VWAP Trend Strategy (Intraday) [KedarArc Quant]Description:

An intraday strategy that anchors to VWAP and only trades when a local EMA trend gate and a volume participation gate are both open. It offers two entry templates—Cross and Cross-and-Retest—with an optional Momentum Exception for impulsive moves. Exits combine a TrendBreak (structure flips) with an ATR emergency stop (risk cap).

Updates will be published under this script.

Why this merits a new script

This is not a simple “VWAP + EMA + ATR” overlay. The components are sequenced as gates and branches that *change the trade set* in ways a visual mashup cannot:

1. Trend Gate first (EMA fast vs. slow on the entry timeframe)

Counter-trend VWAP crosses are suppressed. Many VWAP scripts fire on every cross; here, no entry logic even evaluates unless the trend gate is open.

2. Participation Gate second (Volume SMA × multiplier)

This gate filters thin liquidity moves around VWAP. Without it, the same visuals would produce materially more false triggers.

3. Branching entries with structure awareness

* Cross: Immediate VWAP cross in the trend direction.

* Cross-and-Retest: Requires a revisit to VWAP vicinity within a lookback window (recent low near VWAP for longs; recent high for shorts). This explicitly removes first-touch fakeouts that a plain cross takes.

* Momentum Exception (optional): A quantified body% + volume condition can bypass the retest when flow is impulsive—intentional risk-timing, not “just another indicator.”

4. Dual exits that reference both anchor and structure

* TrendBreak: Close only when price loses VWAP and EMA alignment flips.

* ATR stop: Placed at entry to cap tail risk.

These exits complement the entry structure rather than being generic stop/target add-ons.

What it does

* Trades the session’s fair value anchor (VWAP), but only with local-trend agreement (EMA fast vs. slow) and sufficient participation (volume filter).

* Lets you pick Cross or Cross-and-Retest entries; optionally allow a fast Momentum Exception when candles expand with volume.

* Manages positions with a structure exit (TrendBreak) and an emergency ATR stop from entry.

How it works (concepts & calculations)

* VWAP (session anchor):

Standard VWAP of the active session; entries reference the cross and the retest proximity to VWAP.

* Trend gate:

Long context only if `EMA(fast) > EMA(slow)`; short only if `EMA(fast) < EMA(slow)`.

A *gate*, not a trigger—entries aren’t considered unless this is true.

* Participation (volume) gate:

Require `volume > SMA(volume, volLen) × volMult`.

Screens out low-participation wiggles around VWAP.

Entries:

* Cross: Price crosses VWAP in the trend direction while volume gate is open.

* Cross-and-Retest: After crossing, price revisits VWAP vicinity within `lookback` (recent *low near VWAP* for longs; recent *high near VWAP* for shorts).

* Momentum Exception (optional): If body% (|close−open| / range) and volume exceed thresholds, enter without waiting for the retest.

Exits:

* TrendBreak (structure):

* Longs close when `price < VWAP` and `EMA(fast) < EMA(slow)` (mirror for shorts).

* ATR stop (risk):

* From entry: `stop = entry ± ATR(atrLen) × atrMult`.

How to use it ?

1. Select market & timeframe: Intraday on liquid symbols (equities, futures, crypto).

2. Pick entry mode:

* Start with Cross-and-Retest for fewer, more selective signals.

* Enable Momentum Exception if strong moves leave without retesting.

3. Tune guards:

* Raise `volMult` to ignore thin periods; lower it for more activity.

* Adjust `lookback` if retests come late/early on your symbol.

4. Risk:

* `atrLen` and `atrMult` set the emergency stop distance.

5. Read results per session: Optional panel (if enabled) summarizes Net-R, Win%, and PF for today’s session to evaluate

behavior regime by regime.

⚠️ Disclaimer

This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

Cerca negli script per "vwap"

VWAP StrategyVWAP and volatility filters for structured intraday trades.

How the Strategy Works

1. VWAP Anchored to Session

VWAP is calculated from the start of each trading day.

Standard deviations are used to create bands above/below the VWAP.

2. Entry Triggers: Al Brooks H1/H2 and L1/L2

H1/H2 (Long Entry): Opens below 2nd lower deviation, closes above it.

L1/L2 (Short Entry): Opens above 2nd upper deviation, closes below it.

3. Volatility Filter (ATR)

Skips trades when deviation bands are too tight (< 3 ATRs).

4. Stop Loss

Based on the signal bar’s high/low ± stop buffer.

Longs: signalBarLow - stopBuffer

Shorts: signalBarHigh + stopBuffer

5. Take Profit / Exit Target

Exit logic is customizable per side:

VWAP, Deviation Band, or None

6. Safety Exit

Exits early if X consecutive bars go against the trade.

Longs: X red bars

Shorts: X green bars

Explanation of Strategy Inputs

- Stop Buffer: Distance from signal bar for stop-loss.

- Long/Short Exit Rule: VWAP, Deviation Band, or None

- Long/Short Target Deviation: Standard deviation for target exit.

- Enable Safety Exit: Toggle emergency exit.

- Opposing Bars: Number of opposing candles before safety exit.

- Allow Long/Short Trades: Enable or disable entry side.

- Show VWAP/Entry Bands: Toggle visual aids.

- Highlight Low Vol Zones: Orange shading for low volatility skips.

Tuning Tips

- Stop buffer: Use 1–5 points.

- Target deviation: Start with VWAP. In strong trends use 2nd deviation and turn off the counter-trend entry.

- Safety exit: 3 bars recommended.

- Disable short/long side to focus on one type of reversal.

Backtest Setup Suggestions

- initial_capital = 2000

- default_qty_value = 1 (fixed contracts or percent-of-equity)

VWAP + Fibo Dev Extensions StrategyBased on my VWAP + Fibo deviations indicator, I tested some strategies to see if the indicator can be profitable; and I got it !

