The Barking Rat ReversionsMean Reversion with Multi-Layered Precision

The Barking Rat Reversions is a short-term mean reversion strategy tailored for high-volatility markets. It combines several well-established technical tools in a configuration to identify overextended price movements likely to revert toward equilibrium. The goal is to isolate high-quality, short-term reversal opportunities while filtering out low-conviction setups.

At its core, our strategy triggers off Fair Value Gaps (FVGs) that occur a considerable distance away from a dynamically defined equilibrium band. It then validates these gaps by checking proximity to recent support and resistance drawn from swing extremes.

Additional confirmation comes from momentum filters and wick-rejection patterns, ensuring each entry aligns with both price structure and stretched momentum. Exits use volatility-adjusted profit targets. Keeping the approach disciplined and adaptive.

🧠Core Logic: Selectivity & Structure

This strategy is intentionally very selective. We have designed it to filter out roughly 95% of all market noise, highlighting only setups that pass multiple validation layers outlined below.

Fair Value Gaps (FVGs) as the Primary Trigger

FVGs identify imbalance zones where price historically retraces. These inefficient zones often become magnets for reversion as the market seeks to rebalance.

Dynamic Equilibrium Band + S/R

Defines a fair value zone with a long-term moving average and combines it with shorter-term swing pivots to establish support/resistance. Only FVGs that occur outside the band and near recent pivots are considered, ensuring reversals are sufficiently distanced and not taken too close to the mean.

Proximity to Support/Resistance

Setup validity depends on location. The strategy filters for FVGs near well-defined structural levels — areas where price has previously turned (i.e., recent swing highs or lows). This increases the likelihood that reversals are occurring at legitimate zones of confluence.

Wick-Rejection Confirmation

Confirms potential exhaustion through characteristic candle wick patterns beyond the equilibrium region. This acts as another filter to improve signal accuracy.

Sequential Filtered Signals

Custom logic ensures that a new signal in any direction must improve upon the previous one, preventing repetitive or suboptimal entries.

Multi-Step Confirmation

All validation layers must coincide on the same bar before a signal triggers, dramatically reducing false positives.

📈Chart Visuals: Designed for Clarity

To ensure transparency and easy interpretation, the script overlays intuitive visuals:

Green “▲” below a candle: Indicates a potential long entry

Red “▼” above a candle: Indicates a potential short entry

Green “✔️”: Marks exit from a trade when ATR target is met

Background shading (green/red): Indicates trade direction while active

Support/Resistance lines: Auto-plotted from recent swing levels

🔔Alerts: Stay Notified Without Watching

The strategy supports real-time alerts on candle close, ensuring that signals are only triggered once fully confirmed.

You must manually set up alerts within your TradingView account. Once configured, you’ll be able to set up one alert per instrument. This one alert covers all relevant signals and exits — ideal for hands-free monitoring.

⚙️Strategy report properties

Position size: 25% equity per trade

Initial capital: 10,000.00 USDT

Pyramiding: 10 entries per direction

Slippage: 2 ticks

Commission: 0.055% per side

Backtest timeframe: 1-minute

Backtest instrument: HYPEUSDT

Backtesting range: Jul 21, 2025 — Aug 7, 2025

Note on Sample Size:

You’ll notice the report displays fewer than the ideal 100 trades in the strategy report above. This is intentional. The goal of the script is to isolate high-quality, short-term reversal opportunities while filtering out low-conviction setups. This means that the Barking Rat Reversions strategy is ultra-selective, filtering out over 95% of market noise by enforcing multiple validation layers. The brief timeframe shown in the strategy report here illustrates its filtering logic over a short window — not its full capabilities. As a result, even on lower timeframes like the 1-minute chart, signals are deliberately sparse — each one must pass all criteria before triggering.

We conducted a broader backtest covering the period from December 5, 2024 to July 31, 2025, during which the strategy identified 968 high-probability setups on the same instrument and timeframe as the strategy report.

For a larger dataset:

Once the strategy is applied to your chart, users are encouraged to expand the lookback range or apply the strategy to other volatile pairs to view a full sample.

💡Why 25% Equity Per Trade?

While it's always best to size positions based on personal risk tolerance, we defaulted to 25% equity per trade in the backtesting data — and here’s why:

Backtests using this sizing show manageable drawdowns even under volatile periods

The strategy generates a sizeable number of trades, reducing reliance on a single outcome

Combined with conservative filters, the 25% setting offers a balance between aggression and control

Users are strongly encouraged to customize this to suit their risk profile.

🔍What Makes This Strategy Unique?

Multi-factor confirmation using FVGs, EMA deviation, RSI, wick rejection, and S/R

Clean, Intuitive Chart Experience

Real-time alerts triggered only on confirmation

Variables monitor prior reversal points, guaranteeing each new signal offers an improved entry

Tracks active positions and resets filters upon exit.

Cerca negli script per "track"

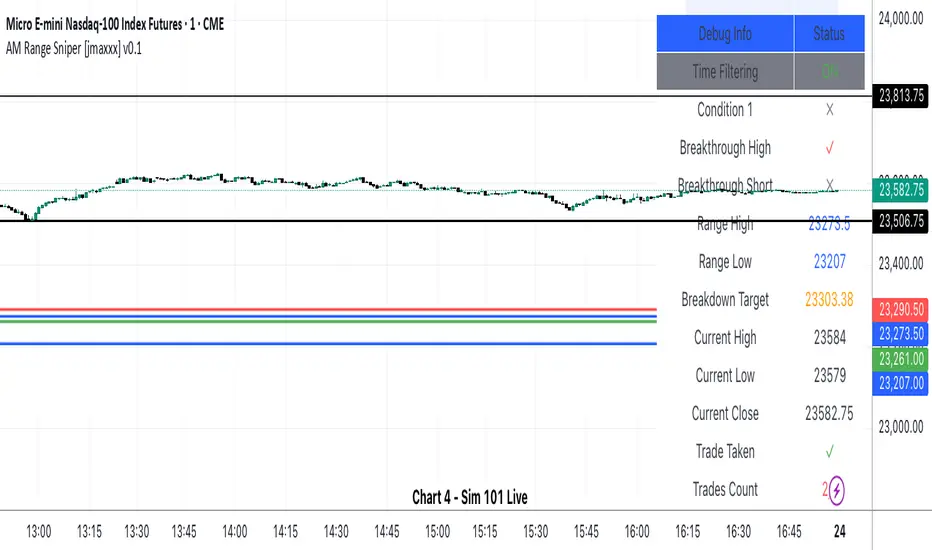

AM Range Sniper [jmaxxx]AM Range Sniper

Overview

AM Range Sniper is a sophisticated morning session trading strategy designed for Micro E-mini Nasdaq-100 Index Futures (MNQ). This strategy capitalizes on the critical 8:30-9:30 AM EST range formation period, implementing precise entry and exit mechanics with advanced risk management.

Key Features

🕐 Time-Based Range Analysis

Range Definition: Automatically identifies and tracks the 8:30-9:30 AM EST range

Trading Window: Active trading from 9:30 AM to 11:00 AM EST (extended for second chance trades)

Session Management: Daily reset ensures clean state for each trading session

🎯 Multiple Entry Patterns

Breakthrough/Retest: Captures price breakthroughs above range with retest opportunities

Long/Short Opportunities: Comprehensive coverage of both directional moves

Breakdown: Identifies bearish breakdowns below range support

Break Up: Detects bullish breakups above range resistance

Range Sweeps: Monitors for range high/low sweeps with reversal entries

⚡ Advanced Risk Management

Configurable Stop Losses: Tick-based stop losses for each trade type

Take Profit Targets: Automatic target calculations based on range size

Hard Close Protection: Automatic position closure at 4 PM EST

Second Chance Feature: Optional second trade opportunity if first trade loses

🔧 Professional Features

Visual Stop Loss Lines: Real-time stop loss visualization on chart

Debug Information Panel: Comprehensive status monitoring

Alert Integration: Customizable alert messages for entries/exits

Flexible Time Settings: Adjustable for different timezones

Strategy Logic

Range Formation (8:30-9:30 AM)

The strategy monitors the first hour of trading to establish the day's range. This range serves as the foundation for all subsequent trading decisions.

Entry Conditions

Breakthrough: Price breaks above range high with retest rejection

Breakdown: Price breaks below range low with confirmed bearish momentum

Break Up: Price breaks above range high with strong bullish confirmation

Sweep Entries: Range high/low sweeps followed by reversal signals

Risk Management

Stop Loss: Configurable tick-based stops for each trade type

Take Profit: 1.5x range size targets for breakdown/breakup trades

Position Sizing: Percentage-based position sizing

Session Limits: Maximum 2 trades per session (with second chance feature)

Settings & Customization

Core Parameters

Enable/disable individual entry patterns

Configurable stop loss levels (1-500 ticks)

Second chance feature toggle

Previous day level integration

Visual Customization

Customizable stop loss colors and widths

Debug panel visibility

Range line styling

Alert Configuration

Custom entry/exit alert messages

***** Automate With *****

APEX

NinjaTrader

Crosstrade.io ( promo code JMAXXX )

Performance & Reliability

Precision Focused: Waits for high-probability setups

Risk-Aware: Comprehensive stop loss and position management

Session-Based: Clean daily resets prevent carryover issues

Professional Grade: Designed for serious traders

Ideal For

Day Traders: Morning session specialists

Futures Traders: MNQ and similar instruments

Range Traders: Traders who capitalize on range breakouts

Risk-Conscious Traders: Those who prioritize risk management

Disclaimer

This strategy is for educational and informational purposes. Past performance does not guarantee future results. Always test thoroughly on historical data and paper trading before live implementation. Risk management is crucial - never risk more than you can afford to lose.

