Chande Momentum Oscillator StrategyThe Chande Momentum Oscillator (CMO) Trading Strategy is based on the momentum oscillator developed by Tushar Chande in 1994. The CMO measures the momentum of a security by calculating the difference between the sum of recent gains and losses over a defined period. The indicator offers a means to identify overbought and oversold conditions, making it suitable for developing mean-reversion trading strategies (Chande, 1997).

Strategy Overview:

Calculation of the Chande Momentum Oscillator (CMO):

The CMO formula considers both positive and negative price changes over a defined period (commonly set to 9 days) and computes the net momentum as a percentage.

The formula is as follows:

CMO=100×(Sum of Gains−Sum of Losses)(Sum of Gains+Sum of Losses)

CMO=100×(Sum of Gains+Sum of Losses)(Sum of Gains−Sum of Losses)

This approach distinguishes the CMO from other oscillators like the RSI by using both price gains and losses in the numerator, providing a more symmetrical measurement of momentum (Chande, 1997).

Entry Condition:

The strategy opens a long position when the CMO value falls below -50, signaling an oversold condition where the price may revert to the mean. Research in mean-reversion, such as by Poterba and Summers (1988), supports this approach, highlighting that prices often revert after sharp movements due to overreaction in the markets.

Exit Conditions:

The strategy closes the long position when:

The CMO rises above 50, indicating that the price may have become overbought and may not provide further upside potential.

Alternatively, the position is closed 5 days after the buy signal is triggered, regardless of the CMO value, to ensure a timely exit even if the momentum signal does not reach the predefined level.

This exit strategy aligns with the concept of time-based exits, reducing the risk of prolonged exposure to adverse price movements (Fama, 1970).

Scientific Basis and Rationale:

Momentum and Mean-Reversion:

The strategy leverages the well-known phenomenon of mean-reversion in financial markets. According to research by Jegadeesh and Titman (1993), prices tend to revert to their mean over short periods following strong movements, creating opportunities for traders to profit from temporary deviations.

The CMO captures this mean-reversion behavior by monitoring extreme price conditions. When the CMO reaches oversold levels (below -50), it signals potential buying opportunities, whereas crossing overbought levels (above 50) indicates conditions for selling.

Market Efficiency and Overreaction:

The strategy takes advantage of behavioral inefficiencies and overreactions, which are often the drivers behind sharp price movements (Shiller, 2003). By identifying these extreme conditions with the CMO, the strategy aims to capitalize on the market’s tendency to correct itself when price deviations become too large.

Optimization and Parameter Selection:

The 9-day period used for the CMO calculation is a widely accepted timeframe that balances responsiveness and noise reduction, making it suitable for capturing short-term price fluctuations. Studies in technical analysis suggest that oscillators optimized over such periods are effective in detecting reversals (Murphy, 1999).

Performance and Backtesting:

The strategy's effectiveness is confirmed through backtesting, which shows that using the CMO as a mean-reversion tool yields profitable opportunities. The use of time-based exits alongside momentum-based signals enhances the reliability of the strategy by ensuring that trades are closed even when the momentum signal alone does not materialize.

Conclusion:

The Chande Momentum Oscillator Trading Strategy combines the principles of momentum measurement and mean-reversion to identify and capitalize on short-term price fluctuations. By using a widely tested oscillator like the CMO and integrating a systematic exit approach, the strategy effectively addresses both entry and exit conditions, providing a robust method for trading in diverse market environments.

References:

Chande, T. S. (1997). The New Technical Trader: Boost Your Profit by Plugging into the Latest Indicators. John Wiley & Sons.

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. The Journal of Finance, 25(2), 383-417.

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. The Journal of Finance, 48(1), 65-91.

Murphy, J. J. (1999). Technical Analysis of the Financial Markets: A Comprehensive Guide to Trading Methods and Applications. New York Institute of Finance.

Poterba, J. M., & Summers, L. H. (1988). Mean Reversion in Stock Prices: Evidence and Implications. Journal of Financial Economics, 22(1), 27-59.

Shiller, R. J. (2003). From Efficient Markets Theory to Behavioral Finance. Journal of Economic Perspectives, 17(1), 83-104.

Cerca negli script per "the strat"

Shark Zone Day Machine V17### **Strategy Overview: Shark Zone Day Machine V14**

The "Shark Zone Day Machine V14" is a daily breakout trading strategy designed for traders who wish to capitalize on intraday price movements based on key levels from the previous day. The strategy operates on a daily timeframe, allowing traders to execute precise entries and manage their trades effectively. It includes both long and short trading capabilities, with user-friendly inputs for customization.

### **Key Features:**

1. **Daily Breakout Logic**:

- **Long Position**: The strategy opens a long position when the price breaks above the previous day's high, indicating potential upward momentum.

- **Short Position**: The strategy opens a short position when the price drops below the previous day's low, signaling possible downward pressure.

2. **Stop Loss Management**:

- The strategy uses a fixed stop loss of 50 points, which is set at the previous day's low for long trades and 50 points above the entry for short trades.

3. **Spread Adjustment**:

- Includes an adjustable spread input to account for bid-ask differences, ensuring entries and exits are accurately calculated.

4. **Activation Controls**:

- Traders can easily enable or disable long and short trading strategies independently using input toggles.

5. **Custom Alert Integration**:

- The strategy includes alert messages configured to work seamlessly with Pine Connector. These alerts can be set up to automatically send trade signals to MT4, enabling a fully automated trading experience.

### **Automated Trading Setup via Pine Connector to MT4**

To implement this strategy for automated trading between TradingView and MT4 using Pine Connector, follow these steps:

1. **Apply the Script on TradingView**:

- Load the "Shark Zone Day Machine V14" script onto your TradingView chart and adjust the input parameters as needed, including activation toggles, spread, and stop loss settings.

2. **Set Up Alerts on TradingView**:

- Click on the `Alerts` button in TradingView.

- Under "Condition," select the strategy and choose "Any alert() function call."

- For each alert, use the predefined messages:

- **Long Entry Alert**: `"BUY_SIGNAL_7683370025173"`

- **Long Exit Alert**: `"BUY_EXIT_SIGNAL_7683370025173"`

- **Short Entry Alert**: `"SELL_SIGNAL_7683370025173"`

- **Short Exit Alert**: `"SELL_EXIT_SIGNAL_7683370025173"`

- Ensure the alert actions are set to "Notify on app" and "Show pop-up" for immediate feedback.

3. **Configure Pine Connector**:

- Pine Connector should be installed and set up on your MT4 platform. Ensure the Pine Connector ID matches the alert messages from the TradingView script.

- Configure your MT4 EA to recognize these signals and execute trades accordingly. For example, a `"BUY_SIGNAL_7683370025173"` alert from TradingView will instruct MT4 to place a buy order.

4. **Test the Setup**:

- It’s essential to test the automation in a demo account first. Monitor how trades are opened and closed on MT4 when alerts are triggered from TradingView.

- Adjust the parameters on TradingView if needed for optimal performance and minimal slippage.

### **Benefits of Automated Trading with This Strategy**:

- **Consistency**: Eliminates the potential for human error by executing trades precisely as per the strategy’s logic.

- **Speed**: Rapid response to breakout conditions, ensuring you capture opportunities as soon as they arise.

- **Flexibility**: The ability to adjust stop loss, spread, and trading size allows for quick adaptation to different market conditions.

