Egg vs Tennis Ball — Drop/Rebound StrengthEgg vs Tennis Ball — Drop/Rebound Meter

What it does

Classifies selloffs as either:

Eggs — dead‑cat, no bounce

Tennis Balls — fast, decisive rebound

Core features

Detects swing drops from a Pivot High (PH) to a Pivot Low (PL)

Requires drops to be meaningful (volatility‑aware, ATR‑scaled)

Draws a bounce threshold line and a deadline

Decides outcome based on speed and extent of rebound

Tracks scores and win rates across multiple lookback windows

Includes a color‑coded meter and current streak display

Visuals at a glance

Gray diagonal — drop from PH to PL

Teal dotted horizontal — bounce threshold, from PH to the deadline

Solid green — Tennis Ball (bounce line broken before the deadline)

Solid red — Egg (deadline expired before the bounce)

Optional PH / PL labels for clarity

How the decision is made

1) Find pivots — symmetric pivots using Pivot Left / Right; PL confirms after Right bars.

2) Qualify the drop — Drop Size = PH − PL; must be ≥ (Drop Threshold × ATR at PL).

3) Define the bounce line — PL + (Bounce Multiple × Drop Size). 1.00× = full retrace to PH; up to 2.00× for overshoot.

4) Set the deadline — Drop Bars = PL index − PH index; Deadline = Drop Bars × Recovery Factor; timer starts from PH or PL.

5) Resolve — Tennis Ball if price hits the bounce line before the deadline; Egg if the deadline passes first.

Scoring system (−100 to +100)

+100 = perfect Tennis Ball (fastest possible + full overshoot)

−100 = perfect Egg (no recovery)

In between: scored by rebound speed and extent, shaped by your weight settings

Meter Table

Columns (toggle on/off)

All (off by default)

Last N1 (default 5)

Last N2 (default 10)

Last N3 (default 20)

Rows

Tennis / Eggs — counts

% Tennis — win rate

Avg Score — normalized quality from −100 to +100

Streak — overall (not windowed), e.g., +3 = 3 Tennis Balls in a row, −4 = 4 Eggs in a row

Alerts

Tennis Ball – Fast Rebound — triggers when the bounce line is broken in time

Egg – Window Expired — triggers when the deadline passes without a bounce

Inputs

① Drop Detection

Pivot Left / Right

ATR Length

Drop Threshold × ATR

② Bounce Requirement

Bounce Multiple × Drop Size (0.10–2.00×)

③ Timing

Timer Start — PH or PL

Recovery Factor × Drop Bars

Break Trigger — Close or High

④ Display

Show Pivot/Outcome Labels

Line Width

Table Position (corner)

⑤ Meter Columns

Show All (off by default)

Show N1 / N2 / N3 (5, 10, 20 by default)

⑥ Scoring Weights

Tennis — Base, Speed, Extent

Egg — Base, Strength

How to use it

Pick strictness — start with Drop Threshold = 2.0 ATR, Bounce Multiple = 1.0×, Recovery Factor = 3.0×; adjust to timeframe and volatility.

Watch the dotted line — it ends at the deadline; turns solid green (Tennis) if broken in time, solid red (Egg) if it expires.

Read the meter — short windows (5–10) show current behavior; Avg Score captures quality; Streak shows momentum.

Blend with your system — combine with trend filters, volume, or regime detection.

Tips

Close vs High trigger: Close is stricter; High is more responsive.

PH vs PL timer start: PH measures round‑trip; PL measures recovery only.

Increase pivot strength for fewer, more reliable signals.

Higher timeframes generally produce cleaner patterns.

Defaults

Pivot L/R: 5 / 5

ATR Length: 14

Drop Threshold: 2.0× ATR

Bounce Multiple: 1.00×

Recovery Factor: 3.0×

Break Trigger: Close

Windows: Last 5, 10, 20 (All off)

Interpreting results

Tennis‑y: Avg Score +30 to +70, %Tennis > 55%

Mixed: Avg Score near 0

Egg‑y: Avg Score −30 to −80, %Tennis < 45%

Cerca negli script per "如何用wind搜索股票的发行价和份数"

Kinetic EMA & Volume with State EngineKinetic EMA & Volume with State Engine (EMVOL)

1. Introduction & Concept

The EMVOL indicator converts a dense family of EMA signals and volume flows into a compact “state engine”. Instead of looking at individual EMA lines or simple crossovers, the script treats each EMA as part of a kinetic vector field and classifies the market into interpretable states:

- Trend direction and strength (from a grid of prime‑period EMAs).

- Volume regime (expansion, contraction, climax, dry‑up).

- Order‑flow bias via delta (buy versus sell volume).

- A combined scenario label that summarises how these three layers interact.

The goal is educational: to help traders see that moving averages and volume become more meaningful when observed as a structure, not as isolated lines. EMVOL is therefore designed as a real‑time teaching tool, not as an automatic signal generator.

2. Volume Settings

Group: “Volume Settings”

A. Calculation Method

- Geometry (Source File) – Default mode.

Buy and sell volume are estimated from each candle’s geometry: the close is compared to the high/low range and the bar’s total volume is split proportionally between buyers and sellers. This approximation works on any TradingView plan and does not require lower‑timeframe data.

- Intrabar (Precise) – Reconstructs buy/sell volume using a lower timeframe via requestUpAndDownVolume(). The script asks TradingView for historical intrabar data (e.g., 15‑second bars) and builds buy/sell volume and delta from that stream. This mode can produce a more accurate view of order flow, but coverage is limited by your account’s history limits and the symbol’s available lower‑timeframe data.

B. Intrabar Resolution (If Precise)

- Intrabar Resolution (If Precise) – Selected only when the calculation method is “Intrabar (Precise)”. It defines which lower timeframe (for example 15S, 30S, 1m) is used to compute up/down volume. Smaller intrabar timeframes may give smoother and more granular deltas, but require more historical depth from the platform.

When “Intrabar (Precise)” is active, the dashboard’s extended section shows the resolution and the number of bars for which precise volume has been successfully retrieved, in the format:

- Mode: Intrabar (15S) – where N is the count of bars with valid high‑resolution volume data.

In Geometry mode this counter simply reflects the processed bars in the current session.

3. Kinetic Vector Settings

Group: “Kinetic Vector”

A. Vector Window

- Vector Window – Controls the temporal smoothing applied to the aggregated vectors (trend, volume, delta, etc.). Internally, each bar’s vector value is averaged with a simple moving window of this length.

- Shorter windows make the state engine more reactive and sensitive to local swings.

- Longer windows make the states more stable and better suited to higher‑timeframe structure.

B. Max Prime Period

- Max Prime Period – Sets the largest prime number used in the EMA grid. The engine builds a family of EMAs on prime lengths (2, 3, 5, 7, …) up to this limit and converts their slopes into angles.

- A higher limit increases the number of long‑horizon EMAs in the grid and makes the vectors sensitive to broader structure.

- A lower limit focuses the analysis on short- and medium‑term behaviour.

C. Price Source

- Price Source – The price series from which the kinetic EMA grid is built (e.g., Close, HLC3, OHLC4). Changing the source modifies the context that the state engine is reading but does not change the core logic.

4. State Engine Settings

Group: “State Engine Settings”

These inputs define how the continuous vectors are translated into discrete states.

A. Trend Thresholds

- Strong Trend Threshold – Value above which the trend vector is treated as “extreme bullish” and below which it is “extreme bearish”.

- Weak Trend Threshold – Inner boundary between neutral and directional conditions.

Roughly:

- |trend| < weak → Neutral trend state.

- weak < |trend| ≤ strong → Bullish/Bearish.

- |trend| > strong → Extreme Bullish/Extreme Bearish.

B. Volume Thresholds

- Volume Climax Threshold – Upper bound at which volume is considered “climax” (unusually expanded participation).

- Volume Expansion Threshold – Boundary for normal expansion versus contraction.

Conceptually:

- Volume above “expansion” indicates increasing activity.

- Volume near or above “climax” marks extreme participation.

- Negative values below the symmetric thresholds map to contraction and extreme dry‑up (liquidity vacuum) states.

C. Delta Thresholds

- Strong Delta Threshold – Cut‑off for extreme buying or selling dominance in delta.

- Weak Delta Threshold – Threshold for mild buy/sell bias versus neutral order flow.

Combined with the sign of the delta vector, these thresholds classify order flow as:

- Extreme Buy, Buy‑Dominant, Neutral, Sell‑Dominant, Extreme Sell.

D. State Hysteresis Bars

- State Hysteresis Bars – Minimum number of bars for which a new state must persist before the engine commits to the change. This prevents the dashboard from flickering during fast spikes and emphasises persistent market behaviour.

