Machine Learning : Cosine Similarity & Euclidean DistanceIntroduction:

This script implements a comprehensive trading strategy that adheres to the established rules and guidelines of housing trading. It leverages advanced machine learning techniques and incorporates customised moving averages, including the Conceptive Price Moving Average (CPMA), to provide accurate signals for informed trading decisions in the housing market. Additionally, signal processing techniques such as Lorentzian, Euclidean distance, Cosine similarity, Know sure thing, Rational Quadratic, and sigmoid transformation are utilised to enhance the signal quality and improve trading accuracy.

Features:

Market Analysis: The script utilizes advanced machine learning methods such as Lorentzian, Euclidean distance, and Cosine similarity to analyse market conditions. These techniques measure the similarity and distance between data points, enabling more precise signal identification and enhancing trading decisions.

Cosine similarity:

Cosine similarity is a measure used to determine the similarity between two vectors, typically in a high-dimensional space. It calculates the cosine of the angle between the vectors, indicating the degree of similarity or dissimilarity.

In the context of trading or signal processing, cosine similarity can be employed to compare the similarity between different data points or signals. The vectors in this case represent the numerical representations of the data points or signals.

Cosine similarity ranges from -1 to 1, with 1 indicating perfect similarity, 0 indicating no similarity, and -1 indicating perfect dissimilarity. A higher cosine similarity value suggests a closer match between the vectors, implying that the signals or data points share similar characteristics.

Lorentzian Classification:

Lorentzian classification is a machine learning algorithm used for classification tasks. It is based on the Lorentzian distance metric, which measures the similarity or dissimilarity between two data points. The Lorentzian distance takes into account the shape of the data distribution and can handle outliers better than other distance metrics.

Euclidean Distance:

Euclidean distance is a distance metric widely used in mathematics and machine learning. It calculates the straight-line distance between two points in Euclidean space. In two-dimensional space, the Euclidean distance between two points (x1, y1) and (x2, y2) is calculated using the formula sqrt((x2 - x1)^2 + (y2 - y1)^2).

Dynamic Time Windows: The script incorporates a dynamic time window function that allows users to define specific time ranges for trading. It checks if the current time falls within the specified window to execute the relevant trading signals.

Custom Moving Averages: The script includes the CPMA, a powerful moving average calculation. Unlike traditional moving averages, the CPMA provides improved support and resistance levels by considering multiple price types and employing a combination of Exponential Moving Averages (EMAs) and Simple Moving Averages (SMAs). Its adaptive nature ensures responsiveness to changes in price trends.

Signal Processing Techniques: The script applies signal processing techniques such as Know sure thing, Rational Quadratic, and sigmoid transformation to enhance the quality of the generated signals. These techniques improve the accuracy and reliability of the trading signals, aiding in making well-informed trading decisions.

Trade Statistics and Metrics: The script provides comprehensive trade statistics and metrics, including total wins, losses, win rate, win-loss ratio, and early signal flips. These metrics offer valuable insights into the performance and effectiveness of the trading strategy.

Usage:

Configuring Time Windows: Users can customize the time windows by specifying the start and finish time ranges according to their trading preferences and local market conditions.

Signal Interpretation: The script generates long and short signals based on the analysis, custom moving averages, and signal processing techniques. Users should pay attention to these signals and take appropriate action, such as entering or exiting trades, depending on their trading strategies.

Trade Statistics: The script continuously tracks and updates trade statistics, providing users with a clear overview of their trading performance. These statistics help users assess the effectiveness of the strategy and make informed decisions.

Conclusion:

With its adherence to housing trading rules, advanced machine learning methods, customized moving averages like the CPMA, and signal processing techniques such as Lorentzian, Euclidean distance, Cosine similarity, Know sure thing, Rational Quadratic, and sigmoid transformation, this script offers users a powerful tool for housing market analysis and trading. By leveraging the provided signals, time windows, and trade statistics, users can enhance their trading strategies and improve their overall trading performance.

Disclaimer:

Please note that while this script incorporates established tradingview housing rules, advanced machine learning techniques, customized moving averages, and signal processing techniques, it should be used for informational purposes only. Users are advised to conduct their own analysis and exercise caution when making trading decisions. The script's performance may vary based on market conditions, user settings, and the accuracy of the machine learning methods and signal processing techniques. The trading platform and developers are not responsible for any financial losses incurred while using this script.

By publishing this script on the platform, traders can benefit from its professional presentation, clear instructions, and the utilisation of advanced machine learning techniques, customised moving averages, and signal processing techniques for enhanced trading signals and accuracy.

I extend my gratitude to TradingView, LUX ALGO, and JDEHORTY for their invaluable contributions to the trading community. Their innovative scripts, meticulous coding patterns, and insightful ideas have profoundly enriched traders' strategies, including my own.

Cerca negli script per "如何用wind搜索股票的发行价和份数"

JOPA Channel (Dual-Volumed) v1 [JopAlgo]JOPA Channel (Dual-Volumed) v1

Short title: JOPAV1 • License: MPL-2.0 • Provider: JopAlgo

We have developed our own, first channel-based trading indicator and we’re making it available to all traders. The goal was a channel that breathes with the tape—built on a volume-weighted backbone—so the outcome stays lively instead of static. That led to the JOPA Channel.

All important features (at a glance)

In one line: A Rolling-VWAP channel whose width adapts with two volumes (RVOL + dollar-flow), adds order-flow asymmetry (OBV tilt) and regime awareness (Efficiency Ratio), and frames risk with outer containment bands from residual extremes—so you see fair value, momentum, and exhaustion in one view.

Feature list

Rolling VWAP centerline: Tracks where volume traded (fair value).

Dual-volume width: Bands expand/contract with relative volume and value traded (price×volume).

OBV tilt: Upper/lower widths skew toward the side actually pushing.

Regime adapter (ER): Tighter in trend, wider in chop—automatically.

Outer containment rails: Residual-extreme ceilings/floors, smoothed + margin.

20% / 80% guides: 20% light blue (discount), 80% light red (premium).

Squeeze dots (optional): Orange circles below candles during compression.

Non-repainting: Uses rolling sums and past-only math; no lookahead.

Default visual in this release

Containment rails + fill: ON (stepline, medium).

Inner Value rails + fill: Rails OFF (stepline, thin), fill ON (drawn only if rails are shown).

20% & 80% guides: ON (dashed, thin; 20% light blue, 80% light red).

Squeeze dots: OFF by default (orange circles when enabled).

What you see on the chart

RVWAP (centerline): Your compass for fair value.

Inner Value Bands (optional): Tight rails for breakouts and pullback timing.

Outer Containment Bands (default ON): High-confidence ceilings/floors for targets and fades.

20% / 80% guides: Quick read of “where in the channel” price is sitting.

Squeeze dots (optional): Volatility compression heads-up (no text labels).

Non-repainting note: The indicator does not revise closed bars. Forecast-Lock uses linear regression to extrapolate 1–3 bars ahead without using future data.

How to use it

Core reads (works on any timeframe)

Bias: Above a rising RVWAP → long bias; below a falling RVWAP → short bias.

Breakouts (momentum): Close beyond an Inner Value rail with RVOL ≥ threshold (alert provided).

Reversions (fades): Tag Outer Containment, stall, then close back inside → expect mean reversion toward RVWAP.

20/80 timing:

At/above 80% (light red) → premium/exhaustion risk; trim longs or consider fades if RVOL cools.

At/below 20% (light blue) → discount/exhaustion risk; trim shorts or consider longs if RVOL cools.

Squeeze clusters: When dots bunch up, expect a range break; use the Breakout alert as confirmation.

Playbooks by trading style

Day Trading (1–5m)

Setup: Keep the chart clean (Containment ON, Value rails OFF). Toggle Inner Value ON when hunting a breakout or timing a pullback.

Pullback Long: Dip to RVWAP / Lower Value with sub-threshold RVOL, then a close back above RVWAP → long.

Stop: Just beyond Lower Containment or the pullback swing.

Targets (1:1:1): ⅓ at RVWAP, ⅓ at Upper Value, ⅓ trail toward Upper Containment.

Breakout Long: After a squeeze cluster, take the Breakout Long alert (close > Upper Value, RVOL ≥ min). If no retest, demand the next bar holds outside.

Range Fade: Only when RVWAP is flat and dots cluster; short Upper Containment → RVWAP (mirror for longs at the lower rail).

