NeuralFlow Forecast Levels | SPY WeeklyThis is a companion script that plots AI-adaptive market equilibrium & expansion mapping levels for SPY on chart.

NeuralFlow Forecast levels are generated though a Artificial Intelligence framework trained to identify where price is statistically inclined to re-balance and where expansion zones historically exhaust rather than extend.

What the Bands Represent

Band Layer Meaning

AI Equilibrium (white core) Primary weekly balance zone where price is most likely to mean-revert

Predictive Rails (aqua / purple) High-confidence corridor of institutional flow containment

Outer Zones (green / red) Expansion limits where continuation historically decays

Extreme Zones (top/bottom) Rare deviation envelope where auction completion is statistically favored

NeuralFlow operates Artificial Intelligence models trained specifically to map statistical re-balancing behavior, not trader predictions or sentiment. No discretionary drawing. No correlations. No lagging overlays.

This engine updates only when underlying structure changes — not when candles fluctuate intraday.

Risk:

Educational & analytical use only. Not financial advice

Cerca negli script per "spy"

RightFlow Universal Volume Profile - Any Market Any TimeframeSummary in one paragraph

RightFlow is a right anchored microstructure volume profile for stocks, futures, FX, and liquid crypto on intraday and daily timeframes. It acts only when several conditions align inside a session window and presents the result as a compact right side profile with value area, POC, a bull bear mix by price bin, and a HUD of profile VWAP and pressure shares. It is original because it distributes each bar’s weight into multiple mid price slices, blends bull bear pressure per bin with a CLV based split, and grows the profile to the right so price action stays readable. Add to a clean chart, read the table, and use the visuals. For conservative workflows read on bar close.

Scope and intent

• Markets. Major FX pairs, index futures, large cap equities and ETFs, liquid crypto.

• Timeframes. One minute to daily.

• Default demo used in the publication. SPY on 15 minute.

• Purpose. See where participation concentrates, which side dominated by price level, and how far price sits from VA and POC.

Originality and usefulness

• Unique fusion. Right anchored growth plus per bar slicing and CLV split, with weight modes Raw, Notional, and DeltaProxy.

• Failure mode addressed. False reads from single bar direction and coarse binning.

• Testability. All parts sit in Inputs and the HUD.

• Portable yardstick. Value Area percent and POC are universal across symbols.

• Protected scripts. Not applicable. Method and use are fully disclosed.

Method overview in plain language

Pick a scope Rolling or Today or This Week. Define a window and number of price bins. For each bar, split its range into small slices, assign each slice a weight from the selected mode, and split that weight by CLV or by bar direction. Accumulate totals per bin. Find the bin with the highest total as POC. Expand left and right until the chosen share of total volume is covered to form the value area. Compute profile VWAP for all, buyers, and sellers and show them with pressure shares.

Base measures

Range basis. High minus low and mid price samples across the bar window.

Return basis. Not used. VWAP trio is price weighted by weights.

Components

• RightFlow Bins. Price histogram that grows to the right.

• Bull Bear Split. CLV based 0 to 1 share or pure bar direction.

• Weight Mode. Raw volume, notional volume times close, or DeltaProxy focus.

• Value Area Engine. POC then outward expansion to target share.

• HUD. Profile VWAP, Buy and Sell percent, winner delta, split and weight mode.

• Session windows optional. Scope resets on day or week.

Fusion rule

Color of each bin is the convex blend of bull and bear shares. Value area shading is lighter inside and darker outside.

Signal rule

This is context, not a trade signal. A strong separation between buy and sell percent with price holding inside VA often confirms balance. Price outside VA with skewed pressure often marks initiative moves.

What you will see on the chart

• Right side bins with blended colors.

• A POC line across the profile width.

• Labels for POC, VAH, and VAL.

• A compact HUD table in the top right.

Table fields and quick reading guide

• VWAP. Profile VWAP.

• Buy and Sell. Pressure shares in percent.

• Delta Winner. Winner side and margin in percent.

• Split and Weight. The active modes.

