Kijun Equilibria [by Oberlunar]The “story” starts with Ichimoku Kinkō Hyō, created by the Japanese journalist Goichi Hosoda in the 1930s and published in the 1960s; its literal meaning is often rendered as a “one-glance equilibrium chart” because it aims to show balance, trend direction, and dynamic support/resistance at a glance.

In that tradition, the Kijun-sen (“base line”) is not just a moving average: it is a reference equilibrium level, classically computed as the midpoint of the high–low range over 26 periods.

Kijun Equilibria keeps that Japanese “equilibrium” idea, but modernises it in two ways. First, it turns the Kijun concept into an adaptive equilibrium line: instead of assuming a fixed market tempo (like the classic 26), it estimates a dominant cycle length using an Ehlers-style Hilbert/cycle approach, then scales internal lengths and smoothers so the equilibrium line responds differently in trending vs choppy regimes.

Second, it makes equilibrium explicitly multi-timeframe: you compute the adaptive Kijun on the chart TF (in this example 30 m) plus three lower TFs (in this example 1, 3, 5 m), then build a “cloud” between the highest and lowest of those equilibria, which becomes a practical map of where timeframes disagree and where price is most likely to “snap back” toward balance.

Bearish bias

This is a signal that the trend may shift into a bearish bias.

Due to this graphical setup, “cloud fog” is a meaningful meta-word here. In classic Ichimoku, the thickness and shape of the cloud provide a visual way to reason about strength and uncertainty.

In my indicator, the “cloud fog fills” reinterpret that same visual principle, but instead of Senkou spans, they shade the space between equilibria across timeframes, making dispersion (and compression) immediately visible.

The Ornstein–Uhlenbeck part then adds a quantitative “pullback detector” that fits the Ichimoku philosophy rather than replacing it. OU was introduced by Ornstein and Uhlenbeck as a mean-reverting stochastic process; in modern terms, it is a canonical model for a variable that is continuously pulled back toward a mean.

Bullish bias

In this case, we have a bullish bias, and the pullback detector based on Ornstein–Uhlenbeck mean-reversion calculations has signalled that the price is re-entering the green cloud, suggesting a potential bullish continuation after the bounce.

In my indicator, the mean is not an arbitrary moving average: it is the Kijun equilibrium itself. I apply OU to the deviation x = price − kijun, estimate a reversion strength (κ/kappa), and convert the deviation into a z-like score.

The result is very “Japanese” in spirit: the model isn’t saying “price is random”; it’s saying “price departs from balance, but balance pulls back”, and you only trust that pullback when κ is strong enough and the deviation is meaningfully stretched.

Bearish bias and Pull-Back idea

In this case, there are multiple pullbacks that may offer short opportunities, but eventually price breaks strongly through the TF baseline—at that point, it’s time to stop treating the trend as bearish-biased.

Finally, ATR is the glue that makes the bias logic practical and comparable across regimes. ATR (popularised by J. Welles Wilder in 1978) is fundamentally a volatility yardstick. Here it becomes, coupled with biased signals, the unit of measure for everything that should scale with volatility: how far price must be outside the cloud to count as “stretched”, how much spacing you require between stacked Kijuns to accept a true long/short bias, and even how far above/below price you place bias labels. In other words, the “Long Bias / Short Bias” is not just alignment across timeframes; it is alignment with enough ATR-separated structure to reduce false signals when all lines are compressed.

This isn’t one of the most advanced tools in my collection, but it can help newcomers. Be careful: despite the safeguards added, it may or may not produce consistently reliable signals. Risk management is central.

However, given its history, I wanted it to be part of my own collection of scripts with my personal mods, and I’m releasing it for free to the community.

by Oberlunar 👁★

Media Mobile Adattata (AMA)

Lorentzian Length Adaptive Moving Average [LLAMA] Adaptation of "Machine Learning: Lorentzian Classification" by

Gradient color by base on work by

LLAMA: A regime-aware adaptive moving average that bends with the market.

Start with a problem traders know:

Traditional moving averages are either too slow (EMA200) or too fast (EMA9)

Adaptive MAs exist, but they often hug price too tightly or smooth too much, failing to balance bias and tactics

LLAMA uses a Lorentzian distance function to adapt its length dynamically. Instead of a fixed smoothing window, it stretches or contracts depending on market conditions. This distortion reduces lag while still providing a clear bias line.

The indicator looks back at recent bars and measures how similar they are using a Lorentzian distance (a log‑scaled absolute difference). It keeps track of the “nearest neighbors” — bars that most resemble the current regime. Each neighbor carries a label (long, short, neutral) based on simple price comparisons. By averaging these labels, LLAMA predicts whether the market is leaning bullish or bearish. That prediction is then mapped into a dynamic length between and .

Bullish bias -> length stretches toward max (smoother, more stable).

Bearish bias -> length contracts toward min (snappier, more reactive).

During breakouts, LLAMA tightens and comes into contact with bars, giving actionable signals. During chop, it stretches to avoid false triggers. It covers both ends of the spectrum (bias and tactics) in one line, something static MA's can't do.

Think of LLAMA as a lens that bends with the market:

Wide lens (max length) for big picture bias.

Narrow lens (min length) for tactical precision.

The "Lorentzian Loop" is the math that decides when to widen or narrow.

Hurst Exponent Adaptive Filter (HEAF) [PhenLabs]📊 PhenLabs - Hurst Exponent Adaptive Filter (HEAF)

Version: PineScript™ v6

📌 Description

The Hurst Exponent Adaptive Filter (HEAF) is an advanced Pine Script indicator designed to dynamically adjust moving average calculations based on real time market regimes detected through the Hurst Exponent. The intention behind the creation of this indicator was not a buy/sell indicator but rather a tool to help sharpen traders ability to distinguish regimes in the market mathematically rather than guessing. By analyzing price persistence, it identifies whether the market is trending, mean-reverting, or exhibiting random walk behavior, automatically adapting the MA length to provide more responsive alerts in volatile conditions and smoother outputs in stable ones. This helps traders avoid false signals in choppy markets and capitalize on strong trends, making it ideal for adaptive trading strategies across various timeframes and assets.

Unlike traditional moving averages, HEAF incorporates fractal dimension analysis via the Hurst Exponent to create a self-tuning filter that evolves with market conditions. Traders benefit from visual cues like color coded regimes, adaptive bands for volatility channels, and an information panel that suggests appropriate strategies, enhancing decision making without constant manual adjustments by the user.

🚀 Points of Innovation

Dynamic MA length adjustment using Hurst Exponent for regime-aware filtering, reducing lag in trends and noise in ranges.

Integrated market regime classification (trending, mean-reverting, random) with visual and alert-based notifications.

Customizable color themes and adaptive bands that incorporate ATR for volatility-adjusted channels.

Built-in information panel providing real-time strategy recommendations based on detected regimes.

Power sensitivity parameter to fine-tune adaptation aggressiveness, allowing personalization for different trading styles.

Support for multiple MA types (EMA, SMA, WMA) within an adaptive framework.

🔧 Core Components

Hurst Exponent Calculation: Computes the fractal dimension of price series over a user-defined lookback to detect market persistence or anti-persistence.

Adaptive Length Mechanism: Maps Hurst values to MA lengths between minimum and maximum bounds, using a power function for sensitivity control.

Moving Average Engine: Applies the chosen MA type (EMA, SMA, or WMA) to the adaptive length for the core filter line.

Adaptive Bands: Creates upper and lower channels using ATR multiplied by a band factor, scaled to the current adaptive length.

Regime Detection: Classifies market state with thresholds (e.g., >0.55 for trending) and triggers alerts on regime changes.

Visualization System: Includes gradient fills, regime-colored MA lines, and an info panel for at-a-glance insights.

🔥 Key Features

Regime-Adaptive Filtering: Automatically shortens MA in mean-reverting markets for quick responses and lengthens it in trends for smoother signals, helping traders stay aligned with market dynamics.

Custom Alerts: Notifies on regime shifts and band breakouts, enabling timely strategy adjustments like switching to trend-following in bullish regimes.

Visual Enhancements: Color-coded MA lines, gradient band fills, and an optional info panel that displays market state and trading tips, improving chart readability.

Flexible Settings: Adjustable lookback, min/max lengths, sensitivity power, MA type, and themes to suit various assets and timeframes.

Band Breakout Signals: Highlights potential overbought/oversold conditions via ATR-based channels, useful for entry/exit timing.

