Anchored Moving AverageAn Anchored Moving Average (AMA) is a technical analysis tool that calculates the average price of an asset starting from a specific point in time. Every closing candle calculates the price.

Cerca negli script per "wave"

Sweep + Cement Candle Coloring with EMA hopdcCertainly! Here's an introduction for the indicator:

---

## Introduction to the Sweep + Cement Candle Coloring with EMA Indicator

The **Sweep + Cement Candle Coloring with EMA Indicator** is a powerful tool designed to enhance your technical analysis and trading strategies. This indicator combines the unique characteristics of Sweep and Cement candle patterns with the dynamic capabilities of Exponential Moving Averages (EMAs), providing traders with insightful signals for potential market movements.

### Key Features:

1. **Candle Coloring**:

- **Sweep + Cement Bullish Candles**: Highlighted in teal when the low of the current candle is lower than the previous candle, and the close is above the previous high. This indicates potential bullish momentum.

- **Sweep + Cement Bearish Candles**: Marked in red when the high of the current candle is higher than the previous candle, and the close is below the previous low, signaling possible bearish pressure.

2. **Exponential Moving Averages (EMAs)**:

- **EMA 0 (Default Length: 9)**: Provides short-term trend direction.

- **EMA 1 (Default Length: 21)** and **EMA 2 (Default Length: 50)**: Offer insights into medium and long-term trends.

- Customizable settings allow traders to adjust EMA lengths and colors based on their preferences.

3. **Trading Signals**:

- **Buy Signal**: Triggered when a bullish Sweep + Cement candle forms, EMA 1 is above EMA 2, and the price closes above all EMAs.

- **Sell Signal**: Activated with a bearish Sweep + Cement candle, EMA 1 below EMA 2, and the price closes below all EMAs.

- Visual arrows on the chart indicate buy and sell opportunities.

4. **Alerts**:

- Configurable alerts notify traders when the price touches any of the EMAs, ensuring you never miss critical levels.

- Alerts for buy and sell signals keep you informed of potential entries and exits.

### How It Benefits Traders:

This indicator is ideal for traders looking to identify and capitalize on market reversals and trend continuations. By integrating candle patterns with EMA analysis, it provides a comprehensive view of market dynamics, making it easier to spot high-probability trading opportunities.

Whether you are a beginner or an experienced trader, the Sweep + Cement Candle Coloring with EMA Indicator can be a valuable addition to your trading toolkit, helping you make informed decisions with confidence.

---

Feel free to adjust the content to better fit your audience or specific use case!

High and Retracement Finder

This Pine Script indicator, titled "High and Retracement Finder," is designed to identify significant highs and lows on a price chart based on a user-defined starting point and retracement threshold. It begins analysis from a manually set bar index and tracks the highest high until the price retraces by a specified percentage (retracement threshold). Once this retracement occurs, it switches focus to finding the lowest low. If the price surpasses the previous high during this phase, the cycle resets, and the script resumes tracking a new highest high. The script visually marks these significant highs and lows with arrows on the chart, helping traders identify potential turning points or retracements in the market.

Boost Candle Indicator by JulianThe Boost Candle Trading Indicator is designed to identify significant price movements by calculating the average candle size for the same direction candles (green for bullish and red for bearish) over a specified number of periods. It then highlights candles that exceed a predefined multiple of this average size, indicating potential strong buying or selling pressure.

Key Features:

Directional Average Calculation: Calculates the average size of the previous candles in the same direction (green for buy signals and red for sell signals), ensuring the boost signal is contextually relevant.

Boost Multiplier: Allows customization of the multiplier to define what constitutes a boost candle, providing flexibility in detecting varying levels of price movement intensity.

Proximity to Moving Average: Integrates a proximity check to the moving average (MA), ensuring that boost candles are identified in context with the overall market trend.

Buy and Sell Signals:

Buy Signal: Triggered when a significant green boost candle appears below the moving average and closes above it, indicating a strong bullish movement.

Sell Signal: Triggered when a significant red boost candle appears above the moving average and closes below it, indicating a strong bearish movement.

Customizable Inputs:

Moving Average Length: Adjust the length of the moving average to suit different trading strategies.

Number of Periods for Average Candle Size: Define the lookback period for calculating the average candle size.

