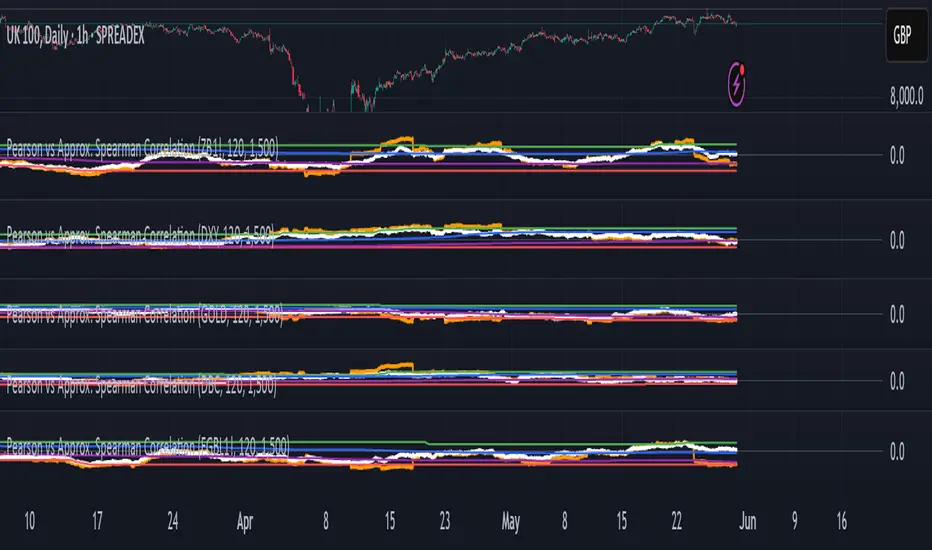

Pearson vs Approx. Spearman CorrelationThis indicator displays the rolling Pearson and approximate Spearman correlation between the chart's asset and a second user-defined asset, based on log returns over a customizable window.

Features:

- Pearson correlation of log returns (standard linear dependency measure)

- Approximate Spearman correlation, using percentile ranks to better capture nonlinear and monotonic relationships

/ Horizontal lines showing:

Maximum and minimum correlation values over a statistical window

1st quartile (25%) and 3rd quartile (75%) — helpful for identifying statistically high or low regimes

This script is useful for identifying dynamic co-movements, regime changes, or correlation breakdowns between assets — applicable in risk management, portfolio construction, and pairs trading strategies.

Cerca negli script per "如何用wind搜索股票的发行价和份数"

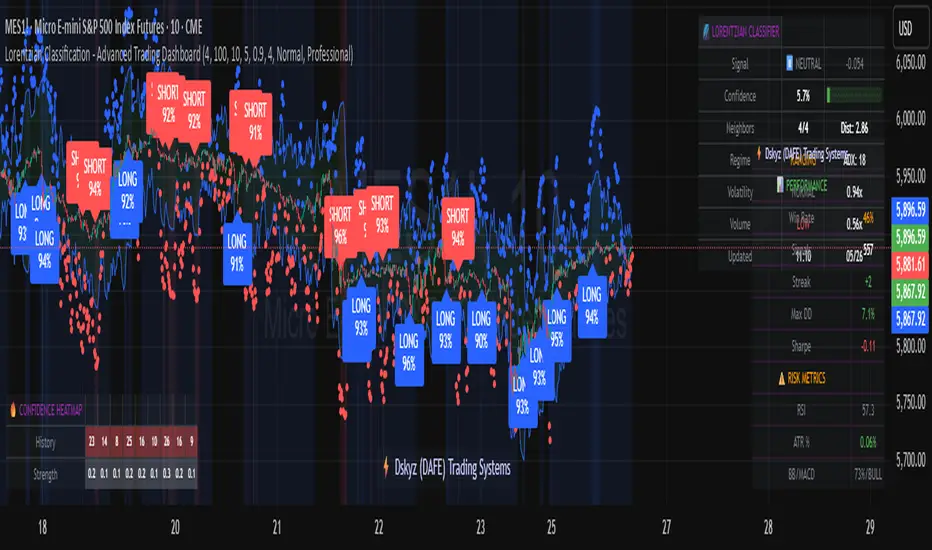

Lorentzian Classification - Advanced Trading DashboardLorentzian Classification - Relativistic Market Analysis

A Journey from Theory to Trading Reality

What began as fascination with Einstein's relativity and Lorentzian geometry has evolved into a practical trading tool that bridges theoretical physics and market dynamics. This indicator represents months of wrestling with complex mathematical concepts, debugging intricate algorithms, and transforming abstract theory into actionable trading signals.

The Theoretical Foundation

Lorentzian Distance in Market Space

Traditional Euclidean distance treats all feature differences equally, but markets don't behave uniformly. Lorentzian distance, borrowed from spacetime geometry, provides a more nuanced similarity measure:

d(x,y) = Σ ln(1 + |xi - yi|)

This logarithmic formulation naturally handles:

Scale invariance: Large price moves don't overwhelm small but significant patterns

Outlier robustness: Extreme values are dampened rather than dominating

Non-linear relationships: Captures market behavior better than linear metrics

K-Nearest Neighbors with Relativistic Weighting

The algorithm searches historical market states for patterns similar to current conditions. Each neighbor receives weight inversely proportional to its Lorentzian distance:

w = 1 / (1 + distance)

This creates a "gravitational" effect where closer patterns have stronger influence on predictions.

The Implementation Challenge

Creating meaningful market features required extensive experimentation:

Price Features: Multi-timeframe momentum (1, 2, 3, 5, 8 bar lookbacks) Volume Features: Relative volume analysis against 20-period average

Volatility Features: ATR and Bollinger Band width normalization Momentum Features: RSI deviation from neutral and MACD/price ratio

Each feature undergoes min-max normalization to ensure equal weighting in distance calculations.

The Prediction Mechanism

For each current market state:

Feature Vector Construction: 12-dimensional representation of market conditions

Historical Search: Scan lookback period for similar patterns using Lorentzian distance

Neighbor Selection: Identify K nearest historical matches

Outcome Analysis: Examine what happened N bars after each match

Weighted Prediction: Combine outcomes using distance-based weights

Confidence Calculation: Measure agreement between neighbors

Technical Hurdles Overcome

Array Management: Complex indexing to prevent look-ahead bias

Distance Calculations: Optimizing nested loops for performance

Memory Constraints: Balancing lookback depth with computational limits

Signal Filtering: Preventing clustering of identical signals

Advanced Dashboard System

Main Control Panel

The primary dashboard provides real-time market intelligence:

Signal Status: Current prediction with confidence percentage

Neighbor Analysis: How many historical patterns match current conditions

Market Regime: Trend strength, volatility, and volume analysis

Temporal Context: Real-time updates with timestamp

Performance Analytics

Comprehensive tracking system monitors:

Win Rate: Percentage of successful predictions

Signal Count: Total predictions generated

Streak Analysis: Current winning/losing sequence

Drawdown Monitoring: Maximum equity decline

Sharpe Approximation: Risk-adjusted performance estimate

Risk Assessment Panel

Multi-dimensional risk analysis:

RSI Positioning: Overbought/oversold conditions

ATR Percentage: Current volatility relative to price

Bollinger Position: Price location within volatility bands

MACD Alignment: Momentum confirmation

Confidence Heatmap

Visual representation of prediction reliability:

Historical Confidence: Last 10 periods of prediction certainty

Strength Analysis: Magnitude of prediction values over time

Pattern Recognition: Color-coded confidence levels for quick assessment

Input Parameters Deep Dive

Core Algorithm Settings

K Nearest Neighbors (1-20): More neighbors create smoother but less responsive signals. Optimal range 5-8 for most markets.

Historical Lookback (50-500): Deeper history improves pattern recognition but reduces adaptability. 100-200 bars optimal for most timeframes.

Feature Window (5-30): Longer windows capture more context but reduce sensitivity. Match to your trading timeframe.

Feature Selection

Price Changes: Essential for momentum and reversal detection Volume Profile: Critical for institutional activity recognition Volatility Measures: Key for regime change detection Momentum Indicators: Vital for trend confirmation

Signal Generation

Prediction Horizon (1-20): How far ahead to predict. Shorter horizons for scalping, longer for swing trading.

Signal Threshold (0.5-0.9): Confidence required for signal generation. Higher values reduce false signals but may miss opportunities.

Smoothing (1-10): EMA applied to raw predictions. More smoothing reduces noise but increases lag.

