Session SFPThis script is a powerful, multi-timeframe tool designed to identify high-probability Swing Failure Patterns (SFPs) at key historical levels.

Instead of looking for traditional "pivots" (like a 3-bar swing), this indicator finds the actual high and low of a previous higher-timeframe (HTF) bar (e.g., the previous weekly high/low) and waits for a lower-timeframe (LTF) candle to sweep that level and fail.

This allows you to spot liquidity sweeps and potential reversals at significant, structural price points.

How It Works

The indicator's logic is based on a simple, two-timeframe process:

Level Detection: First, it finds the high and low of the previous bar on your chosen "Level Timeframe" (e.g., W for Weekly, D for Daily). It plots these as small 'x' markers on your chart.

SFP Identification: Second, it watches price action on a lower "SFP Timeframe" (e.g., 240 for 4H). A potential SFP is identified when a candle's wick sweeps above a key high or below a key low.

Confirmation: The SFP is only confirmed after the SFP candle closes back below the high (for a bearish SFP) or above the low (for a bullish SFP). It then waits for a set number of "Confirmation Bars" to pass. If price does not close back over the level during this window, the signal is locked in, and a label is printed.

How to Use (Key Settings)

Level Timeframe (Most Important): This is the timeframe for the levels you want to trade. Set this to W to find SFPs of the previous weekly high/low. Set it to D to find SFPs of the previous daily high/low.

SFP Timeframe: This is the timeframe you want to use to find the SFP candle itself. This should be lower than your Level Timeframe (e.g., 240 or 60).

Level Lookback: This controls how many old levels the script will track. A value of 10 on a W Level Timeframe will track the highs and lows of the last 10 weeks.

Confirmation Bars: This is your "patience" filter. It's the number of SFP Timeframe bars that must close without reclaiming the level after the SFP. A value of 0 will confirm the SFP immediately on the candle's close.

Enable Wick % Filter: A quality filter. If checked, this ensures the SFP candle's rejection wick is a significant percentage of the candle's total range.

Chart Visuals

'x' Markers: These are the historical highs and lows from your "Level Timeframe". You can turn these on or off in the settings.

SFP Label: When an SFP is fully confirmed, a label (Bearish SFP or Bullish SFP) will appear, detailing the level that was swept and the timeframes used.

SFP Line: A solid horizontal line is drawn from the 'x' marker to the SFP candle to highlight the sweep.

Colored Boxes (Optional): If you are viewing a chart timeframe lower than your "SFP Timeframe", you can enable background boxes to highlight the exact SFP candle and its confirmation bars.

Cerca negli script per "track"

Quantura - Session High/LowIntroduction

“Quantura – Session High/Low” is a professional-grade session mapping indicator that automatically identifies and visualizes the highs, lows, and ranges of key global trading sessions — London, New York, and Asia. It helps traders understand when and where liquidity tends to accumulate, allowing for better market structure analysis and session-based strategy alignment.

Originality & Value

This indicator unifies the three most influential global sessions into a single, adaptive visualization tool. Unlike typical session indicators, it dynamically updates live session highs and lows in real time while marking session boundaries and transitions. Its multi-session management system allows for immediate recognition of overlapping liquidity zones — a crucial feature for institutional and intraday traders.

The value and originality come from:

Real-time tracking of session highs, lows, and developing ranges.

Simultaneous visualization of multiple global sessions.

Optional vertical range lines for clearer visual segmentation.

Customizable session times, colors, and time zone offset for global accuracy.

Automatically extending and updating lines as each session progresses.

Functionality & Core Logic

Detects the start and end of each trading session (London, New York, Asia) using built-in time logic and user-defined UTC offsets.

Initializes session-specific high and low variables at the start of each new session.

Continuously updates session high/low levels as new candles form.

Draws color-coded horizontal lines for each session’s high and low.

Optionally adds vertical dotted lines to visually connect session range extremes.

Locks each session’s range once it ends, preserving historical structure for review.

Parameters & Customization

New York Session: Enable/disable, customize time (default 15:30–21:30), and set color.

London Session: Enable/disable, customize time (default 09:00–16:30), and set color.

Asia Session: Enable/disable, customize time (default 02:30–08:00), and set color.

Vertical Line: Toggle dotted vertical lines connecting session high and low levels.

UTC Offset: Adjust session timing to align with your chart’s local time zone.

Visualization & Display

Each session is color-coded for quick identification (default: blue for London, red for New York, green for Asia).

Horizontal lines track evolving session highs and lows in real time.

Once a session closes, the lines remain fixed to mark historical range boundaries.

Vertical dotted lines (optional) visually connect the session’s high and low for clarity.

Supports full overlay display without interfering with other technical indicators.

Use Cases

Identify liquidity zones and range extremes formed during active trading sessions.

Observe session overlaps (London–New York) to anticipate volatility spikes.

Combine with volume or market structure tools for session-based confluence.

Track how price interacts with prior session highs/lows to detect potential reversals.

Analyze session-specific performance patterns for algorithmic or discretionary systems.

Limitations & Recommendations

The indicator is designed for intraday analysis and may not provide meaningful output on daily or higher timeframes.

Adjust session times and UTC offset based on your broker’s or exchange’s timezone.

Does not provide trading signals — it visualizes session structure only.

Combine with liquidity and volatility indicators for full contextual understanding.

Markets & Timeframes

Compatible with all asset classes — including crypto, forex, indices, and commodities — and optimized for intraday timeframes (1m–4h). Particularly useful for traders analyzing session overlaps and volatility transitions.

Author & Access

Developed 100% by Quantura. Published as a Open-source script indicator. Access is free.

Compliance Note

This description fully complies with TradingView’s Script Publishing Rules and House Rules . It provides a detailed explanation of functionality, parameters, and realistic use cases without making any performance or predictive claims.

DTC Killzones ICT🕐 DTC Killzones ICT — Visualize Market Sessions Like a Pro

The DTC Killzones ICT indicator is a clean and intuitive tool designed for traders who want to analyze and visualize institutional trading sessions directly on their charts.

Inspired by ICT’s Killzone concept , this script makes it easy to identify overlapping market sessions — such as London, New York, and Asian — and track how price behaves within each zone.

💡 What It Does

This indicator automatically highlights key market sessions (Killzones) on your chart with fully customizable colors, labels, and transparency.

Each zone dynamically updates to reflect real-time highs and lows, helping you identify:

Session ranges and liquidity zones

Volatility windows and breakout areas

Institutional footprints across sessions

Whether you trade Forex, Indices, or Crypto , this script gives you visual clarity on when and where smart money is likely to move.

⚙️ Main Features

✅ Up to four customizable sessions (New York, London, Asian, and London Close)

✅ Adjustable timeframes and timezone options — sync with your exchange or custom UTC offset

✅ Dynamic high/low range tracking for each session

✅ Toggle range outlines, session labels , and transparency levels

✅ Optional daily dividers and session transition markers

✅ Works on any timeframe and any symbol

🧠 How Traders Use It

ICT-based traders can easily mark Killzones to align with setups like FVGs, liquidity grabs, or Silver Bullet entries.

Intraday traders can visualize session volatility and overlap periods for potential entries.

Swing traders can identify daily structure shifts by tracking range-to-range behavior.

🛠️ Customization

You can fully rename, recolor, or disable each session block.

Adjust the range transparency for visual comfort, and toggle session or daily dividers to fit your workflow.

Everything is designed to be clean, light, and modular — no clutter, no confusion.

⚡ Recommended Settings

For ICT-style analysis:

London Session: 02:00–05:00

New York Session: 07:00–10:00

Asian Session: 19:30–24:00

London Close Session: 10:00–12:00

These time windows are fully editable to suit your timezone or strategy.

🧩 Compatibility

Works seamlessly with TradingView’s built-in timezone tools

Compatible with all instruments and timeframes

Designed to overlay directly on your price chart

🏁 Final Notes

The DTC Killzones ICT indicator focuses purely on market session visualization — no alerts, entries, or trading signals.

It’s designed to complement your existing strategies and enhance clarity when analyzing market behavior across global sessions.

📈 Built for traders who value precision, structure, and timing.