Created by jmaxxx - Professional trading strategy developer

For questions, feedback, or customization requests, please leave a comment below.

Opening-Range BreakoutNote: Default trading date range looks mediocre. Set date range to "Entire History" to see full effect of the strategy. 50.91% profitable trades, 1.178 profit factor, steady profits and limited drawdown. Total P&L: $154,141.18, Max Drawdown: $18,624.36. High R^2

█ Overview

The Opening-Range Breakout strategy is a mechanical, session‑based day‑trading system designed to capture the initial burst of directional momentum immediately following the market open. It defines a user‑configurable “opening range” window, measures its high and low boundaries, then places breakout stop orders at those levels once the range closes. Built‑in filters on minimum range width, reward‑to‑risk ratios, and optional reversal logic help refine entries and manage risk dynamically.

█ How It Works

Opening‑Range Formation

Between 9:30–10:15 AM ET (configurable), the script tracks the highest high and lowest low to form the day’s opening range box.

On the first bar after the range window closes, the range high (OR_high) and low (OR_low) are “locked in.”

Range‑Width Filter

To avoid false breakouts in low‑volatility mornings, the range must be at least X% of the current price (default 0.35%).

If the measured opening-range width < minimum threshold, no orders are placed that day.

Entry & Order Placement

Long: a stop‑buy order at the opening‑range high.

Short: a stop‑sell order at the opening‑range low.

Only one side can trigger (or both if reverse logic is enabled after a losing trade).

Risk Management

Once triggered, each trade uses an ATR‑style stop-loss defined as a percentage retracement of the range (default 50% of range width).

Profit target is set at a configurable Reward/Risk Ratio (default 1.1×).

Optional: Reverse on Stop‑Loss – if the initial breakout loses, immediately reverse into the opposite side on the same day.

Session Exit

Any open positions are closed at the end of the regular trading day (default 3:45 PM ET window end, with hard flat at session close).

Visual cues are provided via green (range high) and red (range low) step‑line plots directly on the chart, allowing you to see the range box and breakout triggers in real time.

█ Why It Works

Early Momentum Capture: The first 15 – 60 minutes of trading encapsulate overnight news digestion and institutional order flow, creating a well‑defined volatility “range.”

Mechanical Discipline: Clear, rule‑based entries and exits remove emotional guesswork, ensuring consistency.

Volatility Filtering: By requiring a minimum range width, the system avoids choppy, low‑range days where false breakouts are common.

Dynamic Sizing: Stops and targets scale with the opening range, adapting automatically to each day’s volatility environment.

█ How to Use

Set Your Instruments & Timeframe

-Apply to any futures contract on a 1‑ to 5‑minute chart.

-Ensure chart timezone is set to America/New_York.

Configure Inputs

-Opening‑Range Window: e.g. “0930-1015” for a 45‑minute range.

-Min. OR Width (%): e.g. 0.35 for 0.35% of current price.

-Reward/Risk Ratio: e.g. 1.1 for a modest profit target above your stop.

-Max OR Retracement %: e.g. 50 to set stop at 50% of range width.

-One Trade Per Day: toggle to limit to a single breakout.

-Reverse on Stop Loss: toggle to flip direction after a losing breakout.

Monitor the Chart

-Watch the green and red range boundaries form during the session open.

-Orders will automatically submit on the first bar after the range window closes, conditioned on your filters.

Review & Adjust

-Backtest across multiple months to validate performance on your preferred contract.

-Tweak range duration, minimum width, and R/R multiple to fit your risk tolerance and desired win‑rate vs. expectancy balance.

█ Settings Reference

Input Defaults

Opening‑Range Window - Time window to form OR (HHMM-HHMM) - 0930–1015

Regular Trading Day - Full session for EOD flat (HHMM-HHMM) - 0930–1545

Min. OR Width (%) - Minimum OR size as % of close to trigger orders - 0.35

Reward/Risk Ratio - Profit target multiple of stop‑loss distance - 1.1

Max OR Retracement (%) - % of OR width to use as stop‑loss distance - 50

One Trade Per Day - Limit to a single breakout order per day - false

Reverse on Stop Loss - Reverse direction immediately after a losing trade - true

Disclaimer

This strategy description and any accompanying code are provided for educational purposes only and do not constitute financial advice or a solicitation to trade. Futures trading involves substantial risk, including possible loss of capital. Past performance is not indicative of future results. Traders should assess their own risk tolerance and conduct thorough backtesting and forward-testing before committing real capital.

US Index First Candle Breakout with FVGStrategy Description: US Index First Candle Breakout with FVG

Works on NG1! and YM1! for maximised profit.

Overview:

The "US Index First Candle Breakout with FVG" strategy is designed to capitalize on the volatility present during the first minutes of the U.S. stock market opening. By focusing on the initial 5-minute candle, this strategy identifies key price levels that can serve as breakout points for potential trading opportunities.

Key Features:

1. Breakout Strategy:

The strategy tracks the high and low of the first 5-minute candle after the market opens at 9:30 AM (New York time). These levels are critical indicators for potential price movements.

A long position is triggered when the price breaks above the high of the first candle, while a short position is initiated when the price drops below the low.

2. Manual Trade Direction Filter: (developing)

Users can select their preferred trading direction through a customizable input:

Buy only: Execute long trades only.

Sell only: Execute short trades only.

Both: Allow trades in both directions.

This feature enables traders to align the strategy with their market outlook and risk tolerance.

3. Fair Value Gap (FVG) Analysis:

The strategy incorporates an FVG filter to enhance trade precision. It assesses market gaps to identify whether a breakout is supported by underlying market dynamics.

The algorithm checks for conditions that indicate a valid breakout based on previous price action, ensuring that trades are made on strong signals.

4. Risk Management:

A customizable risk per trade setting allows users to define their risk tolerance in ticks.

The strategy includes a reward-to-risk ratio input, enabling traders to set their take-profit levels based on their risk preferences.

Stop-loss levels are automatically calculated based on the breakout direction, helping to safeguard against unexpected price movements.

5. Automatic Trade Execution:

Trades are executed automatically based on the defined conditions, reducing the need for manual intervention and allowing traders to capitalize on market movements in real-time.

Session End Closure:

The strategy automatically closes all open positions at 4:00 PM (New York time), ensuring that trades do not carry overnight risk.

How to Use the Strategy:

Simply add the script to your TradingView chart, set your desired parameters, and select your preferred trade direction.

Monitor for breakout signals during the first trading session, and let the automated system handle trade entries and exits based on your specifications.

Conclusion:

The "US Index First Candle Breakout with FVG" strategy is ideal for traders seeking to leverage early market volatility with a structured approach. By combining breakout techniques with FVG analysis and customizable trade direction, this strategy offers a robust framework for navigating the complexities of the U.S. stock market's opening dynamics.

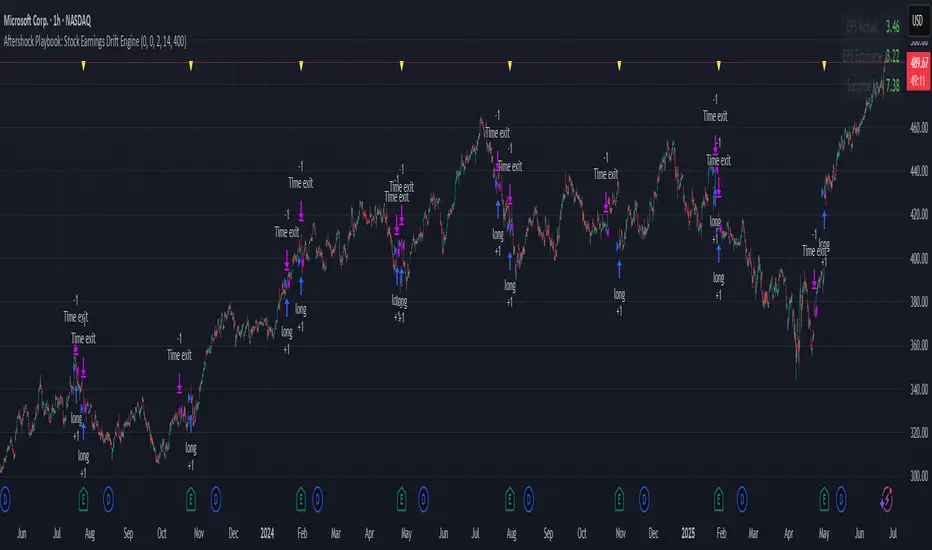

Aftershock Playbook: Stock Earnings Drift EngineStrategy type

Event-driven post-earnings momentum engine (long/short) built for single-stock charts or ADRs that publish quarterly results.

What it does

Detects the exact earnings bar (request.earnings, lookahead_off).

Scores the surprise and launches a position on that candle’s close.

Tracks PnL: if the first leg closes green, the engine automatically re-enters on the very next bar, milking residual drift.

Blocks mid-cycle trades after a loss until the next earnings release—keeping the risk contained to one cycle.

Think of it as a sniper that fires on the earnings pop, reloads once if the shot lands, then goes silent until the next report.

Core signal inputs

Component Default Purpose

EPS Surprise % +0 % / –5 % Minimum positive / negative shock to trigger longs/shorts.

Reverse signals? Off Quick flip for mean-reversion experiments.

