ArbitrageDashboardv3310824This indicator allows you to monitor the spread (difference in exchange rates) between two assets in real-time for up to 12 trading pairs simultaneously.

⚙️ How does the indicator work?

In the settings menu, you can select two trading pairs, such as BTCUSDT on Binance and BTCUSDT on Bybit. The script then fetches prices from both exchanges and compares them, calculating the percentage difference (spread). This process is repeated for all 12 trading pairs added in the settings. The script works only with the assets and exchanges available on TradingView.

⚡️ How to use it?

When the spread is negative, it means the asset's price on the first exchange is lower than on the second. By buying on the first exchange and selling on the second, you can make a profit (taking into account the exchange fees). When the spread is positive, the opposite is true. The buy prices and exchanges are shown in a green Buy row, while sell prices and exchanges are displayed in a red Sell row. If the spread is zero, prices are the same on both exchanges, and no arbitrage opportunity exists. For better accuracy, use the smallest timeframe available in your TradingView subscription, such as minute or second intervals.

🕒 Arbitrage Situation Counter

For each trading pair, the table below the Buy row shows the number of arbitrage situations within a specified timeframe. An arbitrage situation occurs when the spread exceeds the Signal Threshold Level set by the user. Each time this happens, the counter increases by one. It only counts situations that occurred within the selected timeframe, such as the past hour for a 1-hour period. You can track arbitrage situations for up to three different periods simultaneously, ranging from 5 minutes to 24 hours. This counter helps evaluate the potential for arbitrage in the selected trading pairs. If a pair shows only 1-2 arbitrage situations per hour, it might be better to look for another pair.

🔔 Setting Up Alerts

In the script settings, you can set the Spread Signal Threshold. When the spread reaches this level, the table for that asset will be highlighted. This threshold also acts as a signal for setting up alerts. To set alerts, go to the Alerts tab in the TradingView menu on the right, click "Create Alert", and select this indicator under "Condition". You can then name the alert and finish the setup by clicking "Create".

We, the authors, have long been involved in cryptocurrency arbitrage and created this script for our own trading, but you can use it for any assets and markets as you see fit.

We also offer lighter versions of the indicator that track the spread for one or three trading pairs. These versions also display the spread chart, which can be useful for historical analysis. If the full indicator is too resource-intensive for your device, try these lighter versions:

🧩 Arbitrage Spread v1 : 1 pair + 1 chart

🧩 Arbitrage Spread v2 : 3 pairs + 3 charts

If your hardware can handle it, you can use the 12-pair version as a dashboard and add one of the versions with a spread chart for a detailed view of one or three pairs.

--

Этот индикатор позволяет в реальном времени отслеживать изменение спреда (разницы в цене) между двумя активами для 12 торговых пар одновременно.

⚙️ Как работает индикатор?

В меню настроек индикатора пользователь выбирает две торговые пары, например BTCUSDT на бирже Binance и BTCUSDT на бирже Bybit. Скрипт получает цены с обеих бирж и сравнивает их, рассчитывая процентное отклонение (спред). Этот процесс выполняется для всех 12 торговых пар, указанных в настройках. Скрипт работает только с теми активами и биржами, которые доступны на TradingView.

⚡️ Как использовать?

Когда спред отрицательный, это означает, что цена на первый актив ниже, чем на второй. В таком случае можно купить актив на первой бирже и продать на второй, получив прибыль (не забывая учитывать биржевые комиссии). Когда спред положительный, ситуация обратная. Биржи и цены для покупки отображаются в зеленой строке Buy, а для продажи – в красной строке Sell. При нулевом спреде цены на обеих биржах одинаковы, и арбитражная ситуация отсутствует.

Для повышения точности индикатора используйте минимально доступный таймфрейм на TradingView – минутный или секундный.

🕒 Счетчик арбитражных ситуаций

По каждой торговой паре в таблице под строкой Buy отображается количество арбитражных ситуаций за определенный промежуток времени. Арбитражная ситуация возникает, когда спред превышает установленный пользователем сигнальный уровень (Signal Threshold Level). При каждом превышении этого уровня счетчик увеличивается на единицу. Счетчик учитывает арбитражные ситуации за определенный период, например, за последний час для 1-часового периода (1h). Можно отслеживать количество арбитражных ситуаций одновременно для трех временных периодов от 5 минут до суток.

Счетчик помогает оценить перспективность арбитража выбранных пар. Если за час на паре было всего 1-2 арбитражные ситуации, возможно, лучше поискать другую пару.

🔔 Настройка оповещений

В настройках скрипта можно задать пороговое значение спреда (Spread Signal Threshold). Когда спред достигнет этого уровня, таблица для данного актива будет подсвечена. Этот уровень также служит сигналом для настройки оповещений.

Для настройки оповещений откройте вкладку «Оповещения» в меню TradingView справа. Нажмите кнопку «Создать оповещение». В открывшемся окне в строке «Условие» выберите данный индикатор. Затем задайте название и завершите настройку, нажав кнопку «Создать».

Мы, авторы этого скрипта, давно занимаемся арбитражем криптовалют и создали его для себя, но вы можете использовать его для любых активов и на любых рынках по своему усмотрению.

У нас также есть более простая версия индикатора, которая отслеживает спред для одной или трех торговых пар. В этих версиях можно просматривать график самого спреда, что полезно для оценки его динамики. Если этот индикатор кажется вам или вашему устройству слишком тяжелым, вы можете воспользоваться облегченными версиями:

🧩 Arbitrage Spread v1 : 1 пара + 1 график

🧩 Arbitrage Spread v2 : 3 пары + 3 графика

Если ваше оборудование позволяет, вы можете добавить несколько индикаторов на экран. Например, использовать версию с 12 парами как дашборд, а одну из версий с графиком спреда для более детального анализа по одному или трем инструментам.

Cerca negli script per "跨境通12月4日地天板"

PubLibTrendLibrary "PubLibTrend"

trend, multi-part trend, double trend and multi-part double trend conditions for indicator and strategy development

rlut()

return line uptrend condition

Returns: bool

dt()

downtrend condition

Returns: bool

ut()

uptrend condition

Returns: bool

rldt()

return line downtrend condition

Returns: bool

dtop()

double top condition

Returns: bool

dbot()

double bottom condition

Returns: bool

rlut_1p()

1-part return line uptrend condition

Returns: bool

rlut_2p()

2-part return line uptrend condition

Returns: bool

rlut_3p()

3-part return line uptrend condition

Returns: bool

rlut_4p()

4-part return line uptrend condition

Returns: bool

rlut_5p()

5-part return line uptrend condition

Returns: bool

rlut_6p()

6-part return line uptrend condition

Returns: bool

rlut_7p()

7-part return line uptrend condition

Returns: bool

rlut_8p()

8-part return line uptrend condition

Returns: bool

rlut_9p()

9-part return line uptrend condition

Returns: bool

rlut_10p()

10-part return line uptrend condition

Returns: bool

rlut_11p()

11-part return line uptrend condition

Returns: bool

rlut_12p()

12-part return line uptrend condition

Returns: bool

rlut_13p()

13-part return line uptrend condition

Returns: bool

rlut_14p()

14-part return line uptrend condition

Returns: bool

rlut_15p()

15-part return line uptrend condition

Returns: bool

rlut_16p()

16-part return line uptrend condition

Returns: bool

rlut_17p()

17-part return line uptrend condition

Returns: bool

rlut_18p()

18-part return line uptrend condition

Returns: bool

rlut_19p()

19-part return line uptrend condition

Returns: bool

rlut_20p()

20-part return line uptrend condition

Returns: bool

rlut_21p()

21-part return line uptrend condition

Returns: bool

rlut_22p()

22-part return line uptrend condition

Returns: bool

rlut_23p()

23-part return line uptrend condition

Returns: bool

rlut_24p()

24-part return line uptrend condition

Returns: bool

rlut_25p()

25-part return line uptrend condition

Returns: bool

rlut_26p()

26-part return line uptrend condition

Returns: bool

rlut_27p()

27-part return line uptrend condition

Returns: bool

rlut_28p()

28-part return line uptrend condition

Returns: bool

rlut_29p()

29-part return line uptrend condition

Returns: bool

rlut_30p()

30-part return line uptrend condition

Returns: bool

dt_1p()

1-part downtrend condition

Returns: bool

dt_2p()

2-part downtrend condition

Returns: bool

dt_3p()

3-part downtrend condition

Returns: bool

dt_4p()

4-part downtrend condition

Returns: bool

dt_5p()

5-part downtrend condition

Returns: bool

dt_6p()

6-part downtrend condition

Returns: bool

dt_7p()

7-part downtrend condition

Returns: bool

dt_8p()

8-part downtrend condition

Returns: bool

dt_9p()

9-part downtrend condition

Returns: bool

dt_10p()

10-part downtrend condition

Returns: bool

dt_11p()

11-part downtrend condition

Returns: bool

dt_12p()

12-part downtrend condition

Returns: bool

dt_13p()

13-part downtrend condition

Returns: bool

dt_14p()

14-part downtrend condition

Returns: bool

dt_15p()

15-part downtrend condition

Returns: bool

dt_16p()

16-part downtrend condition

Returns: bool

dt_17p()

17-part downtrend condition

Returns: bool

dt_18p()

18-part downtrend condition

Returns: bool

dt_19p()

19-part downtrend condition

Returns: bool

dt_20p()

20-part downtrend condition

Returns: bool

dt_21p()

21-part downtrend condition

Returns: bool

dt_22p()

22-part downtrend condition

Returns: bool

dt_23p()

23-part downtrend condition

Returns: bool

dt_24p()

24-part downtrend condition

Returns: bool

dt_25p()

25-part downtrend condition

Returns: bool

dt_26p()

26-part downtrend condition

Returns: bool

dt_27p()

27-part downtrend condition

Returns: bool

dt_28p()

28-part downtrend condition

Returns: bool

dt_29p()

29-part downtrend condition

Returns: bool

dt_30p()

30-part downtrend condition

Returns: bool

ut_1p()

1-part uptrend condition

Returns: bool

ut_2p()

2-part uptrend condition

Returns: bool

ut_3p()

3-part uptrend condition

Returns: bool

ut_4p()

4-part uptrend condition

Returns: bool

ut_5p()

5-part uptrend condition

Returns: bool

ut_6p()

6-part uptrend condition

Returns: bool

ut_7p()

7-part uptrend condition

Returns: bool

ut_8p()

8-part uptrend condition

Returns: bool

ut_9p()

9-part uptrend condition

Returns: bool

ut_10p()

10-part uptrend condition

Returns: bool

ut_11p()

11-part uptrend condition

Returns: bool

ut_12p()

12-part uptrend condition

Returns: bool

ut_13p()

13-part uptrend condition

Returns: bool

ut_14p()

14-part uptrend condition

Returns: bool

ut_15p()

15-part uptrend condition

Returns: bool

ut_16p()

16-part uptrend condition

Returns: bool

ut_17p()

17-part uptrend condition

Returns: bool

ut_18p()

18-part uptrend condition

Returns: bool

ut_19p()

19-part uptrend condition

Returns: bool

ut_20p()

20-part uptrend condition

Returns: bool

ut_21p()

21-part uptrend condition

Returns: bool

ut_22p()

22-part uptrend condition

Returns: bool

ut_23p()

23-part uptrend condition

Returns: bool

ut_24p()

24-part uptrend condition

Returns: bool

ut_25p()

25-part uptrend condition

Returns: bool

ut_26p()

26-part uptrend condition

Returns: bool

ut_27p()

27-part uptrend condition

Returns: bool

ut_28p()

28-part uptrend condition

Returns: bool

ut_29p()

29-part uptrend condition

Returns: bool

ut_30p()

30-part uptrend condition

Returns: bool

rldt_1p()

1-part return line downtrend condition

Returns: bool

rldt_2p()

2-part return line downtrend condition

Returns: bool

rldt_3p()

3-part return line downtrend condition

Returns: bool

rldt_4p()

4-part return line downtrend condition

Returns: bool

rldt_5p()

5-part return line downtrend condition

Returns: bool

rldt_6p()

6-part return line downtrend condition

Returns: bool

rldt_7p()

7-part return line downtrend condition

Returns: bool

rldt_8p()

8-part return line downtrend condition

Returns: bool

rldt_9p()

9-part return line downtrend condition

Returns: bool

rldt_10p()

10-part return line downtrend condition

Returns: bool

rldt_11p()

11-part return line downtrend condition

Returns: bool

rldt_12p()

12-part return line downtrend condition

Returns: bool

rldt_13p()

13-part return line downtrend condition

Returns: bool

rldt_14p()

14-part return line downtrend condition

Returns: bool

rldt_15p()

15-part return line downtrend condition

Returns: bool

rldt_16p()

16-part return line downtrend condition

Returns: bool

rldt_17p()

17-part return line downtrend condition

Returns: bool

rldt_18p()

18-part return line downtrend condition

Returns: bool

rldt_19p()

19-part return line downtrend condition

Returns: bool

rldt_20p()

20-part return line downtrend condition

Returns: bool

rldt_21p()

21-part return line downtrend condition

Returns: bool

rldt_22p()

22-part return line downtrend condition

Returns: bool

rldt_23p()

23-part return line downtrend condition

Returns: bool

rldt_24p()

24-part return line downtrend condition

Returns: bool

rldt_25p()

25-part return line downtrend condition

Returns: bool

rldt_26p()

26-part return line downtrend condition

Returns: bool

rldt_27p()

27-part return line downtrend condition

Returns: bool

rldt_28p()

28-part return line downtrend condition

Returns: bool

rldt_29p()

29-part return line downtrend condition

Returns: bool

rldt_30p()

30-part return line downtrend condition

Returns: bool

dut()

double uptrend condition

Returns: bool

ddt()

double downtrend condition

Returns: bool

dut_1p()

1-part double uptrend condition

Returns: bool

dut_2p()

2-part double uptrend condition

Returns: bool

dut_3p()

3-part double uptrend condition

Returns: bool

dut_4p()

4-part double uptrend condition

Returns: bool

dut_5p()

5-part double uptrend condition

Returns: bool

dut_6p()

6-part double uptrend condition

Returns: bool

dut_7p()

7-part double uptrend condition

Returns: bool

dut_8p()

8-part double uptrend condition

Returns: bool

dut_9p()

9-part double uptrend condition

Returns: bool

dut_10p()

10-part double uptrend condition

Returns: bool

dut_11p()

11-part double uptrend condition

Returns: bool

dut_12p()

12-part double uptrend condition

Returns: bool

dut_13p()

13-part double uptrend condition

Returns: bool

dut_14p()

14-part double uptrend condition

Returns: bool

dut_15p()

15-part double uptrend condition

Returns: bool

dut_16p()

16-part double uptrend condition

Returns: bool

dut_17p()

17-part double uptrend condition

Returns: bool

dut_18p()

18-part double uptrend condition

Returns: bool

dut_19p()

19-part double uptrend condition

Returns: bool

dut_20p()

20-part double uptrend condition

Returns: bool

dut_21p()

21-part double uptrend condition

Returns: bool

dut_22p()

22-part double uptrend condition

Returns: bool

dut_23p()

23-part double uptrend condition

Returns: bool

dut_24p()

24-part double uptrend condition

Returns: bool

dut_25p()

25-part double uptrend condition

Returns: bool

dut_26p()

26-part double uptrend condition

Returns: bool

dut_27p()

27-part double uptrend condition

Returns: bool

dut_28p()

28-part double uptrend condition

Returns: bool

dut_29p()

29-part double uptrend condition

Returns: bool

dut_30p()

30-part double uptrend condition

Returns: bool

ddt_1p()

1-part double downtrend condition

Returns: bool

ddt_2p()

2-part double downtrend condition

Returns: bool

ddt_3p()

3-part double downtrend condition

Returns: bool

ddt_4p()

4-part double downtrend condition

Returns: bool

ddt_5p()

5-part double downtrend condition

Returns: bool

ddt_6p()

6-part double downtrend condition

Returns: bool

ddt_7p()

7-part double downtrend condition

Returns: bool

ddt_8p()

8-part double downtrend condition

Returns: bool

ddt_9p()

9-part double downtrend condition

Returns: bool

ddt_10p()

10-part double downtrend condition

Returns: bool

ddt_11p()

11-part double downtrend condition

Returns: bool

ddt_12p()

12-part double downtrend condition

Returns: bool

ddt_13p()

13-part double downtrend condition

Returns: bool

ddt_14p()

14-part double downtrend condition

Returns: bool

ddt_15p()

15-part double downtrend condition

Returns: bool

ddt_16p()

16-part double downtrend condition

Returns: bool

ddt_17p()

17-part double downtrend condition

Returns: bool

ddt_18p()

18-part double downtrend condition

Returns: bool

ddt_19p()

19-part double downtrend condition

Returns: bool

ddt_20p()

20-part double downtrend condition

Returns: bool

ddt_21p()

21-part double downtrend condition

Returns: bool

ddt_22p()

22-part double downtrend condition

Returns: bool

ddt_23p()

23-part double downtrend condition

Returns: bool

ddt_24p()

24-part double downtrend condition

Returns: bool

ddt_25p()

25-part double downtrend condition

Returns: bool

ddt_26p()

26-part double downtrend condition

Returns: bool

ddt_27p()

27-part double downtrend condition

Returns: bool

ddt_28p()

28-part double downtrend condition

Returns: bool

ddt_29p()

29-part double downtrend condition

Returns: bool

ddt_30p()

30-part double downtrend condition

Returns: bool

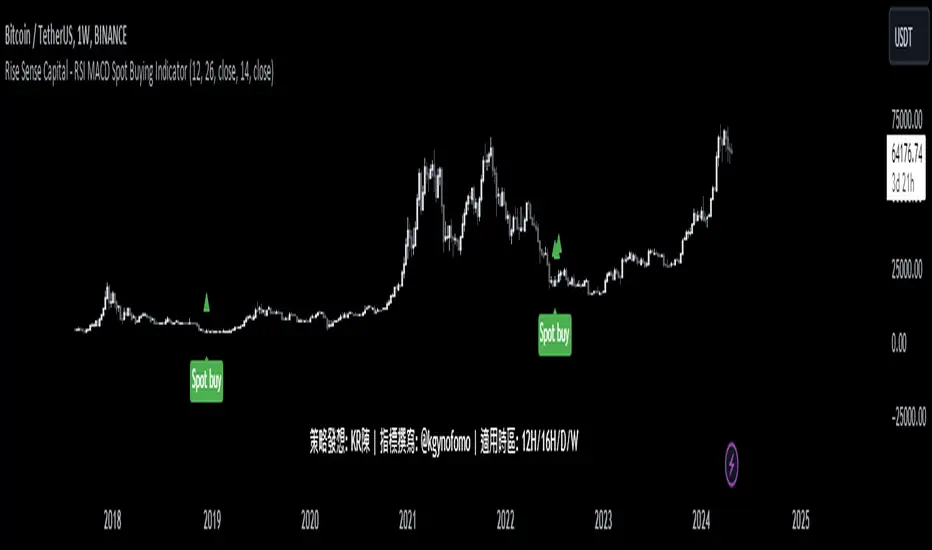

Rise Sense Capital - RSI MACD Spot Buying IndicatorToday, I'll share a spot buying strategy shared by a member @KR陳 within the DATA Trader Alliance Alpha group. First, you need to prepare two indicators:

今天分享一個DATA交易者聯盟Alpha群組裏面的群友@KR陳分享的現貨買入策略。

首先需要準備兩個指標

RSI Indicator (Relative Strength Index) - RSI is a technical analysis tool based on price movements over a period of time to evaluate the speed and magnitude of price changes. RSI calculates the changes in price over a period to determine whether the recent trend is relatively strong (bullish) or weak (bearish).

RSI指標,(英文全名:Relative Strength Index),中文稱為「相對強弱指標」,是一種以股價漲跌為基礎,在一段時間內的收盤價,用於評估價格變動的速度 (快慢) 與變化 (幅度) 的技術分析工具,RSI藉由計算一段期間內股價的漲跌變化,判斷最近的趨勢屬於偏強 (偏多) 還是偏弱 (偏空)。

MACD Indicator (Moving Average Convergence & Divergence) - MACD is a technical analysis tool proposed by Gerald Appel in the 1970s. It is commonly used in trading to determine trend reversals by analyzing the convergence and divergence of fast and slow lines.

MACD 指標 (Moving Average Convergence & Divergence) 中文名為平滑異同移動平均線指標,MACD 是在 1970 年代由美國人 Gerald Appel 所提出,是一項歷史悠久且經常在交易中被使用的技術分析工具,原理是利用快慢線的交錯,藉以判斷股價走勢的轉折。

In MACD analysis, the most commonly used values are 12, 26, and 9, known as MACD (12,26,9). The market often uses the MACD indicator to determine the future direction of assets and to identify entry and exit points.

在 MACD 的技術分析中,最常用的值為 12 天、26 天、9 天,也稱為 MACD (12,26,9),市場常用 MACD 指標來判斷操作標的的後市走向,確定波段漲幅並找到進、出場點。

Strategy analysis by member KR陳:

策略解析 by群友 KR陳 :

Condition 1: RSI value in the previous candle is below oversold zone(30).

條件1:RSI 在前一根的數值低於超賣區(30)

buycondition1 = RSI <30

Condition 2: MACD histogram changes from decreasing to increasing.

條件2:MACD柱由遞減轉遞增

buycondition2 = hist >hist and hist

Absolute Momentum (Time Series Momentum)Absolute momentum , also known as time series momentum , focuses on the trend of an asset's own past performance to predict its future performance. It involves analyzing an asset's own historical performance, rather than comparing it to other assets.

The strategy determines whether an asset's price is exhibiting an upward (positive momentum) or downward (negative momentum) trend by assessing the asset's return over a given period (standard look-back period: 12 months or approximately 250 trading days). Some studies recommend calculating momentum by deducting the corresponding Treasury bill rate from the measured performance.

Absolute Momentum Indicator

The Absolute Momentum Indicator displays the rolling 12-month performance (measured over 250 trading days) and plots it against a horizontal line representing 0%. If the indicator crosses above this line, it signifies positive absolute momentum, and conversely, crossing below indicates negative momentum. An additional, optional look-back period input field can be accessed through the settings.

Hint: This indicator is a simplified version, as some academic approaches measure absolute momentum by subtracting risk-free rates from the 12-month performance. However, even with higher rates, the values will still remain close to the 0% line.

Benefits of Absolute Momentum

Absolute momentum, which should not be confused with relative momentum or the momentum indicator, serves as a timing instrument for both individual assets and entire markets.

Gary Antonacci , a key contributor to the absolute momentum strategy (find study below), emphasizes its effectiveness in multi-asset portfolios and its importance in long-only investing. This is particularly evident in a) reducing downside volatility and b) mitigating behavioral biases.

Moskowitz, Ooi, and Pedersen document significant 'time series momentum' across various asset classes, including equity index, currency, commodity, and bond futures, in 58 liquid instruments (find study below). There's a notable persistence in returns ranging from one to 12 months, which tends to partially reverse over longer periods. This pattern aligns with sentiment theories suggesting initial under-reaction followed by delayed over-reaction.

Despite its surprising ease of implementation, the academic community has successfully measured the effects of absolute momentum across decades and in every major asset class, including stocks, bonds, commodities, and foreign exchange (FX).

Strategies for Implementing Absolute Momentum:

To Buy a Stock:

Select a Look-Back Period: Choose a historical period to analyze the stock's performance. A common period is 12 months, but this can vary based on your investment strategy.

Calculate Excess Return: Determine the stock's excess return over this period. You can also assume a risk-free rate of "0" to simplify the process.

Evaluate Momentum:

If the excess return is positive, it indicates positive absolute momentum. This suggests the stock is in an upward trend and could be a good buying opportunity.

If the excess return is negative, it suggests negative momentum, and you might want to delay buying.

Consider further conditions: Align your decision with broader market trends, economic indicators, or fundamental analysis, for additional context.

To Sell a Stock You Own:

Regularly Monitor Performance: Use the same look-back period as for buying (e.g., 12 months) to regularly assess the stock's performance.

Check for Negative Momentum: Calculate the excess return for the look-back period. Again, you can assume a risk-free rate of "0" to simplify the process. If the stock shows negative momentum, it might be time to consider selling.

Consider further conditions:Align your decision with broader market trends, economic indicators, or fundamental analysis, for additional context.

Important note: Note: Entering a position (i.e., buying) based on positive absolute momentum doesn't necessarily mean you must sell it if it later exhibits negative absolute momentum. You can initiate a position using positive absolute momentum as an entry indicator and then continue holding it based on other criteria, such as fundamental analysis.

General Tips:

Reassessment Frequency: Decide how often you will reassess the momentum (monthly, quarterly, etc.).

Remember, while absolute momentum provides a systematic approach, it's recommendable to consider it as part of a broader investment strategy that includes diversification, risk management, fundamental analysis, etc.

Relevant Capital Market Studies:

Antonacci, Gary. "Absolute momentum: A simple rule-based strategy and universal trend-following overlay." Available at SSRN 2244633 (2013)

Moskowitz, Tobias J., Yao Hua Ooi, and Lasse Heje Pedersen. "Time series momentum." Journal of financial economics 104.2 (2012): 228-250

S&P 500 Quandl Data & RatiosTradingView has a little-known integration that allows you to pull in 3rd party data-sets from Nasdaq Data Link, also known as Quandl. Today, I am open-sourcing for the community an indicator that uses the Quandl integration to pull in historical data and ratios on the S&P500. I originally coded this to study macro P/E ratios during peaks and troughs of boom/bust cycles.

The indicator pulls in each of the following datasets, as defined and provided by Quandl. The user can select which datasets to pull in using the indicator settings:

Dividend Yield : S&P 500 dividend yield (12 month dividend per share)/price. Yields following June 2022 (including the current yield) are estimated based on 12 month dividends through June 2022, as reported by S&P. Sources: Standard & Poor's for current S&P 500 Dividend Yield. Robert Shiller and his book Irrational Exuberance for historic S&P 500 Dividend Yields.

Price Earning Ratio : Price to earnings ratio, based on trailing twelve month as reported earnings. Current PE is estimated from latest reported earnings and current market price. Source: Robert Shiller and his book Irrational Exuberance for historic S&P 500 PE Ratio.

CAPE/Shiller PE Ratio : Shiller PE ratio for the S&P 500. Price earnings ratio is based on average inflation-adjusted earnings from the previous 10 years, known as the Cyclically Adjusted PE Ratio (CAPE Ratio), Shiller PE Ratio, or PE 10 FAQ. Data courtesy of Robert Shiller from his book, Irrational Exuberance.

Earnings Yield : S&P 500 Earnings Yield. Earnings Yield = trailing 12 month earnings divided by index price (or inverse PE) Yields following March, 2022 (including current yield) are estimated based on 12 month earnings through March, 2022 the latest reported by S&P. Source: Standard & Poor's

Price Book Ratio : S&P 500 price to book value ratio. Current price to book ratio is estimated based on current market price and S&P 500 book value as of March, 2022 the latest reported by S&P. Source: Standard & Poor's

Price Sales Ratio : S&P 500 Price to Sales Ratio (P/S or Price to Revenue). Current price to sales ratio is estimated based on current market price and 12 month sales ending March, 2022 the latest reported by S&P. Source: Standard & Poor's

Inflation Adjusted SP500 : Inflation adjusted SP500. Other than the current price, all prices are monthly average closing prices. Sources: Standard & Poor's Robert Shiller and his book Irrational Exuberance for historic S&P 500 prices, and historic CPIs.

Revenue Per Share : Trailing twelve month S&P 500 Sales Per Share (S&P 500 Revenue Per Share) non-inflation adjusted current dollars. Source: Standard & Poor's

Earnings Per Share : S&P 500 Earnings Per Share. 12-month real earnings per share inflation adjusted, constant August, 2022 dollars. Sources: Standard & Poor's for current S&P 500 Earnings. Robert Shiller and his book Irrational Exuberance for historic S&P 500 Earnings.

Disclaimer: This is not financial advice. Open-source scripts I publish in the community are largely meant to spark ideas that can be used as building blocks for part of a more robust trade management strategy. If you would like to implement a version of any script, I would recommend making significant additions/modifications to the strategy & risk management functions. If you don’t know how to program in Pine, then hire a Pine-coder. We can help!

Argo II - (alerts for 3commas composite bots) - publicThis script lets users create BUY/SELL alerts for 3commas composite bots (1 alert = 12 pairs) in a simple way, based on a built in set of indicators that can be tweaked to work together or alone through the study settings.

There is a version of this script for single pair bots, with slightly more features here .

If the user choses to create both BUY and SELL signals from the study settings, the (1) alert created will send both BUY and SELL signals for all 12 pairs selected. At this stage, the script forces the user to select 12 pairs in the study settings. If less pairs are inserted, it will not work. Also, the script will only send alerts for the pairs selected in the study settings, not for the current chart (if different).

How to use:

- Add the script to the current chart

- Open the study settings , insert bot details and select 12 pairs. You should write the pairs manually, using the format BTC , ADA, ETH, etc. They MUST be in capital letters or 3commas will not recognize them.

- Still in the study settings, tweak the deal start/close conditions from various indicators until happy. The study will plot the entry / exit points below the current chart (1 = buy, 2 = sell)

- Make sure your strategy works for all the pairs you have selected, simply by checking each chart with the same study settings

- When happy, right click on the "..." next to the study name, then "Add alert'".

- Under "Condition", on the second line, chose "Any alert () function call". Add the webhook from 3commas, give it a name, and "create".

That's it.

Notes:

- If you insert coins that are not available for the quote currency and exchange of your choosing, the script will not work and return an error.

- Make sure you run tests with paper trading or dummy bots (i.e without actual bot ID) to ensure your alerts trigger as intended on all coins.

- If alerts trigger too much (i.e they all trigger at the same time for all coins), Trading View will stop the alert. So probably not ideal for a scalping bot. It could also be the sign the script doesn't work as intended.

- The script is a bit slow on my side. I am a beginner in pinescript, so if anyone knows how to simplify it, please let me know.

- if anyone knows how to tell the script to function with less than 12 pairs (when not filling the 12 fields in the setting), please also let me know :)

XPloRR MA-Buy ATR-Trailing-Stop Long Term Strategy Beating B&HXPloRR MA-Buy ATR-MA-Trailing-Stop Strategy

Long term MA Trailing Stop strategy to beat Buy&Hold strategy

None of the strategies that I tested can beat the long term Buy&Hold strategy. That's the reason why I wrote this strategy.

Purpose: beat Buy&Hold strategy with around 10 trades. 100% capitalize sold trade into new trade.

My buy strategy is triggered by the EMA(blue) crossing over the SMA curve(orange).

My sell strategy is triggered by another EMA(lime) of the close value crossing the trailing stop(green) value.

The trailing stop value(green) is set to a multiple of the ATR(15) value.

ATR(15) is the SMA(15) value of the difference between high and low values.

Every stock has it's own "DNA", so first thing to do is find the right parameters to get the best strategy values voor EMA, SMA and Trailing Stop.

Then keep using these parameter for future buy/sell signals only for that particular stock.

Do the same for other stocks.

Here are the parameters:

Exponential MA: buy trigger when crossing over the SMA value (use values between 11-50)

Simple MA: buy trigger when EMA crosses over the SMA value (use values between 20 and 200)

Stop EMA: sell trigger when Stop EMA of close value crosses under the trailing stop value (use values between 8 and 16)

Trailing Stop #ATR: defines the trailing stop value as a multiple of the ATR(15) value

Example parameters for different stocks (Start capital: 1000, Order=100% of equity, Period 1/1/2005 to now):

BAR(Barco): EMA=11, SMA=82, StopEMA=12, Stop#ATR=9

Buy&HoldProfit: 45.82%, NetProfit: 294.7%, #Trades:8, %Profit:62.5%, ProfitFactor: 12.539

AAPL(Apple): EMA=12, SMA=45, StopEMA=12, Stop#ATR=6

Buy&HoldProfit: 2925.86%, NetProfit: 4035.92%, #Trades:10, %Profit:60%, ProfitFactor: 6.36

BEKB(Bekaert): EMA=12, SMA=42, StopEMA=12, Stop#ATR=7

Buy&HoldProfit: 81.11%, NetProfit: 521.37%, #Trades:10, %Profit:60%, ProfitFactor: 2.617

SOLB(Solvay): EMA=12, SMA=63, StopEMA=11, Stop#ATR=8

Buy&HoldProfit: 43.61%, NetProfit: 151.4%, #Trades:8, %Profit:75%, ProfitFactor: 3.794

PHIA(Philips): EMA=11, SMA=80, StopEMA=8, Stop#ATR=10

Buy&HoldProfit: 56.79%, NetProfit: 198.46%, #Trades:6, %Profit:83.33%, ProfitFactor: 23.07

I am very curious to see the parameters for your stocks and please make suggestions to improve this strategy.

Dskyz (DAFE) Quantum Sentiment Flux - Beginners Dskyz (DAFE) Quantum Sentiment Flux - Beginners:

Welcome to the Dskyz (DAFE) Quantum Sentiment Flux - Beginners , a strategy and concept that’s your ultimate wingman for trading futures like MNQ, NQ, MES, and ES. This gem combines lightning-fast momentum signals, market sentiment smarts, and bulletproof risk management into a system so intuitive, even newbies can trade like pros. With clean DAFE visuals, preset modes for every vibe, and a revamped dashboard that’s basically a market GPS, this strategy makes futures trading feel like a high-octane sci-fi mission.

Built on the Dskyz (DAFE) legacy of Aurora Divergence, the Quantum Sentiment Flux is designed to empower beginners while giving seasoned traders a lean, sentiment-driven edge. It uses fast/slow EMA crossovers for entries, filters trades with VIX, SPX trends, and sector breadth, and keeps your account safe with adaptive stops and cooldowns. Tuned for more action with faster signals and a slick bottom-left dashboard, this updated version is ready to light up your charts and outsmart institutional traps. Let’s dive into why this strat’s a must-have and break down its brilliance.

Why Traders Need This Strategy

Futures markets are a wild ride—fast moves, volatility spikes (like the April 28, 2025 NQ 1k-point drop), and institutional games that can wreck unprepared traders. Beginners often get lost in complex systems or burned by impulsive trades. The Quantum Sentiment Flux is the antidote, offering:

Dead-Simple Setup: Preset modes (Aggressive, Balanced, Conservative) auto-tune signals, risk, and sizing, so you can trade without a quant degree.

Sentiment Superpower: VIX filter, SPX trend, and sector breadth visuals keep you aligned with market health, dodging chop and riding trends.

Ironclad Safety: Tighter ATR-based stops, 2:1 take-profits, and preset cooldowns protect your capital, even in chaotic sessions.

Next-Level Visuals: Green/red entry triangles, vibrant EMAs, a sector breadth background, and a beefed-up dashboard make signals and context pop.

DAFE Swagger: The clean aesthetics, sleek dashboard—ties it to Dskyz’s elite brand, making your charts a work of art.

Traders need this because it’s a plug-and-play system that blends beginner-friendly simplicity with pro-level market awareness. Whether you’re just starting or scalping 5min MNQ, this strat’s your key to trading with confidence and style.

Strategy Components

1. Core Signal Logic (High-Speed Momentum)

The strategy’s engine is a momentum-based system using fast and slow Exponential Moving Averages (EMAs), now tuned for faster, more frequent trades.

How It Works:

Fast/Slow EMAs: Fast EMA (Aggressive: 5, Balanced: 7, Conservative: 9 bars) and slow EMA (12/14/18 bars) track short-term vs. longer-term momentum.

Crossover Signals:

Buy: Fast EMA crosses above slow EMA, and trend_dir = 1 (fast EMA > slow EMA + ATR * strength threshold).

Sell: Fast EMA crosses below slow EMA, and trend_dir = -1 (fast EMA < slow EMA - ATR * strength threshold).

Strength Filter: ma_strength = fast EMA - slow EMA must exceed an ATR-scaled threshold (Aggressive: 0.15, Balanced: 0.18, Conservative: 0.25) for robust signals.

Trend Direction: trend_dir confirms momentum, filtering out weak crossovers in choppy markets.

Evolution:

Faster EMAs (down from 7–10/21–50) catch short-term trends, perfect for active futures markets.

Lower strength thresholds (0.15–0.25 vs. 0.3–0.5) make signals more sensitive, boosting trade frequency without sacrificing quality.

Preset tuning ensures beginners get optimized settings, while pros can tweak via mode selection.

2. Market Sentiment Filters

The strategy leans hard into market sentiment with a VIX filter, SPX trend analysis, and sector breadth visuals, keeping trades aligned with the big picture.

VIX Filter:

Logic: Blocks long entries if VIX > threshold (default: 20, can_long = vix_close < vix_limit). Shorts are always allowed (can_short = true).

Impact: Prevents longs during high-fear markets (e.g., VIX spikes in crashes), while allowing shorts to capitalize on downturns.

SPX Trend Filter:

Logic: Compares S&P 500 (SPX) close to its SMA (Aggressive: 5, Balanced: 8, Conservative: 12 bars). spx_trend = 1 (UP) if close > SMA, -1 (DOWN) if < SMA, 0 (FLAT) if neutral.

Impact: Provides dashboard context, encouraging trades that align with market direction (e.g., longs in UP trend).

Sector Breadth (Visual):

Logic: Tracks 10 sector ETFs (XLK, XLF, XLE, etc.) vs. their SMAs (same lengths as SPX). Each sector scores +1 (bullish), -1 (bearish), or 0 (neutral), summed as breadth (-10 to +10).

Display: Green background if breadth > 4, red if breadth < -4, else neutral. Dashboard shows sector trends (↑/↓/-).

Impact: Faster SMA lengths make breadth more responsive, reflecting sector rotations (e.g., tech surging, energy lagging).

Why It’s Brilliant:

- VIX filter adds pro-level volatility awareness, saving beginners from panic-driven losses.

- SPX and sector breadth give a 360° view of market health, boosting signal confidence (e.g., green BG + buy signal = high-probability trade).

- Shorter SMAs make sentiment visuals react faster, perfect for 5min charts.

3. Risk Management

The risk controls are a fortress, now tighter and more dynamic to support frequent trading while keeping accounts safe.

Preset-Based Risk:

Aggressive: Fast EMAs (5/12), tight stops (1.1x ATR), 1-bar cooldown. High trade frequency, higher risk.

Balanced: EMAs (7/14), 1.2x ATR stops, 1-bar cooldown. Versatile for most traders.

Conservative: EMAs (9/18), 1.3x ATR stops, 2-bar cooldown. Safer, fewer trades.

Impact: Auto-scales risk to match style, making it foolproof for beginners.

Adaptive Stops and Take-Profits:

Logic: Stops = entry ± ATR * atr_mult (1.1–1.3x, down from 1.2–2.0x). Take-profits = entry ± ATR * take_mult (2x stop distance, 2:1 reward/risk). Longs: stop below entry, TP above; shorts: vice versa.

Impact: Tighter stops increase trade turnover while maintaining solid risk/reward, adapting to volatility.

Trade Cooldown:

Logic: Preset-driven (Aggressive/Balanced: 1 bar, Conservative: 2 bars vs. old user-input 2). Ensures bar_index - last_trade_bar >= cooldown.

Impact: Faster cooldowns (especially Aggressive/Balanced) allow more trades, balanced by VIX and strength filters.

Contract Sizing:

Logic: User sets contracts (default: 1, max: 10), no preset cap (unlike old 7/5/3 suggestion).

Impact: Flexible but risks over-leverage; beginners should stick to low contracts.

Built To Be Reliable and Consistent:

- Tighter stops and faster cooldowns make it a high-octane system without blowing up accounts.

- Preset-driven risk removes guesswork, letting newbies trade confidently.

- 2:1 TPs ensure profitable trades outweigh losses, even in volatile sessions like April 27, 2025 ES slippage.

4. Trade Entry and Exit Logic

The entry/exit rules are simple yet razor-sharp, now with VIX filtering and faster signals:

Entry Conditions:

Long Entry: buy_signal (fast EMA crosses above slow EMA, trend_dir = 1), no position (strategy.position_size = 0), cooldown passed (can_trade), and VIX < 20 (can_long). Enters with user-defined contracts.

Short Entry: sell_signal (fast EMA crosses below slow EMA, trend_dir = -1), no position, cooldown passed, can_short (always true).

Logic: Tracks last_entry_bar for visuals, last_trade_bar for cooldowns.

Exit Conditions:

Stop-Loss/Take-Profit: ATR-based stops (1.1–1.3x) and TPs (2x stop distance). Longs exit if price hits stop (below) or TP (above); shorts vice versa.

No Other Exits: Keeps it straightforward, relying on stops/TPs.

5. DAFE Visuals

The visuals are pure DAFE magic, blending clean function with informative metrics utilized by professionals, now enhanced by faster signals and a responsive breadth background:

EMA Plots:

Display: Fast EMA (blue, 2px), slow EMA (orange, 2px), using faster lengths (5–9/12–18).

Purpose: Highlights momentum shifts, with crossovers signaling entries.

Sector Breadth Background:

Display: Green (90% transparent) if breadth > 4, red (90%) if breadth < -4, else neutral.

Purpose: Faster breadth_sma_len (5–12 vs. 10–50) reflects sector shifts in real-time, reinforcing signal strength.

- Visuals are intuitive, turning complex signals into clear buy/sell cues.

- Faster breadth background reacts to market rotations (e.g., tech vs. energy), giving a pro-level edge.

6. Sector Breadth Dashboard

The new bottom-left dashboard is a game-changer, a 3x16 table (black/gray theme) that’s your market command center:

Metrics:

VIX: Current VIX (red if > 20, gray if not).

SPX: Trend as “UP” (green), “DOWN” (red), or “FLAT” (gray).

Trade Longs: “OK” (green) if VIX < 20, “BLOCK” (red) if not.

Sector Breadth: 10 sectors (Tech, Financial, etc.) with trend arrows (↑ green, ↓ red, - gray).

Placeholder Row: Empty for future metrics (e.g., ATR, breadth score).

Purpose: Consolidates regime, volatility, market trend, and sector data, making decisions a breeze.

- VIX and SPX metrics add context, helping beginners avoid bad trades (e.g., no longs if “BLOCK”).

Sector arrows show market health at a glance, like a cheat code for sentiment.

Key Features

Beginner-Ready: Preset modes and clear visuals make futures trading a breeze.

Sentiment-Driven: VIX filter, SPX trend, and sector breadth keep you in sync with the market.

High-Frequency: Faster EMAs, tighter stops, and short cooldowns boost trade volume.

Safe and Smart: Adaptive stops/TPs and cooldowns protect capital while maximizing wins.

Visual Mastery: DAFE’s clean flair, EMAs, dashboard—makes trading fun and clear.

Backtestable: Lean code and fixed qty ensure accurate historical testing.

How to Use

Add to Chart: Load on a 5min MNQ/ES chart in TradingView.

Pick Preset: Aggressive (scalping), Balanced (versatile), or Conservative (safe). Balanced is default.

Set Contracts: Default 1, max 10. Stick low for safety.

Check Dashboard: Bottom-left shows preset, VIX, SPX, and sectors. “OK” + green breadth = strong buy.

Backtest: Run in strategy tester to compare modes.

Live Trade: Connect to Tradovate or similar. Watch for slippage (e.g., April 27, 2025 ES issues).

Replay Test: Try April 28, 2025 NQ drop to see VIX filter and stops in action.

Why It’s Brilliant

The Dskyz (DAFE) Quantum Sentiment Flux - Beginners is a masterpiece of simplicity and power. It takes pro-level tools—momentum, VIX, sector breadth—and wraps them in a system anyone can run. Faster signals and tighter stops make it a trading machine, while the VIX filter and dashboard keep you ahead of market chaos. The DAFE visuals and bottom-left command center turn your chart into a futuristic cockpit, guiding you through every trade. For beginners, it’s a safe entry to futures; for pros, it’s a scalping beast with sentiment smarts. This strat doesn’t just trade—it transforms how you see the market.

Final Notes

This is more than a strategy—it’s your launchpad to mastering futures with Dskyz (DAFE) flair. The Quantum Sentiment Flux blends accessibility, speed, and market savvy to help you outsmart the game. Load it, watch those triangles glow, and let’s make the markets your canvas!

Official Statement from Pine Script Team

(see TradingView help docs and forums):

"This warning may appear when you call functions such as ta.sma inside a request.security in a loop. There is no runtime impact. If you need to loop through a dynamic list of tickers, this cannot be avoided in the present version... Values will still be correct. Ignore this warning in such contexts."

(This publishing will most likely be taken down do to some miscellaneous rule about properly displaying charting symbols, or whatever. Once I've identified what part of the publishing they want to pick on, I'll adjust and repost.)

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

Created by Dskyz, powered by DAFE Trading Systems. Trade fast, trade bold.

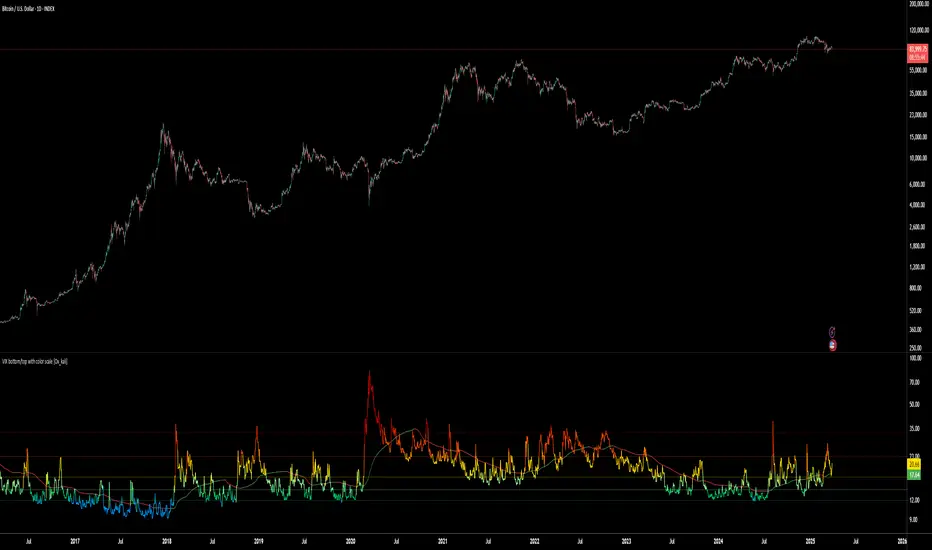

VIX bottom/top with color scale [Ox_kali]📊 Introduction

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

The “VIX Bottom/Top with Color Scale” script is designed to provide an intuitive, color-coded visualization of the VIX (Volatility Index), helping traders interpret market sentiment and volatility extremes in real time.

It segments the VIX into clear threshold zones, each associated with a specific market condition—ranging from fear to calm—using a dynamic color-coded system.

This script offers significant value for the following reasons:

Intuitive Risk Interpretation: Color-coded zones make it easy to interpret market sentiment at a glance.

Dynamic Trend Detection: A 200-period SMA of the VIX is plotted and dynamically colored based on trend direction.

Customization and Flexibility: All colors are editable in the parameters panel, grouped under “## Color parameters ##”.

Visual Clarity: Key thresholds are marked with horizontal lines for quick reference.

Practical Trading Tool: Helps identify high-risk and low-risk environments based on volatility levels.

🔍 Key Indicators

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

VIX (CBOE Volatility Index) : Measures market volatility and investor fear.

SMA 200 : Long-term trendline of the VIX, with color-coded direction (green = uptrend, red = downtrend).

Color-coded VIX Levels:

🔴 33+ → Something bad just happened

🟠 23–33 → Something bad is happening

🟡 17–23 → Something bad might happen

🟢 14–17 → Nothing bad is happening

✅ 12–14 → Nothing bad will ever happen

🔵 <12 → Something bad is going to happen

🧠 Originality and Purpose

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Unlike traditional VIX indicators that only plot a line, this script enhances interpretation through visual segmentation and dynamic trend tracking.

It serves as a risk-awareness tool that transforms the VIX into a simple, emotional market map.

This is the first version of the script, and future updates may include alerts, background fills, and more advanced features.

⚙️ How It Works

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

The script maps the current VIX value to a range and applies the corresponding color.

It calculates a SMA 200 and colors it green or red depending on its slope.

It displays horizontal dotted lines at key thresholds (12, 14, 17, 23, 33).

All colors are configurable via input parameters under the group: "## Color parameters ##".

🧭 Indicator Visualization and Interpretation

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

The VIX line changes color based on market condition zones.

The SMA line shows long-term direction with dynamic color.

Horizontal threshold lines visually mark the transitions between volatility zones.

Ideal for quickly identifying periods of fear, caution, or stability.

🛠️ Script Parameters

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Grouped under “## Color parameters ##”, the following elements are customizable:

🎨 VIX Zone Colors:

33+ → Red

23–33 → Orange

17–23 → Yellow

14–17 → Light Green

12–14 → Dark Green

<12 → Blue

📈 SMA Colors:

Uptrend → Green

Downtrend → Red

These settings allow users to match the script’s visuals to their preferred chart style or theme.

✅ Conclusion

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

The “VIX Bottom/Top with Color Scale” is a clean, powerful script designed to simplify how traders view volatility.

By combining long-term trend data with real-time color-coded sentiment analysis, this script becomes a go-to reference for managing risk, timing trades, or simply staying in tune with market mood.

🧪 Notes

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

This is version 1 of the script. More features such as alert conditions, background fill, and dashboard elements may be added soon. Feedback is welcome!

💡 Color code concept inspired by the original VIX interpretation chart by @nsquaredvalue on Twitter. Big thanks for the visual clarity! 💡

⚠️ Disclaimer

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

This script is a visual tool designed to assist in market analysis. It does not guarantee future performance and should be used in conjunction with proper risk management. Past performance is not indicative of future results.

AEST High-Low MarkerOverview

This TradingView indicator, AEST High-Low Marker, is designed to mark the highest and lowest price levels observed between 5:00 PM and 6:00 PM AEST and extend these levels visually on the chart only between 5:00 PM and 12:00 AM AEST.

Functionality

Time Conversion for AEST

Since TradingView operates in UTC, the script translates AEST (UTC+10 or UTC+11 during daylight savings) into UTC time.

The script starts tracking from 5:00 PM AEST (7 AM UTC) to 6:00 PM AEST (8 AM UTC).

The high and low lines will be displayed only between 5:00 PM and 12:00 AM AEST (7 AM to 2 PM UTC).

Real-Time High & Low Calculation

The indicator dynamically updates the session high and low as new candles form during the 5 PM - 6 PM AEST period.

It captures the maximum high and minimum low during this timeframe.

Line Display Restrictions

The session high and low lines will only be drawn between 5:00 PM and 12:00 AM AEST to prevent chart clutter.

The lines disappear after 12:00 AM AEST.

Visual Representation

Blue Line: Marks the session high recorded between 5 PM - 6 PM AEST.

Red Line: Marks the session low recorded between 5 PM - 6 PM AEST.

Both lines extend until 12 AM AEST and then disappear.

Use Case

This indicator is useful for traders looking to track key price levels formed between 5 PM and 6 PM AEST and observe how price interacts with these levels until midnight.

It is particularly beneficial for intraday and short-term trading strategies, allowing users to identify potential support and resistance zones based on early evening price action.

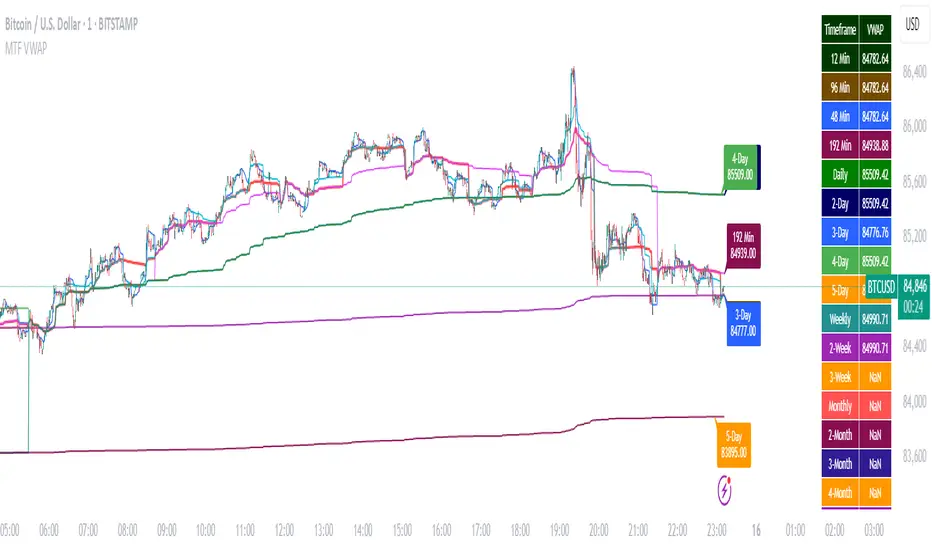

Multi-Timeframe VWAP DashboardMulti-Timeframe VWAP Dashboard with Advanced Customization**

Unlock the power of **Volume-Weighted Average Price (VWAP)** across multiple timeframes with this highly customizable and feature-rich Pine Script. Designed for traders who demand precision and flexibility, this script provides a **comprehensive VWAP dashboard** that adapts to your trading style and strategy. Whether you're a day trader, swing trader, or long-term investor, this tool offers unparalleled insights into market trends and price levels.

---

### **Key Features:**

1. **Multi-Timeframe VWAP Calculation:**

- Calculate VWAP across **12-minute, 48-minute, 96-minute, 192-minute, daily, weekly, monthly, and even yearly timeframes**.

- Supports **custom timeframes** for tailored analysis.

2. **Price Source Selection:**

- Choose from multiple price sources for VWAP calculation, including **Open, High, Low, Close, HL2, HLC3, HLCC4, and All**.

- Optimize VWAP for **uptrends and downtrends** by selecting the most relevant price source.

3. **Customizable Labels:**

- Add **dynamic labels** to each VWAP line for quick reference.

- Customize label **colors, sizes, and offsets** to suit your chart setup.

- Display **price values** and **session types** (e.g., "12 Min", "Daily", "Weekly") directly on the chart.

4. **Advanced Session Detection:**

- Automatically detect new sessions for **intraday, daily, weekly, monthly, and yearly timeframes**.

- Ensures accurate VWAP calculations for each session.

5. **Plot Visibility Control:**

- Toggle the visibility of individual VWAP plots to **reduce clutter** and focus on the most relevant timeframes.

- Includes options for **short-term, medium-term, and long-term VWAPs**.

6. **Comprehensive Timeframe Coverage:**

- From **12-minute intervals** to **12-month intervals**, this script covers all major timeframes.

- Perfect for traders who analyze markets across multiple horizons.

7. **User-Friendly Inputs:**

- Intuitive input options for **timeframes, colors, labels, and offsets**.

- Easily customize the script to match your trading preferences.

8. **Dynamic Label Positioning:**

- Labels adjust automatically based on price movements and session changes.

- Choose from **multiple offset options** to position labels precisely.

9. **Miscellaneous Customization:**

- Adjust **text color, label size, and price display settings**.

- Enable or disable **price values** and **session type labels** for a cleaner chart.

---

### **Why Use This Script?**

- **Versatility:** Suitable for all trading styles, including scalping, day trading, swing trading, and long-term investing.

- **Precision:** Accurate VWAP calculations across multiple timeframes ensure you never miss key price levels.

- **Customization:** Tailor the script to your specific needs with a wide range of input options.

- **Clarity:** Dynamic labels and customizable plots make it easy to interpret market trends at a glance.

---

### **How It Works:**

1. **Select Your Price Source:**

- Choose the price source (e.g., Open, Close, HL2) for VWAP calculation based on your trading strategy.

2. **Choose Timeframes:**

- Define the timeframes for VWAP calculation, from intraday to yearly intervals.

3. **Customize Labels and Plots:**

- Enable or disable labels and plots for each timeframe.

- Adjust colors, sizes, and offsets to match your chart setup.

4. **Analyze Market Trends:**

- Use the VWAP lines and labels to identify **support/resistance levels**, **trend direction**, and **potential reversal points**.

5. **Adapt to Market Conditions:**

- Switch between timeframes and price sources to adapt to changing market conditions.

---

### **Ideal For:**

- **Day Traders:** Use short-term VWAPs (e.g., 12-minute, 48-minute) to identify intraday trends and key levels.

- **Swing Traders:** Leverage medium-term VWAPs (e.g., 96-minute, daily) to spot swing opportunities.

- **Long-Term Investors:** Analyze long-term VWAPs (e.g., weekly, monthly) to gauge overall market direction.

---

### **How to Get Started:**

1. Add the script to your TradingView chart.

2. Customize the inputs to match your trading preferences.

3. Analyze the VWAP lines and labels to make informed trading decisions.

---

### **Pro Tip:**

Combine this script with other technical indicators (e.g., moving averages, RSI) for a **holistic view** of the market. Use the VWAP lines as dynamic support/resistance levels to enhance your entry and exit strategies.

This script is a must-have tool for traders who value precision, flexibility, and clarity. Share it with your audience to help them elevate their trading game. Whether they're beginners or seasoned professionals, this **Multi-Timeframe VWAP Dashboard** will become an essential part of their toolkit.

Anchored Geometric Brownian Motion Projections w/EVAnchored GBM (Geometric Brownian Motion) Projections + EV & Confidence Bands

Version: Pine Script v6

Overlay: Yes

Author:

Published On:

Overview

The Anchored GBM Projections + EV & Confidence Bands indicator leverages the Geometric Brownian Motion (GBM) model to project future price movements based on historical data. By simulating multiple potential future price paths, it provides traders with insights into possible price trajectories, their expected values, and confidence intervals. Additionally, it offers a "Mean of EV" (EV of EV) line, representing the running average of expected values across the projection period.

Key Features

Anchor Time Setup:

Define a specific point in time from which the projections commence.

By default, it uses the current bar's timestamp but can be customized.

Projection Parameters:

Projection Candles (Bars): Determines the number of future bars (time periods) to project.

Number of Simulations: Specifies how many GBM paths to simulate, ensuring statistical relevance via the Central Limit Theorem (CLT).

Display Toggles:

Simulation Lines: Visual representation of individual GBM simulation paths.

Expected Value (EV) Line: The average price across all simulations at each projection bar.

Upper & Lower Confidence Bands: 95% confidence intervals indicating potential price boundaries.

EV of EV Line: Running average of EV values, providing a smoothed central tendency across the projection period. Additionally, this line often acts as an indicator of trend direction.

Visualization:

Clear and distinguishable lines with customizable colors and styles.

Overlayed on the price chart for direct comparison with actual price movements.

Mathematical Foundation

Geometric Brownian Motion (GBM):

Definition: GBM is a continuous-time stochastic process used to model stock prices. It assumes that the logarithm of the stock price follows a Brownian motion with drift.

Equation:

S(t)=S0⋅e(μ−12σ2)t+σW(t)

S(t)=S0⋅e(μ−21σ2)t+σW(t) Where:

S(t)S(t) = Stock price at time tt

S0S0 = Initial stock price

μμ = Drift coefficient (average return)

σσ = Volatility coefficient (standard deviation of returns)

W(t)W(t) = Wiener process (standard Brownian motion)

Drift (μμ) and Volatility (σσ):

Drift (μμ) represents the expected return of the stock.

Volatility (σσ) measures the stock's price fluctuation intensity.

Central Limit Theorem (CLT):

Principle: With a sufficiently large number of independent simulations, the distribution of the sample mean (EV) approaches a normal distribution, regardless of the underlying distribution.

Application: Ensures that the EV and confidence bands are statistically reliable.

Expected Value (EV) and Confidence Bands:

EV: The mean price across all simulations at each projection bar.

Confidence Bands: Range within which the actual price is expected to lie with a specified probability (e.g., 95%).

EV of EV (Mean of Sample Means):

Definition: Represents the running average of EV values across the projection period, offering a smoothed central tendency.

Methodology

Anchor Time Setup:

The indicator starts projecting from a user-defined Anchor Time. If not customized, it defaults to the current bar's timestamp.

Purpose: Allows users to analyze projections from a specific historical point or the latest market data.

Calculating Drift and Volatility:

Returns Calculation: Computes the logarithmic returns from the Anchor Time to the current bar.

returns=ln(StSt−1)

returns=ln(St−1St)

Drift (μμ): Calculated as the simple moving average (SMA) of returns over the period since the Anchor Time.

Volatility (σσ): Determined using the standard deviation (stdev) of returns over the same period.

Simulation Generation:

Number of Simulations: The user defines how many GBM paths to simulate (e.g., 30).

Projection Candles: Determines the number of future bars to project (e.g., 12).

Process:

For each simulation:

Start from the current close price.

For each projection bar:

Generate a random number zz from a standard normal distribution.

Calculate the next price using the GBM formula:

St+1=St⋅e(μ−12σ2)+σz

St+1=St⋅e(μ−21σ2)+σz

Store the projected price in an array.

Expected Value (EV) and Confidence Bands Calculation:

EV Path: At each projection bar, compute the mean of all simulated prices.

Variance and Standard Deviation: Calculate the variance and standard deviation of simulated prices to determine the confidence intervals.

Confidence Bands: Using the standard normal z-score (1.96 for 95% confidence), establish upper and lower bounds:

Upper Band=EV+z⋅σEV

Upper Band=EV+z⋅σEV

Lower Band=EV−z⋅σEV

Lower Band=EV−z⋅σEV

EV of EV (Running Average of EV Values):

Calculation: For each projection bar, compute the average of all EV values up to that bar.

EV of EV =1j+1∑k=0jEV

EV of EV =j+11k=0∑jEV

Visualization: Plotted as a dynamic line reflecting the evolving average EV across the projection period.

Visualization Elements

Simulation Lines:

Appearance: Semi-transparent blue lines representing individual GBM simulation paths.

Purpose: Illustrate a range of possible future price trajectories based on current drift and volatility.

Expected Value (EV) Line:

Appearance: Solid orange line.

Purpose: Shows the average projected price at each future bar across all simulations.

Confidence Bands:

Upper Band: Dashed green line indicating the upper 95% confidence boundary.

Lower Band: Dashed red line indicating the lower 95% confidence boundary.

Purpose: Highlight the range within which the price is statistically expected to remain with 95% confidence.

EV of EV Line:

Appearance: Dashed purple line.

Purpose: Displays the running average of EV values, providing a smoothed trend of the central tendency across the projection period. As the mean of sample means it approximates the population mean (i.e. the trend since the anchor point.)

Current Price:

Appearance: Semi-transparent white line.

Purpose: Serves as a reference point for comparing actual price movements against projected paths.

Usage Instructions

Configuring User Inputs:

Anchor Time:

Set to a specific timestamp to start projections from a historical point or leave it as default to use the current bar's time.

Projection Candles (Bars):

Define the number of future bars to project (e.g., 12). Adjust based on your trading timeframe and analysis needs.

Number of Simulations:

Specify the number of GBM paths to simulate (e.g., 30). Higher numbers yield more accurate EV and confidence bands but may impact performance.

Display Toggles:

Show Simulation Lines: Toggle to display or hide individual GBM simulation paths.

Show Expected Value Line: Toggle to display or hide the EV path.

Show Upper Confidence Band: Toggle to display or hide the upper confidence boundary.

Show Lower Confidence Band: Toggle to display or hide the lower confidence boundary.

Show EV of EV Line: Toggle to display or hide the running average of EV values.

Managing TradingView's Object Limits:

Understanding Limits:

TradingView imposes a limit on the number of graphical objects (e.g., lines) that can be rendered. High values for projection candles and simulations can quickly consume these limits. TradingView appears to only allow a total of 55 candles to be projected, so if you want to see two complete lines, you would have to set the projection length to 27: since 27 * 2 = 54 and 54 < 55.

Optimizing Performance:

Use Toggles: Enable only the necessary visual elements. For instance, disable simulation lines and confidence bands when focusing on the EV and EV of EV lines. You can also use the maximum projection length of 55 with the lower limit confidence band as the only line, visualizing a long horizon for your risk.

Adjust Parameters: Lower the number of projection candles or simulations to stay within object limits without compromising essential insights.

Interpreting the Indicator:

Simulation Lines (Blue):

Represent individual potential future price paths based on GBM. A wider spread indicates higher volatility.

Expected Value (EV) Line (Goldenrod):

Shows the mean projected price at each future bar, providing a central trend.

Confidence Bands (Green & Red):

Indicate the statistical range (95% confidence) within which the price is expected to remain.

EV of EV Line (Dotted Line - Goldenrod):

Reflects the running average of EV values, offering a smoothed perspective of expected price trends over the projection period.

Current Price (White):

Serves as a benchmark for assessing how actual prices compare to projected paths.

Practical Applications

Risk Management:

Confidence Bands: Help in identifying potential support and resistance levels based on statistical confidence intervals.

EV Path: Assists in setting realistic target prices and stop-loss levels aligned with projected expectations.

Trend Analysis:

EV of EV Line: Offers a smoothed trendline, aiding in identifying overarching market directions amidst price volatility. Indicative of the population mean/overall trend of the data since your anchor point.

Scenario Planning:

Simulation Lines: Enable traders to visualize multiple potential outcomes, fostering better decision-making under uncertainty.

Performance Evaluation:

Comparing Actual vs. Projected Prices: Assess how actual price movements align with projected scenarios, refining trading strategies over time.

Mathematical and Statistical Insights

Simulation Integrity:

Independence: Each simulation path is generated independently, ensuring unbiased and diverse projections.

Randomness: Utilizes a Gaussian random number generator to introduce variability in diffusion terms, mimicking real market randomness.

Statistical Reliability:

Central Limit Theorem (CLT): By simulating a sufficient number of paths (e.g., 30), the sample mean (EV) converges to the population mean, ensuring reliable EV and confidence band calculations.

Variance Calculation: Accurate computation of variance from simulation data ensures precise confidence intervals.

Dynamic Projections:

Running Average (EV of EV): Provides a cumulative perspective, allowing traders to observe how the average expectation evolves as the projection progresses.

Customization and Enhancements

Adjustable Parameters:

Tailor the projection length and simulation count to match your trading style and analysis depth.

Visual Customization:

Modify line colors, styles, and transparency to enhance clarity and fit chart aesthetics.

Extended Statistical Metrics:

Future iterations can incorporate additional metrics like median projections, skewness, or alternative confidence intervals.

Dynamic Recalculation:

Implement logic to automatically update projections as new data becomes available, ensuring real-time relevance.

Performance Considerations

Object Count Management:

High simulation counts and extended projection periods can lead to a significant number of graphical objects, potentially slowing down chart performance.

Solution: Utilize display toggles effectively and optimize projection parameters to balance detail with performance.

Computational Efficiency:

The script employs efficient array handling and conditional plotting to minimize unnecessary computations and object creation.

Conclusion

The Anchored GBM Projections + EV & Confidence Bands indicator is a robust tool for traders seeking to forecast potential future price movements using statistical models. By integrating Geometric Brownian Motion simulations with expected value calculations and confidence intervals, it offers a comprehensive view of possible market scenarios. The addition of the "EV of EV" line further enhances analytical depth by providing a running average of expected values, aiding in trend identification and strategic decision-making.

Hope it helps!

CSVParser█ OVERVIEW

The library contains functions for parsing and importing complex CSV configurations (with a special simple syntax) into a special hierarchical object (of type objProps ) as follows:

Functions:

parseConfig() - reads CSV text into an objProps object.

toT() - displays the contents of an objProps object in a table form, which allows to check the CSV text for syntax errors.

getPropAr() - returns objProps.arS array for child object with `prop` key in mpObj map (or na if not found)

This library is handy in allowing users to store presets for the scripts and switch between them (see, e.g., my HTF moving averages script where users can switch between several preset configuations of 24 MA's across 5 timeframes).

█ HOW THE SCRIPT WORKS.

The script works as follows:

all values read from config text are stored as strings

Nested brackets in config text create a named nested objects of objProps0, ... , objProps9 types.

objProps objects of each level have the following fields:

- array arS for storing values without names (e.g. "12, 23" will be imported into a string array arS as )

- map mpS for storing items with names (e.g. "tf = 60, length = 21" will be imported as <"tf", "60"> and <"length", "21"> pairs into mpS )

- map mpObj for storing nested objects (e.g. "TF1(tf=60, length(21,50,100))" creates a <"TF1, objProps0 object> pair in mpObj map property of the top level object (objProps) , "tf=60" is stored as <"tf", "60"> key-value pair in mpS map property of a next level object (objProps0) and "length (...)" creates a <"length", objProps1> pair in objProps0.mpObj map while length values are stored in objProps1.arS array as strings. Every opening bracket creates a next level objProps object.

If objects or properties with duplicate names are encountered only the latest is imported

(e.g. for "TF1(length(12,22)), TF1(tf=240)" only "TF1(tf=240)" will be imported

Line breaks are not regarded as part of syntax (i.e. values are imported with line breaks, you can supply

symbols "(" , ")" , "," and "=" are special characters and cannot be used within property values (with the exception of a quoted text as a value of a property as explained below)

named properties can have quoted text as their value. In that case special characters within quotation marks are regarded as normal characters. Text between "=" and opening quotation mark as well as text following the closing quotation mark and until next property value is ignored. E.g. "quote = ignored "The quote" also ignored" will be imported as <"quote", "The quote">. Quotation marks within quotes must be excaped with "\" .

if a key names happens to be a multi-line then only first line containing non-space characters (trimmed from spaces) is taken as a key.

")," or ") ," and similar do not create an empty ("") array item while ",," does. (",)" creates an "" array item)

█ CSV CONFIGURATION SYNTAX

Unnamed values: just list them comma separated and they will be imported into arS of the object of the current level.

Named values: use "=" sign as follows: "property1=value1, property2 = value2"

Value of several objects: Use brackets after the name of the object ant list all object properties within the brackets (including its child objects if necessary). E.g. "TF1(tf =60, length(21,200), TF2(tf=240, length(50,200)"

Named and unnamed values as well as objects can go in any order. E.g. "12, tf=60, 21" will be imported as follows: "12", "21" will go to arS array and <"tf", "60"> will go to mpS maP of objProps (the top level object).

You can play around and test your config text using demo in this library, just edit your text in script settings and see how it is parsed into objProps objects.

█ USAGE RECOMMENDATIONS AND SAMPLE USE

I suggest the following approach:

- create functions for your UDT which can set properties by name.

- create enumerator functions which iterates through all the property names (supplied as a const string array) and imports their values into the object

█ SAMPLE USE

A sample use of this library can be seen in my Multi-timeframe 24 moving averages + BB+SAR+Supertrend+VWAP script where settings for the MAs across many timeframes are imported from CSV configurations (presets).

█ FULL LIST OF FUNCTIONS AND PROPERTIES

nzs(_s, nz)

Like nz() but for strings. Returns `nz` arg (default = "") if _s is na.

Parameters:

_s (string)

nz (string)

method init(this)

Initializes objProps obj (creates child maps and arrays)

Namespace types: objProps

Parameters:

this (objProps)

method toT(this, nz)

Outputs objProps to string matrices for further display using autotable().

Namespace types: objProps, objProps1, ..., objProps9

Parameters:

this (objProps/objProps1/..../objProps9)

nz (string)

Returns: A tuple - value, merge and color matrix (autotable() parameters)

method parseConfig(this, s)

Reads config text into objProps (unnamed values into arS, named into mpS, sub-levels into mpObj)

Namespace types: objProps

Parameters:

this (objProps)

s (string)

method getPropArS(this, prop)

Returns a string array of values for a given property name `prop`. Looks for a key `prop` in objProps.mpObj

if finds pair returns obj.arS, otherwise returns na. Returns a reference to the original, not a copy.

Namespace types: objProps, objProps1, ..., objProps8

Parameters:

this (objProps/objProps1/..../objProps8)

prop (string)

method getPropVal(this, prop, id)

Checks if there is an array of values for property `prop` and returns its `id`'s element or na if not found

Namespace types: objProps, objProps1, ..., objProps8

Parameters:

this (objProps/objProps1/..../objProps8) : objProps object containing array of property values in a child objProp object corresponding to propertty name.

prop (string) : (string) Name of the property

id (int) : (int) Id of the element to be returned from the array pf property values

objProps9 type

Object for storing values read from CSV relating to a particular object or property name.

Fields:

mpS (map) : (map() Stores property values as pairs

arS (array) : (string ) Array of values

objProps, objProps0, ... objProps8 types

Object for storing values read from CSV relating to a particular object or property name.

Fields:

mpS (map) : (map() Stores property values as pairs

arS (array) : (string ) Array of values

mpObj (map) : (map() Stores objProps objects containing properties's data as pairs

@tk · fractal emas█ OVERVIEW