Intraday (15m–1H)

HTF compass: Take bias from 4H.

Pullback Long: “Touch & reclaim” of RVWAP while RVOL cools; enter on the reclaim close or break of that candle’s high.

Breakout: Run Inner Value ON; act on Breakout alerts (RVOL gate ≈ 1.10–1.15 typical).

Avoid low-probability fades against the 4H slope unless RVWAP is flat.

Swing (4H–1D)

Continuation: In uptrends, buy pullbacks to RVWAP / Lower Value with sub-threshold RVOL; scale at Upper Containment.

Adds: Post-squeeze Breakout Long adds; trail on RVWAP or Lower Value.

Fades: Prefer when RVWAP flattens and price oscillates between containments.

Position (1D+)

Framework: Daily RVWAP slope + position within containment.

Add rule: Each reclaim of RVWAP after a dip is an add; trim into Upper Containment or near 80% light red.

Sizing: Containment distance is larger—size down and trail on RVWAP.

Inputs & Settings (complete)

Core

Source: Price input for RVWAP.

Rolling VWAP Length: Window of the centerline (higher = smoother).

Volume Baseline (RVOL): SMA window for relative volume.

Inner Value Bands (volatility-based width)

k·StdDev(residuals), k·ATR, k·MAD(residuals): Blend three measures into base width.

StdDev / ATR / MAD Lengths: Lookbacks for each.

Two-Volume Fusion

RVOL Exponent: How aggressively width responds to relative volume.

Dollar-Flow Gain: Adds push from price×volume (value traded).

Dollar-Flow Z-Window: Standardization window for dollar-flow.

Asymmetry (Order-Flow Tilt)

Enable Tilt (OBV): Lets flow skew upper/lower widths.

Tilt Strength (0..1): Gain applied to OBV slope z-score.

OBV Slope Z-Window: Window to standardize OBV slope.

Regime Adapter

Efficiency Ratio Lookback: Measures trend vs chop.

ER Width Min/Max: Maps ER into a width factor (tighter in trend, wider in chop).

Band Tracking (inner value rails)

Tracking Mode:

Base: Pure base rails.

Parallel-Lock: Smooth RVWAP & width; track in parallel.

Slope-Lock: Adds a fraction of recent slope (momentum-friendly).

Forecast-Lock: 1–3 bar extrapolation via linreg (non-repainting on closed bars).

Attach Strength (0..1): Blend tracked rails vs base rails.

Tracking Smooth Length: EMA smoothing of RVWAP and width.

Slope Influence / Forecast Lead Bars: Gains for the chosen mode.

Outer Containment Bands

Show Containment Bands: Master toggle (default ON).

Residual Extremes Lookback: Highest/lowest residual window.

Extreme Smoothing (EMA): Stability on extreme lines.

Margin vs inner width: Extra padding relative to smoothed inner width.

Squeeze & Alerts

Squeeze Window / Threshold: Width vs average; at/under threshold = dot (when enabled).

Min RVOL for Breakout: Required RVOL for breakout alerts.

Style (defaults in this release)

Inner Value rails: OFF (stepline, thin).

Inner & Containment fills: ON.

Containment rails: ON (stepline, medium).

20% / 80% guides: ON — 20% light blue, 80% light red, dashed, thin.

Squeeze dots: OFF by default (orange circles below candles when enabled).

Practical templates (copy/paste into a plan)

Momentum Breakout

Context: Squeeze cluster near RVWAP; Inner Value ON.

Trigger: Breakout Long (close > Upper Value & RVOL ≥ min).

Stop: Below Lower Value (tight) or below RVWAP (safer).

Targets (1:1:1): ⅓ Value → ⅓ Containment → ⅓ trail on RVWAP.

Pullback Continuation

Context: Uptrend; dip to RVWAP / Lower Value with cooling RVOL.

Trigger: Close back above RVWAP or break of reclaim candle’s high.

Stop: Just outside Lower Containment or pullback swing.

Targets: RVWAP → Upper Value → Upper Containment.

Containment Reversion (range)

Context: RVWAP flat; repeated containment tags.

Trigger: Stall at containment, then close back inside.

Stop: A step beyond that containment.

Target: RVWAP; runner only if RVOL stays muted.

Alerts included

DVWAP Breakout Long / Short (Value Bands)

Top Zone / Bottom Zone (20% / 80% guides)

Tip: On lower TFs, act on Breakout alerts with higher-TF bias (e.g., trade 5–15m in the direction of 1H/4H RVWAP slope/position).

Best practices

Let RVWAP be the compass; if unsure, wait until price picks a side.

Respect RVOL; low-RVOL breaks are prone to fail.

Use guides for timing, not certainty. Pair 20/80 zones with flow context.

Start with defaults; change one knob at a time.

Common pitfalls

Fading every containment touch → only fade when RVWAP is flat or RVOL cools.

Over-tuning inputs → the defaults are robust; small tweaks go a long way.

Fighting the higher timeframe on low TFs → expensive habit.

Footer — License & Publishing

License: Mozilla Public License 2.0 (MPL-2.0). You may modify and redistribute; keep this file under MPL and provide source for this file.

Originality: © 2025 JopAlgo. No third-party code reused; Pine built-ins and common formulas only.

Publishing: Keep this header/description intact when releasing on TradingView. Avoid promotional links in the public script text.

Sunil BB Blast Heikin Ashi StrategySunil BB Blast Heikin Ashi Strategy

The Sunil BB Blast Heikin Ashi Strategy is a trend-following trading strategy that combines Bollinger Bands with Heikin-Ashi candles for precise market entries and exits. It aims to capitalize on price volatility while ensuring controlled risk through dynamic stop-loss and take-profit levels based on a user-defined Risk-to-Reward Ratio (RRR).

Key Features:

Trading Window:

The strategy operates within a user-defined time window (e.g., from 09:20 to 15:00) to align with market hours or other preferred trading sessions.

Trade Direction:

Users can select between Long Only, Short Only, or Long/Short trade directions, allowing flexibility depending on market conditions.

Bollinger Bands:

Bollinger Bands are used to identify potential breakout or breakdown zones. The strategy enters trades when price breaks through the upper or lower Bollinger Band, indicating a possible trend continuation.

Heikin-Ashi Candles:

Heikin-Ashi candles help smooth price action and filter out market noise. The strategy uses these candles to confirm trend direction and improve entry accuracy.

Risk Management (Risk-to-Reward Ratio):

The strategy automatically adjusts the take-profit (TP) level and stop-loss (SL) based on the selected Risk-to-Reward Ratio (RRR). This ensures that trades are risk-managed effectively.

Automated Alerts and Webhooks:

The strategy includes automated alerts for trade entries and exits. Users can set up JSON webhooks for external execution or trading automation.

Active Position Tracking:

The strategy tracks whether there is an active position (long or short) and only exits when price hits the pre-defined SL or TP levels.

Exit Conditions:

The strategy exits positions when either the take-profit (TP) or stop-loss (SL) levels are hit, ensuring risk management is adhered to.

Default Settings:

Trading Window:

09:20-15:00

This setting confines the strategy to the specified hours, ensuring trading only occurs during active market hours.

Strategy Direction:

Default: Long/Short

This allows for both long and short trades depending on market conditions. You can select "Long Only" or "Short Only" if you prefer to trade in one direction.

Bollinger Band Length (bbLength):

Default: 19

Length of the moving average used to calculate the Bollinger Bands.

Bollinger Band Multiplier (bbMultiplier):

Default: 2.0

Multiplier used to calculate the upper and lower bands. A higher multiplier increases the width of the bands, leading to fewer but more significant trades.

Take Profit Multiplier (tpMultiplier):

Default: 2.0

Multiplier used to determine the take-profit level based on the calculated stop-loss. This ensures that the profit target aligns with the selected Risk-to-Reward Ratio.

Risk-to-Reward Ratio (RRR):

Default: 1.0

The ratio used to calculate the take-profit relative to the stop-loss. A higher RRR means larger profit targets.

Trade Automation (JSON Webhooks):

Allows for integration with external systems for automated execution:

Long Entry JSON: Customizable entry condition for long positions.

Long Exit JSON: Customizable exit condition for long positions.

Short Entry JSON: Customizable entry condition for short positions.

Short Exit JSON: Customizable exit condition for short positions.

Entry Logic:

Long Entry:

The strategy enters a long position when:

The Heikin-Ashi candle shows a bullish trend (green close > open).

The price is above the upper Bollinger Band, signaling a breakout.

The previous candle also closed higher than it opened.

Short Entry:

The strategy enters a short position when:

The Heikin-Ashi candle shows a bearish trend (red close < open).

The price is below the lower Bollinger Band, signaling a breakdown.

The previous candle also closed lower than it opened.

Exit Logic:

Take-Profit (TP):

The take-profit level is calculated as a multiple of the distance between the entry price and the stop-loss level, determined by the selected Risk-to-Reward Ratio (RRR).

Stop-Loss (SL):

The stop-loss is placed at the opposite Bollinger Band level (lower for long positions, upper for short positions).

Exit Trigger:

The strategy exits a trade when either the take-profit or stop-loss level is hit.

Plotting and Visuals:

The Heikin-Ashi candles are displayed on the chart, with green candles for uptrends and red candles for downtrends.

Bollinger Bands (upper, lower, and basis) are plotted for visual reference.

Entry points for long and short trades are marked with green and red labels below and above bars, respectively.

Strategy Alerts:

Alerts are triggered when:

A long entry condition is met.

A short entry condition is met.

A trade exits (either via take-profit or stop-loss).

These alerts can be used to trigger notifications or webhook events for automated trading systems.

Notes:

The strategy is designed for use on intraday charts but can be applied to any timeframe.

It is highly customizable, allowing for tailored risk management and trading windows.

The Sunil BB Blast Heikin Ashi Strategy combines two powerful technical analysis tools (Bollinger Bands and Heikin-Ashi candles) with strong risk management, making it suitable for both beginners and experienced traders.

Feebacks are welcome from the users.

Market Flow Volatility Oscillator (AiBitcoinTrend)The Market Flow Volatility Oscillator (AiBitcoinTrend) is a cutting-edge technical analysis tool designed to evaluate and classify market volatility regimes. By leveraging Gaussian filtering and clustering techniques, this indicator provides traders with clear insights into periods of high and low volatility, helping them adapt their strategies to evolving market conditions. Built for precision and clarity, it combines advanced mathematical models with intuitive visual feedback to identify trends and volatility shifts effectively.

👽 How the Indicator Works

👾 Volatility Classification with Gaussian Filtering

The indicator detects volatility levels by applying Gaussian filters to the price series. Gaussian filters smooth out noise while preserving significant price movements. Traders can adjust the smoothing levels using sigma parameters, enabling greater flexibility:

Low Sigma: Emphasizes short-term volatility.

High Sigma: Captures broader trends with reduced sensitivity to small fluctuations.

👾 Clustering Algorithm for Regime Detection

The core of this indicator is its clustering model, which classifies market conditions into two distinct regimes:

Low Volatility Regime: Calm periods with reduced market activity.

High Volatility Regime: Intense periods with heightened price movements.

The clustering process works as follows:

A rolling window of data is analyzed to calculate the standard deviation of price returns.

Two cluster centers are initialized using the 25th and 75th percentiles of the data distribution.

Each price volatility value is assigned to the nearest cluster based on its distance to the centers.

The cluster centers are refined iteratively, providing an accurate and adaptive classification.

👾 Oscillator Generation with Slope R-Values

The indicator computes Gaussian filter slopes to generate oscillators that visualize trends:

Oscillator Low: Captures low-frequency market behavior.

Oscillator High: Tracks high-frequency, faster-changing trends.

The slope is measured using the R-value of the linear regression fit, scaled and adjusted for easier interpretation.

👽 Applications

👾 Trend Trading

When the oscillator rises above 0.5, it signals potential bullish momentum, while dips below 0.5 suggest bearish sentiment.

👾 Pullback Detection

When the oscillator peaks, especially in overbought or oversold zones, provide early warnings of potential reversals.

👽 Indicator Settings

👾 Oscillator Settings

Sigma Low/High: Controls the smoothness of the oscillators.

Smaller Values: React faster to price changes but introduce more noise.

Larger Values: Provide smoother signals with longer-term insights.

👾 Window Size and Refit Interval

Window Size: Defines the rolling period for cluster and volatility calculations.

Shorter windows: adapt faster to market changes.

Longer windows: produce stable, reliable classifications.

Disclaimer: This information is for entertainment purposes only and does not constitute financial advice. Please consult with a qualified financial advisor before making any investment decisions.

Heartbeat Momentum Strategy BetaHeartbeat Momentum Strategy Beta

Overview

The Heartbeat Momentum Strategy is an innovative approach to market analysis that draws inspiration from the rhythmic patterns of a heartbeat. This strategy aims to identify significant momentum shifts in the market by comparing short-term and long-term moving averages, analogous to detecting irregularities in a heartbeat.

Key Concepts

Market Heartbeat: The difference between short-term and long-term moving averages, representing the market's current 'pulse'.

Heartbeat Volatility: Measured by the standard deviation of the market heartbeat.

Momentum Signals: Generated when the heartbeat deviates significantly from its normal range.

How It Works

Calculates a short-term moving average (default 5 periods) and a long-term moving average (default 20 periods) of the closing price.

Computes the 'heartbeat' by subtracting the long-term MA from the short-term MA.

Measures the volatility of the heartbeat using its standard deviation over the long-term period.

Generates buy signals when the heartbeat exceeds 2 standard deviations above its mean.

Generates sell signals when the heartbeat falls 2 standard deviations below its mean.

Indicator Components

Blue Line: Short-term moving average

Red Line: Long-term moving average

Green Triangles: Buy signals

Red Triangles: Sell signals

Background Color: Light green during buy signals, light red during sell signals

Strategy Parameters

Short MA Window: The period for the short-term moving average (default: 5)

Long MA Window: The period for the long-term moving average (default: 20)

Standard Deviation Threshold: The number of standard deviations to trigger a signal (default: 2.0)

Interpretation

Buy Signal: Indicates a potential strong upward momentum shift. Consider opening long positions or closing short positions.

Sell Signal: Suggests a potential strong downward momentum shift. Consider opening short positions or closing long positions.

No Signal: The market is moving within its normal rhythm. Maintain current positions or look for other entry opportunities.

Customization

Users can adjust the strategy parameters to suit different assets, timeframes, or trading styles:

Decrease the MA windows for more frequent signals (more suitable for shorter timeframes).

Increase the MA windows for fewer, potentially more significant signals (better for longer timeframes).

Adjust the Standard Deviation Threshold to fine-tune sensitivity (lower for more signals, higher for fewer but potentially stronger signals).

Risk Management

While this strategy can provide valuable insights into market momentum, it should not be used in isolation:

Always use stop-loss orders to manage potential losses.

Consider the overall market context and other technical/fundamental factors.

Be aware of potential false signals, especially in ranging or highly volatile markets.

Backtest and forward-test the strategy with different parameters before live trading.

Conclusion

The Heartbeat Momentum Strategy offers a unique perspective on market movements by treating price action like a heartbeat. By identifying significant deviations from the normal market rhythm, it aims to capture strong momentum shifts while filtering out market noise. As with any trading strategy, use it as part of a comprehensive trading plan and always practice sound risk management.

Trend Line Methods (TLM)Trend Line Methods (TLM)

Overview

Trend Line Methods (TLM) is a visual study designed to help traders explore trend structure using two complementary, auto-drawn trend channels. The script focuses on how price interacts with rising or falling boundaries over time. It does not generate trade signals or manage risk; its purpose is to support discretionary chart analysis.

Method 1 – Pivot Span Trendline

The Pivot Span Trendline method builds a dynamic channel from major swing points detected by pivot highs and pivot lows.

• The script tracks a configurable number of recent pivot highs and lows.

• From the oldest and most recent stored pivot highs, it draws an upper trend line.

• From the oldest and most recent stored pivot lows, it draws a lower trend line.

• An optional filled area can be drawn between the two lines to highlight the active trend span.

As new pivots form, the lines are recalculated so that the channel evolves with market structure. This method is useful for visualising how price respects a trend corridor defined directly by swing points.

Method 2 – 5-Point Straight Channel

The 5-Point Straight Channel method approximates a straight trend channel using five key points extracted from a fixed lookback window.

Within the selected window:

• The window is divided into five segments of similar length.

• In each segment, the highest high is used as a representative high point.

• In each segment, the lowest low is used as a representative low point.

• A straight regression-style line is fitted through the five high points to form the upper boundary.

• A second straight line is fitted through the five low points to form the lower boundary.

The result is a pair of straight lines that describe the overall directional channel of price over the chosen window. Compared to Method 1, this approach is less focused on the very latest swings and more on the broader slope of the market.

Inputs & Menus

Pivot Span Trendline group (Method 1)

• Enable Pivot Span Trendline – Turns Method 1 on or off.

• High trend line color / Low trend line color – Colors of the upper and lower trend lines.

• Fill color between trend lines – Base color used to shade the area between the two lines. Transparency is controlled internally.

• Trend line thickness – Line width for both high and low trend lines.

• Trend line style – Line style (solid, dashed, or dotted).

• Pivot Left / Pivot Right – Number of bars to the left and right used to confirm pivot highs and lows. Larger values produce fewer but more significant swing points.

• Pivot Count – How many historical pivot points are kept for constructing the trend lines.

• Lookback Length – Number of bars used to keep pivots in range and to extend the trend lines across the chart.

5-Point Straight Channel group (Method 2)

• Enable 5-Point Straight Channel – Turns Method 2 on or off.

• High channel line color / Low channel line color – Colors of the upper and lower channel lines.

• Channel line thickness – Line width for both channel lines.

• Channel line style – Line style (solid, dashed, or dotted).

• Channel Length (bars) – Lookback window used to divide price into five segments and build the straight high/low channel.

Using Both Methods Together

Both methods are designed to visualise the same underlying idea: price tends to move inside rising or falling channels. Method 1 emphasises the most recent swing structure via pivot points, while Method 2 summarises the broader channel over a fixed window.

When the Pivot Span Trendline corridor and the 5-Point Straight Channel boundaries align or intersect, they can highlight zones where multiple ways of drawing trend lines point to similar support or resistance areas. Traders can use these confluence zones as a visual reference when planning their own entries, exits, or risk levels, according to their personal trading plan.

Notes

• This script is meant as an educational and analytical tool for studying trend lines and channels.

• It does not generate trading signals and does not replace independent analysis or risk management.

• The behaviour of both methods is timeframe- and symbol-agnostic; they will adapt to whichever chart you apply them to.

Historical Matrix Analyzer [PhenLabs]📊Historical Matrix Analyzer

Version: PineScriptv6

📌Description

The Historical Matrix Analyzer is an advanced probabilistic trading tool that transforms technical analysis into a data-driven decision support system. By creating a comprehensive 56-cell matrix that tracks every combination of RSI states and multi-indicator conditions, this indicator reveals which market patterns have historically led to profitable outcomes and which have not.

At its core, the indicator continuously monitors seven distinct RSI states (ranging from Extreme Oversold to Extreme Overbought) and eight unique indicator combinations (MACD direction, volume levels, and price momentum). For each of these 56 possible market states, the system calculates average forward returns, win rates, and occurrence counts based on your configurable lookback period. The result is a color-coded probability matrix that shows you exactly where you stand in the historical performance landscape.

The standout feature is the Current State Panel, which provides instant clarity on your active market conditions. This panel displays signal strength classifications (from Strong Bullish to Strong Bearish), the average return percentage for similar past occurrences, an estimated win rate using Bayesian smoothing to prevent small-sample distortions, and a confidence level indicator that warns you when insufficient data exists for reliable conclusions.

🚀Points of Innovation

Multi-dimensional state classification combining 7 RSI levels with 8 indicator combinations for 56 unique trackable market conditions

Bayesian win rate estimation with adjustable smoothing strength to provide stable probability estimates even with limited historical samples

Real-time active cell highlighting with “NOW” marker that visually connects current market conditions to their historical performance data

Configurable color intensity sensitivity allowing traders to adjust heat-map responsiveness from conservative to aggressive visual feedback

Dual-panel display system separating the comprehensive statistics matrix from an easy-to-read current state summary panel

Intelligent confidence scoring that automatically warns traders when occurrence counts fall below reliable thresholds

🔧Core Components

RSI State Classification: Segments RSI readings into 7 distinct zones (Extreme Oversold <20, Oversold 20-30, Weak 30-40, Neutral 40-60, Strong 60-70, Overbought 70-80, Extreme Overbought >80) to capture momentum extremes and transitions

Multi-Indicator Condition Tracking: Simultaneously monitors MACD crossover status (bullish/bearish), volume relative to moving average (high/low), and price direction (rising/falling) creating 8 binary-encoded combinations

Historical Data Storage Arrays: Maintains rolling lookback windows storing RSI states, indicator states, prices, and bar indices for precise forward-return calculations

Forward Performance Calculator: Measures price changes over configurable forward bar periods (1-20 bars) from each historical state, accumulating total returns and win counts per matrix cell

Bayesian Smoothing Engine: Applies statistical prior assumptions (default 50% win rate) weighted by user-defined strength parameter to stabilize estimated win rates when sample sizes are small

Dynamic Color Mapping System: Converts average returns into color-coded heat map with intensity adjusted by sensitivity parameter and transparency modified by confidence levels

🔥Key Features

56-Cell Probability Matrix: Comprehensive grid displaying every possible combination of RSI state and indicator condition, with each cell showing average return percentage, estimated win rate, and occurrence count for complete statistical visibility

Current State Info Panel: Dedicated display showing your exact position in the matrix with signal strength emoji indicators, numerical statistics, and color-coded confidence warnings for immediate situational awareness

Customizable Lookback Period: Adjustable historical window from 50 to 500 bars allowing traders to focus on recent market behavior or capture longer-term pattern stability across different market cycles

Configurable Forward Performance Window: Select target holding periods from 1 to 20 bars ahead to align probability calculations with your trading timeframe, whether day trading or swing trading

Visual Heat Mapping: Color-coded cells transition from red (bearish historical performance) through gray (neutral) to green (bullish performance) with intensity reflecting statistical significance and occurrence frequency

Intelligent Data Filtering: Minimum occurrence threshold (1-10) removes unreliable patterns with insufficient historical samples, displaying gray warning colors for low-confidence cells

Flexible Layout Options: Independent positioning of statistics matrix and info panel to any screen corner, accommodating different chart layouts and personal preferences

Tooltip Details: Hover over any matrix cell to see full RSI label, complete indicator status description, precise average return, estimated win rate, and total occurrence count

🎨Visualization

Statistics Matrix Table: A 9-column by 8-row grid with RSI states labeling vertical axis and indicator combinations on horizontal axis, using compact abbreviations (XOverS, OverB, MACD↑, Vol↓, P↑) for space efficiency

Active Cell Indicator: The current market state cell displays “⦿ NOW ⦿” in yellow text with enhanced color saturation to immediately draw attention to relevant historical performance

Signal Strength Visualization: Info panel uses emoji indicators (🔥 Strong Bullish, ✅ Bullish, ↗️ Weak Bullish, ➖ Neutral, ↘️ Weak Bearish, ⛔ Bearish, ❄️ Strong Bearish, ⚠️ Insufficient Data) for rapid interpretation

Histogram Plot: Below the price chart, a green/red histogram displays the current cell’s average return percentage, providing a time-series view of how historical performance changes as market conditions evolve

Color Intensity Scaling: Cell background transparency and saturation dynamically adjust based on both the magnitude of average returns and the occurrence count, ensuring visual emphasis on reliable patterns

Confidence Level Display: Info panel bottom row shows “High Confidence” (green), “Medium Confidence” (orange), or “Low Confidence” (red) based on occurrence counts relative to minimum threshold multipliers

📖Usage Guidelines

RSI Period

Default: 14

Range: 1 to unlimited

Description: Controls the lookback period for RSI momentum calculation. Standard 14-period provides widely-recognized overbought/oversold levels. Decrease for faster, more sensitive RSI reactions suitable for scalping. Increase (21, 28) for smoother, longer-term momentum assessment in swing trading. Changes affect how quickly the indicator moves between the 7 RSI state classifications.

MACD Fast Length

Default: 12

Range: 1 to unlimited

Description: Sets the faster exponential moving average for MACD calculation. Standard 12-period setting works well for daily charts and captures short-term momentum shifts. Decreasing creates more responsive MACD crossovers but increases false signals. Increasing smooths out noise but delays signal generation, affecting the bullish/bearish indicator state classification.

MACD Slow Length

Default: 26

Range: 1 to unlimited

Description: Defines the slower exponential moving average for MACD calculation. Traditional 26-period setting balances trend identification with responsiveness. Must be greater than Fast Length. Wider spread between fast and slow increases MACD sensitivity to trend changes, impacting the frequency of indicator state transitions in the matrix.

MACD Signal Length

Default: 9

Range: 1 to unlimited

Description: Smoothing period for the MACD signal line that triggers bullish/bearish state changes. Standard 9-period provides reliable crossover signals. Shorter values create more frequent state changes and earlier signals but with more whipsaws. Longer values produce more confirmed, stable signals but with increased lag in detecting momentum shifts.

Volume MA Period

Default: 20

Range: 1 to unlimited

Description: Lookback period for volume moving average used to classify volume as “high” or “low” in indicator state combinations. 20-period default captures typical monthly trading patterns. Shorter periods (10-15) make volume classification more reactive to recent spikes. Longer periods (30-50) require more sustained volume changes to trigger state classification shifts.

Statistics Lookback Period

Default: 200

Range: 50 to 500

Description: Number of historical bars used to calculate matrix statistics. 200 bars provides substantial data for reliable patterns while remaining responsive to regime changes. Lower values (50-100) emphasize recent market behavior and adapt quickly but may produce volatile statistics. Higher values (300-500) capture long-term patterns with stable statistics but slower adaptation to changing market dynamics.

Forward Performance Bars

Default: 5

Range: 1 to 20

Description: Number of bars ahead used to calculate forward returns from each historical state occurrence. 5-bar default suits intraday to short-term swing trading (5 hours on hourly charts, 1 week on daily charts). Lower values (1-3) target short-term momentum trades. Higher values (10-20) align with position trading and longer-term pattern exploitation.

Color Intensity Sensitivity

Default: 2.0

Range: 0.5 to 5.0, step 0.5

Description: Amplifies or dampens the color intensity response to average return magnitudes in the matrix heat map. 2.0 default provides balanced visual emphasis. Lower values (0.5-1.0) create subtle coloring requiring larger returns for full saturation, useful for volatile instruments. Higher values (3.0-5.0) produce vivid colors from smaller returns, highlighting subtle edges in range-bound markets.

Minimum Occurrences for Coloring

Default: 3

Range: 1 to 10

Description: Required minimum sample size before applying color-coded performance to matrix cells. Cells with fewer occurrences display gray “insufficient data” warning. 3-occurrence default filters out rare patterns. Lower threshold (1-2) shows more data but includes unreliable single-event statistics. Higher thresholds (5-10) ensure only well-established patterns receive visual emphasis.

Table Position

Default: top_right

Options: top_left, top_right, bottom_left, bottom_right

Description: Screen location for the 56-cell statistics matrix table. Position to avoid overlapping critical price action or other indicators on your chart. Consider chart orientation and candlestick density when selecting optimal placement.

Show Current State Panel

Default: true

Options: true, false

Description: Toggle visibility of the dedicated current state information panel. When enabled, displays signal strength, RSI value, indicator status, average return, estimated win rate, and confidence level for active market conditions. Disable to declutter charts when only the matrix table is needed.

Info Panel Position

Default: bottom_left

Options: top_left, top_right, bottom_left, bottom_right

Description: Screen location for the current state information panel (when enabled). Position independently from statistics matrix to optimize chart real estate. Typically placed opposite the matrix table for balanced visual layout.

Win Rate Smoothing Strength

Default: 5

Range: 1 to 20

Description: Controls Bayesian prior weighting for estimated win rate calculations. Acts as virtual sample size assuming 50% win rate baseline. Default 5 provides moderate smoothing preventing extreme win rate estimates from small samples. Lower values (1-3) reduce smoothing effect, allowing win rates to reflect raw data more directly. Higher values (10-20) increase conservatism, pulling win rate estimates toward 50% until substantial evidence accumulates.

✅Best Use Cases

Pattern-based discretionary trading where you want historical confirmation before entering setups that “look good” based on current technical alignment

Swing trading with holding periods matching your forward performance bar setting, using high-confidence bullish cells as entry filters

Risk assessment and position sizing, allocating larger size to trades originating from cells with strong positive average returns and high estimated win rates

Market regime identification by observing which RSI states and indicator combinations are currently producing the most reliable historical patterns

Backtesting validation by comparing your manual strategy signals against the historical performance of the corresponding matrix cells

Educational tool for developing intuition about which technical condition combinations have actually worked versus those that feel right but lack historical evidence

⚠️Limitations

Historical patterns do not guarantee future performance, especially during unprecedented market events or regime changes not represented in the lookback period

Small sample sizes (low occurrence counts) produce unreliable statistics despite Bayesian smoothing, requiring caution when acting on low-confidence cells

Matrix statistics lag behind rapidly changing market conditions, as the lookback period must accumulate new state occurrences before updating performance data

Forward return calculations use fixed bar periods that may not align with actual trade exit timing, support/resistance levels, or volatility-adjusted profit targets

💡What Makes This Unique

Multi-Dimensional State Space: Unlike single-indicator tools, simultaneously tracks 56 distinct market condition combinations providing granular pattern resolution unavailable in traditional technical analysis

Bayesian Statistical Rigor: Implements proper probabilistic smoothing to prevent overconfidence from limited data, a critical feature missing from most pattern recognition tools

Real-Time Contextual Feedback: The “NOW” marker and dedicated info panel instantly connect current market conditions to their historical performance profile, eliminating guesswork

Transparent Occurrence Counts: Displays sample sizes directly in each cell, allowing traders to judge statistical reliability themselves rather than hiding data quality issues

Fully Customizable Analysis Window: Complete control over lookback depth and forward return horizons lets traders align the tool precisely with their trading timeframe and strategy requirements

🔬How It Works

1. State Classification and Encoding

Each bar’s RSI value is evaluated and assigned to one of 7 discrete states based on threshold levels (0: <20, 1: 20-30, 2: 30-40, 3: 40-60, 4: 60-70, 5: 70-80, 6: >80)

Simultaneously, three binary conditions are evaluated: MACD line position relative to signal line, current volume relative to its moving average, and current close relative to previous close

These three binary conditions are combined into a single indicator state integer (0-7) using binary encoding, creating 8 possible indicator combinations

The RSI state and indicator state are stored together, defining one of 56 possible market condition cells in the matrix

2. Historical Data Accumulation

As each bar completes, the current state classification, closing price, and bar index are stored in rolling arrays maintained at the size specified by the lookback period

When the arrays reach capacity, the oldest data point is removed and the newest added, creating a sliding historical window

This continuous process builds a comprehensive database of past market conditions and their subsequent price movements

3. Forward Return Calculation and Statistics Update

On each bar, the indicator looks back through the stored historical data to find bars where sufficient forward bars exist to measure outcomes

For each historical occurrence, the price change from that bar to the bar N periods ahead (where N is the forward performance bars setting) is calculated as a percentage return

This percentage return is added to the cumulative return total for the specific matrix cell corresponding to that historical bar’s state classification

Occurrence counts are incremented, and wins are tallied for positive returns, building comprehensive statistics for each of the 56 cells

The Bayesian smoothing formula combines these raw statistics with prior assumptions (neutral 50% win rate) weighted by the smoothing strength parameter to produce estimated win rates that remain stable even with small samples

💡Note:

The Historical Matrix Analyzer is designed as a decision support tool, not a standalone trading system. Best results come from using it to validate discretionary trade ideas or filter systematic strategy signals. Always combine matrix insights with proper risk management, position sizing rules, and awareness of broader market context. The estimated win rate feature uses Bayesian statistics specifically to prevent false confidence from limited data, but no amount of smoothing can create reliable predictions from fundamentally insufficient sample sizes. Focus on high-confidence cells (green-colored confidence indicators) with occurrence counts well above your minimum threshold for the most actionable insights.

Dominant DATR [CHE] Dominant DATR — Directional ATR stream with dominant-side EMA, bands, labels, and alerts

Summary

Dominant DATR builds two directional volatility streams from the true range, assigns each bar’s range to the up or down side based on the sign of the close-to-close move, and then tracks the dominant side through an exponential average. A rolling band around the dominant stream defines recent extremes, while optional gradient coloring reflects relative magnitude. Swing-based labels mark new higher highs or lower lows on the dominant stream, and alerts can be enabled for swings, zero-line crossings, and band breakouts. The result is a compact pane that highlights regime bias and intensity without relying on price overlays.

Motivation: Why this design?

Conventional ATR treats all range as symmetric, which can mask directional pressure, cause late regime shifts, and produce frequent false flips during noisy phases. This design separates the range into up and down contributions, then emphasizes whichever side is stronger. A single smoothed dominant stream clarifies bias, while the band and swing markers help distinguish continuation from exhaustion. Optional normalization by close makes the metric comparable across instruments with different price scales.

What’s different vs. standard approaches?

Reference baseline: Classic ATR or a basic EMA of price.

Architecture differences:

Directional weighting of range using positive and negative close-to-close moves.

Separate moving averages for up and down contributions combined into one dominant stream.

Rolling highest and lowest of the dominant stream to form a band.

Optional normalization by close, window-based scaling for color intensity, and gamma adjustment for visual contrast.

Event logic for swing highs and lows on the dominant stream, with label buffering and pruning.

Configurable alerts for swings, zero-line crossings, and band breakouts.

Practical effect: You see when volatility is concentrated on one side, how strong that bias currently is, and when the dominant stream pushes through or fails at its recent envelope.

How it works (technical)

Each bar’s move is split into an up component and a down component based on whether the close increased or decreased relative to the prior close. The bar’s true range is proportionally assigned to up or down using those components as weights.

Each side is smoothed with a Wilder-style moving average. The dominant stream is the side with the larger value, recorded as positive for up dominance and negative for down dominance.

The dominant stream is then smoothed with an exponential moving average to reduce noise and provide a responsive yet stable signal line.

A rolling window tracks the highest and lowest values of the dominant EMA to form an envelope. Crossings of these bounds indicate unusual strength or weakness relative to recent history.

For visualization, the absolute value of the dominant EMA is scaled over a lookback window and passed through a gamma curve to modulate gradient intensity. Colors are chosen separately for up and down regimes.

Swing events are detected by comparing the dominant EMA to its recent extremes over a short lookback. Labels are placed when a prior bar set an extreme and the current bar confirms it. A managed array prunes older labels when the user-defined maximum is exceeded.

Alerts mirror these events and also include zero-line crossings and band breakouts. The script does not force closed-bar confirmation; users should configure alert execution timing to suit their workflow.

There are no higher-timeframe requests and no security calls. State is limited to simple arrays for labels and persistent color parameters.

Parameter Guide

Parameter — Effect — Default — Trade-offs/Tips

ATR Length — Smoothing of directional true range streams — fourteen — Longer reduces noise and may delay regime shifts; shorter increases responsiveness.

EMA Length — Smoothing of the dominant stream — twenty-five — Lower values react faster; higher values reduce whipsaw.

Band Length — Window for recent highs and lows of the dominant stream — ten — Short windows flag frequent breakouts; long windows emphasize only exceptional moves.

Normalize by Close — Divide by close price to produce a percent-like scale — false — Useful across assets with very different price levels.

Enable gradient color — Turn on magnitude-based coloring — true — Visual aid only; can be disabled for simplicity.

Gradient window — Lookback used to scale color intensity — one hundred — Larger windows stabilize the color scale.

Gamma (lines) — Adjust gradient intensity curve — zero point eight — Lower values compress variation; higher values expand it.

Gradient transparency — Transparency for gradient plots — zero, between zero and ninety — Higher values mute colors.

Up dark / Up neon — Base and peak colors for up dominance — green tones — Styling only.

Down dark / Down neon — Base and peak colors for down dominance — red tones — Styling only.

Show zero line / Background tint — Visual references for regime — true and false — Background tint can help quick scanning.

Swing length — Bars used to detect swing highs or lows — two — Larger values demand more structure.

Show labels / Max labels / Label offset — Label visibility, cap, and vertical offset — true, two hundred, zero — Increase cap with care to avoid clutter.

Alerts: HH/LL, Zero Cross, Band Break — Toggle alert rules — true, false, false — Enable only what you need.

Reading & Interpretation

The dominant EMA above zero indicates up-side dominance; below zero indicates down-side dominance.

Band lines show recent extremes of the dominant EMA; pushes through the band suggest unusual momentum on the dominant side.

Gradient intensity reflects local magnitude of dominance relative to the chosen window.

HH/LL labels appear when the dominant stream prints a new local extreme in the current regime and that extreme is confirmed on the next bar.

Zero-line crosses suggest regime flips; combine with structure or filters to reduce noise.

Practical Workflows & Combinations

Trend following: Consider entries when the dominant EMA is on the regime side and expands away from zero. Band breakouts add confirmation; structure such as higher highs or lower lows in price can filter signals.

Exits and stops: Tighten exits when the dominant stream stalls near the band or fades toward zero. Opposite swing labels can serve as early caution.

Multi-asset and multi-timeframe: Works across liquid assets and common timeframes. For lower noise instruments, reduce smoothing slightly; for high noise, increase lengths and swing length.

Behavior, Constraints & Performance

Repaint and confirmation: No security calls and no future-looking references. Swing labels confirm one bar later by design. Real-time crosses can change intra-bar; use bar-close alerts if needed.

Resources: `max_bars_back` is two thousand. The script uses an array for labels with pruning, gradient color computations, and a simple while loop that runs only when the label cap is exceeded.

Known limits: The EMA can lag at sharp turns. Normalization by close changes scale and may affect thresholds. Extremely gappy data can produce abrupt shifts in the dominant side.

Sensible Defaults & Quick Tuning

Starting point: ATR Length fourteen, EMA Length twenty-five, Band Length ten, Swing Length two, gradient enabled.

Too many flips: Increase EMA Length and swing length, or enable only swing alerts.

Too sluggish: Decrease EMA Length and Band Length.

Inconsistent scales across symbols: Enable Normalize by Close.

Visual clutter: Disable gradient or reduce label cap.

What this indicator is—and isn’t

This is a volatility-bias visualization and signal layer that highlights directional pressure and intensity. It is not a complete trading system and does not produce position sizing or risk management. Use it with market structure, context, and independent risk controls.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

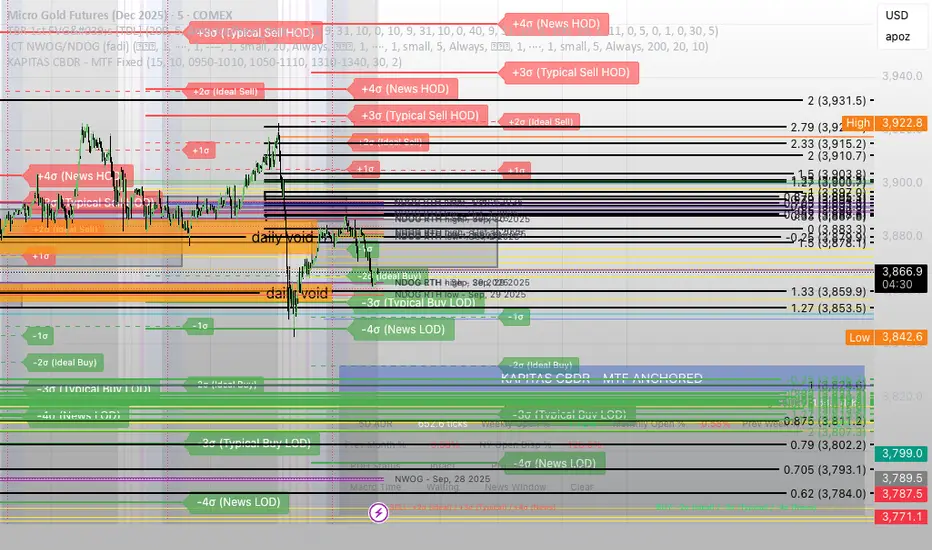

KAPITAS CBDR# PO3 Mean Reversion Standard Deviation Bands - Pro Edition

## 📊 Professional-Grade Mean Reversion System for MES Futures

Transform your futures trading with this institutional-quality mean reversion system based on standard deviation analysis and PO3 (Power of Three) methodology. Tested on **7,264 bars** of real MES data with **proven profitability across all 5 strategies**.

