Strategy TemplateTrying to include few basic things which is needed for strategy which can be used as template.

Few important components

Strategy parameters

Few important parameters include - initial_capital, default_qty_type, default_qty_value, commission_type, pyramiding and commission_value. All my strategies will have similar settings with initial captial set to 20000 to 100000. 100% of equity per trade with no pyramiding (set to 1) and minimal commission.

margin_long and margin_short can be used for leveraged trading. But, since we are not using pyramiding, it will make no effect.

Trade Limiting parameters

Two types of limiting is available in the scripts

Limiting trading direction : this is done through method strategy.risk.allow_entry_in and input parameter tradeDirection

Limiting trades to particular time window : This is achieved through adding start time and end time parameters of type input.time and check whether time is within this window

Custom Methods

customized security method to get higher timeframe data

customized moving average method to get moving average of any type

Custom Parameters

Moving average Type option list which I use quite often. Any strategy where there is need to use moving average, I try to scan through different moving average types and lengths to see which one is more appropriate for the given strategy. Hence, keeping this parameter in template to make it readily available when I start with new strategy

waitForCloseBeforeExit - this is used if trailing stop need to activated as soon as price hits the stop or only on close price. This is again something I switch quite often based on strategy. Hence, keeping this as part of the template.

Entry and Exit statements for long and short

These statements from line (57 to 62) can remain as is even with new strategy. Only thing to be set are variables - buyCondition, sellCondition, closeBuyCondition and closeSellCondition

Last but not the least

In pinescript, a long and short position cannot coexist in a strategy at any point of time. Any short positions created will automatically stop long positions and vice versa. Hence, it is important make short and long trades mutually exclusive. In this example, I have used 200 weekly moving average as trend bias. No short positions are taken when price is trading above 200 weekly moving average low/close and no long positions are taken when price is less than 200 weekly moving average high/close. Any rule built on top of this (In this case a simple supertrend rules) ensures that there are no conflicting signals and hence avoids confusing trades on the stratgy.

Cerca negli script per "weekly"

CheckmateTrades - Pivots End GameThis indicator is based on the Pivot study. Traders will be able to plot CPR, Standard floor pivots as well as Camarilla Pivots on multiple timeframes.

Why pivots from multiple timeframes are relevant and included in this one indicator?

We can analyse pivots on multiple timeframes for different trading setups. As in, Daily floor pivots are best suited for analysing the market trend for Day trading. Similarly, Weekly and Monthly floor pivots can be analysed for Swing and positional trading entries. Whereas yearly pivot is best suited for trend analysis for investment purpose.

What is the relevance of plotting tomorrow's pivot level in advance?

Pivot are calculated based on the price happened on a previous day. And hence trader can plot tomorrow pivots in advance to shortlist stocks for tomorrow's trading session.

TimeFrames Available to traders are –

1. Daily

2. Weekly

3. Monthly

A) Daily Pivots

Present Day –

1. Trader can plot Daily CPR

2. Trader can plot Daily R1, R2, R3 and R4 pivot resistance levels

3. Trader can plot Daily S1, S2, S3 and S4 pivot support levels

4. Trader can plot Daily Camarilla levels

Future Day –

1. Trader can plot Tomorrow CPR

2. Trader can plot Tomorrow R1, R2, R3 and R4 pivot resistance levels

3. Trader can plot Tomorrow S1, S2, S3 and S4 pivot support levels

4. Trader can plot Tomorrow Camarilla levels

5. Previous Day High and Low

B) Weekly Pivots

Present Week –

1. Trader can plot Present week CPR

2. Trader can plot Present week R1, R2, R3 and R4 pivot resistance levels

3. Trader can plot Present week S1, S2, S3 and S4 pivot support levels

4. Trader can plot Present week Camarilla levels

Next Week –

1. Trader can plot Next week CPR

2. Trader can plot Next week R1, R2, R3 and R4 pivot resistance levels

3. Trader can plot Next week S1, S2, S3 and S4 pivot support levels

4. Trader can plot Next week Camarilla levels

5. Previous Week High and Low

C) Monthly Pivots

Present Month –

1. Trader can plot Present Month CPR

2. Trader can plot Present Month R1, R2, R3 and R4 pivot resistance levels

3. Trader can plot Present Month S1, S2, S3 and S4 pivot support levels

4. Trader can plot Present Month Camarilla levels

Next Month –

1. Trader can plot Next Month CPR

2. Trader can plot Next Month R1, R2, R3 and R4 pivot resistance levels

3. Trader can plot Next Month S1, S2, S3 and S4 pivot support levels

4. Trader can plot Next Month Camarilla levels

5. Previous Month High and Low

Moreover, I have also included SMA (Simple moving averages) study in this indicator. Trader can add 20,50 & 200 SMA on there charts.

Why is it relevant? Trader can get a visual confirmation of an up-trending or an down-trending move by looking at rising or falling 20 & 50 SMA respectively

Usually in an uptrending stocks. 20 & 50 SMA will move in parallel to each other and will rise upwards. Price will tend to trade above the 20 SMA and 20 SMA will continue to act as a support.