🎨 Visualization

Main Adaptive MA Line: Plotted with regime-based colors (e.g., green for trending) to visually indicate market state and filter position relative to price.

Adaptive Bands: Upper and lower lines with gradient fills between them, showing volatility channels that widen in random regimes and tighten in trends.

Price vs. MA Fills: Color-coded areas between price and MA (e.g., bullish green above MA in trending modes) for quick trend strength assessment.

Information Panel: Top-right table displaying current regime (e.g., "Trending Market") and strategy suggestions like "Follow trends" or "Trade ranges."

📖 Usage Guidelines

Core Settings

Hurst Lookback Period

Default: 100

Range: 20-500

Description: Sets the period for Hurst Exponent calculation; longer values provide more stable regime detection but may lag, while shorter ones are more responsive to recent changes.

Minimum MA Length

Default: 10

Range: 5-50

Description: Defines the shortest possible adaptive MA length, ideal for fast responses in mean-reverting conditions.

Maximum MA Length

Default: 200

Range: 50-500

Description: Sets the longest adaptive MA length for smoothing in strong trends; adjust based on asset volatility.

Sensitivity Power

Default: 2.0

Range: 1.0-5.0

Description: Controls how aggressively the length adapts to Hurst changes; higher values make it more sensitive to regime shifts.

MA Type

Default: EMA

Options: EMA, SMA, WMA

Description: Chooses the moving average calculation method; EMA is more responsive, while SMA/WMA offer different weighting.

🖼️ Visual Settings

Show Adaptive Bands

Default: True

Description: Toggles visibility of upper/lower bands for volatility channels.

Band Multiplier

Default: 1.5

Range: 0.5-3.0

Description: Scales band width using ATR; higher values create wider channels for conservative signals.

Show Information Panel

Default: True

Description: Displays regime info and strategy tips in a top-right panel.

MA Line Width

Default: 2

Range: 1-5

Description: Adjusts thickness of the main MA line for better visibility.

Color Theme

Default: Blue

Options: Blue, Classic, Dark Purple, Vibrant

Description: Selects color scheme for MA, bands, and fills to match user preferences.

🚨 Alert Settings

Enable Alerts

Default: True

Description: Activates notifications for regime changes and band breakouts.

✅ Best Use Cases

Trend-Following Strategies: In detected trending regimes, use the adaptive MA as a trailing stop or entry filter for momentum trades.

Range Trading: During mean-reverting periods, monitor band breakouts for buying dips or selling rallies within channels.

Risk Management in Random Markets: Reduce exposure when random walk is detected, using tight stops suggested in the info panel.

Multi-Timeframe Analysis: Apply on higher timeframes for regime confirmation, then drill down to lower ones for entries.

Volatility-Based Entries: Use upper/lower band crossovers as signals in adaptive channels for overbought/oversold trades.

⚠️ Limitations

Lagging in Transitions: Regime detection may delay during rapid market shifts, requiring confirmation from other tools.

Not a Standalone System: Best used in conjunction with other indicators; random regimes can lead to whipsaws if traded aggressively.

Parameter Sensitivity: Optimal settings vary by asset and timeframe, necessitating backtesting.

💡 What Makes This Unique

Hurst-Driven Adaptation: Unlike static MAs, it uses fractal analysis to self-tune, providing regime-specific filtering that's rare in standard indicators.

Integrated Strategy Guidance: The info panel offers actionable tips tied to regimes, bridging analysis and execution.

Multi-Regime Visualization: Combines adaptive bands, colored fills, and alerts in one tool for comprehensive market state awareness.

🔬 How It Works

Hurst Exponent Computation:

Calculates log returns over the lookback period to derive the rescaled range (R/S) ratio.

Normalizes to a 0-1 value, where >0.55 indicates trending, <0.45 mean-reverting, and in-between random.

Length Adaptation:

Maps normalized Hurst to an MA length via a power function, clamping between min and max.

Applies the selected MA type to close prices using this dynamic length.

Visualization and Signals:

Plots the MA with regime colors, adds ATR-based bands, and fills areas for trend strength.

Triggers alerts on regime changes or band crosses, with the info panel suggesting strategies like momentum riding in trends.

💡 Note:

For optimal results, backtest settings on your preferred assets and combine with volume or momentum indicators. Remember, no indicator guarantees profits—use with proper risk management. Access premium features and support at PhenLabs.

Adaptive Strength MACD [UM]Indicator Description

Adaptive Strength MACD is an adaptive variant of the classic MACD that uses a customized Strength Momentum moving average for both its oscillator and signal lines. This makes the indicator more responsive in trending conditions and more stable in sideways markets.

Key Features

1. Adaptive Strength Momentum MA

Leverages the Adaptive Momentum Oscillator to scale smoothing coefficients dynamically.

2. Trend-Validity Filters

Optional ADX filter ensures signals only fire when trend strength (ADX) exceeds a user threshold.

3. Directional Filter (DI+) confirms bullish or bearish momentum.

4. Color-Coded Histogram

5. Bars turn bright when momentum accelerates, faded when slowing.

6. Grayed out when trend filters disqualify signals.

7. Alerts

Bullish crossover (histogram from negative to positive) and bearish crossover (positive to negative) only when filters validate trend.

Comparison with Regular MACD

1. Moving Averages

Classic MACD uses fixed exponential moving averages (EMAs) for its fast and slow lines, so the smoothing factor is constant regardless of how strong or weak price momentum is.

Adaptive Strength MACD replaces those EMAs with a dynamic “Strength Momentum” MA that speeds up when momentum is strong and slows down in quiet or choppy markets.

2. Signal Line Smoothing

In the classic MACD, the signal is simply an EMA of the MACD line, with one user-selected period.

In the Adaptive Strength MACD , the signal line also uses the Strength Momentum MA on the MACD series—so both oscillator and signal adapt together to the underlying momentum strength.

3. Responsiveness to Momentum

A static EMA reacts the same way whether momentum is surging or fading; you either get too-slow entries when momentum spikes or too-fast whipsaws in noise.

The adaptive MA in your indicator automatically gives you quicker crossovers when there’s a trending burst, while damping down during low-momentum chop.

4. Trend Validation Filters

The classic MACD has no built-in mechanism to know whether price is actually trending versus ranging—you’ll see crossovers in both regimes.

Adaptive Strength MACD includes optional ADX filtering (to require a minimum trend strength) and a DI filter (to confirm bullish vs. bearish directional pressure). When those filters aren’t met, the histogram grays out to warn you.

5. Histogram Coloring & Clarity

Typical MACD histograms often use two colors (above/below zero) or a simple ramp but don’t distinguish accelerating vs. decelerating moves.

Your version employs four distinct states—accelerating bulls, decelerating bulls, accelerating bears, decelerating bears—plus a gray “no-signal” state when filters fail. This makes it easy at a glance to see not just direction but the quality of the move.

6. False-Signal Reduction

Because the classic MACD fires on every crossover, it can generate whipsaws in ranging markets.

The adaptive MA smoothing combined with ADX/DI gating in your script helps suppress those false breaks and keeps you focused on higher-quality entries.

7. Ideal Use Cases

Use the classic MACD when you need a reliable, well-understood trend-following oscillator and you’re comfortable manually filtering choppy signals.

Choose Adaptive Strength MACD \ when you want an all-in-one, automated way to speed up in strong trends, filter out noise, and receive clearer visual cues and alerts only when conditions align.

How to Use

1. Setup

- Adjust Fast and Slow Length to tune sensitivity.

- Change Signal Smoothing to smooth the histogram reaction.

- Enable ADX/DI filters and set ADX Threshold to suit your preferred trend strength (default = 20).

2. Interpretation

- Histogram > 0: Short‐term momentum above long‐term → bullish.

- Histogram < 0: Short‐term below long‐term → bearish.

- Faded greyed bars indicate a weakening move; gray bars show filter invalidation.

How to Trade

Buy Setup:

- Histogram crosses from negative to positive.

- ADX ≥ threshold and DI+ > DI–.

- Look for confirmation (bullish candlestick patterns or support zone).

Sell Setup:

- Histogram crosses from positive to negative.

- ADX ≥ threshold and DI– > DI+.

- Confirm with bearish price action (resistance test or bearish pattern).

Stop & Target

- Place stop just below recent swing low (long) or above recent swing high (short).

- Target risk–reward of at least 1:2, or trail with a shorter‐period adaptive MA.