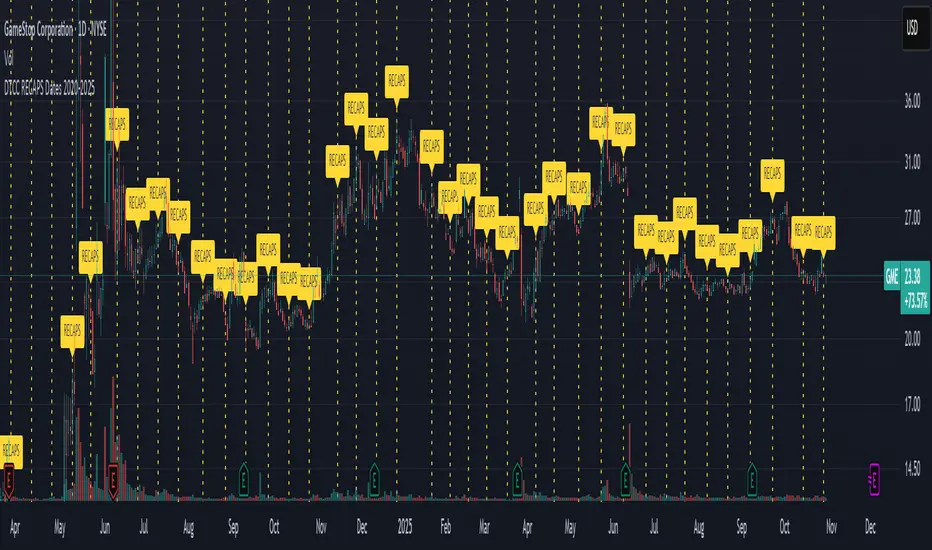

DTCC RECAPS Dates 2020-2025This is a simple indicator which marks the RECAPS dates of the DTCC, during the periods of 2020 to 2025.

These dates have marked clear settlement squeezes in the past, such as GME's squeeze of January 2021.

------------------------------------------------------------------------------------------------------------------

The Depository Trust & Clearing Corporation (DTCC) has published the 2025 schedule for its Reconfirmation and Re-pricing Service (RECAPS) through the National Securities Clearing Corporation (NSCC). RECAPS is a monthly process for comparing and re-pricing eligible equities, municipals, corporate bonds, and Unit Investment Trusts (UITs) that have aged two business days or more .

At its core, the Reconfirmation and Re-pricing Service (RECAPS) is a risk management tool used by the National Securities Clearing Corporation (NSCC), a subsidiary of the DTCC. Its primary purpose is to reduce the risks associated with aged, unsettled trades in the U.S. securities market .

When a trade is executed, it is sent to the NSCC for clearing and settlement. However, for various reasons, some trades may not settle on their scheduled date and become "aged." These unsettled trades create risk for both the trading parties and the clearinghouse (NSCC) because the value of the underlying securities can change over time. If a trade fails to settle and one of the parties defaults, the NSCC may have to step in to complete the transaction at the current market price, which could result in a loss.

RECAPS mitigates this risk by systematically re-pricing these aged, open trading obligations to the current market value. This process ensures that the financial obligations of the clearing members accurately reflect the present value of the securities, preventing the accumulation of significant, unmanaged market risk .

Detailed Mechanics: How Does it Work?

The RECAPS process revolves around two key dates you asked about: the RECAPS Date and the Settlement Date .

The RECAPS Date: On this day, the NSCC runs a process to identify all eligible trades that have remained unsettled for two business days or more. These "aged" trades are then re-priced to the current market value. This re-pricing is not just a simple recalculation; it generates new settlement instructions. The original, unsettled trade is effectively cancelled and replaced with a new one at the current market price. This is done through the NSCC's Obligation Warehouse.

The Settlement Date: This is typically the business day following the RECAPS date. On this date, the financial settlement of the re-priced trades occurs. The difference in value between the original trade price and the new, re-priced value is settled between the two trading parties. This "mark-to-market" adjustment is processed through the members' settlement accounts at the DTCC.

Essentially, the process ensures that any gains or losses due to price changes in the underlying security are realized and settled periodically, rather than being deferred until the trade is ultimately settled or cancelled.

Are These Dates Used to Check Margin Requirements?

Yes, indirectly, this process is closely tied to managing margin and collateral requirements for NSCC members. Here’s how:

The NSCC requires its members to post collateral to a clearing fund, which acts as a mutualized guarantee against defaults. The amount of collateral each member must provide is calculated based on their potential risk exposure to the clearinghouse.

By re-pricing aged trades to current market values through RECAPS, the NSCC gets a more accurate picture of each member's outstanding obligations and, therefore, their current risk profile. If a member has a large number of unsettled trades that have moved against them in value, the re-pricing will crystallize that loss, which will be settled the next day.

This regular re-pricing and settlement of aged trades prevent the build-up of large, unrealized losses that could increase a member's risk profile beyond what their posted collateral can cover. While RECAPS is not the only mechanism for calculating margin (the NSCC has a complex system for daily margin calls based on overall portfolio risk), it is a crucial component for managing the specific risk posed by aged, unsettled transactions. It ensures that the value of these obligations is kept current, which in turn helps ensure that collateral levels remain adequate.

--------------------------------------------------------------------------------------------------------------

Future dates of 2025:

- November 12, 2025 (Wed)

- November 25, 2025 (Tue)

- December 11, 2025 (Thu)

- December 29, 2025 (Mon)

The dates for 2026 haven't been published yet at this time.

The RECAPS process is essentially the industry's way of retrying the settlement of all unresolved FTDs, netting outstanding obligations, and gradually forcing resolution (either delivery or buy-in). Monitoring RECAPS cycles is one way to track the lifecycle, accumulation, and eventual resolution (or persistence) of failures to deliver in the U.S. market.

The US Stock market has become a game of settlement dates and FTDs, therefore this can be useful to track.

ProScalper📊 ProScalper - Professional 1-Minute Scalping System

🎯 Overview

ProScalper is a sophisticated, multi-confluence scalping indicator designed specifically for 1-minute chart trading. Combining advanced technical analysis with intelligent signal filtering, it provides high-probability trade setups with clear entry, stop loss, and take profit levels.

✨ Key Features

🔺 Smart Signal Detection

Range Filter Technology: Fast-responding trend detection (25-period) optimized for 1-minute timeframe

Medium-sized triangles appear above/below candles for clear buy/sell signals

Only most recent signal shown - no chart clutter

Automatically deletes old signals when new ones appear

📋 Real-Time Signal Table

Top-center display shows complete trade breakdown

Grade system: A+, A, B+, B, C+ ratings for every setup

All confluence reasons listed with checkmarks

Score and R:R displayed for instant trade quality assessment

Color-coded: Green for LONG, Red for SHORT

📐 Multi-Confluence Analysis

ProScalper combines 10+ technical factors:

✅ EMA Trend: 4 EMAs (200, 48, 13, 8) for multi-timeframe alignment

✅ VWAP: Dynamic support/resistance

✅ Fibonacci Retracement: Golden ratio (61.8%), 50%, 38.2%, 78.6%

✅ Range Filter: Adaptive trend confirmation

✅ Pivot Points: Smart reversal detection

✅ Volume Analysis: Spike detection and volume profile

✅ Higher Timeframe: 5-minute trend confirmation

✅ HTF Support/Resistance: Key levels from higher timeframes

✅ Liquidity Sweeps: Smart money detection

✅ Opening Range Breakout: First 15-minute range

💰 Complete Trade Management

Entry Lines: Dashed green (LONG) or red (SHORT) showing exact entry

Stop Loss: Red dashed line with price label

Take Profit: Blue dashed line with price label and R:R

Partial Exits: 1R level marked with orange dashed line

All lines extend 10 bars for clean alignment with Fibonacci levels

📊 Dynamic Risk/Reward

Adaptive R:R calculation based on market volatility

Targets adjusted for pivot distances

Minimum 1.2:1 to maximum 3.5:1 for scalping

Position sizing based on account risk percentage

🎨 Professional Visualization

Clean chart layout - no clutter, only essential information

Custom EMA colors: Red (200), Aqua (48), Green (13), White (8)

Gold VWAP line for key support/resistance

Color-coded Fibonacci: Bright yellow (61.8%), white (50%), orange (38.2%), fuchsia (78.6%)

No shaded zones - pure price action focus

📈 Performance Tracking

Real-time statistics table (optional)

Win rate, total trades, P&L tracking

Average R:R and win/loss ratios

Setup-specific performance metrics

⚙️ Settings & Customization

Risk Management

Adjustable account risk per trade (default: 0.5%)

ATR-based stop loss multiplier (default: 0.8 for tight scalping)

Dynamic position sizing

Signal Sensitivity

Confluence Score Threshold: 40-100 (default: 55 for balanced signals)

Range Filter Period: 25 bars (fast signals for 1-min)

Range Filter Multiplier: 2.2 (tighter bands for more signals)

Visual Controls

Toggle signal table on/off

Show/hide Fibonacci levels

Control EMA visibility

Adjust table text size

Partial Exits

1R: 50% (default)

2R: 30% (default)

3R: 20% (default)

Fully customizable percentages

Trailing Stops

ATR-Based (best for scalping)

Pivot-Based

EMA-Based

Breakeven trigger at 0.8R

🎯 Best Use Cases

Ideal For:

✅ 1-minute scalping on liquid instruments

✅ Day traders looking for quick 2-8 minute trades

✅ High-frequency trading with 8-15 signals per session

✅ Trending markets where Range Filter excels

✅ Crypto, Forex, Futures - works on all liquid assets

Trading Style:

Timeframe: 1-minute (can work on 3-5 min with adjusted settings)

Hold Time: 3-8 minutes average

Target: 1.2-3R per trade

Frequency: 8-15 signals per day

Win Rate: 45-55% (with proper risk management)

📋 How to Use

Step 1: Wait for Signal

Watch for green triangle (BUY) or red triangle (SELL)

Signal table appears at top center automatically

Step 2: Review Confluence

Check grade (prefer A+, A, B+ for best quality)

Review all reasons listed in table

Confirm score is above your threshold (55+ recommended)

Note the R:R ratio

Step 3: Enter Trade

Enter at current market price

Set stop loss at red dashed line

Set take profit at blue dashed line

Mark 1R level (orange line) for partial exit

Step 4: Manage Trade

Exit 50% at 1R (orange line)

Move to breakeven after 0.8R

Trail remaining position using your chosen method

Exit fully at TP or opposite signal

🎨 Chart Setup Recommendations

Optimal Display:

Timeframe: 1-minute

Chart Type: Candles or Heikin Ashi

Background: Dark theme for best color visibility

Volume: Enable volume bars below chart

Complementary Indicators (optional):

Order flow/Delta for institutional confirmation

Market profile for key levels

Economic calendar for news avoidance

⚠️ Important Notes

Risk Disclaimer:

Not financial advice - for educational purposes only

Always use proper risk management (0.5-1% per trade max)

Past performance doesn't guarantee future results

Test on demo account before live trading

Best Practices:

✅ Trade during high liquidity hours (9:30-11 AM, 2-4 PM EST)

✅ Avoid news events and market open/close (first/last 2 minutes)

✅ Use tight stops (0.8-1.0 ATR) for 1-minute scalping

✅ Take partial profits quickly (1R = 50% off)

✅ Respect max daily loss limits (3% recommended)

✅ Focus on A and B grade setups for consistency

What Makes This Different:

🎯 Complete system - not just signals, but full trade management

📊 Multi-confluence - 10+ factors analyzed per trade

🎨 Professional visualization - clean, focused chart design

⚡ Optimized for 1-min - settings specifically tuned for fast scalping

📋 Transparent reasoning - see exactly why each trade was taken

🏆 Grade system - instantly know trade quality

🔧 Technical Details

Pine Script Version: 5

Overlay: Yes (plots on price chart)

Max Lines: 500

Max Labels: 100

Non-repainting: All signals confirmed on bar close

Alerts: Compatible with TradingView alerts

📞 Support & Updates

This indicator is actively maintained and optimized for 1-minute scalping. Settings can be adjusted for different timeframes and trading styles, but default configuration is specifically tuned for high-frequency 1-minute scalping.

🚀 Get Started

Add ProScalper to your 1-minute chart

Adjust settings to your risk tolerance

Wait for signals (green/red triangles)

Follow the signal table guidance

Manage trades using provided levels

Track performance with stats table

Happy Scalping! 📊⚡💰

CMF, RSI, CCI, MACD, OBV, Fisher, Stoch RSI, ADX (+DI/-DI)Eight normalized indicators are used in conjunction with the CMF, CCI, MACD, and Stoch RSI indicators. You can track buy and sell decisions by tracking swings. The zero line is for reversal tracking at -20, +20, +50, and +80. You can use any of the nine indicators individually or in combination.

CMF, RSI, CCI, MACD, OBV, Fisher, Stoch RSI, ADX (+DI/-DI)Eight normalized indicators are used in conjunction with the CMF, CCI, MACD, and Stoch RSI indicators. You can track buy and sell decisions by tracking swings. The zero line is for reversal tracking at -20, +20, +50, and +80. You can use any of the nine indicators individually or in combination.

[delta2win] ShockSentinel Early Warnings🚀 ShockSentinel Early Warnings — Advanced Multi-Symbol Shock Detection System

📊 UNIQUE METHODOLOGY:

This indicator implements a proprietary concordance-based shock detection system that goes beyond simple price movement analysis. Unlike basic pump/dump detectors, it uses a sophisticated multi-symbol correlation algorithm to validate signals across multiple assets simultaneously, significantly reducing false positives while maintaining sensitivity to genuine market shocks.

🔬 TECHNICAL APPROACH:

• Adaptive Threshold System: Automatically adjusts detection sensitivity based on timeframe using proprietary scaling algorithms:

- 1m: 0.5% threshold (ultra-sensitive for scalping)

- 3m: 1.0% threshold (high-frequency trading)

- 5m: 2.0% threshold (short-term momentum)

- 15m: 3.0% threshold (intraday swings)

- 1h: 6.0% threshold (daily moves)

- 4h+: 10.0% threshold (swing trading)

• Dual Detection Modes:

- Percent Mode: Calculates maximum percentage change within configurable lookback window (1-6 bars) using the formula: max(|(close - close ) / close * 100|) for i = 1 to window

- ATR-Normalized Mode: Uses Average True Range for volatility-adjusted detection across different market regimes: max(|close - close | / ATR) for i = 1 to window

• Concordance Algorithm: Proprietary multi-symbol validation system that requires minimum correlation count across up to 4 additional symbols, ensuring signals are validated by market-wide participation rather than isolated price movements

• Non-Repainting Architecture: Optional bar-close confirmation prevents false signals from intraday noise while maintaining real-time alert capability for immediate response

🎯 MATHEMATICAL FOUNDATION:

The core algorithm implements a sliding window maximum change detection:

Percent Change Calculation:

For each bar, the system calculates the maximum absolute percentage change over the specified window:

- PctChange = (close - close ) / close * 100

- MaxPct = max(|PctChange |) for i = 1 to window

- Signal triggers when MaxPct >= threshold

ATR-Normalized Calculation:

For volatility-adjusted detection:

- ATRChange = (close - close ) / ATR

- MaxATR = max(|ATRChange |) for i = 1 to window

- Signal triggers when MaxATR >= ATR_multiplier

Concordance Validation:

- Requires minimum N symbols showing same directional movement

- Validates signal strength through market participation

- Reduces false signals from isolated price movements

- Improves signal quality through correlation analysis

⚙️ ADVANCED FEATURES:

• Preset System: 7 pre-configured strategies with optimized parameters:

- Scalp (Ultra-Fast): 0.6x scaling, 2-bar window, real-time alerts

- Aggressive: 0.7x scaling, 2-bar window, real-time alerts

- Balanced: 1.0x scaling, 3-bar window, confirmed signals

- Conservative: 1.3x scaling, 4-bar window, confirmed signals

- Volatility-Adaptive: ATR mode, 7-period ATR, 2.5x multiplier

- Momentum (Intraday): ATR mode, 10-period ATR, 2.0x multiplier

- Swing (Slow): ATR mode, 14-period ATR, 2.8x multiplier

• Real-time vs Confirmed: Choose between immediate alerts or bar-close confirmation

• Visual Analytics: Integrated signal history table with concordance gauges and performance metrics

• Professional Alerts: Multi-format alert system (Compact, Extended, Plain, CSV) with Telegram integration and customizable messaging

💡 UNIQUE VALUE PROPOSITION:

Unlike simple price change detectors, this system provides:

1. Multi-Symbol Validation: Validates signals across multiple correlated assets, ensuring market-wide participation

2. Adaptive Thresholds: Automatically adjusts sensitivity based on timeframe and market conditions

3. Dual Signal Types: Provides both real-time and confirmed signal options for different trading styles

4. Comprehensive Analytics: Includes signal history, concordance gauges, and performance tracking

5. Advanced Concordance: Uses sophisticated correlation algorithms for signal validation

6. Professional Integration: Built-in Telegram support with customizable message formats

🔧 USAGE INSTRUCTIONS:

1. Select Preset: Choose appropriate strategy for your trading style and timeframe

2. Configure Symbols: Add up to 4 additional symbols for concordance validation

3. Set Concordance: Adjust minimum count (higher = more selective, lower = more sensitive)

4. Choose Mode: Select between real-time or confirmed signals based on your risk tolerance

5. Enable Alerts: Configure notification preferences and message formats

6. Monitor Performance: Use integrated tables to track signal quality and concordance

📈 PERFORMANCE CHARACTERISTICS:

• Optimized for Crypto: Designed specifically for high-volatility cryptocurrency markets

• Multi-Timeframe: Effective across all timeframes from 1-minute to 4-hour charts

• False Signal Reduction: Multi-symbol validation significantly reduces false positives

• Flexible Sensitivity: Adjustable thresholds allow customization for different market conditions