CPR, Camarilla & Moving AverageThis script is created primarily for Intraday trading but can also be used for short and long term trading. This is a combination of Central Pivot Range (CPR), Moving Averages and Camarilla Pivot levels (with inner levels). This helps you to combine the strategies of CPR and Moving Averages to identify the best trading opportunities with greater edge. Central Pivot Range and Camarilla pivots are taken from PivotBoss by Franc Ochoa.

Key features:

# Daily CPR levels

# Weekly CPR levels

# Monthly CPR levels

# Previous Day High and Lows

# Previous Week Highs and Lows

# Previous Month Highs and Lows

# Camarilla Pivots with inner Levels

# CPR Levels for the next Day, Week and Month

# 5 Simple moving averages and 5 Exponential Moving Averages

What separates this script from other scripts with CPR and Moving averages?

# One of the few indicators (if not the only one) which combines the 2 types of Moving Averages, CPR and also Camarilla Pivots.

# CPR Levels for not just the next Day, but for next Week(Weekly CPR) and Month(Monthly CPR) also.

# Hide the previous day's levels according to your wish. This is the most unique feature of this indicator. You can set the number of Daily CPR levels you want to load in the chart. This is not just for the Daily CPR but also for the Weekly and Monthly CPR also. This makes the chart less cluttered and prevents the candles from getting buried in the indicators. Please notice how the previous day's CPR levels are hidden in the displayed demo chart on the script page. In the chart, only one trading day's data is shown(by default).

# This script is OPEN SOURCE.

Strategies :

For CPR & Camarilla Strategies for intraday trading and swing trading refer to the book 'Secrets of a Pivot Boss: Revealing Proven Methods for Profiting in the Market' by Franklin O. Ochoa.

Moving averages strategies :

Moving averages can be combined and also used individually for several strategies

* 9 EMA can be used as trailing stop loss for strong moving trends that helps you to catch big moves.

* 20sma can be used not just trailing stop loss but also for taking re-entry to the trend.

* Golden cross - The golden cross occurs when a short-term moving average crosses over a major long-term moving average to the upside. This indicates a bullish turn in the market. Eg: 50 SMA cuts 200 SMA from below.

* Death Cross - The death cross occurs when the short term moving average crosses the long-term average from above. This indicates a bearish turn in the market. Eg: 50 SMA cuts 200 SMA from above.

* When 20 SMA is above 50 SMA and 20 SMA and 50 SMA are angling up like parallel lines, then it denotes bullish strength. If this happens right after Golden Cross, big moves to the upside can be expected.

* When 20 SMA is below 50 SMA and 20 SMA and 50 SMA are angling down like parallel lines, then it denotes bearish strength. If this happens right after Death Cross, big moves to the downside can be expected.

* When 20SMA and 50 SMA are going flat and crossing each other, then it denotes sideways sentiment.

Moving average strategies are taken from the book 'How to Make Money in Intraday Trading' by Ashwani Gujral. For learning more about how to combine CPR and Moving averages in your trading please refer to this book.

[JL] High-Low CloudJust got this idea and made this one.

Default use 1-hour chart to watch 5-hour, daily and weekly high-low. Of course you can set up any parameters as you like.

It is more like an art. So I do not really know how to use it to trade at this moment. If you have good ideas, feel free to post comments. Thanks.

- Green cloud, SMA - Weekly HL ~ SMA - Daily HL

- Lime cloud, SMA - Daily HL ~ SMA - 5-Hour HL

- White cloud, SMA - 5-Hour HL ~ SMA + 5-Hour HL

- Organge cloud, SMA + 5-Hour HL ~ SMA + Daily HL

- Red Cloud, SMA + Daily HL ~ SMA + Weekly HL

To watch it, probably take care of :

- Angles

- cloud size changes

- divergence

- Oversold, overbought

[RickAtw] O1 Opening Market LineThis indicator helps to identify current support and resistance based on the opening of the Asian, London and New York sessions.

Function

You can make good trade entries based on these lines. Shows daily and weekly openings of each session

It will also help you to look at which session you are currently trading)

Purple ----> Asian session

Red ----> London session

Blue ----> New York session

Key Signal

buy ---> A strong buy signal is a bounce from the low and the presence of a weekly or day open line.

sell ---> A strong sell signal is a bounce from the maximum and the presence of a weekly or day open line.

P.S. Be sure to test on your pair!

Remarks

This will help you determine the approximate area of support and resistance.

Since we cannot look into the future, it does not inform you about the exact records, but a possible change in trends.

Readme

In real life, I am a professional investor. And I check each of my indicators on my portfolio and how effective it is. I will not post a non-working method. The main thing is to wait for the beginning of trends and make money!

I would be grateful if you subscribe ❤️

Chart Champions - Part 3 - SessionsThank you for sparing you time to read my indicator.

This indicator has been created as a suite of 3. This was to ensure that those with only the Free Trading View account could benefit (with their restriction to 3 indicators). Please ensure you install each indicator and read each indicator write up to fully understand what has tried to achieved.

Chart Champions – Part 1 –Lvls nPOC VWAPS

This indicator is broken down into:

• Levels

• VWAPS

• Naked Point of Control

Levels

It displays the levels to the right of the price Axis to enable the user to have a cleaner chart.

The below levels will automatically appear:

dOpen – pdHigh – pdLow – pdEQ – pwEQ

Optional Levels include:

mOpen – pmOpen – pdOpen – dbyOpen – wOpen – pwOpen

VWAPs

Optional VWAPs

Daily (including pdVWAP close) – Weekly – Monthly

Naked Points of Control (nPOC)

To view the nPOC move the chart back in time to pick up the nPOCs.

Chart Champions – Part 2 – CCV IBs POC

This indicator is broken down into:

• Chart Champions Value

• Initial Balance

• Points of Control

Chart Champions Value (CCV)

CCV is based on the 80% rule of the dOpen opening outside of the pdVAH/pdVAL. Please do you own research to fully understand how this trading strategy works (readily avaliable online).

Initial Balance (IB)

IB is based on the first 60 minutes of the market opening. It captures the highest and lowest points within that 60 minutes. Please do you own research to fully understand how this trading strategy works (readily avaliable online).

Points of Control (POCs)

POC are the price levels where the most volume was traded.

Developing POC (dPOC) will constantly move with volume/price action through out the day.

Optional POCs

Previous Day POC (pdPOC) – Day Before Yesterday POC (dbyPOC)

Chart Champions – Part 3 – Sessions - Manual Input

This indicator is broken down into:

• Manual Inputs (daily, weekly, monthly)

• IGOR SessionsTtimes

• Pre + Market Openings

Manual Input

Daily x3

Weekly x 3

Monthly x 3

This allows the trader to put in specific levels.

IGOR Session Times

This is a user specific requirement to highlight cetain times during the day, displayed at the bottom of the chart in the colour strip.

Pre + Market Openings

This allows the user to see when pre market trading has started and with the live maket has started, displayed at the top of the chart in colours.

A huge thank you goes out to:

Stackoverflow users AnyDozer and Bjorn.

TV user ahancock for allow me use of this code.

Disclaimer the lower the timeframe the more information it processes.

Chart Champions - Part 2 - CCV IBs POCsThank you for sparing you time to read my indicator.

This indicator has been created as a suite of 3. This was to ensure that those with only the Free Trading View account could benefit (with their restriction to 3 indicators). Please ensure you install each indicator and read each indicator write up to fully understand what has tried to achieved.

Chart Champions – Part 1 –Lvls nPOC VWAPS

This indicator is broken down into:

• Levels

• VWAPS

• Naked Point of Control

Levels

It displays the levels to the right of the price Axis to enable the user to have a cleaner chart.

The below levels will automatically appear:

dOpen – pdHigh – pdLow – pdEQ – pwEQ

Optional Levels include:

mOpen – pmOpen – pdOpen – dbyOpen – wOpen – pwOpen

VWAPs

Optional VWAPs

Daily (including pdVWAP close) – Weekly – Monthly

Naked Points of Control (nPOC)

To view the nPOC move the chart back in time to pick up the nPOCs.

Chart Champions – Part 2 – CCV IBs POC

This indicator is broken down into:

• Chart Champions Value

• Initial Balance

• Points of Control

Chart Champions Value (CCV)

CCV is based on the 80% rule of the dOpen opening outside of the pdVAH/pdVAL. Please do you own research to fully understand how this trading strategy works (readily avaliable online).

Initial Balance (IB)

IB is based on the first 60 minutes of the market opening. It captures the highest and lowest points within that 60 minutes. Please do you own research to fully understand how this trading strategy works (readily avaliable online).

Points of Control (POCs)

POC are the price levels where the most volume was traded.

Developing POC (dPOC) will constantly move with volume/price action through out the day.

Optional POCs

Previous Day POC (pdPOC) – Day Before Yesterday POC (dbyPOC)

Chart Champions – Part 3 – Sessions - Manual Input

This indicator is broken down into:

• Manual Inputs (daily, weekly, monthly)

• IGOR SessionsTtimes

• Pre + Market Openings

Manual Input

Daily x3

Weekly x 3

Monthly x 3

This allows the trader to put in specific levels.

IGOR Session Times

This is a user specific requirement to highlight cetain times during the day, displayed at the bottom of the chart in the colour strip.

Pre + Market Openings

This allows the user to see when pre market trading has started and with the live maket has started, displayed at the top of the chart in colours.

A huge thank you goes out to:

Stackoverflow users AnyDozer and Bjorn.

TV user ahancock for allow me use of this code.

Disclaimer the lower the timeframe the more information it processes.

Chart Champions - Part 1 - nPOC - Levels - VWAPsThank you for sparing you time to read my indicator.

This indicator has been created as a suite of 3. This was to ensure that those with only the Free Trading View account could benefit (with their restriction to 3 indicators). Please ensure you install each indicator and read each indicator write up to fully understand what has tried to achieved.

