Vegas Wave - MSSimple Vegas Wave implementation, all 3 EMA's in one indicator for those of you with indicator limitations :D

Cerca negli script per "wave"

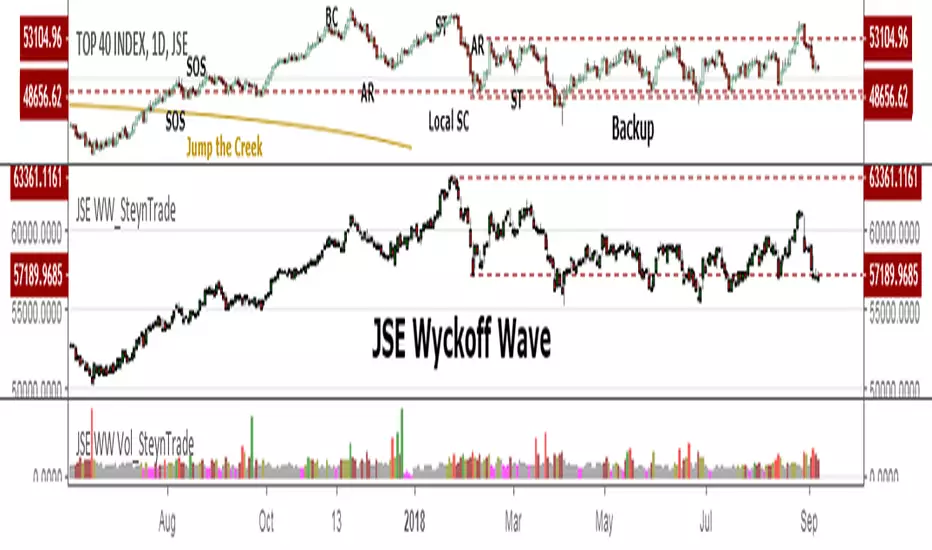

JSE Wyckoff WaveThe Stock Market Institute (SMI) describes an propriety indicator the "SMI Wyckoff Wave" for US Stocks. This code is an attempt to make a Wyckoff Wave for the Johannesburg Stock Exchange (JSE). Once the wave has been established the volume can also be calculated. Please see code for the JSE Wyckoff Wave Volume which goes with this indicator.

The Wave presents a normalized price for the 10 selected stocks (An Index for the 10 stocks). The theory is to select stocks that are widely held, market leaders, actively traded and participate in important market moves. This is only my attempt to select 10 stocks and a different selection can be made. I am not certain how SMI determine their weightings but what I have done it to equalize the Rand value of the stock so that moves are of equal magnitude. The then provides a view of the overall condition of the market and volume flow in the market.

I have used the September 2018 price to normalize the stock price for the 10 selected stocks based. The stocks and weightings can be changed periodically depending on the performance and leadership.

Most Indecies when constructed assume that all high prices and all low prices happen at the same time and therefor inflate the wicks of the bars. To make the wave more representatives for the SMI Wyckoff Wave the price is determined on the 5 minute timeframe which removes this bias. However, TradingView does not calculate properly when selecting a lower timeframe than in current period. A work around is to call the sma of the highs and add these which provides more realistic tails. Please, let me know if there is a better work around this.

The stocks and their weightings are:

"JSE:BTI"*0.79

"JSE:SHP"*2.87

"JSE:NPN"*0.18

"JSE:AGL"*1.96

"JSE:SOL"*1.0

"JSE:CFR"*4.42

"JSE:MND"*1.40

"JSE:MTN"*7.63

"JSE:SLM"*7.29

"JSE:FSR"*8.25

Weis Wave Volume-v1This is lazy bear Weis Wave Volume when we make it little different

the crossing is higlighted

3x EMA / VEGAS WAVEmade changes on the 3x EMA of AREAY to suit the TD's vegas wave since free trading view only allows limited indicators.

