SMT Divergences [OutOfOptions]Smart Money Technique (SMT) Divergence is designed to identify discrepancies between correlated assets within the same timeframe. It occurs when two related assets exhibit opposing signals, such as one forming a higher low while the other forms a lower low. This technique is particularly useful for anticipating market shifts or reversals before they become evident through other Premium Discount (PD) Arrays.

This indicator works by identifying the highs and lows that have formed for an asset on the current chart and the correlated symbol defined in the settings. Once a pivot on either asset is formed, it checks if the pivot has taken liquidity as identified by the previous pivot in the same direction (i.e., a new high taking out a previous high). If this is the case and the corresponding asset has not taken a similar pivot, the condition is determined to be a potential valid divergence. The indicator will then filter out SMTs formed by adjacent candles, requiring at least one candle difference between the candles forming the SMT.

If the “Candle Direction Validation” setting is enabled, the indicator will further check both assets to ensure that for bullish SMTs, the last high on both assets was formed by down candle, and for bearish SMTs, the low was formed by an up candle. This check can often eliminate low-probability SMTs that are frequently broken.

The referenced chart shows divergence between Nasdaq (NQ) and S&P 500 (ES) futures, which are normally closely correlated assets that move in the same direction. The lines shown represent bullish and bearish divergences between the two when they are formed. As you can see from the chart, SMT Divergences may not always indicate a reversal, or a reversal might be just a short-term retrace. Therefore, SMT Divergences should not be used independently. However, in conjunction with other PD arrays, they can provide strong confirmation of a change in market direction.

Configurability:

Pivot strength - Indicates how many bars to the left/right of a high for pivot to be considered, recommended to keep at 1 for maximum detection speed

Candle Direction Validation - Additional SMT validation to filter out weak/low-probability SMTs be examining candle direction

Line Styling for Bullish/Bearish SMTs - Ability to customize line style, color & width for bullish/bearish SMTs

Label Control - Whether or not to show SMT label and if shown what font size & color should be used

What makes this indicator different:

Unlike other SMT indicators, this indicators has additional built-in controls to remove low-probability SMTs

Cerca negli script per "摩根标普500指数基金的收益如何"

Financial Crisis Predictor - Doomsday ClockThe **Financial Crisis Predictor - Doomsday Clock** is a composite indicator that evaluates multiple market conditions to determine financial risk levels. It combines four key metrics: market volatility (via VIX), yield curve spread, stock market momentum, and credit risk (via high-yield spread). Each metric contributes to a weighted "risk score," scaled between 0 and 100, which helps gauge the probability of a financial crisis. Here's a breakdown of how it works:

### 1. **Market Volatility (VIX)**

- **How it's measured:**

- Uses the VIX index, which represents expected market volatility.

- Applies two exponential moving averages (EMAs) to smooth out the data—one fast and one slow.

- Triggers a signal if the fast EMA crosses above the slow EMA and VIX exceeds a defined threshold (default is 30).

- **Weighting:**

- Contributes up to 35% of the total risk score when active.

### 2. **Yield Curve Spread**

- **How it's measured:**

- Takes the difference between the yields of 10-year and 2-year U.S. Treasury bonds (inversion indicates recession risk).

- If the spread drops below a certain threshold (default is 0.2), it signals a potential recession.

- **Weighting:**

- Contributes up to 25% of the risk score.

### 3. **Stock Market Momentum**

- **How it's measured:**

- Analyzes the S&P 500 (SPY) using a 20-day EMA for price momentum.

- Checks for a cross under the 20-day EMA and if the 5-day rate of change (ROC) is less than -2.

- This combination signals bearish market momentum.

- **Weighting:**

- Contributes up to 20% of the risk score.

### 4. **Credit Risk (High Yield Spread)**

- **How it's measured:**

- Assesses high-yield corporate bond spreads using EMAs, similar to the VIX logic.

- A crossover of the fast EMA above the slow EMA combined with spreads exceeding a defined threshold (default is 5.0) indicates increased credit risk.

- **Weighting:**

- Contributes up to 20% of the total risk score.

### 5. **Risk Score Calculation**

- The final **risk score** ranges from 0 to 100 and is calculated using the weighted sum of the four indicators.

- The score is smoothed to minimize false signals and maintain stability.

### 6. **Risk Zones**

- **Extreme Risk:** If the risk score is ≥ 75, indicating a severe crisis warning.

- **High Risk:** If the risk score is between 15 and 75, signaling heightened risk.

- **Moderate Risk:** If the risk score is between 10 and 15, representing potential concerns.

- **Low Risk:** If the risk score is < 10, suggesting stable conditions.

### 7. **Visual & Alerts**

- The indicator plots the risk score on a chart with color-coded backgrounds to indicate risk levels: green (low), yellow (moderate), orange (high), and red (extreme).

- Alert conditions are set for each risk zone, notifying users when the risk level transitions into a higher zone.

This indicator aims to quickly detect potential financial crises by aggregating signals from key market factors, making it a versatile tool for traders, analysts, and risk managers.

Williams %R StrategyThe Williams %R Strategy implemented in Pine Script™ is a trading system based on the Williams %R momentum oscillator. The Williams %R indicator, developed by Larry Williams in 1973, is designed to identify overbought and oversold conditions in a market, helping traders time their entries and exits effectively (Williams, 1979). This particular strategy aims to capitalize on short-term price reversals in the S&P 500 (SPY) by identifying extreme values in the Williams %R indicator and using them as trading signals.

Strategy Rules:

Entry Signal:

A long position is entered when the Williams %R value falls below -90, indicating an oversold condition. This threshold suggests that the market may be near a short-term bottom, and prices are likely to reverse or rebound in the short term (Murphy, 1999).

Exit Signal:

The long position is exited when:

The current close price is higher than the previous day’s high, or

The Williams %R indicator rises above -30, indicating that the market is no longer oversold and may be approaching an overbought condition (Wilder, 1978).

Technical Analysis and Rationale:

The Williams %R is a momentum oscillator that measures the level of the close relative to the high-low range over a specific period, providing insight into whether an asset is trading near its highs or lows. The indicator values range from -100 (most oversold) to 0 (most overbought). When the value falls below -90, it indicates an oversold condition where a reversal is likely (Achelis, 2000). This strategy uses this oversold threshold as a signal to initiate long positions, betting on mean reversion—an established principle in financial markets where prices tend to revert to their historical averages (Jegadeesh & Titman, 1993).

Optimization and Performance:

The strategy allows for an adjustable lookback period (between 2 and 25 days) to determine the range used in the Williams %R calculation. Empirical tests show that shorter lookback periods (e.g., 2 days) yield the most favorable outcomes, with profit factors exceeding 2. This finding aligns with studies suggesting that shorter timeframes can effectively capture short-term momentum reversals (Fama, 1970; Jegadeesh & Titman, 1993).

Scientific Context:

Mean Reversion Theory: The strategy’s core relies on mean reversion, which suggests that prices fluctuate around a mean or average value. Research shows that such strategies, particularly those using oscillators like Williams %R, can exploit these temporary deviations (Poterba & Summers, 1988).

Behavioral Finance: The overbought and oversold conditions identified by Williams %R align with psychological factors influencing trading behavior, such as herding and panic selling, which often create opportunities for price reversals (Shiller, 2003).

Conclusion:

This Williams %R-based strategy utilizes a well-established momentum oscillator to time entries and exits in the S&P 500. By targeting extreme oversold conditions and exiting when these conditions revert or exceed historical ranges, the strategy aims to capture short-term gains. Scientific evidence supports the effectiveness of short-term mean reversion strategies, particularly when using indicators sensitive to momentum shifts.

References:

Achelis, S. B. (2000). Technical Analysis from A to Z. McGraw Hill.

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. The Journal of Finance, 25(2), 383-417.

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. The Journal of Finance, 48(1), 65-91.

Murphy, J. J. (1999). Technical Analysis of the Financial Markets: A Comprehensive Guide to Trading Methods and Applications. New York Institute of Finance.

Poterba, J. M., & Summers, L. H. (1988). Mean Reversion in Stock Prices: Evidence and Implications. Journal of Financial Economics, 22(1), 27-59.