Chart Champions – Part 1 –Lvls nPOC VWAPS

This indicator is broken down into:

• Levels

• VWAPS

• Naked Point of Control

Levels

It displays the levels to the right of the price Axis to enable the user to have a cleaner chart.

The below levels will automatically appear:

dOpen – pdHigh – pdLow – pdEQ – pwEQ

Optional Levels include:

mOpen – pmOpen – pdOpen – dbyOpen – wOpen – pwOpen

VWAPs

Optional VWAPs

Daily (including pdVWAP close) – Weekly – Monthly

Naked Points of Control (nPOC)

To view the nPOC move the chart back in time to pick up the nPOCs.

Chart Champions – Part 2 – CCV IBs POC

This indicator is broken down into:

• Chart Champions Value

• Initial Balance

• Points of Control

Chart Champions Value (CCV)

CCV is based on the 80% rule of the dOpen opening outside of the pdVAH/pdVAL. Please do you own research to fully understand how this trading strategy works (readily avaliable online).

Initial Balance (IB)

IB is based on the first 60 minutes of the market opening. It captures the highest and lowest points within that 60 minutes. Please do you own research to fully understand how this trading strategy works (readily avaliable online).

Points of Control (POCs)

POC are the price levels where the most volume was traded.

Developing POC (dPOC) will constantly move with volume/price action through out the day.

Optional POCs

Previous Day POC (pdPOC) – Day Before Yesterday POC (dbyPOC)

Chart Champions – Part 3 – Sessions - Manual Input

This indicator is broken down into:

• Manual Inputs (daily, weekly, monthly)

• IGOR SessionsTtimes

• Pre + Market Openings

Manual Input

Daily x3

Weekly x 3

Monthly x 3

This allows the trader to put in specific levels.

IGOR Session Times

This is a user specific requirement to highlight cetain times during the day, displayed at the bottom of the chart in the colour strip.

Pre + Market Openings

This allows the user to see when pre market trading has started and with the live maket has started, displayed at the top of the chart in colours.

A huge thank you goes out to:

Stackoverflow users AnyDozer and Bjorn.

TV user ahancock for allow me use of this code.

Disclaimer the lower the timeframe the more information it processes.

Bitcoin Bulls and Bears by @dbtrBitcoin 🔥 Bulls & Bears 🔥

v1.0

This free-of-charge BTC market analysis indicator helps you better understand what's going with Bitcoin from a high-level perspective. At a glance, it will give you an immediate understanding of Bitcoin’s historic price channel dating back to 2011, past and current market cycles, as well as current key support levels.

Usage

Use this indicator with any BTCUSD pairs , ideally with a long price history (such as BNC:BLX )

We recommend to use this indicator in log mode, combined with Weekly or Monthly timeframe.

Features

🕵🏻♂️ Historic price channel curve since 2011

🚨 Bull & bear market cycles (dynamic)

🔥 All-time highs (dynamic)

🌟 Weekly support (dynamic, based on 20 SMA )

💪 Long-term support (channel bottom)

🔝 Potential future price targets (dynamic)

❎ Overbought RSI coloring

📏 Log/non-log support

🌚 Dark mode support

Remarks

With exception of the price channel curve, anything in this indicator is calculated dynamically , including bull/bear market cycles (based on a tweaked 20SMA), ATHs, and so on. As a result, historic market cycles may not be 100% accurately reflected and may also differ slightly in between various time-frames (closest result: Monthly). The indicator may even consider periods of heavy ups/downs as their own market cycles, even though they weren’t. Due to its dynamic nature, this indicator can however adapt to the future and helps you quickly identify potential changes in market structure, even if the indicator is no longer updated.

On top of that bullmarket cycles (colored in green) feature an ingrained RSI: the darker the green color, the more the RSI is overbought and close to a correction (darkest color in the chart = 90 Weekly RSI). In comparison with past bull cycles, it helps you easily spot potential reversal zones.

Thanks

Thanks to @quantadelic and @mabonyi which both have worked on the BTC "growth zones" indicator including the price channel, of which I have used parts of the code as well as the actual price channel data.

Follow me

Follow me here on TradingView to be notified as soon as new free and premium indicators and trading strategies are published. Inquire me for any other requests.

Enjoy & happy trading!