This strategy uses:

H1 timeframe

Weekly VWAP

+1.618 / +2.618 / -1.618 / -2.618 Deviations Extensions to create 2 bands

The value of the deviation

First, the 2 bands are plotted : +1.618/+2.618 painted in red and -1.618/-2.618 painted in lime.

Then, we wait for the deviation value to reach at least 150 (see thumbnail) to avoid littles moves when the gaps between bands are too short.

Entry long position :

first candle must crossunder the -1.618 level and low have to stay over the -2.618

low of the second one must stay in the lime band

enter the third one if the deviation value is over limit (150)

Exit long position :

TP : when a high crossover VWAP

SL : when a low crossunder -2.618

Entry short position :

first candle must crossover the +1.618 level and high have to stay under the +2.618

high of the second one must stay in the red band

enter the third one if the deviation value is over limit (150)

Exit short position :

TP : when a low crossunder VWAP

SL : when a high crossover +2.618

Notes :

this strategy uses pyramiding (5), be careful and calculate your risk management

the comission value is set to 0.08% to include slippages when entering a trade because of market orders

This strategy is not an advice to invest, make your own decisions.

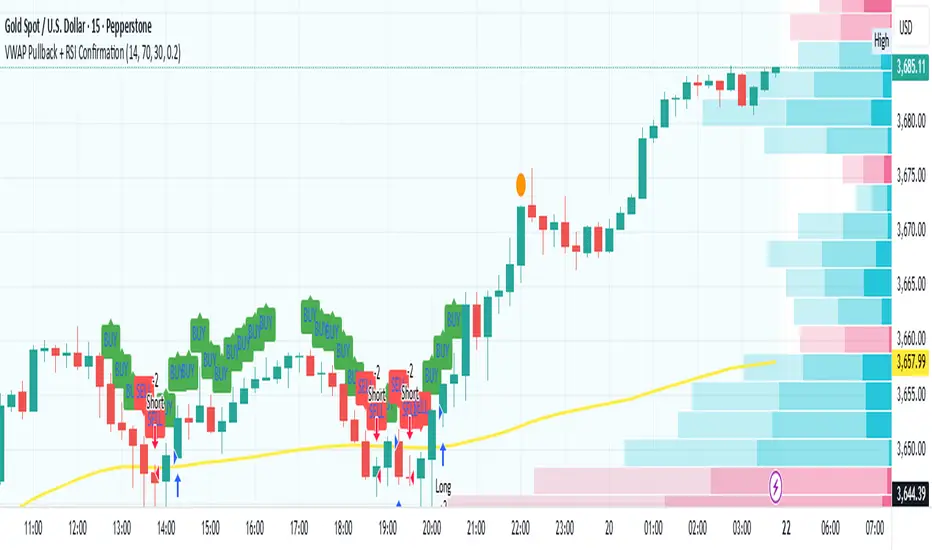

VWAP Pullback + RSI ConfirmationThis strategy focuses on trend continuation entries. Instead of betting on reversions, it looks for opportunities when price pulls back to VWAP but the dominant trend remains intact.

Trend Bias:

Price above VWAP = bullish environment → look for BUY pullbacks.

Price below VWAP = bearish environment → look for SELL pullbacks.

Entry Logic:

BUY: Price pulls back near VWAP, RSI stays above oversold (momentum intact).

SELL: Price pulls back near VWAP, RSI stays below overbought (momentum intact).

Exit Rule:

Stop-loss just below/above VWAP.

Take-profit at 1.5–2x risk (default script uses ~2%).

Best Timeframes:

15m–1H → good for intraday trend-following setups.

Daily → captures stronger, longer trends.

⚡ This strategy is powerful in trending markets because VWAP acts as a "magnet" for pullbacks, while RSI prevents overbought/oversold traps.

VWAP Push StrategyThis strategy is unfortunately not finished yet.

A pretty simple strategy. If price broke through VWAP and had three consecutive candles following the breakthroughs trend, the high of the third candle will be drawn. If this happened after a crossover of the vwap and price breaks through the high of the third candle, strategy will go long. Short will be the same after crossing under the vwap. A long or short will be closed after crossing the vwap in the opposite direction, so the vwap is kind of a trailing stop.

Unfortunately, I could not manage to stop the script from entering multiple times into one drawn high or low. Of course, if a high was crossed the script should wait for a new formed high before entering a new long. If someone would find a solution to this, it would be great, because I think it is a nice strategy .

Should work great scalping 5min charts (when scripting, I used the SPX for reference).

VWAP H/L Break - NQVWAP crossover with fib targets

bar closing over VWAP(high) go long

bar closing under VWAP (low) go short

fib targets based on closing candle and previous candle.

VWAP+15EMA with RSIVWAP+EMA+RSI Strategy for the group MelléCasH

This strategy will enter a long position when the closing price is above both the VWAP and the 15 EMA, and the RSI is above the specified overbought level. It will exit the position when the price falls by the specified stop loss percentage, rises by the specified take profit percentage, or when the trailing stop loss (which trails the highest price achieved after the position was entered by the specified percentage) is hit. The VWAP, EMA, and RSI indicators are also plotted on the chart for reference.

VWAPStrategyCross ema3 with VWAP. Just to give imression of how a day migth be divided in a long- and short bias zone. Not suited as trading signal.