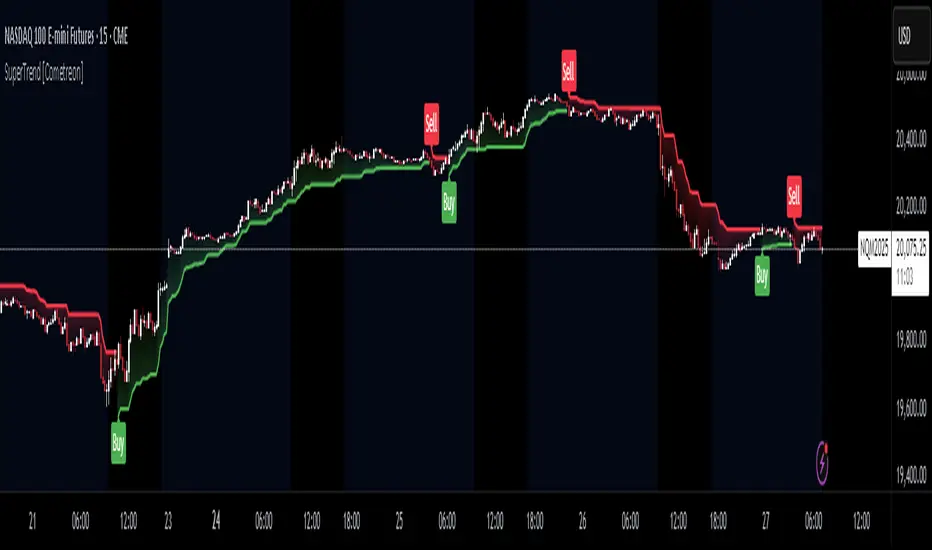

SuperTrend MTF Pro [Cometreon]The SuperTrend MTF Pro takes the classic SuperTrend to a whole new level of customization and accuracy. Unlike the standard version, this indicator allows you to select different moving averages, apply it to various chart types, and fine-tune every key parameter.

If you're looking for an advanced, non-repainting, and highly configurable SuperTrend, this is the right choice for you.

🔷 New Features and Improvements

🟩 Multi-MA SuperTrend

Now you can customize the SuperTrend calculation by choosing from 15 different moving averages:

SMA (Simple Moving Average)

EMA (Exponential Moving Average)

WMA (Weighted Moving Average)

RMA (Smoothed Moving Average)

HMA (Hull Moving Average)

JMA (Jurik Moving Average)

DEMA (Double Exponential Moving Average)

TEMA (Triple Exponential Moving Average)

LSMA (Least Squares Moving Average)

VWMA (Volume-Weighted Moving Average)

SMMA (Smoothed Moving Average)

KAMA (Kaufman’s Adaptive Moving Average)

ALMA (Arnaud Legoux Moving Average)

FRAMA (Fractal Adaptive Moving Average)

VIDYA (Variable Index Dynamic Average)

🟩 Multiple Chart Types

You're no longer limited to candlestick charts! Now you can use SuperTrend with different chart formats, including:

Heikin Ashi

Renko

Kagi

Line Break

Point & Figure

🟩 Customizable Timeframe

Now you can adjust the SuperTrend timeframe without repainting issues, avoiding signal distortions.

🔷 Technical Details and Customizable Inputs

SuperTrend offers multiple customization options to fit any trading strategy:

1️⃣ ATR Period – Defines the ATR length, affecting the indicator’s sensitivity.

2️⃣ Source – Selects the price value used for calculations (Close, HL2, Open, etc.).

3️⃣ ATR Mult – Multiplies the ATR to determine band distance. Higher values reduce false signals, lower values make it more reactive.

4️⃣ Change ATR Calculation Method – When enabled, uses the default ATR method; when disabled, allows selecting another Moving Average with "Use Different Type".

5️⃣ Source Break – Defines the price source for trend changes (Close for more stability, High/Low for more reactivity).

6️⃣ Use Different Type – Allows selecting an alternative Moving Average for ATR calculation if "Change ATR Calculation Method" is disabled.

7️⃣ SuperTrend Type – Advanced options for specific MAs (JMA, ALMA, FRAMA, VIDYA), with dedicated parameters like Phase, Sigma, and Offset for optimized responsiveness.

8️⃣ Ticker Settings – Customize parameters for special chart types such as Renko, Heikin Ashi, Kagi, Line Break, and Point & Figure, adjusting reversal, number of lines, and ATR length.

9️⃣ Timeframe – Enables using SuperTrend on a higher timeframe.

🔟 Wait for Timeframe Closes -

✅ Enabled – Prevents multiple signals, useful for precise alerts.

❌ Disabled – Displays SuperTrend smoothly without interruptions.

🔷 How to Use SuperTrend MTF Pro

🔍 Identifying Trends

SuperTrend follows the ongoing trend and provides clear visual signals:

When the price is above the line, the trend is bullish.

When the price is below the line, the trend is bearish.

📈 Interpreting Signals

Line color and position change → Possible trend reversal

Bounce off the line → Potential trend continuation

Strong breakout of the line → Possible reversal

🛠 Integration with Other Tools

RSI or MACD to filter false signals

Moving Averages to confirm trend direction

Support and Resistance to improve entry points

☄️ If you find this indicator useful, leave a Boost to support its development!

Every feedback helps to continuously improve the tool, offering an even more effective trading experience. Share your thoughts in the comments! 🚀🔥

Auto-Length Moving Average + Trend Signals (Zeiierman)█ Overview

The Auto-Length Moving Average + Trend Signals (Zeiierman) is an easy-to-use indicator designed to help traders dynamically adjust their moving average length based on market conditions. This tool adapts in real-time, expanding and contracting the moving average based on trend strength and momentum shifts.

The indicator smooths out price fluctuations by modifying its length while ensuring responsiveness to new trends. In addition to its adaptive length algorithm, it incorporates trend confirmation signals, helping traders identify potential trend reversals and continuations with greater confidence.

This indicator suits scalpers, swing traders, and trend-following investors who want a self-adjusting moving average that adapts to volatility, momentum, and price action dynamics.

█ How It Works

⚪ Dynamic Moving Average Length

The core feature of this indicator is its ability to automatically adjust the length of the moving average based on trend persistence and market conditions:

Expands in strong trends to reduce noise.

Contracts in choppy or reversing markets for faster reaction.

This allows for a more accurate moving average that aligns with current price dynamics.

⚪ Trend Confirmation & Signals

The indicator includes built-in trend detection logic, classifying trends based on market structure. It evaluates trend strength based on consecutive bars and smooths out transitions between bullish, bearish, and neutral conditions.

Uptrend: Price is persistently above the adjusted moving average.

Downtrend: Price remains below the adjusted moving average.

Neutral: Price fluctuates around the moving average, indicating possible consolidation.

⚪ Adaptive Trend Smoothing

A smoothing factor is applied to enhance trend readability while minimizing excessive lag. This balances reactivity with stability, making it easier to follow longer-term trends while avoiding false signals.

█ How to Use

⚪ Trend Identification

Bullish Trend: The indicator confirms an uptrend when the price consistently stays above the dynamically adjusted moving average.

Bearish Trend: A downtrend is recognized when the price remains below the moving average.

⚪ Trade Entry & Exit

Enter long when the dynamic moving average is green and a trend signal occurs. Exit when the price crosses below the dynamic moving average.

Enter short when the dynamic moving average is red and a trend signal occurs. Exit when the price crosses above the dynamic moving average.

█ Slope-Based Reset

This mode resets the trend counter when the moving average slope changes direction.

⚪ Interpretation & Insights

Best for trend-following traders who want to filter out noise and only reset when a clear shift in momentum occurs.

Higher slope length (N): More stable trends, fewer resets.

Lower slope length (N): More reactive to small price swings, frequent resets.

Useful in swing trading to track significant trend reversals.

█ RSI-Based Reset

The counter resets when the Relative Strength Index (RSI) crosses predefined overbought or oversold levels.

⚪ Interpretation & Insights

Best for reversal traders who look for extreme overbought/oversold conditions.

High RSI threshold (e.g., 80/20): Fewer resets, only extreme conditions trigger adjustments.

Lower RSI threshold (e.g., 60/40): More frequent resets, detecting smaller corrections.

Great for detecting exhaustion in trends before potential reversals.

█ Volume-Based Reset

A reset occurs when current volume significantly exceeds its moving average, signaling a shift in market participation.

⚪ Interpretation & Insights

Best for traders who follow institutional activity (high volume often means large players are active).

Higher volume SMA length: More stable trends, only resets on massive volume spikes.

