Lorentzian Harmonic Flow - Temporal Market Dynamic Lorentzian Harmonic Flow - Temporal Market Dynamic (⚡LHF)

By: DskyzInvestments

What this is

LHF Pro is a research‑grade analytical instrument that models market time as a compressible medium , extracts directional flow in curved time using heavy‑tailed kernels, and consults a history‑based memory bank for context before synthesizing a final, bounded probabilistic score . It is not a mashup; each subsystem is mathematically coupled to a single clock (time dilation via gamma) and a single lens (Lorentzian heavy‑tailed weighting). This script is dense in logic (and therefore heavy) because it prioritizes rigor, interpretability, and visual clarity.

Intended use

Education and research. This tool expresses state recognition and regime context—not guarantees. It does not place orders. It is fully functional as published and contains no placeholders. Nothing herein is financial advice.

Why this is original and useful

Curved time: Markets do not move at a constant pace. LHF Pro computes a Lorentz‑style gamma (γ) from relative speed so its analytical windows contract when the tape accelerates and relax when it slows.

Heavy‑tailed lens: Lorentzian kernels weight information with fat tails to respect rare but consequential extremes (unlike Gaussian decay).

Memory of regimes: A K‑nearest‑neighbors engine works in a multi‑feature space using Lorentz kernels per dimension and exponential age fade , returning a memory bias (directional expectation) and assurance (confidence mass).

One ecosystem: Squeeze, TCI, flow, acceleration, and memory live on the same clock and blend into a single final_score —visualized and documented on the dashboard.

Cognitive map: A 2D heat map projects memory resonance by age and flow regime, making “where the past is speaking” visible.

Shadow portfolio metaphor: Neighbor outcomes act like tiny hypothetical positions whose weighted average forms an educational pressure gauge (no execution, purely didactic).

Mathematical framework (full transparency)

1) Returns, volatility, and speed‑of‑market

Log return: rₜ = ln(closeₜ / closeₜ₋₁)

Realized vol: rv = stdev(r, vol_len); vol‑of‑vol: burst = |rv − rv |

Speed‑of‑market (analog to c): c = c_multiplier × (EMA(rv) + 0.5 × EMA(burst) + ε)

2) Trend velocity and Lorentz gamma (time dilation)

Trend velocity: v = |close − close | / (vel_len × ATR)

Relative speed: v_rel = v / c

Gamma: γ = 1 / √(1 − v_rel²), stabilized by caps (e.g., ≤10)

Interpretation: γ > 1 compresses market time → use shorter effective windows.

3) Adaptive temporal scale

Adaptive length: L = base_len / γ^power (bounded for safety)

Harmonic horizons: Lₛ = L × short_ratio, Lₘ = L × mid_ratio, Lₗ = L × long_ratio

4) Lorentzian smoothing and Harmonic Flow

Kernel weight per lag i: wᵢ = 1 / (1 + (d/γ)²), d = i/L

Horizon baselines: lw_h = Σ wᵢ·price / Σ wᵢ

Z‑deviation: z_h = (close − lw_h)/ATR

Harmonic Flow (HFL): HFL = (w_short·zₛ + w_mid·zₘ + w_long·zₗ) / (w_short + w_mid + w_long)

5) Flow kinematics

Velocity: HFL_vel = HFL − HFL

Acceleration (curvature): HFL_acc = HFL − 2·HFL + HFL

6) Squeeze and temporal compression

Bollinger width vs Keltner width using L

Squeeze: BB_width < KC_width × squeeze_mult

Temporal Compression Index: TCI = base_len / L; TCI > 1 ⇒ compressed time

7) Entropy (regime complexity)

Shannon‑inspired proxy on |log returns| with numerical safeguards and smoothing. Higher entropy → more chaotic regime.

8) Memory bank and Lorentzian k‑NN

Feature vector (5D):

Outcomes stored: forward returns at H5, H13, H34

Per‑dimension similarity: k(Δ) = 1 / (1 + Δ²), weighted by user’s feature weights

Age fading: weight_age = mem_fade^age_bars

Neighbor score: sᵢ = similarityᵢ × weight_ageᵢ

Memory bias: mem_bias = Σ sᵢ·outcomeᵢ / Σ sᵢ

Assurance: mem_assurance = Σ sᵢ (confidence mass)

Normalization: mem_bias normalized by ATR and clamped into band

Shadow portfolio metaphor: neighbors behave like micro‑positions; their weighted net forward return becomes a continuous, adaptive expectation.

9) Blended score and breakout proxy

Blend factor: α_mem = 0.45 + 0.15 × (γ − 1)

Final score: final_score = (1−α_mem)·tanh(HFL / (flow_thr·1.5)) + α_mem·tanh(mem_bias_norm)

Breakout probability (bounded): energy = cap(TCI−1) + |HFL_acc|×k + cap(γ−1)×k + cap(mem_assurance)×k; breakout_prob = sigmoid(energy). Caps avoid runaway “100%” readings.

Inputs — every control, purpose, mechanics, and tuning

🔮 Lorentz Core

Auto‑Adapt (Vol/Entropy): On = L responds to γ and entropy (breathes with regime), Off = static testing.

Base Length: Calm‑market anchor horizon. Lower (21–28) for fast tapes; higher (55–89+) for slow.

Velocity Window (vel_len): Bars used in v. Shorter = more reactive γ; longer = steadier.

Volatility Window (vol_len): Bars used for rv/burst (c). Shorter = more sensitive c.

Speed‑of‑Market Multiplier (c_multiplier): Raises/lowers c. Lower values → easier γ spikes (more adaptation). Aim for strong trends to peak around γ ≈ 2–4.

Gamma Compression Power: Exponent of γ in L. <1 softens; >1 amplifies adaptation swings.

Max Kernel Span: Upper bound on smoothing loop (quality vs CPU).

🎼 Harmonic Flow

Short/Mid/Long Horizon Ratios: Partition L into fast/medium/slow views. Smaller short_ratio → faster reaction; larger long_ratio → sturdier bias.

Weights (w_short/w_mid/w_long): Governs HFL blend. Higher w_short → nimble; higher w_long → stable.

📈 Signals

Squeeze Strictness: Threshold for BB1 = compressed (coiled spring); <1 = dilated.

v/c: Relative speed; near 1 denotes extreme pacing. Diagnostic only.

Entropy: Regime complexity; high entropy suggests caution, smaller size, or waiting for order to return.

HFL: Curved‑time directional flow; sign and magnitude are the instantaneous bias.

HFL_acc: Curvature; spikes often accompany regime ignition post‑squeeze.

Mem Bias: Directional expectation from historical analogs (ATR‑normalized, bounded). Aligns or conflicts with HFL.

Assurance: Confidence mass from neighbors; higher → more reliable memory bias.

Squeeze: ON/RELEASE/OFF from BB

Cerca negli script per "蔚山现代vs川崎前锋"

Advanced Speedometer Gauge [PhenLabs]Advanced Speedometer Gauge

Version: PineScript™v6

📌 Description

The Advanced Speedometer Gauge is a revolutionary multi-metric visualization tool that consolidates 13 distinct trading indicators into a single, intuitive speedometer display. Instead of cluttering your workspace with multiple oscillators and panels, this gauge provides a unified interface where you can switch between different metrics while maintaining consistent visual interpretation.

Built on PineScript™ v6, the indicator transforms complex technical calculations into an easy-to-read semi-circular gauge with color-coded zones and a precision needle indicator. Each of the 13 available metrics has been carefully normalized to a 0-100 scale, ensuring that whether you’re analyzing RSI, volume trends, or volatility extremes, the visual interpretation remains consistent and intuitive.

The gauge is designed for traders who value efficiency and clarity. By consolidating multiple analytical perspectives into one compact display, you can quickly assess market conditions without the visual noise of traditional multi-indicator setups. All metrics are non-overlapping, meaning each provides unique insights into different aspects of market behavior.

