Buy The Retrace backtest strategyA trend-following strategy entering pullbacks

Simple but efficient

Mostly used it on 1 min chart but it works extremely well on 5 min as well.

The components of the strategy:

-MTF ATR based Trend

-Fib based cloud to help determine the trend - Caution when trend and cloud shows a different trend - a reversal may be possible.

-Optional values for the signals -how often you would like to get one- can be changed based on - the current close relative to the close-only high-low range over a given period of time.

-3x take profit levels

- all adjustable in %

- take profit quantities adjustable in % for each level

-paints a line where your average position is

-labels the current position size

Be careful where the cloud is broken, a reversal may happen.

Be careful longing / shorting the same levels which acted as a support/resistance before - this is why the win ratio is around 80% only as a small percentage gets stopped out usually.

Would like to get access? Pm me I'll grant it.

Cerca negli script per "trend"

Grid ToolThe core idea of this grid tool is that you have to concentrate less on the trade entries (this happens automatically time-independent but price-dependant) but rather on the validity of the macro trend. Exiting a trend when it is no longer valid is more important than entering a trade. But as long as the trend is valid, the trader participates exponentially in the overall trend.

It is advisable to start with a basic position and then "set up" the grid on this in a ratio of 1/10.

A major advantage of grid trading is that the average entry price in a trend moves further and further away from the current market price while the position continues to grow.

A small timeframe should be used so that the distance between the trades corresponds as closely as possible to the selected grid gap and since TV backtests are carried out with closed bars.

Before starting a grid, pre-analysis the market to make sure it is trending. Select the grid gap and grid position size that you are comfortable with. Monitor the trend and from time to time take some profit :).

PS: The ADX filter looks interesting.

Double EMA CROSS

Double EMA CROSS (DEC)

Useful for identifying and receiving alerts about uptrends and downtrends.

This script uses two Exponential Moving Averages (EMAs) to find price uptrends and downtrends.

An Exponential Moving Average ( EMA ) is a type of moving average that places a greater weight and significance on the most recent data points.

The script produces uptrend and downtrend signals based on crossovers and divergences between the two EMAs,

the user will be able to spot a trend change (when the EMAs crossover) and to determine the strength of the current trend (when the EMAs diverge).

It is also posible to get alerts for uptrends and downtrends on the web and mobile app with sound and pop-ups as well as via email.

The optimal time to enter and exit the market can be concluded from this trend changes.

The user can set their own EMAs, by default they are set to 25 and 75 periods for medium and long term respectively.

When the medium term EMA crosses below the long term EMA the asset is in a downtrend and the price will decline, and when the

medium term EMA crosses above the long term EMA the asset is in an uptrend and price will increase.

This scripts plots the following indicators and signals on the chart to help the user to identify trends:

1.- Medium and long term EMAs as lines overlaid on the price chart.

2.- Up green triangles above bars when the price is on an uptrend and down red triangles below bars when the price is on a downtrend.

3.- Arrows with text to indicate the start of an uptrend or downtrend.

The user can enable and disable the indicators and signals as well as set colors and shapes to their liking.

This script also lets the user create alerts for uptrends and downtrends. To create a new alert using this script follow this instructions:

1.- Once you added this script to your chart, go to the alerts panel (right on web or bottom tool bar on the mobile app) and add a new alert (alarm clock icon with a plus sign).

2.- A modal window will open. On the “Condition” dropdown menu select “DEC”.

3.- On the next dropdown menu (right below the “Condition” one) you can select.

4.- Lastly you can set all the normal alert options and create the alert.

Bitcoin - MA Crossover StrategyBefore You Begin:

Please read these warnings carefully before using this script, you will bear all fiscal responsibility for your own trades.

Trading Strategy Warning - Past performance of this strategy may not equal future performance, due to macro-environment changes, etc.

Account Size Warning - Performance based upon default 10% risk per trade, of account size $100,000. Adjust BEFORE you trade to see your own drawdown.

Time Frame - D1 and H4. H4 has a lower profit factor (more fake-outs, and account drawdown), D1 recommended.

Trend Following System - Profitability of this system is dependent on STRONG future trends in Bitcoin (BTCUSD).

Default Settings:

This script was tested on Daily and 4 Hourly charts using the following default settings. Note that 4 Hourly exhibits higher drawdowns and lower profit factor, whilst Daily appears more stable.

Account Size ($): 100,000 (please adjust to simulate your own risk)

Equity Risk (%): 10 (please adjust to simulate your own risk)

Fast Moving Average (Period): 20

Slow Moving Average (Period): 40

Relative Strength Index (Period): 14

Trading Mechanism:

Trend following strategies work well for assets that display the tendency of long-trends. Please do not use this script on financial assets that have a historical tendency for mean reversion. Bitcoin has historically exhibited strong trends, and thus this script is designed to capitalise on that behaviour. It is hoped (but we cannot predict), that Bitcoin will strongly trend in the coming days.

LONG:

Enter Long - When fast moving average (20) crosses ABOVE slow moving average (40)

Exit Long - When fast moving average (20) crosses BELOW slow moving average (40)

SHORT:

Enter Short - When fast moving average (20) crosses BELOW slow moving average (40)

Exit Short - When fast moving average (20) crosses ABOVE slow moving average (40)

Risk Warnings:

Do note that "moving averages" are a lagging indicator, and as such heavy drawdowns could occur when a trade is open. If you are trading this system manually, it is best to avoid emotions and let the system tell you when to enter and exit. Do not panic and exit manually when under heavy drawdown, always follow the system. Do not be emotional. If possible, connect this to your broker for auto-trading. Ensure that your risk per trade (Equity Risk) is SMALL enough that it does not result in a margin-call on your trading account. Equity risk must always be considered relative to your total account size.

Remember: You bear all financial responsibility for your trades, best of luck.

The MATRIX: Ultimate Crypto Position StrategyHi all,

We are cryptocurrency miners and 'hodlers’ since 2013, with unwavering confidence in the technology behind it. We’d always thought that it would be a life-changing êvent. And we were right. We went from “broke” to making shit loads of money and all the way back to bitter nothing. If you are lucky, you probably haven’t experienced what if feels to be high on cash and then fall very deep low, but let me reassure you, it is a nasty feeling.

Then we wondered, what the hell did we do wrong? Or better say, what didn’t we do right! The answer was dead simple: We had no experience in trading, we were overwhelmed by emotions and we didn't use any trading strategy. Hence, we were doomed to fail from the beginning.

In order to build an all-in-one profitable trading strategy, we had to start from zero. The one thing we learned is that your goal for financial gain cannot be achieved without discipline and consistency. Our prime focus was to absorb as much info as possible regarding trading and coding by doing an extensive self-study, which consequentially took us to the next level.

One of the secrets to being successful from a trading perspective is to have an indefatigable and undying thirst for information and knowledge. As Bruce Lee once said: “Learning is never cumulative; it is a movement of knowing which has no beginning nor end”. So, we adapted what was useful, rejected what was useless, and added our own preferences based on our mindset. We were totally committed to be the best. Our goal was never to lose money again! Of course, this is an illusion, as no single strategy is correct all of the time.

Therefore, the final trading strategy was based on the following key elements:

• The avoidance of risk is more important than absolute profit. Do not anticipate and do not move without market confirmation. Being a little late in your trade is your indication if you are right or wrong.

• Offering simplicity and practicality, for those that do not have the time to trade 24/7.

• Believe in analysis and not in forecasting. Trading is a skill for those who are smart and gambling for those who are not.

In conclusion, we are absolutely thrilled to finally release this trading strategy after one year of extensive back testing and optimization. The script was supposed to be for personal use only, but because Tradingview has helped us a lot in this process, we want to share it with all of you and give something back to this amazing community. If you learned something new today and found value, please give us a like to show your support! We’d really appreciate it.

***The script is invite-only, message us to get script access***

-------------------------------------------------------------------------------------------------

The MATRIX: Ultimate Crypto Position Strategy should be used as follows:

• The trading strategy was designed and optimized for trading cryptocurrencies only ; furthermore it works best on established high market cap cryptocurrencies that have a clear trend such as:

BTCUSD

ETHUSD

LTCUSD

XRMUSD

EOSUSD

ADAUSD

DASHUSD

ETCUSD

• The trading strategy is based on swing/position methodology. The script must therefore be used on daily timeframe candles only (1D) .

• Use USD trading pairs only (e.g. use ETHUSD instead of the ETHBTC) since the individual trend is captured more effectively and therefore gives better results.

-------------------------------------------------------------------------------------------------

The MATRIX:Ultimate Crypto Position Strategy is based on the following indicators:

• Ichimoku Cloud ; acts as the leading indicator.

• Volume ; without strong volume , a market move is not valid.

• MACD and Vortex ; both being used as confirmation indicators.

• Choppiness index ; avoids trading in choppy markets.