### **Important Notes**:

- Ensure your TradingView account remains active and has real-time data enabled for accurate alerts.

- Verify that Pine Connector and MT4 settings are configured correctly to prevent missed trades or incorrect lot sizes.

- Be mindful of market conditions, as breakout strategies may perform differently during high-volatility periods.

By following this guide, you'll be able to leverage the "Shark Zone Day Machine V14" strategy to its full potential, automating your trades and optimizing your trading efficiency.

Williams %R StrategyThe Williams %R Strategy implemented in Pine Script™ is a trading system based on the Williams %R momentum oscillator. The Williams %R indicator, developed by Larry Williams in 1973, is designed to identify overbought and oversold conditions in a market, helping traders time their entries and exits effectively (Williams, 1979). This particular strategy aims to capitalize on short-term price reversals in the S&P 500 (SPY) by identifying extreme values in the Williams %R indicator and using them as trading signals.

Strategy Rules:

Entry Signal:

A long position is entered when the Williams %R value falls below -90, indicating an oversold condition. This threshold suggests that the market may be near a short-term bottom, and prices are likely to reverse or rebound in the short term (Murphy, 1999).

Exit Signal:

The long position is exited when:

The current close price is higher than the previous day’s high, or

The Williams %R indicator rises above -30, indicating that the market is no longer oversold and may be approaching an overbought condition (Wilder, 1978).

Technical Analysis and Rationale:

The Williams %R is a momentum oscillator that measures the level of the close relative to the high-low range over a specific period, providing insight into whether an asset is trading near its highs or lows. The indicator values range from -100 (most oversold) to 0 (most overbought). When the value falls below -90, it indicates an oversold condition where a reversal is likely (Achelis, 2000). This strategy uses this oversold threshold as a signal to initiate long positions, betting on mean reversion—an established principle in financial markets where prices tend to revert to their historical averages (Jegadeesh & Titman, 1993).

Optimization and Performance:

The strategy allows for an adjustable lookback period (between 2 and 25 days) to determine the range used in the Williams %R calculation. Empirical tests show that shorter lookback periods (e.g., 2 days) yield the most favorable outcomes, with profit factors exceeding 2. This finding aligns with studies suggesting that shorter timeframes can effectively capture short-term momentum reversals (Fama, 1970; Jegadeesh & Titman, 1993).

Scientific Context:

Mean Reversion Theory: The strategy’s core relies on mean reversion, which suggests that prices fluctuate around a mean or average value. Research shows that such strategies, particularly those using oscillators like Williams %R, can exploit these temporary deviations (Poterba & Summers, 1988).

Behavioral Finance: The overbought and oversold conditions identified by Williams %R align with psychological factors influencing trading behavior, such as herding and panic selling, which often create opportunities for price reversals (Shiller, 2003).

Conclusion:

This Williams %R-based strategy utilizes a well-established momentum oscillator to time entries and exits in the S&P 500. By targeting extreme oversold conditions and exiting when these conditions revert or exceed historical ranges, the strategy aims to capture short-term gains. Scientific evidence supports the effectiveness of short-term mean reversion strategies, particularly when using indicators sensitive to momentum shifts.

References:

Achelis, S. B. (2000). Technical Analysis from A to Z. McGraw Hill.

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. The Journal of Finance, 25(2), 383-417.

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. The Journal of Finance, 48(1), 65-91.

Murphy, J. J. (1999). Technical Analysis of the Financial Markets: A Comprehensive Guide to Trading Methods and Applications. New York Institute of Finance.

Poterba, J. M., & Summers, L. H. (1988). Mean Reversion in Stock Prices: Evidence and Implications. Journal of Financial Economics, 22(1), 27-59.

Shiller, R. J. (2003). From Efficient Markets Theory to Behavioral Finance. Journal of Economic Perspectives, 17(1), 83-104.

Williams, L. (1979). How I Made One Million Dollars… Last Year… Trading Commodities. Windsor Books.

Wilder, J. W. (1978). New Concepts in Technical Trading Systems. Trend Research.

This explanation provides a scientific and evidence-based perspective on the Williams %R trading strategy, aligning it with fundamental principles in technical analysis and behavioral finance.

Simple RSI stock Strategy [1D] The "Simple RSI Stock Strategy " is designed to long-term traders. Strategy uses a daily time frame to capitalize on signals generated by the Relative Strength Index (RSI) and the Simple Moving Average (SMA). This strategy is suitable for low-leverage trading environments and focuses on identifying potential buy opportunities when the market is oversold, while incorporating strong risk management with both dynamic and static Stop Loss mechanisms.

This strategy is recommended for use with a relatively small amount of capital and is best applied by diversifying across multiple stocks in a strong uptrend, particularly in the S&P 500 stock market. It is specifically designed for equities, and may not perform well in other markets such as commodities, forex, or cryptocurrencies, where different market dynamics and volatility patterns apply.

Indicators Used in the Strategy:

1. RSI (Relative Strength Index):

- The RSI is a momentum oscillator used to identify overbought and oversold conditions in the market.

- This strategy enters long positions when the RSI drops below the oversold level (default: 30), indicating a potential buying opportunity.

- It focuses on oversold conditions but uses a filter (SMA 200) to ensure trades are only made in the context of an overall uptrend.

2. SMA 200 (Simple Moving Average):

- The 200-period SMA serves as a trend filter, ensuring that trades are only executed when the price is above the SMA, signaling a bullish market.

- This filter helps to avoid entering trades in a downtrend, thereby reducing the risk of holding positions in a declining market.

3. ATR (Average True Range):

- The ATR is used to measure market volatility and is instrumental in setting the Stop Loss.

- By multiplying the ATR value by a custom multiplier (default: 1.5), the strategy dynamically adjusts the Stop Loss level based on market volatility, allowing for flexibility in risk management.

How the Strategy Works:

Entry Signals:

The strategy opens long positions when RSI indicates that the market is oversold (below 30), and the price is above the 200-period SMA. This ensures that the strategy buys into potential market bottoms within the context of a long-term uptrend.

Take Profit Levels:

The strategy defines three distinct Take Profit (TP) levels:

TP 1: A 5% from the entry price.

TP 2: A 10% from the entry price.

TP 3: A 15% from the entry price.

As each TP level is reached, the strategy closes portions of the position to secure profits: 33% of the position is closed at TP 1, 66% at TP 2, and 100% at TP 3.

Visualizing Target Points:

The strategy provides visual feedback by plotting plotshapes at each Take Profit level (TP 1, TP 2, TP 3). This allows traders to easily see the target profit levels on the chart, making it easier to monitor and manage positions as they approach key profit-taking areas.

Stop Loss Mechanism:

The strategy uses a dual Stop Loss system to effectively manage risk:

ATR Trailing Stop: This dynamic Stop Loss adjusts based on the ATR value and trails the price as the position moves in the trader’s favor. If a price reversal occurs and the market begins to trend downward, the trailing stop closes the position, locking in gains or minimizing losses.

Basic Stop Loss: Additionally, a fixed Stop Loss is set at 25%, limiting potential losses. This basic Stop Loss serves as a safeguard, automatically closing the position if the price drops 25% from the entry point. This higher Stop Loss is designed specifically for low-leverage trading, allowing more room for market fluctuations without prematurely closing positions.

to determine the level of stop loss and target point I used a piece of code by RafaelZioni, here is the script from which a piece of code was taken

Together, these mechanisms ensure that the strategy dynamically manages risk while offering robust protection against significant losses in case of sharp market downturns.