Lower volume SMA length: More reactive to short-term volume shifts.

Useful in identifying breakout conditions and trend acceleration points.

█ Bollinger Band-Based Reset

A reset occurs when price closes above the upper Bollinger Band or below the lower Bollinger Band, signaling potential overextension.

⚪ Interpretation & Insights

Best for traders looking for volatility-based trend shifts.

Higher Bollinger Band multiplier (k = 2.5+): Captures only major price extremes.

Lower Bollinger Band multiplier (k = 1.5): Resets on moderate volatility changes.

Useful for detecting overextensions in strong trends before potential retracements.

█ MACD-Based Reset

A reset occurs when the MACD line crosses the signal line, indicating a momentum shift.

⚪ Interpretation & Insights

Best for momentum traders looking for trend continuation vs. exhaustion signals.

Longer MACD lengths (260, 120, 90): Captures major trend shifts.

Shorter MACD lengths (10, 5, 3): Reacts quickly to momentum changes.

Useful for detecting strong divergences and market shifts.

█ Stochastic-Based Reset

A reset occurs when Stochastic %K crosses overbought or oversold levels.

⚪ Interpretation & Insights

Best for short-term traders looking for fast momentum shifts.

Longer Stochastic length: Filters out false signals.

Shorter Stochastic length: Captures quick intraday shifts.

█ CCI-Based Reset

A reset occurs when the Commodity Channel Index (CCI) crosses predefined overbought or oversold levels. The CCI measures the price deviation from its statistical mean, making it a useful tool for detecting overextensions in price action.

⚪ Interpretation & Insights

Best for cycle traders who aim to identify overextended price deviations in trending or ranging markets.

Higher CCI threshold (e.g., ±200): Detects extreme overbought/oversold conditions before reversals.

Lower CCI threshold (e.g., ±10): More sensitive to trend shifts, useful for early signal detection.

Ideal for detecting momentum shifts before price reverts to its mean or continues trending strongly.

█ Momentum-Based Reset

A reset occurs when Momentum (Rate of Change) crosses zero, indicating a potential shift in price direction.

⚪ Interpretation & Insights

Best for trend-following traders who want to track acceleration vs. deceleration.

Higher momentum length: Captures longer-term shifts.

Lower momentum length: More responsive to short-term trend changes.

█ How to Interpret the Trend Strength Table

The Trend Strength Table provides valuable insights into the current market conditions by tracking how the dynamic moving average is adjusting based on trend persistence. Each metric in the table plays a role in understanding the strength, longevity, and stability of a trend.

⚪ Counter Value

Represents the current length of trend persistence before a reset occurs.

The higher the counter, the longer the current trend has been in place without resetting.

When this value reaches the Counter Break Threshold, the moving average resets and contracts to become more reactive.

Example:

A low counter value (e.g., 10) suggests a recent trend reset, meaning the market might be changing directions frequently.

A high counter value (e.g., 495) means the trend has been ongoing for a long time, indicating strong trend persistence.

⚪ Trend Strength

Measures how strong the current trend is based on the trend confirmation logic.

Higher values indicate stronger trends, while lower values suggest weaker trends or consolidations.

This value is dynamic and updates based on price action.

Example:

Trend Strength of 760 → Indicates a high-confidence trend.

Trend Strength of 50 → Suggests weak price action, possibly a choppy market.

⚪ Highest Trend Score

Tracks the strongest trend score recorded during the session.

Helps traders identify the most dominant trend observed in the timeframe.

This metric is useful for analyzing historical trend strength and comparing it with current conditions.

Example:

Highest Trend Score = 760 → Suggests that at some point, there was a strong trend in play.

If the current trend strength is much lower than this value, it could indicate trend exhaustion.

⚪ Average Trend Score

This is a rolling average of trend strength across the session.

Provides a bigger picture of how the trend strength fluctuates over time.

If the average trend score is high, the market has had persistent trends.

If it's low, the market may have been choppy or sideways.

Example:

Average Trend Score of 147 vs. Current Trend Strength of 760 → Indicates that the current trend is significantly stronger than the historical average, meaning a breakout might be occurring.

Average Trend Score of 700+ → Suggests a strong trending market overall.

█ Settings

⚪ Dynamic MA Controls

Base MA Length – Sets the starting length of the moving average before dynamic adjustments.

Max Dynamic Length – Defines the upper limit for how much the moving average can expand.

Trend Confirmation Length – The number of bars required to validate an uptrend or downtrend.

⚪ Reset & Adaptive Conditions

Reset Condition Type – Choose what triggers the moving average reset (Slope, RSI, Volume, MACD, etc.).

Trend Smoothing Factor – Adjusts how smoothly the moving average responds to price changes.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Multi-Scale Adaptive MAs (Hurst, CVaR, Fractal) // AlgoFyreThe Multi-Scale Adaptive MAs (Hurst, CVaR, Fractal) indicator adjusts moving averages based on market conditions, using Hurst Exponent for trend persistence, CVaR for extreme risk assessment, and Fractal Dimension for market complexity. It enhances trend detection and risk management across various timeframes.

TABLE OF CONTENTS

🔶 ORIGINALITY 🔸Adaptive Mechanisms

🔸Multi-Faceted Analysis

🔸Versatility Across Timeframes

🔸Multi-Scale Combination

🔶 FUNCTIONALITY 🔸Hurst Exponent (H)

🞘 How it works

🞘 How to calculate

🞘 Code extract

🔸Conditional Value at Risk (CVaR)

🞘 How it works

🞘 How to calculate

🞘 Code extract

🔸Fractal Dimension (FD)

🞘 How it works

🞘 How to calculate

🞘 Code extract

🔶 INSTRUCTIONS 🔸Step-by-Step Guidelines

🞘 Setting Up the Indicator

🞘 Understanding What to Look For on the Chart

🞘 Possible Entry Signals

🞘 Possible Take Profit Strategies

🞘 Possible Stop-Loss Levels

🞘 Additional Tips

🔸Customize settings

🔶 CONCLUSION

▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅

🔶 ORIGINALITY The Multi-Scale Adaptive MAs (Hurst, CVaR, Fractal) indicator stands out due to its unique approach of dynamically adjusting moving averages based on advanced statistical measures, making it highly responsive to varying market conditions. Unlike traditional moving averages that rely on static periods, this indicator adapts in real-time using three distinct adaptive methods: Hurst Exponent, CVaR, and Fractal Dimension.

🔸Adaptive Mechanisms

Traditional MA indicators use fixed lengths, which can lead to lagging signals or over-sensitivity in volatile markets. The Multi-Scale Adaptive MAs employ adaptive methods to adjust the MA length dynamically, providing a more accurate reflection of current market conditions.

🔸Multi-Faceted Analysis

By integrating Hurst Exponent, CVaR, and Fractal Dimension, the indicator offers a comprehensive market analysis. It captures different aspects of market behavior, including trend persistence, risk of extreme movements, and complexity, which are often missed by standard MAs.

🔸Versatility Across Timeframes

The indicator’s ability to switch between different adaptive methods based on market conditions allows traders to analyze short-term, medium-term, and long-term trends with enhanced precision.

🔸Multi-Scale Combination

Utilizing multiple adaptive MAs in combination provides a more nuanced view of the market, allowing traders to see how short, medium, and long-term trends interact. This layered approach helps in identifying the strength and consistency of trends across different scales, offering more reliable signals and aiding in complex decision-making processes. When combined, these MAs can also signal key market shifts when they converge or diverge, offering deeper insights than a single MA could provide.

🔶 FUNCTIONALITY The indicator adjusts moving averages based on a variety of different choosable adaptives. The Hurst Exponent to identify trend persistence or mean reversion, adapting to market conditions for both short-term and long-term trends. Using CVaR, it evaluates the risk of extreme price movements, ensuring the moving average is more conservative during high-risk periods, protecting against potential large losses. By incorporating the Fractal Dimension, the indicator adapts to market complexity, adjusting to varying levels of price roughness and volatility, which allows it to respond more accurately to different market structures and patterns.

Let's dive into the details:

🔸Hurst Exponent (H)

Measures the degree of trend persistence or mean reversion.

By using the Hurst Exponent, the indicator adjusts to capture the strength and duration of trends, helping traders to stay in profitable trades longer and avoid false reversals in ranging markets.

It enhances the detection of trends, making it suitable for both short-term scalping and identifying long-term trends.

🞘 How it works Rescaled Range (R/S) Analysis Calculate the mean of the closing prices over a set window.