• Bullish/ Bearish Regular Divergences in combination with RSI to spot tops and bottoms.

• Simple and Exponential Moving Averages ; prêvents trading against the trend.

The trading strategy is easy to use, trend based and without repainting, meaning once a signal has been made it is permanent and that no future data is used in the decision making. It detects the trend and filters out market noise based on more than 10 technical indicators. ONLY when all indicators align with each other the algorithm prints a BUY or SELL signal. The trading strategy provides high probability trading signals and minimizes risk! This script aims to capture the profit from longer term trending moves and by doing so filters out non-substantial trends and avoids the associated risks with these trades.

-------------------------------------------------------------------------------------------------

The MATRIX: Ultimate Crypto Position Strategy has the following features:

• Automatically generated Buy / Sell alerts in the form of a label.

• NO Repaint once candle is closed.

• SAFEGUARD ; custom built-in security prevẹnts trading when the price is out of equilibrium.

• Customizable Display for the Ichimoku cloud indicator display.

-------------------------------------------------------------------------------------------------

Below are the backtest results. Keep in mind that this strategy is quite conservative resulting in few long positions. These results are therefore no guarantee for the future.

Back test results: (only Long trades, signal to signal, order size: 100% of equity, commision fee 0.1%, period: start of chart)

Exchange-----Asset---------Timeframe---Percent Profitable----Profit Factor-----Total Trades----Max Drawdown---Average bars in trade-----Net Profit

Coinbase-----BTC/USD---------1D----------------100----------------N/A------------------10---------------0.00---------------------54-------------------6183.6

Coinbase-----ETH/USD---------1D----------------100----------------N/A------------------7----------------0.00---------------------46-------------------11673.0

Coinbase-----LTC/USD---------1D-----------------100---------------N/A-------------------7----------------0.00---------------------46------------------4727.0

Bínance------EOS/USD---------1D-----------------100---------------N/A-------------------3----------------0.00---------------------34------------------42.8

Bínance------ADA/USD---------1D-----------------100---------------N/A-------------------2----------------0.00---------------------40------------------118.4

Coinbase-----XTZ/USD---------1D-----------------100---------------N/A-------------------1----------------0.00---------------------36------------------34.4

Bínance------BNB/USD---------1D-----------------66.7--------------10.8-------------------6---------------24.22--------------------38------------------1488.8

Bínance------ETC/USD---------1D-----------------100---------------N/A-------------------2----------------0.00---------------------33------------------94.9

Bínance------XMR/USD---------1D-----------------100---------------N/A-------------------3----------------0.00---------------------43------------------74.2

Bínance------ICX/USD----------1D-----------------100---------------N/A-------------------2----------------0.00---------------------29------------------215.3

-------------------------------------------------------------------------------------------------

Reminder: Use this trading strategy at your own risk and trade responsibly. We are not responsible for any financial loss using this strategy.

***The script is invite-only, message us to get script access***

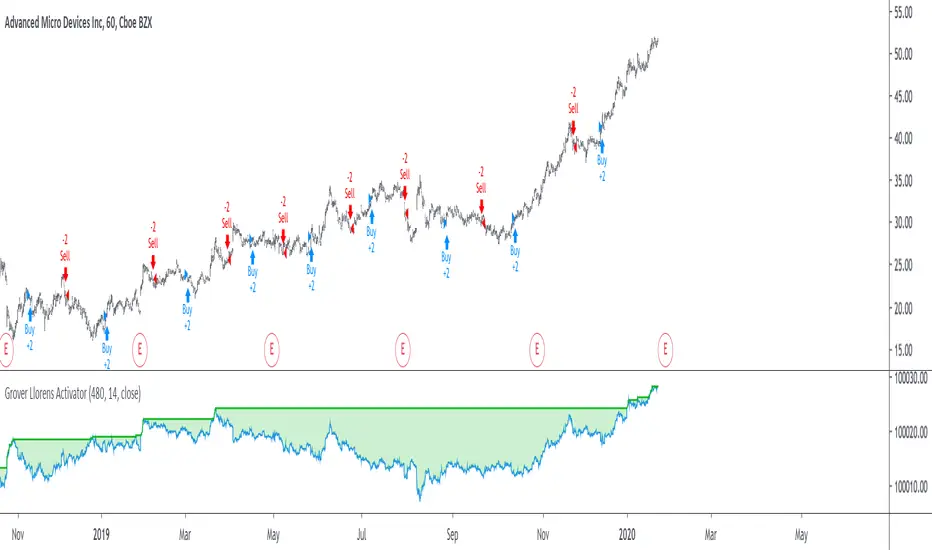

Grover Llorens Activator Strategy AnalysisThe Grover Llorens Activator is a trailing stop indicator deeply inspired by the parabolic SAR indicator, and aim to provide early exit points and reversal detection. The indicator was posted not so long ago, you can find it here :

Today a strategy using the indicator is proposed, and its profitability is analyzed on 3 different markets with the main time frame being 1 hour, remember that lower time frames involve lower absolute price changes, therefore we are way more affected by the spread, and we can require a larger position sizing depending on our investment target, trading higher time-frames is always a good practice and this is why 1 hour is selected. Based on the result we might make various conclusions regarding the indicator accuracy and might have ideas on future improvements of the indicator.

I'am not great when it comes to strategy design, i still hope to share correct and useful information in this post, let me know your thoughts on the post format and if i should make more of these.

Setup And Rules

The analysis is solely based on the indicator signals, money management isn't taken into account, this allow us to have an idea on the indicator robustness and resilience, particularly on extremely volatile markets and ones exhibiting a chaotic structure, altho it is normally good practice to close any position before a market closure in order to avoid any potential major gaps.

The settings used are 480 for length and 14 for mult, this create relatively mid term signals that are suited for a trend indicator such as the Grover Llorens Activator, unfortunately we can't infer the indicator optimal settings, thats how it is with any technical indicator anyway.

Here are the rules of our strategy :

long : closing price cross over the indicator

short : closing price cross under the indicator

We use constant position sizing, once a signal is triggered all the previous positions are closed.

Description Of The Statistics Used

Various statistics are presented in this post, here is a brief description of the main ones :

Percent Profitability (higher = better): Percentage of winning trades, that is : winning trades/total number of trades × 100

Maximum Drawdown (lower = better) : The highest difference between a peak and a valley in the balance, that is : peak - valley , in percentage : (peak - valley)/peak × 100

Profit Factor (higher = better) : Gross profit divided by gross loss, values under 1 represent gross losses superior to the gross profits

Remember that more volatility = more risk, since higher absolute price changes can logically cause larger losses.

EURUSD

The first market analyzed is the Forex market with the EURUSD major pair with a position sizing of 1000 units (1 micro lot). Since October EURUSD is not showing any particular strong trend but posses a discrete rising motion, fortunately cycles can be observed.

The equity was rising until two trades appeared causing a decline in the equity. Before October a bearish market could be observed.

We can see that the equity is rising, the trend still posses various retracements that affect our indicator, however we can see that the indicator totally nail the end of the trend, thats the power of converging toward the price.

In short :

$ 86.63 net profit

340 closed trades

37.65 % profitable (thats a lot of loosing trades)

1.19 profit factor

$ 76.67 max drawdown

Applying a spread would create negative results (in general the average spread is used), not a great start...

BTCUSD

The cryptocurrency market is relatively more volatile than others, which also mean potentially higher returns, we test the indicator using certainly the most traded cryptocurrency, BTCUSD. We will use a position sizing of 1 unit.

In the case of BTCUSD the strategy balance is relatively stationary around the initial capital, with of course high dispersion.

from september to december the market is bearish with various ranging periods, no apparent cycles can be observed, except maybe in the ranging period of october, this ranging period is followed by a non linear trend (relatively parabolic) that the indicator failed to capture in its integrity (this is a recurrent problem and it is starting to piss me off xD).

In short :

$ 2010.64 net profit (aka how i bet the crypto market)

395 closed trades

38.23 % profitable

1.036 profit factor

$ 5738.01 max drawdown (aka how i lost to the crypto market)

AMD

AMD stand for Advanced Micro Devices and is a company focused on the development of computer technology, i love the microprocessor market and i really like AMD who start this year in a pretty great way with a net bullish trend.

The performance of the indicator on AMD is decent (at last !) with the equity producing many new higher highs. The indicator performance still drop in the middle end of 2019 with a large equity drawdown of 17$ caused by the gap of august 8. Unfortunately AMD, like lot of well behaving stocks can only tells us that the indicator has good performances on heavily trending markets with no excess of noise or chaotic structures.

In short :

$ 17.86 net profit (Enough for a consistent lunch)

295 closed trades

36.27 % profitable

1.414 profit factor

$ 10.37 max drawdown.