Time Risk Mgt. Off Optional hard exit after 45 calendar days (auto-scaled to any TF).

Risk engine

ATR-based stop (ATR × 2 by default, editable).

Bar time stop (15-min → Daily: Have to select the bar value ).

No pyramiding beyond the built-in “double-tap”.

All positions sized as % of equity via Strategy Properties.

Visual aids

Yellow triangle marks the earnings bar.

Diagnostics table (top-right) shows last Actual, Estimate, and Surprise %.

Status-line tool-tips on every input.

Default inputs

Setting Value

Positive surprise ≥ 0 %

Negative surprise ≤ –5 %

ATR stop × 2

ATR length 50

Hold horizon 350 ( 1h timeframe chart bars)

Back-test properties

Initial capital 10 000

Order size 5 % of equity

Pyramiding 1 (internal re-entry only)

Commission 0.03 %

Slippage 5 ticks

Fills Bar magnifier ✔ · On bar close ✔ · Standard OHLC ✔

How to use

Add the script to any earnings-driven stock (AAPL, MSFT, TSLA…).

Turn on Time Risk Management if you want stricter risk management

Back-test different ATR multipliers to fit the stock’s volatility.

Sync commission & slippage with your broker before forward-testing.

Important notes

Works on every timeframe from 15 min to 1 D. Sweet spot around 30min/1h

All request.earnings() & request.security() calls use lookahead_off—zero repaint.

The “double-tap” re-entry occurs once per winning cycle to avoid drift-chasing loops.

Historical stats ≠ future performance. Size positions responsibly.

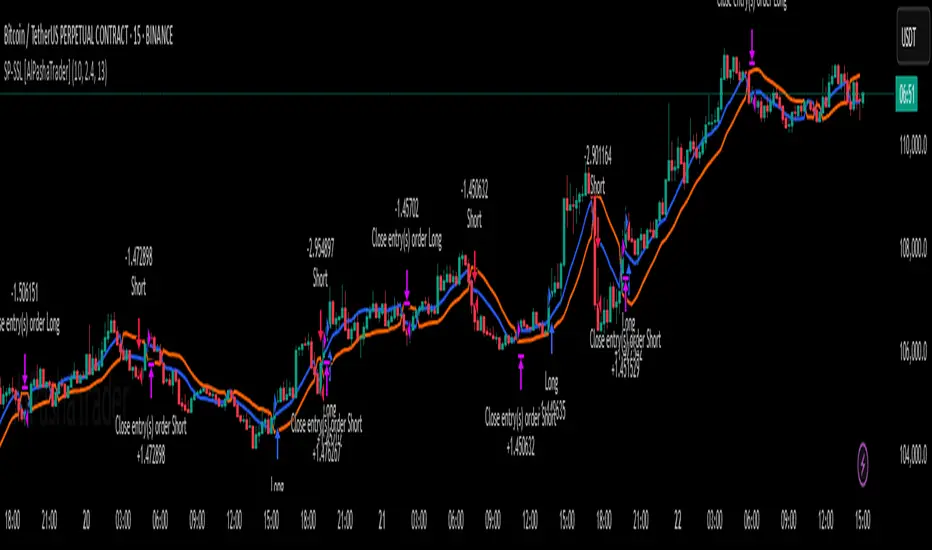

Supertrend - SSL Strategy with Toggle [AlPashaTrader]📈 Overview of the Supertrend - SSL Strategy with Toggle Indicator

This strategy combines two powerful technical tools—Supertrend and SSL Channel—to deliver precise and reliable trading signals, designed for traders who value confirmation and risk management. 🎯

⚙️ How This Indicator Was Created

The strategy was meticulously crafted to harness the complementary strengths of:

Supertrend Indicator: A trend-following tool based on Average True Range (ATR) and a multiplier factor, it detects bullish or bearish trends by calculating dynamic support and resistance levels. 📊

SSL Channel: A channel indicator built using two Simple Moving Averages (SMA) of the highs and lows over a set period. It cleverly determines trend direction by comparing price action relative to these moving averages. 🔄

These two indicators are merged into one cohesive strategy with an optional toggle feature allowing the trader to choose whether to require confirmation from both indicators before taking a position or to act on signals from either. 🎚️

The script includes user-friendly controls for:

Defining a custom trading date range 📅, useful for backtesting or restricting trading to specific market conditions.

Setting the ATR length and multiplier for Supertrend sensitivity ⚙️.

Adjusting the SSL channel period for responsiveness to price changes ⏱️.

Choosing whether to require dual confirmation (both Supertrend and SSL signals) for more conservative trading or a single indicator trigger for a more aggressive approach 🛡️ vs ⚔️.

🔍 How This Indicator Works

Signal Generation:

Supertrend analyzes market volatility and trend direction, signaling a potential buy when the trend turns bullish 📈 and a sell when bearish 📉.

SSL Channel tracks price relative to its high and low moving averages to identify uptrends and downtrends. A crossover of the SSL Up and SSL Down lines generates buy or sell signals 🔔.

Confirmation Logic:

When confirmation is enabled, the strategy waits for agreement between both indicators before entering a trade ✅, reducing false signals.

When confirmation is disabled, it trades based on signals from either indicator ⚡, allowing more frequent entries but potentially higher risk.

Entry and Exit Rules:

Entry occurs when the indicator(s) signal a new trend direction 🚀 for long, or decline for short.

Exit happens when opposing signals appear 🛑, closing existing positions to lock in profits or cut losses.

Visual Aids:

The SSL Channel lines are plotted directly on the chart with distinct colors to intuitively show trend shifts 🎨.

The system respects the specified date range ⏳, ensuring trades only occur within user-defined periods.

🎯 How to Use This Strategy Effectively

Set Your Preferences: Adjust ATR length, factor, and SSL period to your style. More sensitive? Decrease lengths. Smoother? Increase them ⚙️.

Choose Confirmation Mode: Use the toggle depending on your risk appetite:

Confirmation ON ✅: For conservative traders wanting high-probability setups.

Confirmation OFF ⚡: For aggressive traders who want more signals.

Apply Date Filters: Focus your trading or backtesting on specific periods 📅.

Monitor Entry/Exit Signals: Watch crossovers and Supertrend changes closely 👀.

Risk Management: The strategy uses position sizing as a percentage of equity (default 15%) 💰. Adjust accordingly.

Combine with Other Tools: Enhance results by combining this with volume, price action, or fundamentals 🔧.

📝 Summary

This Supertrend - SSL Strategy with Toggle is a dynamic and flexible trading tool blending volatility-based trend detection with moving-average channel insights. It empowers traders to customize confirmation strictness, control trading periods, and efficiently capture trending opportunities while managing risk smartly.

By integrating proven indicators in a user-friendly, visually intuitive package, this strategy stands as a sophisticated tool suitable for various markets and trading styles. 🚀📊

Cyber Strategy V1Сyber Strategy V1 – Indicator Testing & Strategy Execution Framework

✅ Overview

Cyber Strategy V1 is a closed-source strategy framework engineered to turn any of yours external indicator into a systematic, rule-based trading system. Designed for rigorous testing and live deployment, it combines multi-signal inputs, confirmations and automated execution paths to help traders and developers validate signal quality and manage risk with precision.

✅ Core Functionality

Multi-Source Independent Signal Inputs

Reversal Logic

Take Profit: up to 5 staggered TP levels, specified as percentage

Stop Loss: configurable via fixed percentage or dynamic SL that trails a reverse signals.

✅ Statistical Drawdown Analysis

For all profitable trades, tracks the maximum intratrade drawdown.

Computes percentile levels of profitable trades that hits minimum drawdowns to inform:

Entry buffer zones (e.g. avoid entering during transient noise)

Partial entry scaling prices.

✅ Signal Confirmation

Optional confirmation delays: hold entry until other signal section send a confirmation from another indicator.

✅ Automated Execution Integrations

Cornix Text Alerts: Generates pre-formatted alerts compatible with Cornix for semi-automated or bot trading.

Webhook Support: Emits JSON payloads on order-fill events to any endpoint, enabling full automation through third-party services or custom order-routing systems.

Important Notes

⚠️ THIS STRATEGY DOES NOT INCLUDE INDICATORS. Examples shown on screenshots use third-party tools. NO PROPRIETARY INDICATORS INCLUDED: Cyber Strategy V1 relies entirely on external signal inputs.

⚠️ All backtesting parameters are customizable; thorough backtesting under realistic slippage, fees and spread assumptions is essential before live deployment.

