Systemic Net Liquidity (Macro Fuel for Crypto & Stocks)This indicator tracks Systemic Net Liquidity, the single most important macro factor for determining the long-term trend of risk assets like Bitcoin (BTC) and major indices (S&P 500). It measures the amount of actual cash available in the financial system to chase speculative assets, distinguishing between money that is circulating and money that is locked up at the Federal Reserve.

Mechanism (What It Measures)

The script uses direct data from the FRED (Federal Reserve Economic Data) to calculate the true state of market funding:

\text{Net Liquidity} = \text{Fed Assets (WALCL)} - \text{Treasury General Account (TGA)} - \text{Reverse Repo (RRP)}

1. Fed Assets (WALCL): The total balance sheet of the Fed (The overall supply of money).

2. Treasury General Account (TGA): Funds the US Treasury collects via bond issuance. When the TGA rises, liquidity is actively drained from the banking system (A major bearish pressure).

3. Overnight Reverse Repo (RRP): Cash parked by banks and money market funds at the Fed, effectively frozen and not contributing to market activity.

How to Interpret Signals

Treat the Net Liquidity line as the market's "Fuel Gauge":

📈 BULLISH SIGNAL (Liquidity Injection): When the Net Liquidity line is rising, money is flowing back into the system, signalling a tailwind for risk assets.

📉 BEARISH SIGNAL (Liquidity Drain): When the line is falling (often due to high TGA balances), cash is being removed. This signals major friction and pressure on price action.

⚠️ DIVERGENCE WARNING: A strong signal is generated when Price (e.g., BTC) rises, but Net Liquidity falls. This macro divergence strongly suggests a major trend reversal or correction is imminent.

Important Notes

Data Source: Data is directly sourced from FRED and updates daily/weekly. This tool is best used for macro analysis and identifying high-level cycles, not short-term scalping.

Disclaimer: Use this indicator as a confirmation tool within your broader strategy. It is not a standalone trading signal.

Cerca negli script per "做空标普500"

My script// @version=5 indicator("Custom LuxAlgo-Style Levels", overlay=true, max_lines_count=500)

// --- Trend Detection (EMA Based) fastEMA = ta.ema(close, 9) slowEMA = ta.ema(close, 21) trendUp = fastEMA > slowEMA trendDown = fastEMA < slowEMA

plot(fastEMA, title="Fast EMA", color=color.new(color.blue, 0)) plot(slowEMA, title="Slow EMA", color=color.new(color.orange, 0))

// --- Buy / Sell Signals buySignal = trendUp and ta.crossover(fastEMA, slowEMA) sellSignal = trendDown and ta.crossunder(fastEMA, slowEMA)

plotshape(buySignal, title="Buy", style=shape.labelup, color=color.new(color.green,0), size=size.small, text="BUY") plotshape(sellSignal, title="Sell", style=shape.labeldown, color=color.new(color.red,0), size=size.small, text="SELL")

// --- Auto Support & Resistance length = 20 sup = ta.lowest(length) res = ta.highest(length)

plot(sup, title="Support", color=color.new(color.green,70), linewidth=2) plot(res, title="Resistance", color=color.new(color.red,70), linewidth=2)

// --- Market Structure (Simple Swing High/Low) sh = ta.highest(high, 5) == high sl = ta.lowest(low, 5) == low

plotshape(sh, title="Swing High", style=shape.triangledown, location=location.abovebar, color=color.red, size=size.tiny) plotshape(sl, title="Swing Low", style=shape.triangleup, location=location.belowbar, color=color.green, size=size.tiny)

// --- Alerts alertcondition(buySignal, "Buy Signal", "Trend Buy Signal Detected") alertcondition(sellSignal, "Sell Signal", "Trend Sell Signal Detected")

Steff- OBX- DTA OBX – US Open 15-Minute Zone Indicator

This indicator highlights the first 15 minutes of the U.S. stock market opening, also known as the OBX (Opening Balance Extension).

It is designed specifically for Nasdaq and S&P 500, which open at 09:30 New York time — corresponding to 15:30 Danish time.

What this indicator does:

• Marks the price range from 09:30–09:45 (U.S. time) as a zone on your chart

• Automatically adjusts to your local timezone, so the zone always aligns with Danish time

• Extends the zone to the right so you can track how price interacts with OBX throughout the day

• Draws all historical OBX zones so you can analyze previous reactions

• Rebuilds zones automatically when switching timeframes

• Detects breakouts from the zone

• Tracks balancing time only after a real breakout occurs

• Can automatically remove a zone if price spends a continuous amount of time inside it after the breakout (you set the minutes yourself)

• Allows full customization of OBX start time, duration, and behavior

• Individual zones can be manually deleted without being redrawn by the indicator

Why the OBX matters:

The OBX represents one of the most influential time windows in intraday trading because it reflects:

• The first injection of liquidity after the U.S. market opens

• Institutional positioning and algorithmic adjustments

• Early volatility and directional bias

• Common zones for reversals, breakouts, or mean reversion

• Key high-probability reaction levels used by professional traders

This indicator gives you a clear visual representation of when the market reacts to the U.S. open and how price interacts with the opening range throughout the session.

9:00-9:59 NY Range -> 10:00-11:00 Lines (v6)//@version=6

indicator("9:00-9:59 NY Range -> 10:00-11:00 Lines (v6)", overlay=true, max_lines_count=500)

// --- state vars ---

var float sessionHigh = na

var float sessionLow = na

var line hiLine = na

var line loLine = na

var line v10 = na

var line v11 = na

// --- New York time ---

t_ny = time("America/New_York")

hr = hour(t_ny)

mn = minute(t_ny)

// --- reset / clear at 16:00 (4 PM NY) ---

if hr == 16 and mn == 0

sessionHigh := na

sessionLow := na

if not na(hiLine)

line.delete(hiLine)

hiLine := na

if not na(loLine)

line.delete(loLine)

loLine := na

if not na(v10)

line.delete(v10)

v10 := na

if not na(v11)

line.delete(v11)

v11 := na

// --- accumulate 9:00 - 9:59 NY range ---

if hr == 9

if mn == 0

sessionHigh := high

sessionLow := low

else

sessionHigh := na(sessionHigh) ? high : math.max(sessionHigh, high)

sessionLow := na(sessionLow) ? low : math.min(sessionLow, low)

// --- at 10:00 NY: draw horizontal lines (start) and vertical dashed at 10:00 ---

if hr == 10 and mn == 0

// delete previous day's horizontal lines if any

if not na(hiLine)

line.delete(hiLine)

hiLine := na

if not na(loLine)

line.delete(loLine)

loLine := na

hiLine := line.new(bar_index, sessionHigh, bar_index, sessionHigh, color=color.red, width=1, extend=extend.none)

loLine := line.new(bar_index, sessionLow, bar_index, sessionLow, color=color.red, width=1, extend=extend.none)

if not na(v10)

line.delete(v10)

v10 := na

v10 := line.new(bar_index, low, bar_index, high, color=color.red, width=1, style=line.style_dashed)

// --- at 11:00 NY: draw vertical dashed at 11:00 ---

if hr == 11 and mn == 0

if not na(v11)

line.delete(v11)

v11 := na

v11 := line.new(bar_index, low, bar_index, high, color=color.red, width=1, style=line.style_dashed)

// --- extend the horizontal lines forward every bar, but only until 11:00 ---

if hr < 11

if not na(hiLine)

line.set_x2(hiLine, bar_index)

if not na(loLine)

line.set_x2(loLine, bar_index)

// --- required output so script compiles (hidden) ---

plot(na)

HH/HL/LH/LL - Bigger Letter MArkingAlam's Money

//@version=6

indicator("HH/HL/LH/LL - Clean Letters Only", overlay = true, max_labels_count = 500)

// Pivot confirmation bars (fixed)

L = 2

R = 2

// Confirmed pivots (appear R bars after turn)

sh = ta.pivothigh(high, L, R)

sl = ta.pivotlow(low, L, R)

// Keep last confirmed swing values

var float lastHigh = na

var float lastLow = na

// Swing highs → HH / LH

if not na(sh)

if na(lastHigh)

lastHigh := sh

else

string txtH = sh > lastHigh ? "HH" : "LH"

label.new(bar_index - R, sh, txtH, xloc.bar_index, yloc.price, color.new(color.white, 100), label.style_label_down, color.red, size.large)

lastHigh := sh

// Swing lows → HL / LL

if not na(sl)

if na(lastLow)

lastLow := sl

else

string txtL = sl > lastLow ? "HL" : "LL"

label.new(bar_index - R, sl, txtL, xloc.bar_index, yloc.price, color.new(color.white, 100), label.style_label_up, color.green, size.large)

lastLow := sl

Static Beta for Pair and Quant Trading A beta coefficient shows the volatility of an individual stock compared to the systematic risk of the entire market. Beta represents the slope of the line through a regression of data points. In finance, each point represents an individual stock's returns against the market.

Beta effectively describes the activity of a security's returns as it responds to swings in the market. It is used in the capital asset pricing model (CAPM), which describes the relationship between systematic risk and expected return for assets. CAPM is used to price risky securities and to estimate the expected returns of assets, considering the risk of those assets and the cost of capital.