Visual Design Philosophy

Color Themes

Professional: Corporate blue/red for institutional environments Neon: Cyberpunk cyan/magenta for modern aesthetics

Matrix: Green/red hacker-inspired palette Classic: Traditional trading colors

Information Hierarchy

The dashboard system prioritizes information by importance:

Primary Signals: Largest, most prominent display

Confidence Metrics: Secondary but clearly visible

Supporting Data: Detailed but unobtrusive

Historical Context: Available but not distracting

Trading Applications

Signal Interpretation

Long Signals: Prediction > threshold with high confidence

Look for volume confirmation

- Check trend alignment

- Verify support levels

Short Signals: Prediction < -threshold with high confidence

Confirm with resistance levels

- Check for distribution patterns

- Verify momentum divergence

- Market Regime Adaptation

Trending Markets: Higher confidence in directional signals

Ranging Markets: Focus on reversal signals at extremes

Volatile Markets: Require higher confidence thresholds

Low Volume: Reduce position sizes, increase caution

Risk Management Integration

Confidence-Based Sizing: Larger positions for higher confidence signals

Regime-Aware Stops: Wider stops in volatile regimes

Multi-Timeframe Confirmation: Align signals across timeframes

Volume Confirmation: Require volume support for major signals

Originality and Innovation

This indicator represents genuine innovation in several areas:

Mathematical Approach

First application of Lorentzian geometry to market pattern recognition. Unlike Euclidean-based systems, this naturally handles market non-linearities.

Feature Engineering

Sophisticated multi-dimensional feature space combining price, volume, volatility, and momentum in normalized form.

Visualization System

Professional-grade dashboard system providing comprehensive market intelligence in intuitive format.

Performance Tracking

Real-time performance analytics typically found only in institutional trading systems.

Development Journey

Creating this indicator involved overcoming numerous technical challenges:

Mathematical Complexity: Translating theoretical concepts into practical code

Performance Optimization: Balancing accuracy with computational efficiency

User Interface Design: Making complex data accessible and actionable

Signal Quality: Filtering noise while maintaining responsiveness

The result is a tool that brings institutional-grade analytics to individual traders while maintaining the theoretical rigor of its mathematical foundation.

Best Practices

- Parameter Optimization

- Start with default settings and adjust based on:

Market Characteristics: Volatile vs. stable

Trading Timeframe: Scalping vs. swing trading

Risk Tolerance: Conservative vs. aggressive

Signal Confirmation

Never trade on Lorentzian signals alone:

Price Action: Confirm with support/resistance

Volume: Verify with volume analysis

Multiple Timeframes: Check higher timeframe alignment

Market Context: Consider overall market conditions

Risk Management

Position Sizing: Scale with confidence levels

Stop Losses: Adapt to market volatility

Profit Targets: Based on historical performance

Maximum Risk: Never exceed 2-3% per trade

Disclaimer

This indicator is for educational and research purposes only. It does not constitute financial advice or guarantee profitable trading results. The Lorentzian classification system reveals market patterns but cannot predict future price movements with certainty. Always use proper risk management, conduct your own analysis, and never risk more than you can afford to lose.

Market dynamics are inherently uncertain, and past performance does not guarantee future results. This tool should be used as part of a comprehensive trading strategy, not as a standalone solution.

Bringing the elegance of relativistic geometry to market analysis through sophisticated pattern recognition and intuitive visualization.

Thank you for sharing the idea. You're more than a follower, you're a leader!

@vasanthgautham1221

Trade with precision. Trade with insight.

— Dskyz , for DAFE Trading Systems

Multi-Session ORBThe Multi-Session ORB Indicator is a customizable Pine Script (version 6) tool designed for TradingView to plot Opening Range Breakout (ORB) levels across four major trading sessions: Sydney, Tokyo, London, and New York. It allows traders to define specific ORB durations and session times in Central Daylight Time (CDT), making it adaptable to various trading strategies.

Key Features:

1. Customizable ORB Duration: Users can set the ORB duration (default: 15 minutes) via the inputMax parameter, determining the time window for calculating the high and low of each session’s opening range.

2. Flexible Session Times: The indicator supports user-defined session and ORB times for:

◦ Sydney: Default ORB (17:00–17:15 CDT), Session (17:00–01:00 CDT)

◦ Tokyo: Default ORB (19:00–19:15 CDT), Session (19:00–04:00 CDT)

◦ London: Default ORB (02:00–02:15 CDT), Session (02:00–11:00 CDT)

◦ New York: Default ORB (08:30–08:45 CDT), Session (08:30–16:00 CDT)

3. Session-Specific ORB Levels: For each session, the indicator calculates and tracks the high and low prices during the specified ORB period. These levels are updated dynamically if new highs or lows occur within the ORB timeframe.

4. Visual Representation:

◦ ORB high and low lines are plotted only during their respective session times, ensuring clarity.

◦ Each session’s lines are color-coded for easy identification:

▪ Sydney: Light Yellow (high), Dark Yellow (low)

▪ Tokyo: Light Pink (high), Dark Pink (low)

▪ London: Light Blue (high), Dark Blue (low)

▪ New York: Light Purple (high), Dark Purple (low)

◦ Lines are drawn with a linewidth of 2 and disappear when the session ends or if the timeframe is not intraday (or exceeds the ORB duration).

5. Intraday Compatibility: The indicator is optimized for intraday timeframes (e.g., 1-minute to 15-minute charts) and only displays when the chart’s timeframe multiplier is less than or equal to the ORB duration.

How It Works:

• Session Detection: The script uses the time() function to check if the current bar falls within the user-defined ORB or session time windows, accounting for all days of the week.

• ORB Logic: At the start of each session’s ORB period, the script initializes the high and low based on the first bar’s prices. It then updates these levels if subsequent bars within the ORB period exceed the current high or fall below the current low.

• Plotting: ORB levels are plotted as horizontal lines during the respective session, with visibility controlled to avoid clutter outside session times or on incompatible timeframes.

Use Case:

Traders can use this indicator to identify key breakout levels for each trading session, facilitating strategies based on price action around the opening range. The flexibility to adjust ORB and session times makes it suitable for various markets (e.g., forex, stocks, or futures) and time zones.

Limitations:

• The indicator is designed for intraday timeframes and may not display on higher timeframes (e.g., daily or weekly) or if the timeframe multiplier exceeds the ORB duration.

• Time inputs are in CDT, requiring users to adjust for their local timezone or market requirements.

• If you need to use this for GC/CL/SPY/QQQ you have to adjust the times by one hour.

This indicator is ideal for traders focusing on session-based breakout strategies, offering clear visualization and customization for global market sessions.

SMPivot Gaussian Trend Strategy [Js.K]This open-source strategy combines a Gaussian-weighted moving average with “Smart Money” swing-pivot breaks (BoS = Break-of-Structure) to capture trend continuations and early reversals. It is intended for educational and research purposes only and must not be interpreted as financial advice.

How the logic works

-------------------

1. Gaussian Moving Average (GMA)

• A custom Gaussian kernel (length = 30 by default) smooths price while preserving turning points.

• A second pass (“Smoothed GMA”) further filters noise; only its direction is used for bias.

2. Swing-Pivot detection

• High/Low pivots are found with a symmetric look-back/forward window (Pivot Length = 20).

• The most recent confirmed pivot creates a dynamic structure level (UpdatedHigh / UpdatedLow).

3. Entry rules

Long

• Price closes above the most recent pivot high **and** above Smoothed GMA.

Short

• Price closes below the most recent pivot low **and** below Smoothed GMA.

4. Exit rules

• Fixed stop-loss and take-profit in percent of current price (user-defined).

• Separate parameters and on/off switches for longs and shorts.

5. Visuals

• GMA (dots) and Smoothed GMA (line).

• Structure break lines plus “BoS PH/PL” labels at the midpoint between pivot and break.

Inputs

------

Gaussian

• Gaussian Length (default 30) – smoothing window.

• Gaussian Scatterplot – toggle GMA dots.

Smart-Money Pivot

• Pivot Length (default 20).

• Bull / Bear colors.

Risk settings

• Long / Short enable.

• Individual SL % and TP % (default 1 % SL, 30 % TP).

• Strategy uses percent-of-equity sizing; initial capital defaults to 10 000 USD.

Adjust these to reflect your own account size, realistic commission and slippage.

Best practice & compliance notes

--------------------------------

• Test on a data sample that yields ≥ 100 trades to obtain statistically relevant results.

• Keep risk per trade below 5–10 % of equity; the default values comply with this guideline.

• Explain any custom settings you publish that differ from the defaults.

• Do **not** remove the code header or licence notice (MPL-2.0).

• Include realistic commission and slippage in your back-test before publishing.

• The script does **not** repaint; orders are processed on bar close.