Conclusion

A strategy using the recently proposed Grover Llorens activator has been presented. We can easily conclude that the indicator can't possibly generate long term returns under chaotic and volatile markets, and could even produce unnecessary trades in trending markets without much parasitic fluctuations such as noise and retracements (think about a simple linear trend) since the indicator converge toward the price and would therefore automatically cross over/under the trend, thus guaranteeing a false signal.

However we have seen its ability to provide accurate early reversal detection shine from time to time, thus over performing lagging indicators in this aspect, however the duration of price fluctuations isn't fixed at a certain period, the rate of convergence should be way faster during volatile fluctuations, of moderate speed during more cyclic fluctuations, and really slow with apparent long term trends, this could be achieved by making the indicator adaptive, but it won't really make it necessarily perform better.

That said i still believe that converging trend indicators are really interesting and aim to capture the non lasting behavior of price fluctuations, they shouldn't receive so much hate (think about the poor p-sar).

Thanks for reading !

Matrix Trend Reverse EngineeringSelling algorithms.

Contact me to code your own indicators or strategy.

Strategy: HMA 50 + Supertrend SniperHMA 50 + Supertrend Confluence Strategy (Trend Following with Noise Filtering)

Description:

Introduction and Concept This strategy is designed to solve a common problem in trend-following trading: Lag vs. False Signals. Standard Moving Averages often lag too much, while price action indicators can generate false signals during choppy markets. This script combines the speed of the Hull Moving Average (HMA) with the volatility-based filtering of the Supertrend indicator to create a robust "Confluence System."

The primary goal of this script is not just to overlay two indicators, but to enforce a strict rule where a trade is only taken when Momentum (HMA) and Volatility Direction (Supertrend) are in perfect agreement.

Why this combination? (The Logic Behind the Mashup)

Hull Moving Average (HMA 50): We use the HMA because it significantly reduces lag compared to SMA or EMA by using weighted calculations. It acts as our primary Trend Direction detector. However, HMA can be too sensitive and "whipsaw" during sideways markets.

Supertrend (ATR-based): We use the Supertrend (Factor 3.0, Period 10) as our Volatility Filter. It uses Average True Range (ATR) to determine the significant trend boundary.

How it Works (Methodology) The strategy uses a boolean logic system to filter out low-quality trades:

Bullish Confluence: The HMA must be rising (Slope > 0) AND the Close Price must be above the Supertrend line (Uptrend).

Bearish Confluence: The HMA must be falling (Slope < 0) AND the Close Price must be below the Supertrend line (Downtrend).

The "Choppy Zone" (Noise Filter): This is a unique feature of this script. If the HMA indicates one direction (e.g., Rising) but the Supertrend indicates the opposite (e.g., Downtrend), the market is considered "Choppy" or indecisive. In this state, the script paints the candles or HMA line Gray and exits all positions (optional setting) to preserve capital.

Visual Guide & Signals To make the script easy to interpret for traders who do not read Pine Script, I have implemented specific visual cues:

Green Cross (+): Indicates a LONG entry signal. Both HMA and Supertrend align bullishly.

Red Cross (X): Indicates a SHORT entry signal. Both HMA and Supertrend align bearishly.

Thick Line (HMA): The main line changes color based on the trend.

Green: Bullish Confluence.

Red: Bearish Confluence.

Gray: Divergence/Choppy (No Trade Zone).

Thin Step Line: This is the Supertrend line, serving as your dynamic Trailing Stop Loss.

Strategy Settings

HMA Length: Default is 50 (Mid-term trend).

ATR Factor/Period: Default is 3.0/10 (Standard for trend catching).

Exit on Choppy: A toggle switch allowing users to decide whether to hold through noise or exit immediately when indicators disagree.

Risk Warning This strategy performs best in trending markets (Forex, Crypto, Indices). Like all trend-following systems, it may experience drawdown during prolonged accumulation/distribution phases. Please backtest with your specific asset before using it with real capital.

Trend Flow & Volatility Guard Strategy [ROSTOK V5]Description:

This strategy is a comprehensive trend-following system designed to identify high-probability entries by aligning long-term market direction with short-term momentum, while strictly filtering out low-quality "choppy" market conditions.

How it Works:

The strategy operates on a multi-stage logic system:

Trend Identification: The core direction is determined by a customizable Main Trend Line (selectable between a long-period EMA or Supertrend). Trades are only taken in the direction of the dominant trend.

Signal Generation: Entries are triggered when a fast-moving Signal Line crosses the Main Trend Line, confirmed by specific candlestick price action (Close > Open).

Advanced Filtering (Confluence): To avoid false signals, the strategy employs a robust set of filters. A trade is only valid if:

Momentum: RSI is within safe operating zones (avoiding extreme overbought/oversold unless a strong trend override is active).

Cycle: CCI and MACD histograms align with the trade direction.

Volatility: The ADX is analyzed to ensure sufficient trend strength, while a Choppiness Index filter blocks trades during sideways/ranging markets.

Risk Management & Recovery: The strategy features built-in money management tools, including:

ADR (Average Daily Range) Filter: Prevents entering trades when the asset has already moved its expected daily distance.

Daily Limits: Hard stops for Max Daily Loss and Target Daily Profit to preserve capital.

Recovery Logic: An optional mechanism to manage drawdowns on difficult days using calculated recovery targets.

Settings & Customization: Users can toggle individual filters (Volume, Choppiness, ADX) and adjust the sensitivity of the trend lines to fit different assets and timeframes (e.g., EURAUD 15m).

Disclaimer: Past performance is not indicative of future results. This script is for educational purposes and backtesting analysis.

Superior-Range Bound Renko - Strategy - 11-29-25 - SignalLynxSuperior-Range Bound Renko Strategy with Advanced Risk Management Template

Signal Lynx | Free Scripts supporting Automation for the Night-Shift Nation 🌙

1. Overview

Welcome to Superior-Range Bound Renko (RBR) — a volatility-aware, structure-respecting swing-trading system built on top of a full Risk Management (RM) Template from Signal Lynx.

Instead of relying on static lookbacks (like “14-period RSI”) or plain MA crosses, Superior RBR:

Adapts its range definition to market volatility in real time

Emulates Renko Bricks on a standard, time-based chart (no Renko chart type required)

Uses a stack of Laguerre Filters to detect genuine impulse vs. noise

Adds an Adaptive SuperTrend powered by a small k-means-style clustering routine on volatility

Under the hood, this script also includes the full Signal Lynx Risk Management Engine:

A state machine that separates “Signal” from “Execution”

Layered exit tools: Stop Loss, Trailing Stop, Staged Take Profit, Advanced Adaptive Trailing Stop (AATS), and an RSI-style stop (RSIS)

Designed for non-repainting behavior on closed candles by basing execution-critical logic on previous-bar data

We are publishing this as an open-source template so traders and developers can leverage a professional-grade RM engine while integrating their own signal logic if they wish.

2. Quick Action Guide (TL;DR)

Best Timeframe:

4 Hours (H4) and above. This is a high-conviction swing-trading system, not a scalper.

Best Assets:

Volatile instruments that still respect market structure:

Bitcoin, Ethereum, Gold (XAUUSD), high-volatility Forex pairs (e.g., GBPJPY), indices with clean ranges.

Strategy Type:

Volatility-Adaptive Trend Following + Impulse Detection.

It hunts for genuine expansion out of ranges, not tiny mean-reversion nibbles.

Key Feature:

Renko Emulation on time-based candles.

We mathematically model Renko Bricks and overlay them on your standard chart to define:

“Equilibrium” zones (inside the brick structure)

“Breakout / impulse” zones (when price AND the impulse line depart from the bricks)

Repainting:

Designed to be non-repainting on closed candles.

All RM execution logic uses confirmed historical data (no future bars, no security() lookahead). Intrabar flicker during formation is allowed, but once a bar closes the engine’s decisions are stable.

Core Toggles & Filters:

Enable Longs and Shorts independently

Optional Weekend filter (block trades on Saturday/Sunday)

Per-module toggles: Stop Loss, Trailing Stop, Staged Take Profits, AATS, RSIS

3. Detailed Report: How It Works

A. The Strategy Logic: Superior RBR

Superior RBR builds its entry signal from multiple mathematical layers working together.

1) Adaptive Lookback (Volatility Normalization)

Instead of a fixed 100-bar or 200-bar range, the script:

Computes ATR-based volatility over a user-defined period.

Normalizes that volatility relative to its recent min/max.

Maps the normalized value into a dynamic lookback window between a minimum and maximum (e.g., 4 to 100 bars).

High Volatility:

The lookback shrinks, so the system reacts faster to explosive moves.

Low Volatility:

The lookback expands, so the system sees a “bigger picture” and filters out chop.

All the core “Range High/Low” and “Range Close High/Low” boundaries are built on top of this adaptive window.