VWAP Trendfollow Strategy [wbburgin]This is an experimental strategy that enters long when the instrument crosses over the upper standard deviation band of a VWAP and enters short when the instrument crosses below the bottom standard deviation band of the VWAP. I have added a trend filter as well, which stops entries that are opposite to the current trend of the VWAP. The trend filter will reduce total false breakouts, thus improving the % profitable while maintaining the overall returns of the strategy. Because this is a trend-following breakout strategy, the % profitable will typically be low but the average % return will be higher. As a rule, be sure to look at the average winning trade % compared to the average losing trade %, and compare that to the % profitable to judge the effectiveness of a strategy. Factor in fees and slippage as well.

This strategy appears to work better with the lower timeframes, and I was impressed with its results. It also appears to work on a wide range of asset classes. There isn't a stop loss or take profit built-in (other than the reversal signals, which close the current trade), so I would encourage you to expand on the strategy based on your own trading parameters.

You can toggle off the bar colors and the trend filter if you so desire.

Future updates to this script (or ideas of improving on it) might include a take profit level set at one standard deviation past the current level and a stop loss level set at one standard deviation closer to the vwap from the current level - or applying a multiple to the two based off of your reward/risk ratio.

About the strategy results below: this is with commissions of 0.5 % per trade.

SwingTrade VWAP Strategy[TiamatCrypto]V1.1This Pine Script® code creates a trading strategy called "SwingTrade VWAP Strategy V1.1." This strategy incorporates various trading tools, such as VWAP (Volume Weighted Average Price), ADX (Average Directional Index), and volume signals. Below is an explanation of the components and logic within the script:

### Overview of Features

- **VWAP:** A volume-weighted moving average that assesses price trends relative to the VWAP level.

- **ADX:** A trend strength indicator that helps confirm the strength of bullish or bearish trends.

- **Volume Analysis:** Leverages volume data to gauge momentum and identify volume-weighted buy/sell conditions.

- **Dynamic Entry/Exit Signals:** Combines the above indicators to produce actionable buy/sell or exit signals.

- **Customizable Inputs:** Inputs for tuning parameters like VWAP period, ADX thresholds, and volume sensitivity.

---

### **Code Breakdown**

#### **Input Parameters**

The script begins by defining several user-configurable variables under groups. These include indicators' on/off switches (`showVWAP`, `enableADX`, `enableVolume`) and input parameters for VWAP, ADX thresholds, and volume sensitivity:

- **VWAP Period and Threshold:** Controls sensitivity for VWAP signal generation.

- **ADX Settings:** Allows users to configure the ADX period and strength threshold.

- **Volume Ratio:** Detects bullish/bearish conditions based on relative volume patterns.

---

#### **VWAP Calculation**

The script calculates VWAP using the formula:

\

Where `P` is the typical price (`(high + low + close)/3`) and `V` is the volume.

- It resets cumulative values (`sumPV` and `sumV`) at the start of each day.

- Delta percentage (`deltaPercent`) is calculated as the percentage difference between the close price and the VWAP.

---

#### **Indicators and Signals**

1. **VWAP Trend Signals:**

- Identifies bullish/bearish conditions based on price movement (`aboveVWAP`, `belowVWAP`) and whether the price is crossing the VWAP level (`crossingUp`, `crossingDown`).

- Also detects rising/falling delta changes based on the VWAP threshold.

2. **ADX Calculation:**

- Calculates the directional movement (`PlusDM`, `MinusDM`) and smoothed values for `PlusDI`, `MinusDI`, and `ADX`.

- Confirms strong bullish/bearish trends when ADX crosses the defined threshold.

3. **Volume-Based Signals:**

- Evaluates the ratio of bullish volume (when `close > VWAP`) to bearish volume (when `close < VWAP`) over a specified lookback period.

---

#### **Trade Signals**

The buy and sell signals are determined by combining conditions from the VWAP, ADX, and volume signals:

- **Buy Signal:** Triggered when price upward crossover VWAP, delta rises above the threshold, ADX indicates a strong bullish trend, and volume confirms bullish momentum.

- **Sell Signal:** Triggered under inverse conditions.

- Additionally, exit conditions (`exitLong` and `exitShort`) are based on VWAP crossovers combined with the reversal of delta values.

---

#### **Plotting and Display**

The strategy plots VWAP on the chart and adds signal markers for:

- **Buy/Long Entry:** Green triangle below bars.

- **Sell/Short Entry:** Red triangle above bars.

- **Exit Signals:** Lime or orange "X" shapes for exits from long/short positions.

- Additionally, optional text labels are displayed to indicate the type of signal.

---

#### **Trading Logic**

The script's trading logic executes as follows:

- **Entries:**

- Executes long trades when the `buySignal` condition is true.

- Executes short trades when the `sellSignal` condition is true.

- **Exits:**

- Closes long positions upon `exitLong` conditions.

- Closes short positions upon `exitShort` conditions.

- The strategy calculates profits and visualizes the trade entry, exit, and running profit within the chart.

---

#### **Alerts**

Alerts are set up to notify traders via custom signals for buy and sell trades.

---

### **Use Case**

This script is suitable for day traders, swing traders, or algorithmic traders who rely on confluence signals from VWAP, ADX, and volume momentum. Its modular structure (e.g., the ability to enable/disable specific indicators) makes it highly customizable for various trading styles and financial instruments.

#### **Customizability**

- Adjust VWAP, ADX, and volume sensitivity levels to fit unique market conditions or asset classes.

- Turn off specific criteria to focus only on VWAP or ADX signals if desired.

#### **Caution**

As with all trading strategies, this script should be used for backtesting and analysis before live implementation. It's essential to validate its performance on historical data while considering factors like slippage and transaction costs.

VWAP Breakout Strategy (Momentum, Vol, VWAP, RSI, TrSL)General Description and Unique Features of this Script

Introducing the VWAP Breakout Trading Algorithm for TradingView – the timeless strategy designed to identify the highest probability entries and trades for all financial securities and timeframes.

