Silver Bullet 5 minutes Box - By KaVeHThis indicator plots high-low range boxes based on selected intraday time windows on the 5-minute chart. It's inspired by the "Silver Bullet" trading concept, highlighting key liquidity grabs and volatility pockets at predefined times. It helps traders visually identify potential smart money trading windows during the New York session and other time anchors.

⚠️ This script only works on the 5-minute chart.

📦 Main Features:

⏰ Customizable Time Boxes:

Define up to 4 separate time windows per day:

3:00 AM – 3:05 AM (New York time) (Box 1)

10:00 AM – 10:05 AM (New York time) (Box 2)

2:00 PM – 2:05 PM (New York time) (Box 3)

8:00 PM – 8:05 PM (New York time) (Box 4)

🎨 Color and Visibility Control:

Each box can be independently toggled and colored for visual distinction.

🕔 New York Time Based:

All timestamps are automatically adjusted to New York Time, aligning with institutional market behavior.

📉 Post-Box Projection:

After each time window closes, a box extends forward 6 hours (72 bars on a 5-minute chart) to highlight the range.

💡 Use Case:

These boxes are best used to:

Detect liquidity sweeps.

Mark potential entry or exit zones.

Track price behavior after specific time-based events.

For example, the 10 AM box is often used to identify setups just after the NYSE open and into the first hour of volatility.

⚠️ TradingView Compliance Notes:

This script is original and does not replicate or resell premium/paid indicators.

All logic is coded from scratch by kaveh_mirmousavi, using public concepts from ICT/Smart Money Trading.

Fully complies with the Mozilla Public License 2.0.

Does not include financial advice or signals — for educational use only.

✅ How to Use:

Apply to a 5-minute chart.

Adjust the desired time boxes in the input panel.

Watch for price action within and after the boxes.

Enjoy and feel free to share feedback or ideas for improvement!

Cerca negli script per "如何用wind搜索股票的发行价和份数"

Harmony in Havoc - The Entropy of VoVix Harmony in Havoc – The Entropy of VoVix

There are moments in the market when chaos and order are not opposites, but partners in a dance.

Harmony in Havoc is not just an indicator—it’s a window into that dance.

Most tools try to tame the market by smoothing it, boxing it in, or chasing after what’s already happened. This script does the opposite: it listens for the music beneath the noise, the rare moments when volatility and unpredictability align, and the market’s next movement is about to begin.

What is Harmony in Havoc?

VoVix Spike:

The pulse of volatility-of-volatility. Not just how much the market is moving, but how violently its own heartbeat is changing.

Entropy:

A real-time measure of surprise. When entropy is high, the market is not just moving—it’s breaking its own patterns, rewriting its own rules.

Progression Bar & Status:

The yellow bar is your visual gauge of tension. As it fills, the market is winding up.

Wait: The world is calm.

Get ready!: The storm is building.

Take Action!!: The probability of a regime eruption is at its peak.

Yellow Background:

When the background glows, the market is at its most unstable—this is not a buy or sell signal, but a quant alert.

How does it work?

Every tick, Harmony in Havoc measures the distance between the market’s current volatility and its own unpredictability. When the VoVix spike approaches or exceeds the entropy threshold, the system knows:

“This is the moment when the improbable becomes possible.”

Why is this different?

It doesn’t tell you what to do.

It doesn’t chase price.

It doesn’t care about trends, bands, or the past.

Instead, it gives you a quantitative sense of anticipation—a way to see when the market is most likely to break from its own history, and when the edge is at its sharpest.

How to use it:

Watch for the yellow background and “Take Action!!” status.

Use it as a regime filter, a volatility dashboard, or a warning system for your own strategies.

Tune the inputs for your asset and timeframe—make it your own.

Inputs—explained for you:

VoVix Fast/Slow ATR & Stdev:

Control how sensitive the system is to volatility shocks. Lower = more signals, higher = only the rarest events.

Entropy Window & Bins:

Control how “surprised” the entropy engine is by current volatility. Shorter window = more responsive, more bins = finer detail.

Show/Hide Controls:

Toggle the VoVix spike, entropy line, and their glows to customize your visual experience.

Bottom line:

This is not a buy or sell script.

This is a quant regime detector for those who want to feel the market’s tension—to sense when harmony and havoc are about to collide.

Disclaimer:

Trading is risky. This script is for research and informational purposes only, not financial advice. Backtest, paper trade, and know your risk before going live. Past performance is not a guarantee of future results.

*I've only tested this on 1 and 5 min frames.

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

3 days ago

Release Notes

* Now mobile friendly. I've added a toggle to switch the dashboard on/off, and added a mobile information line that shows the same information on the dashboard. This is to allow the script to stay visually in balance and this also has a toggle.

* Background color added that coresponds with Buy or Sell areas.

BPCO Z-ScoreBPCO Z-Score with Scaled Z-Value and Table

Description:

This custom indicator calculates the Z-Score of a specified financial instrument (using the closing price as a placeholder for the BPCO value), scales the Z-Score between -2 and +2 based on user-defined thresholds, and displays it in a table for easy reference.

The indicator uses a simple moving average (SMA) and standard deviation to calculate the original Z-Score, and then scales the Z-Score within a specified range (from -2 to +2) based on the upper and lower thresholds set by the user.

Additionally, the scaled Z-Score is displayed in a separate table on the right side of the chart, providing a clear, numerical value for users to track and interpret.

Key Features:

BPCO Z-Score: Calculates the Z-Score using a simple moving average and standard deviation over a user-defined window (default: 365 days). This provides a measure of how far the current price is from its historical average in terms of standard deviations.

Scaled Z-Score: The original Z-Score is then scaled between -2 and +2, based on the user-specified upper and lower thresholds. The thresholds default to 3.5 (upper) and -1.5 (lower), and can be adjusted as needed.

Threshold Bands: Horizontal lines are plotted on the chart to represent the upper and lower thresholds. These help visualize when the Z-Score crosses critical levels, indicating potential market overbought or oversold conditions.

Dynamic Table Display: The scaled Z-Score is shown in a dynamic table at the top-right of the chart, providing a convenient reference for traders. The table updates automatically as the Z-Score fluctuates.

How to Use:

Adjust Time Window: The "Z-Score Period (Days)" input allows you to adjust the time period used for calculating the moving average and standard deviation. By default, this is set to 365 days (1 year), but you can adjust this depending on your analysis needs.

Set Upper and Lower Thresholds: Use the "BPCO Upper Threshold" and "BPCO Lower Threshold" inputs to define the bands for your Z-Score. The default values are 3.5 for the upper band and -1.5 for the lower band, but you can adjust them based on your strategy.

Interpret the Z-Score: The Z-Score provides a standardized measure of how far the current price (or BPCO value) is from its historical mean, relative to the volatility. A value above the upper threshold (e.g., 3.5) may indicate overbought conditions, while a value below the lower threshold (e.g., -1.5) may indicate oversold conditions.

Use the Scaled Z-Score: The scaled Z-Score is calculated based on the original Z-Score, but it is constrained to a range between -2 and +2. When the BPCO value hits the upper threshold (3.5), the scaled Z-Score will be +2, and when it hits the lower threshold (-1.5), the scaled Z-Score will be -2. This gives you a clear, easy-to-read value to interpret the market's condition.

Data Sources:

BPCO Data: In this indicator, the BPCO value is represented by the closing price of the asset. The calculation of the Z-Score and scaled Z-Score is based on this price data, but you can modify it to incorporate other data streams as needed (e.g., specific economic indicators or custom metrics).

Indicator Calculation: The Z-Score is calculated using the following formulas:

Mean (SMA): A simple moving average of the BPCO (close price) over the selected period (365 days by default).

Standard Deviation (Std): The standard deviation of the BPCO (close price) over the same period.

Z-Score: (Current BPCO - Mean) / Standard Deviation

Scaled Z-Score: The Z-Score is normalized to fall within a specified range (from -2 to +2), based on the upper and lower threshold inputs.

Important Notes:

Customization: The indicator allows users to adjust the period (window) for calculating the Z-Score, as well as the upper and lower thresholds to suit different timeframes and trading strategies.

Visual Aids: Horizontal lines are drawn to represent the upper and lower threshold levels, making it easy to visualize when the Z-Score crosses critical levels.

Limitations: This indicator relies on historical price data (or BPCO) and assumes that the standard deviation and mean are representative of future price behavior. It does not account for potential market shifts or extreme events that may fall outside historical norms.

