VWAP 10:00–15:00 (MSK, daily reset)Calculates the volume-weighted average price (VWAP) from 10:00 to 15:00 MSK.

The data is used to determine the funding rate of MOEX perpetual futures by comparing the average price of the perpetual contract with the official Central Bank exchange rate on the following day.

Cerca negli script per "vwap"

VWAP Suite█ OVERVIEW

This indicator is an attempt to bring all VWAP functionalities under one umbrella suite, the existing VWAPs are great and this was made to provide all functionalities. (pending more updates as well)

█ FEATURES

Multiple VWAPs MTF

Individual Band configuration

Previous vwap closes

Date tracking of previous closes

MTF Options

Enabling the other VWAPS with any timeframe will allow the user to use the "VWAP Anchor" setting to choose what HTF Vwap to be displayed

"Prev Close"

This setting enables all historical closes to be displayed with extension

"Track Dates"

Can be used to keep date information of 2 previous closes and further back

█ HOW TO USE IT

The indicator is quite straight forward in its application, as you would expect of a normal VWAP.

At the top of the settings pane the indicator has some functionality that would control the VWAPs globally, e.g. disabling show bands disables all bands for all the VWAPs.

Each VWAP has individual settings that can be controlled such as coloring, which bands enabled, previous closes, labelling...

█ SUGGESTION

My suggestion for clarity is to use 1 VWAP with bands, and a 2nd with no bands + Previous close enabled at a higher timeframe

█ LIMITATIONS OF PINE (Please read)

I see many users going on different indicators with MTF in mind and trying to use it for LTF data e.g. 1hour chart, and selecting 5min in chart settings.

This is not recommended by the team themselves and should be noted for use always use HTF: www.tradingview.com

To understand how to use VWAP please refer to some education that can be found for free online

Heres an example of a trader using the tool himself: www.youtube.com

█ Future Updates:

Previous Close Line extensions

Previous Highs and Lows of VWAP mapped out for users

Suggestions Welcome!

VWAP Bands [TradingFinder] 26 Brokers Data (Forex + Crypto)🔵 Introduction

Indicators are tools that help analysts predict the price trend of a stock through mathematical calculations on price or trading volume. It is evident that trading volume significantly impacts the price trend of a stock symbol.

The Volume-Weighted Average Price (VWAP) indicator combines the influence of trading volume and price, providing technical analysts with a practical tool.

This technical indicator determines the volume-weighted average price of a symbol over a specified time period. Consequently, this indicator can be used to identify trends and entry or exit points.

🟣 Calculating the VWAP Indicator

Adding the VWAP indicator to a chart will automatically perform all calculations for you. However, if you wish to understand how this indicator is calculated, the following explains the steps involved.

Consider a 5-minute chart. In the first candle of this chart (which represents price information in the first 5 minutes), sum the high, low, and close prices, and divide by 3. Multiply the resulting number by the volume for the period and call it a variable (e.g., X).

Then, divide the resulting output by the total volume for that period to calculate your VWAP. To maintain the VWAP sequence throughout the trading day, it is necessary to add the X values obtained from each period to the previous period and divide by the total volume up to that time. It is worth noting that the calculation method is the same for intervals shorter than a day.

The mathematical formula for this VWAP indicator : VWAP = ∑ (Pi×Vi) / ∑ Vi

🔵 How to Use

Traders might consider the VWAP indicator as a tool for predicting trends. For example, they might buy a stock when the price is above the VWAP level and sell it when the price is below the VWAP.

In other words, when the price is above the VWAP, the price is rising, and when it is below the VWAP, the price is falling. Major traders and investment funds also use the VWAP ratio to help enter or exit stocks with the least possible market impact.

It is important to note that one should not rely solely on the VWAP indicator when analyzing symbols. This is because if prices rise quickly, the VWAP indicator may not adequately describe the conditions. This indicator is generally used for daily or shorter time frames because using longer intervals can distort the average.

Since this indicator uses past data in its calculations, it can be considered a lagging indicator. As a result, the more data there is, the greater the delay.

🟣 Difference Between VWAP and Simple Moving Average

On a chart, the VWAP and the simple moving average may look similar, but these two indicators have different calculations. The VWAP calculates the total price considering volume, while the simple moving average does not consider volume.

In simpler terms, the VWAP indicator measures each day's price change relative to the trading volume that occurred that day. In contrast, the simple moving average implicitly assumes that all trading days have the same volume.

🟣 Reasons Why Traders Like the VWAP Indicator

The VWAP Considers Volume: Since VWAP takes volume into account, it can be more reliable than a simple arithmetic average of prices. Theoretically, one person can buy 200,000 shares of a symbol in one transaction at a single price.

However, during the same time frame, 100 other people might place 200 different orders at various prices that do not total 100,000 shares. In this case, if you only consider the average price, you might be mistaken because trading volume is ignored.

The Indicator Can Help Day Traders: While reviewing your trades, you might notice that the shares you bought at market price are trading below the VWAP indicator.

In this case, there's no need to worry because with the help of VWAP, you always get a price below the average. By knowing the volume-weighted average price of a stock, you can easily make an informed decision about paying more or less than other traders for the stock.