The position size has been estimated by me at 75% of the total capital. For optimal capital allocation, a recommended value based on the Kelly Criterion, which is calculated to be 59.13% of the total capital per trade, can also be considered.

Enjoy !

Overnight Positioning w EMA - Strategy [presentTrading]I've recently started researching Market Timing strategies, and it’s proving to be quite an interesting area of study. The idea of predicting optimal times to enter and exit the market, based on historical data and various indicators, brings a dynamic edge to trading. Additionally, it is integrated with the 3commas bot for automated trade execution.

I'm still working on it. Welcome to share your point of view.

█ Introduction and How it is Different

The "Overnight Positioning with EMA " is designed to capitalize on market inefficiencies during the overnight trading period. This strategy takes a position shortly before the market closes and exits shortly after it opens the following day. What sets this strategy apart is the integration of an optional Exponential Moving Average (EMA) filter, which ensures that trades are aligned with the underlying trend. The strategy provides flexibility by allowing users to select between different global market sessions, such as the US, Asia, and Europe.

It is integrated with the 3commas bot for automated trade execution and has a built-in mechanism to avoid holding positions over the weekend by force-closing positions on Fridays before the market closes.

BTCUSD 20 mins Performance

█ Strategy, How it Works: Detailed Explanation

The core logic of this strategy is simple: enter trades before market close and exit them after market open, taking advantage of potential price movements during the overnight period. Here’s how it works in more detail:

🔶 Market Timing

The strategy determines the local market open and close times based on the selected market (US, Asia, Europe) and adjusts entry and exit points accordingly. The entry is triggered a specific number of minutes before market close, and the exit is triggered a specific number of minutes after market open.

🔶 EMA Filter

The strategy includes an optional EMA filter to help ensure that trades are taken in the direction of the prevailing trend. The EMA is calculated over a user-defined timeframe and length. The entry is only allowed if the closing price is above the EMA (for long positions), which helps to filter out trades that might go against the trend.

The EMA formula:

```

EMA(t) = +

```

Where:

- EMA(t) is the current EMA value

- Close(t) is the current closing price

- n is the length of the EMA

- EMA(t-1) is the previous period's EMA value

🔶 Entry Logic

The strategy monitors the market time in the selected timezone. Once the current time reaches the defined entry period (e.g., 20 minutes before market close), and the EMA condition is satisfied, a long position is entered.

- Entry time calculation:

```

entryTime = marketCloseTime - entryMinutesBeforeClose * 60 * 1000

```

🔶 Exit Logic

Exits are triggered based on a specified time after the market opens. The strategy checks if the current time is within the defined exit period (e.g., 20 minutes after market open) and closes any open long positions.

- Exit time calculation:

exitTime = marketOpenTime + exitMinutesAfterOpen * 60 * 1000

🔶 Force Close on Fridays

To avoid the risk of holding positions over the weekend, the strategy force-closes any open positions 5 minutes before the market close on Fridays.

- Force close logic:

isFriday = (dayofweek(currentTime, marketTimezone) == dayofweek.friday)

█ Trade Direction

This strategy is designed exclusively for long trades. It enters a long position before market close and exits the position after market open. There is no shorting involved in this strategy, and it focuses on capturing upward momentum during the overnight session.

█ Usage

This strategy is suitable for traders who want to take advantage of price movements that occur during the overnight period without holding positions for extended periods. It automates entry and exit times, ensuring that trades are placed at the appropriate times based on the market session selected by the user. The 3commas bot integration also allows for automated execution, making it ideal for traders who wish to set it and forget it. The strategy is flexible enough to work across various global markets, depending on the trader's preference.

█ Default Settings

1. entryMinutesBeforeClose (Default = 20 minutes):

This setting determines how many minutes before the market close the strategy will enter a long position. A shorter duration could mean missing out on potential movements, while a longer duration could expose the position to greater price fluctuations before the market closes.

2. exitMinutesAfterOpen (Default = 20 minutes):

This setting controls how many minutes after the market opens the position will be exited. A shorter exit time minimizes exposure to market volatility at the open, while a longer exit time could capture more of the overnight price movement.

3. emaLength (Default = 100):

The length of the EMA affects how the strategy filters trades. A shorter EMA (e.g., 50) reacts more quickly to price changes, allowing more frequent entries, while a longer EMA (e.g., 200) smooths out price action and only allows entries when there is a stronger underlying trend.

The effect of using a longer EMA (e.g., 200) would be:

```

EMA(t) = +

```

4. emaTimeframe (Default = 240):

This is the timeframe used for calculating the EMA. A higher timeframe (e.g., 360) would base entries on longer-term trends, while a shorter timeframe (e.g., 60) would respond more quickly to price movements, potentially allowing more frequent trades.

5. useEMA (Default = true):

This toggle enables or disables the EMA filter. When enabled, trades are only taken when the price is above the EMA. Disabling the EMA allows the strategy to enter trades without any trend validation, which could increase the number of trades but also increase risk.

6. Market Selection (Default = US):

This setting determines which global market's open and close times the strategy will use. The selection of the market affects the timing of entries and exits and should be chosen based on the user's preference or geographic focus.

Martingale with MACD+KDJ opening conditionsStrategy Overview:

This strategy is based on a Martingale trading approach, incorporating MACD and KDJ indicators. It features pyramiding, trailing stops, and dynamic profit-taking mechanisms, suitable for both long and short trades. The strategy increases position size progressively using a Multiplier, a key feature of Martingale systems.

Key Concepts:

Martingale Strategy: A trading system where positions are doubled or increased after a loss to recover previous losses with a single successful trade. In this script, the position size is incremented using a Multiplier for each addition.

Pyramiding: Allows adding to existing trades when market conditions are favorable, enhancing profitability during trends.

Settings:

Basic Inputs:

Initial Order: Defines the starting size of the position.

Default: 150.0

MACD Settings: Customize the fast, slow, and signal smoothing lengths.

Default: Fast Length: 9, Slow Length: 26, Signal Smoothing: 9

KDJ Settings: Customize the length and smoothing parameters for KDJ.

Default: Length: 14, Smooth K: 3, Smooth D: 3

Max Additions: Sets the number of additional positions (pyramiding).

Default: 5 (Min: 1, Max: 10)

Position Sizing: Percent to add to positions on favorable conditions.

Default: 1.0%

Martingale Multiplier:

Add Multiplier: This value controls the scaling of additional positions according to the Martingale principle. After each loss, a new position is added, and its size is increased by the Multiplier factor. For example, with a multiplier of 2, each new addition will be twice as large as the previous one, accelerating recovery if the price moves favorably.

Default: 1.0 (no multiplication)

Can be adjusted up to 10x to aggressively increase position size after losses.

Trade Execution:

Long Trades:

Entry Condition: A long position is opened when the MACD line crosses over the signal line, and the KDJ’s %K crosses above %D.

Additions (Martingale): After the initial long position, new positions are added if the price drops by the defined percentage, and each new addition is increased using the Multiplier. This continues up to the set Max Additions.

Short Trades:

Entry Condition: A short position is opened when the MACD line crosses under the signal line, and the KDJ’s %K crosses below %D.

