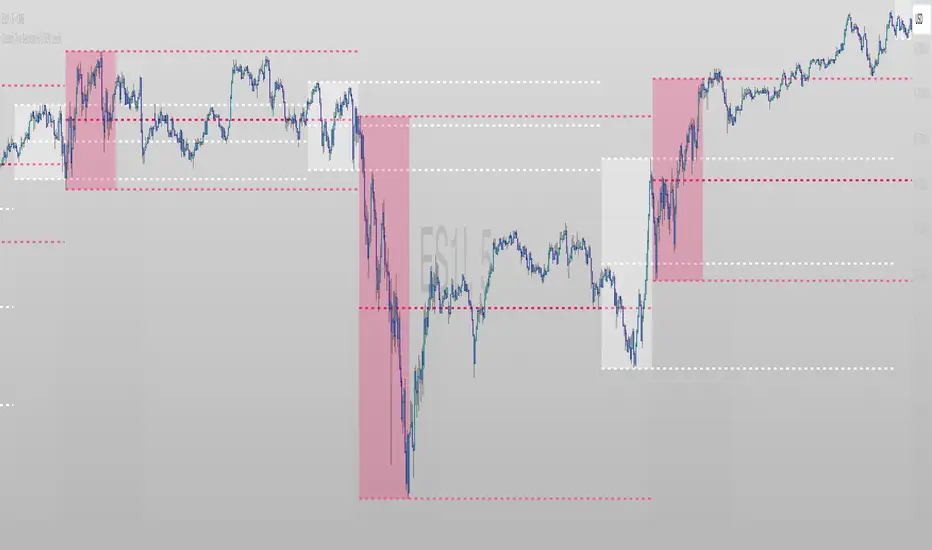

Custom Two Sessions H/L/50% LevelsTrack high/low/midpoint levels across two customizable time sessions. Perfect for monitoring H4 blocks, session ranges, or any custom time periods as reference levels for lower timeframe trading.

What This Indicator Does:

Tracks and projects High, Low, and 50% Midpoint levels for two fully customizable time sessions. Unlike fixed-session indicators, you define EXACTLY when each session starts and ends.

Key Features:

• Two independent sessions with custom start/end times (hour and minute)

• High/Low/50% midpoint tracking for each session

• Visual session boxes showing calculation periods

• Horizontal lines projecting levels into the future

• Historical session levels remain visible for reference

• Works on any chart timeframe (M1, M5, M15, H1, H4, etc.)

• Full visual customization (colors, line styles, widths)

• DST timezone support

Common Use Cases:

H4 Candle Tracking - Set sessions to 4-hour blocks (e.g., 6-10am, 10am-2pm) to track individual H4 highs/lows

H1 Candle Tracking - 1-hour blocks for scalping reference levels

Session Trading - ETH vs RTH, London vs NY, Asian session, etc.

Custom Time Periods - Any time range you want to monitor

How to Use:

The indicator identifies key price levels from higher timeframe periods. Use previous session H/L/50% as reference levels for:

Identifying sweep and reclaim setups

Lower timeframe structural flip confirmations

Support/resistance zones for entries

Delivery targets after breaks of structure

Settings:

Configure each session's start/end times independently. The indicator automatically triggers at the first bar crossing into your specified time, making it compatible with all chart timeframes.

Cerca negli script per "track"

Top N Candle HighlighterTrack highest candle sizes on current timeframes. This short script:

1. Tracks the **top N largest candles** on the current chart

2. Option to use **body size** or **full candle range**

3. Highlights candles using `box.new()` (fully v6 compatible)

4. Optionally shows **rank and size labels**

5. Handles red, green, and doji candles differently with color

Run-Stacked Percentage MoveTracks cumulative percentage change from a dynamic baseline that resets when price direction flips.

The baseline resets to the previous bar's close whenever a non-zero return has the opposite sign from the last non-zero return. Zero-change bars are ignored for flip detection but continue displaying the running cumulative percentage.

Teal histogram bars indicate positive moves from the baseline, red bars indicate negative moves. Useful for comparing directional momentum persistence across different instruments - configure the symbol input to track any security.