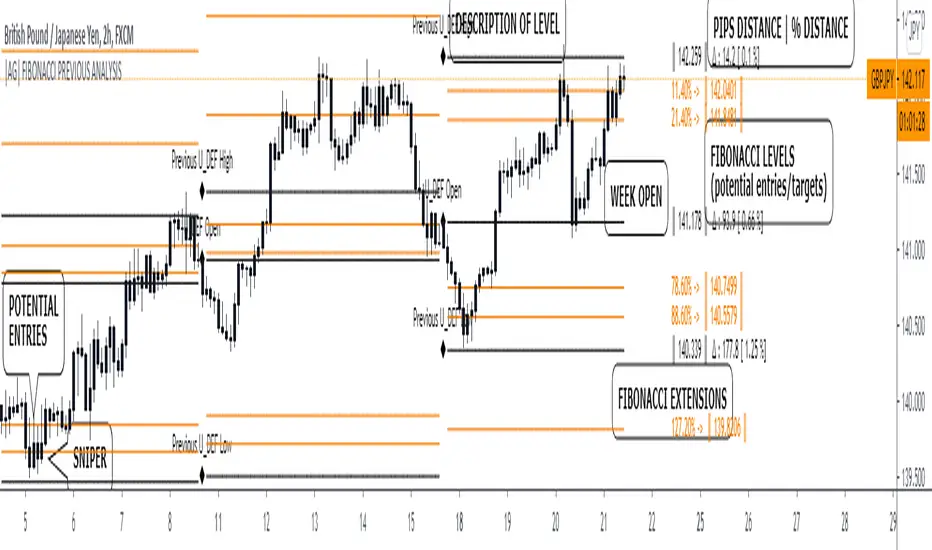

|AG| Previous Analysis█ OVERVIEW

Analysis of previous levels is one of the best strategies in order to get good entries or take profits levels. This analysis involves Monthly and Weekly Previous Levels and One User Definition Option. So u could select any period like Daily or even hours according to ur trading style. The previous levels are High and Low. And the Current (NOT PREVIOUS) open level.

This script also includes one Fibonacci Selector that will calculate the Fibbo level between previous High and Low Levels of the user selection. Almost everything could be modified in the input panel.

Input Options

A detailed explanation of input settings:

• # Of Previous

• This option leads us to select the number of previous weeks, months, or the user selection back.

• Example: If we select Previous High, Low WEEKLY so if # Of previous is one is going to be the past levels but if is 2 so consequently 2 previous levels.

• In the case of 0 is going to be the actual levels

• Fibbo & Label Selector

Here we can select the period.

• Monthly, Weekly, And User Definition is available.

• Fibonacci Selector :

• Here we could choose between different levels of Fibonacci or No_Plot Option

• Label Offset

• Here we select the amount of distance between label and actual price

• Time Start

• Here we could highlight one period START and END like one Week start day and end day.

• User Definition Value in order to be more flexible.

Interesting Code Lines:

• Fibonacci function

getFib(a, b)=>

fib1 = a + (b - a) * -0.618

fib2 = a + (b - a) * -0.270

fib3 = a + (b - a) * 0.114

fib4 = a + (b - a) * 0.214

fib5 = a + (b - a) * 0.382

fib6 = a + (b - a) * 0.500

fib7 = a + (b - a) * 0.618

fib8 = a + (b - a) * 0.786

fib9 = a + (b - a) * 0.886

ext_ = a + (b - a) * 1.270

ext1 = a + (b - a) * 1.618

• Exact Distance and % Distance

f_dist (_src, _src3) =>

float _dist = _src3 - _src

float _perc = _dist / _src3 //* 100

|AG| VWAP ANALYSIS|AG| VWAP ANALYSIS

The volume-weighted average price (VWAP) is a trading benchmark used by traders that gives the average price security has traded throughout the day, based on both volume and price.

It is important because it provides traders with insight into both the trend and value of the security.

VWAP is calculated by adding up the $ traded for every transaction (price multiplied by the number of shares traded) and then dividing by the total shares traded.

A detailed formula and calculations could be found here:

-> fanf2.user.srcf.net

Actually, TradingView has an option for Anchored Vwap is a really good implementation for specific analysis.

The following script takes into account the #Time_Period_Change and plots the VWAP calculation.

The #Time_Period Available for this script are:

-> Day

-> Week

-> Monthly

-> Quarter

-> Year

1. The option that we have is the SOURCE:

-> HLC3 (High, Low, Close)/3 is the right way to calculate VWAP.

-> But I included other traditional options:

-> open, high, low, close, hl2, hlc3, ohlc4

2. The option of Turn ON/OFF VWAP

-> Timeframe selection:

-> All, 1. Day, 2. Week, 3. Month, 4. Quarter, 5. Year, 6. >=Weekly, 7. >=Montlhy

-> With this, we could select the time for plotting the VWAP. And some cool features such as >= that we are going to plot different Timeframes VWAP calculations.

-> Vwap Label:

-> We could select if show labels or not

3. The option of Turn ON/OFF Previous VWAP Level

-> VWAP of one selected Time Period is going to end with a final price this level most of the time is retested and gives us a good opportunity for entry into one trade.

Or could be used as Stop Loss.

-> Timeframe selection:

-> 1. Day, 2. Week, 3. Month, 4. Quarter, 5. Year, 6. >=Weekly, 7. >=Montlhy, 8. >=Daily

-> Factor

-> The factor options lead as increment the extension of the previous time period.

-> Example: D is the normal time period and with factor, we change from 1D to 2D in order to extend previous levels of VWAP.

->The Factor option is only available in 1. Day and 2. Week. With a Min Value of 1 and a Maximum Value of 50.