Additions (Martingale): After the initial short position, new positions are added if the price rises by the defined percentage, and each new addition is increased using the Multiplier.

Exit Conditions:

Take Profit: Exits are triggered when the price reaches the take-profit threshold.

Stop Loss: If the price moves unfavorably, the position will be closed at the set stop-loss level.

Trailing Stop: Adjusts dynamically as the price moves in favor of the trade to lock in profits.

On-Chart Visuals:

Long Signals: Blue triangles below the bars indicate long entries, and green triangles mark additional long positions.

Short Signals: Red triangles above the bars indicate short entries, and orange triangles mark additional short positions.

Information Table:

The strategy displays a table with key metrics:

Open Price: The entry price of the trade.

Average Price: The average price of the current position.

Additions: The number of additional positions taken.

Next Add Price: The price level for the next position.

Take Profit: The price at which profits will be taken.

Stop Loss: The stop-loss level to minimize risk.

Usage Instructions:

Adjust the parameters to your trading style using the input settings.

The Multiplier amplifies your position size after each addition, so use it cautiously, especially in volatile markets.

Monitor the signals and table on the chart for entry/exit decisions and trade management.

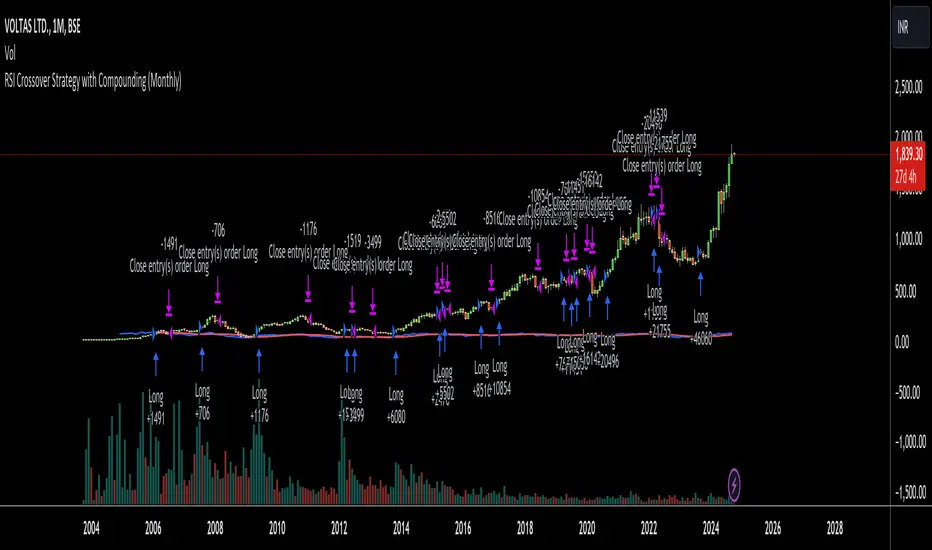

RSI Crossover Strategy with Compounding (Monthly)Explanation of the Code:

Initial Setup:

The strategy initializes with a capital of 100,000.

Variables track the capital and the amount invested in the current trade.

RSI Calculation:

The RSI and its SMA are calculated on the monthly timeframe using request.security().

Entry and Exit Conditions:

Entry: A long position is initiated when the RSI is above its SMA and there’s no existing position. The quantity is based on available capital.

Exit: The position is closed when the RSI falls below its SMA. The capital is updated based on the net profit from the trade.

Capital Management:

After closing a trade, the capital is updated with the net profit plus the initial investment.

Plotting:

The RSI and its SMA are plotted for visualization on the chart.

A label displays the current capital.

Notes:

Test the strategy on different instruments and historical data to see how it performs.

Adjust parameters as needed for your specific trading preferences.

This script is a basic framework, and you might want to enhance it with risk management, stop-loss, or take-profit features as per your trading strategy.

Feel free to modify it further based on your needs!

KAMA Cloud STIndicator:

Description:

The KAMA Cloud indicator is a sophisticated trading tool designed to provide traders with insights into market trends and their intensity. This indicator is built on the Kaufman Adaptive Moving Average (KAMA), which dynamically adjusts its sensitivity to filter out market noise and respond to significant price movements. The KAMA Cloud leverages multiple KAMAs to gauge trend direction and strength, offering a visual representation that is easy to interpret.

How It Works:

The KAMA Cloud uses twenty different KAMA calculations, each set to a distinct lookback period ranging from 5 to 100. These KAMAs are calculated using the average of the open, high, low, and close prices (OHLC4), ensuring a balanced view of price action. The relative positioning of these KAMAs helps determine the direction of the market trend and its momentum.

By measuring the cumulative relative distance between these KAMAs, the indicator effectively assesses the overall trend strength, akin to how the Average True Range (ATR) measures market volatility. This cumulative measure helps in identifying the trend’s robustness and potential sustainability.

The visualization component of the KAMA Cloud is particularly insightful. It plots a 'cloud' formed between the base KAMA (set at a 100-period lookback) and an adjusted KAMA that incorporates the cumulative relative distance scaled up. This cloud changes color based on the trend direction — green for upward trends and red for downward trends, providing a clear, visual representation of market conditions.

How the Strategy Works:

The KAMA Cloud ST strategy employs multiple KAMA calculations with varying lengths to capture the nuances of market trends. It measures the relative distances between these KAMAs to determine the trend's direction and strength, much like the original indicator. The strategy enhances decision-making by plotting a 'cloud' formed between the base KAMA (set to a 100-period lookback) and an adjusted KAMA that scales according to the cumulative relative distance of all KAMAs.

Key Components of the Strategy:

Multiple KAMA Layers: The strategy calculates KAMAs for periods ranging from 5 to 100 to analyze short to long-term market trends.

Dynamic Cloud: The cloud visually represents the trend’s strength and direction, updating in real-time as the market evolves.

Signal Generation: Trade signals are generated based on the orientation of the cloud relative to a smoothed version of the upper KAMA boundary. Long positions are initiated when the market trend is upward, and the current cloud value is above its smoothed average. Conversely, positions are closed when the trend reverses, indicated by the cloud falling below the smoothed average.

Suggested Usage:

Market: Stocks, not cryptocurrency

Timeframe: 1 Hour

Indicator:

Trend Following ADX + Parabolic SAR### Strategy Description: Trend Following using **ADX** and **Parabolic SAR**

This strategy is designed to follow market trends using two popular indicators: **Average Directional Index (ADX)** and **Parabolic SAR**. The strategy attempts to enter trades when the market shows a strong trend (using ADX) and confirms the trend direction using the Parabolic SAR. Here's a breakdown:

### Key Indicators:

1. **ADX (Average Directional Index)**:

- **Purpose**: ADX measures the strength of a trend, regardless of direction.

- **Usage**: The strategy uses ADX to confirm that the market is trending. When ADX is above a certain threshold (e.g., 25), it indicates a strong trend.

- **Directional Indicators**:

- **DI+ (Directional Indicator Plus)**: Indicates upward movement strength.

- **DI- (Directional Indicator Minus)**: Indicates downward movement strength.

2. **Parabolic SAR**:

- **Purpose**: Parabolic SAR is a trend-following indicator used to identify potential reversals in the price direction.

- **Usage**: It provides specific price points above or below which the strategy confirms buy or sell signals.

