EMA/VWAP SuiteEMA/VWAP Suite

Overview

The EMA/VWAP Suite is a versatile and customizable Pine Script indicator designed for traders who want to combine Exponential Moving Averages (EMAs) and Volume Weighted Average Prices (VWAPs) in a single, powerful tool. It overlays up to eight EMAs and six VWAPs (three anchored, three rolling) on the chart, each with percentage difference labels to show how far the current price is from these key levels. This indicator is perfect for technical analysis, supporting strategies like trend following, mean reversion, and VWAP-based trading.

By default, the indicator displays eight EMAs and a session-anchored VWAP (AVWAP 1, in fuchsia) with their respective percentage difference labels, keeping the chart clean yet informative. Other VWAPs and their bands are disabled by default but can be enabled and customized as needed. The suite is designed to minimize clutter while providing maximum flexibility for traders.

Features

- Eight Customizable EMAs: Plot up to eight EMAs with user-defined lengths (default: 3, 9, 19, 38, 50, 65, 100, 200), each with a unique color for easy identification.

- EMA Percentage Difference Labels: Show the percentage difference between the current price and each EMA, displayed only for visible EMAs when enabled.

- Three Anchored VWAPs: Plot VWAPs anchored to the start of a session, week, or month, with customizable source, offset, and band multipliers. AVWAP 1 (session-anchored, fuchsia) is enabled by default.

- Three Rolling VWAPs: Plot VWAPs calculated over fixed periods (default: 20, 50, 100), with customizable source, offset, and band multipliers.

- VWAP Bands: Optional upper and lower bands for each VWAP, based on standard deviation with user-defined multipliers.

- VWAP Percentage Difference Labels: Display the percentage difference between the current price and each VWAP, shown only for visible VWAPs. Enabled by default to show the AVWAP 1 label.

- Customizable Colors: Each VWAP has a user-defined color via input settings, with labels matching the VWAP line colors (e.g., AVWAP 1 defaults to fuchsia).

Flexible Display Options: Toggle individual EMAs, VWAPs, bands, and labels on or off to reduce chart clutter.

Settings

The indicator is organized into intuitive setting groups:

EMA Settings

Show EMA 1–8 : Toggle each EMA on or off (default: all enabled).

EMA 1–8 Length : Set the period for each EMA (default: 3, 9, 19, 38, 50, 65, 100, 200).

Show EMA % Difference Labels : Enable/disable percentage difference labels for all EMAs (default: enabled).

EMA Label Font Size (8–20) : Adjust the font size for EMA labels (default: 10, mapped to “tiny”).

Anchored VWAP 1–3 Settings

Show AVWAP 1–3 : Toggle each anchored VWAP on or off (default: AVWAP 1 enabled, others disabled).

AVWAP 1–3 Color : Set the color for each VWAP line and its label (default: fuchsia for AVWAP 1, purple for AVWAP 2, teal for AVWAP 3).

AVWAP 1–3 Anchor : Choose the anchor period (“Session,” “Week,” “Month”; default: Session for AVWAP 1, Week for AVWAP 2, Month for AVWAP 3).

AVWAP 1–3 Source : Select the price source (default: hlc3).

AVWAP 1–3 Offset : Set the horizontal offset for the VWAP line (default: 0).

Show AVWAP 1–3 Bands : Toggle upper/lower bands (default: disabled).

AVWAP 1–3 Band Multiplier : Adjust the standard deviation multiplier for bands (default: 1.0).

Rolling VWAP 1–3 Settings

Show RVWAP 1–3 : Toggle each rolling VWAP on or off (default: disabled).

RVWAP 1–3 Color : Set the color for each VWAP line and its label (default: navy for RVWAP 1, maroon for RVWAP 2, fuchsia for RVWAP 3).

RVWAP 1–3 Period Length : Set the period for the rolling VWAP (default: 20, 50, 100).

RVWAP 1–3 Source : Select the price source (default: hlc3).

RVWAP 1–3 Offset : Set the horizontal offset (default: 0).

Show RVWAP 1–3 Bands : Toggle upper/lower bands (default: disabled).

RVWAP 1–3 Band Multiplier : Adjust the standard deviation multiplier for bands (default: 1.0).

VWAP Label Settings

Show VWAP % Difference Labels : Enable/disable percentage difference labels for all VWAPs (default: enabled, showing AVWAP 1 label).

VWAP Label Font Size (8–20) : Adjust the font size for VWAP labels (default: 10, mapped to “tiny”).

How It Works

EMAs : Calculated using ta.ema(close, length) for each user-defined period. Percentage differences are computed as ((close - ema) / close) * 100 and displayed as labels for visible EMAs when show_ema_labels is enabled.

Anchored VWAPs : Calculated using ta.vwap(source, anchor, 1), where the anchor is determined by the selected timeframe (Session, Week, or Month). Bands are computed using the standard deviation from ta.vwap.

Rolling VWAPs : Calculated using ta.vwap(source, length), with bands based on ta.stdev(source, length).

Labels : Updated on each new bar (ta.barssince(ta.change(time) != 0) == 0) to show percentage differences. Labels are only displayed for visible EMAs/VWAPs to avoid clutter.

Color Matching: VWAP labels use the same color as their corresponding VWAP lines, set via input settings (e.g., avwap1_color for AVWAP 1).

Example Use Cases

- Trend Following: Use longer EMAs (e.g., 100, 200) to identify trends and shorter EMAs (e.g., 3, 9) for entry/exit signals.

- Mean Reversion: Monitor percentage difference labels to spot overbought/oversold conditions relative to EMAs or VWAPs.

- VWAP Trading: Use the default session-anchored AVWAP 1 for intraday trading, adding weekly/monthly VWAPs or rolling VWAPs for broader context.

- Intraday Analysis: Leverage the session-anchored AVWAP 1 (enabled by default) for day trading, with bands as support/resistance zones.

Cerca negli script per "北证50+指数成分股"

Market Spiralyst [Hapharmonic]Hello, traders and creators! 👋

Market Spiralyst: Let's change the way we look at analysis, shall we? I've got to admit, I scratched my head on this for weeks, Haha :). What you're seeing is an exploration of what's possible when code meets art on financial charts. I wanted to try blending art with trading, to do something new and break away from the same old boring perspectives. The goal was to create a visual experience that's not just analytical, but also relaxing and aesthetically pleasing.

This work is intended as a guide and a design example for all developers, born from the spirit of learning and a deep love for understanding the Pine Script™ language. I hope it inspires you as much as it challenged me!

🧐 Core Concept: How It Works

Spiralyst is built on two distinct but interconnected engines:

The Generative Art Engine: At its core, this indicator uses a wide range of mathematical formulas—from simple polygons to exotic curves like Torus Knots and Spirographs—to draw beautiful, intricate shapes directly onto your chart. This provides a unique and dynamic visual backdrop for your analysis.

The Market Pulse Engine: This is where analysis meets art. The engine takes real-time data from standard technical indicators (RSI and MACD in this version) and translates their states into a simple, powerful "Pulse Score." This score directly influences the appearance of the "Scatter Points" orbiting the main shape, turning the entire artwork into a living, breathing representation of market momentum.

🎨 Unleash Your Creativity! This Is Your Playground

We've included 25 preset shapes for you... but that's just the starting point !

The real magic happens when you start tweaking the settings yourself. A tiny adjustment can make a familiar shape come alive and transform in ways you never expected.

I'm genuinely excited to see what your imagination can conjure up! If you create a shape you're particularly proud of or one that looks completely unique, I would love to see it. Please feel free to share a screenshot in the comments below. I can't wait to see what you discover! :)

Here's the default shape to get you started:

The Dynamic Scatter Points: Reading the Pulse

This is where the magic happens! The small points scattered around the main shape are not just decorative; they are the visual representation of the Market Pulse Score.

The points have two forms:

A small asterisk (`*`): Represents a low or neutral market pulse.

A larger, more prominent circle (`o`): Represents a high, strong market pulse.

Here’s how to read them:

The indicator calculates the Pulse Strength as a percentage (from 0% to 100%) based on the total score from the active indicators (RSI and MACD). This percentage determines the ratio of circles to asterisks.

High Pulse Strength (e.g., 80-100%): Most of the scatter points will transform into large circles (`o`). This indicates that the underlying momentum is strong and It could be an uptrend. It's a visual cue that the market is gaining strength and might be worth paying closer attention to.

Low Pulse Strength (e.g., 0-20%): Most or all of the scatter points will remain as small asterisks (`*`). This suggests weak, neutral, or bearish momentum.

The key takeaway: The more circles you see, the stronger the bullish momentum is according to the active indicators. Watch the artwork "breathe" as the circles appear and disappear with the market's rhythm!

And don't worry about the shape you choose; the scatter points will intelligently adapt and always follow the outer boundary of whatever beautiful form you've selected.

How to Use

Getting started with Spiralyst is simple:

Choose Your Canvas: Start by going into the settings and picking a `Shape` and `Palette` from the "Shape Selection & Palette" group that you find visually appealing. This is your canvas.