Calculating Beta

A security's beta is calculated by dividing the product of the covariance of the security's returns and the market's returns by the variance of the market's returns over a specified period. The calculation helps investors understand whether a stock moves in the same direction as the rest of the market. It also provides insights into how volatile—or how risky—a stock is relative to the rest of the market.

For beta to provide useful insight, the market used as a benchmark should be related to the stock. For example, a bond ETF's beta with the S&P 500 as the benchmark would not be helpful to an investor because bonds and stocks are too dissimilar.

Beta Values

Beta equal to 1: A stock with a beta of 1.0 means its price activity correlates with the market. Adding a stock to a portfolio with a beta of 1.0 doesn’t add any risk to the portfolio, but it doesn’t increase the likelihood that the portfolio will provide an excess return.

Beta less than 1: A beta value less than 1.0 means the security is less volatile than the market. Including this stock in a portfolio makes it less risky than the same portfolio without the stock. Utility stocks often have low betas because they move more slowly than market averages.

Beta greater than 1: A beta greater than 1.0 indicates that the security's price is theoretically more volatile than the market. If a stock's beta is 1.2, it is assumed to be 20% more volatile than the market. Technology stocks tend to have higher betas than the market benchmark. Adding the stock to a portfolio will increase the portfolio’s risk, but may also increase its return.

Negative beta: A beta of -1.0 means that the stock is inversely correlated to the market benchmark on a 1:1 basis. Put options and inverse ETFs are designed to have negative betas. There are also a few industry groups, like gold miners, where a negative beta is common.

LET'S START

Now I'll give my own definition.

Beta:

If we assume market caps are equal ,

it is an indicator that shows how much of the second instrument we should buy if we buy one of the first, taking into account the price volatility of two instruments.

But if the market caps are not equal:

For example, the ETF for A is $300.

The ETF for B is $600.

If static beta predicted by this script is 0.5:

300 * 1 * a = 600 * 0.5 * b

Then we should use 1 b for 1 a.

(Long a and short b or vice versa )

So, we can try pair trading for a/b or a-b.

However, these values are generally close to each other, such as 0.8 and 0.93. However, the closer we can adjust our lot purchases to bring the double beta to a value closer to 1, the higher the hedge ratio will be.

Large commercials use dynamic betas, which are updated periodically, in addition to static betas

However, scaling this is very difficult for individual investors with limited investment tools.

But a static beta of 5,000 bars is still much better than not considering any beta at all.

Note: The presence of a beta value for two instruments does not necessarily mean they can be included in pair trading.

It is also important (%99) to consider historically very high correlations and cointegration relationships, as well as the compatibility of security structures.

Note 2 : This script is designed for low timeframes.

Do not use betas from different timeframes.

Beta dynamics are different for each timeframe.

Note 3 : I created this script with the help of ChatGPT.

Source for beta definition ( ) :

www.investopedia.com

Regards.

Relative Performance Areas [LuxAlgo]The Relative Performance Areas tool enables traders to analyze the relative performance of any asset against a user-selected benchmark directly on the chart, session by session.

The tool features three display modes for rescaled benchmark prices, as well as a statistics panel providing relevant information about overperforming and underperforming streaks.

🔶 USAGE

Usage is straightforward. Each session is highlighted with an area displaying the asset price range. By default, a green background is displayed when the asset outperforms the benchmark for the session. A red background is displayed if the asset underperforms the benchmark.

The benchmark is displayed as a green or red line. An extended price area is displayed when the benchmark exceeds the asset price and is set to SPX by default, but traders can choose any ticker from the settings panel.

Using benchmarks to compare performance is a common practice in trading and investing. Using indexes such as the S&P 500 (SPX) or the NASDAQ 100 (NDX) to measure our portfolio's performance provides a clear indication of whether our returns are above or below the broad market.

As the previous chart shows, if we have a long position in the NASDAQ 100 and buy an ETF like QQQ, we can clearly see how this position performs against BTSUSD and GOLD in each session.

Over the last 15 sessions, the NASDAQ 100 outperformed the BTSUSD in eight sessions and the GOLD in six sessions. Conversely, it underperformed the BTCUSD in seven sessions and the GOLD in nine sessions.

🔹 Display Mode

The display mode options in the Settings panel determine how benchmark performance is calculated. There are three display modes for the benchmark:

Net Returns: Uses the raw net returns of the benchmark from the start of the session.

Rescaled Returns: Uses the benchmark net returns multiplied by the ratio of the benchmark net returns standard deviation to the asset net returns standard deviation.

Standardized Returns: Uses the z-score of the benchmark returns multiplied by the standard deviation of the asset returns.

Comparing net returns between an asset and a benchmark provides traders with a broad view of relative performance and is straightforward.

When traders want a better comparison, they can use rescaled returns. This option scales the benchmark performance using the asset's volatility, providing a fairer comparison.

Standardized returns are the most sophisticated approach. They calculate the z-score of the benchmark returns to determine how many standard deviations they are from the mean. Then, they scale that number using the asset volatility, which is measured by the asset returns standard deviation.

As the chart above shows, different display modes produce different results. All of these methods are useful for making comparisons and accounting for different factors.

🔹 Dashboard

The statistics dashboard is a great addition that allows traders to gain a deep understanding of the relationship between assets and benchmarks.

First, we have raw data on overperforming and underperforming sessions. This shows how many sessions the asset performance at the end of the session was above or below the benchmark.

Next, we have the streaks statistics. We define a streak as two or more consecutive sessions where the asset overperformed or underperformed the benchmark.

Here, we have the number of winning and losing streaks (winning means overperforming and losing means underperforming), the median duration of each streak in sessions, the mode (the number of sessions that occurs most frequently), and the percentages of streaks with durations equal to or greater than three, four, five, and six sessions.

As the image shows, these statistics are useful for traders to better understand the relative behavior of different assets.

🔶 SETTINGS

Benchmark: Benchmark for comparison

Display Mode: Choose how to display the benchmark; Net Returns: Uses the raw net returns of the benchmark. Rescaled Returns: Uses the benchmark net returns multiplied by the ratio of the benchmark and asset standard deviations. Standardized Returns: Uses the benchmark z-score multiplied by the asset standard deviation.

🔹 Dashboard

Dashboard: Enable or disable the dashboard.

Position: Select the location of the dashboard.

Size: Select the dashboard size.

🔹 Style

Overperforming: Enable or disable displaying overperforming sessions and choose a color.

Underperforming: Enable or disable displaying underperforming sessions and choose a color.

Benchmark: Enable or disable displaying the benchmark and choose colors.

Bitcoin vs M2 Global Liquidity (Lead 3M) - Table Ticker═══════════════════════════════════════════════════════════════

Bitcoin vs M2 Global Liquidity - Regression Indicator

═══════════════════════════════════════════════════════════════

TECHNICAL SPECS

• Pine Script v6

• Overlay: false (separate pane)

• Data sources: 5 M2 series + 4 FX pairs (request.security)

• Calculation: Rolling OLS linear regression with configurable lead

• Output: Regression line + ±1σ/±2σ confidence bands + R² ticker

CORE FUNCTIONALITY

Aggregates M2 money supply from 5 central banks (CN, US, EU, JP, GB),

converts to USD, applies time-lead, runs rolling linear regression

vs Bitcoin price, plots predicted value with confidence intervals.

CONFIGURABLE PARAMETERS

Input Controls:

• Lead Period: 0-365 days (default: 90)

• Lookback Window: 50-2000 bars (default: 750)

• Bands: Toggle ±1σ and ±2σ visibility

• Colors: BTC, M2, regression line, confidence zones

• Ticker: Position, size, colors, transparency

Advanced Settings:

• Table display: R², lead, M2 total, country breakdown (%)

• Ticker customization: 9 position options, 6 text sizes

• Border: Width 0-10px, color, outline-only mode

DATA AGGREGATION

Sources (via request.security):

• ECONOMICS:CNM2, USM2, EUM2, JPM2, GBM2

• FX_IDC:CNYUSD, JPYUSD (others: FX:EURUSD, GBPUSD)

• Conversion: All M2 → USD → Sum / 1e12 (trillions)

REGRESSION ENGINE

• Arrays: m2Array, btcArray (dynamic sizing, auto-trim)

• Window: Rolling (lookbackPeriod bars)

• Lead: Time-shift via array indexing (i + leadPeriodDays)

• Calc: Manual OLS (covariance/variance), no built-in ta functions

• Outputs: slope, intercept, r2, stdResiduals

CONFIDENCE BANDS

±1σ and ±2σ calculated from standard deviation of residuals.

Fill zones between upper/lower bounds with configurable transparency.

ALERTS

5 pre-configured alertcondition():

• Divergence > 15%

• Price crosses ±1σ bands (up/down)

• Price crosses ±2σ bands (up/down)

TICKER TABLE

Dynamic table.new() with 9 rows:

• R² value (4 decimals)

• Lead period (days + months)

• M2 Global total (trillions USD)

• Country breakdown: CN, US, EU, JP, GB (absolute + %)

• Optional: Hide/show M2 details

VISUAL CUSTOMIZATION

All plot() elements support:

• Color picker inputs (group="Couleurs")

• Line width: 1-3px

• Transparency: 0-100% for zones

• Offset: M2 plot has +leadPeriodDays offset option

PERFORMANCE

• Max arrays size: lookbackPeriod + leadPeriodDays + 200

• Calculations: Only when array.size >= lookbackPeriod + leadPeriodDays

• Table update: barstate.islast (once per bar)

• Request.security: gaps_off mode

CODE STRUCTURE

1. Inputs (lines 7-54)

2. Data fetch (lines 56-76)

3. M2 aggregation (line 78)

4. Array management (lines 84-95)

5. Regression calc (lines 97-172)

6. Prediction + bands (lines 174-183)

7. Plots (lines 185-199)

8. Ticker table (lines 201-236)

9. Alerts (lines 238-246)

DEPENDENCIES

None. Pure Pine Script v6. No external libraries.

LIMITATIONS

• Daily timeframe recommended (1D)

• Requires 750+ bars history for optimal calculation

• M2 data availability: TradingView ECONOMICS feed

• Max lines: 500 (declared in indicator())

CUSTOMIZATION EXAMPLES

• Shorter lookback (200d): More reactive, lower R²

• Longer lookback (1500d): More stable, regime mixing

• No bands: Set showBands=false for clean view

• Different lead: Test 60d, 120d for sensitivity analysis

TECHNICAL NOTES

• Manual OLS implementation (no ta.linreg)

• Array-based lead application (not plot offset)

• M2 values stored in trillions (/ 1e12) for readability

• Residuals array cleared/rebuilt each calculation

OPEN SOURCE

Code fully visible. Modify, fork, analyze freely.

No hidden calculations. No proprietary data.

VERSION

1.0 | November 2025 | Pine Script v6

═══════════════════════════════════════════════════════════════

Match Finder [theUltimator5]Match Finder is the dating app of indicators. It takes your current ticker and finds the most compatible match over a recent time period. The match may not be Mr. right, but it is Mr. right now. It doesn't forecast future connection, but it tells you current compatibility for today.

Jokes aside, it is a pattern–comparison tool that was designed to find the ticker that tracks most closely to the one you are currently looking at. It scans a user-defined list of 40 tickers (pre-set to a bunch of liquid ETFs) and finds which one most closely matches the recent price action of the current chart over a fixed lookback window.

LOGIC BEHIND THE SCENES

For each bar, the script:

Takes the last N bars (Correlation Window Length) of the current symbol.

Takes the last N bars of each selected comparison ticker.

Calculates the Pearson correlation between the current symbol and each comparison ticker.

Identifies the single best-matching ticker (highest positive correlation, excluding the current symbol itself).

Rescales and overlays that matched segment on the chart so you can visually compare shapes.

Optionally shows a correlation table with all tickers and their correlation values.

The use case of this indicator is to help you see which symbol has recently moved most similarly to your current chart, and how that shape looks when overlaid in the same panel. It helps you see which sectors it may be following most closely to.

Here is an image with arrows showing the elements of this indicator that will be mostly explained later.

USER INPUTS

1. Correlation Window Length

Default: 30

Range: 10–500

This is the number of bars used to compare the current symbol against each ticker.

Important - Larger values produce more “global” shape comparison but increase computational load and may cause the indicator to timeout if the length is too long

2. Drawing Mode

Options:

Scale Only - Adjusts min and max of the plotted line segment to match the chart over the range

Scale & Rotate - Scales as above, but matches the first and last point to the close of the chart over the range. This effectively rotates the pattern to force it to track the chart to an extent.

3. Show Correlation Table

When enabled (disabled by default), shows a table in the bottom-right of the chart that displays the correlation values over the lookback range for all 40 tickers. The best fit ticker is highlighted.

4. Best Fit Line Color

Color used to draw the overlaid best-match segment (yellow by default).

5. Ticker inputs (1–40)

Default set to a broad universe of major ETFs (e.g., SPY, QQQ, IWM, sector and bond ETFs, commodities, etc.).

You can replace these with any symbols supported by your data feed (stocks, ETFs, indexes, etc.).

The script always excludes the current chart’s symbol from being considered as its own best match.

NOTE: THIS INDICATOR IS EXTREMELY MEMORY INTENSIVE AND MAY TAKE SEVERAL SECONDS TO LOAD. PLEASE BE PATIENT AND GIVE THE INDICATOR UP TO 20 SECONDS FOR THE DATA TO DISPLAY

Session Volume Profile - Open Source (DeadCat) Decided to make this Open Source so everyone can make edits.

Volume Profile is a charting study that displays trading activity over specific time periods at various price levels. It appears as a horizontal histogram on the chart, revealing where traders have shown the most interest based on volume concentration.

This Volume Profile automatically anchors to user-selected timeframes, creating fresh volume analysis for each new period while maintaining clean, systematic visualization of price-volume relationships.

Core Components:

Point of Control (POC): The price level with the highest volume activity during the selected period, marked with a yellow line and left-side label.

Value Area High/Low (VAH/VAL): Price boundaries that contain a specified percentage of the total volume (default 40%), helping identify the main trading range where most activity occurred.

Volume Histogram: Left-aligned bars showing volume distribution across price levels, with value area highlighting for enhanced visual clarity.

Key Features:

- Automatic Period Detection: Supports hourly, daily, weekly, and monthly timeframe anchoring

- Customizable Granularity: Adjustable rows (10-500) for different price resolution needs

- Labels: Clear POC, VAH, and VAL identification positioned at profile start

- Toggle Controls**: Optional display for volume rows, key levels, and background fills

- Clean Visualization: Profiles reset automatically at each new period for current market focus

Display Options:

- Profile Rows: Show/hide the volume histogram bars

- Key Level Lines: Individual controls for POC, VAH, and VAL display

- Value Area Background: Optional shading between VAH and VAL levels

- Color Customization: Separate color controls for all visual elements

The indicator provides systematic volume analysis by creating fresh profiles at regular intervals, helping traders identify significant price levels and volume patterns within their preferred timeframe structure.

Disclaimer: This indicator is for educational and informational purposes only. Trading decisions should be based on comprehensive analysis and proper risk management. Past performance does not guarantee future results.

Global M2 Money Supply Growth (GDP-Weighted)📊 Global M2 Money Supply Growth (GDP-Weighted)

This indicator tracks the weighted aggregate M2 money supply growth across the world's four largest economies: United States, China, Eurozone, and Japan. These economies represent approximately 69.3 trillion USD in combined GDP and account for the majority of global liquidity, making this a comprehensive macro indicator for analyzing worldwide monetary conditions.

════════════════════════════════════════════

🔧 KEY FEATURES:

📈 GDP-Weighted Aggregation

Each economy is weighted proportionally by its nominal GDP using 2025 IMF World Economic Outlook data:

• United States: 44.2% (30.62 trillion USD)

• China: 28.0% (19.40 trillion USD)

• Eurozone: 21.6% (15.0 trillion USD)

• Japan: 6.2% (4.28 trillion USD)

The weights are fully adjustable through the indicator settings, allowing you to update them annually as new IMF forecasts are released (typically April and October).

⏱️ Multiple Time Period Options

Choose between three calculation methods to analyze different timeframes:

• YoY (Year-over-Year): 12-month growth rate for identifying long-term liquidity trends and cycles

• MoM (Month-over-Month): 1-month growth rate for detecting short-term monetary policy shifts

• QoQ (Quarter-over-Quarter): 3-month growth rate for medium-term trend analysis

🔄 Advanced Offset Function

Shift the entire indicator forward by 0-365 days to test lead/lag relationships between global liquidity and asset prices. Research suggests a 56-70 day lag between M2 changes and Bitcoin price movements, but you can experiment with different offsets for various assets (equities, gold, commodities, etc.).

🌍 Individual Country Breakdown

Real-time display of each economy's M2 growth rate with:

• Current percentage change (YoY/MoM/QoQ)

• GDP weight contribution

• Color-coded values (green = monetary expansion, red = contraction)

📊 Smart Overlay Capability

Displays directly on your main price chart with an independent left-side scale, allowing you to visually correlate global liquidity trends with any asset's price action without cluttering the chart.

🔧 Customizable GDP Weights

All GDP values can be adjusted through the indicator settings without editing code, making annual updates simple and accessible for all users.

════════════════════════════════════════════

📡 DATA SOURCES:

All M2 money supply data is sourced from ECONOMICS (Trading Economics) for consistency and reliability:

• ECONOMICS:USM2 (United States)

• ECONOMICS:CNM2 (China)

• ECONOMICS:EUM2 (Eurozone)

• ECONOMICS:JPM2 (Japan)

All values are normalized to USD using current daily exchange rates (USDCNY, EURUSD, USDJPY) before GDP-weighted aggregation, ensuring accurate cross-country comparisons.

══════════════════════════════════════════════

💡 USE CASES & APPLICATIONS:

🔹 Liquidity Cycle Analysis

Track global monetary expansion/contraction cycles to identify when central banks are coordinating loose or tight monetary policies.

🔹 Market Timing & Risk Assessment

High M2 growth (>10%) historically correlates with risk-on environments and rising asset prices across crypto, equities, and commodities. Negative M2 growth signals monetary tightening and potential market corrections.

🔹 Bitcoin & Crypto Correlation

Compare with Bitcoin price using the offset feature to identify the optimal lag period. Many traders use 60-70 day offsets to predict crypto market movements based on liquidity changes.

🔹 Macro Portfolio Allocation

Use as a regime filter to adjust portfolio exposure: increase risk assets during liquidity expansion, reduce during contraction.