Determine the deviation of each price from the mean.

Compute the cumulative sum of these deviations over the window.

Calculate the range (R) of the cumulative deviations (maximum minus minimum).

Compute the standard deviation (S) of the price series over the window.

Obtain the R/S ratio as R/S.

Linear Regression for Hurst Exponent Calculate the logarithm of multiple window sizes and their corresponding R/S values.

Use linear regression to determine the slope of the line fitting the log(R/S) against log(window size).

The slope of this line is an estimate of the Hurst Exponent.

🞘 How to calculate Range (R)

Calculate the maximum cumulative deviation:

R=max(sum(deviation))−min(sum(deviation))

Where deviation is the difference between each price and the mean.

Standard Deviation (S)

Calculate the standard deviation of the price series:

S=sqrt((1/(n−1))∗sum((Xi−mean)2))

Rescaled Range (R/S)

Divide the range by the standard deviation:

R/S=R/S

Hurst Exponent

Perform linear regression to estimate the slope of:

log(R/S) versus log(windowsize)

The slope of this line is the Hurst Exponent.

🞘 Code extract // Hurst Exponent

calc_hurst(source_, adaptive_window_) =>

window_sizes = array.from(adaptive_window_/10, adaptive_window_/5, adaptive_window_/2, adaptive_window_)

float hurst_exp = 0.5

// Calculate Hurst Exponent proxy

rs_list = array.new_float()

log_length_list = array.new_float()

for i = 0 to array.size(window_sizes) - 1

len = array.get(window_sizes, i)

// Ensure we have enough data

if bar_index >= len * 2

mean = adaptive_sma(source_, len)

dev = source_ - mean

// Calculate cumulative deviations over the window

cum_dev = ta.cum(dev) - ta.cum(dev )

r = ta.highest(cum_dev, len) - ta.lowest(cum_dev, len)

s = ta.stdev(source_, len)

if s != 0

rs = r / s

array.push(rs_list, math.log(rs))

array.push(log_length_list, math.log(len))

// Linear regression to estimate Hurst Exponent

n = array.size(log_length_list)

if n > 1

mean_x = array.sum(log_length_list) / n

mean_y = array.sum(rs_list) / n

sum_num = 0.0

sum_den = 0.0

for i = 0 to n - 1

x = array.get(log_length_list, i)

y = array.get(rs_list, i)

sum_num += (x - mean_x) * (y - mean_y)

sum_den += (x - mean_x) * (x - mean_x)

hurst_exp := sum_den != 0 ? sum_num / sum_den : 0.5

else

hurst_exp := 0.5 // Default to 0.5 if not enough data

hurst_exp

🔸Conditional Value at Risk (CVaR)

Assesses the risk of extreme losses by focusing on tail risk.

This method adjusts the moving average to account for market conditions where extreme price movements are likely, providing a more conservative approach during periods of high risk.

Traders benefit by better managing risk and avoiding major losses during volatile market conditions.

🞘 How it works Calculate Returns Determine the returns as the percentage change between consecutive closing prices over a specified window.

Percentile Calculation Identify the percentile threshold (e.g., the 5th percentile) for the worst returns in the dataset.

Average of Extreme Losses Calculate the average of all returns that are less than or equal to this percentile, representing the CVaR.

🞘 How to calculate Return Calculation

Calculate the return as the percentage change between consecutive prices:

Return = (Pt − Pt−1) / Pt−1

Where Pt is the price at time t.

Percentile Threshold

Identify the return value at the specified percentile (e.g., 5th percentile):

PercentileValue=percentile(returns,percentile_threshold)

CVaR Calculation

Compute the average of all returns below the percentile threshold:

CVaR = (1/n)∗sum(Return) for all Return≤PercentileValue

Where n is the total number of returns.

🞘 Code extract // Percentile

calc_percentile(data, percentile, window) =>

arr = array.new_float(0)

for i = 0 to window - 1

array.push(arr, data )

array.sort(arr)

index = math.floor(percentile / 100 * (window - 1))

array.get(arr, index)

// Conditional Value at Risk

calc_cvar(percentile_value, returns, window) =>

// Collect returns worse than the threshold

cvar_sum = 0.0

cvar_count = 0

for i = 0 to window - 1

ret = returns

if ret <= percentile_value

cvar_sum += ret

cvar_count += 1

// Calculate CVaR

cvar = cvar_count > 0 ? cvar_sum / cvar_count : 0.0

cvar

🔸Fractal Dimension (FD)

Evaluates market complexity and roughness by analyzing how price movements behave across different scales.

It enables the moving average to adapt based on the level of market noise or structure, allowing for smoother MAs during complex, volatile periods and more sensitive MAs during clear trends.

This adaptability is crucial for traders dealing with varying market states, improving the indicator's responsiveness to price changes.

🞘 How it works Total Distance (L) Calculation Sum the absolute price movements between consecutive periods over a given window.

Maximum Distance (D) Calculation Calculate the maximum displacement from the first to the last price point within the window.

Calculate Fractal Dimension Use Katz's method to estimate the Fractal Dimension as the ratio of the logarithms of L and D, divided by the logarithm of the number of steps (N).

🞘 How to calculate Total Distance (L)

Sum the absolute price changes over the window:

L=sum(abs(Pt−Pt−1)) for t from 2 to n

Where Pt is the price at time t.

Maximum Distance (D)

Find the maximum absolute displacement from the first to the last price in the window:

D=max(abs(Pn-P1))

Fractal Dimension Calculation

Use Katz's method to estimate fractal dimension:

FD=log(L/D)/log(N)

Where N is the number of steps in the window.

🞘 Code extract // Fractal Dimension

calc_fractal(source_, adaptive_window_) =>

// Calculate the total distance (L) traveled by the price

L = 0.0

for i = 1 to adaptive_window_

L += math.abs(source_ - source_ )

// Calculate the maximum distance between first and last price

D = math.max(math.abs(source_ - source_ ), 1e-10) // Avoid division by zero

// Calculate the number of steps (N)

N = adaptive_window_

// Estimate the Fractal Dimension using Katz's formula

math.log(L / D) / math.log(N)

🔶 INSTRUCTIONS The Multi-Scale Adaptive MAs indicator can be set up by adding it to your TradingView chart and configuring the adaptive method (Hurst, CVaR, or Fractal) to match current market conditions. Look for price crossovers and changes in the slope for potential entry signals. Set take profit and stop-loss levels based on dynamic changes in the moving average, and consider combining it with other indicators for confirmation. Adjust settings and use adaptive strategies for enhanced trend detection and risk management.

🔸Step-by-Step Guidelines 🞘 Setting Up the Indicator Adding the Indicator to the Chart: Go to your TradingView chart.

Click on the "Indicators" button at the top.

Search for "Multi-Scale Adaptive MAs (Hurst, CVaR, Fractal)" in the indicators list.

Click on the indicator to add it to your chart.

Configuring the Indicator: Open the indicator settings by clicking on the gear icon next to its name on the chart.

Adaptive Method: Choose between "Hurst," "CVaR," and "Fractal" depending on the market condition and your trading style.

Length: Set the base length for the moving average (e.g., 20, 50, or 100). This length will be adjusted dynamically based on the selected adaptive method.

Other Parameters: Adjust any other parameters as needed, such as window sizes or scaling factors specific to each adaptive method.

Chart Setup: Ensure you have an appropriate timeframe selected (e.g., 1-hour, 4-hour, daily) based on your trading strategy.

Consider using additional indicators like volume or RSI to confirm signals.

🞘 Understanding What to Look For on the Chart Indicator Behavior: Observe how the adaptive moving average (AMA) behaves compared to standard moving averages, e.g. notice how it might change direction with strength (Hurst).

For example, the AMA may become smoother during high market volatility (CVaR) or more responsive during strong trends (Hurst).

Crossovers: Look for crossovers between the price and the adaptive moving average.

A bullish crossover occurs when the price crosses above the AMA, suggesting a potential uptrend.

A bearish crossover occurs when the price crosses below the AMA, indicating a possible downtrend.

Slope and Direction: Pay attention to the slope of the AMA. A rising slope suggests a bullish trend, while a declining slope indicates a bearish trend.

The slope’s steepness can give you clues about the trend's strength.

🞘 Possible Entry Signals Bullish Entry: Crossover Entry: Enter a long position when the price crosses above the AMA and the AMA has a positive slope.

Confirmation Entry: Combine the crossover with other indicators like RSI (above 50) or increasing volume for confirmation.