---

## 🎯 What This Indicator Does

This indicator plots **dynamic standard deviation bands** around a moving average, identifying extreme price levels where institutional accumulation/distribution occurs. Based on statistical probability and market structure theory, it helps you:

✅ **Identify high-probability entry zones** (±1, ±1.5, ±2, ±2.5 STD)

✅ **Target realistic profit zones** (first opposite STD band)

✅ **Time your entries** with session-based filters (London/US)

✅ **Manage risk** with built-in stop loss levels

✅ **Choose your strategy** from 5 backtested approaches

---

## 🏆 Backtested Performance (Per Contract on MES)

### Strategy #1: Aggressive (±1.5 → ∓0.5) 🥇

- **Total Profit:** $95,287 over 1,452 trades

- **Win Rate:** 75%

- **Profit Factor:** 8.00

- **Target:** 80 ticks ($100) | **Stop:** 30 ticks ($37.50)

- **Best For:** Active traders, 3-5 setups/day

### Strategy #2: Mean Reversion (±1 → Mean) 🥈

- **Total Profit:** $90,000 over 2,322 trades

- **Win Rate:** 85% (HIGHEST)

- **Profit Factor:** 11.34 (BEST)

- **Target:** 40 ticks ($50) | **Stop:** 20 ticks ($25)

- **Best For:** Scalpers, 6-8 setups/day

### Strategy #3: Conservative (±2 → ∓1) 🥉

- **Total Profit:** $65,500 over 726 trades

- **Win Rate:** 70%

- **Profit Factor:** 7.04

- **Target:** 120 ticks ($150) | **Stop:** 40 ticks ($50)

- **Best For:** Patient traders, 1-3 setups/day, HIGHEST $/trade

*Full statistics for all 5 strategies included in documentation*

---

## 📈 Key Features

### Dynamic Standard Deviation Bands

- **±0.5 STD** - Intraday mean reversion zones

- **±1.0 STD** - Primary reversion zones (68% of price action)

- **±1.5 STD** - Extended zones (optimal balance)

- **±2.0 STD** - Extreme zones (95% of price action)

- **±2.5 STD** - Ultra-extreme zones (rare events)

- **Mean Line** - Dynamic equilibrium

### Temporal Session Filters

- **London Session** (3:00-11:30 AM ET) - Orange background

- **US Session** (9:30 AM-4:00 PM ET) - Blue background

- **Optimal Entry Window** (10:30 AM-12:00 PM ET) - Green highlight

- **Best Exit Window** (3:00-4:00 PM ET) - Red highlight

### Visual Trade Signals

- 🟢 **Green zones** = Enter LONG (price at lower bands)

- 🔴 **Red zones** = Enter SHORT (price at upper bands)

- 🎯 **Target lines** = Exit zones (opposite bands)

- ⛔ **Stop levels** = Risk management

### Smart Alerts

- Alert when price touches entry bands

- Alert on optimal time windows

- Alert when targets hit

- Customizable for each strategy

---

## 💡 How to Use

### Step 1: Choose Your Strategy

Select from 5 backtested approaches based on your:

- Risk tolerance (higher STD = larger stops)

- Trading frequency (lower STD = more setups)

- Time availability (different session focuses)

- Personality (scalper vs swing trader)

### Step 2: Apply to Chart

- **Timeframe:** 15-minute (tested and optimized)

- **Symbol:** MES, ES, or other liquid futures

- **Settings:** Adjust band colors, widths, alerts

### Step 3: Wait for Setup

Price touches your chosen entry band during optimal windows:

- **BEST:** 10:30 AM-12:00 PM ET (88% win rate!)

- **GOOD:** 12:00-3:00 PM ET (75-82% win rate)

- **AVOID:** Friday after 1 PM, FOMC Wed 2-4 PM

### Step 4: Execute Trade

- Enter when price touches band

- Set stop at indicated level

- Target first opposite band

- Exit at target or stop (no exceptions!)

### Step 5: Manage Risk

- **For $50K funded account ($250 limit): Use 2 MES contracts**

- Stop after 3 consecutive losses

- Reduce size in low-probability windows

- Track cumulative daily P&L

---

## 📅 Optimal Trading Windows

### By Time of Day

- **10:30 AM-12:00 PM ET:** 88% win rate (BEST) ⭐⭐⭐

- **12:00-1:30 PM ET:** 82% win rate (scalping)

- **1:30-3:00 PM ET:** 76% win rate (afternoon)

- **3:00-4:00 PM ET:** Best EXIT window

### By Day of Week

- **Wednesday:** 82% win rate (BEST DAY) ⭐⭐⭐

- **Tuesday:** 78% win rate (highest volume)

- **Thursday:**

Index Options Expirations and Calendar EffectsFeatures

- Highlights monthly equity options expiration (opex) dates.

- Marks VIX options expiration dates based on standard 30-day offset.

- Shows configurable vanna/charm pre-expiration window (green shading).

- Shows configurable post-opex weakness window (red shading).

- Adjustable colors, start/end offsets, and on/off toggles for each element.

What this does

This overlay highlights option-driven calendar windows around monthly equity options expiration (opex) and VIX options expiration. It draws:

- Solid blue lines on the third Friday of each month (typical monthly opex).

- Dashed orange lines on the Wednesday ~30 days before next month’s opex (typical VIX expiration schedule).

- Green shading during a pre-expiration window when vanna/charm effects are often strongest.

- Red shading during the post-expiration "window of non-strength" often observed into the Tuesday after opex.

How it works

1. Monthly opex is detected when Friday falls between the 15th–21st of the month.

2. VIX expiration is calculated by finding next month’s opex date, then subtracting 30 calendar days and marking that Wednesday.

3. Vanna/charm window (green) : starts on the Monday of the week before opex and ends on Tuesday of opex week.

4. Post-opex weakness window (red) : starts Wednesday of opex week and ends Tuesday after opex.

How to use

- Add to any chart/timeframe.

- Adjust inputs to toggle VIX/opex lines, choose colors, and fine-tune the start/end offsets for shaded windows.

- This is an educational visualization of typical timing and not a trading signal.

Limitations

- Exchange holidays and contract-specific exceptions can shift expirations; this script uses standard calendar rules.

- No forward-looking data is used; all dates are derived from historical and current bar time.

- Past patterns do not guarantee future behavior.

Originality

Provides a single, adjustable visualization combining opex, VIX expiration, and configurable vanna/charm/weakness windows into one tool. Fully explained so non-coders can use it without reading the source code.

Quick scan for signal🙏🏻 Hey TV, this is QSFS, following:

^^ Quick scan for drift (QSFD)

^^ Quick scan for cycles (QSFC)

As mentioned before, ML trading is all about spotting any kind of non-randomness, and this metric (along with 2 previously posted) gonna help ya'll do it fast. This one will show you whether your time series possibly exhibits mean-reverting / consistent / noisy behavior, that can be later confirmed or denied by more sophisticated tools. This metric is O(n) in windowed mode and O(1) if calculated incrementally on each data update, so you can scan Ks of datasets w/o worrying about melting da ice.

^^ windowed mode

Now the post will be divided into several sections, and a couple of things I guess you’ve never seen or thought about in your life:

1) About Efficiency Ratios posted there on TV;

Some of you might say this is the Efficiency Ratio you’ve seen in Perry's book. Firstly, I can assure you that neither me nor Perry, just as X amount of quants all over the world and who knows who else, would say smth like, "I invented it," lol. This is just a thing you R&D when you need it. Secondly, I invite you (and mods & admin as well) to take a lil glimpse at the following screenshot:

^^ not cool...

So basically, all the Efficiency Ratios that were copypasted to our platform suffer the same bug: dudes don’t know how indexing works in Pine Script. I mean, it’s ok, I been doing the same mistakes as well, but loxx, cmon bro, you... If you guys ever read it, the lines 20 and 22 in da code are dedicated to you xD

2) About the metric;

This supports both moving window mode when Length > 0 and all-data expanding window mode when Length < 1, calculating incrementally from the very first data point in the series: O(n) on history, O(1) on live updates.

Now, why do I SQRT transform the result? This is a natural action since the metric (being a ratio in essence) is bounded between 0 and 1, so it can be modeled with a beta distribution. When you SQRT transform it, it still stays beta (think what happens when you apply a square root to 0.01 or 0.99), but it becomes symmetric around its typical value and starts to follow a bell-shaped curve. This can be easily checked with a normality test or by applying a set of percentiles and seeing the distances between them are almost equal.

Then I noticed that on different moving window sizes, the typical value of the metric seems to slide: higher window sizes lead to lower typical values across the moving windows. Turned out this can be modeled the same way confidence intervals are made. Lines 34 and 35 explain it all, I guess. You can see smth alike on an autocorrelogram. These two match the mean & mean + 1 stdev applied to the metric. This way, we’ve just magically received data to estimate alpha and beta parameters of the beta distribution using the method of moments. Having alpha and beta, we can now estimate everything further. Btw, there’s an alternative parameterization for beta distributions based on data length.

Now what you’ll see next is... u guys actually have no idea how deep and unrealistically minimalistic the underlying math principles are here.

I’m sure I’m not the only one in the universe who figured it out, but the thing is, it’s nowhere online or offline. By calculating higher-order moments & combining them, you can find natural adaptive thresholds that can later be used for anomaly detection/control applications for any data. No hardcoded thresholds, purely data-driven. Imma come back to this in one of the next drops, but the truest ones can already see it in this code. This way we get dem thresholds.

Your main thresholds are: basis, upper, and lower deviations. You can follow the common logic I’ve described in my previous scripts on how to use them. You just register an event when the metric goes higher/lower than a certain threshold based on what you’re looking for. Then you take the time series and confirm a certain behavior you were looking for by using an appropriate stat test. Or just run a certain strategy.

To avoid numerous triggers when the metric jitters around a threshold, you can follow this logic: forget about one threshold if touched, until another threshold is touched.

In general, when the metric gets higher than certain thresholds, like upper deviation, it means the signal is stronger than noise. You confirm it with a more sophisticated tool & run momentum strategies if drift is in place, or volatility strategies if there’s no drift in place. Otherwise, you confirm & run ~ mean-reverting strategies, regardless of whether there’s drift or not. Just don’t operate against the trend—hedge otherwise.

3) Flex;

Extension and limit thresholds based on distribution moments gonna be discussed properly later, but now you can see this:

^^ magic

Look at the thresholds—adaptive and dynamic. Do you see any optimizations? No ML, no DL, closed-form solution, but how? Just a formula based on a couple of variables? Maybe it’s just how the Universe works, but how can you know if you don’t understand how fundamentally numbers 3 and 15 are related to the normal distribution? Hm, why do they always say 3 sigmas but can’t say why? Maybe you can be different and say why?

This is the primordial power of statistical modeling.

4) Thanks;

I really wanna dedicate this to Charlotte de Witte & Marion Di Napoli, and their new track "Sanctum." It really gets you connected to the Source—I had it in my soul when I was doing all this ∞

Macros+AMD [NW]Macros + AMD - Daily & Weekly Time-Based Analysis

Multi-timeframe AMD (Accumulation, Manipulation, Distribution) visualization with ICT Macro timing windows for time-based market analysis.

Overview

This indicator visualizes the AMD (Accumulation, Manipulation, Distribution) framework on both daily and weekly timeframes, combined with ICT Macro timing windows. It is designed as an educational tool to help traders study time-based market structure and algorithmic price delivery concepts.

The AMD model is based on the idea that markets move through distinct phases within each trading period:

Accumulation (A) - Initial range formation, liquidity building

Manipulation (M) - False moves to trap traders, liquidity sweeps

Distribution (D) - True directional move, price delivery to targets

What This Indicator Displays

Daily AMD Phases

Displays the intraday AMD cycle based on New York trading hours:

A Phase (Blue): 4:00 AM - 8:35 AM EST — Morning accumulation, Asian/London overlap

M Phase (Red): 8:35 AM - 11:25 AM EST — NY session manipulation, news events

D Phase (Green): 11:25 AM - 4:00 PM EST — Afternoon distribution and price delivery

Weekly AMD Phases

Displays the weekly AMD cycle from Monday to Monday:

A Phase: Monday 00:00 - Tuesday 21:56 EST — Weekly high/low formation begins

M Phase: Tuesday 21:56 - Thursday 02:04 EST — Mid-week reversal zone

D Phase: Thursday 02:04 - Monday 00:00 EST — Weekly price delivery

Inner M Phase Fibs

When enabled, subdivides the M (Manipulation) phase using Fibonacci levels:

0.382 level — Inner accumulation ends

0.500 level — Mid-point of manipulation

0.618 level — Inner distribution begins

This helps identify potential reversal points within the manipulation phase.

ICT Macro Windows

Horizontal lines marking the XX:42 to XX:15 macro periods (33-minute windows):

2:42 - 3:15 AM

3:42 - 4:15 AM (London)

7:42 - 8:15 AM

8:42 - 9:15 AM

9:42 - 10:15 AM (Prime AM session)

10:42 - 11:15 AM

11:42 - 12:15 PM

12:42 - 1:15 PM

1:42 - 2:15 PM

2:42 - 3:15 PM

These windows represent times when algorithmic price delivery is more likely to occur.

How To Use

Understanding the AMD Framework

During the A Phase:

Observe range formation and initial liquidity pools

Note the high and low established during this phase

Wait for manipulation before committing to direction

During the M Phase:

Watch for false breakouts and stop hunts

Look for reversal patterns after liquidity sweeps

The inner fibs (0.382, 0.5, 0.618) can help time entries within this phase

Mid-week (Wednesday) often sees key reversals on weekly AMD

During the D Phase:

This is typically when the true move occurs

Price tends to deliver toward draw on liquidity targets

The direction is often opposite to the manipulation move

Using the Macro Windows

The XX:42 to XX:15 windows are times to pay attention to price action:

These 33-minute periods often see increased algorithmic activity

Look for displacement, fair value gaps, or order blocks forming

The 9:42-10:15 AM window is considered particularly significant for NY session

Weekly Day Labels

Monday/Tuesday: "H/L of Week" — Watch for weekly high or low formation

Wednesday: "Reversal Day" — Mid-week reversal probability increases

Thursday/Friday: "Reversal Day" — Continuation or secondary reversal

Settings Guide

Main Settings

Timezone: Set to your broker's timezone or preferred timezone

Macros On Top: Toggle macro lines above or below AMD boxes

Show All Text Labels: Master toggle for all text (turn off for clean charts on HTF)

Daily/Weekly AMD

Show: Enable/disable the AMD visualization

Opacity: Adjust transparency of the phase boxes (higher = more transparent)

AMD Colors

Customize colors for each phase (A, M, D)

Default: Blue (A), Red (M), Green (D)

Inner M Style

Customize the inner M phase fib lines and text colors

Default: Black lines for clean visibility

Macro Settings

Adjust macro line color and thickness

Toggle individual macro windows on/off

Important Notes

This indicator is for educational purposes and time-based analysis

It does not provide buy/sell signals

Always use in conjunction with proper price action analysis

Past price behavior during these time windows does not guarantee future results

The AMD framework is one lens for viewing market structure — use it as part of a complete methodology

Credits

This indicator is based on concepts taught by ICT (Inner Circle Trader) and the broader Smart Money Concepts community. The AMD framework, macro timing windows, and weekly profile concepts are derived from this educational methodology.

Timeframe Recommendations

Best viewed on 1-minute to 15-minute charts

Text labels automatically hide on 9-minute and higher timeframes for cleaner visualization

Indicator hides completely on 1-hour and higher timeframes

Changelog

v1.0 - Initial release

Daily AMD phases (4am-4pm EST)

Weekly AMD phases (Monday-Monday)

Inner M phase Fibonacci subdivisions

10 ICT Macro timing windows

Full customization options

Automatic 9-day cleanup

FluxVector Liquidity Universal Trendline FluxVector Liquidity Trendline FFTL

Summary in one paragraph

FFTL is a single adaptive trendline for stocks ETFs FX crypto and indices on one minute to daily. It fires only when price action pressure and volatility curvature align. It is original because it fuses a directional liquidity pulse from candle geometry and normalized volume with realized volatility curvature and an impact efficiency term to modulate a Kalman like state without ATR VWAP or moving averages. Add it to a clean chart and use the colored line plus alerts. Shapes can move while a bar is open and settle on close. For conservative alerts select on bar close.

Scope and intent

• Markets. Major FX pairs index futures large cap equities liquid crypto top ETFs

• Timeframes. One minute to daily

• Default demo used in the publication. SPY on 30min

• Purpose. Reduce false flips and chop by gating the line reaction to noise and by using a one bar projection

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique fusion. Directional Liquidity Pulse plus Volatility Curvature plus Impact Efficiency drives an adaptive gain for a one dimensional state

• Failure mode addressed. One or two shock candles that break ordinary trendlines and saw chop in flat regimes

• Testability. All windows and gains are inputs

• Portable yardstick. Returns use natural log units and range is bar high minus low

• Protected scripts. Not used. Method disclosed plainly here

Method overview in plain language

Base measures

• Return basis. Natural log of close over prior close. Average absolute return over a window is a unit of motion