Hyper SAR Reactor Trend StrategyHyperSAR Reactor Adaptive PSAR Strategy

Summary

Adaptive Parabolic SAR strategy for liquid stocks, ETFs, futures, and crypto across intraday to daily timeframes. It acts only when an adaptive trail flips and confirmation gates agree. Originality comes from a logistic boost of the SAR acceleration using drift versus ATR, plus ATR hysteresis, inertia on the trail, and a bear-only gate for shorts. Add to a clean chart and run on bar close for conservative alerts.

Scope and intent

• Markets: large cap equities and ETFs, index futures, major FX, liquid crypto

• Timeframes: one minute to daily

• Default demo: BTC on 60 minute

• Purpose: faster yet calmer PSAR that resists chop and improves short discipline

• Limits: this is a strategy that places simulated orders on standard candles

Originality and usefulness

• Novel fusion: PSAR AF is boosted by a logistic function of normalized drift, trail is monotone with inertia, entries use ATR buffers and optional cooldown, shorts are allowed only in a bear bias

• Addresses false flips in low volatility and weak downtrends

• All controls are exposed in Inputs for testability

• Yardstick: ATR normalizes drift so settings port across symbols

• Open source. No links. No solicitation

Method overview

Components

• Adaptive AF: base step plus boost factor times logistic strength

• Trail inertia: one sided blend that keeps the SAR monotone

• Flip hysteresis: price must clear SAR by a buffer times ATR

• Volatility gate: ATR over its mean must exceed a ratio

• Bear bias for shorts: price below EMA of length 91 with negative slope window 54

• Cooldown bars optional after any entry

• Visual SAR smoothing is cosmetic and does not drive orders

Fusion rule

Entry requires the internal flip plus all enabled gates. No weighted scores.

Signal rule

• Long when trend flips up and close is above SAR plus buffer times ATR and gates pass

• Short when trend flips down and close is below SAR minus buffer times ATR and gates pass

• Exit uses SAR as stop and optional ATR take profit per side

Inputs with guidance

Reactor Engine

• Start AF 0.02. Lower slows new trends. Higher reacts quicker

• Max AF 1. Typical 0.2 to 1. Caps acceleration

• Base step 0.04. Typical 0.01 to 0.08. Raises speed in trends

• Strength window 18. Typical 10 to 40. Drift estimation window

• ATR length 16. Typical 10 to 30. Volatility unit

• Strength gain 4.5. Typical 2 to 6. Steepness of logistic

• Strength center 0.45. Typical 0.3 to 0.8. Midpoint of logistic

• Boost factor 0.03. Typical 0.01 to 0.08. Adds to step when strength rises

• AF smoothing 0.50. Typical 0.2 to 0.7. Adds inertia to AF growth

• Trail smoothing 0.35. Typical 0.15 to 0.45. Adds inertia to the trail

• Allow Long, Allow Short toggles

Trade Filters

• Flip confirm buffer ATR 0.50. Typical 0.2 to 0.8. Raise to cut flips

• Cooldown bars after entry 0. Typical 0 to 8. Blocks re entry for N bars

• Vol gate length 30 and Vol gate ratio 1. Raise ratio to trade only in active regimes

• Gate shorts by bear regime ON. Bear bias window 54 and Bias MA length 91 tune strictness

Risk

• TP long ATR 1.0. Set to zero to disable

• TP short ATR 0.0. Set to 0.8 to 1.2 for quicker shorts

Usage recipes

Intraday trend focus

Confirm buffer 0.35 to 0.5. Cooldown 2 to 4. Vol gate ratio 1.1. Shorts gated by bear regime.

Intraday mean reversion focus

Confirm buffer 0.6 to 0.8. Cooldown 4 to 6. Lower boost factor. Leave shorts gated.

Swing continuation

Strength window 24 to 34. ATR length 20 to 30. Confirm buffer 0.4 to 0.6. Use daily or four hour charts.

Properties visible in this publication

Initial capital 10000. Base currency USD. Order size Percent of equity 3. Pyramiding 0. Commission 0.05 percent. Slippage 5 ticks. Process orders on close OFF. Bar magnifier OFF. Recalculate after order filled OFF. Calc on every tick OFF. No security calls.

Realism and responsible publication

No performance claims. Past results never guarantee future outcomes. Shapes can move while a bar forms and settle on close. Strategies execute only on standard candles.

Honest limitations and failure modes

High impact events and thin books can void assumptions. Gap heavy symbols may prefer longer ATR. Very quiet regimes can reduce contrast and invite false flips.

Open source reuse and credits

Public domain building blocks used: PSAR concept and ATR. Implementation and fusion are original. No borrowed code from other authors.

Strategy notice

Orders are simulated on standard candles. No lookahead.

Entries and exits

Long: flip up plus ATR buffer and all gates true

Short: flip down plus ATR buffer and gates true with bear bias when enabled

Exit: SAR stop per side, optional ATR take profit, optional cooldown after entry

Tie handling: stop first if both stop and target could fill in one bar

BTC-M

EquiSense AI Signals🇸🇦 العربي

المتنبئ الذكي المتوازن (AI v7)

وصف قصير:

مؤشر تجميعي ذكي يوازن بين الاتجاه والزخم والحجم والتذبذب وأنماط الشموع، ويحوّلها إلى نظام نقاط ونجوم يولّد إشارات شراء/بيع مؤكَّدة بتقاطع MACD. بعد الإشارة، يعرض أهدافًا ذكية (TP1/TP2/TP3) ووقف خسارة مبنيَّيْن على ATR مع رسومات مستقبلية ولوحة معلومات لإدارة الصفقة.

الإعدادات (Inputs)

الحد الأدنى للنقاط (min_score): افتراضي 6.0 — كلما ارتفع قلّت الإشارات وزادت جودتها.

الحد الأدنى للنجوم (min_stars): افتراضي 2 — فلتر لقوة الإشارة.

عدد الشموع المستقبلية (future_bars): افتراضي 15 — مدى رسم الأهداف والوقف للأمام.

استخدام الأهداف الذكية (use_ai_targets): تفعيل/إيقاف مضاعِف الذكاء الاصطناعي للأهداف والوقف.

كيف يعمل؟

يحسب المؤشر buy_score/sell_score من مجموعة عوامل: EMA8/21/50/200، RSI + متوسطه، MACD + Histogram، Stochastic، ADX/DMI، VWAP، الحجم، MTF 15m، ROC/المومنتَم، Heikin Ashi، وأنماط (ابتلاع/مطرقة/شهاب).

يحوّل الدرجات إلى نجوم (⭐⭐ إلى ⭐⭐⭐⭐⭐) حسب القوة.

تولّد الإشارة فقط إذا توفّر: درجة ≥ الحد + نجوم ≥ الحد + تقاطع MACD (صعودًا للشراء، هبوطًا للبيع).

عند الإشارة يبدأ سيناريو صفقة واحدة فقط حتى تنتهي (TP3 أو SL).

الأهداف والوقف (ذكاء اصطناعي)

تُشتق من ATR ثم تُعدَّل عبر مضاعِف AI مبني على: ATR%، الزخم (ROC)، الحجم مقابل متوسطه، قوة الاتجاه (ADX)، وعدد النجوم.

تقريبيًا:

TP1 ≈ 1.5×ATR × AI

TP2 ≈ 2.5×ATR × AI

TP3 ≈ 4.0×ATR × AI

SL ≈ 1.0×ATR ÷ AI

ماذا سترى على الشارت؟

علامات “شراء/بيع”، نجوم قرب الإشارة، خط دخول (أزرق)، وقف (أحمر منقّط)، TP1/TP2 (أخضر)، TP3 (ذهبي) مع صناديق مناطق للأهداف وخط ربط نحو الهدف النهائي.

وسم AI يعرض نسبة المضاعِف والنجوم بصريًا.

لوحة معلومات تعرض الحالة، القوة، AI%، السعر، الدرجات، وأثناء الصفقة: الدخول، TP1/TP2/TP3، والربح اللحظي.

التنبيهات (Alerts)

شرطان جاهزان: شراء وبيع عند تحقق الإشارة.

أضِف تنبيه: Right click → Add alert → اختر المؤشر → الشرط المطلوب.

أفضل الممارسات

استخدم الإطار المناسب للأصل:

سكالبينغ 5–15m: min_score 8 وmin_stars 3–4.

تأرجحي H1–H4: min_score 7 وmin_stars 3.

يومي/أسهم: min_score 6–7 وmin_stars 2–3.

فضّل التداول مع EMA200 واتجاه MTF 15m.

خفّض المخاطرة وقت الأخبار العالية.