Boost Multiplier and Proximity Tolerance: Fine-tune the sensitivity of the indicator to suit different market conditions.

How to Use:

Buy Signals: Look for green labels ("B") below significant bullish candles, indicating a potential upward price movement.

Sell Signals: Look for red labels ("S") above significant bearish candles, indicating a potential downward price movement.

Proximity to Moving Average: Use the proximity tolerance setting to filter out signals that are not closely aligned with the moving average trend.

This indicator is ideal for traders looking to identify strong market movements and align their trades with significant price actions. Customize the settings to fit your trading style and enhance your market analysis.

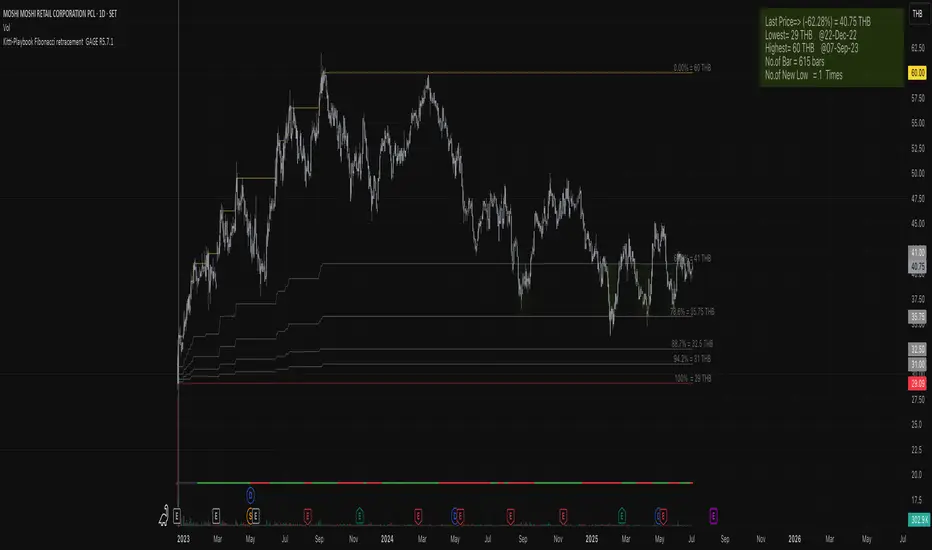

Kitti-Playbook Fibonacci retracement GAGE R0.00

Release Notes: Oct 25 2021

OVERVIEW :Kitti-Playbook Fibonacci retracement GAGE R0.00

Easy for visualize Fibonacci retracement level

CONCEPTS

1)Minimum Line = Lowest level of Source form start

2)Maximum Line = Highest level of Source form New Low

3)Calculation

a) Fibonacci Retracement of 61.8% form Maximum level

b) Fibonacci Retracement of 78.6% form Maximum level

c) Fibonacci Retracement of 88.7% form Maximum level

d) Fibonacci Retracement of 94.2% form Maximum level

4)Information Display

a) Information Bar show Number of New Low , Max level , Min Level , Last Bar No, Current Pricel

b) GAGE Scale Number

c) New Low

Quant Signals: Market Sentiment Monitor HUDWavelets & Scale Spectrum

This indicator is ideal for traders who adapt their strategy to market conditions — such as swing traders, intraday traders, and system developers.

Trend-followers can use it to confirm trending conditions before entering.

Mean-reversion traders can spot choppy markets where reversals are more likely.

Risk managers can monitor volatility shifts and regime changes to adjust position size or pause trading.

It works best as a market context filter — telling you the “weather” before you decide on the trade.

Wavelets are like tiny “measuring rulers” for price changes. Instead of looking at the whole chart at once, a wavelet looks at differences in price over a specific time scale — for example, 2 bars, 4 bars, 8 bars, and so on.

The scale spectrum is what you get when you measure volatility at several of these scales and then plot them against scale size.

If the spectrum forms a straight line on a log–log chart, it means price changes follow a consistent pattern across time scales (a power-law relationship).

The slope of that line gives the Hurst exponent (H) — telling you whether moves tend to persist (trend) or reverse (mean-revert).

The height of the line gives you the volatility (σ) — the average size of moves.

This approach works like a microscope, revealing whether the market’s behaviour is consistent across short-term and long-term horizons, and when that behaviour changes.

This tool applies a wavelet-based scale-spectrum analysis to price data to estimate three key market state measures inside a rolling window:

Hurst exponent (H) — measures persistence in price moves:

H > ~0.55 → market is trending (moves tend to continue).

H < ~0.45 → market is choppy/mean-reverting (moves tend to reverse).

Values near 0.5 indicate a neutral, random-walk-like regime.

Volatility (σ) — the average size of price swings at your chart’s timeframe, optionally annualized. Rising volatility means larger price moves, falling volatility means smaller moves.

Fit residual — how well the observed multi-scale volatility fits a clean power-law line. Low residual = stable behaviour; high residual = structural change (possible regime shift).

WaveRider [Scalping-Algo]# 📊 TrendPulse Pro - Indicator Guide

## 🎯 What is it?

A clean all-in-one trend tool. Combines 4 smoothed MAs, candlestick patterns & session highlights. No clutter, just signals.

---

## 🔧 Features

### 📈 4 Smoothed Moving Averages

- **21 SMMA** (Cyan) → Fast trend, scalping

- **50 SMMA** (Green) → Swing entries

- **100 SMMA** (Gold) → Medium trend filter

- **200 SMMA** (Red) → Major trend direction

💡 *Price above all = strong bull. Below all = strong bear.*

---

### ⚡ 3 Line Strike Pattern

Rare but powerful reversal signal.

- 🟢 **Bull 3LS** → 3 red candles + 1 big green that closes above first candle

- 🔴 **Bear 3LS** → 3 green candles + 1 big red that closes below first candle

💡 *Best near support/resistance zones.*

---

### 💎 Engulfing Candles

Shows momentum shift.

- 🟢 **Bull Engulf** → Green candle swallows previous red

- 🔴 **Bear Engulf** → Red candle swallows previous green

💡 *Filter with trend direction for better win rate.*

---

### 🕐 Session Highlight

See your trading window clearly.

- Light shade = Pre-session (prep time)

- Darker shade = Active session (go time)

💡 *Default is CME hours. Adjust in settings.*

---

## 📝 Quick Setup

1. Add to chart

2. Pick your timeframe (works on any)

3. Toggle what you need ON/OFF

4. Set your session times

5. Trade with confidence

---

## 🎨 Color Guide

| Element | Default Color | Meaning |

|---------|---------------|---------|

| 21 MA | Cyan | Fast trend |

| 50 MA | Green | Swing trend |

| 100 MA | Gold | Filter |

| 200 MA | Red | Big picture |

| Fill Green | Light Green | Bullish bias |

| Fill Red | Light Red | Bearish bias |

---

## ⚠️ Tips

✅ Use MA stack for trend bias

✅ Wait for patterns AT key levels

✅ Combine with volume

✅ Respect the 200 MA

❌ Don't trade against all MAs

❌ Don't chase every signal

❌ Don't ignore session times

---

## 🚀 Best Practices

**For Scalping:**

- Focus on 21 & 50 MA

- Trade engulfing patterns

- Use 1-5 min charts

**For Swing:**

- Focus on 100 & 200 MA

- Trade 3 Line Strike

- Use 1H-4H charts

---

Made with ☕ by a trader, for traders.

*"Keep it simple. Let price do the talking."*

WaveTrend with Bollinger BandsPlots TTM Squeeze momentum histogram (green/red).

Plots RSI (blue) in the same pane.

Shows squeeze dots and RSI overbought/oversold lines.

WaveTrend MultiEMAThis is a modification of LazyBear's WaveTrend. The SMA trend has been removed and a shorter time frame EMA has been added in black. The idea is to buy when the shorter time frame starts to curl up and the longer time frame, green, has started to either flatten out or curl up too. Sell when the shorter time frame has started down and green has either flattened or bottomed out as well. The black line will generate some noise so the key is to use the two in combination. My final goal would be to have the green line looking at daily candles and the black line looking at a 2 or 4 hour candle, but I haven't figured out how to do that.

WaveTrend with Crosses and Alerts - Jab ZootaLazy bear created this script. I added alertconditions to send alerts on crossovers.

wt+ichmokuwaveTrend is very very very nice script.

and i also like ichmoku

yesterday 'nssoholik' gave me some idea that is rsi+ichmoku

and this is wt+ichmoku

easily

red to green = buy

green to red = sell

WaveTrend [DagoDias]@author LazyBear -- Modificado por Dagodias adicionado títulos às variáveis e traduzido para o Português.

Através dos títulos fica melhor para customizar o indicador e criar alertas a partir do indicador.

Para utilização em Criptomoedas acredito ser interessante suavemente levantar as linhas base; tornando a área de sobre venda antecipada.

Este indicador não é recomendado para fortes tendências.

WaveTrend [MastroFran]Great indicator to show short term price movements. 5 day moving average oscillator. When green crosses red and under the 60 mark, buy with caution. when over the 60 mark and red crosses green sell immediately for highest profits.

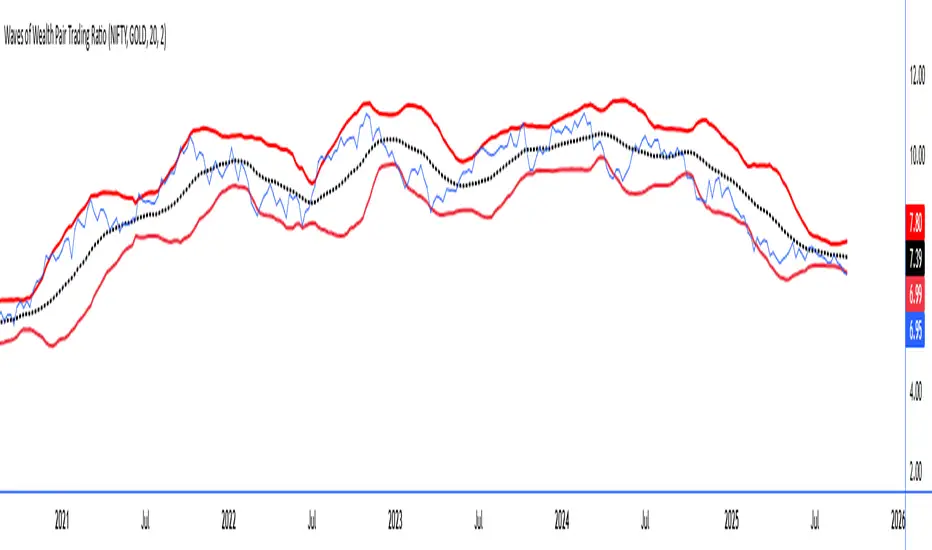

Waves of Wealth Pair Trading RatioThis versatile indicator dynamically plots the ratio between two user-selected instruments, helping traders visualize relative performance and detect potential mean-reversion or trend continuation opportunities.

Features include:

User inputs for selecting any two instrument symbols for comparison.

Adjustable moving average period to track the average ratio over time.

Customizable standard deviation multiplier to define statistical bands for overbought and oversold conditions.

Visual display of the ratio line alongside upper and lower bands for clear trading signals.

Ideal for pair traders and market analysts seeking a flexible tool to monitor inter-asset relationships and exploit deviations from historical norms.

Simply set your preferred symbols and parameters to tailor the indicator to your trading style and assets of interest.

How to Use the Custom Pair Trading Ratio Indicator

Select symbols: Use the indicator inputs to set any two instruments you want to compare—stocks, commodities, ETFs, or indices. No coding needed, just type or select from the dropdown.

Adjust parameters: Customize the moving average length to suit your trading timeframe and style. The standard deviation multiplier lets you control sensitivity—higher values mean wider bands, capturing only larger deviations.

Interpret the chart:

The ratio line shows relative strength between the two instruments.

The middle line represents the average ratio (mean).

The upper and lower bands indicate statistical extremes where price action is usually overextended.

Trading signals:

Look to enter pair trades when the ratio moves outside the bands—expecting a return to the mean.

Use the bands and mean to set stop-loss and profit targets.

Combine with other analysis or fundamental insight for best results.

Wave Trend Arrows [Salty]This is just like WT_LB, but with arrows that increase in size to show cross over points. The larger down arrows indicate resistance for overbought levels, and the larger up arrows indicate support for oversold levels.