• Real-time Capability: Provides immediate alerts for fast-moving markets

• Confirmation Option: Bar-close confirmation for conservative trading approaches

⚠️ TECHNICAL CONSIDERATIONS:

• Real-time Mode: May generate multiple alerts per bar; use cooldown settings to manage frequency

• Data Dependencies: Concordance requires data availability for all configured symbols

• Market Regimes: ATR mode provides better performance in varying volatility conditions

• Signal Quality: Higher concordance requirements reduce false signals but may miss opportunities

• Latency: request.security calls depend on data provider latency and availability

🎯 TARGET MARKETS:

• Cryptocurrency Trading: High-volatility crypto markets with frequent shock events

• Scalping: Short-term trading strategies requiring immediate signal detection

• Swing Trading: Medium-term strategies benefiting from confirmed signals

• Portfolio Management: Multi-asset correlation analysis for risk management

• Algorithmic Trading: Systematic strategies requiring reliable signal validation

📊 SIGNAL INTERPRETATION:

• Green Arrows (Pump): Upward price shock with sufficient concordance

• Red Arrows (Dump): Downward price shock with sufficient concordance

• Large Markers: Confirmed signals with high concordance

• Small Markers: Early signals with lower concordance

• Background Colors: Visual intensity based on concordance strength

• Tables: Historical signal tracking with performance metrics

Sat Stacking Strategies Simulation (SSSS)Sat Stacking Strategies Simulation (SSSS)

This indicator simulates and compares different Bitcoin stacking strategies over time, allowing you to visualize performance, cost basis, and stacking behavior directly on your chart.

Core Features:

Three Stacking Strategies

• Trend-Based – Stack only when price is above/below a long-term SMA.

• Stack the Dip – Buy during sharp pullbacks or oversold conditions.

• Price Zone – Stack only in “cheap”, “fair”, or “expensive” zones based on a simulated Short-Term Holder (STH) cost basis.

Always Stack Benchmark

Compare your chosen strategy against a simple “Always Stack” approach for a real-world DCA reference.

Performance Metrics Table

Track:

• Total Fiat Added

• Total BTC Accumulated

• Current Value

• Average Cost per BTC

• PnL %

• CAGR

• Sharpe Ratio & Stdev

• Stack Events & Time Underwater

Advanced Options

• Simulate cash-secured puts on unused fiat.

• Simulate covered calls on BTC holdings.

• Roll over unused stacking amounts for future buys.

This tool is designed for Bitcoiners, stackers, and DCA enthusiasts who want to backtest and visualize their stacking plan—whether you keep it simple or go full quant.

Sometimes the best alpha is just showing up every week with your wallet open… and occasionally wearing a helmet. 🪖💰

cd_HTF_bias_CxOverview:

No matter our trading style or model, to increase our success rate, we must move in the direction of the trend and align with the Higher Time Frame (HTF). Trading "gurus" call this the HTF bias. While we small fish tend to swim in all directions, the smart way is to flow with the big wave and the current. This indicator is designed to help us anticipate that major wave.

________________________________________

Details and Usage:

This indicator observes HTF price action across preferably seven different pairs, following specific rules. It confirms potential directional moves using CISD levels on a Medium Time Frame (MTF). In short, it forecasts the likely direction (HTF bias). The user can then search for trade opportunities aligned with this bias on a Lower Time Frame (LTF), using their preferred pair, entry model, and style.

________________________________________

Timeframe Alignment:

The commonly accepted LTF/MTF/HTF combinations include:

• 1m – 15m – H4

• 3m – H1 – Daily / 3m – 30m – Daily

• 5m – H1 – Daily

• 15m – H4 – Weekly

• H1 – Daily – Monthly

• H4 – Weekly – Quarterly

Example: If you're trading with a 3m model on a 30m/3m setup, you should seek trades in the direction of the H1/Daily bias.

________________________________________

How It Works:

The indicator first looks for sweeps on the selected HTF — when any of the last four candles are swept, the first condition is met.

The second step is confirmation with a CISD close on the MTF — once a candle closes above/below the CISD level, the second condition is fulfilled. This suggests the price has made its directional decision.

Example: If a previous HTF candle is swept and we receive a bearish CISD confirmation on H1, the HTF bias becomes bearish.

After this, you may switch to a more granular setup like HTF: 30m and MTF: 3m to look for trade entries aligned with the bias (e.g., 30m sweep + 3m CISD).

________________________________________

How Is Bias Determined?

• HTF Sweep + MTF CISD = SC (Sweep & CISD)

• Latest Bullish SC → Bias: Bullish

• Latest Bearish SC → Bias: Bearish

• Price closes above the last Bearish SC → Bias: Strong Bullish

• Price closes below the last Bullish SC → Bias: Strong Bearish

• Strong Bullish bias + Bearish CISD (without HTF sweep) → Bias: Bullish

• Strong Bearish bias + Bullish CISD (without HTF sweep) → Bias: Bearish

• Bearish price violates SC high, but Bullish SC is untouched → Bias: Bullish

• Bullish price violates SC low, but Bearish SC is untouched → Bias: Bearish

• If neither side generates SC → Bias: No Bias

The logic is built on the idea that a price overcoming resistance is stronger, and encountering resistance is weaker. This model is based on the well-known “Daily Bias” structure, but with personal refinements.

________________________________________

What’s on the Screen?

• Classic HTF zones (boxes)

• Potential MTF CISD levels

• Confirmed MTF lines

• Sweep zones when HTF sweeps occur

• Result table showing current bias status

________________________________________

Usage:

• Select HTF and MTF timeframes aligned with your trading timeframe.

• Adjust color and position settings as needed.

• Enter up to seven pairs to track via the menu.

• Use the checkbox next to each pair to enable/disable them.

• If “Ignore these assets” is checked, all pairs will be disabled, and only the currently open chart pair will be tracked.

________________________________________

Alerts:

You can choose alerts for Bullish, Bearish, Strong Bullish, or Strong Bearish conditions.

There are two types of alert sources:

1. From the indicator’s internal list

2. From TradingView’s watchlist

Visual example:

________________________________________

How I Use It:

• For spot trades, I use HTF: Weekly and MTF: H4 and look for Bullish or Strong Bullish pairs.

• For scalping, I follow bias from HTF: Daily and MTF: H1.

Example: If the indicator shows a Bearish HTF Bias, I switch to HTF: 30m and MTF: 3m and enter trades once bearish conditions are met (timeframe alignment).

________________________________________

Important Notes:

• The indicator defines CISD levels only at HTF high and low levels.

• If your chart is on a higher timeframe than your selected HTF/MTF, no data will appear.

Example: If HTF = H1 and MTF = 5m, opening a chart on H4 will result in a blank screen.

• The drawn CISD level on screen is the MTF CISD level.

• Not every alert should be traded. Always confirm with personal experience and visual validation.

• Receiving multiple Strong Bullish/Bearish alerts is intentional. (Trick 😊)

• Please share your feedback and suggestions!

________________________________________

And Most Importantly:

Don't leave street animals without water and food!

Happy trading!

Discord Levels (Label Toggle)This indicator is designed to streamline your multi-asset level tracking by displaying custom price levels directly on your chart for up to eight different stocks. It allows you to define key support, resistance, and moving average levels, enhancing your analysis across various instruments.

Key Features:

Multi-Stock Level Display: Track important levels for up to 8 distinct stock symbols simultaneously.

Customizable Level Inputs: Define all your desired price levels using a simple space-separated string for each stock.

Intelligent Color-Coding: Levels are automatically color-coded for quick identification based on the associated notes in your input string:

White Line: Standard price levels (e.g., 123.45).

Yellow Line: Levels designated as 200 Daily EMA (e.g., 18.70=daily 200 ema).

Blue Line: Levels designated as 50 Daily EMA (e.g., 18.70=daily 50 ema).

Gray Line: Levels designated as 34 Daily EMA (e.g., 18.70=daily 34 ema).

Green Line: Levels designated as 9 Daily EMA (e.g., 18.70=daily 9 ema).

Red Line: Critical or Cautionary levels (e.g., 9.00=cautionary).

Dynamic Label Positioning: Price labels are displayed next to the lines, dynamically positioned to the right of the current bar (30 bars offset) for optimal visibility across different timeframes.

Global Label Toggle: Easily enable or disable all price labels from the indicator's settings.

How to Use:

Input Stock Symbol: For each slot (Stock 1 to Stock 8) you wish to use, enter the exact TradingView symbol (e.g., AAPL, MSFT, TSLA).

Input Levels String: In the corresponding "Levels" input field, enter your desired price levels separated by spaces.

Basic Level: Just enter the number (e.g., 12.34).