Reading tip. When Session scope is Today or This Week and Buy minus Sell is clearly positive or negative, that side often controls the day’s narrative.

Inputs with guidance

Setup

• Profile scope. Rolling or session reset. Rolling uses window bars.

• Rolling window bars. Typical 100 to 300. Larger is smoother.

Binning

• Price bins. Typical 32 to 128. More bins increase detail.

• Slices per bar. Typical 3 to 7. Raising it smooths distribution.

Weighting

• Weight mode. Raw, Notional, DeltaProxy. Notional emphasizes expensive prints.

• Bull Bear split. CLV or BarDir. CLV is more nuanced.

• Value Area percent. Typical 68 to 75.

View

• Profile width in bars, color split toggle, value area shading, opacities, POC line, VA labels.

Usage recipes

Intraday trend focus

• Scope Today, bins 64, slices 5, Value Area 70.

• Split CLV, Weight Notional.

Intraday mean reversion

• Scope Today, bins 96, Value Area 75.

• Watch fades back to POC after initiative pushes.

Swing continuation

• Scope Rolling 200 bars, bins 48.

• Use Buy Sell skew with price relative to VA.

Realism and responsible publication

No performance claims. Shapes can move while a bar forms and settle on close. Education only.

Honest limitations and failure modes

Thin liquidity and data gaps can distort bin weights. Very quiet regimes reduce contrast. Session time is the chart venue time.

Open source reuse and credits

None.

Legal

Education and research only. Not investment advice. Test on history and simulation before live use.

FluxVector Liquidity Universal Trendline FluxVector Liquidity Trendline FFTL

Summary in one paragraph

FFTL is a single adaptive trendline for stocks ETFs FX crypto and indices on one minute to daily. It fires only when price action pressure and volatility curvature align. It is original because it fuses a directional liquidity pulse from candle geometry and normalized volume with realized volatility curvature and an impact efficiency term to modulate a Kalman like state without ATR VWAP or moving averages. Add it to a clean chart and use the colored line plus alerts. Shapes can move while a bar is open and settle on close. For conservative alerts select on bar close.

Scope and intent

• Markets. Major FX pairs index futures large cap equities liquid crypto top ETFs

• Timeframes. One minute to daily

• Default demo used in the publication. SPY on 30min

• Purpose. Reduce false flips and chop by gating the line reaction to noise and by using a one bar projection

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique fusion. Directional Liquidity Pulse plus Volatility Curvature plus Impact Efficiency drives an adaptive gain for a one dimensional state

• Failure mode addressed. One or two shock candles that break ordinary trendlines and saw chop in flat regimes

• Testability. All windows and gains are inputs

• Portable yardstick. Returns use natural log units and range is bar high minus low

• Protected scripts. Not used. Method disclosed plainly here

Method overview in plain language

Base measures

• Return basis. Natural log of close over prior close. Average absolute return over a window is a unit of motion

Components

• Directional Liquidity Pulse DLP. Measures signed participation from body and wick imbalance scaled by normalized volume and variance stabilized

• Volatility Curvature. Second difference of realized volatility from returns highlights expansion or compression

• Impact Efficiency. Price change per unit range and volume boosts gain during efficient moves

• Energy score. Z scores of the above form a single energy that controls the state gain

• One bar projection. Current slope extended by one bar for anticipatory checks

Fusion rule

Weighted sum inside the energy score then logistic mapping to a gain between k min and k max. The state updates toward price plus a small flow push.