### Strategy Logic:

#### **Entry Conditions**:

1. **Long Position** (Buy):

- **ADX** is above the threshold (default: 25), indicating a strong trend.

- **DI+ > DI-**, indicating the upward trend is stronger than the downward.

- The price is above the **Parabolic SAR** level, confirming the upward trend.

2. **Short Position** (Sell):

- **ADX** is above the threshold (default: 25), indicating a strong trend.

- **DI- > DI+**, indicating the downward trend is stronger than the upward.

- The price is below the **Parabolic SAR** level, confirming the downward trend.

#### **Exit Conditions**:

- Positions are closed when an opposite signal is detected.

- For example, if a long position is open and the conditions for a short position are met, the long position is closed, and a short position is opened.

### Parameters:

1. **ADX Period**: Defines the length of the period for the ADX calculation (default: 14).

2. **ADX Threshold**: The minimum value of ADX to confirm a strong trend (default: 25).

3. **Parabolic SAR Start**: The initial step for the SAR (default: 0.02).

4. **Parabolic SAR Increment**: The step increment for SAR (default: 0.02).

5. **Parabolic SAR Max**: The maximum step for SAR (default: 0.2).

### Example Trade Flow:

#### **Long Trade**:

1. ADX > 25, confirming a strong trend.

2. DI+ > DI-, indicating the market is trending upward.

3. The price is above the Parabolic SAR, confirming the upward direction.

4. **Action**: Enter a long (buy) position.

5. Exit the long position when a short signal is triggered (i.e., DI- > DI+, price below Parabolic SAR).

#### **Short Trade**:

1. ADX > 25, confirming a strong trend.

2. DI- > DI+, indicating the market is trending downward.

3. The price is below the Parabolic SAR, confirming the downward direction.

4. **Action**: Enter a short (sell) position.

5. Exit the short position when a long signal is triggered (i.e., DI+ > DI-, price above Parabolic SAR).

### Strengths of the Strategy:

- **Trend-Following**: It performs well in markets with strong trends, whether upward or downward.

- **Dual Confirmation**: The combination of ADX and Parabolic SAR reduces false signals by ensuring both trend strength and direction are considered before entering a trade.

### Weaknesses:

- **Range-Bound Markets**: This strategy may perform poorly in choppy, non-trending markets because both ADX and SAR are trend-following indicators.

- **Lagging Nature**: Since both ADX and SAR are lagging indicators, the strategy may enter trades after the trend has already started, potentially missing early profits.

### Customization:

- **ADX Threshold**: You can increase the threshold if you only want to trade in very strong trends, or lower it to capture more moderate trends.

- **SAR Parameters**: Adjusting the SAR `start`, `increment`, and `max` values will make the Parabolic SAR more or less sensitive to price changes.

### Summary:

This strategy combines the ADX and Parabolic SAR to take advantage of strong market trends. By confirming both trend strength (ADX) and trend direction (Parabolic SAR), it aims to enter high-probability trades in trending markets while minimizing false signals. However, it may struggle in sideways or non-trending markets.

For Educational purposes only !!!

Fibonacci Swing Trading BotStrategy Overview for "Fibonacci Swing Trading Bot"

Strategy Name: Fibonacci Swing Trading Bot

Version: Pine Script v5

Purpose: This strategy is designed for swing traders who want to leverage Fibonacci retracement levels and candlestick patterns to enter and exit trades on higher time frames.

Key Components:

1. Multiple Timeframe Analysis:

The strategy uses a customizable timeframe for analysis. You can choose between 4hour, daily, weekly, or monthly time frames to fit your preferred trading horizon. The high and low-price data is retrieved from the selected timeframe to identify swing points.

2. Fibonacci Retracement Levels:

The script calculates two key Fibonacci retracement levels:

0.618: A common level where price often retraces before resuming its trend.

0.786: A deeper retracement level, often used to identify stronger support/resistance areas.

These levels are dynamically plotted on the chart based on the highest high and lowest low over the last 50 bars of the selected timeframe.

3. Candlestick Based Entry Signals:

The strategy uses candlestick patterns as the only indicator for trade entries:

Bullish Candle: A green candle (close > open) that forms between the 0.618 retracement level and the swing high.

Bearish Candle: A red candle (close < open) that forms between the 0.786 retracement level and the swing low.

When these candlestick patterns align with the Fibonacci levels, the script triggers buy or sell signals.

4. Risk Management:

Stop Loss: The stop loss is set at 1% below the entry price for long trades and 1% above the entry price for short trades. This tight risk management ensures controlled losses.

Take Profit: The strategy uses a 2:1 risk-to-reward ratio. The take profit is automatically calculated based on this ratio relative to the stop loss.

5. Buy/Sell Logic:

Buy Signal: Triggered when a bullish candle forms above the 0.618 retracement level and below the swing high. The bot then places a long position.

Sell Signal: Triggered when a bearish candle forms below the 0.786 retracement level and above the swing low. The bot then places a short position.

The stop loss and take profit levels are automatically managed once the trade is placed.

Strengths of This Strategy:

Swing Trading Focus: The strategy is ideal for swing traders, targeting longer-term price moves that can take days or weeks to play out.

Simple Yet Effective Indicators: By only relying on Fibonacci retracement levels and basic candlestick patterns, the strategy avoids complexity while capitalizing on well-known support and resistance zones.

Automated Risk Management: The built-in stop loss and take profit mechanism ensures trades are protected, adhering to a strict 2:1 risk/reward ratio.

Multiple Timeframe Analysis: The script adapts to various market conditions by allowing users to switch between different timeframes (4hour, daily, weekly, monthly), giving traders flexibility.

Strategy Use Cases:

Retracement Traders: Traders who focus on entering the market at key retracement levels (0.618 and 0.786) will find this strategy especially useful.

Trend Reversal Traders: The strategy’s reliance on candlestick formations at Fibonacci levels helps traders spot potential reversals in price trends.

Risk Conscious Traders: With its 1% risk per trade and 2:1 risk/reward ratio, the strategy is ideal for traders who prioritize risk management in their trades.

Commitment of Trader %R StrategyThis Pine Script strategy utilizes the Commitment of Traders (COT) data to inform trading decisions based on the Williams %R indicator. The script operates in TradingView and includes various functionalities that allow users to customize their trading parameters.

Here’s a breakdown of its key components:

COT Data Import:

The script imports the COT library from TradingView to access historical COT data related to different trader groups (commercial hedgers, large traders, and small traders).

User Inputs:

COT data selection mode (e.g., Auto, Root, Base currency).

Whether to include futures, options, or both.

The trader group to analyze.

The lookback period for calculating the Williams %R.

Upper and lower thresholds for triggering trades.

An option to enable or disable a Simple Moving Average (SMA) filter.

Williams %R Calculation: The script calculates the Williams %R value, which is a momentum indicator that measures overbought or oversold levels based on the highest and lowest prices over a specified period.

SMA Filter: An optional SMA filter allows users to limit trades to conditions where the price is above or below the SMA, depending on the configuration.

Trade Logic: The strategy enters long positions when the Williams %R value exceeds the upper threshold and exits when the value falls below it. Conversely, it enters short positions when the Williams %R value is below the lower threshold and exits when the value rises above it.

Visual Elements: The script visually indicates the Williams %R values and thresholds on the chart, with the option to plot the SMA if enabled.

