OPEN-SOURCE SCRIPT

Aggiornato Band Pass Normalized Suite (BPNS)

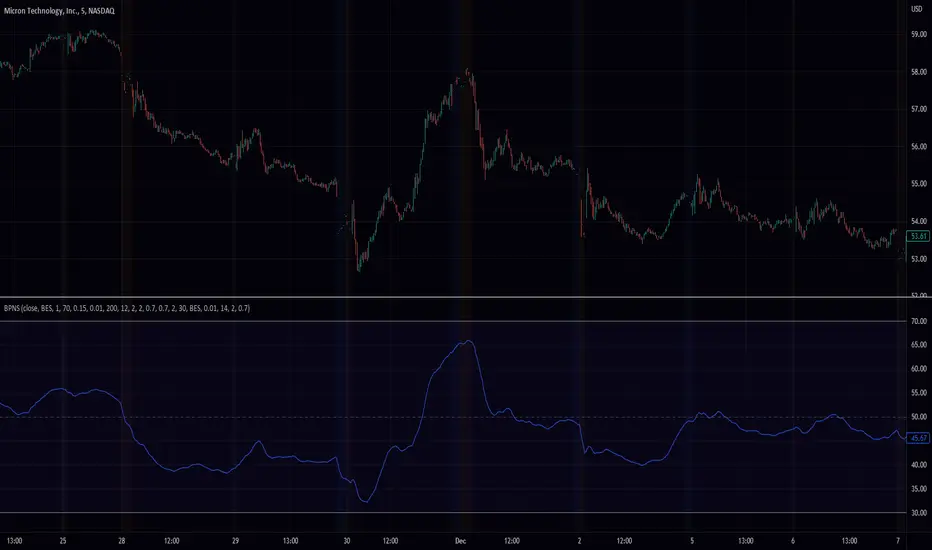

Outlier-Free Normalization and Band Pass Filtering

We present a technique for normalizing and filtering a given time series, source, in order to improve its stationarity and enhance its features. The technique includes two stages: outlier-free normalization and band pass filtering.

Outlier-Free Normalization:

In order to normalize source and reduce the impact of outliers, we first smooth the time series using an exponential moving average with a smoothing factor of alpha. The smoothed time series is then normalized by subtracting the minimum value within a given lookback period, dev_lookback, and dividing the result by the range (maximum - minimum) within the same lookback period. Outliers are detected and excluded from the normalization process by identifying values that are more than outlier_level standard deviations away from the exponentially smoothed average.

Band Pass Filtering:

After normalization, the time series is passed through a band pass filter to remove low and high frequency components. The specifics of the band pass filter implementation are not provided.

Code snippet:

bes(float source = close, float alpha = 0.7) =>

var float smoothed = na

smoothed := na(smoothed) ? source : alpha * source + (1 - alpha) * nz(smoothed[1])

max(source, outlier_level, dev_lookback)=>

var float max = na

src = array.new<float>()

stdev = math.abs((source - bes(source, 0.1))/ta.stdev(source, dev_lookback))

array.push(src, stdev < outlier_level ? source : -1.7976931348623157e+308)

max := math.max(nz(max[1]), array.get(src, 0))

min(source, outlier_level, dev_lookback) =>

var float min = na

src = array.new<float>()

stdev = math.abs((source - bes(source, 0.1))/ta.stdev(source, dev_lookback))

array.push(src, stdev < outlier_level ? source : 1.7976931348623157e+308)

min := math.min(nz(min[1]), array.get(src, 0))

min_max(src, outlier_level, dev_lookback) =>

(src - min(src, outlier_level, dev_lookback))/(max(src, outlier_level, dev_lookback) - min(src, outlier_level, dev_lookback)) * 100

To apply the outlier-free normalization and band pass filter to a given time series, source, the min_max() function can be called with the desired values for outlier_level and dev_lookback as arguments. For example:

normalized_source = min_max(source, 2, 50)

This will apply the outlier-free normalization and band pass filter to source, using an outlier_level of 2 standard deviations and a lookback period of 50 data points for both the normalization and outlier detection steps. The resulting normalized and filtered time series will be stored in normalized_source.

It is important to note that the choice of values for outlier_level and dev_lookback will have a significant impact on the resulting normalized and filtered time series. These values should be chosen carefully based on the characteristics of the input time series and the desired properties of the normalized and filtered output.