Levels with Notes: Use the format PRICE=NOTE for specific annotations (e.g., 18.70=daily 200 ema, 9.00=cautionary).

Supported Notes for Automatic Coloring: daily 200 ema, daily 50 ema, daily 34 ema, daily 9 ema, cautionary, critical. (Case-insensitive)

Manage Slots: If you need to track more than 8 stocks, simply clear the symbol and levels for an old stock and use that slot for your new entry.

This indicator is a powerful tool for traders who rely on fixed price levels and moving averages across multiple securities, providing clear visual cues without cluttering your main chart analysis.

Perfect MA Touch – Full Setup 1,3,5,7,8,9This indicator helps you track a precise candle countdown from a moving average touch, labeling key bars (1, 3, 5, 7, 8, 9) for timing entries and momentum setups — with optional coloring, alerts, and full customization.

What It Detects

1. MA Touch Trigger

The sequence starts when any selected moving average (up to 6 MAs, customizable) is touched by the candle's high/low range.

This "perfect touch" initiates the count and labels that candle as "1".

2. Candle Number Labels

After a perfect MA touch:

Candle 1 = the bar that touches the MA

Candle 3 = two bars after Candle 1

Candle 5 = the fifth bar after the touch

Candle 7 = third bar after Candle 5

Candle 8 = fourth bar after Candle 5

Candle 9 = fifth bar after Candle 5

It creates a time-based sequence you can use to anticipate reactions or momentum shifts.

3. Customization

You can:

Choose between EMA or SMA for each MA (6 total)

Set custom lengths for each MA (9, 20, 50, 100, 150, 200)

Choose which candle numbers (1, 3, 5, 7, 8, 9) to highlight

Pick font size and label color

4. Highlighting and Alerts

Highlight candles (with color) when certain bars (like 3, 5, 7) print

Alerts are available for all tracked bars (1, 3, 5, 7, 8, 9)

Use Case Example

Let’s say you want to enter trades on the 3rd candle after a perfect MA touch:

You set the script to highlight candle 3.

When a candle hits your chosen MA (say EMA 9), it’s labeled “1”.

Two bars later, bar 3 appears — giving you a timed signal to enter if price behavior aligns.

This method is especially useful when paired with:

Volume confirmation

Breakout or reversal patterns

Support/resistance or order block zones

Multi-Position DashMulti-Position Dash — Risk Dashboard for Forex, Stocks & Indices

Overview:

The Multi-Position Dash is a highly customizable trading dashboard designed to help active traders manage up to 8 simultaneous positions across Forex, Stocks, and Indices. Whether you're trading single entries, layering positions, using DCA (Dollar Cost Averaging), or running complex hedging setups, this tool provides essential, real-time risk and P&L insights—directly on your chart.

Key Features:

✔️ Supports Forex, Stocks, Indices — with automatic pip and contract conversions

✔️ Track up to 8 manual positions, each with customizable direction, lot size or contracts, entry price, Take Profit, and Stop Loss

✔️ Full GBP-based P&L and risk calculation, including automatic USD-to-GBP conversion for non-FX assets

✔️ Real-time display of:

Total potential Take Profit (GBP)

Total potential Stop Loss (GBP)

Risk % relative to account balance

Live P&L (GBP) based on current price

✔️ Breakeven price calculation, even across mixed-direction positions (DCA & hedging aware)

✔️ Visual breakeven line, live P&L arrows, and entry price markers

✔️ Shared Stop Loss option for all positions — perfect for DCA traders

✔️ Easy export strings for logging trades to external tools like spreadsheets

Ideal For:

✅ Forex traders using lot-based risk models

✅ Stock & Index traders wanting simplified contract-based position tracking

✅ Traders managing multiple active positions, with or without hedging

✅ Anyone needing at-a-glance P&L and risk monitoring, independent of broker platforms

Notes & Usage:

This is a manual tracking tool—you enter your positions, TP, SL levels, etc., and the dashboard calculates the rest. It does not place or manage live orders.

Supports both Long and Short positions.

All calculations are based on your inputs and market price—accuracy depends on maintaining your inputs properly.

Shared Stop Loss feature applies a single, unified stop across all active positions for simplified risk control in DCA setups.

GBP is used as the account currency—USD-to-GBP conversion is applied to stocks and indices as needed.

Disclaimer:

This tool is for educational and planning purposes only. It does not place or manage live trades, and is not a substitute for broker risk management tools. Always double-check your own position sizing and risk before placing live orders.

Liquidity Hunter HeatmapLiquidity Hunter (GPS Companion Tool)

Liquidity Hunter is a specialized script designed to help traders visualize and track potential liquidation zones, clusters, and imbalance traps in real-time. It is particularly useful for scalpers and short-term traders who rely on liquidity sweeps, stop hunts, and reversion plays.

This tool does not replicate open-source liquidation trackers. Instead, it uses a proprietary combination of volume surges, candle displacement, VWAP deviation, and high-timeframe wicks to infer areas of trapped traders and display them with clear, color-coded markers.

Key Features:

• Real-Time Liquidation Estimates: Detects where major stop losses (and potential liquidations) may have occurred, based on proprietary volume + price action logic.

• Cluster Strength Bubbles: Visual bubbles (scaled by cluster size) show where liquidations are stacking. Purple for bearish, white for bullish — intensity reflects strength.

• Pre-Liquidation Warning Zones: Highlights areas where price is likely to sweep liquidity before reversing, helping traders avoid chasing moves.

• Dollar-Based Labels (Optional): Displays the estimated value liquidated, helping traders size the significance of a move (e.g., $8.4M).

• Minimal Clutter Mode: Designed for intraday clarity — hides excess lines and uses bubbles, not shapes, for cleaner visualization.

Trend Flow Trail [AlgoAlpha]OVERVIEW

This script overlays a custom hybrid indicator called the Money Flow Trail which combines a volatility-based trend-following trail with a volume-weighted momentum oscillator. It’s built around two core components: the AlphaTrail—a dynamic band system influenced by Hull MA and volatility—and a smoothed Money Flow Index (MFI) that provides insights into buying or selling pressure. Together, these tools are used to color bars, generate potential reversal markers, and assist traders in identifying trend continuation or exhaustion phases in any market or timeframe.

CONCEPTS

The AlphaTrail calculates a volatility-adjusted channel around price using the Hull Moving Average as the base and an EMA of range as the spread. It adaptively shifts based on price interaction to capture trend reversals while avoiding whipsaws. The direction (bullish or bearish) determines both the band being tracked and how the trail locks in. The Money Flow Index (MFI) is derived from hlc3 and volume, measuring buying vs selling pressure, and is further smoothed with a short Hull MA to reduce noise while preserving structure. These two systems work in tandem: AlphaTrail governs directional context, while MFI refines the timing.

FEATURES

Dynamic AlphaTrail line with regime switching logic that controls directional bias and bar coloring.

Smoothed MFI with gradient coloring to visually communicate pressure and exhaustion levels.

Overbought/oversold thresholds (80/20), mid-level (50), and custom extreme zones (90/10) for deeper signal granularity.

Built-in take-profit signal logic: crossover of MFI into overbought with bullish AlphaTrail, or into oversold with bearish AlphaTrail.

Visual fills between price and AlphaTrail for clearer confirmation during trend phases.

Alerts for regime shifts, MFI crossovers, trail interactions, and bar color regime changes.

USAGE

Add the indicator to any chart. Use the AlphaTrail plot to define trend context: bullish (trailing below price) or bearish (trailing above). MFI values give supporting confirmation—favor long setups when MFI is rising and above 50 in a bullish regime, and shorts when MFI is falling and below 50 in a bearish regime. The colored fills help visually track strength; sharp changes in MFI crossing 80/20 or 90/10 zones often precede pullbacks or reversals. Use the plotted circles as optional take-profit signals when MFI and trend are extended. Adjust AlphaTrail length/multiplier and MFI smoothing to better match the asset’s volatility profile.

Langlands-Operadic Möbius Vortex (LOMV)Langlands-Operadic Möbius Vortex (LOMV)

Where Pure Mathematics Meets Market Reality

A Revolutionary Synthesis of Number Theory, Category Theory, and Market Dynamics

🎓 THEORETICAL FOUNDATION

The Langlands-Operadic Möbius Vortex represents a groundbreaking fusion of three profound mathematical frameworks that have never before been combined for market analysis:

The Langlands Program: Harmonic Analysis in Markets

Developed by Robert Langlands (Fields Medal recipient), the Langlands Program creates bridges between number theory, algebraic geometry, and harmonic analysis. In our indicator:

L-Function Implementation:

- Utilizes the Möbius function μ(n) for weighted price analysis

- Applies Riemann zeta function convergence principles

- Calculates quantum harmonic resonance between -2 and +2

- Measures deep mathematical patterns invisible to traditional analysis

The L-Function core calculation employs:

L_sum = Σ(return_val × μ(n) × n^(-s))

Where s is the critical strip parameter (0.5-2.5), controlling mathematical precision and signal smoothness.

