparison (1 Level) Stock → Industry ETF (e.g., "SOXX" for all semiconductors)

To: NQUSB Hierarchical Comparison (4 Levels)

Level 4 (Primary): NQUSB10102010 → Semiconductors (most specific)

Level 3 (Secondary): NQUSB101020 → Technology Hardware and Equipment

Level 2 (Tertiary): NQUSB101010 → Software and Computer Services

Level 1 (Quaternary): NQUSB10 → Technology (broadest sector)

Users can now drill up and down the industry hierarchy to see how their stock performs against different levels of industry classification!

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

═══ WHY THIS MATTERS ═══

Original Limitations:

Single comparison level - ETF only

No drill-down capability - Can't zoom in to more specific industries

No drill-up capability - Can't zoom out to broader sectors

ETF limitations - Not all industries have dedicated ETFs

Arbitrary mappings - Manual ETF selection may not represent true industry

Improved Capabilities:

4-level hierarchical navigation - Drill-down and drill-up through industry classifications

361 NQUSB official indices - NASDAQ US Benchmark Index structure

Official NASDAQ classification - Industry-standard taxonomy

Large Mid Cap (LM) option - Focus on larger companies when needed

Enhanced UI - Clear level indicators and full index descriptions

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

═══ EXAMPLE: ANALYZING NVDA (Semiconductors) ═══

Level 4 - Primary (Most Specific):

NQUSB10102010 - Semiconductors

→ NVDA vs. AMD, AVGO, QCOM, TXN, etc. (direct competitors)

Level 3 - Secondary (Broader):

NQUSB101020 - Tech Hardware & Equipment

→ NVDA vs. AAPL, CSCO + semiconductors

Level 2 - Tertiary (Even Broader):

NQUSB101010 - Software and Computer Services

→ NVDA vs. all tech hardware

Level 1 - Quaternary (Broadest):

NQUSB10 - Technology Sector

→ NVDA vs. entire technology sector

You can now zoom in to see direct competitors or zoom out to understand macro sector trends - all in one indicator!

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

═══ COMPARISON SUMMARY ═══

Original Version:

Comparison System: Industry ETFs

Industry Levels: 1 (flat ETF mapping)

Total Classifications: ~140 industries

Hierarchy Navigation: ❌ No

Data Source: Manual ETF curation

Improved Version:

Comparison System: NQUSB Official Indices

Industry Levels: 4 (hierarchical drill-down/up)

Total Classifications: 361 NQUSB indices

Hierarchy Navigation: ✅ 4-level drill navigation

Data Source: NASDAQ official taxonomy

Large/Mid Cap Option: ✅ LM variant toggle

Level Indicator: ✅ to labels

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

═══ ADDITIONAL FEATURES ═══

Dual Comparison System - Toggle between ETF mode (original) and Index Benchmark mode (NQUSB hierarchy)

Better Fallback Logic - Manual Override > NQUSB Index > ETF > SPY default

Enhanced Display - 4-row information table with full NQUSB index description

Backward Compatible - All original ETF mappings still work, existing charts won't break

Large Mid Cap Toggle - Optional "LM" suffix for focusing on larger companies only

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

For complete documentation, data files, technical details, and the full NQUSB hierarchy structure, visit the GitHub repository.

The result: More accurate, more flexible, and more comprehensive industry strength analysis - enabling traders to understand exactly where their stock's performance comes from by drilling through multiple levels of industry classification.

Kai GoNoGo 2mKai GoNoGo 2m is a multi-factor trend confirmation system designed for fast intraday trading on the 2-minute chart.

It combines EMAs, MACD, RSI and ADX through a weighted scoring model to generate clear Go / NoGo conditions for both CALL (long) and PUT (short) setups.

The indicator paints the candles with pure colors to show the current strength of the trend:

Strong Go (Bright Blue): Full bullish alignment across EMAs, momentum and trend strength.

Weak Go (Light Blue): Bullish structure but with softer momentum.

Weak NoGo (Light Pink): Bearish structure starting to develop.

Strong NoGo (Bright Pink): Full bearish alignment across all components.

Neutral (Gray): No trend, compression or transition phase.

Components included:

EMA Trend Structure (9/21/50/100/200)

MACD Momentum (12-26-9)

RSI Confirmation (14)

ADX Trend Strength Filter via DMI (14,14)

Scoring system inspired by the original GoNoGo concept, improved for speed-based trading.

Designed for:

Scalping, 0DTE options, FAST trend continuation entries, and momentum confirmation on QQQ, SPY, NQ, ES and high-beta names.

This version uses pure colors (no gradients) for maximum clarity when trading fast charts.

Pivot Reversal Signals - Multi ConfirmationPivot Reversal Signals - Multi-Confirmation System

Overview

A comprehensive reversal detection indicator designed for daytraders that combines six independent technical signals to identify high-probability pivot points. The indicator uses a scoring system to classify signal strength as Weak, Medium, or Strong based on the number of confirmations present.

How It Works

The indicator monitors six key reversal signals simultaneously:

1. RSI Divergence - Detects when price makes new highs/lows but RSI shows weakening momentum

2. MACD Divergence - Identifies divergence between price action and MACD histogram

3. Key Level Touch - Confirms price is at significant support/resistance (previous day high/low, premarket high/low, VWAP, 50 SMA)

4. Reversal Candlestick Patterns - Recognizes bullish/bearish engulfing, hammers, and shooting stars

5. Moving Average Confluence - Validates bounces/rejections at stacked moving averages (9/20/50)

6. Volume Spike - Confirms increased participation (default: 1.5x average volume)

Signal Strength Classification

• Weak (3/6 confirmations) - Small circles for situational awareness only

• Medium (4/6 confirmations) - Regular triangles, viable entry signals

• Strong (5-6/6 confirmations) - Large triangles with background highlight, highest probability setups

Visual Features

• Entry Signals: Green triangles (up) for long entries, red triangles (down) for short entries

• Exit Warnings: Orange X markers when opposing signals appear

• Signal Labels: Show confirmation score (e.g., "5/6") and strength level

• Key Levels Displayed:

o Previous Day High/Low - Solid green/red lines (uses actual daily data)

o Premarket High/Low - Blue/orange circles (4:00 AM - 9:30 AM EST)

o VWAP - Purple line

o Moving Averages - 9 EMA (blue), 20 EMA (orange), 50 SMA (red)

• Background Tinting: Subtle color on strongest reversal zones

Key Level Detection

The indicator uses request.security() to accurately fetch previous day's high/low from daily timeframe data, ensuring precise level placement. Premarket high/low levels are dynamically tracked during premarket sessions (4:00 AM - 9:30 AM EST) and plotted throughout the trading day, providing critical support/resistance zones that often influence price action during regular hours.