Usage

-----

1. Add the script to any symbol / timeframe; intraday and swing timeframes both work—adjust lengths accordingly.

2. Configure SL/TP and position size to match your personal risk management.

3. Run “List of trades” and the performance summary to evaluate expectancy; forward-test before live use.

Disclaimer

----------

Trading involves substantial risk. Past performance based on back-testing is not necessarily indicative of future results. The author is **not** responsible for any financial losses arising from the use of this script.

Hippo Battlefield - Bulls VS Bears 20 bars## Hippo Battlefield – Bulls VS Bears (20 Bars)

**What it is**

A multi-dimensional momentum-and-sentiment oscillator that combines classic Bull/Bear Power with ATR- or peak-normalization, then layers on RSI and MACD-derived metrics into:

1. **A colored bar series** showing net Bull+Bear Power strength over the last 20 bars,

2. **A dynamic table** of each of those 20 BBP values (grouped into four 5-bar “quartals”), with symbols, per-bar change, and rolling averages, and

3. **A composite “Weighted BBP” histogram** blending normalized RSI, MACD, and BBP into a single view.

---

### Key Inputs

- **Length (EMA)** – look-back for the underlying EMA (default 60)

- **Normalization Length** – look-back window for peak-normalization (default 60)

- **Use ATR for Norm.** – toggle ATR-based normalization vs. highest-abs(BBP)

- **Show Tables** – toggle the bottom-right 21×11 grid of raw and average BBP values

---

### What You See

#### 1. Colored Bars (Overlay = false)

- Bars are colored by normalized BBP intensity:

- Extreme Bull (≥+10): deep blue

- Strong Bull (+5 to +10): green/yellow

- Weak Bull (+0 to +5): dark green

- Weak Bear (–0 to –5): dark red

- Strong Bear (–5 to –10): pink/red

- Extreme Bear (<–10): magenta

#### 2. Bottom-Right Table (20 Bars of Data)

- Divided into four columns (0–4, 5–9, 10–14, 15–19 bars ago) and one “average” row.

- Each cell shows:

1. Bar index (1–20),

2. Normalized BBP value (to four decimals),

3. Direction symbol (↑/↓/=),

4. Bar-to-bar change (± value),

5. A separator “|”.

- At the very bottom, each column’s 5-bar average is displayed as “Avg: X.XXXX” with a dot marker.

#### 3. Top-Center Mini-Table

- When ≥20 bars have elapsed, shows the date at 20 bars ago and the average BBP across the full 20-bar window.

#### 4. Normalized RSI Line

- Rescales the classic 14-period RSI into a –20…+20 band to align with BBP.

#### 5. MACD Lines (Hidden) & Composite Histogram

- MACD and signal lines are calculated but not plotted by default.

- A “Weighted BBP” histogram combines:

- 20% normalized RSI,

- 20% average of (MACD + signal + normalized BBP),

- 60% normalized BBP

- Plotted as columns, color-coded by strength using the same palette as the main bars.

#### 6. Middle Reference Line

- A horizontal zero line to anchor over/under-zero readings.

---

### How to Use It

- **Trend confirmation**: Strong blue/green bars alongside a rising histogram suggest bull conviction; strong reds/magentas signal bear dominance.

- **Divergence spotting**: Watch for price making new highs/lows while BBP or the histogram fails to follow.

- **Quartal analysis**: The 5-bar group averages can reveal whether recent momentum is accelerating or waning.

- **Cross-indicator weighting**: Because RSI, MACD, and raw BBP all feed into the final histogram, you get a smoothed, blended view of momentum shifts.

---

**Tip:** Tweak the EMA and normalization length to suit your preferred timeframe (e.g. shorter for intraday scalps, longer for swing trades). Enable/disable the table if you prefer a cleaner pane.

Aggregate PDH High Break Alert**Aggregate PDH High Break Alert**

**Overview**

The “Aggregate PDH High Break Alert” is a lightweight Pine Script v6 indicator designed to instantly notify you when today’s price breaks above any prior-day high in a user-defined lookback window. Instead of manually scanning dozens of daily highs, this script automatically loops through the last _N_ days (up to 100) and fires a single-bar alert the moment price eclipses a specific day’s high.

**Key Features**

- **Dynamic Lookback**: Choose any lookback period from 1 to 100 days via a single `High-Break Lookback` input.

- **Single Security Call**: Efficiently retrieves the entire daily-high series in one call to avoid TradingView’s 40-call security limit.

- **Automatic Looping**: Internally loops through each prior-day high, so there’s no need to manually code dozens of lines.

- **Custom Alerts**: Generates a clear, formatted alert message—e.g. “Crossed high from 7 day(s) ago”—for each breakout.

- **Lightweight & Maintainable**: Compact codebase (<15 lines) makes tweaking and debugging a breeze.

**Inputs**

- **High-Break Lookback (days)**: Number of past days to monitor for high breaks. Valid range: 1–100.

**How to Use**

1. **Add to Chart**: Open TradingView, click “Indicators,” then “Create,” and paste in the code.

2. **Configure Lookback**: In the script’s settings, set your desired lookback window (e.g., 20 for the past 20 days).

3. **Enable Alerts**: Right-click the indicator’s name on your chart, select “Add Alert on Aggregate PDH High Break Alert,” and choose “Once per bar close.”

4. **Receive Notifications**: Whenever price crosses above any of the specified prior-day highs, you’ll get an on-screen and/or mobile push alert with the exact number of days ago.

**Use Cases**

- **Trend Confirmation**: Confirm fresh bullish momentum when today’s high outpaces any of the last _N_ days.

- **Breakout Trading**: Automate entries off multi-day highs without manual chart scanning.

- **System Integration**: Integrate with alerts to trigger orders in third-party bots or webhook receivers.

**Disclaimer**

Breakouts alone do not guarantee sustained moves. Combine with your preferred risk management, volume filters, and other indicators for higher-probability setups. Use on markets and timeframes where daily breakout behavior aligns with your strategy.

RSI Divergence Strategy - AliferCryptoStrategy Overview

The RSI Divergence Strategy is designed to identify potential reversals by detecting regular bullish and bearish divergences between price action and the Relative Strength Index (RSI). It automatically enters positions when a divergence is confirmed and manages risk with configurable stop-loss and take-profit levels.

Key Features

Automatic Divergence Detection: Scans for RSI pivot lows/highs vs. price pivots using user-defined lookback windows and bar ranges.

Dual SL/TP Methods:

- Swing-based: Stops placed a configurable percentage beyond the most recent swing high/low.

- ATR-based: Stops placed at a multiple of Average True Range, with a separate risk/reward multiplier.

Long and Short Entries: Buys on bullish divergences; sells short on bearish divergences.

Fully Customizable: Input groups for RSI, divergence, swing, ATR, and general SL/TP settings.

Visual Plotting: Marks divergences on chart and plots stop-loss (red) and take-profit (green) lines for active trades.

Alerts: Built-in alert conditions for both bullish and bearish RSI divergences.

Detailed Logic

RSI Calculation: Computes RSI of chosen source over a specified period.

Pivot Detection:

- Identifies RSI pivot lows/highs by scanning a lookback window to the left and right.

- Uses ta.barssince to ensure pivots are separated by a minimum/maximum number of bars.

Divergence Confirmation:

- Bullish: Price makes a lower low while RSI makes a higher low.

- Bearish: Price makes a higher high while RSI makes a lower high.

Entry:

- Opens a Long position when bullish divergence is true.

- Opens a Short position when bearish divergence is true.

Stop-Loss & Take-Profit:

- Swing Method: Computes the recent swing high/low then adjusts by a percentage margin.

- ATR Method: Uses the current ATR × multiplier applied to the entry price.

- Take-Profit: Calculated as entry price ± (risk × R/R ratio).

Exit Orders: Uses strategy.exit to place bracket orders (stop + limit) for both long and short positions.

Inputs and Configuration

RSI Settings: Length & price source for the RSI.

Divergence Settings: Pivot lookback parameters and valid bar ranges.

SL/TP Settings: Choice between Swing or ATR method.

Swing Settings: Swing lookback length, margin (%), and risk/reward ratio.

ATR Settings: ATR length, stop multiplier, and risk/reward ratio.

Usage Notes

Adjust the Pivot Lookback and Range values to suit the volatility and timeframe of your market.

Use higher ATR multipliers for wider stops in choppy conditions, or tighten swing margins in trending markets.

Backtest different R/R ratios to find the balance between win rate and reward.

Disclaimer

This script is for educational purposes only and does not constitute financial advice. Trading carries significant risk and you may lose more than your initial investment. Always conduct your own research and consider consulting a professional before making any trading decisions.

ICT SMC Liquidity Grabs and OBsICT SMC Liquidity Grabs + Order Blocks + Fibonacci OTE Levels

A High-Probability Entry Engine for Smart Money Concept Traders

This script combines three powerful Smart Money Concepts (SMC) into a single tool: Liquidity Grabs, Order Block Zones, and Fibonacci OTE Levels, allowing traders to identify institutional entry models with clean, rule-based visual signals.

It’s designed to simplify SMC trading by highlighting confluence zones where price is likely to reverse or continue — with clear visual zones, entry arrows, and take profit projections.

🔍 What This Script Does:

Detects Liquidity Grabs

Identifies when price sweeps above/below the highest high or lowest low within a user-defined lookback period and closes back inside.

Plots orange labels on the chart to signal potential liquidity events (LG-H / LG-L).

Plots Order Blocks After Liquidity Grabs

After a liquidity grab, the script looks for displacement candles (strong bullish or bearish moves) and draws highlighted OB zones extending several bars to the right.

These zones represent potential institutional footprints for price reversals.

Draws Fibonacci OTE Levels (Optimal Trade Entry)

Uses recent swing high and low pivots to automatically calculate OTE zones (default: 62% and 75% retracement levels).

Draws these retracement zones for both bullish and bearish setups.

Marks Valid OTE Entry Zones

Buy/Sell zones only trigger when:

A liquidity grab occurs,

Price enters the OTE zone,

And a strong confirming candle is present.

Plots green/red arrows for valid buy/sell OTE entries.

Auto-Draws Take Profit Zones

TP1 = Previous swing high/low

TP2 = Risk-based R-multiplied extension (e.g., 1.5R — customizable)

Alerts

Triggers alerts when valid buy or sell OTE setups are detected.

⚙️ Customization Features:

Toggle each feature: Liquidity Grabs, Order Blocks, Fibonacci OTE levels

Set Fibonacci retracement percentages (e.g., 0.62 / 0.75)

Adjust lookback window for liquidity detection

Customize the take-profit multiplier (R-based)

Full control over visuals: colors, labels, and lines

💡 How to Use:

Use this script to scan for high-confluence trade setups based on Smart Money principles.

Combine with session timing (e.g., New York open), major swing structure, or Kill Zone windows for maximum edge.

Look for arrows inside OB zones or OTE levels following liquidity sweeps for cleaner entries.

🔗 Works Best With:

✅ First FVG — Opening Range Fair Value Gap Detector: Identify early inefficiencies to set the narrative for the day.

✅ Liquidity Levels — Smart Swing Lows: Spot key structural lows that can fuel stop hunts and reversals.

✅ ICT Turtle Soup — Liquidity Reversal: Add a classic reversal pattern to your toolkit to catch fakeouts cleanly.

Together, these tools build a complete Smart Money ecosystem for entry precision, risk management, and price behavior forecasting.

ICT Liquidity Sweep MAX RETRI (ALERT)Strategy Description: SMC + ICT Reversal Sniper | 5-Min | R2 TP

This strategy applies Smart Money Concepts (SMC) and ICT methodology to identify high-probability reversal trades using a clean, rule-based system designed for the 5-minute timeframe.

⸻

Core Logic:

• Liquidity Sweep: Identifies stop hunts beyond recent swing highs/lows using a configurable lookback window.

• Break of Structure (BOS): Validates a directional shift after the sweep.

• Fixed R2 Risk-Reward: Entry is followed by a 2:1 take-profit target. Stop loss is set at the sweep candle’s high/low.

• No Entry Between 8 PM–12 AM NY Time: Avoids the manipulation-prone and illiquid zone.

• Discreet SL Handling: SL hits close trades silently — no labels or visuals.

⸻

Entry Precision & Timing Notes:

• The strategy may occasionally fire before a confirmed liquidity sweep — this is expected. If a sweep occurs later, you may still re-enter toward equilibrium, with take profit also targeted at equilibrium.

• Alerts or trades that trigger near 9:30 AM NY often align with real direction, but this time can be volatile.

• For more reliable and lower-risk entries, focus on the 1:30 PM to 2:00 PM silver bullet window, which tends to produce cleaner setups with more favorable flow. 🖤

ICT MACRO MAX RETRI ( ALERT )🖤 ICT Reversal Detector – Minimalist Edition

This indicator is designed for traders who follow Inner Circle Trader (ICT) concepts, particularly focused on liquidity sweeps and displacement reversals.

It detects:

• Swing Highs & Lows that occur during the most reactive windows of each hour

→ Specifically the last 20 minutes and first 15 minutes

(ICT teaches these moments often reveal macro-level reversals. I’ve expanded the window slightly to give the indicator more room to catch valid setups.)

• Liquidity Sweeps of previous highs/lows

• Displacement (State Change): defined as a manipulation wick followed by 1–3 strong candles closing in the opposite direction

Visually:

• Clean black lines pointing right from the liquidity sweep wick

• White triangle markers inside black label boxes only when valid displacement occurs

• No clutter, no unnecessary shapes — just focused signal

Built for:

• 5-minute charts, especially NASDAQ (NAS100) and S&P 500 (SPX500)

• Confirm setups manually on the 15-minute chart for extra precision

This is a partial automation tool for ICT-style reversal traders who prefer clarity, minimalism, and sharp intuition over noise.

Let it alert you to setups — then decide like a sniper.

Uptrick: Z-Score FlowOverview

Uptrick: Z-Score Flow is a technical indicator that integrates trend-sensitive momentum analysi s with mean-reversion logic derived from Z-Score calculations. Its primary objective is to identify market conditions where price has either stretched too far from its mean (overbought or oversold) or sits at a statistically “normal” range, and then cross-reference this observation with trend direction and RSI-based momentum signals. The result is a more contextual approach to trade entry and exit, emphasizing precision, clarity, and adaptability across varying market regimes.

Introduction

Financial instruments frequently transition between trending modes, where price extends strongly in one direction, and ranging modes, where price oscillates around a central value. A simple statistical measure like Z-Score can highlight price extremes by comparing the current price against its historical mean and standard deviation. However, such extremes alone can be misleading if the broader market structure is trending forcefully. Uptrick: Z-Score Flow aims to solve this gap by combining Z-Score with an exponential moving average (EMA) trend filter and a smoothed RSI momentum check, thus filtering out signals that contradict the prevailing market environment.

Purpose

The purpose of this script is to help traders pinpoint both mean-reversion opportunities and trend-based pullbacks in a way that is statistically grounded yet still mindful of overarching price action. By pairing Z-Score thresholds with supportive conditions, the script reduces the likelihood of acting on random price spikes or dips and instead focuses on movements that are significant within both historical and current contextual frameworks.

Originality and Uniquness

Layered Signal Verification: Signals require the fulfillment of multiple layers (Z-Score extreme, EMA trend bias, and RSI momentum posture) rather than merely breaching a statistical threshold.

RSI Zone Lockout: Once RSI enters an overbought/oversold zone and triggers a signal, the script locks out subsequent signals until RSI recovers above or below those zones, limiting back-to-back triggers.

Controlled Cooldown: A dedicated cooldown mechanic ensures that the script waits a specified number of bars before issuing a new signal in the opposite direction.

Gradient-Based Visualization: Distinct gradient fills between price and the Z-Mean line enhance readability, showing at a glance whether price is trading above or below its statistical average.

Comprehensive Metrics Panel: An optional on-chart table summarizes the Z-Score’s key metrics, streamlining the process of verifying current statistical extremes, mean levels, and momentum directions.

Why these indicators were merged

Z-Score measurements excel at identifying when price deviates from its mean, but they do not intrinsically reveal whether the market’s trajectory supports a reversion or if price might continue along its trend. The EMA, commonly used for spotting trend directions, offers valuable insight into whether price is predominantly ascending or descending. However, relying solely on a trend filter overlooks the intensity of price moves. RSI then adds a dedicated measure of momentum, helping confirm if the market’s energy aligns with a potential reversal (for example, price is statistically low but RSI suggests looming upward momentum). By uniting these three lenses—Z-Score for statistical context, EMA for trend direction, and RSI for momentum force—the script offers a more comprehensive and adaptable system, aiming to avoid false positives caused by focusing on just one aspect of price behavior.

Calculations

The core calculation begins with a simple moving average (SMA) of price over zLen bars, referred to as the basis. Next, the script computes the standard deviation of price over the same window. Dividing the difference between the current price and the basis by this standard deviation produces the Z-Score, indicating how many standard deviations the price is from its mean. A positive Z-Score reveals price is above its average; a negative reading indicates the opposite.