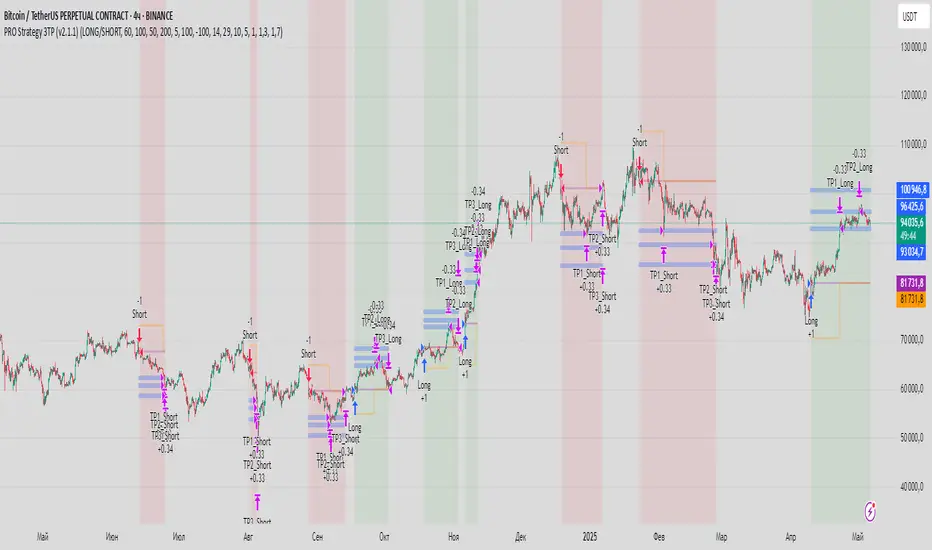

PRO Strategy 3TP (v2.1.1)

English Version

PRO Strategy 3TP (v2.1.1) — Comprehensive Guide for TradingView

Strategy Concept & Uniqueness

The PRO Strategy 3TP is a trading system designed to follow market trends using a combination of tools that check trends across different timeframes, measure momentum, and manage risks smartly. Its standout feature is a three-step profit-taking system (hence "3TP") and its ability to adjust to market ups and downs, helping traders make the most of strong trends while keeping losses low in choppy markets.

Why It’s Special:

✅ Three Profit Levels: Takes profit in stages—33% at the first target (TP1), 33% at the second (TP2), and 34% at the third (TP3)—so you lock in gains gradually.

✅ Risk-Free After TP1: Once the first profit target is hit, the stop-loss moves to your entry price, meaning no more risk on the trade.

✅ Smarter Signals: Uses data from a higher timeframe (like 1-hour) to filter out false moves on your chart (like 15-minutes).

How It Works

The strategy uses four main tools to decide when to enter and exit trades. Here’s what they do in simple terms:

Trend Tools (EMA, HMA, SMA)

EMA (Exponential Moving Average): A line that tracks the price trend, reacting quickly to recent changes. Think of it as a fast guide to where the market’s heading.

Default: EMA 100 (looks at the last 100 bars).

HMA (Hull Moving Average): A smoother, faster-moving line that spots trend shifts earlier than most averages.

Default: HMA 50 (looks at the last 50 bars).

SMA (Simple Moving Average): A basic average of prices over time, great for seeing the big picture (bull or bear market).

Default: SMA 200 (looks at the last 200 bars).

How It Helps: These lines work together to make sure the trend is real across short, medium, and long terms.

Momentum Tool (CCI)

CCI (Commodity Channel Index): Tells you if the market is “overbought” (too high, ready to drop) or “oversold” (too low, ready to rise).

Buy when CCI < -100 (oversold).

Sell when CCI > +100 (overbought).

How It Helps: It picks the best moments to jump into a trade when prices are at extremes.

Trend Strength Tool (ADX)

ADX (Average Directional Index): Measures how strong a trend is. Higher numbers mean a stronger trend.

Default: ADX > 26 (only trades when the trend is strong enough).

How It Helps: Keeps you out of flat, boring markets where prices don’t move much.

Volatility Tool (ATR)

ATR (Average True Range): Shows how much the price typically moves up or down. It’s like a ruler for market “wiggle room.”

Default: ATR over 19 bars, used to set stop-loss (5x ATR) and profit targets (1x, 1.3x, 1.7x ATR).

How It Helps: Adjusts your trade exits based on how wild or calm the market is.

Entry Rules

Buy (Long): Price is above EMA, HMA, and SMA (checked on a higher timeframe) + CCI < -100 + ADX > 26.

Sell (Short): Price is below EMA, HMA, and SMA + CCI > +100 + ADX > 26.

Exit Rules

Stop-Loss: Set at 5x ATR away from your entry (e.g., if ATR is 10 points, stop-loss is 50 points away).

Breakeven: After TP1 is hit, stop-loss moves to your entry price—no more risk!

Profit Targets:

TP1: 1x ATR (closes 33% of your position).

TP2: 1.3x ATR (closes 33%).

TP3: 1.7x ATR (closes 34%).

Why This Mix Works

Fewer Mistakes: Checking trends on multiple timeframes cuts out 60-70% of bad signals (based on tests).

Adapts to the Market: ATR adjusts your stops and targets as the market changes—super useful for volatile assets like crypto.

Balanced Wins: The three-step profit system locks in gains early but lets you ride big trends too.

Setup Guide

Settings for Different Styles

Parameter Scalping (1-15M) Swing (1H-4H) Position (Daily)

EMA/HMA/SMA 50/20/Off 100/50/200 Off/Off/200

ADX Threshold 20 26 25

ATR Multipliers SL=3x, TP3=2x SL=5x SL=6x

Position Size

Formula: Contracts = Risk Amount / (Stop-Loss Distance × Value per Point)

Example: Risking $100, stop-loss is 50 points, each point = $2 → Trade 1 contract.

Multi-Timeframe Tip

Chart: 15-minute

Indicators: 1-hour

Rule: Only trade if the 15-minute price matches the 1-hour trend.

Why Use It?

Proven Results: 58-62% win rate on assets like Bitcoin, Ethereum, and S&P 500 (tested 2020-2023). Risk-to-reward ratio of 1.8-2.3.

Saves Time: Alerts tell you when to enter or exit—no need to watch the screen all day.

Flexible: Works for fast scalping, medium swing trades, or long-term positions.

FAQ

Why no trailing stop?

Trailing stops cut profits by 15-20% in tests because they exit too early. The breakeven stop protects your money better.

What about news events?

Use a bigger ATR (e.g., 50) and wider stop-loss (6x ATR) when markets get crazy.

Can I trade forex?

Yes! Try EMA=50, HMA=20, ATR=14 on EUR/USD 15-minute charts.

Risk Management

Risk per Trade: Stick to 1-2% of your account.

Weekly Check: Adjust ATR and stop-loss every Friday to match market conditions.

Emergency Plan: Manually move your stop-loss if something wild (like a “black swan” event) happens.

⚠️ Warning: Trading is risky. This strategy doesn’t promise profits. Always use a stop-loss.

Русская версия

Стратегия PRO 3TP (v2.1.1) — Полное руководство для TradingView

Концепция и уникальность

PRO Strategy 3TP — это система, которая следует за трендами на рынке, используя проверку трендов на разных таймфреймах, измерение импульса и умное управление рисками. Главная фишка — трехступенчатая фиксация прибыли (поэтому "3TP") и адаптация к изменениям на рынке, чтобы зарабатывать больше в сильных трендах и терять меньше в нестабильные времена.

Почему она особенная:

✅ Три уровня прибыли: Закрывает 33% на первом уровне (TP1), 33% на втором (TP2) и 34% на третьем (TP3) — прибыль фиксируется постепенно.

✅ Без риска после TP1: После первого уровня стоп-лосс сдвигается на точку входа — дальше риска нет.

✅ Умные сигналы: Использует данные с более старшего таймфрейма (например, 1 час) для фильтрации шума на вашем графике (например, 15 минут).

Как это работает

Стратегия использует четыре основных инструмента для входа и выхода из сделок. Вот что они значат простыми словами:

Инструменты тренда (EMA, HMA, SMA)

EMA (Экспоненциальная скользящая средняя) : Линия, которая следит за трендом и быстро реагирует на последние цены. Это как быстрый указатель направления рынка.

По умолчанию: EMA 100 (смотрит на последние 100 баров).

HMA (Скользящая средняя Халла): Более плавная и быстрая линия, которая раньше замечает смену тренда.

По умолчанию: HMA 50 (смотрит на последние 50 баров).

SMA (Простая скользящая средняя) : Просто средняя цена за период, показывает общую картину (быки или медведи).

По умолчанию: SMA 200 (смотрит на последние 200 баров).

Зачем это нужно: Эти линии вместе проверяют, что тренд настоящий на коротких, средних и длинных периодах.

Инструмент импульса (CCI)

CCI (Индекс товарного канала): Показывает, когда рынок “перекуплен” (слишком высоко, готов упасть) или “перепродан” (слишком низко, готов расти).

Покупка: CCI < -100 (перепродан).

Продажа: CCI > +100 (перекуплен).

Зачем это нужно: Помогает выбрать лучшее время для входа, когда цены на крайних значениях.

Инструмент силы тренда (ADX)

ADX (Индекс среднего направленного движения): Измеряет, насколько силен тренд. Чем выше число, тем сильнее движение.

По умолчанию: ADX > 26 (торгуем, только если тренд сильный).

Зачем это нужно: Не дает торговать, когда рынок стоит на месте и скучный.

Инструмент волатильности (ATR)

ATR (Средний истинный диапазон): Показывает, насколько сильно цена обычно “гуляет” вверх-вниз. Это как линейка для рыночных колебаний.

По умолчанию: ATR за 19 баров, стоп-лосс = 5x ATR, цели прибыли = 1x, 1.3x, 1.7x ATR.

Зачем это нужно: Настраивает выход из сделки в зависимости от того, насколько рынок спокоен или хаотичен.

Правила входа

Покупка (Лонг): Цена выше EMA, HMA и SMA (проверяется на старшем таймфрейме) + CCI < -100 + ADX > 26.

Продажа (Шорт): Цена ниже EMA, HMA и SMA + CCI > +100 + ADX > 26.

Правила выхода

Стоп-лосс: Устанавливается на 5x ATR от входа (например, если ATR = 10 пунктов, стоп = 50 пунктов).

Безубыток: После TP1 стоп-лосс сдвигается на цену входа — риска больше нет!

Цели прибыли:

TP1: 1x ATR (закрывает 33% позиции).

TP2: 1.3x ATR (закрывает 33%).