Commitment of Traders (COT) Data

The COT report is a weekly publication by the Commodity Futures Trading Commission (CFTC) that provides a breakdown of open interest positions held by different types of traders in the U.S. futures markets. It is widely used by traders and analysts to gauge market sentiment and potential price movements.

Data Collection: The COT data is collected from futures commission merchants and is published every Friday, reflecting positions as of the previous Tuesday. The report categorizes traders into three main groups:

Commercial Traders: These are typically hedgers (like producers and processors) who use futures to mitigate risk.

Non-Commercial Traders: Often referred to as speculators, these traders do not have a commercial interest in the underlying commodity but seek to profit from price changes.

Non-reportable Positions: Small traders who do not meet the reporting threshold set by the CFTC.

Interpretation:

Market Sentiment: By analyzing the positions of different trader groups, market participants can gauge sentiment. For instance, if commercial traders are heavily short, it may suggest they expect prices to decline.

Extreme Positions: Some traders look for extreme positions among non-commercial traders as potential reversal signals. For example, if speculators are overwhelmingly long, it might indicate an overbought condition.

Statistical Insights: COT data is often used in conjunction with technical analysis to inform trading decisions. Studies have shown that analyzing COT data can provide valuable insights into future price movements (Lund, 2018; Hurst et al., 2017).

Scientific References

Lund, J. (2018). Understanding the COT Report: An Analysis of Speculative Trading Strategies.

Journal of Derivatives and Hedge Funds, 24(1), 41-52. DOI:10.1057/s41260-018-00107-3

Hurst, B., O'Neill, R., & Roulston, M. (2017). The Impact of COT Reports on Futures Market Prices: An Empirical Analysis. Journal of Futures Markets, 37(8), 763-785.

DOI:10.1002/fut.21849

Commodity Futures Trading Commission (CFTC). (2024). Commitment of Traders. Retrieved from CFTC Official Website.

Advanced Position Management [Mr_Rakun]Advanced Position Management

This Pine Script code is for a strategy titled "Advanced Position Management," aimed at effective trade execution and management using multiple take profit levels, trailing stop loss, and dynamic position sizing.

Take Profit Levels: It defines up to three take profit (TP) levels, allowing partial position exits at different price thresholds. The take profit levels and their respective quantities are adjustable using inputs.

Stop Loss and Trailing Stop: The script implements an initial stop loss based on a percentage from the entry price. Additionally, it features a trailing stop that moves based on either a percentage or previous TP levels, dynamically adjusting to maximize gains while protecting profits.

Position Size: The position size is customizable and based on USD value, allowing the trader to manage risk more effectively.

Advantages:

Flexibility: Multiple take profit levels and a dynamic stop loss system allow traders to lock in profits while keeping the position open for further gains.

Risk Management: The initial stop loss and trailing stop help to limit losses and protect profits as the trade moves in the desired direction.

Automation: Once the strategy is deployed, it automatically handles entry, exit, and stop management, reducing the need for constant monitoring.

------ TR ------

Gelişmiş Pozisyon Yönetimi

Bu Pine Script kodu, Gelişmiş Pozisyon Yönetimi için kendi stratejilerinize kolayca entegre edeceğiniz bir risk yönetimidir. Çoklu kâr al seviyeleri, takip eden stop-loss ve dinamik pozisyon büyüklüğü kullanarak işlem yürütme ve yönetiminde etkilidir.

Gelişmiş Pozisyon Yönetimi

Kâr Alma Seviyeleri;

Kod, pozisyonların farklı fiyat seviyelerinde kısmi kapatılmasını sağlayan üç farklı kâr alma (TP) seviyesini tanımlar. Bu kâr alma seviyeleri ve ilgili miktarları, girişlerle ayarlanabilir.

Stop Loss ve Takip Eden Stop;

Koda, giriş fiyatından bir yüzdeye dayalı olarak başlangıçta stop-loss uygulanır. Ayrıca, fiyat hareketine göre kendini ayarlayan takip eden bir stop-loss sistemi bulunur. Ayrıca TP seviyelerini takip eden stop loss özelliğide vardır.

Avantajları:

Esneklik;

Çoklu kâr alma seviyeleri ve dinamik stop-loss sistemi, trader'ların kazançlarını kilitleyip aynı zamanda pozisyonu açık tutmalarına olanak tanır.

Risk Yönetimi;

Başlangıç stop-loss ve takip eden stop, zararı sınırlamaya ve kazançları korumaya yardımcı olur.

Otomasyon;

Strateji bir kez devreye alındığında, giriş, çıkış ve stop yönetimi otomatik olarak gerçekleştirilir, bu da sürekli takip ihtiyacını azaltır.

Neural Momentum StrategyThis strategy combines Exponential Moving Average (EMA) analysis with a multi-timeframe approach. It uses a neural scoring system to evaluate market momentum and generate precise trading signals. The strategy is implemented in Pine Script v5 and is designed for use on TradingView.

Key Components

The strategy utilizes short-term (10-period) and long-term (25-period) EMAs. It calculates the difference between these EMAs to assess trend direction and strength. A neural scoring system evaluates EMA crossovers (weight: 12 points), trend strength (weight: 10 points), and price acceleration (weight: 4 points). The system implements a score smoothing algorithm using a 10-period EMA.

Multi-timeframe Analysis

The strategy automatically selects a higher timeframe based on the current chart timeframe. It calculates scores for both the current and higher timeframes, then combines these scores using a weighted average. The higher timeframe factor ranges from 3 to 6, depending on the current timeframe.

Trading Logic

Entry occurs when the final combined score turns positive after a change. Exit happens when the final combined score turns negative after a change. The strategy recalculates scores on each bar, ensuring responsive trading decisions.

Risk Management

An optional adaptive stop-loss system based on Average True Range (ATR) is available. The default ATR period is 10, and the stop factor is 1.2. Stop levels are dynamically adjusted on the higher timeframe.

Customization Options

Users can adjust EMA periods, signal line period, scoring weights, and enable/disable multi-timeframe analysis. The strategy allows setting specific date ranges for backtesting and deployment.

Position Sizing

The strategy uses a percentage-of-equity position sizing method, with a default of 30% of account equity per trade.

Code Structure

The strategy is built using TradingView's strategy framework. It employs efficient use of the request.security() function for multi-timeframe analysis. The main calculation function, calculate_score(), computes the neural score based on EMA differences and acceleration.

Performance Considerations

The strategy adapts to various market conditions through its multi-faceted scoring system. Multi-timeframe analysis helps filter out noise and identify stronger trends. The neural scoring approach aims to capture subtle market dynamics often missed by traditional indicators.

Limitations

Performance may vary across different markets and timeframes. The strategy's effectiveness relies on proper calibration of its numerous parameters. Users should thoroughly backtest and forward test before live implementation.

To summarize, the Neural Momentum Strategy represents a sophisticated approach to market analysis. It combines traditional technical indicators with advanced scoring techniques and multi-timeframe analysis. This strategy is designed for traders seeking a data-driven and adaptive method. It aims to identify high-probability trading opportunities across various market conditions.

This Neural Momentum Strategy is for informational and educational purposes only. It should not be considered financial advice. The strategy may exhibit slight repainting behavior due to the nature of multi-timeframe analysis and the use of the request.security() function. Historical values might change as new data becomes available.