2) Range Construction & Quick Ranges

The engine constructs several nested ranges:

Outer Range:

rangeHighFinal – dynamic highest high

rangeLowFinal – dynamic lowest low

Inner Close Range:

rangeCloseHighFinal – highest close

rangeCloseLowFinal – lowest close

Quick Ranges:

“Half-length” variants of those, used to detect more responsive changes in structure and volatility.

These ranges define:

The macro box price is trading inside

Shorter-term “pressure zones” where price is coiling before expansion

3) Renko Emulation (The Bricks)

Rather than using the Renko chart type (which discards time), this script emulates Renko behavior on your normal candles:

A “brick size” is defined either:

As a standard percentage move, or

As a volatility-driven (ATR) brick, optionally inhibited by a minimum standard size

The engine tracks a base value and derives:

brickUpper – top of the emulated brick

brickLower – bottom of the emulated brick

When price moves sufficiently beyond those levels, the brick “shifts”, and the directional memory (renkoDir) updates:

renkoDir = +2 when bricks are advancing upward

renkoDir = -2 when bricks are stepping downward

You can think of this as a synthetic Renko tape overlaid on time-based candles:

Inside the brick: equilibrium / consolidation

Breaking away from the brick: momentum / expansion

4) Impulse Tracking with Laguerre Filters

The script uses multiple Laguerre Filters to smooth price and brick-derived data without traditional lag.

Key filters include:

LagF_1 / LagF_W: Based on brick upper/lower baselines

LagF_Q: Based on HLCC4 (high + low + 2×close)/4

LagF_Y / LagF_P: Complex averages combining brick structures and range averages

LagF_V (Primary Impulse Line):

A smooth, high-level impulse line derived from a blend of the above plus the outer ranges

Conceptually:

When the impulse line pushes away from the brick structure and continues in one direction, an impulse move is underway.

When its direction flips and begins to roll over, the impulse is fading, hinting at mean reversion back into the range.

5) Fib-Based Structure & Swaps

The system also layers in Fib levels derived from the adaptive ranges:

Standard levels (12%, 23.6%, 38.2%, 50%, 61%, 76.8%, 88%) from the main range

A secondary “swap” set derived from close-range dynamics (fib12Swap, fib23Swap, etc.)

These Fibs are used to:

Bucket price into structural zones (below 12, between 23–38, etc.)

Detect breakouts when price and Laguerre move beyond key Fib thresholds

Drive zSwap logic (where a secondary Fib set becomes the active structure once certain conditions are met)

6) Adaptive SuperTrend with K-Means-Style Volatility Clustering

Under the hood, the script uses a small k-means-style clustering routine on ATR:

ATR is measured over a fixed period

The range of ATR values is split into Low, Medium, High volatility centroids

Current ATR is assigned to the nearest centroid (cluster)

From that, a SuperTrend variant (STK) is computed with dynamic sensitivity:

In quiet markets, SuperTrend can afford to be tighter

In wild markets, it widens appropriately to avoid constant whipsaw

This SuperTrend-based oscillator (LagF_K and its signals) is then combined with the brick and Laguerre stack to confirm valid trend regimes.

7) Final Baseline Signals (+2 / -2)

The “brain” of Superior RBR lives in the Baseline & Signal Generation block:

Two composite signals are built: B1 and B2:

They combine:

Fib breakouts

Renko direction (renkoDir)

Expansion direction (expansionQuickDir)

Multiple Laguerre alignments (LagF_Q, LagF_W, LagF_Y, LagF_Z, LagF_P, LagF_V)

They also factor in whether Fib structures are expanding or contracting.

A user toggle selects the “Baseline” signal:

finalSig = B2 (default) or B1 (alternate baseline)

finalSig is then filtered through the RM state machine and only when everything aligns, we emit:

+2 = Long / Buy signal

-2 = Short / Sell signal

0 = No new trade

Those +2 / -2 values are what feed the Risk Management Engine.

B. The Risk Management (RM) Engine

This script features the Signal Lynx Risk Management Engine, a proprietary state machine built to separate Signal from Execution.

Instead of firing orders directly on indicator conditions, we:

Convert the raw signal into a clean integer (Fin = +2 / -2 / 0)

Feed it into a Trade State Machine that understands:

Are we flat?

Are we in a long or short?

Are we in a closing sequence?

Should we permit re-entry now or wait?

Logic Injection / Template Concept:

The RM engine expects a simple integer:

+2 → Buy

-2 → Sell

Everything else (0) is “no new trade”

This makes the script a template:

You can remove the Superior RBR block

Drop in your own logic (RSI, MACD, price action, etc.)

As long as you output +2 or -2 into the same signal channel, the RM engine can drive all exits and state transitions.

Aggressive vs Conservative Modes:

The input AgressiveRM (Aggressive RM) governs how we interpret signals:

Conservative Mode (Aggressive RM = false):

Uses a more filtered internal signal (AF) to open trades

Effectively waits for a clean trend flip / confirmation before new entries

Minimizes whipsaw at the cost of fewer trades

Aggressive Mode (Aggressive RM = true):

Reacts directly to the fresh alert (AO) pulses

Allows faster re-entries in the same direction after RM-based exits

Still respects your pyramiding setting; this script ships with pyramiding = 0 by default, so it will not stack multiple positions unless you change that parameter in the strategy() call.

The state machine enforces discipline on top of your signal logic, reducing double-fires and signal spam.

C. Advanced Exit Protocols (Layered Defense)

The exit side is where this template really shines. Instead of a single “take profit or stop loss,” it uses multiple, cooperating layers.

1) Hard Stop Loss

A classic percentage-based Stop Loss (SL) relative to the entry price.

Acts as a final “catastrophic protection” layer for unexpected moves.

2) Standard Trailing Stop

A percentage-based Trailing Stop (TS) that:

Activates only after price has moved a certain percentage in your favor (tsActivation)

Then trails price by a configurable percentage (ts)

This is a straightforward, battle-tested trailing mechanism.

3) Staged Take Profits (Three Levels)

The script supports three staged Take Profit levels (TP1, TP2, TP3):

Each stage has:

Activation percentage (how far price must move in your favor)

Trailing amount for that stage

Position percentage to close

Example setup:

TP1:

Activate at +10%

Trailing 5%

Close 10% of the position

TP2:

Activate at +20%

Trailing 10%

Close another 10%

TP3:

Activate at +30%

Trailing 5%

Close the remaining 80% (“runner”)

You can tailor these quantities for partial scaling out vs. letting a core position ride.

4) Advanced Adaptive Trailing Stop (AATS)

AATS is a sophisticated volatility- and structure-aware stop:

Uses Hirashima Sugita style levels (HSRS) to model “floors” and “ceilings” of price:

Dungeon → Lower floors → Mid → Upper floors → Penthouse

These levels classify where current price sits within a long-term distribution.

Combines HSRS with Bollinger-style envelopes and EMAs to determine:

Is price extended far into the upper structure?

Is it compressed near the lower ranges?

From this, it computes an adaptive factor that controls how tight or loose the trailing level (aATS / bATS) should be:

High Volatility / Penthouse areas:

Stop loosens to avoid getting wicked out by inevitable spikes.

Low Volatility / compressed structure:

Stop tightens to lock in and protect profit.

AATS is designed to be the “smart last line” that responds to context instead of a single fixed percentage.

5) RSI-Style Stop (RSIS)

On top of AATS, the script includes a RSI-like regime filter:

A McGinley Dynamic mean of price plus ATR bands creates a dynamic channel.

Crosses above the top band and below the lower band change a directional state.

When enabled (UseRSIS):

RSIS can confirm or veto AATS closes:

For longs: A shift to bearish RSIS can force exits sooner.

For shorts: A shift to bullish RSIS can do the same.

This extra layer helps avoid over-reactive stops in strong trends while still respecting a regime change when it happens.

D. Repainting Protection

Many strategies look incredible in the Strategy Tester but fail in live trading because they rely on intrabar values or future-knowledge functions.

This template is built with closed-candle realism in mind:

The Risk Management logic explicitly uses previous bar data (open , high , low , close ) for the key decisions on:

Trailing stop updates

TP triggers

SL hits

RM state transitions

No security() lookahead or future-bar access is used.

This means:

Backtest behavior is designed to match what you can actually get with TradingView alerts and live automation.

Signals may “flicker” intrabar while the candle is forming (as with any strategy), but on closed candles, the RM decisions are stable and non-repainting.

4. For Developers & Modders

We strongly encourage you to mod this script.

To plug your own strategy into the RM engine:

Look for the section titled:

// BASELINE & SIGNAL GENERATION

You will see composite logic building B1 and B2, and then selecting:

baseSig = B2

altSig = B1

finalSig = sigSwap ? baseSig : altSig

You can replace the content used to generate baseSig / altSig with your own logic, for example:

RSI crosses

MACD histogram flips

Candle pattern detectors

External condition flags

Requirements are simple:

Your final logic must output:

2 → Buy signal

-2 → Sell signal

0 → No new trade

That output flows into the RM engine via finalSig → AlertOpen → state machine → Fin.