🔹 Central Bank Policy Divergence

Monitor individual country metrics to identify when major central banks are pursuing divergent policies (e.g., Fed tightening while China eases).

🔹 Inflation & Economic Forecasting

Rapid M2 growth often leads inflation by 12-18 months, making this a leading indicator for future inflation trends.

🔹 Recession Early Warning

Negative M2 growth is extremely rare and has preceded major recessions, making this a valuable risk management tool.

════════════════════════════════════════════

📊 INTERPRETATION GUIDE:

🟢 +10% or Higher

Aggressive monetary expansion, typically during crises (2001, 2008, 2020). The COVID-19 period saw M2 growth reach 20-27%, which preceded significant inflation and asset price surges. Strong bullish signal for risk assets.

🟢 +6% to +10%

Above-average liquidity growth. Central banks are providing stimulus beyond normal levels. Generally favorable for equities, crypto, and commodities.

🟡 +3% to +6%

Normal/healthy growth rate, roughly in line with GDP growth plus 2% inflation targets. Neutral environment with moderate support for risk assets.

🟠 0% to +3%

Slowing liquidity, potential tightening phase beginning. Central banks may be raising rates or reducing balance sheets. Caution warranted for high-beta assets.

🔴 Negative Growth

Monetary contraction - extremely rare. Only occurred during aggressive Fed tightening in 2022-2023. Strong warning signal for risk assets, often precedes recessions or major market corrections.

════════════════════════════════════════════

🎯 OPTIMAL USAGE:

📅 Recommended Timeframes:

• Daily or Weekly charts for macro analysis

• Monthly charts for very long-term trends

💹 Compatible Asset Classes:

• Cryptocurrencies (especially Bitcoin, Ethereum)

• Equity indices (S&P 500, NASDAQ, global markets)

• Commodities (Gold, Silver, Oil)

• Forex majors (DXY correlation analysis)

⚙️ Suggested Settings:

• Default: YoY calculation with 0 offset for current liquidity conditions

• Bitcoin traders: YoY with 60-70 day offset for predictive analysis

• Short-term traders: MoM with 0 offset for recent policy changes

• Quarterly rebalancers: QoQ with 0 offset for medium-term trends

════════════════════════════════════════════

📋 VISUAL DISPLAY:

The indicator plots a blue line showing the selected growth metric (YoY/MoM/QoQ), with a dashed reference line at 0% to clearly identify expansion vs. contraction regimes.

A comprehensive table in the top-right corner displays:

• Current global M2 growth rate (large, prominent display)

• Individual country breakdowns with their GDP weights

• Color-coded growth rates (green for positive, red for negative)

════════════════════════════════════════════

🔄 MAINTENANCE & UPDATES:

GDP weights should be updated annually (ideally in April or October) when the IMF releases new World Economic Outlook forecasts. Simply adjust the four GDP input parameters in the indicator settings - no code editing required.

The relative GDP proportions between the Big 4 economies change very gradually (typically <1-2% per year), so even if you update weights once every 1-2 years, the impact on the indicator's accuracy is minimal.

════════════════════════════════════════════

💭 TRADING PHILOSOPHY:

This indicator embodies the principle that "liquidity drives markets." By tracking the combined M2 money supply of the world's largest economies, weighted by their economic size, you gain insight into the fundamental liquidity conditions that underpin all asset prices.

Unlike single-country M2 indicators, this GDP-weighted approach captures the true global picture, accounting for the fact that US monetary policy has 2x the impact of Japanese policy due to economic size differences.

Perfect for macro-focused traders, long-term investors, and anyone seeking to understand the "tide that lifts all boats" in financial markets.

════════════════════════════════════════════

Created for traders and investors who incorporate global liquidity trends into their decision-making process. Best used alongside other technical and fundamental analysis tools for comprehensive market assessment.

⚠️ Disclaimer: M2 money supply is a lagging macroeconomic indicator. Past correlations do not guarantee future results. Always use proper risk management and combine with other analysis methods.

EMA Cross Strategy v5 (30 lots) (15 min candle only)- safe flip🚀 EMA Cross Strategy v5 (30 Lots) (15 min candle only)— Safe Flip Edition

Fully Automated | Fast | Reliable | Battle-tested

Welcome to a clean, powerful, and automation-friendly EMA crossover system.

This strategy is built for traders who want consistent trend-based entries without the risk of unwanted pyramiding or doubled positions.

🔥 How It Works

This strategy uses a fast EMA (10) crossing a slow EMA (20) to detect trend shifts:

Bullish Crossover → LONG (30 lots)

Bearish Crossover → SHORT (30 lots)

Every opposite signal safely flips the position by first closing the current trade, then opening a fresh position of exactly 30 lots.

No doubling.

No runaway position size.

No surprises.

Just clean, mechanical trend-following.

📈 Why This Strategy Stands Out

Unlike basic EMA crossbots, this version:

✔ Prevents unintended pyramiding

✔ Never over-allocates capital

✔ Works perfectly with webhook-based automation

✔ Produces stable, systematic entries

✔ Executes directional flips with precision

🔍 Backtest Highlights (1-Year)

(Backtests will vary by instrument/timeframe)

1,500+ trades executed

Profit factor above 1.27

Strong trend performance

Balanced long/short behavior

No margin calls

Consistent trade execution

This strategy thrives in trending markets and maintains strict discipline even in choppy conditions.

⚙️ Automation Ready

Designed for automated execution via webhook and API setups on supported platforms.

Just connect, run, and let the bot follow the rules without hesitation.

No emotions.

No overtrading.

No fear or greed.

Pure logic.

BS by bigmmBS by bigmm is a powerful tool designed to track and display cumulative trading volumes for bullish (green) and bearish (red) bars over a user-defined period. This indicator provides valuable insights into market sentiment by quantifying buying and selling pressure through volume analysis.

Adjustable lookback period from 20 to 10,000 bars

Default setting of 500 bars for balanced analysis

Real-time calculation updates on each new bar

BUY Volume: Total volume of green bars (close > open)

SELL Volume: Total volume of red bars (close < open)

Interpretation:

Higher BUY Volume: Indicates stronger buying pressure

Higher SELL Volume: Suggests stronger selling pressure

Balanced Volumes: Shows equilibrium between buyers and sellers

Ideal For:

Swing traders analyzing medium-term trends

Position traders evaluating long-term market sentiment

Volume-based trading strategies

Market structure analysis

🎯 Wyckoff Order Block Entry System🎯 Wyckoff Order Block Entry System

📝 INDICATOR DESCRIPTION

🎯 Wyckoff Order Block Entry System Short Description:

Professional institutional zone trading combined with Wyckoff methodology. Identifies high-probability entries where smart money meets classic price action patterns.

Full Description:

Wyckoff Order Block Entry System is a precision trading tool that combines two powerful concepts:

Order Blocks - Institutional zones where large players place their orders

Wyckoff Method - Classic price action patterns revealing smart money behavior

🎯 What Makes This Different?

Unlike traditional indicators that flood your chart with signals, this system only triggers entries when BOTH conditions are met:

Price enters an institutional Order Block zone (current timeframe OR higher timeframe)

A Wyckoff pattern occurs (Spring, SOS, Upthrust, or SOW)

This dual-confirmation approach ensures you're trading with institutional flow at optimal entry points.

📊 Key Features:

✅ Order Block Detection

Automatically identifies institutional buying/selling zones

Current timeframe order blocks (solid lines)

Higher timeframe order blocks (dashed lines) for stronger zones

Customizable strength and extension settings

✅ 4 Wyckoff Entry Patterns

SPRING (Bullish Reversal): Fake breakdown below support → Quick recovery

SOS (Sign of Strength): Strong bullish candle after accumulation

UPTHRUST (Bearish Reversal): Fake breakout above resistance → Quick rejection

SOW (Sign of Weakness): Strong bearish candle after distribution

✅ Clean Visual Design

Minimalist approach - only essential information

Color-coded zones (Green = Bullish, Red = Bearish, Cyan/Magenta = HTF)

Clear entry signals with pattern type labels

No chart clutter - focus on what matters

✅ Multi-Timeframe Analysis

Integrates higher timeframe order blocks

HTF signals marked with "+HTF" tag for extra confidence

Fully customizable HTF selection (H1, H4, Daily, etc.)

✅ Smart Alerts

Entry signal alerts (Long/Short)

Order block formation alerts

HTF order block alerts

Customizable alert messages

💡 How To Use:

Setup: Add indicator to your chart, configure HTF timeframe (default H1)

Wait: Let order blocks form (green/red boxes appear)

Watch: Price returns to order block zone

Entry: Signal appears when Wyckoff pattern confirms

Trade: Enter with the signal, stop below/above order block

📈 Best For:

Forex pairs (all majors and crosses)

Gold (XAUUSD)

Crypto (BTC, ETH, etc.)

Indices (SPX, NAS100, etc.)

