MA Correlation CoefficientThis script helps you visualize the correlation between the price of an asset and 4 moving averages of your choice. This indicator can help you identify trendy markets as well as trend-shifts.

Disclaimer

Bear in mind that there is always some lag when using Moving-Averages, hence the purpose of this indicator is as a trend identification tool rather than an entry-exit strategy.

Working Principle

The basic idea behind this indicator is the following:

In a trendy market you will find high correlation between price and all kinds of Moving-Averages. This works both ways, no matter bull or bear trend.

In sideways markets you might find a mix of correlations accross timeframes (2018) or high correlation with Low-Timeframe averages and low correlation with High-Timeframe averages (2021/2022).

Trend shifts might be characterised by a 'staircase' type of correlation (yellow), where the asset regains correlation with higher timeframe averages

Indicator Options

1. Source : data used for indicator calculation

1. Correlation Window : size of moving window for correlation calculation

2. Average Type :

Simple-Moving-Average (SMA)

Exponential-Moving-Average (EMA)

Hull-Moving-Average (HMA)

Volume-Weighted-Moving-Average (VWMA)

3. Lookback : number of past candles to calculate average

4. Gradient : modify gradient colors. colors relate to correlation values.

Plot Explanation

The indicator plots, using colors, the correlation of the asset with 4 averages. For every candle, 4 correlation values are generated, corresponding to 4 colors. These 4 colors are stacked one on top of the other generating the patterns explained above. These patterns may help you identify what kind of market you're in.

Cerca negli script per "宁德时代2021年净利润+资产负债率"

JS-TechTrading: VWAP Momentum_Pullback StrategyGeneral Description and Unique Features of this Script

Introducing the VWAP Momentum-Pullback Strategy (long-only) that offers several unique features:

1. Our script/strategy utilizes Mark Minervini's Trend-Template as a qualifier for identifying stocks and other financial securities in confirmed uptrends.

NOTE: In this basic version of the script, the Trend-Template has to be used as a separate indicator on TradingView (Public Trend-Template indicators are available on TradingView – community scripts). It is recommended to only execute buy signals in case the stock or financial security is in a stage 2 uptrend, which means that the criteria of the trend-template are fulfilled.

2. Our strategy is based on the supply/demand balance in the market, making it timeless and effective across all timeframes. Whether you are day trading using 1- or 5-min charts or swing-trading using daily charts, this strategy can be applied and works very well.

3. We have also integrated technical indicators such as the RSI and the MA / VWAP crossover into this strategy to identify low-risk pullback entries in the context of confirmed uptrends. By doing so, the risk profile of this strategy and drawdowns are being reduced to an absolute minimum.

Minervini’s Trend-Template and the ‘Stage-Analysis’ of the Markets

This strategy is a so-called 'long-only' strategy. This means that we only take long positions, short positions are not considered.

The best market environment for such strategies are periods of stable upward trends in the so-called stage 2 - uptrend.

In stable upward trends, we increase our market exposure and risk.

In sideways markets and downward trends or bear markets, we reduce our exposure very quickly or go 100% to cash and wait for the markets to recover and improve. This allows us to avoid major losses and drawdowns.

This simple rule gives us a significant advantage over most undisciplined traders and amateurs!

'The Trend is your Friend'. This is a very old but true quote.

What's behind it???

• 98% of stocks made their biggest gains in a Phase 2 upward trend.

• If a stock is in a stable uptrend, this is evidence that larger institutions are buying the stock sustainably.

• By focusing on stocks that are in a stable uptrend, the chances of profit are significantly increased.

• In a stable uptrend, investors know exactly what to expect from further price developments. This makes it possible to locate low-risk entry points.

The goal is not to buy at the lowest price – the goal is to buy at the right price!

Each stock goes through the same maturity cycle – it starts at stage 1 and ends at stage 4

Stage 1 – Neglect Phase – Consolidation

Stage 2 – Progressive Phase – Accumulation

Stage 3 – Topping Phase – Distribution

Stage 4 – Downtrend – Capitulation

This strategy focuses on identifying stocks in confirmed stage 2 uptrends. This in itself gives us an advantage over long-term investors and less professional traders.

By focusing on stocks in a stage 2 uptrend, we avoid losses in downtrends (stage 4) or less profitable consolidation phases (stages 1 and 3). We are fully invested and put our money to work for us, and we are fully invested when stocks are in their stage 2 uptrends.

But how can we use technical chart analysis to find stocks that are in a stable stage 2 uptrend?

Mark Minervini has developed the so-called 'trend template' for this purpose. This is an essential part of our JS-TechTrading pullback strategy. For our watchlists, only those individual values that meet the tough requirements of Minervini's trend template are eligible.

The Trend Template

• 200d MA increasing over a period of at least 1 month, better 4-5 months or longer

• 150d MA above 200d MA

• 50d MA above 150d MA and 200d MA

• Course above 50d MA, 150d MA and 200d MA

• Ideally, the 50d MA is increasing over at least 1 month

• Price at least 25% above the 52w low

• Price within 25% of 52w high

• High relative strength according to IBD.

NOTE: In this basic version of the script, the Trend-Template has to be used as a separate indicator on TradingView (Public Trend-Template indicators are available in TradingView – community scripts). It is recommended to only execute buy signals in case the stock or financial security is in a stage 2 uptrend, which means that the criteria of the trend-template are fulfilled.

This strategy can be applied to all timeframes from 5 min to daily.

The VWAP Momentum-Pullback Strateg y

For the JS-TechTrading VWAP Momentum-Pullback Strategy, only stocks and other financial instruments that meet the selected criteria of Mark Minervini's trend template are recommended for algorithmic trading with this startegy.

A further prerequisite for generating a buy signals is that the individual value is in a short-term oversold state (RSI).

When the selling pressure is over and the continuation of the uptrend can be confirmed by the MA / VWAP crossover after reaching a price low, a buy signal is issued by this strategy.

Stop-loss limits and profit targets can be set variably.

Relative Strength Index (RSI)

The Relative Strength Index (RSI) is a technical indicator developed by Welles Wilder in 1978. The RSI is used to perform a market value analysis and identify the strength of a trend as well as overbought and oversold conditions. The indicator is calculated on a scale from 0 to 100 and shows how much an asset has risen or fallen relative to its own price in recent periods.

The RSI is calculated as the ratio of average profits to average losses over a certain period of time. A high value of the RSI indicates an overbought situation, while a low value indicates an oversold situation. Typically, a value > 70 is considered an overbought threshold and a value < 30 is considered an oversold threshold. A value above 70 signals that a single value may be overvalued and a decrease in price is likely , while a value below 30 signals that a single value may be undervalued and an increase in price is likely.

For example, let's say you're watching a stock XYZ. After a prolonged falling movement, the RSI value of this stock has fallen to 26. This means that the stock is oversold and that it is time for a potential recovery. Therefore, a trader might decide to buy this stock in the hope that it will rise again soon.