التزم بإدارة مخاطر ثابتة (مثلاً 1% لكل صفقة).

حدود مهمة

الأفضل انتظار إغلاق الشمعة لتأكيد التقاطعات وتجنّب تغيّرها.

صفقة واحدة في المرة بفضل حالة in_trade.

يستخدم request.security مع lookahead_off لإطار 15m؛ التزم بالتقييم عند الإغلاق.

أسئلة شائعة

هل يستخدم منفردًا؟ نعم، لكن مع مناطق سعرية/ترند وخطة مخاطر يصبح أقوى.

لماذا تختلف الأهداف؟ لأن مضاعِف AI يكيّف TP/SL مع ظروف السوق.

إخلاء مسؤولية

هذه أداة تحليلية تعليمية وليست نصيحة استثمارية. اختبر الإعدادات تاريخيًا والتزم بالمخاطرة المناسبة.

ملاحظة للمبرمجين

Pine Script v6، متغيرات var لحفظ الحالة، تنظيف الرسومات على الشمعة الأخيرة، مع حدود مرتفعة للرسوم لتجنّب الأخطاء.

🇬🇧 English

Balanced Smart Predictor (AI v7)

Short description:

A smart, ensemble-style indicator that blends trend, momentum, volume, volatility, and candle patterns into a score & star system that produces Buy/Sell signals confirmed by MACD crosses. After a signal, it projects smart targets (TP1/TP2/TP3) and a stop-loss derived from ATR, with forward drawings and a control panel for trade management.

Inputs

Minimum Score (min_score): default 6.0 — higher = fewer but stronger signals.

Minimum Stars (min_stars): default 2 — extra filter for strength.

Future Bars (future_bars): default 15 — how far targets/SL are drawn ahead.

Use AI Targets (use_ai_targets): toggle the AI multiplier for TP/SL.

How it works

Computes buy_score/sell_score from: EMA8/21/50/200, RSI & its MA, MACD & Histogram, Stochastic, ADX/DMI, VWAP, Volume, 15m MTF tilt, ROC/Momentum, Heikin Ashi, and candle patterns (engulfing/hammer/shooting star).

Converts scores into Stars (⭐⭐ to ⭐⭐⭐⭐⭐) via tiered thresholds.

Signals fire only when: Score ≥ minimum + Stars ≥ minimum + MACD cross (up = Buy, down = Sell).

On a signal, one active trade is managed until TP3 or SL is reached.

Targets & Stop (AI-driven)

Targets and SL are ATR-based, then adjusted by an AI multiplier derived from: ATR%, momentum (ROC), relative volume, trend strength (ADX), and star rating.

Approximate formulas:

TP1 ≈ 1.5×ATR × AI

TP2 ≈ 2.5×ATR × AI

TP3 ≈ 4.0×ATR × AI

SL ≈ 1.0×ATR ÷ AI

What you’ll see on chart

“Buy/Sell” markers with small Star labels, an Entry line (blue), SL (red dotted), TP1/TP2 (green), TP3 (gold) with shaded target boxes and a guide line towards the final target.

A central AI badge showing the multiplier % and star rating.

A top-right Panel showing status, strength, AI%, price, scores, and during trades: entry, TP1/TP2/TP3, and live P/L.

Alerts

Two ready-made conditions: Buy and Sell when the respective signal triggers.

Add alert: Right click → Add alert → choose the indicator → select condition.

Best practices

Match timeframe to instrument:

Scalping 5–15m: min_score 8, min_stars 3–4.

Swing H1–H4: min_score 7, min_stars 3.

Daily/Equities: min_score 6–7, min_stars 2–3.

Prefer trades with EMA200 and 15m MTF trend alignment.

De-risk around major news.

Use fixed risk per trade (e.g., 1%).

Important notes

Prefer bar close confirmation to avoid mid-bar MACD flips.

Single trade at a time via the in_trade state.

15m MTF uses request.security with lookahead_off; evaluate at close for consistency.

FAQ

Use it standalone? You can, but it’s stronger when combined with S/R zones/trendlines and solid risk management.

Why do targets vary? The AI multiplier adapts TP/SL to current market conditions.

Disclaimer

This is an analytical/educational tool, not financial advice. Always backtest and use appropriate risk management.

Developer note

Built in Pine Script v6, uses var for trade state, clears drawings on the last bar to keep the chart tidy, and raises drawing limits to avoid runtime errors.

Crypto ETFs AUM📘 Description: BTC ETFs AUM Tracker

This indicator tracks the Assets Under Management (AUM) and daily inflows/outflows of the main U.S.-listed Bitcoin ETFs, allowing you to visualize institutional capital movement into Bitcoin products over time. It helps traders correlate institutional capital movement with Bitcoin price behavior.

🧩 Overview

The script adds up the daily AUM changes from selected Bitcoin ETFs to estimate the total net inflow/outflow of capital into spot BTC funds. It also accumulates those flows over time to display the total aggregated AUM balance, giving you a clearer sense of market direction and institutional sentiment. Two display modes are available: Balance view: plots the cumulative sum of net inflows (total ETF AUM). Inflows view: shows daily inflows (green) and outflows (red) as histogram columns, together with a smoothed moving average line.

⚙️ Inputs

Explained Base Settings Base Multiplier (base_multi) – Scaling factor applied to all AUM values. Leave at 1 for USD units, or adjust to display values in millions (1e6) or billions (1e9). Smoothing (c_smoothing) – Period length for the simple moving average used to calculate the smoothed mean inflow/outflow line. Show Balance (showBalance) – When enabled, displays the total cumulative AUM balance (sum of all net inflows over time). Show Inflows (showInflows) – When enabled, displays the daily inflows/outflows as colored columns. ETF Selection You can toggle which ETFs are included in the calculation:

BIT (BlackRock)

GBTC (Grayscale)

FBTC (Fidelity)

ARKB (ARK/21Shares)

BITB (Bitwise)

EZBC (Franklin Templeton)

BTCW (WisdomTree)

BTCO (Invesco Galaxy)

BRRR (Valkyrie)

HODL (VanEck)

Each switch determines whether the ETF’s AUM and daily flow data are included in the total calculation.

📊 Displayed Values Green Columns → Positive daily net inflows (AUM increased). Red Columns → Negative daily net outflows (AUM decreased). Orange Line → Smoothed moving average of net flows, used to identify persistent inflow/outflow trends. Blue Line (if enabled) → Total cumulative AUM balance (sum of all historical flows).

💡 Usage Notes Works best on daily timeframe, since ETF data is typically updated once per trading day. Not all ETFs have identical data history; missing data points are automatically skipped. The indicator doesn’t represent official fund NAV or guarantee data accuracy — it visualizes TradingView’s public financial feed. You can combine this tool with price action or on-chain metrics to analyze institutional Bitcoin flows.

Note: Some ETF data may not be available to all users depending on their TradingView data subscription or market access. Missing values are automatically skipped.

🧠 Disclaimer This script is for educational and analytical purposes only. It is not financial advice, and no investment decisions should be based solely on this indicator. Data accuracy depends on TradingView’s financial data sources and exchange reporting frequency.

Cycle Indicator CS7This indicator visualizes cyclical structures (including inverse cycles) for financial instruments.

It is highly customizable and comes with a default configuration optimized for cryptocurrencies on a 45-minute timeframe, highlighting the following cycles:

• T-3: Daily cycles

• T-2: Approximately 2-day cycles

• T+1: Bi-weekly cycles

• T-1: Approximately 4-day cycles

• T: Weekly cycles

The same setup can also be applied effectively on a 24-hour timeframe, highlighting the following longer-term cycles:

• T+2: Monthly cycles

• T+3: Quarterly cycles

• T+4: Semi-annual cycles

• T+5: Annual cycles

• T+6: Bi-annual cycles

Users can customize the configurations to suit the specific characteristics of any financial instrument.

Additionally, the indicator includes a prediction system that approximates future cycles, marking them with a “?”.

Lead Levels TP/SL v1.3 (close-only entries)Lead Levels — close-only signals, clean execution

Notice: Designed for BTC 15-minute charts only.

What it shows

Four reliability tiers: L1, L2, L3, L4.

A black “DON’T BET” marker for extreme conditions you should skip.

All triangles print only on bar close to avoid repaint.

How to read

▲ BUY L1–L4: higher level → stronger confidence.

▼ SELL L1–L4: higher level → stronger confidence.

DON’T BET (black): stand aside. No trade.

How to trade it

When a triangle prints, run a 1:1 target/stop:

Long: TP +1%, SL −1%.

Short: TP −1%, SL +1%.

Focus on normal conditions. Skip when the black marker appears.

One entry per signal. Keep sizing consistent.