To detect overall market direction, the script calculates an exponential moving average (emaTrend) over emaTrendLen bars. If price is above this EMA, the script deems the market bullish; if below, it’s considered bearish. For momentum confirmation, the script computes a standard RSI over rsiLen bars, then applies a smoothing EMA over rsiEmaLen bars. This smoothed RSI (rsiEma) is monitored for both its absolute level (oversold or overbought) and its slope (the difference between the current and previous value). Finally, slopeIndex determines how many bars back the script compares the basis to check whether the Z-Mean line is generally rising, falling, or flat, which then informs the coloring scheme on the chart.

Calculations and Rational

Simple Moving Average for Baseline: An SMA is used for the core mean because it places equal weight on each bar in the lookback period. This helps maintain a straightforward interpretation of overbought or oversold conditions in the context of a uniform historical average.

Standard Deviation for Volatility: Standard deviation measures the variability of the data around the mean. By dividing price’s difference from the mean by this value, the Z-Score can highlight whether price is unusually stretched given typical volatility.

Exponential Moving Average for Trend: Unlike an SMA, an EMA places more emphasis on recent data, reacting quicker to new price developments. This quicker response helps the script promptly identify trend shifts, which can be crucial for filtering out signals that go against a strong directional move.

RSI for Momentum Confirmation: RSI is an oscillator that gauges price movement strength by comparing average gains to average losses over a set period. By further smoothing this RSI with another EMA, short-lived oscillations become less influential, making signals more robust.

SlopeIndex for Slope-Based Coloring: To clarify whether the market’s central tendency is rising or falling, the script compares the basis now to its level slopeIndex bars ago. A higher current reading indicates an upward slope; a lower reading, a downward slope; and similar readings, a flat slope. This is visually represented on the chart, providing an immediate sense of the directionality.

Inputs

zLen (Z-Score Period)

Specifies how many bars to include for computing the SMA and standard deviation that form the basis of the Z-Score calculation. Larger values produce smoother but slower signals; smaller values catch quick changes but may generate noise.

emaTrendLen (EMA Trend Filter)

Sets the length of the EMA used to detect the market’s primary direction. This is pivotal for distinguishing whether signals should be considered (price aligning with an uptrend or downtrend) or filtered out.

rsiLen (RSI Length)

Defines the window for the initial RSI calculation. This RSI, when combined with the subsequent smoothing EMA, forms the foundation for momentum-based signal confirmations.

rsiEmaLen (EMA of RSI Period)

Applies an exponential moving average over the RSI readings for additional smoothing. This step helps mitigate rapid RSI fluctuations that might otherwise produce whipsaw signals.

zBuyLevel (Z-Score Buy Threshold)

Determines how negative the Z-Score must be for the script to consider a potential oversold signal. If the Z-Score dives below this threshold (and other criteria are met), a buy signal is generated.

zSellLevel (Z-Score Sell Threshold)

Determines how positive the Z-Score must be for a potential overbought signal. If the Z-Score surpasses this threshold (and other checks are satisfied), a sell signal is generated.

cooldownBars (Cooldown (Bars))

Enforces a bar-based delay between opposite signals. Once a buy signal has fired, the script must wait the specified number of bars before registering a new sell signal, and vice versa.

slopeIndex (Slope Sensitivity (Bars))

Specifies how many bars back the script compares the current basis for slope coloration. A bigger slopeIndex highlights larger directional trends, while a smaller number emphasizes shorter-term shifts.

showMeanLine (Show Z-Score Mean Line)

Enables or disables the plotting of the Z-Mean and its slope-based coloring. Traders who prefer minimal chart clutter may turn this off while still retaining signals.

Features

Statistical Core (Z-Score Detection):

This feature computes the Z-Score by taking the difference between the current price and the basis (SMA) and dividing by the standard deviation. In effect, it translates price fluctuations into a standardized measure that reveals how significant a move is relative to the typical variation seen over the lookback. When the Z-Score crosses predefined thresholds (zBuyLevel for oversold and zSellLevel for overbought), it signals that price could be at an extreme.

How It Works: On each bar, the script updates the SMA and standard deviation. The Z-Score is then refreshed accordingly. Traders can interpret particularly large negative or positive Z-Score values as scenarios where price is abnormally low or high.

EMA Trend Filter:

An EMA over emaTrendLen bars is used to classify the market as bullish if the price is above it and bearish if the price is below it. This classification is applied to the Z-Score signals, accepting them only when they align with the broader price direction.

How It Works: If the script detects a Z-Score below zBuyLevel, it further checks if price is actually in a downtrend (below EMA) before issuing a buy signal. This might seem counterintuitive, but a “downtrend” environment plus an oversold reading often signals a potential bounce or a mean-reversion play. Conversely, for sell signals, the script checks if the market is in an uptrend first. If it is, an overbought reading aligns with potential profit-taking.

RSI Momentum Confirmation with Oversold/Overbought Lockout:

RSI is calculated over rsiLen, then smoothed by an EMA over rsiEmaLen. If this smoothed RSI dips below a certain threshold (for example, 30) and then begins to slope upward, the indicator treats it as a potential sign of recovering momentum. Similarly, if RSI climbs above a certain threshold (for instance, 70) and starts to slope downward, that suggests dwindling momentum. Additionally, once RSI is in these zones, the indicator locks out repetitive signals until RSI fully exits and re-enters those extreme territories.

How It Works: Each bar, the script measures whether RSI has dropped below the oversold threshold (like 30) and has a positive slope. If it does, the buy side is considered “unlocked.” For sell signals, RSI must exceed an overbought threshold (70) and slope downward. The combination of threshold and slope helps confirm that a reversal is genuinely in progress instead of issuing signals while momentum remains weak or stuck in extremes.

Cooldown Mechanism:

The script features a custom bar-based cooldown that prevents issuing new signals in the opposite direction immediately after one is triggered. This helps avoid whipsaw situations where the market quickly flips from oversold to overbought or vice versa.

How It Works: When a buy signal fires, the indicator notes the bar index. If the Z-Score and RSI conditions later suggest a sell, the script compares the current bar index to the last buy signal’s bar index. If the difference is within cooldownBars, the signal is disallowed. This ensures a predefined “quiet period” before switching signals.

Slope-Based Coloring (Z-Mean Line and Shadow):

The script compares the current basis value to its value slopeIndex bars ago. A higher reading now indicates a generally upward slope, while a lower reading indicates a downward slope. The script then shades the Z-Mean line in a corresponding bullish or bearish color, or remains neutral if little change is detected.

How It Works: This slope calculation is refreshingly straightforward: basis – basis . If the result is positive, the line is colored bullish; if negative, it is colored bearish; if approximately zero, it remains neutral. This provides a quick visual cue of the medium-term directional bias.

Gradient Overlays:

With gradient fills, the script highlights where price stands in relation to the Z-Mean. When price is above the basis, a purple-shaded region is painted, visually indicating a “bearish zone” for potential overbought conditions. When price is below, a teal-like overlay is used, suggesting a “bullish zone” for potential oversold conditions.

How It Works: Each bar, the script checks if price is above or below the basis. It then applies a fill between close and basis, using distinct colors to show whether the market is trading above or below its mean. This creates an immediate sense of how extended the market might be.

Buy and Sell Labels (with Alerts):

When a legitimate buy or sell condition passes every check (Z-Score threshold, EMA trend alignment, RSI gating, and cooldown clearance), the script plots a corresponding label directly on the chart. It also fires an alert (if alerts are set up), making it convenient for traders who want timely notifications.

How It Works: If rawBuy or rawSell conditions are met (refined by RSI, EMA trend, and cooldown constraints), the script calls the respective plot function to paint an arrow label on the chart. Alerts are triggered simultaneously, carrying easily recognizable messages.

Metrics Table:

The optional on-chart table (activated by showMetrics) presents real-time Z-Score data, including the current Z-Score, its rolling mean, the maximum and minimum Z-Score values observed over the last zLen bars, a percentile position, and a short-term directional note (rising, falling, or flat).

Current – The present Z-Score reading

Mean – Average Z-Score over the zLen period

Min/Max – Lowest and highest Z-Score values within zLen

Position – Where the current Z-Score sits between the min and max (as a percentile)

Trend – Whether the Z-Score is increasing, decreasing, or flat

Conclusion

Uptrick: Z-Score Flow offers a versatile solution for traders who need a statistically informed perspective on price extremes combined with practical checks for overall trend and momentum. By leveraging a well-defined combination of Z-Score, EMA trend classification, RSI-based momentum gating, slope-based visualization, and a cooldown mechanic, the script reduces the occurrence of false or premature signals. Its gradient fills and optional metrics table contribute further clarity, ensuring that users can quickly assess market posture and make more confident trading decisions in real time.