Elliot Wave Oscillator [River]Based on the usual Elliot Wave Oscillator but divided by price so it scales with history better, added the 4 colours and a signal line.

Sine Wave This is John F. Ehlers, Hilbert Sine Wave with barcolor and bgcolor.

When fast line red crosses down slow line blue that is a zone of resistance in the price chart, and when fast line crosses up slow line blue that is a zone of support.

When close of the bar is equal or greater than the zone of resistance there is a trend up mode in place and trending instruments like Hull moving average should be used, and when the close of the bar is equal or greater than the zone of resistance there is a trend down in place and trending instruments should be used too.

When none of the preceeding conditions are valid there is a cycle mode, and cycle instruments like oscillators, stochastics and the Sine Wave itself should be used. Note that the Sine Wave is almost always a leading indicator when in a cycle mode.

Barcolor and bgcolor mean: Green = Trend Up , Red = Trend Down, Yellow= Cycle mode

Hilbert Sine Wave Support and ResistanceSupport and Resistance plotted to match John Ehler's Hilbert Sine Wave

[RS]Swing Charts V0 Trend Counter V0EXPERIMENTAL:

wave counting using swing charts, use at your own discretion.

[RS]Neo Wave V0EXPERIMENTAL: Request for IvanLabrie.

Method for reading Neo Wave's.

note: some issues arent possible to work around/fix due to limitations in pinescript.

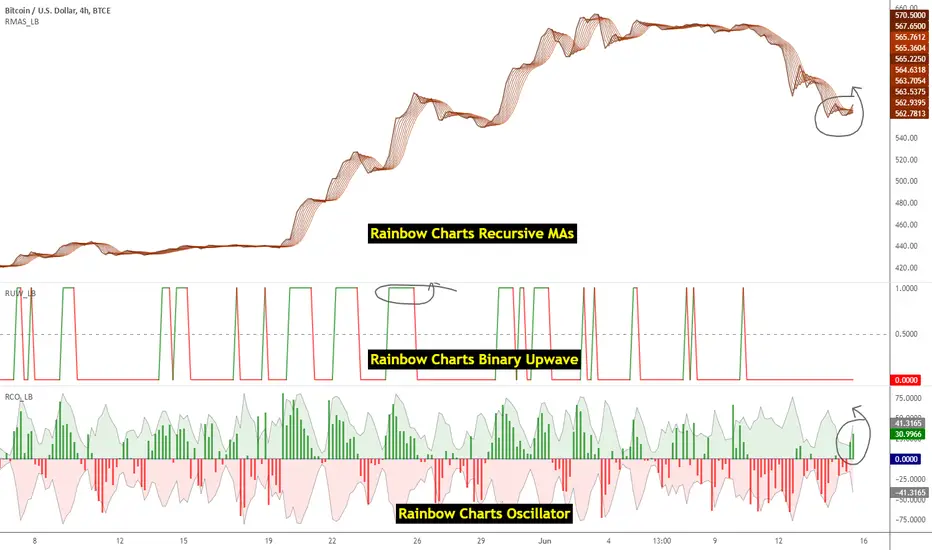

Indicators: Rainbow Charts Oscillator, Binary Wave and MAsRainbow Charts, by Mel Widner, is a trend detector. It uses recursively smoothed MAs (remember, this idea was proposed back in 1997 -- it was certainly cool back then!) and also builds an oscillator out of the MAs. Oscillator bands indicate the stability range.

I have also included a simple binary wave based on whether all the MAs are in an upward slope or not. If you see any value above 0.5 there, the trend is definitely up (all MAs pointing up).

More info:

www.traders.com

Here's my complete list of indicators (With these 3, the total count should be above 100 now...will update the list later today)

20 Day Moving Average with Profit TargetsThis Pine Script indicator plots a 20-day simple moving average (SMA) on the chart and displays profit target labels relative to an initial buy price.