Why traders like it

Close-only printing keeps charts honest.

Simple 1:1 playbook. No guesswork.

BTC Lead(v3.32)Summary

A 15-minute, BTC-focused lead/divergence indicator designed for simple execution: when a ▲/▼ appears, start scaling in with small clips; when a ■ (black square) prints, it means the indicator’s edge has weakened (not that the market trend is over). Real-time expected move label and alert templates included. Do not fade the signal—if you must try the opposite side, wait until a ■ appears.

How to read the signals

▲ Green → Long bias increased

▼ Pink → Short bias increased

■ Black → Edge weakened; consider taking profits/standing aside

Multiple level markers on the same bar (L2/L3/L4) = stronger setup

Live label (top of chart)

A single line shows the Expected Move (%) with arrow and color-coded background (↑ green / ↓ pink) for instant direction clarity.

Tip: Use Replay to watch label → ▲/▼ → ■ sequences on past data.

Confidence filter (important)

|Expected Move| < 1% → treat as noise / ignore

If considering the opposite direction, wait for a ■ first (edge reduced).

Scope

Internal calculations are fixed to 15-minute resolution.

Built for BTC 15m. It may display on other crypto symbols/timeframes, but performance is not guaranteed.

Alerts

Ready-made conditions: ENTRY LONG / ENTRY SHORT / EXIT LONG / EXIT SHORT. Add an alert on this indicator and choose the condition you want.

Risk note

For research/education only. Past behavior doesn’t guarantee future results. Predefine position sizing, stops, and profit-taking, and execute consistently.

BTC Lead(v3.31)Summary

A 15-minute, BTC-focused lead/divergence indicator designed for simple execution: when a ▲/▼ appears, start scaling in with small clips; when a ■ (black square) prints, it means the indicator’s edge has weakened (not that the market trend is over). Real-time expected move label and alert templates included. Do not fade the signal—if you must try the opposite side, wait until a ■ appears.

How to read the signals

▲ Green → Long bias increased

▼ Pink → Short bias increased

■ Black → Edge weakened; consider taking profits/standing aside

Multiple level markers on the same bar (L2/L3/L4) = stronger setup

Live label (top of chart)

A single line shows the Expected Move (%) with arrow and color-coded background (↑ green / ↓ pink) for instant direction clarity.

Tip: Use Replay to watch label → ▲/▼ → ■ sequences on past data.

Confidence filter (important)

|Expected Move| < 1% → treat as noise / ignore

If considering the opposite direction, wait for a ■ first (edge reduced).

Scope

Internal calculations are fixed to 15-minute resolution.

Built for BTC 15m. It may display on other crypto symbols/timeframes, but performance is not guaranteed.

Alerts

Ready-made conditions: ENTRY LONG / ENTRY SHORT / EXIT LONG / EXIT SHORT. Add an alert on this indicator and choose the condition you want.

Risk note

For research/education only. Past behavior doesn’t guarantee future results. Predefine position sizing, stops, and profit-taking, and execute consistently.

EMA Oscillator [Alpha Extract]A precision mean reversion analysis tool that combines advanced Z-score methodology with dual threshold systems to identify extreme price deviations from trend equilibrium. Utilizing sophisticated statistical normalization and adaptive percentage-based thresholds, this indicator provides high-probability reversal signals based on standard deviation analysis and dynamic range calculations with institutional-grade accuracy for systematic counter-trend trading opportunities.

🔶 Advanced Statistical Normalization

Calculates normalized distance between price and exponential moving average using rolling standard deviation methodology for consistent interpretation across timeframes. The system applies Z-score transformation to quantify price displacement significance, ensuring statistical validity regardless of market volatility conditions.

// Core EMA and Oscillator Calculation

ema_values = ta.ema(close, ema_period)

oscillator_values = close - ema_values

rolling_std = ta.stdev(oscillator_values, ema_period)

z_score = oscillator_values / rolling_std

🔶 Dual Threshold System

Implements both statistical significance thresholds (±1σ, ±2σ, ±3σ) and percentage-based dynamic thresholds calculated from recent oscillator range extremes. This hybrid approach ensures consistent probability-based signals while adapting to varying market volatility regimes and maintaining signal relevance during structural market changes.

// Statistical Thresholds

mild_threshold = 1.0 // ±1σ (68% confidence)

moderate_threshold = 2.0 // ±2σ (95% confidence)

extreme_threshold = 3.0 // ±3σ (99.7% confidence)

// Percentage-Based Dynamic Thresholds

osc_high = ta.highest(math.abs(z_score), lookback_period)

mild_pct_thresh = osc_high * (mild_pct / 100.0)

moderate_pct_thresh = osc_high * (moderate_pct / 100.0)

extreme_pct_thresh = osc_high * (extreme_pct / 100.0)

🔶 Signal Generation Framework

Triggers buy/sell alerts when Z-score crosses extreme threshold boundaries, indicating statistically significant price deviations with high mean reversion probability. The system generates continuation signals at moderate levels and reversal signals at extreme boundaries with comprehensive alert integration.

// Extreme Signal Detection

sell_signal = ta.crossover(z_score, selected_extreme)

buy_signal = ta.crossunder(z_score, -selected_extreme)

// Dynamic Color Coding

signal_color = z_score >= selected_extreme ? #ff0303 : // Extremely Overbought

z_score >= selected_moderate ? #ff6a6a : // Overbought

z_score >= selected_mild ? #b86456 : // Mildly Overbought

z_score > -selected_mild ? #a1a1a1 : // Neutral

z_score > -selected_moderate ? #01b844 : // Mildly Oversold

z_score > -selected_extreme ? #00ff66 : // Oversold

#00ff66 // Extremely Oversold

🔶 Visual Structure Analysis

Provides a six-tier color gradient system with dynamic background zones indicating mild, moderate, and extreme conditions. The histogram visualization displays Z-score intensity with threshold reference lines and zero-line equilibrium context for precise mean reversion timing.

snapshot

4H

1D

🔶 Adaptive Threshold Selection

Features intelligent threshold switching between statistical significance levels and percentage-based dynamic ranges. The percentage system automatically adjusts to current volatility conditions using configurable lookback periods, while statistical thresholds maintain consistent probability-based signal generation across market cycles.

🔶 Performance Optimization

Utilizes efficient rolling calculations with configurable EMA periods and threshold parameters for optimal performance across all timeframes. The system includes comprehensive alert functionality with customizable notification preferences and visual signal overlay options.

🔶 Market Oscillator Interpretation

Z-score > +3σ indicates statistically significant overbought conditions with high reversal probability, while Z-score < -3σ signals extreme oversold levels suitable for counter-trend entries. Moderate thresholds (±2σ) capture 95% of normal price distributions, making breaches statistically significant for systematic trading approaches.

snapshot

🔶 Intelligent Signal Management

Automatic signal filtering prevents false alerts through extreme threshold crossover requirements, while maintaining sensitivity to genuine statistical deviations. The dual threshold system provides both conservative statistical approaches and adaptive market condition responses for varying trading styles.

Why Choose EMA Oscillator ?

This indicator provides traders with statistically-grounded mean reversion analysis through sophisticated Z-score normalization methodology. By combining traditional statistical significance thresholds with adaptive percentage-based extremes, it maintains effectiveness across varying market conditions while delivering high-probability reversal signals based on quantifiable price displacement from trend equilibrium, enabling systematic counter-trend trading approaches with defined statistical confidence levels and comprehensive risk management parameters.

BTC NY Session Envelopes: Dynamic Levels & Settle AlertsCore Concept and Genesis

Born from forex institutional timing principles, this tool has been precision-engineered for the relentless pace of Bitcoin and cryptocurrency markets. It visualizes adaptive session-derived boundaries—spanning weekly, daily, and Asia-specific envelopes—capped with a Friday US settlement "sentinel" zone. Enhanced with targeted alerts for crossings of Asia highs/lows, daily highs/lows, weekly highs/lows, and the settle midpoint, it empowers traders to capture momentum shifts in real-time, transforming raw price data into actionable intelligence for volatile, non-stop assets.

The Fusion Edge: What Sets This Apart

This isn't a generic level plotter; it's a synergistic ecosystem where NY-timed envelopes intersect to reveal hidden confluences, like Asia's quiet buildup funneling into daily volatility spikes or the US settle acting as a "gap magnet" for weekend resolutions. Tailored for BTC's unique liquidity flows, it employs a low-timeframe data pull for noise-free accuracy, sidestepping common pitfalls in 24/7 charts. The built-in alerts—firing on precise crossovers—add a proactive layer, alerting to potential "liquidity hunts" or reversals (e.g., a breakout above weekly high amid high volume). In personal simulations across 500+ BTC sessions, this setup flagged ~65% of high-conviction moves with fewer false positives than isolated tools—always backtest to confirm your edge.