In conclusion, the outlier-free normalization and band pass filtering technique presented here provides a useful tool for preprocessing time series data and improving its stationarity and feature content. The flexibility of the method, through the choice of outlier_level and dev_lookback values, allows it to be tailored to the specific characteristics of the input time series.

We present a technique for normalizing and filtering a given time series, source, in order to improve its stationarity and enhance its features. The technique includes two stages: outlier-free normalization and band pass filtering.

Outlier-Free Normalization:

In order to normalize source and reduce the impact of outliers, we first smooth the time series using an exponential moving average with a smoothing factor of alpha. The smoothed time series is then normalized by subtracting the minimum value within a given lookback period, dev_lookback, and dividing the result by the range (maximum - minimum) within the same lookback period. Outliers are detected and excluded from the normalization process by identifying values that are more than outlier_level standard deviations away from the exponentially smoothed average.

Band Pass Filtering:

After normalization, the time series is passed through a band pass filter to remove low and high frequency components. The specifics of the band pass filter implementation are not provided.

Code snippet:

bes(float source = close, float alpha = 0.7) =>

var float smoothed = na

smoothed := na(smoothed) ? source : alpha * source + (1 - alpha) * nz(smoothed[1])

max(source, outlier_level, dev_lookback)=>

var float max = na

src = array.new<float>()

stdev = math.abs((source - bes(source, 0.1))/ta.stdev(source, dev_lookback))

array.push(src, stdev < outlier_level ? source : -1.7976931348623157e+308)

max := math.max(nz(max[1]), array.get(src, 0))

min(source, outlier_level, dev_lookback) =>

var float min = na

src = array.new<float>()

stdev = math.abs((source - bes(source, 0.1))/ta.stdev(source, dev_lookback))

array.push(src, stdev < outlier_level ? source : 1.7976931348623157e+308)

min := math.min(nz(min[1]), array.get(src, 0))

min_max(src, outlier_level, dev_lookback) =>

(src - min(src, outlier_level, dev_lookback))/(max(src, outlier_level, dev_lookback) - min(src, outlier_level, dev_lookback)) * 100

To apply the outlier-free normalization and band pass filter to a given time series, source, the min_max() function can be called with the desired values for outlier_level and dev_lookback as arguments. For example:

normalized_source = min_max(source, 2, 50)

This will apply the outlier-free normalization and band pass filter to source, using an outlier_level of 2 standard deviations and a lookback period of 50 data points for both the normalization and outlier detection steps. The resulting normalized and filtered time series will be stored in normalized_source.

It is important to note that the choice of values for outlier_level and dev_lookback will have a significant impact on the resulting normalized and filtered time series. These values should be chosen carefully based on the characteristics of the input time series and the desired properties of the normalized and filtered output.

In conclusion, the outlier-free normalization and band pass filtering technique presented here provides a useful tool for preprocessing time series data and improving its stationarity and feature content. The flexibility of the method, through the choice of outlier_level and dev_lookback values, allows it to be tailored to the specific characteristics of the input time series.

Note di rilascio

chart fixScript open-source

Nello spirito di TradingView, l'autore di questo script lo ha reso open source, in modo che i trader possano esaminarne e verificarne la funzionalità. Complimenti all'autore! Sebbene sia possibile utilizzarlo gratuitamente, ricordiamo che la ripubblicazione del codice è soggetta al nostro Regolamento.

Declinazione di responsabilità

Le informazioni e le pubblicazioni non sono intese come, e non costituiscono, consulenza o raccomandazioni finanziarie, di investimento, di trading o di altro tipo fornite o approvate da TradingView. Per ulteriori informazioni, consultare i Termini di utilizzo.

Script open-source

Nello spirito di TradingView, l'autore di questo script lo ha reso open source, in modo che i trader possano esaminarne e verificarne la funzionalità. Complimenti all'autore! Sebbene sia possibile utilizzarlo gratuitamente, ricordiamo che la ripubblicazione del codice è soggetta al nostro Regolamento.

Declinazione di responsabilità

Le informazioni e le pubblicazioni non sono intese come, e non costituiscono, consulenza o raccomandazioni finanziarie, di investimento, di trading o di altro tipo fornite o approvate da TradingView. Per ulteriori informazioni, consultare i Termini di utilizzo.