Signal rule

• Long suggestion and order when close is below trend and the one bar projection is above the trend

• Short suggestion and flip when close is above trend and the one bar projection is below the trend

• WAIT is implicit when neither condition holds

• In position states end on the opposite condition

What you will see on the chart

• Colored trendline teal for rising red for falling gray for flat

• Optional projection line one bar ahead

• Optional background can be enabled in code

• Alerts on price cross and on slope flips

Inputs with guidance

Setup

• Price source. Close by default

Logic

• Flow window. Typical range 20 to 80. Higher smooths the pulse and reduces flips

• Vol window. Typical range 30 to 120. Higher calms curvature

• Energy window. Typical range 20 to 80. Higher slows regime changes

• Min gain and Max gain. Raise max to react faster. Raise min to keep momentum in chop

UI

• Show 1 bar projection. Colors for up down flat

Properties visible in this publication

• Initial capital 25000

• Base currency USD

• Commission percent 0.03

• Slippage 5

• Default order size method percent of equity value 3%

• Pyramiding 0

• Process orders on close off

• Calc on every tick off

• Recalculate after order is filled off

Realism and responsible publication

• No performance claims

• Intrabar reminder. Shapes can move while a bar forms and settle on close

• Strategy uses standard candles only

Honest limitations and failure modes

• Sudden gaps and thin liquidity can still produce fast flips

• Very quiet regimes reduce contrast. Use larger windows and lower max gain

• Session time uses the exchange time of the chart if you enable any windows later

• Past results never guarantee future outcomes

Open source reuse and credits

• None

QQQ Ladder → Adjusted to Active Ticker (5s & 10s)This indicator allows you to a grid of QQQ levels directly on futures chart like NQ, MNQ, ES and MES, automatically adjusting for the spread between the displayed symbol and QQQ. This is particularly useful for traders who perform technical analysis on QQQ but execute trades on Futures.

Features:

Renders every 5 and 10 points steps of QQQ in your current chart.

The script adjusts these levels in real-time based on the current spread between QQQ and the displayed symbol!

Plots updated horizontal lines that move with the spread

Supports Multiple Tickers, ES1!, MES1!, NQ1!, MNQ1! SPY and SPX500USD.

SPX Ladder → Adjusted to Active Ticker (5s & 10s)This indicator allows you to a grid of SPX levels directly on the ES1! (E-mini S&P 500 Futures) chart, automatically adjusting for the spread between SPX and ES1!. This is particularly useful for traders who perform technical analysis on SPX but execute trades on ES1!.

Features:

Renders every 5 and 10 points steps of the SPX in your current chart.

The script adjusts these levels in real-time based on the current spread between SPX and ES1!

Plots updated horizontal lines that move with the spread

Supports Multiple Tickers, ES1!, SPY and SPX500USD.

Ideal for futures traders who want SPX context while trading ES1!.

200 SMA (5%/-3% Buffer) for SPY & QQQ In my testing TQQQ is an absolute monster of an ETF that performs extremely well even from a buy and hold standpoint over long periods of time, its largest drawback is the massive drawdown exposure that it faces which can be easily sidestepped with this strategy.

This strategy is meant to basically abuse TQQQ's insane outperformance while augmenting the typical 200SMA strategy in a way that uses all of its strengths while avoiding getting whipsawed in sideways markets.

The strategy BUYS when price crosses 5% over the 200SMA and then SELLS when price drops 3% below the 200SMA. Between trades I'll be parking my entire account in SGOV.

So maximizing profit while minimizing risk.

You use the strategy based off of QQQ and then make the trades on TQQQ when it tells you to BUY/SELL.

Here are some reasons why I will be using this strategy:

Simple emotionless BUY and SELL signals where I don't care who the president is, what is happening in the world, who is bombing who, who the leadership team is, no attachment to individual companies and diversified across the NASDAQ.

~85% win percentage and when it does lose the loses are nothing compared to the wins and after a loss you're basically set up for a massive win in the next trade.

Max drawdown of around 53% when using TQQQ

You benefit massively when the market is doing well and when there is a recession you basically sit in SGOV for a year and then are set up for a monster recovery with a clear easy BUY signal. So as long as you're patient you win regardless of what happens.

The trades are often very long term resulting in you taking advantage of Long Term Capital Gains tax advantage which could mean saving up to 15-20% in taxes.

With only a few trades you can spend time doing other stuff and don't have to track or pay attention to anything that is happening.

Simple, easy, and massively profitable.