Customizable Parameters

• Signal strength thresholds (adjust required confirmations)

• RSI settings (length, overbought/oversold levels)

• MACD parameters (fast/slow/signal lengths)

• Moving average periods

• Volume spike multiplier

• Toggle individual display elements (levels, MAs, labels)

Best Practices

• Use on 5-minute charts for entries, confirm on 15-minute for direction

• Focus on Medium and Strong signals; Weak signals provide context only

• Strong signals (5-6 confirmations) have the highest win rate

• Pay special attention to reversals at premarket high/low - these levels frequently hold

• Previous day high/low often acts as major support/resistance

• Always use proper risk management and stop losses

• Works best in moderately trending markets

Alert Capabilities

Set custom alerts for:

• Strong long/short signals

• All entry signals (medium + strong)

• Exit warnings for open positions

Ideal For

• Daytraders and scalpers (especially SPY, QQQ, and liquid equities)

• Swing traders seeking precise entries

• Traders who prefer confirmation-based systems

• Anyone looking to reduce false signals with multi-factor validation

• Traders who utilize premarket levels in their strategy

Technical Notes

• Uses Pine Script v6

• Premarket hours: 4:00 AM - 9:30 AM EST

• Previous day levels pulled from daily timeframe for accuracy

• Maximum 500 labels to maintain chart performance

• All key levels update dynamically in real-time

________________________________________

Note: This indicator provides signal analysis only and should be used as part of a complete trading strategy. Past performance does not guarantee future results. Always practice proper risk management.

Vital Wave 20-50Simplicity is almost always the most effective approach, and here I’m giving you a trend-following system that exploits the bullish bias of traditional markets and their trending nature, with very basic rules.

Rules (long entries only)

• Market entry: When the EMA 20 crosses above the EMA 50 (from below)

• Main market exit: When the EMA 20 crosses below the EMA 50 (from above)

• Fixed Stop Loss: Placed at the price level of the Lower Bollinger Band at the moment the trade is entered.

In my strategy, the primary exit is when the EMA 20 crosses below the EMA 50. However, this crossover can sometimes take a while to occur, and in the meantime the price may have already dropped significantly. The Stop Loss based on the Lower Bollinger Band is designed to limit losses in case the market moves sharply against the position without giving the bearish crossover signal in time. Having two exit conditions makes the strategy much more robust in terms of risk management.

Risk Management:

• Initial capital: $10,000

• Position size: 10% of available capital per trade

• Commissions: 0.1% on traded volume

• Stop Loss: Based on the Lower Bollinger Band

• Take Profit / Exit: When EMA 20 crosses below EMA 50

Recommended Markets:

XAUUSD (OANDA) (Daily)

Period: January 3, 1833 – November 23, 2025

Total Profit & Loss: +$6,030.62 USD (+57.57%)

Maximum Drawdown: $541.53 USD (3.83%)

Total Trades: 136

Winning Trades (Win Rate): 36.03% (49/136)

Profit Factor: 2.483

XAUUSD (OANDA) (12-hour)

Period: March 19, 2006 – November 23, 2025

Total Profit & Loss: +$1,209.56 USD (+11.89%)

Maximum Drawdown: $384.58 USD (3.61%)

Total Trades: 97

Winning Trades (Win Rate): 35.05% (34/97)

Profit Factor: 1.676

XAUUSD (OANDA) (8-hour)

Period: March 19, 2006 – November 23, 2025

Total Profit & Loss: +$1,179.36 USD (+11.81%)

Maximum Drawdown: $246.88 USD (2.32%)

Total Trades: 147

Winning Trades (Win Rate): 31.97% (47/147)

Profit Factor: 1.626

Tesla (NASDAQ) (4-hour)

Period: June 29, 2010 – November 23, 2025

Total Profit & Loss (Absolute): +$11,687.90 USD (+116.88%)

Maximum Drawdown: $922.05 USD (6.50%)

Total Trades: 68

Winning Trades (Win Rate): 39.71% (27/68)

Profit Factor: 4.156

Tesla (NASDAQ) (3-hour)

Total Profit & Loss: +$11,522.33 USD (+115.22%)

Maximum Drawdown: $1,247.60 USD (8.80%)

Total Trades: 114

Winning Trades: 33.33% (38/114)

Profit Factor: 2.811

Additional Recommendations

(These assets have shown good trending behavior with the same strategy across multiple timeframes):

• NVDA (15 min, 30 min, 1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• NFLX (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• MA (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• META (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• AAPL (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• SPY (12h, Daily)

About the Code

The user can modify:

• EMA periods (20 and 50 by default)

• Bollinger Bands length (20 periods)

• Standard deviation (2.0)

Visualization

• EMA 20: Blue line

• EMA 50: Red line

• Green background when EMA20 > EMA50 (bullish trend)

• Red background when EMA20 < EMA50 (bearish trend)

Important Note:

We can significantly increase the profit factor and overall profitability by risking a fixed percentage per trade instead of a fixed amount. This would prevent losses from fluctuating with changes in volatility.

This could be implemented by reducing position size or adjusting leverage based on the volatility percentage required for each trade, but I’m not sure if this is fully possible in Pine Script. In my other script, “ Golden Cross 50/200 EMA ,” I go deeper into this topic and provide examples.

I hope you enjoy this contribution. Best regards!

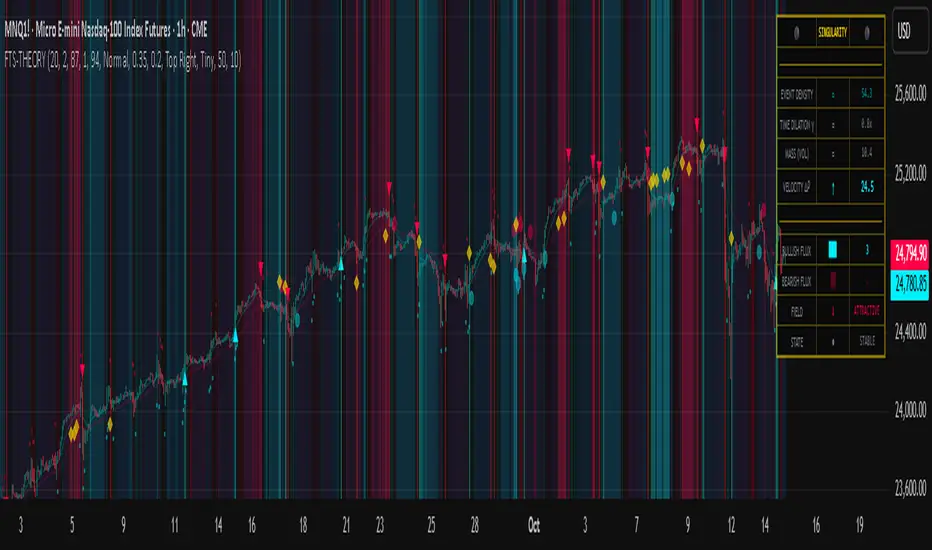

Flux-Tensor Singularity [FTS]Flux-Tensor Singularity - Multi-Factor Market Pressure Indicator

The Flux-Tensor Singularity (FTS) is an advanced multi-factor oscillator that combines volume analysis, momentum tracking, and volatility-weighted normalization to identify critical market inflection points. Unlike traditional single-factor indicators, FTS synthesizes price velocity, volume mass, and volatility context into a unified framework that adapts to changing market regimes.

This indicator identifies extreme market conditions (termed "singularities") where multiple confirming factors converge, then uses a sophisticated scoring system to determine directional bias. It is designed for traders seeking high-probability setups with built-in confluence requirements.