Once you wire your signals into finalSig, the entire Risk Management system (Stops, TPs, AATS, RSIS, re-entry logic, weekend filters, long/short toggles) becomes available for your custom strategy without re-inventing the wheel.

This makes Superior RBR not just a strategy, but a reference architecture for serious Pine dev work.

5. About Signal Lynx

Automation for the Night-Shift Nation 🌙

Signal Lynx focuses on helping traders and developers bridge the gap between indicator logic and real-world automation. The same RM engine you see here powers multiple internal systems and templates, including other public scripts like the Super-AO Strategy with Advanced Risk Management.

We provide this code open source under the Mozilla Public License 2.0 (MPL-2.0) to:

Demonstrate how Adaptive Logic and structured Risk Management can outperform static, one-layer indicators

Give Pine Script users a battle-tested RM backbone they can reuse, remix, and extend

If you are looking to automate your TradingView strategies, route signals to exchanges, or simply want safer, smarter strategy structures, please keep Signal Lynx in your search.

License: Mozilla Public License 2.0 (Open Source).

If you make beneficial modifications, please consider releasing them back to the community so everyone can benefit.

RSI Strategy [PrimeAutomation]⯁ OVERVIEW

The RSI Strategy is a momentum-driven trading system built around the behavior of the Relative Strength Index (RSI).

Instead of using traditional overbought/oversold zones, this strategy focuses on RSI breakouts with volatility-based trailing stops, adaptive profit-targets, and optional early-exit logic.

It is designed to capture strong continuation moves after momentum shifts while protecting trades using ATR-based dynamic risk management.

⯁ CONCEPTS

RSI Breakout Momentum: Entries happen when RSI breaks above/below custom thresholds, signaling a shift in momentum rather than mean reversion.

Volatility-Adjusted Risk: ATR defines both stop-loss and profit-target distances, scaling positions based on market volatility.

Dynamic Trailing Stop: The strategy maintains an adaptive trailing level that tightens as price moves in the trade’s favor.

Single-Position System: Only one trade at a time (no pyramiding), maximizing clarity and simplifying execution.

⯁ KEY FEATURES

RSI Signal Engine

• Long when RSI crosses above Upper threshold

• Short when RSI crosses below Lower threshold

These levels are configurable and optimized for trend-momentum detection.

ATR-Based Stop-Loss

A custom ATR multiplier defines the initial stop.

• Long stop = price – ATR × multiplier

• Short stop = price + ATR × multiplier

Stops adjust continuously using a trailing model.

ATR-Based Take Profit (Optional)

Profit targets scale with volatility.

• Long TP = entry + ATR × TP-multiplier

• Short TP = entry – ATR × TP-multiplier

Users can disable TP and rely solely on trailing stops.

Real-Time Trailing Logic

The stop updates bar-by-bar:

• In a long trade → stop moves upward only

• In a short trade → stop moves downward only

This keeps the stop tight as trends develop.

Early Exit Module (Optional)

After X bars in a trade, opposite RSI signals trigger exit.

This reduces holding time during weak follow-through phases.

Full Visual Layer

• RSI plotted with threshold fills

• Entry/TP/Stop visual lines

• Color-coded zones for clarity

⯁ HOW TO USE

Look for RSI Breakouts:

Focus on RSI crossing above the upper boundary (long) or below the lower boundary (short). These moments identify fresh momentum surges.

Use ATR Levels to Manage Risk:

Because stops and targets scale with volatility, the strategy adapts well to both quiet and explosive market phases.

Monitor Trailing Stops for Trend Continuation:

The trailing stop is the primary driver of exits—often outperforming fixed targets by catching larger runs.

Use on Liquid Markets & Mid-Higher Timeframes:

The system performs best where RSI and ATR signals are clean—crypto majors, FX, and indices.

⯁ CONCLUSION

The RSI Strategy is a modern RSI breakout system enhanced with volatility-adaptive risk management and flexible exit logic. It is designed for traders who prefer momentum confirmation over mean reversion, offering a disciplined framework with robust protections and dynamic trend-following capability.

Its blend of ATR-based stops, optional profit targets, and RSI-driven entries makes it a reliable strategy across a wide range of market conditions.

DEMA ATR Strategy [PrimeAutomation]⯁ OVERVIEW

The DEMA ATR Strategy combines trend-following logic with adaptive volatility filters to identify strong momentum phases and manage trades dynamically.

It uses a Double Exponential Moving Average (DEMA) anchored to ATR volatility bands, creating a self-adjusting trend baseline.

When the adjusted DEMA shifts direction, the strategy enters positions and scales out profit in phases based on ATR-driven targets.

This system adapts to volatility, filters noise, and seeks sustained directional moves.

⯁ KEY FEATURES

DEMA-Volatility Hybrid Filter

Uses Double EMA with ATR expansion/compression logic to form a dynamic trend baseline.

Directional Shift Entries

Entries occur when the adjusted DEMA flips trend (bullish crossover or bearish crossunder vs its past value).

Noise Reduction Mechanism

ATR range caps extreme moves and prevents false flips during choppy volatility spikes.

Multi-Level Take Profits

Targets scale out positions at 1×, 2×, and 3× ATR multiples in the trade direction.

Volatility-Adaptive Targets

ATR multiplier ensures profit targets expand/contract based on market conditions.

Single-Direction Exposure

No pyramiding; the strategy flips position only when trend shifts.

Automated Trade Finalization

When all profit targets trigger, the position is fully closed.

⯁ STRATEGY LOGIC

Trend Direction:

DEMA baseline is modified using ATR upper/lower envelopes.

• If the adjusted DEMA rises above previous value → Bullish

• If it falls below previous value → Bearish

Entry Rules:

• Enter Long when bullish shift occurs and no long position exists

• Enter Short when bearish shift occurs and no short position exists

Take Profit Logic:

3 partial exits for each trade based on ATR:

• TP1 = ±1× ATR

• TP2 = ±2× ATR

• TP3 = ±3× ATR

Profit distribution: 30% / 30% / 40%

Exit Conditions:

• Exit when all TPs hit (full scale-out if sum of all TPs 100%)

• Opposite trend signal closes current trade and opens new one

⯁ WHEN TO USE

Trending environments

Medium–high volatility phases

Swing trading and intraday trend plays

Markets that respect momentum continuation (crypto, indices, FX majors)

⯁ CONCLUSION

This strategy blends DEMA trend recognition with ATR-based volatility adaptation to generate cleaner directional entries and structured take-profit exits. It is designed to capture momentum phases while avoiding noise-driven false signals, delivering a disciplined and scalable trend-following approach.

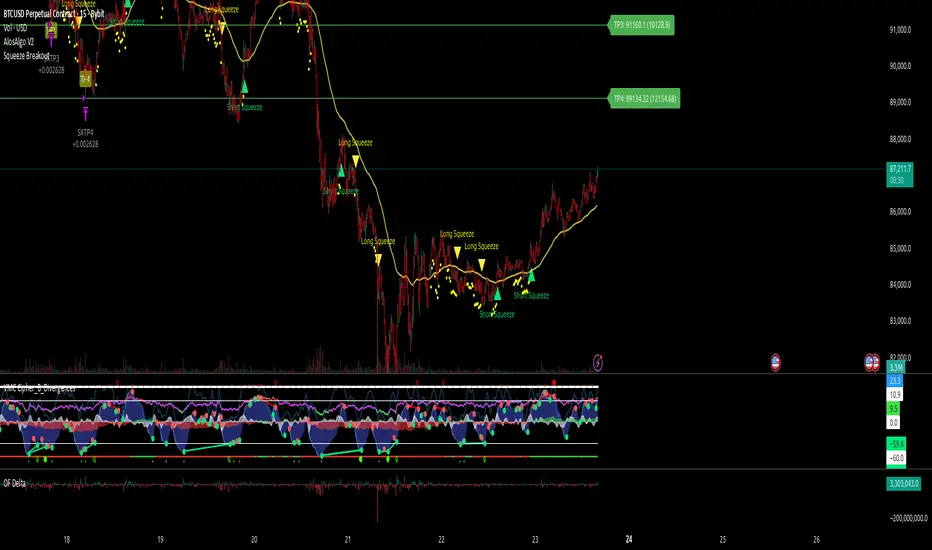

AlosAlgo V2 (BETA)— V2 BETA —

V2 – 2025-11-21 (Update)

• Rebuilt the core signal engine to remove repainting – higher-timeframe Heikin Ashi / Renko now use confirmed bars only for more stable signals & alerts.

• Added Trend Filter MA so longs are only taken above the MA and shorts only below (optional).