VWAP Can Signal Market Trend Changes: Buying low and selling high can be an excellent strategy for individuals. However, you are looking to buy when prices start to rise and sell your shares when prices start to fall.

Since the VWAP indicator simulates a balanced price in the market, when the price crosses above the VWAP line, one can assume that traders are willing to pay more to acquire shares, and as a result, the market will grow. Conversely, when the price crosses below the line, this can be considered a sign of a downward movement.

🔵 Setting

Period : Indicator calculation time frame.

Source : The Price used for calculations.

Market Ultra Data : If you turn on this feature, 26 large brokers will be included in the calculation of the trading volume.

The advantage of this capability is to have more reliable volume data. You should be careful to specify the market you are in, FOREX brokers and Crypto brokers are different.

Multiplier : Coefficient of band lines.

VWAP with RSIVWAP with RSI Indicator

Overview

The VWAP with RSI Indicator is a powerful tool that combines the Volume Weighted Average Price (VWAP) with the Relative Strength Index (RSI) to provide traders with comprehensive insights into price trends, volume-weighted price levels, and market momentum. This dual-indicator setup enhances your trading strategy by offering a clearer understanding of the market conditions, potential entry and exit points, and trend reversals.

Key Features

VWAP (Volume Weighted Average Price):

Calculation: The VWAP is calculated using the high, low, and close prices, weighted by trading volume over a specified period.

Purpose: VWAP provides an average price that reflects the trading volume at different price levels, helping traders identify the true average price over a given period.

Visualization: The VWAP line is plotted in blue on the price chart, indicating the volume-weighted average price.

RSI (Relative Strength Index):

Calculation: RSI is based on the average gains and losses over a specified period (default is 14 periods) and ranges from 0 to 100.

Purpose: RSI measures the speed and change of price movements, identifying overbought or oversold conditions in the market.

Overbought/Oversold Levels:

Overbought: RSI above 70 (red line).

Oversold: RSI below 30 (green line).

Midline: RSI at 50 (gray dashed line).

Visualization: The RSI line changes color based on its value (purple for normal, red for overbought, green for oversold) and is plotted below the price chart.

Background Fill for RSI:

Overbought Area: Shaded red when RSI is above 70.

Oversold Area: Shaded green when RSI is below 30.

Bullish and Bearish Divergence Detection:

Bullish Divergence: Occurs when price forms a lower low, but RSI forms a higher low, indicating potential upward reversal.

Visualization: Bullish divergence points are marked with a green line and labeled "Bull."

Bearish Divergence: Occurs when price forms a higher high, but RSI forms a lower high, indicating potential downward reversal.

Visualization: Bearish divergence points are marked with a red line and labeled "Bear."

Alerts: Conditions for bullish and bearish divergences trigger alerts.

Settings

VWAP Settings:

hideonDWM: Option to hide VWAP on daily or higher timeframes.

src: Source for VWAP calculation (default is hlc3 - (high + low + close)/3).

offset: Offset for plotting the VWAP.

RSI Settings:

rsiLengthInput: Period length for RSI calculation (default is 14).

rsiSourceInput: Source for RSI calculation (default is close price).

maTypeInput: Type of moving average applied to RSI (options: SMA, EMA).

maLengthInput: Length of the moving average applied to RSI.

How to Use

Trend Identification: Use VWAP to identify the average price level and market trend. If the price is above VWAP, it suggests an uptrend, and if below, it suggests a downtrend.

Overbought/Oversold Conditions: Use RSI to identify potential reversal points. RSI above 70 indicates overbought conditions, and below 30 indicates oversold conditions.

Divergence: Look for bullish or bearish divergences between price and RSI to anticipate potential trend reversals.

Conclusion

By combining VWAP and RSI, this indicator provides a robust framework for analyzing market conditions, identifying trends, and making more informed trading decisions. Enhance your trading strategy today with the VWAP with RSI Indicator!

VWAP Composites📊 VWAP Composite - Advanced Multi-Period Volume Weighted Average Price Indicator

═══════════════════════════════════════════════════════════════════

🎯 OVERVIEW

VWAP Composite is an advanced volume-weighted average price (VWAP) indicator that goes beyond traditional single-period VWAP calculations by offering composite multi-period analysis and unprecedented customization. This indicator solves a common problem traders face: traditional VWAP resets at arbitrary intervals (session start, day, week), but significant price action and volume accumulation often spans multiple periods. VWAP Composite allows you to anchor VWAP calculations to any timeframe—or combine multiple periods into a single composite VWAP—giving you a true representation of average price weighted by volume across the exact periods that matter to your analysis.

═══════════════════════════════════════════════════════════════════

⚙️ HOW IT WORKS - CALCULATION METHODOLOGY

📌 CORE VWAP CALCULATION

The indicator calculates VWAP using the standard volume-weighted formula:

• Typical Price = (High + Low + Close) / 3

• VWAP = Σ(Typical Price × Volume) / Σ(Volume)

This calculation is performed across user-defined time periods, ensuring each bar's contribution to the average is proportional to its trading volume.