Bearish Entry: Crossover Entry: Enter a short position when the price crosses below the AMA and the AMA has a negative slope.

Confirmation Entry: Use additional indicators like RSI (below 50) or decreasing volume to confirm the bearish trend.

Adaptive Method Confirmation: Hurst: Enter when the AMA indicates a strong trend (steeper slope). Suitable for trend-following strategies.

CVaR: Be cautious during high-risk periods. Enter only if confirmed by other indicators, as the AMA may become more conservative.

Fractal: Ideal for capturing reversals in complex markets. Look for crossovers in volatile markets.

🞘 Possible Take Profit Strategies Static Take Profit Levels: Set take profit levels based on predefined ratios (e.g., 1:2 or 1:3 risk-reward ratio).

Place take profit orders at recent swing highs (for long positions) or swing lows (for short positions).

Trailing Stop Loss: Use a trailing stop based on a percentage of the AMA value to lock in profits as the trend progresses.

Adjust the trailing stop dynamically to follow the AMA, allowing profits to run while protecting gains.

Adaptive Method Based Exits: Hurst: Exit when the AMA begins to flatten or turn in the opposite direction, signaling a potential trend reversal.

CVaR: Consider taking profits earlier during high-risk periods when the AMA suggests caution.

Fractal: Use the AMA to exit in complex markets when it smooths out, indicating reduced volatility.

🞘 Possible Stop-Loss Levels Initial Stop Loss: Place an initial stop loss below the AMA (for long positions) or above the AMA (for short positions) to protect against adverse movements.

Use a buffer (e.g., ATR value) to avoid being stopped out by normal price fluctuations.

Adaptive Stop Loss: Adjust the stop loss dynamically based on the AMA. Move the stop loss along the AMA as the trend progresses to minimize risk.

This helps in adapting to changing market conditions and avoiding premature exits.

Adaptive Method-Specific Stop Loss: Hurst: Use wider stops during trending markets to allow for minor pullbacks.

CVaR: Adjust stops in high-risk periods to avoid being stopped out prematurely during price fluctuations.

Fractal: Place stops at recent support/resistance levels in highly volatile markets.

🞘 Additional Tips Combine with Other Indicators: Enhance your strategy by combining the AMA with other technical indicators like MACD, RSI, or Bollinger Bands for better signal confirmation.

Backtesting and Practice: Backtest the indicator on historical data to understand how it performs in different market conditions.

Practice using the indicator on a demo account before applying it to live trading.

Market Awareness: Always be aware of market conditions and fundamental events that might impact price movements, as the AMA reacts to price action and may not account for sudden news-driven events.

🔸Customize settings 🞘 Time Override: Enables or disables the ability to override the default time frame for the moving averages. When enabled, you can specify a custom time frame for the calculations.

🞘 Time: Specifies the custom time frame to use when the Time Override setting is enabled.

🞘 Enable MA: Enables or disables the moving average. When disabled, MA will not be displayed on the chart.

🞘 Show Smoothing Line: Enables or disables the display of a smoothing line for the moving average. The smoothing line helps to reduce noise and provide a clearer trend.

🞘 Show as Horizontal Line: Displays the moving average as a horizontal line instead of a dynamic line that follows the price.

🞘 Source: Specifies the data source for the moving average calculation (e.g., close, open, high, low).

🞘 Length: Sets the period length for the moving average. A longer length will result in a smoother moving average, while a shorter length will make it more responsive to price changes.

🞘 Time: Specifies a custom time frame for the moving average, overriding the default time frame if Time Override is enabled.

🞘 Method: Selects the calculation method for the moving average (e.g., SMA, EMA, SMMA, WMA, VWMA).

🞘 Offset: Shifts the moving average forward or backward by the specified number of bars.

🞘 Color: Sets the color for the moving average line.

🞘 Adaptive Method: Selects the adaptive method to dynamically adjust the moving average based on market conditions (e.g., Hurst, CVaR, Fractal).

🞘 Window Size: Sets the window size for the adaptive method, determining how much historical data is used for the calculation.

🞘 CVaR Scaling Factor: Adjusts the influence of CVaR on the moving average length, controlling how much the length changes based on calculated risk.

🞘 CVaR Risk: Specifies the percentile cutoff for the worst-case returns used in the CVaR calculation to assess extreme losses.

🞘 Smoothing Method: Selects the method for smoothing the moving average (e.g., SMA, EMA, SMMA, WMA, VWMA).

🞘 Smoothing Length: Sets the period length for smoothing the moving average.

🞘 Fill Color to Smoothing Moving Average: Enables or disables the color fill between the moving average and its smoothing line.

🞘 Transparency: Sets the transparency level for the color fill between the moving average and its smoothing line.

🞘 Show Label: Enables or disables the display of a label for the moving average on the chart.

🞘 Show Label for Smoothing: Enables or disables the display of a label for the smoothing line of the moving average on the chart.

🔶 CONCLUSION The Multi-Scale Adaptive MAs indicator offers a sophisticated approach to trend analysis and risk management by dynamically adjusting moving averages based on Hurst Exponent, CVaR, and Fractal Dimension. This adaptability allows traders to respond more effectively to varying market conditions, capturing trends and managing risks with greater precision. By incorporating advanced statistical measures, the indicator goes beyond traditional moving averages, providing a nuanced and versatile tool for both short-term and long-term trading strategies. Its unique ability to reflect market complexity and extreme risks makes it an invaluable asset for traders seeking a deeper understanding of market dynamics.

Kaufman Adaptive Moving Average (KAMA) Strategy [TradeDots]"The Kaufman Adaptive Moving Average (KAMA) Strategy" is a trend-following system that leverages the adaptive qualities of the Kaufman Adaptive Moving Average (KAMA). This strategy is distinguished by its ability to adjust dynamically to market volatility, enhancing trading accuracy by minimizing the effects of false and delayed signals often associated with the Simple Moving Average (SMA).

HOW IT WORKS

This strategy is centered around use of the Kaufman Adaptive Moving Average (KAMA) indicator, which refines the principles of the Exponential Moving Average (EMA) with a superior smoothing technique.

KAMA distinguishes itself by its responsiveness to changes in market prices through an "Efficiency Ratio (ER)." This ratio is computed by dividing the recent absolute net price change by the cumulative sum of the absolute price changes over a specified period. The resulting ER value ranges between 0 and 1, where 0 indicates high market noise and 1 reflects stronger market momentum.

Using ER, we could get the smoothing constant (SC) for the moving average derived using the following formula:

fastest = 2/(fastma_length + 1)

slowest = 2/(slowma_length + 1)

SC = math.pow((ER * (fastest-slowest) + slowest), 2)

The KAMA line is then calculated by applying the SC to the difference between the current price and the previous KAMA.

APPLICATION

For entering long positions, this strategy initializes when there is a sequence of 10 consecutive rising KAMA lines. Conversely, a sequence of 10 consecutive falling KAMA lines triggers sell orders for long positions. The same logic applies inversely for short positions.

DEFAULT SETUP

Commission: 0.01%

Initial Capital: $10,000

Equity per Trade: 80%

Users are advised to adjust and personalize this trading strategy to better match their individual trading preferences and style.

RISK DISCLAIMER

Trading entails substantial risk, and most day traders incur losses. All content, tools, scripts, articles, and education provided by TradeDots serve purely informational and educational purposes. Past performances are not definitive predictors of future results.

Adaptive Moving Average (AMA) Signals (Zeiierman)█ Overview

The Adaptive Moving Average (AMA) Signals indicator, enhances the classic concept of moving averages by making them adaptive to the market's volatility. This adaptability makes the AMA particularly useful in identifying market trends with varying degrees of volatility.

The core of the AMA's adaptability lies in its Efficiency Ratio (ER), which measures the directionality of the market over a given period. The ER is calculated by dividing the absolute change in price over a period by the sum of the absolute differences in daily prices over the same period.

⚪ Why It's Useful

The AMA Signals indicator is particularly useful because of its adaptability to changing market conditions. Unlike static moving averages, it dynamically adjusts, providing more relevant signals that can help traders capture trends earlier or identify reversals with greater accuracy. Its configurability makes it suitable for various trading strategies and timeframes, from day trading to swing trading.