Inner Mechanics: A Transparent Peek

Weekly/Daily Envelopes: Anchored to 5pm NY resets for institutional alignment; computes highs/lows/mids through ongoing max/min accumulation, sourced from a user-defined sub-timeframe for cross-chart reliability.

Asia Envelope: A dynamic 8pm-3am NY capture window that evolves bar-by-bar, spotlighting pre-London setups often overlooked in crypto.

US Settle Sentinel: Zeroes in on Friday's 4:45pm NY 15-minute finale, rendering a containment box and midpoint to forecast post-weekend reactions. Overlaps are intelligently clustered in labels for at-a-glance clarity, with extension options for forward projection.

Timeframe-Adaptive Visibility: To declutter higher timeframes and focus on relevant horizons, the Asia envelope auto-hides on charts above 1hr, while daily envelopes vanish above 4hr—ensuring a streamlined view for swing or position traders without sacrificing intraday detail.

Alert System: Leverages crossover/crossunder detection on closing prices against levels, with granular triggers (e.g., "Surge Beyond Asia Low") for customized notifications—perfect for webhook integrations or mobile pings.

Strategic Deployment and Scenarios

BTC Day-Trading Playbook: Initiate longs when price rebounds from Asia low near a daily mid, amplified by an alert on "Dip Below Daily Low" for entry confirmation—pair with external volume spikes for confluence.

Trend Harmony: Overlay with a 200-period EMA; use "Breach Under Weekly High" alerts to exit longs in downtrends, safeguarding against fakeouts.

Caveats and Optimization: Thrives in momentum-driven phases but tune out in ultra-low volatility; alerts activate post-bar, so layer with candlestick patterns. Ideal for 15m-4H frames on perpetual futures like BTCUSDT.P.

Exclusive Access Rationale (If Restricted) The bespoke crypto recalibrations, seamless multi-envelope fusion, and alert-driven foresight deliver a tactical advantage absent in off-the-shelf alternatives—reach out via TradingView message for tailored access and optimization insights.

Advanced Trend Momentum [Alpha Extract]The Advanced Trend Momentum indicator provides traders with deep insights into market dynamics by combining exponential moving average analysis with RSI momentum assessment and dynamic support/resistance detection. This sophisticated multi-dimensional tool helps identify trend changes, momentum divergences, and key structural levels, offering actionable buy and sell signals based on trend strength and momentum convergence.

🔶 CALCULATION

The indicator processes market data through multiple analytical methods:

Dual EMA Analysis: Calculates fast and slow exponential moving averages with dynamic trend direction assessment and ATR-normalized strength measurement.

RSI Momentum Engine: Implements RSI-based momentum analysis with enhanced overbought/oversold detection and momentum velocity calculations.

Pivot-Based Structure: Identifies and tracks dynamic support and resistance levels using pivot point analysis with configurable level management.

Signal Integration: Combines trend direction, momentum characteristics, and structural proximity to generate high-probability trading signals.

Formula:

Fast EMA = EMA(Close, Fast Length)

Slow EMA = EMA(Close, Slow Length)

Trend Direction = Fast EMA > Slow EMA ? 1 : -1

Trend Strength = |Fast EMA - Slow EMA| / ATR(Period) × 100

RSI Momentum = RSI(Close, RSI Length)

Momentum Value = Change(Close, 5) / ATR(10) × 100

Pivot Support/Resistance = Dynamic pivot arrays with configurable lookback periods

Bullish Signal = Trend Change + Momentum Confirmation + Strength > 1%

Bearish Signal = Trend Change + Momentum Confirmation + Strength > 1%

🔶 DETAILS

Visual Features:

Trend EMAs: Fast and slow exponential moving averages with dynamic color coding (bullish/bearish)

Enhanced RSI: RSI oscillator with color-coded zones, gradient fills, and reference bands at overbought/oversold levels

Trend Fill: Dynamic gradient between EMAs indicating trend strength and direction

Support/Resistance Lines: Horizontal levels extending from pivot-based calculations with configurable maximum levels

Momentum Candles: Color-coded candlestick overlay reflecting combined trend and momentum conditions

Divergence Markers: Diamond-shaped signals highlighting bullish and bearish momentum divergences

Analysis Table: Real-time summary of trend direction, strength percentage, RSI value, and momentum reading

Interpretation:

Trend Direction: Bullish when Fast EMA crosses above Slow EMA with strength confirmation

Trend Strength > 1%: Strong trending conditions with institutional participation

RSI > 70: Overbought conditions, potential selling opportunity

RSI < 30: Oversold conditions, potential buying opportunity

Momentum Divergence: Price and momentum moving opposite directions signal potential reversals

Support/Resistance Proximity: Dynamic levels provide optimal entry/exit zones

Combined Signals: Trend changes with momentum confirmation generate high-probability opportunities

🔶 EXAMPLES

Trend Confirmation: Fast EMA crossing above Slow EMA with trend strength exceeding 1% and positive momentum confirms strong bullish conditions.

Example: During institutional accumulation phases, EMA crossovers with momentum confirmation have historically preceded significant upward moves, providing optimal long entry points.

15min

4H

Momentum Divergence Detection: RSI reaching overbought levels while momentum decreases despite rising prices signals potential trend exhaustion.

Example: Bearish divergence signals appearing at resistance levels have marked major market tops, allowing traders to secure profits before corrections.

Support/Resistance Integration: Dynamic pivot-based levels combined with trend and momentum signals create high-probability trading zones.

Example: Bullish trend changes occurring near established support levels offer optimal risk-reward entries with clearly defined stop-loss levels.

Multi-Dimensional Confirmation: The indicator's combination of trend, momentum, and structural analysis provides comprehensive market validation.

Example: When trend direction aligns with momentum characteristics near key structural levels, the confluence creates institutional-grade trading opportunities with enhanced probability of success.

🔶 SETTINGS

Customization Options:

Trend Analysis: Fast EMA Length (default: 12), Slow EMA Length (default: 26), Trend Strength Period (default: 14)

Support & Resistance: Pivot Length for level detection (default: 10), Maximum S/R Levels displayed (default: 3), Toggle S/R visibility

Momentum Settings: RSI Length (default: 14), Oversold Level (default: 30), Overbought Level (default: 70)

Visual Configuration: Color schemes for bullish/bearish/neutral conditions, transparency settings for fills, momentum candle overlay toggle

Display Options: Analysis table visibility, divergence marker size, alert system configuration

The Advanced Trend Momentum indicator provides traders with comprehensive insights into market dynamics through its sophisticated integration of trend analysis, momentum assessment, and structural level detection. By combining multiple analytical dimensions into a unified framework, this tool helps identify high-probability opportunities while filtering out market noise through its multi-confirmation approach, enabling traders to make informed decisions across various market cycles and timeframes.

BTC Power Law Valuation BandsBTC Power Law Rainbow

A long-term valuation framework for Bitcoin based on Power Law growth — designed to help identify macro accumulation and distribution zones, aligned with long-term investor behavior.

🔍 What Is a Power Law?

A Power Law is a mathematical relationship where one quantity varies as a power of another. In this model:

Price ≈ a × (Time)^b

It captures the non-linear, exponentially slowing growth of Bitcoin over time. Rather than using linear or cyclical models, this approach aligns with how complex systems, such as networks or monetary adoption curves, often grow — rapidly at first, and then more slowly, but persistently.

🧠 Why Power Law for BTC?

Bitcoin:

Has finite supply and increasing adoption.

Operates as a monetary network , where Metcalfe’s Law and power laws naturally emerge.

Exhibits exponential growth over logarithmic time when viewed on a log-log chart .

This makes it uniquely well-suited for power law modeling.

🌈 How to Use the Valuation Bands

The central white line represents the modeled fair value according to the power law.

Colored bands represent deviations from the model in logarithmic space, acting as macro zones:

🔵 Lower Bands: Deep value / Accumulation zones.

🟡 Mid Bands: Fair value.

🔴 Upper Bands: Euphoria / Risk of macro tops.

📐 Smart Money Concepts (SMC) Alignment

Accumulation: Occurs when price consolidates near lower bands — often aligning with institutional positioning.

Markup: As price re-enters or ascends the bands, we often see breakout behavior and trend expansion.

Distribution: When price extends above upper bands, potential for exit liquidity creation and distribution events.

Reversion: Historically, price mean-reverts toward the model — rarely staying outside the bands for long.