• Added MACD momentum filter and Price Action filter (Higher Low for longs, Lower High for shorts) to cut a lot of chop.

• Introduced a loss-streak “circuit breaker” – after X consecutive losing trades the strategy pauses for a set number of bars.

• New TP/SL engine with 2 modes: ATR-based or Fixed % moves, with 4 staged TPs plus an optional runner and break-even SL after TP2.

• Cleaned up TP/SL lines & labels so levels are fixed per trade and easier to read.

• General refactor for more realistic backtests, better live behaviour and easier parameter tuning compared to V1.

ABOUT

AlosAlgo V2 is a multi-timeframe trend + momentum strategy designed for BTC and other high-liquidity markets. It takes directional bias from a higher timeframe, then filters that bias with volatility, momentum and simple price-action structure before it ever opens a trade.

Purely rule-based, no AI / Bayesian / ML.

Core idea

– Use higher-timeframe structure for direction.

– Only trade when trend, momentum and basic price action agree.

– Manage exits with multiple TPs, an optional runner and a hard SL so risk is defined from the start.

Setups

Two main engines:

• Open/Close – Higher-timeframe Heikin Ashi body direction (close vs open) as the core trend signal.

• Renko – ATR-based Renko feed with EMA cross (fast vs slow) as the core trend signal.

Classic sideways filters (ATR + RSI) can be layered on top if you want to only trade in trending or ranging conditions.

Filters added in V2

• Trend Filter MA – Longs only above the MA, shorts only below (length configurable).

• Momentum Filter – Optional MACD filter; only takes longs when MACD is bullish and shorts when MACD is bearish.

• Price Action Filter – Optional HL/LH logic using pivots: longs after a Higher Low, shorts after a Lower High.

• Loss-Streak Circuit Breaker – After N losing trades in a row, the strategy pauses entries for a set number of bars to avoid bad regimes / tilt.

Risk & exits

Two TP/SL modes:

• ATR mode – SL and TP1–TP4 based on ATR at entry (stopFactor / profitFactor).

• Fixed % mode – SL and TP1–TP4 defined as % moves from entry.

On entry the strategy:

• Opens a single position.

• Places 4 staged TPs (TP1–TP4) with user-defined % sizing.

• Optionally leaves a “runner” managed only by SL and trend changes.

• Can move SL to break-even automatically after TP2 (toggle).

All TP/SL levels are locked at entry and drawn on the chart with labels so you can see exactly what the trade is trying to do.

Non-repainting behaviour

V2 is refactored to avoid the repainting behaviour that V1 used. Higher-timeframe and Renko data are taken from confirmed bars only, and entries are based on state (e.g. > / <) instead of repaint-prone crosses. Backtests are much closer to what you’ll see live, and alerts line up with executed trades more reliably.

How to use (suggested defaults)

• Setup: Open/Close

• TPSType: Fixed %

• Trend Filter: ON

• Momentum Filter: ON

• Price Action Filter: ON

• Sideways Filter: No Filtering

Then tweak TP/SL distances and filters per asset + timeframe, and forward-test before sizing up.

Disclaimer

This is not financial advice, not a guarantee of profit and not a “set and forget” money printer. Always forward-test, paper trade and tune risk before using real capital or automation. Markets change – this is a tool, not a promise.

QQQ TimingThis is a trend-following position trading strategy designed for the QQQ and the leveraged ETF QLD (ProShares Ultra QQQ). The primary goal is to capture multi-month holds for maximal profit.

Key Instruments & Performance

The strategy performs best with QLD, which yields far superior results compared to QQQ.

TQQQ (triple-leveraged) results in higher drawdowns and is not the optimal choice.

Important: The system is not intended for use with other indexes, individual stocks, or investments (like crypto or gold), as performance can vary widely.

Buy Signals

The strategy's signals are rooted in the S&P 500 Index (SPX), as testing showed it provides more reliable triggers than using QQQ itself.

Primary Buy Signal (Credit to IBD/Mike Webster): The SPX triggers a buy when its low closes above the 21-day Exponential Moving Average (EMA) for three consecutive days.

Refinement with Downtrend Lines: During corrective or bear periods, results and drawdowns can be significantly improved by incorporating downtrend lines. These lines connect lower highs. The strategy waits for the price to close above a drawn downtrend line before executing a buy. This refinement can modify the primary signal, either by allowing for an earlier entry or, in some cases, completely nullifying a false signal until the trend change proves itself.

Risk Management & Exit Strategy

Initial Buy Risk: A 3.7% stop loss is applied immediately upon the initial entry.

Initial Exit Rule: An exit is required if the QQQ's low drops below the 50-day Simple Moving Average (SMA).

Note: The 3.7% stop often provides protection when the initial buy occurs below the 50-day SMA. However, if QQQ is already trading above its 50-day SMA at the time of the SPX signal (indicating relative strength), historically, it has been better to use the 50-day SMA rule to give the position more room to run.

Trend Exit (Profit-Taking): To stay in a strong trend for the optimal amount of time, the long position is exited when a moving average crossover to the downside is triggered, based around the 107-day Simple Moving Average (SMA).

RastaRasta — Educational Strategy (Pine v5)

Momentum · Smoothing · Trend Study

Overview

The Rasta Strategy is a visual and educational framework designed to help traders study momentum transitions using the interaction between a fast-reacting EMA line and a slower smoothed reference line.

It is not a signal generator or profit system; it’s a learning tool for understanding how smoothing, crossovers, and filters interact under different market conditions.

The script displays:

A primary EMA line (the fast reactive wave).

A Smoothed line (using your chosen smoothing method).

Optional fog zones between them for quick visual context.

Optional DNA rungs connecting both lines to illustrate volatility compression and expansion.

Optional EMA 8 / EMA 21 trend filter to observe higher-time-frame alignment.

Core Idea

The Rasta model focuses on wave interaction. When the fast EMA crosses above the smoothed line, it reflects a shift in short-term momentum relative to background trend pressure. Cross-unders suggest weakening or reversal.

Rather than treating this as a trading “signal,” use it to observe structure, study trend alignment, and test how smoothing type affects reaction speed.

Smoothing Types Explained

The script lets you experiment with multiple smoothing techniques:

Type Description Use Case

SMA (Simple Moving Average) Arithmetic mean of the last n values. Smooth and steady, but slower. Trend-following studies; filters noise on higher time frames.

EMA (Exponential Moving Average) Weights recent data more. Responds faster to new price action. Momentum or reactive strategies; quick shifts and reversals.

RMA (Relative Moving Average) Used internally by RSI; smooths exponentially but slower than EMA. Momentum confirmation; balanced response.

WMA (Weighted Moving Average) Linear weights emphasizing the most recent data strongly. Intraday scalping; crisp but potentially noisy.

None Disables smoothing; uses the EMA line alone. Raw comparison baseline.

Each smoothing method changes how early or late the strategy reacts:

Faster smoothing (EMA/WMA) = more responsive, good for scalping.

Slower smoothing (SMA/RMA) = more stable, good for trend following.

Modes of Study

🔹 Scalper Mode

Use short EMA lengths (e.g., 3–5) and fast smoothing (EMA or WMA).

Focus on 1 min – 15 min charts.

Watch how quick crossovers appear near local tops/bottoms.

Fog and rung compression reveal volatility contraction before bursts.

Goal: study short-term rhythm and liquidity pulses.

🔹 Momentum Mode

Use moderate EMA (5–9) and RMA smoothing.

Ideal for 1 H–4 H charts.

Observe how the fog color aligns with trend shifts.

EMA 8 / 21 filter can act as macro bias; “Enter” labels will appear only in its direction when enabled.

Goal: study sustained motion between pullbacks and acceleration waves.

🔹 Trend-Follower Mode

Use longer EMA (13–21) with SMA smoothing.

Great for daily/weekly charts.

Focus on periods where fog stays unbroken for long stretches — these illustrate clear trend dominance.

Watch rung spacing: tight clusters often precede consolidations; wide rungs signal expanding volatility.

Goal: visualize slow-motion trend transitions and filter whipsaw conditions.

Components

EMA Line (Red): Fast-reacting short-term direction.

Smoothed Line (Yellow): Reference trend baseline.

Fog Zone: Green when EMA > Smoothed (up-momentum), red when below.

DNA Rungs: Thin connectors showing volatility structure.

EMA 8 / 21 Filter (optional):

When enabled, the strategy will only allow Enter events if EMA 8 > EMA 21.

Use this to study higher-trend gating effects.

Educational Applications

Momentum Visualization: Observe how the fast EMA “breathes” around the smoothed baseline.

Trend Transitions: Compare different smoothing types to see how early or late reversals are detected.

Noise Filtering: Experiment with fog opacity and smoothing lengths to understand trade-off between responsiveness and stability.

Risk Concept Simulation: Includes a simple fixed stop-loss parameter (default 13%) for educational demonstrations of position management in the Strategy Tester.