SPX Levels Adjusted to Active TickerThis indicator allows you to plot custom SPX levels directly on the ES1! (E-mini S&P 500 Futures) chart, automatically adjusting for the spread between SPX and ES1!. This is particularly useful for traders who perform technical analysis on SPX but execute trades on ES1!.

Features:

Input up to three SPX key levels to track (e.g., 5000, 4950, 4900)

The script adjusts these levels in real-time based on the current spread between SPX and ES1!

Displays the spread in the chart header for quick reference

Plots updated horizontal lines that move with the spread

Includes optional labels showing the spread periodically to reduce clutter

Supports Multiple Tickers, ES1!, SPY and SPX500USD.

Ideal for futures traders who want SPX context while trading ES1!.

Market Strength Buy Sell Indicator [TradeDots]A specialized tool designed to assist traders in evaluating market conditions through a multifaceted analysis of relative performance, beta-adjusted returns, momentum, and volume—allowing you to identify optimal points for long or short trades. By integrating multiple benchmarks (default S&P 500) and percentile-based thresholds, the script provides clear, actionable insights suitable for both day trading and higher-level timeframe assessments.

📝 HOW IT WORKS

1. Multi-Factor Composite Score

Relative Performance (RS Ratio): Compares your asset’s performance to a chosen benchmark (default: SPY). Values above 1.0 indicate outperformance, while below 1.0 suggest underperformance.

Beta-Adjusted Returns: Checks the ticker’s excess movement relative to expected market-related moves. This helps distinguish pure “alpha” from broad market effects.

Volume & Correlation: Volume spikes often confirm the momentum behind a move, while correlation measures how closely the asset tracks or diverges from its benchmark.

These components merge into a 0–100 composite score. Scores above 50 frequently imply bullish strength; drops below 50 often point to underperformance—potentially flagging short opportunities.

2. Intraday & Day Trading Focus

Monitoring Below 50: During the trading day, the script calculates live data against the benchmark, offering an intraday-sensitive composite score. A dip under 50 may indicate a short bias for that session, especially when accompanied by high volume or momentum shifts.

3. Higher Timeframe Monitoring

Daily Strategies: On daily or weekly charts, the script reveals overall relative strength or weakness compared to the S&P 500. This higher-level perspective helps form broader trading biases—crucial for swing or position trades spanning multiple days.

Long/Short Thresholds: Persistent readings above 50 on a daily chart typically reinforce a long bias, while consistent dips below 50 can sustain a short or cautious outlook.

4. Pair Trading Applications

Custom Benchmark Selection: By setting a specific ticker pair as your benchmark instead of the default S&P 500, you can identify spread trading opportunities between two correlated assets. This allows you to go long the outperforming asset while shorting the underperforming one when the spread reaches extreme levels.

4. Color-Coded Signals & Alerts

Visual Zones (25–75): Color-coded bands highlight strong outperformance (above 75) or pronounced underperformance (below 25).

Alerts on Strong Shifts: Automatic alerts can notify you of sudden entries or exits from bullish or bearish zones, so you can potentially act on new market information without delay.

⚙️ HOW TO USE

1. Select Your Timeframe: For scalping or day trading, lower intervals (e.g., 5-minute) offer immediate data resets at the session’s start. For multi-day insight, daily or weekly charts reveal broader performance trends.

2. Watch Key Levels Around 50: Intraday dips under 50 may be a cue to consider short trades, while bounces above 50 can confirm renewed strength.

3. Assess Benchmark Relationships: Compare your asset’s score and signals to the broader market. A stock falling below its pair’s relative strength line might lag overall market momentum.

4. Combine Tools & Validate: This script excels when integrated with other technical analysis methods (e.g., support/resistance, chart patterns) and fundamental factors for a holistic market view.

❗ LIMITATIONS

No Direction Guarantee: The indicator identifies relative strength but does not guarantee directional price moves.

Delayed Updates: Since calculations update after each bar close, sudden intrabar changes may not immediately reflect.

Market-Specific Behaviors: Some assets or unusual market conditions may deviate from typical benchmarks, weakening signal reliability.