Unlike other strategies, the VWAP Breakout Strategy considers the buying/selling pressure in the market and supply/demand balance to generate real-time trading signals. The Relative Strength Index (RSI) is used as a technical measure to capture typical breakouts from consolidation periods and pullback entries.

With flexible backtesting options, traders can improve parameter settings depending on their time horizon and the type of financial securities being used. Plus, this pro-version of the VWAP Breakout Strategy offers stop-loss, take-profit, and trailing stop-loss exit strategies for better risk management.

The VWAP Breakout Strategy combines a number of technical indicators, the Moving Average (MA), the Volume Weighted Average Price (VWAP) and the RSI-qualifier to identify potential trend reversals and entry/exit points in the market. The VWAP Breakout Strategy can be used in conjunction with other technical indicators and fundamental analysis to make more informed trading decisions.

To further optimize trading results, this strategy generates trading signals based on real-time price action, rather than relying on the close / open of candles.

The VWAP Breakout Strategy

One important qualifier for generating buy signals is that the stock or other financial security is not in a short-term overbought status (for long-positions), or in a short-term oversold status (for short-positions), respectively.

Additionally, the stock or other financial security needs to go through a consolidation period before buy signals are being generated.

The RSI-indicator is being used as a technical measure in this strategy for that.

• Using moderate parameters for the RSI-qualifier (oversold-level 40 or higher, overbought level 60 or lower) will capture more typical breakouts from consolidation periods.

• Using more extreme parameters for the RSI-qualifier (oversold-level 35 or lower, overbought level 65 or higher) will capture the so-called pullback entries.

Long Entries

When the selling pressure is over and the continuation of the uptrend can be confirmed by the MA / VWAP crossover after reaching a price low, a buy signal is issued by this strategy.

Short Entries

When the byuing pressure is over and the continuation of the downtrend can be confirmed by the MA / VWAP crossover after reaching a price high, a sell signal is issued by this strategy.

Timeless Strategy

The underlying principles of this strategy are based on the buying- / selling pressure in the market as well as the supply and demand balance. The buying / selling volumes are being considered for the generation of trading signals. These sophisticated market principles make this strategy timeless which means it can be applied to 1min-charts, weekly charts as well as anything between those.

Generation of Trading Signals

Real-time process are considered for this pro-version of the VWAP Breakout Strategy. This is another benefit versus many other strategies which only consider the close or open of the canldes for trading signals:

Exit Strategies

This pro-version offers the following exit strategies:

• Stop-Loss

• Take-Profit

• Trailing Stop-Loss

The trailing SL functionality provides another benefit versus most other trading strategies resulting in significantly backtesting- and real-time trading results.

Trades will also be closed when an opposite trading signal is being generated (only applicable for combined long/short strategies).

Flexible Backtesting Option

The strategy offers fully flexible backtesting options to improve the parameter setting strategy, depending on time horizon and type of financial securities being used.

Relative Strength Index (RSI)

The Relative Strength Index (RSI) is a technical indicator developed by Welles Wilder in 1978. The RSI is used to perform a market value analysis and identify the strength of a trend as well as overbought and oversold conditions. The indicator is calculated on a scale from 0 to 100 and shows how much an asset has risen or fallen relative to its own price in recent periods.

The RSI is calculated as the ratio of average profits to average losses over a certain period of time. A high value of the RSI indicates an overbought situation, while a low value indicates an oversold situation. Typically, a value > 70 is considered an overbought threshold and a value < 30 is considered an oversold threshold. A value above 70 signals that a single value may be overvalued and a decrease in price is likely , while a value below 30 signals that a single value may be undervalued and an increase in price is likely.

For example, let's say you're watching a stock XYZ. After a prolonged falling movement, the RSI value of this stock has fallen to 26. This means that the stock is oversold and that it is time for a potential recovery. Therefore, a trader might decide to buy this stock in the hope that it will rise again soon.

The MA / VWAP Crossover Trading Strategy

This strategy combines two popular technical indicators: the Moving Average (MA) and the Volume Weighted Average Price (VWAP). The MA VWAP crossover strategy is used to identify potential trend reversals and entry/exit points in the market.

The VWAP is calculated by taking the average price of an asset for a given period, weighted by the volume traded at each price level. The MA, on the other hand, is calculated by taking the average price of an asset over a specified number of periods. When the MA crosses above the VWAP, it suggests that buying pressure is increasing, and it may be a good time to enter a long position. When the MA crosses below the VWAP, it suggests that selling pressure is increasing, and it may be a good time to exit a long position or enter a short position.

Traders typically use the MA VWAP crossover strategy in conjunction with other technical indicators and fundamental analysis to make more informed trading decisions. As with any trading strategy, it is important to carefully consider the risks and potential rewards before making any trades.

This strategy is applicable to all timeframes and the relevant parameters for the underlying indicators (RSI and MA/VWAP) can be adjusted and optimized as needed.

Backtesting Results

Backtesting gives outstanding results on all timeframes and drawdowns can be reduced to a minimum level. In this example, the hourly chart for MCFT has been used.

Settings for backtesting are:

- Period from April 2020 until April 2021 (1 yr)

- Starting capital 100k USD

- Position size = 25% of equity

- 0.01% commission = USD 2.50.- per Trade

- Slippage = 2 ticks

Other comments

• This strategy has been designed to identify the most promising, highest probability entries and trades for each stock or other financial security.

• The RSI qualifier is highly selective and filters out the most promising swing-trading entries. As a result, you will normally only find a low number of trades for each stock or other financial security per year in case you apply this strategy for the daily charts. Shorter timeframes will result in a higher number of trades / year.

• As a result, traders need to apply this strategy for a full watchlist rather than just one financial security.