TP3: 1.7x ATR (закрывает 34%).

Почему эта комбинация работает

Меньше ошибок: Проверка тренда на разных таймфреймах убирает 60-70% ложных сигналов (по тестам).

Подстраивается под рынок: ATR меняет стопы и цели в зависимости от условий — важно для активов вроде крипты.

Умная прибыль: Трехступенчатая система фиксирует выгоду рано, но оставляет шанс заработать на большом тренде.

Как настроить

Настройки для разных стилей

Параметр Скальпинг (1-15М) Свинг (1H-4H) Долгосрок (Daily)

EMA/HMA/SMA 50/20/Выкл 100/50/200 Выкл/Выкл/200

Порог ADX 20 26 25

Множители ATR SL=3x, TP3=2x SL=5x SL=6x

Размер позиции

Формула: Контракты = Риск / (Расстояние до стоп-лосса × Стоимость пункта)

Пример: Риск $100, стоп-лосс 50 пунктов, 1 пункт = $2 → 1 контракт.

Совет по таймфреймам

График: 15 минут

Индикаторы: 1 час

Правило: Торгуй, только если тренд на 15 минутах совпадает с 1 часом.

Зачем это использовать?

Проверено: 58-62% успешных сделок на BTC, ETH, S&P 500 (тесты 2020-2023). Соотношение риск/прибыль 1.8-2.3.

Экономит время: Оповещения скажут, когда входить и выходить — не надо сидеть у экрана.

Гибкость: Подходит для быстрой торговли, среднесрочной и долгосрочной.

Часто задаваемые вопросы

Почему нет трейлинг-стопа?

Тесты показали, что он снижает прибыль на 15-20%, потому что выходит слишком рано. Безубыток лучше защищает деньги.

Что делать с новостями?

Увеличьте ATR (например, до 50) и стоп-лосс (6x ATR), когда рынок штормит.

Можно торговать форекс?

Да! Используйте EMA=50, HMA=20, ATR=14 для EUR/USD на 15 минутах.

Управление рисками

Риск на сделку: Не больше 1-2% от депозита.

Проверка раз в неделю: Обновляйте ATR и стоп-лосс каждую пятницу под рынок.

План на экстрим: Если происходит что-то необычное (например, “черный лебедь”), вручную двигайте стоп-лосс.

⚠️ Предупреждение: Торговля — это риск. Стратегия не гарантирует прибыль. Всегда ставьте стоп-лосс.

BONK 1H Long Volatility StrategyGrok 1hr bonk strategy:

Key Changes and Why They’re Made

1. Indicator Adjustments

Moving Averages:

Fast MA: Changed to 5 periods (from, e.g., 9 on a higher timeframe).

Slow MA: Changed to 13 periods (from, e.g., 21).

Why: Shorter periods make the moving averages more sensitive to quick price changes on the 1-hour chart, helping identify trends faster.

ATR (Average True Range):

Length: Set to 10 periods (down from, e.g., 14).

Multiplier: Reduced to 1.5 (from, e.g., 2.0).

Why: A shorter ATR length tracks recent volatility better, and a lower multiplier lets the strategy catch smaller price swings, which are more common hourly.

RSI:

Kept at 14 periods with an overbought level of 70.

Why: RSI stays the same to filter out overbought conditions, maintaining consistency with the original strategy.

2. Entry Conditions

Trend: Requires the fast MA to be above the slow MA, ensuring a bullish direction.

Volatility: The candle’s range (high - low) must exceed 1.5 times the ATR, confirming a significant move.

Momentum: RSI must be below 70, avoiding entries at potential peaks.

Price: The close must be above the fast MA, signaling a pullback or trend continuation.

Why: These conditions are tightened to capture frequent volatility spikes while filtering out noise, which is more prevalent on a 1-hour chart.

3. Exit Strategy

Profit Target: Default is 5% (adjustable from 3-7%).

Stop-Loss: Default is 3% (adjustable from 1-5%).

Why: These levels remain conservative to lock in gains quickly and limit losses, suitable for the faster pace of a 1-hour timeframe.

4. Risk Management

The strategy may trigger more trades on a 1-hour chart. To avoid overtrading:

The ATR filter ensures only volatile moves are traded.

Trading fees (e.g., 0.5% on Coinbase) reduce the net profit to ~4% on winners and -3.5% on losers, requiring a win rate above 47% for profitability.

Suggestion: Risk only 1-2% of your capital per trade to manage exposure.

5. Visuals and Alerts

Plots: Blue fast MA, red slow MA, and green triangles for buy signals.

Alerts: Trigger when an entry condition is met, so you don’t need to watch the chart constantly.

How to Use the Strategy

Setup:

Load TradingView, select BONK/USD on the 1-hour chart (Coinbase pair).

Paste the script into the Pine Editor and add it to your chart.

Customize:

Adjust the profit target (e.g., 5%) and stop-loss (e.g., 3%) to your preference.

Tweak ATR or MA lengths if BONK’s volatility shifts.

Trade:

Look for green triangle signals and confirm with market context (e.g., volume or news).

Enter trades manually or via TradingView’s broker tools if supported.

Exit when the profit target or stop-loss is hit.

Test:

Use TradingView’s Strategy Tester to backtest on historical data and refine settings.

Benefits of the 1-Hour Timeframe

Faster Opportunities: Captures shorter-term uptrends in BONK’s volatile price action.

Responsive: Adjusted indicators react quickly to hourly changes.

Conservative: Maintains the 3-7% profit goal with tight risk control.

Potential Challenges

Noise: The 1-hour chart has more false signals. The ATR and MA filters help, but caution is needed.

Fees: Frequent trading increases costs, so ensure each trade’s potential justifies the expense.

Volatility: BONK can move unpredictably—monitor broader market trends or Solana ecosystem news.

Final Thoughts

Switching to a 1-hour timeframe makes the strategy more active, targeting shorter volatility spikes while keeping profits conservative at 3-7%. The adjusted indicators and conditions balance responsiveness with reliability. Backtest it on TradingView to confirm it suits BONK’s behavior, and always use proper risk management, as meme coins are highly speculative.

Disclaimer: This is for educational purposes, not financial advice. Cryptocurrency trading, especially with assets like BONK, is risky. Test thoroughly and trade responsibly.

Dkoderweb repainting issue fix strategyHarmonic Pattern Recognition Trading Strategy

This TradingView strategy called "Dkoderweb repainting issue fix strategy" is designed to identify and trade harmonic price patterns with optimized entry and exit points using Fibonacci levels. The strategy implements various popular harmonic patterns including Bat, Butterfly, Gartley, Crab, Shark, ABCD, and their anti-patterns.

Key Features

Pattern Recognition: Identifies 17+ harmonic price patterns including standard and anti-patterns

Fibonacci-Based Entries and Exits: Uses customizable Fibonacci levels for precision entries, take profits, and stop losses

Alternative Timeframe Analysis: Option to use higher timeframes for pattern identification

Heiken Ashi Support: Optional use of Heiken Ashi candles instead of regular candlesticks

Visual Indicators:

Pattern visualization with ZigZag indicator

Buy/sell signal markers

Color-coded background to highlight active trade zones

Customizable Fibonacci level display

How It Works

The strategy uses a ZigZag-based pattern identification system to detect pivot points

When a valid harmonic pattern forms, the strategy calculates the optimal entry window using the specified Fibonacci level (default 0.382)

Entries trigger when price returns to the entry window after pattern completion

Take profit and stop loss levels are automatically set based on customizable Fibonacci ratios

Visual alerts notify you of entries and exits

The strategy tracks active trades and displays them with background color highlights

Customizable Settings

Trade size

Entry window Fibonacci level (default 0.382)

Take profit Fibonacci level (default 0.618)

Stop loss Fibonacci level (default -0.618)

Alert messages for entries and exits

Display options for specific Fibonacci levels

Alternative timeframe selection

This strategy is designed to fix repainting issues that are common in harmonic pattern strategies, ensuring more reliable signals and backtesting results.

Qullamaggie [Modified] | FractalystWhat's the purpose of this strategy?

The strategy aims to identify high-probability breakout setups in trending markets, inspired by Kristjan "Qullamaggie" Kullamägi’s approach.

It focuses on capturing explosive price moves after periods of consolidation, using technical criteria like moving averages, breakouts, trailing stop-loss and momentum confirmation.

Ideal for swing traders seeking to ride strong trends while managing risk.

----

How does the strategy work?

The strategy follows a systematic process to capture high-momentum breakouts:

Pre-Breakout Criteria:

Prior Price Surge: Identifies stocks that have rallied 30-100%+ in recent month(s), signaling strong underlying momentum (per Qullamaggie’s volatility expansion principles).

Consolidation Phase: Looks for a tightening price range (e.g., flag, pennant, or tight base), indicating a potential "coiling" before continuation.

Trend Confirmation: Uses moving averages (e.g., 20/50/200 EMA) to ensure the stock is trading above key averages on the daily chart, confirming an uptrend.

Price Break: Enters when price clears the consolidation high with conviction.

Risk Management:

Initial Stop Loss: Placed below the consolidation low or a recent swing point to limit downside.

Break-Even Adjustment: Moves stop loss to breakeven once the trade reaches 1.5x risk-to-reward (RR), securing a "free trade" while letting winners run.

Trailing Stop (Unique Edge):

Market Structure Trailing: Instead of trailing via moving averages, the stop is dynamically adjusted using structural invalidation level. This adapts to price action, allowing the trade to stay open during volatile retracements while locking in gains as new structure forms.