Past ≠ Future: High or low relative strength in the past may not predict continued performance.

RISK DISCLAIMER

All forms of trading and investing involve risk, including the possible loss of principal. This indicator analyzes relative performance but cannot assure profits or eliminate losses. Past performance of any strategy does not guarantee future results. Always combine analysis with proper risk management and your broader trading plan. Consult a licensed financial advisor if you are unsure of your individual risk tolerance or investment objectives.

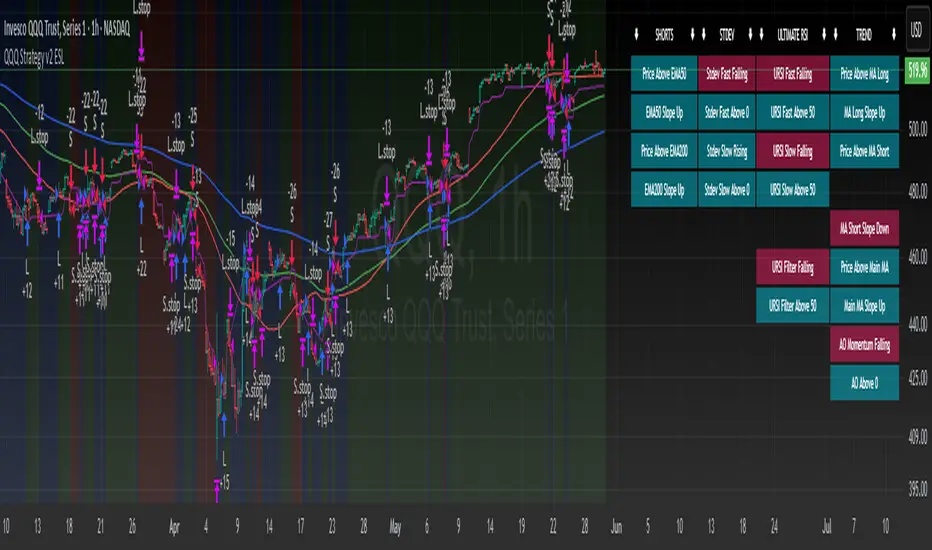

QQQ Strategy v2 ESL | easy-peasy-x This is a strategy optimized for QQQ (and SPY) for the 1H timeframe. It significantly outperforms passive buy-and-hold approach. With settings adjustments, it can be used on various assets like stocks and cryptos and various timeframes, although the default out of the box settings favor QQQ 1H.

The strategy uses various triggers to take both long and short trades. These can be adjusted in settings. If you try a different asset, see what combination of triggers works best for you.

Some of the triggers employ LuxAlgo's Ultimate RSI - shoutout to him for great script, check it out here .

Other triggers are based on custom signed standard deviation - basically the idea is to trade Bollinger Bands expansions (long to the upside, short to the downside) and fade or stay out of contractions.

There are three key moving averages in the strategy - LONG MA, SHORT MA, BASIC MA. Long and Short MAs are guides to eyes on the chart and also act as possible trend filters (adjustable in settings). Basic MA acts as guide to eye and a possible trade trigger (adjustable in settings).

There are a few trend filters the strategy can use - moving average, signed standard deviation, ultimate RSI or none. The filters act as an additional condition on triggers, making the strategy take trades only if both triggers and trend filter allows. That way one can filter out trades with unfavorable risk/reward (for instance, don't long if price is under the MA200). Different trade filters can be used for long and short trades.

The strategy employs various stop loss types, the default of which is a trailing %-based stop loss type. ATR-based stop loss is also available. The default 1.5% trailing stop loss is suitable for leveraged trading.

Lastly, the strategy can trigger take profit orders if certain conditions are met, adjustable in settings. Also, it can hold onto winning trades and exit only after stop out (in which case, consecutive triggers to take other positions will be ignored until stop out).

Let me know if you like it and if you use it, what kind of tweaks would you like to see.

