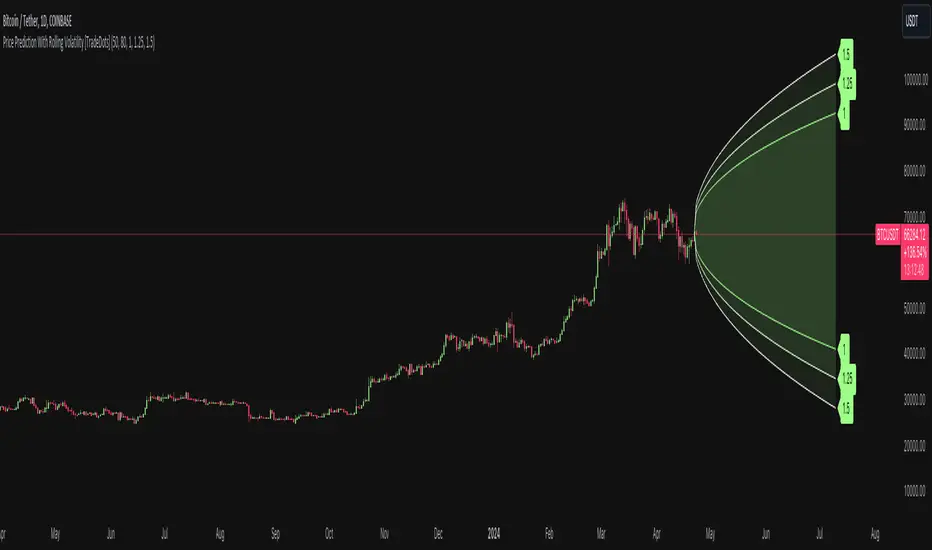

Standard Deviation Channel (4x)Standard Deviation Channel (4x)

A linear regression channel with up to 4 standard deviation bands on each side, plus built-in moving averages and high/low levels from higher timeframes. Basically everything I need on one indicator without cluttering my chart with 5 different scripts.

What it does

The core is a standard deviation channel based on linear regression. You get the regression line (base) and can enable up to 4 deviation levels above and below (±1σ, ±2σ, ±3σ, ±4σ). Each level can be toggled independently and the multipliers are adjustable if you want something like 1.5 or 2.5 instead of whole numbers. The fills between bands help visualize the zones.

Pearson's R is available if you want to see the correlation strength of the regression.

Moving Averages

6 MAs included, each fully configurable:

- Type: SMA, EMA, WMA, VWMA, RMA, HMA, DEMA, TEMA

- Custom length and source

- Individual colors

High/Low Levels

Shows horizontal lines at:

- Weekly High/Low

- Monthly High/Low

- Yearly High/Low

- Previous Week/Month/Year High/Low

Useful for spotting key levels without switching timeframes. Labels included so you know which line is which.

Alerts

- Deviation band breaks (all 8 levels)

- MA crossovers (price crossing above/below)

- High/Low level breaks

Settings

Everything is off by default except the ±1σ and ±2σ bands. Enable what you need, disable what you don't. Colors are fully customizable.

Standarddevation

Adaptive ML VWAP v1.0Overview

Adaptive ML VWAP is a next-generation "Smart Indicator" that moves beyond static deviations (Standard Deviation). Instead of assuming market volatility is distributed normally (Bell Curve), this indicator uses a k-Nearest Neighbors (k-NN) machine learning engine to learn the specific volatility behavior of the asset you are trading.

It answers the question: "When price extends away from VWAP, how far does it actually go before reversing?"

The Adaptive ML Engine

This script features a 5-Dimensional ML Engine that tracks every major extension or pullback event. It records:

Deviation Depth (Normalized to ATR)

Trend Slope (Is the trend steep or flat?)

ADX (Trend Strength)

VWAP Deviation (Relative Position)

Time of Day (Session Context)

When a new setup occurs, the k-NN engine instantly searches its memory for the 5 most similar historical events and calculates the probability of success based on what happened last time.

Two Strategy Modes

You can toggle the logic to suit your trading style:

1. Mean Reversion Mode (Default)

"Fade The Move"

Goal: Catch price at an exhaustion point returning to VWAP.

Signal: Triggers when price touches a Smart Band and reverses back toward the center.

k-NN Learning: Learns which conditions favor a snap-back.

Best For: Ranging markets, Lunch hours, Choppy sessions.

2. Trend Following Mode

"Ride The Move"

Goal: Catch breakouts that are launching away from value.

Signal: Triggers when price breaks out of the Inner Band (1.0).

k-NN Learning: Learns which breakouts tend to extend to the Outer Bands.

Best For: Morning Drives, News Events, Strong Trends.

Visual Guide

The indicator uses a Dynamic Gradient system to visualize risk/reward:

Cyan Mist (0.5 - 1.0): The Value Zone. Noise area. Safe for trend entries.

Deep Cyan (1.0 - 2.0): The Trend Zone. Price is moving proactively.

Orange Glow (2.0 - 3.0): The Danger Zone. Price is statistically overextended. Reversals are highly probable here.

"Fractal" Math

Unlike standard indicators that break when you change timeframes, Adaptive ML VWAP uses Fractal Normalization.

A "2.0 Band" on a 15-second chart means the same statistical extreme as a "2.0 Band" on a 4-hour chart.

Auto-Adaptive Lookback: The indicator automatically boosts the ML memory (Lookback) on lower timeframes (seconds/minutes) where more noise requires larger sample sizes, ensuring robust predictions without manual tweaking.

Settings

Auto-Adapting Lookback: (Default: True) automatically increases Lookback to 100+ for seconds charts and 50+ for minute charts.

Lookback (Events): Manual override base value (Default: 100).

Strategy Mode: Toggle between Mean Reversion and Trend Following.

k-Neighbors: The number of similar past events to structurally compare (Default: 5).

Disclaimer: This tool is for educational purposes. Machine learning performance is dependent on market conditions and historical recursion.

Kijun Sen Standard Deviation | QuantLapse SystemsOverview

The Kijun Sen Standard Deviation indicator by QuantLapse Systems is a volatility-aware trend-following framework that combines the structural equilibrium of the Kijun Sen (基準線) with statistically adaptive standard deviation bands.

By anchoring trend detection to market structure and confirming direction through volatility expansion, the indicator delivers a cleaner, more reliable regime classification across varying market conditions.

Rather than reacting to short-term noise, the system focuses on identifying statistically justified trend phases , making it well-suited for disciplined, rule-based trading.

Technical Composition, Calculation, Key Components & Features

📌 Kijun Sen (基準線) – Structural Trend Baseline

Calculated as the midpoint between the highest high and lowest low over a user-defined period.

Represents market equilibrium and structural balance rather than short-term momentum.

Naturally adapts to expanding and contracting price ranges.

Provides a stable baseline for regime detection and volatility validation.

Acts as the anchor for deviation bands and persistent trend-state logic.

Unlike fast or reactive moving averages, the Kijun Sen emphasizes price structure and equilibrium , making it especially effective for higher-quality trend confirmation.

📌 Volatility Adjustment – Standard Deviation Bands

Standard deviation is calculated over a configurable lookback to measure current price dispersion.

Upper and lower envelopes are formed by applying a deviation multiplier to the Kijun Sen.

Band width expands during volatility surges and contracts during consolidation.

Creates proportional, volatility-aware thresholds instead of static offsets.

Visually represents market energy through expanding and compressing channels.

These adaptive bands ensure that trend signals only occur when volatility supports directional movement.

📌 Trend Signal & Regime Calculation

Bullish Trend is confirmed when price closes above the upper deviation band.

Bearish Trend is confirmed when price closes below the lower deviation band.

Once established, the trend state persists until an opposing volatility break occurs.

This persistence reduces whipsaws and improves regime stability.

Trend state is reinforced with color-coded lines, envelopes, and background shading.

This volatility-confirmed persistence model is visible in the chart, where trends remain intact through minor pullbacks and only flip on decisive expansion.

How It Works in Trading

✅ Volatility-Confirmed Trend Detection – Requires expansion beyond deviation bands.

✅ Noise Suppression – Filters low-energy price movement within volatility envelopes.

✅ Regime Persistence – Maintains trend state until statistical invalidation.

✅ Immediate Visual Context – Direction, strength, and transitions are clear at a glance.

Visual Representation

Trend signals are displayed directly on price using both line and background context:

🟢 Green / Teal Kijun & Envelope → Confirmed bullish regime.

🔴 Red / Pink Kijun & Envelope → Confirmed bearish regime.

Semi-transparent band fill visualizes volatility expansion and compression.

Buy and Sell labels appear only on confirmed regime transitions.

The lower panel includes:

Strategy equity curve based on trend exposure.

Buy & Hold equity for performance comparison.

Background regime shading synchronized with trend state.

Features and User Inputs

The Kijun Sen Standard Deviation framework offers a focused yet powerful set of configurable inputs:

Kijun Sen Length – Controls structural trend sensitivity.

Standard Deviation Controls – Adjust lookback length and multiplier for regime strictness.

Backtesting & Date Filters – Define evaluation periods and starting conditions.

Display Options – Toggle labels, equity curves, and background shading.

Color Customization – Fully configurable buy/sell colors for trends and equity curves.

These controls allow users to balance responsiveness, stability, and clarity without overfitting.

Practical Applications

The Kijun Sen Standard Deviation indicator is designed for traders who prioritize structure, volatility confirmation, and regime awareness.

Primary Trend Filtering – Identify and stay aligned with dominant market direction.

Volatility-Aware Trend Following – Participate only when price expansion confirms intent.

Risk-Managed Exposure – Avoid chop during compression and transitional phases.

Systematic Strategy Development – Use as a regime engine or higher-timeframe filter.

Performance Evaluation – Compare trend-following equity against buy-and-hold benchmarks.

This framework bridges classical Ichimoku structure with modern statistical validation.

Conclusion

The Kijun Sen Standard Deviation indicator by QuantLapse Systems represents a refined evolution of Ichimoku-based trend analysis.

By integrating the structural equilibrium of the Kijun Sen with adaptive standard deviation confirmation, the system delivers clearer regime classification, reduced noise, and more reliable trend participation.

Rather than attempting to predict price, it focuses on confirming when trends are statistically justified .

Who should use Kijun Sen Standard Deviation:

📊 Trend-Following Traders – Stay aligned with dominant market structure.

⚡ Momentum & Swing Traders – Enter only on volatility-backed expansions.

🤖 Systematic & Algorithmic Traders – Ideal as a regime filter or trend-state engine.

Past performance is not indicative of future results.

Disclaimer: All trading involves risk, and no indicator can guarantee profitability.

Strategic Advice: Always backtest thoroughly, optimize parameters responsibly, and align settings with your timeframe, asset class, and risk tolerance before live deployment.

Consolidation Zones Volume Delta | Flux ChartsGENERAL OVERVIEW:

The Consolidation Zones Volume Delta | Flux Charts indicator is designed to identify and visualize consolidation zones on the chart. Rather than only outlining areas of sideways price movement, the indicator analyzes volume activity occurring inside each consolidation zone. This is done by aggregating lower-timeframe volume data into the higher-timeframe consolidation range, allowing users to see how buying and selling activity evolves while price remains in a range.

What is the theory behind the indicator?:

The indicator is built around three core analytical concepts that guide how consolidation zones are detected and evaluated.

1. Consolidation as a structural phase

Periods of consolidation are characterized by reduced directional movement and compressed price ranges. During these phases, price action often alternates within a defined high–low boundary, creating a structure that can be objectively measured and tracked over time.

2. Volume behavior inside consolidation

While price may appear balanced within a consolidation range, volume activity inside that range can vary. The indicator evaluates volume contributions occurring within the vertical boundaries of the consolidation zone by using lower-timeframe data and weighting each candle’s volume based on its overlap with the zone. This produces an internal volume delta profile that reflects how buying and selling volume accumulates throughout the consolidation.

Delta behavior inside a zone may show:

Persistent dominance of buying or selling volume

Alternating shifts between buyers and sellers

Periods of relatively balanced participation

3. Markets consolidate in multiple ways, one detection method is not enough

Markets do not consolidate in a single, uniform way. To account for this, the indicator includes three distinct consolidation detection methods. Each method is calculated objectively, does not repaint, and targets a different type of sideways or low-expansion price behavior:

Candle Compression

ADX Low Trend Strength

Visual Range Boundaries

CONSOLIDATION ZONES VOLUME DELTA FEATURES:

The Consolidation Zones Volume Delta indicator includes 4 main features:

Consolidation Zones

Volume Delta

Standard Deviation Bands

Alerts

CONSOLIDATION ZONES:

🔹What is a Consolidation Zone?

A consolidation zone is a defined price range where market movement becomes compressed and price remains contained within clear upper and lower boundaries for a sustained period of time. During this phase, price does not establish a strong directional trend and instead oscillates within a relatively narrow range.

🔹Consolidation Zone Detection

The indicator automatically detects consolidation zones using three independent, rule-based methods. Each method evaluates a different market condition and can be selected individually depending on how you want consolidation to be defined. Regardless of the method used, all zones are calculated objectively and finalized once confirmed.

◇ Candles (Candle Compression)

The Candles method identifies consolidation by detecting periods of candle compression and reduced range expansion. A candle is considered part of a consolidation sequence when:

The candle body is small relative to its total range

The candle’s high–low range is smaller than the short-term Average True Range (ATR)

ATR is calculated using a 4-period average true range and is used as a volatility reference. If consecutive candles continue to meet these compression conditions, the indicator increments an internal count.

Under the Consolidation Candles section in the settings, you’ll find two controls.

Min. Consolidation Candles setting

This defines how many consecutive compressed candles are required before a consolidation zone is confirmed. Candle compression is determined using candle structure and short-term ATR, ensuring that only periods of reduced range expansion are counted. Once the minimum threshold is reached, the indicator creates a consolidation zone using the highest high and lowest low formed during the compressed sequence.

Mark Consolidation Candles

When enabled, the indicator highlights candles that meet the compression criteria, making it easy to visually identify which candles contributed to the formation of the consolidation zone.

◇ ADX (Low Trend Strength)

The ADX method identifies consolidation based on weak or declining trend strength rather than candle structure. This method uses the Average Directional Index (ADX) to determine when directional movement is reduced.

ADX is calculated using directional movement values that are smoothed over time. When ADX remains below a user-defined threshold, price is treated as being in a low-trend market. While this condition persists, the indicator tracks the highest high and lowest low formed during the low-trend period.

Under the ADX Settings section in the settings, you’ll find the following controls.

ADX Length

Defines the lookback period used to calculate directional movement for ADX.

ADX Smoothing

Controls the smoothing applied to the ADX calculation.

ADX Threshold

Sets the level below which ADX must remain for the market to be considered consolidating.

Consolidation Strength

Defines how many consecutive candles’ ADX must stay below the threshold before a consolidation zone is confirmed. Once this requirement is met, the indicator creates a consolidation zone using the accumulated high and low from the low-trend window.

Mark Candles Below Threshold

When enabled, the indicator highlights candles where ADX remains below the threshold.

◇ Visual Range

The Visual Range method identifies consolidation by detecting clearly defined horizontal price ranges where price remains contained for a sustained period of time. The indicator continuously tracks the rolling highest high and lowest low across recent candles. When price remains inside the same high–low boundaries without breaking above or below the range, an internal counter advances.

Under the Visual Range section in the settings, you’ll find the following control.

Min. Candles in Range

Defines how many consecutive candles must remain fully contained within the same high–low range before a consolidation zone is confirmed. Once this requirement is met, the indicator creates a consolidation zone using the established range boundaries.

🔹Consolidation Zone Settings

◇ Invalidation Method

Users can choose how Consolidation Zones are invalidated, selecting between Close Break or Wick Break.

Close Break: A Consolidation Zone is invalidated when a candle closes above/below the zone.

Wick Break: A Consolidation Zone is invalidated when a candle’s wick goes above/below the zone.

◇ Merge Overlapping Zones

When enabled, overlapping Consolidation Zones are automatically combined into one unified zone.

◇ Show Last

This setting determines how many Consolidation Zones are displayed on your chart. For example, setting this to 5 will display the 5 most recent zones.

VOLUME DELTA:

Delta Volume visualizes how buying and selling volume accumulates inside each consolidation zone. Instead of using the full candle volume, the indicator isolates only the volume that occurs within the vertical boundaries of the zone. This allows you to see whether bullish or bearish volume is dominating while price remains range-bound. The visualization updates in real time while the zone is active and reflects cumulative participation rather than individual candles.

🔹How Volume Delta is Calculated

Delta Volume is calculated using lower-timeframe data and applied to the higher-timeframe consolidation zone.

Each candle’s volume is split into bullish or bearish volume based on candle direction.

Lower-timeframe candles are pulled using the selected delta timeframe.

For each lower-timeframe candle, only the portion of volume that vertically overlaps the consolidation zone is counted.

Volume is weighted by the amount of overlap between the candle’s range and the zone’s range.

Bullish and bearish volume are accumulated over time to form a running, cumulative delta profile for the zone.

🔹Volume Delta Settings

◇ Enable

Turns the Delta Volume visualization on or off. Consolidation zones continue to plot when disabled.

◇ Show Delta %

Displays the percentage breakdown of bullish versus bearish volume inside the consolidation zone. Percentages are derived from cumulative volume totals.

◇ 3D Visual

When enabled, the delta blocks are extended diagonally using a depth offset derived from the instrument’s daily ATR. This creates visible side faces and top faces for the delta blocks, simulating depth without altering any calculations. The 3D effect is purely visual. It does not change how volume is calculated, weighted, or accumulated.

Users can control the intensity of the 3D effect choosing a value between 1 and 5. Increasing this value increases:

The horizontal offset of the delta blocks

The vertical depth projection applied to the volume faces

Higher values produce a more pronounced 3D appearance by pushing the delta visualization further away from the consolidation box. Lower values keep the visualization flatter and closer to the box boundaries. The depth scaling is normalized using ATR, so the effect adapts proportionally to the instrument’s volatility.

◇ Volume Delta Display Style

Controls how bullish and bearish volume are displayed inside the Consolidation Zone:

Horizontal: Volume is split top-to-bottom within the zone

Vertical: Volume is split left-to-right across the zone

◇ Timeframe

Defines the lower timeframe used for Volume Delta calculations. When a timeframe is selected, the indicator pulls lower-timeframe price and volume data and maps it into the higher-timeframe consolidation zone. Each lower-timeframe candle is evaluated individually. Only the portion of its volume that vertically overlaps the consolidation zone is included, and that volume is weighted based on the candle’s overlap with the zone’s price range. If the Timeframe field is left empty, the indicator defaults to using the chart’s current timeframe for delta calculations.

Using a lower timeframe increases the granularity of the delta calculation, allowing volume changes inside the zone to be measured more precisely. Using a higher timeframe produces a smoother, less granular delta profile.

Please Note: Delta rendering is automatically limited to available lower-timeframe data to prevent incomplete or distorted visuals when historical lower-timeframe volume is unavailable due to TradingView data limits.

STANDARD DEVIATION BANDS:

Standard Deviation Bands project measured price distance away from a confirmed consolidation zone using the size of that zone as the reference unit. Rather than calculating volatility from historical price dispersion, the bands are derived directly from the height of the consolidation range itself. Each band represents a fixed multiple of the consolidation zone’s height and is plotted symmetrically above and below the zone.

🔹How the bands are calculated

Once a consolidation zone is finalized, the indicator calculates the zone height as:

Zone Height = Zone High − Zone Low

This value becomes the base measurement for all deviation calculations. For each enabled band:

Upper bands are placed above the consolidation zone’s high

Lower bands are placed below the consolidation zone’s low

The distance of each band from the zone is calculated by multiplying the zone height by the selected band multiplier. These band levels are fixed relative to the consolidation zone and do not recalculate based on future price movement.

🔹Standard Deviation Band Settings

◇ Band 1

Enables the first deviation band above and below the consolidation zone. The Band 1 multiplier defines how far the band is placed from the zone in terms of zone height. For example, a multiplier of 1 plots the band one full zone height above and below the consolidation range.

◇ Band 2

Enables a second deviation band at a greater distance from the consolidation zone. Band 2 uses its own multiplier and is calculated independently of Band 1, allowing multiple expansion levels to be displayed simultaneously.

◇ Fill Bands

When enabled, the area between the consolidation zone and each deviation band is filled with a semi-transparent color. Upper fills apply to bands above the zone, and lower fills apply to bands below the zone. Fills are static and tied directly to the consolidation zone boundaries.

◇ Color Customization

Each deviation band has independent color controls for:

Upper band lines and fills

Lower band lines and fills

This allows users to visually distinguish between bullish and bearish extensions as well as between multiple deviation levels.

ALERTS:

Users can create alerts for the following:

New Consolidation Zone Formed

Consolidation Zone Break

UNIQUENESS:

This indicator combines multiple consolidation detection methods with lower-timeframe volume delta analysis inside each consolidation zone. It visualizes bullish and bearish volume using weighted overlap logic and optional 3D rendering for improved clarity. Users can choose how volume is displayed, apply structure-based deviation bands, and enable alerts for new zones and zone breaks. All features are rule-based, configurable, and designed to work together within a single framework.

SMC Statistical Liquidity Walls [PhenLabs]📊 SMC Statistical Liquidity Walls

Version: PineScript™ v6

📌 Description

The SMC Statistical Liquidity Walls indicator is designed to visualize market volatility and potential reversal zones using advanced statistical modeling. Unlike traditional Bollinger Bands that use simple lines, this script utilizes an “Inverted Sigmoid” opacity function to create a “fog of war” effect. This visualizes the density of liquidity: the further price moves from the equilibrium (mean), the “harder” the liquidity wall becomes.

This tool solves the problem of over-trading in low-probability areas. By automatically mapping “Premium” (Resistance) and “Discount” (Support) zones based on Standard Deviation (SD), traders can instantly see when price is overextended. The result is a clean, intuitive overlay that helps you identify high-probability mean reversion setups without cluttering your chart with manual drawings.

🚀 Points of Innovation

Inverted Sigmoid Logic: A custom mathematical function maps Standard Deviation to opacity, creating a realistic “wall” density effect rather than linear gradients.

Dynamic “Solidity”: The indicator is transparent at the center (Equilibrium) and becomes visually solid at the edges, mimicking physical resistance.

Separated Directional Bias: distinct Red (Premium) and Green (Discount) coding helps SMC traders instantly recognize expensive vs. cheap pricing.

Smart “Safe” Deviation: Includes fallback logic to handle calculation errors if deviation hits zero, ensuring the indicator never crashes during data gaps.

🔧 Core Components

Basis Calculation: Uses a Simple Moving Average (SMA) to determine the market’s equilibrium point.

Standard Deviation Zones: Calculates 1SD, 2SD, and 3SD levels to define the statistical extremes of price action.

Sigmoid Alpha Calculation: Converts the SD distance into a transparency value (0-100) to drive the visual gradient.

🔥 Key Features

Automated Premium/Discount Zones: Red zones indicate overbought (Premium) areas; Green zones indicate oversold (Discount) areas.

Customizable Density: Users can adjust the “Steepness” and “Midpoint” of the sigmoid curve to control how fast the walls become solid.

Integrated Alerts: Built-in alert conditions trigger when price hits the “Solid” wall (2SD or higher), perfect for automated trading or notifications.

Visual Clarity: The center of the chart remains clear (high transparency) to keep focus on price action where it matters most.

🎨 Visualization

Equilibrium Line: A gray line representing the mean price.

Gradient Fills: The space between bands fills with color that increases in opacity as it moves outward.

Premium Wall: Upper zones fade from transparent red to solid red.

Discount Wall: Lower zones fade from transparent green to solid green.

📖 Usage Guidelines

Range Period: Default 20. Controls the lookback period for the SMA and Standard Deviation calculation.

Source: Default Close. The price data used for calculations.

Center Transparency: Default 100 (Clear). Controls how transparent the middle of the chart is.

Edge Transparency: Default 45 (Solid). Controls the opacity of the outermost liquidity wall.

Wall Steepness: Default 2.5. Adjusts how aggressively the gradient transitions from clear to solid.

Wall Start Point: Default 1.5 SD. The deviation level where the gradient shift begins to accelerate.

✅ Best Use Cases

Mean Reversion Trading: Enter trades when price hits the solid 2SD or 3SD wall and shows rejection wicks.

Take Profit Targets: Use the Equilibrium (Gray Line) as a logical first target for reversal trades.

Trend Filtering: Do not initiate new long positions when price is deep inside the Red (Premium) wall.

⚠️ Limitations

Lagging Nature: As a statistical tool based on Moving Averages, the walls react to past price data and may lag during sudden volatility spikes.

Trending Markets: In strong parabolic trends, price can “ride” the bands for extended periods; mean reversion should be used with caution in these conditions.

💡 What Makes This Unique

Physics-Based Visualization: We treat liquidity as a physical barrier that gets denser the deeper you push, rather than just a static line on a chart.

🔬 How It Works

Step 1: The script calculates the mean (SMA) and the Standard Deviation (SD) of the source price.

Step 2: It defines three zones above and below the mean (1SD, 2SD, 3SD).

Step 3: The custom `get_inverted_sigmoid` function calculates an Alpha (transparency) value based on the SD distance.

Step 4: Plot fills are colored dynamically, creating a seamless gradient that hardens at the extremes to visualize the “Liquidity Wall.”

💡 Note

For best results, combine this indicator with Price Action confirmation (such as pin bars or engulfing candles) when price touches the solid walls.

Z-EMA Fusion BandsDesigned with crypto markets in mind, particularly Bitcoin , it builds on the concept that the 1-Week 50 EMA often serves as a long-term bull/bear market threshold — an area where institutional bias, momentum shifts, and cyclical rotations tend to occur.

🔹 Core Components & Synergies:

1. 1W 50 EMA (Higher Timeframe)

- This EMA is calculated on a weekly timeframe, regardless of your current chart.

- In crypto, price above the 1W 50 EMA typically aligns with long-term bull market phases, while extended periods below can signify bearish macro structure.

- The slope of the EMA is also analyzed to add directional confidence to trend strength.

2. ±1 Standard Deviation Bands

- Surrounding the 50 EMA, these bands visualize normal price dispersion relative to trend.

- When price consistently hugs or breaks outside these bands, it often reflects market expansion, volatility events, or mean-reversion opportunity.

3. Z-Score Gradient Fill

- The area between the bands is filled using a Z-score-based gradient, which dynamically adjusts color based on how far price is from the EMA (in terms of standard deviations).

- Color shifts from aqua (near EMA) to fuchsia (far from EMA) help you spot price compression, equilibrium, or overextension at a glance.

- The fill also uses transparency scaling, making it fade as price stretches further, emphasizing the core structure.

4. Directional EMA Coloring

- The EMA line itself is colored based on:

- The slope of the EMA (rising/falling)

- Whether the HTF candle is bullish or bearish

- This provides intuitive color-coded confirmation of momentum alignment or potential exhaustion.

5. Price/EMA Divergence Detection

- The script detects bullish and bearish divergence between price and the EMA (rather than using a traditional oscillator).

- Bullish Divergence: Price makes a lower low, EMA makes a higher low.

- Bearish Divergence: Price makes a higher high, EMA makes a lower high.

- These signals often mark transitional zones where momentum fades before a trend reversal or correction.

📊 Suggested Uses:

🔸 Swing and Position Trading:

- Use the 1W 50 EMA as a macro-trend anchor.

- Stay long-biased when price is above with positive slope, and short-biased when below.

- Consider entries near band edges for mean-reversion plays, especially if confluence forms with divergence signals.

🔸 Volatility-Based Filtering:

- Use the Z-score fill to identify volatility compression (near EMA) or expansion (edge of bands).

- Combine this with breakout strategies or dynamic position sizing.

🔸 Divergence Confirmation:

- Combine divergence markers with HTF EMA slope for high-probability setups.

- Bullish div + EMA flattening/rising can signal the start of accumulation after a macro dip.

🔸 Multi-Timeframe Analysis:

- Works well as a structural overlay on intraday charts (1H, 4H, 1D).

- Use this indicator to track long-term bias while executing lower timeframe trades.

⚠️ Disclaimer:

This indicator is designed for educational and informational purposes only. It does not constitute financial advice or a recommendation to buy or sell any asset.

Always use proper risk management, and combine with your own analysis, tools, and strategy. Performance in past market conditions does not guarantee future results.

VWAP Composites📊 VWAP Composite - Advanced Multi-Period Volume Weighted Average Price Indicator

═══════════════════════════════════════════════════════════════════

🎯 OVERVIEW

VWAP Composite is an advanced volume-weighted average price (VWAP) indicator that goes beyond traditional single-period VWAP calculations by offering composite multi-period analysis and unprecedented customization. This indicator solves a common problem traders face: traditional VWAP resets at arbitrary intervals (session start, day, week), but significant price action and volume accumulation often spans multiple periods. VWAP Composite allows you to anchor VWAP calculations to any timeframe—or combine multiple periods into a single composite VWAP—giving you a true representation of average price weighted by volume across the exact periods that matter to your analysis.

═══════════════════════════════════════════════════════════════════

⚙️ HOW IT WORKS - CALCULATION METHODOLOGY

📌 CORE VWAP CALCULATION

The indicator calculates VWAP using the standard volume-weighted formula:

• Typical Price = (High + Low + Close) / 3

• VWAP = Σ(Typical Price × Volume) / Σ(Volume)

This calculation is performed across user-defined time periods, ensuring each bar's contribution to the average is proportional to its trading volume.

📌 STANDARD DEVIATION BANDS

The indicator calculates volume-weighted standard deviation to measure price dispersion around the VWAP:

• Variance = Σ / Σ(Volume)

• Standard Deviation = √Variance

• Upper Band = VWAP + (StdDev × Multiplier)

• Lower Band = VWAP - (StdDev × Multiplier)

These bands help identify overbought/oversold conditions relative to the volume-weighted mean, with high-volume price excursions having greater impact on band width than low-volume moves.

📌 COMPOSITE PERIOD METHODOLOGY (Auto Mode)

Unlike traditional VWAP that resets at fixed intervals, Auto Mode creates composite VWAPs by combining the current period with N previous periods:

• Period Span = 1: Current period only (standard VWAP behavior)

• Period Span = 2: Current period + 1 previous period combined

• Period Span = 3: Current period + 2 previous periods combined

• And so on...

Example: A 3-period Weekly composite VWAP calculates from the start of 2 weeks ago through the current week's end, creating a single VWAP that represents 21 days of continuous price and volume data. This provides context about where price stands relative to the volume-weighted average over multiple weeks, not just the current week.

═══════════════════════════════════════════════════════════════════

🔧 KEY FEATURES & ORIGINALITY

✅ DUAL OPERATING MODES

1️⃣ MANUAL MODE (5 Independent VWAPs)

Define up to 5 separate VWAP calculations with custom start/end times:

• Perfect for anchoring VWAP to specific events (earnings, Fed announcements, major reversals)

• Each VWAP has independent color settings for lines and deviation band backgrounds

• Individual control over calculation extension and visual extension (explained below)

• Useful for tracking multiple institutional accumulation/distribution zones simultaneously

2️⃣ AUTO MODE (Composite Period VWAP)

Automatically calculates VWAP across combined time periods:

• Supported periods: Daily, Weekly, Monthly, Quarterly, Yearly

• Configurable period span (1-20 periods)

• Always up-to-date, recalculates on each new bar

• Ideal for systematic analysis across consistent timeframes

✅ DUAL EXTENSION SYSTEM (Manual Mode Innovation)

Most VWAP indicators only offer "on/off" for extending calculations. This indicator provides two distinct extension options:

🔹 EXTEND CALCULATION TO CURRENT BAR

When enabled, continues including new bars in the VWAP calculation after the defined end time. The VWAP value updates dynamically as new volume enters the market.

Use case: You anchored VWAP to a major low 3 weeks ago. You want the VWAP to continue evolving with new volume data to track ongoing institutional positioning.

🔹 EXTEND VISUAL LINE ONLY

When enabled (and calculation extension is disabled), projects the "frozen" VWAP value forward as a reference line. The VWAP value remains fixed at what it was at the end time, but the line and deviation bands visually extend to current price.

Use case: You want to see how price is behaving relative to the VWAP that existed at a specific point in time (e.g., "Where is price now vs. the 5-day VWAP that existed at last Friday's close?").

This dual system gives you unprecedented control over whether you're tracking a "living" VWAP that incorporates new data or using historical VWAP levels as static reference points.

✅ CUSTOMIZABLE STANDARD DEVIATION BANDS

• Adjustable multiplier (0.1 to 5.0)

• Independent background colors with opacity control for each VWAP

• Dashed band lines for easy visual distinction from main VWAP

• Bands extend when visual extension is enabled, maintaining zone visibility

✅ COMPREHENSIVE LABELING SYSTEM

Each VWAP displays:

• Current VWAP value

• Upper deviation band value (High)

• Lower deviation band value (Low)

• Extension status indicator (Calc Extended / Visual Extended)

• Color-coded for quick identification

═══════════════════════════════════════════════════════════════════

📖 HOW TO USE THIS INDICATOR

🎯 SCENARIO 1: EVENT-ANCHORED VWAP (Manual Mode)

Use case: A stock gaps down 15% on earnings and you want to track where institutions are positioning during the recovery.

Setup:

1. Switch to Manual Mode

2. Enable VWAP 1

3. Set Start Time to the earnings gap bar

4. Set End Time to current time (or leave far in future)

5. Enable "Extend Calculation to Current Bar"

6. Watch how price respects the VWAP as a dynamic support/resistance

Interpretation:

• Price above VWAP = buyers in control since the event

• Price testing VWAP from above = potential support

• Volume-weighted standard deviation bands show normal price range

• Price outside bands = potential exhaustion/mean reversion setup

🎯 SCENARIO 2: MULTI-WEEK INSTITUTIONAL ACCUMULATION ZONE (Auto Mode)

Use case: You trade swing setups and want to identify where institutions have been accumulating over the past 3 weeks.

Setup:

1. Switch to Auto Mode

2. Select "Weekly" period type

3. Set Period Span to 3

4. Enable standard deviation bands

Interpretation:

• 3-week composite VWAP shows the true average institutional entry

• Price bouncing off VWAP repeatedly = strong support (institutions defending their average)

• Price breaking below VWAP on high volume = potential distribution

• Deviation bands contracting = consolidation; expanding = volatility increase

🎯 SCENARIO 3: COMPARING MULTIPLE TIME HORIZONS (Manual Mode)

Use case: You want to see short-term vs medium-term vs long-term VWAP alignments.

Setup:

1. Switch to Manual Mode

2. VWAP 1: Last 5 trading days (blue)

3. VWAP 2: Last 10 trading days (orange)

4. VWAP 3: Last 20 trading days (purple)

5. Enable "Extend Calculation" for all

6. Set different background colors for visual separation

Interpretation:

• All VWAPs aligned upward = strong trend across all timeframes

• Price between VWAPs = finding equilibrium between different trader timeframes

• Short-term VWAP crossing long-term VWAP = momentum shift

• Price rejecting at higher-timeframe VWAP = that timeframe's traders defending their average

🎯 SCENARIO 4: HISTORICAL VWAP REFERENCE LEVELS (Manual Mode)

Use case: You want to see where the 1-month VWAP was at each month-end as static reference levels.

Setup:

1. Switch to Manual Mode

2. VWAP 1: Set to last month's start/end dates

3. VWAP 2: Set to 2 months ago start/end dates

4. VWAP 3: Set to 3 months ago start/end dates

5. Disable "Extend Calculation"

6. Enable "Extend Visual Line Only"

Interpretation:

• Each VWAP represents the volume-weighted average for that complete month

• These become static support/resistance levels

• Price returning to old monthly VWAPs = institutional memory/gap fill behavior

• Useful for identifying longer-term value areas

═══════════════════════════════════════════════════════════════════

🎨 CUSTOMIZATION OPTIONS

GENERAL SETTINGS

• Show/hide labels

• Line style: Solid, Dashed, or Dotted

• Standard deviation multiplier (impacts band width)

• Toggle standard deviation bands on/off

MANUAL MODE (Per VWAP)

• Custom start and end times

• Line color picker

• Background color picker (with transparency control)

• Extend calculation option

• Extend visual option

• Show/hide individual VWAPs

AUTO MODE

• Period type selection (Daily/Weekly/Monthly/Quarterly/Yearly)

• Period span (1-20 periods)

• Line color

• Background color (with transparency control)

═══════════════════════════════════════════════════════════════════

💡 TRADING APPLICATIONS

✓ Mean Reversion: Use deviation bands to identify stretched prices likely to return to VWAP

✓ Trend Confirmation: Price sustained above VWAP = bullish bias; below = bearish bias

✓ Support/Resistance: VWAP often acts as dynamic S/R, especially on higher volume periods

✓ Institutional Positioning: Multi-day/week VWAPs show where large players have established positions

✓ Entry Timing: Wait for pullbacks to VWAP in trending markets

✓ Stop Placement: Use VWAP ± standard deviation as volatility-adjusted stop levels

✓ Breakout Confirmation: Breakouts from consolidation with price reclaiming VWAP = stronger signal

✓ Multi-Timeframe Analysis: Compare short vs long-period VWAPs to gauge momentum alignment

═══════════════════════════════════════════════════════════════════

⚠️ IMPORTANT NOTES

• The indicator redraws on each bar to maintain accurate visual representation (uses `barstate.islast`)

• Maximum lookback is limited to 5000 bars for performance optimization

• Time range calculations work across all timeframes but are most effective on intraday to daily charts

• Standard deviation bands assume volume-weighted distribution; extreme events may violate assumptions

• Auto mode always calculates to current bar; use Manual mode for fixed historical periods

═══════════════════════════════════════════════════════════════════

This indicator is open-source. Feel free to examine the code, learn from it, and adapt it to your needs.

Relative Volatility Mass [SciQua]The ⚖️ Relative Volatility Mass (RVM) is a volatility-based tool inspired by the Relative Volatility Index (RVI) .

While the RVI measures the ratio of upward to downward volatility over a period, RVM takes a different approach:

It sums the standard deviation of price changes over a rolling window, separating upward volatility from downward volatility .

The result is a measure of the total “volatility mass” over a user-defined period, rather than an average or normalized ratio.

This makes RVM particularly useful for identifying sustained high-volatility conditions without being diluted by averaging.

────────────────────────────────────────────────────────────

╭────────────╮

How It Works

╰────────────╯

1. Standard Deviation Calculation

• Computes the standard deviation of the chosen `Source` over a `Standard Deviation Length` (`stdDevLen`).

2. Directional Separation

• Volatility on up bars (`chg > 0`) is treated as upward volatility .

• Volatility on down bars (`chg < 0`) is treated as downward volatility .

3. Rolling Sum

• Over a `Sum Length` (`sumLen`), the upward and downward volatilities are summed separately using `math.sum()`.

4. Relative Volatility Mass

• The two sums are added together to get the total volatility mass for the rolling window.

Formula:

RVM = Σ(σ up) + Σ(σ down)

where σ is the standard deviation over `stdDevLen`.

╭────────────╮

Key Features

╰────────────╯

Directional Volatility Tracking – Differentiates between volatility during price advances vs. declines.

Rolling Volatility Mass – Shows the total standard deviation accumulation over a given period.

Optional Smoothing – Multiple MA types, including SMA, EMA, SMMA (RMA), WMA, VWMA.

Bollinger Band Overlay – Available when SMA is selected, with adjustable standard deviation multiplier.

Configurable Source – Apply RVM to `close`, `open`, `hl2`, or any custom source.

╭─────╮

Usage

╰─────╯

Trend Confirmation: High RVM values can confirm strong trending conditions.

Breakout Detection: Spikes in RVM often precede or accompany price breakouts.

Volatility Cycle Analysis: Compare periods of contraction and expansion.

RVM is not bounded like the RVI, so absolute values depend on market volatility and chosen parameters.

Consider normalizing or using smoothing for easier visual comparison.

╭────────────────╮

Example Settings

╰────────────────╯

Short-term volatility detection: `stdDevLen = 5`, `sumLen = 10`

Medium-term trend volatility: `stdDevLen = 14`, `sumLen = 20`

Enable `SMA + Bollinger Bands` to visualize when volatility is unusually high or low relative to recent history.

╭───────────────────╮

Notes & Limitations

╰───────────────────╯

Not a directional signal by itself — use alongside price structure, volume, or other indicators.

Higher `sumLen` will smooth short-term fluctuations but reduce responsiveness.

Because it sums, not averages, values will scale with both volatility and chosen window size.

╭───────╮

Credits

╰───────╯

Based on the Relative Volatility Index concept by Donald Dorsey (1993).

TradingView

SciQua - Joshua Danford

Dynamic Laguerre Filter Bands | OttoThis indicator combines trend-following and volatility analysis by enhancing the traditional Laguerre filter with a dynamic, volatility-adjusted band system. Instead of using fixed thresholds, the bands adapt in real-time to changing market conditions by applying smoothed standard deviation calculations. This design keeps the indicator responsive to significant price movements while effectively filtering out short-term market noise, resulting in more accurate trend identification and breakout signals.

Core Concept

The indicator is built around the following key components:

Laguerre Filter:

The Laguerre filter is designed to smooth out price data by reducing market noise while still being quick enough to detect real changes in price direction. Its goal is to create a clear, smooth trend line that helps traders/investors focus on the overall market trend without getting distracted by small, random price swings.

It uses a parameter called gamma to control how it balances smoothness and responsiveness:

A lower gamma gives more weight to recent price data, making the filter react faster to new price changes. This means the trend line is more sensitive but may also be less smooth and more prone to small fluctuations.

A higher gamma gives more weight to past price data, making the filter smoother and less sensitive to quick changes. This helps reduce noise and produces a steadier trend line, but it also introduces more lag, meaning the filter reacts slower to new price moves.

By adjusting gamma, the Laguerre filter lets you choose the balance between following price changes quickly and having a stable, noise-free trend signal.

Standard Deviation:

shows how much price varies from the mean. In this indicator, it’s used to measure market volatility.

Volatility Bands: The upper and lower bands are based on an EMA-smoothed standard deviation of price. The EMA reduces sudden jumps in volatility, creating smoother and more stable bands that still respond to changing market conditions. These bands are plotted around the Laguerre filter line, expanding and contracting in a controlled way to stay aligned with real market movement while avoiding short-term noise.

Signal Logic:

A long signal is triggered when the close price crosses above the upper band.

A short signal occurs when the close price falls below the lower band.

⚙️ Inputs

Source: Price source used in calculations

Gamma: Adjusts how much the Laguerre filter responds to price changes. Lower gamma values make the filter react more to recent prices, while higher values give more influence to older data, making the line smoother but slower to respond.

Volatility Length: Period used to calculate standard deviation

Volatility Smoothing Length: EMA smoothing length for standard deviation

Multiplier: Scales the width of the bands based on volatility

📈 Visual Output

Laguerre Filter Line: Plots the laguerre filter line, colored dynamically based on signal direction (green for bullish, purple for bearish)

Upper & Lower Bands: Volatility-based bands that adjust with market conditions. (green for bullish, purple for bearish)

Glow Effect: Optional glow layer to enhance visibility of the laguerre filter trend line (green for bullish, purple for bearish)

Bar Coloring: Candlesticks and bar colors reflect the active signal state for fast visual interpretation (green for bullish, purple for bearish)

How to Use

Apply the indicator to your chart and monitor for signal events:

Long Signal: When price closes above the upper band

Short Signal: When price closes below the lower band

🔔 Alerts

This indicator supports optional alert conditions you can enable for:

Long Signal: Close price crossing above the upper band

Short Signal: Close price crossing below the lower band

⚠️ Disclaimer:

This indicator is intended for educational and informational purposes only. Trading/investing involves risk, and past performance does not guarantee future results. Always test and evaluate indicators/strategies before applying them in live markets. Use at your own risk.

Spent Output Profit Ratio (SOPR) Z-Score | [DeV]SOPR Z-Score

The Spent Output Profit Ratio (SOPR) is an advanced on-chain metric designed to provide deep insights into Bitcoin market dynamics by measuring the ratio between the combined USD value of all Bitcoin outputs spent on a given day and their combined USD value at the time of creation (typically, their purchase price). As a member of the Realized Profit/Loss family of metrics, SOPR offers a window into aggregate seller behavior, effectively representing the USD amount received by sellers divided by the USD amount they originally paid. This indicator enhances this metric by normalizing it into a Z-Score, enabling a statistically robust analysis of market sentiment relative to historical trends, augmented by a suite of customizable features for precision and visualization.

SOPR Settings -

Lookback Length (Default: 150 days): Determines the historical window for calculating the Z-Score’s mean and standard deviation. A longer lookback captures broader market cycles, providing a stable baseline for identifying extreme deviations, which is particularly valuable for long-term strategic analysis.

Smoothing Period (Default: 100 days): Applies an EMA to the raw SOPR, balancing responsiveness to recent changes with noise reduction. This extended smoothing period ensures the indicator focuses on sustained shifts in seller behavior, ideal for institutional-grade trend analysis.

Moving Average Settings -

MA Lookback Length (Default: 90 days): Sets the period for the Z-Score’s moving average, offering a shorter-term trend signal relative to the 150-day Z-Score lookback. This contrast enhances the ability to detect momentum shifts within the broader context.

MA Type (Default: EMA): Provides six moving average types, from the simple SMA to the volume-weighted VWMA. The default EMA strikes an optimal balance between smoothness and responsiveness, while alternatives like HMA (Hull) or VWMA (volume-weighted) allow for specialized applications, such as emphasizing recent price action or incorporating volume dynamics.

Display Settings -

Show Moving Average (Default: True): Toggles the visibility of the Z-Score MA plot, enabling users to focus solely on the raw Z-Score when preferred.

Show Background Colors (Default: True): Activates dynamic background shading, enhancing visual interpretation of market regimes.

Background Color Source (Default: SOPR): Allows users to tie the background color to either the SOPR Z-Score’s midline (reflecting adjustedZScore > 0) or the MA’s trend direction (zScoreMA > zScoreMA ). This dual-source option provides flexibility to align the visual context with the primary analytical focus.

Analytical Applications -

Bear Market Resistance: When the Z-Score approaches or exceeds zero (raw SOPR near 1), it often signals resistance as sellers rush to exit at break-even, a pattern historically observed during downtrends. A rising Z-Score MA crossing zero can confirm this pressure.

Bull Market Support: Conversely, a Z-Score dropping below zero in uptrends indicates reluctance to sell at a loss, forming support as sell pressure diminishes. The MA’s bullish coloring reinforces confirmation of renewed buying interest.

Extreme Deviations: Values significantly above or below zero highlight overbought or oversold conditions, respectively, offering opportunities for contrarian positioning when paired with other on-chain or price-based metrics.

Standard Deviation (fadi)The Standard Deviation indicator uses standard deviation to map out price movements. Standard deviation measures how much prices stray from their average—small values mean steady trends, large ones mean wild swings. Drawing from up to 20 years of data, it plots key levels using customizable Fibonacci lines tied to that standard deviation, giving traders a snapshot of typical price behavior.

These levels align with a bell curve: about 68% of price moves stay within 1 standard deviation, 95% within roughly 2, and 99.7% within roughly 3. When prices break past the 1 StDev line, they’re outliers—only 32% of moves go that far. Prices often snap back to these lines or the average, though the reversal might not happen the same day.

How Traders Use It

If prices surge past the 1 StDev line, traders might wait for momentum to fade, then trade the pullback to that line or the average, setting a target and stop.

If prices dip below, they might buy, anticipating a bounce—sometimes a day or two later. It’s a tool to spot overstretched prices likely to revert and/or measure the odds of continuation.

Settings

Higher Timeframe: Sets the Higher Timeframe to calculate the Standard Deviation for

Show Levels for the Last X Days: Displays levels for the specified number of days.

Based on X Period: Number of days to calculate standard deviation (e.g., 20 years ≈ 5,040 days). Larger periods smooth out daily level changes.

Mirror Levels on the Other Side: Plots symmetric positive and negative levels around the average.

Fibonacci Levels Settings: Defines which levels and line styles to show. With mirroring, negative values aren’t needed.

Background Transparency: Turn on Background color derived from the level colors with the specified transparency

Overrides: Lets advanced users input custom standard deviations for specific tickers (e.g., NQ1! at 0.01296).

Daily Standard Deviation (fadi)The Daily Standard Deviation indicator uses standard deviation to map out daily price movements. Standard deviation measures how much prices stray from their average—small values mean steady trends, large ones mean wild swings. Drawing from up to 20 years of data, it plots key levels using customizable Fibonacci lines tied to that standard deviation, giving traders a snapshot of typical price behavior.

These levels align with a bell curve: about 68% of price moves stay within 1 standard deviation, 95% within roughly 2, and 99.7% within roughly 3. When prices break past the 1 StDev line, they’re outliers—only 32% of moves go that far. Prices often snap back to these lines or the average, though the reversal might not happen the same day.

How Traders Use It

If prices surge past the 1 StDev line, traders might wait for momentum to fade, then trade the pullback to that line or the average, setting a target and stop.

If prices dip below, they might buy, anticipating a bounce—sometimes a day or two later. It’s a tool to spot overstretched prices likely to revert and/or measure the odds of continuation.

Settings

Open Hour: Sets the trading day’s start (default: 18:00 EST).

Show Levels for the Last X Days: Displays levels for the specified number of days.

Based on X Period: Number of days to calculate standard deviation (e.g., 20 years ≈ 5,040 days). Larger periods smooth out daily level changes.

Mirror Levels on the Other Side: Plots symmetric positive and negative levels around the average.

Fibonacci Levels Settings: Defines which levels and line styles to show. With mirroring, negative values aren’t needed.

Overrides: Lets advanced users input custom standard deviations for specific tickers (e.g., NQ1! at 0.01296).

Midnight Opening Ranges[TDL]Midnight Opening Range Indicator for TradingView

Description:

The Midnight Opening Range Indicator as taught by Micheal J. Huddleston is a powerful tool designed for traders who want to analyze price action during the critical midnight to 00:30 timeframe. This indicator highlights the opening range for both the current day and previous days, providing valuable insights into market behavior during this specific period. It also calculates and displays deviations from the opening range, as well as allows for custom opening prices to be set, making it highly adaptable to your trading strategy.

Key Features:

Today's Opening Range (00:00 - 00:30):

The indicator plots the high and low of the price range between 00:00 and 00:30 for the current day.

This range is highlighted on the chart, making it easy to identify the initial market movement and potential support/resistance levels.

Previous Days' Opening Ranges:

The indicator also displays the opening ranges for previous days, allowing you to how price reacts off of previous days ranges not just todays.

This feature helps in identifying patterns or recurring behaviors in the market in which price uses this range and previous days ranges throughout the trading day.

Deviations from the Opening Range:

The indicator calculates and plots deviations from the opening range, both above and below the high and low of the range.

These deviations can be used to identify potential breakout or reversal points, giving you an edge in anticipating market moves.

Custom Opening Prices:

The indicator allows you to set custom opening prices, which can be useful if you want to analyze the market based on a specific reference point rather than the default midnight opening.

This feature is particularly useful for traders who follow alternative trading sessions or have specific entry criteria.

Customizable Visuals:

The indicator offers customizable colors and styles for the opening range, deviations, and custom opening prices, allowing you to tailor the visual representation to your preferences.

How to Use:

Identify Key Levels: Use the highlighted opening range to identify key support and resistance levels for the day.

Monitor Deviations: Watch for price movements beyond the opening range deviations to spot potential breakouts or reversals.

Previous Range Data: Use previous days to identify areas of potential AMD.

Set Custom Prices: Adjust the custom opening price to align with your trading strategy or session preferences.

Ideal For:

Day Traders: Perfect for traders who focus on the early hours of the market to capture initial momentum.

Swing Traders: Useful for identifying key levels that could influence price action over several days.

Algorithmic Traders: Can be integrated into automated trading systems to trigger trades based on the opening range and deviations.

Conclusion:

The Midnight Opening Range Indicator is an essential tool for any trader looking to gain an edge in the market by focusing on the critical midnight to 00:30 timeframe. With its ability to highlight opening ranges, calculate deviations, and accommodate custom opening prices, this indicator provides a comprehensive view of market behavior during this pivotal period. Whether you're a day trader, swing trader, or algorithmic trader, this indicator will help you make more informed trading decisions.

Correlation Coefficient Master TableThe Correlation Coefficient Master Table is a comprehensive tool designed to calculate and visualize the correlation coefficient between a selected base asset and multiple other assets over various time periods. It provides traders and analysts with a clear understanding of the relationships between assets, enabling them to analyze trends, diversification opportunities, and market dynamics. You can define key parameters such as the base asset’s data source (e.g., close price), the assets to compare against (up to six symbols), and multiple lookback periods for granular analysis.

The indicator calculates the covariance and normalizes it by the product of the standard deviations. The correlation coefficient ranges from -1 to +1, with +1 indicating a perfect positive relationship, -1 a perfect negative relationship, and 0 no relationship.

You can specify the lookback periods (e.g., 15, 30, 90, or 120 bars) to tailor the calculation to their analysis needs. The results are visualized as both a line plot and a table. The line plot shows the correlation over the primary lookback period (the Chart Length), which can be used to inspect a certain length close up, or could be used in conjunction with the table to provide you with five lookback periods at once for the same base asset. The dynamically created table provides a detailed breakdown of correlation values for up to six target assets across the four user-defined lengths. The table’s cells are formatted with rounded values and color-coded for easy interpretation.

This indicator is ideal for traders, portfolio managers, and market researchers who need an in-depth understanding of asset interdependencies. By providing both the numerical correlation coefficients and their visual representation, users can easily identify patterns, assess diversification strategies, and monitor correlations across multiple timeframes, making it a valuable tool for decision-making.

Enhanced Price Z-Score OscillatorThe Enhanced Price Z-Score Oscillator by tkarolak is a powerful tool that transforms raw price data into an easy-to-understand statistical visualization using Z-Score-derived candlesticks. Simply put, it shows how far prices stray from their average in terms of standard deviations (Z-Scores), helping traders identify when prices are unusually high (overbought) or unusually low (oversold).

The indicator’s default feature displays Z-Score Candlesticks, where each candle reflects the statistical “distance” of the open, high, low, and close prices from their average. This creates a visual map of market extremes and potential reversal points. For added flexibility, you can also switch to Z-Score line plots based on either Close prices or OHLC4 averages.

With clear threshold lines (±2σ and ±3σ) marking moderate and extreme price deviations, and color-coded zones to highlight overbought and oversold areas, the oscillator simplifies complex statistical concepts into actionable trading insights.

Truly Iterative Gaussian ChannelOVERVIEW

The Truly Iterative Gaussian Channel is a robust channeling system that integrates a Gaussian smoothing kernel with a rolling standard deviation to create dynamically adaptive upper and lower boundaries around price. This indicator provides a smooth, yet responsive representation of price movements while minimizing lag and dynamically adjusting channel width to reflect real-time market volatility. Its versatility makes it effective across various timeframes and trading styles, offering significant potential for experimentation and integration into advanced trading systems.

TRADING USES

The Gaussian indicator can be used for multiple trading strategies. Trend following relies on the middle Gaussian line to gauge trend direction: prices above this line indicate bullish momentum, while prices below signal bearish momentum. The upper and lower boundaries act as dynamic support and resistance levels, offering breakout or pullback entry opportunities. Mean reversion focuses on identifying reversal setups when price approaches or breaches the outer boundaries, aiming for a return to the Gaussian centerline. Volatility filtering helps assess market conditions, with narrow channels indicating low volatility or consolidation and suggesting fewer trading opportunities or an impending breakout. Adaptive risk management uses channel width to adjust for market volatility, with wider channels signaling higher risk and tighter channels indicating lower volatility and potentially safer entry points.

THEORY

Gaussian kernel smoothing, derived from the Gaussian normal distribution, is a cornerstone of probability and statistics, valued for its ability to reduce noise while preserving critical signal features. In this indicator, it ensures price movements are smoothed with precision, minimizing distortion while maintaining responsiveness to market dynamics.

The rolling standard deviation complements this by dynamically measuring price dispersion from the mean, enabling the channel to adapt in real time to changing market conditions. This combination leverages the mathematical correctness of both tools to balance smoothness and adaptability.

An iterative framework processes data efficiently, bar by bar, without recalculating historical value to ensure reliability and preventing repainting to create a mathematically grounded channel system suitable for a wide range of market environments.

The Gaussian channel excels at filtering noise while remaining responsive to price action, providing traders with a dependable tool for identifying trends, reversals, and volatility shifts with consistency and precision.

CALIBRATION

Calibration of the Gaussian channel involves adjusting its length to modify sensitivity and adaptability based on trading style. Shorter lengths (e.g., 50-100) are ideal for intraday traders seeking quick responses to price fluctuations. Medium lengths (e.g., 150-200) cater to swing traders aiming to capture broader market trends. Longer lengths (e.g., 250-400+) are better suited for positional traders focusing on long-term price movements and stability.

MARKET USAGE

Stock, Forex, Crypto, Commodities, and Indices.

Dema Percentile Standard DeviationDema Percentile Standard Deviation

The Dema Percentile Standard Deviation indicator is a robust tool designed to identify and follow trends in financial markets.

How it works?

This code is straightforward and simple:

The price is smoothed using a DEMA (Double Exponential Moving Average).

Percentiles are then calculated on that DEMA.

When the closing price is below the lower percentile, it signals a potential short.

When the closing price is above the upper percentile and the Standard Deviation of the lower percentile, it signals a potential long.

Settings

Dema/Percentile/SD/EMA Length's: Defines the period over which calculations are made.

Dema Source: The source of the price data used in calculations.

Percentiles: Selects the type of percentile used in calculations (options include 60/40, 60/45, 55/40, 55/45). In these settings, 60 and 55 determine percentile for long signals, while 45 and 40 determine percentile for short signals.

Features

Fully Customizable

Fully Customizable: Customize colors to display for long/short signals.

Display Options: Choose to show long/short signals as a background color, as a line on price action, or as trend momentum in a separate window.

EMA for Confluence: An EMA can be used for early entries/exits for added signal confirmation, but it may introduce noise—use with caution!

Built-in Alerts.

Indicator on Diffrent Assets

INDEX:BTCUSD 1D Chart (6 high 56 27 60/45 14)

CRYPTO:SOLUSD 1D Chart (24 open 31 20 60/40 14)

CRYPTO:RUNEUSD 1D Chart (10 close 56 14 60/40 14)

Remember no indicator would on all assets with default setting so FAFO with setting to get your desired signal.

STANDARD DEVIATION INDICATOR BY WISE TRADERWISE TRADER STANDARD DEVIATION SETUP: The Ultimate Volatility and Trend Analysis Tool

Unlock the power of STANDARD DEVIATIONS like never before with the this indicator, a versatile and comprehensive tool designed for traders who seek deeper insights into market volatility, trend strength, and price action. This advanced indicator simultaneously plots three sets of customizable Deviations, each with unique settings for moving average types, standard deviations, and periods. Whether you’re a swing trader, day trader, or long-term investor, the STANDARD DEVIATION indicator provides a dynamic way to spot potential reversals, breakouts, and trend-following opportunities.

Key Features:

STANDARD DEVIATIONS Configuration : Monitor three different Bollinger Bands at the same time, allowing for multi-timeframe analysis within a single chart.

Customizable Moving Average Types: Choose from SMA, EMA, SMMA (RMA), WMA, and VWMA to calculate the basis of each band according to your preferred method.

Dynamic Standard Deviations: Set different standard deviation multipliers for each band to fine-tune sensitivity for various market conditions.

Visual Clarity: Color-coded bands with adjustable thicknesses provide a clear view of upper and lower boundaries, along with fill backgrounds to highlight price ranges effectively.

Enhanced Trend Detection: Identify potential trend continuation, consolidation, or reversal zones based on the position and interaction of price with the three bands.

Offset Adjustment: Shift the bands forward or backward to analyze future or past price movements more effectively.

Why Use Triple STANDARD DEVIATIONS ?

STANDARD DEVIATIONS are a popular choice among traders for measuring volatility and anticipating potential price movements. This indicator takes STANDARD DEVIATIONS to the next level by allowing you to customize and analyze three distinct bands simultaneously, providing an unparalleled view of market dynamics. Use it to:

Spot Volatility Expansion and Contraction: Track periods of high and low volatility as prices move toward or away from the bands.

Identify Overbought or Oversold Conditions: Monitor when prices reach extreme levels compared to historical volatility to gauge potential reversal points.

Validate Breakouts: Confirm the strength of a breakout when prices move beyond the outer bands.

Optimize Risk Management: Enhance your strategy's risk-reward ratio by dynamically adjusting stop-loss and take-profit levels based on band positions.

Ideal For:

Forex, Stocks, Cryptocurrencies, and Commodities Traders looking to enhance their technical analysis.

Scalpers and Day Traders who need rapid insights into market conditions.

Swing Traders and Long-Term Investors seeking to confirm entry and exit points.

Trend Followers and Mean Reversion Traders interested in combining both strategies for maximum profitability.

Harness the full potential of STANDARD DEVIATIONS with this multi-dimensional approach. The "STANDARD DEVIATIONS " indicator by WISE TRADER will become an essential part of your trading arsenal, helping you make more informed decisions, reduce risks, and seize profitable opportunities.

Who is WISE TRADER ?

Wise Trader is a highly skilled trader who launched his channel in 2020 during the COVID-19 pandemic, quickly building a loyal following. With thousands of paid subscribed members and over 70,000 YouTube subscribers, Wise Trader has become a trusted authority in the trading world. He is known for his ability to navigate significant events, such as the Indian elections and stock market crashes, providing his audience with valuable insights into market movements and volatility. With a deep understanding of macroeconomics and its correlation to global stock markets, Wise Trader shares informed strategies that help traders make better decisions. His content covers technical analysis, trading setups, economic indicators, and market trends, offering a comprehensive approach to understanding financial markets. The channel serves as a go-to resource for traders who want to enhance their skills and stay informed about key market developments.

Panoramic VWAP### Panoramic VWAP Indicator Overview

The Panoramic VWAP indicator provides a way to display up to four Volume Weighted Average Price (VWAP) lines on a chart, each anchored to different timeframes. This indicator also includes options for displaying standard deviation bands and close lines, offering a comprehensive view of price action across multiple time horizons.

### Key Features

Quad VWAPs : The indicator allows for the display of four VWAP lines simultaneously. Each line can be set to a different timeframe, enabling traders to analyze market conditions across various periods on a single chart.

Standard Deviation Bands : Users can enable bands around each VWAP line, which represent standard deviations or percentage levels from the VWAP. These bands help in assessing volatility and identifying potential overbought or oversold conditions.

Close Lines : The indicator includes an option to show close lines, marking the price's closing level relative to the VWAP. This feature is useful for examining how the market closes in relation to VWAP, which can be important for understanding trend strength or potential reversals.

### How It Looks

VWAP Lines : Multiple VWAP lines are displayed, each reflecting different timeframes. The lines change color depending on whether the price is above or below the VWAP, indicating bullish or bearish momentum.

Bands : Optional bands around the VWAP lines provide a visual indication of volatility, with the potential to identify overbought or oversold areas.

Close Lines : These lines represent the price's closing level relative to the VWAP and can be displayed to add further context to the analysis.

### How to Use It

Trend Analysis :

- Price above a VWAP line indicates bullish momentum .

- Price below a VWAP line suggests bearish momentum .

Support and Resistance :

- VWAP lines often act as dynamic support and resistance. Price approaching a VWAP line from above may find support, while approaching from below may encounter resistance.

Volatility Assessment :

- Bands around the VWAP lines can signal areas of potential reversal. Upper bands may indicate overbought conditions, while lower bands may indicate oversold conditions.

Multiple Timeframe Analysis :

- The ability to display VWAPs from different timeframes simultaneously allows for the identification of confluence zones, where multiple VWAP levels align, indicating potentially significant support or resistance levels.

Customization :

- The indicator settings are customizable, allowing users to choose which VWAP lines, bands, and close lines to display, along with adjustments for visual preferences like line thickness and colors.

### Practical Application

Intraday Trading : Traders can use the VWAPs and bands to identify potential entry and exit points during the trading day based on price interactions with these levels.

Swing Trading : Monitoring VWAP lines across different timeframes can help identify key levels where price might reverse or gain momentum, aiding in decisions about holding or exiting positions.

Long-Term Analysis : VWAP lines on higher timeframes can serve as dynamic support or resistance levels, providing context for long-term trend analysis and investment decisions.

The Panoramic VWAP indicator allows for a detailed analysis of price trends and levels across multiple timeframes, combining VWAPs, standard deviation bands, and close lines in a single, customizable tool.

Stochastic Z-Score Oscillator Strategy [TradeDots]The "Stochastic Z-Score Oscillator Strategy" represents an enhanced approach to the original "Buy Sell Strategy With Z-Score" trading strategy. Our upgraded Stochastic model incorporates an additional Stochastic Oscillator layer on top of the Z-Score statistical metrics, which bolsters the affirmation of potential price reversals.

We also revised our exit strategy to when the Z-Score revert to a level of zero. This amendment gives a much smaller drawdown, resulting in a better win-rate compared to the original version.

HOW DOES IT WORK

The strategy operates by calculating the Z-Score of the closing price for each candlestick. This allows us to evaluate how significantly the current price deviates from its typical volatility level.