█ How It Works

The AMA Signals indicator operates on the principle of adapting to market efficiency through the calculation of the Efficiency Ratio (ER), which measures the directionality of the market over a specified period. By comparing the net price change to total price movements, the AMA adjusts its sensitivity, becoming faster during trending markets and slower during sideways markets. This adaptability is enhanced by a gamma parameter that filters signals for either trend continuation or reversal, making it versatile across different market conditions.

change = math.abs(close - close )

volatility = math.sum(math.abs(close - close ), n)

ER = change / volatility

Efficiency Ratio (ER) Calculation: The AMA begins with the computation of the Efficiency Ratio (ER), which measures the market's directionality over a specified period. The ER is a ratio of the net price change to the total price movements, serving as a measure of the efficiency of price movements.

Adaptive Smoothing: Based on the ER, the indicator calculates the smoothing constants for the fastest and slowest Exponential Moving Averages (EMAs). These constants are then used to compute a Scaled Smoothing Coefficient (SC) that adapts the moving average to the market's efficiency, making it faster during trending periods and slower in sideways markets.

Signal Generation: The AMA applies a filter, adjusted by a "gamma" parameter, to identify trading signals. This gamma influences the sensitivity towards trend or reversal signals, with options to adjust for focusing on either trend-following or counter-trend signals.

█ How to Use

Trend Identification: Use the AMA to identify the direction of the trend. An upward moving AMA indicates a bullish trend, while a downward moving AMA suggests a bearish trend.

Trend Trading: Look for buy signals when the AMA is trending upwards and sell signals during a downward trend. Adjust the fast and slow EMA lengths to match the desired sensitivity and timeframe.

Reversal Trading: Set the gamma to a positive value to focus on reversal signals, identifying potential market turnarounds.

█ Settings

Period for ER calculation: Defines the lookback period for calculating the Efficiency Ratio, affecting how quickly the AMA responds to changes in market efficiency.

Fast EMA Length and Slow EMA Length: Determine the responsiveness of the AMA to recent price changes, allowing traders to fine-tune the indicator to their trading style.

Signal Gamma: Adjusts the sensitivity of the filter applied to the AMA, with the ability to focus on trend signals or reversal signals based on its value.

AMA Candles: An innovative feature that plots candles based on the AMA calculation, providing visual cues about the market trend and potential reversals.

█ Alerts

The AMA Signals indicator includes configurable alerts for buy and sell signals, as well as positive and negative trend changes.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Optimal Length BackTester [YinYangAlgorithms]This Indicator allows for a ‘Optimal Length’ to be inputted within the Settings as a Source. Unlike most Indicators and/or Strategies that rely on either Static Lengths or Internal calculations for the length, this Indicator relies on the Length being derived from an external Indicator in the form of a Source Input.

This may not sound like much, but this application may allows limitless implementations of such an idea. By allowing the input of a Length within a Source Setting you may have an ‘Optimal Length’ that adjusts automatically without the need for manual intervention. This may allow for Traditional and Non-Traditional Indicators and/or Strategies to allow modifications within their settings as well to accommodate the idea of this ‘Optimal Length’ model to create an Indicator and/or Strategy that adjusts its length based on the top performing Length within the current Market Conditions.

This specific Indicator aims to allow backtesting with an ‘Optimal Length’ inputted as a ‘Source’ within the Settings.

This ‘Optimal Length’ may be used to display and potentially optimize multiple different Traditional Indicators within this BackTester. The following Traditional Indicators are included and available to be backtested with an ‘Optimal Length’ inputted as a Source in the Settings:

Moving Average; expressed as either a: Simple Moving Average, Exponential Moving Average or Volume Weighted Moving Average

Bollinger Bands; expressed based on the Moving Average Type

Donchian Channels; expressed based on the Moving Average Type

Envelopes; expressed based on the Moving Average Type

Envelopes Adjusted; expressed based on the Moving Average Type

All of these Traditional Indicators likewise may be displayed with multiple ‘Optimal Lengths’. They have the ability for multiple different ‘Optimal Lengths’ to be inputted and displayed, such as:

Fast Optimal Length

Slow Optimal Length

Neutral Optimal Length

By allowing for the input of multiple different ‘Optimal Lengths’ we may express the ‘Optimal Movement’ of such an expressed Indicator based on different Time Frames and potentially also movement based on Fast, Slow and Neutral (Inclusive) Lengths.

This in general is a simple Indicator that simply allows for the input of multiple different varieties of ‘Optimal Lengths’ to be displayed in different ways using Tradition Indicators. However, the idea and model of accepting a Length as a Source is unique and may be adopted in many different forms and endless ideas.

Tutorial:

You may add an ‘Optimal Length’ within the Settings as a ‘Source’ as followed in the example above. This Indicator allows for the input of a:

Neutral ‘Optimal Length’

Fast ‘Optimal Length’

Slow ‘Optimal Length’

It is important to account for all three as they generally encompass different min/max length values and therefore result in varying ‘Optimal Length’s’.

For instance, say you’re calculating the ‘Optimal Length’ and you use:

Min: 1

Max: 400

This would therefore be scanning for 400 (inclusive) lengths.

As a general way of calculating you may assume the following for which lengths are being used within an ‘Optimal Length’ calculation:

Fast: 1 - 199

Slow: 200 - 400

Neutral: 1 - 400

This allows for the calculation of a Fast and Slow length within the predetermined lengths allotted. However, it likewise allows for a Neutral length which is inclusive to all lengths alloted and may be deemed the ‘Most Accurate’ for these reasons. However, just because the Neutral is inclusive to all lengths, doesn’t mean the Fast and Slow lengths are irrelevant. The Fast and Slow length inputs may be useful for seeing how specifically zoned lengths may fair, and likewise when they cross over and/or under the Neutral ‘Optimal Length’.

This Indicator features the ability to display multiple different types of Traditional Indicators within the ‘Display Type’.

We will go over all of the different ‘Display Types’ with examples on how using a Fast, Slow and Neutral length would impact it:

Simple Moving Average:

In this example above have the Fast, Slow and Neutral Optimal Length formatted as a Slow Moving Average. The first example is on the 15 minute Time Frame and the second is on the 1 Day Time Frame, demonstrating how the length changes based on the Time Frame and the effects it may have.

Here we can see that by inputting ‘Optimal Lengths’ as a Simple Moving Average we may see moving averages that change over time with their ‘Optimal Lengths’. These lengths may help identify Support and/or Resistance locations. By using an 'Optimal Length' rather than a static length, we may create a Moving Average which may be more accurate as it attempts to be adaptive to current Market Conditions.

Bollinger Bands:

Bollinger Bands are a way to see a Simple Moving Average (SMA) that then uses Standard Deviation to identify how much deviation has occurred. This Deviation is then Added and Subtracted from the SMA to create the Bollinger Bands which help Identify possible movement zones that are ‘within range’. This may mean that the price may face Support / Resistance when it reaches the Outer / Inner bounds of the Bollinger Bands. Likewise, it may mean the Price is ‘Overbought’ when outside and above or ‘Underbought’ when outside and below the Bollinger Bands.

By applying All 3 different types of Optimal Lengths towards a Traditional Bollinger Band calculation we may hope to see different ranges of Bollinger Bands and how different lookback lengths may imply possible movement ranges on both a Short Term, Long Term and Neutral perspective. By seeing these possible ranges you may have the ability to identify more levels of Support and Resistance over different lengths and Trading Styles.

Donchian Channels:

Above you’ll see two examples of Machine Learning: Optimal Length applied to Donchian Channels. These are displayed with both the 15 Minute Time Frame and the 1 Day Time Frame.

Donchian Channels are a way of seeing potential Support and Resistance within a given lookback length. They are a way of withholding the High’s and Low’s of a specific lookback length and looking for deviation within this length. By applying a Fast, Slow and Neutral Machine Learning: Optimal Length to these Donchian Channels way may hope to achieve a viable range of High’s and Low’s that one may use to Identify Support and Resistance locations for different ranges of Optimal Lengths and likewise potentially different Trading Strategies.

Envelopes / Envelopes Adjusted:

Envelopes are an interesting one in the sense that they both may be perceived as useful; however we deem that with the use of an ‘Optimal Length’ that the ‘Envelopes Adjusted’ may work best. We will start with examples of the Traditional Envelope then showcase the Adjusted version.

Envelopes:

As you may see, a Traditional form of Envelopes even produced with a Machine Learning: Optimal Length may not produce optimal results. Unfortunately this may occur with some Traditional Indicators and they may need some adjustments as you’ll notice with the ‘Envelopes Adjusted’ version. However, even without the adjustments, these Envelopes may be useful for seeing ‘Overbought’ and ‘Oversold’ locations within a Machine Learning: Optimal Length standpoint.