- Smaller values switch states quickly; larger values demand more confirmation.

5. Visual Interface

Group: “Visual Interface”

A. Ribbon Base Color

- Ribbon Base Color – Base hue for the multi‑layer EMA ribbon drawn around price. The script plots a dense grid of hidden EMAs and fills the gaps between them to form a semi‑transparent band. Narrow, overlapping bands hint at compression; wider separation hints at dispersion across EMA horizons.

B. Show Dashboard

- Show Dashboard – Toggles the on‑chart table which summarises the current state engine output. Disable this if you only want to keep the EMA ribbon and volume‑based structure on the price chart.

C. Color Theme

- Color Theme – Switch between a dark and light style for the dashboard background and text colours so that the table matches your chart theme.

D. Table Position

- Table Position – Places the dashboard at any corner or edge of the chart (Top / Middle / Bottom × Left / Centre / Right).

E. Table Size

- Table Size – Changes the dashboard’s text size (Tiny, Small, Normal, Large). Use a larger size on high‑resolution screens or when streaming.

F. Show Extended Info

- Show Extended Info – Adds diagnostic rows under the main state summary:

- Mode / Primes / Vector – Shows the current calculation mode (Geometry / Intrabar), the selected intrabar resolution and coverage in bars ( ), how many prime periods are active, and the vector window.

- Values – Displays the current aggregated vectors:

- P: price vector

- V: volume vector

- B: buy‑volume vector

- S: sell‑volume vector

- D: delta vector

Values are bounded between ‑1 and +1.

- Volume Stats – Prints the last bar’s raw buy volume, sell volume and delta as formatted numbers.

- Footer – A final row with the symbol and current time: #SYMBOL | HH:MM.

These extended rows are meant for inspecting how the engine is behaving under the hood while you scroll the chart and compare different assets or timeframes.

6. Language Settings

Group: “Language Settings”

- Select Language – Switches the entire dashboard between English and Turkish.

The underlying calculations and scenario logic are identical; only the labels, titles and comments in the table are translated.

7. Dashboard Structure & Reading Guide

The table summarises the current situation in a few rows:

1. System Header – Shows the script name and the active calculation method (“Geometry” or “Intrabar”).

2. Scenario Title – High‑level description of the current combined scenario (e.g., “Trending Buy Confirmed”, “Sideways Balanced”, “Bull Trap”, “Blow‑Off Top”). The background colour is derived from the scenario family (trending, compression, exhaustion, anomaly, etc.).

3. Bias / Trend Line – States the dominant trend bias derived from the trend vector (Extreme Bullish, Bullish, Neutral, Bearish, Extreme Bearish).

4. Signal / Consideration Line – A short sentence giving qualitative guidance about the current state (for example: continuation risk, exhaustion risk, trap‑like behaviour, or compression). This is deliberately phrased as a consideration, not as a direct trading signal.

5. Trend / Volume / Delta Rows – Three separate rows explain, in plain language, how the trend, volume regime and delta are classified at this bar.

6. Extended Info (optional) – Mode / primes / vector settings, current vector values, and last‑bar volume statistics, as described above.

Together, these rows are meant to be read as a narrative of what price, volume and order‑flow are doing, not as mechanical instructions.

8. State Taxonomy

The state engine organizes market behaviour in three stages.

8.1 Trend States (from the Price Vector)

- Extreme Bullish Trend – The prime‑grid price vector is strongly upward; most EMAs are aligned to the upside.

- Bullish Trend – Upward bias is present, but less extreme.

- Neutral Trend – EMAs are mixed or flat; price is effectively sideways relative to the grid.

- Bearish Trend – Downward bias, with the EMA grid sloping down.

- Extreme Bearish Trend – Strong downside alignment across the grid.

8.2 Volume Regime States (from the Volume Vector)

- Volume Climax (Buy‑Side) – Strong positive volume vector; participation is unusually high in the current direction.

- Volume Expansion – Activity above normal but below the climax threshold.

- Neutral Volume – No major expansion or contraction versus recent history.

- Volume Contraction – Activity is drying up compared with the past.

- Extreme Dry‑Up / Liquidity Vacuum – Very low participation; the market is thin and prone to slippage.

8.3 Delta Behaviour States (from the Delta Vector)

- Extreme Buy Delta – Buying pressure dominates strongly.

- Buy‑Dominant Delta – Buy volume exceeds sell volume, but not at an extreme.

- Neutral Delta – Buy and sell flows are roughly balanced.

- Sell‑Dominant Delta – Selling pressure dominates.

- Extreme Sell Delta – Aggressive, one‑sided selling.

8.4 Combined Scenario State s

EMVOL uses the three base states above to generate a single scenario label. These scenarios are designed to be read as context, not as entry or exit signals.

Trending Scenarios

1. Trending Buy Confirmed

- Bullish or extreme bullish trend, supported by expanding or climax volume and buy‑side delta.

- Educational idea: a healthy uptrend where both participation and order flow agree with the direction.

2. Trending Buy – Weak Volume

- Bullish trend, but volume is neutral, contracting or in dry‑up while delta is still buy‑side.

- Educational idea: price is advancing, yet participation is thinning; trend continuation becomes more fragile.

3. Trending Sell Confirmed

- Bearish or extreme bearish trend, with expanding or climax volume and sell‑side delta.

- Educational idea: strong downtrend with both volume and order‑flow confirmation.

4. Trending Sell – Weak Volume

- Bearish trend, but volume is neutral, contracting or very low while delta remains sell‑side.

- Educational idea: downside continues but with limited participation; vulnerable to short‑covering.

Sideways / Range Scenarios

5. Sideways Balanced

- Neutral trend, neutral delta, neutral volume.

- Classic range environment; low directional edge, suitable for observation and context rather than trend trading.

6. Sideways with Buy Pressure

- Neutral trend, but buy‑side delta is dominant or extreme.

- Range with latent accumulation: price may still appear sideways, but buyers are quietly more active.

7. Sideways with Sell Pressure

- Neutral trend with dominant or extreme sell‑side delta.

- Distribution‑like environment where price chops while sellers are gradually more aggressive.

Exhaustion & Volume Extremes

8. Exhaustion – Buy Risk

- Extreme bullish trend, volume climax and strong buy‑side delta.

- Educational idea: very strong up‑move where both participation and delta are already stretched; risk of exhaustion or blow‑off.

9. Exhaustion – Sell Risk

- Extreme bearish trend, volume dry‑up and strong sell‑side delta.

- Suggests one‑sided selling into increasingly thin liquidity.

10. Volume Climax (Buy)

- Neutral trend, neutral delta, but volume at climax levels.

- Often associated with a “big event” bar where participation spikes without a clear directional commitment.

11. Volume Climax (Sell / Dry‑Up)

- Neutral trend and neutral delta, while the volume vector indicates an extreme dry‑up.

- Highlights a stand‑still episode: very limited interest from both sides, increasing the sensitivity to future impulses.

Divergences

12. Divergence – Bullish Context

- Bullish or extreme bullish trend, but delta has faded back to neutral.

- Price trend continues while order‑flow conviction softens; can precede pauses or complex corrections.

13. Divergence – Bearish Context

- Bearish or extreme bearish trend with a neutral delta.

- Downtrend persists, but selling pressure no longer dominates as clearly.

Consolidation & Compression

14. Consolidation

- Default state when no specific pattern dominates and the market is broadly balanced.

- Educational use: treat this as a “no strong edge” label; focus on structure rather than direction.

15. Breakout Imminent

- Neutral trend with contracting volume.

- Compression phase where energy is building up; often precedes transitions into trending or shock scenarios.

Traps & Hidden Divergences

16. Bull Trap

- Bullish trend, with neutral or contracting volume and sell‑side delta.

- Price appears strong, but order‑flow shifts against it; often seen near fake breakouts or failing rallies.

17. Bear Trap

- Bearish trend, neutral or contracting volume, but buy‑side delta.

- Downtrend “looks” intact, while buyers become more aggressive underneath the surface.

18. Hidden Bullish Divergence

- Bullish trend, contracting volume, but strong buy‑side delta.

- Educational idea: price dips or slows while aggressive buyers step in, often inside an ongoing uptrend.

19. Hidden Bearish Divergence

- Bearish trend, volume expansion and strong sell‑side delta.

- Reinforced downside pressure even if price is temporarily retracing.

Reversal & Transition Patterns

20. Reversal to Bearish

- Neutral trend, volume climax and strong sell‑side delta.

- Suggests that heavy selling appears at the top of a move, turning a previously neutral or rising context into potential downside.

21. Reversal to Bullish

- Neutral trend, extreme volume dry‑up and strong buy‑side delta.