Shiller, R. J. (2003). From Efficient Markets Theory to Behavioral Finance. Journal of Economic Perspectives, 17(1), 83-104.

Williams, L. (1979). How I Made One Million Dollars… Last Year… Trading Commodities. Windsor Books.

Wilder, J. W. (1978). New Concepts in Technical Trading Systems. Trend Research.

This explanation provides a scientific and evidence-based perspective on the Williams %R trading strategy, aligning it with fundamental principles in technical analysis and behavioral finance.

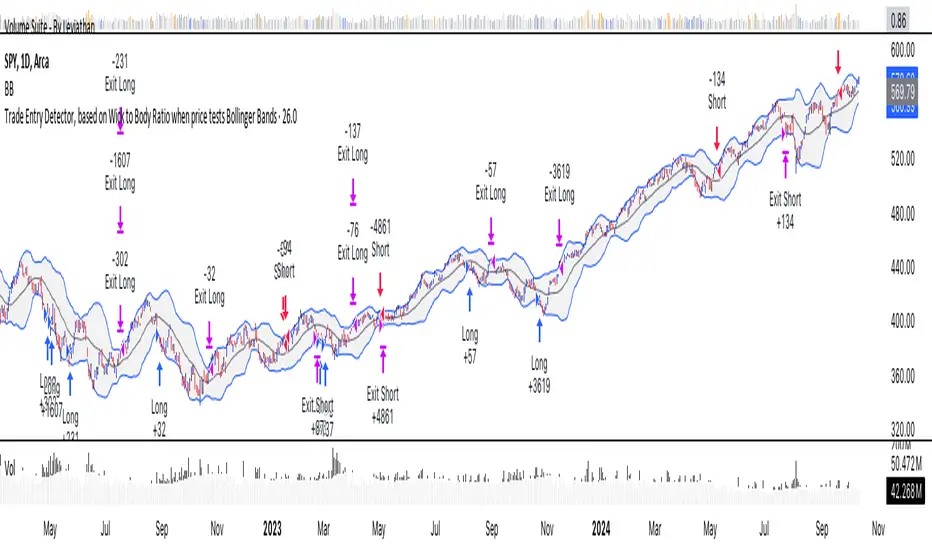

Trade Entry Detector, Wick to Body Ratio Trade Entry Detector: Wick-to-Body Ratio Strategy with Bollinger Bands

Overview

The Trade Entry Detector is a custom strategy for TradingView that leverages the Bollinger Bands and a unique wick-to-body ratio approach to capture precise entry opportunities. This indicator is designed for traders who want to pinpoint high-probability reversal points when price interacts with Bollinger Bands, all while offering flexible entry fill options.

The strategy performs primary analysis on the daily time frame, regardless of your current chart setting, allowing you to view daily Bollinger Band levels and entry signals even on lower time frames. This approach is suitable for swing traders and short-term traders looking to align intraday moves with higher time frame signals.

How the Strategy Works

1. Bollinger Band Analysis on the Daily Time Frame

Bollinger Bands are calculated using a 20-period simple moving average (SMA) and a standard deviation multiplier (default is 2). These bands dynamically expand and contract based on market volatility, making them ideal for identifying overbought and oversold conditions:

* Upper Band: Indicates potential overbought levels.

* Lower Band: Indicates potential oversold levels.

2. Wick-to-Body Ratio Condition

This strategy places significant emphasis on candle wicks relative to the candle body. Here’s why:

* A large upper wick relative to the body signals potential selling pressure after testing the upper Bollinger Band.

* A large lower wick relative to the body indicates buying support after testing the lower Bollinger Band.

* Ratio Threshold: You can set a minimum wick-to-body ratio (default is 1.0), meaning that the wick must be at least equal in size to the body. This ensures only candles with significant reversals are considered for entry.

3. Flexible Entry Timing

To adapt to various trading styles, the indicator allows you to choose the entry fill timing:

* Daily Close: Enter at the close of the daily candle.

* Daily Open: Enter at the open of the following daily candle.

* HOD (High of Day): Set entry at the daily high, for those who want confirmation of upward momentum.

* LOD (Low of Day): Set entry at the daily low, ideal for confirming downward movement.

4. Position Sizing and Risk Management

The strategy calculates position size based on a fixed risk percentage of your account balance (default is 1%). This approach dynamically adjusts position sizes based on stop-loss distance:

* Stop Loss: Placed at the nearest swing high (for shorts) or swing low (for longs).

* Take Profit: Exits are triggered when the price reaches the opposite Bollinger Band.

5. Order Expiration

Each pending order (long or short) expires after two days if unfilled, allowing for new setups on subsequent candles if conditions are met again.

Using the Trade Entry Detector

Step-by-Step Guide

1. Set the Primary Time Frame

The core calculations run on the daily time frame, but the strategy can be applied to intraday charts (e.g., 65-minute or 15-minute) for deeper insights.

2. Adjust Bollinger Band Settings

* Length: Default is 20, which determines the period for calculating the moving average.

* Standard Deviation Multiplier: Default is 2.0, which sets the width of the bands. Adjusting this can help you capture broader or tighter volatility ranges.

3. Define the Wick-to-Body Ratio

Set the minimum ratio between wick and body (default 1.0). Higher values filter out candles with less wick-to-body contrast, focusing on stronger rejection moves.

4. Choose Entry Fill Timing

Select your preferred fill condition:

* Daily Close: Confirms the trade at the end of the daily session.

* Daily Open: Executes the entry at the open of the next day.

* HOD/LOD: Uses the daily high or low as an additional confirmation for upward or downward moves.

5. Position Sizing and Risk Management

* Set your account balance and risk percentage. The strategy automatically calculates position sizes based on the stop distance to manage risk efficiently.

* Stop Loss and Take Profit points are automatically set based on swing highs/lows and opposing Bollinger Bands, respectively.

Practical Example

Let’s say SPY (S&P 500 ETF) tests the lower Bollinger Band on the daily time frame, with a lower wick that is twice the size of the body (meeting the 1.0 ratio threshold). Here’s how the strategy might proceed:

1. Signal: The lower wick on SPY suggests buying interest at the lower Bollinger Band.

2. Entry Fill Timing: If you’ve selected "Daily Open," the entry order will be placed at the next day's open price.

3. Stop Loss: Positioned at the nearest daily swing low to minimize risk.

4. Take Profit: If SPY price moves up and reaches the upper Bollinger Band, the position is automatically closed.

Indicator Features and Benefits

* Multi-Time Frame Compatibility: Perform daily analysis while tracking signals on any intraday chart.

* Automatic Position Sizing: Tailor risk per trade based on account balance and desired risk percentage.

* Flexible Entry Options: Choose from close, open, HOD, or LOD for optimal timing.

* Effective Trend Reversal Identification: Uses wick-to-body ratio and Bollinger Band interaction to pinpoint potential reversals.

* Dynamic Visualization: Bollinger Bands are displayed on your chosen time frame, allowing seamless intraday tracking.

Summary

The Trade Entry Detector provides a unique, data-driven way to spot reversal points with customizable entry options. By combining Bollinger Bands with wick-to-body ratio conditions, it identifies potential trade setups where price has tested extremes and shown reversal signals. With its flexible entry timing, risk management features, and multi-time frame compatibility, this indicator is ideal for traders looking to blend daily market context with shorter-term execution.

Tips for Usage:

* For swing trading, consider the Daily Open or Close entry options.

* For momentum entries, HOD or LOD may offer better alignment with the direction of the wick.

* Backtest on different assets to find optimal Bollinger Band and wick-to-body settings for your market.

Use this indicator to enhance your understanding of price behavior at key levels and improve the precision of your entry points. Happy trading!

Simple RSI stock Strategy [1D] The "Simple RSI Stock Strategy " is designed to long-term traders. Strategy uses a daily time frame to capitalize on signals generated by the Relative Strength Index (RSI) and the Simple Moving Average (SMA). This strategy is suitable for low-leverage trading environments and focuses on identifying potential buy opportunities when the market is oversold, while incorporating strong risk management with both dynamic and static Stop Loss mechanisms.

This strategy is recommended for use with a relatively small amount of capital and is best applied by diversifying across multiple stocks in a strong uptrend, particularly in the S&P 500 stock market. It is specifically designed for equities, and may not perform well in other markets such as commodities, forex, or cryptocurrencies, where different market dynamics and volatility patterns apply.