Stocks

Commodities

⏱️ Recommended Timeframes:

M15 for scalping

M30 for day trading

H1 for swing trading

H4 for position trading

🎯 Win Rate Expectations:

Current TF signals: 60-70%

HTF signals (+HTF tag): 70-80%

Spring/Upthrust patterns: Highest probability

Works on ALL liquid markets

⚙️ Customizable Settings:

Order block detection parameters

HTF timeframe selection

Wyckoff sensitivity (swing length, volume threshold)

Zone extension duration

Color schemes

📚 Trading Strategy:

This indicator works best when:

Trading in the direction of higher timeframe trend

Using proper risk management (1-2% per trade)

Placing stops just outside order block zones

Taking profits at opposite order blocks

Focusing on HTF signals for higher quality

🔒 Risk Management:

Always use stop losses! Recommended placement:

LONG: 10-20 pips below order block

SHORT: 10-20 pips above order block

Target: Minimum 1:2 risk/reward ratio

💎 Why Traders Love This System:

"Finally, an indicator that doesn't spam my chart with useless signals!" - The quality-over-quantity approach means you only get high-probability setups.

"The HTF order blocks changed my trading!" - Multi-timeframe analysis built-in removes the need for manual higher timeframe checks.

"Wyckoff + Order Blocks = Perfect combination!" - Two proven concepts working together create powerful confluence.

📊 Universal Application:

This system works on ANY liquid market with sufficient volume:

✅ Forex (EUR/USD, GBP/USD, USD/JPY, etc.)

✅ Commodities (Gold, Silver, Oil, etc.)

✅ Indices (S&P 500, NASDAQ, DAX, etc.)

✅ Cryptocurrencies (Bitcoin, Ethereum, etc.)

✅ Stocks (Large cap with good liquidity)

🎓 Educational Value:

Beyond just signals, this indicator teaches you:

How institutional traders think

Where smart money places orders

Classic Wyckoff accumulation/distribution patterns

Multi-timeframe analysis techniques

⚡ Performance:

Lightning-fast calculations

No repainting

Real-time signal generation

Clean code, optimized for speed

🚀 Get Started:

Add to your favorite chart

Adjust HTF timeframe to match your trading style

Wait for high-quality signals

Trade with confidence

Remember: Quality beats quantity. This system prioritizes precision over frequency. You might see 2-5 signals per day on M30 - and that's exactly the point. Each signal is carefully filtered for maximum probability.

Ready to trade like institutions?

👉 Add this indicator to your chart now

👉 Configure your preferred HTF timeframe

👉 Start catching high-probability setups

👉 Trade smarter, not harder

Questions or feedback? Drop a comment below!

Found this useful? Hit that ⭐ button and share with fellow traders!

Happy Trading! 🚀📈

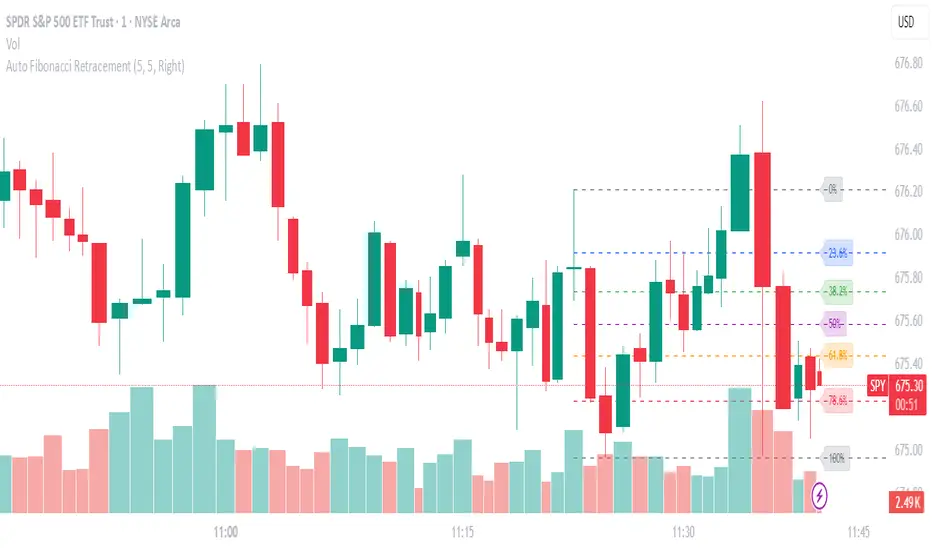

Auto Fibonacci RetraceNOTE: This script is for educational purposes only.

This Pine Script v6 indicator automates the drawing of Fibonacci retracement levels on a TradingView chart based on detected pivot highs and lows. It's designed to identify the most recent swing points in a price trend and plot horizontal lines at standard Fibonacci ratios (0%, 23.6%, 38.2%, 50%, 61.8%, 78.6%, 100%), along with optional labels for each level. The script is useful for traders who want dynamic, hands-free Fib retracements that update as new pivots form, helping to spot potential support/resistance zones without manual intervention.

Key Features

Automatic Pivot Detection: Uses TradingView's built-in ta.pivothigh and ta.pivotlow functions to find recent swing highs and lows. The sensitivity is adjustable via user inputs for "Left Bars" and "Right Bars" (default: 5 each), which define how many bars are checked on either side to confirm a pivot.

Trend Direction Awareness: Determines if the current swing is an uptrend (recent high after low) or downtrend (recent low after high) and orients the Fib levels accordingly—starting from the low in uptrends or high in downtrends.

Dynamic Drawing:

Plots dashed horizontal lines extending to the right of the chart for each Fib level.

Colors are predefined for visual distinction (e.g., blue for 23.6%, orange for 61.8%).

Lines and labels are cleared and redrawn only when a new pivot is detected or on initial load to prevent chart clutter.

Customizable Labels: Optional labels show the percentage (e.g., "61.8%") and can be positioned on the "Left" (at the swing start) or "Right" (pinned to the current bar, updating dynamically). Labels use semi-transparent backgrounds for readability.

Performance Optimizations: Uses arrays to manage lines and labels efficiently, with reverse-indexed loops for safe deletion. The max_bars_back=500 ensures it handles historical data without excessive computation.

User Inputs:

Left/Right Bars: Tune pivot detection (higher values for major trends, lower for shorter swings).

Show Fib Levels/Labels: Toggle visibility.

Label Position: "Left" or "Right" for placement flexibility.

Usage Instructions

Adding to Chart: Copy-paste into TradingView's Pine Editor, save as a new indicator, and add it to your chart via the "Indicators" menu.

Customization: Adjust inputs in the indicator settings panel. For example, set Left/Right Bars to 10 for daily charts in strong trends.

Best Practices:

Use on trending markets (e.g., stocks, forex, crypto like BTC/USD); avoid choppy sideways action.

Combine with other indicators (e.g., RSI for overbought/oversold confirmation) for better trade signals.

Test on historical data—zoom out to see how it redraws on past swings.

Limitations: Relies on pivot functions, so it may lag slightly (pivots confirm after "Right Bars"). Not a trading strategy—use for analysis only. No alerts built-in, but you can add alertcondition if extending it.

Potential Enhancements: Add extensions (e.g., 161.8%), user-defined levels, or alerts on price touches via simple modifications.

This script provides a clean, efficient way to visualize Fib retracements automatically, saving time compared to manual drawing. If you need further tweaks or integration into a full strategy, let me know!

EMA Cross + RSI + ADX - Autotrade Strategy V2Overview

A versatile trend-following strategy combining EMA 9/21 crossovers with RSI momentum filtering and optional ADX trend strength confirmation. Designed for both cryptocurrency and traditional futures/options markets with built-in stop loss management and automated position reversals.

Key Features

Multi-Market Compatibility: Works on both crypto futures (Bitcoin, Ethereum) and traditional markets (NIFTY, Bank NIFTY, S&P 500 futures, equity options)

Triple Confirmation System: EMA crossover + RSI filter + ADX strength (optional)

Automated Risk Management: 2% stop loss with wick-touch detection

Position Auto-Reversal: Opposite signals automatically close and reverse positions

Webhook Ready: Six distinct alert messages for automation (Entry Buy/Sell, Close Long/Short, SL Hit Long/Short)

Performance Metrics

NIFTY Futures (15min): 50%+ win rate with ADX filter OFF

Crypto Markets: Requires extensive backtesting before live deployment

Optimal Timeframes: 15-minute to 1-hour charts (patience required for higher timeframes)

Strategy Logic

Entry Signals:

LONG: EMA 9 crosses above EMA 21 + RSI > 55 + ADX > 20 (if enabled)

SHORT: EMA 9 crosses below EMA 21 + RSI < 45 + ADX > 20 (if enabled)

Exit Signals:

Opposite EMA crossover (auto-closes current position)

Stop loss hit at 2% from entry price (tracks candle wicks)

Technical Indicators:

Fast EMA: 9-period (short-term trend)

Slow EMA: 21-period (primary trend)

RSI: 14-period with 55/45 thresholds (momentum confirmation)

ADX: 14-period with 20 threshold (trend strength filter - optional)

Market-Specific Settings

Traditional Markets (NIFTY, Bank NIFTY, S&P Futures, Options)

Recommended Settings:

ADX Filter: Turn OFF (less choppy, cleaner trends)

Timeframe: 15-minute chart

Win Rate: 50%+ on NIFTY Futures

Why No ADX: Traditional markets have more institutional participation and smoother price action, making ADX unnecessary

Cryptocurrency Markets (BTC, ETH, Altcoins)

Recommended Settings:

ADX Filter: Turn ON (ADX > 20)