How to Use

Add to Chart → “Strategy.”

Works on any timeframe and instrument.

Adjust Parameters:

Length: base EMA speed.

Smoothing Type: choose SMA, EMA, RMA, or WMA.

Smoothing Length: controls delay and smoothness.

EMA 8 / 21 Filter: toggles trend gating.

Fog & Rungs: visual study options only.

Study Behavior:

Use Strategy Tester → List of Trades for entry/exit context.

Observe how different smoothing types affect early vs. late “Enter” points.

Compare trend periods vs. ranging periods to evaluate efficiency.

Combine with External Tools:

Overlay RSI, MACD, or Volume for deeper correlation analysis.

Use replay mode to visualize crossovers in live sequence.

Interpreting the Labels

Enter: Marks where fast EMA crosses above the smoothed line (or when filter flips positive).

Exit: Marks where fast EMA crosses back below.

These are purely analytical markers — they do not represent trade advice.

Educational Value

The Rasta framework helps learners explore:

Reaction time differences between moving-average algorithms.

Impact of smoothing on signal clarity.

Interaction of local and global trends.

Visualization of volatility contraction (tight DNA rungs) and expansion (wide fog zones).

It’s a sandbox for studying price structure, not a promise of profit.

Disclaimer

This script is provided for educational and research purposes only.

It does not constitute financial advice, trading signals, or performance guarantees. Past market behavior does not predict future outcomes.

Users are encouraged to experiment responsibly, record observations, and develop their own understanding of price behavior.

Author: Michael Culpepper (mikeyc747)

License: Educational / Open for study and modification with credit.

Philosophy:

“Learning the rhythm of the market is more valuable than chasing its profits.” — Rasta

Sigma Trinity ModelAbstract

Sigma Trinity Model is an educational framework that studies how three layers of market behavior interact within the same trend: (1) structural momentum (Rasta), (2) internal strength (RSI), and (3) continuation/compounding structure (Pyramid). The model deliberately combines bar-close momentum logic with intrabar, wick-aware strength checks to help users see how reversals form, confirm, and extend. It is not a signal service or automation tool; it is a transparent learning instrument for chart study and backtesting.

Why this is not “just a mashup”

Many scripts merge indicators without explaining the purpose. Sigma Trinity is a coordinated, three-engine study designed for a specific learning goal:

Rasta (structure): defines when momentum actually flips using a dual-line EMA vs smoothed EMA. It gives the entry/exit framework on bar close for clean historical study.

RSI (energy): measures internal strength with wick-aware triggers. It uses RSI of LOW (for bottom touches/reclaims) and RSI of HIGH (for top touches/exhaustion) so users can see intrabar strength/weakness that the close can hide.

Pyramid (progression): demonstrates how continuation behaves once momentum and strength align. It shows the logic of adds (compounding) as a didactic layer, also on bar close to keep historical alignment consistent.

These three roles are complementary, not redundant: structure → strength → progression.

Architecture Overview

Execution model

Rasta & Pyramid: bar close only by default (historically stable, easy to audit).

RSI: per tick (realtime) with bar-close backup by default, using RSI of LOW for entries and RSI of HIGH for exits. This makes the module sensitive to intra-bar wicks while still giving a close-based safety net for backtests.

Stops (optional in strategy builds): wick-accurate: trail arms/ratchets on HIGH; stop hit checks with LOW (or Close if selected) with a small undershoot buffer to avoid micro-noise hits.

Visual model

Dual lines (EMA vs smoothed EMA) for Rasta + color fog to see direction and compression/expansion.

Rungs (small vertical lines) drawn between the two Rasta lines to visualize wave spacing and rhythm.

Clean labels for Entry/Exit/Pyramid Add/RSI events. Everything is state-locked to avoid spamming.

Module 1 — Rasta (Structural Momentum Layer)

Goal: Identify structural momentum reversals and maintain a consistent, replayable backbone for study.

Method:

Compute an EMA of a chosen price source (default Close), and a smoothed version (SMA/EMA/RMA/WMA/None selectable).

Flip points occur when the EMA line crosses the smoothed line.

Optional EMA 8/21 trend filter can gate entries (long-bias when EMA8 > EMA21). A small “adaptive on flip” option lets an entry fire when the filter itself flips to ON and the EMA is already above the smoothed line—useful for trend resumption.

Why bar close only?

Bar-close Rasta gives a stable, auditable timeline for the structure of the trend. It teaches users to separate “structure” (close-resolved) from “energy” (intrabar, via RSI).

Visuals:

Fog between the lines (green/red) to show regime.

Rungs between lines to show spread (compression vs expansion).

Optional plotting of EMA8/EMA21 so users can see the gating effect.

Module 2 — RSI (Internal Strength / Energy Layer)

Goal: Reveal the intrabar strength/weakness that often precedes or confirms structural flips.

Method:

Standard RSI with adjustable length and signal smoothing for the panel view.

Logic uses wick-aware sources:

Entry trigger: RSI of LOW (same RSI length) touching or below a lower band (default 15). Think of it as intraband reactivation from the bottom, using the candle’s deepest excursion.

Exit trigger: RSI of HIGH touching or above an upper band (default 85). Think of it as exhaustion at the top, using the candle’s highest excursion.

Realtime + Close Backup: fires intrabar on tick, but if the realtime event was missed, the close backup will note it at bar end.

Cooldown control: optional bars-between-signals to avoid rapid re-triggers on choppy sequences.

Why wick-aware RSI?

A close-only RSI can miss the true micro-extremes that cause reversals. Using LOW/HIGH for triggers captures the behavior that traders actually react to during the bar, while the bar-close backup preserves historical reproducibility.

Module 3 — Pyramid (Continuation / Compounding Layer)

Goal: Teach how continuation behaves once a trend is underway, and how adds can be structured.

Method:

Same dual-line logic as Rasta (EMA vs smoothed EMA), but only fires when already in a position (or after prior entry conditions).

Supports the same EMA 8/21 filter and optional adaptive-on-flip behavior.

Bar close only to maintain historical cohesion.

What it teaches:

Adds tend to cluster when momentum persists.

Students can experiment with add spacing and compare “one-shot entries” vs “laddered adds” during strong regimes.

How the Pieces Work Together

Rasta establishes the structural frame (when the wave flip is real enough to record at close).

RSI validates or challenges that structure by tracking intrabar energy at the extremes (low/high touches).

Pyramid shows what sustained continuation looks like once (1) and (2) align.

This produces a layered view: Structure → Energy → Progression. Users can see when all three line up (strongest phases) and when they diverge (riskier phases or transitions).

How to Use It (Step-by-Step)

Quick Start

Apply script to any symbol/timeframe.

In Strategy/Indicator Properties:

Enable On every tick (recommended).

If available, enable Using bar magnifier and choose a lower resolution (e.g., 1m) to simulate intrabar fills more realistically.

Keep On bar close unchecked if you want to observe realtime logic in live charts (strategies still place orders on close by platform design).

Default behavior: Rasta & Pyramid = bar close; RSI = per tick with close backup.

Reading the Chart

Watch for Rasta Entry/Exit labels: they define clean structural turns on close.

Watch RSI Entry (LOW touch at/below lower band) and RSI Exit (HIGH touch at/above upper band) to gauge internal energy extremes.

Pyramid Add labels reveal continuation phases once a move is already in progress.

Tuning

Rasta smoothing: choose SMA/EMA/RMA/WMA or None. Higher smoothing → later but cleaner flips; lower smoothing → earlier but choppier.

RSI bands: a common educational setting is 15/85 for strong extremes; 20/80 is a bit looser.

Cooldown: increase if you see too many RSI re-fires in chop.

EMA 8/21 filter: toggle ON to study “trend-gated” entries, OFF to study raw momentum flips.

Backtesting Notes (for Strategy Builds)

Stops (optional): trail is armed when price advances by a trigger (default D–F₀), ratchets only upward from HIGH, and hits from LOW (or Close if chosen) with a tiny undershoot buffer to avoid micro-wicks.

Order sequencing per bar (mirrors the script’s code comments):

Trail ratchet via HIGH

Intrabar stop hit via LOW/CLOSE → immediate close

If still in position at bar close: process exits (Rasta/RSI)

If still in position at bar close: process Pyramid Add

If flat at bar close: process entries (Rasta/RSI)

Platform reality: strategies place orders at bar close in historical testing; the intrabar logic improves realism for stops and event marking but final order timestamps are still close-resolved.

Inputs Reference (common)

Modules: enable/disable RSI and Pyramid learning layers.

Rasta: EMA length, smoothing type/length, EMA8/21 filter & adaptive flip, fog opacity, rungs on/off & limit.

RSI: RSI length, signal MA length (panel), Entry band (LOW), Exit band (HIGH), cooldown bars, labels.