Pump Detector - EMA 4H + Retest H1 (Valid 10x4H bars)📈 Pump Detector – EMA 12/21 on 4H + Retest on H1

This indicator is designed to detect sudden bullish moves ("pumps") on the 4-hour timeframe, and alert traders of potential retest entry points on the 1-hour timeframe.

🔍 Pump activation conditions (on 4H):

EMA 12 crosses above EMA 21

Current volume exceeds the 20-period SMA of volume (on 4H)

When both conditions are met, a pump alert is triggered and a time window opens.

📉 Retest detection logic (on H1):

For the next 10 bars on the 4H chart (~40 hours), the indicator monitors price behavior on the 1H timeframe

If the LOW of any H1 candle touches or drops below EMA 12 or 21 (on H1), a second alert is triggered

✅ Key Features:

Draws EMA 12/21 from the 4H timeframe directly on the chart

Enforces 4H and H1 timeframes, regardless of the chart the script is applied to

One-time detection per pump window: once the 10-bar window expires, the retest alert is disabled until a new pump is detected

Ideal for capturing momentum breakouts followed by technical pullbacks

⚠️ Recommended for:

Traders looking for scalping or swing trading setups on crypto, forex, or stocks. Helps identify post-breakout entry opportunities using a structured and disciplined approach.

Entropy Chart Analysis [PhenLabs]📊 Entropy Chart analysis -

Version: PineScript™ v6

📌 Description

The Entropy Chart indicator analysis applies Approximate Entropy (ApEn) to identify zones of potential support and resistance on your price chart. It is designed to locate changes in the market’s predictability, with a focus on zones near significant psychological price levels (e.g., multiples of 50). By quantifying entropy, the indicator aims to identify zones where price action might stabilize (potential support) or become randomized (potential resistance).

This tool automates the visualization of these key areas for traders, which may have the effect of revealing reversal levels or consolidation zones that would be hard to discern through traditional means. It also filters the signals by proximity to key levels in an attempt to reduce noise and highlight higher-probability setups. These dynamic zones adapt to changing market conditions by stretching, merging, and expiring based on user-inputted rules.

🚀 Points of Innovation

Combines Approximate Entropy (ApEn) calculation with price action near significant levels.

Filters zone signals based on proximity (in ticks) to predefined significant price levels (multiples of 50).

Dynamically merges overlapping or nearby zones to consolidate signals and reduce chart clutter.

Uses ApEn crossovers relative to its moving average as the core trigger mechanism.

Provides distinct visual coloring for bullish, bearish, and merged (mixed-signal) zones.

Offers comprehensive customization for entropy calculation, zone sensitivity, level filtering, and visual appearance.

🔧 Core Components

Approximate Entropy (ApEn) Calculation : Measures the regularity or randomness of price fluctuations over a specified window. Low ApEn suggests predictability, while high ApEn suggests randomness.

Zone Trigger Logic : Creates potential support zones when ApEn crosses below its average (indicating increasing predictability) and potential resistance zones when it crosses above (indicating increasing randomness).

Significant Level Filter : Validates zone triggers only if they occur within a user-defined tick distance from significant price levels (multiples of 50).

Dynamic Zone Management : Automatically creates, extends, merges nearby zones based on tick distance, and removes the oldest zones to maintain a maximum limit.

Zone Visualization : Draws and updates colored boxes on the chart to represent active support, resistance, or mixed zones.

🔥 Key Features

Entropy-Based S/R Detection : Uses ApEn to identify potential support (low entropy) and resistance (high entropy) areas.

Significant Level Filtering : Enhances signal quality by focusing on entropy changes near key psychological price points.

Automatic Zone Drawing & Merging : Visualizes zones dynamically, merging close signals for clearer interpretation.

Highly Customizable : Allows traders to adjust parameters for ApEn calculation, zone detection thresholds, level filter sensitivity, merging distance, and visual styles.

Integrated Alerts : Provides built-in alert conditions for the formation of new bullish or bearish zones near significant levels.

Clear Visual Output : Uses distinct, customizable colors for buy (support), sell (resistance), and mixed (merged) zones.

🎨 Visualization

Buy Zones : Represented by greenish boxes (default: #26a69a), indicating potential support areas formed during low entropy periods near significant levels.

Sell Zones : Represented by reddish boxes (default: #ef5350), indicating potential resistance areas formed during high entropy periods near significant levels.

Mixed Zones : Represented by bluish/purple boxes (default: #8894ff), formed when a buy zone and a sell zone merge, indicating areas of potential consolidation or conflict.

Dynamic Extension : Active zones are automatically extended to the right with each new bar.

📖 Usage Guidelines

Calculation Parameters

Window Length

Default: 15

Range: 10-100

Description: Lookback period for ApEn calculation. Shorter lengths are more responsive; longer lengths are smoother.

Embedding Dimension (m)

Default: 2

Range: 1-6

Description: Length of patterns compared in ApEn calculation. Higher values detect more complex patterns but require more data.

Tolerance (r)

Default: 0.5

Range: 0.1-1.0 (step 0.1)

Description: Sensitivity factor for pattern matching (as a multiple of standard deviation). Lower values require closer matches (more sensitive).

Zone Settings

Zone Lookback

Default: 5

Range: 5-50

Description: Lookback period for the moving average of ApEn used in threshold calculations.

Zone Threshold

Default: 0.5

Range: 0.5-3.0

Description: Multiplier for the ApEn average to set crossover trigger levels. Higher values require larger ApEn deviations to create zones.

Maximum Zones

Default: 5

Range: 1-10

Description: Maximum number of active zones displayed. The oldest zones are removed first when the limit is reached.

Zone Merge Distance (Ticks)

Default: 5

Range: 1-50

Description: Maximum distance in ticks for two separate zones to be merged into one.

Level Filter Settings

Tick Size

Default: 0.25

Description: The minimum price increment for the asset. Must be set correctly for the specific instrument to ensure accurate level filtering.

Max Ticks Distance from Levels

Default: 40

Description: Maximum allowed distance (in ticks) from a significant level (multiple of 50) for a zone trigger to be valid.

Visual Settings

Buy Zone Color : Default: color.new(#26a69a, 83). Sets the fill color for support zones.

Sell Zone Color : Default: color.new(#ef5350, 83). Sets the fill color for resistance zones.

Mixed Zone Color : Default: color.new(#8894ff, 83). Sets the fill color for merged zones.

Buy Border Color : Default: #26a69a. Sets the border color for support zones.

Sell Border Color : Default: #ef5350. Sets the border color for resistance zones.

Mixed Border Color : Default: color.new(#a288ff, 50). Sets the border color for mixed zones.

Border Width : Default: 1, Range: 1-3. Sets the thickness of zone borders.

✅ Best Use Cases

Identifying potential support/resistance near significant psychological price levels (e.g., $50, $100 increments).

Detecting potential market turning points or consolidation zones based on shifts in price predictability.

Filtering entries or exits by confirming signals occurring near significant levels identified by the indicator.

Adding context to other technical analysis approaches by highlighting entropy-derived zones.

⚠️ Limitations

Parameter Dependency : Indicator performance is sensitive to parameter settings ( Window Length , Tolerance , Zone Threshold , Max Ticks Distance ), which may need optimization for different assets and timeframes.

Volatility Sensitivity : High market volatility or erratic price action can affect ApEn calculations and potentially lead to less reliable zone signals.

Fixed Level Filter : The significant level filter is based on multiples of 50. While common, this may not capture all relevant levels for every asset or market condition. Accurate Tick Size input is essential.

Not Standalone : Should be used in conjunction with other analysis methods (price action, volume, other indicators) for confirmation, not as a sole basis for trading decisions.

💡 What Makes This Unique

Entropy + Level Context : Uniquely combines ApEn analysis with a specific filter for proximity to significant price levels (multiples of 50), adding locational context to entropy signals.

Intelligent Zone Merging : Automatically consolidates nearby buy/sell zones based on tick distance, simplifying visual analysis and highlighting stronger confluence areas.

Targeted Signal Generation : Focuses alerts and zone creation on specific market conditions (entropy shifts near key levels).

🔬 How It Works

Calculate Entropy : The script computes the Approximate Entropy (ApEn) of the closing prices over the defined Window Length to quantify price predictability.

Check Triggers : It monitors ApEn relative to its moving average. A crossunder below a calculated threshold (avg_apen / zone_threshold) indicates potential support; a crossover above (avg_apen * zone_threshold) indicates potential resistance.

Filter by Level : A potential zone trigger is confirmed only if the low (for support) or high (for resistance) of the trigger bar is within the Max Ticks Distance of a significant price level (multiple of 50).

Manage & Draw Zones : If a trigger is confirmed, a new zone box is created. The script checks for overlaps with existing zones within the Zone Merge Distance and merges them if necessary. Zones are extended forward, and the oldest are removed to respect the Maximum Zones limit. Active zones are drawn and updated on the chart.

💡 Note:

Crucially, set the Tick Size parameter correctly for your specific trading instrument in the “Level Filter Settings”. Incorrect Tick Size will make the significant level filter inaccurate.

Experiment with parameters, especially Window Length , Tolerance (r) , Zone Threshold , and Max Ticks Distance , to tailor the indicator’s sensitivity to your preferred asset and timeframe.

Always use this indicator as part of a comprehensive trading plan, incorporating risk management and seeking confirmation from other analysis techniques.

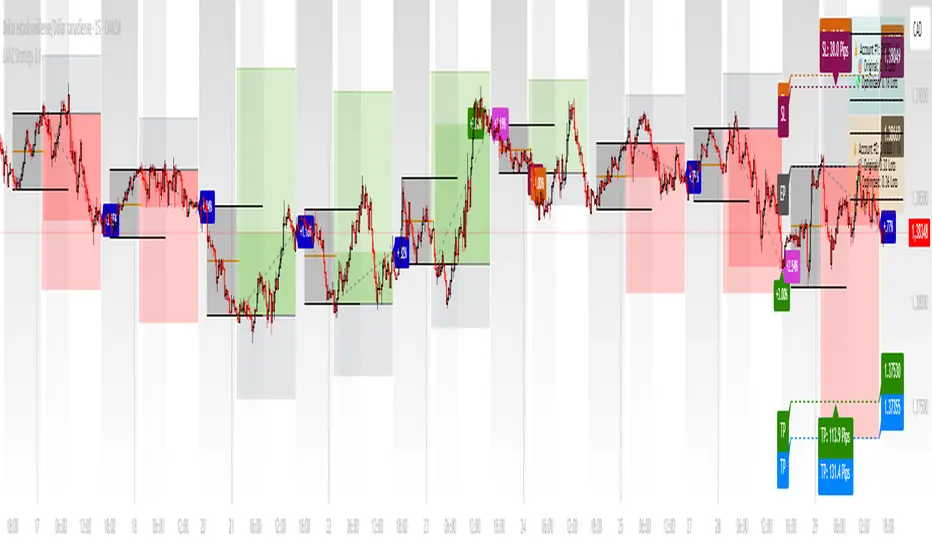

LANZ Strategy 3.0🔷 LANZ Strategy 3.0 — Asian Range Fibonacci Strategy with Execution Window Logic

LANZ Strategy 3.0 is a rule-based trading system that utilizes the Asian session range to project Fibonacci levels and manage entries during a defined execution window. Designed for Forex and index traders, this strategy focuses on structured price behavior around key levels before the New York session.

🧠 Core Components:

Asian Session Range Mapping: Automatically detects the high, low, and midpoint during the Asian session.

Fibonacci Level Projection: Projects configurable Fibonacci retracement and extension levels based on the Asian range.

Execution Window Logic: Uses the 01:15 NY candle as a reference to validate potential reversals or continuation setups.

Conditional Entry System: Includes logic for limit order entries (buy or sell) at specific Fib levels, with reversal logic if price breaks structure before execution.

Risk Management: Entry orders are paired with dynamic SL and TP based on Fibonacci-based distances, maintaining a risk-reward ratio consistent with intraday strategies.

📊 Visual Features:

Asian session high/low/mid lines.

Fibonacci levels: Original (based on raw range) and Optimized (user-adjustable).

Session background coloring for Asia, Execution Window, and NY session.

Labels and lines for entry, SL, and TP targets.

Dynamic deletion of untriggered orders after execution window expires.

⚙️ How It Works:

The script calculates the Asian session range.

Projects Fibonacci levels from the range.

Waits for the 01:15 NY candle to close to validate a signal.

If valid, a limit entry order (BUY or SELL) is plotted at the selected level.

If price structure changes (e.g., breaks the high/low), reversal logic may activate.

If no trade is triggered, orders are cleared before the NY session.

🔔 Alerts:

Alerts trigger when a valid setup appears after 01:15 NY candle.

Optional alerts for order activation, SL/TP hit, or trade cancellation.

📝 Notes:

Intended for semi-automated or discretionary trading.

Best used on highly liquid markets like Forex majors or indices.

Script parameters include session times, Fib ratios, SL/TP settings, and reversal logic toggle.

Credits:

Developed by LANZ, this script merges traditional session-based analysis with Fibonacci tools and structured execution timing, offering a unique framework for morning volatility plays.

DrawIndicatorOnTheChartLibrary "DrawIndicatorOnTheChart"

this library is used to show an indicator (such RSI, CCI, MOM etc) on the main chart with indicator's horizontal lines in a window. Location of the window is calculated dynamically by last price movemements

drawIndicator(enabled, indicatorName, indicator1, indicator2, indicator3, indicatorcolors, period, indimax_, indimin_, levels, precision, xlocation, lnwidth)

draws the realted indicator on the chart

Parameters:

enabled (bool) : if it's enabled to show

indicatorName (string) : is the indicator name as string such "RSI", "CCI" etc

indicator1 (float) : is first indicator you want to show, such rsi(close, 14), mom(close, 10) etc

indicator2 (float) : is second indicator you want to show, such -DI of DMI

indicator3 (float) : is third indicator you want to show, such ADX of DMI

indicatorcolors (array)

period (int) : is the length of the window to show

indimax_ (float) : is the maximum value of the indicator, for example for RSI it's 100.0, if the indicator (such CCI, MOM etc) doesn't have maximum value then use "na"

indimin_ (float) : is the minimum value of the indicator, for example for RSI it's 0.0, if the indicator (such CCI, MOM etc)doesn't have maximum value then use "na"

levels (array) : is the levels of the array for the horizontal lines. for example if you want horizontal lines at 30.0, and 70.0 then use array.from(30.0, 70.0). if no horizontal lines then use array.from(na)

precision (int) : is the precision/nuber of decimals that is used to show indicator values, for example for RSI set it 2

xlocation (int) : is end location of the indicator window, for example if xlocation = 0 window is created on the index of the last bar/candle

lnwidth (int) : is the line width of the indicator lines

Returns: none

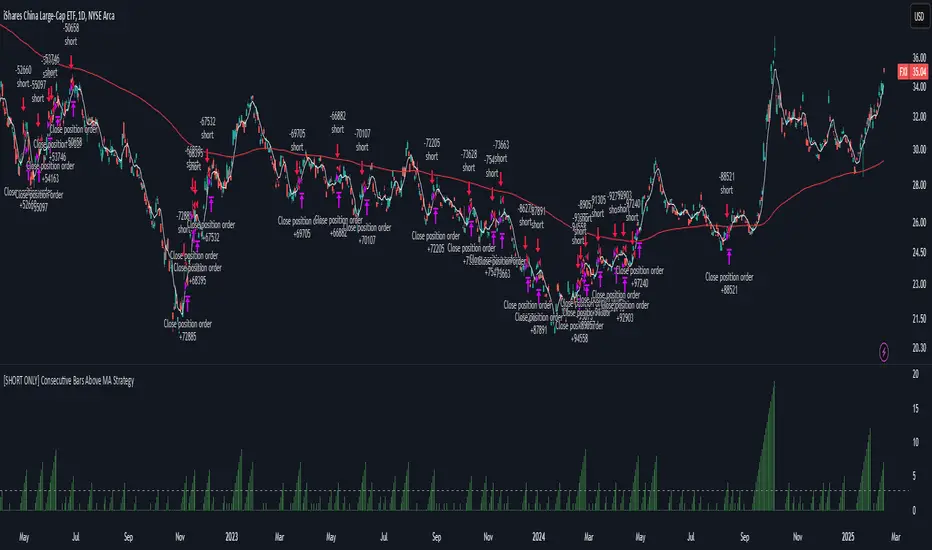

[SHORT ONLY] Consecutive Bars Above MA Strategy█ STRATEGY DESCRIPTION

The "Consecutive Bars Above MA Strategy" is a contrarian trading system aimed at exploiting overextended bullish moves in stocks and ETFs. It monitors the number of consecutive bars that close above a chosen short-term moving average (which can be either a Simple Moving Average or an Exponential Moving Average). Once the count reaches a preset threshold and the current bar’s close exceeds the previous bar’s high within a designated trading window, a short entry is initiated. An optional EMA filter further refines entries by requiring that the current close is below the 200-period EMA, helping to ensure that trades are taken in a bearish environment.

█ HOW ARE THE CONSECUTIVE BULLISH COUNTS CALCULATED?

The strategy utilizes a counter variable, `bullCount`, to track consecutive bullish bars based on their relation to the short-term moving average. Here’s how the count is determined:

Initialize the Counter

The counter is initialized at the start:

var int bullCount = na

Bullish Bar Detection

For each bar, if the close is above the selected moving average (either SMA or EMA, based on user input), the counter is incremented:

bullCount := close > signalMa ? (na(bullCount) ? 1 : bullCount + 1) : 0

Reset on Non-Bullish Condition

If the close does not exceed the moving average, the counter resets to zero, indicating a break in the consecutive bullish streak.

█ SIGNAL GENERATION

1. SHORT ENTRY

A short signal is generated when:

The number of consecutive bullish bars (i.e., bars closing above the short-term MA) meets or exceeds the defined threshold (default: 3).

The current bar’s close is higher than the previous bar’s high.

The signal occurs within the specified trading window (between Start Time and End Time).

Additionally, if the EMA filter is enabled, the entry is only executed when the current close is below the 200-period EMA.

2. EXIT CONDITION

An exit signal is triggered when the current close falls below the previous bar’s low, prompting the strategy to close the short position.

█ ADDITIONAL SETTINGS

Threshold: The number of consecutive bullish bars required to trigger a short entry (default is 3).

Trading Window: The Start Time and End Time inputs define when the strategy is active.

Moving Average Settings: Choose between SMA and EMA, and set the MA length (default is 5), which is used to assess each bar’s bullish condition.

EMA Filter (Optional): When enabled, this filter requires that the current close is below the 200-period EMA, supporting entries in a downtrend.

█ PERFORMANCE OVERVIEW

This strategy is designed for stocks and ETFs and can be applied across various timeframes.

It seeks to capture mean reversion by shorting after a series of bullish bars suggests an overextended move.

The approach employs a contrarian short entry by waiting for a breakout (close > previous high) following consecutive bullish bars.

The adjustable moving average settings and optional EMA filter allow for further optimization based on market conditions.

Comprehensive backtesting is recommended to fine-tune the threshold, moving average parameters, and filter settings for optimal performance.

Anomaly DetectorPrice Anomaly Detector

This is a script designed to identify unusual price movements. By analyzing deviations from typical price behavior, this tool helps traders spot potential trading opportunities and manage risks effectively.

---

Features

- Anomaly Detection: Flags price points that significantly deviate from the average.

- Visual Indicators: Highlights anomalies with background colors and cross markers.

- Customizable Settings: Adjust sensitivity and window size to match your trading strategy.

- Real-Time Analysis: Continuously updates anomaly signals as new data is received.

---

Usage

After adding the indicator to your chart:

1. View Anomalies: Red backgrounds and cross markers indicate detected anomalies.

2. Adjust Settings: Modify the `StdDev Threshold` and `Window Length` to change detection sensitivity.

3. Interpret Signals:

- Red Background: Anomaly detected on that bar.

- Red Cross: Specific point of anomaly.

---

Inputs

- StdDev Threshold: Higher values reduce anomaly sensitivity. Default: 2.0.

- Window Length: Larger windows smooth data, reducing false positives. Default: 20.

---

Limitations

- Approximation Method: Uses a simple method to detect anomalies, which may not capture all types of unusual price movements.

- Performance: Extremely large window sizes may impact script performance.

- Segment Detection: Does not group consecutive anomalies into segments.

---

Disclaimer : This tool is for educational purposes only. Trading involves risk, and you should perform your own analysis before making decisions. The author is not liable for any losses incurred.

SPY/TLT Strategy█ STRATEGY OVERVIEW

The "SPY/TLT Strategy" is a trend-following crossover strategy designed to trade the relationship between TLT and its Simple Moving Average (SMA). The default configuration uses TLT (iShares 20+ Year Treasury Bond ETF) with a 20-period SMA, entering long positions on bullish crossovers and exiting on bearish crossunders. **This strategy is NOT optimized and performs best in trending markets.**

█ KEY FEATURES

SMA Crossover System: Uses price/SMA relationship for signal generation (Default: 20-period)

Dynamic Time Window: Configurable backtesting period (Default: 2014-2099)

Equity-Based Position Sizing: Default 100% equity allocation per trade

Real-Time Visual Feedback: Price/SMA plot with trend-state background coloring

Event-Driven Execution: Processes orders at bar close for accurate backtesting

█ SIGNAL GENERATION

1. LONG ENTRY CONDITION

TLT closing price crosses ABOVE SMA

Occurs within specified time window

Generates market order at next bar open

2. EXIT CONDITION

TLT closing price crosses BELOW SMA

Closes all open positions immediately

█ ADDITIONAL SETTINGS

SMA Period: Simple Moving Average length (Default: 20)

Start Time and End Time: The time window for trade execution (Default: 1 Jan 2014 - 1 Jan 2099)

Security Symbol: Ticker for analysis (Default: TLT)

█ PERFORMANCE OVERVIEW

Ideal Market Conditions: Strong trending environments

Potential Drawbacks: Whipsaws in range-bound markets

Backtesting results should be analyzed to optimize the MA Period and EMA Filter settings for specific instruments

Multi-Step Vegas SuperTrend - strategy [presentTrading]Long time no see! I am back : ) Please allow me to gain some warm-up.

█ Introduction and How it is Different

The "Vegas SuperTrend Strategy" is an enhanced trading strategy that leverages both the Vegas Channel and SuperTrend indicators to generate buy and sell signals.

What sets this strategy apart from others is its dynamic adjustment to market volatility and its multi-step take profit mechanism. Unlike traditional single-step profit-taking approaches, this strategy allows traders to systematically scale out of positions at predefined profit levels, thereby optimizing their risk-reward ratio and maximizing potential gains.

BTCUSD 6hr performance

█ Strategy, How it Works: Detailed Explanation

The Vegas SuperTrend Strategy combines the strengths of the Vegas Channel and SuperTrend indicators to identify market trends and generate trade signals. The following subsections delve into the details of how each component works and how they are integrated.

🔶 Vegas Channel Calculation

The Vegas Channel is based on a simple moving average (SMA) and the standard deviation (STD) of the closing prices over a specified period. The channel is defined by upper and lower bounds that are dynamically adjusted based on market volatility.

Simple Moving Average (SMA):

SMA_vegas = (1/N) * Σ(Close_i) for i = 0 to N-1

where N is the length of the Vegas Window.

Standard Deviation (STD):

STD_vegas = sqrt((1/N) * Σ(Close_i - SMA_vegas)^2) for i = 0 to N-1

Vegas Channel Upper and Lower Bounds:

VegasChannelUpper = SMA_vegas + STD_vegas

VegasChannelLower = SMA_vegas - STD_vegas

The details are here:

🔶 Trend Detection and Trade Signals

The strategy determines the current market trend based on the closing price relative to the SuperTrend bounds:

Market Trend:

MarketTrend = 1 if Close > SuperTrendPrevLower

-1 if Close < SuperTrendPrevUpper

Previous Trend otherwise

Trade signals are generated when there is a shift in the market trend:

Bullish Signal: When the market trend shifts from -1 to 1.

Bearish Signal: When the market trend shifts from 1 to -1.

🔶 Multi-Step Take Profit Mechanism

The strategy incorporates a multi-step take profit mechanism that allows for partial exits at predefined profit levels. This helps in locking in profits gradually and reducing exposure to market reversals.

Take Profit Levels:

The take profit levels are calculated as percentages of the entry price:

TakeProfitLevel_i = EntryPrice * (1 + TakeProfitPercent_i/100) for long positions

TakeProfitLevel_i = EntryPrice * (1 - TakeProfitPercent_i/100) for short positions

Multi-steps take profit local picture:

█ Trade Direction

The trade direction can be customized based on the user's preference:

Long: The strategy only takes long positions.

Short: The strategy only takes short positions.

Both: The strategy can take both long and short positions based on the market trend.

█ Usage

To use the Vegas SuperTrend Strategy, follow these steps:

Configure Input Settings:

- Set the ATR period, Vegas Window length, SuperTrend Multiplier, and Volatility Adjustment Factor.

- Choose the desired trade direction (Long, Short, Both).

- Enable or disable the take profit mechanism and set the take profit percentages and amounts for each step.

█ Default Settings

The default settings of the strategy are designed to provide a balanced approach to trading. Below is an explanation of each setting and its effect on the strategy's performance:

ATR Period (10): This setting determines the length of the ATR used in the SuperTrend calculation. A longer period smoothens the ATR, making the SuperTrend less sensitive to short-term volatility. A shorter period makes the SuperTrend more responsive to recent price movements.

Vegas Window Length (100): This setting defines the period for the Vegas Channel's moving average. A longer window provides a broader view of the market trend, while a shorter window makes the channel more responsive to recent price changes.

SuperTrend Multiplier (5): This base multiplier adjusts the sensitivity of the SuperTrend to the ATR. A higher multiplier makes the SuperTrend less sensitive, reducing the frequency of trade signals. A lower multiplier increases sensitivity, generating more signals.

Volatility Adjustment Factor (5): This factor dynamically adjusts the SuperTrend multiplier based on the width of the Vegas Channel. A higher factor increases the sensitivity of the SuperTrend to changes in market volatility, while a lower factor reduces it.

Take Profit Percentages (3.0%, 6.0%, 12.0%, 21.0%): These settings define the profit levels at which portions of the trade are exited. They help in locking in profits progressively as the trade moves in favor.

Take Profit Amounts (25%, 20%, 10%, 15%): These settings determine the percentage of the position to exit at each take profit level. They are distributed to ensure that significant portions of the trade are closed as the price reaches the set levels, reducing exposure to reversals.

Adjusting these settings can significantly impact the strategy's performance. For instance, increasing the ATR period or the SuperTrend multiplier can reduce the number of trades, potentially improving the win rate but also missing out on some profitable opportunities. Conversely, lowering these values can increase trade frequency, capturing more short-term movements but also increasing the risk of false signals.

Fusion MFI RSIHello fellas,

This superb indicator summons two monsters called Relative Strength Index (RSI) and Money Flow Index (MFI) and plays the Yu-Gi-Oh! card "Polymerization" to combine them.

Overview

The Fusion MFI RSI Indicator is an advanced analytical tool designed to provide a nuanced understanding of market dynamics by combining the Relative Strength Index (RSI) and the Money Flow Index (MFI). Enhanced with sophisticated smoothing techniques and the Inverse Fisher Transform (IFT), this indicator excels in identifying key market conditions such as overbought and oversold states, trends, and potential reversal points.

Key Features (Brief Overview)

Fusion of RSI and MFI: Integrates momentum and volume for a comprehensive market analysis.

Advanced Smoothing Techniques: Employs Hann Window, Jurik Moving Average (JMA), T3 Smoothing, and Super Smoother to refine signals.

Inverse Fisher Transform (IFT) Enhances the clarity and distinctiveness of indicator outputs.

Detailed Feature Analysis

Fusion of RSI and MFI

RSI (Relative Strength Index): Developed by J. Welles Wilder Jr., the RSI measures the speed and magnitude of directional price movements. Wilder recommended using a 14-day period and identified overbought conditions above 70 and oversold conditions below 30.

MFI (Money Flow Index): Created by Gene Quong and Avrum Soudack, the MFI combines price and volume to measure trading pressure. It is typically calculated using a 14-day period, with over 80 considered overbought and under 20 as oversold.

Application in Fusion: By combining RSI and MFI, the indicator leverages RSI's sensitivity to price changes with MFI's volume-weighted confirmation, providing a robust analysis tool. This combination is particularly effective in confirming the strength behind price movements, making the signals more reliable.

Advanced Smoothing Techniques

Hann Window: Traditionally used to reduce the abrupt data discontinuities at the edges of a sample, it is applied here to smooth the price data.

Jurik Moving Average (JMA): Known for preserving the timing and smoothness of the data, JMA reduces market noise effectively without significant lag.

T3 Smoothing: Developed to respond quickly to market changes, T3 provides a smoother response to price fluctuations.

Super Smoother: Filters out high-frequency noise while retaining important trends.

Application in Fusion: These techniques are chosen to refine the output of the combined RSI and MFI values, ensuring the indicator remains responsive yet stable, providing clearer and more actionable signals.

Inverse Fisher Transform (IFT):

Developed by John Ehlers, the IFT transforms oscillator outputs to enhance the clarity of extreme values. This is particularly useful in this fusion indicator to make critical turning points more distinct and actionable.

Mathematical Calculations for the Fusion MFI RSI Indicator

RSI (Relative Strength Index)

The RSI is calculated using the following steps:

Average Gain and Average Loss: First, determine the average gain and average loss over the specified period (typically 14 days). This is done by summing all the gains and losses over the period and then dividing each by the period.

Average Gain = (Sum of Gains over the past 14 periods) / 14

Average Loss = (Sum of Losses over the past 14 periods) / 14

Relative Strength (RS): This is the ratio of average gain to average loss.

RS = Average Gain / Average Loss

RSI: Finally, the RSI is calculated using the RS value:

RSI = 100 - (100 / (1 + RS))

MFI (Money Flow Index)

The MFI is calculated using several steps that incorporate both price and volume:

Typical Price: Calculate the typical price for each period.

Typical Price = (High + Low + Close) / 3

Raw Money Flow: Multiply the typical price by the volume for the period.

Raw Money Flow = Typical Price * Volume

Positive and Negative Money Flow: Compare the typical price of the current period to the previous period to determine if the money flow is positive or negative.

If today's Typical Price > Yesterday's Typical Price, then Positive Money Flow = Raw Money Flow; Negative Money Flow = 0

If today's Typical Price < Yesterday's Typical Price, then Negative Money Flow = Raw Money Flow; Positive Money Flow = 0

Money Flow Ratio: Calculate the ratio of the sum of Positive Money Flows to the sum of Negative Money Flows over the past 14 periods.

Money Flow Ratio = (Sum of Positive Money Flows over 14 periods) / (Sum of Negative Money Flows over 14 periods)

MFI: Finally, calculate the MFI using the Money Flow Ratio.

MFI = 100 - (100 / (1 + Money Flow Ratio))

Fusion of RSI and MFI

The final Fusion MFI RSI value could be calculated by averaging the IFT-transformed values of RSI and MFI, providing a single oscillator value that reflects both momentum and volume-weighted price action:

Fusion MFI RSI = (MFI weight * MFI) + (RSI weight * RSI)

Suggested Settings and Trading Rules

Original Usage

RSI: Wilder suggested buying when the RSI moves above 30 from below (enter long) and selling when the RSI moves below 70 from above (enter short). He recommended exiting long positions when the RSI reaches 70 or higher and exiting short positions when the RSI falls below 30.

MFI: Quong and Soudack recommended buying when the MFI is below 20 and starts rising (enter long), and selling when it is above 80 and starts declining (enter short). They suggested exiting long positions when the MFI reaches 80 or higher and exiting short positions when the MFI falls below 20.

Fusion Application

Settings: Use a 14-day period for this indicator's calculations to maintain consistency with the original settings suggested by the inventors.

Trading Rules:

Enter Long Signal: Consider entering a long position when both RSI and MFI are below their respective oversold levels and begin to rise. This indicates strong buying pressure supported by both price momentum and volume.

Exit Long Signal: Exit the long position when either RSI or MFI reaches its respective overbought threshold, suggesting a potential reversal or decrease in buying pressure.

Enter Short Signal: Consider entering a short position when both indicators are above their respective overbought levels and begin to decline, suggesting that selling pressure is mounting.

Exit Short Signal: Exit the short position when either RSI or MFI falls below its respective oversold threshold, indicating diminishing selling pressure and a potential upward reversal.

How to Use the Indicator

Select Source and Timeframe: Choose the data source and the timeframe for analysis.

Configure Fusion Settings: Adjust the weights for RSI and MFI.

Choose Smoothing Technique: Select and configure the desired smoothing method to suit the market conditions and personal preference.

Enable Fisherization: Optionally apply the Inverse Fisher Transform to enhance signal clarity.

Customize Visualization: Set up gradient coloring, background plots, and bands according to your preferences.

Interpret the Indicator: Use the Fusion value and visual cues to identify market conditions and potential trading opportunities.

Conclusion

The Fusion MFI RSI Indicator integrates classical and modern technical analysis concepts to provide a comprehensive tool for market analysis. By combining RSI and MFI with advanced smoothing techniques and the Inverse Fisher Transform, this indicator offers enhanced insights, aiding traders in making more informed and timely trading decisions. Customize the settings to align with your trading strategy and leverage this powerful tool to navigate financial markets effectively.

Best regards,

simwai

---

Credits to:

@loxx – T3

@everget – JMA

@cheatcountry – Hann Window

Volume Footprint Voids [BigBeluga]Volume Footprint Voids is a unique tool that uses lower timeframe calculation to plot different styles of single candle POC.

This indicator is very powerful for scalping and finding very precise entry and exits, spotting potential trapped traders, and more.

Unlike many other volume profiles, this aims to plot single candle profiles as well as their own footprints.

🔶 FEATURES

The script includes the following settings:

Windows: Plotting style and calculations

Coloring modes

Display modes

lower-timeframe calculations

🔶 CALCULATION

In the image above we can see how the script calculates each level position that will serve as a calculation process to see how much volume/closes there are within the levels.

In the image above, we can have a more clear example of how we count each candle close.

We use the prior screenshot as an example, after setting each level we will use the lower-timeframe input to measure the amount of closes within the ranges.

Depending on the lot size, the box will be larger or smaller, usually the POC will always have the highest box size.

NOTE: Size is the starting point, always from the low of the candle.

To find more voids, select a closer LTF to the current one you're using.

To find fewer voids, select a timeframe away from your current one.

Due to Pine Script limitations, we are only able to plot a certain amount of footprints, and we can't plot the whole history chart.

POC will be the largest block displayed, indicating the time point of control

Gray areas are closes above the average

Black are Void or imbalance that price will fill in the future, like FVG

The image above shows an incorrect size input that will lead to bad calculations, while on the other side, a correct size input that will lead to a clear vision and better calculation.

🔶 WINDOWS

The "▲▼" Mode will display delta buyers and delta sellers coloring with voids as black.

It also offers a gradient mode for a beautier visualization

The "Total Volume" mode will display the net volume within the lot size (closes within the levels).

This is useful to spot possible highest net volume within the same highest lot size.

The "POC + Gaps" will show both POC and Gaps as the highest block while all the rest will be considered as the smaller block.

This is useful to see where the highest lot were and if there are higher or lower imbalances within the candle

The last option "Gaps" will simply display the gaps as the highest block, while the POC as the lowest block.

This is useful to have a better view of the gaps areas

🔶 EXAMPLE

This is one of the most basic examples of how this script can be used. POC at the bottom creating a strong support area as price holds and creates higher voids gap that price fills while rising.

🔶 SETTINGS

Users have full control over the script, from colors to choosing the lower-timeframe inputs to disabling the lot size.

LIT - TimingIntroduction

This Script displays the Asia Session Range, the London Open Inducement Window, the NY Open Inducement Window, the Previous Week's high and low, the Previous Day's highs and lows, and the Day Open price in the cleanest way possible.

Description

The Indicator is based on UTC -7 timing but displays the Session Boxes automatically correct at your chart so you do not have to adjust any timings based on your Time Zone and don't have to do any calculations based on your UTC. It is already perfect.

You will see on default settings the purple Asia Box and 2 grey boxes, the first one is for the London Open Inducement Window (1 hour) and the second grey box is for the NY Open Inducement Window (also 1 hour)

Asia Range comes with default settings with the Asia Range high, low, and midline, you can remove these 3 lines in the settings "style" and untick the "Lines" box, that way you only will have the boxes displayed.

Special Feature

Most Timing-based Indicators have "bugged" boxes or don't show clean boxes at all and don't adjust at daylight savings times, we made sure that everything automatically gets adjusted so you don't have to! So the timings will always display at the correct time regarding the daylight savings times.

Combining Timing with Liquidity Zones the right way and in a clear, clean, and simple format.

Different than others this script also shows the "true" Asia range as it respects the "day open gap" which affects the Asia range in other scripts and it also covers the full 8 hours of Asia Session.

Additions

You can add in the settings menu the last week's high and low, the previous day's high and low, and also the day's open price by ticking the boxes in the settings menu

All colors of the boxes are fully adjustable and customizable for your personal preferences. Same for the previous weeks and day highs and lows. Just go to "Style" and you can adjust the Line types or colors to your preferred choice.

Recommended Use

The most beautiful display is on the M5 Timeframe as you have a clear overview of all sessions without losing the intraday view. You can also use it on the M1 for more details or the M15 for the bigger picture. The Template can hide on higher time frames starting from the H1 to not flood your chart with boxes.

How to use the Asia Session Range Box

Use the Asia Range Box as your intraday Guide, keep in mind that a Breakout of Asia high or low induces Liquidity and a common price behavior is a reversal after the fake breakout of that range.

How to use the London Open and NY Open Inducement Windows

Both grey boxes highlight the Open of either London Open or NY Open and you should keep an eye out for potential Liquditiy Graps or Mitigations during that times as this is when they introduce major Liquidity for the regarding Session.

How to use the Asia high, low and midline and day open price

After Asia Range got taken out in one direction, often price comes back to those levels to mitigate or bounce off, so you can imagine those zones as support and resistance on some occasions, recommended in combination with Imbalances.

How to use the previous day and week's highs and lows

Once added in the settings, you can display those price levels, you can use them either as Liquidity Targets or as Inducement Levels once they are taken out.

Enjoy!

Bollinger Bands Liquidity Cloud [ChartPrime]This indicator overlays a heatmap on the price chart, providing a detailed representation of Bollinger bands' profile. It offers insights into the price's behavior relative to these bands. There are two visualization styles to choose from: the Volume Profile and the Z-Score method.

Features

Volume Profile: This method illustrates how the price interacts with the Bollinger bands based on the traded volume.

Z-Score: In this mode, the indicator samples the real distribution of Z-Scores within a specified window and rescales this distribution to the desired sample size. It then maps the distribution as a heatmap by calculating the corresponding price for each Z-Score sample and representing its weight via color and transparency.

Parameters

Length: The period for the simple moving average that forms the base for the Bollinger bands.

Multiplier: The number of standard deviations from the moving average to plot the upper and lower Bollinger bands.

Main:

Style: Choose between "Volume" and "Z-Score" visual styles.

Sample Size: The size of the bin. Affects the granularity of the heatmap.

Window Size: The lookback window for calculating the heatmap. When set to Z-Score, a value of `0` implies using all available data. It's advisable to either use `0` or the highest practical value when using the Z-Score method.

Lookback: The amount of historical data you want the heatmap to represent on the chart.

Smoothing: Implements sinc smoothing to the distribution. It smoothens out the heatmap to provide a clearer visual representation.

Heat Map Alpha: Controls the transparency of the heatmap. A higher value makes it more opaque, while a lower value makes it more transparent.

Weight Score Overlay: A toggle that, when enabled, displays a letter score (`S`, `A`, `B`, `C`, `D`) inside the heatmap boxes, based on the weight of each data point. The scoring system categorizes each weight into one of these letters using the provided percentile ranks and the median.

Color

Color: Color for high values.

Standard Deviation Color: Color to represent the standard deviation on the Bollinger bands.

Text Color: Determines the color of the letter score inside the heatmap boxes. Adjusting this parameter ensures that the score is visible against the heatmap color.

Usage

Once this indicator is applied to your chart, the heatmap will be overlaid on the price chart, providing a visual representation of the price's behavior in relation to the Bollinger bands. The intensity of the heatmap is directly tied to the price action's intensity, defined by your chosen parameters.

When employing the Volume Profile style, a brighter and more intense area on the heatmap indicates a higher trading volume within that specific price range. On the other hand, if you opt for the Z-Score method, the intensity of the heatmap reflects the Z-Score distribution. Here, a stronger intensity is synonymous with a more frequent occurrence of a specific Z-Score.

For those seeking an added layer of granularity, there's the "Weight Score Overlay" feature. When activated, each box in your heatmap will sport a letter score, ranging from `S` to `D`. This score categorizes the weight of each data point, offering a concise breakdown:

- `S`: Data points with a weight of 1.

- `A`: Weights below 1 but greater than or equal to the 75th percentile rank.

- `B`: Weights under the 75th percentile but at or above the median.

- `C`: Weights beneath the median but surpassing the 25th percentile rank.

- `D`: All that fall below the 25th percentile rank.

This scoring feature augments the heatmap's visual data, facilitating a quicker interpretation of the weight distribution across the dataset.

Further Explanations

Volume Profile

A volume profile is a tool used by traders to visualize the amount of trading volume occurring at specific price levels. This kind of profile provides a deep insight into the market's structure and helps traders identify key areas of support and resistance, based on where the most trading activity took place. The concept behind the volume profile is that the amount of volume at each price level can indicate the potential importance of that price.

In this indicator:

- The volume profile mode creates a visual representation by sampling trading volumes across price levels.

- The representation displays the balance between bullish and bearish volumes at each level, which is further differentiated using a color gradient from `low_color` to `high_color`.

- The volume profile becomes more refined with sinc smoothing, helping to produce a smoother distribution of volumes.

Z-Score and Distribution Resampling

Z-Score, in the context of trading, represents the number of standard deviations a data point (e.g., closing price) is from the mean (average). It’s a measure of how unusual or typical a particular data point is in relation to all the data. In simpler terms, a high Z-Score indicates that the data point is far away from the mean, while a low Z-Score suggests it's close to the mean.

The unique feature of this indicator is that it samples the real distribution of z-scores within a window and then resamples this distribution to fit the desired sample size. This process is termed as "resampling in the context of distribution sampling" . Resampling provides a way to reconstruct and potentially simplify the original distribution of z-scores, making it easier for traders to interpret.

In this indicator:

- Each Z-Score corresponds to a price value on the chart.

- The resampled distribution is then used to display the heatmap, with each Z-Score related price level getting a heatmap box. The weight (or importance) of each box is represented as a combination of color and transparency.

How to Interpret the Z-Score Distribution Visualization:

When interpreting the Z-Score distribution through color and alpha in the visualization, it's vital to understand that you're seeing a representation of how unusual or typical certain data points are without directly viewing the numerical Z-Score values. Here's how you can interpret it:

Intensity of Color: This often corresponds to the distance a particular data point is from the mean.

Lighter shades (closer to `low_color`) typically indicate data points that are more extreme, suggesting overbought or oversold conditions. These could signify potential reversals or significant deviations from the norm.

Darker shades (closer to `high_color`) represent data points closer to the mean, suggesting that the price is relatively typical compared to the historical data within the given window.

Alpha (Transparency): The degree of transparency can indicate the significance or confidence of the observed deviation. More opaque boxes might suggest a stronger or more reliable deviation from the mean, implying that the observed behavior is less likely to be a random occurrence.

More transparent boxes could denote less certainty or a weaker deviation, meaning that the observed price behavior might not be as noteworthy.

- Combining Color and Alpha: By observing both the intensity of color and the level of transparency, you get a richer understanding. For example:

- A light, opaque box could suggest a strong, significant deviation from the mean, potentially signaling an overbought or oversold scenario.

- A dark, transparent box might indicate a weak, insignificant deviation, suggesting the price is behaving typically and is close to its average.

Candlestick Pattern Criteria and Analysis Indicator█ OVERVIEW

Define, then locate the presence of a candle that fits a specific criteria. Run a basic calculation on what happens after such a candle occurs.

Here, I’m not giving you an edge, but I’m giving you a clear way to find one.

IMPORTANT NOTE: PLEASE READ:

THE INDICATOR WILL ALWAYS INITIALLY LOAD WITH A RUNTIME ERROR. WHEN INITIALLY LOADED THERE NO CRITERIA SELECTED.

If you do not select a criteria or run a search for a criteria that doesn’t exist, you will get a runtime error. If you want to force the chart to load anyway, enable the debug panel at the bottom of the settings menu.

Who this is for:

- People who want to engage in TradingView for tedious and challenging data analysis related to candlestick measurement and occurrence rate and signal bar relationships with subsequent bars. People who don’t know but want to figure out what a strong bullish bar or a strong bearish bar is.

Who this is not for:

- People who want to be told by an indicator what is good or bad or buy or sell. Also, not for people that don’t have any clear idea on what they think is a strong bullish bar or a strong bearish bar and aren’t willing to put in the work.

Recommendation: Use on the candle resolution that accurately reflects your typical holding period. If you typically hold a trade for 3 weeks, use 3W candles. If you hold a trade for 3 minutes, use 3m candles.

Tldr; Read the tool tips and everything above this line. Let me know any issues that arise or questions you have.

█ CONCEPTS

Many trading styles indicate that a certain candle construct implies a bearish or bullish future for price. That said, it is also common to add to that idea that the context matters. Of course, this is how you end up with all manner of candlestick patterns accounting for thousands of pages of literature. No matter the context though, we can distill a discretionary trader's decision to take a trade based on one very basic premise: “A trader decides to take a trade on the basis of the rightmost candle's construction and what he/she believes that candle construct implies about the future price.” This indicator vets that trader’s theory in the most basic way possible. It finds the instances of any candle construction and takes a look at what happens on the next bar. This current bar is our “Signal Bar.”

█ GUIDE

I said that we vet the theory in the most basic way possible. But, in truth, this indicator is very complex as a result of there being thousands of ways to define a ‘strong’ candle. And you get to define things on a very granular level with this indicator.

Features:

1. Candle Highlighting

When the user’s criteria is met, the candle is highlighted on the chart.

The following candle is highlighted based on whether it breaks out, breaks down, or is an inside bar.

2. User-Defined Criteria

Criteria that you define include:

Candle Type: Bull bars, Bear bars, or both

Candle Attributes

Average Size based on Standard Deviation or Average of all potential bars in price history

Search within a specific price range

Search within a specific time range

Clarify time range using defined sessions and with or without weekends

3. Strike Lines on Candle

Often you want to know how price reacts when it gets back to a certain candle. Also it might be true that candle types cluster in a price region. This can be identified visually by adding lines that extend right on candles that fit the criteria.

4. User-Defined Context

Labeled “Alternative Criteria,” this facet of the script allows the user to take the context provided from another indicator and import it into the indicator to use as a overriding criteria. To account for the fact that the external indicator must be imported as a float value, true (criteria of external indicator is met) must be imported as 1 and false (criteria of external indicator is not met) as 0. Basically a binary Boolean. This can be used to create context, such as in the case of a traditional fractal, or can be used to pair with other signals.

If you know how to code in Pinescript, you can save a copy and simply add your own code to the section indicated in the code and set your bull and bear variables accordingly and the code should compile just fine with no further editing needed.

Included with the script to maximize out-of-the-box functionality, there is preloaded as alternative criteria a code snippet. The criteria is met on the bull side when the current candle close breaks out above the prior candle high. The bear criteria is met when the close breaks below the prior candle. When Alternate Criteria is run by itself, this is the only criteria set and bars are highlighted when it is true. You can qualify these candles by adding additional attributes that you think would fit well.

Using Alternative Criteria, you are essentially setting a filter for the rest of the criteria.

5. Extensive Read Out in the Data Window (right side bar pop out window).

As you can see in the thumbnail, there is pasted a copy of the Data Window Dialogue. I am doubtful I can get the thumbnail to load up perfectly aligned. Its hard to get all these data points in here. It may be better suited for a table at this point. Let me know what you think.

The primary, but not exclusive, purpose of what is in the Data Window is to talk about how often your criteria happens and what happens on the next bar. There are a lot of pieces to this.

Red = Values pertaining to the size of the current bar only

Blue = Values pertaining or related to the total number of signals

Green = Values pertaining to the signal bars themselves, including their measurements

Purple = Values pertaining to bullish bars that happen after the signal bar

Fuchsia = Values pertaining to bearish bars that happen after the signal bar

Lime = Last four rows which are your percentage occurrence vs total signals percentages

The best way I can explain how to understand parts you don’t understand otherwise in the data window is search the title of the row in the code using ‘ctrl+f’ and look at it and see if it makes more sense.

█ [b}Available Candle Attributes

Candle attributes can be used in any combination. They include:

[*}Bodies

[*}High/Low Range

[*}Upper Wick

[*}Lower Wick

[*}Average Size

[*}Alternative Criteria

Criteria will evaluate each attribute independently. If none is set for a particular attribute it is bypassed.

Criteria Quantity can be in Ticks, Points, or Percentage. For percentage keep in mind if using anything involving the candle range will not work well with percentage.

Criteria Operators are “Greater Than,” “Less Than,” and “Threshold.” Threshold means within a range of two numbers.

█ Problems with this methodology and opportunities for future development:

#1 This kind of work is hard.

If you know what you’re doing you might be able to find success changing out the inputs for loops and logging results in arrays or matrices, but to manually go through and test various criteria is a lot of work. However, it is rewarding. At the time of publication in early Oct 2022, you will quickly find that you get MUCH more follow through on bear bars than bull bars. That should be obvious because we’re in the middle of a bear market, but you can still work with the parameters and contextual inputs to determine what maximizes your probability. I’ve found configurations that yield 70% probability across the full series of bars. That’s an edge. That means that 70% of the time, when this criteria is met, the next bar puts you in profit.

#2 The script is VERY heavy.

Takes an eternity to load. But, give it a break, it’s doing a heck of a lot! There is 10 unique arrays in here and a loop that is a bit heavy but gives us the debug window.

#3 If you don’t have a clear idea its hard to know where to start.

There are a lot of levers to pull on in this script. Knowing which ones are useful and meaningful is very challenging. Combine that with long load times… its not great.

#4 Your brain is the only thing that can optimize your results because the criteria come from your mind.

Machine learning would be much more useful here, but for now, you are the machine. Learn.

#5 You can’t save your settings.

So, when you find a good combo, you’ll have to write it down elsewhere for future reference. It would be nice if we could save templates on custom indicators like we can on some of the built in drawing tools, but I’ve had no success in that. So, I recommend screenshotting your settings and saving them in Notion.so or some other solid record keeping database. Then you can go back and retrieve those settings.

#6 no way to export these results into conditions that can be copy/pasted into another script.

Copy/Paste of labels or tables would be the best feature ever at this point. Because you could take the criteria and put it in a label, copy it and drop it into another strategy script or something. But… men can dream.

█ Opportunities to PineCoders Learn:

1. In this script I’m importing libraries, showing some of my libraries functionality. Hopefully that gives you some ideas on how to use them too.

The price displacement library (which I love!)

Creative and conventional ways of using debug()

how to display arrays and matrices on charts

I didn’t call in the library that holds the backtesting function. But, also demonstrating, you can always pull the library up and just copy/paste the function out of there and into your script. That’s fine to do a lot of the time.

2. I am using REALLY complicated logic in this script (at least for me). I included extensive descriptions of this ? : logic in the text of the script. I also did my best to bracket () my logic groups to demonstrate how they fit together, both for you and my future self.

3. The breakout, built-in, “alternative criteria” is actually a small bit of genius built in there if you want to take the time to understand that block of code and think about some of the larger implications of the method deployed.

As always, a big thank you to TradingView and the Pinescript community, the Pinescript pros who have mentored me, and all of you who I am privileged to help in their Pinescripting journey.

"Those who stay will become champions" - Bo Schembechler

Real-Fast Fourier Transform of Price w/ Linear Regression [Loxx]Real-Fast Fourier Transform of Price w/ Linear Regression is a indicator that implements a Real-Fast Fourier Transform on Price and modifies the output by a measure of Linear Regression. The solid line is the Linear Regression Trend of the windowed data, The green/red line is the Real FFT of price.

What is the Discrete Fourier Transform?

In mathematics, the discrete Fourier transform (DFT) converts a finite sequence of equally-spaced samples of a function into a same-length sequence of equally-spaced samples of the discrete-time Fourier transform (DTFT), which is a complex-valued function of frequency. The interval at which the DTFT is sampled is the reciprocal of the duration of the input sequence. An inverse DFT is a Fourier series, using the DTFT samples as coefficients of complex sinusoids at the corresponding DTFT frequencies. It has the same sample-values as the original input sequence. The DFT is therefore said to be a frequency domain representation of the original input sequence. If the original sequence spans all the non-zero values of a function, its DTFT is continuous (and periodic), and the DFT provides discrete samples of one cycle. If the original sequence is one cycle of a periodic function, the DFT provides all the non-zero values of one DTFT cycle.

What is the Complex Fast Fourier Transform?

The complex Fast Fourier Transform algorithm transforms N real or complex numbers into another N complex numbers. The complex FFT transforms a real or complex signal x in the time domain into a complex two-sided spectrum X in the frequency domain. You must remember that zero frequency corresponds to n = 0, positive frequencies 0 < f < f_c correspond to values 1 ≤ n ≤ N/2 −1, while negative frequencies −fc < f < 0 correspond to N/2 +1 ≤ n ≤ N −1. The value n = N/2 corresponds to both f = f_c and f = −f_c. f_c is the critical or Nyquist frequency with f_c = 1/(2*T) or half the sampling frequency. The first harmonic X corresponds to the frequency 1/(N*T).

The complex FFT requires the list of values (resolution, or N) to be a power 2. If the input size if not a power of 2, then the input data will be padded with zeros to fit the size of the closest power of 2 upward.

What is Real-Fast Fourier Transform?

Has conditions similar to the complex Fast Fourier Transform value, except that the input data must be purely real. If the time series data has the basic type complex64, only the real parts of the complex numbers are used for the calculation. The imaginary parts are silently discarded.

Inputs:

src = source price

uselreg = whether you wish to modify output with linear regression calculation

Windowin = windowing period, restricted to powers of 2: "4", "8", "16", "32", "64", "128", "256", "512", "1024", "2048"

Treshold = to modified power output to fine tune signal

dtrendper = adjust regression calculation

barsback = move window backward from bar 0

mutebars = mute bar coloring for the range

Further reading:

Real-valued Fast Fourier Transform Algorithms IEEE Transactions on Acoustics, Speech, and Signal Processing, June 1987

Related indicators utilizing Fourier Transform

Fourier Extrapolator of Variety RSI w/ Bollinger Bands

Fourier Extrapolation of Variety Moving Averages

Fourier Extrapolator of Price w/ Projection Forecast

Debug_Window_LibraryLibrary "Debug_Window_Library"

Provides a framework for logging debug information to a window on the chart.

consoleWrite(txt, maxLines) Adds a line of text to the debug window. The text is rolled off the bottom of the window as it fills up.

Parameters:

txt : - this is the text to be appended to the window

maxLines : - this is the size of the window in lines.

Returns: nothing

The example above shows the close value for the last 10 bars.

Here's the code.

//@version=5

indicator("Debug Library test Script", overlay=true)

import sp2432/Debug_Window_Library/1 as dbg

// add some text to the debug window

dbg .consoleWrite( str .tostring(close), 10)

Sentiment Estimator [AstrideUnicorn]Sentiment Estimator is an indicator that estimates market sentiment using only its pricing data. It counts bullish and bearish candles in a rolling window and calculates their relative values as percentages of the total amount of candles in the window. Market sentiment shows the direction in which the market is biased to move or the current trend direction. Extreme values of the market sentiment are contrarian signals. When the market sentiment is too bullish, it is time to sell and vice versa.

HOW TO USE

Sentiment Estimator plots a pair of green and red circles for each candle. They represent bullish and bearish sentiments, respectively.

The vertical positions of the circles show corresponding sentiment values in percentage units. For example, if a green circle's height is 60, the market is 60% bullish. In this case, the red circle's height will be 40, as bullish and bearish parts of the market sentiment sum to 100%.

The blue line plotted at the 50% level shows the neutral sentiment level. If a green circle is above the blue line, the prevailing market sentiment at that time is bullish, and the market is biased to move up. If a red one is above, the market has predominantly bearish sentiment and is prone to move down.

The red level shows extreme sentiment level. If a green or red circle is above this line, it means that the market is extremely bullish or bearish, respectively. It is a contrarian signal, and one can expect a reversal soon. In this case, a blue label with the text "reversal expected" is shown.

SETTINGS

Timeframe - allows choosing a timeframe other than the chart's one for the indicator calculation.

Look-Back Window - sets the historical window length used to perform the calculations. You can adjust the window to get the best results for a particular market or timeframe.

DrawIndicatorOnTheChartLibrary "DrawIndicatorOnTheChart"

this library is used to show an indicator (such RSI, CCI, MOM etc) on the main chart with indicator's horizontal lines in a window. Location of the window is calculated dynamically by last price movemements

drawIndicator(indicatorName, indicator, indicatorcolor, period, indimax_, indimin_, levels, precision, xlocation) draws the related indicator on the chart

Parameters:

indicatorName : is the indicator name as string such "RSI", "CCI" etc

indicator : is the indicator you want to show, such rsi(close, 14), mom(close, 10) etc

indicatorcolor : is the color of indicator line

period : is the length of the window to show

indimax_ : is the maximum value of the indicator, for example for RSI it's 100.0, if the indicator (such CCI, MOM etc) doesn't have maximum value then use "na"

indimin_ : is the minimum value of the indicator, for example for RSI it's 0.0, if the indicator (such CCI, MOM etc)doesn't have maximum value then use "na"

levels : is the levels of the array for the horizontal lines. for example if you want horizontal lines at 30.0, and 70.0 then use array.from(30.0, 70.0). if no horizontal lines then use array.from(na)

precision : is the precision/number of decimals that is used to show indicator values, for example for RSI set it 2

xlocation : is end location of the indicator window, for example if xlocation = 0 window is created on the index of the last bar/candle

Returns: none

Alma Moving Average Ribbon Reverse Length [DM]Greetings Colleagues

Following some recommendations and ideas I share this moving average, put all of them together

The length calculation is automatic there is only one input.

The length is inverse so it will wrap from the longest reference point, hence using phi

Moving averages will wrap around the price.

I've also added gradient color to plots and fill plots

There is an alert selector in case you are interested in a particular crossing, "remember that the order is reversed".

There is an alert visual plotshapes with offset signal.