Tune Your Engine: Go to the "Market Pulse Engine" settings. Here, you can enable or disable the RSI and MACD scoring engines. Want to see the pulse based only on RSI? Just uncheck the MACD box. You can also fine-tune the parameters for each indicator to match your trading style.

Read the Vibe: Observe the scatter points. Are they mostly small asterisks or are they transforming into large, vibrant circles? Use this visual feedback as a high-level gauge of market momentum.

Check the Dashboard: For a precise breakdown, look at the "Market Pulse Analysis" table on the top-right. It gives you the exact values, scores, and total strength percentage.

Explore & Experiment: Play with the different shapes and color palettes! The core analysis remains the same, but the visual experience can be completely different.

⚙️ Settings & Customization

Spiralyst is designed to be highly customizable.

Shape Selection & Palette: This is your main control panel. Choose from over 25 unique shapes, select a color palette, and adjust the line extension style ( `extend` ) or horizontal position ( `offsetXInput` ).

scatterLabelsInput: This setting controls the total number of points (both asterisks and circles) that orbit the main shape. Think of it as adjusting the density or visual granularity of the market pulse feedback.

The Market Pulse engine will always calculate its strength as a percentage (e.g., 75%). This percentage is then applied to the `scatterLabelsInput` number you've set to determine how many points transform into large circles.

Example: If the Pulse Strength is 75% and you set this to `100` , approximately 75 points will become circles. If you increase it to `200` , approximately 150 points will transform.

A higher number provides a more detailed, high-resolution view of the market pulse, while a lower number offers a cleaner, more minimalist look. Feel free to adjust this to your personal visual preference; the underlying analytical percentage remains the same.

Market Pulse Engine:

`⚙️ RSI Settings` & `⚙️ MACD Settings`: Each indicator has its own group.

Enable Scoring: Use the checkbox at the top of each group to include or exclude that indicator from the Pulse Score calculation. If you only want to use RSI, simply uncheck "Enable MACD Scoring."

Parameters: All standard parameters (Length, Source, Fast/Slow/Signal) are fully adjustable.

Individual Shape Parameters (01-25): Each of the 25+ shapes has its own dedicated group of settings, allowing you to fine-tune every aspect of its geometry, from the number of petals on a flower to the windings of a knot. Feel free to experiment!

For Developers & Pine Script™ Enthusiasts

If you are a developer and wish to add more indicators (e.g., Stochastic, CCI, ADX), you can easily do so by following the modular structure of the code. You would primarily need to:

Add a new `PulseIndicator` object for your new indicator in the `f_getMarketPulse()` function.

Add the logic for its scoring inside the `calculateScore()` method.

The `calculateTotals()` method and the dashboard table are designed to be dynamic and will automatically adapt to include your new indicator!

One of the core design philosophies behind Spiralyst is modularity and scalability . The Market Pulse engine was intentionally built using User-Defined Types (UDTs) and an array-based structure so that adding new indicators is incredibly simple and doesn't require rewriting the main logic.

If you want to add a new indicator to the scoring engine—let's use the Stochastic Oscillator as a detailed example—you only need to modify three small sections of the code. The rest of the script, including the adaptive dashboard, will update automatically.

Here’s your step-by-step guide:

#### Step 1: Add the User Inputs

First, you need to give users control over your new indicator. Find the `USER INTERFACE: INPUTS` section and add a new group for the Stochastic settings, right after the MACD group.

Create a new group name: `string GRP_STOCH = "⚙️ Stochastic Settings"`

Add the inputs: Create a boolean to enable/disable it, and then add the necessary parameters (`%K`, `%D`, `Smooth`). Use the `active` parameter to link them to the enable/disable checkbox.

// Add this code block right after the GRP_MACD and MACD inputs

string GRP_STOCH = "⚙️ Stochastic Settings"

bool stochEnabledInput = input.bool(true, "Enable Stochastic Scoring", group = GRP_STOCH)

int stochKInput = input.int(14, "%K Length", minval=1, group = GRP_STOCH, active = stochEnabledInput)

int stochDInput = input.int(3, "%D Smoothing", minval=1, group = GRP_STOCH, active = stochEnabledInput)

int stochSmoothInput = input.int(3, "Smooth", minval=1, group = GRP_STOCH, active = stochEnabledInput)

#### Step 2: Integrate into the Pulse Engine (The "Factory")

Next, go to the `f_getMarketPulse()` function. This function acts as a "factory" that builds and configures the entire market pulse object. You need to teach it how to build your new Stochastic indicator.

Update the function signature: Add the new `stochEnabledInput` boolean as a parameter.

Calculate the indicator: Add the `ta.stoch()` calculation.

Create a `PulseIndicator` object: Create a new object for the Stochastic, populating it with its name, parameters, calculated value, and whether it's enabled.

Add it to the array: Simply add your new `stochPulse` object to the `array.from()` list.

Here is the complete, updated `f_getMarketPulse()` function :

// Factory function to create and calculate the entire MarketPulse object.

f_getMarketPulse(bool rsiEnabled, bool macdEnabled, bool stochEnabled) =>

// 1. Calculate indicator values

float rsiVal = ta.rsi(rsiSourceInput, rsiLengthInput)

= ta.macd(close, macdFastInput, macdSlowInput, macdSignalInput)

float stochVal = ta.sma(ta.stoch(close, high, low, stochKInput), stochDInput) // We'll use the main line for scoring

// 2. Create individual PulseIndicator objects

PulseIndicator rsiPulse = PulseIndicator.new("RSI", str.tostring(rsiLengthInput), rsiVal, na, 0, rsiEnabled)

PulseIndicator macdPulse = PulseIndicator.new("MACD", str.format("{0},{1},{2}", macdFastInput, macdSlowInput, macdSignalInput), macdVal, signalVal, 0, macdEnabled)

PulseIndicator stochPulse = PulseIndicator.new("Stoch", str.format("{0},{1},{2}", stochKInput, stochDInput, stochSmoothInput), stochVal, na, 0, stochEnabled)

// 3. Calculate score for each

rsiPulse.calculateScore()

macdPulse.calculateScore()

stochPulse.calculateScore()

// 4. Add the new indicator to the array

array indicatorArray = array.from(rsiPulse, macdPulse, stochPulse)

MarketPulse pulse = MarketPulse.new(indicatorArray, 0, 0.0)

// 5. Calculate final totals

pulse.calculateTotals()

pulse

// Finally, update the function call in the main orchestration section:

MarketPulse marketPulse = f_getMarketPulse(rsiEnabledInput, macdEnabledInput, stochEnabledInput)

#### Step 3: Define the Scoring Logic

Now, you need to define how the Stochastic contributes to the score. Go to the `calculateScore()` method and add a new case to the `switch` statement for your indicator.

Here's a sample scoring logic for the Stochastic, which gives a strong bullish score in oversold conditions and a strong bearish score in overbought conditions.

Here is the complete, updated `calculateScore()` method :

// Method to calculate the score for this specific indicator.

method calculateScore(PulseIndicator this) =>

if not this.isEnabled

this.score := 0

else

this.score := switch this.name

"RSI" => this.value > 65 ? 2 : this.value > 50 ? 1 : this.value < 35 ? -2 : this.value < 50 ? -1 : 0

"MACD" => this.value > this.signalValue and this.value > 0 ? 2 : this.value > this.signalValue ? 1 : this.value < this.signalValue and this.value < 0 ? -2 : this.value < this.signalValue ? -1 : 0

"Stoch" => this.value > 80 ? -2 : this.value > 50 ? 1 : this.value < 20 ? 2 : this.value < 50 ? -1 : 0

=> 0

this

#### That's It!

You're done. You do not need to modify the dashboard table or the total score calculation.

Because the `MarketPulse` object holds its indicators in an array , the rest of the script is designed to be adaptive:

The `calculateTotals()` method automatically loops through every indicator in the array to sum the scores and calculate the final percentage.

The dashboard code loops through the `enabledIndicators` array to draw the table. Since your new Stochastic indicator is now part of that array, it will appear automatically when enabled!

---

Remember, this is your playground! I'm genuinely excited to see the unique shapes you discover. If you create something you're proud of, feel free to share it in the comments below.

Happy analyzing, and may your charts be both insightful and beautiful! 💛

Optimized Trend-Momentum SignalsThis indicator combines trend, momentum, and volume-strength factors into a single buy/sell signal system. It integrates:

SMA 200 → Identifies the long-term trend (price above = bullish bias, below = bearish bias).

MACD (12,26,9) → Confirms momentum direction with line crossovers.

RSI (7) → Filters strength (above 50 = bullish, below 50 = bearish).

ROC (45) → Validates positive or negative rate of change.

Signal Logic:

Buy Signal → Price above SMA 200, MACD bullish, RSI > 50, and ROC > 0.

Sell Signal → Price below SMA 200, MACD bearish, RSI < 50, and ROC < 0.

Features:

Clear arrows for BUY and SELL signals.