The MA / VWAP Crossover Trading Strategy

This strategy combines two popular technical indicators: the Moving Average (MA) and the Volume Weighted Average Price (VWAP). The MA VWAP crossover strategy is used to identify potential trend reversals and entry/exit points in the market.

The VWAP is calculated by taking the average price of an asset for a given period, weighted by the volume traded at each price level. The MA, on the other hand, is calculated by taking the average price of an asset over a specified number of periods. When the MA crosses above the VWAP, it suggests that buying pressure is increasing, and it may be a good time to enter a long position. When the MA crosses below the VWAP, it suggests that selling pressure is increasing, and it may be a good time to exit a long position or enter a short position.

Traders typically use the MA VWAP crossover strategy in conjunction with other technical indicators and fundamental analysis to make more informed trading decisions. As with any trading strategy, it is important to carefully consider the risks and potential rewards before making any trades.

This strategy is applicable to all timeframes and the relevant parameters for the underlying indicators (RSI and MA/VWAP) can be adjusted and optimized as needed.

Backtesting

Backtesting gives outstanding results on all timeframes and drawdowns can be reduced to a minimum level. In this example, the hourly chart for MCFT has been used.

Settings for backtesting are:

- Period from April 2020 until April 2021 (1 yr)

- Starting capital 100k USD

- Position size = 25% of equity

- 0.01% commission = USD 2.50.- per Trade

- Slippage = 2 ticks

Other comments

• This strategy has been designed to identify the most promising, highest probability entries and trades for each stock or other financial security.

• The RSI qualifier is highly selective and filters out the most promising swing-trading entries. As a result, you will normally only find a low number of trades for each stock or other financial security per year in case you apply this strategy for the daily charts. Shorter timeframes will result in a higher number of trades / year.

• As a result, traders need to apply this strategy for a full watchlist rather than just one financial security.

Momentum Traffic LightScript was first published 30 May 2021 on twitter by @lehlutz

This script visualizes long, short and neutral phases of any asset class as follows:

The differences A, B, C are formed from 3 moving averages

(3-EMA exponential moving average, 20-SMA simple moving average and 50-SMA simple moving average)

namely

A: (3-EMA minus 20-SMA)

B: (3-EMA minus 50-SMA)

C: (20-SMA minus 50-SMA).

Then the following rules apply to the traffic light (where ∂ means slope).

green traffic light (bullish): (A>0,B>0,C>0), (A>0,B>0,∂C>0), (A>0,∂B>0,C>0) or (A>0,∂B>0,∂C>0, whereas ∂A>0)

red traffic light (bearish): (A<0,B<0,C<0, whereas at least ∂A or ∂B or ∂C is <0) or (A<0,B<0,∂C<0 whereas ∂A and ∂B<0);

yellow traffic light (neutral): all other

Indicator should not be considered as financial advice

Reinforced RSI - The Quant Science This strategy was designed and written with the goal of showing and motivating the community how to integrate our 'Probabilities' module with their own script.

We have recreated one of the simplest strategies used by many traders. The strategy only trades long and uses the overbought and oversold levels on the RSI indicator.

We added stop losses and take profits to offer more dynamism to the strategy. Then the 'Probabilities' module was integrated to create a probabilistic reinforcement on each trade.

Specifically, each trade is executed, only if the past probabilities of making a profitable trade is greater than or equal to 51%. This greatly increased the performance of the strategy by avoiding possible bad trades.

The backtesting was calculated on the NASDAQ:TSLA , on 15 minutes timeframe.

The strategy works on Tesla using the following parameters:

1. Lenght: 13

2. Oversold: 40

3. Overbought: 70

4. Lookback: 50

5. Take profit: 3%

6. Stop loss: 3%

Time period: January 2021 to date.

Our Probabilities Module, used in the strategy example:

Market Breadth: Trends & BreakoutsVisualize the percentage of stocks in an index participating in trends and breakouts/breakdowns.

The default data source is the S & P 500: the percent of stocks above/below the 200 and 50 day moving averages, and the percentage of stocks making new 52 week breakouts/breakdowns. You can pick new data sources in the settings.

The blue band represents the percentage of stocks above/below the 200 day moving average. (It's always 100% in width, unlike say Bollinger bands). The thin blue lines are the same but for the 50 day moving average. The red and green areas represent the percentage of stocks making new 52 week highs/lows.

In the example chart you can see a divergence between the market as a whole which continues up and to the right throughout 2021, where as fewer and fewer stocks were above their own 200 day moving average, causing the blue band to trend down. Before the market turns beginning 2022 you can see more stocks making new 52 week lows, even as other stocks make 52 week highs. After the market tops, the percentage of 52 week lows intensifies and the percentage of stocks below their 200 day moving average is already over 50%.

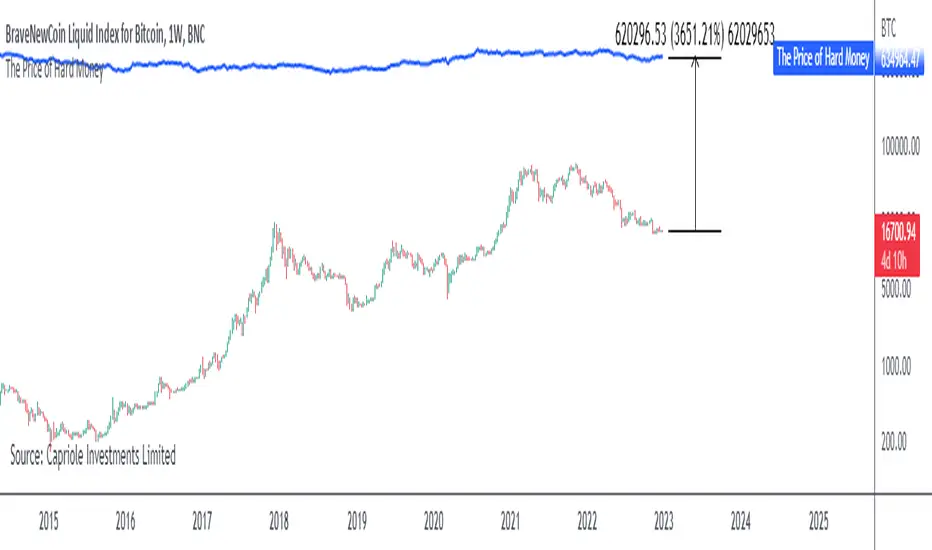

The Price of Hard MoneyIf we calculate “the price of hard money” (the market capitalization weighted price of gold plus Bitcoin); we get this chart.

Since 2017, Bitcoin’s share of hard money growth has been increasing, we can see it visibly on the gold chart by a widening delta between the price of hard money and the Gold price. We can also see some interesting technical behaviours.