🚀 Points of Innovation

13 selectable metrics covering momentum, volume, volatility, trend, and statistical analysis, all accessible through a single dropdown menu

Universal 0-100 normalization system that standardizes different indicator scales for consistent visual interpretation across all metrics

Semi-circular gauge design with 21 arc segments providing smooth precision and clear visual feedback through color-coded zones

Non-redundant metric selection ensuring each indicator provides unique market insights without analytical overlap

Advanced metrics including MFI (volume-weighted momentum), CCI (statistical deviation), Volatility Rank (extended lookback), Trend Strength (ADX-style), Choppiness Index, Volume Trend, and Price Distance from MA

Flexible positioning system with 5 chart locations, 3 size options, and fully customizable color schemes for optimal workspace integration

🔧 Core Components

Metric Selection Engine: Dropdown interface allowing instant switching between 13 different technical indicators, each with independent parameter controls

Normalization System: All metrics converted to 0-100 scale using indicator-specific algorithms that preserve the statistical significance of each measurement

Semi-Circular Gauge: Visual display using 21 arc segments arranged in curved formation with two-row thickness for enhanced visibility

Color Zone System: Three distinct zones (0-40 green, 40-70 yellow, 70-100 red) providing instant visual feedback on metric extremes

Needle Indicator: Dynamic pointer that positions across the gauge arc based on precise current metric value

Table Implementation: Professional table structure ensuring consistent positioning and rendering across different chart configurations

🔥 Key Features

RSI (Relative Strength Index): Classic momentum oscillator measuring overbought/oversold conditions with adjustable period length (default 14)

Stochastic Oscillator: Compares closing price to price range over specified period with smoothing, ideal for identifying momentum shifts

MFI (Money Flow Index): Volume-weighted RSI that combines price movement with volume to measure buying and selling pressure intensity

CCI (Commodity Channel Index): Measures statistical deviation from average price, normalized from typical -200 to +200 range to 0-100 scale

Williams %R: Alternative overbought/oversold indicator using high-low range analysis, inverted to match 0-100 scale conventions

Volume %: Current volume relative to moving average expressed as percentage, capped at 100 for extreme spikes

Volume Trend: Cumulative directional volume flow showing whether volume is flowing into up moves or down moves over specified period

ATR Percentile: Current Average True Range position within historical range using specified lookback period (default 100 bars)

Volatility Rank: Close-to-close volatility measured against extended historical range (default 252 days), differs from ATR in calculation method

Momentum: Rate of change calculation showing price movement speed, centered at 50 and normalized to 0-100 range

Trend Strength: ADX-style calculation using directional movement to quantify trend intensity regardless of direction

Choppiness Index: Measures market choppiness versus trending behavior, where high values indicate ranging markets and low values indicate strong trends

Price Distance from MA: Measures current price over-extension from moving average using standard deviation calculations

🎨 Visualization

Semi-Circular Arc Display: Curved gauge spanning from 0 (left) to 100 (right) with smooth progression and two-row thickness for visibility

Color-Coded Zones: Green zone (0-40) for low/oversold conditions, yellow zone (40-70) for neutral readings, red zone (70-100) for high/overbought conditions

Needle Indicator: Downward-pointing triangle (▼) positioned precisely at current metric value along the gauge arc

Scale Markers: Vertical line markers at 0, 25, 50, 75, and 100 positions with corresponding numerical labels below

Title Display: Merged cell showing “𓄀 PhenLabs” branding plus currently selected metric name in monospace font

Large Value Display: Current metric value shown with two decimal precision in large text directly below title

Table Structure: Professional table with customizable background color, text color, and transparency for minimal chart obstruction

📖 Usage Guidelines

Metric Selection

Select Metric: Default: RSI | Options: RSI, Stochastic, Volume %, ATR Percentile, Momentum, MFI (Money Flow), CCI (Commodity Channel), Williams %R, Volatility Rank, Trend Strength, Choppiness Index, Volume Trend, Price Distance | Choose the technical indicator you want to display on the gauge based on your current analytical needs

RSI Settings

RSI Length: Default: 14 | Range: 1+ | Controls the lookback period for RSI calculation, shorter periods increase sensitivity to recent price changes

Stochastic Settings

Stochastic Length: Default: 14 | Range: 1+ | Lookback period for stochastic calculation comparing close to high-low range

Stochastic Smooth: Default: 3 | Range: 1+ | Smoothing period applied to raw stochastic value to reduce noise and false signals

Volume Settings

Volume MA Length: Default: 20 | Range: 1+ | Moving average period used to calculate average volume for comparison with current volume

Volume Trend Length: Default: 20 | Range: 5+ | Period for calculating cumulative directional volume flow trend

ATR and Volatility Settings

ATR Length: Default: 14 | Range: 1+ | Period for Average True Range calculation used in ATR Percentile metric

ATR Percentile Lookback: Default: 100 | Range: 20+ | Historical range used to determine current ATR position as percentile

Volatility Rank Lookback (Days): Default: 252 | Range: 50+ | Extended lookback period for Volatility Rank metric using close-to-close volatility

Momentum and Trend Settings

Momentum Length: Default: 10 | Range: 1+ | Lookback period for rate of change calculation in Momentum metric

Trend Strength Length: Default: 20 | Range: 5+ | Period for directional movement calculations in ADX-style Trend Strength metric

Advanced Metric Settings

MFI Length: Default: 14 | Range: 1+ | Lookback period for Money Flow Index calculation combining price and volume

CCI Length: Default: 20 | Range: 1+ | Period for Commodity Channel Index statistical deviation calculation

Williams %R Length: Default: 14 | Range: 1+ | Lookback period for Williams %R high-low range analysis

Choppiness Index Length: Default: 14 | Range: 5+ | Period for calculating market choppiness versus trending behavior

Price Distance MA Length: Default: 50 | Range: 10+ | Moving average period used for Price Distance standard deviation calculation

Visual Customization

Position: Default: Top Right | Options: Top Left, Top Right, Bottom Left, Bottom Right, Middle Right | Controls gauge placement on chart for optimal workspace organization

Size: Default: Normal | Options: Small, Normal, Large | Adjusts overall gauge dimensions and text size for different monitor resolutions and preferences

Low Zone Color (0-40): Default: Green (#00FF00) | Customize color for low/oversold zone of gauge arc

Medium Zone Color (40-70): Default: Yellow (#FFFF00) | Customize color for neutral/medium zone of gauge arc

High Zone Color (70-100): Default: Red (#FF0000) | Customize color for high/overbought zone of gauge arc

Background Color: Default: Semi-transparent dark gray | Customize gauge background for contrast and chart integration

Text Color: Default: White (#FFFFFF) | Customize all text elements including title, value, and scale labels

✅ Best Use Cases

Quick visual assessment of market conditions when you need instant feedback on whether an asset is in extreme territory across multiple analytical dimensions

Workspace organization for traders who monitor multiple indicators but want to reduce chart clutter and visual complexity

Metric comparison by switching between different indicators while maintaining consistent visual interpretation through the 0-100 normalization

Overbought/oversold identification using RSI, Stochastic, Williams %R, or MFI depending on whether you prefer price-only or volume-weighted analysis

Volume analysis through Volume %, Volume Trend, or MFI to confirm price movements with corresponding volume characteristics

Volatility monitoring using ATR Percentile or Volatility Rank to identify expansion/contraction cycles and adjust position sizing

Trend vs range identification by comparing Trend Strength (high values = trending) against Choppiness Index (high values = ranging)

Statistical over-extension detection using CCI or Price Distance to identify when price has deviated significantly from normal behavior

Multi-timeframe analysis by duplicating the gauge on different timeframe charts to compare metric readings across time horizons

Educational purposes for new traders learning to interpret technical indicators through consistent visual representation

⚠️ Limitations

The gauge displays only one metric at a time, requiring manual switching to compare different indicators rather than simultaneous multi-metric viewing

The 0-100 normalization, while providing consistency, may obscure the raw values and specific nuances of each underlying indicator

Table-based visualization cannot be exported or saved as an image separately from the full chart screenshot

Optimal parameter settings vary by asset type, timeframe, and market conditions, requiring user experimentation for best results

💡 What Makes This Unique

Unified Multi-Metric Interface: The only gauge-style indicator offering 13 distinct metrics through a single interface, eliminating the need for multiple oscillator panels

Non-Overlapping Analytics: Each metric provides genuinely unique insights—MFI combines volume with price, CCI measures statistical deviation, Volatility Rank uses extended lookback, Trend Strength quantifies directional movement, and Choppiness Index measures ranging behavior

Universal Normalization System: All metrics standardized to 0-100 scale using indicator-appropriate algorithms that preserve statistical meaning while enabling consistent visual interpretation

Professional Visual Design: Semi-circular gauge with 21 arc segments, precision needle positioning, color-coded zones, and clean table implementation that maintains clarity across all chart configurations

Extensive Customization: Independent parameter controls for each metric, five position options, three size presets, and full color customization for seamless workspace integration

🔬 How It Works

1. Metric Calculation Phase:

All 13 metrics are calculated simultaneously on every bar using their respective algorithms with user-defined parameters

Each metric applies its own specific calculation method—RSI uses average gains vs losses, Stochastic compares close to high-low range, MFI incorporates typical price and volume, CCI measures deviation from statistical mean, ATR calculates true range, directional indicators measure up/down movement, and statistical metrics analyze price relationships

2. Normalization Process:

Each calculated metric is converted to a standardized 0-100 scale using indicator-appropriate transformations

Some metrics are naturally 0-100 (RSI, Stochastic, MFI, Williams %R), while others require scaling—CCI transforms from ±200 range, Momentum centers around 50, Volume ratio caps at 2x for 100, ATR and Volatility Rank calculate percentile positions, and Price Distance scales by standard deviations