LTC Arb ObserverTracks Litecoin price variance across 6 exchanges. Code mostly stolen from Spreadeagle1's "Crypto Strength" script. Could easily be modified to track a different crypto/magic internet coin. Enjoy

Bitcoin Cycles IndicatorTrack Bitcoin's cyclical price patterns across multiple timeframes with this cycle analysis tool. The indicator automatically identifies cycle lows and highs, marking them with clear visual labels that show cycle day counts and failed cycle detection.

Key Features:

Multi-Time frame Support - Optimized settings for Daily, Weekly, Monthly, and Custom time frames

Cycle Tracking - Identifies and labels cycle lows (green) and highs (red) with day counts

Failed Cycle Detection - Highlights when cycles break below previous lows

Customizable Settings - Adjust cycle lengths, colors, and display options for each timeframe

Info Box - Real-time cycle information display with current cycle day count

Projection Boxes - Visual cycle length projections for better analysis

Perfect for Bitcoin traders and analysts who want to understand market cycles and timing. Works best on Daily charts for short-term cycles and Weekly/Monthly charts for longer-term analysis.

Session-Based Sentiment Oscillator [TradeDots]Track, analyze, and monitor market sentiment across global trading sessions with this advanced multi-session sentiment analysis tool. This script provides session-specific sentiment readings for Asian (Tokyo), European (London), and US (New York) markets, combining price action, volume analysis, and volatility factors into a comprehensive sentiment oscillator. It is an original indicator designed to help traders understand regional market psychology and capitalize on cross-session sentiment shifts directly on TradingView.

📝 HOW IT WORKS

1. Multi-Component Sentiment Engine

Price Action Momentum : Calculates normalized price movement relative to recent trading ranges, providing directional sentiment readings.

Volume-Weighted Analysis : When volume data is available, incorporates volume flow direction to validate price-based sentiment signals.

Volatility-Adjusted Factors : Accounts for changing market volatility conditions by comparing current ATR against historical averages.

Weighted Combination : Merges all components using optimized weightings (Price: 1.0, Volume: 0.3, Volatility: 0.2) for balanced sentiment readings.

2. Session-Segregated Tracking

Automatic Session Detection : Precisely identifies active trading sessions based on user-configured time parameters.

Independent Calculations : Maintains separate sentiment accumulation for each major session, updated only during respective active hours.

Historical Preservation : Stores session-specific sentiment values even when sessions are closed, enabling cross-session comparison.

Real-Time Updates : Continuously processes sentiment during active sessions while preserving inactive session data.

3. Cross-Session Transition Analysis

Sentiment Differential Detection : Monitors sentiment changes when transitioning between trading sessions.

Configurable Thresholds : Generates signals only when sentiment shifts exceed user-defined minimum thresholds.

Directional Signals : Provides distinct bullish and bearish transition alerts with visual markers.

Smart Filtering : Applies smoothing algorithms to reduce false signals from minor sentiment variations.

⚙️ KEY FEATURES

1. Session-Specific Dashboard

Real-Time Status Display : Shows current session activity (ACTIVE/CLOSED) for all three major sessions.

Sentiment Percentages : Displays precise sentiment readings as percentages for easy interpretation.

Strength Classification : Automatically categorizes sentiment as HIGH (>50%), MEDIUM (20-50%), or LOW (<20%).

Customizable Positioning : Place dashboard in any corner with adjustable size options.

2. Advanced Signal Generation

Transition Alerts : Triangle markers indicate significant sentiment shifts between sessions.

Extreme Conditions : Diamond markers highlight overbought/oversold threshold breaches.

Configurable Sensitivity : Adjust signal thresholds from 0.05 to 0.50 based on trading style.

Alert Integration : Built-in TradingView alert conditions for automated notifications.

3. Forex Currency Strength Analysis

Base/Quote Decomposition : For forex pairs, separates sentiment into individual currency strength components.

Major Currency Support : Analyzes USD, EUR, GBP, JPY, CHF, CAD, AUD, NZD strength relationships.

Relative Strength Display : Shows which currency is driving pair movement during active sessions.

4. Visual Enhancement System

Session Background Colors : Distinct background shading for each active trading session.