Timeframe: 15-minute to 1-hour

Extensive backtesting required before live trading

Why ADX: Crypto markets are highly volatile and prone to false breakouts; ADX filters low-quality chop

Best Practices

✅ Backtest thoroughly on your specific instrument and timeframe

✅ Use larger timeframes (1H, 4H) for higher quality signals and better risk/reward

✅ Adjust RSI thresholds based on market volatility (try 52/48 for more signals, 60/40 for fewer but stronger)

✅ Monitor ADX effectiveness - disable for traditional markets, enable for crypto

✅ Proper position sizing - adjust default_qty_value based on your capital and instrument price

✅ Paper trade first - test for 2-4 weeks before risking real capital

Risk Management

Fixed 2% stop loss per trade (adjustable)

Stop loss tracks candle wicks for accurate execution

Positions auto-reverse on opposite signals (no manual intervention needed)

0.075% commission built into backtest (adjust for your broker)

Customization Options

All parameters are adjustable via inputs:

EMA periods (default: 9/21)

RSI length and thresholds (default: 14-period, 55/45 levels)

ADX length and threshold (default: 14-period, 20 threshold)

Stop loss percentage (default: 2%)

Webhook Automation

This strategy includes six distinct alert messages for automated trading:

"Entry Buy" - Long position opened

"Entry Sell" - Short position opened

"Close Long" - Long position closed on opposite crossover

"Close Short" - Short position closed on opposite crossover

"SL Hit Long" - Long stop loss triggered

"SL Hit Short" - Short stop loss triggered

Compatible with Delta Exchange, Binance Futures, 3Commas, Alertatron, and other webhook platforms.

Important Notes

⚠️ Crypto markets require extensive backtesting - volatility patterns differ significantly from traditional markets

⚠️ Higher timeframes = better results - 15min works but 1H/4H provide cleaner signals

⚠️ ADX toggle is critical - OFF for traditional markets, ON for crypto

⚠️ Not financial advice - always conduct your own research and use proper risk management

⚠️ Past performance ≠ future results - backtest results may not reflect live trading conditions

Disclaimer

This strategy is for educational and informational purposes only. Trading futures and options involves substantial risk of loss. Always backtest thoroughly, start with paper trading, and never risk more than you can afford to lose. The author assumes no responsibility for any trading losses incurred using this strategy.

FVG ATRFVG ATR — Fair Value Gap Size Measured in ATR Units

This Pine Script v6 indicator detects Fair Value Gaps and displays their size as a ratio of the Average True Range, providing traders with a normalized measurement of gap significance across different market conditions and timeframes.

Key Features

Automatic FVG Detection

The indicator identifies bullish and bearish Fair Value Gaps using the standard three-candle pattern. Bullish FVGs occur when the current low exceeds the high from two bars ago, while bearish FVGs occur when the current high falls below the low from two bars ago.

ATR Ratio Calculation

Each detected FVG is measured against the current Average True Range at the moment of detection. The ratio is displayed as a compact label next to the gap, showing values like "ATR: 0.75" or "ATR: 1.41". This normalization allows comparison of gap significance across volatile and calm market periods.

Minimal Visual Footprint

Labels are displayed directly on the chart without boxes or lines, using customizable text sizes from tiny to large. The default tiny size ensures the chart remains uncluttered while providing essential information at a glance.

Highly Customizable Display

All visual aspects are configurable through input parameters, including label position (top, middle, or bottom of gap), text size, text color, optional background, and horizontal offset from the detection candle.

Customizable Parameters

Detection Settings

Detect Bullish FVG: Enable or disable detection of bullish gaps. Default is enabled.

Detect Bearish FVG: Enable or disable detection of bearish gaps. Default is enabled.

Min Size (pips): Filter out small gaps below the specified threshold. One pip equals 10 ticks for most Forex pairs. Default is 10 pips.

ATR Calculation

ATR Period: Period length for Average True Range calculation. Default is 14, adjustable to match your trading strategy.

Label Settings

Label Position: Vertical placement of the text label relative to the FVG zone. Options are Top, Middle, or Bottom. Default is Middle.

Label Size: Text size from Tiny (smallest), Small, Normal, to Large. Default is Tiny for minimal chart clutter.

Text Color: Custom color for label text. Default is white for visibility on dark themes.

Show Background: Toggle to display labels with a colored background box or as transparent text only. Default is disabled for cleaner appearance.

Background Color: Custom color for label background when enabled. Default is semi-transparent gray.

Label Offset (bars): Horizontal distance in bars between the detection candle and the label. Set to 0 for labels directly on the candle, or increase for separation. Default is 0.

Recommended Use Cases

Multi-Timeframe Analysis

Compare FVG significance across different timeframes by observing ATR ratios. A 1.5 ATR gap on the 1-hour chart may indicate different significance than the same ratio on the daily chart.

Volatility-Adjusted Trading

Use ATR ratios to filter for only the most significant gaps. For example, only trade FVGs with ratios above 1.0 to focus on gaps larger than typical price movement.

Risk Management

Size positions based on gap magnitude relative to current volatility. Larger ATR ratios may warrant tighter stops or smaller position sizes.

Market Efficiency Analysis

Track how quickly and completely different-sized gaps get filled. Gaps with higher ATR ratios may take longer to fill or act as stronger support and resistance zones.

Technical Details

This indicator is written in Pine Script v6 and follows all recommended coding standards including strict 4-space indentation, lazy boolean evaluation, and proper type declarations. The script uses array-based storage to maintain up to 500 labels simultaneously.

The ATR ratio is calculated at the moment of FVG detection and remains fixed, never repainting. The calculation divides the FVG height (distance between gap boundaries) by the current ATR value using the specified period. Division by zero is protected with conditional logic.

Label positioning uses the xloc.bar_index and yloc.price system for precise placement. The horizontal offset parameter allows traders to adjust label spacing based on chart zoom level and personal preference. Text formatting uses str.tostring with two decimal places for clear ratio display.

Important Notes

The indicator never repaints as all FVG detections and ATR calculations are fixed upon bar confirmation. Labels persist on the chart until the maximum label count is reached, at which point the oldest labels are automatically removed by TradingView.

For optimal performance on charts with many FVGs, consider increasing the minimum pip size filter or using smaller label sizes. The tiny size option provides the smallest possible text for maximum chart clarity.

Installation and Usage

Copy the source code into the TradingView Pine Editor and add the indicator to your chart. The overlay parameter is set to true, allowing labels to display directly on price candles. Configure all parameters through the indicator settings panel to match your trading style and visual preferences.

100% Pine Script v6 indicator — No repaint — Open source

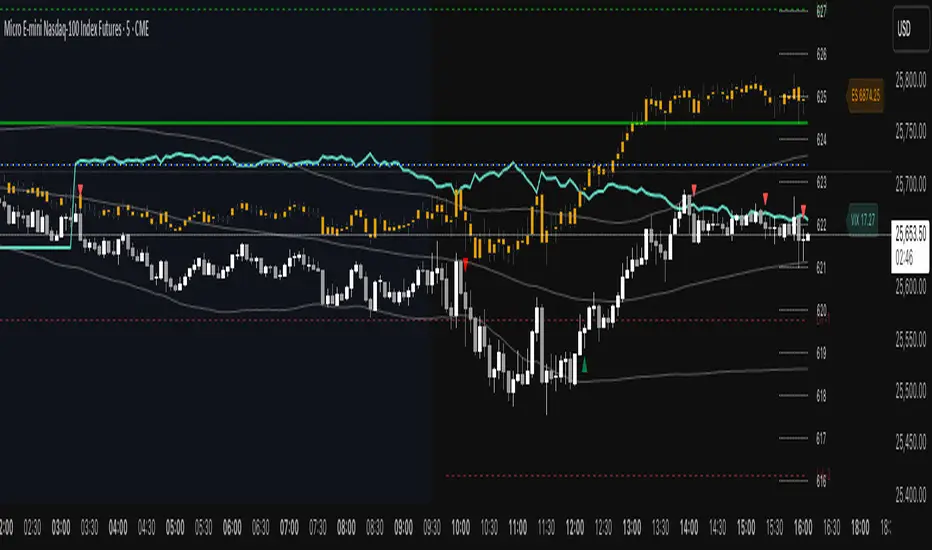

ES VIX on MNQ🧭 ES + VIX Overlay on MNQ

This indicator overlays the ES (S&P 500 futures) and VIX (Volatility Index) directly on the MNQ (Micro Nasdaq Futures) chart, allowing traders to visualize in real time the correlation, divergence, and volatility influence between the three instruments.

⸻

⚙️ How It Works

• The VIX is dynamically rescaled to the MNQ’s daily open, so its moves appear on the same price scale.

• The ES line is projected based on its percentage move relative to the session open (18:00 NY).

• Both are plotted in sync with MNQ to expose relative strength and divergence zones that often precede strong directional moves.

⸻

🧩 Inputs

• VIX Symbol: choose between VIX, CBOE:VIX, TVC:VIX

• Invert VIX Correlation: flips the VIX line for inverse-correlation setups

• VIX Step: controls how sensitively the VIX moves on the MNQ scale

• ES Symbol: defines the ES contract (e.g. ES1!)