Long-term SMA plotted for trend visualization.

Alerts built-in for real-time notifications.

This tool helps traders filter out noise and act only when all major confirmation factors align, reducing false signals and improving decision-making.

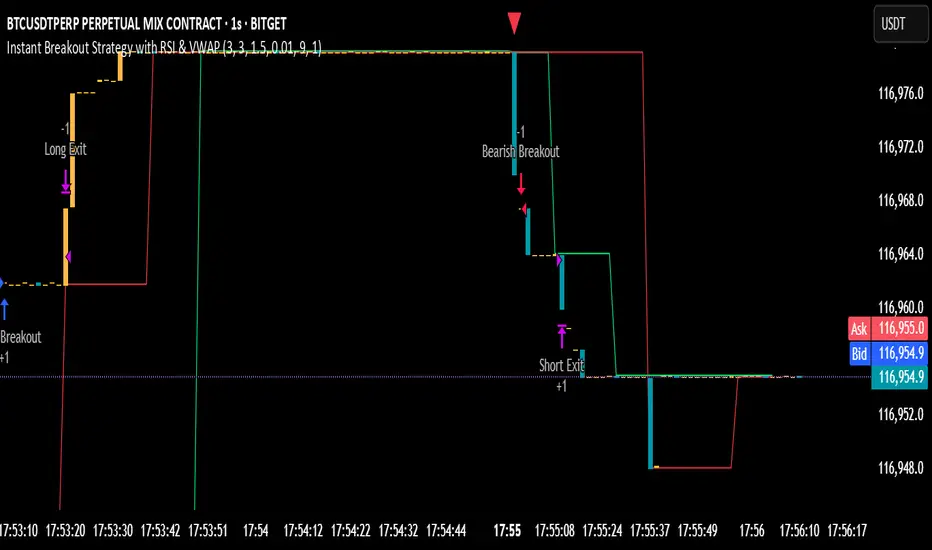

Instant Breakout Strategy with RSI & VWAPInstant Breakout Strategy with RSI & VWAP

This TradingView strategy (Pine Script v6) trades breakouts using pivot points, with optional filters for volume, momentum, RSI, and VWAP. It’s optimized for the 1-second timeframe.

Overview

The strategy identifies breakouts when price crosses above resistance (pivot highs) or below support (pivot lows). It can use basic pivot breakouts or add filters for stronger signals. Take-profit and stop-loss levels are set using ATR, and signals are shown on the chart.

Inputs

Left/Right Pivot Bars: Bars to detect pivots (default: 3). Lower values increase sensitivity.

Volume Surge Multiplier: Volume threshold vs. 20-period average (default: 1.5).

Momentum Threshold: Minimum % price change from bar open (default: 1%).

Take-Profit ATR Multiplier: ATR multiplier for take-profit (default: 9.0).

Stop-Loss ATR Multiplier: ATR multiplier for stop-loss (default: 1.0).

Use Filters: Enable/disable volume, momentum, RSI, and VWAP filters (default: off).

How It Works

1. Pivot Detection

Finds pivot highs (resistance) and lows (support) using ta.pivothigh and ta.pivotlow.

Tracks the latest pivot levels.

2. Volume Surge

Compares current volume to a 20-period volume average.

A surge occurs if volume exceeds the average times the multiplier.

3. Momentum

Measures price change from the bar’s open.

Bullish: Price rises >1% from open.

Bearish: Price falls >1% from open.

4. RSI and VWAP

RSI: 3-period RSI. Above 50 is bullish; below 50 is bearish.

VWAP: Price above VWAP is bullish; below is bearish.

5. ATR

14-period ATR sets take-profit (close ± atr * 9.0) and stop-loss (close ± atr * 1.0).

Trading Rules

Breakout Conditions

Bullish Breakout:

Price crosses above the latest pivot high.

With filters: Volume surge, bullish momentum, RSI > 50, price > VWAP.

Without filters: Only the crossover is needed.

Bearish Breakout:

Price crosses below the latest pivot low.

With filters: Volume surge, bearish momentum, RSI < 50, price < VWAP.

Without filters: Only the crossunder is needed.

Entries and Exits

Long: Enter on bullish breakout. Set take-profit and stop-loss. Close any short position.

Short: Enter on bearish breakout. Set take-profit and stop-loss. Close any long position.

Visuals

Signals: Green triangles (bullish) below bars, red triangles (bearish) above bars.

Pivot Levels: Green line (resistance), red line (support).

Indicators: RSI (blue, separate pane), VWAP (purple, on chart).

How to Use

Apply to a 1-second chart in TradingView for best results.

Adjust inputs (e.g., pivot bars, multipliers). Enable filters for stricter signals.

Watch for buy/sell triangles and monitor RSI/VWAP.

Use ATR-based take-profit/stop-loss for risk management.

Notes

Best on 1-second timeframe due to fast RSI and responsiveness.

Disable filters for more signals (less confirmation).

Backtest before live trading to check performance.

This strategy uses pivots, volume, momentum, RSI, and VWAP for clear breakout trades on the 1-second timeframe.

Market Outlook Score (MOS)Overview

The "Market Outlook Score (MOS)" is a custom technical indicator designed for TradingView, written in Pine Script version 6. It provides a quantitative assessment of market conditions by aggregating multiple factors, including trend strength across different timeframes, directional movement (via ADX), momentum (via RSI changes), volume dynamics, and volatility stability (via ATR). The MOS is calculated as a weighted score that ranges typically between -1 and +1 (though it can exceed these bounds in extreme conditions), where positive values suggest bullish (long) opportunities, negative values indicate bearish (short) setups, and values near zero imply neutral or indecisive markets.

This indicator is particularly useful for traders seeking a holistic "outlook" score to gauge potential entry points or market bias. It overlays on a separate pane (non-overlay mode) and visualizes the score through horizontal threshold lines and dynamic labels showing the numeric MOS value along with a simple trading decision ("Long", "Short", or "Neutral"). The script avoids using the plot function for compatibility reasons (e.g., potential TradingView bugs) and instead relies on hline for static lines and label.new for per-bar annotations.

Key features:

Multi-Timeframe Analysis: Incorporates slope data from 5-minute, 15-minute, and 30-minute charts to capture short-term trends.

Trend and Strength Integration: Uses ADX to weight trend bias, ensuring stronger signals in trending markets.

Momentum and Volume: Includes RSI momentum impulses and volume deviations for added confirmation.

Volatility Adjustment: Factors in ATR changes to assess market stability.

Customizable Inputs: Allows users to tweak periods for lookback, ADX, and ATR.

Decision Labels: Automatically classifies the MOS into actionable categories with visual labels.

This indicator is best suited for intraday or swing trading on volatile assets like stocks, forex, or cryptocurrencies. It does not generate buy/sell signals directly but can be combined with other tools (e.g., moving averages or oscillators) for comprehensive strategies.

Inputs

The script provides three user-configurable inputs via TradingView's input panel:

Lookback Period (lookback):

Type: Integer

Default: 20

Range: Minimum 10, Maximum 50

Purpose: Defines the number of bars used in slope calculations for trend analysis. A shorter lookback makes the indicator more sensitive to recent price action, while a longer one smooths out noise for longer-term trends.

ADX Period (adxPeriod):

Type: Integer

Default: 14

Range: Minimum 5, Maximum 30

Purpose: Sets the smoothing period for the Average Directional Index (ADX) and its components (DI+ and DI-). Standard value is 14, but shorter periods increase responsiveness, and longer ones reduce false signals.

ATR Period (atrPeriod):

Type: Integer

Default: 14

Range: Minimum 5, Maximum 30

Purpose: Determines the period for the Average True Range (ATR) calculation, which measures volatility. Adjust this to match your trading timeframe—shorter for scalping, longer for positional trading.

These inputs allow customization without editing the code, making the indicator adaptable to different market conditions or user preferences.

Core Calculations

The MOS is computed through a series of steps, blending trend, momentum, volume, and volatility metrics. Here's a breakdown:

Multi-Timeframe Slopes:

The script fetches data from higher timeframes (5m, 15m, 30m) using request.security.

Slope calculation: For each timeframe, it computes the linear regression slope of price over the lookback period using the formula:

textslope = correlation(close, bar_index, lookback) * stdev(close, lookback) / stdev(bar_index, lookback)

This measures the rate of price change, where positive slopes indicate uptrends and negative slopes indicate downtrends.

Variables: slope5m, slope15m, slope30m.

ATR (Average True Range):

Calculated using ta.atr(atrPeriod).

Represents average volatility over the specified period. Used later to derive volatility stability.

ADX (Average Directional Index):

A detailed, manual implementation (not using built-in ta.adx for customization):

Computes upward movement (upMove = high - high ) and downward movement (downMove = low - low).

Derives +DM (Plus Directional Movement) and -DM (Minus Directional Movement) by filtering non-relevant moves.

Smooths true range (trur = ta.rma(ta.tr(true), adxPeriod)).