In 2021, Hard Money broke out and held this breakout above the 2011 Gold high. Only later in 2022 did a correction of 20% occur – typical of Golds historic volatility in periods of inflation and high interest rates.

Hard Money is at major support and we have evidence for a fundamental shift in investor capital flows away from gold and into Bitcoin.

This Indicator is useful:

- To track the market capitalization of Gold (estimated), Bitcoin and combined market capitalization of Hard Money.

- To track the price action and respective change in investor flows from Gold to Bitcoin .

Provided Bitcoin continues to suck more value out of gold with time, this chart will be useful for tracking price action of the combined asset classes into the years to come.

Day Trading Booster by DGTTiming when day trading can be everything

In Stock markets typically more volatility (or price activity) occurs at market opening and closings

When it comes to Forex (foreign exchange market), the world’s most traded market, unlike other financial markets, there is no centralized marketplace, currencies trade over the counter in whatever market is open at that time, where time becomes of more importance and key to get better trading opportunities. There are four major forex trading sessions, which are Sydney , Tokyo , London and New York sessions

Forex market is traded 24 hours a day, 5 days a week across by banks, institutions and individual traders worldwide, but that doesn’t mean it’s always active the entire day. It may be very difficult time trying to make money when the market doesn’t move at all. The busiest times with highest trading volume occurs during the overlap of the London and New York trading sessions, because U.S. dollar (USD) and the Euro (EUR) are the two most popular currencies traded. Typically most of the trading activity for a specific currency pair will occur when the trading sessions of the individual currencies overlap. For example, Australian Dollar (AUD) and Japanese Yen (JPY) will experience a higher trading volume when both Sydney and Tokyo sessions are open

There is one influence that impacts Forex matkets and should not be forgotten : the release of the significant news and reports. When a major announcement is made regarding economic data, currency can lose or gain value within a matter of seconds

Cryptocurrency markets on the other hand remain open 24/7, even during public holidays

Until 2021, the Asian impact was so significant in Cryptocurrency markets but recent reasearch reports shows that those patterns have changed and the correlation with the U.S. trading hours is becoming a clear evolving trend.

Unlike any other market Crypto doesn’t rest on weekends, there’s a drop-off in participation and yet algorithmic trading bots and market makers (or liquidity providers) can create a high volume of activity. Never trust the weekend’ is a good thing to remind yourself

One more factor that needs to be taken into accout is Blockchain transaction fees, which are responsive to network congestion and can change dramatically from one hour to the next

In general, Cryptocurrency markets are highly volatile, which means that the price of a coin can change dramatically over a short time period in either direction

The Bottom Line

The more traders trading, the higher the trading volume, and the more active the market. The more active the market, the higher the liquidity (availability of counterparties at any given time to exit or enter a trade), hence the tighter the spreads (the difference between ask and bid price) and the less slippage (the difference between the expected fill price and the actual fill price) - in a nutshell, yield to many good trading opportunities and better order execution (a process of filling the requested buy or sell order)

The best time to trade is when the market is the most active and therefore has the largest trading volume, trading all day long will not only deplete a trader's reserves quickly, but it can burn out even the most persistent trader. Knowing when the markets are more active will give traders peace of mind, that opportunities are not slipping away when they take their eyes off the markets or need to get a few hours of sleep

What does the Day Trading Booster do?

Day Trading Booster is designed ;

- to assist in determining market peak times, the times where better trading opportunities may arise

- to assist in determining the probable trading opportunities

- to help traders create their own strategies. An example strategy of when to trade or not is presented below

For Forex markets specifically includes

- Opening channel of Asian session, Europien session or both

- Opening price, opening range (5m or 15m) and day (session) range of the major trading center sessions, including Frankfurt

- A tabular view of the major forex markets oppening/closing hours, with a countdown timer

- A graphical presentation of typically traded volume and various forext markets oppening/clossing events (not only the major markets but many other around the world)

For All type of markets Day Trading Booster plots

- Day (Session) Open, 5m, 15m or 1h Opening Range

- Day (Session) Referance Levels, based on Average True Range (ATR) or Previous Day (Session) Range (PH - PL)

- Week and Month Open

Day Trading Booster also includes some of the day trader's preffered indicaotrs, such as ;

- VWAP - A custom interpretaion of VWAP is presented here with Auto, Interactive and Manual anchoring options.

- Pivot High/Low detection - Another custom interpretation of Pivot Points High Low indicator.

- A Moving Average with option to choose among SMA, EMA, WMA and HMA

An example strategy - Channel Bearkout Strategy

When day trading a trader usually monitors/analyzes lower timeframe charts and from time to time may loose insight of what really happens on the market from higher time porspective. Do not to forget to look at the larger time frame (than the one chosen to trade with) which gives the bigger picture of market price movements and thus helps to clearly define the trend

Disclaimer : Trading success is all about following your trading strategy and the indicators should fit within your trading strategy, and not to be traded upon solely

The script is for informational and educational purposes only. Use of the script does not constitutes professional and/or financial advice. You alone the sole responsibility of evaluating the script output and risks associated with the use of the script. In exchange for using the script, you agree not to hold dgtrd TradingView user liable for any possible claim for damages arising from any decision you make based on use of the script

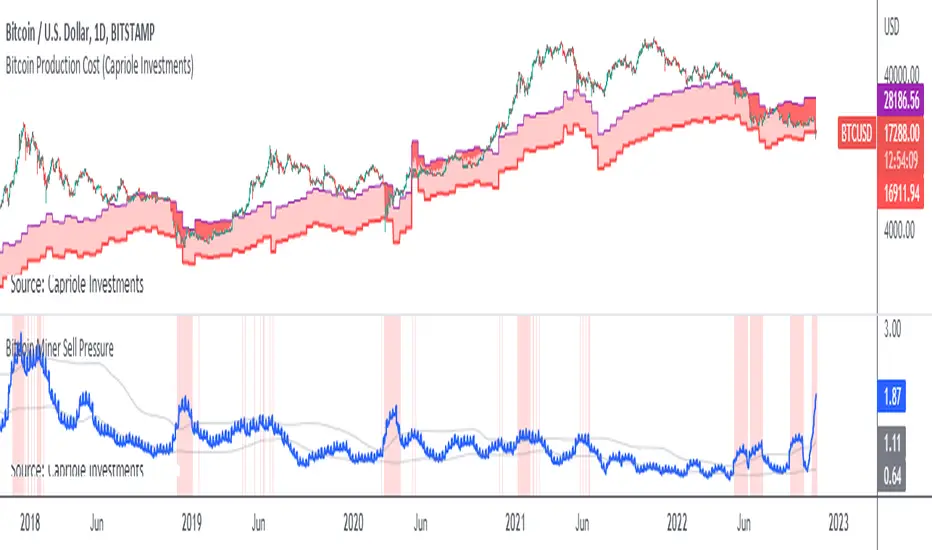

Bitcoin Miner Sell PressureBitcoin miners are in pain and now (November 2022) selling more than they have in almost 5 years!

Introducing: Bitcoin Miner Sell Pressure.

A free, open-source indicator which tracks on-chain data to highlight when Bitcoin miners are selling more of their reserves than usual.

The indicator tracks the ratio of on-chain miner Bitcoin outflows to miner Bitcoin reserves.

- Higher = more selling than usual

- Lower = less selling than usual

- Red = extraordinary sell pressure

Today , it's red.

What can we see now ?

Miners are not great at treasury management. They tend to sell most when they are losing money (like today). But there have been times when they sold well into high profit, such as into the 2017 $20K top and in early 2021 when Bitcoin breached $40K.

Bitcoin Miner Sell Pressure identifies industry stress, excess and miner capitulation.

Unsurprisingly, there is a high correlation with Bitcoin Production Cost; giving strong confluence to both.

In some instances, BMSP spots capitulation before Hash Ribbons. Such as today!

NetLiquidityLibraryLibrary "NetLiquidityLibrary"

The Net Liquidity Library provides daily values for net liquidity. Net liquidity is measured as Fed Balance Sheet - Treasury General Account - Reverse Repo. Time series for each individual component included too.

get_net_liquidity_for_date(t)

Function takes date in timestamp form and returns the Net Liquidity value for that date. If date is not present, 0 is returned.

Parameters:

t : The timestamp of the date you are requesting the Net Liquidity value for.

Returns: The Net Liquidity value for the specified date.

get_net_liquidity()

Gets the Net Liquidity time series from Dec. 2021 to current. Dates that are not present are represented as 0.

Returns: The Net Liquidity time series.

YOY[TV1]Year-to-year comparison is a popular and effective way to evaluate a company's financial performance and investment performance.

Any measurable event that repeats yearly can be compared based on YoY.

As a rule, the indicator YoY (year to year) is the number of percentages indicating an increase or regression in relation to the future or past period.

For example, you can compare WM2NS using the YOY (Year to Year) method.

The Offset argument sets the data comparison period. For daily, weekly and monthly timeframes, if Offset is set to 0, it will be determined automatically.

Сравнение Год к году - популярный и эффективный способ оценки финансовых показателей компании и эффективность инвестиций.

Любое измеримое событие, которое повторяется ежегодно можно сравнить на основе YoY.

Как правило, показателем YoY (year to year) является количество процентов указывающее на прирост или регресс по отношению к будущему или прошлому периоду.

Например, вы можете сравнить WM2NS (эмиссию доллара) с помощью метода YOY (Год к году).

Допустим, в 2021 году вы эмитировали А долларов, а в 2022 вы эмитировали Б долларов

Итак итоговой формулой будет: ((Б - А) / А) * 100

Аргумент Offset устанавливает период сравнения данных. Для дневного, недельного и месячного таймфрейма, если Offset установлен в 0, будет определен автоматически.

RSI Past Can Turn RSI Into a Directional ToolThe Relative Strength Index was created by J. Welles Wilder to measure overbought and oversold conditions. It’s also found popularity as an overall measure of direction because upward-trending stocks often hit overbought conditions. The opposite can be true with underperformers.

Today’s custom script, RSI Past, attempts to capture this secondary use of RSI as a directional indicator.

RSI Past achieves this by comparing how many bars have passed since RSI's most recent overbought and oversold readings. It then plots a simple difference between those two numbers.

Stocks with “bullish” signals will have positive readings that will increase each time RSI hits an overbought condition.

“Bearish” readings are just the opposite, growing more negative as oversold conditions occur.

An examination of some individual stocks may show the usefulness of this approach.

Meta Platforms , for example, hit an oversold condition almost exactly one year ago, and has remained under heavy selling pressure since:

Exxon Mobil , on the other hand, flipped to a bullish reading last October and has trended higher since:

This raises some interesting questions for Apple, shown on the main chart above. AAPL’s RSI Past has maintained a bullish reading for over a year -- unlike most other big technology stocks and the broader Nasdaq-100. Could this reflect bigger directional strength, especially with prices holding the $150 level that’s had relevance several times mid-2021?

TradeStation has, for decades, advanced the trading industry, providing access to stocks, options, futures and cryptocurrencies. See our Overview for more.

Important Information

TradeStation Securities, Inc., TradeStation Crypto, Inc., and TradeStation Technologies, Inc. are each wholly owned subsidiaries of TradeStation Group, Inc., all operating, and providing products and services, under the TradeStation brand and trademark. You Can Trade, Inc. is also a wholly owned subsidiary of TradeStation Group, Inc., operating under its own brand and trademarks. TradeStation Crypto, Inc. offers to self-directed investors and traders cryptocurrency brokerage services. It is neither licensed with the SEC or the CFTC nor is it a Member of NFA. When applying for, or purchasing, accounts, subscriptions, products, and services, it is important that you know which company you will be dealing with. Please click here for further important information explaining what this means.

This content is for informational and educational purposes only. This is not a recommendation regarding any investment or investment strategy. Any opinions expressed herein are those of the author and do not represent the views or opinions of TradeStation or any of its affiliates.

Investing involves risks. Past performance, whether actual or indicated by historical tests of strategies, is no guarantee of future performance or success. There is a possibility that you may sustain a loss equal to or greater than your entire investment regardless of which asset class you trade (equities, options, futures, or digital assets); therefore, you should not invest or risk money that you cannot afford to lose. Before trading any asset class, first read the relevant risk disclosure statements on the Important Documents page, found here: www.tradestation.com .

STD-Filtered, Variety FIR Digital Filters w/ ATR Bands [Loxx]STD-Filtered, Variety FIR Digital Filters w/ ATR Bands is a FIR Digital Filter indicator with ATR bands. This indicator contains 12 different digital filters. Some of these have already been covered by indicators that I've recently posted. The difference here is that this indicator has ATR bands, allows for frequency filtering, adds a frequency multiplier, and attempts show causality by lagging price input by 1/2 the period input during final application of weights. Period is restricted to even numbers.

The 3 most important parameters are the frequency cutoff, the filter window type and the "causal" parameter.

Included filter types:

- Hamming

- Hanning

- Blackman

- Blackman Harris

- Blackman Nutall

- Nutall

- Bartlet Zero End Points

- Bartlet Hann

- Hann

- Sine

- Lanczos

- Flat Top

Frequency cutoff can vary between 0 and 0.5. General rule is that the greater the cutoff is the "faster" the filter is, and the smaller the cutoff is the smoother the filter is.

You can read more about discrete-time signal processing and some of the windowing functions in this indicator here:

Window function

Window Functions and Their Applications in Signal Processing

What are FIR Filters?

In discrete-time signal processing, windowing is a preliminary signal shaping technique, usually applied to improve the appearance and usefulness of a subsequent Discrete Fourier Transform. Several window functions can be defined, based on a constant (rectangular window), B-splines, other polynomials, sinusoids, cosine-sums, adjustable, hybrid, and other types. The windowing operation consists of multipying the given sampled signal by the window function. For trading purposes, these FIR filters act as advanced weighted moving averages.

A finite impulse response (FIR) filter is a filter whose impulse response (or response to any finite length input) is of finite duration, because it settles to zero in finite time. This is in contrast to infinite impulse response (IIR) filters, which may have internal feedback and may continue to respond indefinitely (usually decaying).

The impulse response (that is, the output in response to a Kronecker delta input) of an Nth-order discrete-time FIR filter lasts exactly {\displaystyle N+1}N+1 samples (from first nonzero element through last nonzero element) before it then settles to zero.

FIR filters can be discrete-time or continuous-time, and digital or analog.

A FIR filter is (similar to, or) just a weighted moving average filter, where (unlike a typical equally weighted moving average filter) the weights of each delay tap are not constrained to be identical or even of the same sign. By changing various values in the array of weights (the impulse response, or time shifted and sampled version of the same), the frequency response of a FIR filter can be completely changed.

An FIR filter simply CONVOLVES the input time series (price data) with its IMPULSE RESPONSE. The impulse response is just a set of weights (or "coefficients") that multiply each data point. Then you just add up all the products and divide by the sum of the weights and that is it; e.g., for a 10-bar SMA you just add up 10 bars of price data (each multiplied by 1) and divide by 10. For a weighted-MA you add up the product of the price data with triangular-number weights and divide by the total weight.

What is a Standard Deviation Filter?

If price or output or both don't move more than the (standard deviation) * multiplier then the trend stays the previous bar trend. This will appear on the chart as "stepping" of the moving average line. This works similar to Super Trend or Parabolic SAR but is a more naive technique of filtering.

Included

Bar coloring

Loxx's Expanded Source Types

Signals

Alerts

Related indicators

STD/C-Filtered, N-Order Power-of-Cosine FIR Filter

STD/C-Filtered, Power-of-Cosine FIR Filter

STD/C-Filtered, Truncated Taylor Family FIR Filter

STD/Clutter-Filtered, Variety FIR Filters

STD/Clutter-Filtered, Kaiser Window FIR Digital Filter

Ehlers Linear Extrapolation Predictor [Loxx]Ehlers Linear Extrapolation Predictor is a new indicator by John Ehlers. The translation of this indicator into PineScript™ is a collaborative effort between @cheatcountry and I.

The following is an excerpt from "PREDICTION" , by John Ehlers

Niels Bohr said “Prediction is very difficult, especially if it’s about the future.”. Actually, prediction is pretty easy in the context of technical analysis. All you have to do is to assume the market will behave in the immediate future just as it has behaved in the immediate past. In this article we will explore several different techniques that put the philosophy into practice.

LINEAR EXTRAPOLATION

Linear extrapolation takes the philosophical approach quite literally. Linear extrapolation simply takes the difference of the last two bars and adds that difference to the value of the last bar to form the prediction for the next bar. The prediction is extended further into the future by taking the last predicted value as real data and repeating the process of adding the most recent difference to it. The process can be repeated over and over to extend the prediction even further.

Linear extrapolation is an FIR filter, meaning it depends only on the data input rather than on a previously computed value. Since the output of an FIR filter depends only on delayed input data, the resulting lag is somewhat like the delay of water coming out the end of a hose after it supplied at the input. Linear extrapolation has a negative group delay at the longer cycle periods of the spectrum, which means water comes out the end of the hose before it is applied at the input. Of course the analogy breaks down, but it is fun to think of it that way. As shown in Figure 1, the actual group delay varies across the spectrum. For frequency components less than .167 (i.e. a period of 6 bars) the group delay is negative, meaning the filter is predictive. However, the filter has a positive group delay for cycle components whose periods are shorter than 6 bars.

Figure 1

Here’s the practical ramification of the group delay: Suppose we are projecting the prediction 5 bars into the future. This is fine as long as the market is continued to trend up in the same direction. But, when we get a reversal, the prediction continues upward for 5 bars after the reversal. That is, the prediction fails just when you need it the most. An interesting phenomenon is that, regardless of how far the extrapolation extends into the future, the prediction will always cross the signal at the same spot along the time axis. The result is that the prediction will have an overshoot. The amplitude of the overshoot is a function of how far the extrapolation has been carried into the future.

But the overshoot gives us an opportunity to make a useful prediction at the cyclic turning point of band limited signals (i.e. oscillators having a zero mean). If we reduce the overshoot by reducing the gain of the prediction, we then also move the crossing of the prediction and the original signal into the future. Since the group delay varies across the spectrum, the effect will be less effective for the shorter cycles in the data. Nonetheless, the technique is effective for both discretionary trading and automated trading in the majority of cases.

EXPLORING THE CODE

Before we predict, we need to create a band limited indicator from which to make the prediction. I have selected a “roofing filter” consisting of a High Pass Filter followed by a Low Pass Filter. The tunable parameter of the High Pass Filter is HPPeriod. Think of it as a “stone wall filter” where cycle period components longer than HPPeriod are completely rejected and cycle period components shorter than HPPeriod are passed without attenuation. If HPPeriod is set to be a large number (e.g. 250) the indicator will tend to look more like a trending indicator. If HPPeriod is set to be a smaller number (e.g. 20) the indicator will look more like a cycling indicator. The Low Pass Filter is a Hann Windowed FIR filter whose tunable parameter is LPPeriod. Think of it as a “stone wall filter” where cycle period components shorter than LPPeriod are completely rejected and cycle period components longer than LPPeriod are passed without attenuation. The purpose of the Low Pass filter is to smooth the signal. Thus, the combination of these two filters forms a “roofing filter”, named Filt, that passes spectrum components between LPPeriod and HPPeriod.

Since working into the future is not allowed in EasyLanguage variables, we need to convert the Filt variable to the data array XX . The data array is first filled with real data out to “Length”. I selected Length = 10 simply to have a convenient starting point for the prediction. The next block of code is the prediction into the future. It is easiest to understand if we consider the case where count = 0. Then, in English, the next value of the data array is equal to the current value of the data array plus the difference between the current value and the previous value. That makes the prediction one bar into the future. The process is repeated for each value of count until predictions up to 10 bars in the future are contained in the data array. Next, the selected prediction is converted from the data array to the variable “Prediction”. Filt is plotted in Red and Prediction is plotted in yellow.

The Predict Extrapolation indicator is shown above for the Emini S&P Futures contract using the default input parameters. Filt is plotted in red and Predict is plotted in yellow. The crossings of the Predict and Filt lines provide reliable buy and sell timing signals. There is some overshoot for the shorter cycle periods, for example in February and March 2021, but the only effect is a late timing signal. Further reducing the gain and/or reducing the BarsFwd inputs would provide better timing signals during this period.

ADDITIONS

Loxx's Expanded source types:

Library for expanded source types:

Explanation for expanded source types:

Three different signal types: 1) Prediction/Filter crosses; 2) Prediction middle crosses; and, 3) Filter middle crosses.

Bar coloring to color trend.

Signals, both Long and Short.

Alerts, both Long and Short.

Bollinger Bands and RSI Short Selling (by Coinrule)The Bollinger Bands are among the most famous and widely used indicators. A Bollinger Band is a technical analysis tool defined by a set of trendlines plotted two standard deviations (positively and negatively) away from a simple moving average ( SMA ) of a security's price, but which can be adjusted to user preferences. They can suggest when an asset is oversold or overbought in the short term, thus provide the best time for buying and selling it.

The relative strength index ( RSI ) is a momentum indicator used in technical analysis . RSI measures the speed and magnitude of a security's recent price changes to evaluate overvalued or undervalued conditions in the price of that security. The RSI can do more than point to overbought and oversold securities. It can also indicate securities that may be primed for a trend reversal or corrective pullback in price. It can signal when to buy and sell. Traditionally, an RSI reading of 70 or above indicates an overbought situation. A reading of 30 or below indicates an oversold condition.

The short order is placed on assets that present strong momentum when it's more likely that it is about to decrease further. The rule strategy places and closes the order when the following conditions are met:

ENTRY

The closing price is greater than the upper standard deviation of the Bollinger Bands

The RSI is less than 70

EXIT

The trade is closed in profit when the RSI is less than 70

Upper standard deviation of the Bollinger Band is greater than the the closing price.

This strategy comes with a stop loss and a take profit, and as you can see by the results, it is well suited for a bear market.

This trade works very well with ETH (1h timeframe), AVA (4h timeframe), and SOL (3h timeframe) and is backtested from the 1 December 2021 to capture how this strategy would perform in a bear market.

To make the results more realistic, the strategy assumes each order to trade 30% of the available capital. A trading fee of 0.1% is taken into account. The fee is aligned to the base fee applied on Binance, which is the largest cryptocurrency exchange.

Weighted Harrell-Davis Quantile Estimator with AD Oscillatorxel_arjona

Licensing:

This work is licensed under a Attribution-NonCommercial-ShareAlike 4.0 International Copyright (c) 2021 ( CC BY-NC-SA 4.0)

Copyright's & Mentions:

The Gamma Functions & Beta Probability Density Functions C# implementations by the Math.NET Numerics, part of the Math.NET Project.

The Regularized Incomplete (Left) Beta Function C# implementation by the SAMTools, htslib project.

The Weighted Harrell-Davis Quantile estimator; C# & R implementations by Andrey Akinshin.

External PineScript code, methods, support & consultancy by @PineCoders staff with special mention for:

+ "ma sorter ('sort by array' example)- JD" by @Duyck.

+ Porting, mods, compilation and debugging for this script by @XeL_Arjona for the TradingView's @PineCoders community.

I made it an oscillator. Features include normalization, line display, and smoothing. :DDD Enjoy!

(Ive been wanting to do this for a while but I wanted to make the library first but you know what this was fun so there you go its here now)

Short Swing Bearish MACD Cross (By Coinrule)This strategy is oriented towards shorting during downside moves, whilst ensuring the asset is trading in a higher timeframe downtrend, and exiting after further downside.

This script can work well on coins you are planning to hodl for long-term and works especially well whilst using an automated bot that can execute your trades for you. It allows you to hedge your investment by allocating a % of your coins to trade with, whilst not risking your entire holding. This mitigates unrealised losses from hodling as it provides additional cash from the profits made. You can then choose to hodl this cash, or use it to reinvest when the market reaches attractive buying levels. Alternatively, you can use this when trading contracts on futures markets where there is no need to already own the underlying asset prior to shorting it.

ENTRY

This script utilises the MACD indicator accompanied by the Exponential Moving Average (EMA) 450 to enter trades. The MACD is a trend following momentum indicator and provides identification of short-term trend direction. In this variation it utilises the 11-period as the fast and 26-period as the slow length EMAs, with signal smoothing set at 9.

The EMA 450 is used as additional confirmation to prevent the script from shorting when price is above this long-term moving average. Once price is above the EMA 450 the script will not open any shorts - preventing the rule from attempting to short uptrends. Due to this, this strategy is ideal for setting and forgetting.

The script will enter trades based on two conditions:

1) When the MACD signals a bearish cross. This occurs when the EMA 11 crosses below the EMA 26 within the MACD signalling the start of a potential downtrend.

2) Price has closed below the EMA 450. Price closing below this long-term EMA signals that the asset is in a sustained downtrend. Price breaking above this could indicate a bullish strength in which shorting would not be profitable.

EXIT

This script utilises a set take-profit and stop-loss from the entry of the trade. The take profit is set at 8% and the stop loss of 4%, providing a risk reward ratio of 2. This indicates the script will be profitable if it has a win ratio greater than 33%.

Take-Profit Exit: -8% price decrease from entry price.

OR

Stop-Loss Exit: +4% price increase from entry price.

Based on backtesting results across a selection of assets, the 45-minute and 1-hour timeframes are the best for this strategy.

The strategy assumes each order is using 30% of the available coins to make the results more realistic and to simulate you only ran this strategy on 30% of your holdings. A trading fee of 0.1% is also taken into account and is aligned to the base fee applied on Binance.

The backtesting data was recorded from December 1st 2021, just as the market was beginning its downtrend. We therefore recommend analysing the market conditions prior to utilising this strategy as it operates best on weak coins during downtrends and bearish conditions, however the EMA 450 condition should mitigate entries during bullish market conditions.

Pi Cycle Bottom IndicatorBack in June 2021, I was able to find two moving averages that crossed when Bitcoin reached it's cycle bottom, similar to Philip Swift's Pi-Cycle Top indicator.

The moving average pair used here was the x0.475 multiple of the 471 MA and the 150 EMA ( EMA to take into account of short term volatility ).

I have a more in-depth analysis and explanation of my findings on my medium page .

Trader Dončić.

Jurik Composite Fractal Behavior (CFB) on EMA [Loxx]Jurik Composite Fractal Behavior (CFB) on EMA is an exponential moving average with adaptive price trend duration inputs. This purpose of this indicator is to introduce the formulas for the calculation Composite Fractal Behavior. As you can see from the chart above, price reacts wildly to shifts in volatility--smoothing out substantially while riding a volatility wave and cutting sharp corners when volatility drops. Notice the chop zone on BTC around August 2021, this was a time of extremely low relative volatility.