The script allows the user to input a custom buy price and calculates profit levels at 10%, 20%, 30%, and 50% above the buy price. Labels are shown on the last bar of the chart for each profit level and the buy price, with the labels offset to the right to avoid overlapping with the price action.

The labels are color-coded based on the profit levels, and the buy price label is blue.

Volume with SD+2Volume with SD+2

Volume with SMA20 and Standard Deviation +2

If Volume < SMA20 , mean Volume Low and less momentum.

If Volume > SMA20 and < SD2 , mean Volume Increase and more momentum.

If Volume > SD2 , mean Volume Climax , show strong trend but show reversal point in someitmes.

PriceCounterPrice Counter

Use to identify Price Short Term Trend By

PC = Present Close - 4 Previous Close

PC > 0 Show Value in Green bar

PC 0

Dot = Present Close - 2 Previous High

If PC = 0 or < 0

Dot = Present Close - 2 Previous Low

Indicator will Show momentum of price. PC bar is long mean price move fast .

PC bars are the same color continuously , mean price in trend.

PC bars are often flip color and small bar , mean price sideway and weak momentum.

The Zone Trades v1.0The Zone v.1.0

The Zone is mention in New Trading Dimensions by Bill Williams,PhD. The Zone is used for Entry Signal of Both Long and Short side.

Green Zone are painting Green Bars when Awesome Oscillator (AO) and Accelerater/Decelerator (AC) are both increasing.

Red Zone are painting Red Bars when Awesome Oscillator (AO) and Accelerater/Decelerator (AC) are both decreasing.

Gray Zone are painting Gray Bars AO and AC in difference changing. Gray Zone are indicate the indecision between bulls and bears.

Bill Williams, PhD. mention that Green Zone or Red Zone usually happen 6-8 bars Continuously.

The First Bar that change to be Green or Red color is the Signal Bar.

Entry Signal is the second bar in the same color as the Signal bar happen with Volume

Price go higher the high of previous Green Bar is Buy Signal. Entry Buy (Long) and place Stop at 1 tick lower the Low of previous bar.

Price go ;ower the Low of previous Red Bars is Sell Signal. Entry Sell (Short) and place Stop at 1 tick higher the High of previous bar.

Do not Entry if Green Bars or Red Bars completed 5 bars continuously.

&BAMM&

This indicator shows a break of the peak and a pullback if the trend was upward and the path changed to downward, along with an indication of the targets, and the opposite in a downward trend.

mehja,atops and bottoms

This indicator shows a break of the peak and a pullback if the trend was upward and the path changed to downward, along with an indication of the targets, and the opposite in a downward trend.

Test shift level strategyTesting this on all timelines where in it checks the candle color and takes call to buy or sell

RSI with SMA + 70/60/50/40/30 LevelsIndicator Name:

RSI with SMA + 70/60/50/40/30 Levels

🧩 Concept Overview:

यह indicator दो popular tools को combine करता है:

RSI (Relative Strength Index) – momentum indicator जो market ke overbought aur oversold zones ko identify karta hai.

SMA (Simple Moving Average) – trend smoother jo RSI ke movement ko average karke lagging confirmation deta hai.

इन दोनों के साथ 70, 60, 50, 40, और 30 की multiple reference lines draw की जाती हैं, ताकि trader को RSI ke swings aur reversals easily samajh aaye.

⚙️ Indicator Components:

RSI Line:

Default Period: 14 (customize kar sakte ho).

Show karta hai price momentum – agar RSI 70 ke upar jaata hai to market overbought zone me hota hai; agar 30 ke niche jaata hai to oversold zone me.

SMA on RSI:

RSI ka smooth version (usually 9-period SMA).

Trend confirmation ke liye – jab RSI line SMA ke upar cross karti hai to bullish signal, aur neeche cross kare to bearish signal.

Horizontal Levels:

70: Overbought zone (potential sell area).

60: Strong bullish momentum line (trend confirmation).