THEORETICAL FOUNDATION

The indicator is built on the premise that market time is not constant - different market conditions contain varying levels of information density. A 1-minute bar during a major news event contains far more actionable information than a 1-minute bar during overnight low-volume trading. Traditional indicators treat all bars equally; FTS does not.

The theoretical framework draws conceptual parallels to physics (purely as a mental model, not literal physics):

Volume as Mass: Large volume represents significant market participation and "weight" behind price moves. Just as massive objects have stronger gravitational effects, high-volume moves carry more significance.

Price Change as Velocity: The rate of price movement through price space represents momentum and directional force.

Volatility as Time Dilation: When volatility is high relative to its historical norm, the "information density" of each bar increases. The indicator weights these periods more heavily, similar to how time dilates near massive objects in physics.

This is a pedagogical metaphor to create a coherent mental model - the underlying mathematics are standard financial calculations combined in a novel way.

MATHEMATICAL FRAMEWORK

The indicator calculates a composite singularity value through four distinct steps:

Step 1: Raw Singularity Calculation

S_raw = (ΔP × V) × γ²

Where:

ΔP = Price Velocity = close - close

V = Volume Mass = log(volume + 1)

γ² = Time Dilation Factor = (ATR_local / ATR_global)²

Volume Transformation: Volume is log-transformed because raw volume can have extreme outliers (10x-100x normal). The logarithm compresses these spikes while preserving their significance. This is standard practice in volume analysis.

Volatility Weighting: The ratio of short-term ATR (5 periods) to long-term ATR (user-defined lookback) is squared to create a volatility amplification factor. When local volatility exceeds global volatility, this ratio increases, amplifying the raw singularity value. This makes the indicator regime-aware.

Step 2: Normalization

The raw singularity values are normalized to a 0-100 scale using a stochastic-style calculation:

S_normalized = ((S_raw - S_min) / (S_max - S_min)) × 100

Where S_min and S_max are the lowest and highest raw singularity values over the lookback period.

Step 3: Epsilon Compression

S_compressed = 50 + ((S_normalized - 50) / ε)

This is the critical innovation that makes the sensitivity control functional. By applying compression AFTER normalization, the epsilon parameter actually affects the final output:

ε < 1.0: Expands range (more signals)

ε = 1.0: No change (default)

ε > 1.0: Compresses toward 50 (fewer, higher-quality signals)

For example, with ε = 2.0, a normalized value of 90 becomes 70, making threshold breaches rarer and more significant.

Step 4: Smoothing

S_final = EMA(S_compressed, smoothing_period)

An exponential moving average removes high-frequency noise while preserving trend.

SIGNAL GENERATION LOGIC

When the tensor crosses above the upper threshold (default 90) or below the lower threshold (default 10), an extreme event is detected. However, the indicator does NOT immediately generate a buy or sell signal. Instead, it analyzes market context through a multi-factor scoring system:

Scoring Components:

Price Structure (+1 point): Current bar bullish/bearish

Momentum (+1 point): Price higher/lower than N bars ago

Trend Context (+2 points): Fast EMA above/below slow EMA (weighted heavier)

Acceleration (+1 point): Rate of change increasing/decreasing

Volume Multiplier (×1.5): If volume > average, multiply score

The highest score (bullish vs bearish) determines signal direction. This prevents the common indicator failure mode of "overbought can stay overbought" by requiring directional confirmation.

Signal Conditions:

A BUY signal requires:

Extreme event detection (tensor crosses threshold)

Bullish score > Bearish score

Price confirmation: Bullish candle (optional, user-controlled)

Volume confirmation: Volume > average (optional, user-controlled)

Momentum confirmation: Positive momentum (optional, user-controlled)

A SELL signal requires the inverse conditions.

INPUTS EXPLAINED - Core Parameters:

Global Horizon (Context): Default 20. Lookback period for normalization and volatility comparison. Higher values = smoother but less responsive. Lower values = more signals but potentially more noise.

Tensor Smoothing: Default 3. EMA period applied to final output. Removes "quantum foam" (high-frequency noise). Range 1-20.

Singularity Threshold: Default 90. Values above this (or below 100-threshold) trigger extreme event detection. Higher = rarer, stronger signals.

Signal Sensitivity (Epsilon): Default 1.0. Post-normalization compression factor. This is the key innovation - it actually works because it's applied AFTER normalization. Range 0.1-5.0.

Signal Interpreter Toggles:

Require Price Confirmation: Default ON. Only generates buy signals on bullish candles, sell signals on bearish candles. Reduces false signals but may delay entry.

Require Volume Confirmation: Default ON. Only signals when volume > average. Critical for stocks/crypto, less important for forex (unreliable volume data).

Use Momentum Filter: Default ON. Requires momentum agreement with signal direction. Prevents counter-trend signals.

Momentum Lookback: Default 5. Number of bars for momentum calculation. Shorter = more responsive, longer = trend-following bias.

Visual Controls:

Colors: Customizable colors for bullish flux, bearish flux, background, and event horizon.

Visual Transparency: Default 85. Master control for all visual elements (accretion disk, field lines, particles, etc.). Range 50-99. Signals and dashboard have separate controls.

Visibility Toggles: Individual on/off switches for:

Gravitational field lines (trend EMAs)

Field reversals (trend crossovers)

Accretion disk (background gradient)

Singularity diamonds (neutral extreme events)

Energy particles (volume bursts)

Event horizon flash (extreme event background)

Signal background flash

Signal Size: Tiny/Small/Normal triangle size

Signal Offsets: Separate controls for buy and sell signal vertical positioning (percentage of price)

Dashboard Settings:

Show Dashboard: Toggle on/off

Position: 9 placement options (all corners, centers, middles)

Text Size: Tiny/Small/Normal/Large

Background Transparency: 0-50, separate from visual transparency

VISUAL ELEMENTS EXPLAINED

1. Accretion Disk (Background Gradient):

A three-layer gradient background that intensifies as the tensor approaches extremes. The outer disk appears at any non-neutral reading, the inner disk activates above 70 or below 30, and the core layer appears above 85 or below 15. Color indicates direction (cyan = bullish, red = bearish). This provides instant visual feedback on market pressure intensity.

2. Gravitational Field Lines (EMAs):

Two trend-following EMAs (10 and 30 period) visualized as colored lines. These represent the "curvature" of market trend - when they diverge, trend is strong; when they converge, trend is weakening. Crossovers mark potential trend reversals.

3. Field Reversals (Circles):

Small circles appear when the fast EMA crosses the slow EMA, indicating a potential trend change. These are distinct from extreme events and appear at normal market structure shifts.

4. Singularity Diamonds:

Small diamond shapes appear when the tensor reaches extreme levels (>90 or <10) but doesn't meet the full signal criteria. These are "watch" events - extreme pressure exists but directional confirmation is lacking.

5. Energy Particles (Dots):

Tiny dots appear when volume exceeds 2× average, indicating significant participation. Color matches bar direction. These highlight genuine high-conviction moves versus low-volume drifts.

6. Event Horizon Flash:

A golden background flash appears the instant any extreme threshold is breached, before directional analysis. This alerts you to pay attention.

7. Signal Background Flash:

When a full buy/sell signal is confirmed, the background flashes cyan (buy) or red (sell). This is your primary alert that all conditions are met.