Operadic Composition Theory: Multi-Strategy Democracy

Category theory and operads provide the mathematical framework for composing multiple trading strategies into a unified signal. This isn't simple averaging - it's mathematical composition using:

Strategy Composition Arity (2-5 strategies):

- Momentum analysis via RSI transformation

- Mean reversion through Bollinger Band mathematics

- Order Flow Polarity Index (revolutionary T3-smoothed volume analysis)

- Trend detection using Directional Movement

- Higher timeframe momentum confirmation

Agreement Threshold System: Democratic voting where strategies must reach consensus before signal generation. This prevents false signals during market uncertainty.

Möbius Function: Number Theory in Action

The Möbius function μ(n) forms the mathematical backbone:

- μ(n) = 1 if n is a square-free positive integer with even number of prime factors

- μ(n) = -1 if n is a square-free positive integer with odd number of prime factors

- μ(n) = 0 if n has a squared prime factor

This creates oscillating weights that reveal hidden market periodicities and harmonic structures.

🔧 COMPREHENSIVE INPUT SYSTEM

Langlands Program Parameters

Modular Level N (5-50, default 30):

Primary lookback for quantum harmonic analysis. Optimized by timeframe:

- Scalping (1-5min): 15-25

- Day Trading (15min-1H): 25-35

- Swing Trading (4H-1D): 35-50

- Asset-specific: Crypto 15-25, Stocks 30-40, Forex 35-45

L-Function Critical Strip (0.5-2.5, default 1.5):

Controls Riemann zeta convergence precision:

- Higher values: More stable, smoother signals

- Lower values: More reactive, catches quick moves

- High frequency: 0.8-1.2, Medium: 1.3-1.7, Low: 1.8-2.3

Frobenius Trace Period (5-50, default 21):

Galois representation lookback for price-volume correlation:

- Measures harmonic relationships in market flows

- Scalping: 8-15, Day Trading: 18-25, Swing: 25-40

HTF Multi-Scale Analysis:

Higher timeframe context prevents trading against major trends:

- Provides market bias and filters signals

- Improves win rates by 15-25% through trend alignment

Operadic Composition Parameters

Strategy Composition Arity (2-5, default 4):

Number of algorithms composed for final signal:

- Conservative: 4-5 strategies (higher confidence)

- Moderate: 3-4 strategies (balanced approach)

- Aggressive: 2-3 strategies (more frequent signals)

Category Agreement Threshold (2-5, default 3):

Democratic voting minimum for signal generation:

- Higher agreement: Fewer but higher quality signals

- Lower agreement: More signals, potential false positives

Swiss-Cheese Mixing (0.1-0.5, default 0.382):

Golden ratio φ⁻¹ based blending of trend factors:

- 0.382 is φ⁻¹, optimal for natural market fractals

- Higher values: Stronger trend following

- Lower values: More contrarian signals

OFPI Configuration:

- OFPI Length (5-30, default 14): Order Flow calculation period

- T3 Smoothing (3-10, default 5): Advanced exponential smoothing

- T3 Volume Factor (0.5-1.0, default 0.7): Smoothing aggressiveness control

Unified Scoring System

Component Weights (sum ≈ 1.0):

- L-Function Weight (0.1-0.5, default 0.3): Mathematical harmony emphasis

- Galois Rank Weight (0.1-0.5, default 0.2): Market structure complexity

- Operadic Weight (0.1-0.5, default 0.3): Multi-strategy consensus

- Correspondence Weight (0.1-0.5, default 0.2): Theory-practice alignment

Signal Threshold (0.5-10.0, default 5.0):

Quality filter producing:

- 8.0+: EXCEPTIONAL signals only

- 6.0-7.9: STRONG signals

- 4.0-5.9: MODERATE signals

- 2.0-3.9: WEAK signals

🎨 ADVANCED VISUAL SYSTEM

Multi-Dimensional Quantum Aura Bands

Five-layer resonance field showing market energy:

- Colors: Theme-matched gradients (Quantum purple, Holographic cyan, etc.)

- Expansion: Dynamic based on score intensity and volatility

- Function: Multi-timeframe support/resistance zones

Morphism Flow Portals

Category theory visualization showing market topology:

- Green/Cyan Portals: Bullish mathematical flow

- Red/Orange Portals: Bearish mathematical flow

- Size/Intensity: Proportional to signal strength

- Recursion Depth (1-8): Nested patterns for flow evolution

Fractal Grid System

Dynamic support/resistance with projected L-Scores:

- Multiple Timeframes: 10, 20, 30, 40, 50-period highs/lows

- Smart Spacing: Prevents level overlap using ATR-based minimum distance

- Projections: Estimated signal scores when price reaches levels

- Usage: Precise entry/exit timing with mathematical confirmation

Wick Pressure Analysis

Rejection level prediction using candle mathematics:

- Upper Wicks: Selling pressure zones (purple/red lines)

- Lower Wicks: Buying pressure zones (purple/green lines)

- Glow Intensity (1-8): Visual emphasis and line reach

- Application: Confluence with fractal grid creates high-probability zones

Regime Intensity Heatmap

Background coloring showing market energy:

- Black/Dark: Low activity, range-bound markets

- Purple Glow: Building momentum and trend development

- Bright Purple: High activity, strong directional moves

- Calculation: Combines trend, momentum, volatility, and score intensity

Six Professional Themes

- Quantum: Purple/violet for general trading and mathematical focus

- Holographic: Cyan/magenta optimized for cryptocurrency markets

- Crystalline: Blue/turquoise for conservative, stability-focused trading

- Plasma: Gold/magenta for high-energy volatility trading

- Cosmic Neon: Bright neon colors for maximum visibility and aggressive trading

📊 INSTITUTIONAL-GRADE DASHBOARD

Unified AI Score Section

- Total Score (-10 to +10): Primary decision metric

- >5: Strong bullish signals

- <-5: Strong bearish signals

- Quality ratings: EXCEPTIONAL > STRONG > MODERATE > WEAK

- Component Analysis: Individual L-Function, Galois, Operadic, and Correspondence contributions

Order Flow Analysis

Revolutionary OFPI integration:

- OFPI Value (-100% to +100%): Real buying vs selling pressure

- Visual Gauge: Horizontal bar chart showing flow intensity

- Momentum Status: SHIFTING, ACCELERATING, STRONG, MODERATE, or WEAK

- Trading Application: Flow shifts often precede major moves

Signal Performance Tracking

- Win Rate Monitoring: Real-time success percentage with emoji indicators

- Signal Count: Total signals generated for frequency analysis

- Current Position: LONG, SHORT, or NONE with P&L tracking

- Volatility Regime: HIGH, MEDIUM, or LOW classification

Market Structure Analysis

- Möbius Field Strength: Mathematical field oscillation intensity

- CHAOTIC: High complexity, use wider stops

- STRONG: Active field, normal position sizing

- MODERATE: Balanced conditions

- WEAK: Low activity, consider smaller positions

- HTF Trend: Higher timeframe bias (BULL/BEAR/NEUTRAL)

- Strategy Agreement: Multi-algorithm consensus level

Position Management

When in trades, displays:

- Entry Price: Original signal price

- Current P&L: Real-time percentage with risk level assessment

- Duration: Bars in trade for timing analysis

- Risk Level: HIGH/MEDIUM/LOW based on current exposure

🚀 SIGNAL GENERATION LOGIC

Balanced Long/Short Architecture

The indicator generates signals through multiple convergent pathways:

Long Entry Conditions:

- Score threshold breach with algorithmic agreement

- Strong bullish order flow (OFPI > 0.15) with positive composite signal

- Bullish pattern recognition with mathematical confirmation

- HTF trend alignment with momentum shifting

- Extreme bullish OFPI (>0.3) with any positive score

Short Entry Conditions:

- Score threshold breach with bearish agreement

- Strong bearish order flow (OFPI < -0.15) with negative composite signal

- Bearish pattern recognition with mathematical confirmation

- HTF trend alignment with momentum shifting

- Extreme bearish OFPI (<-0.3) with any negative score

Exit Logic:

- Score deterioration below continuation threshold

- Signal quality degradation

- Opposing order flow acceleration

- 10-bar minimum between signals prevents overtrading

⚙️ OPTIMIZATION GUIDELINES

Asset-Specific Settings

Cryptocurrency Trading:

- Modular Level: 15-25 (capture volatility)

- L-Function Precision: 0.8-1.3 (reactive to price swings)

- OFPI Length: 10-20 (fast correlation shifts)