50: Neutral / midline (trend direction flip area).

40: Weak bearish zone (trend losing strength).

30: Oversold zone (potential buy area).

💡 How to Use:

Trend Identification:

RSI > 60 aur SMA ke upar → Bullish trend.

RSI < 40 aur SMA ke neeche → Bearish trend.

Reversal Spotting:

RSI 70 ke upar jaake wapas niche aaye → Sell signal.

RSI 30 ke neeche jaake wapas upar aaye → Buy signal.

Confirmation Using SMA:

RSI cross SMA from below → Confirmed bullish reversal.

RSI cross SMA from above → Confirmed bearish reversal.

Custom Grid LinesThe Custom Grid Lines Indicator is a versatile tool designed for traders who want to manually define key price zones and visualize them with precision. This indicator allows users to select their own starting and ending price levels and automatically divides the range into user-defined grids using horizontal lines.

🔧 Key Features:

📍 User-Controlled Price Range:

Manually set the starting (bottom) and ending (top) price levels based on your trading plan, key zones, or market structure.

📊 Flexible Grid Setup:

Easily choose the number of grid lines to divide your selected range into equal price intervals.

📏 Automatic Grid Calculation:

The indicator calculates grid spacing and plots horizontal lines at each level, providing a clean and structured visual guide.

✅ Simple and Effective Visualization:

Ideal for grid trading, manual support/resistance plotting, or price zone tracking.

⚙️ How to Use:

Input the desired starting price (bottom of your range).

Input the ending price (top of your range).

Select the number of grids you want between these two levels.

The indicator will automatically draw all grid lines across your chart.

💡 Best For:

Grid Trading Strategies

Visualizing Custom Price Zones

Manual Support and Resistance Mapping

Session-Based Trading Ranges

Simple Pips GridOverview

This is a clean, simple, and highly practical indicator that draws horizontal grid lines at user-defined pip intervals.

Unlike other complex grid indicators, this script is designed to be lightweight and error-free. It eliminates automatic symbol detection and instead gives you full manual control, ensuring it works perfectly with any symbol you trade—FX, CFDs, Crypto, Stocks, Indices, and more.

Key Features

Universal Compatibility: Works with any trading pair by letting you manually define the pip value.

Fully Customizable: Easily set the pip interval for your grid (e.g., 10 pips, 50 pips, 100 pips).

Lightweight & Fast: Simple code ensures smooth performance without lagging your chart.

Visual Customization: Change the color, width, and style (solid, dashed, dotted) of the grid lines.

How to Use

It's incredibly simple to set up. You only need to configure two main settings:

Step 1: Set the "Pip Value"

This is the most important setting. You need to tell the indicator what "1 pip" means for the symbol you are currently viewing.

Go to the indicator settings and find the "Pip Value" input. Here are some common examples:

Symbol Pip Value (Input this number)

USD/JPY 0.01

EUR/USD 0.0001

GBP/USD 0.0001

XAU/USD (Gold) 0.1

JP225 (Nikkei 225) 10

US500 (S&P 500) 1

BTC/USD 0.1 or 1.0 (depending on your preference)

Step 2: Set the "Pip Interval"

Next, in the "Pip Interval" input, simply type how many pips you want between each line.

For a 10-pip grid, enter 10.

For a 50-pip grid, enter 50.

That's it! The grid will now be perfectly aligned to your specifications.

Additional Settings

Line Color, Width, Style: Customize the appearance of the lines to match your chart theme.

Number of Lines: Adjust how many lines are drawn above and below the current price to optimize performance and visibility.

This script was created with the assistance of Gemini (Google's AI) to be a simple and reliable tool for all traders. Feel free to use and modify it. Happy trading!

Anchored Moving AverageAn Anchored Moving Average (AMA) is a technical analysis tool that calculates the average price of an asset starting from a specific point in time. Every closing candle calculates the price.