📌 STANDARD DEVIATION BANDS

The indicator calculates volume-weighted standard deviation to measure price dispersion around the VWAP:

• Variance = Σ / Σ(Volume)

• Standard Deviation = √Variance

• Upper Band = VWAP + (StdDev × Multiplier)

• Lower Band = VWAP - (StdDev × Multiplier)

These bands help identify overbought/oversold conditions relative to the volume-weighted mean, with high-volume price excursions having greater impact on band width than low-volume moves.

📌 COMPOSITE PERIOD METHODOLOGY (Auto Mode)

Unlike traditional VWAP that resets at fixed intervals, Auto Mode creates composite VWAPs by combining the current period with N previous periods:

• Period Span = 1: Current period only (standard VWAP behavior)

• Period Span = 2: Current period + 1 previous period combined

• Period Span = 3: Current period + 2 previous periods combined

• And so on...

Example: A 3-period Weekly composite VWAP calculates from the start of 2 weeks ago through the current week's end, creating a single VWAP that represents 21 days of continuous price and volume data. This provides context about where price stands relative to the volume-weighted average over multiple weeks, not just the current week.

═══════════════════════════════════════════════════════════════════

🔧 KEY FEATURES & ORIGINALITY

✅ DUAL OPERATING MODES

1️⃣ MANUAL MODE (5 Independent VWAPs)

Define up to 5 separate VWAP calculations with custom start/end times:

• Perfect for anchoring VWAP to specific events (earnings, Fed announcements, major reversals)

• Each VWAP has independent color settings for lines and deviation band backgrounds

• Individual control over calculation extension and visual extension (explained below)

• Useful for tracking multiple institutional accumulation/distribution zones simultaneously

2️⃣ AUTO MODE (Composite Period VWAP)

Automatically calculates VWAP across combined time periods:

• Supported periods: Daily, Weekly, Monthly, Quarterly, Yearly

• Configurable period span (1-20 periods)

• Always up-to-date, recalculates on each new bar

• Ideal for systematic analysis across consistent timeframes

✅ DUAL EXTENSION SYSTEM (Manual Mode Innovation)

Most VWAP indicators only offer "on/off" for extending calculations. This indicator provides two distinct extension options:

🔹 EXTEND CALCULATION TO CURRENT BAR

When enabled, continues including new bars in the VWAP calculation after the defined end time. The VWAP value updates dynamically as new volume enters the market.

Use case: You anchored VWAP to a major low 3 weeks ago. You want the VWAP to continue evolving with new volume data to track ongoing institutional positioning.

🔹 EXTEND VISUAL LINE ONLY

When enabled (and calculation extension is disabled), projects the "frozen" VWAP value forward as a reference line. The VWAP value remains fixed at what it was at the end time, but the line and deviation bands visually extend to current price.

Use case: You want to see how price is behaving relative to the VWAP that existed at a specific point in time (e.g., "Where is price now vs. the 5-day VWAP that existed at last Friday's close?").

This dual system gives you unprecedented control over whether you're tracking a "living" VWAP that incorporates new data or using historical VWAP levels as static reference points.

✅ CUSTOMIZABLE STANDARD DEVIATION BANDS

• Adjustable multiplier (0.1 to 5.0)

• Independent background colors with opacity control for each VWAP

• Dashed band lines for easy visual distinction from main VWAP

• Bands extend when visual extension is enabled, maintaining zone visibility

✅ COMPREHENSIVE LABELING SYSTEM

Each VWAP displays:

• Current VWAP value

• Upper deviation band value (High)

• Lower deviation band value (Low)

• Extension status indicator (Calc Extended / Visual Extended)

• Color-coded for quick identification

═══════════════════════════════════════════════════════════════════

📖 HOW TO USE THIS INDICATOR

🎯 SCENARIO 1: EVENT-ANCHORED VWAP (Manual Mode)

Use case: A stock gaps down 15% on earnings and you want to track where institutions are positioning during the recovery.

Setup:

1. Switch to Manual Mode

2. Enable VWAP 1

3. Set Start Time to the earnings gap bar

4. Set End Time to current time (or leave far in future)

5. Enable "Extend Calculation to Current Bar"

6. Watch how price respects the VWAP as a dynamic support/resistance

Interpretation:

• Price above VWAP = buyers in control since the event

• Price testing VWAP from above = potential support

• Volume-weighted standard deviation bands show normal price range

• Price outside bands = potential exhaustion/mean reversion setup

🎯 SCENARIO 2: MULTI-WEEK INSTITUTIONAL ACCUMULATION ZONE (Auto Mode)

Use case: You trade swing setups and want to identify where institutions have been accumulating over the past 3 weeks.

Setup:

1. Switch to Auto Mode

2. Select "Weekly" period type

3. Set Period Span to 3

4. Enable standard deviation bands

Interpretation:

• 3-week composite VWAP shows the true average institutional entry

• Price bouncing off VWAP repeatedly = strong support (institutions defending their average)

• Price breaking below VWAP on high volume = potential distribution

• Deviation bands contracting = consolidation; expanding = volatility increase

🎯 SCENARIO 3: COMPARING MULTIPLE TIME HORIZONS (Manual Mode)

Use case: You want to see short-term vs medium-term vs long-term VWAP alignments.