- Often associated with selling exhaustion where buyers start to take control.

22. Indecision Spike

- Neutral trend with extreme volume (climax or dry‑up) but neutral delta.

- Crowd participation changes sharply while order‑flow remains undecided; treat as an informational spike rather than a direction.

Extended Compression & Acceleration

23. Coiling Phase

- Neutral trend, contracting volume, and delta that is neutral or only mildly one‑sided.

- Extended compression where price, volume and delta all contract into a tightly coiled range, often preceding a strong move.

24. Bullish Acceleration

- Bullish trend with volume expansion and strong buy‑side delta.

- Uptrend not only continues but gains kinetic strength; educationally, this illustrates how trend, volume and delta align in the strongest phases of a move.

25. Bearish Acceleration

- Bearish trend with volume expansion and strong sell‑side delta.

- Mirror image of Bullish Acceleration on the downside.

Trend Exhaustion & Climax Reversal

26. Bull Exhaustion

- Bullish or extreme bullish trend, with contraction or dry‑up in volume and buy‑side or neutral delta.

- The move has already travelled far; participation fades while price is still elevated.

27. Bear Exhaustion

- Bearish or extreme bearish trend, with volume climax or contraction and sell‑side or neutral delta.

- Down‑move may be approaching a point where additional selling pressure has diminishing impact.

28. Blow‑Off Top

- Extreme bullish trend, volume climax and extreme buy delta all at once.

- Classic blow‑off behaviour: price, volume and order‑flow are simultaneously stretched in the same direction.

29. Selling Climax Reversal

- Extreme bearish trend with extreme volume dry‑up and extreme sell‑side delta.

- Marks a very aggressive capitulation phase that can precede major rebounds.

Advanced VSA / Anomaly Scenarios

30. Absorption

- Typically neutral trend with expanding or climax volume and extreme delta (either buy or sell).

- Educational focus: large participants are aggressively absorbing liquidity from the opposite side, while price remains relatively contained.

31. Distribution

- Scenario where volume remains elevated while directional conviction weakens and the trend slows.

- Represents potential “selling into strength” or “buying into weakness”, depending on the active side.

32. Liquidity Vacuum

- Combination of thin liquidity (extreme dry‑up) with a directional trend or strong delta.

- Highlights environments where even small orders can move price disproportionately.

33. Anomaly / Shock Event

- Triggered when the vector z‑scores detect rare combinations of price, volume and delta behaviour that deviate from their own historical distribution.

- Intended as a warning label for unusual events rather than a specific tradeable pattern.

9. Educational Usage Notes

- EMVOL does not produce mechanical “buy” or “sell” commands. Instead, it classes each bar into an interpretable state so that traders can study how trends, volume and order‑flow interact over time.

- A common exercise is to overlay your usual EMA crossovers, support/resistance or price patterns and observe which EMVOL scenarios appear around entries, exits, traps and climaxes.

- Because the vectors are normalized (bounded between ‑1 and +1) and then discretized, the same conceptual states can be compared across different symbols and timeframes.

10. Disclaimer & Educational Purpose

This indicator is provided strictly as an educational and analytical tool. Its purpose is to help visualise how price, volume and order‑flow interact; it is not designed to function as a stand‑alone trading system.

Please note:

1. No Automated Strategy – The script does not implement a complete trading strategy. Scenario labels and dashboard messages are descriptive and should not be followed as unconditional entry or exit signals.

2. No Financial Advice – All information produced by this indicator is general market analysis. It must not be interpreted as investment, financial or trading advice, or as a recommendation to buy or sell any instrument.

3. Risk Warning – Trading and investing involve substantial risk, including the risk of loss. Always perform your own analysis, use appropriate position sizing and risk management, and consult a qualified professional if needed. You are solely responsible for any decisions made using this tool.

4. Data Precision & Platform Limits – The “Intrabar (Precise)” mode depends on the availability of high‑resolution historical data at the chosen intrabar timeframe. If your TradingView plan or the symbol’s history does not provide sufficient depth, this mode may only partially cover the visible chart. In such cases, consider switching to “Geometry (Source File)” for a fully populated view.

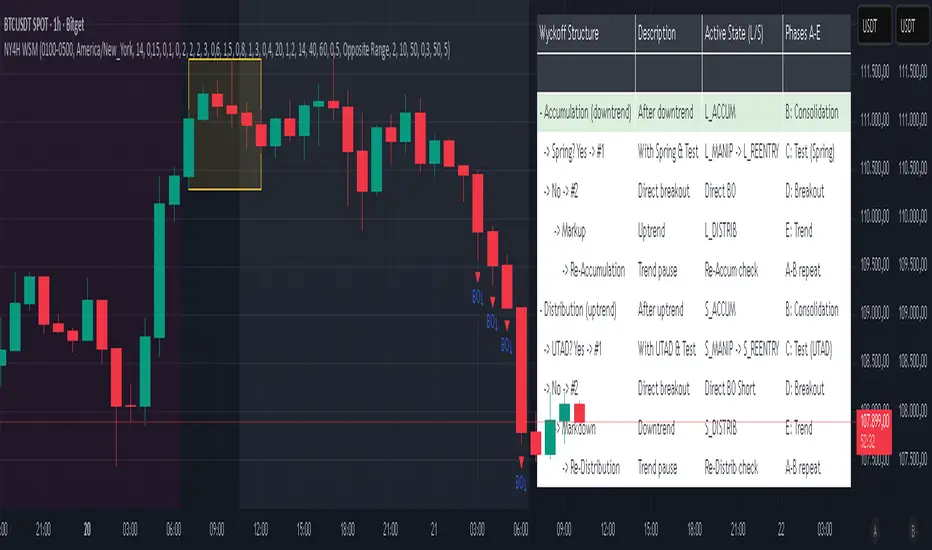

NY 4H Wyckoff State Machine [CHE] NY 4H Wyckoff State Machine — Full (Re-Entry, Breakout, Wick, Re-Accum/Distrib, Dynamic Table) — One-Candle Wyckoff Re-Entry (OCWR)

Summary

OCWR operationalizes a one-candle session workflow: mark the first four-hour New York candle, fix its high and low as the session range when the window closes, and drive entries through a Wyckoff-style state machine on intraday bars. The script adds an ATR-scaled buffer around the range and requires multi-bar acceptance before treating breaks or re-entries as valid. Optional wick-cluster evidence, a proximity retest, and simple volume or RSI gates increase selectivity. Background tints expose regimes, shapes mark events, a dynamic table explains the current state, and hidden plots supply alert payloads. The design reduces random flips and makes state transitions auditable without higher-timeframe calls.

Origin and name

Method name: One-Candle Wyckoff Re-Entry (OCWR)

Transcript origin: The source idea is a “stupid simple one-candle scalping” routine: mark the first New York four-hour candle (commonly between one and five in the morning New York time), drop to five minutes, observe accumulation inside, wait for a manipulation move outside, then trade the re-entry back inside. Stops go beyond the excursion extreme; targets are either a fixed reward multiple or the opposite side of the range. Preference is given to several manipulation candles. This indicator codifies that workflow with explicit states, acceptance counters, buffers, and optional quality filters. Any external performance claims are not part of the code.

Motivation: Why this design?

Session levels are widely respected, yet single-bar breaches around them are noisy. OCWR separates range discovery from trade logic. It locks the range at the end of the window, applies an ATR-scaled buffer to ignore marginal oversteps, and requires acceptance over several bars for breaks and re-entries. Wick evidence and optional retest proximity help confirm that an excursion likely cleared liquidity rather than launched a trend. This yields cleaner transitions from test to commitment.

What’s different vs. standard approaches?

Baseline: Static session lines or one-shot Wyckoff tags without process control.

Architecture: Dual long and short state machines; ATR-buffered edges; multi-bar acceptance for breaks and re-entries; optional wick dominance and cluster checks; optional retest tolerance; direct and opposite breakout paths; cooldown after fires; distribution timeout; dynamic table with highlighted row.

Practical effect: Fewer single-bar head-fakes, clearer hand-offs, and on-chart explanations of the machine’s view.

Wyckoff structure by example — OCWR on five minutes

One-candle setup:

On the four-hour chart, mark the first New York candle’s high and low, then switch to five minutes. Solid lines show the fixed range; dashed lines show ATR-buffered edges.

Long path (verbal mapping):

Phase A, Stopping Action: Price stabilizes inside the range.

Phase B, Consolidation: Sustained balance while the window is closed and after the range is fixed.

Phase C, Test (Spring): Excursion below the buffered low with preference for several outside bars and dominant lower wicks, then a return inside.