Overbought/Oversold Zones : Configurable extreme sentiment level visualization with colored zones.

Multi-Timeframe Compatibility : Works across all timeframes while maintaining session accuracy.

Customizable Color Schemes : Full color customization for dashboard, signals, and plot elements.

🚀 HOW TO USE IT

1. Add the Script

Search for "Session-Based Sentiment Oscillator " in the Indicators tab or manually add it to your chart. The indicator will appear in a separate pane below your main chart.

2. Configure Session Times

Asian Session : Set Tokyo market hours (default: 00:00-09:00) based on your chart timezone.

European Session : Configure London market hours (default: 07:00-16:00) for European analysis.

US Session : Define New York market hours (default: 13:00-22:00) for American markets.

Timezone Adjustment : Ensure session times match your broker's specifications and account for daylight saving changes.

3. Optimize Analysis Parameters

Sentiment Period : Choose 5-50 bars (default: 14) for sentiment calculation lookback period.

Smoothing Settings : Select 1-10 bars smoothing (default: 3) with SMA, EMA, or RMA options.

Component Selection : Enable/disable volume analysis, price action, and volatility factors based on available data.

Signal Sensitivity : Adjust threshold from 0.05-0.50 (default: 0.15) for transition signal generation.

4. Interpret Readings and Signals

Positive Values : Indicate bullish sentiment for the active session.

Negative Values : Suggest bearish sentiment conditions.

Dashboard Status : Monitor which session is currently active and their respective sentiment strengths.

Transition Signals : Watch for triangle markers indicating significant cross-session sentiment changes.

Extreme Alerts : Note diamond markers when sentiment reaches overbought (>70%) or oversold (<-70%) levels.

5. Set Up Alerts

Configure TradingView alerts for:

- Bullish session transitions

- Bearish session transitions

- Overbought condition alerts

- Oversold condition alerts

❗️LIMITATIONS

1. Data Dependency

Volume Requirements : Volume-based analysis only functions when volume data is provided by your broker. Many forex brokers do not supply reliable volume data.

Price Action Focus : In absence of volume data, sentiment calculations rely primarily on price movement and volatility factors.

2. Session Time Sensitivity

Manual Adjustment Required : Session times must be manually updated for daylight saving time changes.

Broker Variations : Different brokers may have slightly different session definitions requiring time parameter adjustments.

3. Ranging Market Limitations

Trend Bias : Sentiment calculations may be less reliable during extended sideways or low-volatility market conditions.

Lag Consideration : As with all sentiment indicators, readings may lag during rapid market transitions.

4. Regional Market Focus

Major Session Coverage : Designed primarily for major global sessions; may not capture sentiment from smaller regional markets.

Weekend Gaps : Does not account for weekend gap effects on sentiment calculations.

⚠️ RISK DISCLAIMER

Trading and investing carry significant risk and can result in financial loss. The "Session-Based Sentiment Oscillator " is provided for informational and educational purposes only. It does not constitute financial advice.

- Always conduct your own research and analysis

- Use proper risk management and position sizing in all trades

- Past sentiment patterns do not guarantee future market behavior

- Combine this indicator with other technical and fundamental analysis tools

- Consider overall market context and your personal risk tolerance

This script is an original creation by TradeDots, published under the Mozilla Public License 2.0.

Session-based sentiment analysis should be used as part of a comprehensive trading strategy. No single indicator can predict market movements with certainty. Exercise proper risk management and maintain realistic expectations about indicator performance across varying market conditions.

Straddle Charts - Live (Enhanced)Track options straddles with ease using the Straddle Charts - Live (Enhanced) indicator! Originally inspired by @mudraminer, this Pine Script v5 tool visualizes live call, put, and straddle prices for instruments like BANKNIFTY. Plotting call (green), put (red), and straddle (black) prices in a separate pane, it offers real-time insights for straddle strategy traders.

Key Features:

Live Data: Fetches 1-minute (customizable) option prices with error handling for invalid symbols.

Price Table: Displays call, put, straddle prices, and percentage change in a top-left table.

Volatility Alerts: Highlights bars with straddle price changes above a user-defined threshold (default 5%) with a yellow background and concise % labels.