• Show Signals: toggles on/off buy & sell markers

• Step (points): minimum distance between MNQ and VIX for a valid signal

• Block Signals: disables signals between 16:15 – 03:15 (illiquid hours)

⸻

💡 Signal Logic

The system tracks crossings between MNQ and the projected VIX line:

• Buy signal → when MNQ crosses above the VIX and expands upward by ≥ X points.

• Sell signal → when MNQ crosses below the VIX and expands downward by ≥ X points.

A time filter avoids noise during low-volume sessions.

⸻

📊 Visual Guide

• Cyan line = VIX on MNQ scale

• Orange line = ES on MNQ scale

• Labels on the right = current VIX / ES values

• BUY/SELL markers = potential volatility-based reversals

⸻

🚀 Practical Use

Perfect for traders who monitor:

• VIX–price divergence

• ES vs MNQ momentum confirmation

• Early volatility expansions before trend moves

⸻

💬 Core Idea:

“Volatility leads — price confirms.”

QQQ TimingThis is a trend-following position trading strategy designed for the QQQ and the leveraged ETF QLD (ProShares Ultra QQQ). The primary goal is to capture multi-month holds for maximal profit.

Key Instruments & Performance

The strategy performs best with QLD, which yields far superior results compared to QQQ.

TQQQ (triple-leveraged) results in higher drawdowns and is not the optimal choice.

Important: The system is not intended for use with other indexes, individual stocks, or investments (like crypto or gold), as performance can vary widely.

Buy Signals

The strategy's signals are rooted in the S&P 500 Index (SPX), as testing showed it provides more reliable triggers than using QQQ itself.

Primary Buy Signal (Credit to IBD/Mike Webster): The SPX triggers a buy when its low closes above the 21-day Exponential Moving Average (EMA) for three consecutive days.

Refinement with Downtrend Lines: During corrective or bear periods, results and drawdowns can be significantly improved by incorporating downtrend lines. These lines connect lower highs. The strategy waits for the price to close above a drawn downtrend line before executing a buy. This refinement can modify the primary signal, either by allowing for an earlier entry or, in some cases, completely nullifying a false signal until the trend change proves itself.

Risk Management & Exit Strategy

Initial Buy Risk: A 3.7% stop loss is applied immediately upon the initial entry.

Initial Exit Rule: An exit is required if the QQQ's low drops below the 50-day Simple Moving Average (SMA).

Note: The 3.7% stop often provides protection when the initial buy occurs below the 50-day SMA. However, if QQQ is already trading above its 50-day SMA at the time of the SPX signal (indicating relative strength), historically, it has been better to use the 50-day SMA rule to give the position more room to run.

Trend Exit (Profit-Taking): To stay in a strong trend for the optimal amount of time, the long position is exited when a moving average crossover to the downside is triggered, based around the 107-day Simple Moving Average (SMA).

Anchored ATH Drawdown LevelsThe Anchored ATH Drawdown Levels plots horizontal lines from a chosen anchor price (ATH), showing potential pullback zones at set percentage drops below it.

This indicator's use lies in its anchored ATH framework, which rapidly visualizes precise drawdown levels as dynamic levels of interest or price targets enabling traders to anticipate pullback depths and potential reversal levels without manual calculations.

Pick "True ATH" for the all-time high or "Period ATH" for anchored highs reset weekly, monthly, or quarterly. Lines stretch right for a cleaner visual.

Key Features

Anchoring: True ATH (lifetime max) or Period ATH (resets on 1W/1M/3M intervals).

Drawdown Levels: 8 adjustable levels (defaults: -5%, -10%, -15%, -20% on; -25% to -50% off). Toggle each, set drop % (0.1-99.9), pick color, style (solid/dashed/dotted), width (1-3).

ATH Line: Optional ATH line with custom color, style, width.

Unified Look: Global overrides for all levels' color, style, width.

Labels: Show % drops (with/without prices) via text boxes or full tags; sizes from tiny to large.

Projection: Lines extend 5-100 bars right (default 20).

Settings

Anchor: Mode and timeframe.

Display: Toggle levels/ATH, set extension.

Labels: Style (text/full/none), size, price display.

Global/ATH/Levels: Colors, styles, widths (per-level or shared).

How to Use

Load on chart (overlays prices; handles up to 500 lines).

Choose anchor for your high.

Tune levels for key pullbacks (e.g., -5% minor, -20% major).

Customize visuals where the lines update on new peaks.

Relative Strength vs Benchmark SPYRelative Strength vs Benchmark (SPY)

This indicator compares the performance of the charted symbol (stock or ETF) against a benchmark index — by default, SPY (S&P 500). It plots a Relative Strength (RS) ratio line (Symbol / SPY) and its EMA(50) to visualize when the asset is outperforming or underperforming the market.

Key Features

📈 RS Line (blue): Shows how the asset performs relative to SPY.

🟠 EMA(50): Smooths the RS trend to highlight sustained leadership.

🟩 Green background: Symbol is outperforming SPY (RS > EMA).

🟥 Red background: Symbol is underperforming SPY (RS < EMA).

🔔 Alerts: Automatic notifications when RS crosses above/below its EMA — signaling new leadership or weakness.

How to Use

Apply to any stock or ETF chart.

Keep benchmark = SPY, or switch to another index (e.g., QQQ, IWM, XLK).

Watch for RS crossovers and trends:

Rising RS → money flowing into the asset.

Falling RS → rotation away from the asset.

Perfect for sector rotation, ETF comparison, and momentum analysis workflows.

Ben's BTC Macro Fair Value OscillatorBen's BTC Macro Fair Value Oscillator

Overview

The **BTC Macro Fair Value Oscillator** is a non-crypto fair value framework that uses macro asset relationships (equities, dollar, gold) to estimate Bitcoin's "macro-driven fair value" and identify mean-reversion opportunities.

"Is BTC cheap or expensive right now?" on the 4 Hour Timeframe ONLY

### Key Features

✅ **Macro-driven**: Uses QQQ, DXY, XAUUSD instead of on-chain or crypto metrics

✅ **Dynamic weighting**: Assets weighted by rolling correlation strength

✅ **Mean-reversion signals**: Identifies when BTC is cheap/expensive vs macro

✅ **Validated parameters**: Optimized through 5-year backtest (Sharpe 6.7-9.9)

✅ **Visual transparency**: Live correlation panel, fair value bands, statistics

✅ **Non-repainting**: All calculations use confirmed historical data only

### What This Indicator Does

- Builds a **synthetic macro composite** from traditional assets

- Runs a **rolling regression** to predict BTC price from macro

- Calculates **deviation z-score** (how far BTC is from macro fair value)

- Generates **entry signals** when BTC is extremely cheap vs macro (dev < -2)

- Generates **exit signals** when BTC returns to fair value (dev > 0)

### What This Indicator Is NOT

❌ Not a high-frequency trading system (sparse signals by design)

❌ Not optimized for absolute returns (optimized for Sharpe ratio)

❌ Not suitable as standalone trading system (best as overlay/confirmation)

❌ Not predictive of short-term price movements (mean-reversion timeframe: days to weeks)

---

## Core Concept

### The Premise

Bitcoin doesn't trade in a vacuum. It's influenced by:

- **Risk appetite** (equities: QQQ, SPX)

- **Dollar strength** (DXY - inverse to risk assets)

- **Safe haven flows** (Gold: XAUUSD)

When macro conditions are "good for BTC" (risk-on, weak dollar, strong equities), BTC should trade higher. When macro conditions turn against it, BTC should trade lower.

### The Innovation

Instead of looking at BTC in isolation, this indicator:

1. **Measures how strongly** BTC currently correlates with each macro asset

2. **Builds a weighted composite** of those macro returns (the "D" driver)

3. **Regresses BTC price on D** to estimate "macro fair value"

4. **Tracks the deviation** between actual price and fair value

5. **Signals mean reversion** when deviation becomes extreme

### The Edge

The validated edge comes from:

- **Extreme deviations predict future returns** (dev < -2 → +1.67% over 12 bars)

- **Monotonic relationship** (more negative dev → higher forward returns)

- **Works out-of-sample** (test Sharpe +83-87% better than training)

- **Low correlation with buy & hold** (provides diversification value)

---

## Methodology

### Step 1: Macro Composite Driver D(t)

The indicator builds a weighted composite of macro asset returns:

**Process:**

1. Calculate **log returns** for BTC and each macro reference (QQQ, DXY, XAUUSD)

2. Compute **rolling correlation** between BTC and each reference over `corrLen` bars

3. **Weight each asset** by `|correlation|` if above `minCorrAbs` threshold, else 0

4. **Sign-adjust** weights (+1 for positive corr, -1 for negative) to handle inverse relationships

5. **Z-score normalize** each reference's returns over `fvWindow`

6. **Composite D(t)** = weighted sum of sign-adjusted z-scores

**Formula:**

```

For each reference i:

corr_i = correlation(BTC_returns, ref_i_returns, corrLen)

weight_i = |corr_i| if |corr_i| >= minCorrAbs else 0

sign_i = +1 if corr_i >= 0 else -1

z_i = (ref_i_returns - mean) / std

contrib_i = sign_i * z_i * weight_i

D(t) = sum(contrib_i) / sum(weight_i)

```

**Key Insight:** D(t) represents "how good macro conditions are for BTC right now" in a normalized, correlation-weighted way.