Indicators Used in the Strategy:

1. RSI (Relative Strength Index):

- The RSI is a momentum oscillator used to identify overbought and oversold conditions in the market.

- This strategy enters long positions when the RSI drops below the oversold level (default: 30), indicating a potential buying opportunity.

- It focuses on oversold conditions but uses a filter (SMA 200) to ensure trades are only made in the context of an overall uptrend.

2. SMA 200 (Simple Moving Average):

- The 200-period SMA serves as a trend filter, ensuring that trades are only executed when the price is above the SMA, signaling a bullish market.

- This filter helps to avoid entering trades in a downtrend, thereby reducing the risk of holding positions in a declining market.

3. ATR (Average True Range):

- The ATR is used to measure market volatility and is instrumental in setting the Stop Loss.

- By multiplying the ATR value by a custom multiplier (default: 1.5), the strategy dynamically adjusts the Stop Loss level based on market volatility, allowing for flexibility in risk management.

How the Strategy Works:

Entry Signals:

The strategy opens long positions when RSI indicates that the market is oversold (below 30), and the price is above the 200-period SMA. This ensures that the strategy buys into potential market bottoms within the context of a long-term uptrend.

Take Profit Levels:

The strategy defines three distinct Take Profit (TP) levels:

TP 1: A 5% from the entry price.

TP 2: A 10% from the entry price.

TP 3: A 15% from the entry price.

As each TP level is reached, the strategy closes portions of the position to secure profits: 33% of the position is closed at TP 1, 66% at TP 2, and 100% at TP 3.

Visualizing Target Points:

The strategy provides visual feedback by plotting plotshapes at each Take Profit level (TP 1, TP 2, TP 3). This allows traders to easily see the target profit levels on the chart, making it easier to monitor and manage positions as they approach key profit-taking areas.

Stop Loss Mechanism:

The strategy uses a dual Stop Loss system to effectively manage risk:

ATR Trailing Stop: This dynamic Stop Loss adjusts based on the ATR value and trails the price as the position moves in the trader’s favor. If a price reversal occurs and the market begins to trend downward, the trailing stop closes the position, locking in gains or minimizing losses.

Basic Stop Loss: Additionally, a fixed Stop Loss is set at 25%, limiting potential losses. This basic Stop Loss serves as a safeguard, automatically closing the position if the price drops 25% from the entry point. This higher Stop Loss is designed specifically for low-leverage trading, allowing more room for market fluctuations without prematurely closing positions.

to determine the level of stop loss and target point I used a piece of code by RafaelZioni, here is the script from which a piece of code was taken

Together, these mechanisms ensure that the strategy dynamically manages risk while offering robust protection against significant losses in case of sharp market downturns.

The position size has been estimated by me at 75% of the total capital. For optimal capital allocation, a recommended value based on the Kelly Criterion, which is calculated to be 59.13% of the total capital per trade, can also be considered.

Enjoy !

Trend Following Regression CloudTrend Following Regression Cloud Indicator

The Trend Following Regression Cloud is a versatile trading tool designed to help you effortlessly identify the market's prevailing trend. By analyzing price movements over multiple time frames, it provides a clear visual representation of whether the market is trending upwards or downwards.

How It Works:

- Adaptive Analysis: The indicator calculates linear regression lines over various periods ranging from short-term to long-term (e.g., 10, 20, 50, up to 500 periods). This means it adapts quickly to recent market changes, capturing new trends as they develop.

- Noise Reduction: By comparing and weighting the slopes of these regression lines, it filters out insignificant price fluctuations (market noise). This ensures that the signals you receive are more reliable and less prone to false alarms.

- Cloud Calculation: The cloud is generated by first calculating the slopes of multiple linear regression lines over different lengths. The differences between the slopes of shorter-term and longer-term regressions are then computed and weighted by their respective lengths. By summing up these weighted differences, the indicator produces a "total distance" value. This value is applied to a baseline (such as a 100-period simple moving average) to create the cloud line. The area between the baseline and the cloud line is filled, and its color changes based on whether the total distance is positive or negative, providing a visual cue of the market's trend direction.

- Visual Representation: The indicator plots two lines—a base line and a cloud line—creating a shaded area (the "cloud") between them. The color of this cloud changes based on market conditions:

- Green Cloud: Indicates that short-term trends are stronger than long-term trends, suggesting an upward market movement. This could be a good time to consider buying.

- Red Cloud: Signifies that the market may be trending downwards, as long-term trends overpower short-term ones. This could be an opportune moment to consider selling.

Enhanced Economic Composite with Dynamic WeightEnhanced Economic Composite with Dynamic Weight

Overview of the Indicator :

The "Enhanced Economic Composite with Dynamic Weight" is a comprehensive tool that combines multiple economic indicators, technical signals, and dynamic weighting to provide insights into market and economic health. It adjusts based on current volatility and recession risk, offering a detailed view of market conditions.

What This Indicator Does :

Tracks Economic Health: Uses key economic and market indicators to assess overall market conditions.

Dynamic Weighting: Adjusts the importance of components like stock indices, gold, and bonds based on volatility (VIX) and yield curve inversion.

Technical Signals: Identifies market momentum shifts through key crossovers like the Golden Cross, Death Cross, Silver Cross, and Hospice Cross.

Recession Shading: Marks known recessions for historical context.

Economic Factors Considered :

TIP (Treasury Inflation-Protected Securities): Reflects inflation expectations.

Gold: A safe-haven asset, increases in weight during volatility or rising momentum.

US Dollar Index (DXY): Measures USD strength, fixed weight of 10%, smoothed with EMA.

Commodities (DBC): Indicates global demand; weight increases with momentum or volatility.

Volatility Index (VIX): Reflects market risk, inversely related to market confidence.

Stock Indices (S&P 500, DJIA, NASDAQ, Russell 2000): Represent market performance, with weights reduced during high volatility or negative yield spread.

Yield Spread (10Y - 2Y Treasuries): Predicts recessions; negative spread reduces stock weighting.

Credit Spread (HYG - TLT): Indicates market risk through corporate vs. government bond yields.

How and Why Factors are Weighted:

Stock Indices get more weight in stable markets (low VIX, positive yield spread), while safe-haven assets like gold and bonds gain weight in volatile markets or during yield curve inversions. This dynamic adjustment ensures the composite reflects current market sentiment.

Technical Signals:

Golden Cross: 50 EMA crossing above 200 SMA, signaling bullish momentum.

Death Cross: 50 EMA below 200 SMA, indicating bearish momentum.

Silver Cross: 21 EMA crossing above 50 EMA, plotted only if below the 200-day SMA, signaling potential upside in downtrend conditions.

Hospice Cross: 50 EMA crosses below 21 EMA, plotted only if 21 EMA is below 200 SMA, a leading bearish signal.

Recession Shading:

Recession periods like the Great Recession, Early 2000s Recession, and COVID-19 Recession are shaded to provide historical context.

Benefits of Using This Indicator:

Comprehensive Analysis: Combines economic fundamentals and technical analysis for a full market view.

Dynamic Risk Adjustment: Weights shift between growth and safe-haven assets based on volatility and recession risk.

Early Signals: The Silver Cross and Hospice Cross provide early warnings of potential market shifts.

Recession Forecasting: Helps predict downturns through the yield curve and recession indicators.

Who Can Benefit:

Traders: Identify market momentum shifts early through crossovers.

Long-term Investors: Use recession warnings and dynamic adjustments to protect portfolios.

Analysts: A holistic tool for analyzing both economic trends and market movements.

This indicator helps users navigate varying market conditions by dynamically adjusting based on economic factors and providing early technical signals for market momentum shifts.

Custom 4-Hour Candle Colors with Opening Price LinesDescription:

This indicator enhances the visual clarity of 4-hour candles by allowing users to assign custom colors to each 4-hour time block on their chart. It also provides the option to plot horizontal lines at the opening price of each 4-hour candle, with the lines extending for a customizable duration (up to 36 hours), making it easy to track the opening price levels over time.