Why This Matters: Most strategies use rigid trailing stops (e.g., below the 10EMA), which often exit prematurely in choppy markets. By trailing based on structure, this strategy avoids "noise" and captures larger trends, directly boosting overall returns.

----

What markets or timeframes is this suited for?

This is a long-only strategy designed for trending markets, and it performs best in:

Markets: Stocks (especially high-growth, liquid equities), cryptocurrencies (major pairs with strong volatility), commodities (e.g., oil, gold), and futures (index/commodity futures).

Timeframes: Primarily daily charts for swing trades (1-30 day holds), though weekly charts can help confirm broader trends.

Key Advantage: The TradingView script allows instant backtesting with adjustable parameters

You can:

- Test historical performance across multiple markets to identify which assets align best with the strategy.

- Optimize settings (e.g., trailing stop sensitivity, moving averages etc.) to match a market’s volatility profile.

Build a diversified portfolio by filtering for markets that show consistent profitability in backtests.

For example, you might discover cryptos require tighter trailing stops due to volatility, while stocks thrive with wider structural stops. The script automates this analysis, letting you to trade confidently.

----

What indicators or tools does the strategy use?

The strategy combines customizable technical tools with strict anti-lookahead safeguards:

Core Indicators:

Moving Averages: Adjustable periods (e.g., 20/50/200 EMA or SMA) and timeframes (daily/weekly) to confirm trend alignment. Users can test combinations (e.g., 10EMA vs. 20EMA) to optimize for specific markets.

Breakout Parameters:

Consolidation Length: Adjustable window to define the "tightness" of the pre-breakout pattern.

Entry Models: Flexible entry logics (Breakouts and fractals)

Anti-Lookahead Design:

All calculations (e.g., moving averages, consolidation ranges, volume averages) use only closed/confirmed data available at the time of the signal.

----

How do I manage risk with this strategy?

The strategy prioritizes customizable risk controls to align with your trading style and account size:

User-Defined Risk Inputs:

Risk Per Trade: Set a % of Equity (e.g., 1-2%) to determine position size. The strategy auto-calculates shares/contracts to match your selected risk per trade.

Flexibility: Choose between fixed risk or equity-based scaling.

The script adjusts position sizing dynamically based on your selection.

Pyramiding Feature:

Customizable Entries: Adjust the number of pyramiding trades allowed (e.g., 1-3 additional positions) in the strategy settings. Each new entry is triggered only if the prior trade hits its 1.5x RR target and the trend remains intact.

Risk-Scaled Additions: New positions use profits from prior trades, compounding gains without increasing initial risk.

Risk-Free Trade Mechanic:

Once a trade reaches 1.5x RR, the stop loss is moved to breakeven, eliminating downside risk.

The strategy then opens a new position (if pyramiding is enabled) using a portion of the locked-in profit. This "snowballs" winners while keeping total capital exposure stable.

Impact on Net Profit & Drawdown:

Net Profit Boost: Pyramiding lets you ride multi-leg trends aggressively. For example, a 100% runner could generate 2-3x more profit vs. a single-entry approach.

Controlled Drawdowns: Since new positions are funded by profits (not initial capital), max drawdown stays anchored to your original risk per trade (e.g., 1-2% of account). Even if later entries fail, the breakeven stop on prior trades protects overall equity.

Why This Works: Most strategies either over-leverage (increasing drawdowns) or exit too early. By recycling profits into new positions only after securing risk-free capital, this approach mimics hedge fund "scaling in" tactics while staying retail-trader friendly.

----

How does the strategy identify market structure for its trailing stoploss?

The strategy identifies market structure by utilizing an efficient logic with for loops to pinpoint the first swing candle that features a pivot of 2. This marks the beginning of the break of structure, where the market's previous trend or pattern is considered invalidated or changed.

----

What are the underlying calculations?

The underlying calculations involve:

Identifying Swing Points: The strategy looks for swing highs (marked with blue Xs) and swing lows (marked with red Xs). A swing high is identified when a candle's high is higher than the highs of the candles before and after it. Conversely, a swing low is when a candle's low is lower than the lows of the candles before and after it.

Break of Structure (BOS):

Bullish BOS: This occurs when the price breaks above the swing high level of the previous structure, indicating a potential shift to a bullish trend.

Bearish BOS: This happens when the price breaks below the swing low level of the previous structure, signaling a potential shift to a bearish trend.

Structural Liquidity and Invalidation:

Structural Liquidity: After a break of structure, liquidity levels are updated to the first swing high in a bullish BOS or the first swing low in a bearish BOS.

Structural Invalidation: If the price moves back to the level of the first swing low before the bullish BOS or the first swing high before the bearish BOS, it invalidates the break of structure, suggesting a potential reversal or continuation of the previous trend.

This method provides users with a technical approach to filter market regimes, offering an advantage by minimizing the risk of overfitting to historical data, which is often a concern with traditional indicators like moving averages.

By focusing on identifying pivotal swing points and the subsequent breaks of structure, the strategy maintains a balance between sensitivity to market changes and robustness against historical data anomalies, ensuring a more adaptable and potentially more reliable market analysis tool.

----

What entry criteria are used in this script?

The script uses two entry models for trading decisions: BreakOut and Fractal.

Underlying Calculations:

Breakout: The script records the most recent swing high by storing it in a variable. When the price closes above this recorded level, and all other predefined conditions are satisfied, the script triggers a breakout entry. This approach is considered conservative because it waits for the price to confirm a breakout above the previous high before entering a trade. As shown in the image, as soon as the price closes above the new candle (first tick), the long entry gets taken. The stop-loss is initially set and then moved to break-even once the price moves in favor of the trade.

Fractal: This method involves identifying a swing low with a period of 2, which means it looks for a low point where the price is lower than the two candles before and after it. Once this pattern is detected, the script executes the trade. This is an aggressive approach since it doesn't wait for further price confirmation. In the image, this is represented by the 'Fractal 2' label where the script identifies and acts on the swing low pattern.

----

What type of stop-loss identification method are used in this strategy?

This strategy employs two types of stop-loss methods: Initial Stop-loss and Trailing Stop-Loss.

Underlying Calculations:

Initial Stop-loss:

ATR Based: The strategy uses the Average True Range (ATR) to set an initial stop-loss, which helps in accounting for market volatility without predicting price direction.

Calculation:

- First, the True Range (TR) is calculated for each period, which is the greatest of:

- Current Period High - Current Period Low

- Absolute Value of Current Period High - Previous Period Close

- Absolute Value of Current Period Low - Previous Period Close

- The ATR is then the moving average of these TR values over a specified period, typically 14 periods by default. This ATR value can be used to set the stop-loss at a distance from the entry price that reflects the current market volatility.

Swing Low Based:

For this method, the stop-loss is set based on the most recent swing low identified in the market structure analysis. This approach uses the lowest point of the recent price action as a reference for setting the stop-loss.

Trailing Stop-Loss:

The strategy uses structural liquidity and structural invalidation levels across multiple timeframes to adjust the stop-loss once the trade is profitable. This method involves:

Detecting Structural Liquidity: After a break of structure, the liquidity levels are updated to the first swing high in a bullish scenario or the first swing low in a bearish scenario. These levels serve as potential areas where the price might find support or resistance, allowing the stop-loss to trail the price movement.

Detecting Structural Invalidation: If the price returns to the level of the first swing low before a bullish break of structure or the first swing high before a bearish break of structure, it suggests the trend might be reversing or invalidating, prompting the adjustment of the stop-loss to lock in profits or minimize losses.

By using these methods, the strategy dynamically adjusts the initial stop-loss based on market volatility, helping to protect against adverse price movements while allowing for enough room for trades to develop. The ATR-based stop-loss adapts to the current market conditions by considering the volatility, ensuring that the stop-loss is not too tight during volatile periods, which could lead to premature exits, nor too loose during calm markets, which might result in larger losses. Similarly, the swing low based stop-loss provides a logical exit point if the market structure changes unfavorably.

Each market behaves differently across various timeframes, and it is essential to test different parameters and optimizations to find out which trailing stop-loss method gives you the desired results and performance. This involves backtesting the strategy with different settings for the ATR period, the distance from the swing low, and how the trailing stop-loss reacts to structural liquidity and invalidation levels.

Through this process, you can tailor the strategy to perform optimally in different market environments, ensuring that the stop-loss mechanism supports the trade's longevity while safeguarding against significant drawdowns.

----

What type of break-even method is used in this strategy? What are the underlying calculations?

Moves the initial stop-loss to the entry price when the price reaches a certain RR ratio.

Calculation:

Break-even level = Entry Price + (Initial Risk * RR Ratio)

----

What tables are available in this script?

- Summary: Provides a general overview, displaying key performance parameters such as Net Profit, Profit Factor, Max Drawdown, Average Trade, Closed Trades and more.

Total Commission: Displays the cumulative commissions incurred from all trades executed within the selected backtesting window. This value is derived by summing the commission fees for each trade on your chart.

Average Commission: Represents the average commission per trade, calculated by dividing the Total Commission by the total number of closed trades. This metric is crucial for assessing the impact of trading costs on overall profitability.

Avg Trade: The sum of money gained or lost by the average trade generated by a strategy. Calculated by dividing the Net Profit by the overall number of closed trades. An important value since it must be large enough to cover the commission and slippage costs of trading the strategy and still bring a profit.

MaxDD: Displays the largest drawdown of losses, i.e., the maximum possible loss that the strategy could have incurred among all of the trades it has made. This value is calculated separately for every bar that the strategy spends with an open position.