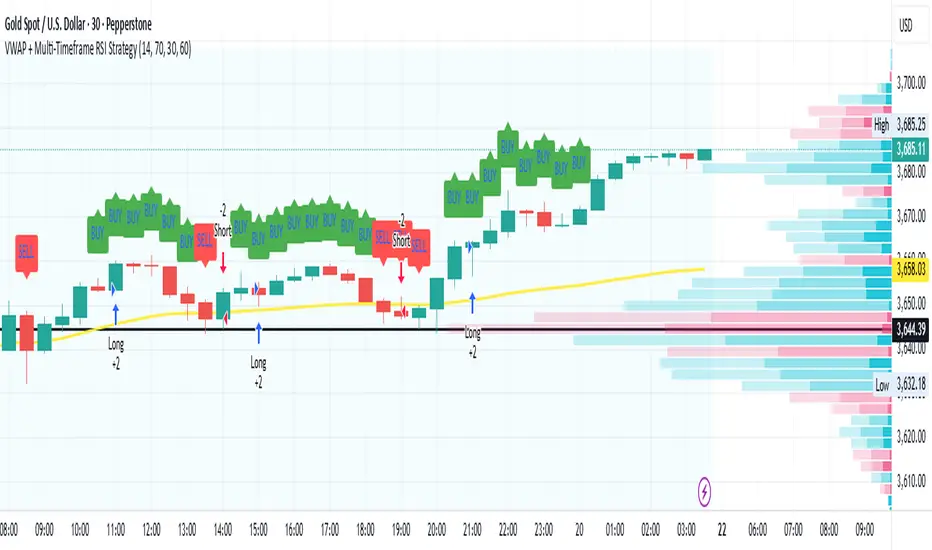

VWAP + Multi-Timeframe RSI StrategyThis strategy combines VWAP trend direction with confirmation from RSI on a higher timeframe. The idea is to only take trades when both intraday momentum and higher-timeframe trend are aligned, increasing accuracy.

LONG Entry:

Price above VWAP (bullish environment).

RSI on the current timeframe is below overbought (room to rise).

RSI on the higher timeframe (default H1) is above 50 (bullish confirmation).

SHORT Entry:

Price below VWAP (bearish environment).

RSI on the current timeframe is above oversold (room to fall).

RSI on the higher timeframe is below 50 (bearish confirmation).

Exit Rule:

Stop-loss near VWAP.

Take-profit at ~2x risk or when major levels are reached.

Best Timeframes:

Use 15m or 30m chart with H1 RSI for intraday trading.

Use 1H chart with Daily RSI for swing trading.

⚡ The higher-timeframe RSI filter reduces false signals and aligns trades with institutional flow.

Dynamic Swing Anchored VWAP STRAT (Zeiierman/PineIndicators)Dynamic Swing Anchored VWAP STRATEGY — Zeiierman × PineIndicators (Pine Script v6)

A pivot-to-pivot Anchored VWAP strategy that adapts to volatility, enters long on bullish structure, and closes on bearish structure. Built for TradingView in Pine Script v6.

Full credits to zeiierman.

Repainting notice: The original indicator logic is repainting. Swing labels (HH/HL/LH/LL) are finalized after enough bars have printed, so labels do not occur in real time. It is not possible to execute at historical label points. Treat results as educational and validate with Bar Replay and paper trading before considering any discretionary use.

Concept

The script identifies swing highs/lows over a user-defined lookback ( Swing Period ). When structure flips (most recent swing low is newer than the most recent swing high, or vice versa), a new regime begins.

At each confirmed pivot, a fresh Anchored VWAP segment is started and updated bar-by-bar using an EWMA-style decay on price×volume and volume.

Responsiveness is controlled by Adaptive Price Tracking (APT) . Optionally, APT auto-adjusts with an ATR ratio so that high volatility accelerates responsiveness and low volatility smooths it.

Longs are opened/held in bullish regimes and closed when the regime turns bearish. No short positions are taken by design.

How it works (under the hood)

Swing detection: Uses ta.highestbars / ta.lowestbars over prd to update swing highs (ph) and lows (pl), plus their bar indices (phL, plL).

Regime logic: If phL > plL → bullish regime; else → bearish regime. A change in this condition triggers a re-anchor of the VWAP at the newest pivot.

Adaptive VWAP math: APT is converted to an exponential decay factor ( alphaFromAPT ), then applied to running sums of price×volume and volume, producing the current VWAP estimate.

Rendering: Each pivot-anchored VWAP segment is drawn as a polyline and color-coded by regime. Optional structure labels (HH/HL/LH/LL) annotate the swing character.

Orders: On bullish flips, strategy.entry("L") opens/maintains a long; on bearish flips, strategy.close("L") exits.

Inputs & controls

Swing Period (prd) — Higher values identify larger, slower swings; lower values catch more frequent pivots but add noise.

Adaptive Price Tracking (APT) — Governs the VWAP’s “half-life.” Smaller APT → faster/closer to price; larger APT → smoother/stabler.

Adapt APT by ATR ratio — When enabled, APT scales with volatility so the VWAP speeds up in turbulent markets and slows down in quiet markets.

Volatility Bias — Tunes the strength of APT’s response to volatility (above 1 = stronger effect; below 1 = milder).

Style settings — Colors for swing labels and VWAP segments, plus line width for visibility.

Trade logic summary

Entry: Long when the swing structure turns bullish (latest swing low is more recent than the last swing high).

Exit: Close the long when structure turns bearish.

Position size: qty = strategy.equity / close × 5 (dynamic sizing; scales with account equity and instrument price). Consider reducing the multiplier for a more conservative profile.

Recommended workflow

Apply to instruments with reliable volume (equities, futures, crypto; FX tick volume can work but varies by broker).