Features:

Custom 4-Hour Candle Colors: Define unique colors for each 4-hour candle block on the chart. You can configure the colors for six different 4-hour periods, making it easier to visually differentiate between different parts of the trading day.

Opening Price Lines: The indicator plots horizontal lines at the opening price of each 4-hour candle, with the option to extend the lines for up to 36 hours into the future. The lines can also have different colors, which you can configure separately for each time block.

Flexible Time Configuration: Set custom open times for each 4-hour candle block, allowing you to adjust the indicator to match specific market sessions or time zones.

Fully Customizable: Choose both the candle colors and the opening price line colors independently for each 4-hour period. This allows for a highly personalized chart setup.

Use Cases:

Session Tracking: Easily track different trading sessions by assigning specific colors to different time periods.

Key Price Levels: Keep an eye on important opening price levels throughout the day by extending opening price lines into the future.

Visual Organization: For traders who prefer color-coded charts for improved readability, this indicator helps to organize trading days visually by color-blocking each time segment.

Important Notes:

Due to TradingView’s limitations, the opening price lines can only extend up to 500 bars into the future. The indicator automatically limits the duration of the lines to this maximum.

The script is designed to be flexible and user-friendly, allowing for easy adjustments to suit different trading styles and market conditions.

Pivot Points LIVE [CHE]Title:

Pivot Points LIVE Indicator

Subtitle:

Advanced Pivot Point Analysis for Real-Time Trading

Presented by:

Chervolino

Date:

September 24, 2024

Introduction

What are Pivot Points?

Definition:

Pivot Points are technical analysis indicators used to determine potential support and resistance levels in financial markets.

Purpose:

They help traders identify possible price reversal points and make informed trading decisions.

Overview of Pivot Points LIVE :

A comprehensive indicator designed for real-time pivot point analysis.

Offers advanced features for enhanced trading strategies.

Key Features

Pivot Points LIVE Includes:

Dynamic Pivot Highs and Lows:

Automatically detects and plots pivot high (HH, LH) and pivot low (HL, LL) points.

Customizable Visualization:

Multiple options to display markers, price labels, and support/resistance levels.

Fractal Breakouts:

Identifies and marks breakout and breakdown events with symbols.

Line Connection Modes:

Choose between "All Separate" or "Sequential" modes for connecting pivot points.

Pivot Extension Lines:

Extends lines from the latest pivot point to the current bar for trend analysis.

Alerts:

Configurable alerts for breakout and breakdown events.

Inputs and Configuration

Grouping Inputs for Easy Customization:

Source / Length Left / Length Right:

Pivot High Source: High price by default.

Pivot Low Source: Low price by default.

Left and Right Lengths: Define the number of bars to the left and right for pivot detection.

Colors: Customizable colors for pivot high and low markers.

Options:

Display Settings:

Show HH, LL, LH, HL markers and price labels.

Display support/resistance level extensions.

Option to show levels as a fractal chaos channel.

Enable fractal breakout/down symbols.

Line Connection Mode:

Choose between "All Separate" or "Sequential" for connecting lines.

Line Management:

Set maximum number of lines to display.

Customize line colors, widths, and styles.

Pivot Extension Line:

Visibility: Toggle the display of the last pivot extension line.

Customization: Colors, styles, and width for extension lines.

How It Works - Calculating Pivot Points

Pivot High and Pivot Low Detection:

Pivot High (PH):

Identified when a high price is higher than a specified number of bars to its left and right.

Pivot Low (PL):

Identified when a low price is lower than a specified number of bars to its left and right.

Higher Highs, Lower Highs, Higher Lows, Lower Lows:

Higher High (HH): Current PH is higher than the previous PH.

Lower High (LH): Current PH is lower than the previous PH.

Higher Low (HL): Current PL is higher than the previous PL.

Lower Low (LL): Current PL is lower than the previous PL.

Visual Elements

Markers and Labels:

Shapes:

HH and LH: Downward triangles above the bar.

HL and LL: Upward triangles below the bar.

Labels:

Optionally display the price levels of HH, LH, HL, and LL on the chart.

Support and Resistance Levels:

Extensions:

Lines extending from pivot points to indicate potential support and resistance zones.

Chaos Channels:

Display levels as a fractal chaos channel for enhanced trend analysis.

Fractal Breakout Symbols:

Buy Signals: Upward triangles below the bar.

Sell Signals: Downward triangles above the bar.

Slide 7: Line Connection Modes

All Separate Mode:

Description:

Connects pivot highs with pivot highs and pivot lows with pivot lows separately.

Use Case:

Ideal for traders who want to analyze highs and lows independently.

Sequential Mode:

Description:

Connects all pivot points in the order they occur, regardless of being high or low.

Use Case:

Suitable for identifying overall trend direction and momentum.

Pivot Extension Lines

Purpose:

Trend Continuation:

Visualize the continuation of the latest pivot point's price level.

Customization:

Colors:

Differentiate between bullish and bearish extensions.

Styles:

Solid, dashed, or dotted lines based on user preference.

Width:

Adjustable line thickness for better visibility.

Dynamic Updates:

The extension line updates in real-time as new bars form, providing ongoing trend insights.

Alerts and Notifications

Configurable Alerts:

Fractal Break Arrow:

Triggered when a breakout or breakdown occurs.

Long and Short Signals:

Specific alerts for bullish breakouts (Long) and bearish breakdowns (Short).

Benefits:

Timely Notifications:

Stay informed of critical market movements without constant monitoring.

Automated Trading Strategies:

Integrate with trading bots or automated systems for executing trades based on alerts.

Customization and Optimization

User-Friendly Inputs:

Adjustable Parameters:

Tailor pivot detection sensitivity with left and right lengths.

Color and Style Settings:

Match the indicator aesthetics to personal or platform preferences.

Line Management:

Maximum Lines Displayed:

Prevent chart clutter by limiting the number of lines.

Dynamic Line Handling:

Automatically manage and delete old lines to maintain chart clarity.

Flexibility:

Adapt to Different Markets:

Suitable for various financial instruments including stocks, forex, and cryptocurrencies.

Scalability:

Efficiently handles up to 500 labels and 100 lines for comprehensive analysis.

Practical Use Cases

Identifying Key Support and Resistance:

Entry and Exit Points:

Use pivot levels to determine optimal trade entry and exit points.

Trend Confirmation:

Validate market trends through the connection of pivot points.

Breakout and Breakdown Strategies:

Trading Breakouts:

Enter long positions when price breaks above pivot highs.

Trading Breakdowns:

Enter short positions when price breaks below pivot lows.

Risk Management:

Setting Stop-Loss and Take-Profit Levels:

Utilize pivot levels to place strategic stop-loss and take-profit orders.

Slide 12: Benefits for Traders

Real-Time Analysis:

Provides up-to-date pivot points for timely decision-making.

Enhanced Visualization:

Clear markers and lines improve chart readability and analysis efficiency.

Customizable and Flexible:

Adapt the indicator to fit various trading styles and strategies.

Automated Alerts:

Stay ahead with instant notifications on key market events.

Comprehensive Toolset:

Combines pivot points with fractal analysis for deeper market insights.

Conclusion

Pivot Points LIVE is a robust and versatile indicator designed to enhance your trading strategy through real-time pivot point analysis. With its advanced features, customizable settings, and automated alerts, it equips traders with the tools needed to identify key market levels, execute timely trades, and manage risks effectively.

Ready to Elevate Your Trading?

Explore Pivot Points LIVE and integrate it into your trading toolkit today!

Q&A

Questions?

Feel free to ask any questions or request further demonstrations of the Pivot Points LIVE indicator.

Institutional Levels (Whole, Half, Quarter) By CapitalwithcalebThis Pine Script indicator is designed to plot institutional levels, which are key price levels that traders often monitor. These levels include whole numbers (like 12000, 12500), half levels (like 12250), and quarter levels (like 12375). The script allows full customization of colors, line styles, and line widths for each type of level (whole, half, and quarter).

Key Features:

Range of Levels:

The user defines a minimum (minLevel) and maximum (maxLevel) price level, and the script plots levels in increments of 50 points (step size of 50 covers quarter, half, and whole levels).

Customizable Appearance:

Color Customization: You can choose separate colors for whole, half, and quarter levels.