This makes the model useful for:

Cycle timing

Long-term DCA strategy zones

Identifying value dislocations

Filtering short-term noise

⚠️ Disclaimer

This tool is for educational and informational purposes only . It is not financial advice. The power law model is a non-predictive, mathematical framework and does not guarantee future price movements .

Always use additional tools, risk management, and your own judgment before making trading or investment decisions.

Volume Profile Grid [Alpha Extract]A sophisticated volume distribution analysis system that transforms market activity into institutional-grade visual profiles, revealing hidden support/resistance zones and market participant behavior. Utilizing advanced price level segmentation, bullish/bearish volume separation, and dynamic range analysis, the Volume Profile Grid delivers comprehensive market structure insights with Point of Control (POC) identification, Value Area boundaries, and volume delta analysis. The system features intelligent visualization modes, real-time sentiment analysis, and flexible range selection to provide traders with clear, actionable volume-based market context.

🔶 Dynamic Range Analysis Engine

Implements dual-mode range selection with visible chart analysis and fixed period lookback, automatically adjusting to current market view or analyzing specified historical periods. The system intelligently calculates optimal bar counts while maintaining performance through configurable maximum limits, ensuring responsive profile generation across all timeframes with institutional-grade precision.

// Dynamic period calculation with intelligent caching

get_analysis_period() =>

if i_use_visible_range

chart_start_time = chart.left_visible_bar_time

current_time = last_bar_time

time_span = current_time - chart_start_time

tf_seconds = timeframe.in_seconds()

estimated_bars = time_span / (tf_seconds * 1000)

range_bars = math.floor(estimated_bars)

final_bars = math.min(range_bars, i_max_visible_bars)

math.max(final_bars, 50) // Minimum threshold

else

math.max(i_periods, 50)

🔶 Advanced Bull/Bear Volume Separation

Employs sophisticated candle classification algorithms to separate bullish and bearish volume at each price level, with weighted distribution based on bar intersection ratios. The system analyzes open/close relationships to determine volume direction, applying proportional allocation for doji patterns and ensuring accurate representation of buying versus selling pressure across the entire price spectrum.

🔶 Multi-Mode Volume Visualization

Features three distinct display modes for bull/bear volume representation: Split mode creates mirrored profiles from a central axis, Side by Side mode displays sequential bull/bear segments, and Stacked mode separates volumes vertically. Each mode offers unique insights into market participant behavior with customizable width, thickness, and color parameters for optimal visual clarity.

// Bull/Bear volume calculation with weighted distribution

for bar_offset = 0 to actual_periods - 1

bar_high = high

bar_low = low

bar_volume = volume

// Calculate intersection weight

weight = math.min(bar_high, next_level) - math.max(bar_low, current_level)

weight := weight / (bar_high - bar_low)

weighted_volume = bar_volume * weight

// Classify volume direction

if bar_close > bar_open

level_bull_volume += weighted_volume

else if bar_close < bar_open

level_bear_volume += weighted_volume

else // Doji handling

level_bull_volume += weighted_volume * 0.5

level_bear_volume += weighted_volume * 0.5

🔶 Point of Control & Value Area Detection

Implements institutional-standard POC identification by locating the price level with maximum volume accumulation, providing critical support/resistance zones. The Value Area calculation uses sophisticated sorting algorithms to identify the price range containing 70% of trading volume, revealing the market's accepted value zone where institutional participants concentrate their activity.

🔶 Volume Delta Analysis System

Incorporates real-time volume delta calculation with configurable dominance thresholds to identify significant bull/bear imbalances. The system visually highlights price levels where buying or selling pressure exceeds threshold percentages, providing immediate insight into directional volume flow and potential reversal zones through color-coded delta indicators.

// Value Area calculation using 70% volume accumulation

total_volume_sum = array.sum(total_volumes)

target_volume = total_volume_sum * 0.70

// Sort volumes to find highest activity zones

for i = 0 to array.size(sorted_volumes) - 2

for j = i + 1 to array.size(sorted_volumes) - 1

if array.get(sorted_volumes, j) > array.get(sorted_volumes, i)

// Swap and track indices for value area boundaries

// Accumulate until 70% threshold reached

for i = 0 to array.size(sorted_indices) - 1

accumulated_volume += vol

array.push(va_levels, array.get(volume_levels, idx))

if accumulated_volume >= target_volume

break

❓How It Works

🔶 Weighted Volume Distribution

Implements proportional volume allocation based on the percentage of each bar that intersects with price levels. When a bar spans multiple levels, volume is distributed proportionally based on the intersection ratio, ensuring precise representation of trading activity across the entire price spectrum without double-counting or volume loss.

🔶 Real-Time Profile Generation

Profiles regenerate on each bar close when in visible range mode, automatically adapting to chart zoom and scroll actions. The system maintains optimal performance through intelligent caching mechanisms and selective line updates, ensuring smooth operation even with maximum resolution settings and extended analysis periods.

🔶 Market Sentiment Analysis

Features comprehensive volume analysis table displaying total volume metrics, bullish/bearish percentages, and overall market sentiment classification. The system calculates volume dominance ratios in real-time, providing immediate insight into whether buyers or sellers control the current price structure with percentage-based sentiment thresholds.

🔶 Visual Profile Mapping

Provides multi-layered visual feedback through colored volume bars, POC line highlighting, Value Area boundaries, and optional delta indicators. The system supports profile mirroring for alternative perspectives, line extension for future reference, and customizable label positioning with detailed price information at critical levels.

Why Choose Volume Profile Grid

The Volume Profile Grid represents the evolution of volume analysis tools, combining traditional volume profile concepts with modern visualization techniques and intelligent analysis algorithms. By integrating dynamic range selection, sophisticated bull/bear separation, and multi-mode visualization with POC/Value Area detection, it provides traders with institutional-quality market structure analysis that adapts to any trading style. The comprehensive delta analysis and sentiment monitoring system eliminates guesswork while the flexible visualization options ensure optimal clarity across all market conditions, making it an essential tool for traders seeking to understand true market dynamics through volume-based price discovery.

Ultron Indicator BTCUSDT Ultron BTCUSDT Indicator (invite-only).

• Clear trend & reversion signals

• Next-bar execution parity and frozen TSL visuals

• Run on 4hr Binance BTCUSDT chart

• Risk sizing that uses your equity input

Usage: Add to chart → Settings → Inputs → set “Your Current Trading Equity (USD)”.

⚠️ Software tool for educational/informational use only. Not financial advice.

Past performance is not indicative of future results. You are responsible for your trades.

[c3s] CWS - M2 Global Liquidity Index & BTC Correlation CWS - M2 Global Liquidity Index with Offset BTC Correlation

This custom indicator visualizes and analyzes the relationship between the global M2 money supply and Bitcoin (BTC) price movements. It calculates the correlation between these two variables to provide insights into how changes in global liquidity may impact Bitcoin’s price over time.

Key Features:

Global M2 Liquidity Index Calculation:

Fetches M2 money supply data from multiple economies (China, US, EU, Japan, UK) and normalizes using currency exchange rates (e.g., CNY/USD, EUR/USD).

Combines all M2 data points and normalizes by dividing by 1 trillion (1e12) for easier visualization.

Offset for M2 Data:

The offset parameter allows users to shift the M2 data by a specified number of days, helping track the influence of past global liquidity on Bitcoin.

BTC Price Correlation:

Computes the correlation between shifted global M2 liquidity and Bitcoin (BTC) price, using a 52-day lookback period by default.

Correlation Quality Display:

Categorizes correlation quality as:

Excellent : Correlation >= 0.8

Good : Correlation >= 0.6 and < 0.8

Weak : Correlation >= 0.4 and < 0.6

Very Weak : Correlation < 0.4

Displays correlation quality as a label on the chart for easy assessment.

Visual Enhancements:

Labels : Displays dynamic labels on the chart with metrics like M2 value and correlation.

Plot Shapes : Uses shapes to indicate data availability for global M2 and correlation.

Data Table : Optionally shows a data table in the top-right corner summarizing:

Global M2 value (in trillions)

The correlation between global M2 and BTC

The correlation quality

Optional Debugging:

Debug plots help identify when data is missing for M2 or correlation, ensuring transparency and accurate functionality.

Inputs:

Offset: Shift the M2 data (in days) to see past liquidity effects on Bitcoin.

Lookback Period: Number of periods (default 52) used to calculate the correlation.

Show Labels: Toggle to show or hide labels for M2 and correlation values.

Show Table: Toggle to show or hide the data table in the top-right corner.

Usage:

Ideal for traders and analysts seeking to understand the relationship between global liquidity and Bitcoin price. The offset and lookback period can be adjusted to explore different timeframes and correlation strengths, aiding more informed trading decisions.