Trading carries a high level of risk, and may not be suitable for all investors. Before deciding to trade, you should carefully consider your investment objectives, level of experience, and risk appetite. The possibility exists that you could sustain a loss of some or all of your initial investment. Therefore, you should not invest money that you cannot afford to lose.

Past performance is not indicative of future results. The author and TradingView are not responsible for any losses incurred as a result of using this strategy. Always exercise caution when using this or any trading strategy, and thoroughly test it before implementing in live trading scenarios.

Users are solely responsible for any trading decisions they make based on this strategy. It is strongly recommended that you seek advice from an independent financial advisor if you have any doubts.

Bitcoin CME-Spot Z-Spread - Strategy [presentTrading]This time is a swing trading strategy! It measures the sentiment of the Bitcoin market through the spread of CME Bitcoin Futures and Bitfinex BTCUSD Spot prices. By applying Bollinger Bands to the spread, the strategy seeks to capture mean-reversion opportunities when prices deviate significantly from their historical norms

█ Introduction and How it is Different

The Bitcoin CME-Spot Bollinger Bands Strategy is designed to capture mean-reversion opportunities by exploiting the spread between CME Bitcoin Futures and Bitfinex BTCUSD Spot prices. The strategy uses Bollinger Bands to detect when the spread between these two correlated assets has deviated significantly from its historical norm, signaling potential overbought or oversold conditions.

What sets this strategy apart is its focus on spread trading between futures and spot markets rather than price-based indicators. By applying Bollinger Bands to the spread rather than individual prices, the strategy identifies price inefficiencies across markets, allowing traders to take advantage of the natural reversion to the mean that often occurs in these correlated assets.

BTCUSD 8hr Performance

█ Strategy, How It Works: Detailed Explanation

The strategy relies on Bollinger Bands to assess the volatility and relative deviation of the spread between CME Bitcoin Futures and Bitfinex BTCUSD Spot prices. Bollinger Bands consist of a moving average and two standard deviation bands, which help measure how much the spread deviates from its historical mean.

🔶 Spread Calculation:

The spread is calculated by subtracting the Bitfinex spot price from the CME Bitcoin futures price:

Spread = CME Price - Bitfinex Price

This spread represents the difference between the futures and spot markets, which may widen or narrow based on supply and demand dynamics in each market. By analyzing the spread, the strategy can detect when prices are too far apart (potentially overbought or oversold), indicating a trading opportunity.

🔶 Bollinger Bands Calculation:

The Bollinger Bands for the spread are calculated using a simple moving average (SMA) and the standard deviation of the spread over a defined period.

1. Moving Average (SMA):

The simple moving average of the spread (mu_S) over a specified period P is calculated as:

mu_S = (1/P) * sum(S_i from i=1 to P)

Where S_i represents the spread at time i, and P is the lookback period (default is 200 bars). The moving average provides a baseline for the normal spread behavior.

2. Standard Deviation:

The standard deviation (sigma_S) of the spread is calculated to measure the volatility of the spread:

sigma_S = sqrt((1/P) * sum((S_i - mu_S)^2 from i=1 to P))

3. Upper and Lower Bollinger Bands:

The upper and lower Bollinger Bands are derived by adding and subtracting a multiple of the standard deviation from the moving average. The number of standard deviations is determined by a user-defined parameter k (default is 2.618).

- Upper Band:

Upper Band = mu_S + (k * sigma_S)

- Lower Band:

Lower Band = mu_S - (k * sigma_S)

These bands provide a dynamic range within which the spread typically fluctuates. When the spread moves outside of these bands, it is considered overbought or oversold, potentially offering trading opportunities.

Local view

🔶 Entry Conditions:

- Long Entry: A long position is triggered when the spread crosses below the lower Bollinger Band, indicating that the spread has become oversold and is likely to revert upward.

Spread < Lower Band

- Short Entry: A short position is triggered when the spread crosses above the upper Bollinger Band, indicating that the spread has become overbought and is likely to revert downward.

Spread > Upper Band

🔶 Risk Management and Profit-Taking:

The strategy incorporates multi-step take profits to lock in gains as the trade moves in favor. The position is gradually reduced at predefined profit levels, reducing risk while allowing part of the trade to continue running if the price keeps moving favorably.

Additionally, the strategy uses a hold period exit mechanism. If the trade does not hit any of the take-profit levels within a certain number of bars, the position is closed automatically to avoid excessive exposure to market risks.

█ Trade Direction

The trade direction is based on deviations of the spread from its historical norm:

- Long Trade: The strategy enters a long position when the spread crosses below the lower Bollinger Band, signaling an oversold condition where the spread is expected to narrow.

- Short Trade: The strategy enters a short position when the spread crosses above the upper Bollinger Band, signaling an overbought condition where the spread is expected to widen.

These entries rely on the assumption of mean reversion, where extreme deviations from the average spread are likely to revert over time.

█ Usage

The Bitcoin CME-Spot Bollinger Bands Strategy is ideal for traders looking to capitalize on price inefficiencies between Bitcoin futures and spot markets. It’s especially useful in volatile markets where large deviations between futures and spot prices occur.

- Market Conditions: This strategy is most effective in correlated markets, like CME futures and spot Bitcoin. Traders can adjust the Bollinger Bands period and standard deviation multiplier to suit different volatility regimes.

- Backtesting: Before deployment, backtesting the strategy across different market conditions and timeframes is recommended to ensure robustness. Adjust the take-profit steps and hold periods to reflect the trader’s risk tolerance and market behavior.

█ Default Settings

The default settings provide a balanced approach to spread trading using Bollinger Bands but can be adjusted depending on market conditions or personal trading preferences.

🔶 Bollinger Bands Period (200 bars):

This defines the number of bars used to calculate the moving average and standard deviation for the Bollinger Bands. A longer period smooths out short-term fluctuations and focuses on larger, more significant trends. Adjusting the period affects the responsiveness of the strategy:

- Shorter periods (e.g., 100 bars): Makes the strategy more reactive to short-term market fluctuations, potentially generating more signals but increasing the risk of false positives.

- Longer periods (e.g., 300 bars): Focuses on longer-term trends, reducing the frequency of trades and focusing only on significant deviations.

🔶 Standard Deviation Multiplier (2.618):

The multiplier controls how wide the Bollinger Bands are around the moving average. By default, the bands are set at 2.618 standard deviations away from the average, ensuring that only significant deviations trigger trades.

- Higher multipliers (e.g., 3.0): Require a more extreme deviation to trigger trades, reducing trade frequency but potentially increasing the accuracy of signals.

- Lower multipliers (e.g., 2.0): Make the bands narrower, increasing the number of trade signals but potentially decreasing their reliability.

🔶 Take-Profit Levels:

The strategy has four take-profit levels to gradually lock in profits:

- Level 1 (3%): 25% of the position is closed at a 3% profit.

- Level 2 (8%): 20% of the position is closed at an 8% profit.

- Level 3 (14%): 15% of the position is closed at a 14% profit.

- Level 4 (21%): 10% of the position is closed at a 21% profit.

Adjusting these take-profit levels affects how quickly profits are realized:

- Lower take-profit levels: Capture gains more quickly, reducing risk but potentially cutting off larger profits.

- Higher take-profit levels: Let trades run longer, aiming for bigger gains but increasing the risk of price reversals before profits are locked in.