Line Style Customization: You can choose between solid, dashed, or dotted lines for each level type (whole, half, and quarter).

Line Width Customization: You can adjust the width of the lines (1 to 5).

Automatic Level Detection:

The script automatically determines whether a level is a whole, half, or quarter level based on whether it is a multiple of 1000 (whole), 500 (half), or 250 (quarter).

Plotting of Lines:

It draws horizontal lines across the entire chart (extend.both) at the calculated levels.

For each level, it determines its type (whole, half, quarter) and plots it using the user-specified colors, line styles, and widths.

Functions:

getLineStyle(styleStr): A functional helper that converts the string input from the user ("Solid", "Dashed", "Dotted") into Pine Script's corresponding line style constants.

plotLevel(level, color, width, style): Another functional helper that plots a line at the given price level with the provided color, width, and line style.

Execution Flow:

User Input: The user specifies the minimum and maximum levels to display on the chart. They also configure the appearance of the lines (color, style, width).

Level Calculation: The script iterates over all levels between the minLevel and maxLevel with a step size of 50, checking if the level is a whole, half, or quarter level.

Line Plotting: The appropriate lines are drawn on the chart, based on the type of level and user settings.

Example Use Case:

If a user sets the minLevel to 12000 and maxLevel to 13000, the script will automatically plot lines at key institutional levels like:

12000 (whole), 12250 (quarter), 12500 (whole), 12750 (quarter), etc.

Connors VIX Reversal III invented by Dave LandryThis strategy is based on trading signals derived from the behavior of the Volatility Index (VIX) relative to its 10-day moving average. The rules are split into buying and selling conditions:

Buy Conditions:

The VIX low must be above its 10-day moving average.

The VIX must close at least 10% above its 10-day moving average.

If both conditions are met, a buy signal is generated at the market's close.

Sell Conditions:

The VIX high must be below its 10-day moving average.

The VIX must close at least 10% below its 10-day moving average.

If both conditions are met, a sell signal is generated at the market's close.

Exit Conditions:

For long positions, the strategy exits when the VIX trades intraday below its previous day’s 10-day moving average.

For short positions, the strategy exits when the VIX trades intraday above its previous day’s 10-day moving average.

This strategy is primarily a mean-reversion strategy, where the market is expected to revert to a more normal state after the VIX exhibits extreme behavior (i.e., large deviations from its moving average).

About Dave Landry

Dave Landry is a well-known figure in the world of trading, particularly in technical analysis. He is an author, trader, and educator, best known for his work on swing trading strategies. Landry focuses on trend-following and momentum-based techniques, teaching traders how to capitalize on shorter-term price swings in the market. He has written books like "Dave Landry on Swing Trading" and "The Layman's Guide to Trading Stocks," which emphasize practical, actionable trading strategies.

About Connors Research

Connors Research is a financial research firm known for its quantitative research in financial markets. Founded by Larry Connors, the firm specializes in developing high-probability trading systems based on historical market behavior. Connors’ work is widely respected for its data-driven approach, including systems like the RSI(2) strategy, which focuses on short-term mean reversion. The firm also provides trading education and tools for institutional and retail traders alike, emphasizing strategies that can be backtested and quantified.

Risks of the Strategy

While this strategy may appear to offer promising opportunities to exploit extreme VIX movements, it carries several risks:

Market Volatility: The VIX itself is a measure of market volatility, meaning the strategy can be exposed to sudden and unpredictable market swings. This can result in whipsaws, where positions are opened and closed in rapid succession due to sharp reversals in the VIX.

Overfitting: Strategies based on specific conditions like the VIX closing 10% above or below its moving average can be subject to overfitting, meaning they work well in historical tests but may underperform in live markets. This is a common issue in quantitative trading systems that are not adaptable to changing market conditions .

Mean-Reversion Assumption: The core assumption behind this strategy is that markets will revert to their mean after extreme movements. However, during periods of sustained trends (e.g., market crashes or rallies), this assumption may break down, leading to prolonged drawdowns.

Liquidity and Slippage: Depending on the asset being traded (e.g., S&P 500 futures, ETFs), liquidity issues or slippage could occur when executing trades at market close, particularly in volatile conditions. This could increase costs or worsen trade execution.

Scientific Explanation of the Strategy

The VIX is often referred to as the "fear gauge" because it measures the market's expectations of volatility based on options prices. Research has shown that the VIX tends to spike during periods of market stress and revert to lower levels when conditions stabilize . Mean reversion strategies like this one assume that extreme VIX levels are unsustainable in the long run, which aligns with findings from academic literature on volatility and market behavior.

Studies have found that the VIX is inversely correlated with stock market returns, meaning that higher VIX levels often correspond to lower stock prices and vice versa . By using the VIX’s relationship with its 10-day moving average, this strategy aims to capture reversals in market sentiment. The 10% threshold is designed to identify moments when the VIX is significantly deviating from its norm, signaling a potential reversal.

However, academic research also highlights the limitations of relying on the VIX alone for trading signals. The VIX does not predict market direction, only volatility, meaning that it cannot indicate the magnitude of price movements . Furthermore, extreme VIX levels can persist longer than expected, particularly during financial crises.

In conclusion, while the strategy is grounded in well-established financial principles (e.g., mean reversion and the relationship between volatility and market performance), it carries inherent risks and should be used with caution. Backtesting and careful risk management are essential before applying this strategy in live markets.

Correlation with AveragesThe "Correlation with Averages" indicator is designed to visualize and analyze the correlation between a selected asset's price and a base symbol's price, such as the S&P 500 (SPY). This indicator allows users to evaluate how closely an asset’s price movements align with those of the base symbol over various time periods, providing insights into market trends and potential portfolio adjustments.

Key Features:

Base Symbol and Correlation Period:

Users can specify the base symbol (default is SPY) and the period for correlation measurement (default is 252 trading days, approximating one year).

Correlation Calculation:

The indicator computes the correlation between the asset’s closing price and the base symbol’s closing price for the defined period.

Visualization:

The correlation value is plotted on the chart, with conditional background colors indicating the strength and direction of the correlation:

Red for negative correlation (below -0.5)

Green for positive correlation (above 0.5)

Yellow for neutral correlation (between -0.5 and 0.5)

Average Correlation Over Time:

Average correlations are calculated and displayed for various periods: one week, one month, one year, and five years.

A table on the chart provides dynamic updates of these average values with color-coded backgrounds to indicate correlation strength.

The Role of Correlation in Portfolio Management

Correlation is a crucial concept in portfolio management because it measures the degree to which two securities move in relation to each other. Understanding correlation helps investors construct diversified portfolios that balance risk and return. Here's why correlation is important:

Diversification:

By including assets with low or negative correlation in a portfolio, investors can reduce overall portfolio volatility and risk. For instance, if one asset is negatively correlated with another, when one performs poorly, the other may perform well, thus smoothing the overall returns.

Risk Management:

Correlation analysis helps in identifying the potential impact of one asset’s performance on the entire portfolio. Assets with high correlation can lead to concentrated risk, while those with low correlation offer better risk management.

Performance Analysis:

Correlation measures the degree to which asset returns move together. This can inform strategic decisions, such as whether to adjust positions based on expected market conditions.

Scientific References

Markowitz, H. M. (1952). "Portfolio Selection." Journal of Finance, 7(1), 77-91.

This foundational paper introduced Modern Portfolio Theory, highlighting the importance of diversification and correlation in reducing portfolio risk.

Jorion, P. (2007). Financial Risk Manager Handbook. Wiley.

This handbook provides an in-depth exploration of risk management techniques, including the use of correlation in portfolio management.

Elton, E. J., Gruber, M. J., Brown, S. J., & Goetzmann, W. N. (2014). Modern Portfolio Theory and Investment Analysis. Wiley.

This book elaborates on the concepts of correlation and diversification, offering practical insights into portfolio construction and risk management.

By utilizing the "Correlation with Averages" indicator, traders and portfolio managers can make informed decisions based on the relationship between asset prices and the base symbol, ultimately enhancing their investment strategies.

best indicator at 15 minut This Pine Script code builds an indicator called EMA Crossover with Historical Price Projection that combines two components:

EMA Crossover Strategy:

EMA 9 and EMA 21: The script calculates two exponential moving averages (EMAs) using the ta.ema() function. The crossover between these EMAs generates buy/sell signals.