Setup:

1. Switch to Manual Mode

2. VWAP 1: Last 5 trading days (blue)

3. VWAP 2: Last 10 trading days (orange)

4. VWAP 3: Last 20 trading days (purple)

5. Enable "Extend Calculation" for all

6. Set different background colors for visual separation

Interpretation:

• All VWAPs aligned upward = strong trend across all timeframes

• Price between VWAPs = finding equilibrium between different trader timeframes

• Short-term VWAP crossing long-term VWAP = momentum shift

• Price rejecting at higher-timeframe VWAP = that timeframe's traders defending their average

🎯 SCENARIO 4: HISTORICAL VWAP REFERENCE LEVELS (Manual Mode)

Use case: You want to see where the 1-month VWAP was at each month-end as static reference levels.

Setup:

1. Switch to Manual Mode

2. VWAP 1: Set to last month's start/end dates

3. VWAP 2: Set to 2 months ago start/end dates

4. VWAP 3: Set to 3 months ago start/end dates

5. Disable "Extend Calculation"

6. Enable "Extend Visual Line Only"

Interpretation:

• Each VWAP represents the volume-weighted average for that complete month

• These become static support/resistance levels

• Price returning to old monthly VWAPs = institutional memory/gap fill behavior

• Useful for identifying longer-term value areas

═══════════════════════════════════════════════════════════════════

🎨 CUSTOMIZATION OPTIONS

GENERAL SETTINGS

• Show/hide labels

• Line style: Solid, Dashed, or Dotted

• Standard deviation multiplier (impacts band width)

• Toggle standard deviation bands on/off

MANUAL MODE (Per VWAP)

• Custom start and end times

• Line color picker

• Background color picker (with transparency control)

• Extend calculation option

• Extend visual option

• Show/hide individual VWAPs

AUTO MODE

• Period type selection (Daily/Weekly/Monthly/Quarterly/Yearly)

• Period span (1-20 periods)

• Line color

• Background color (with transparency control)

═══════════════════════════════════════════════════════════════════

💡 TRADING APPLICATIONS

✓ Mean Reversion: Use deviation bands to identify stretched prices likely to return to VWAP

✓ Trend Confirmation: Price sustained above VWAP = bullish bias; below = bearish bias

✓ Support/Resistance: VWAP often acts as dynamic S/R, especially on higher volume periods

✓ Institutional Positioning: Multi-day/week VWAPs show where large players have established positions

✓ Entry Timing: Wait for pullbacks to VWAP in trending markets

✓ Stop Placement: Use VWAP ± standard deviation as volatility-adjusted stop levels

✓ Breakout Confirmation: Breakouts from consolidation with price reclaiming VWAP = stronger signal

✓ Multi-Timeframe Analysis: Compare short vs long-period VWAPs to gauge momentum alignment

═══════════════════════════════════════════════════════════════════

⚠️ IMPORTANT NOTES

• The indicator redraws on each bar to maintain accurate visual representation (uses `barstate.islast`)

• Maximum lookback is limited to 5000 bars for performance optimization

• Time range calculations work across all timeframes but are most effective on intraday to daily charts

• Standard deviation bands assume volume-weighted distribution; extreme events may violate assumptions

• Auto mode always calculates to current bar; use Manual mode for fixed historical periods

═══════════════════════════════════════════════════════════════════

This indicator is open-source. Feel free to examine the code, learn from it, and adapt it to your needs.

VWAP Trend Strategy (Intraday) [KedarArc Quant]Description:

An intraday strategy that anchors to VWAP and only trades when a local EMA trend gate and a volume participation gate are both open. It offers two entry templates—Cross and Cross-and-Retest—with an optional Momentum Exception for impulsive moves. Exits combine a TrendBreak (structure flips) with an ATR emergency stop (risk cap).

Updates will be published under this script.

Why this merits a new script

This is not a simple “VWAP + EMA + ATR” overlay. The components are sequenced as gates and branches that *change the trade set* in ways a visual mashup cannot:

1. Trend Gate first (EMA fast vs. slow on the entry timeframe)

Counter-trend VWAP crosses are suppressed. Many VWAP scripts fire on every cross; here, no entry logic even evaluates unless the trend gate is open.

2. Participation Gate second (Volume SMA × multiplier)

This gate filters thin liquidity moves around VWAP. Without it, the same visuals would produce materially more false triggers.

3. Branching entries with structure awareness

* Cross: Immediate VWAP cross in the trend direction.

* Cross-and-Retest: Requires a revisit to VWAP vicinity within a lookback window (recent low near VWAP for longs; recent high for shorts). This explicitly removes first-touch fakeouts that a plain cross takes.

* Momentum Exception (optional): A quantified body% + volume condition can bypass the retest when flow is impulsive—intentional risk-timing, not “just another indicator.”

4. Dual exits that reference both anchor and structure

* TrendBreak: Close only when price loses VWAP and EMA alignment flips.

* ATR stop: Placed at entry to cap tail risk.

These exits complement the entry structure rather than being generic stop/target add-ons.