With kind regards,

easy-peasy-x

TICK Extreme Levels & AlertsAutomatically draws horizontal lines at +1000 and -1000 TICK levels

Sends alerts when TICK crosses those levels (for potential scalping/reversal setups)

Strategy: How to Use TICK in Real-Time Trading

1. Confirm Market Breadth

Use TICK to confirm broad participation in the move:

• Long S&P futures or SPY? Only buy breakouts if TICK is above +600 to +1000

• Shorting? Confirm with TICK below –600 to –1000

2. Fade Extremes for Scalps

Look for reversals at extreme levels:

• Fade +1200+: market likely overbought short term → scalp short

• Fade –1200–: market likely oversold → scalp long

Use in combo with other signals (like price exhaustion, candlestick reversal, or VWAP touches)

3. Avoid Trading in the Choppy Zone

If TICK remains between –400 and +400, institutions are not committed. This is where fakeouts are common.

4. Time Entries with TICK Swings

For example:

• TICK moves from –800 to +600 = momentum shift → look for long entries

• TICK stalling around +1000 = momentum climax → partial profit or fade play

True Range/Expected MoveThis indicator plots the ratio of True Range/Expected Move of SPX. True Range is simple the high-low range of any period. Expected move is the amount that SPX is predicted to increase or decrease from its current price based on the current level of implied volatility. There are several choices of volatility indexes to choose from. The shift in color from red to green is set by default to 1 but can be adjusted in the settings.

Red bars indicate the true range was below the expected move and green bars indicate it was above. Because markets tend to overprice volatility it is expected that there would be more red bars than green. If you sell SPX or SPY option premium red days tend to be successful while green days tend to get stopped out. On a 1D chart it is interesting to look at the clusters of bar colors.

SPDR TrackerMonitor all SPDR Index Funds in one location! The purpose of this indicator is to review which sectors are trend up vs down to better manage risk against SPY, other funds and/or individual stocks.

With this indicator it may become more apparent which sectors to begin investment in that are at lows compared to others, or use it to determine which stocks may be undervalued or overvalued against SPY.

There is a small table at the bottom where each fund symbol is presented along with it's mode value, last period change as well as last period volume - there's a tooltip that shows the description for each symbol for a quick reminder.

Review the configuration pane where:

Individual funds can have their visibility toggled

Change funds colors

Adjust display mode for each fund (SMA, EMA, VWMA, BBW, Change, ATR, VWAP - many more!)

Some presentation modes may look better on some timeframes vs others, adjust lengths and use anchor point for VWAP.

Future updates may bring about new features, I have some code organization and refactoring to do but wanted to share the idea anyways.

Feel free to drop any suggestions for feature enhancement and I hope it brings success to many, enjoy.

Pre-market Highs & Lows on regular trading hours (RTH) chartShows pre-market highs and lows on RTH or ETH chart

-Pre-market duration user input (default is 16 'bar hours'; covering the time from S&P RTH close at 4pm >> 9:30am RTH open next day

-Displays on both RTH and ETH charts

-Written for ES (ES1! or e.g ESM2023), but tested and working on SPY, SPX

-Works across timeframes

Example usage on Electronic trading hours (ETH) chart; showing the 'bar hours' user input lookback duration visually

TICK - Custom Tickers [Pt]Traditionally, the TICK index is a technical analysis indicator that shows the difference in the number of stocks that are trading on an uptick vs a downtick in a particular period of time. This indicator allows user to choose up to 40 tickers to calculate TICK.

By default, it uses the SPY Top 40 stocks, but can be changed to any tickers.

There are options to show:

- Top 7 , ie. can be used for just showing TICK for FAANGMT => $FB + $AMZN + $AAPL + $NFLX + $GOOG + $MSFT + $TSLA

- Top 10

- Top 20

- Top 30

- Top 40

Data can be displayed in candle bars, line, or both.

Enjoy~

Balance of Power Heikin Ashi Investing Strategy Balance of Power Heikin Ashi Investing Strategy

This is a swing strategy designed for investment help.