Calculates +DI and -DI: plusDI = 100 * ta.rma(plusDM, adxPeriod) / trur, similarly for minusDI.

DX: dx = 100 * abs(plusDI - minusDI) / max(plusDI + minusDI, 0.0001).

ADX: adx = ta.rma(dx, adxPeriod).

ADX values above 25 typically indicate strong trends; here, it's normalized (divided by 50) to influence the trend bias.

Volume Delta (5m Timeframe):

Fetches 5m volume: volume_5m = request.security(syminfo.tickerid, "5", volume, lookahead=barmerge.lookahead_on).

Computes a 12-period SMA of volume: avgVolume = ta.sma(volume_5m, 12).

Delta: (volume_5m - avgVolume) / avgVolume (or 0 if avgVolume is zero).

This measures relative volume spikes, where positive deltas suggest increased interest (bullish) and negative suggest waning activity (bearish).

MOS Components and Final Calculation:

Trend Bias: Average of the three slopes, normalized by close price and scaled by 100, then weighted by ADX influence: (slope5m + slope15m + slope30m) / 3 / close * 100 * (adx / 50).

Emphasizes trends in strong ADX conditions.

Momentum Impulse: Change in 5m RSI(14) over 1 bar, divided by 50: ta.change(request.security(syminfo.tickerid, "5", ta.rsi(close, 14), lookahead=barmerge.lookahead_on), 1) / 50.

Captures short-term momentum shifts.

Volatility Clarity: 1 - ta.change(atr, 1) / max(atr, 0.0001).

Measures ATR stability; values near 1 indicate low volatility changes (clearer trends), while lower values suggest erratic markets.

MOS Formula: Weighted average:

textmos = (0.35 * trendBias + 0.25 * momentumImpulse + 0.2 * volumeDelta + 0.2 * volatilityClarity)

Weights prioritize trend (35%) and momentum (25%), with volume and volatility at 20% each. These can be adjusted in code for experimentation.

Trading Decision:

A variable mosDecision starts as "Neutral".

If mos > 0.15, set to "Long".

If mos < -0.15, set to "Short".

Thresholds (0.15 and -0.15) are hardcoded but can be modified.

Visualization and Outputs

Threshold Lines (using hline):

Long Threshold: Horizontal dashed green line at +0.15.

Short Threshold: Horizontal dashed red line at -0.15.

Neutral Line: Horizontal dashed gray line at 0.

These provide visual reference points for MOS interpretation.

Dynamic Labels (using label.new):

Placed at each bar's index and MOS value.

Text: Formatted MOS value (e.g., "0.2345") followed by a newline and the decision (e.g., "Long").

Style: Downward-pointing label with gray background and white text for readability.

This replaces a traditional plot line, showing exact values and decisions per bar without cluttering the chart.

The indicator appears in a separate pane below the main price chart, making it easy to monitor alongside price action.

Usage Instructions

Adding to TradingView:

Copy the script into TradingView's Pine Script editor.

Save and add to your chart via the "Indicators" menu.

Select a symbol and timeframe (e.g., 1-minute for intraday).

Interpretation:

Long Signal: MOS > 0.15 – Consider bullish positions if supported by other indicators.

Short Signal: MOS < -0.15 – Potential bearish setups.

Neutral: Between -0.15 and 0.15 – Avoid trades or wait for confirmation.

Watch for MOS crossings of thresholds for momentum shifts.

Combine with price patterns, support/resistance, or volume for better accuracy.

Limitations and Considerations:

Lookahead Bias: Uses barmerge.lookahead_on for multi-timeframe data, which may introduce minor forward-looking bias in backtesting (use with caution).

No Alerts Built-In: Add custom alerts via TradingView's alert system based on MOS conditions.

Performance: Tested for compatibility; may require adjustments for illiquid assets or extreme volatility.

Backtesting: Use TradingView's strategy tester to evaluate historical performance, but remember past results don't guarantee future outcomes.

Customization: Edit weights in the MOS formula or thresholds to fit your strategy.

This indicator distills complex market data into a single score, aiding decision-making while encouraging users to verify signals with additional analysis. If you need modifications, such as restoring plot functionality or adding features, provide details for further refinement.

Advanced Volume Profile Pro Delta + POC + VAH/VAL# Advanced Volume Profile Pro - Delta + POC + VAH/VAL Analysis System

## WHAT THIS SCRIPT DOES

This script creates a comprehensive volume profile analysis system that combines traditional volume-at-price distribution with delta volume calculations, Point of Control (POC) identification, and Value Area (VAH/VAL) analysis. Unlike standard volume indicators that show only total volume over time, this script analyzes volume distribution across price levels and estimates buying vs selling pressure using multiple calculation methods to provide deeper market structure insights.

## WHY THIS COMBINATION IS ORIGINAL AND USEFUL

**The Problem Solved:** Traditional volume indicators show when volume occurs but not where price finds acceptance or rejection. Standalone volume profiles lack directional bias information, while basic delta calculations don't provide structural context. Traders need to understand both volume distribution AND directional sentiment at key price levels.

**The Solution:** This script implements an integrated approach that:

- Maps volume distribution across price levels using configurable row density

- Estimates delta (buying vs selling pressure) using three different methodologies

- Identifies Point of Control (highest volume price level) for key support/resistance

- Calculates Value Area boundaries where 70% of volume traded

- Provides real-time alerts for key level interactions and volume imbalances

**Unique Features:**

1. **Developing POC Visualization**: Real-time tracking of Point of Control migration throughout the session via blue dotted trail, revealing institutional accumulation/distribution patterns before they complete

2. **Multi-Method Delta Calculation**: Price Action-based, Bid/Ask estimation, and Cumulative methods for different market conditions

3. **Adaptive Timeframe System**: Auto-adjusts calculation parameters based on chart timeframe for optimal performance

4. **Flexible Profile Types**: N Bars Back (precise control), Days Back (calendar-based), and Session-based analysis modes

5. **Advanced Imbalance Detection**: Identifies and highlights significant buying/selling imbalances with configurable thresholds

6. **Comprehensive Alert System**: Monitors POC touches, Value Area entry/exit, and major volume imbalances

## HOW THE SCRIPT WORKS TECHNICALLY

### Core Volume Profile Methodology:

**1. Price Level Distribution:**

- Divides price range into user-defined rows (10-50 configurable)

- Calculates row height: `(Highest Price - Lowest Price) / Number of Rows`

- Distributes each bar's volume across price levels it touched proportionally

**2. Delta Volume Calculation Methods:**

**Price Action Method:**

```

Price Range = High - Low

Buy Pressure = (Close - Low) / Price Range

Sell Pressure = (High - Close) / Price Range

Buy Volume = Total Volume × Buy Pressure

Sell Volume = Total Volume × Sell Pressure

Delta = Buy Volume - Sell Volume

```

**Bid/Ask Estimation Method:**

```

Average Price = (High + Low + Close) / 3

Buy Volume = Close > Average ? Volume × 0.6 : Volume × 0.4

Sell Volume = Total Volume - Buy Volume

```

**Cumulative Method:**

```

Buy Volume = Close > Open ? Volume : Volume × 0.3

Sell Volume = Close ≤ Open ? Volume : Volume × 0.3

```

**3. Point of Control (POC) Identification:**

- Scans all price levels to find maximum volume concentration

- POC represents the price level with highest trading activity

- Acts as significant support/resistance level

- **Developing POC Feature**: Tracks POC evolution in real-time via blue dotted trail, showing how institutional interest migrates throughout the session. Upward POC migration indicates accumulation patterns, downward migration suggests distribution, providing early trend signals before price confirmation.

**4. Value Area Calculation:**

- Starts from POC and expands up/down to encompass 70% of total volume

- VAH (Value Area High): Upper boundary of value area

- VAL (Value Area Low): Lower boundary of value area

- Expansion algorithm prioritizes direction with higher volume

**5. Adaptive Range Selection:**

Based on profile type and timeframe optimization:

- **N Bars Back**: Fixed lookback period with performance optimization (20-500 bars)

- **Days Back**: Calendar-based analysis with automatic timeframe adjustment (1-365 days)

- **Session**: Current trading session or custom session times

### Performance Optimization Features:

- **Sampling Algorithm**: Reduces calculation load on large datasets while maintaining accuracy

- **Memory Management**: Clears previous drawings to prevent performance degradation

- **Safety Constraints**: Prevents excessive memory usage with configurable limits

## HOW TO USE THIS SCRIPT

### Initial Setup:

1. **Profile Configuration**: Select profile type based on trading style:

- N Bars Back: Precise control over data range

- Days Back: Intuitive calendar-based analysis

- Session: Real-time session development

2. **Row Density**: Set number of rows (30 default) - more rows = higher resolution, slower performance

3. **Delta Method**: Choose calculation method based on market type:

- Price Action: Best for trending markets

- Bid/Ask Estimate: Good for ranging markets

- Cumulative: Smoothed approach for volatile markets

4. **Visual Settings**: Configure colors, position (left/right), and display options