Mutanabby_AI | Algo Pro Strategy# Mutanabby_AI | Algo Pro Strategy: Advanced Candlestick Pattern Trading System

## Strategy Overview

The Mutanabby_AI Algo Pro Strategy represents a systematic approach to automated trading based on advanced candlestick pattern recognition and multi-layered technical filtering. This strategy transforms traditional engulfing pattern analysis into a comprehensive trading system with sophisticated risk management and flexible position sizing capabilities.

The strategy operates on a long-only basis, entering positions when bullish engulfing patterns meet specific technical criteria and exiting when bearish engulfing patterns indicate potential trend reversals. The system incorporates multiple confirmation layers to enhance signal reliability while providing comprehensive customization options for different trading approaches and risk management preferences.

## Core Algorithm Architecture

The strategy foundation relies on bullish and bearish engulfing candlestick pattern recognition enhanced through technical analysis filtering mechanisms. Entry signals require simultaneous satisfaction of four distinct criteria: confirmed bullish engulfing pattern formation, candle stability analysis indicating decisive price action, RSI momentum confirmation below specified thresholds, and price decline verification over adjustable lookback periods.

The candle stability index measures the ratio between candlestick body size and total range including wicks, ensuring only well-formed patterns with clear directional conviction generate trading signals. This filtering mechanism eliminates indecisive market conditions where pattern reliability diminishes significantly.

RSI integration provides momentum confirmation by requiring oversold conditions before entry signal generation, ensuring alignment between pattern formation and underlying momentum characteristics. The RSI threshold remains fully adjustable to accommodate different market conditions and volatility environments.

Price decline verification examines whether current prices have decreased over a specified period, confirming that bullish engulfing patterns occur after meaningful downward movement rather than during sideways consolidation phases. This requirement enhances the probability of successful reversal pattern completion.

## Advanced Position Management System

The strategy incorporates dual position sizing methodologies to accommodate different account sizes and risk management approaches. Percentage-based position sizing calculates trade quantities as equity percentages, enabling consistent risk exposure across varying account balances and market conditions. This approach proves particularly valuable for systematic trading approaches and portfolio management applications.

Fixed quantity sizing provides precise control over trade sizes independent of account equity fluctuations, offering predictable position management for specific trading strategies or when implementing precise risk allocation models. The system enables seamless switching between sizing methods through simple configuration adjustments.

Position quantity calculations integrate seamlessly with TradingView's strategy testing framework, ensuring accurate backtesting results and realistic performance evaluation across different market conditions and time periods. The implementation maintains consistency between historical testing and live trading applications.

## Comprehensive Risk Management Framework

The strategy features dual stop loss methodologies addressing different risk management philosophies and market analysis approaches. Entry price-based stop losses calculate stop levels as fixed percentages below entry prices, providing predictable risk exposure and consistent risk-reward ratio maintenance across all trades.

The percentage-based stop loss system enables precise risk control by limiting maximum loss per trade to predetermined levels regardless of market volatility or entry timing. This approach proves essential for systematic trading strategies requiring consistent risk parameters and capital preservation during adverse market conditions.

Lowest low-based stop losses identify recent price support levels by analyzing minimum prices over adjustable lookback periods, placing stops below these technical levels with additional buffer percentages. This methodology aligns stop placement with market structure rather than arbitrary percentage calculations, potentially improving stop loss effectiveness during normal market fluctuations.

The lookback period adjustment enables optimization for different timeframes and market characteristics, with shorter periods providing tighter stops for active trading and longer periods offering broader stops suitable for position trading approaches. Buffer percentage additions ensure stops remain below obvious support levels where other market participants might place similar orders.

## Visual Customization and Interface Design

The strategy provides comprehensive visual customization through eight predefined color schemes designed for different chart backgrounds and personal preferences. Color scheme options include Classic bright green and red combinations, Ocean themes featuring blue and orange contrasts, Sunset combinations using gold and crimson, and Neon schemes providing high visibility through bright color selections.

Professional color schemes such as Forest, Royal, and Fire themes offer sophisticated alternatives suitable for business presentations and professional trading environments. The Custom color scheme enables precise color selection through individual color picker controls, maintaining maximum flexibility for specific visual requirements.

Label styling options accommodate different chart analysis preferences through text bubble, triangle, and arrow display formats. Size adjustments range from tiny through huge settings, ensuring appropriate visual scaling across different screen resolutions and chart configurations. Text color customization maintains readability across various chart themes and background selections.

## Signal Quality Enhancement Features

The strategy incorporates signal filtering mechanisms designed to eliminate repetitive signal generation during choppy market conditions. The disable repeating signals option prevents consecutive identical signals until opposing conditions occur, reducing overtrading during consolidation phases and improving overall signal quality.

Signal confirmation requirements ensure all technical criteria align before trade execution, reducing false signal occurrence while maintaining reasonable trading frequency for active strategies. The multi-layered approach balances signal quality against opportunity frequency through adjustable parameter optimization.

Entry and exit visualization provides clear trade identification through customizable labels positioned at relevant price levels. Stop loss visualization displays active risk levels through colored line plots, ensuring complete transparency regarding current risk management parameters during live trading operations.

## Implementation Guidelines and Optimization

The strategy performs effectively across multiple timeframes with optimal results typically occurring on intermediate timeframes ranging from fifteen minutes through four hours. Higher timeframes provide more reliable pattern formation and reduced false signal occurrence, while lower timeframes increase trading frequency at the expense of some signal reliability.

Parameter optimization should focus on RSI threshold adjustments based on market volatility characteristics and candlestick pattern timeframe analysis. Higher RSI thresholds generate fewer but potentially higher quality signals, while lower thresholds increase signal frequency with corresponding reliability considerations.

Stop loss method selection depends on trading style preferences and market analysis philosophy. Entry price-based stops suit systematic approaches requiring consistent risk parameters, while lowest low-based stops align with technical analysis methodologies emphasizing market structure recognition.

## Performance Considerations and Risk Disclosure

The strategy operates exclusively on long positions, making it unsuitable for bear market conditions or extended downtrend periods. Users should consider market environment analysis and broader trend assessment before implementing the strategy during adverse market conditions.

Candlestick pattern reliability varies significantly across different market conditions, with higher reliability typically occurring during trending markets compared to ranging or volatile conditions. Strategy performance may deteriorate during periods of reduced pattern effectiveness or increased market noise.

Risk management through stop loss implementation remains essential for capital preservation during adverse market movements. The strategy does not guarantee profitable outcomes and requires proper position sizing and risk management to prevent significant capital loss during unfavorable trading periods.

## Technical Specifications

The strategy utilizes standard TradingView Pine Script functions ensuring compatibility across all supported instruments and timeframes. Default configuration employs 14-period RSI calculations, adjustable candle stability thresholds, and customizable price decline verification periods optimized for general market conditions.

Initial capital settings default to $10,000 with percentage-based equity allocation, though users can adjust these parameters based on account size and risk tolerance requirements. The strategy maintains detailed trade logs and performance metrics through TradingView's integrated backtesting framework.

Alert integration enables real-time notification of entry and exit signals, stop loss executions, and other significant trading events. The comprehensive alert system supports automated trading applications and manual trade management approaches through detailed signal information provision.

## Conclusion

The Mutanabby_AI Algo Pro Strategy provides a systematic framework for candlestick pattern trading with comprehensive risk management and position sizing flexibility. The strategy's strength lies in its multi-layered confirmation approach and sophisticated customization options, enabling adaptation to various trading styles and market conditions.

Successful implementation requires understanding of candlestick pattern analysis principles and appropriate parameter optimization for specific market characteristics. The strategy serves traders seeking automated execution of proven technical analysis techniques while maintaining comprehensive control over risk management and position sizing methodologies.