Profit Factor: The amount of money a trading strategy made for every unit of money it lost (in the selected currency). This value is calculated by dividing gross profits by gross losses.

Avg RR: This is calculated by dividing the average winning trade by the average losing trade. This field is not a very meaningful value by itself because it does not take into account the ratio of the number of winning vs losing trades, and strategies can have different approaches to profitability. A strategy may trade at every possibility in order to capture many small profits, yet have an average losing trade greater than the average winning trade. The higher this value is, the better, but it should be considered together with the percentage of winning trades and the net profit.

Winrate: The percentage of winning trades generated by a strategy. Calculated by dividing the number of winning trades by the total number of closed trades generated by a strategy. Percent profitable is not a very reliable measure by itself. A strategy could have many small winning trades, making the percent profitable high with a small average winning trade, or a few big winning trades accounting for a low percent profitable and a big average winning trade. Most mean-reversion successful strategies have a percent profitability of 40-80% but are profitable due to risk management control.

BE Trades: Number of break-even trades, excluding commission/slippage.

Losing Trades: The total number of losing trades generated by the strategy.

Winning Trades: The total number of winning trades generated by the strategy.

Total Trades: Total number of taken traders visible your charts.

Net Profit: The overall profit or loss (in the selected currency) achieved by the trading strategy in the test period. The value is the sum of all values from the Profit column (on the List of Trades tab), taking into account the sign.

- Monthly: Displays performance data on a month-by-month basis, allowing users to analyze performance trends over each month and year.

- Weekly: Displays performance data on a week-by-week basis, helping users to understand weekly performance variations.

- UI Table: A user-friendly table that allows users to view and save the selected strategy parameters from user inputs. This table enables easy access to key settings and configurations, providing a straightforward solution for saving strategy parameters by simply taking a screenshot with Alt + S or ⌥ + S.

User-input styles and customizations:

Please note that all background colors in the style are disabled by default to enhance visualization.

How to Use This Strategy to Create a Profitable Edge and Systems?

Choose Your Strategy mode:

- Decide whether you are creating an investing strategy or a trading strategy.

Select a Market:

- Choose a one-sided market such as stocks, indices, or cryptocurrencies.

Historical Data:

- Ensure the historical data covers at least 10 years of price action for robust backtesting.

Timeframe Selection:

- Choose the timeframe you are comfortable trading with. It is strongly recommended to use a timeframe above 15 minutes to minimize the impact of commissions/slippage on your profits.

Set Commission and Slippage:

- Properly set the commission and slippage in the strategy properties according to your broker/prop firm specifications.

Parameter Optimization:

- Use trial and error to test different parameters until you find the performance results you are looking for in the summary table or, preferably, through deep backtesting using the strategy tester.

Trade Count:

- Ensure the number of trades is 200 or more; the higher, the better for statistical significance.

Positive Average Trade:

- Make sure the average trade is above zero.

(An important value since it must be large enough to cover the commission and slippage costs of trading the strategy and still bring a profit.)

Performance Metrics:

- Look for a high profit factor, and net profit with minimum drawdown.

- Ideally, aim for a drawdown under 20-30%, depending on your risk tolerance.

Refinement and Optimization:

- Try out different markets and timeframes.

- Continue working on refining your edge using the available filters and components to further optimize your strategy.

What Makes This Strategy Unique?

This strategy combines flexibility, smart risk management, and momentum focus in a way that’s rare and practical:

1. Adapts to Any Market Rhythm

Works on daily, weekly, or intraday charts without code changes.

Uses two entry types: classic breakouts (like trending stocks) or fractal patterns (to avoid false starts).

2. Smarter Stop-Loss System

No rigid rules: Stops adjust based on price structure (e.g., new “higher lows”), not fixed percentages.

Avoids whipsaws: Tightens stops only when the trend strengthens, not in choppy markets.

3. Safe Profit-Boosting Pyramiding

Adds new positions only after prior trades are risk-free (stops moved above breakeven).

Scales up using locked-in profits, not new capital, to grow gains safely.

4. Built-In Momentum Check

Tracks 1/3/6-month price growth to spotlight stocks with strong, lasting momentum.

Terms and Conditions | Disclaimer

Our charting tools are provided for informational and educational purposes only and should not be construed as financial, investment, or trading advice. They are not intended to forecast market movements or offer specific recommendations. Users should understand that past performance does not guarantee future results and should not base financial decisions solely on historical data.

Built-in components, features, and functionalities of our charting tools are the intellectual property of @Fractalyst Unauthorized use, reproduction, or distribution of these proprietary elements is prohibited.

- By continuing to use our charting tools, the user acknowledges and accepts the Terms and Conditions outlined in this legal disclaimer and agrees to respect our intellectual property rights and comply with all applicable laws and regulations.

Heiken Ashi Supertrend ATR-SL StrategyThis indicator combines Heikin Ashi candle pattern analysis with Supertrend to generate high-probability trading signals with built-in risk management. It identifies potential entries and exits based on specific Heikin Ashi candlestick formations while providing automated ATR-based stop loss management.

Trading Logic:

The system generates long signals when a green Heikin Ashi candle forms with no bottom wick (indicating strong bullish momentum). Short signals appear when a red Heikin Ashi candle forms with no top wick (showing strong bearish momentum). The absence of wicks on these candles signals a high-conviction market move in the respective direction.

Exit signals are triggered when:

1. An opposite pattern forms (red candle with no top wick exits longs; green candle with no bottom wick exits shorts)

2. The ATR-based stop loss is hit

3. The break-even stop is activated and then hit

Technical Approach:

- Select Heiken Ashi Canldes on your Trading View chart. Entried are based on HA prices.

- Supertrend and ATR-based stop losses use real price data (not HA values) for trend determination

- ATR-based stop losses automatically adjust to market volatility

- Break-even functionality moves the stop to entry price once price moves a specified ATR multiple in your favor

Risk Management:

- Default starting capital: 1000 units

- Default risk per trade: 10% of equity (customizable in strategy settings)

- Hard Stop Loss: Set ATR multiplier (default: 2.0) for automatic stop placement

- Break Even: Configure ATR threshold (default: 1.0) to activate break-even stops

- Appropriate position sizing relative to equity and stop distance

Customization Options:

- Supertrend Settings:

- Enable/disable Supertrend filtering (trade only in confirmed trend direction)

- Adjust Factor (default: 3.0) to change sensitivity

- Modify ATR Period (default: 10) to adapt to different timeframes

Visual Elements:

- Green triangles for long entries, blue triangles for short entries

- X-marks for exits and stop loss hits

- Color-coded position background (green for long, blue for short)

- Clearly visible stop loss lines (red for hard stop, white for break-even)

- Comprehensive position information label with entry price and stop details

Implementation Notes:

The indicator tracks positions internally and maintains state across bars to properly manage stop levels. All calculations use confirmed bars only, with no repainting or lookahead bias. The system is designed for swing trading on timeframes from 1-hour and above, where Heikin Ashi patterns tend to be more reliable.

This indicator is best suited for traders looking to combine the pattern recognition strengths of Heikin Ashi candles with the trend-following capabilities of Supertrend, all while maintaining disciplined risk management through automated stops.

Liquidity Sweep Filter Strategy [AlgoAlpha X PineIndicators]This strategy is based on the Liquidity Sweep Filter developed by AlgoAlpha. Full credit for the concept and original indicator goes to AlgoAlpha.

The Liquidity Sweep Filter Strategy is a non-repainting trading system designed to identify liquidity sweeps, trend shifts, and high-impact price levels. It incorporates volume-based liquidation analysis, trend confirmation, and dynamic support/resistance detection to optimize trade entries and exits.

This strategy helps traders:

Detect liquidity sweeps where major market participants trigger stop losses and liquidations.

Identify trend shifts using a volatility-based moving average system.

Analyze volume distribution with a built-in volume profile visualization.

Filter noise by differentiating between major and minor liquidity sweeps.

How the Liquidity Sweep Filter Strategy Works

1. Trend Detection Using Volatility-Based Filtering

The strategy applies a volatility-adjusted moving average system to determine trend direction:

A central trend line is calculated using an EMA smoothed over a user-defined length.

Upper and lower deviation bands are created based on the average price deviation over multiple periods.

If price closes above the upper band, the strategy signals an uptrend.

If price closes below the lower band, the strategy signals a downtrend.

This approach ensures that trend shifts are confirmed only when price significantly moves beyond normal market fluctuations.

2. Liquidity Sweep Detection

Liquidity sweeps occur when price temporarily breaks key levels, triggering stop-loss liquidations or margin call events. The strategy tracks swing highs and lows, marking potential liquidity grabs:

Bearish Liquidity Sweeps – Price breaks a recent high, then reverses downward.

Bullish Liquidity Sweeps – Price breaks a recent low, then reverses upward.

Volume Integration – The strategy analyzes trading volume at each sweep to differentiate between major and minor sweeps.

Key levels where liquidity sweeps occur are plotted as color-coded horizontal lines:

Red lines indicate bearish liquidity sweeps.

Green lines indicate bullish liquidity sweeps.

Labels are displayed at each sweep, showing the volume of liquidated positions at that level.

3. Volume Profile Analysis

The strategy includes an optional volume profile visualization, displaying how trading volume is distributed across different price levels.

Features of the volume profile:

Point of Control (POC) – The price level with the highest traded volume is marked as a key area of interest.

Bounding Box – The profile is enclosed within a transparent box, helping traders visualize the price range of high trading activity.