8. Signal Triangles:

The actual buy (▲) and sell (▼) markers. These only appear when ALL selected confirmation criteria are satisfied. Position is offset from bars to avoid overlap with other indicators.

DASHBOARD METRICS EXPLAINED

The dashboard displays real-time calculated values:

Event Density: Current tensor value (0-100). Above 90 or below 10 = critical. Icon changes: 🔥 (extreme high), ❄️ (extreme low), ○ (neutral).

Time Dilation (γ): Current volatility ratio squared. Values >2.0 indicate extreme volatility environments. >1.5 = elevated, >1.0 = above average. Icon: ⚡ (extreme), ⚠ (elevated), ○ (normal).

Mass (Vol): Log-transformed volume value. Compared to volume ratio (current/average). Icon: ● (>2× avg), ◐ (>1× avg), ○ (below avg).

Velocity (ΔP): Raw price change. Direction arrow indicates momentum direction. Shows the actual price delta value.

Bullish Flux: Current bullish context score. Displayed as both a bar chart (visual) and numeric value. Brighter when bullish score dominates.

Bearish Flux: Current bearish context score. Same visualization as bullish flux. These scores compete - the winner determines signal direction.

Field: Trend direction based on EMA relationship. "Repulsive" (uptrend), "Attractive" (downtrend), "Neutral" (ranging). Icon: ⬆⬇↔

State: Current market condition:

🚀 EJECTION: Buy signal active

💥 COLLAPSE: Sell signal active

⚠ CRITICAL: Extreme event, no directional confirmation

● STABLE: Normal market conditions

HOW TO USE THE INDICATOR

1. Wait for Extreme Events:

The indicator is designed to be selective. Don't trade every fluctuation - wait for tensor to reach >90 or <10. This alone is not a signal.

2. Check Context Scores:

Look at the Bullish Flux vs Bearish Flux in the dashboard. If scores are close (within 1-2 points), the market is indecisive - skip the trade.

3. Confirm with Signals:

Only act when a full triangle signal appears (▲ or ▼). This means ALL your selected confirmation criteria have been met.

4. Use with Price Structure:

Combine with support/resistance levels. A buy signal AT support is higher probability than a buy signal in the middle of nowhere.

5. Respect the Dashboard State:

When State shows "CRITICAL" (⚠), it means extreme pressure exists but direction is unclear. These are the most dangerous moments - wait for resolution.

6. Volume Matters:

Energy particles (dots) and the Mass metric tell you if institutions are participating. Signals without volume confirmation are lower probability.

MARKET AND TIMEFRAME RECOMMENDATIONS

Scalping (1m-5m):

Lookback: 10-14

Smoothing: 5-7

Threshold: 85

Epsilon: 0.5-0.7

Note: Expect more noise. Confirm with Level 2 data. Best on highly liquid instruments.

Intraday (15m-1h):

Lookback: 20-30 (default settings work well)

Smoothing: 3-5

Threshold: 90

Epsilon: 1.0

Note: Sweet spot for the indicator. High win rate on liquid stocks, forex majors, and crypto.

Swing Trading (4h-1D):

Lookback: 30-50

Smoothing: 3

Threshold: 90-95

Epsilon: 1.5-2.0

Note: Signals are rare but high conviction. Combine with higher timeframe trend analysis.

Position Trading (1D-1W):

Lookback: 50-100

Smoothing: 5-7

Threshold: 95

Epsilon: 2.0-3.0

Note: Extremely rare signals. Only trade the most extreme events. Expect massive moves.

Market-Specific Settings:

Forex (EUR/USD, GBP/USD, etc.):

Volume data is unreliable (spot forex has no centralized volume)

Disable "Require Volume Confirmation"

Focus on momentum and trend filters

News events create extreme singularities

Best on 15m-1h timeframes

Stocks (High-Volume Equities):

Volume confirmation is CRITICAL - keep it ON

Works excellently on AAPL, TSLA, SPY, etc.

Morning session (9:30-11:00 ET) shows highest event density

Earnings announcements create guaranteed extreme events

Best on 5m-1h for day trading, 1D for swing trading

Crypto (BTC, ETH, major alts):

Reduce threshold to 85 (crypto has constant high volatility)

Volume spikes are THE primary signal - keep volume confirmation ON

Works exceptionally well due to 24/7 trading and high volatility

Epsilon can be reduced to 0.7-0.8 for more signals

Best on 15m-4h timeframes

Commodities (Gold, Oil, etc.):

Gold responds to macro events (Fed announcements, geopolitical events)

Oil responds to supply shocks

Use daily timeframe minimum

Increase lookback to 50+

These are slow-moving markets - be patient

Indices (SPX, NDX, etc.):

Institutional volume matters - keep volume confirmation ON

Opening hour (9:30-10:30 ET) = highest singularity probability

Strong correlation with VIX - high VIX = more extreme events

Best on 15m-1h for day trading

WHAT MAKES THIS INDICATOR UNIQUE

1. Post-Normalization Sensitivity Control:

Unlike most oscillators where sensitivity controls don't actually work (they're applied before normalization, which then rescales everything), FTS applies epsilon compression AFTER normalization. This means the sensitivity parameter genuinely affects signal frequency. This is a novel implementation not found in standard oscillators.

2. Multi-Factor Confluence Requirement:

The indicator doesn't just detect "overbought" or "oversold" - it detects extreme conditions AND THEN analyzes context through five separate factors (price structure, momentum, trend, acceleration, volume). Most indicators are single-factor; FTS requires confluence.

3. Volatility-Weighted Normalization:

By squaring the ATR ratio (local/global), the indicator adapts to changing market regimes. A 1% move in a low-volatility environment is treated differently than a 1% move in a high-volatility environment. Traditional indicators treat all moves equally regardless of context.

4. Volume Integration at the Core:

Volume isn't an afterthought or optional filter - it's baked into the fundamental equation as "mass." The log transformation handles outliers elegantly while preserving significance. Most price-based indicators completely ignore volume.

5. Adaptive Scoring System:

Rather than fixed buy/sell rules ("RSI >70 = sell"), FTS uses competitive scoring where bullish and bearish evidence compete. The winner determines direction. This solves the classic problem of "overbought markets can stay overbought during strong uptrends."

6. Comprehensive Visual Feedback:

The multi-layer visualization system (accretion disk, field lines, particles, flashes) provides instant intuitive feedback on market state without requiring dashboard reading. You can see pressure building before extreme thresholds are hit.

7. Separate Extreme Detection and Signal Generation:

"Singularity diamonds" show extreme events that don't meet full criteria, while "signal triangles" only appear when ALL conditions are met. This distinction helps traders understand when pressure exists versus when it's actionable.

COMPARISON TO EXISTING INDICATORS

vs. RSI/Stochastic:

These normalize price relative to recent range. FTS normalizes (price change × log volume × volatility ratio) - a composite metric, not just price position.

vs. Chaikin Money Flow:

CMF combines price and volume but lacks volatility context and doesn't use adaptive normalization or post-normalization compression.

vs. Bollinger Bands + Volume:

Bollinger Bands show volatility but don't integrate volume or create a unified oscillator. They're separate components, not synthesized.

vs. MACD:

MACD is pure momentum. FTS combines momentum with volume weighting and volatility context, plus provides a normalized 0-100 scale.

The specific combination of log-volume weighting, squared volatility amplification, post-normalization epsilon compression, and multi-factor directional scoring is unique to this indicator.

LIMITATIONS AND PROPER DISCLOSURE

Not a Holy Grail:

No indicator is perfect. This tool identifies high-probability setups but cannot predict the future. Losses will occur. Use proper risk management.

Requires Confirmation:

Best used in conjunction with price action analysis, support/resistance levels, and higher timeframe trend. Don't trade signals blindly.

Volume Data Dependency:

On forex (spot) and some low-volume instruments, volume data is unreliable or tick-volume only. Disable volume confirmation in these cases.

Lagging Components:

The EMA smoothing and trend filters are inherently lagging. In extremely fast moves, signals may appear after the initial thrust.

Extreme Event Rarity:

With conservative settings (high threshold, high epsilon), signals can be rare. This is by design - quality over quantity. If you need more frequent signals, reduce threshold to 85 and epsilon to 0.7.

Not Financial Advice:

This indicator is an analytical tool. All trading decisions and their consequences are solely your responsibility. Past performance does not guarantee future results.

BEST PRACTICES

Don't trade every singularity - wait for context confirmation

Higher timeframes = higher reliability

Combine with support/resistance for entry refinement

Volume confirmation is CRITICAL for stocks/crypto (toggle off only for forex)

During major news events, singularities are inevitable but direction may be uncertain - use wider stops

When bullish and bearish flux scores are close, skip the trade

Test settings on your specific instrument/timeframe before live trading

Use the dashboard actively - it contains critical diagnostic information

Taking you to school. — Dskyz, Trade with insight. Trade with anticipation.

Bifurcation Zone - CAEBifurcation Zone — Cognitive Adversarial Engine (BZ-CAE)

Bifurcation Zone — CAE (BZ-CAE) is a next-generation divergence detection system enhanced by a Cognitive Adversarial Engine that evaluates both sides of every potential trade before presenting signals. Unlike traditional divergence indicators that show every price-oscillator disagreement regardless of context, BZ-CAE applies comprehensive market-state intelligence to identify only the divergences that occur in favorable conditions with genuine probability edges.

The system identifies structural bifurcation points — critical junctures where price and momentum disagree, signaling potential reversals or continuations — then validates these opportunities through five interconnected intelligence layers: Trend Conviction Scoring , Directional Momentum Alignment , Multi-Factor Exhaustion Modeling , Adversarial Validation , and Confidence Scoring . The result is a selective, context-aware signal system that filters noise and highlights high-probability setups.

This is not a "buy the arrow" indicator. It's a decision support framework that teaches you how to read market state, evaluate divergence quality, and make informed trading decisions based on quantified intelligence rather than hope.

What Sets BZ-CAE Apart: Technical Architecture

The Problem With Traditional Divergence Indicators

Most divergence indicators operate on a simple rule: if price makes a higher high and RSI makes a lower high, show a bearish signal. If price makes a lower low and RSI makes a higher low, show a bullish signal. This creates several critical problems:

Context Blindness : They show counter-trend signals in powerful trends that rarely reverse, leading to repeated losses as you fade momentum.

Signal Spam : Every minor price-oscillator disagreement generates an alert, overwhelming you with low-quality setups and creating analysis paralysis.

No Quality Ranking : All signals are treated identically. A marginal divergence in choppy conditions receives the same visual treatment as a high-conviction setup at a major exhaustion point.

Single-Sided Evaluation : They ask "Is this a good long?" without checking if the short case is overwhelmingly stronger, leading you into obvious bad trades.

Static Configuration : You manually choose RSI 14 or Stochastic 14 and hope it works, with no systematic way to validate if that's optimal for your instrument.

BZ-CAE's Solution: Cognitive Adversarial Intelligence

BZ-CAE solves these problems through an integrated five-layer intelligence architecture:

1. Trend Conviction Score (TCS) — 0 to 1 Scale

Most indicators check if ADX is above 25 to determine "trending" conditions. This binary approach misses nuance. TCS is a weighted composite metric:

Formula : 0.35 × normalize(ADX, 10, 35) + 0.35 × structural_strength + 0.30 × htf_alignment

Structural Strength : 10-bar SMA of consecutive directional bars. Captures persistence — are bulls or bears consistently winning?

HTF Alignment : Multi-timeframe EMA stacking (20/50/100/200). When all EMAs align in the same direction, you're in institutional trend territory.

Purpose : Quantifies how "locked in" the trend is. When TCS exceeds your threshold (default 0.80), the system knows to avoid counter-trend trades unless other factors override.

Interpretation :

TCS > 0.85: Very strong trend — counter-trading is extremely high risk

TCS 0.70-0.85: Strong trend — favor continuation, require exhaustion for reversals

TCS 0.50-0.70: Moderate trend — context matters, both directions viable

TCS < 0.50: Weak/choppy — reversals more viable, range-bound conditions

2. Directional Momentum Alignment (DMA) — ATR-Normalized

Formula : (EMA21 - EMA55) / ATR14

This isn't just "price above EMA" — it's a regime-aware momentum gauge. The same $100 price movement reads completely differently in high-volatility crypto versus low-volatility forex. By normalizing with ATR, DMA adapts its interpretation to current market conditions.

Purpose : Quantifies the directional "force" behind current price action. Positive = bullish push, negative = bearish push. Magnitude = strength.

Interpretation :

DMA > 0.7: Strong bullish momentum — bearish divergences risky

DMA 0.3 to 0.7: Moderate bullish bias

DMA -0.3 to 0.3: Balanced/choppy conditions

DMA -0.7 to -0.3: Moderate bearish bias

DMA < -0.7: Strong bearish momentum — bullish divergences risky

3. Multi-Factor Exhaustion Modeling — 0 to 1 Probability

Single-metric exhaustion detection (like "RSI > 80") misses complex market states. BZ-CAE aggregates five independent exhaustion signals:

Volume Spikes : Current volume versus 50-bar average

2.5x average: 0.25 weight

2.0x average: 0.15 weight

1.5x average: 0.10 weight

Divergence Present : The fact that a divergence exists contributes 0.30 weight — structural momentum disagreement is itself an exhaustion signal.

RSI Extremes : Captures oscillator climax zones

RSI > 80 or < 20: 0.25 weight

RSI > 75 or < 25: 0.15 weight

Pin Bar Detection : Identifies rejection candles (2:1 wick-to-body ratio, indicating failed breakout attempts): 0.15 weight

Extended Runs : Consecutive bars above/below EMA20 without pullback

30+ bars: 0.15 weight (market hasn't paused to consolidate)

Total exhaustion score is the sum of all applicable weights, capped at 1.0.

Purpose : Detects when strong trends become vulnerable to reversal. High exhaustion can override trend filters, allowing counter-trend trades at genuine turning points that basic indicators would miss.