Robust Design: Prevents plot errors with na checks and provides clear error messages.

How to Use: Input your call/put option symbols (e.g., NSE:NIFTY250814C24700), set the timeframe, and adjust the volatility threshold. Monitor straddle costs and volatility for informed trading decisions.

Perfect for options traders seeking a simple, reliable tool to track straddle performance. Check it out and share your feedback!

Intraday Percentage Drawdown from ATHTrack Intraday ATH:

The script maintains an intradayATH variable to track the highest price reached during the trading day up to the current point.

This variable is updated whenever a new high is reached.

Calculate Drawdown and Percentage Drawdown:

The drawdown is calculated as the difference between the intradayATH and the current closing price (close).

The percentage drawdown is calculated by dividing the drawdown by the intradayATH and multiplying by 100.

Plot Percentage Drawdown:

The percentageDrawdown is plotted on the chart with a red line to visually represent the drawdown from the intraday all-time high.

Draw Recession Line:

A horizontal red line is drawn at the 20.00 level, labeled "Recession". The line is styled as dotted and has a width of 2 for better visibility.

Draw Correction Line:

A horizontal yellow line is drawn at the 10.00 level, labeled "Correction". The line is styled as dotted and has a width of 2 for better visibility.

Draw All Time High Line:

A horizontal green line is drawn at the 0.0 level to represent the all-time high, labeled "All Time High". The line is styled as dotted and has a width of 2 for better visibility.

This script will display the percentage drawdown along with reference lines at 20% (recession), 10% (correction), and 0% (all-time high).

BTC ETF Flow Trading SignalsTracks large money flows (500M+) across major Bitcoin ETFs (IBIT, BTCO, FBTC, ARKB, BITB)

Generates long/short signals based on institutional money movement

Shows flow trends and strength of movements

This script provides a foundation for comparing ETF inflows and Bitcoin price. The effectiveness of the analysis depends on the quality of the data and your interpretation of the results. Key levels of 500M and 350M Inflow/Outflow Enjoy

Collaboration with Vivid Vibrations

Enjoy & improve!

VIX Term Structure BackwardationTracks backwardation of the VIX Term Structure using the difference between 2 custom durations VIX / VIX3M /VIX6M/VIX1Y

S&P 5Tracks the 5 largest stocks by market cap in the S&P 500. As of May 2020 they make up 50% of the index

SMA & EMA Simple CrossoverTracks and highlights trends by using a simple SMA and EMA indicator. When a shorter SMA (default set to 10 periods) and a longer EMA (default set to 20 periods) cross over, a cross is placed upon the chart at the crossover point. Defaults settings for the periods and colours can be changed the user to meet their own preferences using the settings button (i.e. without having to edit the script).

weekend rally bloody mondayTracks the gain-loss of the price on Mondays and the range gain-loss from Monday (configurable) to Sunday. Then, it identifies Sunday's pumps that end with a Monday dump.

Moving Gain Loss PercentTracks the percentage gain/loss in three ranges:

single candle (can be turned on or off)

custom range of candles

custom range of candles

For example, with a range of 3 candles, and the serie:

1 - close 10

2 - close 5

3 - close 20

The moving gain would be:

1 - close 10 - gain 10, infinite%

2 - close 5 - gain 5, infinite%

3 - close 18 - gain 8, 80%

Or, for example if the range is 12 candles on a monthly chart, then the result is the Year-To-Date gain/loss plotted as a percentage.

Relative Strength OscillatorTracks an EMA and SMA of the 14 day RSI. Also avoids the market with 14 day RSI is above 90.

Buy when green, sell when red.

Average Price BUY-SELL_Bulent-V2Tracking prices that you have defined and trigger the crossing of them

Tracking Lines with TP/SL + Labels at LeftA simple indicator so you can set your TP and SL tolerance along with capital and leverage.

A red line and green line will represent where current TP and SL would be on the chart along with the number of tokens you need to trade to meet the USD capital to be trades.

Just gives a visual representation of SL to key zones on the chart so you can judge scalp entries a little better :)

Cumulative Price Change %Tracking cumulative percentage change in price for each candle over a period.