-> Labels:

-> We could select if show labels or not

4. The option of Turn ON/OFF Standard Deviation Bands

-> Label:

-> We could select if show labels or not

-> Timeframe selection:

-> 1. Day, 2. Week, 3. Month, 4. Quarter, 5. Year

5. The option of Turn ON/OFF Previous Standard Deviation

-> Timeframe selection:

-> None, 1. Day, 2. Week, 3. Month, 4. Quarter, 5. Year, 6. >=Weekly, 7. >=Montlhy, 8. Quarter & Year

-> STDEV LEVEL

-> Since there are different options for Standard Deviation I included 4 options

-> 1

-> 2

-> 3

-> User Selection

-> In this option we could select any NUMBER for STVDEV 0.25 of step.

-> Label:

-> We could select if show labels or not

6. The Lockback Setting

-> This Script also includes an option to only plot a certain amount of days back.

The main reason in order to have a more clear chart.

-> We could select between:

-> PLOT ALL

-> CUSTOM

-> If we select Custom Then we could select the Number of Days Back that is going to be plotted.

7. Color Theme

Here we select the color (Visual Desing)

-> Color Theme

-> Text Color

-> Here I use the recent input.color option added for TradingView making the color selection really simple

8. Time Period Highlighter

-> In this option, we could select one time period in order to plot one tiny background and identify the change in the time period.

-> Timeframe selection:

-> 1. Day, 2. Week, 3. Month, 4. Quarter, 5. Year

9. Label Offset

-> Finally, this option leads us to change the position of the labels into the X-axis by default 20.

This script has many options the combinations and the possibilities of making different analyses are bast.

Here some examples of what we could make:

DEFAULT SETTING:

PREVIOUS VWAP FOR TIME PERIOD >= WEEK

(work good as S&D levels)

PREVIOUS VWAP Week WITH A FACTOR OF 4

STANDARD DEVIATION BANDS - DAY

STANDARD DEVIATION BANDS - WEEK

STANDARD DEVIATION BANDS - MONTH

STANDARD DEVIATION BANDS - QUARTER

STANDARD DEVIATION BANDS - YEAR

PREVIOUS STANDARD DEVIATION - DAY SDTV 3

PREVIOUS STANDARD DEVIATION - WEEK SDTV 3

USING STANDARD DEVIATION BANDS - WEEK

WITH LOCKBACK -> PLOT ALL

WITH CUSTOM 30 DAYS

I think the options possibilities of analysis using #VWAP are truly awesome.

I like the relationship that one previous VWAP has with Standard Pivot Points.

Good Luck,

Anderson,

RSI of VWAP [SHORT selling]This is SHORT selling version of RSIofVWAP strategy. Settings and Logic are totally different from LONG side version , hence I am publishing it as a new strategy.

Settings

============

VWAP of RSI Length 15

Slow EMA Length 200

Short entry level 25

Cover short level 70

stop loss 5

SHORT Entry

============

condition1 : When RSIofVWAP crossdown below 25 and VWAP is below ema200

condition2: When weekly RSIofVWAP crossdown 70 and VWAP (note : session vwap , not weekly vwap) is below ema200

condition3: Use VIX value , if you want to short when the price is above ema200

vwap RSI crossing down 70 and VIX RSI is cossing up 70

enter short ... This is like falling knife :-)

I need to add the code -- later

if any of above condition is TRUE , SHORT entry will be taken

Take Profit

============

When close less than short entry price and RSIofVWAp is crossing up 25 , take profit ...close 1/3 of the position

Exit

============

When RSIofVWAP crossing up 70 level

Stop Loss

============

Stop Loss is set to 5%

Note:

1. When strategy is in SHORT position , background and bar color changes to gray

2. When strategy is already in short position , possible entries are shown in yellow background

3. RSI Length 15 is working most of the equities on hourly chart. ( RSI length 9 and 14 also works good , but not for all ... You may want to try which setting works for your symbol)

4. weekly VWAP (blue color) is also plotted by default ... you can disable it if you dont want to see it. But there is advantage keeping it on the chart , you can notice whenever weekly VWAP crosses above 70 line , trend is UP ... if you have LONG position you can hold on it ... Hurray :-)

Warning

============

For the educational purposes only

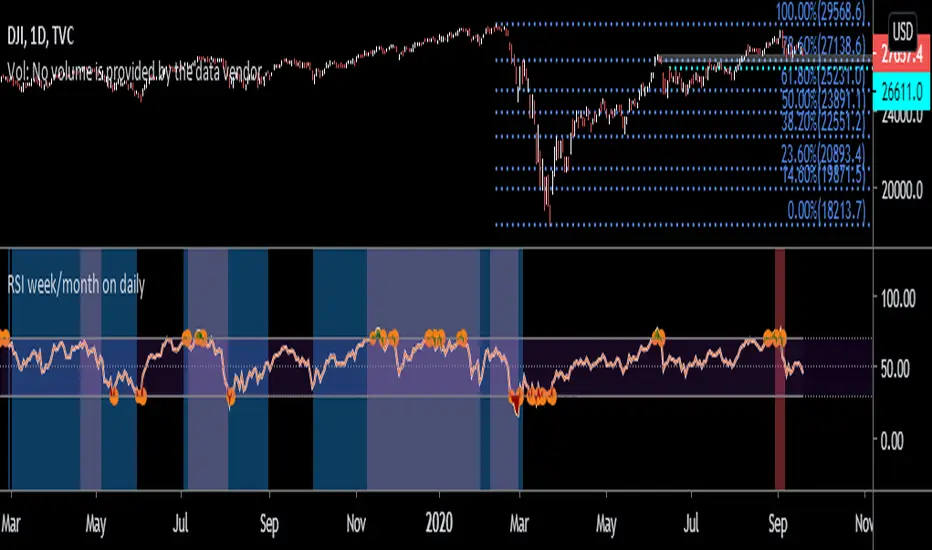

BTC risk gagueThis indicator measures the risk of buying/selling BTC at a certain price. It calculates the percentage difference between the 20 weekly SMA and price at the weekly close. This indicator is designed to be used under weekly scale.

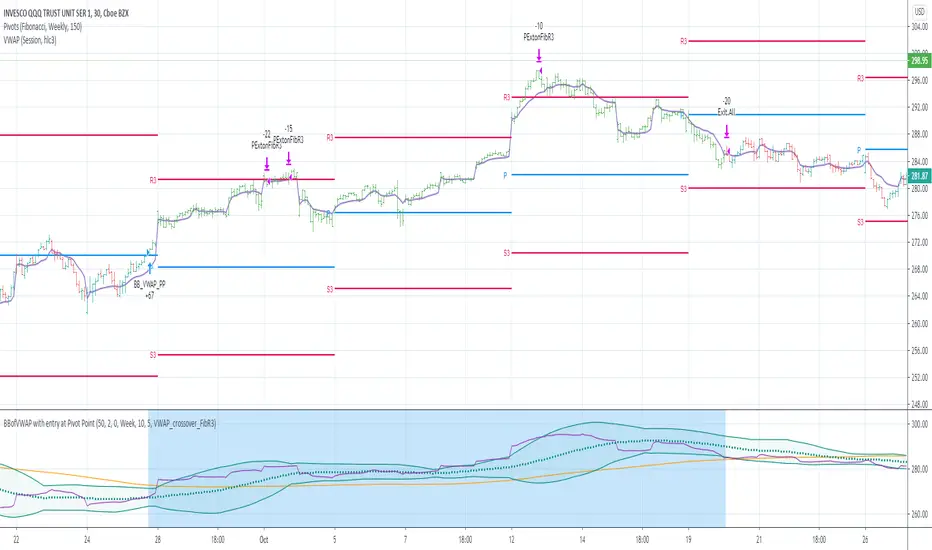

BBofVWAP with entry at Pivot PointThis strategy uses BB of VWAP and Pivot point to enter and exit the Long position.

settings

BB length 50

BB Source VWAP

Entry

When VWAP crossing up BB midline and price/close is above weekly PivotPoint ( you can also use Daily pivot point )

Exit

When VWAP is crossing down BB lower band

Stop Loss

Stop loss defaulted to 5%

Note : Long will position will be exited on either VWAP crossing down BB lower band or stop loss is hit - whichever comes first . Being said that some time your stop loss exit is less than 5% which saves from more losses.

Entry is based on weekly Pivot point , so any time frame below weekly will work perfect. I have tested t on 30 min , 1 HR , 4 Hr , Daily charts. Even weekly setting shows good results , that will work for long term investing style.

if you change Pivot period to Daily , chose time frames below Daily.

I also noticed this strategy mostly do not enter Long position in a down trend. Even it finds one , it will be exited with minimal loss.

Warning

For the use of educational purposes only

Multi RSI based on Timeframe

This code has been inherited from " 3 RSI Multi Timeframe Inception" by pranjalchaubey and enhanced/modified to include 2 more RSI indicators. The RSIs considered are 15 minutes, 1 Hour, Daily, Weekly and Monthly displayed based on chart time frame.

The number of RSI indicators displayed is context dependant or time frame based, as below,

15min, hourly and daily RSIs are displayed on 15 mins or hourly charts, often used for Intraday trading,

Daily, Weekly and Monthly RSIs are displayed for Daily charts / Swing trading and

Weekly and Monthly RSIs for Weekly time frame / Positional trades.

RSI week/month level on daily Time frame- You can analyse the trend strength on daily time frame by looking of weekly and monthly is greater than 60.

- Divergence code is taken from tradingview's Divergence Indicator code.

#Strategy 1 : BUY ON DIPS

- This will help in identifying bullish zone of the price when RSI on DAILY, WEEKLY and Monthly is >60

-Take a trade when monthly and weekly rsi is >60 but daily RSI is less thaN 40.

Static + Dynamic LevelsShows static and dynamic levels which can act as support/resistance. These are important as there is a lot of users who are interested in buying/selling at these prices.

Static Levels include -

Daily/Weekly/Monthly/Yearly Open (changes color depending on if below or above price)

Previous Daily/Weekly/Monthly/Yearly Open

Previous day's High/Low

Dynamic Levels include -

100/200 Daily MA

100/200 Weekly MA

Momentum_GalluThis plots the ratio of 5EMA to 21EMA on current timeframe basis and compares this with plot of the ratio of weekly 4EMA to Weekly 12 EMA

This is in attempt to find if recent momentum beats weekly momentum

Combined Candle CounterThis script combines multiple indicators and count their results in a label

- Shows the weekly moving average in a daily chart

- Count the days where the underlying is above & below the moving average and shows the figure in a label

- Shows & Count Distribution days in relation to the weekly moving average

- Daily / Weekly Moving Averages can be configured (length, type, reference)

CPR with SMA, EMA, VWAP & Super Trend by GuruprasadMeduriThis script will allow to add CPR with Standard Pivots and 4 Indicators.

Standard Pivot has 9 levels of support and 9 levels of resistance lines. It has CPR , 3 levels of Day-wise pivots , 3 levels of Weekly pivots and 3 Levels of Monthly Pivots .

In Addition to the CPR and Pivot, this script will allow user to Add 4 more Indicators - SMA, EMA, VWAP and SuperTrend as well.

All the Support and resistance levels can be enabled / disabled from settings. It will allow to select multiple combinations of support and resistance levels across 3 levels at any of the 3 time-frames individually and combined.

All 4 Indicators can be can be enabled / disabled from settings. This will allow the indicators to be plotted individually and combined along with any combination of CPR & Pivots.

These number of combinations will allow user to visualize the charts with desired indicators, pivot support & resistance levels on all or any of the 3 time frames.

For Ease of access, listed few points on how the script works..

- CPR and day-wise level 1 & 2 (S1 & R1) enabled by default and can be changed from settings

- Day-wise Level 2 & 3 (S2, R2, S3 & L3) can be enabled from settings

- Weekly 3 levels and Monthly 3 levels can be enabled from settings

- CPR & pivot levels colored in blue lines

- All support levels colored in Green

- All resistance levels Colored in Red

- Day-wise pivot , support & resistance are straight lines

- Weekly pivot , support & resistance are cross (+) lines

- Weekly pivot , support & resistance are circle (o) lines

- SMA, EMA, VWAP and SuperTrend Enabled by Default

- SMA Colored in Orange

- EMA Colored in Red

- EMA Colored in Teal

- SuperTrend Colored in standard Red & Green with triangle arrows

- Any combinations can be selected from settings-> Inputs & style

Elder Impulse SnapshotNASDAQ:AMZN

I've always been intrigued by the Elder Impulse System but found it labour intensive with its flipping back and forth between daily and weekly charts. I also wasn't fond of the way it repainted the candlesticks. So I set out to build a version where you could get every trade signal filtered down in one chart and still see the real price action.

This article provides a decent overview of the original system: www.investopedia.com

Elder Impulse Snapshot uses two EMAs and two MACDs, one of each to process both the daily and weekly data. The daily data gets an EMA of 13 periods and the standard MACD settings. For the weekly info, the EMA is set to 65 periods and all the MACD values are also multiplied by five (60, 130, 45). Buy signals are generated when both EMAs and both MACD histograms are rising. When all four of these elements are falling, sell signals are generated. If any of the indicators disagree, no signal is generated and entering any trade is not advised.

The blue and red arrows are the buy and sell signals. From my reading, it appears Dr. Elder recommended exiting the trade as soon as the system no longer generated a signal, though the case could be made for taking partial profit and moving up your stop loss to ride the trend out longer provided you haven't been stopped out yet.

CPR by GuruprasadMeduriThis script will allow to add CPR with Standard Pivot ad 9 levels of support and 9 levels of resistance lines. It has CPR, 3 levels of Day-wise pivots, 3 levels of Weekly pivots and 3 Levels of Monthly Pivots. All the Support and resistance levels can be enabled / disabled from settings. It will allow to select multiple combinations of support and resistance levels across 3 levels at any of the 3 time-frames individually and combined.

These number of combinations will allow user to visualize the charts with desired pivot support & resistance levels on all or any of the 3 time frames.

For Ease of access, listed few points on how the script works..

- CPR and day-wise level 1 & 2 (S1, R1, S2 R2) enabled by default and can be changed from settings

- Day-wise Level 3 (S3 & L3) can be enabled from settings

- Weekly 3 levels and Monthly 3 levels can be enabled from settings

- CPR & pivot levels colored in blue lines

- All support levels colored in Green

- All resistance levels Colored in Red

- Day-wise pivot, support & resistance are straight lines

- Weekly pivot, support & resistance are cross (+) lines

- Weekly pivot, support & resistance are circle (o) lines

- Any combinations can be selected from stettings-> Inputs & style

// - This is an iterative development. Will add more features due course of time. Suggestions are always welcomed!!

All past LevelsContains all past levels that we need

1. Previous Monthly High

2. Previous Monthly Low

3. Previous Weekly High

4. Previous Weekly Low

5. Previous Daily High

6. Previous Daily Low

7. Previous Monthly Range Average (PMH+PML)/2

8. Previous WeeklyRange Average (PWH+PWL)/2

9. Previous Daily Range Average (PDH+PDL)/2

10. Monthly Open

11. Weekly Open

12. Daily Open