Interpretation :

Exhaustion > 0.75: High probability of climax — yellow background shading alerts you visually

Exhaustion 0.50-0.75: Moderate overextension — watch for confirmation

Exhaustion < 0.50: Fresh move — trend can continue, counter-trend trades higher risk

4. Adversarial Validation — Game Theory Applied to Trading

This is BZ-CAE's signature innovation. Before approving any signal, the engine quantifies BOTH sides of the trade simultaneously:

For Bullish Divergences , it calculates:

Bull Case Score (0-1+) :

Distance below EMA20 (pullback quality): up to 0.25

Bullish EMA alignment (close > EMA20 > EMA50): 0.25

Oversold RSI (< 40): 0.25

Volume confirmation (> 1.2x average): 0.25

Bear Case Score (0-1+) :

Price below EMA50 (structural weakness): 0.30

Very oversold RSI (< 30, indicating knife-catching): 0.20

Differential = Bull Case - Bear Case

If differential < -0.10 (default threshold), the bear case is dominating — signal is BLOCKED or ANNOTATED.

For Bearish Divergences , the logic inverts (Bear Case vs Bull Case).

Purpose : Prevents trades where you're fighting obvious strength in the opposite direction. This is institutional-grade risk management — don't just evaluate your trade, evaluate the counter-trade simultaneously.

Why This Matters : You might see a bullish divergence at a local low, but if price is deeply below major support EMAs with strong bearish momentum, you're catching a falling knife. The adversarial check catches this and blocks the signal.

5. Confidence Scoring — 0 to 1 Quality Assessment

Every signal that passes initial filters receives a comprehensive quality score:

Formula :

0.30 × normalize(TCS) // Trend context

+ 0.25 × normalize(|DMA|) // Momentum magnitude

+ 0.20 × pullback_quality // Entry distance from EMA20

+ 0.15 × state_quality // ADX + alignment + structure

+ 0.10 × divergence_strength // Slope separation magnitude

+ adversarial_bonus (0-0.30) // Your side's advantage

Purpose : Ranks setup quality for filtering and position sizing decisions. You can set a minimum confidence threshold (default 0.35) to ensure only quality setups reach your chart.

Interpretation :

Confidence > 0.70: Premium setup — consider increased position size

Confidence 0.50-0.70: Good quality — standard size

Confidence 0.35-0.50: Acceptable — reduced size or skip if conservative

Confidence < 0.35: Marginal — blocked in Filtering mode, annotated in Advisory mode

CAE Operating Modes: Learning vs Enforcement

Off : Disables all CAE logic. Raw divergence pipeline only. Use for baseline comparison.

Advisory : Shows ALL signals regardless of CAE evaluation, but annotates signals that WOULD be blocked with specific warnings (e.g., "Bull: strong downtrend (TCS=0.87)" or "Adversarial bearish"). This is your learning mode — see CAE's decision logic in action without missing educational opportunities.

Filtering : Actively blocks low-quality signals. Only setups that pass all enabled gates (Trend Filter, Adversarial Validation, Confidence Gating) reach your chart. This is your live trading mode — trust the system to enforce discipline.

CAE Filter Gates: Three-Layer Protection

When CAE is enabled, signals must pass through three independent gates (each can be toggled on/off):

Gate 1: Strong Trend Filter

If TCS ≥ tcs_threshold (default 0.80)

And signal is counter-trend (bullish in downtrend or bearish in uptrend)

And exhaustion < exhaustion_required (default 0.50)

Then: BLOCK signal

Logic: Don't fade strong trends unless the move is clearly overextended

Gate 2: Adversarial Validation

Calculate both bull case and bear case scores

If opposing case dominates by more than adv_threshold (default 0.10)

Then: BLOCK signal

Logic: Avoid trades where you're fighting obvious strength in the opposite direction

Gate 3: Confidence Gating

Calculate composite confidence score (0-1)

If confidence < min_confidence (default 0.35)

Then: In Filtering mode, BLOCK signal; in Advisory mode, ANNOTATE with warning

Logic: Only take setups with minimum quality threshold

All three gates work together. A signal must pass ALL enabled gates to fire.

Visual Intelligence System

Bifurcation Zones (Supply/Demand Blocks)

When a divergence signal fires, BZ-CAE draws a semi-transparent box extending 15 bars forward from the signal pivot:

Demand Zones (Bullish) : Theme-colored box (cyan in Cyberpunk, blue in Professional, etc.) labeled "Demand" — marks where smart money likely placed buy orders as price diverged at the low.

Supply Zones (Bearish) : Theme-colored box (magenta in Cyberpunk, orange in Professional) labeled "Supply" — marks where smart money likely placed sell orders as price diverged at the high.

Theory : Divergences represent institutional disagreement with the crowd. The crowd pushed price to an extreme (new high or low), but momentum (oscillator) is waning, indicating smart money is taking the opposite side. These zones mark order placement areas that become future support/resistance.

Use Cases :

Exit targets: Take profit when price returns to opposite-side zone

Re-entry levels: If price returns to your entry zone, consider adding

Stop placement: Place stops just beyond your zone (below demand, above supply)

Auto-Cleanup : System keeps the last 20 zones to prevent chart clutter.

Adversarial Bar Coloring — Real-Time Market Debate Heatmap

Each bar is colored based on the Bull Case vs Bear Case differential:

Strong Bull Advantage (diff > 0.3): Full theme bull color (e.g., cyan)

Moderate Bull Advantage (diff > 0.1): 50% transparency bull

Neutral (diff -0.1 to 0.1): Gray/neutral theme

Moderate Bear Advantage (diff < -0.1): 50% transparency bear

Strong Bear Advantage (diff < -0.3): Full theme bear color (e.g., magenta)

This creates a real-time visual heatmap showing which side is "winning" the market debate. When bars flip from cyan to magenta (or vice versa), you're witnessing a shift in adversarial advantage — a leading indicator of potential momentum changes.

Exhaustion Shading

When exhaustion score exceeds 0.75, the chart background displays a semi-transparent yellow highlight. This immediate visual warning alerts you that the current move is at high risk of reversal, even if trend indicators remain strong.

Visual Themes — Six Aesthetic Options

Cyberpunk : Cyan/Magenta/Yellow — High contrast, neon aesthetic, excellent for dark-themed trading environments

Professional : Blue/Orange/Green — Corporate color palette, suitable for presentations and professional documentation

Ocean : Teal/Red/Cyan — Aquatic palette, calming for extended monitoring sessions

Fire : Orange/Red/Coral — Warm aggressive colors, high energy

Matrix : Green/Red/Lime — Code aesthetic, homage to classic hacker visuals

Monochrome : White/Gray — Minimal distraction, maximum focus on price action

All visual elements (signal markers, zones, bar colors, dashboard) adapt to your selected theme.

Divergence Engine — Core Detection System

What Are Divergences?

Divergences occur when price action and momentum indicators disagree, creating structural tension that often resolves in a change of direction:

Regular Divergence (Reversal Signal) :

Bearish Regular : Price makes higher high, oscillator makes lower high → Potential trend reversal down

Bullish Regular : Price makes lower low, oscillator makes higher low → Potential trend reversal up

Hidden Divergence (Continuation Signal) :

Bearish Hidden : Price makes lower high, oscillator makes higher high → Downtrend continuation

Bullish Hidden : Price makes higher low, oscillator makes lower low → Uptrend continuation

Both types can be enabled/disabled independently in settings.