### Reading the Profile:

**Volume Bars:**

- **Length**: Represents relative volume at that price level

- **Color**: Green = net buying pressure, Red = net selling pressure

- **Intensity**: Darker colors indicate volume imbalances above threshold

**Key Levels:**

- **POC (Blue Line)**: Highest volume price - major support/resistance

- **VAH (Purple Dashed)**: Value Area High - upper boundary of fair value

- **VAL (Orange Dashed)**: Value Area Low - lower boundary of fair value

- **Value Area Fill**: Shaded region showing main trading range

**Developing POC Trail:**

- **Blue Dotted Lines**: Show real-time POC evolution throughout the session

- **Migration Patterns**: Upward trail indicates bullish accumulation, downward trail suggests bearish distribution

- **Early Signals**: POC movement often precedes price movement, providing advance warning of institutional activity

- **Institutional Footprints**: Reveals where smart money concentrated volume before final POC establishment

### Trading Applications:

**Support/Resistance Analysis:**

- POC acts as magnetic price level - expect reactions

- VAH/VAL provide intermediate support/resistance levels

- Profile edges show areas of low volume acceptance

**Developing POC Analysis:**

- **Upward Migration**: POC moving higher = institutional accumulation, bullish bias

- **Downward Migration**: POC moving lower = institutional distribution, bearish bias

- **Stable POC**: Tight clustering = balanced market, range-bound conditions

- **Early Trend Detection**: POC direction change often precedes price breakouts

**Entry Strategies:**

- Buy at VAL with POC as target (in uptrends)

- Sell at VAH with POC as target (in downtrends)

- Breakout plays above/below profile extremes

**Volume Imbalance Trading:**

- Strong buying imbalance (>60% threshold) suggests continued upward pressure

- Strong selling imbalance suggests continued downward pressure

- Imbalances near key levels provide high-probability setups

**Multi-Timeframe Context:**

- Use higher timeframe profiles for major levels

- Lower timeframe profiles for precise entries

- Session profiles for intraday trading structure

## SCRIPT SETTINGS EXPLANATION

### Volume Profile Settings:

- **Profile Type**: Determines data range for calculation

- N Bars Back: Exact number of bars (20-500 range)

- Days Back: Calendar days with timeframe adaptation (1-365 days)

- Session: Trading session-based (intraday focus)

- **Number of Rows**: Profile resolution (10-50 range)

- **Profile Width**: Visual width as chart percentage (10-50%)

- **Value Area %**: Volume percentage for VA calculation (50-90%, 70% standard)

- **Auto-Adjust**: Automatically optimizes for different timeframes

### Delta Volume Settings:

- **Show Delta Volume**: Enable/disable delta calculations

- **Delta Calculation Method**: Choose methodology based on market conditions

- **Highlight Imbalances**: Visual emphasis for significant volume imbalances

- **Imbalance Threshold**: Percentage for imbalance detection (50-90%)

### Session Settings:

- **Session Type**: Daily, Weekly, Monthly, or Custom periods

- **Custom Session Time**: Define specific trading hours

- **Previous Sessions**: Number of historical sessions to display

### Days Back Settings:

- **Lookback Days**: Number of calendar days to analyze (1-365)

- **Automatic Calculation**: Script automatically converts days to bars based on timeframe:

- Intraday: Accounts for 6.5 trading hours per day

- Daily: 1 bar per day

- Weekly/Monthly: Proportional adjustment

### N Bars Back Settings:

- **Lookback Bars**: Exact number of bars to analyze (20-500)

- **Precise Control**: Best for systematic analysis and backtesting

### Visual Customization:

- **Colors**: Bullish (green), Bearish (red), and level colors

- **Profile Position**: Left or Right side of chart

- **Profile Offset**: Distance from current price action

- **Labels**: Show/hide level labels and values

- **Smooth Profile Bars**: Enhanced visual appearance

### Alert Configuration:

- **POC Touch**: Alerts when price interacts with Point of Control

- **VA Entry/Exit**: Alerts for Value Area boundary interactions

- **Major Imbalance**: Alerts for significant volume imbalances

## VISUAL FEATURES

### Profile Display:

- **Horizontal Bars**: Volume distribution across price levels

- **Color Coding**: Delta-based coloring for directional bias

- **Smooth Rendering**: Optional smoothing for cleaner appearance

- **Transparency**: Configurable opacity for chart readability

### Level Lines:

- **POC**: Solid blue line with optional label

- **VAH/VAL**: Dashed colored lines with value displays

- **Extension**: Lines extend across relevant time periods

- **Value Area Fill**: Optional shaded region between VAH/VAL

### Information Table:

- **Current Values**: Real-time POC, VAH, VAL prices

- **VA Range**: Value Area width calculation

- **Positioning**: Multiple table positions available

- **Text Sizing**: Adjustable for different screen sizes

## IMPORTANT USAGE NOTES

**Realistic Expectations:**

- Volume profile analysis provides structural context, not trading signals

- Delta calculations are estimations based on price action, not actual order flow

- Past volume distribution does not guarantee future price behavior

- Combine with other analysis methods for comprehensive market view

**Best Practices:**

- Use appropriate profile types for your trading style:

- Day Trading: Session or Days Back (1-5 days)

- Swing Trading: Days Back (10-30 days) or N Bars Back

- Position Trading: Days Back (60-180 days)

- Consider market context (trending vs ranging conditions)

- Verify key levels with additional technical analysis

- Monitor profile development for changing market structure

**Performance Considerations:**

- Higher row counts increase calculation complexity

- Large lookback periods may affect chart performance

- Auto-adjust feature optimizes for most use cases

- Consider using session profiles for intraday efficiency

**Limitations:**

- Delta calculations are estimations, not actual transaction data

- Profile accuracy depends on available price/volume history

- Effectiveness varies across different instruments and market conditions

- Requires understanding of volume profile concepts for optimal use

**Data Requirements:**

- Requires volume data for accurate calculations

- Works best on liquid instruments with consistent volume

- May be less effective on very low volume or exotic instruments

This script serves as a comprehensive volume analysis tool for traders who need detailed market structure information with integrated directional bias analysis and real-time POC development tracking for informed trading decisions.

GrayZone Sniper [CHE] — Breakout Validation System GrayZone Sniper — Breakout Validation System

Trade only the clean breakouts. Detect the sideways “gray zone,” wait for a confirmed breach, and act only when momentum (TFRSI) and range expansion (Mean Deviation) align. Clear long/short triggers, one-shot exit signals, and persistent levels keep your manual trading disciplined and repeatable.

Why it boosts manual trading

* No guesswork: Grey box marks consolidation; you trade the validated break.

* Fewer fakeouts: Triggers require momentum + volatility—not just a wick through a level.

* Rules > bias: Optional close-only signals stop intrabar noise.

* Built-in exits: One-shot LS/SS (Long/Short Stop) when conditions degrade.

* Actionable visuals: Gray-zone boxes, persistent highs/lows, and a smooth T3 trendline.

What it does (short + precise)

1. Maps consolidation as a gray box (running high/low while state is neutral).

2. Validates breakouts only when:

* Mean Deviation filter says current range expands vs. its own baseline, and

* TFRSI momentum is above 50 + deadzone (long) or below 50 − deadzone (short), and

* Price closes beyond the last gray high/low (optional close-only).

→ You get L (long) or S (short).

3. Manages exits with a smooth T3 trendline plus MD trend: when MD weakens and T3 turns against the prior side, you get a single LS/SS stop signal.

4. Extends structure: Last gray-zone H/L can persist as right-extended levels for retests/targets.

5. Ready for alerts: Prebuilt alert conditions for L, S, LS, SS.

Signals at a glance

* L – Long Trigger (validated breakout up)

* S – Short Trigger (validated breakout down)

* LS – Long Stop (exit hint for open long)

* SS – Short Stop (exit hint for open short)

Why TFRSI + Mean Deviation is a killer combo

They measure different, complementary things—and that reduces correlated errors.

* Mean Deviation (MD) = range expansion filter. It checks whether current absolute deviation of Typical Price from its SMA (|TP − SMA(TP)|) is greater than its own historical mean deviation baseline. In plain English: *is the market actually moving beyond its usual wiggle?* If not, most breakouts are noise.

* TFRSI = directional momentum around a 50 baseline, normalized and smoothed to react fast while avoiding raw RSI twitchiness.

* Synergy:

* MD confirms there’s energy (volatility regime has expanded).

* TFRSI confirms where that energy points (bull or bear).

* Requiring both gives you high-quality, directional expansion—the exact condition that tends to produce follow-through, while filtering the classic “thin break, immediate snap-back.”

Result: Fewer trades, better quality. You skip most range breaks without momentum or momentum pops without real expansion.

Inputs & Functions (clean overview)

Core: TFRSI & MD

* TFRSI Length (`tfrsiLen`, default 6): Longer = smoother, slower.

* TFRSI Smoothing (`tfrsiSignalLen`, default 2): SMA on TFRSI for cleaner signals.

* Mean Deviation Period (`mdLen`, default 20): Baseline for expansion filter.

* Use classical MD (`useTaDev`, default off):

* Off: MD vs current SMA (warning-free internal baseline).

* On: Classical `ta.dev` implementation.

* TFRSI Deadzone ± around 50 (`tfrsiDeadzone`, default 1.0): Wider deadzone = stricter momentum confirmation (less chop).

Triggers & Logic

* Trigger only on bar close (`fireOnCloseOnly`, default on): Confirmed signals only; no intrabar flicker.

* Reset gray bounds after trigger (`resetGrayBoundsAfterTrigger`, default on): Clears last gray H/L once a trade triggers.

* Auto-deactivate on neutral (`autoDeactivateOnNeutral`, default off): Strict disarm when state flips back to neutral.

Gray-Zone Boxes

* Show boxes (`showGrayBoxes`, default on): Draws the neutral consolidation box.

* Max boxes (`maxGrayBoxes`, default 10): How many historic boxes to keep.

* Transparency (`boxFillTransp`/`boxBorderTransp`, defaults 85/30): Visual tuning.

Trendline (T3)

* T3 Length (`t3Length`, default 3): Smoothing depth (higher = smoother).

* T3 Volume Factor (`t3VolumeFactor`, default 0.7): Controls responsiveness of the T3 curve.

Persistent Levels

* Persist gray H/L (`saveGrayLevels`, default on): Extend last gray high/low to the right.

* Max saved level pairs (`maxSavedGrayLvls`, default 1): How many H/L pairs to keep.

* Reset levels on trigger (`resetLevelsOnTrig`, default off): Clean slate after new trigger.

Debug & Visuals

* Show debug markers (`showDebugMarkers`, default on): Display L/S/LS/SS in the pane.

* Show legend (`showLegend`, default on): Compact legend (top-right).

How to trade it (practical)

1. Keep close-only on. Let the market finish the candle.

2. Wait for a clean gray box. Let the range define itself.

3. Take only L/S triggers where MD filter passes and TFRSI confirms.

4. Use persistent levels for retests/partials/targets.

5. Respect LS/SS. When expansion fades and T3 turns, exit without debate.

Tuning tips:

* More chop? Increase `tfrsiDeadzone` or `mdLen`.

* Want faster entries? Slightly reduce `t3Length` or deadzone, but expect more noise.

* Works across assets/timeframes (crypto/FX/indices/equities).

Bottom line

GrayZone Sniper enforces a simple, robust rule: Don’t touch the market until it breaks a defined range with real expansion and aligned momentum. That’s why TFRSI + Mean Deviation is hard to beat—and why your manual breakout trades get cleaner, calmer, and more consistent.

Disclaimer:

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Enhance your trading precision and confidence with Triple Power Stop (CHE)! 🚀

Happy trading

Chervolino

U Table • LITEA compact, educational version of my workflow that combines trend, momentum, trend strength, and a clean trigger:

Trend: EMA Fast vs EMA Slow (auto-lengths by chart TF)

Momentum: RSI > 50 for longs / < 50 for shorts

Strength: ADX above a user-set threshold (fallback implementation; can be replaced by ta.adx() when available)

Trigger: price crosses the Bollinger basis (center line)

Signals

LONG: crossover(close, BB basis) while EMA Fast > EMA Slow, RSI > 50, ADX > threshold

SHORT: crossunder(close, BB basis) while EMA Fast < EMA Slow, RSI < 50, ADX > threshold

Visuals

EMA Fast / EMA Slow / BB basis

Markers “L” / “S” on triggers

Latest confirmed pivot high/low (broken line style)

Small diagnostics table (ADX, EMA relation, RSI, last pivots) on the last bar

Inputs

Pivot length: pivot confirmation window (default 5)

ADX threshold: minimum trend strength to allow signals (default 20)

Notes

Signals are intended to be evaluated on bar close. Intrabar values may change until the bar closes.

Pivot lines appear after confirmation; they do not repaint once confirmed.

No external data or security() calls are used.

This LITE build focuses on clarity and speed (few calculations, overlay-friendly). It can be used as a stand-alone study or as a scaffold for your own research and risk management.

FlowScape PredictorFlowScape Predictor is a non-repainting, regime-aware entry qualifier that turns complex market context into two readiness scores (Long & Short, each 0/25/50/75/100) and clean, confirmed-bar signals. It blends three orthogonal pillars so you act only when trend energy, momentum, and location agree:

Regime (energy): ATR-normalized linear-regression slope of a smooth HMA → EMA baseline, gated by ADX to confirm when pressure is meaningful.

Momentum (push): RSI slope alignment so price has directional follow-through, not just drift.

Structure (location): proximity to pivot-confirmed swings, scaled by ATR, so “ready” appears near constructive pullbacks—not mid-trend chases.

A soft ATR cloud wraps the baseline for context. A yellow Predictive Baseline extends beyond the last bar to visualize near-term trajectory. It is visual-only: scores/alerts never use it.

What you see

Baseline line that turns green/red when regime is strong in that direction; gray when weak.

ATR cloud around the baseline (context for stretch and pullbacks).

Scores (Long & Short, 0–100 in steps of 25) and optional “L/S” icons on bar close.

Yellow Predictive Baseline that extends to the right for a few bars (visual trajectory of the smoothed baseline).

The scoring system (simple and transparent)

Each side (Long/Short) sums four binary checks, 25 points each:

Regime aligned: trendStrong is true and LR slope sign favors that side.

Momentum aligned: RSI side (>50 for Long, <50 for Short) and RSI slope confirms direction.

Baseline side: price is above (Long) / below (Short) the baseline.

Location constructive: distance from the last confirmed pivot is healthy (ATR-scaled; not overstretched).

Valid totals are 0, 25, 50, 75, 100.

Best-quality signal: 100/0 (your side/opposite) on bar close.

Good, still valid: 75/0, especially when the missing block is only “location” right as price re-engages the cloud/baseline.

Avoid: 75/25 or any opposition > 0 in a weak (gray) regime.

The Predictive (Kalman) line — what it is and isn’t

The yellow line is a visual forward extension of the smoothed baseline to help you see the current trajectory and time pullback resumptions. It does not predict price and is excluded from scores and alerts.

How it’s built (plain English):

We maintain a one-dimensional Kalman state x as a smoothed estimate of the baseline. Each bar we observe the current baseline z.

The filter adjusts its trust using the Kalman gain K = P / (P + R) and updates:

x := x + K*(z − x), then P := (1 − K)*P + Q.

Q (process noise): Higher Q → expects faster change → tracks turns quicker (less smoothing).

R (measurement noise): Higher R → trusts raw baseline less → smoother, steadier projection.

What you control:

Lead (how many bars forward to draw).

Kalman Q/R (visual smoothness vs. responsiveness).

Toggle the line on/off if you prefer a minimal chart.

Important: The predictive line extends the baseline, not price. It’s a visual timing aid—don’t automate off it.

How to use (step-by-step)

Keep the chart clean and use a standard OHLC/candlestick chart.

Read the regime: Prefer trades with green/red baseline (trendStrong = true).

Check scores on bar close:

Take Long 100 / Short 0 or Long 75 / Short 0 when the chart shows a tidy pullback re-engaging the cloud/baseline.

Mirror the logic for shorts.

Confirm location: If price is > ~1.5 ATR from its reference pivot, let it come back—avoid chasing.

Set alerts: Add an alert on Long Ready or Short Ready; these fire on closed bars only.

Risk management: Use ATR-buffered stops beyond the recent pivot; target fixed-R multiples (e.g., 1.5–3.0R). Manage the trade with the baseline/cloud if you trail.

Best-practice playbook (quick rules)

Green light: 100/0 (best) or 75/0 (good) on bar close in a colored (non-gray) regime.

Location first: Prefer entries near the baseline/cloud right after a pullback, not far above/below it.

Avoid mixed signals: Skip 75/25 and anything with opposition while the baseline is gray.

Use the yellow line with discretion: It helps you see rhythm; it’s not a signal source.

Timeframes & tuning (practical defaults)

Intraday indices/FX (5m–15m): Demand 100/0 in chop; allow 75/0 when ADX is awake and pullback is clean.

Crypto intraday (15m–1h): Prefer 100/0; 75/0 on the first pullback after a regime turn.

Swing (1h–4h/D1): 75/0 is often sufficient; 100/0 is excellent (fewer but cleaner signals).

If choppy: raise ADX threshold, raise the readiness bar (insist on 100/0), or lengthen the RSI slope window.

What makes FlowScape different

Energy-first regime filter: ATR-normalized LR slope + ADX gate yields a consistent read of trend quality across symbols and timeframes.

Location-aware entries: ATR-scaled pivot proximity discourages mid-air chases, encouraging pullback timing.

Separation of concerns: The predictive line is visual-only, while scores/alerts are confirmed on close for non-repainting behavior.

One simple score per side: A single 0–100 readiness figure is easier to tune than juggling multiple indicators.

Transparency & limitations

Scores are coarse by design (25-point blocks). They’re a gatekeeper, not a promise of outcomes.

Pivots confirm after right-side bars, so structure signals appear after swings form (non-repainting by design).

Avoid using non-standard chart types (Heikin Ashi, Renko, Range, etc.) for signals; use a clean, standard chart.

No lookahead, no higher-timeframe requests; alerts fire on closed bars only.

WaveTrend Dynamic (Lazy Bear Style)█ OVERVIEW

The WaveTrend Dynamic indicator (in the style of Lazy Bear) is an advanced tool based on the Exponential Smoothing Average (ESA), which adapts to the volatility and price of a financial instrument. It is more flexible than the classic WaveTrend but shares a similar concept of bands around a main oscillator line.

The indicator uses dynamic bands calculated as distances from the ESA, with their width adjustable via the "level" parameter. This allows it to be tailored to various markets, timeframes, and volatility conditions, making it easier to identify trends, reversal points, and buy/sell signals.

█ CONCEPTS

The WaveTrend Dynamic combines oscillator functions with trend analysis. Below, we explain the key components in a simple way, understandable even for beginner users.

Core Calculations

The indicator relies on the adaptive ESA and a few straightforward steps:

1 — ESA (Adaptive Average): Calculated as a smoothed average of the price (from high, low, and close, or HLC3) using the ESA Length parameter (default: 10). This number determines how many past candles are considered in the calculation. The ESA quickly responds to price changes, helping to track trends.

2 — Deviation (D): Measures how much the price deviates from the ESA, factoring in market volatility. This allows the indicator to adapt to different instruments.

3 — Price Distance Indicator (CI): Shows how far the price is from the ESA relative to market volatility. This forms the basis for the main indicator line, reacting to price movements.

4 — WT1 (WaveTrend 1): The main line, smoothing the Price Distance Indicator (CI) with the Average Length parameter (default: 21). It reflects the direction of price movement and momentum.

5 — WT2 (WaveTrend 2): A signal line that further smooths WT1 (with a period of 4). It helps confirm signals through crossovers with WT1.

6 — Bands (UpperBand and LowerBand): These form a dynamic channel around the ESA. Their width depends on the level parameter (default: 100). Wider bands result in fewer but more reliable signals. In the original WaveTrend, the oscillator bands use lower values, such as 50 or 60. To achieve classic oscillator signals (more frequent WT1/WT2 crossovers outside the bands), set the level to 50–60.

Trend Identification

The indicator identifies two types of trends:

• Major Trend: Determined by the position of WT1 relative to the ESA. When WT1 is above the ESA, it indicates a bullish trend. When below, it signals a bearish trend. Line and fill colors reflect this trend.

• Mini-Trend: Based on WT1 and WT2 crossovers. When the lines cross, they change to the same color, signaling short-term changes or reversal points. This is ideal for quick trading decisions.

Visuals and Effects

• WT1 and WT2 Lines: Scaled to price and displayed on the price chart for easier analysis.

• Fills: Between the bands (UpperBand/LowerBand) and between WT1/WT2, with a "wave" effect that adjusts transparency based on the trend (green for bullish, red for bearish).

• Signals: Three types—return-to-band, WT1/WT2 crossovers outside the bands, and crossovers inside the bands. Signals are displayed as triangles with different colors for buy and sell.

█ FEATURES

Detailed features of the indicator, aligned with the order of settings in the script:

• Basic Parameters: ESA Length — controls ESA smoothing; Average Length — affects WT1 responsiveness; level (WT Level) — adjusts band width for signal filtering.

• Display Elements: Options to show/hide ESA, bands, WT1/WT2; customizable colors for lines, fills, and the wave effect.

• Signals: Three signal groups (return-to-band, crossovers outside bands, crossovers inside bands) with display and color customization options.

█ HOW TO USE

1 — Add the indicator to your TradingView chart and adjust parameters: — Increase ESA Length and Average Length for low-volatility markets (e.g., stocks), or decrease for cryptocurrencies or forex. — Set level to 50–60 for classic WaveTrend signals with WT1/WT2 crossovers outside bands. The default value of 100 creates wider bands and fewer signals.

2 — Analyze trends: — Major trend (WT1 vs. ESA) shows the overall market direction. — Mini-trends (WT1/WT2 crossovers) help time short-term entries.

3 — Use signals: — Return-to-band: Buy at the lower band, sell at the upper band (mean-reversion). — Crossovers outside bands: Indicate strong momentum (with a lower level, e.g., 50). — Crossovers inside bands: Signal weaker trend changes.

4 — Combine with other tools: Use with volume, RSI, or support/resistance for better decisions. Test on historical data to optimize settings.

Key Indicators Dashboard (KID)Key Indicators Dashboard (KID) — Comprehensive Market & Trend Metrics

📌 Overview

The Key Indicators Dashboard (KID) is an advanced multi-metric market analysis tool designed to consolidate essential technical, volatility, and relative performance data into a single on-chart table. Instead of switching between multiple indicators, KID centralizes these key measures, making it easier to assess a stock’s technical health, volatility state, trend status, and relative strength at a glance.

🛠 Key Features

⦿ Average Daily Range (ADR %): Measures average daily price movement over a specified period. It is calculated by averaging the daily price range (high - low) over a set number of days (default 20 days).

⦿ Average True Range (ATR): Measures volatility by calculating the average of a true range over a specific period (default 14). It helps traders gauge the typical extent of price movement, regardless of the direction.

⦿ ATR%: Expresses the Average True Range as a percentage of the price, which allows traders to compare the volatility of stocks with different prices.

⦿ Relative Strength (RS): Compares a stock’s performance to a chosen benchmark index (default NIFTYMIDSML400) over a specific period (default 50 days).

⦿ RS Score (IBD-style): A normalized 1–100 rating inspired by Investor’s Business Daily methodology.

How it works: The RS Score is based on a weighted average of price changes over 3 months (40%), 6 months (20%), 9 months (20%), and 12 months (20%).

The raw value is converted into a percentage return, then normalized over the past 252 trading days so the lowest value maps to 1 and the highest to 100.

This produces a percentile-style score that highlights the strongest stocks in relative terms.

⦿ Relative Volume (RVol): Compares a stock's current volume to its average volume over a specific period (default 50). It is calculated by dividing the current volume by the average historical volume.

⦿ Average ₹ Volume (Turnover): Represents the total monetary value of shares traded for a stock. It's calculated by multiplying a day's closing price by its volume, with the final value converted to crores for clarity. This metric is a key indicator of a stock's liquidity and overall market interest.

⦿ Moving Average Extension: Measures how far a stock's current price has moved from from a selected moving average (EMA or SMA). This deviation is normalized by the stock's volatility (ATR%), with a default threshold of 6 ATR used to indicate that the stock is significantly extended and is marked with a selected shape (default Red Flag).

⦿ 52-Weeks High & Low: Measures a stock's current price in relation to its highest and lowest prices over the past year. It calculates the percentage a stock is below its 52-week high and above its 52-week low.

⦿ Market Capitalization: Market Cap represents the total value of all outstanding.

⦿ Free Float: It is the value of shares readily available for public trading, with the Free Float Percentage showing the proportion of shares available to the public.

⦿ Trend: Uses Supertrend indicator to identify the current trend of a stock's price. A factor (default 3) and an ATR period (default 10) is used to signal whether the trend is up or down.

⦿ Minervini Trend Template (MTT): It is a set of technical criteria designed to identify stocks in strong uptrends.

Price > 50-DMA > 150-DMA > 200-DMA

200-DMA is trending up for at least 1 month

Price is at least 30% above its 52-week low.

Price is within at least 25 percent of its 52-week high

Table highlights when a stock meets all above criteria.

⦿ Sector & Industry: Display stock's sector and industry, provides categorical classification to assist sector-based analysis. The sector is a broad economic classification, while the industry is a more specific group within that sector.

⦿ Moving Averages (MAs): Plot up to four customizable Moving Averages on a chart. You can independently set the type (Simple or Exponential), the source price, and the length for each MA to help visualize a stock's underlying trend.

MA1: Default 10-EMA

MA2: Default 20-EMA

MA3: Default 50-EMA

MA4: Default 200-EMA

⦿ Moving Average (MA) Crossover: It is a trend signal that occurs when a shorter-term moving average crosses a longer-term one. This script identifies these crossover events and plots a marker on the chart to visually signal a potential change in trend direction.

User-configurable MAs (short and long).

A bullish crossover occurs when the short MA crosses above the long MA.

A bearish crossover occurs when the short MA crosses below the long MA.

⦿ Inside Bar (IB): An Inside Bar is a candlestick whose entire price range is contained within the range of the previous bar. This script identifies this pattern, which often signals consolidation, and visually marks bullish and bearish inside bars on the chart with distinct colors and labels.

⦿ Tightness: Identifies periods of low volatility and price consolidation. It compares the price range over a short lookback period (default 3) to the average daily range (ADR). When the lookback range is smaller than the ADR, the indicator plots a marker on the chart to signal consolidation.

⦿ PowerBar (Purple Dot): Identifies candles with a strong price move on high volume. By default, it plots a purple dot when a stock moves up or down by at least 5% and has a minimum volume of 500,000. More dots indicate higher volatility and liquidity.

⦿ Squeezing Range (SQ): Identifies periods of low volatility, which can often precede a significant price move. It checks if the Bollinger Bands have narrowed to a range that is smaller than the Average True Range (ATR) for a set number of consecutive bars (default 3).

(UpperBB - LowerBB) < (ATR × 2)

⦿ Mark 52-Weeks High and Low: Marks and labels a stock's 52-Week High and Low prices directly on the chart. It draws two horizontal lines extending from the candles where the highest and lowest prices occurred over the past year, providing a clear visual reference for long-term price extremes.

⏳PineScreener Filters

The indicator’s alert conditions act as filters for PineScreener.

Price Filter: Minimum and maximum price cutoffs (default ₹25 - ₹10000).

Daily Price Change Filter: Minimum and maximum daily percent change (default -5% and 5%).

🔔 Built-in Alerts

Supports alert creation for:

ADR%, ATR/ATR %, RS, RS Rating, Turnover

Moving Average Crossover (Bullish/Bearish)

Minervini Trend Template

52-Week High/Low

Inside Bars (Bullish/Bearish)

Tightness

Squeezing Range (SQ)

⚙️ Customizable Visualization

Switchable between vertical or horizontal layout.

Works in dark/light mode

User-configurable to toggle any indicator ON or OFF.

User-configurable Moving (EMA/SMA), Period/Lengths and thresholds.

⦿ (Optional) : For horizontal table orientation increase Top Margin to 16% in Chart (Canvas) settings to avoid chart overlapping with table.

⚡ Add this script to your chart and start making smarter trade decisions today! 🚀

caracalla ema long short signal📌 Indicator Name

caracalla ema long short signal

This script generates long and short trading signals using multiple technical indicators: EMAs, MACD, RSI, Stochastic, and volume.

🔧 Indicators Used

1. Exponential Moving Averages (EMA)

ema5, ema20, ema60, ema120 — used to determine overall trend direction.

2. Trend Confirmation (MA Alignment)

Bullish alignment: ema5 > ema20 > ema60 > ema120

Bearish alignment: ema5 < ema20 < ema60 < ema120

3. Crossover Signals

Golden Cross: ema5 crosses above ema20

Dead Cross: ema5 crosses below ema20

4. MACD

Standard parameters: 12, 26, 9

MACD Long: MACD line crosses above signal line

MACD Short: MACD line crosses below signal line

5. RSI & Stochastic

RSI(14): checks momentum

Stochastic (%K, %D)

Bullish: RSI > 50 and Stochastic %K crosses above %D

Bearish: RSI < 50 and Stochastic %K crosses below %D

6. Volume Filter

20-period simple average volume

Volume Up: Current volume > 120% of average

Volume Down: Current volume < 80% of average

✅ Signal Logic

📈 Long Signal (longSignal)

Triggered when 3 or more of the following are true:

EMA bullish alignment

Golden cross

MACD bullish crossover

RSI > 50 and Stochastic bullish crossover

High volume

📉 Short Signal (shortSignal)

Triggered when 3 or more of the following are true:

EMA bearish alignment

Dead cross

MACD bearish crossover

RSI < 50 and Stochastic bearish crossover

Low volume

📊 Visual Elements

Long Signal: Green “롱” label below the candle

Short Signal: Red “숏” label above the candle

EMA Lines:

EMA5 (Blue)

EMA20 (Orange)

EMA60 (Green)

EMA120 (Red)

SMA50 - Relleno + AlertasThis is about the 50 SMA and its relationship to price. When the price is above the 50 SMA, it is colored green, indicating a bullish trend. If the price is below the 50 SMA, it is colored red, indicating a bearish trend. It also has alerts when the trend crosses the 50 SMA.

FEDFUNDS Rate Divergence Oscillator [BackQuant]FEDFUNDS Rate Divergence Oscillator

1. Concept and Rationale

The United States Federal Funds Rate is the anchor around which global dollar liquidity and risk-free yield expectations revolve. When the Fed hikes, borrowing costs rise, liquidity tightens and most risk assets encounter head-winds. When it cuts, liquidity expands, speculative appetite often recovers. Bitcoin, a 24-hour permissionless asset sometimes described as “digital gold with venture-capital-like convexity,” is particularly sensitive to macro-liquidity swings.

The FED Divergence Oscillator quantifies the behavioural gap between short-term monetary policy (proxied by the effective Fed Funds Rate) and Bitcoin’s own percentage price change. By converting each series into identical rate-of-change units, subtracting them, then optionally smoothing the result, the script produces a single bounded-yet-dynamic line that tells you, at a glance, whether Bitcoin is outperforming or underperforming the policy backdrop—and by how much.

2. Data Pipeline

• Fed Funds Rate – Pulled directly from the FRED database via the ticker “FRED:FEDFUNDS,” sampled at daily frequency to synchronise with crypto closes.

• Bitcoin Price – By default the script forces a daily timeframe so that both series share time alignment, although you can disable that and plot the oscillator on intraday charts if you prefer.

• User Source Flexibility – The BTC series is not hard-wired; you can select any exchange-specific symbol or even swap BTC for another crypto or risk asset whose interaction with the Fed rate you wish to study.

3. Math under the Hood

(1) Rate of Change (ROC) – Both the Fed rate and BTC close are converted to percent return over a user-chosen lookback (default 30 bars). This means a cut from 5.25 percent to 5.00 percent feeds in as –4.76 percent, while a climb from 25 000 to 30 000 USD in BTC over the same window converts to +20 percent.

(2) Divergence Construction – The script subtracts the Fed ROC from the BTC ROC. Positive values show BTC appreciating faster than policy is tightening (or falling slower than the rate is cutting); negative values show the opposite.

(3) Optional Smoothing – Macro series are noisy. Toggle “Apply Smoothing” to calm the line with your preferred moving-average flavour: SMA, EMA, DEMA, TEMA, RMA, WMA or Hull. The default EMA-25 removes day-to-day whips while keeping turning points alive.

(4) Dynamic Colour Mapping – Rather than using a single hue, the oscillator line employs a gradient where deep greens represent strong bullish divergence and dark reds flag sharp bearish divergence. This heat-map approach lets you gauge intensity without squinting at numbers.

(5) Threshold Grid – Five horizontal guides create a structured regime map:

• Lower Extreme (–50 pct) and Upper Extreme (+50 pct) identify panic capitulations and euphoria blow-offs.

• Oversold (–20 pct) and Overbought (+20 pct) act as early warning alarms.

• Zero Line demarcates neutral alignment.

4. Chart Furniture and User Interface

• Oscillator fill with a secondary DEMA-30 “shader” offers depth perception: fat ribbons often precede high-volatility macro shifts.

• Optional bar-colouring paints candles green when the oscillator is above zero and red below, handy for visual correlation.

• Background tints when the line breaches extreme zones, making macro inflection weeks pop out in the replay bar.

• Everything—line width, thresholds, colours—can be customised so the indicator blends into any template.

5. Interpretation Guide

Macro Liquidity Pulse

• When the oscillator spends weeks above +20 while the Fed is still raising rates, Bitcoin is signalling liquidity tolerance or an anticipatory pivot view. That condition often marks the embryonic phase of major bull cycles (e.g., March 2020 rebound).

• Sustained prints below –20 while the Fed is already dovish indicate risk aversion or idiosyncratic crypto stress—think exchange scandals or broad flight to safety.

Regime Transition Signals

• Bullish cross through zero after a long sub-zero stint shows Bitcoin regaining upward escape velocity versus policy.

• Bearish cross under zero during a hiking cycle tells you monetary tightening has finally started to bite.

Momentum Exhaustion and Mean-Reversion

• Touches of +50 (or –50) come rarely; they are statistically stretched events. Fade strategies either taking profits or hedging have historically enjoyed positive expectancy.

• Inside-bar candlestick patterns or lower-timeframe bearish engulfings simultaneously with an extreme overbought print make high-probability short scalp setups, especially near weekly resistance. The same logic mirrors for oversold.

Pair Trading / Relative Value

• Combine the oscillator with spreads like BTC versus Nasdaq 100. When both the FED Divergence oscillator and the BTC–NDQ relative-strength line roll south together, the cross-asset confirmation amplifies conviction in a mean-reversion short.

• Swap BTC for miners, altcoins or high-beta equities to test who is the divergence leader.

Event-Driven Tactics

• FOMC days: plot the oscillator on an hourly chart (disable ‘Force Daily TF’). Watch for micro-structural spikes that resolve in the first hour after the statement; rapid flips across zero can front-run post-FOMC swings.

• CPI and NFP prints: extremes reached into the release often mean positioning is one-sided. A reversion toward neutral in the first 24 hours is common.

6. Alerts Suite