- Cascade Levels: 5-7, Theme: Holographic

Stock Index Trading:

- Modular Level: 25-35 (balanced trending)

- L-Function Precision: 1.5-1.8 (stable patterns)

- OFPI Length: 14-20 (standard correlation)

- Cascade Levels: 4-5, Theme: Quantum

Forex Trading:

- Modular Level: 35-45 (smooth trends)

- L-Function Precision: 1.6-2.1 (high smoothing)

- OFPI Length: 18-25 (disable volume amplification)

- Cascade Levels: 3-4, Theme: Crystalline

Timeframe Optimization

Scalping (1-5 minute charts):

- Reduce all lookback parameters by 30-40%

- Increase L-Function precision for noise reduction

- Enable all visual elements for maximum information

- Use Small dashboard to save screen space

Day Trading (15 minute - 1 hour):

- Use default parameters as starting point

- Adjust based on market volatility

- Normal dashboard provides optimal information density

- Focus on OFPI momentum shifts for entries

Swing Trading (4 hour - Daily):

- Increase lookback parameters by 30-50%

- Higher L-Function precision for stability

- Large dashboard for comprehensive analysis

- Emphasize HTF trend alignment

🏆 ADVANCED TRADING STRATEGIES

The Mathematical Confluence Method

1. Wait for Fractal Grid level approach

2. Confirm with projected L-Score > threshold

3. Verify OFPI alignment with direction

4. Enter on portal signal with quality ≥ STRONG

5. Exit on score deterioration or opposing flow

The Regime Trading System

1. Monitor Aether Flow background intensity

2. Trade aggressively during bright purple periods

3. Reduce position size during dark periods

4. Use Möbius Field strength for stop placement

5. Align with HTF trend for maximum probability

The OFPI Momentum Strategy

1. Watch for momentum shifting detection

2. Confirm with accelerating flow in direction

3. Enter on immediate portal signal

4. Scale out at Fibonacci levels

5. Exit on flow deceleration or reversal

⚠️ RISK MANAGEMENT INTEGRATION

Mathematical Position Sizing

- Use Galois Rank for volatility-adjusted sizing

- Möbius Field strength determines stop width

- Fractal Dimension guides maximum exposure

- OFPI momentum affects entry timing

Signal Quality Filtering

- Trade only STRONG or EXCEPTIONAL quality signals

- Increase position size with higher agreement levels

- Reduce risk during CHAOTIC Möbius field periods

- Respect HTF trend alignment for directional bias

🔬 DEVELOPMENT JOURNEY

Creating the LOMV was an extraordinary mathematical undertaking that pushed the boundaries of what's possible in technical analysis. This indicator almost didn't happen. The theoretical complexity nearly proved insurmountable.

The Mathematical Challenge

Implementing the Langlands Program required deep research into:

- Number theory and the Möbius function

- Riemann zeta function convergence properties

- L-function analytical continuation

- Galois representations in finite fields

The mathematical literature spans decades of pure mathematics research, requiring translation from abstract theory to practical market application.

The Computational Complexity

Operadic composition theory demanded:

- Category theory implementation in Pine Script

- Multi-dimensional array management for strategy composition

- Real-time democratic voting algorithms

- Performance optimization for complex calculations

The Integration Breakthrough

Bringing together three disparate mathematical frameworks required:

- Novel approaches to signal weighting and combination

- Revolutionary Order Flow Polarity Index development

- Advanced T3 smoothing implementation

- Balanced signal generation preventing directional bias

Months of intensive research culminated in breakthrough moments when the mathematics finally aligned with market reality. The result is an indicator that reveals market structure invisible to conventional analysis while maintaining practical trading utility.

🎯 PRACTICAL IMPLEMENTATION

Getting Started

1. Apply indicator with default settings

2. Select appropriate theme for your markets

3. Observe dashboard metrics during different market conditions

4. Practice signal identification without trading

5. Gradually adjust parameters based on observations

Signal Confirmation Process

- Never trade on score alone - verify quality rating

- Confirm OFPI alignment with intended direction

- Check fractal grid level proximity for timing

- Ensure Möbius field strength supports position size

- Validate against HTF trend for bias confirmation

Performance Monitoring

- Track win rate in dashboard for strategy assessment

- Monitor component contributions for optimization

- Adjust threshold based on desired signal frequency

- Document performance across different market regimes

🌟 UNIQUE INNOVATIONS

1. First Integration of Langlands Program mathematics with practical trading

2. Revolutionary OFPI with T3 smoothing and momentum detection

3. Operadic Composition using category theory for signal democracy

4. Dynamic Fractal Grid with projected L-Score calculations

5. Multi-Dimensional Visualization through morphism flow portals

6. Regime-Adaptive Background showing market energy intensity

7. Balanced Signal Generation preventing directional bias

8. Professional Dashboard with institutional-grade metrics

📚 EDUCATIONAL VALUE

The LOMV serves as both a practical trading tool and an educational gateway to advanced mathematics. Traders gain exposure to:

- Pure mathematics applications in markets

- Category theory and operadic composition

- Number theory through Möbius function implementation

- Harmonic analysis via L-function calculations

- Advanced signal processing through T3 smoothing

⚖️ RESPONSIBLE USAGE

This indicator represents advanced mathematical research applied to market analysis. While the underlying mathematics are rigorously implemented, markets remain inherently unpredictable.

Key Principles:

- Use as part of comprehensive trading strategy

- Implement proper risk management at all times

- Backtest thoroughly before live implementation

- Understand that past performance does not guarantee future results

- Never risk more than you can afford to lose

The mathematics reveal deep market structure, but successful trading requires discipline, patience, and sound risk management beyond any indicator.

🔮 CONCLUSION

The Langlands-Operadic Möbius Vortex represents a quantum leap forward in technical analysis, bringing PhD-level pure mathematics to practical trading while maintaining visual elegance and usability.

From the harmonic analysis of the Langlands Program to the democratic composition of operadic theory, from the number-theoretic precision of the Möbius function to the revolutionary Order Flow Polarity Index, every component works in mathematical harmony to reveal the hidden order within market chaos.

This is more than an indicator - it's a mathematical lens that transforms how you see and understand market structure.

Trade with mathematical precision. Trade with the LOMV.

*"Mathematics is the language with which God has written the universe." - Galileo Galilei*

*In markets, as in nature, profound mathematical beauty underlies apparent chaos. The LOMV reveals this hidden order.*

— Dskyz, Trade with insight. Trade with anticipation.

VWAP Supply & Demand Zones PRO**Overview:**

This script represents a major evolution of the original "VWAP Supply and Demand Zones" indicator. Initially created to explore price interaction with VWAP, it has now matured into a robust and feature-rich tool for identifying high-probability zones of institutional buying and selling pressure. The update introduces volume and momentum validation, dynamic zone management, alert logic, and a visual dashboard (HUD) — all designed for improved precision and clarity. The structural improvements, anti-repainting logic, and significant added utility warranted releasing this as a new script rather than a minor update.

---

### What It Does:

This indicator dynamically detects **supply and demand zones** using VWAP-based logic combined with **volume** and **momentum confirmation**. When price crosses VWAP with strength, it identifies the potential zone of excess demand (below VWAP) or supply (above VWAP), marking it visually with colored regions on the chart.

Each zone is extended for a user-defined duration, monitored for touch interactions (tests), and tracked for possible breaks. The script helps traders interpret price behavior around these institutional zones as either **reversal** opportunities or **continuation** confirmation depending on context and strategy preference.

---

### How It Works:

* **VWAP Basis**: Zones are anchored at VWAP at the time of a significant cross.

* **Volume & Momentum Filters**: Crosses are only considered valid if backed by above-average volume and notable price momentum.

* **Zone Drawing**: Validated supply and demand zones are drawn as boxes on the chart. Each is extended forward for a customizable number of bars.

* **Touch Counting**: Zones track the number of price touches. Alerts are issued after a user-defined number of tests.

* **Break Detection**: If price closes significantly beyond a zone boundary, the zone is marked as broken and visually dimmed.

* **Visual Dashboard (HUD)**: A compact real-time HUD displays VWAP value, active zone counts, and current market bias.

---

### How to Use It:

**Reversal Trading:**

* Look for price **rejecting** a zone after touching it.

* Use rejection candles or secondary indicators (e.g., RSI divergence) to confirm.

* These setups may offer low-risk entries when price respects the zone.

**Continuation Trading:**

* A **break of a zone** suggests strong directional bias.

* Use confirmed zone breaks to enter in the direction of momentum.

* Ideal in trending environments, especially with high volume and ATR movement.