🔶 Hold Days (20 bars):

The strategy automatically closes the position after 20 bars if none of the take-profit levels are hit. This feature prevents trades from being held indefinitely, especially if market conditions are stagnant. Adjusting this:

- Shorter hold periods: Reduce the duration of exposure, minimizing risks from market changes but potentially closing trades too early.

- Longer hold periods: Allow trades to stay open longer, increasing the chance for mean reversion but also increasing exposure to unfavorable market conditions.

By understanding how these default settings affect the strategy’s performance, traders can optimize the Bitcoin CME-Spot Bollinger Bands Strategy to their preferences, adapting it to different market environments and risk tolerances.

High/Low Breakout Statistical Analysis StrategyThis Pine Script strategy is designed to assist in the statistical analysis of breakout systems on a monthly, weekly, or daily timeframe. It allows the user to select whether to open a long or short position when the price breaks above or below the respective high or low for the chosen timeframe. The user can also define the holding period for each position in terms of bars.

Core Functionality:

Breakout Logic:

The strategy triggers trades based on price crossing over (for long positions) or crossing under (for short positions) the high or low of the selected period (daily, weekly, or monthly).

Timeframe Selection:

A dropdown menu enables the user to switch between the desired timeframe (monthly, weekly, or daily).

Trade Direction:

Another dropdown allows the user to select the type of trade (long or short) depending on whether the breakout occurs at the high or low of the timeframe.

Holding Period:

Once a trade is opened, it is automatically closed after a user-defined number of bars, making it useful for analyzing how breakout signals perform over short-term periods.

This strategy is intended exclusively for research and statistical purposes rather than real-time trading, helping users to assess the behavior of breakouts over different timeframes.

Relevance of Breakout Systems:

Breakout trading systems, where trades are executed when the price moves beyond a significant price level such as the high or low of a given period, have been extensively studied in financial literature for their potential predictive power.

Momentum and Trend Following:

Breakout strategies are a form of momentum-based trading, exploiting the tendency of prices to continue moving in the direction of a strong initial movement after breaching a critical support or resistance level. According to academic research, momentum strategies, including breakouts, can produce returns above average market returns when applied consistently. For example, Jegadeesh and Titman (1993) demonstrated that stocks that performed well in the past 3-12 months continued to outperform in the subsequent months, suggesting that price continuation patterns, like breakouts, hold value .

Market Efficiency Hypothesis:

While the Efficient Market Hypothesis (EMH) posits that markets are generally efficient, and it is difficult to outperform the market through technical strategies, some studies show that in less liquid markets or during specific times of market stress, breakout systems can capitalize on temporary inefficiencies. Taylor (2005) and other researchers have found instances where breakout systems can outperform the market under certain conditions.

Volatility and Breakouts:

Breakouts are often linked to periods of increased volatility, which can generate trading opportunities. Coval and Shumway (2001) found that periods of heightened volatility can make breakouts more significant, increasing the likelihood that price trends will follow the breakout direction. This correlation between volatility and breakout reliability makes it essential to study breakouts across different timeframes to assess their potential profitability .

In summary, this breakout strategy offers an empirical way to study price behavior around key support and resistance levels. It is useful for researchers and traders aiming to statistically evaluate the effectiveness and consistency of breakout signals across different timeframes, contributing to broader research on momentum and market behavior.

References:

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. Journal of Finance, 48(1), 65-91.

Fama, E. F., & French, K. R. (1996). Multifactor Explanations of Asset Pricing Anomalies. Journal of Finance, 51(1), 55-84.

Taylor, S. J. (2005). Asset Price Dynamics, Volatility, and Prediction. Princeton University Press.

Coval, J. D., & Shumway, T. (2001). Expected Option Returns. Journal of Finance, 56(3), 983-1009.

High Yield Spread Strategy with SMA FilterThis Pine Script strategy is designed for statistical analysis and research purposes only, not for live trading or financial decision-making. The script evaluates the relationship between financial volatility (measured by either the VIX or the High Yield Spread) and market positioning strategies (long or short) based on user-defined conditions. Specifically, it allows users to test the assumption that elevated levels of VIX or the High Yield Spread may justify short positions in the market—a widely held belief in financial circles—but this script demonstrates that shorting is not always the optimal choice, even under these conditions.

Key Components:

1. High Yield Spread and VIX:

• High Yield Spread is the difference between the yields of corporate high-yield (or “junk”) bonds and U.S. Treasury securities. A rising spread often reflects increased market risk perception.

• VIX (Volatility Index) is often referred to as the market’s “fear gauge.” Higher VIX levels usually indicate heightened market uncertainty or expected volatility.

2. Strategy Logic:

• The script allows users to specify a threshold for the VIX or High Yield Spread, and it automatically evaluates if the spread exceeds this level, which traditionally would suggest an environment for higher market risk and thus potentially favoring short trades.

• However, the strategy provides flexibility to enter long or short positions, even in a high-risk environment, emphasizing that a high VIX or High Yield Spread does not always warrant shorting.

3. SMA Filter:

• A Simple Moving Average (SMA) filter can be applied to the price data, where positions are only entered if the price is above or below the SMA (depending on the trade direction). This adds a technical component to the strategy, incorporating price trends into decision-making.

4. Hold Duration:

• The script also allows users to define how long to hold a position after entering, enabling an analysis of different timeframes.

Theoretical Background:

The traditional belief that high VIX or High Yield Spreads favor short positions is not universally supported by research. While a spike in the VIX or credit spreads is often associated with increased market risk, research suggests that excessive volatility does not always lead to negative returns. In fact, high volatility can sometimes signal an approaching market rebound.

For example:

• Studies have shown that long-term investments during periods of heightened volatility can yield favorable returns due to mean reversion. Whaley (2000) notes that VIX spikes are often followed by market recoveries as volatility tends to revert to its mean over time .

• Research by Blitz and Vliet (2007) highlights that low-volatility stocks have historically outperformed high-volatility stocks, suggesting that volatility may not always predict negative returns .

• Furthermore, credit spreads can widen in response to broader market stress, but these may overshoot the actual credit risk, presenting opportunities for long positions when spreads are high and risk premiums are mispriced .

Educational Purpose:

The goal of this script is to challenge assumptions about shorting during volatile periods, showing that long positions can be equally, if not more, effective during market stress. By incorporating an SMA filter and customizable logic for entering trades, users can test different hypotheses regarding the effectiveness of both long and short positions under varying market conditions.

Note: This strategy is not intended for live trading and should be used solely for educational and statistical exploration. Misinterpreting financial indicators can lead to incorrect investment decisions, and it is crucial to conduct comprehensive research before trading.

References:

1. Whaley, R. E. (2000). “The Investor Fear Gauge”. The Journal of Portfolio Management, 26(3), 12-17.

2. Blitz, D., & van Vliet, P. (2007). “The Volatility Effect: Lower Risk Without Lower Return”. Journal of Portfolio Management, 34(1), 102-113.

3. Bhamra, H. S., & Kuehn, L. A. (2010). “The Determinants of Credit Spreads: An Empirical Analysis”. Journal of Finance, 65(3), 1041-1072.

This explanation highlights the academic and research-backed foundation of the strategy and the nuances of volatility, while cautioning against the assumption that high VIX or High Yield Spread always calls for shorting.