Envelopes Adjusted:

By adding an adjustment to these Envelopes, we may hope to better reflect our Optimal Length within it. This is caused by adding a ratio reflection towards the current length of the Optimal Length and the max Length used. This allows for the Fast and Neutral (and potentially Slow if Neutral is greater) to achieve a potentially more accurate result.

Envelopes, much like Bollinger Bands are a way of seeing potential movement zones along with potential Support and Resistance. However, unlike Bollinger Bands which are based on Standard Deviation, Envelopes are based on percentages +/- from the Simple Moving Average.

We will conclude our Tutorial here. Hopefully this has given you some insight into how useful adding a ‘Optimal Length’ within an external (secondary) Indicator as a Source within the Settings may be. Likewise, how useful it may be for automation sake in the sense that when the ‘Optimal Length’ changes, it doesn’t rely on an alert where you need to manually update it yourself; instead it will update Automatically and you may reap the benefits of such with little manual input needed (aside from the initial setup).

If you have any questions, comments, ideas or concerns please don't hesitate to contact us.

HAPPY TRADING!

SOFEX Strong Volatility Trend Follower + BacktestingWhat is the SOFEX Strong Volatility Trend Follower + Backtesting script?

🔬 Trading Philosophy

This script is trend-following, attempting to avoid choppy markets.

It has been developed for Bitcoin and Ethereum trading, on 1H timeframe.

The strategy does not aim to make a lot of trades, or to always remain in a position and switch from long to short. Many times there is no direction and the market is in "random walk mode", and chasing trades is futile.

Expectations of performance should be realistic.

The script focuses on a balanced take-profit to stop-loss ratio. In the default set-up of the script, that is a 2% : 2% (1:1) ratio. A relatively low stop loss and take profit build onto the idea that positions should be exited promptly. There are many options to edit these values, including enabling trailing take profit and stop loss. Traders can also completely turn off TP and SL levels, and rely on opposing signals to exit and enter new trades.

Extreme scenarios can happen on the cryptocurrency markets, and disabling stop-loss levels completely is not recommended. The position size should be monitored since all of it is at risk with no stop-loss.

⚙️ Logic of the indicator

The Strong Volatility Trend Follower indicator aims at evading ranging market conditions. It does not seek to chase volatile, yet choppy markets. It aims at aggressively following confirmed trends. The indicator works best during strong, volatile trends, however, it has the downside of entering trades at trend tops or bottoms.

This indicator also leverages proprietary adaptive moving averages to identify and follow strong trend volatility effectively. Furthermore, it uses the Average Directional Index, Awesome Oscillator, ATR and a modified version of VWAP, to categorize trends into weak or strong ones. The VWAP indicator is used to identify the monetary (volume) inflow into a given trend, further helping to avoid short-term manipulations. It also helps to distinguish choppy-market volatility with a trending market one.

📟 Parameters Menu

The script has a comprehensive parameter menu:

Preset Selection : Choose between Bitcoin or Ethereum presets to tailor the indicator to your preferred cryptocurrency market.

Indicator Sensitivity Parameter : Adjust the sensitivity to adapt the indicator, particularly to make it seek higher-strength trends.

Indicator Signal Direction : Set the signal direction as Long, Short, or Both, depending on your preference.

Exit of Signals : You have options regarding Take-Profit (TP) and Stop-Loss (SL) levels. Enable TP/SL levels to exit trades at predetermined levels, or disable them to rely on direction changes for exits. Be aware that removing stop losses can introduce additional risk, and position sizing should be carefully monitored.

By enabling Trailing TP/SL, the system switches to a trailing approach, allowing you to:

- Place an initial customizable SL.

- Specify a level (%) for the Trailing SL to become active.

- When the activation level is reached, the system moves the trailing stop by a given Offset (%).

Additionally, you can enable exit at break-even, where the system places an exit order when the trail activation level is reached, accounting for fees and slippage.

Alert Messages : Define the fields for alert messages based on specific conditions. You can set up alerts to receive email, SMS, and in-app notifications. If you use webhooks for alerts, exercise caution, as these alerts can potentially execute trades without human supervision.

Backtesting : Default backtesting parameters are set to provide realistic backtesting performance:

- 0.04% Commission per trade (for both entries and exits)

- 3 ticks Slippage (highly dependent on exchange)

- Initial capital of $1000

- Order size of $1000

While the order size is equal to the initial capital, the script employs a 2% stop-loss order to limit losses and attempts to prevent risky trades from creating big losses. The order size is a set dollar value, so that the backtesting performance is linear, instead of using % of capital which may result in unrealistic backtesting performance.

Risk Disclaimer

Please be aware that backtesting results, while valuable for statistical overview, do not guarantee future performance in any way. Cryptocurrency markets are inherently volatile and risky. Always trade responsibly and do not risk more than you can afford to lose.

Volume-Weighted Kaufman's Adaptive Moving AverageThe Volume-Weighted Kaufman's Adaptive Moving Average (VW-KAMA) is a technical indicator that combines the Volume-Weighted Moving Average (VWMA) and the Kaufman's Adaptive Moving Average (KAMA) to create a more responsive and adaptable moving average.

Advantages:

Volume-Weighted: It takes into account the volume of trades, giving more weight to periods with higher trading volume, which can help filter out periods of low activity.

Adaptive: The indicator adjusts its smoothing constant based on market conditions, becoming more sensitive in trending markets and less sensitive in choppy or sideways markets.

Versatility: VW-KAMA can be used for various purposes, including trend identification, trend following, and determining potential reversal points and act as dynamic support and resistance level.

T3 JMA KAMA VWMAEnhancing Trading Performance with T3 JMA KAMA VWMA Indicator

Introduction

In the dynamic world of trading, staying ahead of market trends and capitalizing on volume-driven opportunities can greatly influence trading performance. To address this, we have developed the T3 JMA KAMA VWMA Indicator, an innovative tool that modifies the traditional Volume Weighted Moving Average (VWMA) formula to increase responsiveness and exploit high-volume market conditions for optimal position entry. This article delves into the idea behind this modification and how it can benefit traders seeking to gain an edge in the market.

The Idea Behind the Modification

The core concept behind modifying the VWMA formula is to leverage more responsive moving averages (MAs) that align with high-volume market activity. Traditional VWMA utilizes the Simple Moving Average (SMA) as the basis for calculating the weighted average. While the SMA is effective in providing a smoothed perspective of price movements, it may lack the desired responsiveness to capitalize on short-term volume-driven opportunities.

To address this limitation, our T3 JMA KAMA VWMA Indicator incorporates three advanced moving averages: T3, JMA, and KAMA. These MAs offer enhanced responsiveness, allowing traders to react swiftly to changing market conditions influenced by volume.

T3 (T3 New and T3 Normal):

The T3 moving average, one of the components of our indicator, applies a proprietary algorithm that provides smoother and more responsive trend signals. By utilizing T3, we ensure that the VWMA calculation aligns with the dynamic nature of high-volume markets, enabling traders to capture price movements accurately.

JMA (Jurik Moving Average):

The JMA component further enhances the indicator's responsiveness by incorporating phase shifting and power adjustment. This adaptive approach ensures that the moving average remains sensitive to changes in volume and price dynamics. As a result, traders can identify turning points and anticipate potential trend reversals, precisely timing their position entries.

KAMA (Kaufman's Adaptive Moving Average):

KAMA is an adaptive moving average designed to dynamically adjust its sensitivity based on market conditions. By incorporating KAMA into our VWMA modification, we ensure that the moving average adapts to varying volume levels and captures the essence of volume-driven price movements. Traders can confidently enter positions during periods of high trading volume, aligning their strategies with market activity.

Benefits and Usage

The modified T3 JMA KAMA VWMA Indicator offers several advantages to traders looking to exploit high-volume market conditions for position entry:

Increased Responsiveness: By incorporating more responsive moving averages, the indicator enables traders to react quickly to changes in volume and capture short-term opportunities more effectively.

Enhanced Entry Timing: The modified VWMA aligns with high-volume periods, allowing traders to enter positions precisely during price movements influenced by significant trading activity.

Improved Accuracy: The combination of T3, JMA, and KAMA within the VWMA formula enhances the accuracy of trend identification, reversals, and overall market analysis.

Comprehensive Market Insights: The T3 JMA KAMA VWMA Indicator provides a holistic view of market conditions by considering both price and volume dynamics. This comprehensive perspective helps traders make informed decisions.

Analysis and Interpretation