---

### Key Inputs:

* **VWAP Length**: Moving VWAP period (default: 20)

* **Zone Width %**: Percentage size of zone buffer (default: 0.5%)

* **Min Touches**: How many times price must test a zone before alerts trigger

* **Zone Extension**: How far into the future zones are projected

* **Volume & ATR Filters**: Ensure only strong, valid crossovers create zones

---

### Alerts:

You can enable alerts for:

* **New zone creation**

* **Zone tests (after minimum touch count)**

* **Zone breaks**

* **VWAP crosses**

* **Active presence inside a zone (entry conditions)**

These alerts help automate market monitoring, making it suitable for discretionary or systematic workflows.

---

### Why It's a New Script:

This is not a cosmetic update. The internal logic, signal generation, filtering methodology, visual engine, and UX framework have been entirely rebuilt from the ground up. The result is a highly adaptive, precision-oriented tool — appropriate for intraday scalpers and swing traders alike. It goes far beyond the original in terms of functionality and reliability, justifying a fresh release.

---

### Suitable Markets and Timeframes:

* Works across all liquid markets (crypto, equities, futures, forex)

* Best used on timeframes where volume data is stable (5m and above recommended)

* Recalibrate inputs for optimal detection across instruments

Trend Matrix Multi-Timeframe Dashboard(TechnoBlooms)Trend Matrix Multi-Timeframe Dashboard is a Minimalist Multi-Timeframe Trend Analyzer with Smart Indicator Integration. Trend Matrix MTF Dashboard is a clean, efficient, and visually intuitive trend analyzer built for traders who value simplicity without compromising on technical depth.

This dashboard empowers you to track trend direction across multiple timeframes using a curated set of powerful technical indicators—all from one compact visual panel. The design philosophy is simple: eliminate clutter, highlight trend clarity, and accelerate your decision-making process.

Key Features

✅ Minimalist Design with Maximum Insight

A compact dashboard view designed for clean charts and focused trading

Optimized layout shows everything you need—nothing you don’t

✅ Multi-Timeframe Access at a Glance

Instantly read the trend direction of selected indicators on multiple timeframes (e.g., 15m, 1h, 4h, 1D)

Customize the timeframe stack to fit scalping, intraday, swing, or positional strategies

✅ Robust Technical Indicators Built In

Each one is hand-picked for trend reliability:

MACD – Momentum and crossover confirmation

RSI – Overbought/oversold and directional shift

EMA – Dynamic support/resistance and trend bias

Bollinger Bands – Volatility structure and trend containment

PVT – Volume-Weighted Trend Confirmation

Supertrend – Price-following trend tracker

✅ Live Updates & Lightweight Performance

Built to update efficiently on every bar close

Minimal performance impact even with multiple timeframes active

By offering multi-timeframe (MTF) access to proven trend-following indicators, Trend Matrix helps you confidently align with the market’s dominant direction—without jumping between charts or analyzing indicators one by one.

This indicator offers customizable settings. The trader can choose the input parameters timeframes as per the choice.

Trend Matrix Multi-Timeframe Dashboard helps traders to identify trend based on technical indications. Trader can refer this while taking trading decisions.

🧠 Ideal For

Scalpers who need higher timeframe confirmation

Swing traders identifying clean entries aligned with the macro trend

Trend followers seeking clarity before committing capital

Price action & SMC traders validating market structure setups

Beginners who want a high-level trend guide without messy indicators

VNIndex Over 6.5% Downside Drop Indicator with TableOverview: The VNIndex 6.5% Downside Drop Indicator is a powerful tool designed to help traders and investors identify significant market drops on the VNIndex (or any other asset) based on a 6.5% downside threshold. This Pine Script® indicator automatically detects when the price of an asset drops by more than 6.5% within a single day, and visually marks those events on the chart.

Key Features:

6.5% Downside Drop Detection: Automatically calculates the daily percentage drop and identifies when the price falls by more than 6.5%.

Table Display: Displays the dates and corresponding percentage drops of all identified instances in a convenient table at the bottom right of the chart.

Markers: Red down-pointing markers are plotted above bars where the price drop exceeds the 6.5% threshold, making it easy to spot critical drop events at a glance.

Easy-to-Read Table: The table lists the date and drop percentage, updating dynamically as new drops are detected. This allows for easy tracking of significant downside moves over time.

How to Use:

Install the Script: Add this indicator to your TradingView chart.

Monitor Price Drops: The indicator will automatically detect when the price drops by over 6.5% from the previous close and display a marker on the chart and the table in the bottom right corner.

View the Table: The table displays the date and the percentage drop of each detected event, making it easy to track past significant moves.

Alerts: You can set an alert for 6.5% drops to receive notifications in real-time.

Customization Options:

The drop percentage threshold (6.5%) can be adjusted in the script to fit other market conditions or assets.

The table can be resized or styled based on user preference for better visibility.

Why Use This Indicator? This indicator is perfect for traders looking to spot large, significant price movements quickly. Large downside drops can signal potential market reversals or trading opportunities, and this tool helps you track such events effortlessly. Whether you're monitoring the VNIndex or any other asset, this indicator provides crucial insights into volatile price action, helping you make more informed decisions.

Open Source License: This indicator is open source and free to use under the Mozilla Public License 2.0. You are welcome to modify, distribute, and contribute to the project.

Contributions: Feel free to contribute improvements, fixes, or new features by creating a pull request. Let’s collaborate to make this indicator even better for the community!

real_time_candlesIntroduction

The Real-Time Candles Library provides comprehensive tools for creating, manipulating, and visualizing custom timeframe candles in Pine Script. Unlike standard indicators that only update at bar close, this library enables real-time visualization of price action and indicators within the current bar, offering traders unprecedented insight into market dynamics as they unfold.

This library addresses a fundamental limitation in traditional technical analysis: the inability to see how indicators evolve between bar closes. By implementing sophisticated real-time data processing techniques, traders can now observe indicator movements, divergences, and trend changes as they develop, potentially identifying trading opportunities much earlier than with conventional approaches.

Key Features

The library supports two primary candle generation approaches:

Chart-Time Candles: Generate real-time OHLC data for any variable (like RSI, MACD, etc.) while maintaining synchronization with chart bars.

Custom Timeframe (CTF) Candles: Create candles with custom time intervals or tick counts completely independent of the chart's native timeframe.

Both approaches support traditional candlestick and Heikin-Ashi visualization styles, with options for moving average overlays to smooth the data.

Configuration Requirements

For optimal performance with this library:

Set max_bars_back = 5000 in your script settings

When using CTF drawing functions, set max_lines_count = 500, max_boxes_count = 500, and max_labels_count = 500

These settings ensure that you will be able to draw correctly and will avoid any runtime errors.

Usage Examples

Basic Chart-Time Candle Visualization

// Create real-time candles for RSI

float rsi = ta.rsi(close, 14)

Candle rsi_candle = candle_series(rsi, CandleType.candlestick)

// Plot the candles using Pine's built-in function

plotcandle(rsi_candle.Open, rsi_candle.High, rsi_candle.Low, rsi_candle.Close,

"RSI Candles", rsi_candle.candle_color, rsi_candle.candle_color)

Multiple Access Patterns

The library provides three ways to access candle data, accommodating different programming styles:

// 1. Array-based access for collection operations

Candle candles = candle_array(source)

// 2. Object-oriented access for single entity manipulation

Candle candle = candle_series(source)

float value = candle.source(Source.HLC3)

// 3. Tuple-based access for functional programming styles

= candle_tuple(source)

Custom Timeframe Examples

// Create 20-second candles with EMA overlay

plot_ctf_candles(

source = close,

candle_type = CandleType.candlestick,

sample_type = SampleType.Time,

number_of_seconds = 20,

timezone = -5,

tied_open = true,

ema_period = 9,

enable_ema = true

)

// Create tick-based candles (new candle every 15 ticks)

plot_ctf_tick_candles(

source = close,

candle_type = CandleType.heikin_ashi,

number_of_ticks = 15,

timezone = -5,

tied_open = true

)

Advanced Usage with Custom Visualization

// Get custom timeframe candles without automatic plotting

CandleCTF my_candles = ctf_candles_array(

source = close,

candle_type = CandleType.candlestick,

sample_type = SampleType.Time,

number_of_seconds = 30

)

// Apply custom logic to the candles

float ema_values = my_candles.ctf_ema(14)

// Draw candles and EMA using time-based coordinates

my_candles.draw_ctf_candles_time()

ema_values.draw_ctf_line_time(line_color = #FF6D00)

Library Components

Data Types

Candle: Structure representing chart-time candles with OHLC, polarity, and visualization properties

CandleCTF: Extended candle structure with additional time metadata for custom timeframes

TickData: Structure for individual price updates with time deltas

Enumerations

CandleType: Specifies visualization style (candlestick or Heikin-Ashi)

Source: Defines price components for calculations (Open, High, Low, Close, HL2, etc.)