Pivot Detection Methods

BZ-CAE uses symmetric pivot detection with separate lookback and lookforward periods (default 5/5):

Pivot High : Bar where high > all highs within lookback range AND high > all highs within lookforward range

Pivot Low : Bar where low < all lows within lookback range AND low < all lows within lookforward range

This ensures structural validity — the pivot must be a clear local extreme, not just a minor wiggle.

Divergence Validation Requirements

For a divergence to be confirmed, it must satisfy:

Slope Disagreement : Price slope and oscillator slope must move in opposite directions (for regular divs) or same direction with inverted highs/lows (for hidden divs)

Minimum Slope Change : |osc_slope| > min_slope_change / 100 (default 1.0) — filters weak, marginal divergences

Maximum Lookback Range : Pivots must be within max_lookback bars (default 60) — prevents ancient, irrelevant divergences

ATR-Normalized Strength : Divergence strength = min(|price_slope| × |osc_slope| × 10, 1.0) — quantifies the magnitude of disagreement in volatility context

Regular divergences receive 1.0× weight; hidden divergences receive 0.8× weight (slightly less reliable historically).

Oscillator Options — Five Professional Indicators

RSI (Relative Strength Index) : Classic overbought/oversold momentum indicator. Best for: General purpose divergence detection across all instruments.

Stochastic : Range-bound %K momentum comparing close to high-low range. Best for: Mean reversion strategies and range-bound markets.

CCI (Commodity Channel Index) : Measures deviation from statistical mean, auto-normalized to 0-100 scale. Best for: Cyclical instruments and commodities.

MFI (Money Flow Index) : Volume-weighted RSI incorporating money flow. Best for: Volume-driven markets like stocks and crypto.

Williams %R : Inverse stochastic looking back over period, auto-adjusted to 0-100. Best for: Reversal detection at extremes.

Each oscillator has adjustable length (2-200, default 14) and smoothing (1-20, default 1). You also set overbought (50-100, default 70) and oversold (0-50, default 30) thresholds.

Signal Timing Modes — Understanding Repainting

BZ-CAE offers two timing policies with complete transparency about repainting behavior:

Realtime (1-bar, peak-anchored)

How It Works :

Detects peaks 1 bar ago using pattern: high > high AND high > high

Signal prints on the NEXT bar after peak detection (bar_index)

Visual marker anchors to the actual PEAK bar (bar_index - 1, offset -1)

Signal locks in when bar CONFIRMS (closes)

Repainting Behavior :

On the FORMING bar (before close), the peak condition may change as new prices arrive

Once bar CLOSES (barstate.isconfirmed), signal is locked permanently

This is preview/early warning behavior by design

Best For :

Active monitoring and immediate alerts

Learning the system (seeing signals develop in real-time)

Responsive entry if you're watching the chart live

Confirmed (lookforward)

How It Works :

Uses Pine Script's built-in ta.pivothigh() and ta.pivotlow() functions

Requires full pivot validation period (lookback + lookforward bars)

Signal prints pivot_lookforward bars after the actual peak (default 5-bar delay)

Visual marker anchors to the actual peak bar (offset -pivot_lookforward)

No Repainting Behavior

Best For :

Backtesting and historical analysis

Conservative entries requiring full confirmation

Automated trading systems

Swing trading with larger timeframes

Tradeoff :

Delayed entry by pivot_lookforward bars (typically 5 bars)

On a 5-minute chart, this is a 25-minute delay

On a 4-hour chart, this is a 20-hour delay

Recommendation : Use Confirmed for backtesting to verify system performance honestly. Use Realtime for live monitoring only if you're actively watching the chart and understand pre-confirmation repainting behavior.

Signal Spacing System — Anti-Spam Architecture

Even after CAE filtering, raw divergences can cluster. The spacing system enforces separation:

Three Independent Filters

1. Min Bars Between ANY Signals (default 12):

Prevents rapid-fire clustering across both directions

If last signal (bull or bear) was within N bars, block new signal

Ensures breathing room between all setups

2. Min Bars Between SAME-SIDE Signals (default 24, optional enforcement):

Prevents bull-bull or bear-bear spam

Separate tracking for bullish and bearish signal timelines

Toggle enforcement on/off

3. Min ATR Distance From Last Signal (default 0, optional):

Requires price to move N × ATR from last signal location

Ensures meaningful price movement between setups

0 = disabled, 0.5-2.0 = typical range for enabled

All three filters work independently. A signal must pass ALL enabled filters to proceed.

Practical Guidance :

Scalping (1-5m) : Any 6-10, Same-side 12-20, ATR 0-0.5

Day Trading (15m-1H) : Any 12, Same-side 24, ATR 0-1.0

Swing Trading (4H-D) : Any 20-30, Same-side 40-60, ATR 1.0-2.0

Dashboard — Real-Time Control Center

The dashboard (toggleable, four corner positions, three sizes) provides comprehensive system intelligence:

Oscillator Section

Current oscillator type and value

State: OVERBOUGHT / OVERSOLD / NEUTRAL (color-coded)

Length parameter

Cognitive Engine Section

TCS (Trend Conviction Score) :

Current value with emoji state indicator

🔥 = Strong trend (>0.75)

📊 = Moderate trend (0.50-0.75)

〰️ = Weak/choppy (<0.50)

Color: Red if above threshold (trend filter active), yellow if moderate, green if weak

DMA (Directional Momentum Alignment) :

Current value with emoji direction indicator

🐂 = Bullish momentum (>0.5)

⚖️ = Balanced (-0.5 to 0.5)

🐻 = Bearish momentum (<-0.5)

Color: Green if bullish, red if bearish

Exhaustion :

Current value with emoji warning indicator

⚠️ = High exhaustion (>0.75)

🟡 = Moderate (0.50-0.75)

✓ = Low (<0.50)

Color: Red if high, yellow if moderate, green if low

Pullback :

Quality of current distance from EMA20

Values >0.6 are ideal entry zones (not too close, not too far)

Bull Case / Bear Case (if Adversarial enabled):

Current scores for both sides of the market debate

Differential with emoji indicator:

📈 = Bull advantage (>0.2)

➡️ = Balanced (-0.2 to 0.2)

📉 = Bear advantage (<-0.2)

Last Signal Metrics Section (New Feature)

When a signal fires, this section captures and displays:

Signal type (BULL or BEAR)

Bars elapsed since signal

Confidence % at time of signal

TCS value at signal time

DMA value at signal time

Purpose : Provides a historical reference for learning. You can see what the market state looked like when the last signal fired, helping you correlate outcomes with conditions.

Statistics Section

Total Signals : Lifetime count across session

Blocked Signals : Count and percentage (filter effectiveness metric)

Bull Signals : Total bullish divergences

Bear Signals : Total bearish divergences

Purpose : System health monitoring. If blocked % is very high (>60%), filters may be too strict. If very low (<10%), filters may be too loose.

Advisory Annotations

When CAE Mode = Advisory, this section displays warnings for signals that would be blocked in Filtering mode:

Examples:

"Bull spacing: wait 8 bars"

"Bear: strong uptrend (TCS=0.87)"

"Adversarial bearish"

"Low confidence 32%"

Multiple warnings can stack, separated by " | ". This teaches you CAE's decision logic transparently.