3. Gauge Rendering:

The selected metric’s normalized value determines the needle position across 21 arc segments spanning 0-100

Each arc segment receives its color based on position—segments 0-8 are green zone, segments 9-14 are yellow zone, segments 15-20 are red zone

The needle indicator (▼) appears in row 5 at the column corresponding to the current metric value, providing precise visual feedback

4. Table Construction:

The gauge uses TradingView’s table system with merged cells for title and value display, ensuring consistent positioning regardless of chart configuration

Rows are allocated as follows: Row 0 merged for title, Row 1 merged for large value display, Row 2 for spacing, Rows 3-4 for the semi-circular arc with curved shaping, Row 5 for needle indicator, Row 6 for scale markers, Row 7 for numerical labels at 0/25/50/75/100

All visual elements update on every bar when barstate.islast is true, ensuring real-time accuracy without performance impact

💡 Note:

This indicator is designed for visual analysis and market condition assessment, not as a standalone trading system. For best results, combine gauge readings with price action analysis, support and resistance levels, and broader market context. Parameter optimization is recommended based on your specific trading timeframe and asset class. The gauge works on all timeframes but may require different parameter settings for intraday versus daily/weekly analysis. Consider using multiple instances of the gauge set to different metrics for comprehensive market analysis without switching between settings.

Adaptive Z-Momentum (AZM) [Blk0ut]Adaptive Z-Momentum (AZM) is a momentum indicator that expresses the normalized deviation of price from a dynamic anchor (VWAP or EMA) in standard-score (z-score) terms, with adaptive “extreme” thresholds, trend sensitivity, and optional regime filtering. The line color, background shading, and labels help you visually discern when momentum is mild, building, or overextended.

---

## Features & Concept

* Computes **z = (price – anchor) / σ**, where the anchor is either Session VWAP (intraday) or EMA (non-intraday).

* Uses exponential moving averages (EWMA) to adaptively estimate the running mean and variance, making the indicator responsive to regime changes.

* Defines an **adaptive extreme threshold** (±z threshold) based on the chosen percentile of |z| over a lookback window (e.g. 90th percentile) — dynamically adjusting to volatility environment.

* Colors the main z-line **differently when inside vs. outside the extreme thresholds**, giving immediate visual feedback.

* Optionally shades the background when momentum is over the extremes (bullish or bearish).

* Supports a **self-tuning mode** (ADX-aware) that tightens or relaxes lookback/smoothing in strong trend vs. chop regimes.

* Regime filtering options (EMA slope or ADX threshold) let you filter signals in trend vs. non-trend markets.

* Plots Δz (the change in z) in various styles to help detect acceleration or deceleration in momentum.

* Adds optional thrust/fade labels to highlight when z crosses ±extreme zones, or when momentum stalls.

---

## How to Use

* Look for **z crossing** above zero (bullish momentum) or below zero (bearish momentum).

* When **z enters the extreme band**, it suggests strong momentum; when it exits, that may indicate exhaustion or reversal.

* Watch **Δz** (momentum acceleration) for clues of weakening or strengthening momentum before z itself reacts.

* Use the **regime filter** to enforce that signals only count in favorable directional markets.

* Customize inputs: lookback window, smoothing length, extreme percentile, ADX/auto settings, colors, etc., to match your trading style and timeframe.

*Use VWAP as the anchor on intraday/session charts — because it resets each session, it highlights deviations from session “fair value” and captures volume-flow bias.

*Use EMA on swing or multi-day charts — it doesn’t reset, so it preserves trend structure and gives a smoother momentum baseline across sessions.

*In trending markets, EMA tends to deliver more reliable momentum extremes; in range or mean-reversion regimes, VWAP often gives more intuitive reversal zones.

---

## Limitations & Disclaimers

* Like all indicators, AZM is **lagging** (though adaptive) and should not be used as a standalone entry/exit trigger — always combine with price action, structure, or confirmation.

* The extreme thresholds are **percentile-based**, meaning in very quiet or very noisy periods, “extreme” may shift rapidly; use your eyes alongside the indicator.

* Because the script uses historical data and smoothing, earlier bars may differ from real-time behavior.

* Past behavior is no guarantee of future performance. Use proper risk management and test ideas on historical data before trading live.

---

## Inputs & Customization

* **Anchor** mode: Session VWAP (intraday) or EMA

* **Lookback window** and **smoothing EMA** for computing z

* **Extreme percentile** (e.g. 90) to define ±z thresholds

* **Auto / ADX-based tuning** to allow dynamic parameter changes in trending vs chop markets

* **Regime filter** (EMA slope or ADX) to restrict signals to trending conditions

* **Color settings** for inside vs outside extremes, background shading, zero line, Δz style, labels, etc.

* **Show/hide labels**, choose Δz style (columns, histogram, line, etc.)

---

## Why It’s Useful

By combining standard-score normalization with adaptive thresholds and regime sensitivity, AZM helps you see **relative momentum extremes** in a way that adjusts to market regime shifts. The dual visual cues (line color + background) reduce ambiguity at a glance.

---

Session-Conditioned Regime ATRWhy this exists

Classic ATR is great—until the open. The first few bars often inherit overnight gaps and 24-hour noise that have nothing to do with the intraday regime you actually trade. That inflates early ATR, scrambles thresholds, and invites hyper-recency bias (“today is crazy!”) when it’s just the open being the open.

This tool was built to:

Separate session reality from 24h noise. Measure volatility only inside your defined session (e.g., NYSE 09:30–16:00 ET).

Judge candles against the current regime, not the last 2–3 bars. A rolling statistic from the last N completed sessions defines what “typical” means right now.

Label “large” and “small” objectively. Bars are colored only when True Range meaningfully departs from the session regime—no gut feel, no open-bar distortion (gap inclusion optional).

Overview

Purpose: objectively identify unusually big or small candles within the active trading session, compared to the recent session regime.

Use cases: volatility filters, entry/exit confirmation, session bias detection, adaptive sizing.

This indicator replaces generic ATR with a session-conditioned, regime-aware measure. It colors candles only when their True Range (TR) is abnormally large/small versus the last N completed sessions of the same session window.

How it works

Session gating: Only bars inside the selected session are evaluated (presets for NYSE, CME RTH, FX NY; custom supported).

Per-bar TR: TR = max(high, prevRef) − min(low, prevRef).

prevRef is the prior close for in-session bars.

First bar of the session can include the overnight gap (optional; default off).

Regime statistic: For any bar in session k, aggregate all in-session TRs from the previous N completed sessions (k−N … k−1), then compute Median (default) or Mean.

Today’s anchor: Running statistic from today’s session start → current bar (for context and the on-chart ratio).

Color logic:

Big if TR ≥ bigMult × RegimeStat

Small if TR ≤ smallMult × RegimeStat

Colored states: big bull, big bear, small bull, small bear.

Non-triggering bars retain the chart’s native colors.

Panel (top-right by default)

Regime ATR (Nd): session-conditioned statistic over the past N completed sessions.

Today ATR (anchored): running statistic for the current session.

Ratio (Today/Regime): intraday volatility vs regime.

Sample size n: number of bars used in the regime calculation.

Inputs

Session Preset: NYSE (09:30–16:00 ET), CME RTH (08:30–15:00 CT), FX NY (08:00–17:00 ET), Custom (session + IANA timezone).

Regime Window: number of completed sessions (default 5).

Statistic: Median (robust) or Mean.

Include Open Gap: include overnight gap in the first in-session bar’s TR (default off).

Big/Small thresholds: multipliers relative to RegimeStat (defaults: Big=1.5×, Small=0.67×).

Colors: four independent colors for big/small × bull/bear.

Panel position & text size.

Hidden outputs: expose RegimeStat, TodayStat, Ratio, and Z-score to other scripts.

Alerts

RegimeATR: BIG bar — triggers when a bar meets the “Big” condition.

RegimeATR: SMALL bar — triggers when a bar meets the “Small” condition.

Hidden outputs (for strategies/screeners)

RegimeATR_stat, TodayATR_stat, Today_vs_Regime_Ratio, BarTR_Zscore.

Notes & limitations

No look-ahead: calculations only use information available up to that bar. Historical colors reflect what would have been known then.

Warm-up: colors begin once there are at least N completed sessions; before that, regime is undefined by design.

Changing inputs (session window, multipliers, median/mean, gap toggle) recomputes the full series using the same rolling regime logic per bar.

Designed for standard candles. Styling respects existing chart colors when no condition triggers.

Practical tips

For a broader or tighter notion of “unusual,” adjust Big/Small multipliers.

Prefer Median in markets prone to outliers; use Mean if you want Z-score alignment with the panel’s regime mean/std.

Use the Ratio readout to spot compression/expansion days quickly (e.g., <0.7× = compressed session, >1.3× = expanded).

Roadmap

More session presets:

24h continuous (crypto, index CFDs).

23h/Globex futures (CME ETH with a 60-minute maintenance break).

Regional equities (LSE, Xetra, TSE), Asia/Europe/NY overlaps for FX.

Half-day/holiday templates and dynamic calendars.

Multi-regime comparison: track multiple overlapping regimes (e.g., RTH vs ETH for futures) and show separate stats/ratios.

Robust stats options: trimmed mean, MAD/Huber alternatives; optional percentile thresholds instead of fixed multipliers.

Subpanel visuals: rolling TodayATR and Ratio plots; optional Z-score ribbon.

Screener/strategy hooks: export boolean series for BIG/SMALL, plus a lightweight strategy template for backtesting entries/exits conditioned on regime volatility.

Performance/QOL: per-symbol presets, smarter warm-up, and finer control over sample caps for ultra-low TF charts.

Changelog

v0.9b (Beta)

Session presets (NYSE/CME RTH/FX NY/Custom) with timezone handling.

Panel enhancements: ratio + sample size n.

Four-state bar coloring (big/small × bull/bear).

Alerts for BIG/SMALL bars.

Hidden Z-score stream for downstream use.

Gap-in-TR toggle for the first in-session bar.

Disclaimer

For educational purposes only. Not investment advice. Validate thresholds and session settings across symbols/timeframes before live use.

Aggression Bulbs v3.1 (Sessions + Bias, fixed)EYLONAggression Bulbs v3.2 (Sessions + Bias + Volume Surge)

This indicator highlights aggressive buy and sell activity during the London and New York sessions, using volume spikes and candle body dominance to detect institutional momentum.

⚙️ Main Logic

Compares each candle’s volume vs average volume (Volume Surge).

Checks body size vs full candle range to detect strong directional moves.

Uses an EMA bias filter to align signals with the current trend.

Displays green bubbles for aggressive buyers and red bubbles for aggressive sellers.

🕐 Sessions

London: 08:00–12:59 UTC+1

New York: 14:00–18:59 UTC+1

(Backgrounds: Yellow = London, Orange = New York)

📊 How to Read

🟢 Green bubble below bar → Aggressive BUY candle (strong demand).

🔴 Red bubble above bar → Aggressive SELL candle (strong supply).

Bubble size = relative strength (volume × candle dominance).

Use in confluence with key POI zones, volume profile, or delta clusters.

⚠️ Tips

Use on 1m–15m charts for scalping or intraday analysis.

Combine with your session bias or FVG zones for higher accuracy.

Set alerts when score ≥ threshold to catch early momentum.

NS ND - EVR - Daily Bias - TRFxVolume & Price Action Signals

What It Does

Combines three proven trading methodologies: Effort vs Result (EVR), No Supply/No Demand (NS/ND), and Daily Bias tracking for intraday traders.

Features

Effort vs Result (EVR)

- **Bullish**: Green triangle below bar when price sweeps previous low with high volume and significant wick

- **Bearish**: Red triangle above bar when price sweeps previous high with high volume and significant wick

- Identifies potential reversals where volume doesn't match price movement

No Supply / No Demand (NS/ND)

- **No Demand (Red dot)**: Up-candle with declining volume - buyers weakening

- **No Supply (Green dot)**: Down-candle with declining volume - sellers weakening

- Grey dots = unconfirmed, colored dots = confirmed within lookahead period

- Based on Volume Spread Analysis (VSA) principles

Daily Bias Label

Top-right corner shows market direction:

- **BULLISH ↑** - Closed above Previous Day High

- **BEARISH ↓** - Closed below Previous Day Low

- **BULLISH/BEARISH REV** - Swept level but closed back inside

- **RANGE ↔** - Trading between PDH/PDL

## Settings

- **EVR**: Toggle on/off, volume multiplier, wick %, inside bars, transparency

- **NS/ND**: Toggle on/off, lookahead bars (default: 10)

- **Daily Bias**: Toggle label display

## Best For

✓ Intraday trading (1m-1h timeframes)

✓ Reversal setups

✓ Volume analysis

✓ Confluence trading (all signals align)

How to Use

1. Enable components you want (all can be toggled independently)

2. Trade EVR signals in direction of Daily Bias

3. Look for NS/ND confirmation at key levels

4. Wait for colored dots (confirmed signals) over grey (unconfirmed)

**Note**: Works on intraday timeframes only. NS/ND signals may repaint during confirmation period.

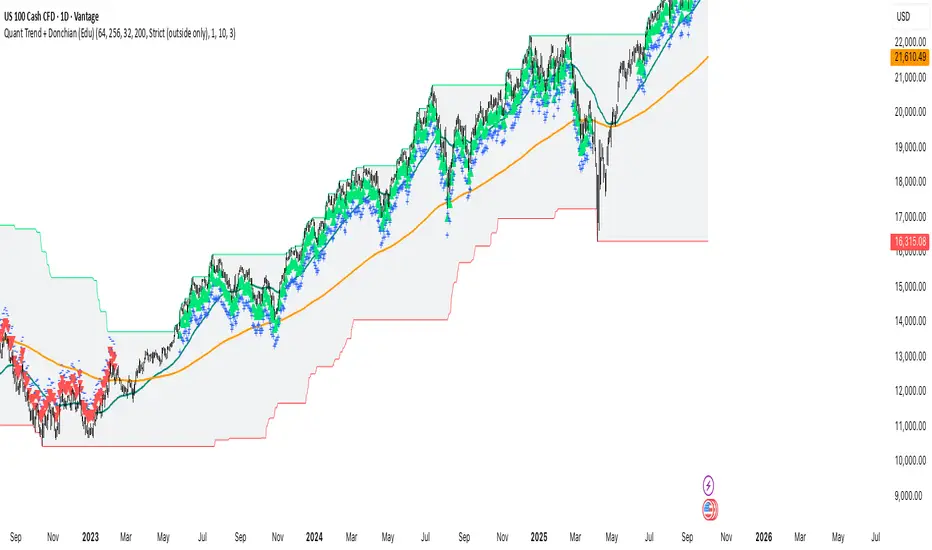

Quant Trend + Donchian (Educational, Public-Safe)What this does

Educational, public-safe visualization of a quant regime model:

• Trend : EMA(64) vs EMA(256) (EWMAC proxy)

• Breakout : Donchian channel (200)

• Volatility-awareness : internal z-scores (not plotted) for concept clarity

Why it’s useful

• Shows when trend & breakout align (clean regimes) vs conflict (chop)

• Helps explain why volatility-aware systems size up in smooth trends and scale down in noise

How to read it

• EMA64 above EMA256 with price near/above Donchian high → trend-following alignment

• EMA64 below EMA256 with price near/below Donchian low → bearish alignment

• Inside channel with EMAs tangled → range/chop risk

Notes

• Indicator is educational only (no orders).

• Built entirely with TradingView built-ins.

• For consistent visuals: enable “Indicator values on price scale” and disable “Scale price chart only” in Settings → Scales .

Volume Aggregated Spot & Futures -- Crypto (by plyst & more)📊 Volume Aggregated Spot & Futures - Enhanced Edition

🎯 Overview

Advanced volume aggregation indicator that combines spot and perpetual futures volume across the top 10 cryptocurrency exchanges. This enhanced version builds upon the original work by @HALDRO Project with optimized calculations and expanded functionality.

✨ Key Features

- 📈 Real-time aggregated volume from 10 major exchanges (Binance, Bybit, OKX, Coinbase, Bitget, KuCoin, Kraken, MEXC, Gate.io, HTX)

- 🔄 Multiple visualization modes: Volume, Delta, Cumulative Delta, Spot vs Perp analysis, Liquidations, OBV, and MFI

- 💱 Multi-currency support: Display volume in COIN, USD, or EUR

- 🎨 Clean, single-color bar chart showing total cumulative volume

- 📊 Multiple calculation methods: SUM, AVG, MEDIAN, VARIANCE

- 🎯 Separate spot (USDT, USD, USDC, etc.) and perpetual futures (.P contracts) tracking

🔧 Technical Improvements

✓ Corrected MFI formula for accurate money flow calculations

✓ Optimized volume aggregation logic with proper NA handling

✓ Support for 10 exchanges (up from 9)

✓ Streamlined codebase for better performance

✓ Updated perpetual contract naming conventions (.P format)

📖 Usage

Perfect for analyzing total market volume, identifying liquidation events, tracking buyer/seller pressure through delta analysis, and understanding the spot vs futures market dynamics.

🙏 Credits

Original concept and framework by @HALDRO Project. This version includes mathematical corrections, code optimizations, and expanded exchange support.

⚠️ Note

Aggregated volume is calculated from external exchange data using request.security(). Ensure your plan supports the necessary security calls for optimal performance.

Round Number Analyzer v3Round Number Analyzer v3 is an indicator designed to analyze how price interacts with round number levels (levels spaced at fixed intervals in points or pips).

The indicator does not generate entry/exit signals, but provides detailed statistics to better understand market dynamics around these key levels.

✨ Key Features

Cross Counting: detects every time the price crosses a round number level (up = Long, down = Short).

Continuations & Reversals: classifies each cross as:

Continuation: the move continues in the same direction as the previous sequence.

Reversal: the move changes direction compared to the previous sequence.

Sequence Classification (L1…L5+): each level is labelled based on its position within the consecutive cross sequence:

L1 = first level of the sequence,

L2 = second consecutive,

…

L5+ = fifth or higher.

Comprehensive Stats Table (top right corner):

Total crosses (Long, Short, Totals).

Total continuations + breakdown by L1…L5+.

Total reversals + breakdown by L1…L5+.

Percentages calculated against the proper denominator, displayed directly inside the cells next to the absolute values.

Date range of analysis (user-defined).

Customizable Step: Works in both points and pips, making the indicator suitable for indices and forex.

⚙️ Main Inputs

Start date / End date → sets the analysis period.

Step mode → Points or Pips.

Step value → distance between round levels.

Pip size → pip size (default = 0.0001, typical for forex).

📈 How to Interpret

A high continuation percentage after L1–L2 suggests the market tends to extend multiple times beyond the first breakout levels.

Higher reversal percentages at advanced levels (L4–L5+) may signal trend exhaustion.

The analysis helps estimate the probability of continuation or reversal depending on how many consecutive levels have already been crossed.

🔎 Practical Applications

Support for breakout or mean-reversion strategies.

Comparative analysis across different markets (e.g. indices vs forex) or different time periods.

📝 Notes

The indicator is timeframe-robust, as it accounts for multiple steps within the same candle, ensuring results do not depend on the selected timeframe (except for TradingView’s historical data limits).

It does not provide automatic trading signals, but serves as a quantitative analysis tool to refine your strategies.

---

Round Number Analyzer v3 è un indicatore pensato per analizzare come il prezzo interagisce con i livelli di round number (livelli a distanza fissa in punti o pips).

L’indicatore non genera segnali di ingresso/uscita, ma fornisce statistiche dettagliate utili per comprendere la dinamica del mercato attorno a questi livelli.

✨ Funzionalità principali

Conteggio dei Cross: rileva ogni volta che il prezzo attraversa un livello round (verso l’alto = Long, verso il basso = Short).

Continuations & Reversals: classifica ogni attraversamento come:

Continuation: il movimento prosegue nella stessa direzione della sequenza precedente.

Reversal: il movimento inverte la direzione rispetto alla sequenza precedente.

Classificazione per sequenza (L1…L5+): ogni livello è etichettato in base alla sua posizione nella sequenza di cross consecutivi:

L1 = primo livello della sequenza,

L2 = secondo consecutivo,

…

L5+ = quinto o superiore.

Statistiche complete in tabella (in alto a destra):

Cross totali (Long, Short, Totals).

Continuations totali + breakdown per L1…L5+.

Reversals totali + breakdown per L1…L5+.

Percentuali calcolate sul denominatore corretto, mostrate direttamente dentro le celle accanto ai valori assoluti.

Date range di analisi (impostabile dall’utente).

Step personalizzabile: puoi lavorare sia in punti che in pips, così l’indicatore è adatto sia per indici che per forex.

⚙️ Input principali

Start date / End date → imposta l’intervallo temporale di analisi.

Step mode → punti o pips.

Step value → ampiezza tra i livelli round.

Pip size → dimensione del pip (default = 0.0001, tipico per il forex).

📈 Come interpretarlo

Una percentuale di continuation molto alta dopo L1–L2 indica che il mercato tende a proseguire più volte oltre i primi livelli di breakout.

Percentuali di reversal più elevate nei livelli avanzati (L4–L5+) possono suggerire esaurimento della spinta.

L’analisi permette di stimare la probabilità che un movimento in corso continui o si inverta in base a quanti livelli sono già stati attraversati consecutivamente.

🔎 Applicazioni pratiche

Supporto per strategie di breakout o mean reversion.

Analisi comparativa tra mercati (es. indici vs forex) o tra periodi temporali diversi.

📝 Note

L’indicatore è timeframe-robust: il conteggio tiene conto di multipli step dentro la stessa candela, così i risultati non dipendono dal timeframe scelto (salvo i limiti di caricamento storico di TradingView).

Non fornisce segnali operativi automatici, ma è un tool di analisi quantitativa per affinare le proprie strategie.

Volume Based Sampling [BackQuant]Volume Based Sampling

What this does

This indicator converts the usual time-based stream of candles into an event-based stream of “synthetic” bars that are created only when enough trading activity has occurred . You choose the activity definition:

Volume bars : create a new synthetic bar whenever the cumulative number of shares/contracts traded reaches a threshold.

Dollar bars : create a new synthetic bar whenever the cumulative traded dollar value (price × volume) reaches a threshold.

The script then keeps an internal ledger of these synthetic opens, highs, lows, closes, and volumes, and can display them as candles, plot a moving average calculated over the synthetic closes, mark each time a new sample is formed, and optionally overlay the native time-bars for comparison.

Why event-based sampling matters

Markets do not release information on a clock: activity clusters during news, opens/closes, and liquidity shocks. Event-based bars normalize for that heteroskedastic arrival of information: during active periods you get more bars (finer resolution); during quiet periods you get fewer bars (coarser resolution). Research shows this can reduce microstructure pathologies and produce series that are closer to i.i.d. and more suitable for statistical modeling and ML. In particular:

Volume and dollar bars are a common event-time alternative to time bars in quantitative research and are discussed extensively in Advances in Financial Machine Learning (AFML). These bars aim to homogenize information flow by sampling on traded size or value rather than elapsed seconds.

The Volume Clock perspective models market activity in “volume time,” showing that many intraday phenomena (volatility, liquidity shocks) are better explained when time is measured by traded volume instead of seconds.

Related market microstructure work on flow toxicity and liquidity highlights that the risk dealers face is tied to information intensity of order flow, again arguing for activity-based clocks.

How the indicator works (plain English)

Choose your bucket type

Volume : accumulate volume until it meets a threshold.

Dollar Bars : accumulate close × volume until it meets a dollar threshold.

Pick the threshold rule

Dynamic threshold : by default, the script computes a rolling statistic (mean or median) of recent activity to set the next bucket size. This adapts bar size to changing conditions (e.g., busier sessions produce more frequent synthetic bars).

Fixed threshold : optionally override with a constant target (e.g., exactly 100,000 contracts per synthetic bar, or $5,000,000 per dollar bar).

Build the synthetic bar

While a bucket fills, the script tracks:

o_s: first price of the bucket (synthetic open)

h_s: running maximum price (synthetic high)

l_s: running minimum price (synthetic low)

c_s: last price seen (synthetic close)

v_s: cumulative native volume inside the bucket

d_samples: number of native bars consumed to complete the bucket (a proxy for “how fast” the threshold filled)

Emit a new sample

Once the bucket meets/exceeds the threshold, a new synthetic bar is finalized and stored. If overflow occurs (e.g., a single native bar pushes you past the threshold by a lot), the code will emit multiple synthetic samples to account for the extra activity.

Maintain a rolling history efficiently

A ring buffer can overwrite the oldest samples when you hit your Max Stored Samples cap, keeping memory usage stable.

Compute synthetic-space statistics

The script computes an SMA over the last N synthetic closes and basic descriptors like average bars per synthetic sample, mean and standard deviation of synthetic returns, and more. These are all in event time , not clock time.

Inputs and options you will actually use

Data Settings

Sampling Method : Volume or Dollar Bars.

Rolling Lookback : window used to estimate the dynamic threshold from recent activity.

Filter : Mean or Median for the dynamic threshold. Median is more robust to spikes.

Use Fixed? / Fixed Threshold : override dynamic sizing with a constant target.

Max Stored Samples : cap on synthetic history to keep performance snappy.

Use Ring Buffer : turn on to recycle storage when at capacity.

Indicator Settings

SMA over last N samples : moving average in synthetic space . Because its index is sample count, not minutes, it adapts naturally: more updates in busy regimes, fewer in quiet regimes.

Visuals

Show Synthetic Bars : plot the synthetic OHLC candles.

Candle Color Mode :

Green/Red: directional close vs open

Volume Intensity: opacity scales with synthetic size

Neutral: single color

Adaptive: graded by how large the bucket was relative to threshold

Mark new samples : drop a small marker whenever a new synthetic bar prints.

Comparison & Research

Show Time Bars : overlay the native time-based candles to visually compare how the two sampling schemes differ.

How to read it, step by step

Turn on “Synthetic Bars” and optionally overlay “Time Bars.” You will see that during high-activity bursts, synthetic bars print much faster than time bars.

Watch the synthetic SMA . Crosses in synthetic space can be more meaningful because each update represents a roughly comparable amount of traded information.

Use the “Avg Bars per Sample” in the info table as a regime signal. Falling average bars per sample means activity is clustering, often coincident with higher realized volatility.

Try Dollar Bars when price varies a lot but share count does not; they normalize by dollar risk taken in each sample. Volume Bars are ideal when share count is a better proxy for information flow in your instrument.

Quant finance background and citations

Event time vs. clock time : Easley, López de Prado, and O’Hara advocate measuring intraday phenomena on a volume clock to better align sampling with information arrival. This framing helps explain volatility bursts and liquidity droughts and motivates volume-based bars.

Flow toxicity and dealer risk : The same authors show how adverse selection risk changes with the intensity and informativeness of order flow, further supporting activity-based clocks for modeling and risk management.

AFML framework : In Advances in Financial Machine Learning , event-driven bars such as volume, dollar, and imbalance bars are presented as superior sampling units for many ML tasks, yielding more stationary features and fewer microstructure distortions than fixed time bars. ( Alpaca )

Practical use cases

1) Regime-aware moving averages

The synthetic SMA in event time is not fooled by quiet periods: if nothing of consequence trades, it barely updates. This can make trend filters less sensitive to calendar drift and more sensitive to true participation.

2) Breakout logic on “equal-information” samples

The script exposes simple alerts such as breakout above/below the synthetic SMA . Because each bar approximates a constant amount of activity, breakouts are conditioned on comparable informational mass, not arbitrary time buckets.

3) Volatility-adaptive backtests

If you use synthetic bars as your base data stream, most signal rules become self-paced : entry and exit opportunities accelerate in fast markets and slow down in quiet regimes, which often improves the realism of slippage and fill modeling in research pipelines (pair this indicator with strategy code downstream).

4) Regime diagnostics

Avg Bars per Sample trending down: activity is dense; expect larger realized ranges.

Return StdDev (synthetic) rising: noise or trend acceleration in event time; re-tune risk.

Interpreting the info panel

Method : your sampling choice and current threshold.

Total Samples : how many synthetic bars have been formed.

Current Vol/Dollar : how much of the next bucket is already filled.

Bars in Bucket : native bars consumed so far in the current bucket.

Avg Bars/Sample : lower means higher trading intensity.

Avg Return / Return StdDev : return stats computed over synthetic closes .

Research directions you can build from here

Imbalance and run bars

Extend beyond pure volume or dollar thresholds to imbalance bars that trigger on directional order flow imbalance (e.g., buy volume minus sell volume), as discussed in the AFML ecosystem. These often further homogenize distributional properties used in ML. alpaca.markets

Volume-time indicators

Re-compute classical indicators (RSI, MACD, Bollinger) on the synthetic stream. The premise is that signals are updated by traded information , not seconds, which may stabilize indicator behavior in heteroskedastic regimes.

Liquidity and toxicity overlays

Combine synthetic bars with proxies of flow toxicity to anticipate spread widening or volatility clustering. For instance, tag synthetic bars that surpass multiples of the threshold and test whether subsequent realized volatility is elevated.

Dollar-risk parity sampling for portfolios

Use dollar bars to align samples across assets by notional risk, enabling cleaner cross-asset features and comparability in multi-asset models (e.g., correlation studies, regime clustering). AFML discusses the benefits of event-driven sampling for cross-sectional ML feature engineering.

Microstructure feature set

Compute duration in native bars per synthetic sample , range per sample , and volume multiple of threshold as inputs to state classifiers or regime HMMs . These features are inherently activity-aware and often predictive of short-horizon volatility and trend persistence per the event-time literature. ( Alpaca )

Tips for clean usage

Start with dynamic thresholds using Median over a sensible lookback to avoid outlier distortion, then move to Fixed thresholds when you know your instrument’s typical activity scale.

Compare time bars vs synthetic bars side by side to develop intuition for how your market “breathes” in activity time.

Keep Max Stored Samples reasonable for performance; the ring buffer avoids memory creep while preserving a rolling window of research-grade data.

SuperTrend Optimizer Remastered[CHE] SuperTrend Optimizer Remastered — Grid-ranked SuperTrend with additive or multiplicative scoring

Summary

This indicator evaluates a fixed grid of one hundred and two SuperTrend parameter pairs and ranks them by a simple flip-to-flip return model. It auto-selects the currently best-scoring combination and renders its SuperTrend in real time, with optional gradient coloring for faster visual parsing. The original concept is by KioseffTrading Thanks a lot for it.

For years I wanted to shorten the roughly two thousand three hundred seventy-one lines; I have now reduced the core to about three hundred eighty lines without triggering script errors. The simplification is generalizable to other indicators. A multiplicative return mode was added alongside the existing additive aggregation, enabling different rankings and often more realistic compounding behavior.

Motivation: Why this design?

SuperTrend is sensitive to its factor and period. Picking a single pair statically can underperform across regimes. This design sweeps a compact parameter grid around user-defined lower bounds, measures flip-to-flip outcomes, and promotes the combination with the strongest cumulative return. The approach keeps the visual footprint familiar while removing manual trial-and-error. The multiplicative mode captures compounding effects; the additive mode remains available for linear aggregation.

Originally (by KioseffTrading)

Very long script (~2,371 lines), monolithic structure.

SuperTrend optimization with additive (cumulative percentage-sum) scoring only.

Heavier use of repetitive code; limited modularity and fewer UI conveniences.

No explicit multiplicative compounding option; rankings did not reflect sequence-sensitive equity growth.

Now (remastered by CHE)

Compact core (~380 lines) with the same functional intent, no compile errors.

Adds multiplicative (compounding) scoring alongside additive, changing rankings to reflect real equity paths and penalize drawdown sequences.

Fixed 34×3 grid sweep, live ranking, gradient-based bar/wick/line visuals, top-table display, and an optional override plot.

Cleaner arrays/state handling, last-bar table updates, and reusable simplification pattern that can be applied to other indicators.

What’s different vs. standard approaches?

Baseline: A single SuperTrend with hand-picked inputs.

Architecture differences:

Fixed grid of thirty-four factor offsets across three ATR offsets.

Per-combination flip-to-flip backtest with additive or multiplicative aggregation.

Live ranking with optional “Best” or “Worst” table output.

Gradient bar, wick, and line coloring driven by consecutive trend counts.

Optional override plot to force a specific SuperTrend independent of ranking.

Practical effect: Charts show the currently best-scoring SuperTrend, not a static choice, plus an on-chart table of top performers for transparency.

How it works (technical)

For each parameter pair, the script computes SuperTrend value and direction. It monitors direction transitions and treats a change from up to down as a long entry and the reverse as an exit, measuring the move between entry and exit using close prices. Results are aggregated per pair either by summing percentage changes or by compounding return factors and then converting to percent for comparison. On the last bar, open trades are included as unrealized contributions to ranking. The best combination’s line is plotted, with separate styling for up and down regimes. Consecutive regime counts are normalized within a rolling window and mapped to gradients for bars, wicks, and lines. A two-column table reports the best or worst performers, with an optional row describing the parameter sweep.

Parameter Guide

Factor (Lower Bound) — Starting SuperTrend factor; the grid adds offsets between zero and three point three. Default three point zero. Higher raises distance to price and reduces flips.

ATR Period (Lower Bound) — Starting ATR length; the grid adds zero, one, and two. Default ten. Longer reduces noise at the cost of responsiveness.

Best vs Worst — Ranks by top or bottom cumulative return. Default Best. Use Worst for stress tests.

Calculation Mode — Additive sums percents; Multiplicative compounds returns. Multiplicative is closer to equity growth and can change the leaderboard.

Show in Table — “Top Three” or “All”. Fewer rows keep charts clean.

Show “Parameters Tested” Label — Displays the effective sweep ranges for auditability.

Plot Override SuperTrend — If enabled, the override factor and ATR are plotted instead of the ranked winner.

Override Factor / ATR Period — Values used when override is on.

Light Mode (for Table) — Adjusts table colors for bright charts.

Gradient/Coloring controls — Toggles for gradient bars and wick coloring, window length for normalization, gamma for contrast, and transparency settings. Use these to emphasize or tone down visual intensity.

Table Position and Text Size — Places the table and sets typography.

Reading & Interpretation

The auto SuperTrend plots one line for up regimes and one for down regimes. Color intensity reflects consecutive trend persistence within the chosen window. A small square at the bottom encodes the same gradient as a compact status channel. Optional wick coloring uses the same gradient for maximum contrast. The performance table lists parameter pairs and their cumulative return under the chosen aggregation; positive values are tinted with the up color, negative with the down color. “Long” labels mark flips that open a long in the simplified model.

Practical Workflows & Combinations

Trend following: Use the auto line as your primary bias. Enter on flips aligned with structure such as higher highs and higher lows. Filter with higher-timeframe trend or volatility contraction.

Exits/Stops: Consider conservative exits when color intensity fades or when the opposite line is approached. Aggressive traders can trail near the plotted line.

Override mode: When you want stability across instruments, enable override and standardize factor and ATR; keep the table visible for sanity checks.

Multi-asset/Multi-TF: Defaults travel well on liquid instruments and intraday to daily timeframes. Heavier assets may prefer larger lower bounds or multiplicative mode.

Behavior, Constraints & Performance

Repaint/confirmation: Signals are based on SuperTrend direction; confirmation is best assessed on closed bars to avoid mid-bar oscillation. No higher-timeframe requests are used.

Resources: One hundred and two SuperTrend evaluations per bar, arrays for state, and a last-bar table render. This is efficient for the grid size but avoid stacking many instances.

Known limits: The flip model ignores costs, slippage, and short exposure. Rapid whipsaws can degrade both aggregation modes. Gradients are cosmetic and do not change logic.

Sensible Defaults & Quick Tuning

Start with the provided lower bounds and “Top Three” table.

Too many flips → raise the lower bound factor or period.

Too sluggish → lower the bounds or switch to additive mode.

Rankings feel unstable → prefer multiplicative mode and extend the normalization window.

Visuals too strong → increase gradient transparency or disable wick coloring.

What this indicator is—and isn’t

This is a parameter-sweep and visualization layer for SuperTrend selection. It is not a complete trading system, not predictive, and does not include position sizing, transaction costs, or risk management. Combine with market structure, higher-timeframe context, and explicit risk controls.

Attribution and refactor note: The original work is by KioseffTrading. The script has been refactored from approximately two thousand three hundred seventy-one lines to about three hundred eighty core lines, retaining behavior without compiler errors. The general simplification pattern is reusable for other indicators.

Metadata

Name/Tag: SuperTrend Optimizer Remastered

Pine version: v6

Overlay or separate pane: true (overlay)

Core idea/principle: Grid-based SuperTrend selection by cumulative flip returns with additive or multiplicative aggregation.

Primary outputs/signals: Auto-selected SuperTrend up and down lines, optional override lines, gradient bar and wick colors, “Long” labels, performance table.

Inputs with defaults: See Parameter Guide above.

Metrics/functions used: SuperTrend, ATR, arrays, barstate checks, windowed normalization, gamma-based contrast adjustment, table API, gradient utilities.

Special techniques: Fixed grid sweep, compounding vs linear aggregation, last-bar UI updates, gradient encoding of persistence.

Performance/constraints: One hundred and two SuperTrend calls, arrays of length one hundred and two, label budget, last-bar table updates, no higher-timeframe requests.

Recommended use-cases/workflows: Trend bias selection, quick parameter audits, override standardization across assets.

Compatibility/assets/timeframes: Standard OHLC charts across intraday to daily; liquid instruments recommended.

Limitations/risks: Costs and slippage omitted; mid-bar instability possible; not suitable for synthetic chart types.

Debug/diagnostics: Ranking table, optional tested-range label; internal counters for consecutive trends.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Extreme Pressure Zones Indicator (EPZ) [BullByte]Extreme Pressure Zones Indicator(EPZ)

The Extreme Pressure Zones (EPZ) Indicator is a proprietary market analysis tool designed to highlight potential overbought and oversold "pressure zones" in any financial chart. It does this by combining several unique measurements of price action and volume into a single, bounded oscillator (0–100). Unlike simple momentum or volatility indicators, EPZ captures multiple facets of market pressure: price rejection, trend momentum, supply/demand imbalance, and institutional (smart money) flow. This is not a random mashup of generic indicators; each component was chosen and weighted to reveal extreme market conditions that often precede reversals or strong continuations.

What it is?

EPZ estimates buying/selling pressure and highlights potential extreme zones with a single, bounded 0–100 oscillator built from four normalized components. Context-aware weighting adapts to volatility, trendiness, and relative volume. Visual tools include adaptive thresholds, confirmed-on-close extremes, divergence, an MTF dashboard, and optional gradient candles.

Purpose and originality (not a mashup)

Purpose: Identify when pressure is building or reaching potential extremes while filtering noise across regimes and symbols.

Originality: EPZ integrates price rejection, momentum cascade, pressure distribution, and smart money flow into one bounded scale with context-aware weighting. It is not a cosmetic mashup of public indicators.

Why a trader might use EPZ

EPZ provides a multi-dimensional gauge of market extremes that standalone indicators may miss. Traders might use it to:

Spot Reversals: When EPZ enters an "Extreme High" zone (high red), it implies selling pressure might soon dominate. This can hint at a topside reversal or at least a pause in rallies. Conversely, "Extreme Low" (green) can highlight bottom-fish opportunities. The indicator's divergence module (optional) also finds hidden bullish/bearish divergences between price and EPZ, a clue that price momentum is weakening.

Measure Momentum Shifts: Because EPZ blends momentum and volume, it reacts faster than many single metrics. A rising MPO indicates building bullish pressure, while a falling MPO shows increasing bearish pressure. Traders can use this like a refined RSI: above 50 means bullish bias, below 50 means bearish bias, but with context provided by the thresholds.

Filter Trades: In trend-following systems, one could require EPZ to be in the bullish (green) zone before taking longs, or avoid new trades when EPZ is extreme. In mean-reversion systems, one might specifically look to fade extremes flagged by EPZ.

Multi-Timeframe Confirmation: The dashboard can fetch a higher timeframe EPZ value. For example, you might trade a 15-minute chart only when the 60-minute EPZ agrees on pressure direction.

Components and how they're combined

Rejection (PRV) – Captures price rejection based on candle wicks and volume (see Price Rejection Volume).

Momentum Cascade (MCD) – Blends multiple momentum periods (3,5,8,13) into a normalized momentum score.

Pressure Distribution (PDI) – Measures net buy/sell pressure by comparing volume on up vs down candles.

Smart Money Flow (SMF) – An adaptation of money flow index that emphasizes unusual volume spikes.

Each of these components produces a 0–100 value (higher means more bullish pressure). They are then weighted and averaged into the final Market Pressure Oscillator (MPO), which is smoothed and scaled. By combining these four views, EPZ stands out as a comprehensive pressure gauge – the whole is greater than the sum of parts

Context-aware weighting:

Higher volatility → more PRV weight

Trendiness up (RSI of ATR > 25) → more MCD weight

Relative volume > 1.2x → more PDI weight

SMF holds a stable weight

The weighted average is smoothed and scaled into MPO ∈ with 50 as the neutral midline.

What makes EPZ stand out

Four orthogonal inputs (price action, momentum, pressure, flow) unified in a single bounded oscillator with consistent thresholds.

Adaptive thresholds (optional) plus robust extreme detection that also triggers on crossovers, so static thresholds work reliably too.

Confirm Extremes on Bar Close (default ON): dots/arrows/labels/alerts print on closed bars to avoid repaint confusion.

Clean dashboard, divergence tools, pre-alerts, and optional on-price gradients. Visual 3D layering uses offsets for depth only,no lookahead.

Recommended markets and timeframes

Best: liquid symbols (index futures, large-cap equities, major FX, BTC/ETH).

Timeframes: 5–15m (more signals; consider higher thresholds), 1H–4H (balanced), 1D (clear regimes).

Use caution on illiquid or very low TFs where wick/volume geometry is erratic.

Logic and thresholds

MPO ∈ ; 50 = neutral. Above 50 = bullish pressure; below 50 = bearish.

Static thresholds (defaults): thrHigh = 70, thrLow = 30; warning bands 5 pts inside extremes (65/35).

Adaptive thresholds (optional):

thrHigh = min(BaseHigh + 5, mean(MPO,100) + stdev(MPO,100) × ExtremeSensitivity)

thrLow = max(BaseLow − 5, mean(MPO,100) − stdev(MPO,100) × ExtremeSensitivity)

Extreme detection

High: MPO ≥ thrHigh with peak/slope or crossover filter.

Low: MPO ≤ thrLow with trough/slope or crossover filter.

Cooldown: 5 bars (default). A new extreme will not print until the cooldown elapses, even if MPO re-enters the zone.

Confirmation

"Confirm Extremes on Bar Close" (default ON) gates extreme markers, pre-alerts, and alerts to closed bars (non-repainting).

Divergences

Pivot-based bullish/bearish divergence; tags appear only after left/right bars elapse (lookbackPivot).

MTF

HTF MPO retrieved with lookahead_off; values can update intrabar and finalize at HTF close. This is disclosed and expected.

Inputs and defaults (key ones)

Core: Sensitivity=1.0; Analysis Period=14; Smoothing=3; Adaptive Thresholds=OFF.

Extremes: Base High=70, Base Low=30; Extreme Sensitivity=1.5; Confirm Extremes on Bar Close=ON; Cooldown=5; Dot size Small/Tiny.

Visuals: Heatmap ON; 3D depth optional; Strength bars ON; Pre-alerts OFF; Divergences ON with tags ON; Gradient candles OFF; Glow ON.

Dashboard: ON; Position=Top Right; Size=Normal; MTF ON; HTF=60m; compact overlay table on price chart.

Advanced caps: Max Oscillator Labels=80; Max Extreme Guide Lines=80; Divergence objects=60.

Dashboard: what each element means

Header: EPZ ANALYSIS.

Large readout: Current MPO; color reflects state (extreme, approaching, or neutral).

Status badge: "Extreme High/Low", "Approaching High/Low", "Bullish/Neutral/Bearish".

HTF cell (when MTF ON): Higher-timeframe MPO, color-coded vs extremes; updates intrabar, settles at HTF close.

Predicted (when MTF OFF): Simple MPO extrapolation using momentum/acceleration—illustrative only.

Thresholds: Current thrHigh/thrLow (static or adaptive).

Components: ASCII bars + values for PRV, MCD, PDI, SMF.

Market metrics: Volume Ratio (x) and ATR% of price.

Strength: Bar indicator of |MPO − 50| × 2.

Confidence: Heuristic gauge (100 in extremes, 70 in warnings, 50 with divergence, else |MPO − 50|). Convenience only, not probability.

How to read the oscillator

MPO Value (0–100): A reading of 50 is neutral. Values above ~55 are increasingly bullish (green), while below ~45 are increasingly bearish (red). Think of these as "market pressure".

Extreme Zones: When MPO climbs into the bright orange/red area (above the base-high line, default 70), the chart will display a dot and downward arrow marking that extreme. Traders often treat this as a sign to tighten stops or look for shorts. Similarly, a bright green dot/up-arrow appears when MPO falls below the base-low (30), hinting at a bullish setup.

Heatmap/Candles: If "Pressure Heatmap" is enabled, the background of the oscillator pane will fade green or red depending on MPO. Users can optionally color the price candles by MPO value (gradient candles) to see these extremes on the main chart.

Prediction Zone(optional): A dashed projection line extends the MPO forward by a small number of bars (prediction_bars) using current MPO momentum and acceleration. This is a heuristic extrapolation best used for short horizons (1–5 bars) to anticipate whether MPO may touch a warning or extreme zone. It is provisional and becomes less reliable with longer projection lengths — always confirm predicted moves with bar-close MPO and HTF context before acting.

Divergences: When price makes a higher high but EPZ makes a lower high (bearish divergence), the indicator can draw dotted lines and a "Bear Div" tag. The opposite (lower low price, higher EPZ) gives "Bull Div". These signals confirm waning momentum at extremes.

Zones: Warning bands near extremes; Extreme zones beyond thresholds.

Crossovers: MPO rising through 35 suggests easing downside pressure; falling through 65 suggests waning upside pressure.

Dots/arrows: Extreme markers appear on closed bars when confirmation is ON and respect the 5-bar cooldown.

Pre-alert dots (optional): Proximity cues in warning zones; also gated to bar close when confirmation is ON.

Histogram: Distance from neutral (50); highlights strengthening or weakening pressure.

Divergence tags: "Bear Div" = higher price high with lower MPO high; "Bull Div" = lower price low with higher MPO low.

Pressure Heatmap : Layered gradient background that visually highlights pressure strength across the MPO scale; adjustable intensity and optional zone overlays (warning / extreme) for quick visual scanning.

A typical reading: If the oscillator is rising from neutral towards the high zone (green→orange→red), the chart may see strong buying culminating in a stall. If it then turns down from the extreme, that peak EPZ dot signals sell pressure.

Alerts

EPZ: Extreme Context — fires on confirmed extremes (respects cooldown).

EPZ: Approaching Threshold — fires in warning zones if no extreme.

EPZ: Divergence — fires on confirmed pivot divergences.

Tip: Set alerts to "Once per bar close" to align with confirmation and avoid intrabar repaint.

Practical usage ideas

Trend continuation: In positive regimes (MPO > 50 and rising), pullbacks holding above 50 often precede continuation; mirror for bearish regimes.

Exhaustion caution: E High/E Low can mark exhaustion risk; many wait for MPO rollover or divergence to time fades or partial exits.

Adaptive thresholds: Useful on assets with shifting volatility regimes to maintain meaningful "extreme" levels.

MTF alignment: Prefer setups that agree with the HTF MPO to reduce countertrend noise.

Examples

Screenshots captured in TradingView Replay to freeze the bar at close so values don't fluctuate intrabar. These examples use default settings and are reproducible on the same bars; they are for illustration, not cherry-picking or performance claims.

Example 1 — BTCUSDT, 1h — E Low

MPO closed at 26.6 (below the 30 extreme), printing a confirmed E Low. HTF MPO is 26.6, so higher-timeframe pressure remains bearish. Components are subdued (Momentum/Pressure/Smart$ ≈ 29–37), with Vol Ratio ≈ 1.19x and ATR% ≈ 0.37%. A prior Bear Div flagged weakening impulse into the drop. With cooldown set to 5 bars, new extremes are rate-limited. Many traders wait for MPO to curl up and reclaim 35 or for a fresh Bull Div before considering countertrend ideas; if MPO cannot reclaim 35 and HTF stays weak, treat bounces cautiously. Educational illustration only.

Example 2 — ETHUSD, 30m — E High

A strong impulse pushed MPO into the extreme zone (≥ 70), printing a confirmed E High on close. Shortly after, MPO cooled to ~61.5 while a Bear Div appeared, showing momentum lag as price pushed a higher high. Volume and volatility were elevated (≈ 1.79x / 1.25%). With a 5-bar cooldown, additional extremes won't print immediately. Some treat E High as exhaustion risk—either waiting for MPO rollover under 65/50 to fade, or for a pullback that holds above 50 to re-join the trend if higher-timeframe pressure remains constructive. Educational illustration only.

Known limitations and caveats

The MPO line itself can change intrabar; extreme markers/alerts do not repaint when "Confirm Extremes on Bar Close" is ON.

HTF values settle at the close of the HTF bar.

Illiquid symbols or very low TFs can be noisy; consider higher thresholds or longer smoothing.

Prediction line (when enabled) is a visual extrapolation only.

For coders

Pine v6. MTF via request.security with lookahead_off.

Extremes include crossover triggers so static thresholds also yield E High/E Low.

Extreme markers and pre-alerts are gated by barstate.isconfirmed when confirmation is ON.

Arrays prune oldest objects to respect resource limits; defaults (80/80/60) are conservative for low TFs.

3D layering uses negative offsets purely for drawing depth (no lookahead).

Screenshot methodology:

To make labels legible and to demonstrate non-repainting behavior, the examples were captured in TradingView Replay with "Confirm Extremes on Bar Close" enabled. Replay is used only to freeze the bar at close so plots don't change intrabar. The examples use default settings, include both Extreme Low and Extreme High cases, and can be reproduced by scrolling to the same bars outside Replay. This is an educational illustration, not a performance claim.

Disclaimer

This script is for educational purposes only and does not constitute financial advice. Markets involve risk; past behavior does not guarantee future results. You are responsible for your own testing, risk management, and decisions.

Historical VolatilityHistorical Volatility Indicator with Custom Trading Sessions

Overview

This indicator calculates **annualized Historical Volatility (HV)** using logarithmic returns and standard deviation. Unlike standard HV indicators, this version allows you to **customize trading sessions and holidays** for different markets, ensuring accurate volatility calculations for options pricing and risk management.

Key Features

✅ Custom Trading Sessions - Define multiple trading sessions per day with precise start/end times

✅ Multiple Markets Support - Pre-configured for US, Russian, European, and crypto markets

✅ Clearing Periods Handling - Account for intraday clearing breaks

✅ Flexible Calendar - Set trading days per year for different countries

✅ All Timeframes - Works correctly on intraday, daily, weekly, and monthly charts

✅ Info Table - Optional display showing calculation parameters

How It Works

The indicator uses the classical volatility formula:

σ_annual = σ_period × √(periods per year)

Where:

- σ_period = Standard deviation of logarithmic returns over the specified period

- Periods per year = Calculated based on actual trading time (not calendar time)

Calculation Method

1. Computes log returns: ln(close / close )

2. Calculates standard deviation over the lookback period