What it does

* Trades the session’s fair value anchor (VWAP), but only with local-trend agreement (EMA fast vs. slow) and sufficient participation (volume filter).

* Lets you pick Cross or Cross-and-Retest entries; optionally allow a fast Momentum Exception when candles expand with volume.

* Manages positions with a structure exit (TrendBreak) and an emergency ATR stop from entry.

How it works (concepts & calculations)

* VWAP (session anchor):

Standard VWAP of the active session; entries reference the cross and the retest proximity to VWAP.

* Trend gate:

Long context only if `EMA(fast) > EMA(slow)`; short only if `EMA(fast) < EMA(slow)`.

A *gate*, not a trigger—entries aren’t considered unless this is true.

* Participation (volume) gate:

Require `volume > SMA(volume, volLen) × volMult`.

Screens out low-participation wiggles around VWAP.

Entries:

* Cross: Price crosses VWAP in the trend direction while volume gate is open.

* Cross-and-Retest: After crossing, price revisits VWAP vicinity within `lookback` (recent *low near VWAP* for longs; recent *high near VWAP* for shorts).

* Momentum Exception (optional): If body% (|close−open| / range) and volume exceed thresholds, enter without waiting for the retest.

Exits:

* TrendBreak (structure):

* Longs close when `price < VWAP` and `EMA(fast) < EMA(slow)` (mirror for shorts).

* ATR stop (risk):

* From entry: `stop = entry ± ATR(atrLen) × atrMult`.

How to use it ?

1. Select market & timeframe: Intraday on liquid symbols (equities, futures, crypto).

2. Pick entry mode:

* Start with Cross-and-Retest for fewer, more selective signals.

* Enable Momentum Exception if strong moves leave without retesting.

3. Tune guards:

* Raise `volMult` to ignore thin periods; lower it for more activity.

* Adjust `lookback` if retests come late/early on your symbol.

4. Risk:

* `atrLen` and `atrMult` set the emergency stop distance.

5. Read results per session: Optional panel (if enabled) summarizes Net-R, Win%, and PF for today’s session to evaluate

behavior regime by regime.

⚠️ Disclaimer

This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

VWAP FadeVWAP fade indicator simple parameters for how it works and the logic behind VWAP fade

You can try other products but recommended for Copper/Silver futures due to how they tend to do the VWAP fade

Identify VWAP retest:

Price moves back into VWAP after trending away.

Fail condition:

Candle touches VWAP but fails to close across it (stays on trend side).

Signal:

Short if price came from below and fails to close above VWAP.

Long if price came from above and fails to close below VWAP.

Confirm with volume spike (optional filter).

VWAP HMA Trends

It visually syncs Trend, VWAP, and Confidence — giving you instant clarity to trade with calm precision.

⚙️ The Three Core Gauges:

1. 📈 Trend Green for up, Red for down (Trend: Confirms direction)

2. 💰 VWAP Price vs. Volume Weighted Average Price. Institutional Fair Value. (Bull or Bear)

3. 🎯 Confidence Agreement between trend & VWAP. Dont fight the trend.

Bonus Feature: Confidence Turns 🟢 Confident when aligned, 🟡 Cautious when mixed.

Together, these create a clean, visual readout of the market’s health.

🧩 How to Use

Watch the Color Flow:

🟢 Green Cloud → Buyers in control.

🔴 Red Cloud → Sellers in control.

Check VWAP (Orange Line):

Price above VWAP → bullish strength.

Price below VWAP → bearish control.

Hovering at VWAP → indecision. Wait.

---

Act With Discipline:

Trade only when all gauges agree.

Add size only in Confident conditions.

Trim or tighten stops when it shifts to Cautious.

⚡ Quick Reference:

🟢 Green cloud + above VWAP + Confident | Uptrend continuation | Favor long bias

🔴 Red cloud + below VWAP + Confident | Downtrend continuation | Favor short bias

Mixed colors or Cautious: Wait or scale back

Cloud flips color: Possible shift. Reassess bias next bar

⚖️ Disclaimer: Educational and informational use only. Not financial advice. Always use independent judgment and position sizing.

VWAP Daily/Weekly/Monthly - Automatic AnchoredExplanation:

This script plots Volume-Weighted Average Price (VWAP) lines that are automatically anchored to the beginning of key timeframes — daily, weekly, and monthly. VWAP is a widely used trading indicator that shows the average price of an asset weighted by trading volume, making it useful for identifying fair value and institutional trading levels.

The “automatic anchored” feature means that you don’t have to manually select starting points. Instead, the script automatically resets the VWAP at the start of each day, week, or month, depending on the chosen setting. This ensures the VWAP always reflects the true average price for that period, providing traders with a consistent reference for support, resistance, and trend direction across multiple timeframes.

Notice:

On the chart, you may notice visible “jumps” in the VWAP lines. These are intentional. Each jump marks the reset point at the start of a new day, week, or month, depending on the selected setting. This design keeps the VWAP history from the previous period intact, allowing you to clearly see how price interacted with VWAP in past sessions.

By keeping these historical resets, you can easily compare short-term (daily) VWAP behavior against longer-term levels like weekly and monthly VWAP. This provides valuable context, helping you spot when price respects or diverges from fair value across different timeframes.

In short:

Daily VWAP resets at the start of each trading day.

Weekly VWAP resets at the beginning of each trading week.

Monthly VWAP resets at the start of each month.

This makes it easy to analyze how price interacts with VWAP levels across different time horizons without manual adjustments.

Vwap SalvatierraVwap Salvatierra. an indicator that must be accompanied by other volume indicators.

Benefits:

- Long term Vwap.

- Middle Std. deviations, Calculated automatically.

- Previous zones available.

How to use:

when the price is >= stdev+3, look for shorts till came back to vwap

whe the price is <= stdev-3, look for longs till came back to vwap

if the vwap cannot be broken, as resistance, after several attempts, then sell

if the vwap can't be broken, like support, after several tries, then buy.

VWAP Price ChannelVWAP Price Channel cuts the crust off of a traditional price channel (Donchian Channel) by anchoring VWAPs at the highs and lows. By doing this, the flat levels, characteristic of traditional Donchian Channels, are no more!

Author's Note: This indicator is formed with no inherent use, and serves solely as a thought experiment.

> Concept

I would be hesitant to call this a "predictive" indicator, however the behavior of it would suggest it could be considered at least partially predictive

Essentially, the Anchored VWAPs creates something from otherwise nothing.

While the DC upper or lower values are staying flat, the VWAPs improvise based on price and volume to project a level that may be a better representation of where future highs or lows may settle.

Visually, this looks like we have cut off the corners of the Donchian Channel.

Note: Notice how we are calculating values before the corners are realized.

> Implementation

While this is only a concept indicator, The specific application I've gone with for this, is a sort of supertrend-ish display (A Trend Flipping Trailing Stop Loss).

The script uses basic logic to create a trend direction, and then displays the Anchored VWAPs as a form of trailing stop loss.

While "In Trend", the script fills in the area between the VWAP and Price in the direction of trend.

When new highs or lows are made while in trend, the opposite VWAP will start to generate at the new highs or lows. These happen on every new high or low, so they are not indicating the trend shift, but could be interpreted as breakout levels for the current trend direction in order for continuation.

Note: All values are drawn live, but when using higher timeframes, there is a natural calculation discrepancy when using live data vs. historical.

> Technicals

In this script, I'm simply detecting new highs or lows from the DC and using those as the anchor frequency on the built-in VWAP function.

So each time a new high or low is made based on DC, the VWAP function re-anchors to the high or low of the candle.

Past that, I have implemented some logic in order to account for a common occurrence I faced during development.

Frequently, the price would outpace the anchored VWAP, so we would end up with the VWAP being further from price than the actual DC upper or lower.

Due to this, what I have ended up with was a third value which, rather than switching between raw VWAP values and DC values, it adjusts the value based on the change in the VWAP value.

This can be simply thought of as a "Start + Change" type of setup.

By doing this, I can use the change values from the actual anchored VWAP, and under normal conditions, this will also be the true VWAP value.

However, situationally, I am able to update the start value which we're applying the VWAP change to.

In other words, when these situations happen, the VWAP change is added to the new (closer to price) DC value.

The specific trend logic being used is nothing fancy at all, we are simply checking if a new high or low is created and setting the trend in that direction.

This is in line with some traditional DC Strategies.

To those who made it here,

Just remember:

The chart may be ugly, but it's the fastest analysis of the data you can get.

Nicer displays often come at the hidden cost of latency.

You have to shoot your shot to make it.

Choose 2: Fast, Clean, Useful

Enjoy!

VWAP StrategyVWAP and volatility filters for structured intraday trades.

How the Strategy Works

1. VWAP Anchored to Session

VWAP is calculated from the start of each trading day.

Standard deviations are used to create bands above/below the VWAP.

2. Entry Triggers: Al Brooks H1/H2 and L1/L2

H1/H2 (Long Entry): Opens below 2nd lower deviation, closes above it.

L1/L2 (Short Entry): Opens above 2nd upper deviation, closes below it.

3. Volatility Filter (ATR)

Skips trades when deviation bands are too tight (< 3 ATRs).

4. Stop Loss

Based on the signal bar’s high/low ± stop buffer.

Longs: signalBarLow - stopBuffer

Shorts: signalBarHigh + stopBuffer

5. Take Profit / Exit Target

Exit logic is customizable per side:

VWAP, Deviation Band, or None

6. Safety Exit

Exits early if X consecutive bars go against the trade.

Longs: X red bars

Shorts: X green bars

Explanation of Strategy Inputs

- Stop Buffer: Distance from signal bar for stop-loss.

- Long/Short Exit Rule: VWAP, Deviation Band, or None

- Long/Short Target Deviation: Standard deviation for target exit.

- Enable Safety Exit: Toggle emergency exit.

- Opposing Bars: Number of opposing candles before safety exit.

- Allow Long/Short Trades: Enable or disable entry side.

- Show VWAP/Entry Bands: Toggle visual aids.

- Highlight Low Vol Zones: Orange shading for low volatility skips.

Tuning Tips

- Stop buffer: Use 1–5 points.

- Target deviation: Start with VWAP. In strong trends use 2nd deviation and turn off the counter-trend entry.

- Safety exit: 3 bars recommended.

- Disable short/long side to focus on one type of reversal.

Backtest Setup Suggestions

- initial_capital = 2000

- default_qty_value = 1 (fixed contracts or percent-of-equity)

VWAP Entry Assistant (v1.0)Description:

Anchored VWAP with a lightweight assistant for VWAP reversion trades.

It shows the distance to VWAP, an estimated hit probability for the current bar, the expected number of bars to reach VWAP, and a recommended entry price.

If the chance of touching VWAP is low, the script suggests an adjusted limit using a fraction of ATR.

The VWAP line is white by default, and a compact summary table appears at the bottom-left.

Educational tool. Not financial advice. Not affiliated with TradingView or any exchange. Always backtest before use.

VWAP Balance ZonesVWAP Balance Zones (VBZ) Is based on 3 concepts.

Many Traders use VWAP to help determine Price Trends.

Trends are typically identified by new Highs or new Lows.

Balanced is found when Supply and Demand are mostly Equal.

VBZ tracks the daily, weekly, and monthly highs and lows; Then plots the average (50%) between the VWAP and the respective extremes.

50% VWAP Zones can be considered significant since they attempt to identify the equilibrium between market participants within the current trend, serving as key reference points to consider for decision making. >While in an uptrend, Buyers may see price falling to the Hi 50% as an attractive value entry for the continuation upwards.

>While ALSO in an uptrend, Sellers may see price falling to the Hi 50% as a change in sentiment with more downwards movement on the way.

Because of these conflicting mindsets, these zones are thought to display areas of balance between buyers and sellers, which can serve as potential decision points throughout the day.

VBZ Draws Zones from the Daily (High/Low/Close) VWAPs and the Day's (High/Low/Close) extremes as seen below.

Technically speaking, an average between vwap and extreme is a single point, to make these into zones I am using multiple sources for vwap and tracking different points of the bar throughout the day (ex. Close VWAP & Daily Highest Close)

Weekly and Monthly are only displaying the Average Price between the VWAP and the (Weekly or Monthly) High/Low.

These hold up as important levels for speculation; however, since most action will be discovered at the daily zones, I am not displaying the zones for the Weekly and Monthly to keep noise to a minimum.

Unique Behaviors:

- Weekly values are hidden on the first day of the week since they are similar to the daily values on the first day of the week.

- Monthly values are hidden in the first week of the month for the same reason.

VWAP + Fibo Dev Extensions StrategyBased on my VWAP + Fibo deviations indicator, I tested some strategies to see if the indicator can be profitable; and I got it !

This strategy uses:

H1 timeframe

Weekly VWAP

+1.618 / +2.618 / -1.618 / -2.618 Deviations Extensions to create 2 bands

The value of the deviation

First, the 2 bands are plotted : +1.618/+2.618 painted in red and -1.618/-2.618 painted in lime.

Then, we wait for the deviation value to reach at least 150 (see thumbnail) to avoid littles moves when the gaps between bands are too short.

Entry long position :

first candle must crossunder the -1.618 level and low have to stay over the -2.618

low of the second one must stay in the lime band

enter the third one if the deviation value is over limit (150)

Exit long position :

TP : when a high crossover VWAP

SL : when a low crossunder -2.618

Entry short position :

first candle must crossover the +1.618 level and high have to stay under the +2.618

high of the second one must stay in the red band

enter the third one if the deviation value is over limit (150)

Exit short position :

TP : when a low crossunder VWAP

SL : when a high crossover +2.618

Notes :

this strategy uses pyramiding (5), be careful and calculate your risk management

the comission value is set to 0.08% to include slippages when entering a trade because of market orders

This strategy is not an advice to invest, make your own decisions.

VWAP + VWAP Distance Avg + Alert Lines (%)VWAP Distance & Average Distance Indicator – Detailed Description

The VWAP + VWAP Distance Avg + Alert Lines (%) indicator is designed to measure the distance of the current price from the VWAP (Volume Weighted Average Price), as well as the average distance over a specified period. This tool is particularly useful for traders who use the VWAP as a magnet for price, helping to identify potential trend changes and areas where price may revert toward the VWAP.

Key Features

Current Distance (%)

Calculates the absolute percentage difference between the current price and the VWAP

This line shows how far the price has moved away from the VWAP at any given moment.

Average Distance (%)

Calculates a simple moving average (SMA) of the distance over a specified lookback period.

This provides a reference for typical price deviations from the VWAP, helping traders assess whether the current distance is unusually high or low.

Alert Lines (%)

Allows up to three customizable horizontal alert lines, which can be turned on or off individually.

Each line can be configured with:

Value in percent.

Color.

Line thickness.

These lines serve as visual thresholds, helping traders detect extreme deviations from the VWAP that may precede trend reversals.

Use Case – Detecting Potential Trend Changes

Traders often treat the VWAP as a price magnet, where price tends to revert after significant deviations.

When the current distance exceeds typical average levels or crosses an alert line, it can signal that the price may revert toward the VWAP, potentially indicating a shift in trend or a high-probability mean-reversion scenario.

Disclaimer

This indicator is provided for educational and analytical purposes only. It does not constitute financial advice, and trading decisions are always the sole responsibility of the individual trader. Users should carefully evaluate market conditions and their own risk tolerance before taking any trade.

Better used with VWAP on chart , and be careful around the end of session, for now this works just for session...

still improving on this....

VWAP TrendSignalVWAP TrendSignal

VWAP (Volume-Weighted Average Price) is the market’s true fair value — the benchmark institutions use to see when price is balanced, extended, or trending with real intent.

Price often snaps back when it moves too far (mean reversion), and only shows genuine strength when it holds above or below VWAP.

VWAP TrendSignal makes this insight effortless by color-coding VWAP direction:

Yellow = VWAP rising → bullish pressure

Red = VWAP falling → bearish pressure

No bands. No noise. Just pure directional clarity.

Anchor VWAP to the Session, Week, Month, Quarter, or Year, and tailor the Slope Smoothing Filter to your timeframe:

1–2 smoothing → fast & reactive (1–5m scalping)

3–5 smoothing → clean & stable (5–15m intraday)

6–10 smoothing → slow flips (1H–4H swings)

10–15 smoothing → macro bias only (Daily/Weekly)

The line adapts to how you trade.

How to Use It

Mean Reversion

When price stretches far from VWAP, expect pullbacks or snapbacks.

Trend Direction

Yellow supports long bias, red supports short bias.

Simple, reliable, instantly visible.

Balance Zones

Price sitting near VWAP = compression, buildup, or chop.

A perfect signal to wait or prepare for a breakout.

Why It Works

VWAP TrendSignal distills institutional logic into a clean, single-line tool.

It shows fair value, trend slope, and balance all at once — making your chart clearer and your decisions faster.

Once you get used to reading it, trading without it feels blind.

VWAP Multi-Period with SD & Value ZonesVWAP Multi-Period with SD & Value Zones

A dynamic VWAP indicator that works on Weekly, Monthly, Quarterly (3M) and Yearly (12M) timeframes.

VWAP line: true volume-weighted average price

±1, ±2, ±3 SD bands: volume-weighted volatility levels

Value Zone: filled area between ±1 SD

Prior Value Zone: last period’s ±1 SD area extended into the new period

Usage: Add to chart, select your period (W/M/3M/12M), and use the bands and zones as volume-weighted support/resistance and risk boundaries.

Demander à ChatGPT

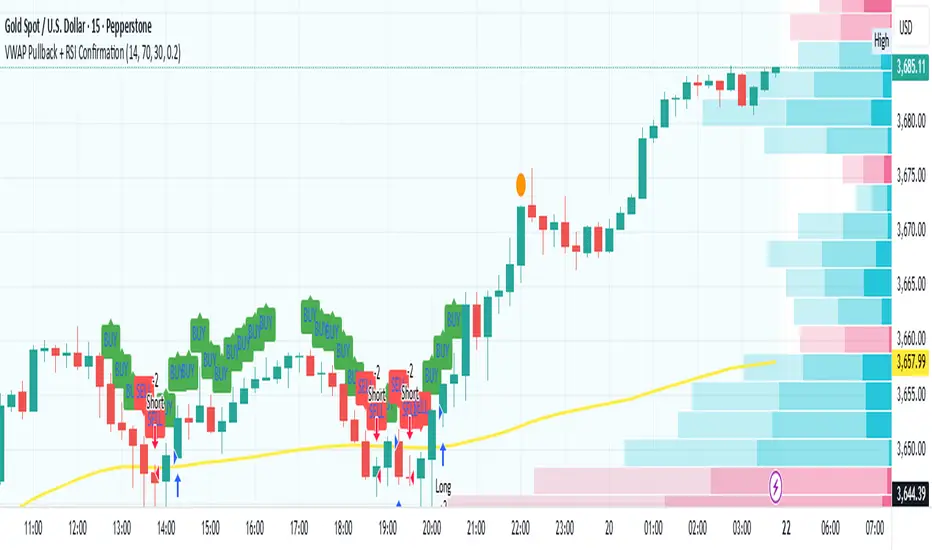

VWAP Pullback + RSI ConfirmationThis strategy focuses on trend continuation entries. Instead of betting on reversions, it looks for opportunities when price pulls back to VWAP but the dominant trend remains intact.

Trend Bias:

Price above VWAP = bullish environment → look for BUY pullbacks.

Price below VWAP = bearish environment → look for SELL pullbacks.

Entry Logic:

BUY: Price pulls back near VWAP, RSI stays above oversold (momentum intact).

SELL: Price pulls back near VWAP, RSI stays below overbought (momentum intact).

Exit Rule:

Stop-loss just below/above VWAP.

Take-profit at 1.5–2x risk (default script uses ~2%).

Best Timeframes:

15m–1H → good for intraday trend-following setups.

Daily → captures stronger, longer trends.

⚡ This strategy is powerful in trending markets because VWAP acts as a "magnet" for pullbacks, while RSI prevents overbought/oversold traps.