Start on your preferred timeframe. Intraday often benefits from smaller APT (more reactive); higher timeframes may prefer larger APT (smoother).

Begin with defaults ( prd=50, APT=20 ); then toggle “Adapt by ATR” and vary Volatility Bias to observe how segments tighten/loosen.

Use Bar Replay to watch how pivots confirm and how the strategy re-anchors VWAP at those confirmations.

Layer your own risk rules (stops/targets, max position cap, session filters) before any discretionary use.

Practical tips

Context filter: Consider combining with a higher-timeframe bias (e.g., daily trend) and using this strategy as an entry timing layer.

First pivot preference: Some traders prefer only the first bullish pivot after a bearish regime (and vice versa) to reduce whipsaw in choppy ranges.

Deviations: You can add VWAP deviation bands to pre-plan partial exits or re-entries on mean-reversion pulls.

Sessions: Session-based filters (RTH vs. ETH) can materially change behavior on futures and equities.

Extending the script (ideas)

Add stops/targets (e.g., ATR stop below last swing low; partial profits at k×VWAP deviation).

Introduce mirrored short logic for two-sided testing.

Include alert conditions for regime flips or for price-VWAP interactions.

Incorporate HTF confirmation (e.g., only long when daily VWAP slope ≥ 0).

Throttle entries (e.g., once per regime flip) to avoid over-trading in ranges.

Known limitations

Repainting: Swing labels and pivot confirmations depend on future bars; historical labels can look “perfect.” Treat them as annotations, not executable signals.

Execution realism: Strategy includes commission and slippage fields, yet actual fills differ by venue/liquidity.

No guarantees: Past behavior does not imply future results. This publication is for research/education only and not financial advice.

Defaults (backtest environment)

Initial capital: 10,000

Commission value: 0.01

Slippage: 1

Overlay: true

Max bars back: 5000; Max labels/polylines set for deep swing histories

Quick checklist

Add to chart and verify that the instrument has volume.

Use defaults, then tune APT and Volatility Bias with/without ATR adaptation.

Observe how each pivot re-anchors VWAP and how regime flips drive entries/exits.

Paper trade across several symbols/timeframes before any discretionary decisions.

Attribution & license

Original indicator concept and logic: Zeiierman — please credit the author.

Strategy wrapper and publication: PineIndicators .

License: CC BY-NC-SA 4.0 (Attribution-NonCommercial-ShareAlike). Respect the license when forking or publishing derivatives.

JS-TechTrading: VWAP Momentum_Pullback StrategyGeneral Description and Unique Features of this Script

Introducing the VWAP Momentum-Pullback Strategy (long-only) that offers several unique features:

1. Our script/strategy utilizes Mark Minervini's Trend-Template as a qualifier for identifying stocks and other financial securities in confirmed uptrends.

NOTE: In this basic version of the script, the Trend-Template has to be used as a separate indicator on TradingView (Public Trend-Template indicators are available on TradingView – community scripts). It is recommended to only execute buy signals in case the stock or financial security is in a stage 2 uptrend, which means that the criteria of the trend-template are fulfilled.

2. Our strategy is based on the supply/demand balance in the market, making it timeless and effective across all timeframes. Whether you are day trading using 1- or 5-min charts or swing-trading using daily charts, this strategy can be applied and works very well.

3. We have also integrated technical indicators such as the RSI and the MA / VWAP crossover into this strategy to identify low-risk pullback entries in the context of confirmed uptrends. By doing so, the risk profile of this strategy and drawdowns are being reduced to an absolute minimum.

Minervini’s Trend-Template and the ‘Stage-Analysis’ of the Markets

This strategy is a so-called 'long-only' strategy. This means that we only take long positions, short positions are not considered.

The best market environment for such strategies are periods of stable upward trends in the so-called stage 2 - uptrend.

In stable upward trends, we increase our market exposure and risk.

In sideways markets and downward trends or bear markets, we reduce our exposure very quickly or go 100% to cash and wait for the markets to recover and improve. This allows us to avoid major losses and drawdowns.

This simple rule gives us a significant advantage over most undisciplined traders and amateurs!

'The Trend is your Friend'. This is a very old but true quote.

What's behind it???

• 98% of stocks made their biggest gains in a Phase 2 upward trend.

• If a stock is in a stable uptrend, this is evidence that larger institutions are buying the stock sustainably.

• By focusing on stocks that are in a stable uptrend, the chances of profit are significantly increased.

• In a stable uptrend, investors know exactly what to expect from further price developments. This makes it possible to locate low-risk entry points.

The goal is not to buy at the lowest price – the goal is to buy at the right price!

Each stock goes through the same maturity cycle – it starts at stage 1 and ends at stage 4

Stage 1 – Neglect Phase – Consolidation

Stage 2 – Progressive Phase – Accumulation

Stage 3 – Topping Phase – Distribution

Stage 4 – Downtrend – Capitulation

This strategy focuses on identifying stocks in confirmed stage 2 uptrends. This in itself gives us an advantage over long-term investors and less professional traders.

By focusing on stocks in a stage 2 uptrend, we avoid losses in downtrends (stage 4) or less profitable consolidation phases (stages 1 and 3). We are fully invested and put our money to work for us, and we are fully invested when stocks are in their stage 2 uptrends.

But how can we use technical chart analysis to find stocks that are in a stable stage 2 uptrend?

Mark Minervini has developed the so-called 'trend template' for this purpose. This is an essential part of our JS-TechTrading pullback strategy. For our watchlists, only those individual values that meet the tough requirements of Minervini's trend template are eligible.