This indicator uses three previous indicators from my public scripts. These are:

JCFBaux Volatility

Jurik Filter

Jurik Volty

The CFB is also related to the following indicator

Jurik Velocity ("smoother moment")

Now let's dive in...

What is Composite Fractal Behavior (CFB)?

All around you mechanisms adjust themselves to their environment. From simple thermostats that react to air temperature to computer chips in modern cars that respond to changes in engine temperature, r.p.m.'s, torque, and throttle position. It was only a matter of time before fast desktop computers applied the mathematics of self-adjustment to systems that trade the financial markets.

Unlike basic systems with fixed formulas, an adaptive system adjusts its own equations. For example, start with a basic channel breakout system that uses the highest closing price of the last N bars as a threshold for detecting breakouts on the up side. An adaptive and improved version of this system would adjust N according to market conditions, such as momentum, price volatility or acceleration.

Since many systems are based directly or indirectly on cycles, another useful measure of market condition is the periodic length of a price chart's dominant cycle, (DC), that cycle with the greatest influence on price action.

The utility of this new DC measure was noted by author Murray Ruggiero in the January '96 issue of Futures Magazine. In it. Mr. Ruggiero used it to adaptive adjust the value of N in a channel breakout system. He then simulated trading 15 years of D-Mark futures in order to compare its performance to a similar system that had a fixed optimal value of N. The adaptive version produced 20% more profit!

This DC index utilized the popular MESA algorithm (a formulation by John Ehlers adapted from Burg's maximum entropy algorithm, MEM). Unfortunately, the DC approach is problematic when the market has no real dominant cycle momentum, because the mathematics will produce a value whether or not one actually exists! Therefore, we developed a proprietary indicator that does not presuppose the presence of market cycles. It's called CFB (Composite Fractal Behavior) and it works well whether or not the market is cyclic.

CFB examines price action for a particular fractal pattern, categorizes them by size, and then outputs a composite fractal size index. This index is smooth, timely and accurate

Essentially, CFB reveals the length of the market's trending action time frame. Long trending activity produces a large CFB index and short choppy action produces a small index value. Investors have found many applications for CFB which involve scaling other existing technical indicators adaptively, on a bar-to-bar basis.

What is Jurik Volty used in the Juirk Filter?

One of the lesser known qualities of Juirk smoothing is that the Jurik smoothing process is adaptive. "Jurik Volty" (a sort of market volatility ) is what makes Jurik smoothing adaptive. The Jurik Volty calculation can be used as both a standalone indicator and to smooth other indicators that you wish to make adaptive.

What is the Jurik Moving Average?

Have you noticed how moving averages add some lag (delay) to your signals? ... especially when price gaps up or down in a big move, and you are waiting for your moving average to catch up? Wait no more! JMA eliminates this problem forever and gives you the best of both worlds: low lag and smooth lines.

Ideally, you would like a filtered signal to be both smooth and lag-free. Lag causes delays in your trades, and increasing lag in your indicators typically result in lower profits. In other words, late comers get what's left on the table after the feast has already begun.

Modifications and improvements

1. Jurik's original calculation for CFB only allowed for depth lengths of 24, 48, 96, and 192. For theoretical purposes, this indicator allows for up to 20 different depth inputs to sample volatility. These depth lengths are

2, 3, 4, 6, 8, 12, 16, 24, 32, 48, 64, 96, 128, 192, 256, 384, 512, 768, 1024, 1536

Including these additional length inputs is arguable useless, but they are are included for completeness of the algorithm.

2. The result of the CFB calculation is forced to be an integer greater than or equal to 1.

3. The result of the CFB calculation is double filtered using an advanced, (and adaptive itself) filtering algorithm called the Jurik Filter. This filter and accompanying internal algorithm are discussed above.

Short Selling EMA Cross (By Coinrule)BINANCE:AVAXUSDT

This short selling script works best in periods of downtrends and general bearish market conditions, with the ultimate goal to sell as the the price decreases further and buy back before a rebound.

This script can work well on coins you are planning to hodl for long-term and works especially well whilst using an automated bot that can execute your trades for you. It allows you to hedge your investment by allocating a % of your coins to trade with, whilst not risking your entire holding. This mitigates unrealised losses from hodling as it provides additional cash from the profits made. You can then choose to to hodl this cash, or use it to reinvest when the market reaches attractive buying levels.

Entry

The exponential moving average ( EMA ) 20 and EMA 50 have been used for the variables determining the entry to the short. EMAs can operate better than simple moving averages due to the additional weighting placed on the most recent data points, whereas simple moving averages weight all the data the same. This means that price is tracked more closely and the most recent volatile moves can be captured and exploited more efficiently using EMAs.

Our backtesting data revealed that the most profitable timeframe was the 30-minute timeframe, this also enabled a good frequency of trades and high profitability.

A fast (shorter term) exponential moving average , in this strategy the EMA 20, crossing under a slow (longer term) moving average, in this example the EMA 50, signals the price of an asset has started to trend to the downside, as the most recent data signals price is declining compared to earlier data. The entry acts on this principle and executes when the EMA 20 crosses under the EMA 50.

Enter Short: EMA 20 crosses under EMA 50.

Exit

This script utilises a take profit and stop loss for the exit. The take profit is set at -8% and the stop loss is set at +16% from the entry price. This would normally be a poor trade due to the risk:reward equalling 0.5. However, when looking at the backtesting data, the high profitability of the strategy (93.33%) leads to increased confidence and showcases the high probability of success according to historical data.

The take profit (-8%) and the stop loss (+16%) of the strategy are widely placed to ensure the move is captured without being stopped out due to relief rallies. The stop loss also plays a role of mitigating losses and minimising risk of being stuck in a short position once there has been a fundamental trend reversal and the market has become bullish .

Exit Short: -8% price decrease from entry price.

OR

Exit Short: +16% price increase from entry price.

Tip: Research what coins have consistent and large token unlocks / highly inflationary tokenomics, and target these during bear markets to short as they will most likely have substantial selling pressure that outweighs demand - leading to declining prices.

The strategy assumes each order is using 30% of the available coins to make the results more realistic and to simulate you only ran this strategy on 30% of your holdings. A trading fee of 0.1% is also taken into account and is aligned to the base fee applied on Binance.

The backtesting data was recorded from December 1st 2021, just as the market was beginning its downtrend. We therefore recommend analysing the market conditions prior to utilising this strategy as it operates best on weak coins during downtrends and bearish conditions.

MTF Stochastic ScannerThis Stochastic scanner can be use to identify overbought and oversold of 10 symbols over multiple timeframes

it will give you a quick overview which pair is more overbough or more oversold and also signals tops and bottoms in the AVG row

light red/green cell = weak bearish (Stoch = 30-20) / bullish (Stoch = 70-80)

medium red/green cell = bearish (Stoch = 20-10) / bullish (Stoch = 80-90)

dark red/green cell = strong bearish (Stoch <= 10) / bullish (Stoch >= 90)

gray cell = neutral (Stoch = 30-70)

Usage

If AVG (average of all 4 timeframes) falls below 20, the cell will get green, indicating a good time to enter long (buy)

If AVG (average of all 4 timeframes) rises above 80, the cell will get red, indicating a good time to enter short (sell)

Use the "MTF Stochastic Scanner" in combination with the " MTF RSI Scanner "

to find tops (RSI MTF avg >=70 AND Stochastic MTF avg >= 80)

or bottoms (RSI MTF avg <= 30 AND Stochastic MTF avg <= 20)

Here is how the two MTF scanners looked on Nov 08 2021 (ATH) »

and here how the MTF scanners looked on June 21 2022

use TradingViews Replay function to check how it would have worked in the past and when not.

As always… there NOT a single indicator that can show to the top & bottom 100% every single time. So use with caution, with other indicators and/or deeper understanding of technicals analysis ☝️☝️☝️

Settings

You can change the timeframes, symbols, Stochastic settings, overbought/oversold levels and colors to your liking

Drag the table onto the price chart, if you want to use it as an overlay.

NOTE:

Because of the 4x10 security requests, it can take up to 1 minute for changed settings to take effect! Please be patient 🙃

If you have any idea on how to optimise the code, please feel free to share 🙏

*** Inspired by "Binance CHOP Dashboard" from @Cazimiro and "RSI MTF Table" from @mobester16 ***

MTF RSI ScannerThis RSI scanner can be use to identify the relative strength of 10 symbols over multiple timeframes

it will give you a quick overview which pair is more bearish or more bullish and also signals tops and bottoms in the AVG row

light red/green cell = weak bearish (RSI = 45-35) / bullish (RSI = 55-65)

medium red/green cell = bearish (RSI = 35-25) / bullish (RSI = 65-75)

dark red/green cell = strong bearish (RSI <= 25) / bullish (RSI >= 75)

gray cell = neutral (RSI= 45-55)

Usage

If AVG (average of all 4 timeframes) falls below 30, the cell will get green, indicating a good time to enter long (buy)

If AVG (average of all 4 timeframes) rises above 70, the cell will get red, indicating a good time to enter short (sell)

Use the "MTF RSI Scanner" in combination with the "MTF Stochastic Scanner"

to find tops (RSI MTF avg >=70 AND Stochastic MTF avg >= 80)

or bottoms (RSI MTF avg <= 30 AND Stochastic MTF avg <= 20)

Here is how the two MTF scanners looked on Nov 08 2021 (ATH) »

and here how the MTF scanners looked on June 21 2022

use TradingViews Replay function to check how it would have worked in the past and when not.

As always… there NOT a single indicator that can show to the top & bottom 100% every single time. So use with caution, with other indicators and/or deeper understanding of technicals analysis ☝️☝️☝️

Settings

You can change the timeframes, symbols, RSI settings, overbought/oversold levels and colors to your liking

Drag the table onto the price chart, if you want to use it as an overlay.

NOTE:

Because of the 4x10 security requests, it can take up to 1 minute for changed settings to take effect! Please be patient 🙃

If you have any idea on how to optimise the code, please feel free to share 🙏

*** Inspired by "Binance CHOP Dashboard" from @Cazimiro and "RSI MTF Table" from @mobester16 ***

[GarufiCommunity] Multi Indicator: VWAPs, MA, Pivot PointsThis script provides a collection of indicators to help traders look at multiple trends while maintaining a consistent configuration, even when jumping around different timeframes and symbols.

Additionally, this collection is particularly useful when trading decisions involve looking at dozens of indicators and analyzing, in aggregate, their confluence.

With this collection of indicators you can configure anchored VWAPs, MA, and Pivot Points:

- Anchored VWAPs: For each you define a fixed time and date to anchor it in the graph, and it stays consistent even when you change the symbol. An example use case can be setting one of the VWAPs to always start on the first candle on January 1st 2021, and a second VWAP a decade prior, so you don’t need to keep manually adjusting/adding VWAPs to the graph. At the moment you can define up to 4 anchored VWAPs.

- MA and Pivot Points: For each you can set independent timeframes, periods, and types, while using a single configuration panel. This helps reduce the amount of clicking needed when trying different configurations, such as testing different MA and Pivot periods and comparing how each behave in the graph (this personally helps me build trust in indicators). Permits use of up to 3 MAs and 2 Pivot Points.

Lastly, this script leverages and reuses modified code from the sources below:

- Médias e Tempos-v.2.1 by VeraLucia (with permission);

- Multiple Anchored VWAP v1.0 by GuilhermeNogueira (with permission);

- Pivot Point by TradingView.

TASC 2022.04 S&P500 Hybrid Seasonal System█ OVERVIEW

TASC's April 2022 edition of Traders' Tips includes the "Sell In May? Stock Market Seasonality" article authored by Markos Katsanos. This is the code implementing the "Hybrid Seasonal System" from the article.

█ CONCEPTS

In his article, Markos Katsanos takes an updated look at the "Sell in May" adage by reviewing recent historical data for seasonal equity market tendencies. The author explores the development of a trading strategy (a set of buy and sell rules) based on this research.

He starts from the enhanced buy & hold system featured in his July 2021 TASC article, and adds additional technical conditions. These include volatility conditions ( VIX and ATR ) plus the "Volume Flow Indicator" (VFI), which is a custom money flow indicator that Katsanos introduced in his June 2004 TASC article. He provides an example of a trading system that others can test for themselves and modify as they see fit. The author notes that the system could likely be improved further by adding money management conditions (such as a stop-loss), or by adding more technical conditions not considered in the scope of this article.

█ CALCULATIONS

The entry and exit rules that constitute the trading system are defined below. The critical values of VIX, ATR and VFI (specified below) used in the calculations were determined by optimization for a daily chart of the SPY ETF . By default, the strategy only allows long entries. However, the script offers the possibility to initiate short entries upon exiting long trades through the "Long Only" toggle in the script's inputs.

Long Entry Rules

• Seasonal: The seasonal trade is initiated on the first business day October at the open.

• Volatility: In case of high volatility, that is if the VIX is above 60% or the 15-day ATR was above 90% over the past 25 days, the seasonal trade is deferred until later in the month or year, when the volatility subsides.

Exit/Short Entry Rules

• Seasonal: The exit/short signal is triggered on the first business day of August at the open.

• Volatility: The exit/short signal is triggered if VIX is above 120 % (i.e. 2 times the corresponding threshold parameter).

• Money flow (VFI): The exit/short signal is triggered if the VFI crosses under a critical value (-20) while its 10-day moving average is pointing down.

Join TradingView!