Prev-Week-Month with V-StopPrevious Week map: It automatically plots last week’s high/low and key Fibonacci levels (50%, 61.8%, 78.6), plus optional extensions, and can extend those lines into the current week with labels.

Previous Month “Golden Zones”: It shades the prior month’s two main retracement zones (61.8%–78.6% from the month’s range) as bullish/bearish areas, optionally adds boundary lines, and labels them.

Volatility Stop (V-Stop): It draws an ATR-based trailing stop that flips between uptrend/downtrend. You can run it on the chart timeframe or a higher timeframe, and it marks reversals and HTF breach/“limbo” events. **bits of code taken from TradingView script**

Volatilityindicator

Apex Adaptive Trend Navigator [Pineify]Apex Adaptive Trend Navigator

The Apex Adaptive Trend Navigator is a comprehensive trend-following indicator that combines adaptive moving average technology, dynamic volatility bands, and market structure analysis into a single, cohesive trading tool. Designed for traders who want to identify trend direction with precision while filtering out market noise, this indicator adapts its sensitivity based on real-time market efficiency calculations.

Key Features

Adaptive Moving Average with efficiency-based smoothing factor

Dynamic ATR-based volatility bands that expand and contract with market conditions

Market Structure detection including BOS (Break of Structure) and CHoCH (Change of Character)

Real-time performance dashboard displaying trend status and efficiency metrics

Color-coded cloud visualization for intuitive trend identification

How It Works

The core of this indicator is built on an Adaptive Moving Average that uses a unique efficiency-based calculation method inspired by the Kaufman Adaptive Moving Average (KAMA) and TRAMA concepts. The efficiency ratio measures the directional movement of price relative to total price movement over the lookback period:

Efficiency = |Price Change over N periods| / Sum of |Individual Bar Changes|

This ratio ranges from 0 to 1, where values closer to 1 indicate a strong trending market with minimal noise, and values closer to 0 indicate choppy, sideways conditions. The smoothing factor is then squared to penalize noisy markets more aggressively, causing the adaptive line to flatten during consolidation and respond quickly during strong trends.

The Dynamic Volatility Bands are calculated using the Average True Range (ATR) multiplied by a user-defined factor. These bands create a channel around the adaptive moving average, helping traders visualize the current volatility regime and potential support/resistance zones.

Trading Ideas and Insights

When price stays above the adaptive line with the bullish cloud forming, consider this a confirmation of uptrend strength

The efficiency percentage in the dashboard indicates trend quality - higher values suggest more reliable trends

Watch for price interactions with the upper and lower bands as potential reversal or continuation zones

A flat adaptive line indicates consolidation - wait for a clear directional break before entering trades

How Multiple Indicators Work Together

This indicator integrates three complementary analytical approaches:

The Adaptive Moving Average serves as the trend backbone, providing a dynamic centerline that automatically adjusts to market conditions. Unlike fixed-period moving averages, it reduces lag during trends while minimizing whipsaws during ranging markets.

The ATR Volatility Bands work in conjunction with the adaptive MA to create a volatility envelope. When the adaptive line is trending and price remains within the cloud (between the MA and outer band), this confirms trend strength. Price breaking through the opposite band may signal exhaustion or reversal.

The Market Structure Analysis using swing point detection adds a Smart Money Concepts (SMC) layer. BOS signals indicate trend continuation when price breaks previous swing highs in uptrends or swing lows in downtrends. CHoCH signals warn of potential reversals when the structure shifts against the prevailing trend.

Unique Aspects

The squared efficiency factor creates a non-linear response that dramatically reduces noise sensitivity

Cloud fills only appear on the trend side, providing clear visual distinction between bullish and bearish regimes

The integrated dashboard eliminates the need to switch between multiple indicators for trend assessment

Pivot-based swing detection ensures accurate market structure identification

How to Use

Add the indicator to your chart and adjust the Lookback Period based on your trading timeframe (shorter for scalping, longer for swing trading)

Monitor the cloud color - green clouds indicate bullish conditions, red clouds indicate bearish conditions

Use the efficiency reading in the dashboard to gauge trend reliability before entering positions

Consider entries when price pulls back to the adaptive line during strong trends (high efficiency)

Use the volatility bands as dynamic take-profit or stop-loss reference levels

Customization

Lookback Period : Controls the sensitivity of trend detection and swing point identification (default: 20)

Volatility Multiplier : Adjusts the width of the ATR bands (default: 2.0)

Show Market Structure : Toggle visibility of BOS and CHoCH labels

Show Performance Dashboard : Toggle the trend status table

Color Settings : Customize bullish, bearish, and neutral colors to match your chart theme

Conclusion

The Apex Adaptive Trend Navigator offers traders a sophisticated yet intuitive approach to trend analysis. By combining adaptive smoothing technology with volatility measurement and market structure concepts, it provides multiple layers of confirmation for trading decisions. Whether you are a day trader seeking quick trend identification or a swing trader looking for reliable trend-following signals, this indicator adapts to your market conditions and trading style. The efficiency-based calculations ensure you always know not just the trend direction, but also the quality and reliability of that trend.

BE-QuantFlow: Adaptive Momentum Trading█ Overview: QuantFlow: Adaptive Momentum Trading

QuantFlow is a sophisticated algorithmic momentum trading method designed specifically for indices and high-beta stocks. However, its logic is universal; with appropriate parameter tuning, it adapts to various asset classes and timeframes.

While the standard momentum indicators (like RSI or MACD) simply measure how fast price is moving (Velocity), QuantFlow analyzes the quality and conviction of the trend . Features like Dynamic Volatility Filtering and Trend Shielding, combined with volatility weighting and a "Dual-Line" approach to distinguish between a sustainable institutional trend and a temporary retail spike, make the indicator unique and more powerful.

█ Why QuantFlow ?

Quant (The Engine): This replaces subjective guessing with objective math.

Instead of just seeing that the price is "up," we measure "how it got there". For example, a stock that rises 1 currency value every day for 10 days (smooth trend) gets a much higher score than a stock that jumps 10 currency value in one minute and does nothing else (erratic noise). This mathematical rigor provides the structure.

█ Core Logic & Philosophy

To understand how QuantFlow calculates momentum, imagine a "Tug-of-War" between Buyers (Bulls) and Sellers (Bears). Most indicators (like RSI) use a single line. If RSI is at 50, it means "Neutral." But "Neutral" can mean two very different things:

Peace: Nothing is happening. No one is buying or selling.

War: Buyers are pushing hard, but Sellers are pushing back equally hard. Volatility is massive.

A single line hides this reality. QuantFlow splits the market into two separate scores:

Bull Score (Green Line): How hard are the buyers pushing?

Bear Score (Red Line): How hard are the sellers pushing?

The Layman's Advantage:

If both lines are low = Sleepy Market (Avoid).

If Green is high and Red is low = Clean Uptrend (Buy).

If Red is high and Green is low = Clean Downtrend (Sell).

If both lines are high = Chaos/War Zone (Wait).

█ How it Weight "Sustenance" (The Critical Quality Check)

This is the most unique aspect of QuantFlow: Trend direction alone is not enough; Sustenance is weighed equally . Standard indicators treat every 10 currency value movements the same way with no distinction. However, QuantFlow asks, "Did you hold the ground you gained?"

Scenario A (High Sustenance) : A stock opens at 100, marches to 110, and closes at 110.

Verdict : Buyers pushed up and sustained the price.

QuantFlow Weight : 100%. This is a high-quality move.

Scenario B (Low Sustenance) : A stock opens at 100, spikes to 110, but gets sold off to close at 102.

Verdict : Buyers pushed up (Trend is Up), but failed to sustain it (Long Wick).

QuantFlow Weight : 20%. This is treated as "Noise" or a trap.

By mathematically weighing the Close Location Value (where the candle closes relative to its high/low), QuantFlow filters out "Gap-and-Fade" traps and exhaustion spikes that fool traditional indicators.

Comparisons: QuantFlow vs. The Rest

Calculation Logic : Standard RSI/MACD measures simple price change over time. QuantFlow measures Price Change 'times (x)' Conviction (Sustenance Weighting).

Visual Output : Standard tools show a single line (0-100), often hiding market conflict. QuantFlow displays Dual Lines (Bull vs Bear Intensity) to reveal the true state of the battle.

Trap Handling : Standard indicators are often fooled by sharp spikes. QuantFlow ignores "Gap-and-Fade" moves with poor closing conviction.

Adaptability : Standard tools use static levels (e.g., Overbought > 70). QuantFlow uses Dynamic Bands that adjust automatically to recent volatility.

█ Dynamic Volatility Filtering

Unlike standard indicators that use fixed levels (e.g., "Buy if RSI > 50"), QuantFlow acknowledges that "50" means something different in a quiet market versus a crashing market. This section explains the statistical engine driving the signals.

The Problem with Static Levels : In a low-volatility environment, a momentum score of 55 might indicate a massive breakout. In a high-volatility environment, a score of 55 might just be random noise. A fixed threshold cannot handle both scenarios.

The Solution: Adaptive Statistics : The script maintains a memory of the Momentum Events. It doesn't just look at price; it looks at where the momentum occurred in the past and draws a "Noise Zone" (Grey Band). This logic acts as a "Smart Gatekeeper" for trade entries:

Scenario A: Inside the Noise (The Filter)

If a new momentum signal happens inside the Noise Zone, the script assumes it is likely chop or noise.

Action : It forces a wait period. The signal is delayed until the trend sustains itself for Confirm Bars; else the signal is cancelled. This filters out ~70% of false signals in sideways markets.

Scenario B: Outside the Noise (The Breakout)

If a new momentum signal happens outside the Noise Zone (or the momentum score smashes through the Upper Band), it is statistically significant (an outlier event).

Action: It triggers an Immediate Entry. No waiting is required because the move is powerful enough to escape the historical noise zone.

█ The ⚠️ "Warning" System (Heads-up for Smart Reversals)

While you are directional if there is potential reversal signal, it provides the heads-up warning for a better decision-making

█ Special Utility: Ghost Mode

For intraday traders, the biggest disruption to "Flow" is the mandatory broker square-off at 3:15 PM (considering Indian Market). Often, a trend continues overnight, and the trader misses the gap-up opening the next morning because their algo was flat.

Ghost Mode is a unique feature that runs silently in the background:

At Square-off: The strategy closes your official position to satisfy the broker.

In the Background: It keeps the trade "alive" virtually (Ghost).

Next Morning: If the market opens in the trend's favor, the strategy re-enters the trade automatically. This approach ensures you capture the full swing of the trend, even if you are forced to exit at the previous session.

█ Advice on this indicator:

Parameter Calibration: The default settings are optimized for BankNifty on 5-minute charts. If you trade stocks, crypto, commodities, or any higher timeframes (e.g., 15-min or hourly), you must adjust these.

Low Volatility Assets: Reduce Stop Multiplier to 2.0.

High Volatility Assets: Increase Momentum Lookback to 50 to filter noise.

Confluence (Additional Confirmation): While QuantFlow is a complete system, using it alongside Key Support/Resistance Levels or Volume Profile provides the highest probability setups.

Volatility Regimes | GainzAlgo📊 OVERVIEW:

=========

This is a comprehensive ATR-based trading system designed for professional

traders who need advanced volatility analysis, precise trade management, and

intelligent market regime detection. The indicator combines multiple proven

volatility concepts into one powerful, customizable tool.

⭐ WHY THIS SYSTEM IS UNIQUE AND WORTHY OF PUBLICATION:

====================================================

This is not simply a collection of ATR-based indicators placed together.

It represents a unified volatility analysis framework where each component

is specifically designed to work in concert with the others, creating a

complete trading workflow that cannot be replicated by using multiple

separate indicators.

🔗 SYNERGISTIC INTEGRATION - How Components Work Together:

🧠 1. CONTEXT-AWARE ANALYSIS

The Volatility Regime Detection acts as the "brain" of the system,

classifying market conditions into 4 distinct phases. Every other

component then adapts its behavior based on this regime classification:

- ATR Bands expand/contract with regime changes

- Stop Loss distances automatically adjust (tighter in compression,

wider in high volatility)

- Take Profit targets scale proportionally to current regime

- Signal sensitivity filters itself based on market phase

📐 2. UNIFIED VOLATILITY FOUNDATION

All calculations share a single ATR baseline calculation, ensuring

internal consistency across the entire system. When ATR changes, every

element updates in perfect synchronization:

- Bands recalculate from the same ATR value

- Risk management levels use the same volatility measurement

- Regime classification and signals reference identical data

🛡️ 3. INTEGRATED RISK MANAGEMENT

The system doesn't just show WHERE to enter - it calculates HOW MUCH

to risk:

- Dynamic Stop Loss adapts to current ATR automatically

- Position Size Calculator uses the dynamic stop to compute exact quantities

- Take Profit levels scale proportionally, maintaining optimal risk:reward

✅ 4. TWO-STAGE SIGNAL CONFIRMATION

The alert system creates a logical progression:

Step 1: Volatility Breakout → Market energy is building

Step 2: Trend Confirmation → Direction confirmed with volatility support

This prevents false breakouts by requiring both volatility AND direction.

🏦 5. PROFESSIONAL WORKFLOW INTEGRATION

The system mirrors how institutional traders analyze markets:

Phase 1: Assess regime → What's the market doing?

Phase 2: Identify setup → Where's the opportunity?

Phase 3: Calculate risk → What's my exposure?

Phase 4: Set targets → Where do I take profit?

Phase 5: Monitor regime → When do conditions change?

❌ WHY NOT USE SEPARATE INDICATORS?

- Separate ATR Bands: Don't know about regime changes, remain static

- Separate Regime Indicator: Doesn't automatically adjust stop/targets

- Separate Position Calculator: Doesn't know your actual ATR-based stop

- Manual Integration: Requires constant mental calculation and cross-referencing

🧮 DETAILED CALCULATION METHODOLOGY:

=================================

📏 ATR (AVERAGE TRUE RANGE) CALCULATION:

- True Range = Maximum of:

1. Current High - Current Low

2. Absolute value of (Current High - Previous Close)

3. Absolute value of (Current Low - Previous Close)

- ATR = Simple Moving Average of True Range over specified period (default: 14)

📊 DYNAMIC ATR BANDS:

- Upper Band = Current Close + (ATR × Band Multiplier)

- Lower Band = Current Close - (ATR × Band Multiplier)

- Band 1: 1.0× ATR (closest support/resistance)

- Band 2: 2.0× ATR (intermediate zone)

- Band 3: 3.0× ATR (extended zone)

🌡️ VOLATILITY REGIME CLASSIFICATION:

Step 1: Calculate ATR Baseline

- Baseline ATR = SMA or EMA of ATR over long period (default: 50 bars)

- This represents "normal" volatility for the instrument

Step 2: Calculate ATR Ratio

- ATR Ratio = Current ATR ÷ Baseline ATR

- Example: If current ATR = 70 and baseline = 50, ratio = 1.40

Step 3: Classify Regime Based on Ratio

- COMPRESSION: Ratio < 0.70 (ATR is 30% below normal)

Market consolidating, volatility contracting, energy building

- EXPANSION: Ratio between 1.15 and 1.40 (ATR is 15-40% above normal)

Volatility breaking out, early phase of directional movement

- HIGH VOLATILITY: Ratio > 1.40 (ATR is 40%+ above normal)

Strong sustained trend with high participation

- EXHAUSTION: ATR declining after high volatility period

Requires: Previous high ratio + declining ATR over X bars (default: 5)

Trend maturity, potential reversal or consolidation approaching

🛑 DYNAMIC STOP LOSS CALCULATION:

- For Long Positions: Stop Loss = Entry Price - (ATR × SL Multiplier)

- For Short Positions: Stop Loss = Entry Price + (ATR × SL Multiplier)

- Default Multiplier: 2.0× ATR

- Adjusts automatically: Wider in high volatility, tighter in compression

🎯 TAKE PROFIT LEVELS:

- TP1 = Entry Price ± (ATR × TP1 Multiplier)

- TP2 = Entry Price ± (ATR × TP2 Multiplier)

- TP3 = Entry Price ± (ATR × TP3 Multiplier)

- Direction (+ or -) depends on trade direction

📦 POSITION SIZE CALCULATION:

Formula: Position Size = Account Risk Amount ÷ Stop Loss Distance

Step-by-step:

1. Risk Amount = Account Size × (Risk Percentage ÷ 100)

2. Stop Distance = |Entry Price - Stop Loss Price|

3. Position Size = Risk Amount ÷ Stop Distance

📈 ATR PERCENTILE RANKING:

- >80% = Extremely high volatility

- 20-80% = Normal volatility range

- <20% = Extremely low volatility

🌀 VOLATILITY CONTRACTION PATTERN:

Detects extended low-volatility periods indicating imminent breakout.

🧭 TREND DETECTION SIGNALS:

Bullish: Price > MA AND Current ATR > ATR MA

Bearish: Price < MA AND Current ATR > ATR MA

⚡ VOLATILITY BREAKOUT SIGNALS:

Triggered when ATR exceeds its moving average by a defined threshold.

🧩 CORE FEATURES:

==============

1. ATR BANDS (Dynamic Support/Resistance)

2. VOLATILITY REGIME DETECTION

3. DYNAMIC STOP LOSS SYSTEM

4. MULTIPLE TAKE PROFIT LEVELS

5. SUPPORT & RESISTANCE LEVELS

6. RISK MANAGEMENT CALCULATOR

7. ATR PERCENTILE RANKING

8. VOLATILITY CONTRACTION PATTERN

9. TREND DETECTION SIGNALS

10. VOLATILITY BREAKOUT SIGNALS

⚙️ RECOMMENDED SETTINGS BY TRADING STYLE:

======================================

DAY TRADING • SWING TRADING • POSITION TRADING • SCALPING

📘 HOW TO USE THIS INDICATOR:

==========================

STEP 1: Identify Market Regime

STEP 2: Wait for Entry Signal

STEP 3: Set Stop Loss

STEP 4: Set Take Profits

STEP 5: Position Sizing

STEP 6: Monitor & Manage

🔔 ALERT SYSTEM:

=============

Alerts for volatility breakouts, trend changes, regime transitions,

ATR band crossings, contraction completion, and percentile extremes.

🎨 CUSTOMIZATION:

==============

All visuals, thresholds, multipliers, colors, alerts, and risk parameters

can be fully customized.

⚠️ IMPORTANT DISCLAIMER:

=====================

This indicator is a volatility analysis tool and does NOT provide financial advice.

Past performance does not guarantee future results.

All trading involves substantial risk.

All trading decisions are the sole responsibility of the user.

QUANT TRADING ENGINE [PointAlgo]Quant Trading Engine is a quantitative market-analysis indicator that combines multiple statistical factors to study trend behavior, mean reversion, volatility, execution efficiency, and market stability.

The indicator converts raw price behavior into standardized signals to help evaluate directional bias and risk conditions in a systematic way.

This script focuses on factor alignment and regime awareness, not prediction certainty.

Design Philosophy

Markets move through different regimes such as trending, ranging, volatile expansion, and instability.

This indicator attempts to model these regimes by blending:

Momentum strength

Mean-reversion pressure

Volatility risk

Trend filtering

Execution context (VWAP)

Correlation structure

Each component is normalized and combined into a single Quant Alpha framework.

Factor Construction

1. Momentum Factor

Measures directional strength using percentage price change over a rolling window.

Standardized using mean and standard deviation.

Represents trend continuation pressure.

2. Mean Reversion Factor

Measures deviation from a longer moving average.

Standardized to identify stretched conditions.

Designed to capture counter-trend behavior.

Directional Clamping

Mean-reversion signals are dynamically restricted:

No counter-trend buying during downtrends.

No counter-trend selling during uptrends.

Allows both sides only in neutral regimes.

This prevents conflicting signals in strong trends.

3. Volatility Factor

Uses realized volatility derived from price changes.

Penalizes environments where volatility deviates significantly from its norm.

Acts as a risk adjustment rather than a directional driver.

4. Composite Quant Alpha

The final Quant Alpha is a weighted blend of:

Momentum

Mean reversion (trend-clamped)

Volatility risk

The composite is standardized into a Z-score, allowing consistent interpretation across instruments and timeframes.

Signal Logic

Buy signal occurs when Quant Alpha crosses above zero.

Sell signal occurs when Quant Alpha crosses below zero.

Zero-cross logic is used to represent shifts from negative to positive statistical bias and vice versa.

Signals reflect statistical regime change, not trade instructions.

Volatility Smile Context

Measures price deviation from its statistical distribution.

Identifies skewed conditions where upside or downside volatility becomes dominant.

Highlights extreme deviations that may imply elevated derivative risk.

Exotic Risk Conditions

Detects sudden price expansion combined with volatility spikes.

Highlights environments where execution and risk become unstable.

Visual background cues are used for awareness only.

Execution Context (VWAP)

Measures price distance from VWAP.

Used to assess execution efficiency rather than direction.

Helps identify stretched conditions relative to average traded price.

Correlation Structure

Evaluates short-term return correlations.

Detects when price behavior becomes less predictable.

Flags structural instability rather than trend direction.

Visualization

The indicator plots:

Quant Alpha (scaled) with directional coloring

Volatility smile deviation

Price vs VWAP distance

Correlation structure

Signal markers indicate Quant Alpha zero-cross events and risk conditions.

Dashboard

A compact dashboard summarizes:

Trend filter state

Quant Alpha polarity and value

Individual factor readings

Current action state (Buy / Sell / Wait / Risk)

The dashboard provides a real-time snapshot of internal model conditions.

Usage Notes

Designed for analytical interpretation and research.

Best used alongside price action and risk management tools.

Factor behavior depends on instrument liquidity and volatility.

Not optimized for illiquid or irregular markets.

Disclaimer

This script is provided for educational and analytical purposes only.

It does not provide financial, investment, or trading advice.

All outputs should be independently validated before making any trading decisions.

GARCH Volume Volatility [MarkitTick]Title: GARCH Volume Volatility

Description

Overview

The GARCH Volume Volatility (GV) indicator is a sophisticated quantitative tool designed to analyze the rate of change in market participation. While the vast majority of technical indicators focus on Price Volatility (how much price moves), this script focuses on Volume Volatility (how unstable the participation is).

Market volume is rarely distributed evenly; it tends to cluster. Periods of high activity are often followed by more high activity, and periods of calm tend to persist. This behavior is known as "heteroskedasticity." This script utilizes an Exponentially Weighted Moving Average (EWMA) model—a core component of Generalized Autoregressive Conditional Heteroskedasticity (GARCH) frameworks—to model these changing variance regimes.

By isolating volume volatility from raw volume data, this tool helps traders distinguish between sustainable liquidity flows and erratic, unsustainable volume shocks that often precede market reversals or breakouts.

Methodology and Calculations

1. Logarithmic vs. Percentage Returns

The foundation of this indicator is the calculation of "Volume Returns"—the period-over-period change in volume.

- The script defaults to Logarithmic Returns. In financial statistics, log returns are preferred because they normalize data that can vary wildly in magnitude (such as cryptocurrency volume spikes), providing a more symmetric view of changes.

- Users can opt for standard percentage changes if they prefer a linear approach.

2. Variance Proxy (Squared Returns)

To measure volatility, the direction of the volume change (up or down) matters less than the magnitude. The script squares the returns to create a "Variance Proxy." This ensures that a massive drop in volume is treated with the same statistical weight as a massive spike in volume—both represent a significant change in the volatility of participation.

3. GARCH-Style Smoothing (EWMA)

Standard Moving Averages (SMA) treat all data points in the lookback period equally. However, volatility is dynamic. This script uses an EWMA model with a tunable "Lambda" (Decay Factor).

- The Recursive Formula: The current calculation relies on a weighted average of the current variance and the previous period's smoothed variance.

- Memory Effect: This allows the indicator to "remember" recent volatility shocks while gradually letting their influence fade. This mimics the GARCH process of conditional variance.

4. Dynamic Statistical Thresholds

The final output is the Volatility (square root of variance). To make this data actionable, the script calculates a dynamic upper and lower limit based on the standard deviation (Z-Score) of the volatility itself over a user-defined lookback period.

How to Use

The indicator plots a histogram that categorizes the market into four distinct volatility regimes:

1. High Volatility (Red Histogram)

Trigger: Volatility > High Band (Upper Standard Deviation).

Interpretation: This signals an extreme anomaly in volume stability. This is not just "high volume," but "erratic volume behavior." This often occurs at:

- Capitulation bottoms (panic selling).

- Euphoric tops (blow-off tops).

- Major news events or earnings releases.

2. Elevated Volatility (Maroon Histogram)

Trigger: Volatility > Mean Average.

Interpretation: The market is in an active state. Participation is changing rapidly, but within statistically normal bounds. This is common during healthy, trending moves where new participants are entering the market steadily.

3. Normal/Low Volatility (Green Histogram)

Trigger: Volatility is within the lower bands.

Interpretation: The market volume is stable. There are no sudden shocks in participation. This is typical of consolidation phases or "creeping" trends where the price drifts without significant volume conviction.

4. Extremely Low Volatility (Bright Green/Transparent)

Trigger: Volatility < Low Band.

Interpretation: The "calm before the storm." When volume volatility collapses to near-zero, it implies that the market has reached a state of equilibrium or disinterest. Historically, volatility is cyclical; periods of extreme compression often lead to violent expansion.

Settings and Configuration

Core Settings

- Use EWMA: When checked (Default), uses the recursive GARCH-style calculation. If unchecked, it reverts to a simple SMA of variance, which is less sensitive to recent shocks but more stable.

- Log Returns: Uses natural log for calculations. Highly recommended for assets with exponential growth or large volume ranges.

- Length: The baseline period for the calculation.

- Threshold Lookback: The number of bars used to calculate the Mean and Standard Deviation bands.

- EWMA Lambda: The decay factor (0.0 to 1.0). A value of 0.94 is standard for risk metrics.

-- Higher Lambda (e.g., 0.98): The indicator reacts slower and is smoother (long memory).

-- Lower Lambda (e.g., 0.80): The indicator reacts very fast to new data (short memory).

Visuals

- Show Thresholds: Toggles the visibility of the statistical bands on the chart.

- High Band (StdDev): The multiplier for the upper warning zone. Default is 1.5 deviations. Increasing this to 2.0 or 3.0 will filter for only the most extreme events.

Disclaimer This tool is for educational and technical analysis purposes only. Breakouts can fail (fake-outs), and past geometric patterns do not guarantee future price action. Always manage risk and use this tool in conjunction with other forms of analysis.

Low Volatility Profiles [BigBeluga]🔵 OVERVIEW

Low Volatility Profiles is a market compression and breakout-anticipation tool that identifies phases of low volatility using ADX and then builds a real-time volume profile inside the detected range.

This helps traders spot accumulation/distribution zones and prepare for explosive moves when volatility expands.

When volatility is low ➜ price coils ➜ volume organizes ➜ breakouts become highly actionable.

This tool visualizes that process with dynamic range boxes + volume bins + PoC extension.

🔵 CONCEPTS

Low-Volatility Detection — Uses ADX threshold & cross logic to define volatility contraction regimes.

Range Construction — Draws a price box that expands with highs/lows during the compression phase.

Micro Volume Profile — Builds a volume histogram inside the range using bins (micro volume nodes).

Delta Calculation — Tracks positive vs negative volume to gauge buyer/seller pressure within range.

Point of Control (PoC) — Highlights the price level with max traded volume inside the range.

PoC Extension — Optionally extends PoC into future bars to show potential reaction zone after breakout.

Breakout Validation — Ends the profile zone when price breaks above or below the modeled range.

Noise Removal — Automatically removes invalid or small ranges to prevent chart clutter.

This tool turns consolidation into actionable structure by exposing where smart money accumulates before trending moves.

🔵 FEATURES

ADX-Driven Range Detection — Identify when market transitions into low-volatility compression.

Configurable ADX Threshold — Set sensitivity for contraction zones.

Cross-Type Option — Detect low volatility via cross under / crossover logic.

Dynamic Range Box — Expands live with price as contraction unfolds.

Micro Volume Profile (Bins) — Distributes volume across bins inside range for micro POC mapping.

Volume Delta Visualization — Shows imbalance inside consolidation (accumulation vs distribution).

Real-Time PoC Highlight — Instantly shows most traded price inside the compression.

PoC Extension Mode — Extend PoC forward to project reaction levels post-breakout.

Clean Auto-Reset Logic — Removes boxes if range invalid or breakout occurs too fast.

Optional Filled Boxes — Heatmap-style profile visualization inside range body.

ADX Line + Threshold Plot — Visual assistance for volatility state monitoring.

🔵 HOW TO USE

Identify Accumulation Zones — When price enters low-volatility ADX condition and profile builds.

Watch the PoC — PoC acts as battle zone; move above/below can signal initiator strength.

Breakout Strategy — Trade break above/below the range after compression.

Mean Reversion Inside Range — Fade edges while price remains inside compression box.

Combine With Trend Tools — Use trend confirmation (MA/EMA/Flow indicators) after breakout.

Use Delta Clues — Positive delta tilt suggests accumulation; negative suggests distribution.

Monitor Range Size — Longer build + high PoC volume = stronger potential breakout energy.

🔵 CONCLUSION

Low Volatility Profiles isolates accumulation phases and maps volume concentration before volatility expansion.

By combining ADX compression, micro volume distribution, and PoC tracing, traders gain an edge in anticipating powerful breakout cycles and institutional positioning.

Trade the quiet moment before the storm — where smart money prepares the move, and the real opportunity emerges.

Hyper Squeeze Sniper (Dual Side: Long + Short)Hyper Squeeze Sniper (Dual Side Strategy)

This script is a comprehensive Volatility Breakout System designed to identify and trade explosive price moves following periods of consolidation. It combines the classical "Squeeze" theory with Linear Regression Momentum, Volume Analysis, and an ATR-based Trailing Stop to filter false signals and manage risk effectively.

The script operates on a logic of "Compression -> Explosion -> Trend Following" suitable for both Long and Short positions.

🛠 Detailed Methodology (How it works)

1. The Squeeze Detection (Consolidation) The core concept relies on the relationship between Bollinger Bands (BB) and Keltner Channels (KC).

Condition: When the Bollinger Bands (Standard Deviation) contract and fall inside the Keltner Channels (ATR based), it indicates a period of extremely low volatility (The Squeeze).

Visual: The background turns Gray to indicate "Do Not Trade / Wait Mode".

2. Momentum Confirmation (Linear Regression) Instead of using standard lagging indicators, this script utilizes Linear Regression of the price deviation to determine the direction of the breakout.

If the Linear Regression Slope > 0, the bias is Bullish.

If the Linear Regression Slope < 0, the bias is Bearish.

3. Volume Validation To avoid fake breakouts, a Volume Spike filter is applied. A signal is only valid if the current volume exceeds its moving average by a defined multiplier (Default x1.2).

4. Risk Management: ATR Trailing Stop Once a trade is entered, the script calculates a dynamic Trailing Stop based on the Average True Range (ATR).

- Long: The stop line trails below the price and never moves down.

- Short: The stop line trails above the price and never moves up.

- Exit: The position is closed immediately when the price breaches this volatility-based safety line.

How to Use

1. Wait: Look for the Gray Background. This is the accumulation phase.

2. Entry:

LONG: Wait for a Green Triangle ▲ (Price breaks Upper BB + Vol Spike + Bullish Momentum).

SHORT: Wait for a Red Triangle ▼ (Price breaks Lower BB + Vol Spike + Bearish Momentum).

3. Exit: Close the position when the "X" mark appears or when candles cross the trailing safety line.

Settings

- BB Length/Mult: Adjust the sensitivity of the squeeze detection.

- Vol Spike Factor: Increase this to filter out low-volume breakouts.

- ATR Period/Mult: Adjust the trailing stop distance (Higher = Wider stop for swing trading).

TICK & ADD Market Internals SuiteOverview: This is the ultimate Market Internals tool designed for professional SPX/ES and NQ intraday traders.

Traders often monitor both TICK (for short-term timing) and ADD (for daily trend context). However, displaying them on the same chart is usually problematic due to their different scales (TICK ±1000 vs. ADD ±2000), causing chart compression.

Market Internals Suite solves this with a smart "Visual Scaling" algorithm, perfectly fusing TICK Candles and the ADD Line into a single, coherent pane.

Key Features

1.Hybrid Visualization:

· TICK (Foreground): Displayed as OHLC Candles to capture instant liquidity sweeps and wicks.

· ADD (Background): Displayed as a clean Line to show the underlying market breadth trend without clutter.

2.Smart Visual Scaling:

· To prevent chart distortion, the ADD line is visually scaled down (Default Ratio: 1.5).

· This aligns the ADD trend volatility with the TICK range, allowing you to instantly spot divergences or resonance between sentiment and trend.

3.Real-Time Data Dashboard:

· Never lose track of the actual numbers. A dashboard in the top-right corner displays the TRUE values for both TICK and ADD (unscaled).

· Customizable Text Size: You can adjust the dashboard font size (Small/Normal/Large/Huge) in the settings to fit your screen.

4.TICK Extreme Alerts:

· Visual Highlight: The chart background highlights (Green/Red) only when TICK hits the extreme ±1000 levels.

· The ADD line remains clean and alert-free to serve as a stable reference.

Strategy: Context + Timing:

1.Trend Resonance

When the ADD line trends upward and TICK candles consistently maintain levels above zero, it indicates a healthy, strong trend. This is a signal to look for trend-following long setups.

2.Divergence Analysis (The "Holy Grail" Signal)

This combination view makes spotting internal divergences incredibly easy:

· Bearish Divergence: When Price makes a New High, but the ADD line or TICK peaks make a Lower High. This suggests buying exhaustion beneath the surface and often precedes a reversal down.

· Bullish Divergence: When Price makes a New Low, but the ADD line or TICK lows make a Higher Low. This suggests that selling pressure is being absorbed, signaling a potential bounce or reversal up.

ATR Volatility AlertsOverview:

This is a dynamic alert tool based on the Average True Range (ATR), designed to help traders detect sudden price movements that exceed normal volatility levels. Whether you are trading breakouts or monitoring for abnormal spikes, this indicator visualizes these events on the chart and triggers system alerts when the price move exceeds your specified ATR multiplier.

Key Features:

Fully Customizable ATR Range:

You can adjust the ATR Length (Default: 14) and the Multiplier (Default: 1.5x).

Tip: Increase the multiplier (e.g., to 2.0 or 3.0) to catch only extreme volatility, or lower it for scalping smaller moves.

Visual Chart Signals:

Visual markers appear instantly when a bar's movement exceeds the ATR threshold.

Green Triangle: Indicates an Upward Spike.

Red Triangle: Indicates a Downward Spike.

Flexible System Alerts:

Designed to integrate seamlessly with TradingView's alert system. You can choose from three specific alert directions based on your strategy:

1.Price Spike Up: Triggers only on sharp upward moves.

2.Price Spike Down: Triggers only on sharp downward moves.

3.Bidirectional Volatility Alert: Triggers on BOTH huge pumps and dumps.

How to Set Alerts:

Click the "Create Alert" button in TradingView.

Select ATR Volatility Alerts in the "Condition" dropdown.

Choose the specific logic you need:

· Select Price Spike Up for bullish monitoring.

· Select Price Spike Down for bearish monitoring.

· Select Bidirectional Volatility Alert to watch for any volatility expansion.

TICK Indicator with Extreme AlertsOverview:

This indicator is designed to provide intraday traders (especially those trading SPX, ES, and NQ) with a clearer NYSE TICK analysis tool featuring visual alerts. Unlike traditional TICK line charts, this indicator utilizes OHLC Candlesticks to display data, allowing you to fully view the Open, High, Low, and Close within a specific timeframe, thereby capturing instantaneous liquidity sweeps.

Core Features & Logic:

Candlestick Visualization (OHLC Candles): Uses the USI:TICK.US data source by default. The candlestick patterns allow you to clearly see if the TICK pierced key levels intraday but retraced by the close—vital information that standard line charts often miss.

Dual Key Level System: The indicator is designed with two independent reference tiers for trend observation and reversal detection:

Reference Lines (+/- 800): Marked by gray dashed lines. These represent the standard bull/bear dividing zones. When TICK sustains above +800 or below -800, it typically indicates a strong trending market.

Extreme Alerts (+/- 1000): These thresholds are used to identify extreme market sentiment (overbought/oversold conditions).

Background Highlight Alerts (Visual Alerts): To reduce screen-watching fatigue, the indicator automatically highlights the candlestick background when extreme market sentiment occurs:

Green Background: Triggered when TICK High breaks above +1000. Represents extreme buying sentiment, potentially indicating exhaustion or a short squeeze.

Red Background: Triggered when TICK Low drops below -1000. Represents extreme panic selling (Washout), often serving as a potential signal for an intraday reversal or a short-term bottom.

Custom Settings:

All thresholds (800 reference lines, 1000 alert lines) are fully adjustable in the settings.

All colors (Candles, Reference Lines, Background Alert Colors) can be customized.

Use Cases: This tool is ideal for intraday counter-trend or trend-following trading when combined with Price Action analysis and key Support & Resistance levels.

Quantura - Trendchange ZonesIntroduction

“Quantura – Trendchange Zones” is an advanced technical indicator that identifies and visualizes potential market reversal zones using dynamic RSI-based logic. It highlights areas of overbought and oversold conditions, marking them as visual zones directly on the price chart, and generates corresponding bullish and bearish signals when the RSI exits these extremes. The tool helps traders anticipate possible trend change regions and confirm momentum shifts in a clean, intuitive way.

Originality & Value

Unlike traditional RSI indicators that only show a static oscillator, this tool transforms RSI behavior into on-chart visual zones that represent structural overbought and oversold phases. It converts RSI threshold breaches into price-based regions (boxes) and marks reversal signals at the moment of momentum change.

The indicator’s originality and usefulness come from its:

Direct visualization of RSI overbought and oversold areas as dynamic chart zones.

Automatic detection of potential reversal regions where momentum exhaustion is likely.

Integration of RSI-based signals and visual cues without requiring users to monitor the RSI window.

Adjustable sensitivity for RSI length and upper/lower levels.

Clear color-coded separation of bullish and bearish phases.

Functionality & Core Logic

The indicator continuously monitors RSI values relative to the user-defined thresholds.

When RSI moves above the upper level, an Overbought Zone is created and extends until RSI falls back below that threshold.

When RSI moves below the lower level, an Oversold Zone is generated and extends until RSI returns above that level.

When RSI exits one of these zones, a corresponding Trendchange Signal (▲ bullish or ▼ bearish) appears at the transition point.

Each zone dynamically adjusts its high and low levels during formation, representing the complete range of the exhaustion phase.

Parameters & Customization

RSI Length: Defines the sensitivity of RSI calculation. Shorter lengths make signals more responsive; longer lengths filter noise.

Upper Level / Lower Level: Set thresholds for overbought and oversold conditions (default 70 / 30).

Signals: Toggle on/off for displaying bullish (▲) and bearish (▼) reversal signals.

Zones: Toggle the visualization of shaded RSI-based zones.

Colors: Fully customizable bullish and bearish colors for both signals and zones.

Visualization & Display

Bullish reversal zones (oversold exits) are shaded using the chosen bullish color (default: blue).

Bearish reversal zones (overbought exits) are shaded using the chosen bearish color (default: red).

Each completed zone is outlined and filled with transparent shading for better clarity.

Reversal arrows (▲ for bullish, ▼ for bearish) are displayed at the bar where RSI exits the extreme level.

Clean overlay design ensures compatibility with any chart style or color scheme.

Use Cases

Identify overbought and oversold periods directly on the price chart without switching to the RSI window.

Anticipate potential market reversals or exhaustion points based on RSI momentum shifts.

Combine with trend indicators, moving averages, or volume tools for confirmation.

Apply across multiple timeframes to align short-term reversal signals with higher timeframe momentum.

Use zone width and duration to assess the strength and persistence of overbought/oversold conditions.

Limitations & Recommendations

The indicator is not a standalone trading system but a visual confirmation tool.

False signals may occur in strongly trending markets where RSI remains overextended.

Optimal RSI settings may differ between assets (e.g., crypto vs. equities).

Combining this indicator with additional trend or structure filters can enhance accuracy.

Markets & Timeframes

The “Quantura – Trendchange Zones” indicator works across all markets and timeframes, including cryptocurrencies, Forex, stocks, and commodities. It is suitable for both short-term scalping and long-term swing analysis.

Author & Access

Developed 100% by Quantura. Published as a Open-source script indicator. Access is free.

Important

This description complies with TradingView’s Script Publishing and House Rules. It provides a clear explanation of the indicator’s originality, logic, and function while avoiding unrealistic performance or predictive claims.

Volatility Resonance CandlesVolatility Resonance Candles visualize the dynamic interaction between price acceleration, volatility, and volume energy.

They’re designed to reveal moments when volatility expansion and directional momentum resonate — often preceding strong directional moves or reversals.

🔬 Concept

Traditional candles display direction and range, but they miss the energetic structure of volatility itself.

This indicator introduces a resonance model, where ATR ratio, price acceleration, and volume intensity combine to form a composite signal.

* ATR Resonance: compares short-term vs. long-term volatility

* Acceleration: captures the rate of price change

* Volume Energy: reinforces the move’s significance

When these components align, the candle color “resonates” — brighter, more intense candles signal stronger volatility–momentum coupling.

⚙️ Features

* Adaptive Scaling

Normalizes energy intensity dynamically across a user-defined lookback period, ensuring consistency in changing market conditions.

* Power-Law Transformation

Optional non-linear scaling (gamma) emphasizes higher-energy events while keeping low-intensity noise visually subdued.

* Divergence Mode

When enabled, colors can invert to highlight energy divergence from candle direction (e.g., bearish pressure during bullish closes).

* Customizable Styling

Full control over bullish/bearish base colors, transparency scaling, and threshold sensitivity.

🧠 Interpretation

* Bright / High-Intensity Candles → Strong alignment of volatility and directional energy.

Often signals the resonant phase of a move — acceleration backed by volatility expansion and volume participation.

* Dim / Low-Intensity Candles → Energy dispersion or consolidation.

These typically mark quiet zones, pauses, or inefficient volatility.

* Opposite-Colored Candles (if divergence mode on) → Potential inflection zones or hidden stress in the trend structure.

⚠️ Disclaimer

This script is for educational purposes only.

It does not constitute financial advice, and past performance is not indicative of future results. Always do your own research and test strategies before making trading decisions.

Integrated Volatility Intelligence System (IVIS)"Integrated Volatility Intelligence System (IVIS)", shorttitle="VolMind™: Adaptive Volatility Intelligence for Modern Markets"

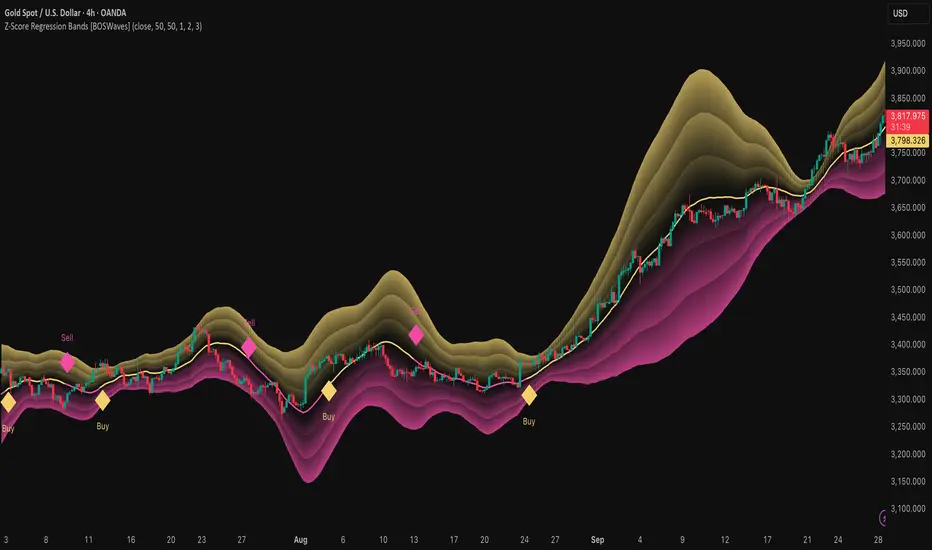

Z-Score Regression Bands [BOSWaves]Z-Score Regression Bands – Adaptive Trend and Volatility Insight

Overview

The Z-Score Regression Bands is a trend and volatility analysis framework designed to give traders a clear, structured view of price behavior. It combines Least Squares Moving Average (LSMA) regression, a statistical method to detect underlying trends, with Z-Score standardization, which measures how far price deviates from its recent average.

Traditional moving average bands, like Bollinger Bands, often lag behind trends or generate false signals in noisy markets. Z-Score Regression Bands addresses these limitations by:

Tracking trends accurately using LSMA regression

Normalizing deviations with Z-Scores to identify statistically significant price extremes

Visualizing multiple bands for normal, strong, and extreme moves

Highlighting trend shifts using diamond markers based on Z-Score crossings

This multi-layered approach allows traders to understand trend strength, detect overextensions, and identify periods of low or high volatility — all from a single, clear chart overlay. It is designed for traders of all levels and can be applied across scalping, day trading, swing trading, and longer-term strategies.

Theoretical Foundation

The Z-Score Regression Bands are grounded in statistical and trend analysis principles. Here’s the idea in plain terms:

Least Squares Moving Average (LSMA) – Unlike standard moving averages, LSMA fits a straight line to recent price data using regression. This “best-fit” line shows the underlying trend more precisely and reduces lag, helping traders see trend changes earlier.

Z-Score Standardization – A Z-Score expresses how far the LSMA is from its recent mean in standard deviation units. This shows whether price is unusually high or low, which can indicate potential reversals, pullbacks, or acceleration of a trend.

Multi-Band Structure – The three bands represent: Band #1: Normal range of price fluctuations; Band #2: Significant deviation from the trend; Band #3: Extreme price levels that are statistically rare. The distance between bands dynamically adapts to market volatility, allowing traders to visualize expansions (higher volatility) and contractions (lower volatility).

Trend Signals – When Z-Score crosses zero, diamonds appear on the chart. These markers signal potential trend initiation, continuation, or reversal, offering a simple alert for shifts in market momentum.

How It Works

The indicator calculates and plots several layers of information:

LSMA Regression (Trend Detection)

Computes a line that best fits recent price points.

The LSMA line smooths out minor fluctuations while reflecting the general direction of the market.

Z-Score Calculation (Deviation Measurement)

Standardizes the LSMA relative to its recent average.

Positive Z-Score → LSMA above average, negative → LSMA below average.

Helps identify overbought or oversold conditions relative to the trend.

Multi-Band Construction (Volatility Envelope)

Upper and lower bands are placed at configurable multiples of standard deviation.

Band #1 captures typical price movement, Band #2 signals stronger deviation, Band #3 highlights extreme moves.

Bands expand and contract with volatility, giving an intuitive visual guide to market conditions.

Trend Signals (Diamonds)

Appear when Z-Score crosses zero.

Indicates moments when momentum may shift, helping traders time entries or exits.

Visual Interpretation

Band width = volatility: wide bands indicate strong movement; narrow bands indicate calm periods.

LSMA shows underlying trend direction, while bands show how far price has strayed from that trend.

Interpretation

The Z-Score Regression Bands provide a multi-dimensional view of market behavior:

Trend Analysis – LSMA line slope shows general market direction.

Momentum & Volatility – Z-Score indicates whether the trend is accelerating or losing strength; band width indicates volatility levels.

Price Extremes – Price touching Band #2 or #3 may suggest overextension and potential reversals.

Trend Shifts – Diamonds signal statistically significant changes in momentum.

Cycle Awareness – Standard deviation bands help distinguish normal market fluctuations from extreme events.

By combining these insights, traders can avoid false signals and react to meaningful structural shifts in the market.

Strategy Integration

Trend Following

Enter trades when diamonds indicate momentum aligns with LSMA direction.

Use Band #1 and #2 for stop placement and partial exits.

Breakout Trading

Watch for narrow bands (low volatility) followed by price pushing outside Band #1 or #2.

Confirm with Z-Score movement in the breakout direction.

Mean Reversion/Pullback

If price reaches Band #2 or #3 without continuation, expect a pullback toward LSMA.

Exhaustion & Reversals

Flattening Z-Score near zero while price remains at extreme bands signals trend weakening.

Tighten stops or scale out before a potential reversal.

Multi-Timeframe Confirmation

High timeframe LSMA confirms the main trend.

Lower timeframe bands provide refined entry and exit points.

Technical Implementation

LSMA Regression : Best-fit line minimizes lag and captures trend slope.

Z-Score Standardization : Normalizes deviation to allow consistent interpretation across markets.

Multi-Band Envelope : Three layers for normal, strong, and extreme deviations.

Trend Signals : Automatic diamonds for Z-Score zero-crossings.

Band Fill Options : Optional shading to visualize volatility expansions and contractions.

Optimal Application

Asset Classes:

Forex : Capture breakouts, overextensions, and trend shifts.

Crypto : High-volatility adaptation with adjustable band multipliers.

Stocks/ETFs : Identify trending sectors, reversals, and pullbacks.

Indices/Futures : Track cycles and structural trends.

Timeframes:

Scalping (1–5 min) : Focus on Band #1 and trend signals for fast entries.

Intraday (15m–1h) : Use Bands #1–2 for continuation and breakout trades.

Swing (4h–Daily) : Bands #2–3 capture trend momentum and exhaustion.

Position (Daily–Weekly) : LSMA trend dominates; Bands #3 highlight regime extremes.

Performance Characteristics

Strong Performance:

Trending markets with moderate-to-high volatility

Assets with steady liquidity and identifiable cycles

Weak Performance:

Flat or highly choppy markets

Very short timeframes (<1 min) dominated by noise

Integration Tips

Combine with support/resistance, volume, or order flow analysis for confirmation.

Use bands for stops, targets, or scaling positions.

Apply multi-timeframe analysis: higher timeframe LSMA confirms main trend, lower timeframe bands refine entries.

Disclaimer

The Z-Score Regression Bands is a trading analysis tool, not a guaranteed profit system. Its effectiveness depends on market conditions, parameter selection, and disciplined risk management. Use it as part of a broader trading strategy, not in isolation.

BBKC Combined Channels OverlayBBKC Combined Channels Overlay (Volatility & Mean Reversion)This indicator provides a clean, single-view envelope combining the Bollinger Bands (BB) and Keltner Channels (KC) directly onto your price chart. It is an essential tool for traders operating with Volatility Compression (The Squeeze) and Mean Reversion strategies in fast-moving markets like Futures, High BTC Beta Equities, and Crypto. The goal of this tool is twofold: to visually frame the market's current volatility state and to identify high-probability entry points based on expansion or extreme contraction. How to Use the BBKC Overlay: Spotting the Squeeze (Accumulation Phase):The Squeeze is identified when the Bollinger Bands (BB) contract and fit inside the Keltner Channels (KC).The area is clearly marked with a subtle Orange Background Highlight on the main chart. This is the Accumulation phase, signaling low volatility before a potential large directional move. Trading Mean Reversion: When price pushes aggressively outside the outermost bands (the BB Upper/Lower), it signals an extreme volatility expansion and over-extension. This is a strong setup for mean reversion—a high-probability trade targeting a snap-back towards the central Basis Line (SMA).Customizing for Extreme Compression: For traders looking only for the tightest, highest-probability Squeezes, adjust the following setting: KC Multiplier (ATR): Lower this value from the default of 1.5 down to 1.25 or 1.0. This narrows the KC, forcing the Bollinger Bands to contract even further to trigger the Squeeze signal, thus filtering for only the most minimal volatility. Recommended Synergy: For a complete volatility system, pair this BBKC Combined Channels Overlay (your visualization tool) with the BBKC Squeeze Indicator (the sub-pane momentum histogram).Overlay (Main Chart): Shows where the Squeeze is occurring and identifies mean reversion targets. Squeeze Indicator (Lower Pane): Shows if the Squeeze is active and the directional momentum building up, helping you time the breakout entry for the Manipulation/Distribution phase.

Omega ATR Indicator📖 Introduction

The Ω ATR Indicator was created to provide a more complete and professional framework for volatility analysis than the classic Average True Range (ATR).

While the traditional ATR is a useful tool, it has limitations: it delivers a simple rolling average of volatility, but it does not adapt to market regimes, it does not highlight extreme events, and it often leaves the trader with incomplete information about risk.

The Ω ATR takes the same foundation and elevates it into a multi-dimensional volatility dashboard, adding statistical layers, adaptive calculations, and clear visual references that allow traders to interpret volatility in a way that is immediately actionable.

🔎 What makes it different from a standard ATR?

This indicator introduces several features beyond the classic formula:

True Range Core – plots the raw True Range (TR) for each bar, providing a direct, bar-by-bar view of volatility impulses.

Standard & Adjusted ATR – includes both the conventional ATR (smoothed average) and an Adjusted ATR that automatically corrects for extreme conditions by incorporating percentile rescaling.

Percentile Volatility Levels – dynamically calculated extreme thresholds (99.8%, 75%, 50%, 25%), plotted as dotted levels across the chart. These act as reference lines for “normal” vs. “abnormal” volatility, useful for spotting unusual price expansions or contractions.

Linear Regression Volatility Trend – overlays a regression line of volatility, showing whether the market is moving toward expansion (rising vol), contraction (falling vol), or stability.

Monetary Value Translation – the indicator converts volatility into points, ticks, and dollar values (based on the instrument’s point value). This allows futures traders and high-value instruments users to immediately see how much volatility is “worth” in cash terms.

Interactive Table Display – a real-time statistics table is displayed directly on the chart, showing:

SMA of ATR in $ and points

Percentile-based volatility range (VAR) in $ and points

Tick equivalences, for quick position sizing

⚡ How traders can use it

The Ω ATR Indicator is designed to be versatile, fitting both discretionary traders and systematic strategy developers.

Risk Management: ATR-based stop losses and position sizing are significantly improved by using the adjusted ATR and percentile thresholds. Traders can size their positions according to volatility regimes, not just raw averages.

Breakout & Exhaustion Detection: When TR or ATR values spike above the 99.8% or 95% percentile levels, this often corresponds to breakout conditions or volatility exhaustion — useful for breakout strategies, mean-reversion setups, and volatility fades.

Market Regime Identification: The regression line helps distinguish if volatility is rising (trending environment, larger swings expected) or compressing (range-bound environment, lower risk opportunities).

Multi-Asset Flexibility: Works equally well on equities, futures, crypto, and FX. Its point/tick/dollar conversion makes it especially powerful for futures traders who need to quantify risk precisely.

Scalping to Swing Trading: On lower timeframes, it acts as a micro-volatility detector; on higher timeframes, it functions as a strategic risk gauge for position management.

⚙️ Settings and Customization

Length: The ATR lookback period (default = 34).

Shorter lengths (14–21) for intraday traders who want fast response.

Longer lengths (34–55) for swing/position traders who want smoother readings.

AVG / ADJ AVG: Toggle to display the standard ATR or the adjusted ATR.

Volatility Levels: Enable/disable up to 4 percentile-based levels (1st = 25%, 2nd = 50%, 3rd = 75%, 4th = 99.8%). Recommended: keep 3 levels active for clarity.

Color Controls: All plots and levels are fully customizable to match your chart style.

Table Display: Positioned on the chart (default: middle-right) with key values updated in real time.

🧭 Best Practices for Use

Combine with Trend Tools: Volatility readings are most powerful when combined with trend filters or volume analysis. For example, a breakout with both high volatility and trend confirmation is stronger than either alone.

ATR Stops: Use the Adjusted ATR rather than the standard one when trailing stops in highly volatile instruments like crypto or Nasdaq futures, as it adapts to outlier spikes.

Dollar Risk Translation: Use the dollar-value outputs to predefine maximum acceptable risk per trade (e.g., “I only risk $250 per position”). This bridges volatility to portfolio risk management.

Event Monitoring: Around economic events or earnings, expect volatility spikes above higher percentile levels. The indicator makes these moves instantly visible.

📌 Summary

The Ω ATR Indicator is not just “another ATR.” It is a comprehensive volatility framework that transforms volatility from a simple statistic into an actionable trading signal.

By combining:

the classic ATR,

an adjusted ATR,

percentile extremes,

regression-based volatility trends,

and real-time dollar conversions,

…this tool allows traders to precisely understand, visualize, and act on volatility in ways that a standard ATR simply cannot provide.

Whether you are scalping intraday moves, swing trading equities, or managing futures positions, the Ω ATR equips you with a professional-grade volatility dashboard that clarifies risk, highlights opportunity, and adapts across all markets and timeframes.

👉 Designed and developed by OmegaTools for traders who demand precision, clarity, and adaptability in their volatility analysis.

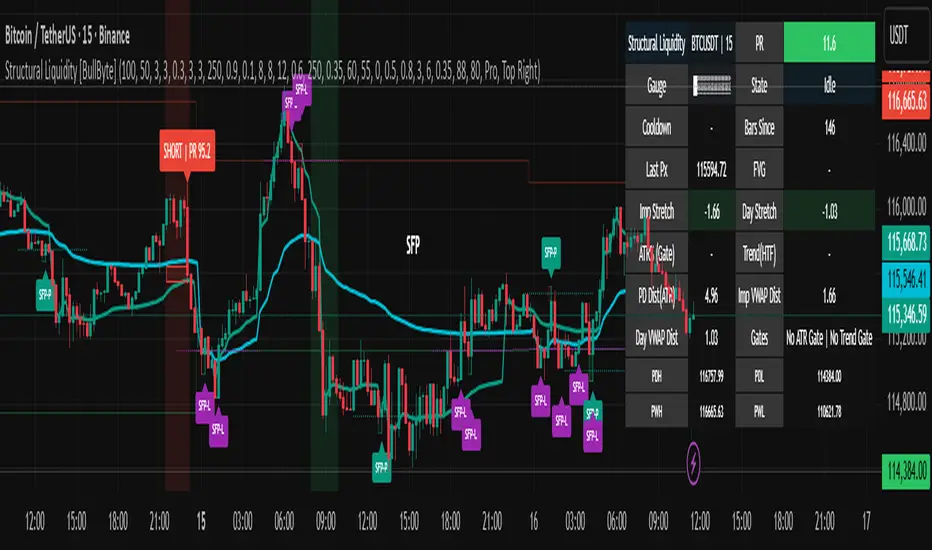

Structural Liquidity Signals [BullByte]Structural Liquidity Signals (SFP, FVG, BOS, AVWAP)

Short description

Detects liquidity sweeps (SFPs) at pivots and PD/W levels, highlights the latest FVG, tracks AVWAP stretch, arms percentile extremes, and triggers after confirmed micro BOS.

Full description

What this tool does

Structural Liquidity Signals shows where price likely tapped liquidity (stop clusters), then waits for structure to actually change before it prints a trigger. It spots:

Liquidity sweeps (SFPs) at recent pivots and at prior day/week highs/lows.

The latest Fair Value Gap (FVG) that often “pulls” price or serves as a reaction zone.

How far price is stretched from two VWAP anchors (one from the latest impulse, one from today’s session), scaled by ATR so it adapts to volatility.

A “percentile” extreme of an internal score. At extremes the script “arms” a setup; it only triggers after a small break of structure (BOS) on a closed bar.

Originality and design rationale, why it’s not “just a mashup”

This is not a mashup for its own sake. It’s a purpose-built flow that links where liquidity is likely to rest with how structure actually changes:

- Liquidity location: We focus on areas where stops commonly cluster—recent pivots and prior day/week highs/lows—then detect sweeps (SFPs) when price wicks beyond and closes back inside.

- Displacement context: We track the last Fair Value Gap (FVG) to account for recent inefficiency that often acts as a magnet or reaction zone.

- Stretch measurement: We anchor VWAP to the latest N-bar impulse and to the Daily session, then normalize stretch by ATR to assess dislocation consistently across assets/timeframes.

- Composite exhaustion: We combine stretch, wick skew, and volume surprise, then bend the result with a tanh transform so extremes are bounded and comparable.

- Dynamic extremes and discipline: Rather than triggering on every sweep, we “arm” at statistical extremes via percent-rank and only fire after a confirmed micro Break of Structure (BOS). This separates “interesting” from “actionable.”

Key concepts

SFP (liquidity sweep): A candle briefly trades beyond a level (where stops sit) and closes back inside. We detect these at:

Pivots (recent swing highs/lows confirmed by “left/right” bars).

Prior Day/Week High/Low (PDH/PDL/PWH/PWL).

FVG (Fair Value Gap): A small 3‑bar gap (bar2 high vs bar1 low, or vice versa). The latest gap often acts like a magnet or reaction zone. We track the most recent Up/Down gap and whether price is inside it.

AVWAP stretch: Distance from an Anchored VWAP divided by ATR (volatility). We use:

Impulse AVWAP: resets on each new N‑bar high/low.

Daily AVWAP: resets each new session.

PR (Percentile Rank): Where the current internal score sits versus its own recent history (0..100). We arm shorts at high PR, longs at low PR.

Micro BOS: A small break of the recent high (for longs) or low (for shorts). This is the “go/no‑go” confirmation.

How the parts work together

Find likely liquidity grabs (SFPs) at pivots and PD/W levels.

Add context from the latest FVG and AVWAP stretch (how far price is from “fair”).

Build a bounded score (so different markets/timeframes are comparable) and compute its percentile (PR).

Arm at extremes (high PR → short candidate; low PR → long candidate).

Only print a trigger after a micro BOS, on a closed bar, with spacing/cooldown rules.

What you see on the chart (legend)

Lines:

Teal line = Impulse AVWAP (resets on new N‑bar extreme).

Aqua line = Daily AVWAP (resets each session).

PDH/PDL/PWH/PWL = prior day/week levels (toggle on/off).

Zones:

Greenish box = latest Up FVG; Reddish box = latest Down FVG.

The shading/border changes after price trades back through it.

SFP labels:

SFP‑P = SFP at Pivot (dotted line marks that pivot’s price).

SFP‑L = SFP at Level (at PDH/PDL/PWH/PWL).

Throttle: To reduce clutter, SFPs are rate‑limited per direction.

Triggers:

Triangle up = long trigger after BOS; triangle down = short trigger after BOS.

Optional badge shows direction and PR at the moment of trigger.

Optional Trigger Zone is an ATR‑sized box around the trigger bar’s close (for visualization only).

Background:

Light green/red shading = a long/short setup is “armed” (not a trigger).

Dashboard (Mini/Pro) — what each item means

PR: Percentile of the internal score (0..100). Near 0 = bullish extreme, near 100 = bearish extreme.

Gauge: Text bar that mirrors PR.

State: Idle, Armed Long (with a countdown), or Armed Short.

Cooldown: Bars remaining before a new setup can arm after a trigger.

Bars Since / Last Px: How long since last trigger and its price.

FVG: Whether price is in the latest Up/Down FVG.

Imp/Day VWAP Dist, PD Dist(ATR): Distance from those references in ATR units.

ATR% (Gate), Trend(HTF): Status of optional regime filters (volatility/trend).

How to use it (step‑by‑step)

Keep the Safety toggles ON (default): triggers/visuals on bar‑close, optional confirmed HTF for trend slope.

Choose timeframe:

Intraday (5m–1h) or Swing (1h–4h). On very fast/thin charts, enable Performance mode and raise spacing/cooldown.

Watch the dashboard:

When PR reaches an extreme and an SFP context is present, the background shades (armed).

Wait for the trigger triangle:

It prints only after a micro BOS on a closed bar and after spacing/cooldown checks.

Use the Trigger Zone box as a visual reference only:

This script never tells you to buy/sell. Apply your own plan for entry, stop, and sizing.

Example:

Bullish: Sweep under PDL (SFP‑L) and reclaim; PR in lower tail arms long; BOS up confirms → long trigger on bar close (ATR-sized trigger zone shown).

Bearish: Sweep above PDH/pivot (SFP‑L/P) and reject; PR in upper tail arms short; BOS down confirms → short trigger on bar close (ATR-sized trigger zone shown).

Settings guide (with “when to adjust”)

Safety & Stability (defaults ON)

Confirm triggers at bar close, Draw visuals at bar close: Keep ON for clean, stable prints.

Use confirmed HTF values: Applies to HTF trend slope only; keeps it from changing until the HTF bar closes.

Performance mode: Turn ON if your chart is busy or laggy.

Core & Context

ATR Length: Bigger = smoother distances; smaller = more reactive.

Impulse AVWAP Anchor: Larger = fewer resets; smaller = resets more often.

Show Daily AVWAP: ON if you want session context.

Use last FVG in logic: ON to include FVG context in arming/score.

Show PDH/PDL/PWH/PWL: ON to see prior day/week levels that often attract sweeps.

Liquidity & Microstructure

Pivot Left/Right: Higher values = stronger/rarer pivots.

Min Wick Ratio (0..1): Higher = only more pronounced SFP wicks qualify.

BOS length: Larger = stricter BOS; smaller = quicker confirmations.

Signal persistence: Keeps SFP context alive for a few bars to avoid flicker.

Signal Gating

Percent‑Rank Lookback: Larger = more stable extremes; smaller = more reactive extremes.

Arm thresholds (qHi/qLo): Move closer to 0.5 to see more arms; move toward 0/1 to see fewer arms.

TTL, Cooldown, Min bars and Min ATR distance: Space out triggers so you’re not reacting to minor noise.

Regime Filters (optional)

ATR percentile gate: Only allow triggers when volatility is at/above a set percentile.

HTF trend gate: Only allow longs when the HTF slope is up (and shorts when it’s down), above a minimum slope.

Visuals & UX

Only show “important” SFPs: Filters pivot SFPs by Volume Z and |Impulse stretch|.

Trigger badges/history and Max badge count: Control label clutter.

Compact labels: Toggle SFP‑P/L vs full names.

Dashboard mode and position; Dark theme.

Reading PR (the built‑in “oscillator”)

PR ~ 0–10: Potential bullish extreme (long side can arm).

PR ~ 90–100: Potential bearish extreme (short side can arm).

Important: “Armed” ≠ “Enter.” A trigger still needs a micro BOS on a closed bar and spacing/cooldown to pass.

Repainting, confirmations, and HTF notes

By default, prints wait for the bar to close; this reduces repaint‑like effects.

Pivot SFPs only appear after the pivot confirms (after the chosen “right” bars).

PD/W levels come from the prior completed candles and do not change intraday.

If you enable confirmed HTF values, the HTF slope will not change until its higher‑timeframe bar completes (safer but slightly delayed).

Performance tips

If labels/zones clutter or the chart lags:

Turn ON Performance mode.

Hide FVG or the Trigger Zone.

Reduce badge history or turn badge history off.

If price scaling looks compressed:

Keep optional “score”/“PR” plots OFF (they overlay price and can affect scaling).

Alerts (neutral)

Structural Liquidity: LONG TRIGGER

Structural Liquidity: SHORT TRIGGER

These fire when a trigger condition is met on a confirmed bar (with defaults).

Limitations and risk

Not every sweep/extreme reverses; false triggers occur, especially on thin markets and low timeframes.

This indicator does not provide entries, exits, or position sizing—use your own plan and risk control.

Educational/informational only; no financial advice.

License and credits

© BullByte - MPL 2.0. Open‑source for learning and research.

Built from repeated observations of how liquidity runs, imbalance (FVG), and distance from “fair” (AVWAPs) combine, and how a small BOS often marks the moment structure actually shifts.

Volatility Cone Forecaster Lite [PhenLabs]📊 Volatility Cone Forecaster

Version: PineScript™v6

📌Description

The Volatility Cone Forecaster (VCF) is an advanced indicator designed to provide traders with a forward-looking perspective on market volatility. Instead of merely measuring past price fluctuations, the VCF analyzes historical volatility data to project a statistical “cone” that outlines a probable range for future price movements. Its core purpose is to contextualize the current market environment, helping traders to anticipate potential shifts from low to high volatility periods (and vice versa). By identifying whether volatility is expanding or contracting relative to historical norms, it solves the critical problem of preparing for significant market moves before they happen, offering a clear statistical edge in strategy development.

This indicator moves beyond lagging measures by employing percentile analysis to rank the current volatility state. This allows traders to understand not just what volatility is, but how significant it is compared to the recent past. The VCF is built for discretionary traders, system developers, and options strategists who need a sophisticated understanding of market dynamics to manage risk and identify high-probability opportunities.

🚀Points of Innovation

Forward-Looking Volatility Projection: Unlike standard indicators that only show historical data, the VCF projects a statistical cone of future volatility.

Percentile-Based Regime Analysis: Ranks current volatility against historical data (e.g., 90th, 75th percentiles) to provide objective context.

Automated Regime Detection: Automatically identifies and labels the market as being in a ‘High’, ‘Low’, or ‘Normal’ volatility regime.

Expansion & Contraction Signals: Clearly indicates whether volatility is currently increasing or decreasing, signaling shifts in market energy.

Integrated ATR Comparison: Plots an ATR-equivalent volatility measure to offer a familiar point of reference against the statistical model.

Dynamic Visual Modeling: The cone visualization directly on the price chart provides an intuitive guide for future expected price ranges.

🔧Core Components

Realized Volatility Engine: Calculates historical volatility using log returns over multiple user-defined lookback periods (short, medium, long) for a comprehensive view.

Percentile Analysis Module: A custom function calculates the 10th, 25th, 50th, 75th, and 90th percentiles of volatility over a long-term lookback (e.g., 252 days).

Forward Projection Calculator: Uses the calculated volatility percentiles to mathematically derive and draw the upper and lower bounds of the future volatility cone.

Volatility Regime Classifier: A logic-based system that compares current volatility to the historical percentile bands to classify the market state.

🔥Key Features

Customizable Lookback Periods: Adjust short, medium, and long-term lookbacks to fine-tune the indicator’s sensitivity to different market cycles.

Configurable Forward Projection: Set the number of days for the forward cone projection to align with your specific trading horizon.

Interactive Display Options: Toggle visibility for percentile labels, ATR levels, and regime coloring to customize the chart display.

Data-Rich Information Table: A clean, on-screen table displays all key metrics, including current volatility, percentile rank, regime, and trend.