The Trend Template

• 200d MA increasing over a period of at least 1 month, better 4-5 months or longer

• 150d MA above 200d MA

• 50d MA above 150d MA and 200d MA

• Course above 50d MA, 150d MA and 200d MA

• Ideally, the 50d MA is increasing over at least 1 month

• Price at least 25% above the 52w low

• Price within 25% of 52w high

• High relative strength according to IBD.

NOTE: In this basic version of the script, the Trend-Template has to be used as a separate indicator on TradingView (Public Trend-Template indicators are available in TradingView – community scripts). It is recommended to only execute buy signals in case the stock or financial security is in a stage 2 uptrend, which means that the criteria of the trend-template are fulfilled.

This strategy can be applied to all timeframes from 5 min to daily.

The VWAP Momentum-Pullback Strateg y

For the JS-TechTrading VWAP Momentum-Pullback Strategy, only stocks and other financial instruments that meet the selected criteria of Mark Minervini's trend template are recommended for algorithmic trading with this startegy.

A further prerequisite for generating a buy signals is that the individual value is in a short-term oversold state (RSI).

When the selling pressure is over and the continuation of the uptrend can be confirmed by the MA / VWAP crossover after reaching a price low, a buy signal is issued by this strategy.

Stop-loss limits and profit targets can be set variably.

Relative Strength Index (RSI)

The Relative Strength Index (RSI) is a technical indicator developed by Welles Wilder in 1978. The RSI is used to perform a market value analysis and identify the strength of a trend as well as overbought and oversold conditions. The indicator is calculated on a scale from 0 to 100 and shows how much an asset has risen or fallen relative to its own price in recent periods.

The RSI is calculated as the ratio of average profits to average losses over a certain period of time. A high value of the RSI indicates an overbought situation, while a low value indicates an oversold situation. Typically, a value > 70 is considered an overbought threshold and a value < 30 is considered an oversold threshold. A value above 70 signals that a single value may be overvalued and a decrease in price is likely , while a value below 30 signals that a single value may be undervalued and an increase in price is likely.

For example, let's say you're watching a stock XYZ. After a prolonged falling movement, the RSI value of this stock has fallen to 26. This means that the stock is oversold and that it is time for a potential recovery. Therefore, a trader might decide to buy this stock in the hope that it will rise again soon.

The MA / VWAP Crossover Trading Strategy

This strategy combines two popular technical indicators: the Moving Average (MA) and the Volume Weighted Average Price (VWAP). The MA VWAP crossover strategy is used to identify potential trend reversals and entry/exit points in the market.

The VWAP is calculated by taking the average price of an asset for a given period, weighted by the volume traded at each price level. The MA, on the other hand, is calculated by taking the average price of an asset over a specified number of periods. When the MA crosses above the VWAP, it suggests that buying pressure is increasing, and it may be a good time to enter a long position. When the MA crosses below the VWAP, it suggests that selling pressure is increasing, and it may be a good time to exit a long position or enter a short position.

Traders typically use the MA VWAP crossover strategy in conjunction with other technical indicators and fundamental analysis to make more informed trading decisions. As with any trading strategy, it is important to carefully consider the risks and potential rewards before making any trades.

This strategy is applicable to all timeframes and the relevant parameters for the underlying indicators (RSI and MA/VWAP) can be adjusted and optimized as needed.

Backtesting

Backtesting gives outstanding results on all timeframes and drawdowns can be reduced to a minimum level. In this example, the hourly chart for MCFT has been used.

Settings for backtesting are:

- Period from April 2020 until April 2021 (1 yr)

- Starting capital 100k USD

- Position size = 25% of equity

- 0.01% commission = USD 2.50.- per Trade

- Slippage = 2 ticks

Other comments

• This strategy has been designed to identify the most promising, highest probability entries and trades for each stock or other financial security.

• The RSI qualifier is highly selective and filters out the most promising swing-trading entries. As a result, you will normally only find a low number of trades for each stock or other financial security per year in case you apply this strategy for the daily charts. Shorter timeframes will result in a higher number of trades / year.

• As a result, traders need to apply this strategy for a full watchlist rather than just one financial security.

Miyagi (VWAP) + DCA BacktestVWAP has been the main condition for entry for our trading community when using the Wick Hunter bot for quite some time now; however using VWAP alone can lead to poor entries and bags.

Miyagi adds filtering conditions which can then be used to improve entries as opposed to simply using VWAP alone.

Miyagi: The attempt at mastering something for the best results.

Miyagi indicators combine multiple trigger conditions and place them in one toolbox for traders to easily use, produce alerts, backtest, reduce risk and increase profitability.

Miyagi (VWAP) + DCA Backtest allows you to backtest your VWAP settings across each pair.

VWAP + Backtest starts with the user selectable take profit and stoploss, both in percent.

Backtesting can be done in any trend direction: Long, Short, or both.

First we start with the VWAP Settings for entry.

The VWAP Settings are based off the original VWAP Indicator found here:

VWAP Timeframe can be adjusted to chart timeframe, or to another timeframe of choice.

VWAP Period is adjustable and should be set to your current period setting.

VWAP Lower Line (Long) is the Percentage Below VWAP = Long Entry.

VWAP Upper Line (Short) is the Percentage Above VWAP = Short Entry.

Once your VWAP Settings are now configured for your current trading settings, you can move onto the DCA and Backtest Settings.

Select DCA to allow and backtest DCA.

Equity %: allows you to select what percent of Equity you will use.

Leverage: Set the leverage you will trade at, from 1-100X.

DCA Start %: This is the percent that your DCA Starts at, in % away from initial entry.

Entry Order Size %: This is the entry order size, in percent of your account, that is used for entry.

DCA Order Size %: This is the DCA order size, in percent of your account, that is used for the first DCA.

DCA Order Size Scale %: This is the DCA size scaling, in %, that is applied to all DCA's after the first.