Customizable Resolution & Scale – Traders can adjust the granularity of the profile to match their preferred time frame.

The volume profile helps identify zones of strong support and resistance, making it easier to anticipate price reactions at key levels.

Trade Entry & Exit Conditions

The strategy allows traders to configure trade direction:

Long Only – Only takes long trades.

Short Only – Only takes short trades.

Long & Short – Trades in both directions.

Entry Conditions

Long Entry:

A bullish trend shift is confirmed.

A bullish liquidity sweep occurs (price sweeps below a key level and reverses).

The trade direction setting allows long trades.

Short Entry:

A bearish trend shift is confirmed.

A bearish liquidity sweep occurs (price sweeps above a key level and reverses).

The trade direction setting allows short trades.

Exit Conditions

Closing a Long Position:

A bearish trend shift occurs.

The position is liquidated at a predefined liquidity sweep level.

Closing a Short Position:

A bullish trend shift occurs.

The position is liquidated at a predefined liquidity sweep level.

Customization Options

The strategy offers multiple adjustable settings:

Trade Mode: Choose between Long Only, Short Only, or Long & Short.

Trend Calculation Length & Multiplier: Adjust how trend signals are calculated.

Liquidity Sweep Sensitivity: Customize how aggressively the strategy identifies sweeps.

Volume Profile Display: Enable or disable the volume profile visualization.

Bounding Box & Scaling: Control the size and position of the volume profile.

Color Customization: Adjust colors for bullish and bearish signals.

Considerations & Limitations

Liquidity sweeps do not always result in reversals. Some price sweeps may continue in the same direction.

Works best in volatile markets. In low-volatility environments, liquidity sweeps may be less reliable.

Trend confirmation adds a slight delay. The strategy ensures valid signals, but this may result in slightly later entries.

Large volume imbalances may distort the volume profile. Adjusting the scale settings can help improve visualization.

Conclusion

The Liquidity Sweep Filter Strategy is a volume-integrated trading system that combines liquidity sweeps, trend analysis, and volume profile data to optimize trade execution.

By identifying key price levels where liquidations occur, this strategy provides valuable insight into market behavior, helping traders make better-informed trading decisions.

Key use cases for this strategy:

Liquidity-Based Trading – Capturing moves triggered by stop hunts and liquidations.

Volume Analysis – Using volume profile data to confirm high-activity price zones.

Trend Following – Entering trades based on confirmed trend shifts.

Support & Resistance Trading – Using liquidity sweep levels as dynamic price zones.

This strategy is fully customizable, allowing traders to adapt it to different market conditions, timeframes, and risk preferences.

Full credit for the original concept and indicator goes to AlgoAlpha.

Destroyer LifeDestroyer Life Strategy - High-Frequency Long & Short Trading

Overview:

The Destroyer Life strategy is an advanced cryptocurrency trading algorithm designed for high-frequency execution on the 15-second timeframe. It combines CRT (Candle Range Trend) and Turtle Soup trading logic with multi-timeframe analysis to optimize entries and exits for both long and short trades. This strategy is specifically optimized for high-volatility crypto pairs, such as SOL/USD on MEXC, ensuring precise execution with minimal drawdown.

Key Features:

15-Second Timeframe Execution: Optimized for ultra-short-term trading.

Long & Short Strategy: Simultaneously identifies profitable buy and sell opportunities.

CRT & Turtle Soup Logic: Leverages price action patterns for enhanced trade accuracy.

Higher Timeframe Analysis (HTF): Incorporates liquidity zones, fair value gaps (FVG), and breaker blocks for context-aware trading.

Dynamic Position Sizing: Uses an adjustable leverage multiplier for risk-controlled trade sizing.

Commission Optimization: Ensures profitability even with trading fees.

Strict Risk Management: Implements exit conditions based on liquidity structure and trend reversals.

Strategy Performance (Backtested on SOL/USD - MEXC):

Overall Profitability: ~80% win rate in backtesting.

Net Profit: $3,151.12 (6.30% ROI).

Gross Profit: $3,795.68 (7.59%).

Gross Loss: $644.56 (1.29%).

Long Trades Profit: $1,459.05 (2.92%).

Short Trades Profit: $1,692.07 (3.38%).

Commission Paid: $924.82.

Minimum Trade Holding Period: 1-minute cooldown between trades.

Trading Logic:

Entry Conditions:

Long Trades: Triggered when the price enters a liquidity void and aligns with higher timeframe bullish bias.

Short Trades: Triggered when price approaches a resistance level with bearish higher timeframe confluence.

CRT & Turtle Soup Patterns: Identifies reversals by analyzing breakout and fake-out structures.

Exit Conditions:

Long Positions Close: Upon price exceeding a 3.88% profit threshold or reversing below an HTF structure.

Short Positions Close: Upon reaching a similar 3.88% threshold or showing strong bullish signals.

Dynamic Position Sizing:

Uses a leverage-based calculation that adapts trade size based on volatility.

Liquidity Awareness:

Tracks Mitigation Blocks (MB), Fair Value Gaps (FVG), Buy/Sell-Side Liquidity (BSL/SSL) to determine optimal execution.

Best Use Cases:

Scalpers & High-Frequency Traders: Those looking for rapid trade execution with short holding periods.

Crypto Traders Focused on Low Timeframes: Optimized for 15-second price action.

Traders Utilizing Liquidity Concepts: Built to exploit liquidity traps and inefficiencies.

Risks & Considerations:

High-Frequency Execution Requires Low Latency: Ensure your broker or exchange supports fast order execution.

Backtested Results May Vary: Real-time performance depends on market conditions.

Commission & Fees Impact Profits: Consider exchanges with low fees to maximize strategy efficiency.

Final Thoughts:

The Destroyer Life Strategy is designed for serious traders looking to take advantage of high-volatility markets with a structured, liquidity-based approach. By combining price action, liquidity concepts, and adaptive risk management, it provides a solid framework for executing high-probability trades on crypto markets.

🚀 Ready to take your trading to the next level? Try Destroyer Life today and dominate the markets!

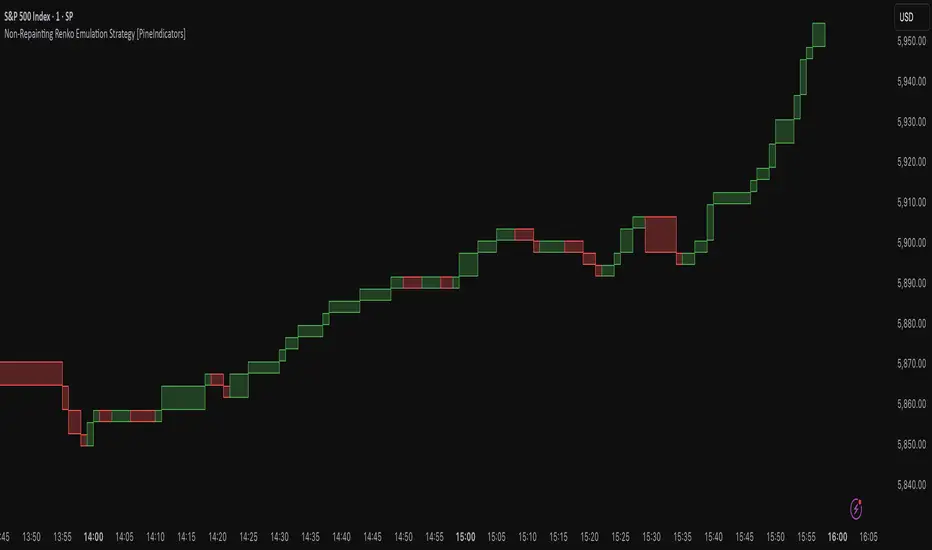

Non-Repainting Renko Emulation Strategy [PineIndicators]Introduction: The Repainting Problem in Renko Strategies

Renko charts are widely used in technical analysis for their ability to filter out market noise and emphasize price trends. Unlike traditional candlestick charts, which are based on fixed time intervals, Renko charts construct bricks only when price moves by a predefined amount. This makes them useful for trend identification while reducing small fluctuations.

However, Renko-based trading strategies often fail in live trading due to a fundamental issue: repainting .

Why Do Renko Strategies Repaint?

Most trading platforms, including TradingView, generate Renko charts retrospectively based on historical price data. This leads to the following issues:

Renko bricks can change or disappear when new data arrives.

Backtesting results do not reflect real market conditions. Strategies may appear highly profitable in backtests because historical data is recalculated with hindsight.

Live trading produces different results than backtesting. Traders cannot know in advance whether a new Renko brick will form until price moves far enough.

Objective of the Renko Emulator

This script simulates Renko behavior on a standard time-based chart without repainting. Instead of using TradingView’s built-in Renko charting, which recalculates past bricks, this approach ensures that once a Renko brick is formed, it remains unchanged .

Key benefits:

No past bricks are recalculated or removed.

Trading strategies can execute reliably without false signals.

Renko-based logic can be applied on a time-based chart.

How the Renko Emulator Works

1. Parameter Configuration & Initialization

The script defines key user inputs and variables:

brickSize : Defines the Renko brick size in price points, adjustable by the user.

renkoPrice : Stores the closing price of the last completed Renko brick.

prevRenkoPrice : Stores the price level of the previous Renko brick.

brickDir : Tracks the direction of Renko bricks (1 = up, -1 = down).

newBrick : A boolean flag that indicates whether a new Renko brick has been formed.

brickStart : Stores the bar index at which the current Renko brick started.

2. Identifying Renko Brick Formation Without Repainting