A bullish crossover (when EMA 9 crosses above EMA 21) signals a buy.

A bearish crossover (when EMA 9 crosses below EMA 21) signals a sell.

These buy/sell signals are visualized on the chart using the plotshape() function with green and red symbols.

Historical Price Projection:

The code projects future prices based on historical price trends. It takes into account growth factors (user-defined drift percentages) to estimate future prices.

Projection Line: It draws a projection line from the anchor point (set by the user) using historical data. The drift factor allows you to control the projection's slope.

Forecasting Area: It shows an optional area around the projected price, adjusting the width with a user-defined growth factor for the forecast's uncertainty.

Key Sections:

Inputs:

User-defined inputs for controlling the growth factor, line styles, and forecasting area settings.

An anchoring point is provided to determine from which bar the price projection should start.

EMA Crossover:

The crossover conditions for EMA 9 and EMA 21 are defined, and the script generates buy and sell signals at those crossovers.

Historical Price Projection:

It stores the percentage changes between bars in barDeltaPercents.

It projects the future price based on these percentages and the user-defined drift factor.

The projected price is visualized using polyline.new(), and a shaded area can be added to show the range of price possibilities.

Execution Logic:

The script runs when the current time is greater than the anchor point.

If the anchor point is too far back in history, it gives a warning via the showInfoPanel function.

As new bars are confirmed, the drift is calculated, and the projection line and area are updated based on historical price changes.

Overall Flow:

It gathers price data up to 500 bars from the anchor point.

Based on the historical price trend, it forecasts the future price with a projection line and an optional shaded area.

The crossover logic for EMA 9 and 21 provides actionable signals on when to buy or sell.

Auto Fib Retracement [Syafiq.Jr]This TradingView script is an advanced indicator titled "Auto Fib Retracement Neo ." It's designed to automatically plot Fibonacci retracement levels on a price chart, aiding in technical analysis for traders. Here's a breakdown of its functionality:

Core Functionality :

The script identifies pivot points (highs and lows) on a chart and draws Fibonacci retracement lines based on these points. The lines are dynamic, updating in real-time as the market progresses.

Customizable Inputs :

Depth: Determines the minimum number of bars considered in the pivot point calculation.

Deviation: Adjusts the sensitivity of the script in identifying new pivots.

Fibonacci Levels: Allows users to select which retracement levels (236, 382, 500, 618, 786, 886) are displayed on the chart.

Visual Settings: Customization options include the colors and styles of pivot points, trend lines, and the retracement meter.

Pivot and Line Calculation:

The script calculates the deviation between the current price and the last pivot point. If the deviation exceeds a certain threshold, it identifies a new pivot and draws a trend line between the previous pivot and the current one.

Visual Aids :

The indicator provides extensive visual aids, including pivot points marked with circles, dashed trend lines connecting pivots, and labels displaying additional information like price and delta rate.

Performance :

Optimized to handle large datasets, the script is configured to process up to 4000 bars and can manage numerous lines and labels efficiently.

Background and Appearance :

The script allows for customization of the chart background color, enhancing visibility based on user preferences.

In essence, this script is a powerful tool for traders who rely on Fibonacci retracement levels to identify potential support and resistance areas, allowing for a more automated and visually guided approach to market analysis.

Rsi Long-Term Strategy [15min]Hello, I would like to present to you The "RSI Long-Term Strategy" for 15min tf

The "RSI Long-Term Strategy " is designed for traders who prefer a combination of momentum and trend-following techniques. The strategy focuses on entering long positions during significant market corrections within an overall uptrend, confirmed by both RSI and volume. The use of long-term SMAs ensures that trades are made in line with the broader market trend. The stop-loss feature provides risk management by limiting losses on trades that do not perform as expected. This strategy is particularly well-suited for longer-term traders who monitor 15-minute charts but look for substantial trend reversals or continuations.

Indicators and Parameters:

Relative Strength Index (RSI):

- The RSI is calculated using a 10-period length. It measures the magnitude of recent price changes to evaluate overbought or oversold conditions. The script defines oversold conditions when the RSI is at or below 30 and overbought conditions when the RSI is at or above 70.

Volume Condition:

-The strategy incorporates a volume condition where the current volume must be greater than 2.5 times the 20-period moving average of volume. This is used to confirm the strength of the price movement.

Simple Moving Averages (SMA):

- The strategy uses two SMAs: SMA1 with a length of 250 periods and SMA2 with a length of 500 periods. These SMAs help identify long-term trends and generate signals based on their crossover.

Strategy Logic:

Entry Logic:

A long position is initiated when all the following conditions are met:

The RSI indicates an oversold condition (RSI ≤ 30).

SMA1 is above SMA2, indicating an uptrend.

The volume condition is satisfied, confirming the strength of the signal.

Exit Logic:

The strategy closes the long position when SMA1 crosses under SMA2, signaling a potential end of the uptrend (a "Death Cross").

Stop-Loss:

A stop-loss is set at 5% below the entry price to manage risk and limit potential losses.

Buy and sell signals are highlighted with circles below or above bars:

Green Circle : Buy signal when RSI is oversold, SMA1 > SMA2, and the volume condition is met.

Red Circle : Sell signal when RSI is overbought, SMA1 < SMA2, and the volume condition is met.

Black Cross: "Death Cross" when SMA1 crosses under SMA2, indicating a potential bearish signal.

to determine the level of stop loss and target point I used a piece of code by RafaelZioni, here is the script from which a piece of code was taken

I hope the strategy will be helpful, as always, best regards and safe trades

;)

Ultra Key LevelsThe "Ultra Key Levels" indicator is a powerful tool designed for traders who seek to identify critical price levels in the market. This Pine Script™ indicator is optimized to plot significant pivot highs and lows directly on your chart, providing a clear visual representation of potential support and resistance zones.

Pivot Detection: Automatically identifies and marks pivot highs and lows using customizable parameters. Traders can fine-tune the length of the pivots, allowing for precise detection of significant price points.

Dynamic Boxes: The indicator draws dynamic boxes around each identified pivot high and low, highlighting key levels. These boxes are adjusted based on the Average True Range (ATR), ensuring they reflect the current market volatility.

Pivot Highs/Lows: Control the appearance and behavior of pivot points with options to adjust source data, length, transparency, and the maximum number of pivots displayed on the chart.

ATR Multiplier: Set the ATR multiplier to determine the size of the boxes around pivot points, helping you assess the strength of each level.

Debug Mode: Activate debug mode to visualize pivot points and fine-tune your settings for optimal performance.

Scalability: Supports up to 500 boxes, making it suitable for both short-term and long-term traders who need to track multiple levels across different timeframes.

The "Ultra Key Levels" indicator is ideal for traders who rely on technical analysis to make informed decisions. By automatically identifying and highlighting key price levels, this tool helps you anticipate potential market movements and optimize your trading strategy.

Proxy Financial Stress Index StrategyThis strategy is based on a Proxy Financial Stress Index constructed using several key financial indicators. The strategy goes long when the financial stress index crosses below a user-defined threshold, signaling a potential reduction in market stress. Once a position is opened, it is held for a predetermined number of bars (periods), after which it is automatically closed.

The financial stress index is composed of several normalized indicators, each representing different market aspects:

VIX - Market volatility.

US 10-Year Treasury Yield - Bond market.

Dollar Index (DXY) - Currency market.

S&P 500 Index - Stock market.

EUR/USD - Currency exchange rate.

High-Yield Corporate Bond ETF (HYG) - Corporate bond market.

Each component is normalized using a Z-score (based on the user-defined moving average and standard deviation lengths) and weighted according to user inputs. The aggregated index reflects overall market stress.

The strategy enters a long position when the stress index crosses below a specified threshold from above, indicating reduced financial stress. The position is held for a defined holding period before being closed automatically.

Scientific References:

The concept of a financial stress index is derived from research that combines multiple financial variables to measure systemic risks in the financial markets. Key research includes:

The Financial Stress Index developed by various Federal Reserve banks, including the Cleveland Financial Stress Index (CFSI)

Bank of America Merrill Lynch Option Volatility Estimate (MOVE) Index as a measure of interest rate volatility, which correlates with financial stress

These indices are widely used in economic research to gauge financial instability and help in policy decisions. They track real-time fluctuations in various markets and are often used to anticipate economic downturns or periods of high financial risk.