DCA % from Avg: This is the % away from Average DCA setting.

Step Size Scale %: This is the step size scale setting in percent, that is placed away from your first DCA.

DCA Buy Count: How many DCAs in total that can be used.

Properties Tab includes generic backtest settings including capital amount, base currency, order size, commission, slippage and margin.

Happy Trading!

[VJ] Viper VWAP IntradayHello Traders, this is a simple intraday strategy involving the ever reliable VWAP and a chop index to add twist to the traditional style . You can modify the values on the stock and see what are your best picks. Comment below if you found something with good returns

Strategy: VWAP based strategy but uses an additional powerful indicator Chop index to help us stay out of false trades.

Indicators used :

VWAP identifies the true average price of a stock by factoring the volume of transactions at a specific price point and not based on the closing price. VWAP can add more value than your standard 10, 50, or 200 moving average indicators because VWAP reacts to price movements based on the volume during a given period.

The Choppiness Index is designed to determine whether the market is choppy or trading sideways, or not choppy and trading within a trend in either direction. Using a scale from 1 - 100, the market is considered to be choppy as values near 100 (over 61.80) and trending when values are lower than 38.20)

Buying/Selling typically happens at VWAP Breakouts which is then validated with extreme CI to ascertain the entries

Aggressive trade stop can be employed by using the % for long and shorts in the strategy.

Usage & Best setting :

Choose a good volatile stock and a time frame - 10m.

CI Index : 14

Trend Factor - anything below 38.2 is considered in trend, you can experiment from 50

There is stop loss and take profit that can be used to optimise your trade

The template also includes daily square off based on your time.

Swing VWAP Weekly Stock and Crypto StrategyThis is a simple yet very efficient swing strategy designed for crypto and stock market, using big timeframes.

Its main component is VWAP weekly, so for best scenarios its better to use big timeframes such as 8h+.

The rules for entry are simple:

If our close if above vwap weekly we enter long .

If our close is below vwap weekly we enter short.

We exit from the trade, when a reverse condition than the entry one is triggered.

Because this strategy has no risk management inside, I recommend to be careful with it.

If you have any questions, let me know

Vwap mtf Swing Stock StrategyThis is a trending strategy designed for stock market, especially long trending assets such as TSLA, NIO, AMAZON and so on.

Its made of volatility bands and weekly VWAP, in this case daily and weekly.

This strategy has been adapted to go long only.

Rules for entry

For long , we want to enter close of a candle is above vwap weekly, and at the same time the close of a candle cross-under the lower volatility band.

For exit , we want to enter close of a candle is below vwap weekly, and at the same time the close of a candle cross-over the upper volatility band.

This strategy does not have a risk management inside, so use it with caution.

If you have any questions, let me know !

ARR VWAP IntradayIntra day VWAP Strategy

Strategy is

Buy when vwap goes up and RSI above 50 (Can be modified) .

Sell wehn vwap goes down and rsi bellow 50 (Can be modified)

Exit all at market close hour specified

VWAP and RSI strategyThis strategy combines VWAP and RSI indicators

BUY RULE

1. EMA50 > EMA 200

2. if current close > vwap session value and close>open

3. check if RSI3 is dipped below 10 for any of last 10 candles (as defined rsi_buy_level)

EXIT RULE

1. RSI3 crossing down 90 level (as defined in rsi_sell_level)

STOP LOSS EXIT

1. default is set to 5%

you need to add EMA 50 , EMA 200 and VWAP (session) indicators to the chart to see how these signals are generated

This strategy is tested on SPY and QQQ index stocks on hourly chart.

Warning

for educational purposes only

VWAP and BB strategy [EEMANI]This strategy combines VWAP and BB indicators

BUY RULE

1. EMA50 > EMA 200

2. if current close > vwap session value

3. check if price dipped BB lower band for any of last 10 candles

EXIT RULE

1. price closes above BB upper band

STOP LOSS EXIT

1. As configured --- default is set to 5%

warning: for the use of educational purposes only

VWAP_X_EMAVWAP and EMA 50 combo indicators

Long : if the close is above the VWAP and EMA

Short : Viceversa

[astropark] Rolling VWAP V2 [strategy]Dear Followers,

today I'm glad to present you yet another awesome Analysis Tool and Strategy, that you may like to use in your trading journey: Rolling VWAP V2 !

This is an upgraded version of my "Progressive VWAP" analysis tool (progressive and rolling are synonymous for me), its description describes quite well what a progressive/rolling vwap is and why they are important to watch:

This indicator can print automatically for you many important Rolling VWAPs:

Daily (D)

2 days (2D)

3 days (3D)

4 days (5D)

Weekly (W)

2 weeks (2W)

Monthly (M)

Quarterly (Q)

Yearly (Y)

As an indicator it will let you:

enable/disable each rolling vwap, change its color and line style and thickness

enable/disable labels and/or price on labels, as well as change their size

As a strategy it will let you:

enable/disable buy/sell signals

choose which strategy to use (all based on rolling vwaps of course)

choose a starting date & time from which to start backtesting

enable/disable individually long and short setups in the backtesting

You should choose low timeframe rolling vwap strategy if you are on a low timeframe, while higher timeframe rolling vwaps are good on medium-high timeframes.

For example D-2D-3D rolling vwap strategies are good at 1h or below, the others on higher timeframes. Backtesting results will help you in understanting this point quite easily.

This indicator works on every timeframe, market and pair. By the way it must be said that, as a bot strategy it has been tested and designed mostly for Bitcoin trading and it works best on 1h or above.

As I always say, all tools are great if you use them correctly: this is not the "Holy Grail", so always use proper money and risk management strategies.

This is a premium indicator , so send me a private message in order to get access to this script.