Its made around the Balace of Power indicator, but has been adapted on using the Monthly Heikin Ashi candle from the SPY asset in order to be used with correlation for US Stock/ETF/Index Markets.

The BOP acts as an oscilallator showing the power of a bull trend when its positive and a bearish trend when its in negative. At the same time we can spot reversals, based on the percentiles ( 99/1)

The rules for entry :

For long : The 99 percentile is ascending, and we are either in a positive value (>0), or we crossed the bottom place ( -0.35)

For short : the 99 and 1 percentile are descending, and we are either in a negative value(<0), or we crossed down the top place ( 0.6)

If you have any questions please let me know !

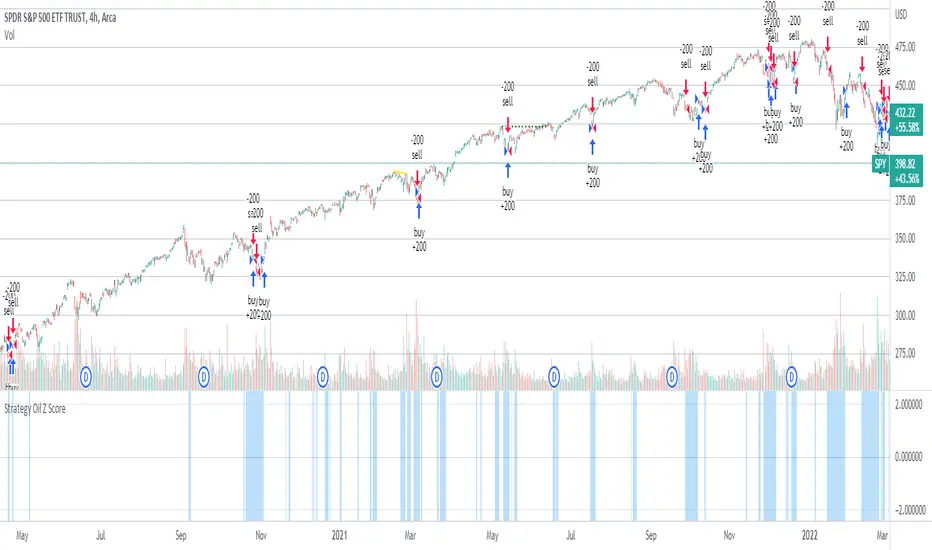

Strategy Oil Z ScoreObjective is to find forward looking indicators to find good entries into major index's.

In similar vein to my Combo Z Score script I have implemented one looking at oil and oil volatility. Interestingly the script out performs WITHOUT applying the EMA in longer timeframes but under performs in shorter timeframes, for example 2007 vs 2019. Likely due to the bullish nature of the past decade (by and large). You have some options on the underlying included Oil vs OVX (Best), MOVE vs OVX and VIX vs OVX. Oil vs OVX out performs Combo Z Script. Favours Spy over QQQ or derivations (SPXL etc).

[Pt] Premarket Breakout StrategyThis is a 1 trade per day strategy for trading SPY or QQQ index. By default, this is designed for 1 min time frame. This was an experimental script that seems to be profitable at the time of publication.

How it works:

Pre-market high and low is defined per trading day between 9:00 to 9:30 EST.

Then we looking for the first breakout on either PM high or PM low.

- Breakout high = long trade

- Breakout low = short trade

If long trade, we wait until Stochastic RSI D signal line to hit a lower threshold (18 by default). Then we enter long when K crosses above D line.

If short trade, we wait until Stochastic RSI D signal line to hit an upper threshold (82 by default). Then we enter short when K crosses below D line.

Stop loss for long

- set to PM low if entry is above PM high + %ATR buffer

- or set to PM range + %ATR buffer

Stop loss for short

- set to PM high if entry is below PM low + %ATR buffer

- or set to PM range + %ATR buffer

Profit target is set to 2x the risk by default.

*Note: Different Stochastic RSI lengths should be used if trading 5 min time frame. See tooltip.

Happy trading~~!