Re-entry acceptance: A required run of inside bars validates the test.

Phase D, Breakout to Markup: Long signal fires; stop beyond the excursion extreme; objective is the opposite range or a fixed reward multiple.

Phase E, Trend (Markup) and Re-Accumulation: Advance continues until target, stop, confirmation back against the box, or timeout. A pause inside trend may register as re-accumulation.

Short path mirrors the above: A UTAD-style move forms above the buffered high, then re-entry leads to Markdown and possible re-distribution.

Variant map (verbal):

Accumulation after a downtrend: with Spring and Test, or without Spring; both proceed to Markup and may pause in Re-Accumulation.

Distribution after an uptrend: with UTAD and Test, or without UTAD; both proceed to Markdown and may pause in Re-Distribution.

Note: Phases A through E occur within each variant and are not separate variants.

How it works (technical)

Session window: A configurable four-hour New York window records its high and low. At window end, the bounds are fixed for the session.

ATR buffer: A margin above and below the fixed range discourages triggers from tiny oversteps.

Inside and outside: Users choose close-based or wick-based detection. Overshoot requirements are expressed verbally as a fraction of the range with an optional absolute minimum.

Manipulation tracking: The machine counts bars spent outside and records the side extreme.

Re-entry acceptance: After a return inside, a specified number of inside bars must print before acceptance.

Direct and opposite breakouts: Direct breakouts from accumulation and opposite breakouts after manipulation are supported, subject to acceptance and optional filters.

Targets and exits: Choose the opposite boundary or a fixed reward multiple. Distribution ends on target, stop, confirmation back against the range, or timeout.

Context filters (optional): Volume above a scaled SMA, RSI thresholds, and a trend SMA for simple regime context.

Diagnostics: Background tints for regimes; arrows for re-entries; triangles for breakouts; table with row highlights; hidden plots for alert values.

Central table (Wyckoff console)

The table sits top-right and explains the machine’s stance. Columns: Structure label, plain-English description, active state pair for long and short, and human phase tags. Rows: Start and range building; accumulation branch with Spring and Test as well as direct breakout; Markup and re-accumulation; distribution branch with UTAD and Test as well as direct short breakout; Markdown and re-distribution. Only the active state cell is rewritten each last bar, for example “L_ACCUM slash S_ACCUM”. Row highlighting is context-aware: accumulation, Spring or UTAD, breakout, Markup or Markdown, and re-accumulation or re-distribution checks can highlight independently so users see simultaneous conditions. The table is created once, updated only on the last bar for efficiency, and functions as a read-only console to audit why a signal fired and where the path currently sits.

Parameter Guide

Session window and time zone: First four hours of New York by default; time zone “America/New_York”.

ATR length and buffer factor: Control buffer size; larger reduces sensitivity, smaller reacts faster.

Minimum overshoot (fraction and absolute): Demand meaningful extension beyond the buffer.

Break mode: Close-based is stricter; wick-based is more reactive.

Acceptance counts: Separate counts for break, re-entry, and opposite breakout; higher values reduce noise.

Minimum bars outside: Ensures manipulation is not a single spike.

Wick detection and clusters (optional): Dominance thresholds and cluster size within a short window.

Retest required and tolerance (optional): Gate re-entry by proximity to the buffered edge.

Volume and RSI filters (optional): Simple gates on activity and momentum.

TP mode and reward multiple: Opposite range or fixed multiple.

Cooldown and distribution timeout: Rate-limit signals and prevent endless distribution.

Visualization toggles: Background phases, labels, table, and helper lines.

Reading & Interpretation

Solid lines are the fixed session bounds; dashed lines are buffers. Backgrounds tint accumulation, manipulation, and distribution. Arrows show accepted re-entries; triangles show direct or opposite breakouts. Labels can summarize entry, stop, target, and risk. The table highlights the active row and the current state pair.

Practical Workflows & Combinations

OCWR baseline: Each morning, mark the New York four-hour candle, move to five minutes, prefer multi-bar manipulation outside, then wait for a qualified re-entry inside. Stop beyond the excursion extreme. Target the opposite range for conservative management or a fixed multiple for uniform sizing.

Trend following: Favor direct breakouts with trend alignment and no contradictory wick evidence.

Quality control: When noise rises, increase acceptance, raise the buffer factor, enable retest, and require wick clusters.

Discretionary confluences: Fair-value gaps and trend lines can be added by the user; they are not computed by this script.

Behavior, Constraints & Performance

Closed-bar confirmation is recommended when you require finality; live-bar conditions can change until close. The script does not call higher-timeframe data. It uses arrays, lines, labels, boxes, and a table; maximum bars back is five thousand; table updates are last-bar only. Known limits include compressed buffers in quiet sessions, unreliable wick evidence in thin markets, and session misalignment if the platform time zone is not New York.

Sensible Defaults & Quick Tuning

Start with ATR length fourteen, buffer factor near zero point fifteen, overshoot fraction near zero point ten, acceptance counts of two, minimum outside duration three, retest required on.

Too many flips: increase acceptance, raise buffer, enable retest, and tighten wick thresholds.

Too slow: reduce acceptance, lower buffer, switch to wick-based breaks, disable retest.

Noisy wicks: increase minimum wick ratio and cluster size, or disable wick detection.

What this indicator is—and isn’t

A session-anchored visualization and signal layer that formalizes a Wyckoff-style re-entry and breakout workflow derived from a single four-hour New York candle. It is not predictive and not a complete trading system. Use with structure analysis, risk controls, and position management.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Bitcoin vs. Gold correlation with lagBTC vs Gold (Lag) + Correlation — multi-timeframe, publication notes

What it does

Plots Gold on the same chart as Bitcoin, with a configurable lead/lag.

Lets you choose how the series is displayed:

Gold shifted forward (+lag on chart) — shows gold ahead of BTC on the time axis (visual offset).

Gold aligned to BTC (gold lag) — standard alignment; gold is lagged for calculation and plotted in place.

BTC 200D Lag (BTC shifted forward) — visualizes BTC shifted forward (like popular “BTC 200D Lag” charts).

Computes Pearson correlations between BTC (no lag) and Gold (with lag) over multiple lookback windows equivalent to:

30d, 60d, 90d, 180d, 365d, 2y (730d), 3y (1095d), 5y (1825d).

Shows a table with the correlation values, automatically scaled to the current timeframe.

Why this is useful

A common macro claim is that BTC tends to follow Gold with a delay (e.g., ~200 trading days). This tool lets you:

Visually advance Gold (or BTC) to see that lead-lag relationship on the chart.

Quantify the relationship with rolling correlations.

Switch timeframes (D/W/M/…): everything automatically stays in sync.

Quick start

Open a BTC chart (any exchange).

Add the indicator.

Set Gold symbol (default TVC:GOLD; alternatives: OANDA:XAUUSD, COMEX:GC1!, etc.).

Choose Lag value and Lag unit (Days/Weeks/Months/Years/Bars).

Pick Visual Mode:

To mirror those “BTC 200D Lag” posts: choose “BTC 200D Lag (BTC shifted forward)” with 200 Days.

To view Gold 200D ahead of BTC: select “Gold shifted forward (+lag on chart)” with 200 Days.

Keep Rebase to 100 ON for an apples-to-apples visual scale. (You can move the study to the left price scale if needed.)

Inputs

Gold symbol: external series to pair with BTC.

Lag value: numeric value.

Lag unit: Days, Weeks, Months (≈30d), Years (≈365d), or direct Bars.

Visual mode:

Gold shifted forward (+lag on chart) → gold is offset to the right by the lag (visual only).

Gold aligned to BTC (gold lag) → standard plot (no visual offset); correlations still use lagged gold.

BTC 200D Lag (BTC shifted forward) → BTC is offset to the right by the lag (visual only).

Rebase to 100 (visual): rescales each series to 100 on its first valid bar for clearer comparison.

Show gold without lag (debug): optional reference line.

Show price tag for gold (lag): toggles the track price label.

Timeframe handling

The study uses the current chart timeframe for both BTC and Gold (timeframe.period).

Lag in time units (Days/Weeks/Months/Years) is internally converted to an integer number of bars of the active timeframe (using timeframe.in_seconds).

Example: on W (weekly), 200 days ≈ 29 bars.

On intraday timeframes, days are converted proportionally.

Correlation math

Correlation = ta.correlation(BTC, Gold_lagged, length_in_bars)

Lookback lengths are the bar-equivalents of 30/60/90/180/365/730/1095/1825 days in the active timeframe.

Important: correlations are computed on prices (not returns). If you prefer returns-based correlation (often more statistically robust), duplicate the script and replace price inputs with change(close) or ta.roc(close, 1).

Reading the table

Window: nominal day label (e.g., 30d, 1y, 5y).

Bars (TF): how many bars that window equals on the current timeframe.

Correlation: Pearson coefficient . Background tint shows intensity and sign.

Tips & caveats

Visual offsets (offset=) move series on screen only; they don’t affect the math. The math always uses BTC (no lag) × Gold (lagged).

With large lags on high timeframes, early bars will be na (normal). Scroll forward / reduce lag.

If your Gold feed doesn’t load, try an alternative symbol that your plan supports.

Rebase to 100 helps visibility when BTC ($100k) and Gold ($2k) share a scale.

Months/Years use 30/365-day approximations. For exact control, use Days or Bars.

Correlations on very short lengths or sparse data can be unstable; consider the longer windows for sturdier signals.

This is a visual/analytical tool, not a trading signal. Always apply independent risk management.

Suggested setups

Replicate “BTC 200D Lag” charts:

Visual Mode: BTC 200D Lag (BTC shifted forward)

Lag: 200 Days

Rebase: ON

Gold leads BTC (Gold ahead):

Visual Mode: Gold shifted forward (+lag on chart)

Lag: 200 Days

Rebase: ON

Compatibility: Pine v6, overlay study.

Best with: BTCUSD (any exchange) + a reliable Gold feed.

Author’s note: Lead-lag relationships are not stable over time; treat correlations as descriptive, not predictive.

ATAI Volume analysis with price action V 1.00ATAI Volume Analysis with Price Action

1. Introduction

1.1 Overview

ATAI Volume Analysis with Price Action is a composite indicator designed for TradingView. It combines per‑side volume data —that is, how much buying and selling occurs during each bar—with standard price‑structure elements such as swings, trend lines and support/resistance. By blending these elements the script aims to help a trader understand which side is in control, whether a breakout is genuine, when markets are potentially exhausted and where liquidity providers might be active.

The indicator is built around TradingView’s up/down volume feed accessed via the TradingView/ta/10 library. The following excerpt from the script illustrates how this feed is configured:

import TradingView/ta/10 as tvta

// Determine lower timeframe string based on user choice and chart resolution

string lower_tf_breakout = use_custom_tf_input ? custom_tf_input :

timeframe.isseconds ? "1S" :

timeframe.isintraday ? "1" :

timeframe.isdaily ? "5" : "60"

// Request up/down volume (both positive)

= tvta.requestUpAndDownVolume(lower_tf_breakout)

Lower‑timeframe selection. If you do not specify a custom lower timeframe, the script chooses a default based on your chart resolution: 1 second for second charts, 1 minute for intraday charts, 5 minutes for daily charts and 60 minutes for anything longer. Smaller intervals provide a more precise view of buyer and seller flow but cover fewer bars. Larger intervals cover more history at the cost of granularity.

Tick vs. time bars. Many trading platforms offer a tick / intrabar calculation mode that updates an indicator on every trade rather than only on bar close. Turning on one‑tick calculation will give the most accurate split between buy and sell volume on the current bar, but it typically reduces the amount of historical data available. For the highest fidelity in live trading you can enable this mode; for studying longer histories you might prefer to disable it. When volume data is completely unavailable (some instruments and crypto pairs), all modules that rely on it will remain silent and only the price‑structure backbone will operate.

Figure caption, Each panel shows the indicator’s info table for a different volume sampling interval. In the left chart, the parentheses “(5)” beside the buy‑volume figure denote that the script is aggregating volume over five‑minute bars; the center chart uses “(1)” for one‑minute bars; and the right chart uses “(1T)” for a one‑tick interval. These notations tell you which lower timeframe is driving the volume calculations. Shorter intervals such as 1 minute or 1 tick provide finer detail on buyer and seller flow, but they cover fewer bars; longer intervals like five‑minute bars smooth the data and give more history.

Figure caption, The values in parentheses inside the info table come directly from the Breakout — Settings. The first row shows the custom lower-timeframe used for volume calculations (e.g., “(1)”, “(5)”, or “(1T)”)

2. Price‑Structure Backbone

Even without volume, the indicator draws structural features that underpin all other modules. These features are always on and serve as the reference levels for subsequent calculations.

2.1 What it draws

• Pivots: Swing highs and lows are detected using the pivot_left_input and pivot_right_input settings. A pivot high is identified when the high recorded pivot_right_input bars ago exceeds the highs of the preceding pivot_left_input bars and is also higher than (or equal to) the highs of the subsequent pivot_right_input bars; pivot lows follow the inverse logic. The indicator retains only a fixed number of such pivot points per side, as defined by point_count_input, discarding the oldest ones when the limit is exceeded.

• Trend lines: For each side, the indicator connects the earliest stored pivot and the most recent pivot (oldest high to newest high, and oldest low to newest low). When a new pivot is added or an old one drops out of the lookback window, the line’s endpoints—and therefore its slope—are recalculated accordingly.

• Horizontal support/resistance: The highest high and lowest low within the lookback window defined by length_input are plotted as horizontal dashed lines. These serve as short‑term support and resistance levels.

• Ranked labels: If showPivotLabels is enabled the indicator prints labels such as “HH1”, “HH2”, “LL1” and “LL2” near each pivot. The ranking is determined by comparing the price of each stored pivot: HH1 is the highest high, HH2 is the second highest, and so on; LL1 is the lowest low, LL2 is the second lowest. In the case of equal prices the newer pivot gets the better rank. Labels are offset from price using ½ × ATR × label_atr_multiplier, with the ATR length defined by label_atr_len_input. A dotted connector links each label to the candle’s wick.

2.2 Key settings

• length_input: Window length for finding the highest and lowest values and for determining trend line endpoints. A larger value considers more history and will generate longer trend lines and S/R levels.

• pivot_left_input, pivot_right_input: Strictness of swing confirmation. Higher values require more bars on either side to form a pivot; lower values create more pivots but may include minor swings.

• point_count_input: How many pivots are kept in memory on each side. When new pivots exceed this number the oldest ones are discarded.

• label_atr_len_input and label_atr_multiplier: Determine how far pivot labels are offset from the bar using ATR. Increasing the multiplier moves labels further away from price.

• Styling inputs for trend lines, horizontal lines and labels (color, width and line style).

Figure caption, The chart illustrates how the indicator’s price‑structure backbone operates. In this daily example, the script scans for bars where the high (or low) pivot_right_input bars back is higher (or lower) than the preceding pivot_left_input bars and higher or lower than the subsequent pivot_right_input bars; only those bars are marked as pivots.

These pivot points are stored and ranked: the highest high is labelled “HH1”, the second‑highest “HH2”, and so on, while lows are marked “LL1”, “LL2”, etc. Each label is offset from the price by half of an ATR‑based distance to keep the chart clear, and a dotted connector links the label to the actual candle.

The red diagonal line connects the earliest and latest stored high pivots, and the green line does the same for low pivots; when a new pivot is added or an old one drops out of the lookback window, the end‑points and slopes adjust accordingly. Dashed horizontal lines mark the highest high and lowest low within the current lookback window, providing visual support and resistance levels. Together, these elements form the structural backbone that other modules reference, even when volume data is unavailable.

3. Breakout Module

3.1 Concept

This module confirms that a price break beyond a recent high or low is supported by a genuine shift in buying or selling pressure. It requires price to clear the highest high (“HH1”) or lowest low (“LL1”) and, simultaneously, that the winning side shows a significant volume spike, dominance and ranking. Only when all volume and price conditions pass is a breakout labelled.

3.2 Inputs

• lookback_break_input : This controls the number of bars used to compute moving averages and percentiles for volume. A larger value smooths the averages and percentiles but makes the indicator respond more slowly.

• vol_mult_input : The “spike” multiplier; the current buy or sell volume must be at least this multiple of its moving average over the lookback window to qualify as a breakout.

• rank_threshold_input (0–100) : Defines a volume percentile cutoff: the current buyer/seller volume must be in the top (100−threshold)%(100−threshold)% of all volumes within the lookback window. For example, if set to 80, the current volume must be in the top 20 % of the lookback distribution.

• ratio_threshold_input (0–1) : Specifies the minimum share of total volume that the buyer (for a bullish breakout) or seller (for bearish) must hold on the current bar; the code also requires that the cumulative buyer volume over the lookback window exceeds the seller volume (and vice versa for bearish cases).

• use_custom_tf_input / custom_tf_input : When enabled, these inputs override the automatic choice of lower timeframe for up/down volume; otherwise the script selects a sensible default based on the chart’s timeframe.

• Label appearance settings : Separate options control the ATR-based offset length, offset multiplier, label size and colors for bullish and bearish breakout labels, as well as the connector style and width.

3.3 Detection logic

1. Data preparation : Retrieve per‑side volume from the lower timeframe and take absolute values. Build rolling arrays of the last lookback_break_input values to compute simple moving averages (SMAs), cumulative sums and percentile ranks for buy and sell volume.

2. Volume spike: A spike is flagged when the current buy (or, in the bearish case, sell) volume is at least vol_mult_input times its SMA over the lookback window.

3. Dominance test: The buyer’s (or seller’s) share of total volume on the current bar must meet or exceed ratio_threshold_input. In addition, the cumulative sum of buyer volume over the window must exceed the cumulative sum of seller volume for a bullish breakout (and vice versa for bearish). A separate requirement checks the sign of delta: for bullish breakouts delta_breakout must be non‑negative; for bearish breakouts it must be non‑positive.

4. Percentile rank: The current volume must fall within the top (100 – rank_threshold_input) percent of the lookback distribution—ensuring that the spike is unusually large relative to recent history.

5. Price test: For a bullish signal, the closing price must close above the highest pivot (HH1); for a bearish signal, the close must be below the lowest pivot (LL1).

6. Labeling: When all conditions above are satisfied, the indicator prints “Breakout ↑” above the bar (bullish) or “Breakout ↓” below the bar (bearish). Labels are offset using half of an ATR‑based distance and linked to the candle with a dotted connector.

Figure caption, (Breakout ↑ example) , On this daily chart, price pushes above the red trendline and the highest prior pivot (HH1). The indicator recognizes this as a valid breakout because the buyer‑side volume on the lower timeframe spikes above its recent moving average and buyers dominate the volume statistics over the lookback period; when combined with a close above HH1, this satisfies the breakout conditions. The “Breakout ↑” label appears above the candle, and the info table highlights that up‑volume is elevated relative to its 11‑bar average, buyer share exceeds the dominance threshold and money‑flow metrics support the move.

Figure caption, In this daily example, price breaks below the lowest pivot (LL1) and the lower green trendline. The indicator identifies this as a bearish breakout because sell‑side volume is sharply elevated—about twice its 11‑bar average—and sellers dominate both the bar and the lookback window. With the close falling below LL1, the script triggers a Breakout ↓ label and marks the corresponding row in the info table, which shows strong down volume, negative delta and a seller share comfortably above the dominance threshold.

4. Market Phase Module (Volume Only)

4.1 Concept

Not all markets trend; many cycle between periods of accumulation (buying pressure building up), distribution (selling pressure dominating) and neutral behavior. This module classifies the current bar into one of these phases without using ATR , relying solely on buyer and seller volume statistics. It looks at net flows, ratio changes and an OBV‑like cumulative line with dual‑reference (1‑ and 2‑bar) trends. The result is displayed both as on‑chart labels and in a dedicated row of the info table.

4.2 Inputs

• phase_period_len: Number of bars over which to compute sums and ratios for phase detection.

• phase_ratio_thresh : Minimum buyer share (for accumulation) or minimum seller share (for distribution, derived as 1 − phase_ratio_thresh) of the total volume.

• strict_mode: When enabled, both the 1‑bar and 2‑bar changes in each statistic must agree on the direction (strict confirmation); when disabled, only one of the two references needs to agree (looser confirmation).

• Color customisation for info table cells and label styling for accumulation and distribution phases, including ATR length, multiplier, label size, colors and connector styles.

• show_phase_module: Toggles the entire phase detection subsystem.

• show_phase_labels: Controls whether on‑chart labels are drawn when accumulation or distribution is detected.

4.3 Detection logic

The module computes three families of statistics over the volume window defined by phase_period_len:

1. Net sum (buyers minus sellers): net_sum_phase = Σ(buy) − Σ(sell). A positive value indicates a predominance of buyers. The code also computes the differences between the current value and the values 1 and 2 bars ago (d_net_1, d_net_2) to derive up/down trends.

2. Buyer ratio: The instantaneous ratio TF_buy_breakout / TF_tot_breakout and the window ratio Σ(buy) / Σ(total). The current ratio must exceed phase_ratio_thresh for accumulation or fall below 1 − phase_ratio_thresh for distribution. The first and second differences of the window ratio (d_ratio_1, d_ratio_2) determine trend direction.

3. OBV‑like cumulative net flow: An on‑balance volume analogue obv_net_phase increments by TF_buy_breakout − TF_sell_breakout each bar. Its differences over the last 1 and 2 bars (d_obv_1, d_obv_2) provide trend clues.

The algorithm then combines these signals:

• For strict mode , accumulation requires: (a) current ratio ≥ threshold, (b) cumulative ratio ≥ threshold, (c) both ratio differences ≥ 0, (d) net sum differences ≥ 0, and (e) OBV differences ≥ 0. Distribution is the mirror case.

• For loose mode , it relaxes the directional tests: either the 1‑ or the 2‑bar difference needs to agree in each category.

If all conditions for accumulation are satisfied, the phase is labelled “Accumulation” ; if all conditions for distribution are satisfied, it’s labelled “Distribution” ; otherwise the phase is “Neutral” .

4.4 Outputs

• Info table row : Row 8 displays “Market Phase (Vol)” on the left and the detected phase (Accumulation, Distribution or Neutral) on the right. The text colour of both cells matches a user‑selectable palette (typically green for accumulation, red for distribution and grey for neutral).

• On‑chart labels : When show_phase_labels is enabled and a phase persists for at least one bar, the module prints a label above the bar ( “Accum” ) or below the bar ( “Dist” ) with a dashed or dotted connector. The label is offset using ATR based on phase_label_atr_len_input and phase_label_multiplier and is styled according to user preferences.

Figure caption, The chart displays a red “Dist” label above a particular bar, indicating that the accumulation/distribution module identified a distribution phase at that point. The detection is based on seller dominance: during that bar, the net buyer-minus-seller flow and the OBV‑style cumulative flow were trending down, and the buyer ratio had dropped below the preset threshold. These conditions satisfy the distribution criteria in strict mode. The label is placed above the bar using an ATR‑based offset and a dashed connector. By the time of the current bar in the screenshot, the phase indicator shows “Neutral” in the info table—signaling that neither accumulation nor distribution conditions are currently met—yet the historical “Dist” label remains to mark where the prior distribution phase began.

Figure caption, In this example the market phase module has signaled an Accumulation phase. Three bars before the current candle, the algorithm detected a shift toward buyers: up‑volume exceeded its moving average, down‑volume was below average, and the buyer share of total volume climbed above the threshold while the on‑balance net flow and cumulative ratios were trending upwards. The blue “Accum” label anchored below that bar marks the start of the phase; it remains on the chart because successive bars continue to satisfy the accumulation conditions. The info table confirms this: the “Market Phase (Vol)” row still reads Accumulation, and the ratio and sum rows show buyers dominating both on the current bar and across the lookback window.

5. OB/OS Spike Module

5.1 What overbought/oversold means here

In many markets, a rapid extension up or down is often followed by a period of consolidation or reversal. The indicator interprets overbought (OB) conditions as abnormally strong selling risk at or after a price rally and oversold (OS) conditions as unusually strong buying risk after a decline. Importantly, these are not direct trade signals; rather they flag areas where caution or contrarian setups may be appropriate.

5.2 Inputs

• minHits_obos (1–7): Minimum number of oscillators that must agree on an overbought or oversold condition for a label to print.

• syncWin_obos: Length of a small sliding window over which oscillator votes are smoothed by taking the maximum count observed. This helps filter out choppy signals.

• Volume spike criteria: kVolRatio_obos (ratio of current volume to its SMA) and zVolThr_obos (Z‑score threshold) across volLen_obos. Either threshold can trigger a spike.

• Oscillator toggles and periods: Each of RSI, Stochastic (K and D), Williams %R, CCI, MFI, DeMarker and Stochastic RSI can be independently enabled; their periods are adjustable.

• Label appearance: ATR‑based offset, size, colors for OB and OS labels, plus connector style and width.

5.3 Detection logic

1. Directional volume spikes: Volume spikes are computed separately for buyer and seller volumes. A sell volume spike (sellVolSpike) flags a potential OverBought bar, while a buy volume spike (buyVolSpike) flags a potential OverSold bar. A spike occurs when the respective volume exceeds kVolRatio_obos times its simple moving average over the window or when its Z‑score exceeds zVolThr_obos.

2. Oscillator votes: For each enabled oscillator, calculate its overbought and oversold state using standard thresholds (e.g., RSI ≥ 70 for OB and ≤ 30 for OS; Stochastic %K/%D ≥ 80 for OB and ≤ 20 for OS; etc.). Count how many oscillators vote for OB and how many vote for OS.

3. Minimum hits: Apply the smoothing window syncWin_obos to the vote counts using a maximum‑of‑last‑N approach. A candidate bar is only considered if the smoothed OB hit count ≥ minHits_obos (for OverBought) or the smoothed OS hit count ≥ minHits_obos (for OverSold).

4. Tie‑breaking: If both OverBought and OverSold spike conditions are present on the same bar, compare the smoothed hit counts: the side with the higher count is selected; ties default to OverBought.

5. Label printing: When conditions are met, the bar is labelled as “OverBought X/7” above the candle or “OverSold X/7” below it. “X” is the number of oscillators confirming, and the bracket lists the abbreviations of contributing oscillators. Labels are offset from price using half of an ATR‑scaled distance and can optionally include a dotted or dashed connector line.

Figure caption, In this chart the overbought/oversold module has flagged an OverSold signal. A sell‑off from the prior highs brought price down to the lower trend‑line, where the bar marked “OverSold 3/7 DeM” appears. This label indicates that on that bar the module detected a buy‑side volume spike and that at least three of the seven enabled oscillators—in this case including the DeMarker—were in oversold territory. The label is printed below the candle with a dotted connector, signaling that the market may be temporarily exhausted on the downside. After this oversold print, price begins to rebound towards the upper red trend‑line and higher pivot levels.

Figure caption, This example shows the overbought/oversold module in action. In the left‑hand panel you can see the OB/OS settings where each oscillator (RSI, Stochastic, Williams %R, CCI, MFI, DeMarker and Stochastic RSI) can be enabled or disabled, and the ATR length and label offset multiplier adjusted. On the chart itself, price has pushed up to the descending red trendline and triggered an “OverBought 3/7” label. That means the sell‑side volume spiked relative to its average and three out of the seven enabled oscillators were in overbought territory. The label is offset above the candle by half of an ATR and connected with a dashed line, signaling that upside momentum may be overextended and a pause or pullback could follow.

6. Buyer/Seller Trap Module

6.1 Concept

A bull trap occurs when price appears to break above resistance, attracting buyers, but fails to sustain the move and quickly reverses, leaving a long upper wick and trapping late entrants. A bear trap is the opposite: price breaks below support, lures in sellers, then snaps back, leaving a long lower wick and trapping shorts. This module detects such traps by looking for price structure sweeps, order‑flow mismatches and dominance reversals. It uses a scoring system to differentiate risk from confirmed traps.

6.2 Inputs

• trap_lookback_len: Window length used to rank extremes and detect sweeps.

• trap_wick_threshold: Minimum proportion of a bar’s range that must be wick (upper for bull traps, lower for bear traps) to qualify as a sweep.

• trap_score_risk: Minimum aggregated score required to flag a trap risk. (The code defines a trap_score_confirm input, but confirmation is actually based on price reversal rather than a separate score threshold.)

• trap_confirm_bars: Maximum number of bars allowed for price to reverse and confirm the trap. If price does not reverse in this window, the risk label will expire or remain unconfirmed.

• Label settings: ATR length and multiplier for offsetting, size, colours for risk and confirmed labels, and connector style and width. Separate settings exist for bull and bear traps.

• Toggle inputs: show_trap_module and show_trap_labels enable the module and control whether labels are drawn on the chart.

6.3 Scoring logic

The module assigns points to several conditions and sums them to determine whether a trap risk is present. For bull traps, the score is built from the following (bear traps mirror the logic with highs and lows swapped):

1. Sweep (2 points): Price trades above the high pivot (HH1) but fails to close above it and leaves a long upper wick at least trap_wick_threshold × range. For bear traps, price dips below the low pivot (LL1), fails to close below and leaves a long lower wick.

2. Close break (1 point): Price closes beyond HH1 or LL1 without leaving a long wick.

3. Candle/delta mismatch (2 points): The candle closes bullish yet the order flow delta is negative or the seller ratio exceeds 50%, indicating hidden supply. Conversely, a bearish close with positive delta or buyer dominance suggests hidden demand.

4. Dominance inversion (2 points): The current bar’s buyer volume has the highest rank in the lookback window while cumulative sums favor sellers, or vice versa.

5. Low‑volume break (1 point): Price crosses the pivot but total volume is below its moving average.

The total score for each side is compared to trap_score_risk. If the score is high enough, a “Bull Trap Risk” or “Bear Trap Risk” label is drawn, offset from the candle by half of an ATR‑scaled distance using a dashed outline. If, within trap_confirm_bars, price reverses beyond the opposite level—drops back below the high pivot for bull traps or rises above the low pivot for bear traps—the label is upgraded to a solid “Bull Trap” or “Bear Trap” . In this version of the code, there is no separate score threshold for confirmation: the variable trap_score_confirm is unused; confirmation depends solely on a successful price reversal within the specified number of bars.

Figure caption, In this example the trap module has flagged a Bear Trap Risk. Price initially breaks below the most recent low pivot (LL1), but the bar closes back above that level and leaves a long lower wick, suggesting a failed push lower. Combined with a mismatch between the candle direction and the order flow (buyers regain control) and a reversal in volume dominance, the aggregate score exceeds the risk threshold, so a dashed “Bear Trap Risk” label prints beneath the bar. The green and red trend lines mark the current low and high pivot trajectories, while the horizontal dashed lines show the highest and lowest values in the lookback window. If, within the next few bars, price closes decisively above the support, the risk label would upgrade to a solid “Bear Trap” label.

Figure caption, In this example the trap module has identified both ends of a price range. Near the highs, price briefly pushes above the descending red trendline and the recent pivot high, but fails to close there and leaves a noticeable upper wick. That combination of a sweep above resistance and order‑flow mismatch generates a Bull Trap Risk label with a dashed outline, warning that the upside break may not hold. At the opposite extreme, price later dips below the green trendline and the labelled low pivot, then quickly snaps back and closes higher. The long lower wick and subsequent price reversal upgrade the previous bear‑trap risk into a confirmed Bear Trap (solid label), indicating that sellers were caught on a false breakdown. Horizontal dashed lines mark the highest high and lowest low of the lookback window, while the red and green diagonals connect the earliest and latest pivot highs and lows to visualize the range.

7. Sharp Move Module

7.1 Concept

Markets sometimes display absorption or climax behavior—periods when one side steadily gains the upper hand before price breaks out with a sharp move. This module evaluates several order‑flow and volume conditions to anticipate such moves. Users can choose how many conditions must be met to flag a risk and how many (plus a price break) are required for confirmation.

7.2 Inputs

• sharp Lookback: Number of bars in the window used to compute moving averages, sums, percentile ranks and reference levels.

• sharpPercentile: Minimum percentile rank for the current side’s volume; the current buy (or sell) volume must be greater than or equal to this percentile of historical volumes over the lookback window.

• sharpVolMult: Multiplier used in the volume climax check. The current side’s volume must exceed this multiple of its average to count as a climax.

• sharpRatioThr: Minimum dominance ratio (current side’s volume relative to the opposite side) used in both the instant and cumulative dominance checks.

• sharpChurnThr: Maximum ratio of a bar’s range to its ATR for absorption/churn detection; lower values indicate more absorption (large volume in a small range).

• sharpScoreRisk: Minimum number of conditions that must be true to print a risk label.

• sharpScoreConfirm: Minimum number of conditions plus a price break required for confirmation.

• sharpCvdThr: Threshold for cumulative delta divergence versus price change (positive for bullish accumulation, negative for bearish distribution).

• Label settings: ATR length (sharpATRlen) and multiplier (sharpLabelMult) for positioning labels, label size, colors and connector styles for bullish and bearish sharp moves.

• Toggles: enableSharp activates the module; show_sharp_labels controls whether labels are drawn.

7.3 Conditions (six per side)

For each side, the indicator computes six boolean conditions and sums them to form a score:

1. Dominance (instant and cumulative):

– Instant dominance: current buy volume ≥ sharpRatioThr × current sell volume.

– Cumulative dominance: sum of buy volumes over the window ≥ sharpRatioThr × sum of sell volumes (and vice versa for bearish checks).

2. Accumulation/Distribution divergence: Over the lookback window, cumulative delta rises by at least sharpCvdThr while price fails to rise (bullish), or cumulative delta falls by at least sharpCvdThr while price fails to fall (bearish).

3. Volume climax: The current side’s volume is ≥ sharpVolMult × its average and the product of volume and bar range is the highest in the lookback window.

4. Absorption/Churn: The current side’s volume divided by the bar’s range equals the highest value in the window and the bar’s range divided by ATR ≤ sharpChurnThr (indicating large volume within a small range).