---

### Step 2: Fair Value Regression

Uses rolling linear regression to predict BTC price from D(t):

**Model:**

```

BTC_price(t) = α + β * D(t)

```

**Calculation (Pine Script approach):**

```

corr_CD = correlation(BTC_price, D, fvWindow)

sd_price = stdev(BTC_price, fvWindow)

sd_D = stdev(D, fvWindow)

cov = corr_CD * sd_price * sd_D

var_D = variance(D, fvWindow)

β = cov / var_D

α = mean(BTC_price) - β * mean(D)

fair_value(t) = α + β * D(t)

```

**Result:** A time-varying "macro fair value" line that adapts as correlations change.

---

### Step 3: Deviation Oscillator

Measures how far BTC price has deviated from fair value:

**Calculation:**

```

residual(t) = BTC_price(t) - fair_value(t)

residual_std = stdev(residual, normWindow)

deviation(t) = residual(t) / residual_std

```

**Interpretation:**

- `dev = 0` → BTC at fair value

- `dev = -2` → BTC is 2 standard deviations **cheap** vs macro

- `dev = +2` → BTC is 2 standard deviations **rich** vs macro

---

### Step 4: Signal Generation

**Long Entry:** `dev` crosses below `-2.0` (BTC extremely cheap vs macro)

**Long Exit:** `dev` crosses above `0.0` (BTC returns to fair value)

**No shorting** in default config (risk management choice - crypto volatility)

---

## How It Works

### Visual Components

#### 1. Price Chart (Main Panel)

**Fair Value Line (Orange):**

- The estimated "macro-driven fair value" for BTC

- Calculated from rolling regression on macro composite

**Fair Value Bands:**

- **±1σ** (light): 68% confidence zone

- **±2σ** (medium): 95% confidence zone

- **±3σ** (dark, dots): 99.7% confidence zone

**Entry/Exit Markers:**

- **Green "LONG" label** below bar: Entry signal (dev < -2)

- **Red "EXIT" label** above bar: Exit signal (dev > 0)

#### 2. Deviation Oscillator (Separate Pane)

**Line plot:**

- Shows current deviation z-score

- **Green** when dev < -2 (cheap)

- **Red** when dev > +2 (rich)

- **Gray** when neutral

**Histogram:**

- Visual representation of deviation magnitude

- Green bars = negative deviation (cheap)

- Red bars = positive deviation (rich)

**Threshold lines:**

- **Green dashed at -2.0**: Entry threshold

- **Red dashed at 0.0**: Exit threshold

- **Gray solid at 0**: Fair value line

#### 3. Correlation Panel (Top-Right)

Shows live correlation and weighting for each macro asset:

| Asset | Corr | Weight |

|-------|------|--------|

| QQQ | +0.45 | 0.45 |

| DXY | -0.32 | 0.32 |

| XAUUSD | +0.15 | 0.00 |

| Avg \|Corr\| | 0.31 | 0.77 |

**Reading:**

- **Corr**: Current rolling correlation with BTC (-1 to +1)

- **Weight**: How much this asset contributes to fair value (0 = excluded)

- **Avg |Corr|**: Average correlation strength (should be > 0.2 for reliable signals)

**Colors:**

- Green/Red corr = positive/negative correlation

- White weight = asset included, Gray = excluded (below minCorrAbs)

#### 4. Statistics Label (Bottom-Right)

```

━━━ BTC Macro FV ━━━

Dev: -2.34

Price: $103,192

FV: $110,500

Status: CHEAP ⬇

β: 103.52

```

**Fields:**

- **Dev**: Current deviation z-score

- **Price**: Current BTC close price

- **FV**: Current macro fair value estimate

- **Status**: CHEAP (< -2), RICH (> +2), or FAIR

- **β**: Current regression beta (sensitivity to macro)

---

## Installation & Setup

### TradingView Setup

1. Open TradingView and navigate to any **BTC chart** (BTCUSD, BTCUSDT, etc.)

2. Open **Pine Editor** (bottom panel)

3. Click **"+ New"** → **"Blank indicator"**

4. **Delete** all default code

5. **Copy** the entire Pine Script from `GHPT_optimized.pine`

6. **Paste** into the editor

7. Click **"Save"** and name it "BTC Macro Fair Value Oscillator"

8. Click **"Add to Chart"**

### Recommended Chart Settings

**Timeframe:** 4h (validated timeframe)

**Chart Type:** Candlestick or Heikin Ashi

**Overlay:** Yes (indicator plots on price chart + separate pane)

**Alternative Timeframes:**

- Daily: Works but slower signals

- 1h-2h: May work but not validated

- < 1h: Not recommended (too noisy)

### Symbol Requirements

**Primary:** BTC/USD or BTC/USDT on any exchange

**Macro References:** Automatically fetched

- QQQ (Nasdaq 100 ETF)

- DXY (US Dollar Index)

- XAUUSD (Gold spot)

**Data Requirements:**

- At least **90 bars** of history (warmup period)

- Premium TradingView recommended for full historical data

---

## Reading the Indicator

### Identifying Signals

#### Strong Long Signal (High Conviction)

- ✅ Deviation < -2.0 (extreme undervaluation)

- ✅ Avg |Corr| > 0.3 (strong macro relationships)

- ✅ Price touching or below -2σ band

- ✅ "LONG" label appears below bar

**Interpretation:** BTC is extremely cheap relative to macro conditions. Historical data shows +1.67% average return over next 12 bars (48 hours at 4h timeframe).

#### Moderate Long Signal (Lower Conviction)

- ⚠️ Deviation between -1.5 and -2.0

- ⚠️ Avg |Corr| between 0.2-0.3

- ⚠️ Price approaching -2σ band

**Interpretation:** BTC is cheap but not extreme. Consider as confirmation for other signals.

#### Exit Signal

- 🔴 Deviation crosses above 0 (returns to fair value)

- 🔴 "EXIT" label appears above bar

**Interpretation:** Mean reversion complete. Close long positions.

#### Strong Short/Avoid Signal

- 🔴 Deviation > +2.0 (extreme overvaluation)

- 🔴 Avg |Corr| > 0.3

- 🔴 Price touching or above +2σ band

**Interpretation:** BTC is expensive vs macro. Historical data shows -1.79% average return over next 12 bars. Consider exiting longs or reducing exposure.

### Regime Detection

**Strong Regime (Reliable Signals):**

- Avg |Corr| > 0.3

- Multiple assets weighted > 0

- Fair value line tracking price reasonably well

**Weak Regime (Unreliable Signals):**

- Avg |Corr| < 0.2

- Most weights = 0 (grayed out)

- Fair value line diverging wildly from price

- **Action:** Ignore signals until correlations strengthen

ROC & Momentum FusionROC & Momentum Fusion

(by HabibiTrades ©)

Purpose:

“ROC & Momentum Fusion” combines the Rate of Change (ROC) with a MACD-style signal engine to identify early momentum reversals, confirmed trend shifts, and low-volatility choppy zones.

It’s built for traders who want early momentum detection with the clarity of trend persistence — adaptable to any instrument and timeframe.

⚙️ How It Works

Rate of Change (ROC):

Measures the percentage speed of price change over time, showing the raw momentum strength.

Signal Line (EMA):

A short EMA of the ROC — responds faster to new directional shifts, similar to a MACD signal line.

Histogram:

Displays acceleration and deceleration between the ROC and its signal line.

Persistent Trend States:

When the ROC crosses the signal line or zero, the indicator enters a new momentum regime

(bullish or bearish) and stays in that color until another flip occurs.

Dynamic Choppy Zone:

When ROC momentum fades within the zero buffer zone, the indicator turns orange, signaling a sideways or indecisive market.

🟢 Visual Regimes

Regime Description Color

Bullish Momentum ROC above zero or signal line 🟢 Neon Green

Bearish Momentum ROC below zero or signal line 🔴 Neon Red

Choppy / Neutral ROC hovering within ±threshold range 🟠 Neon Orange

This color system makes it visually effortless to see whether the market is trending, reversing, or consolidating.

🧭 Adaptive Intelligence

The script automatically adjusts to market type and session for consistent accuracy:

Session Adaptive: Adjusts smoothing based on global sessions (Asian, London, New York, Sydney).

Instrument Adaptive: Fine-tunes sensitivity automatically for major assets — NASDAQ (NQ), S&P 500 (ES), Gold (GC), Oil (CL), Bitcoin (BTC).

Volatility Normalization: Optionally divides ROC by its own standard deviation to stabilize noisy assets and maintain consistent scaling.

🔔 Signals & Alerts

Bullish Reversal:

ROC crosses above its signal or zero line — early momentum flip.

Bearish Reversal:

ROC crosses below its signal or zero line — downward momentum flip.

Alerts:

Both reversal conditions include built-in alert triggers for automation and notifications.

🎨 Visual Features

Main ROC Line: Adaptive EMA of ROC, color-coded by trend regime.

Signal Line: Optional white EMA overlay for MACD-style crossovers.

Histogram: Visual burst display of acceleration (green/red).

Reversal Markers: Optional triangles marking exact crossover points.

Threshold Lines: Highlight the zero and buffer zones for visual clarity.

🧩 Best Use Cases

Identify early momentum shifts before price confirms them.

Confirm trend continuation or exhaustion with color persistence.

Detect choppy / low-volatility periods instantly.