JPM VIX Signal - Non OverlayJPMorgan Chase & Co . strategists have identified what they say is a near bulletproof indicator to strengthen their argument that stock markets are poised to rally.

The buy signal is triggered when the Cboe Volatility Index ( VIX ) rises by more than 50% of its 1-month (30 day) moving average, which it last did on January 25th 2022, according to the strategists led by Mislav Matejka. The indicator has proven 100% accurate outside of recessions over the last three decades.

Instructions:

Symbol - SPY

Timeframe - Daily

Signal - Indicator exceeds horizontal line of 1.5

S&P Sector CorrelationScript for Macro:

This indicator shows the 9 day average of the correlation of the 11 S&P500 sectors with the security.

Recommend you use the indicator on SPX or SPY, but you can change the values to be compared.

GLHF

- DPT

Volatility Bands Reversal Strategy [Long Only]This strategy based on existng indicator available on TV

If finds the reversals for LONG entries ... I have modified the settings to back test it ...

BUY

====

When the price touches lower band , and tries to close above lower band

some signals are mixed up, you can research and look for a confirmation ...

if the middle band is above EMA50 , you can simply follow the strategy BUY signal

but if the middle band is EMA50 , wait for the price to close above middle band

Sell / Close

==========

wait for the sell signa OR close when price touches the upper band

How do you want to close , you can chose in settings. Chnage these values and see the performance

Please note , sell means just closing the existing LONG position , not short selling

Stop Loss

=========

Stop Loss is defaulted to 6%

This is tested in 1HR, 2HR and 4 HRs chart for SPY and QQQ ETFS ...

for long term investing style , 4 Hrs is the best time frme for this strategy

Warning

========

It is not a financial advise , it is for educational purposes only. Please do your own research before taking any trading decission

VFI strategy [based on VFI indicator published by UTS]This strategy is based on VFI indicator published by UTS.

for the strategy purpose , I have added buy line and sell line to the indicator and tested SPY stock/index on one hour chart

BUY RULE

==========

1. EMA 50 is above EMA 200

2. vfi line is pulled down and crossing above -4

EXIT RULE

==========

1. when vfi line crossing down 5

STOP LOSS

=========

1. default stop loss is set to 5%

ALL the above values (Buy Line , Sell line and Stop Loss ) can be modified in settings window

Notes :

more details of VFI indicator can be found at mkatsanos.com and precisiontradingsystems.com

Warning:

for educational purposes only

S&P Bear Warning IndicatorTHIS SCRIPT HAS BEEN BUILT TO BE USED AS A S&P500 SPY CRASH INDICATOR ON A DAILY TIME FRAME (should not be used as a strategy).

THIS SCRIPT HAS BEEN BUILT AS A STRATEGY FOR VISUALIZATION PURPOSES ONLY AND HAS NOT BEEN OPTIMIZED FOR PROFIT.

The script has been built to show as a lower indicator and also gives visual SELL signal on top when conditions are met. BARE IN MIND NO STOP LOSS, NOR ADVANCED EXIT STRATEGY HAS BEEN BUILT.

As well as the chart SELL signal an alert option has also been built into this script.

The script utilizes a VIX indicator (maroon line) and 50 period Momentum (blue line) and Danger/No trade zone(pink shading).

When the Momentum line crosses down across the VIX this is a sell off but in order to only signal major sell offs the SELL signal only triggers if the momentum continues down through the danger zone.

A SELL signal could be given earlier by removing the need to wait for momentum to continue down through the Danger Zone however this is designed only to catch major market weakness not small sell offs.

As you can see from the picture between the big October 2018 and March 2020 market declines only 2 additional SELLS were triggered.

To use this indicator to identify ideal buying then you should only buy when Momentum line is crossed above the VIX and the Momentum line is above the Danger Zone (ideally 3 - 5 days above danger zone)

NYSE_ADVANCE_DECLINE_VOL vs SPYThis script plot a NYSE ADVANCING DECLINING VOLUME LINE on a WMA histogram of SPY. Very new at coding pine script, so use at your own risk