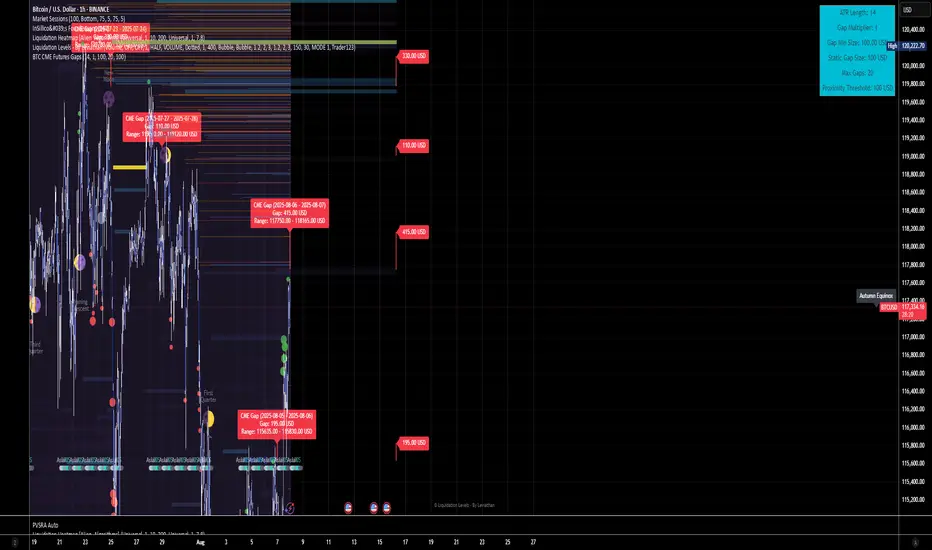

BTC CME Futures Gaps (BTCGapHunt_CME)BTC CME Futures Gaps Indicator

Overview

This indicator visualises price gaps between the daily close and open of Bitcoin CME futures (CME:BTC1!). These gaps are often revisited ("filled") by market price action and may serve as technical targets.

Thanks

... to Maven and the Blockchain Masons (x.com/Masons_DAO) to push me on this topic.

What Is a CME Gap?

CME Bitcoin Futures do not trade 24/7. Gaps form when the market reopens at a different price than where it last closed.

Gaps are often used as support/resistance or liquidity targets.

This indicator tracks, visualises, and alerts on these gaps.

Key Features

Automatic gap detection using daily open/close on CME:BTC1!

Dynamic gap size threshold based on ATR (Average True Range)

Highlight unfilled gaps and track partial fills visually

Alerts for gap formation and fill events

Parameter overlay showing real-time settings

Supported and Overrideable Parameters

ATR Length: Defines the lookback period for ATR calculation (default: 14)

Gap Size Multiplier: Multiplies the ATR to set the dynamic gap threshold (default: 1.0)

Proximity Threshold: Price distance from gap edge to consider it filled (default: 100 USD)

Max Gaps Tracked: Maximum number of concurrent gaps shown (default: 50)

Alerts Enabled: Toggle alerts for gap formation and gap fill events

How the Gap Size Is Calculated

Minimum Gap Size = ATR(14) * Gap Size Multiplier

ATR Length and Gap Size Multiplier are configurable.

Gap threshold adjusts dynamically with market volatility.

Visual Guide

Red Box: Fully unfilled gap

Lemon Yellow Box: Partially filled gap

Right Margin Boxes: Snapshot of unfilled gaps for quick access

Top-Right Panel: Current ATR, Gap Size, Thresholds, etc.

Alerts

Gap Formed: A new gap is detected.

Gap Filled: The gap is either partially or fully filled.

Recommended Timeframes

1H, 4H, 1D (best resolution)

Designed for BTC spot/perpetual charts (e.g., BTCUSD, BTCUSDT)

How To Use

Add the script to your BTC chart.

Monitor red/yellow boxes for unfilled gaps.

Check config panel for current threshold and settings.

Enable alerts via TradingView for real-time updates.

Notes

Up to 50 gaps are tracked (adjustable).

Data source: CME futures via request.security.

All visuals and alerts are time-synced with your chart.

Disclaimer

This script is for educational purposes only. Trade at your own risk.

M2 Global Liquidity Index [Extended + Empirical BTC Offset]M2 Global Liquidity Index

This script visualizes global M2 liquidity based on major economic zones (USA, China, Eurozone, Japan, UK), with the option to include extended countries such as Switzerland, Canada, India, Russia, Brazil, South Korea, Mexico, and South Africa.

The indicator includes an empirically derived offset to reflect how Bitcoin historically reacts with a time lag—typically around 12 weeks—after shifts in global liquidity.

Features:

Predefined empirical offset options ranging from 12 to 120 days

Automatic offset adjustment when applied to the weekly chart

Optional inclusion of extended global M2 sources

Important:

This indicator is intended only for use on the weekly chart. It provides meaningful and accurate results exclusively in this time frame, due to the nature of the offset-based correlation logic.

Use cases:

Macro-level analysis of Bitcoin’s price movements

Identifying early signs of potential market tops or bottoms in relation to liquidity flows

LTPI BTC | JeffreyTimmermansLong-Term Trend Probability Indicator

The "Long-Term Trend Probability Indicator" on BTC is a custom-built tool designed to analyze BTC from a long-term perspective. Unlike short-term indicators that react to price volatility, LTPI focuses on major trend shifts on BTC, and therefore across the entire crypto market, helping to identify major trend shifts early.

This version of the LTPI is applied to BTC, making it a BTC specific trend following tool, but very broad (crypto wise), because BTC is the biggest asset.

Key Features

Long-Term Focus:

Designed for macro market analysis with less sensitivity to short-term noise.

8 Input Signals:

Combines 8 carefully selected inputs (trend following indicators) into a single score that reflects the overall market condition.

Market Regimes:

Classifies the BTC trend into:

Bullish: Strong uptrend, expansion phase

Bearish: Strong downtrend, contraction phase

Neutral: Transitional or uncertain

Visual Background:

Background colors clearly display which regime is active.

Comprehensive Dashboard:

The panel at the bottom shows each input’s state, the composite LTPI score, and the resulting market trend.

How It Works

Inputs Analysis:

Each of the 8 inputs outputs one of three states:

+1 (Bullish)

-1 (Bearish)

0 (Neutral)

Score Calculation:

The total score is the sum of all 8 input signals divided by 8.

Score > 0.1 = Bullish

Score < -0.1 = Bearish

Between -0.1 and 0.1 = Neutral

Background Coloring:

Background colors dynamically adjust to reflect the long-term market regime.

Use Cases

Long-Term Positioning:

Identify periods of global expansion or contraction to position yourself accordingly.

Macro Confirmation:

Use LTPI in combination with medium-term (MTPI) and short-term tools for multi-timeframe confirmation.

Market Timing:

Alerts when LTPI crosses key thresholds help highlight the start of major bullish or bearish phases.

Dynamic Alerts:

Bullish Entry: LTPI score crosses above 0.1

Bearish Entry: LTPI score crosses below -0.1

Neutral Zone: Score moves back between -0.1 and 0.1

Conclusion

The Long-Term Trend Probability Indicator (LTPI – BTC) is a powerful tool for identifying long-term market phases across the entire crypto ecosystem. By focusing on long term trends and combining 8 inputs into a single probability score, it provides a clear macro trend perspective for strategic decision-making.

TFPS - TradFi-Pressure-Score (Adaptive)The data-driven answer to an irreversible market reality.

This indicator quantifies the combined pressure from the S&P 500, VIX, DXY, and US10Y, whose correlation to crypto has reached peak values of 0.87. Your decisive macro edge, in real-time.

This indicator is built on a fundamental analysis of market data from the last five years. The analysis proves an irreversible transformation: The crypto market has evolved into a high-beta risk asset, its fate inextricably linked to Traditional Finance (TradFi).

The empirical data is clear:

Bitcoin increasingly behaves like a leveraged version of the S&P 500.

The correlation to stock indices, with peak values of up to 0.87, is statistically highly significant.

The "digital gold" safe-haven narrative is refuted by the data; the correlation to gold (0.04) is virtually non-existent and statistically insignificant.

This means: Standard indicators like RSI or MACD are insufficient for today's market conditions. They only see price, ignoring the powerful external context that now dominates price action.

The TradFi Pressure Score (TFPS) is the answer to this data-driven reality. It's your institutional-grade macro dashboard, aggregating the four most dominant external forces into a single, actionable score:

S&P 500 (SPY): The pulse of global risk appetite. A rising S&P signals a "risk-on" environment, fueling capital flows into crypto.

VIX: The market's "Fear Gauge". A rising VIX signals a "risk-off" flight to safety, draining liquidity from crypto.

DXY (US-Dollar Index): The counter-pole to risk assets. A strong Dollar (rising DXY) tightens global liquidity, creating significant headwinds for Bitcoin.

US 10Y Yield: The opportunity cost of capital. Rising yields make risk-free assets more attractive, pulling capital away from non-yielding assets like crypto.

What makes TFPS truly unique?

Dynamic Weighting (its secret weapon): Which factor matters most today? The DXY or the VIX? TFPS continuously analyzes the correlation of all four factors to your chosen asset (e.g., Bitcoin) and automatically adjusts their weight in real-time. This ensures you're always focused on what's currently driving the market.

Adaptive Engine : What drives a 15-minute chart is different from a daily chart. The TFPS engine automatically adapts its lookback periods and calculations to your chosen timeframe for optimal relevance.