Pyramid: EMA length, smoothing, EMA8/21 filter & adaptive adds.

Execution: toggle Bar Close Only for Rasta/Pyramid; toggle Realtime + Close Backup for RSI.

Stops (strategy): Fixed Stop % (first), Fixed Stop % (add), Trail Distance %, Trigger rule (auto D–F₀ or custom), undershoot buffer %, and hit source (LOW/CLOSE).

What to Study With It

Convergence: how often RSI-LOW entry touches precede the next Rasta flip.

Divergence: cases where RSI screams exhaustion (HIGH >= upper band) but Rasta hasn’t flipped yet—often transition zones.

Continuation: how Pyramid adds cluster in strong moves; how spacing changes with smoothing/filter choices.

Regime changes: use EMA8/21 filter toggles to see what happens at macro turns vs chop.

Limitations & Scope

This is a learning tool, not a trade copier. It does not provide financial advice or automated execution.

Intrabar results depend on data granularity; bar magnifier (when available) can help simulate lower-resolution ticks, but true tick-by-tick fills are a platform-level feature and not guaranteed across all symbols.

Suggested Publication Settings (Strategy)

Initial capital: 100

Order size: 100 USD (cash)

Pyramiding: 10

Commission: 0.25%

Slippage: 3 ticks

Recalculate: ✓ On every tick

Fill orders: ✓ Using bar magnifier (choose 1m or similar); leave On bar close unchecked for live viewing.

Educational License

Released under the Michael Culpepper Gratitude License (2025).

Use and modify freely for education and research with attribution. No resale. No promises of profitability. Purpose is understanding, not signals.

Strategy Builder v1.0.0 [BigBeluga]🔵 OVERVIEW

The Strategy Builder combines advanced price-action logic, smart-money concepts, and volatility-adaptive momentum signals to automate high-quality entries and exits across any market. It blends trend recognition, market structure shifts, order block reactions, imbalance (FVG) signals, liquidity sweeps, candlestick confirmations, and oscillator-powered divergences into one cohesive engine.

Whether used as a full automation workflow or as a structured confirmation framework, this strategy provides a disciplined, rules-driven method to trade with logic — not emotion.

🔵 BACKTEST WINDOW CONTROL

This module allows you to restrict strategy execution to a specific historical period.

Ideal for performance isolation, regime testing, and forward-walk validation.

Limit Backtest Window

Enabling this option activates custom date filters for the backtest engine.

Start — Define the starting date & time for backtesting

End — Define the ending date & time for backtesting

Only trades and signals inside this window are executed

Reduces computation load on large datasets

Useful for testing specific market environments (e.g., bull cycles, crash periods, sideways regimes)

🔵 SIGNAL GLOSSARY (Advanced Technical Explanation)

Traders can build long and short setups using up to 6 configurable entry conditions for each direction.

Every condition can be set as Bullish or Bearish and mapped to any signal source — allowing deep customization

Below is the full internal logic overview of every signal available in the Strategy Builder.

Signals are based on trend models, volatility structures, liquidity logic, oscillator behavior, and market structure mapping.

Trend Signals (Low-Lag Trend Engine)

Uses a proprietary low-lag baseline + momentum gradient model to detect directional bias.

Trend Signal — Momentum breaks above/below adaptive trend baseline.

Trend Signal+ — Stronger trend confirmation using volatility-weighted momentum.

Trend Signal Any — Triggers when any bullish/bearish trend signal appears.

SmartBand & Retests (Adaptive Volatility Bands)

Dynamic envelope that contracts/expands with volatility & trend strength.

SmartBand Retest — Price retests dynamic band and rejects, confirming continuation.

ActionWave Signals (Impulse-Pullback Engine)

Tracks wave behavior, acceleration and deceleration in price.

ActionWave — Detects directional impulse strength vs pullback weakness.

ActionWave Cross — Momentum acceleration threshold crossed → trend ignition.

Magnet Signals (Liquidity Gravity + Mean Reversion Bias)

Detects zones where price is being drawn due to liquidity voids or imbalance.

Magnet — Trend and liquidity pressure align, creating directional “pull.”

MagnetBar Low Momentum — Low-volatility compression → pre-breakout condition.

Flow Trend (Directional Flow State + ATR Envelope)

Higher-timeframe bias confirmation + dynamic volatility filter.

FlowTrend — Confirms major directional bias (uptrend or downtrend).

FlowTrend Retest — Price tests HTF flow band and rejects → trend resume.

Voltix (Volatility Expansion Pulse)

Detects regime shift from quiet accumulation → trending expansion.

Voltix — Breakout volatility signature, trend acceleration trigger.

Candlestick Pattern (Algorithmic Price Action Recognition)

Auto-recognizes meaningful reversal or continuation candle formations.

Candlestick Pattern — Confirms momentum reversal/continuation via candle logic.

OrderBlock Logic (Institutional Footprint System)

Institutional demand/supply zone tracking with mitigation logic.

Order Block Touch — Price taps institutional zone → reaction filter.

Order Block Break — OB invalidation → institutional flow shift.

Market Structure Engine (Swing Logic + Volume Confirmation)

Tracks major swing breaks and structural reversals.

BoS — Break of Structure in trend direction (continuation bias).

ChoCh — Change of Character — early reversal marker.

Fair Value Gaps (Imbalance & Volume Displacement)

Identifies inefficiencies caused by rapid displacement moves.

FVG Created — Price leaves inefficiency behind.

FVG Retest — Price returns to rebalance inefficiency → reaction zone.

Liquidity Events (Stop-Run & Reversal Logic)

Detects stop-hunt events and liquidity sweeps.

SFP — Swing failure & wick sweep → reversal confirmation.

Liquidity Created — New equal highs/lows form liquidity pool.

Liquidity Grab — Sweep through liquidity line followed by rejection.

Support / Resistance Break Logic

Adaptive zone recognition + momentum confirmation.

Support/Resistance Cross — Zone decisively broken → structural shift.

Pattern Breakouts (Market Geometry Engine)

Tracks breakout from compression & expansion formations.

Channel Break — Channel breakout → trend acceleration.

Wedge Break — Break from contraction wedge → burst of momentum.

Session Logic (Opening Range Behavior)

Session-based volatility trigger.

Session Break — Break above/below session opening range.

Momentum / Reversal Oscillator Suite

Oscillator-driven exhaustion & reversal signals.

Nautilus Signals — Momentum reversal signature (oscillator shift).

Nautilus Peak — Momentum peak → exhaustion risk.

OverSold/Overbought ❖ — Extreme exhaustion zones → reversal setup.

DipX Signals ✦ — Dip buy / Dip sell timing, micro-reversal engine.

Advanced Divergence Engine

Momentum/price disagreement layer with multi-trigger confirmation.

Normal Divergence — Classic divergence reversal.

Hidden Divergence — Trend continuation divergence.

Multiple Divergence — Multiple divergence confirmations stacked → high confidence.

🔧 Adjustable Signal Logic

Some signals in this system can be additionally refined through the strategy settings panel.

This allows traders to tune internal behavior for different market regimes, assets, and volatility conditions.

🔵 LONG / SHORT EXIT CONDITIONS

This section allows you to automate exits using the same advanced market conditions available for entries.

Each exit rule consists of:

Toggle — Enable/disable individual exit rule.

Direction Filter — Trigger exit only if selected market bias appears (Bullish/Bearish).

Signal Type — Choose which market event triggers the exit (same list as entry conditions).

When the active conditions are met, the strategy automatically closes the current position — ensuring emotion-free risk management and systematic trade control.

🔵 TAKE PROFIT & STOP LOSS SYSTEM

This strategy builder provides a fully dynamic risk-management engine designed for both systematic traders and discretionary confirmation users.

Take Profit Logic

Scale out of trades progressively or exit fully using algorithmic TP levels.

Up to 3 Take-Profit targets available

Choose TP calculation method:

• ATR-based distance (volatility-adaptive targets)

• %-based distance (fixed percentage from entry)

Define Size — ATR multiplier or % value

Custom Exit Size per TP (e.g., 25% / 25% / 50%)

Visual TP plotting on chart for clarity

Stop Loss Logic

Automated protection logic for every trade.

Two SL Modes:

• Fixed Stop Loss — static SL from entry

• Trailing Stop Loss — SL follows price as trade progresses

Distance options:

• ATR multiplier (adapts to volatility)

• %-based from entry (fixed distance)

SL dynamically draws on chart for transparency

Trailing SL behavior:

Follows price only in profitable direction

Never moves against the trade

Locks profits as trend develops

🔵 Strategy Dashboard

A compact on-chart performance dashboard is included to help monitor live trade status and backtest results in real time.

It displays key metrics:

Start Capital — Initial account balance used in simulation.

Position Size — % of capital allocated per trade based on user settings (It changes if the trade hits take profits, when more than one take profit is selected).