How to Use BZ-CAE — Complete Workflow

Phase 1: Initial Setup (First Session)

Apply BZ-CAE to your chart

Select your preferred Visual Theme (Cyberpunk recommended for visibility)

Set Signal Timing to "Confirmed (lookforward)" for learning

Choose your Oscillator Type (RSI recommended for general use, length 14)

Set Overbought/Oversold to 70/30 (standard)

Enable both Regular Divergence and Hidden Divergence

Set Pivot Lookback/Lookforward to 5/5 (balanced structure)

Enable CAE Intelligence

Set CAE Mode to "Advisory" (learning mode)

Enable all three CAE filters: Strong Trend Filter , Adversarial Validation , Confidence Gating

Enable Show Dashboard , position Top Right, size Normal

Enable Draw Bifurcation Zones and Adversarial Bar Coloring

Phase 2: Learning Period (Weeks 1-2)

Goal : Understand how CAE evaluates market state and filters signals.

Activities :

Watch the dashboard during signals :

Note TCS values when counter-trend signals fail — this teaches you the trend strength threshold for your instrument

Observe exhaustion patterns at actual turning points — learn when overextension truly matters

Study adversarial differential at signal times — see when opposing cases dominate

Review blocked signals (orange X-crosses):

In Advisory mode, you see everything — signals that would pass AND signals that would be blocked

Check the advisory annotations to understand why CAE would block

Track outcomes: Were the blocks correct? Did those signals fail?

Use Last Signal Metrics :

After each signal, check the dashboard capture of confidence, TCS, and DMA

Journal these values alongside trade outcomes

Identify patterns: Do confidence >0.70 signals work better? Does your instrument respect TCS >0.85?

Understand your instrument's "personality" :

Trending instruments (indices, major forex) may need TCS threshold 0.85-0.90

Choppy instruments (low-cap stocks, exotic pairs) may work best with TCS 0.70-0.75

High-volatility instruments (crypto) may need wider spacing

Low-volatility instruments may need tighter spacing

Phase 3: Calibration (Weeks 3-4)

Goal : Optimize settings for your specific instrument, timeframe, and style.

Calibration Checklist :

Min Confidence Threshold :

Review confidence distribution in your signal journal

Identify the confidence level below which signals consistently fail

Set min_confidence slightly above that level

Day trading : 0.35-0.45

Swing trading : 0.40-0.55

Scalping : 0.30-0.40

TCS Threshold :

Find the TCS level where counter-trend signals consistently get stopped out

Set tcs_threshold at or slightly below that level

Trending instruments : 0.85-0.90

Mixed instruments : 0.80-0.85

Choppy instruments : 0.75-0.80

Exhaustion Override Level :

Identify exhaustion readings that marked genuine reversals

Set exhaustion_required just below the average

Typical range : 0.45-0.55

Adversarial Threshold :

Default 0.10 works for most instruments

If you find CAE is too conservative (blocking good trades), raise to 0.15-0.20

If signals are still getting caught in opposing momentum, lower to 0.07-0.09

Spacing Parameters :

Count bars between quality signals in your journal

Set min bars ANY to ~60% of that average

Set min bars SAME-SIDE to ~120% of that average

Scalping : Any 6-10, Same 12-20

Day trading : Any 12, Same 24

Swing : Any 20-30, Same 40-60

Oscillator Selection :

Try different oscillators for 1-2 weeks each

Track win rate and average winner/loser by oscillator type

RSI : Best for general use, clear OB/OS

Stochastic : Best for range-bound, mean reversion

MFI : Best for volume-driven markets

CCI : Best for cyclical instruments

Williams %R : Best for reversal detection

Phase 4: Live Deployment

Goal : Disciplined execution with proven, calibrated system.

Settings Changes :

Switch CAE Mode from Advisory to Filtering

System now actively blocks low-quality signals

Only setups passing all gates reach your chart

Keep Signal Timing on Confirmed for conservative entries

OR switch to Realtime if you're actively monitoring and want faster entries (accept pre-confirmation repaint risk)

Use your calibrated thresholds from Phase 3

Enable high-confidence alerts: "⭐ High Confidence Bullish/Bearish" (>0.70)

Trading Discipline Rules :

Respect Blocked Signals :

If CAE blocks a trade you wanted to take, TRUST THE SYSTEM

Don't manually override — if you consistently disagree, return to Phase 2/3 calibration

The block exists because market state failed intelligence checks

Confidence-Based Position Sizing :

Confidence >0.70: Standard or increased size (e.g., 1.5-2.0% risk)

Confidence 0.50-0.70: Standard size (e.g., 1.0% risk)

Confidence 0.35-0.50: Reduced size (e.g., 0.5% risk) or skip if conservative

TCS-Based Management :

High TCS + counter-trend signal: Use tight stops, quick exits (you're fading momentum)

Low TCS + reversal signal: Use wider stops, trail aggressively (genuine reversal potential)

Exhaustion Awareness :

Exhaustion >0.75 (yellow shading): Market is overextended, reversal risk is elevated — consider early exit or tighter trailing stops even on winning trades

Exhaustion <0.30: Continuation bias — hold for larger move, wide trailing stops

Adversarial Context :

Strong differential against you (e.g., bullish signal with bear diff <-0.2): Use very tight stops, consider skipping

Strong differential with you (e.g., bullish signal with bull diff >0.2): Trail aggressively, this is your tailwind

Practical Settings by Timeframe & Style

Scalping (1-5 Minute Charts)

Objective : High frequency, tight stops, quick reversals in fast-moving markets.

Oscillator :

Type: RSI or Stochastic (fast response to quick moves)

Length: 9-11 (more responsive than standard 14)

Smoothing: 1 (no lag)

OB/OS: 65/35 (looser thresholds ensure frequent crossings in fast conditions)

Divergence :

Pivot Lookback/Lookforward: 3/3 (tight structure, catch small swings)

Max Lookback: 40-50 bars (recent structure only)

Min Slope Change: 0.8-1.0 (don't be overly strict)

CAE :

Mode: Advisory first (learn), then Filtering

Min Confidence: 0.30-0.35 (lower bar for speed, accept more signals)

TCS Threshold: 0.70-0.75 (allow more counter-trend opportunities)

Exhaustion Required: 0.45-0.50 (moderate override)

Strong Trend Filter: ON (still respect major intraday trends)

Adversarial: ON (critical for scalping protection — catches bad entries quickly)

Spacing :

Min Bars ANY: 6-10 (fast pace, many setups)

Min Bars SAME-SIDE: 12-20 (prevent clustering)

Min ATR Distance: 0 or 0.5 (loose)

Timing : Realtime (speed over precision, but understand repaint risk)

Visuals :

Signal Size: Tiny (chart clarity in busy conditions)

Show Zones: Optional (can clutter on low timeframes)

Bar Coloring: ON (helps read momentum shifts quickly)

Dashboard: Small size (corner reference, not main focus)

Key Consideration : Scalping generates noise. Even with CAE, expect lower win rate (45-55%) but aim for favorable R:R (2:1 or better). Size conservatively.

Day Trading (15-Minute to 1-Hour Charts)