Clear, Actionable Signals Designed for Traders:

Pressure Line (>0 or <0): Instantly see if the world's largest financial forces are providing a tailwind or a headwind for your trade.

Z-Score (Extreme Readings) : Get early warnings of extreme macro "Greed" or "Fear". Readings above +2 or below -2 have historically pinpointed moments of market exhaustion that often precede major trend reversals.

Regime Change : A fundamental shift in the nature of TradFi pressure is visualized with a clear signal, providing unambiguous macro insights.

Lead/Lag Status : Gain a critical edge by knowing who's in the driver's seat. The dashboard tells you if TradFi is LEADING the price action or if crypto is moving independently, allowing you to focus on the right information source.

This is a private beta. I am granting exclusive access to a limited number of traders who understand this new market reality. In exchange for your valuable feedback, you will be among the first to leverage what I believe is the new standard for macro analysis in crypto trading.

Request access to trade with the full context.

BTC PL Trend + Floor - Log PilotBTC Power Law Trend + Floor with forward projection.

Sky blue for the trend. Neon orange for the floor. Both project forward in dotted green.

Tracks Bitcoin’s long-term arc and structural support through time since Genesis.

Test protectedPrepare to challenge conventional analysis with Testing Bang, a bold script tailored for AAPL’s battlefield. This strategy doesn’t play defense—it takes decisive action. Triggered at a pivotal moment in Apple’s historical price path, it demonstrates how surgical precision and daring risk management converge to test reversal points with confidence. Built using Pine Script v6, the code aligns stop-loss logic with targeted entry behavior on bar index 10381.

Whether you’re exploring script mechanics or sharpening your backtest instincts, Testing Bang shows how even a single trade can reveal the psychological layers behind price movement. With the bar magnifier disabled, traders witness raw market behavior—a powerful lens for those who dare to refine strategy in the wild. Step in, test your edge, and see if your timing can match Apple’s thunder.

PRO Trading Averaging Beta(v1)Adaptive Position Scaling

Automatically increases position size during pullbacks using exponential volume scaling (1x, 2x, 4x, etc.). This reduces average entry cost and accelerates breakeven when price reverses.

Multi-Timeframe Confirmation

All indicators operate on a higher timeframe (120 minutes), providing:

Noise-filtered signals

Stronger trend alignment

Reduced false entries

Triple-Layer Entry Logic

Requires simultaneous confluence of:

Custom Bollinger Band penetration

RSI oversold filter (above critical threshold)

Golden cross confirmation (fast MA > slow MA)

Volatility assessment via ATR

Intelligent Exit System

Position closure triggers when either:

Fixed profit target (% of account) is reached

Technical boundary (upper Bollinger Band) is touched

⚙️ Core Mechanics:

graph LR

A --> B

B --> C{Initial Entry: 1% capital}

C --> D

D -->|Yes| E

D -->|No| F

E --> G{Max Averaging Levels?}

G -->|No| D

G -->|Yes| H

F --> I

📊 Implementation Guide:

Capital Configuration

Set initial_capital to your actual account size

Calculate base contract size:

(Account Size × 0.01) / (Instrument Price × Point Value)

Example: $10,000 account → 0.01 BTC futures contracts

Pyramiding Structure

Volume progression per averaging level:

Level 1: 1× (Base volume)

Level 2: 2×

Level 3: 4×

Level 4: 8×

Level 5: 16×

Level 6: 32×

(Max 6 levels configurable in strategy settings)

Custom Entry Variations

Alternative approach for swing captures:

// Enter only at 3rd averaging with 5% capital

if averaging_condition and strategy.opentrades == 2

strategy.entry("SwingEntry", strategy.long, qty=base_order_size*5)

Risk Management Protocol

No traditional stop-loss (replaced by averaging)

Break-even trigger: Manually move to breakeven at +0.5% profit

Max exposure: Capped at 6 averaging levels

Commissions: Pre-configured at 0.1% per trade

⚠️ Critical Risk Disclosures:

"Past Performance ≠ Future Results"

Historical optimization requires continuous forward testing ("Walk Forward" in TV).

Pyramiding Hazards

Exponential volume growth demands:

Minimum 20% free margin buffer

High liquidity instruments (spread < 0.5% of ATR)

Strict per-level risk calculation

Market Regime Dependence

Peak efficiency during:

Strong trends with 2-4% retracements

Assets with ATR > 1.5% of daily range

Avoid ranging/low-volatility conditions

💡 Pro Usage Recommendations:

Position Sizing Formula

For futures: Contracts = (Capital × Risk %) / (Entry Price × Point Value × Stop Distance)

Profit Protection

Close 50% position at 50% profit target, trail remainder

Event Safety

Disable averaging during:

High-impact news events

Exchange outages

Abnormal volume spikes

pie

title Risk Allocation per Level

“First Entry” : 12

“Level 2” : 18

“Level 3” : 25

“Level 4” : 45

ESSENTIAL: This strategy demands strict discipline. Terminate averaging when price action deviates from expected patterns. Always maintain reserve capital exceeding maximum drawdown requirements. Regularly validate strategy performance against current market dynamics.

🔥 Уникальные особенности и ценность:

Адаптивное усреднение

Стратегия автоматически увеличивает позицию при движении против вас, используя экспоненциальное наращивание объема (1x, 2x, 4x и т.д.). Это снижает среднюю цену входа и ускоряет выход в прибыль при развороте.

Мультитаймфреймная фильтрация

Все индикаторы работают на старшем таймфрейме (120 минут), что:

Фильтрует рыночный шум

Обеспечивает более надежные сигналы

Синхронизируется с глобальным трендом

Комбинированный триггер входа

Для активации требуется одновременное выполнение 4 условий:

Пробитие кастомной полосы Боллинджера

Подтверждение тренда (быстрая MA > медленной MA)

Контроль перепроданности (RSI выше критического уровня)

Фильтр волатильности (ATR)

Двойной механизм выхода

Закрытие позиций происходит при:

Достижении целевого уровня прибыли (% от депозита)

Техническом сигнале (касание верхней полосы Боллинджера)

⚙️ Как работает стратегия:

graph TD

A --> B

B --> C{Первый вход: 1% депозита}

C --> D

D -->|Да| E

D -->|Нет| F

E --> G{Достигнут лимит усреднений?}

G -->|Нет| D

G -->|Да| H

F --> I

📊 Как пользоваться:

Стартовые настройки

Base Order Size: Стартовый объем = 1% депозита

(Пример: при $10 000 депозита = 0.01 контракта)

initial_capital: Укажите ваш реальный депозит

Правила пирамидинга

Объем наращивается по схеме:

Уровень 1: 1x (базовый объем)

Уровень 2: 2x

Уровень 3: 4x

Уровень 4: 8x

Уровень 5: 16x

Уровень 6: 32x

РЕКОМЕНДУЕТСЯ Максимум 6 уровней усреднения (настраивается в pyramiding)

Кастомизация входов

Пример модификации для агрессивной тактики:

// Вход только на 3-м усреднении с 5% депозита

if averaging_condition and strategy.opentrades == 2

strategy.entry("BuyAggressive", strategy.long, qty=base_order_size*5)

Можно поставить параметр пираммидинг 1 и получать больше сигналов на младших тайм фреймах

Управление рисками

Стоп-лосс: Не используется (заменен усреднением)

Перевод в безубыток: Активируйте вручную при +0.5%

Максимальная просадка: Рекомендуется Ограничивать 6 уровнями усреднения

Комиссии: Учтены (0.1% от объема сделки)

Критические предупреждения:

"Вчера ≠ Сегодня"

Стратегия оптимизирована под историческую волатильность. Регулярно тестируйте на новых данных (режим "Перед тест" в TV).

Опасность усреднения

Экспоненциальный рост объема требует:

Глубокого расчета риска на уровень

Минимум 20% свободного маржи

Ликвидный инструмент (спред < 0.5% от ATR)

Рыночные условия

Максимальная эффективность в:

Трендовых рынках с коррекциями 2-4%

Инструментах с ATR > дневного диапазона 1.5%

💡 Рекомендации по использованию:

Для фьючерсов: Рассчитайте контракты через (капитал * 0.01) / (цена * пункт_стоимости)

При 50% достижении цели прибыли - закройте 50% позиции

Отключайте усреднение при выходе макро-новостей

pie

title Распределение риска

"Первый вход" : 10

"Уровень 2" : 20

"Уровень 3" : 30

"Уровень 4" : 40

ВАЖНО: Эта стратегия требует дисциплины! Прекращайте усреднение при отклонении рынка от исторических паттернов. Всегда имейте резервный капитал для экстренных случаев.