5. Percentile rank: The current side’s volume percentile rank is ≥ sharp Percentile.

6. Mirror logic for sellers: The above checks are repeated with buyer and seller roles swapped and the price break levels reversed.

Each condition that passes contributes one point to the corresponding side’s score (0 or 1). Risk and confirmation thresholds are then applied to these scores.

7.4 Scoring and labels

• Risk: If scoreBull ≥ sharpScoreRisk, a “Sharp ↑ Risk” label is drawn above the bar. If scoreBear ≥ sharpScoreRisk, a “Sharp ↓ Risk” label is drawn below the bar.

• Confirmation: A risk label is upgraded to “Sharp ↑” when scoreBull ≥ sharpScoreConfirm and the bar closes above the highest recent pivot (HH1); for bearish cases, confirmation requires scoreBear ≥ sharpScoreConfirm and a close below the lowest pivot (LL1).

• Label positioning: Labels are offset from the candle by ATR × sharpLabelMult (full ATR times multiplier), not half, and may include a dashed or dotted connector line if enabled.

Figure caption, In this chart both bullish and bearish sharp‑move setups have been flagged. Earlier in the range, a “Sharp ↓ Risk” label appears beneath a candle: the sell‑side score met the risk threshold, signaling that the combination of strong sell volume, dominance and absorption within a narrow range suggested a potential sharp decline. The price did not close below the lower pivot, so this label remains a “risk” and no confirmation occurred. Later, as the market recovered and volume shifted back to the buy side, a “Sharp ↑ Risk” label prints above a candle near the top of the channel. Here, buy‑side dominance, cumulative delta divergence and a volume climax aligned, but price has not yet closed above the upper pivot (HH1), so the alert is still a risk rather than a confirmed sharp‑up move.

Figure caption, In this chart a Sharp ↑ label is displayed above a candle, indicating that the sharp move module has confirmed a bullish breakout. Prior bars satisfied the risk threshold — showing buy‑side dominance, positive cumulative delta divergence, a volume climax and strong absorption in a narrow range — and this candle closes above the highest recent pivot, upgrading the earlier “Sharp ↑ Risk” alert to a full Sharp ↑ signal. The green label is offset from the candle with a dashed connector, while the red and green trend lines trace the high and low pivot trajectories and the dashed horizontals mark the highest and lowest values of the lookback window.

8. Market‑Maker / Spread‑Capture Module

8.1 Concept

Liquidity providers often “capture the spread” by buying and selling in almost equal amounts within a very narrow price range. These bars can signal temporary congestion before a move or reflect algorithmic activity. This module flags bars where both buyer and seller volumes are high, the price range is only a few ticks and the buy/sell split remains close to 50%. It helps traders spot potential liquidity pockets.

8.2 Inputs

• scalpLookback: Window length used to compute volume averages.

• scalpVolMult: Multiplier applied to each side’s average volume; both buy and sell volumes must exceed this multiple.

• scalpTickCount: Maximum allowed number of ticks in a bar’s range (calculated as (high − low) / minTick). A value of 1 or 2 captures ultra‑small bars; increasing it relaxes the range requirement.

• scalpDeltaRatio: Maximum deviation from a perfect 50/50 split. For example, 0.05 means the buyer share must be between 45% and 55%.

• Label settings: ATR length, multiplier, size, colors, connector style and width.

• Toggles : show_scalp_module and show_scalp_labels to enable the module and its labels.

8.3 Signal

When, on the current bar, both TF_buy_breakout and TF_sell_breakout exceed scalpVolMult times their respective averages and (high − low)/minTick ≤ scalpTickCount and the buyer share is within scalpDeltaRatio of 50%, the module prints a “Spread ↔” label above the bar. The label uses the same ATR offset logic as other modules and draws a connector if enabled.

Figure caption, In this chart the spread‑capture module has identified a potential liquidity pocket. Buyer and seller volumes both spiked above their recent averages, yet the candle’s range measured only a couple of ticks and the buy/sell split stayed close to 50 %. This combination met the module’s criteria, so it printed a grey “Spread ↔” label above the bar. The red and green trend lines link the earliest and latest high and low pivots, and the dashed horizontals mark the highest high and lowest low within the current lookback window.

9. Money Flow Module

9.1 Concept

To translate volume into a monetary measure, this module multiplies each side’s volume by the closing price. It tracks buying and selling system money default currency on a per-bar basis and sums them over a chosen period. The difference between buy and sell currencies (Δ$) shows net inflow or outflow.

9.2 Inputs

• mf_period_len_mf: Number of bars used for summing buy and sell dollars.

• Label appearance settings: ATR length, multiplier, size, colors for up/down labels, and connector style and width.

• Toggles: Use enableMoneyFlowLabel_mf and showMFLabels to control whether the module and its labels are displayed.

9.3 Calculations

• Per-bar money: Buy $ = TF_buy_breakout × close; Sell $ = TF_sell_breakout × close. Their difference is Δ$ = Buy $ − Sell $.

• Summations: Over mf_period_len_mf bars, compute Σ Buy $, Σ Sell $ and ΣΔ$ using math.sum().

• Info table entries: Rows 9–13 display these values as texts like “↑ USD 1234 (1M)” or “ΣΔ USD −5678 (14)”, with colors reflecting whether buyers or sellers dominate.

• Money flow status: If Δ$ is positive the bar is marked “Money flow in” ; if negative, “Money flow out” ; if zero, “Neutral”. The cumulative status is similarly derived from ΣΔ.Labels print at the bar that changes the sign of ΣΔ, offset using ATR × label multiplier and styled per user preferences.

Figure caption, The chart illustrates a steady rise toward the highest recent pivot (HH1) with price riding between a rising green trend‑line and a red trend‑line drawn through earlier pivot highs. A green Money flow in label appears above the bar near the top of the channel, signaling that net dollar flow turned positive on this bar: buy‑side dollar volume exceeded sell‑side dollar volume, pushing the cumulative sum ΣΔ$ above zero. In the info table, the “Money flow (bar)” and “Money flow Σ” rows both read In, confirming that the indicator’s money‑flow module has detected an inflow at both bar and aggregate levels, while other modules (pivots, trend lines and support/resistance) remain active to provide structural context.

In this example the Money Flow module signals a net outflow. Price has been trending downward: successive high pivots form a falling red trend‑line and the low pivots form a descending green support line. When the latest bar broke below the previous low pivot (LL1), both the bar‑level and cumulative net dollar flow turned negative—selling volume at the close exceeded buying volume and pushed the cumulative Δ$ below zero. The module reacts by printing a red “Money flow out” label beneath the candle; the info table confirms that the “Money flow (bar)” and “Money flow Σ” rows both show Out, indicating sustained dominance of sellers in this period.

10. Info Table

10.1 Purpose

When enabled, the Info Table appears in the lower right of your chart. It summarises key values computed by the indicator—such as buy and sell volume, delta, total volume, breakout status, market phase, and money flow—so you can see at a glance which side is dominant and which signals are active.

10.2 Symbols

• ↑ / ↓ — Up (↑) denotes buy volume or money; down (↓) denotes sell volume or money.

• MA — Moving average. In the table it shows the average value of a series over the lookback period.

• Σ (Sigma) — Cumulative sum over the chosen lookback period.

• Δ (Delta) — Difference between buy and sell values.

• B / S — Buyer and seller share of total volume, expressed as percentages.

• Ref. Price — Reference price for breakout calculations, based on the latest pivot.

• Status — Indicates whether a breakout condition is currently active (True) or has failed.

10.3 Row definitions

1. Up volume / MA up volume – Displays current buy volume on the lower timeframe and its moving average over the lookback period.

2. Down volume / MA down volume – Shows current sell volume and its moving average; sell values are formatted in red for clarity.

3. Δ / ΣΔ – Lists the difference between buy and sell volume for the current bar and the cumulative delta volume over the lookback period.

4. Σ / MA Σ (Vol/MA) – Total volume (buy + sell) for the bar, with the ratio of this volume to its moving average; the right cell shows the average total volume.

5. B/S ratio – Buy and sell share of the total volume: current bar percentages and the average percentages across the lookback period.

6. Buyer Rank / Seller Rank – Ranks the bar’s buy and sell volumes among the last (n) bars; lower rank numbers indicate higher relative volume.

7. Σ Buy / Σ Sell – Sum of buy and sell volumes over the lookback window, indicating which side has traded more.

8. Breakout UP / DOWN – Shows the breakout thresholds (Ref. Price) and whether the breakout condition is active (True) or has failed.

9. Market Phase (Vol) – Reports the current volume‑only phase: Accumulation, Distribution or Neutral.

10. Money Flow – The final rows display dollar amounts and status: