Cerber Strategy ETH/BTC Cerber Strategy: High-Precision Crypto Trend Follower

The Cerber Strategy is a low-frequency, high-conviction trend following system designed to capture massive quarterly crypto moves while

filtering out 90% of consolidation noise. It combines a momentum-based "Sniper Entry" (entering only on verified breakouts) with a

"Trend Confirmation" filter (Weekly DEMA) to ensure capital is only deployed during macro bull runs.

Usage:

* Timeframe: Daily (1D) mandatory.

* Assets: Optimized for BTC and ETH, works on high-volatility alts.

* Style: Position Trading (holding for weeks/months).

* Risk: Extremely high efficiency (high Profit Factor), very low drawdown compared to Buy & Hold. Perfect for a "Set and Forget"

portfolio allocation.

Signals

Trend Signal MomentumOVERVIEW

Signal Trend Momentum is a hybrid strategy that combines multiple confirmations and filters to obtain better potential trading signals. Each confirmation and filter in Signal Trend Momentum aims to avoid possible false and trap signals.

HYBRID CONCEPTS

Smart Money Concept – This indicator forms market structure and Bullish & Bearish Order Block areas to make it easier to identify market trends and strong areas where price reversals often occur. Its purpose is to simplify recognizing market direction and serve as the first confirmation.

MSS + BOS (Market Structure Shift + Break of Structure) – This indicator serves as additional confirmation for the Smart Money Concept. With the presence of two types of market structure, the market trend direction becomes clearer and more convincing.

RSI Momentum Signal – This indicator becomes the third confirmation. When the Market Trend is clear and convincing, supported by the formation of Bearish and Bullish Order Blocks, the role of the Momentum Signal here becomes crucial as it provides trend momentum based on overbought and oversold areas.

Momentum Position – This indicator becomes the next confirmation based on buyer and seller VOLUME in the market. If buyer volume is higher, the momentum position will be depicted on the chart with an upward arrow, and conversely, if seller volume is higher, it will be depicted with a downward arrow.

SnR (Support and Resistance) – This final indicator is Support and Resistance, which will serve as the last and more convincing confirmation. Support and Resistance will strengthen the Order Block areas formed by the Smart Money Concept indicator. A Bullish Order Block + Support creates a higher possibility for an upward trend in the market, conversely, a Bearish Order Block + Resistance creates a higher possibility for a downward trend in the market.

The combination of these several indicators will provide a strong market direction + persistent buyer and seller areas, as well as depict momentum based on volume + RSI which serve as additional confirmations.

These additional confirmations will produce stronger signals and help avoid false and trap signals in the market.

HOW TO USE

A SHORT SIGNAL will be strong if there is a Downtrend Market Structure + Bearish Order Block + Resistance + Oversold RSI Momentum + Strong Seller Volume Momentum.

A LONG SIGNAL will be strong if there is an Uptrend Market Structure + Bullish Order Block + Support + Overbought RSI Momentum + Strong Buyer Volume Momentum.

CONCLUSION

Signal Trend Momentum is a combination of several powerful indicators designed to produce stronger, clearer, and easier-to-read signals.

This strategy is highly suitable for traders seeking more convincing trade signals based on multiple confirmations from the combined indicators, thereby creating a strong signal with a higher probability.

Strategy: HMA 50 + Supertrend SniperHMA 50 + Supertrend Confluence Strategy (Trend Following with Noise Filtering)

Description:

Introduction and Concept This strategy is designed to solve a common problem in trend-following trading: Lag vs. False Signals. Standard Moving Averages often lag too much, while price action indicators can generate false signals during choppy markets. This script combines the speed of the Hull Moving Average (HMA) with the volatility-based filtering of the Supertrend indicator to create a robust "Confluence System."

The primary goal of this script is not just to overlay two indicators, but to enforce a strict rule where a trade is only taken when Momentum (HMA) and Volatility Direction (Supertrend) are in perfect agreement.

Why this combination? (The Logic Behind the Mashup)

Hull Moving Average (HMA 50): We use the HMA because it significantly reduces lag compared to SMA or EMA by using weighted calculations. It acts as our primary Trend Direction detector. However, HMA can be too sensitive and "whipsaw" during sideways markets.

Supertrend (ATR-based): We use the Supertrend (Factor 3.0, Period 10) as our Volatility Filter. It uses Average True Range (ATR) to determine the significant trend boundary.

How it Works (Methodology) The strategy uses a boolean logic system to filter out low-quality trades:

Bullish Confluence: The HMA must be rising (Slope > 0) AND the Close Price must be above the Supertrend line (Uptrend).

Bearish Confluence: The HMA must be falling (Slope < 0) AND the Close Price must be below the Supertrend line (Downtrend).

The "Choppy Zone" (Noise Filter): This is a unique feature of this script. If the HMA indicates one direction (e.g., Rising) but the Supertrend indicates the opposite (e.g., Downtrend), the market is considered "Choppy" or indecisive. In this state, the script paints the candles or HMA line Gray and exits all positions (optional setting) to preserve capital.

Visual Guide & Signals To make the script easy to interpret for traders who do not read Pine Script, I have implemented specific visual cues:

Green Cross (+): Indicates a LONG entry signal. Both HMA and Supertrend align bullishly.

Red Cross (X): Indicates a SHORT entry signal. Both HMA and Supertrend align bearishly.

Thick Line (HMA): The main line changes color based on the trend.

Green: Bullish Confluence.

Red: Bearish Confluence.

Gray: Divergence/Choppy (No Trade Zone).

Thin Step Line: This is the Supertrend line, serving as your dynamic Trailing Stop Loss.

Strategy Settings

HMA Length: Default is 50 (Mid-term trend).

ATR Factor/Period: Default is 3.0/10 (Standard for trend catching).

Exit on Choppy: A toggle switch allowing users to decide whether to hold through noise or exit immediately when indicators disagree.

Risk Warning This strategy performs best in trending markets (Forex, Crypto, Indices). Like all trend-following systems, it may experience drawdown during prolonged accumulation/distribution phases. Please backtest with your specific asset before using it with real capital.

BTR Auto Buy/Sell Trend System

BTR Auto Buy/Sell Trend System — Your New Profit Machine!

Discover the only TradingView system you need to spot powerful trend reversals with precision, confidence, and automation.

Designed for Stocks, Crypto & Commodities, this strategy consistently delivers 60%–80% accuracy in trending markets.

This is not just a script…

👉 It’s your complete plug-and-play trading system.

💡 Why Traders Love This System

✔ Early Trend Identification

Catch major reversals before the crowd.

✔ Non-Repainting Confirmed Signals

All entries are triggered only on candle close, so what you see is what you trade.

✔ Smart ATR + Momentum Engine

Filters bad trades automatically, giving you only high-quality signals.

✔ Works on All Timeframes

From 5-minute scalping to daily swing trading.

✔ Full Auto-Trading Ready

Pre-built JSON alerts for API Algo Trading.

No coding. No setup headache. Just copy → paste → trade.

⚡ How You Make Money With This Strategy

Step 1: Wait for Trend Flip

🔵 BUY when the system flips from bearish → bullish

🔴 SELL when it flips from bullish → bearish

Step 2: Enter on Confirmed Signal

Trade only on the bar after signal closes.

Step 3: Ride the Trend

Let the strategy take the move.

It avoids sideways markets and shines in strong trends.

Step 4: Auto Alerts (Optional)

Turn on Dhan alerts and let the system execute trades automatically.

📈 What You Can Expect (Typical Performance)

✔ 60–80% success rate in trending markets

✔ Works in Stocks, Crypto, Commodities

✔ High accuracy in 15m, 30m, 1H, 4H charts

✔ Avoids most fake breakouts & sideways noise

This system is built for consistency, simplicity, and scalable automation.

⭐ Perfect For:

Beginner traders

Algo traders

Swing traders

Scalpers

Systematic

API users

Anyone who wants clean, high-probability trend signals

⚠ Disclaimer

Trading involves risk. Past results do not guarantee future returns.

Use proper risk management for best results.

Quantura - Quantified Price Action StrategyIntroduction

“Quantura – Quantified Price Action Strategy” is an invite-only Pine Script strategy designed to combine multiple price action concepts into a single trading framework. It integrates supply and demand zones, liquidity sweeps and runs, fair value gaps (FVGs), RSI filters, and EMA trend confirmation. The strategy also provides a visual overlay with dynamic trend-colored candles for easier chart interpretation. It is intended for multi-market use across cryptocurrencies, Forex, equities, and indices.

Originality & Value

The strategy is original in how it unifies several institutional-style price action elements and validates trades only when they align. This reduces noise compared to using single indicators in isolation. Its unique value lies in the combination of:

Supply & Demand detection: Dynamic boxes identified through pivots, ATR, and volume sensitivity.

Liquidity sweeps and runs: Detects when swing highs/lows are broken and retested, distinguishing between liquidity grabs (sweeps) and directional runs.

RSI filter: Can be set to normal or aggressive, confirming momentum before trades.

Fair Value Gaps (FVGs): Optional detection and filtering of price inefficiencies.

EMA filter: Aligns trades with the broader market trend.

Trend candle visualization: Candles dynamically colored bullish, bearish, or neutral, based on strategy positions.

This layered confluence approach ensures that entries are not taken on a single condition but require agreement across several dimensions of market structure, momentum, and order flow.

Functionality & Indicators

Supply & Demand Zones: Zones are created when pivots, ATR sensitivity, and volume thresholds overlap.

Liquidity: Swing highs and lows are tracked, with options for sweep (fakeout/reversal) or run (continuation) detection.

RSI: Confirms long signals when oversold and shorts when overbought, with configurable aggressiveness.

FVG filter: Adds validation by requiring price interaction with inefficiency zones.

EMA filter: Ensures longs are above EMA and shorts below EMA.

Signals & Visualization: Trade entries are marked on the chart, while candles change color to reflect trade direction and status.

Parameters & Customization

Supply & Demand: Sensitivity (swing range, volume multiplier, ATR multiplier) and display options.

Liquidity filter: Mode (Run or Sweep), display, and swing length.

RSI: Enable/disable, length, and style (normal or aggressive).

Fair Value Gaps: Sensitivity via ATR factor, optional volume filter, and display toggles.

EMA: Length, enable/disable, and visualization.

Risk management: Up to three configurable take-profit levels, stop-loss, break-even logic, and capital-based position sizing.

Visualization: Custom candle coloring and optional overlay for better clarity.

Default Properties (Strategy Settings)

Initial Capital: 10,000 USD

Position Size: 100% of equity per trade (backtest default)

Commission: 0.1%

Slippage: 1

Pyramiding: 0 (only one position at a time)

Note: The default of 100% equity per trade is used for testing purposes only and would not be sustainable in real trading. A typical allocation in practice would be between 1–5% of account equity per trade, sometimes up to 10%.

Backtesting & Performance

Backtests on XPTUSD over 2.5 years with the default settings produced:

164 trades

67.68% win rate

Profit factor: 1.7

Maximum drawdown: 27.81%

These results show how the confluence of supply/demand, liquidity, and RSI filters can produce robust setups. However, past performance does not guarantee future results. While the trade count (164) is sufficient for statistical analysis, results may vary across markets and timeframes.

Risk Management

Three configurable take-profit levels with percentage allocation.

Initial stop-loss based on user-defined percentage.

Dynamic stop-loss that adjusts with market movement.

Break-even logic that shifts stops to entry after predefined gains.

Position sizing based on risk percentage of equity.

This framework allows both conservative and aggressive configurations, depending on user preference.

Limitations & Market Conditions

Works best in volatile and liquid markets such as crypto, metals, indices, and FX.

May produce false signals in low-volume or sideways environments.

Unexpected news or macro events can override technical conditions.

Default position sizing of 100% equity is highly aggressive and should be reduced before any practical use.

Usage Guide

Add “Quantura – Quantified Price Action Strategy” to your chart.

Select Supply & Demand, Liquidity, RSI, EMA, and FVG settings according to your market and timeframe.

Configure risk management: take-profits, stop-loss, and risk-per-trade percentage.

Use the Strategy Tester to analyze statistics, equity curve, and performance under different conditions.

Optimize parameters before applying the strategy to different markets.

Author & Access

Developed 100% by Quantura. Published as an Invite-Only script.

Important

This description complies with TradingView’s publishing rules. It clarifies originality, explains the underlying logic, discloses default properties, and presents backtest results with realistic disclaimers.

Quantura - Quantitative AlgorythmIntroduction

“Quantura – Quantitative Algorithm” is an invite-only Pine Script strategy designed for multi-timeframe analysis, combining technical filters with user-adjustable fundamental sentiment. It was primarily developed for cryptocurrency markets but can also be applied across other assets such as Forex, stocks, and indices. The goal is to generate structured trade signals through a confluence of techniques rather than relying on a single indicator.

Originality & Value

Quantura is not a simple mashup of indicators. Its originality comes from how multiple layers of analysis are integrated into a single decision framework . Instead of showing indicators separately, the strategy only issues trades when several conditions align simultaneously:

RSI entry triggers confirm overbought/oversold reversals.

Market structure on a higher timeframe confirms trend direction.

Order block detection highlights zones of concentrated supply and demand.

Premium/Discount zones identify potential over- and undervaluation.

HTF EMA provides trend confirmation.

Optional candlestick patterns strengthen reversal or continuation signals.

An optional correlation filter compares the main asset to a reference instrument.

This design forces agreement between different methodologies (momentum, structure, value, volume, sentiment), which reduces noise compared to using them in isolation.

Functionality & Indicators

Entry trigger: RSI exits from extreme zones.

Filters: Only valid when all selected filters (HTF structure, EMA, order blocks, premium/discount, candlesticks, correlation, volume) confirm the direction.

Fundamental bias: User-defined sentiment and analysis settings (bullish, bearish, neutral) influence whether long or short trades are permitted.

Exits: ATR-based take profit and stop loss, with optional breakeven, opposite-signal exit, and session-end exit.

Visualization: Buy/Sell markers, trend-colored candles, and an optional dashboard summarizing indicator status.

Parameters & Customization

Timeframes: Independent HTF and LTF selection.

Trading direction: Long / Short / Both.

Session and weekday filters.

RSI length and thresholds.

Filters: HTF structure, order blocks, premium/discount, EMA, candlestick, ATR volatility, volume zones, correlation.

Exit rules: ATR multipliers for TP/SL, breakeven logic, session-end exit, opposite-signal exit.

Visuals: Toggle signals, candles, dashboard, custom colors.

Default Properties (Strategy Settings)

Initial Capital: 100,000 USD

Position Size: 15% of equity per trade

Commission: 0.25%

Slippage: enabled

Pyramiding: 0 (one position at a time)

Note: The position sizing of 15% equity per trade is intentionally set for backtesting demonstration. In real trading, risking this much is considered aggressive. Most traders prefer to risk 1-5% of equity, and rarely above 10%.

Backtesting & Performance

Backtests on BTCUSD (2 years) with the above defaults showed:

112 trades

Win rate: 40%

Profit factor: 1.4

Maximum drawdown: 34%

These results illustrate how the confluence model behaves, but they are not predictive of future performance . The trade sample size (72 trades) is below the 100+ usually recommended for statistical robustness. Users should re-test with their own preferred symbols, settings, and timeframes.

Risk Management

ATR-based stops and targets scale with volatility.

Commission and slippage are included by default for realistic modeling.

Opposite-signal exit helps capture trend reversals.

Session-end exit can close intraday positions before illiquid hours.

Breakeven option protects profits when available.

Although the default allocation uses 15% per trade for demonstration, this is not a recommendation. Users are encouraged to adjust risk sizing downwards to sustainable levels (commonly 1-5%).

Limitations & Market Conditions

Performs best in volatile, liquid markets (e.g., crypto).

May struggle in prolonged sideways markets with low volatility.

News events and fundamentals outside user inputs can override signals.

Backtests below 100 trades should be considered exploratory, not statistically conclusive.

Usage Guide

Add “Quantura – Quantitative Algorithm” to your chart in strategy mode.

Select HTF and LTF timeframes, trading direction, and session filters.

Configure confluence filters (structure, EMA, order blocks, premium/discount, candlestick, correlation, volume).

Set sentiment and analysis bias in fundamental settings.

Adjust ATR multipliers and exits.

Review buy/sell signals and analyze performance in the Strategy Tester.

Author & Access

Developed 100% by Quantura . Distributed as an Invite-Only script . Details are provided in the Author’s Instructions field.

Important: This description complies with TradingView’s Script Publishing Rules and House Rules. It does not guarantee profitability, avoids unrealistic claims, and explains how the strategy integrates multiple methods into a coherent decision framework.

Strategy Builder v1.0.0 [BigBeluga]🔵 OVERVIEW

The Strategy Builder combines advanced price-action logic, smart-money concepts, and volatility-adaptive momentum signals to automate high-quality entries and exits across any market. It blends trend recognition, market structure shifts, order block reactions, imbalance (FVG) signals, liquidity sweeps, candlestick confirmations, and oscillator-powered divergences into one cohesive engine.

Whether used as a full automation workflow or as a structured confirmation framework, this strategy provides a disciplined, rules-driven method to trade with logic — not emotion.

🔵 BACKTEST WINDOW CONTROL

This module allows you to restrict strategy execution to a specific historical period.

Ideal for performance isolation, regime testing, and forward-walk validation.

Limit Backtest Window

Enabling this option activates custom date filters for the backtest engine.

Start — Define the starting date & time for backtesting

End — Define the ending date & time for backtesting

Only trades and signals inside this window are executed

Reduces computation load on large datasets

Useful for testing specific market environments (e.g., bull cycles, crash periods, sideways regimes)

🔵 SIGNAL GLOSSARY (Advanced Technical Explanation)

Traders can build long and short setups using up to 6 configurable entry conditions for each direction.

Every condition can be set as Bullish or Bearish and mapped to any signal source — allowing deep customization

Below is the full internal logic overview of every signal available in the Strategy Builder.

Signals are based on trend models, volatility structures, liquidity logic, oscillator behavior, and market structure mapping.

Trend Signals (Low-Lag Trend Engine)

Uses a proprietary low-lag baseline + momentum gradient model to detect directional bias.

Trend Signal — Momentum breaks above/below adaptive trend baseline.

Trend Signal+ — Stronger trend confirmation using volatility-weighted momentum.

Trend Signal Any — Triggers when any bullish/bearish trend signal appears.

SmartBand & Retests (Adaptive Volatility Bands)

Dynamic envelope that contracts/expands with volatility & trend strength.

SmartBand Retest — Price retests dynamic band and rejects, confirming continuation.

ActionWave Signals (Impulse-Pullback Engine)

Tracks wave behavior, acceleration and deceleration in price.

ActionWave — Detects directional impulse strength vs pullback weakness.

ActionWave Cross — Momentum acceleration threshold crossed → trend ignition.

Magnet Signals (Liquidity Gravity + Mean Reversion Bias)

Detects zones where price is being drawn due to liquidity voids or imbalance.

Magnet — Trend and liquidity pressure align, creating directional “pull.”

MagnetBar Low Momentum — Low-volatility compression → pre-breakout condition.

Flow Trend (Directional Flow State + ATR Envelope)

Higher-timeframe bias confirmation + dynamic volatility filter.

FlowTrend — Confirms major directional bias (uptrend or downtrend).

FlowTrend Retest — Price tests HTF flow band and rejects → trend resume.

Voltix (Volatility Expansion Pulse)

Detects regime shift from quiet accumulation → trending expansion.

Voltix — Breakout volatility signature, trend acceleration trigger.

Candlestick Pattern (Algorithmic Price Action Recognition)

Auto-recognizes meaningful reversal or continuation candle formations.

Candlestick Pattern — Confirms momentum reversal/continuation via candle logic.

OrderBlock Logic (Institutional Footprint System)

Institutional demand/supply zone tracking with mitigation logic.

Order Block Touch — Price taps institutional zone → reaction filter.

Order Block Break — OB invalidation → institutional flow shift.

Market Structure Engine (Swing Logic + Volume Confirmation)

Tracks major swing breaks and structural reversals.

BoS — Break of Structure in trend direction (continuation bias).

ChoCh — Change of Character — early reversal marker.

Fair Value Gaps (Imbalance & Volume Displacement)

Identifies inefficiencies caused by rapid displacement moves.

FVG Created — Price leaves inefficiency behind.

FVG Retest — Price returns to rebalance inefficiency → reaction zone.

Liquidity Events (Stop-Run & Reversal Logic)

Detects stop-hunt events and liquidity sweeps.

SFP — Swing failure & wick sweep → reversal confirmation.

Liquidity Created — New equal highs/lows form liquidity pool.

Liquidity Grab — Sweep through liquidity line followed by rejection.

Support / Resistance Break Logic

Adaptive zone recognition + momentum confirmation.

Support/Resistance Cross — Zone decisively broken → structural shift.

Pattern Breakouts (Market Geometry Engine)

Tracks breakout from compression & expansion formations.

Channel Break — Channel breakout → trend acceleration.

Wedge Break — Break from contraction wedge → burst of momentum.

Session Logic (Opening Range Behavior)

Session-based volatility trigger.

Session Break — Break above/below session opening range.

Momentum / Reversal Oscillator Suite

Oscillator-driven exhaustion & reversal signals.

Nautilus Signals — Momentum reversal signature (oscillator shift).

Nautilus Peak — Momentum peak → exhaustion risk.

OverSold/Overbought ❖ — Extreme exhaustion zones → reversal setup.

DipX Signals ✦ — Dip buy / Dip sell timing, micro-reversal engine.

Advanced Divergence Engine

Momentum/price disagreement layer with multi-trigger confirmation.

Normal Divergence — Classic divergence reversal.

Hidden Divergence — Trend continuation divergence.

Multiple Divergence — Multiple divergence confirmations stacked → high confidence.

🔧 Adjustable Signal Logic

Some signals in this system can be additionally refined through the strategy settings panel.

This allows traders to tune internal behavior for different market regimes, assets, and volatility conditions.

🔵 LONG / SHORT EXIT CONDITIONS

This section allows you to automate exits using the same advanced market conditions available for entries.

Each exit rule consists of:

Toggle — Enable/disable individual exit rule.

Direction Filter — Trigger exit only if selected market bias appears (Bullish/Bearish).

Signal Type — Choose which market event triggers the exit (same list as entry conditions).

When the active conditions are met, the strategy automatically closes the current position — ensuring emotion-free risk management and systematic trade control.

🔵 TAKE PROFIT & STOP LOSS SYSTEM

This strategy builder provides a fully dynamic risk-management engine designed for both systematic traders and discretionary confirmation users.

Take Profit Logic

Scale out of trades progressively or exit fully using algorithmic TP levels.

Up to 3 Take-Profit targets available

Choose TP calculation method:

• ATR-based distance (volatility-adaptive targets)

• %-based distance (fixed percentage from entry)

Define Size — ATR multiplier or % value

Custom Exit Size per TP (e.g., 25% / 25% / 50%)

Visual TP plotting on chart for clarity

Stop Loss Logic

Automated protection logic for every trade.

Two SL Modes:

• Fixed Stop Loss — static SL from entry

• Trailing Stop Loss — SL follows price as trade progresses

Distance options:

• ATR multiplier (adapts to volatility)

• %-based from entry (fixed distance)

SL dynamically draws on chart for transparency

Trailing SL behavior:

Follows price only in profitable direction

Never moves against the trade

Locks profits as trend develops

🔵 Strategy Dashboard

A compact on-chart performance dashboard is included to help monitor live trade status and backtest results in real time.

It displays key metrics:

Start Capital — Initial account balance used in simulation.

Position Size — % of capital allocated per trade based on user settings (It changes if the trade hits take profits, when more than one take profit is selected).

Current Trade — Shows active trade direction (Long / Short) and real-time % return from entry.

Closed Trades — Counter of completed positions, useful for reading sample size during testing.

🔵 CONCLUSION

The Strategy Builder brings together a powerful suite of smart-money and momentum-driven signals, allowing traders to automate robust trade logic built on modern market structure concepts. With access to trend filters, order blocks, liquidity events, divergence signals, volatility cues, and session-based triggers, it provides a deeply adaptive trade engine capable of fitting many market environments.

Zero Lag Trend Signals (MTF) [Quant Trading] V7Overview

The Zero Lag Trend Signals (MTF) V7 is a comprehensive trend-following strategy that combines Zero Lag Exponential Moving Average (ZLEMA) with volatility-based bands to identify high-probability trade entries and exits. This strategy is designed to reduce lag inherent in traditional moving averages while incorporating dynamic risk management through ATR-based stops and multiple exit mechanisms.

This is a longer term horizon strategy that takes limited trades. It is not a high frequency trading and therefore will also have limited data and not > 100 trades.

How It Works

Core Signal Generation:

The strategy uses a Zero Lag EMA (ZLEMA) calculated by applying an EMA to price data that has been adjusted for lag:

Calculate lag period: floor((length - 1) / 2)

Apply lag correction: src + (src - src )

Calculate ZLEMA: EMA of lag-corrected price

Volatility bands are created using the highest ATR over a lookback period multiplied by a band multiplier. These bands are added to and subtracted from the ZLEMA line to create upper and lower boundaries.

Trend Detection:

The strategy maintains a trend variable that switches between bullish (1) and bearish (-1):

Long Signal: Triggers when price crosses above ZLEMA + volatility band

Short Signal: Triggers when price crosses below ZLEMA - volatility band

Optional ZLEMA Trend Confirmation:

When enabled, this filter requires ZLEMA to show directional momentum before entry:

Bullish Confirmation: ZLEMA must increase for 4 consecutive bars

Bearish Confirmation: ZLEMA must decrease for 4 consecutive bars

This additional filter helps avoid false signals in choppy or ranging markets.

Risk Management Features:

The strategy includes multiple stop-loss and take-profit mechanisms:

Volatility-Based Stops: Default stop-loss is placed at ZLEMA ± volatility band

ATR-Based Stops: Dynamic stop-loss calculated as entry price ± (ATR × multiplier)

ATR Trailing Stop: Ratcheting stop-loss that follows price but never moves against position

Risk-Reward Profit Target: Take-profit level set as a multiple of stop distance

Break-Even Stop: Moves stop to entry price after reaching specified R:R ratio

Trend-Based Exit: Closes position when price crosses EMA in opposite direction

Performance Tracking:

The strategy includes optional features for monitoring and analyzing trades:

Floating Statistics Table: Displays key metrics including win rate, GOA (Gain on Account), net P&L, and max drawdown

Trade Log Labels: Shows entry/exit prices, P&L, bars held, and exit reason for each closed trade

CSV Export Fields: Outputs trade data for external analysis

Default Strategy Settings

Commission & Slippage:

Commission: 0.1% per trade

Slippage: 3 ticks

Initial Capital: $1,000

Position Size: 100% of equity per trade

Main Calculation Parameters:

Length: 70 (range: 70-7000) - Controls ZLEMA calculation period

Band Multiplier: 1.2 - Adjusts width of volatility bands

Entry Conditions (All Disabled by Default):

Use ZLEMA Trend Confirmation: OFF - Requires ZLEMA directional momentum

Re-Enter on Long Trend: OFF - Allows multiple entries during sustained trends

Short Trades:

Allow Short Trades: OFF - Strategy is long-only by default

Performance Settings (All Disabled by Default):

Use Profit Target: OFF

Profit Target Risk-Reward Ratio: 2.0 (when enabled)

Dynamic TP/SL (All Disabled by Default):

Use ATR-Based Stop-Loss & Take-Profit: OFF

ATR Length: 14

Stop-Loss ATR Multiplier: 1.5

Profit Target ATR Multiplier: 2.5

Use ATR Trailing Stop: OFF

Trailing Stop ATR Multiplier: 1.5

Use Break-Even Stop-Loss: OFF

Move SL to Break-Even After RR: 1.5

Use Trend-Based Take Profit: OFF

EMA Exit Length: 9

Trade Data Display (All Disabled by Default):

Show Floating Stats Table: OFF

Show Trade Log Labels: OFF

Enable CSV Export: OFF

Trade Label Vertical Offset: 0.5

Backtesting Date Range:

Start Date: January 1, 2018

End Date: December 31, 2069

Important Usage Notes

Default Configuration: The strategy operates in its most basic form with default settings - using only ZLEMA crossovers with volatility bands and volatility-based stop-losses. All advanced features must be manually enabled.

Stop-Loss Priority: If multiple stop-loss methods are enabled simultaneously, the strategy will use whichever condition is hit first. ATR-based stops override volatility-based stops when enabled.

Long-Only by Default: Short trading is disabled by default. Enable "Allow Short Trades" to trade both directions.

Performance Monitoring: Enable the floating stats table and trade log labels to visualize strategy performance during backtesting.

Exit Mechanisms: The strategy can exit trades through multiple methods: stop-loss hit, take-profit reached, trend reversal, or trailing stop activation. The trade log identifies which exit method was used.

Re-Entry Logic: When "Re-Enter on Long Trend" is enabled with ZLEMA trend confirmation, the strategy can take multiple long positions during extended uptrends as long as all entry conditions remain valid.

Capital Efficiency: Default setting uses 100% of equity per trade. Adjust "default_qty_value" to manage position sizing based on risk tolerance.

Realistic Backtesting: Strategy includes commission (0.1%) and slippage (3 ticks) to provide realistic performance expectations. These values should be adjusted based on your broker and market conditions.

Recommended Use Cases

Trending Markets: Best suited for markets with clear directional moves where trend-following strategies excel

Medium to Long-Term Trading: The default length of 70 makes this strategy more appropriate for swing trading rather than scalping

Risk-Conscious Traders: Multiple stop-loss options allow traders to customize risk management to their comfort level

Backtesting & Optimization: Comprehensive performance tracking features make this strategy ideal for testing different parameter combinations

Limitations & Considerations

Like all trend-following strategies, performance may suffer in choppy or ranging markets

Default 100% position sizing means full capital exposure per trade - consider reducing for conservative risk management

Higher length values (70+) reduce signal frequency but may improve signal quality

Multiple simultaneous risk management features may create conflicting exit signals

Past performance shown in backtests does not guarantee future results

Customization Tips

For more aggressive trading:

Reduce length parameter (minimum 70)

Decrease band multiplier for tighter bands

Enable short trades

Use lower profit target R:R ratios

For more conservative trading:

Increase length parameter

Enable ZLEMA trend confirmation

Use wider ATR stop-loss multipliers

Enable break-even stop-loss

Reduce position size from 100% default

For optimal choppy market performance:

Enable ZLEMA trend confirmation

Increase band multiplier

Use tighter profit targets

Avoid re-entry on trend continuation

Visual Elements

The strategy plots several elements on the chart:

ZLEMA line (color-coded by trend direction)

Upper and lower volatility bands

Long entry markers (green triangles)

Short entry markers (red triangles, when enabled)

Stop-loss levels (when positions are open)

Take-profit levels (when enabled and positions are open)

Trailing stop lines (when enabled and positions are open)

Optional ZLEMA trend markers (triangles at highs/lows)

Optional trade log labels showing complete trade information

Exit Reason Codes (for CSV Export)

When CSV export is enabled, exit reasons are coded as:

0 = Manual/Other

1 = Trailing Stop-Loss

2 = Profit Target

3 = ATR Stop-Loss

4 = Trend Change

Conclusion

Zero Lag Trend Signals V7 provides a robust framework for trend-following with extensive customization options. The strategy balances simplicity in its core logic with sophisticated risk management features, making it suitable for both beginner and advanced traders. By reducing moving average lag while incorporating volatility-based signals, it aims to capture trends earlier while managing risk through multiple configurable exit mechanisms.

The modular design allows traders to start with basic trend-following and progressively add complexity through ZLEMA confirmation, multiple stop-loss methods, and advanced exit strategies. Comprehensive performance tracking and export capabilities make this strategy an excellent tool for systematic testing and optimization.

Note: This strategy is provided for educational and backtesting purposes. All trading involves risk. Past performance does not guarantee future results. Always test thoroughly with paper trading before risking real capital, and adjust position sizing and risk parameters according to your risk tolerance and account size.

================================================================================

TAGS:

================================================================================

trend following, ZLEMA, zero lag, volatility bands, ATR stops, risk management, swing trading, momentum, trend confirmation, backtesting

================================================================================

CATEGORY:

================================================================================

Strategies

================================================================================

CHART SETUP RECOMMENDATIONS:

================================================================================

For optimal visualization when publishing:

Use a clean chart with no other indicators overlaid

Select a timeframe that shows multiple trade signals (4H or Daily recommended)

Choose a trending asset (crypto, forex major pairs, or trending stocks work well)

Show at least 6-12 months of data to demonstrate strategy across different market conditions

Enable the floating stats table to display key performance metrics

Ensure all indicator lines (ZLEMA, bands, stops) are clearly visible

Use the default chart type (candlesticks) - avoid Heikin Ashi, Renko, etc.

Make sure symbol information and timeframe are clearly visible

================================================================================

COMPLIANCE NOTES:

================================================================================

✅ Open-source publication with complete code visibility

✅ English-only title and description

✅ Detailed explanation of methodology and calculations

✅ Realistic commission (0.1%) and slippage (3 ticks) included

✅ All default parameters clearly documented

✅ Performance limitations and risks disclosed

✅ No unrealistic claims about performance

✅ No guaranteed results promised

✅ Appropriate for public library (original trend-following implementation with ZLEMA)

✅ Educational disclaimers included

✅ All features explained in detail

================================================================================

AstraAlgo BacktesterOVERVIEW

The AstraAlgo Backtester allows traders to simulate and evaluate trading strategies directly on TradingView. By simulating trades across different timeframes and markets, it provides valuable insights into win rates, drawdowns, and overall strategy effectiveness.

SIGNAL MODES

Signal Modes generate proprietary trade signals based on live price data. Users can choose between Off, Basic, Advanced, or Custom modes to evaluate strategies under different conditions and refine their trading approach.

ADJUSTABLE BACKTESTING

Parameters for historical simulations can be customized to test different market conditions and trading scenarios. This allows traders to measure strategy performance, including win rate, profit/loss, and risk/reward ratios, helping refine and optimize strategies before live execution.

BAR COLORING

Bar Coloring highlights bullish and bearish bars on historical charts, allowing traders to visually assess trend direction and trade outcomes during backtesting. This makes it easier to analyze momentum and strategy effectiveness at a glance.

ASTRA CLOUD

Astra Cloud overlays dynamic support and resistance levels on live price data. These zones adapt automatically to past market movements, helping traders identify areas where trades would have reacted, aiding strategy evaluation and optimization.

Delta Drift Allocator - StrategySummary

Bar-close, drift-based allocation alerts that keep exposure centered around a user-set base with full compounding by default. One alert per bar close. Non-repainting. Invite-Only.

Description

Delta Drift Allocator monitors how far current exposure drifts from a reference profile. When drift exceeds your threshold, it issues a single bar-close instruction (BUY/SELL with quantity) to nudge exposure back toward center. The emphasis is path discipline—rules that react to swings without predicting direction—plus a simple one-alert workflow.

A start-sync input lets you align the script with your actual initial fill so subsequent sizes match your account. Profit handling supports Reinvest (compound) or Skim to base (bookkeep excess).

How to use (overview)

Add to chart (recommended timeframe: 4h).

Set Inputs: drift threshold, min notional, start method (Auto or Manual sync at your bar-close time + filled units).

Create one alert: This strategy → Any alert() function call, Once per bar close. Leave Message empty.

Execute externally: place BUY/SELL for exactly the shown qty (manual or your own webhook executor outside TradingView).

Note: A detailled manual is provided after purchase.

Why traders choose it

Bar-close discipline (no intra-bar churn, non-repainting)

Drift-responsive adjustments that can harvest parts of oscillations

Full compounding by default; optional “skim to base” bookkeeping

Start-sync to match real fills; minimal panel plots you can hide

Access (Invite-Only)

To request access, send me a PM on TradingView. You’ll receive detailled information about the process.

Note: Requests for older strategies are no longer processed—please refer to this release only.

Compliance

Signals only; the script does not place orders or read balances. Backtests are approximations and are not indicative of future results. Markets involve risk, including possible loss. Extended one-way advances can lag all-in exposure; starting right after strong rallies may show initial drawdowns.

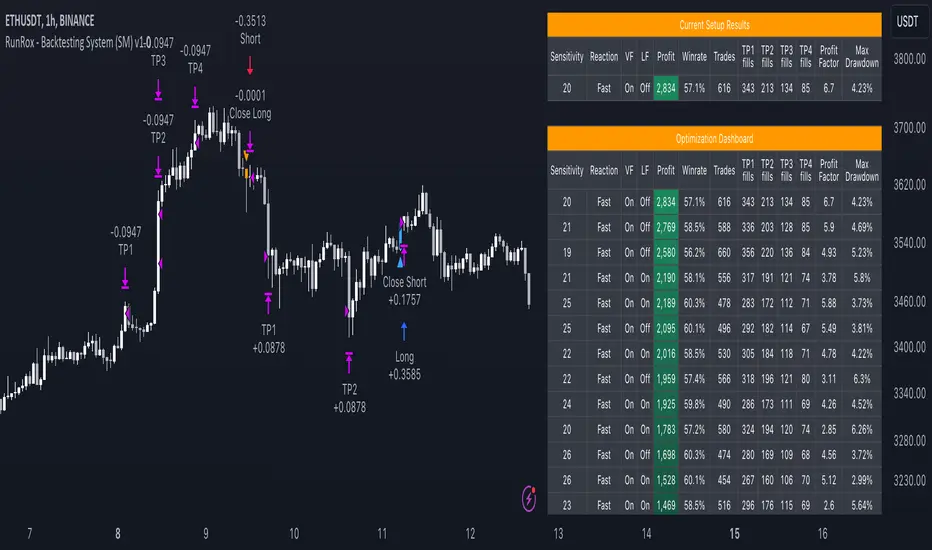

Backtest - Strategy Builder [AlgoAlpha]🟠 OVERVIEW

This script by AlgoAlpha is a modular Strategy Builder designed to let traders test custom trade entry and exit logic on TradingView without writing their own Pine code. It acts as a framework where users can connect multiple external signals, chain them in sequences, and run backtests with built-in leverage, margin, and risk controls. Its main strength is flexibility—you can define up to five sequential steps for entry and exit conditions on both long and short sides, with logic connectors (AND/OR) controlling how conditions combine. This lets you test complex multi-step confirmation workflows in a controlled, visual backtesting environment.

🟠 CONCEPTS

The system works by linking external signals —these can be values from other indicators, and/or custom sources—to conditional checks like “greater than,” “less than,” or “crossover.” You can stack these checks into steps , where all conditions in a step must pass before the sequence moves to the next. This creates a chain of logic that must be completed before a trade triggers. On execution, the strategy sizes positions according to your chosen leverage mode ( Cross or Isolated ) and allocation method ( Percent of equity or absolute USD value]). Liquidation prices are simulated for both modes, allowing realistic margin behaviour in testing. The script also tracks performance metrics like Sharpe, Sortino, profit factor, drawdown, and win rate in real time.

🟠 FEATURES

Up to 5 sequential steps for both long and short entries, each with multiple conditions linked by AND/OR logic.

Two leverage modes ( Cross and Isolated ) with independent long/short leverage multipliers.

Separate multi-step exit triggers for longs and shorts, with optional TP/SL levels or opposite-side triggers for flipping positions.

Position sizing by equity percent or fixed USD amount, applied before leverage.

Realistic liquidation price simulation for margin testing.

Built-in trade gating and validation—prevents trades if configuration rules aren’t met (e.g., no exit defined for an active side).

Full performance dashboard table showing live strategy status, warnings, and metrics.

Configurable bar coloring based on position side and TP/SL level drawing on chart.

Integration with TradingView's strategy backtester, allowing users to view more detailed metrics and test the strategy over custom time horizons.

🟠 USAGE

Add the strategy to your chart. In the settings, under Master Settings , enable longs/shorts, select leverage mode, set leverage multipliers, and define position sizing. Then, configure your Long Trigger and Short Trigger groups: turn on conditions, pick which external signal they reference, choose the comparison type, and assign them to a sequence step. For exits, use the corresponding Exit Long Trigger and Exit Short Trigger groups, with the option to link exits to opposite-side entries for auto-flips. You can also enable TP and/or SL exits with custom sources for the TP/SL levels. Once set, the strategy will simulate trades, show performance stats in the on-chart table, and highlight any configuration issues before execution. This makes it suitable for testing both simple single-signal systems and complex, multi-filtered strategies under realistic leverage and margin constraints.

🟠 EXAMPLE

The backtester on its own does not contain any indicator calculation; it requires input from external indicators to function. In this example, we'll be using AlgoAlpha's Smart Signals Assistant indicator to demonstrate how to build a strategy using this script.

We first define the conditions beforehand:

Entry :

Longs – SSA Bullish signal (strong OR weak)

Shorts – SSA Bearish signal (strong OR weak)

Exit

Longs/Shorts: (TP/SL hit OR opposing signal fires)

Other Parameters (⚠️Example only, tune this based on proper risk management and settings)

Long Leverage: default (3x)

Short Leverage: default (3x)

Position Size: default (10% of equity)

Steps

Load up the required indicators (in this example, the Smart Signals Assistant).

Ensure the required plots are being output by the indicator properly (signals and TP/SL levels are being plotted).

Open the Strategy Builder settings and scroll down to "CONDITION SETUP"; input the signals from the external indicator.

Configure the exit conditions, add in the TP/SL levels from the external indicator, and add an additional exit condition → {{Opposite Direction}} Entry Trigger.

After configuring the entry and exit conditions, the strategy should now be running. You can view information on the strategy in TradingView's backtesting report and also in the Strategy Builder's information table (default top right corner).

It is important to note that the strategy provided above is just an example, and the complexity of possible strategies stretches beyond what was shown in this short demonstration. Always incorporate proper risk management and ensure thorough testing before trading with live capital.

Script a pagamento

[Kpt-Ahab] Simple AlgoPilot Riskmgt and Backtest Simple AlgoPilot Riskmgt and Backtest

This script provides a compact solution for automated risk management and backtesting within TradingView.

It offers the following core functionalities:

Risk Management:

The system integrates various risk limitation mechanisms:

Percentage-based or trailing stop-loss

Maximum losing streak limitation

Maximum drawdown limitation relative to account equity

Flexible position sizing control (based on equity, fixed size, or contracts)

Dynamic repurchasing of positions ("Repurchase") during losses with adjustable size scaling

Supports multi-stage take-profit targets (TP1/TP2) and automatic stop-loss adjustment to breakeven

External Signal Processing for Backtesting:

In addition to its own moving average crossovers, the script can process external trading signals:

External signals are received via a source input variable (e.g., from other indicators or signal generators)

Positive values (+1) trigger long positions, negative values (–1) trigger short positions

This allows for easy integration of other indicator-based strategies into backtests

Additional Backtesting Features:

Selection between different MA types (SMA, EMA, WMA, VWMA, HMA)

Flexible time filtering (trade only within defined start and end dates)

Simulation of commission costs, slippage, and leverage

Optional alert functions for moving average crossovers

Visualization of liquidation prices and portfolio development in an integrated table

Note: This script is primarily intended for strategic backtesting and risk setting optimization.

Real-time applications should be tested with caution. All order executions, alerts, and risk calculations are purely simulation-based.

Explanation of Calculations and Logics:

1. Risk Management and Position Sizing:

The position size is calculated based on the user’s choice using three possible methods:

Percentage of Equity:

The position size is a defined fraction of the available capital, dynamically adjusted based on market price (riskPerc / close).

Fixed Size (in currency): The user defines a fixed monetary amount to be used per trade.

Contracts: A fixed number of contracts is traded regardless of the current price.

Leverage: The selected leverage multiplies the position size for margin calculations.

2. Trade Logic and Signal Triggering:

Trades can be triggered through two mechanisms:

Internal Signals:

When a fast moving average crosses above or below a slower moving average (ta.crossover, ta.crossunder). The type of moving averages (SMA, EMA, WMA, VWMA, HMA) can be freely selected.

External Signals:

Signals from other indicators can be received via an input source field.

+1 triggers a long entry, –1 triggers a short entry.

Position Management:

Once entered, the position is actively managed.

Multiple take-profit targets are set.

Upon reaching a profit target, the stop-loss can optionally be moved to breakeven.

3. Stop-Loss and Take-Profit Logic:

Stop-Loss Types:

Fixed Percentage Stop:

A fixed distance below/above the entry price.

Trailing Stop:

Dynamically adjusts as the trade moves into profit.

Fast Trailing Stop:

A more aggressive variant of trailing that reacts quicker to price changes.

Take-Profit Management:

Two take-profit targets (TP1 and TP2) are supported, allowing partial exits at different stages.

Remaining positions can either reach the second target or be closed by the stop-loss.

4. Repurchase Strategy ("Scaling In" on Losses):

If a position reaches a specified loss threshold (e.g., –15%), an automatic additional purchase can occur.

The position size is increased by a configurable percentage.

Repurchases happen only if an initial position is already open.

5. Backtesting Control and Filters:

Time Filters:

A trading period can be defined (start and end date).

All trades outside the selected period are ignored.

Risk Filters: Trading is paused if:

A maximum losing streak is reached.

A maximum allowed drawdown is exceeded.

6. Liquidation Calculation (Simulation Only):

The script simulates liquidation prices based on the account balance and position size.

Liquidation lines are drawn on the chart to better visualize potential risk exposure.

This is purely a visual aid — no real broker-side liquidation is performed.

[SHORT ONLY] 10 Bar Low Pullback█ STRATEGY DESCRIPTION

The "10 Bar Low Pullback" strategy is a contrarian short trading system designed to capture pullbacks after a new 10‐bar low is made. it identifies a potential short opportunity when the current bar’s low breaks below the lowest low of the previous 10 bars, provided that the bar exhibits strong internal momentum as measured by its IBS value. An optional trend filter further refines entries by requiring that the close is below a 200-period EMA.

█ WHAT IS INTERNAL BAR STRENGTH (IBS)?

Internal Bar Strength (IBS) measures where the closing price falls within the high-low range of a bar. It is calculated as:

ibs = (close - low) / (high - low)

- Low IBS (≤ 0.2): Indicates the close is near the bar's low, suggesting oversold conditions.

- High IBS (≥ 0.8): Indicates the close is near the bar's high, suggesting overbought conditions.

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The current bar’s low is below the lowest low of the past X bars (default: 10).

The bar’s IBS is greater than the specified threshold (default: 0.85).

The signal occurs within the defined trading window (between Start Time and End Time).

If the EMA Filter is enabled, the close must be below the 200-period EMA.

2. EXIT CONDITION

An exit Signal is generated when the current close falls below the previous bar’s low (close < low ), indicating a potential bearish reversal and prompting the strategy to close its short position.

█ ADDITIONAL SETTINGS

Lookback Period: Defines the number of bars (default is 10) over which the lowest low is calculated.

IBS Threshold: Sets the minimum required IBS value (default is 0.85) to qualify as a pullback.

Trading Window: Trades are only executed between the user-defined Start Time and End Time.

EMA Filter (Optional): When enabled, short entries are only considered if the current close is below the 200-period EMA, with the EMA period being adjustable (default is 200).

█ PERFORMANCE OVERVIEW

Designed for shorting opportunities, this strategy aims to capture pullbacks following an aggressive 10-bar low break.

It leverages a combination of a lookback low and IBS measurement to identify overextended bullish moves that may revert.

The optional EMA filter helps confirm a bearish market environment by ensuring the price remains under the trend line.

Suitable for use on various assets, including stocks and ETFs, on daily or similar timeframes.

Backtesting and parameter optimization are recommended to tailor the strategy to specific market conditions.

[SHORT ONLY] ATR Sell the Rip Mean Reversion Strategy█ STRATEGY DESCRIPTION

The "ATR Sell the Rip Mean Reversion Strategy" is a contrarian system that targets overextended price moves on stocks and ETFs. It calculates an ATR‐based trigger level to identify shorting opportunities. When the current close exceeds this smoothed ATR trigger, and if the close is below a 200-period EMA (if enabled), the strategy initiates a short entry, aiming to profit from an anticipated corrective pullback.

█ HOW IS THE ATR SIGNAL BAND CALCULATED?

This strategy computes an ATR-based signal trigger as follows:

Calculate the ATR

The strategy computes the Average True Range (ATR) using a configurable period provided by the user:

atrValue = ta.atr(atrPeriod)

Determine the Threshold

Multiply the ATR by a predefined multiplier and add it to the current close:

atrThreshold = close + atrValue * atrMultInput

Smooth the Threshold

Apply a Simple Moving Average over a specified period to smooth out the threshold, reducing noise:

signalTrigger = ta.sma(atrThreshold, smoothPeriodInput)

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The current close is above the smoothed ATR signal trigger.

The trade occurs within the specified trading window (between Start Time and End Time).

If the EMA filter is enabled, the close must also be below the 200-period EMA.

2. EXIT CONDITION

An exit Signal is generated when the current close falls below the previous bar’s low (close < low ), indicating a potential bearish reversal and prompting the strategy to close its short position.

█ ADDITIONAL SETTINGS

ATR Period: The period used to calculate the ATR, allowing for adaptability to different volatility conditions (default is 20).

ATR Multiplier: The multiplier applied to the ATR to determine the raw threshold (default is 1.0).

Smoothing Period: The period over which the raw ATR threshold is smoothed using an SMA (default is 10).

Start Time and End Time: Defines the time window during which trades are allowed.

EMA Filter (Optional): When enabled, short entries are only executed if the current close is below the 200-period EMA, confirming a bearish trend.

█ PERFORMANCE OVERVIEW

This strategy is designed for use on the Daily timeframe, targeting stocks and ETFs by capitalizing on overextended price moves.

It utilizes a dynamic, ATR-based trigger to identify when prices have potentially peaked, setting the stage for a mean reversion short entry.

The optional EMA filter helps align trades with broader market trends, potentially reducing false signals.

Backtesting is recommended to fine-tune the ATR multiplier, smoothing period, and EMA settings to match the volatility and behavior of specific markets.

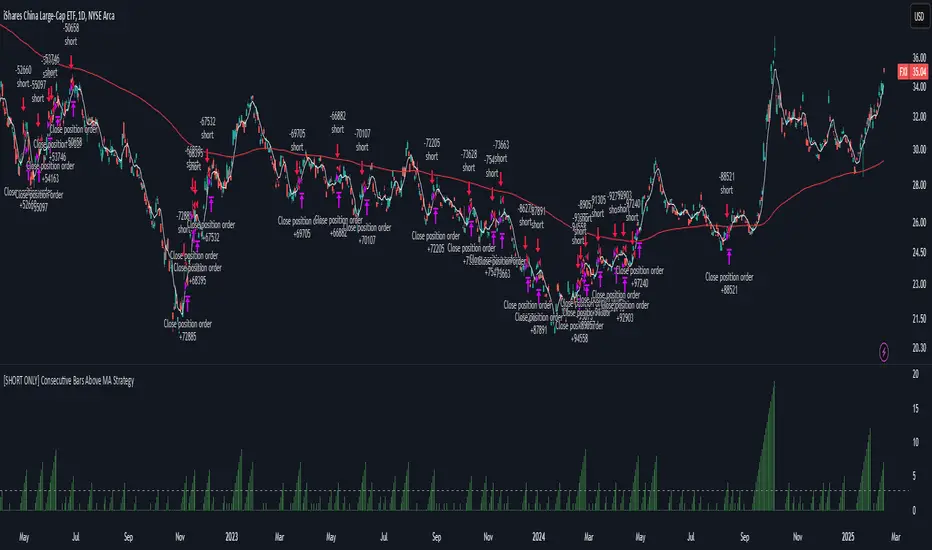

[SHORT ONLY] Consecutive Bars Above MA Strategy█ STRATEGY DESCRIPTION

The "Consecutive Bars Above MA Strategy" is a contrarian trading system aimed at exploiting overextended bullish moves in stocks and ETFs. It monitors the number of consecutive bars that close above a chosen short-term moving average (which can be either a Simple Moving Average or an Exponential Moving Average). Once the count reaches a preset threshold and the current bar’s close exceeds the previous bar’s high within a designated trading window, a short entry is initiated. An optional EMA filter further refines entries by requiring that the current close is below the 200-period EMA, helping to ensure that trades are taken in a bearish environment.

█ HOW ARE THE CONSECUTIVE BULLISH COUNTS CALCULATED?

The strategy utilizes a counter variable, `bullCount`, to track consecutive bullish bars based on their relation to the short-term moving average. Here’s how the count is determined:

Initialize the Counter

The counter is initialized at the start:

var int bullCount = na

Bullish Bar Detection

For each bar, if the close is above the selected moving average (either SMA or EMA, based on user input), the counter is incremented:

bullCount := close > signalMa ? (na(bullCount) ? 1 : bullCount + 1) : 0

Reset on Non-Bullish Condition

If the close does not exceed the moving average, the counter resets to zero, indicating a break in the consecutive bullish streak.

█ SIGNAL GENERATION

1. SHORT ENTRY

A short signal is generated when:

The number of consecutive bullish bars (i.e., bars closing above the short-term MA) meets or exceeds the defined threshold (default: 3).

The current bar’s close is higher than the previous bar’s high.

The signal occurs within the specified trading window (between Start Time and End Time).

Additionally, if the EMA filter is enabled, the entry is only executed when the current close is below the 200-period EMA.

2. EXIT CONDITION

An exit signal is triggered when the current close falls below the previous bar’s low, prompting the strategy to close the short position.

█ ADDITIONAL SETTINGS

Threshold: The number of consecutive bullish bars required to trigger a short entry (default is 3).

Trading Window: The Start Time and End Time inputs define when the strategy is active.

Moving Average Settings: Choose between SMA and EMA, and set the MA length (default is 5), which is used to assess each bar’s bullish condition.

EMA Filter (Optional): When enabled, this filter requires that the current close is below the 200-period EMA, supporting entries in a downtrend.

█ PERFORMANCE OVERVIEW

This strategy is designed for stocks and ETFs and can be applied across various timeframes.

It seeks to capture mean reversion by shorting after a series of bullish bars suggests an overextended move.

The approach employs a contrarian short entry by waiting for a breakout (close > previous high) following consecutive bullish bars.

The adjustable moving average settings and optional EMA filter allow for further optimization based on market conditions.

Comprehensive backtesting is recommended to fine-tune the threshold, moving average parameters, and filter settings for optimal performance.

[SHORT ONLY] Consecutive Close>High[1] Mean Reversion Strategy█ STRATEGY DESCRIPTION

The "Consecutive Close > High " Mean Reversion Strategy is a contrarian daily trading system for stocks and ETFs. It identifies potential shorting opportunities by counting consecutive days where the closing price exceeds the previous day's high. When this consecutive day count reaches a predetermined threshold, and if the close is below a 200-period EMA (if enabled), a short entry is triggered, anticipating a corrective pullback.

█ HOW ARE THE CONSECUTIVE BULLISH COUNTS CALCULATED?

The strategy uses a counter variable called `bullCount` to track how many consecutive bars meet a bullish condition. Here’s a breakdown of the process:

Initialize the Counter

var int bullCount = 0

Bullish Bar Detection

Every time the close exceeds the previous bar's high, increment the counter:

if close > high

bullCount += 1

Reset on Bearish Bar

When there is a clear bearish reversal, the counter is reset to zero:

if close < low

bullCount := 0

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The count of consecutive bullish closes (where close > high ) reaches or exceeds the defined threshold (default: 3).

The signal occurs within the specified trading window (between Start Time and End Time).

2. EXIT CONDITION

An exit Signal is generated when the current close falls below the previous bar’s low (close < low ), prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

Threshold: The number of consecutive bullish closes required to trigger a short entry (default is 3).

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

EMA Filter (Optional): When enabled, short entries are only triggered if the current close is below the 200-period EMA.

█ PERFORMANCE OVERVIEW

This strategy is designed for Stocks and ETFs on the Daily timeframe and targets overextended bullish moves.

It aims to capture mean reversion by entering short after a series of consecutive bullish closes.

Further optimization is possible with additional filters (e.g., EMA, volume, or volatility).

Backtesting should be used to fine-tune the threshold and filter settings for specific market conditions.

[SHORT ONLY] Internal Bar Strength (IBS) Mean Reversion Strategy█ STRATEGY DESCRIPTION

The "Internal Bar Strength (IBS) Strategy" is a mean-reversion strategy designed to identify trading opportunities based on the closing price's position within the daily price range. It enters a short position when the IBS indicates overbought conditions and exits when the IBS reaches oversold levels. This strategy is Short-Only and was designed to be used on the Daily timeframe for Stocks and ETFs.

█ WHAT IS INTERNAL BAR STRENGTH (IBS)?

Internal Bar Strength (IBS) measures where the closing price falls within the high-low range of a bar. It is calculated as:

IBS = (Close - Low) / (High - Low)

- Low IBS (≤ 0.2) : Indicates the close is near the bar's low, suggesting oversold conditions.

- High IBS (≥ 0.8) : Indicates the close is near the bar's high, suggesting overbought conditions.

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The IBS value rises to or above the Upper Threshold (default: 0.9).

The Closing price is greater than the previous bars High (close>high ).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

An exit Signal is generated when the IBS value drops to or below the Lower Threshold (default: 0.3). This prompts the strategy to exit the position.

█ ADDITIONAL SETTINGS

Upper Threshold: The IBS level at which the strategy enters trades. Default is 0.9.

Lower Threshold: The IBS level at which the strategy exits short positions. Default is 0.3.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for Stocks and ETFs markets and performs best when prices frequently revert to the mean.

The strategy can be optimized further using additional conditions such as using volume or volatility filters.

It is sensitive to extreme IBS values, which help identify potential reversals.

Backtesting results should be analyzed to optimize the Upper/Lower Thresholds for specific instruments and market conditions.

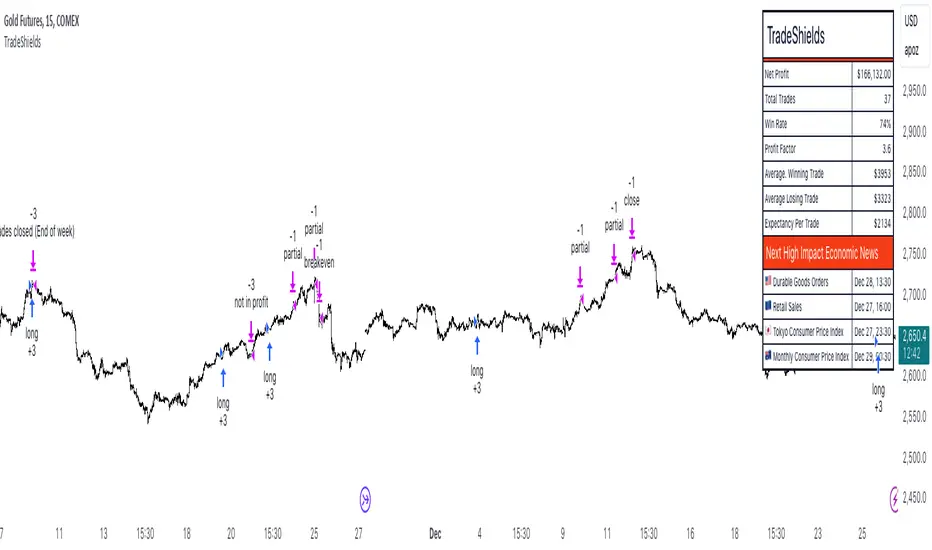

TradeShields Strategy Builder🛡 WHAT IS TRADESHIELDS?

This no-code strategy builder is designed for traders on TradingView, offering an intuitive platform to create, backtest, and automate trading strategies. While identifying signals is often straightforward, the real challenge in trading lies in managing risk and knowing when not to trade. It equips users with advanced tools to address this challenge, promoting disciplined decision-making and structured trading practices.

This is not just a collection of indicators but a comprehensive toolkit that helps identify high-quality opportunities while placing risk management at the core of every strategy. By integrating customizable filters, robust controls, and automation capabilities, it empowers traders to align their strategies with their unique objectives and risk tolerance.

_____________________________________

🛡 THE GOAL: SHIELD YOUR STRATEGY

The mission is simple: to shield your strategy from bad trades . Whether you're a seasoned trader or just starting, the hardest part of trading isn’t finding signals—it’s avoiding trades that can harm your account. This framework prioritizes quality over quantity , helping filter out suboptimal setups and encouraging disciplined execution.

With tools to manage risk, avoid overtrading, and adapt to changing market conditions, it protects your strategy against impulsive decisions and market volatility.

_____________________________________

🛡 HOW TO USE IT

1. Apply Higher Timeframe Filters

Begin by analyzing broader market trends using tools like the 200 EMA, Ichimoku Cloud, or Supertrend on higher timeframes (e.g., daily or 4-hour charts).

- Example: Ensure the price is above the 200 EMA on the daily chart for long trades or below it for short trades.

2. Identify the Appropriate Entry Signal

Choose an entry signal that aligns with your model and the asset you're trading. Options include:

Supertrend changes for trend reversals.

Bollinger Band touches for mean-reversion trades.

RSI strength/weakness for overbought or oversold conditions.

Breakouts of key levels (e.g., daily or weekly highs/lows) for momentum trades.

MACD and TSI flips.

3. Determine Take-Profit and Stop-Loss Levels

Set clear exit strategies to protect your capital and lock in profits:

Use single, dual, or triple take-profit levels based on percentages or price levels.

Choose a stop-loss type, such as fixed percentage, ATR-based, or trailing stops.

Optionally, set breakeven adjustments after hitting your first take-profit target.

4. Apply Risk Management Filters

Incorporate risk controls to ensure disciplined execution:

Limit the number of trades per day, week, or month to avoid overtrading.

Use time-based filters to trade during specific sessions or custom windows.

Avoid trading around high-impact news events with region-specific filters.

5. Automate and Execute

Leverage the advanced automation features to streamline execution. Alerts are tailored specifically for each supported platform, ensuring seamless integration with tools like PineConnector, 3Commas, Zapier, and more.

_____________________________________

🛡 CORE FOCUS: RISK MANAGEMENT, AUTOMATION, AND DISCIPLINED TRADING

This builder emphasizes quality over quantity, encouraging traders to approach markets with structure and control. Its innovative tools for risk management and automation help optimize performance while reducing effort, fostering consistency and long-term success.

_____________________________________

🛡 KEY FEATURES

General Settings

Theme Customization : Light and dark themes for a tailored interface.

Timezone Adjustment : Align session times and news schedules with your local timezone.

Position Sizing : Define lot sizes to manage risk effectively.

Directional Control : Choose between long-only, short-only, or both directions for trading.

Time Filters

Day-of-Week Selection : Enable or disable trading on specific days.

Session-Based Trading : Restrict trades to major market sessions (Asia, London, New York) or custom windows.

Custom Time Windows : Precisely control the timeframes for trade execution.

Risk Management Tools

Trade Limits : Maximum trades per day, week, or month to avoid overtrading.

Automatic Trade Closures : End-of-session, end-of-day, or end-of-week options.

Duration-Based Filters : Close trades if take-profit isn’t reached within a set timeframe or if they remain unprofitable beyond a specific duration.

Stop-Loss and Take-Profit Options : Fixed percentage or ATR-based stop-losses, single/dual/triple take-profit levels, and breakeven stop adjustments.

Economic News Filters

Region-Specific Filters : Exclude trades around major news events in regions like the USA, UK, Europe, Asia, or Oceania.

News Avoidance Windows : Pause trades before and after high-impact events or automatically close trades ahead of scheduled news releases.

Higher Timeframe Filters

Multi-Timeframe Tools : Leverage EMAs, Supertrend, or Ichimoku Cloud on higher timeframes (Daily, 4-hour, etc.) for trend alignment.

Chart Timeframe Filters

Precision Filtering : Apply EMA or ADX-based conditions to refine trade setups on current chart timeframes.

Entry Signals

Customizable Options : Choose from signals like Supertrend, Bollinger Bands, RSI, MACD, Ichimoku Cloud, or EMA pullbacks.

Indicator Parameter Overrides : Fine-tune default settings for specific signals.

Exit Settings

Flexible Take-Profit Targets : Single, dual, or triple targets. Exit at significant levels like daily/weekly highs or lows.

Stop-Loss Variability : Fixed, ATR-based, or trailing stop-loss options.

Alerts and Automation

Third-Party Integrations : Seamlessly connect with platforms like PineConnector, 3Commas, Zapier, and Capitalise.ai.

Precision-Formatted Alerts : Alerts are tailored specifically for each platform, ensuring seamless execution. For example:

- PineConnector alerts include risk-per-trade parameters.

- 3Commas alerts contain bot-specific configurations.

_____________________________________

🛡 PUBLISHED CHART SETTINGS: 15m COMEX:GC1!

Time Filters : Trades are enabled from Tuesday to Friday, as Mondays often lack sufficient data coming off the weekend, and weekends are excluded due to market closures. Custom time sessions are turned off by default, allowing trades throughout the day.

Risk Filters : Risk is tightly controlled by limiting trades to a maximum of 2 per day and enabling a mechanism to close trades if they remain open too long and are unprofitable. Weekly trade closures ensure that no positions are carried over unnecessarily.

Economic News Filters : By default, trades are allowed during economic news periods, giving traders flexibility to decide how to handle volatility manually. It is recommended to enable these filters if you are creating strategies on lower timeframes.

Higher Timeframe Filters : The setup incorporates confluence from higher timeframe indicators. For example, the 200 EMA on the daily timeframe is used to establish trend direction, while the Ichimoku cloud on the 30-minute timeframe adds additional confirmation.

Entry Signals : The strategy triggers trades based on changes in the Supertrend indicator.

Exit Settings : Trades are configured to take partial profits at three levels (1%, 2%, and 3%) and use a fixed stop loss of 2%. Stops are moved to breakeven after reaching the first take profit level.

_____________________________________

🛡 WHY CHOOSE THIS STRATEGY BUILDER?

This tool transforms trading from reactive to proactive, focusing on risk management and automation as the foundation of every strategy. By helping users avoid unnecessary trades, implement robust controls, and automate execution, it fosters disciplined trading.

DAILY Supertrend + EMA Crossover with RSI FilterThis strategy is a technical trading approach that combines multiple indicators—Supertrend, Exponential Moving Averages (EMAs), and the Relative Strength Index (RSI)—to identify and manage trades.

Core Components:

1. Exponential Moving Averages (EMAs):

Two EMAs, one with a shorter period (fast) and one with a longer period (slow), are calculated. The idea is to spot when the faster EMA crosses above or below the slower EMA. A fast EMA crossing above the slow EMA often suggests upward momentum, while crossing below suggests downward momentum.

2. Supertrend Indicator:

The Supertrend uses Average True Range (ATR) to establish dynamic support and resistance lines. These lines shift above or below price depending on the prevailing trend. When price is above the Supertrend line, the trend is considered bullish; when below, it’s considered bearish. This helps ensure that the strategy trades only in the direction of the overall trend rather than against it.

3. RSI Filter:

The RSI measures momentum. It helps avoid buying into markets that are already overbought or selling into markets that are oversold. For example, when going long (buying), the strategy only proceeds if the RSI is not too high, and when going short (selling), it only proceeds if the RSI is not too low. This filter is meant to improve the quality of the trades by reducing the chance of entering right before a reversal.

4. Time Filters:

The strategy only triggers entries during user-specified date and time ranges. This is useful if one wants to limit trading activity to certain trading sessions or periods with higher market liquidity.

5. Risk Management via ATR-based Stops and Targets:

Both stop loss and take profit levels are set as multiples of the ATR. ATR measures volatility, so when volatility is higher, both stops and profit targets adjust to give the trade more breathing room. Conversely, when volatility is low, stops and targets tighten. This dynamic approach helps maintain consistent risk management regardless of market conditions.

Overall Logic Flow:

- First, the market conditions are analyzed through EMAs, Supertrend, and RSI.

- When a buy (long) condition is met—meaning the fast EMA crosses above the slow EMA, the trend is bullish according to Supertrend, and RSI is below the specified “overbought” threshold—the strategy initiates or adds to a long position.

- Similarly, when a sell (short) condition is met—meaning the fast EMA crosses below the slow EMA, the trend is bearish, and RSI is above the specified “oversold” threshold—it initiates or adds to a short position.

- Each position is protected by an automatically calculated stop loss and a take profit level based on ATR multiples.

Intended Result:

By blending trend detection, momentum filtering, and volatility-adjusted risk management, the strategy aims to capture moves in the primary trend direction while avoiding entries at excessively stretched prices. Allowing multiple entries can potentially amplify gains in strong trends but also increases exposure, which traders should consider in their risk management approach.

In essence, this strategy tries to ride established trends as indicated by the Supertrend and EMAs, filter out poor-quality entries using RSI, and dynamically manage trade risk through ATR-based stops and targets.

Project Monday Strategy [AlgoAI System]Overview