Raj - Mark Minervini Stage 2 with RSTitle: Mark Minervini Stage 2 Screener with Custom RS

Description:

This script is designed to identify stocks that meet the criteria for Mark Minervini's Stage 2 trend setup, incorporating custom relative strength (RS) ranking.

Key Features:

Moving Averages: Tracks the 50-day, 150-day, and 200-day Simple Moving Averages (SMA) to identify trend alignment.

Price Conditions: Ensures the stock price is above key moving averages, is within 25% of its 52-week high, and is at least 25% above its 52-week low.

Custom Relative Strength (RS): Compares the stock's performance against a benchmark (e.g., S&P 500) to ensure it has a strong relative strength. The RS is normalized on a 0-100 scale, and only stocks with an RS above 70 are highlighted.

Visual Indicators: The script plots moving averages on the chart and labels points where all conditions for the Stage 2 setup are met.

Usage:

Apply this script to your charts to find stocks that are in a strong uptrend and meet Mark Minervini's Stage 2 criteria.

Customize the benchmark symbol for the RS calculation to fit your market or preference

Correlation Clusters [LuxAlgo]The Correlation Clusters is a machine learning tool that allows traders to group sets of tickers with a similar correlation coefficient to a user-set reference ticker.

The tool calculates the correlation coefficients between 10 user-set tickers and a user-set reference ticker, with the possibility of forming up to 10 clusters.

🔶 USAGE

Applying clustering methods to correlation analysis allows traders to quickly identify which set of tickers are correlated with a reference ticker, rather than having to look at them one by one or using a more tedious approach such as correlation matrices.

Tickers belonging to a cluster may also be more likely to have a higher mutual correlation. The image above shows the detailed parts of the Correlation Clusters tool.

The correlation coefficient between two assets allows traders to see how these assets behave in relation to each other. It can take values between +1.0 and -1.0 with the following meaning

Value near +1.0: Both assets behave in a similar way, moving up or down at the same time

Value close to 0.0: No correlation, both assets behave independently

Value near -1.0: Both assets have opposite behavior when one moves up the other moves down, and vice versa

There is a wide range of trading strategies that make use of correlation coefficients between assets, some examples are:

Pair Trading: Traders may wish to take advantage of divergences in the price movements of highly positively correlated assets; even highly positively correlated assets do not always move in the same direction; when assets with a correlation close to +1.0 diverge in their behavior, traders may see this as an opportunity to buy one and sell the other in the expectation that the assets will return to the likely same price behavior.

Sector rotation: Traders may want to favor some sectors that are expected to perform in the next cycle, tracking the correlation between different sectors and between the sector and the overall market.

Diversification: Traders can aim to have a diversified portfolio of uncorrelated assets. From a risk management perspective, it is useful to know the correlation between the assets in your portfolio, if you hold equal positions in positively correlated assets, your risk is tilted in the same direction, so if the assets move against you, your risk is doubled. You can avoid this increased risk by choosing uncorrelated assets so that they move independently.

Hedging: Traders may want to hedge positions with correlated assets, from a hedging perspective, if you are long an asset, you can hedge going long a negatively correlated asset or going short a positively correlated asset.

Grouping different assets with similar behavior can be very helpful to traders to avoid over-exposure to those assets, traders may have multiple long positions on different assets as a way of minimizing overall risk when in reality if those assets are part of the same cluster traders are maximizing their risk by taking positions on assets with the same behavior.

As a rule of thumb, a trader can minimize risk via diversification by taking positions on assets with no correlations, the proposed tool can effectively show a set of uncorrelated candidates from the reference ticker if one or more clusters centroids are located near 0.

🔶 DETAILS

K-means clustering is a popular machine-learning algorithm that finds observations in a data set that are similar to each other and places them in a group.

The process starts by randomly assigning each data point to an initial group and calculating the centroid for each. A centroid is the center of the group. K-means clustering forms the groups in such a way that the variances between the data points and the centroid of the cluster are minimized.

It's an unsupervised method because it starts without labels and then forms and labels groups itself.

🔹 Execution Window

In the image above we can see how different execution windows provide different correlation coefficients, informing traders of the different behavior of the same assets over different time periods.

Users can filter the data used to calculate correlations by number of bars, by time, or not at all, using all available data. For example, if the chart timeframe is 15m, traders may want to know how different assets behave over the last 7 days (one week), or for an hourly chart set an execution window of one month, or one year for a daily chart. The default setting is to use data from the last 50 bars.

🔹 Clusters

On this graph, we can see different clusters for the same data. The clusters are identified by different colors and the dotted lines show the centroids of each cluster.

Traders can select up to 10 clusters, however, do note that selecting 10 clusters can lead to only 4 or 5 returned clusters, this is caused by the machine learning algorithm not detecting any more data points deviating from already detected clusters.

Traders can fine-tune the algorithm by changing the 'Cluster Threshold' and 'Max Iterations' settings, but if you are not familiar with them we advise you not to change these settings, the defaults can work fine for the application of this tool.

🔹 Correlations

Different correlations mean different behaviors respecting the same asset, as we can see in the chart above.

All correlations are found against the same asset, traders can use the chart ticker or manually set one of their choices from the settings panel. Then they can select the 10 tickers to be used to find the correlation coefficients, which can be useful to analyze how different types of assets behave against the same asset.

🔶 SETTINGS

Execution Window Mode: Choose how the tool collects data, filter data by number of bars, time, or no filtering at all, using all available data.

Execute on Last X Bars: Number of bars for data collection when the 'Bars' execution window mode is active.

Execute on Last: Time window for data collection when the `Time` execution window mode is active. These are full periods, so `Day` means the last 24 hours, `Week` means the last 7 days, and so on.

🔹 Clusters

Number of Clusters: Number of clusters to detect up to 10. Only clusters with data points are displayed.

Cluster Threshold: Number used to compare a new centroid within the same cluster. The lower the number, the more accurate the centroid will be.

Max Iterations: Maximum number of calculations to detect a cluster. A high value may lead to a timeout runtime error (loop takes too long).

🔹 Ticker of Reference

Use Chart Ticker as Reference: Enable/disable the use of the current chart ticker to get the correlation against all other tickers selected by the user.

Custom Ticker: Custom ticker to get the correlation against all the other tickers selected by the user.

🔹 Correlation Tickers

Select the 10 tickers for which you wish to obtain the correlation against the reference ticker.

🔹 Style

Text Size: Select the size of the text to be displayed.

Display Size: Select the size of the correlation chart to be displayed, up to 500 bars.

Box Height: Select the height of the boxes to be displayed. A high height will cause overlapping if the boxes are close together.

Clusters Colors: Choose a custom colour for each cluster.

Risk On/Risk Off Williams %RThe Risk On/Risk Off Williams %R indicator is a technical analysis tool designed to gauge market sentiment by comparing the performance of risk-on and risk-off assets. This indicator combines the Williams %R, a momentum oscillator, with a composite index derived from various financial assets to determine the prevailing market risk sentiment.

Components:

Risk-On Assets: These are typically more volatile and are expected to perform well during bullish market conditions. The indicator uses the following risk-on assets:

SPY (S&P 500 ETF)

QQQ (Nasdaq-100 ETF)

HYG (High-Yield Corporate Bond ETF)

XLF (Financial Select Sector SPDR Fund)

XLK (Technology Select Sector SPDR Fund)

Risk-Off Assets: These are generally considered safer investments and are expected to outperform during bearish market conditions. The indicator includes:

TLT (iShares 20+ Year Treasury Bond ETF)

GLD (SPDR Gold Trust)

DXY (U.S. Dollar Index)

IEF (iShares 7-10 Year Treasury Bond ETF)

XLU (Utilities Select Sector SPDR Fund)

Calculation:

Risk-On Index: The average closing price of the risk-on assets.

Risk-Off Index: The average closing price of the risk-off assets.