Disclaimer

This script is intended solely for informational and educational purposes. Trading in any financial market comes with substantial risk, and there is no guarantee of success or the avoidance of loss. Historical performance does not ensure future results. Always conduct thorough research and consider professional guidance prior to making any investment or trading decisions.

[GYTS-CE] Market Regime Detector🧊 Market Regime Detector (Community Edition)

🌸 Part of GoemonYae Trading System (GYTS) 🌸

🌸 --------- INTRODUCTION --------- 🌸

💮 What is the Market Regime Detector?

The Market Regime Detector is an advanced, consensus-based indicator that identifies the current market state to increase the probability of profitable trades. By distinguishing between trending (bullish or bearish) and cyclic (range-bound) market conditions, this detector helps you select appropriate tactics for different environments. Instead of forcing a single strategy across all market conditions, our detector allows you to adapt your approach based on real-time market behaviour.

💮 The Importance of Market Regimes

Markets constantly shift between different behavioural states or "regimes":

• Bullish trending markets - characterised by sustained upward price movement

• Bearish trending markets - characterised by sustained downward price movement

• Cyclic markets - characterised by range-bound, oscillating behaviour

Each regime requires fundamentally different trading approaches. Trend-following strategies excel in trending markets but fail in cyclic ones, while mean-reversion strategies shine in cyclic markets but underperform in trending conditions. Detecting these regimes is essential for successful trading, which is why we've developed the Market Regime Detector to accurately identify market states using complementary detection methods.

🌸 --------- KEY FEATURES --------- 🌸

💮 Consensus-Based Detection

Rather than relying on a single method, our detector employs two complementary detection methodologies that analyse different aspects of market behaviour:

• Dominant Cycle Average (DCA) - analyzes price movement relative to its lookback period, a proxy for the dominant cycle

• Volatility Channel - examines price behaviour within adaptive volatility bands

These diverse perspectives are synthesised into a robust consensus that minimises false signals while maintaining responsiveness to genuine regime changes.

💮 Dominant Cycle Framework

The Market Regime Detector uses the concept of dominant cycles to establish a reference framework. You can input the dominant cycle period that best represents the natural rhythm of your market, providing a stable foundation for regime detection across different timeframes.

💮 Intuitive Parameter System

We've distilled complex technical parameters into intuitive controls that traders can easily understand:

• Adaptability - how quickly the detector responds to changing market conditions

• Sensitivity - how readily the detector identifies transitions between regimes

• Consensus requirement - how much agreement is needed among detection methods

This approach makes the detector accessible to traders of all experience levels while preserving the power of the underlying algorithms.

💮 Visual Market Feedback

The detector provides clear visual feedback about the current market regime through:

• Colour-coded chart backgrounds (purple shades for bullish, pink for bearish, yellow for cyclic)

• Colour-coded price bars

• Strength indicators showing the degree of consensus

• Customizable colour schemes to match your preferences or trading system

💮 Integration in the GYTS suite

The Market Regime Detector is compatible with the GYTS Suite , i.e. it passes the regime into the 🎼 Order Orchestrator where you can set how to trade the trending and cyclic regime.

🌸 --------- CONFIGURATION SETTINGS --------- 🌸

💮 Adaptability

Controls how quickly the Market Regime detector adapts to changing market conditions. You can see it as a low-frequency, long-term change parameter:

Very Low: Very slow adaptation, most stable but may miss regime changes

Low: Slower adaptation, more stability but less responsiveness

Normal: Balanced between stability and responsiveness

High: Faster adaptation, more responsive but less stable

Very High: Very fast adaptation, highly responsive but may generate false signals

This setting affects lookback periods and filter parameters across all detection methods.

💮 Sensitivity

Controls how sensitive the detector is to market regime transitions. This acts as a high-frequency, short-term change parameter:

Very Low: Requires substantial evidence to identify a regime change

Low: Less sensitive, reduces false signals but may miss some transitions

Normal: Balanced sensitivity suitable for most markets

High: More sensitive, detects subtle regime changes but may have more noise

Very High: Very sensitive, detects minor fluctuations but may produce frequent changes

This setting affects thresholds for regime detection across all methods.

💮 Dominant Cycle Period

This parameter allows you to specify the market's natural rhythm in bars. This represents a complete market cycle (up and down movement). Finding the right value for your specific market and timeframe might require some experimentation, but it's a crucial parameter that helps the detector accurately identify regime changes. Most of the times the cycle is between 20 and 40 bars.

💮 Consensus Mode

Determines how the signals from both detection methods are combined to produce the final market regime:

• Any Method (OR) : Signals bullish/bearish if either method detects that regime. If methods conflict (one bullish, one bearish), the stronger signal wins. More sensitive, catches more regime changes but may produce more false signals.

• All Methods (AND) : Signals only when both methods agree on the regime. More conservative, reduces false signals but might miss some legitimate regime changes.

• Weighted Decision : Balances both methods with equal weighting. Provides a middle ground between sensitivity and stability.

Each mode also calculates a continuous regime strength value that's used for colour intensity in the 'unconstrained' display mode.

💮 Display Mode

Choose how to display the market regime colours:

• Unconstrained regime: Shows the regime strength as a continuous gradient. This provides more nuanced visualisation where the intensity of the colour indicates the strength of the trend.

• Consensus only: Shows only the final consensus regime with fixed colours based on the detected regime type.

The background and bar colours will change to indicate the current market regime:

• Purple shades: Bullish trending market (darker purple indicates stronger bullish trend)

• Pink shades: Bearish trending market (darker pink indicates stronger bearish trend)

• Yellow: Cyclic (range-bound) market

💮 Custom Colour Options

The Market Regime Detector allows you to customize the colour scheme to match your personal preferences or to coordinate with other indicators:

• Use custom colours: Toggle to enable your own colour choices instead of the default scheme

• Transparency: Adjust the transparency level of all regime colours

• Bullish colours: Define custom colours for strong, medium, weak, and very weak bullish trends

• Bearish colours: Define custom colours for strong, medium, weak, and very weak bearish trends

• Cyclic colour: Define a custom colour for cyclic (range-bound) market conditions

🌸 --------- DETECTION METHODS --------- 🌸

💮 Dominant Cycle Average (DCA)

The Dominant Cycle Average method forms a key part of our detection system:

1. Theoretical Foundation :

The DCA method builds on cycle analysis and the observation that in trending markets, price consistently remains on one side of a moving average calculated using the dominant cycle period. In contrast, during cyclic markets, price oscillates around this average.

2. Calculation Process :

• We calculate a Simple Moving Average (SMA) using the specified lookback period - a proxy for the dominant cycle period

• We then analyse the proportion of time that price spends above or below this SMA over a lookback window. The theory is that the price should cross the SMA each half cycle, assuming that the dominant cycle period is correct and price follows a sinusoid.

• This lookback window is adaptive, scaling with the dominant cycle period (controlled by the Adaptability setting)

• The different values are standardised and normalised to possess more resolving power and to be more robust to noise.

3. Regime Classification :

• When the normalised proportion exceeds a positive threshold (determined by Sensitivity setting), the market is classified as bullish trending

• When it falls below a negative threshold, the market is classified as bearish trending

• When the proportion remains between these thresholds, the market is classified as cyclic

💮 Volatility Channel

The Volatility Channel method complements the DCA method by focusing on price movement relative to adaptive volatility bands:

1. Theoretical Foundation :

This method is based on the observation that trending markets tend to sustain movement outside of normal volatility ranges, while cyclic markets tend to remain contained within these ranges. By creating adaptive bands that adjust to current market volatility, we can detect when price behaviour indicates a trending or cyclic regime.

2. Calculation Process :

• We first calculate a smooth base channel center using a low pass filter, creating a noise-reduced centreline for price

• True Range (TR) is used to measure market volatility, which is then smoothed and scaled by the deviation factor (controlled by Sensitivity)

• Upper and lower bands are created by adding and subtracting this scaled volatility from the centreline

• Price is smoothed using an adaptive A2RMA filter, which has a very flat and stable behaviour, to reduce noise while preserving trend characteristics

• The position of this smoothed price relative to the bands is continuously monitored

3. Regime Classification :

• When smoothed price moves above the upper band, the market is classified as bullish trending

• When smoothed price moves below the lower band, the market is classified as bearish trending

• When price remains between the bands, the market is classified as cyclic

• The magnitude of price's excursion beyond the bands is used to determine trend strength

4. Adaptive Behaviour :

• The smoothing periods and deviation calculations automatically adjust based on the Adaptability setting

• The measured volatility is calculated over a period proportional to the dominant cycle, ensuring the detector works across different timeframes

• Both the center line and the bands adapt dynamically to changing market conditions, making the detector responsive yet stable

This method provides a unique perspective that complements the DCA approach, with the consensus mechanism synthesising insights from both methods.

🌸 --------- USAGE GUIDE --------- 🌸

💮 Starting with Default Settings

The default settings (Normal for Adaptability and Sensitivity, Weighted Decision for Consensus Mode) provide a balanced starting point suitable for most markets and timeframes. Begin by observing how these settings identify regimes in your preferred instruments.

💮 Finding the Optimal Dominant Cycle

The dominant cycle period is a critical parameter. Here are some approaches to finding an appropriate value:

• Start with typical values, usually something around 25 works well

• Visually identify the average distance between significant peaks and troughs

• Experiment with different values and observe which provides the most stable regime identification

• Consider using cycle-finding indicators to help identify the natural rhythm of your market

💮 Adjusting Parameters

• If you notice too many regime changes → Decrease Sensitivity or increase Consensus requirement

• If regime changes seem delayed → Increase Adaptability

• If a trending regime is not detected, the market is automatically assigned to be in a cyclic state

• If you want to see more nuanced regime transitions → Try the "unconstrained" display mode (note that this will not affect the output to other indicators)

💮 Trading Applications

Regime-Specific Strategies:

• Bullish Trending Regime - Use trend-following strategies, trail stops wider, focus on breakouts, consider holding positions longer, and emphasize buying dips

• Bearish Trending Regime - Consider shorts, tighter stops, focus on breakdown points, sell rallies, implement downside protection, and reduce position sizes

• Cyclic Regime - Apply mean-reversion strategies, trade range boundaries, apply oscillators, target definable support/resistance levels, and use profit-taking at extremes

Strategy Switching:

Create a set of rules for each market regime and switch between them based on the detector's signal. This approach can significantly improve performance compared to applying a single strategy across all market conditions.

GYTS Suite Integration:

• In the GYTS 🎼 Order Orchestrator, select the '🔗 STREAM-int 🧊 Market Regime' as the market regime source

• Note that the consensus output (i.e. not the "unconstrained" display) will be used in this stream

• Create different strategies for trending (bullish/bearish) and cyclic regimes. The GYTS 🎼 Order Orchestrator is specifically made for this.

• The output stream is actually very simple, and can possibly be used in indicators and strategies as well. It outputs 1 for bullish, -1 for bearish and 0 for cyclic regime.

🌸 --------- FINAL NOTES --------- 🌸

💮 Development Philosophy

The Market Regime Detector has been developed with several key principles in mind:

1. Robustness - The detection methods have been rigorously tested across diverse markets and timeframes to ensure reliable performance.

2. Adaptability - The detector automatically adjusts to changing market conditions, requiring minimal manual intervention.

3. Complementarity - Each detection method provides a unique perspective, with the collective consensus being more reliable than any individual method.

4. Intuitiveness - Complex technical parameters have been abstracted into easily understood controls.

💮 Ongoing Refinement

The Market Regime Detector is under continuous development. We regularly:

• Fine-tune parameters based on expanded market data

• Research and integrate new detection methodologies

• Optimise computational efficiency for real-time analysis

Your feedback and suggestions are very important in this ongoing refinement process!

Clustering & Divergences (RSI-Stoch-CCI) [Sam SDF-Solutions]The Clustering & Divergences (RSI-Stoch-CCI) indicator is a comprehensive technical analysis tool that consolidates three popular oscillators—Relative Strength Index (RSI), Stochastic, and Commodity Channel Index (CCI)—into one unified metric called the Score. This Score offers traders an aggregated view of market conditions, allowing them to quickly identify whether the market is oversold, balanced, or overbought.

Functionality:

Oscillator Clustering: The indicator calculates the values of RSI, Stochastic, and CCI using user-defined periods. These oscillator values are then normalized using one of three available methods: MinMax, Z-Score, or Z-Bins.

Score Calculation: Each normalized oscillator value is multiplied by its respective weight (which the user can adjust), and the weighted values are summed to generate an overall Score. This Score serves as a single, interpretable metric representing the combined oscillator behavior.

Market Clustering: The indicator performs clustering on the Score over a configurable window. By dividing the Score range into a set number of clusters (also configurable), the tool visually represents the market’s state. Each cluster is assigned a unique color so that traders can quickly see if the market is trending toward oversold, balanced, or overbought conditions.

Divergence Detection: The script automatically identifies both Regular and Hidden divergences between the price action and the Score. By using pivot detection on both price and Score data, the indicator marks potential reversal signals on the chart with labels and connecting lines. This helps in pinpointing moments when the price and the underlying oscillator dynamics diverge.

Customization Options: Users have full control over the indicator’s behavior. They can adjust:

The periods for each oscillator (RSI, Stochastic, CCI).

The weights applied to each oscillator in the Score calculation.

The normalization method and its manual boundaries.

The number of clusters and whether to invert the cluster order.

Parameters for divergence detection (such as pivot sensitivity and the minimum/maximum bar distance between pivots).

Visual Enhancements:

Depending on the user’s preference, either the Score or the Cluster Index (derived from the clustering process) is plotted on the chart. Additionally, the script changes the color of the price bars based on the identified cluster, providing an at-a-glance visual cue of the current market regime.

Logic & Methodology:

Input Parameters: The script starts by accepting user inputs for clustering settings, oscillator periods, weights, divergence detection, and manual boundary definitions for normalization.

Oscillator Calculation & Normalization: It computes RSI, Stochastic, and CCI values from the price data. These values are then normalized using either the MinMax method (scaling between a lower and upper band) or the Z-Score method (standardizing based on mean and standard deviation), or using Z-Bins for an alternative scaling approach.

Score Computation: Each normalized oscillator is multiplied by its corresponding weight. The sum of these products results in the overall Score that represents the combined oscillator behavior.

Clustering Algorithm: The Score is evaluated over a moving window to determine its minimum and maximum values. Using these values, the script calculates a cluster index that divides the Score into a predefined number of clusters. An option to invert the cluster calculation is provided to adjust the interpretation of the clustering.

Divergence Analysis: The indicator employs pivot detection (using left and right bar parameters) on both the price and the Score. It then compares recent pivot values to detect regular and hidden divergences. When a divergence is found, the script plots labels and optional connecting lines to highlight these key moments on the chart.

Plotting: Finally, based on the user’s selection, the indicator plots either the Score or the Cluster Index. It also overlays manual boundary lines (for the chosen normalization method) and adjusts the bar colors according to the cluster to provide clear visual feedback on market conditions.

_________

By integrating multiple oscillator signals into one cohesive tool, the Clustering & Divergences (RSI-Stoch-CCI) indicator helps traders minimize subjective analysis. Its dynamic clustering and automated divergence detection provide a streamlined method for assessing market conditions and potentially enhancing the accuracy of trading decisions.

For further details on using this indicator, please refer to the guide available at:

2:30 [LuciTech]this is a technical analysis tool designed to highlight key price levels and patterns during a specific trading window, based on UK time (Europe/London). It overlays visual elements on the chart, including a 12 PM reference line, Buy Side Liquidity (BSL) and Sell Side Liquidity (SSL) levels, a highlighted 2:30 PM candle, and Engulfing Fair Value Gaps (FVGs). This indicator is intended for traders who focus on intraday price action and liquidity zones.

Features

The 12 PM Line displays a vertical line at 12:00 PM (UK time) to mark the start of the session. It’s customizable, allowing you to enable or disable it and adjust its color.

BSL/SSL Lines track the highest high (BSL) and lowest low (SSL) from 12:00 PM to 2:00 PM (UK time). These lines extend horizontally until 3:30 PM, after which they remain static at their last recorded levels. You can customize them by enabling or disabling visibility, adjusting colors, choosing a line style (solid, dashed, or dotted), and setting the width.

The 2:30 PM Candle highlights the candle at 2:30 PM (UK time) with a distinct color. It’s customizable, with options to enable or disable it and change its color.

Engulfing FVG (Fair Value Gap) identifies bullish and bearish engulfing patterns with a gap from the prior candle’s range. It draws a shaded box over the FVG area, and you can customize it by enabling or disabling it and adjusting the box color.

How It Works

The indicator operates within a session starting at 12:00 PM (UK time). BSL/SSL levels update between 12:00 PM and 2:00 PM, with lines extending until 3:30 PM. After 3:30 PM, these lines freeze.

BSL/SSL lines show the highest price (BSL) and lowest price (SSL) reached during the 12:00 PM to 2:00 PM window. After 3:30 PM, they remain static, marking the final range boundaries.

The 2:30 PM candle emphasizes a key timestamp, often of interest to intraday traders.

Engulfing FVGs detect significant price gaps created by engulfing candles, which may indicate potential reversal or continuation zones.

Settings

12 PM Line Settings let you toggle visibility and set the line color.

BSL/SSL Line Settings allow you to toggle visibility, set BSL and SSL colors, choose a line style (Solid, Dashed, Dotted), and adjust width (1-4).

2:30 Candle Settings let you toggle visibility and set the candle color.

Engulfing FVG Settings allow you to toggle visibility and set the box color.

Interpretation

The 12 PM Line serves as a reference for the session start.

BSL/SSL Lines may act as potential support or resistance zones or highlight liquidity areas. After 3:30 PM, they remain static, showing the session’s final range.

The 2:30 PM Candle can be monitored for price action signals, such as reversals or breakouts.

Engulfing FVGs shaded areas may indicate imbalances in supply and demand, useful for identifying trade opportunities or stop-loss placement.

Notes

The timezone is set to Europe/London (UK time). Ensure your chart’s timezone aligns for accurate results.

This indicator is best used on intraday timeframes, such as 1-minute or 5-minute charts.

It provides visual aids for analysis and does not generate buy or sell signals on its own.

CBC Strategy with Trend Confirmation & Separate Stop LossCBC Flip Strategy with Trend Confirmation and ATR-Based Targets

This strategy is based on the CBC Flip concept taught by MapleStax and inspired by the original CBC Flip indicator by AsiaRoo. It focuses on identifying potential reversals or trend continuation points using a combination of candlestick patterns (CBC Flips), trend filters, and a time-based entry window. This approach helps traders avoid false signals and increase trade accuracy.

What is a CBC Flip?

The CBC Flip is a candlestick-based pattern that identifies moments when the market is likely to change direction or strengthen its trend. It checks for a shift in price behavior between consecutive candles, signaling a bullish (upward) or bearish (downward) move.

However, not all flips are created equal! This strategy differentiates between Strong Flips and All Flips, allowing traders to choose between a more conservative or aggressive approach.

Strong Flips vs. All Flips

Strong Flips

A Strong Flip is a high-probability setup that occurs only after liquidity is swept from the previous candle’s high or low.

What is a liquidity sweep? This happens when the price briefly moves beyond the high or low of the previous candle, triggering stop-losses and trapping traders in the wrong direction. These sweeps often create fuel for the next move, making them powerful reversal signals.

Examples:

Long Setup: The price dips below the previous candle’s low (sweeping liquidity) and then closes higher, signaling a potential bullish move.

Short Setup: The price moves above the previous candle’s high and then closes lower, signaling a potential bearish move.

Why Use Strong Flips?

They provide fewer signals, but the accuracy is generally higher.

Ideal for trending markets where liquidity sweeps often mark key turning points.

All Flips

All Flips are less selective, offering both Strong Flips and additional signals without requiring a liquidity sweep.

This approach gives traders more frequent opportunities but comes with a higher risk of false signals, especially in sideways markets.

Examples:

Long Setup: A CBC flip occurs without sweeping the previous low, but the trend direction is confirmed (slow EMA is still above VWAP).

Short Setup: A CBC flip occurs without sweeping the previous high, but the trend is still bearish (slow EMA below VWAP).

Why Use All Flips?

Provides more frequent entries for active or aggressive traders.

Works well in trending markets but requires caution during consolidation periods.

How This Strategy Works

The strategy combines CBC Flips with multiple filters to ensure better trade quality:

Trend Confirmation: The slow EMA (20-period) must be positioned relative to the VWAP to confirm the overall trend direction.

Long Trades: Slow EMA must be above VWAP (upward trend).

Short Trades: Slow EMA must be below VWAP (downward trend).

Time-Based Filter: Traders can specify trading hours to limit entries to a particular time window, helping avoid low-volume or high-volatility periods.

Profit Target and Stop-Loss:

Profit Target: Defined as a multiple of the 14-period ATR (Average True Range). For example, if the ATR is 10 points and the profit target multiplier is set to 1.5, the strategy aims for a 15-point profit.

Stop-Loss: Uses a dynamic, candle-based stop-loss:

Long Trades: The trade closes if the market closes below the low of two candles ago.

Short Trades: The trade closes if the market closes above the high of two candles ago.

This approach adapts to recent price behavior and protects against unexpected reversals.

Customizable Settings

Strong Flips vs. All Flips: Choose between a more selective or aggressive entry style.

Profit Target Multiplier: Adjust the ATR multiplier to control the distance for profit targets.

Entry Time Range: Define specific trading hours for the strategy.

Indicators and Visuals

Fast EMA (10-Period) – Black Line

Slow EMA (20-Period) – Red Line

VWAP (Volume-Weighted Average Price) – Orange Line

Visual Labels:

▵ (Triangle Up) – Marks long entries (buy signals).

▿ (Triangle Down) – Marks short entries (sell signals).

Credits

CBC Flip Concept: Inspired by MapleStax, who teaches this concept.

Original Indicator: Developed by AsiaRoo, this strategy builds on the CBC Flip framework with additional features for improved trade management.

Risks and Disclaimer

This strategy is for educational purposes only and does not constitute financial advice.

Trading involves significant risk and may result in the loss of capital. Past performance does not guarantee future results. Use this strategy in a simulated environment before applying it to live trading.

JJ Highlight Time Ranges with First 5 Minutes and LabelsTo effectively use this Pine Script as a day trader , here’s how the various elements can help you manage trades, track time sessions, and monitor price movements:

Key Components for a Day Trader:

1. First 5-Minute Highlight:

- Purpose: Day traders often rely on the first 5 minutes of the trading session to gauge market sentiment, watch for opening price gaps, or plan entries. This script draws a horizontal line at the high or low of the first 5 minutes, which can act as a key level for the rest of the day.

- How to Use: If the price breaks above or below the first 5-minute line, it can signal momentum. You might enter a long position if the price breaks above the first 5-minute high or a short if it breaks below the first 5-minute low.

2. Session Time Highlights:

- Morning Session (9:15–10:30 AM): The market often shows its strongest price action during the first hour of trading. This session is highlighted in yellow. You can use this highlight to focus on the most volatile period, as this is when large institutional moves tend to occur.

- Afternoon Session (12:30–2:55 PM): The blue highlight helps you track the mid-afternoon session, where liquidity may decrease, and price action can sometimes be choppier. Day traders should be more cautious during this period.

- How to Use: By highlighting these key times, you can:

- Focus on key breakouts during the morning session.

- Be more conservative in your trades during the afternoon, as market volatility may drop.

3. Dynamic Labels:

- Top/Bottom Positioning: The script places labels dynamically based on the selected position (Top or Bottom). This allows you to quickly glance at the session's start and identify where you are in terms of time.

- How to Use: Use these labels to remind yourself when major time segments (morning or afternoon) begin. You can adjust your trading strategy depending on the session, e.g., being more aggressive in the morning and more cautious in the afternoon.

Trading Strategy Suggestions:

1. Momentum Trades:

- After the first 5 minutes, use the high/low of that period to set up breakout trades.

- Long Entry: If the price breaks the high of the first 5 minutes (especially if there's a strong trend).

- Short Entry: If the price breaks the low of the first 5 minutes, signaling a potential downtrend.

2. Session-Based Strategy:

- Morning Session (9:15–10:30 AM):

- Look for strong breakout patterns such as support/resistance levels, moving average crossovers, or candlestick patterns (like engulfing candles or pin bars).

- This is a high liquidity period, making it ideal for executing quick trades.

- Afternoon Session (12:30–2:55 PM):

- The market tends to consolidate or show less volatility. Scalping and mean-reversion strategies work better here.

- Avoid chasing big moves unless you see a clear breakout in either direction.

3. Support and Resistance:

- The first 5-minute high/low often acts as a key support or resistance level for the rest of the day. If the price holds above or below this level, it’s an indication of trend continuation.

4. Breakout Confirmation:

- Look for breakouts from the highlighted session time ranges (e.g., 9:15 AM–10:30 AM or 12:30 PM–2:55 PM).

- If a breakout happens during a key time window, combine that with other technical indicators like volume spikes , RSI , or MACD for confirmation.

---

Example Day Trader Usage:

1. First 5 Minutes Strategy: After the market opens at 9:15 AM, watch the price action for the first 5 minutes. The high and low of these 5 minutes are critical levels. If the price breaks above the high of the first 5 minutes, it might indicate a strong bullish trend for the day. Conversely, breaking below the low may suggest bearish movement.