The composite index is computed as:

Composite Index=Risk On Index−Risk Off Index

Composite Index=Risk On Index−Risk Off Index

Williams %R: This momentum oscillator measures the current price relative to the high-low range over a specified period. It is calculated as:

\text{Williams %R} = \frac{\text{Highest High} - \text{Composite Index}}{\text{Highest High} - \text{Lowest Low}} \times -100

where "Highest High" and "Lowest Low" are the highest and lowest values of the composite index over the lookback period.

Usage:

Williams %R: A momentum oscillator that ranges from -100 to 0. Values above -50 suggest bullish conditions, while values below -50 indicate bearish conditions.

Background Color: The background color of the chart changes based on the Williams %R relative to a predefined threshold level:

Green background: When Williams %R is above the threshold level, indicating a bullish sentiment.

Red background: When Williams %R is below the threshold level, indicating a bearish sentiment.

Purpose:

The indicator is designed to provide a visual representation of market sentiment by comparing the performance of risk-on versus risk-off assets. It helps traders and investors understand whether the market is leaning towards higher risk (risk-on) or safety (risk-off) based on the relative performance of these asset classes. By incorporating the Williams %R, the indicator adds a momentum-based dimension to this analysis, allowing for better decision-making in response to shifting market conditions.

CNN Fear and Greed Index JD modified from minusminusCNN Fear and Greed Index - www.cnn.com

Modified from minusminus -

See Documentation from CNN's website

CNN's Fear and Greed index is an attempt to quantitatively score the Fear and Greed in the SPX using 7 factors:

Market Momentum- S&P 500 (SPX) and its 125-day moving average

Stock Price Strength -Net new 52-week highs and lows on the NYSE

Stock Price Breadth - McClellan Volume Summation Index

Put and Call options - 5-day average put/call ratio

Market Volatility - VIX and its 50-day moving average

Safe Haven Demand - Difference in 20-day stock and bond returns

Junk Bond Demand - Yield spread: junk bonds vs. investment grade

Each Factor has a weight input for the final calculation initially set to a weight of 1. The final calculation of the index is a weighted average of each factor.

3 Factors have separate functions for calculation : See Code for Clarity

SPX Momentum : difference between the Daily CBOE:SPX index value and it's 125 Day Simple moving average.

Stock Price Strength : Net New 52-week highs and lows on the NYSE.

Function calculates a measure of Net New 52-week highs by:

NYSE 52-week highs (INDEX:MAHN) - all new NYSE Highs (INDEX:HIGH)

measure of Net New 52-week lows by:

NYSE 52-week lows (INDEX:MALN) - all new NYSE Lows (INDEX:LOWN)

Then calculate a ratio of Net New 52-week Highs and Lows over Total Highs and Lows then takes a 5-day moving average of that ratio-See Code

Stock Price Breadth is the McClellan Volume Summation Index :

First Calculate the McClellan Oscillator

Second Calculate the Summation Index

4 Factors are Straight data requests

5 Day Simple Moving Average of the Put-Call Ratio on SPY

50 Day Simple Moving Average of the SPX VIX

Difference between 20 Day Simple Moving Average of SPX Daily Close and 20 Day Simple Moving Average of 10Y Constant Maturity US Treasury Note

Yield Spread between ICE BofA US High Yield Index and ICE BofA US Investment Grade Corporate Yield Index

The Fear and Greed Index is a weighted average of these factors - which is then normalized to scale from 0 to 100 using the past 25 values - length parameter.

3 Zones are Shaded: Red for Extreme Fear, Grey for normal jitters, Green for Extreme Greed.

Disclaimer: This is not financial advice. These are just my ideas, and I am not an investment advisor or investment professional. This code is for informational purposes only and do your own analysis before making any investment decisions. This is an attempt to replicate in spirt an index CNN publishes on their website and in no way shape or form infringes on their content, calculations or proprietary information.

From CNN: www.cnn.com

FEAR & GREED INDEX FAQs

What is the CNN Business Fear & Greed Index?

The Fear & Greed Index is a way to gauge stock market movements and whether stocks are fairly priced. The theory is based on the logic that excessive fear tends to drive down share prices, and too much greed tends to have the opposite effect.

How is Fear & Greed Calculated?

The Fear & Greed Index is a compilation of seven different indicators that measure some aspect of stock market behavior. They are market momentum, stock price strength, stock price breadth, put and call options, junk bond demand, market volatility, and safe haven demand. The index tracks how much these individual indicators deviate from their averages compared to how much they normally diverge. The index gives each indicator equal weighting in calculating a score from 0 to 100, with 100 representing maximum greediness and 0 signaling maximum fear.

How often is the Fear & Greed Index calculated?

Every component and the Index are calculated as soon as new data becomes available.

How to use Fear & Greed Index?

The Fear & Greed Index is used to gauge the mood of the market. Many investors are emotional and reactionary, and fear and greed sentiment indicators can alert investors to their own emotions and biases that can influence their decisions. When combined with fundamentals and other analytical tools, the Index can be a helpful way to assess market sentiment.

Tick CVD [Kioseff Trading]Hello!

This script "Tick CVD" employs live tick data to calculate CVD and volume delta! No tick chart required.

Features

Live price ticks are recorded

CVD calculated using live ticks

Delta calculated using live ticks

Tick-based HMA, WMA, EMA, or SMA for CVD and price

Key tick levels (S/R CVD & price) are recorded and displayed

Price/CVD displayable as candles or lines

Polylines are used - data visuals are not limited to 500 points.

Efficiency mode - remove all the bells and whistles to capitalize on efficiently calculated/displayed tick CVD and price

How it works

While historical tick-data isn't available to non-professional subscribers, live tick data is programmatically accessible. Consequently, this indicator records live tick data to calculate CVD, delta, and other metrics for the user!

Generally, Pine Scripts use the following rules to calculate volume/price-related metrics:

Bullish Volume: When the close price is greater than the open price.

Bearish Volume: When the close price is less than the open price.

This script, however, improves on that logic by utilizing live ticks. Instead of relying on time-series charts, it records up ticks as buying volume and down ticks as selling volume. This allows the script to create a more accurate CVD, delta, or price tick chart by tracking real-time buying and selling activity.

Price can tick fast; therefore, tick aggregation can occur. While tick aggregation isn't necessarily "incorrect", if you prefer speed and efficiency it's advised to enable "efficiency mode" in a fast market.

The image above highlights the tick CVD and price tick graph!

Green price tick graph = price is greater than its origin point (first script load)

Red price tick graph = price is less than its origin point

Blue tick CVD graph = CVD, over the calculation period, is greater than 0.

Red tick CVD graph = CVD is less than 0 over the calculation period.

The image above explains the right-oriented scales. The upper scale is for the price graph and the lower scale for the CVD graph.

The image above explains the circles superimposed on the scale lines for the price graph and the CVD graph.

The image above explains the "wavy" lines shown by the indicator. The wavy lines correspond to tick delta - whether the recorded tick was an uptick or down tick and whether buy volume or sell volume transpired.

The image above explains the blue/red boxes displayed by the indicator. The boxes offer an alternative visualization of tick delta, including the magnitude of buying/selling volume for the recorded tick.

Blue boxes = buying volume

Red boxes = selling volume

Bright blue = high buying volume (relative)

Bright red = high selling volume (relative)

Dim blue = low buying volume (relative)

Dim red = low selling volume (relative)

The numbers displayed in the box show the numbered tick and the volume delta recorded for the tick.

The image above further explains visuals for the CVD graph.

Dotted red lines indicate key CVD peaks, while dotted blue lines indicate key CVD bottoms.

The white dotted line reflects the CVD average of your choice: HMA, WMA, EMA, SMA.

The image above offers a similar explanation of visuals for the price graph.

The image above offers an alternative view for the indicator!

The image above shows the indicator when efficiency mode is enabled. When trading a fast market, enabling efficiency mode is advised - the script will perform quicker.

Of course, thank you to @RicardoSantos for his awesome library I use in almost every script :D

Thank you for checking this out!

US Market Real Value Adjusted for CPI and Dollar IndexUS Market Real Value Adjusted for CPI and Dollar Index

Provides quick access to this formula: (SP:SPX+NASDAQ_DLY:IXIC+TVC:DJI+CAPITALCOM:RTY)/4/(ECONOMICS:USCPI*TVC:DXY*100)

Overview: