Cumulative Intraday Volume with Long/Short LabelsThis indicator calculates a running total of volume for each trading day, then shows on the price chart when that total crosses levels you choose. Every day at 6:00 PM Eastern Time, the total goes back to zero so it always reflects only the current day’s activity. From that moment on, each time a new candle appears the indicator looks at whether the candle closed higher than it opened or lower. If it closed higher, the candle’s volume is added to the running total; if it closed lower, the same volume amount is subtracted. As a result, the total becomes positive when buyers have dominated so far today and negative when sellers have dominated.

Because futures markets close at 6 PM ET, the running total resets exactly then, mirroring the way most intraday traders think in terms of a single session. Throughout the day, you will see this running total move up or down according to whether more volume is happening on green or red candles. Once the total goes above a number you specify (for example, one hundred thousand contracts), the indicator will place a small “Long” label at that candle on the main price chart to let you know buying pressure has reached that level. Similarly, once the total goes below a negative number you choose (for example, minus one hundred thousand), a “Short” label will appear at that candle to signal that selling pressure has reached your chosen threshold. You can set these threshold numbers to whatever makes sense for your trading style or the market you follow.

Because raw volume alone never turns negative, this design uses candle direction as a sign. Green candles (where the close is higher than the open) add volume, and red candles (where the close is lower than the open) subtract volume. Summing those signed volume values tells you in a single number whether buying or selling has been stronger so far today. That number resets every evening, so it does not carry over any buying or selling from previous sessions.

Once you have this indicator on your chart, you simply watch the “summed volume” line as it moves throughout the day. If it climbs past your long threshold, you know buyers are firmly in control and a long entry might make sense. If it falls past your short threshold, you know sellers are firmly in control and a short entry might make sense. In quieter markets or times of low volume, you might use a smaller threshold so that even modest buying or selling pressure will trigger a label. During very active periods, a larger threshold will prevent too many signals when volume spikes frequently.

This approach is straightforward but can be surprisingly powerful. It does not rely on complex formulas or hidden statistical measures. Instead, it simply adds and subtracts daily volume based on candle color, then alerts you when that total reaches levels you care about. Over several years of historical testing, this formula has shown an ability to highlight moments when intraday sentiment shifts decisively from buyers to sellers or vice versa. Because the indicator resets every day at 6 PM, it always reflects only today’s sentiment and remains easy to interpret without carrying over past data. You can use it on any intraday timeframe, but it works especially well on five-minute or fifteen-minute charts for futures contracts.

If you want a clear gauge of whether buyers or sellers are dominating in real time, and you prefer a rule-based method rather than a complex model, this indicator gives you exactly that. It shows net buying or selling pressure at a glance, resets each session like most intraday traders do, and marks the moments when that pressure crosses the levels you decide are important. By combining a daily reset with signed volume, you get a single number that tells you precisely what the crowd is doing at any given moment, without any of the guesswork or hidden calculations that more complicated indicators often carry.

Oscillatori centrati

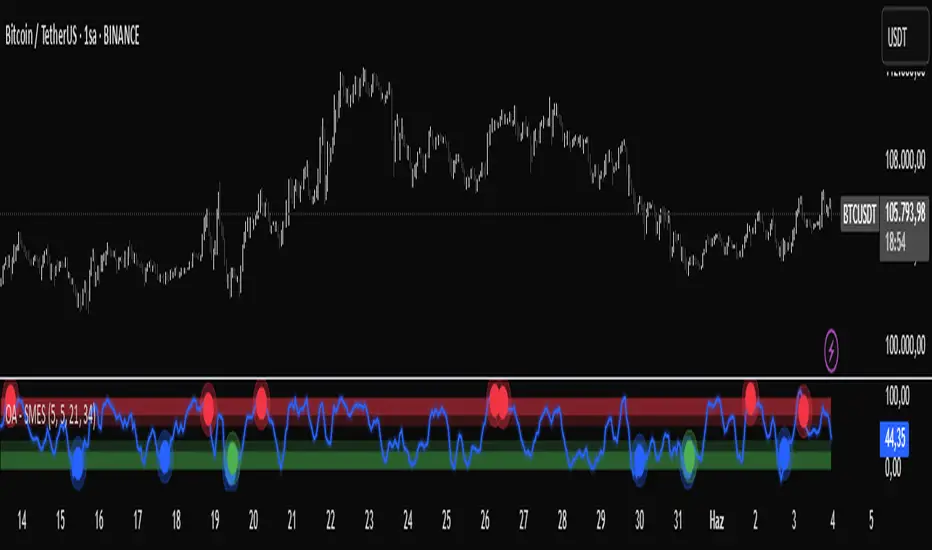

OA - SMESSmart Money Entry Signals (SMES)

The SMES indicator is developed to identify potential turning points in market behavior by analyzing internal price dynamics, rather than relying on external volume or sentiment data. It leverages normalized price movement, directional volatility, and smoothing algorithms to detect potential areas of accumulation or distribution by market participants.

Core Concepts

Smart Money Flow calculation based on normalized price positioning

Directional VHF (Vertical Horizontal Filter) used to enhance signal directionality

Overbought and Oversold regions defined with optional glow visualization

Entry and Exit signals based on dynamic crossovers

Highly customizable input parameters for precision control

Key Inputs

Smart Money Flow Period

Smoothing Period

Price Analysis Length

Fibonacci Lookback Length

Visual toggle options (zones, glow effects, signal display)

Usage

This tool plots the smoothed smart money flow as a standalone oscillator, designed to help traders identify potential momentum shifts or extremes in market sentiment. Entry signals are generated through crossover logic, while optional filters based on price behavior can refine those signals. Exit signals are shown when the smart money line exits extreme regions.

Important Notes

This indicator does not repaint

Works on all timeframes and instruments

Best used as a confirmation tool with other technical frameworks

All calculations are based strictly on price data

Disclaimer

This script is intended for educational purposes only. It does not provide financial advice or guarantee performance. Please do your own research and apply appropriate risk management before making any trading decisions.

Kaufman Trend Strategy# ✅ Kaufman Trend Strategy – Full Description (Script Publishing Version)

**Kaufman Trend Strategy** is a dynamic trend-following strategy based on Kaufman Filter theory.

It detects real-time trend momentum, reduces noise, and aims to enhance entry accuracy while optimizing risk.

⚠️ _For educational and research purposes only. Past performance does not guarantee future results._

---

## 🎯 Strategy Objective

- Smooth price noise using Kaufman Filter smoothing

- Detect the strength and direction of trends with a normalized oscillator

- Manage profits using multi-stage take-profits and adaptive ATR stop-loss logic

---

## ✨ Key Features

- **Kaufman Filter Trend Detection**

Extracts directional signal using a state space model.

- **Multi-Stage Profit-Taking**

Automatically takes partial profits based on color changes and zero-cross events.

- **ATR-Based Volatility Stops**

Stops adjust based on swing highs/lows and current market volatility.

---

## 📊 Entry & Exit Logic

**Long Entry**

- `trend_strength ≥ 60`

- Green trend signal

- Price above the Kaufman average

**Short Entry**

- `trend_strength ≤ -60`

- Red trend signal

- Price below the Kaufman average

**Exit (Long/Short)**

- Blue trend color → TP1 (50%)

- Oscillator crosses 0 → TP2 (25%)

- Trend weakens → Final exit (25%)

- ATR + swing-based stop loss

---

## 💰 Risk Management

- Initial capital: `$3,000`

- Order size: `$100` per trade (realistic, low-risk sizing)

- Commission: `0.002%`

- Slippage: `2 ticks`

- Pyramiding: `1` max position

- Estimated risk/trade: `~0.1–0.5%` of equity

> ⚠️ _No trade risks more than 5% of equity. This strategy follows TradingView script publishing rules._

---

## ⚙️ Default Parameters

- **1st Take Profit**: 50%

- **2nd Take Profit**: 25%

- **Final Exit**: 25%

- **ATR Period**: 14

- **Swing Lookback**: 10

- **Entry Threshold**: ±60

- **Exit Threshold**: ±40

---

## 📅 Backtest Summary

- **Symbol**: USD/JPY

- **Timeframe**: 1H

- **Date Range**: Jan 3, 2022 – Jun 4, 2025

- **Trades**: 924

- **Win Rate**: 41.67%

- **Profit Factor**: 1.108

- **Net Profit**: +$1,659.29 (+54.56%)

- **Max Drawdown**: -$1,419.73 (-31.87%)

---

## ✅ Summary

This strategy uses Kaufman filtering to detect market direction with reduced lag and increased smoothness.

It’s built with visual clarity and strong trade management, making it practical for both beginners and advanced users.

---

## 📌 Disclaimer

This script is for educational and informational purposes only and should not be considered financial advice.

Use with proper risk controls and always test in a demo environment before live trading.

RSI-Adaptive T3 [ChartPrime]The RSI-Adaptive T3 is a precision trend-following tool built around the legendary T3 smoothing algorithm developed by Tim Tillson , designed to enhance responsiveness while reducing lag compared to traditional moving averages. Current implementation takes it a step further by dynamically adapting the smoothing length based on real-time RSI conditions — allowing the T3 to “breathe” with market volatility. This dynamic length makes the curve faster in trending moves and smoother during consolidations.

To help traders visualize volatility and directional momentum, adaptive volatility bands are plotted around the T3 line, with visual crossover markers and a dynamic info panel on the chart. It’s ideal for identifying trend shifts, spotting momentum surges, and adapting strategy execution to the pace of the market.

HOIW IT WORKS

At its core, this indicator fuses two ideas:

The T3 Moving Average — a 6-stage recursively smoothed exponential average created by Tim Tillson , designed to reduce lag without sacrificing smoothness. It uses a volume factor to control curvature.

A Dynamic Length Engine — powered by the RSI. When RSI is low (market oversold), the T3 becomes shorter and more reactive. When RSI is high (overbought), the T3 becomes longer and smoother. This creates a feedback loop between price momentum and trend sensitivity.

// Step 1: Adaptive length via RSI

rsi = ta.rsi(src, rsiLen)

rsi_scale = 1 - rsi / 100

len = math.round(minLen + (maxLen - minLen) * rsi_scale)

pine_ema(src, length) =>

alpha = 2 / (length + 1)

sum = 0.0

sum := na(sum ) ? src : alpha * src + (1 - alpha) * nz(sum )

sum

// Step 2: T3 with adaptive length

e1 = pine_ema(src, len)

e2 = pine_ema(e1, len)

e3 = pine_ema(e2, len)

e4 = pine_ema(e3, len)

e5 = pine_ema(e4, len)

e6 = pine_ema(e5, len)

c1 = -v * v * v

c2 = 3 * v * v + 3 * v * v * v

c3 = -6 * v * v - 3 * v - 3 * v * v * v

c4 = 1 + 3 * v + v * v * v + 3 * v * v

t3 = c1 * e6 + c2 * e5 + c3 * e4 + c4 * e3

The result: an evolving trend line that adapts to market tempo in real-time.

KEY FEATURES

⯁ RSI-Based Adaptive Smoothing

The length of the T3 calculation dynamically adjusts between a Min Length and Max Length , based on the current RSI.

When RSI is low → the T3 shortens, tracking reversals faster.

When RSI is high → the T3 stretches, filtering out noise during euphoria phases.

Displayed length is shown in a floating table, colored on a gradient between min/max values.

⯁ T3 Calculation (Tim Tillson Method)

The script uses a 6-stage EMA cascade with a customizable Volume Factor (v) , as designed by Tillson (1998) .

Formula:

T3 = c1 * e6 + c2 * e5 + c3 * e4 + c4 * e3

This technique gives smoother yet faster curves than EMAs or DEMA/Triple EMA.

⯁ Visual Trend Direction & Transitions

The T3 line changes color dynamically:

Color Up (default: blue) → bullish curvature

Color Down (default: orange) → bearish curvature

Plot fill between T3 and delayed T3 creates a gradient ribbon to show momentum expansion/contraction.

Directional shift markers (“🞛”) are plotted when T3 crosses its own delayed value — helping traders spot trend flips or pullback entries.

⯁ Adaptive Volatility Bands

Optional upper/lower bands are plotted around the T3 line using a user-defined volatility window (default: 100).

Bands widen when volatility rises, and contract during compression — similar to Bollinger logic but centered on the adaptive T3.

Shaded band zones help frame breakout setups or mean-reversion zones.

⯁ Dynamic Info Table

A live stats panel shows:

Current adaptive length

Maximum smoothing (▲ MaxLen)

Minimum smoothing (▼ MinLen)

All values update in real time and are color-coded to match trend direction.

HOW TO USE

Use T3 crossovers to detect trend transitions, especially during periods of volatility compression.

Watch for volatility contraction in the bands — breakouts from narrow band periods often precede trend bursts.

The adaptive smoothing length can also be used to assess current market tempo — tighter = faster; wider = slower.

CONCLUSION

RSI-Adaptive T3 modernizes one of the most elegant smoothing algorithms in technical analysis with intelligent RSI responsiveness and built-in volatility bands. It gives traders a cleaner read on trend health, directional shifts, and expansion dynamics — all in a visually efficient package. Perfect for scalpers, swing traders, and algorithmic modelers alike, it delivers advanced logic in a plug-and-play format.

Momentum Fusion v1Momentum Fusion v1

Overview

Momentum Fusion v1 (MFusion) is a multi-oscillator indicator that combines several components to analyze market momentum and trend strength. It incorporates modified versions of classic indicators such as PVI (Positive Volume Index), NVI (Negative Volume Index), MFI (Money Flow Index), RSI, Stochastic, and Bollinger Bands Oscillator. The indicator displays a histogram that changes color based on momentum strength and includes "FUSION🔥" signal labels when extreme values are reached.

Indicator Settings

Parameters:

EMA Length – Smoothing period for the moving average (default: 255).

Smoothing Period – Internal calculation smoothing parameter (default: 15).

BB Multiplier – Standard deviation multiplier for Bollinger Bands (default: 2.0).

Show verde / marron / media lines – Toggles the display of auxiliary lines.

Show FUSION🔥 label – Enables/disables signal labels.

Indicator Components

1. PVI (Positive Volume Index)

Formula:

pvi := volume > volume ? nz(pvi ) + (close - close ) / close * sval : nz(pvi )

Description:

PVI increases when volume rises compared to the previous bar and accounts for price percentage change. The stronger the price movement with increasing volume, the higher the PVI value.

2. NVI (Negative Volume Index)

Formula:

nvi := volume < volume ? nz(nvi ) + (close - close ) / close * sval : nz(nvi )

Description:

NVI tracks price movements during declining volume. If the price rises on low volume, it may indicate a "stealth" trend.

3. Money Flow Index (MFI)

Formula:

100 - 100 / (1 + up / dn)

Description:

An oscillator measuring money flow strength. Values above 80 suggest overbought conditions, while values below 20 indicate oversold conditions.

4. Stochastic Oscillator

Formula:

k = 100 * (close - lowest(low, length)) / (highest(high, length) - lowest(low, length))

Description:

A classic stochastic oscillator showing price position relative to the selected period's range.

5. Bollinger Bands Oscillator

Formula:

(tprice - BB midline) / (upper BB - lower BB) * 100

Description:

Indicates the price position relative to Bollinger Bands in percentage terms.

Key Lines & Histogram

1. Verde (Green Line)

Calculation:

verde = marron + oscp (normalized PVI)

Interpretation:

Higher values indicate stronger bullish momentum. A FUSION🔥 signal appears when the value reaches 750+.

2. Marron (Brown Line)

Calculation:

marron = (RSI + MFI + Bollinger Osc + Stochastic / 3) / 2

Interpretation:

A composite oscillator combining multiple indicators. Higher values suggest overbought conditions.

3. Media (Red Line)

Calculation:

media = EMA of marron with smoothing period

Interpretation:

Acts as a signal line for trend confirmation.

4. Histogram

Calculation:

histo = verde - marron

Colors:

Bright green (>100) – Strong bullish momentum.

Light green (>0) – Moderate bullish momentum.

Orange (<0) – Bearish momentum.

Red (<-100) – Strong bearish momentum.

Signals & Alerts

1. FUSION🔥 (Strong Momentum)

Condition:

verde >= 750

Visualization:

A "FUSION🔥" label appears below the chart.

Alert:

Can be set to trigger notifications when the condition is met.

2. Background Aura

Condition:

verde > 850

Visualization:

The chart background turns teal, indicating extreme momentum.

Usage Recommendations

FUSION🔥 Signal – Can be used as a long entry point when confirmed by other indicators.

Histogram:

1. Green bars – Potential long entry.

2. Red/orange bars – Potential short entry.

3. Media & Marron Crossover – Can serve as an additional trend filter.

4. Suitable for a 5-15 minute time frame

Conclusion

Momentum Fusion v1 is a powerful tool for momentum analysis, combining multiple indicators into a unified system. It is suitable for:

Trend traders (catching strong movements).

Scalpers (identifying short-term impulses).

Swing traders (filtering entry points).

The indicator features customizable settings and visual signals, making it adaptable to various trading styles.

HARSI PRO v2 - Advanced Adaptive Heikin-Ashi RSI OscillatorThis script is a fully re-engineered and enhanced version of the original Heikin-Ashi RSI Oscillator created by JayRogers. While it preserves the foundational concept and visual structure of the original indicatorusing Heikin-Ashi-style candles to represent RSI movementit introduces a range of institutional-grade engines and real-time analytics modules.

The core idea behind HARSI is to visualize the internal structure of RSI behavior using candle representations. This gives traders a clearer sense of trend continuity, exhaustion, and momentum inflection. In this upgraded version, the system is extended far beyond basic visualization into a comprehensive diagnostic and context-tracking tool.

Core Enhancements and Features

1. Heikin-Ashi RSI Candles

The base HARSI logic transforms RSI values into open, high, low, and close components, which are plotted as Heikin-Ashi-style candles. The open values are smoothed with a user-controlled bias setting, and the high/low are calculated from zero-centered RSI values.

2. Smoothed RSI Histogram and Plot

A secondary RSI plot and histogram are available for traditional RSI interpretation, optionally smoothed using a custom midpoint EMA process.

3. Dynamic Stochastic RSI Ribbon

The indicator optionally includes a smoothed Stochastic RSI ribbon with directional fill to highlight acceleration and reversal zones.

4. Real-Time Meta-State Engine

This engine determines the current market environmentneutral, breakout, or reversalbased on multiple adaptive conditions including volatility compression, momentum thrust, volume behavior, and composite reversal scoring.

5. Adaptive Overbought/Oversold Zone Engine

Instead of using fixed RSI thresholds, this engine dynamically adjusts OB/OS boundaries based on recent RSI range and normalized price volatility. This makes the OB/OS levels context-sensitive and more accurate across different instruments and regimes.

6. Composite Reversal Score Engine

A real-time score between 0 and 5 is generated using four components:

* OB/OS proximity (zone score)

* RSI slope behavior

* Volume state (burst or exhaustion)

* Trend continuation penalty based on position versus trend bias

This score allows for objective filtering of reversal zones and breakout traps.

7. Kalman Velocity Filter

A Kalman-style adaptive smoothing filter is applied to RSI for calculating velocity and acceleration. This allows for real-time detection of stalls and thrusts in RSI behavior.

8. Predictive Breakout Estimator

Uses ATR compression and RSI thrusting conditions to detect likely breakout environments. This logic contributes to the Meta-State Engine and the Breakout Risk dashboard metric.

9. Volume Acceleration Model

Real-time detection of volume bursts and fades based on VWMA baselines. Volume exhaustion warnings are used to qualify or disqualify reversals and breakouts.

10. Trend Bias and Regime Detection

Uses RSI slope, HARSI body impulse, and normalized ATR to classify the current trend state and directional bias. This forms the basis for filtering false reversals during strong trends.

11. Dashboard with Tooltips

A clean, table displays six key metrics in real time:

* Meta State

* Reversal Score

* Trend Bias

* Volume State

* Volatility Regime

* Breakout Risk

Each cell includes a descriptive tooltip explaining why the value is being shown based on internal state calculations.

How It Works Internally

* The system calculates a zero-centered RSI and builds candle structures using high, low, and smoothed open/close values.

* Volatility normalization is used throughout the script, including ATR-based thresholds and dynamic scaling of OB/OS zones.

* Momentum is filtered through smoothed slope calculations and HARSI body size measurements.

* Volume activity is compared against VWMA using configurable multipliers to detect institutional-level activity or exhaustion.

* Each regime detection module contributes to a centralized metaState classifier that determines whether the environment is conducive to reversal, breakout, or neutral action.

* All major signal and context values are continuously updated in a dashboard table with logic-driven color coding and tooltips.

Based On and Credits

This script is based on the original Heikin-Ashi RSI Oscillator by JayRogers . All visual elements from the original version, including candle plotting and color configurations, have been retained and extended. Significant backend enhancements were added by AresIQ for the 2025 release. The script remains open-source under the original attribution license. Credit to JayRogers is preserved and required for any derivative versions.

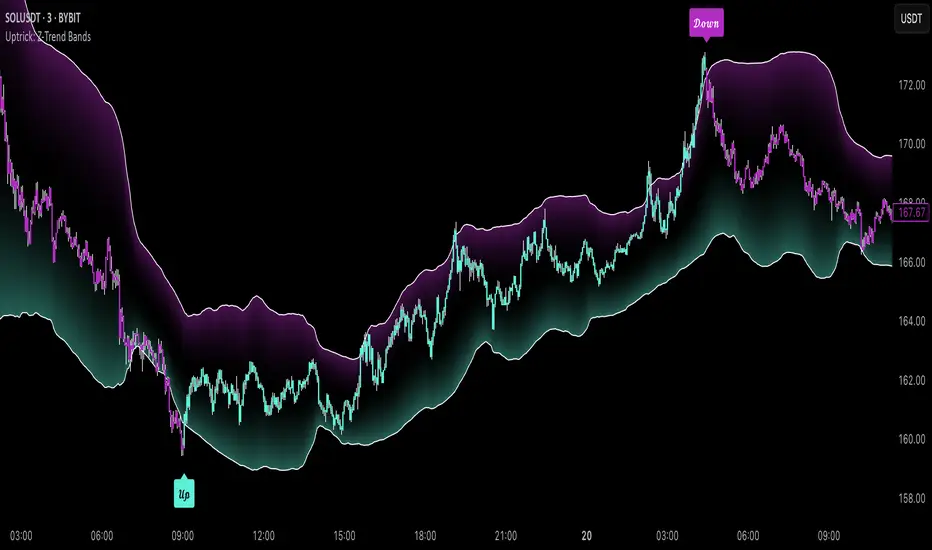

Uptrick: Z-Trend BandsOverview

Uptrick: Z-Trend Bands is a Pine Script overlay crafted to capture high-probability mean-reversion opportunities. It dynamically plots upper and lower statistical bands around an EMA baseline by converting price deviations into z-scores. Once price moves outside these bands and then reenters, the indicator verifies that momentum is genuinely reversing via an EMA-smoothed RSI slope. Signal memory ensures only one entry per momentum swing, and traders receive clear, real-time feedback through customizable bar-coloring modes, a semi-transparent fill highlighting the statistical zone, concise “Up”/“Down” labels, and a live five-metric scoring table.

Introduction

Markets often oscillate between trending and reverting, and simple thresholds or static envelopes frequently misfire when volatility shifts. Standard deviation quantifies how “wide” recent price moves have been, and a z-score transforms each deviation into a measure of how rare it is relative to its own history. By anchoring these bands to an exponential moving average, the script maintains a fluid statistical envelope that adapts instantly to both calm and turbulent regimes. Meanwhile, the Relative Strength Index (RSI) tracks momentum; smoothing RSI with an EMA and observing its slope filters out erratic spikes, ensuring that only genuine momentum flips—upward for longs and downward for shorts—qualify.

Purpose

This indicator is purpose-built for short-term mean-reversion traders operating on lower–timeframe charts. It reveals when price has strayed into the outer 5 percent of its recent range, signaling an increased likelihood of a bounce back toward fair value. Rather than firing on price alone, it demands that momentum follow suit: the smoothed RSI slope must flip in the opposite direction before any trade marker appears. This dual-filter approach dramatically reduces noise-driven, false setups. Traders then see immediate visual confirmation—bar colors that reflect the latest signal and age over time, clear entry labels, and an always-visible table of metric scores—so they can gauge both the validity and freshness of each signal at a glance.

Originality and Uniqueness

Uptrick: Z-Trend Bands stands apart from typical envelope or oscillator tools in four key ways. First, it employs fully normalized z-score bands, meaning ±2 always captures roughly the top and bottom 5 percent of moves, regardless of volatility regime. Second, it insists on two simultaneous conditions—price reentry into the bands and a confirming RSI slope flip—dramatically reducing whipsaw signals. Third, it uses slope-phase memory to lock out duplicate signals until momentum truly reverses again, enforcing disciplined entries. Finally, it offers four distinct bar-coloring schemes (solid reversal, fading reversal, exceeding bands, and classic heatmap) plus a dynamic scoring table, rather than a single, opaque alert, giving traders deep insight into every layer of analysis.

Why Each Component Was Picked

The EMA baseline was chosen for its blend of responsiveness—weighting recent price heavily—and smoothness, which filters market noise. Z-score deviation bands standardize price extremes relative to their own history, adapting automatically to shifting volatility so that “extreme” always means statistically rare. The RSI, smoothed with an EMA before slope calculation, captures true momentum shifts without the false spikes that raw RSI often produces. Slope-phase memory flags prevent repeated alerts within a single swing, curbing over-trading in choppy conditions. Bar-coloring modes provide flexible visual contexts—whether you prefer to track the latest reversal, see signal age, highlight every breakout, or view a continuous gradient—and the scoring table breaks down all five core checks for complete transparency.

Features

This indicator offers a suite of configurable visual and logical tools designed to make reversal signals both robust and transparent:

Dynamic z-score bands that expand or contract in real time to reflect current volatility regimes, ensuring the outer ±zThreshold levels always represent statistically rare extremes.

A smooth EMA baseline that weights recent price more heavily, serving as a fair-value anchor around which deviations are measured.

EMA-smoothed RSI slope confirmation, which filters out erratic momentum spikes by first smoothing raw RSI and then requiring its bar-to-bar slope to flip before any signal is allowed.

Slope-phase memory logic that locks out duplicate buy or sell markers until the RSI slope crosses back through zero, preventing over-trading during choppy swings.

Four distinct bar-coloring modes—Reversal Solid, Reversal Fade, Exceeding Bands, Classic Heat—plus a “None” option, so traders can choose whether to highlight the latest signal, show signal age, emphasize breakout bars, or view a continuous heat gradient within the bands.

A semi-transparent fill between the EMA and the upper/lower bands that visually frames the statistical zone and makes extremes immediately obvious.

Concise “Up” and “Down” labels that plot exactly when price re-enters a band with confirming momentum, keeping chart clutter to a minimum.

A real-time, five-metric scoring table (z-score, RSI slope, price vs. EMA, trend state, re-entry) that updates every two bars, displaying individual +1/–1/0 scores and an averaged Buy/Sell/Neutral verdict for complete transparency.

Calculations

Compute the fair-value EMA over fairLen bars.

Subtract that EMA from current price each bar to derive the raw deviation.

Over zLen bars, calculate the rolling mean and standard deviation of those deviations.

Convert each deviation into a z-score by subtracting the mean and dividing by the standard deviation.

Plot the upper and lower bands at ±zThreshold × standard deviation around the EMA.

Calculate raw RSI over rsiLen bars, then smooth it with an EMA of length rsiEmaLen.

Derive the RSI slope by taking the difference between the current and previous smoothed RSI.

Detect a potential reentry when price exits one of the bands on the prior bar and re-enters on the current bar.

Require that reentry coincide with an RSI slope flip (positive for a lower-band reentry, negative for an upper-band reentry).

On first valid reentry per momentum swing, fire a buy or sell signal and set a memory flag; reset that flag only when the RSI slope crosses back through zero.

For each bar, assign scores of +1, –1, or 0 for the z-score direction, RSI slope, price vs. EMA, trend-state, and reentry status.

Average those five scores; if the result exceeds +0.1, label “Buy,” if below –0.1, label “Sell,” otherwise “Neutral.”

Update bar colors, the semi-transparent fill, reversal labels, and the scoring table every two bars to reflect the latest calculations.

How It Actually Works

On each new candle, the EMA baseline and band widths update to reflect current volatility. The RSI is smoothed and its slope recalculated. The script then looks back one bar to see if price exited either band and forward to see if it reentered. If that reentry coincides with an appropriate RSI slope flip—and no signal has yet been generated in that swing—a concise label appears. Bar colors refresh according to your selected mode, and the scoring table updates to show which of the five conditions passed or failed, along with the overall verdict. This process repeats seamlessly at each bar, giving traders a continuous feed of disciplined, statistically filtered reversal cues.

Inputs

All parameters are fully user-configurable, allowing you to tailor sensitivity, lookbacks, and visuals to your trading style:

EMA length (fairLen): number of bars for the fair-value EMA; higher values smooth more but lag further behind price.

Z-Score lookback (zLen): window for calculating the mean and standard deviation of price deviations; longer lookbacks reduce noise but respond more slowly to new volatility.

Z-Score threshold (zThreshold): number of standard deviations defining the upper and lower bands; common default is 2.0 for roughly the outer 5 percent of moves.

Source (src): choice of price series (close, hl2, etc.) used for EMA, deviation, and RSI calculations.

RSI length (rsiLen): period for raw RSI calculation; shorter values react faster to momentum changes but can be choppier.

RSI EMA length (rsiEmaLen): period for smoothing raw RSI before taking its slope; higher values filter more noise.

Bar coloring mode (colorMode): select from None, Reversal Solid, Reversal Fade, Exceeding Bands, or Classic Heat to control how bars are shaded in relation to signals and band positions.

Show signals (showSignals): toggle on-chart “Up” and “Down” labels for reversal entries.

Show scoring table (enableTable): toggle the display of the five-metric breakdown table.

Table position (tablePos): choose which corner (Top Left, Top Right, Bottom Left, Bottom Right) hosts the scoring table.

Conclusion

By merging a normalized z-score framework, momentum slope confirmation, disciplined signal memory, flexible visuals, and transparent scoring into one Pine Script overlay, Uptrick: Z-Trend Bands offers a powerful yet intuitive tool for intraday mean-reversion trading. Its adaptability to real-time volatility and multi-layered filter logic deliver clear, high-confidence reversal cues without the clutter or confusion of simpler indicators.

Disclaimer

This indicator is provided solely for educational and informational purposes. It does not constitute financial advice. Trading involves substantial risk and may not be suitable for all investors. Past performance is not indicative of future results. Always conduct your own testing and apply careful risk management before trading live.

Triple EMA Momentum Oscillator (TEMO) HistogramThis Pine Script code replicates the Python indicator you provided, calculating the Triple EMA Momentum Oscillator (TEMO) and generating signals based on its value and momentum.

Explanation of the Code:

User Inputs:

Allows you to adjust the periods for the short, mid, and long EMAs.

Calculate EMAs:

Computes the Exponential Moving Averages for the specified periods.

Calculate EMA Spreads (Distances):

Finds the differences between the EMAs to understand the spread between them.

Calculate Spread Velocities:

Determines the change in spreads from the previous period, indicating momentum.

Composite Strength Score:

Weighted calculation of the spreads normalized by the EMA values.

Velocity Accelerator:

Weighted calculation of the velocities normalized by the EMA values.

Final TEMO Oscillator:

Combines the spread strength and velocity accelerator to create the TEMO.

Generate Signals:

Signals are generated when TEMO is positive and increasing (buy), or negative and decreasing (sell).

Plotting:

Zero Line: Helps visualize when TEMO crosses from positive to negative.

TEMO Oscillator: Plotted with green for positive values and red for negative values.

Signals: Displayed as a histogram to indicate buy (1) and sell (-1) signals.

Usage:

Buy Signal: When TEMO is above zero and increasing.

Sell Signal: When TEMO is below zero and decreasing.

Note: This oscillator helps identify momentum changes based on EMAs of different periods. It's useful for detecting trends and potential reversal points in the market.

Supply In Profit Z-ScoreZ-score of BTC Supply in Profit.

Supply in Profit is an On-Chain BTC indicator that shows the percentage of BTC in profit.

In this indicator you can choose to use a Z-Score or not.

BTC Thermocap Z-ScoreBTC Thermocap Indicator Overview

The BTC Thermocap is a specialized on-chain ratio indicator designed to provide deeper insight into Bitcoin's market valuation relative to its cumulative issuance. By comparing the current market price of Bitcoin to the total value of all BTC ever mined (also known as "thermocap"), this indicator helps identify potential overvaluation or undervaluation periods within the Bitcoin market cycle.

Key Features and Customizable Inputs:

Moving Average Length (MA Length)

Moving Average Type (MA Type) - SMA or EMA

Z-Score Calculation Length

Z-Score Toggle (Use Z-Score)

MACD + RSI + EMA + BB + ATR Day Trading StrategyEntry Conditions and Signals

The strategy implements a multi-layered filtering approach to entry conditions, requiring alignment across technical indicators, timeframes, and market conditions .

Long Entry Requirements

Trend Filter: Fast EMA (9) must be above Slow EMA (21), price must be above Fast EMA, and higher timeframe must confirm uptrend

MACD Signal: MACD line crosses above signal line, indicating increasing bullish momentum

RSI Condition: RSI below 70 (not overbought) but above 40 (showing momentum)

Volume & Volatility: Current volume exceeds 1.2x 20-period average and ATR shows sufficient market movement

Time Filter: Trading occurs during optimal hours (9:30-11:30 AM ET) when market volatility is typically highest

Exit Strategies

The strategy employs multiple exit mechanisms to adapt to changing market conditions and protect profits :

Stop Loss Management

Initial Stop: Placed at 2.0x ATR from entry price, adapting to current market volatility

Trailing Stop: 1.5x ATR trailing stop that moves up (for longs) or down (for shorts) as price moves favorably

Time-Based Exits: All positions closed by end of trading day (4:00 PM ET) to avoid overnight risk

Best Practices for Implementation

Settings

Chart Setup: 5-minute timeframe for execution with 15-minute chart for trend confirmation

Session Times: Focus on 9:30-11:30 AM ET trading for highest volatility and opportunity

Reversal Trap Sniper – Verified VersionReversal Trap Sniper

Overview

Reversal Trap Sniper is a counterintuitive momentum-following strategy that identifies "reversal traps"—situations where traders expect a market reversal based on RSI, but the price continues trending. By detecting these failed reversal signals, the strategy enters trades in the trend direction, often catching strong follow-through moves.

How It Works

The system monitors the Relative Strength Index (RSI). When RSI moves above the overbought level (e.g., 70) and then drops back below it, many traders interpret this as a sell signal.

However, this strategy treats such moves with caution. If the RSI pulls back below the overbought threshold but the price continues to rise, the system considers it a "reversal trap"—a fakeout.

In such cases, instead of going short, the strategy enters a long position, assuming that the trend is still valid and those betting on a reversal may fuel a breakout.

Similarly, if RSI rises above the oversold level from below, but price continues falling, a short trade is triggered.

Entries are followed by ATR-based stop-loss and dynamic take-profit (2× risk), with a fallback time-based exit after 30 bars.

Key Features

- Detects failed RSI-based reversals ("traps")

- Follows momentum after the trap is triggered

- Uses ATR for dynamic stop-loss and take-profit

- Auto-exit after a fixed bar count (30 bars)

- Visual markers on chart for transparency

- Realistic trading assumptions: 0.05% commission, slippage, and capped pyramiding

Parameter Explanation

RSI Length (14): Standard RSI calculation period

Overbought/Oversold Levels (70/30): Common thresholds used by many traders

ATR Length (14): Used to define stop-loss and target dynamically

Risk-Reward Ratio (2.0): Take-profit is set at 2× the stop-loss distance

Max Holding Bars (30): Ensures trades don’t remain open indefinitely

Pyramiding (10): Allows scaling into trades, simulating real-world strategy stacking

Originality Note

This strategy inverts traditional RSI logic. Instead of treating overbought/oversold conditions as signals for reversal, it waits for those signals to fail. Only after such failures, confirmed by continued price action in the same direction, does the system enter trades. This logic is based on the behavioral observation that failed reversal signals often trigger stronger trend continuation—making this strategy uniquely positioned to exploit trap scenarios.

Disclaimer

This script is for educational and research purposes only. Trading involves risk, and past performance does not guarantee future results. Always test thoroughly before applying with live capital.

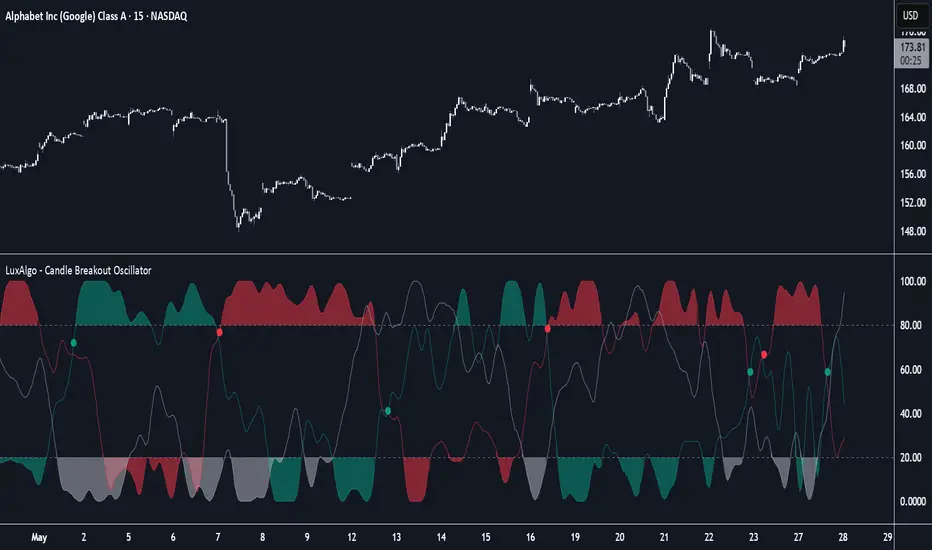

Candle Breakout Oscillator [LuxAlgo]The Candle Breakout Oscillator tool allows traders to identify the strength and weakness of the three main market states: bullish, bearish, and choppy.

Know who controls the market at any given moment with an oscillator display with values ranging from 0 to 100 for the three main plots and upper and lower thresholds of 80 and 20 by default.

🔶 USAGE

The Candle Breakout Oscillator represents the three main market states, with values ranging from 0 to 100. By default, the upper and lower thresholds are set at 80 and 20, and when a value exceeds these thresholds, a colored area is displayed for the trader's convenience.

This tool is based on pure price action breakouts. In this context, we understand a breakout as a close above the last candle's high or low, which is representative of market strength. All other close positions in relation to the last candle's limits are considered weakness.

So, when the bullish plot (in green) is at the top of the oscillator (values above 80), it means that the bullish breakouts (close below the last candle low) are at their maximum value over the calculation window, indicating an uptrend. The same interpretation can be made for the bearish plot (in red), indicating a downtrend when high.

On the other hand, weakness is indicated when values are below the lower threshold (20), indicating that breakouts are at their minimum over the last 100 candles. Below are some examples of the possible main interpretations:

There are three main things to look for in this oscillator:

Value reaches extreme

Value leaves extreme

Bullish/Bearish crossovers

As we can see on the chart, before the first crossover happens the bears come out of strength (top) and the bulls come out of weakness (bottom), then after the crossover the bulls reach strength (top) and the bears weakness (bottom), this process is repeated in reverse for the second crossover.

The other main feature of the oscillator is its ability to identify periods of sideways trends when the sideways values have upper readings above 80, and trending behavior when the sideways values have lower readings below 20. As we just saw in the case of bullish vs. bearish, sideways values signal a change in behavior when reaching or leaving the extremes of the oscillator.

🔶 DETAILS

🔹 Data Smoothing

The tool offers up to 10 different smoothing methods. In the chart above, we can see the raw data (smoothing: None) and the RMA, TEMA, or Hull moving averages.

🔹 Data Weighting

Users can add different weighting methods to the data. As we can see in the image above, users can choose between None, Volume, or Price (as in Price Delta for each breakout).

🔶 SETTINGS

Window: Execution window, 100 candles by default

🔹 Data

Smoothing Method: Choose between none or ten moving averages

Smoothing Length: Length for the moving average

Weighting Method: Choose between None, Volume, or Price

🔹 Thresholds

Top: 80 by default

Bottom: 20 by default

Volatility Pulse with Dynamic ExitVolatility Pulse with Dynamic Exit

Overview

This strategy, Volatility Pulse with Dynamic Exit, is designed to capture impulsive price moves following volatility expansions, while ensuring risk is managed dynamically. It avoids trades during low-volatility periods and uses momentum confirmation to enter positions. Additionally, it features a time-based forced exit system to limit overexposure.

How It Works

A position is opened when the current ATR (Average True Range) significantly exceeds its 20-period average, signaling a volatility expansion.

To confirm the move is directional and not random noise, the strategy checks for momentum: the close must be above/below the close of 20 bars ago.

Low volatility zones are filtered out to avoid chop and poor trade entries.

Upon entry, a dynamic stop-loss is set at 1x ATR, while take-profit is set at 2x ATR, offering a 2:1 reward-to-risk ratio.

If the position remains open for more than 42 bars, it is forcefully closed, even if targets are not hit. This prevents long-lasting, stagnant trades.

Key Features

✅ Volatility-based breakout detection

✅ Momentum confirmation filter

✅ Dynamic stop-loss and take-profit based on real-time ATR

✅ Time-based forced exit (42 bars max holding)

✅ Low-volatility environment filter

✅ Realistic settings with 0.05% commission and slippage included

Parameters Explanation

ATR Length (14): Captures recent volatility over ~2 weeks (14 candles).

Momentum Lookback (20): Ensures meaningful price move confirmation.

Volatility Expansion Threshold (0.5x): Strategy activates only when ATR is at least 50% above its average.

Minimum ATR Filter (1.0x): Avoids entries in tight, compressed market ranges.

Max Holding (42 bars): Trades are closed after 42 bars if no exit signal is triggered.

Risk-Reward (2.0x): Aiming for 2x ATR as profit for every 1x ATR risk.

Originality Note

While volatility and momentum have been used separately in many strategies, this script combines both with a time-based dynamic exit system. This exit rule, combined with an ATR-based filter to exclude low-activity periods, gives the system a practical edge in real-world use. It avoids classic rehashes and integrates real trading constraints for better applicability.

Disclaimer

This is a research-focused trading strategy meant for backtesting and educational purposes. Always use proper risk management and perform due diligence before applying to real funds.

Zero Lag Multi Timeframe MACDCommon parts of the Multi Time Frame MACD

Why This MACD is Special

Traditional MACD (Moving Average Convergence Divergence) is a powerful trend-following indicator, but it has a key limitation: it only reflects price action on a single timeframe. Traders who rely on top-down analysis—analyzing higher timeframes first before moving to lower ones—often face a frustrating delay.

The Problem with Traditional Multi-Timeframe MACD with top down analysis:

If you’re on a 5-minute chart and want to see the 1-hour MACD, you must wait for 12 candles (1 hour) to close before the MACD updates.

This lag means you miss real-time signals and react too late to trend changes.

The Zero Lag Multi-Timeframe MACD solves this by using a custom time-adjusted formula (developed by CoffeeShopCrypto) that projects higher timeframe MACD values onto lower timeframe charts in real time.

How Traders Normally Use MACD

Single-Timeframe MACD (Traditional Approach)

Used for trend identification (bullish/bearish).

Crossovers (MACD line crossing signal line) signal potential entries.

Divergences (price vs. MACD direction) warn of trend exhaustion.

Top-Down Analysis with Standard MACD (Manual Switching)

1. Check higher timeframe (e.g., 1-hour) for trend direction.

2. Switch to lower timeframe (e.g., 5-minute) for entries.

Problem: You must constantly switch charts and wait for higher timeframe candles to close.

This MACD Eliminates the Need for Switching

Higher timeframe MACD is plotted in real time on your lower timeframe chart.

No waiting for candle closes—instant trend confirmation.

Single-chart top-down analysis without switching timeframes.

How to Use This MACD for Trading

Since the MACD is an averaging indicator, it works best when trading with the trend. This version enhances that by showing two trends at once:

Lower Timeframe (LTF) MACD – Your current chart’s trend.

Higher Timeframe (HTF) MACD – The dominant trend.

Key Trading Rules

1. Strong Uptrend Setup (Best for Long Entries)

HTF MACD line is rising & above zero (strong bullish momentum).

LTF MACD line is also rising (confirms alignment).

Entry: Look for LTF MACD to cross above signal line.

Long Entry Confirmation:

When both the High Timeframe and Low Timeframe MACD Lines are moving in the same direction, this is a confirmation that both the HTF is matching the direction of the LTF.

In this example both MACD Lines are moving long so we are only looking to take long entries at this point forward.

Short Entry Confirmation:

When both the High Timeframe and Low Timeframe MACD Lines are moving in the same direction, this is a confirmation that both the HTF is matching the direction of the LTF.

In this example both MACD Lines are moving short so we are only looking to take long entries at this point forward.

2. Potential Reversal or Weak Uptrend

Trend Divergence Confirmation

This example shows you a confirmation of divergence between the trends. Its best to watch for a continuation of the previous major trend. In this example, we just came off a downtrend with a GAP DOWN.

How to see it: (Trend Divergence)

Two things will help you confirm this divergence

1.Notice the LTF and HTF MACD are moving away from each other.

2. Both the HTF and LTF Histogram are shrinking.

This is an expression of lack of trend.

What to do:

High Timeframe Trends are always the lead so wait for the Low Timeframe to catch up to the High Timeframe trend.

Limitations:

The Exponential Moving Average calculation can only be applied to the Low Timeframe MACD because of the way its weighted against more recent price action and closing values.

This same EMA calculation can not be applied to the High Timeframe MACD as its being recalculated and the result means you can not weigh values against its current plot point.

Low Timeframe MACD can use EMA / SMA

High Timeframe MACD can only use SMA

CCI Divergence Detector

A technical analysis tool that identifies divergences between price action and the Commodity Channel Index (CCI) oscillator. Unlike standard divergence indicators, this system employs advanced gradient visualization, multi-layer wave effects, and comprehensive customization options to provide traders with crystal-clear divergence signals and market momentum insights.

Core Detection Mechanism

CCI-Based Analysis: The indicator utilizes the Commodity Channel Index as its primary oscillator, calculated from user-configurable source data (default: HLC3) with adjustable length parameters. The CCI provides reliable momentum readings that effectively highlight price-momentum divergences.

Dynamic Pivot Detection: The system employs adaptive pivot detection with three sensitivity levels (High/Normal/Low) to identify significant highs and lows in both price and CCI values. This dynamic approach ensures optimal divergence detection across different market conditions and timeframes.

Dual Divergence Analysis:

Regular Bullish Divergences: Detected when price makes lower lows while CCI makes higher lows, indicating potential upward reversal

Regular Bearish Divergences: Identified when price makes higher highs while CCI makes lower highs, signaling potential downward reversal

Strength Classification System: Each detected divergence is automatically classified into three strength categories (Weak/Moderate/Strong) based on:

-Price differential magnitude

-CCI differential magnitude

-Time duration between pivot points

-User-configurable strength multiplier

Advanced Visual System

Multi-Layer Wave Effects: The indicator features a revolutionary wave visualization system that creates depth through multiple gradient layers around the CCI line. The wave width dynamically adjusts based on ATR volatility, providing intuitive visual feedback about market conditions.

Professional Color Gradient System: Nine independent color inputs control every visual aspect:

Bullish Colors (Light/Medium/Dark): Control oversold areas, wave effects, and strong bullish signals

Bearish Colors (Light/Medium/Dark): Manage overbought zones, wave fills, and strong bearish signals

Neutral Colors (Light/Medium/Dark): Handle table elements, zero line, and transitional states

Intelligent Color Mapping: Colors automatically adapt based on CCI values:

Overbought territory (>100): Bearish color gradients with increasing intensity

Neutral positive (0 to 100): Blend from neutral to bearish tones

Oversold territory (<-100): Bullish color gradients with increasing intensity

Neutral negative (-100 to 0): Transition from neutral to bullish tones

Key Features & Components

Advanced Configuration System: Eight organized input groups provide granular control:

General Settings: System enable, pivot length, confidence thresholds

Oscillator Selection: CCI parameters, overbought/oversold levels, normalization options

Detection Parameters: Divergence types, minimum strength requirements

Sensitivity Tuning: Pivot sensitivity, divergence threshold, confirmation bars

Visual System: Line thickness, labels, backgrounds, table display

Wave Effects: Dynamic width, volatility response, layer count, glow effects

Transparency Controls: Independent transparency for all visual elements

Smoothing & Filtering: CCI smoothing types, noise filtering, wave smoothing

Professional Alert System: Comprehensive alert functionality with dynamic messages including:

-Divergence type and strength classification

-Current CCI value and confidence percentage

-Customizable alert frequency and conditions

Enhanced Information Table: Real-time display showing:

-Current CCI length and value

-Market status (Overbought/Normal/Oversold)

-Active sensitivity setting

Configurable table positioning (4 corner options)

Visual Elements Explained

Primary CCI Line: Main oscillator plot with gradient coloring that reflects market momentum and CCI intensity. Line thickness is user-configurable (1-8 pixels).

Wave Effect Layers: Multi-layer gradient fills creating a dynamic wave around the

CCI line:

-Outer layers provide broad market context

-Inner layers highlight immediate momentum

-Core layers show precise CCI movement

-All layers respond to volatility and momentum changes

Divergence Lines & Labels:

-Solid lines connecting divergence pivot points

-Color-coded based on divergence type and strength

-Labels displaying divergence type and strength classification

-Customizable transparency and size options

Reference Lines:

-Zero line with neutral color coding

-Overbought level (default: 100) with bearish coloring

-Oversold level (default: -100) with bullish coloring

Background Gradient: Optional background coloring that reflects CCI intensity and market conditions with user-controlled transparency (80-99%).

Configuration Options

Sensitivity Controls:

Pivot sensitivity: High/Normal/Low detection levels

Divergence threshold: 0.1-2.0 sensitivity range

Confirmation bars: 1-5 bar confirmation requirement

Strength multiplier: 0.1-3.0 calculation adjustment

Visual Customization:

Line transparency: 0-90% for main elements

Wave transparency: 0-95% for fill effects

Background transparency: 80-99% for subtle background

Label transparency: 0-50% for text elements

Glow transparency: 50-95% for glow effects

Advanced Processing:

Five smoothing types: None/SMA/EMA/RMA/WMA

Noise filtering with adjustable threshold (0.1-10.0)

CCI normalization for enhanced gradient scaling

Dynamic wave width with ATR-based volatility response

Interpretation Guidelines

Divergence Signals:

Strong divergences: High-confidence reversal signals requiring immediate attention

Moderate divergences: Reliable signals suitable for most trading strategies

Weak divergences: Early warning signals best combined with additional confirmation

Wave Intensity: Wave width and color intensity provide real-time volatility and momentum feedback. Wider, more intense waves indicate higher market volatility and stronger momentum.

Color Transitions: Smooth color transitions between bullish, neutral, and bearish states help identify market regime changes and momentum shifts.

CCI Levels: Traditional overbought (>100) and oversold (<-100) levels remain relevant, but the gradient system provides more nuanced momentum reading between these extremes.

Technical Specifications

Compatible Timeframes: All timeframes supported

Maximum Labels: 500 (for divergence marking)

Maximum Lines: 500 (for divergence drawing)

Pine Script Version: v5 (latest optimization)

Overlay Mode: False (separate pane indicator)

Usage Recommendations

This indicator works best when:

-Combined with price action analysis and support/resistance levels

-Used across multiple timeframes for confirmation

-Integrated with proper risk management protocols

-Applied in trending markets for divergence-based reversal signals

-Utilized with other technical indicators for comprehensive analysis

Risk Disclaimer: Trading involves substantial risk of loss. This indicator is provided for analytical purposes only and does not constitute financial advice. Divergence signals, while powerful, are not guaranteed to predict future price movements. Past performance is not indicative of future results. Always use proper risk management and never trade with capital you cannot afford to lose.

Directionality OscillatorDirectionality Oscillator is a simple momentum tool that measures net price displacement against total price activity over a chosen look-back period. It takes today’s closing price minus the close from “len” bars ago and divides that by the sum of all absolute bar-to-bar moves across the same span. The result is a value between –1 and +1, where positive values show that upward moves dominated and negative values show that downward moves prevailed.

To smooth out short-term noise, the indicator applies a five-bar simple moving average to the normalized value. A color gradient—from red at –1, through gray at 0, to green at +1—paints the line, making it easy to see whether bearish or bullish pressure is strongest. Two horizontal lines at the user-defined threshold and its negative mark zones of extreme directional strength. Readings above the positive threshold signal strong bullish momentum, and readings below the negative threshold signal strong bearish momentum.

Traders can watch for crossings above or below these threshold lines as trend confirmations or potential reversal warnings. A cross of the zero line indicates a shift in net directional control and can serve as an early trend-change alert when supported by price action or volume. Because it filters out sideways noise by normalizing against total activity, it highlights sustained directional thrust more clearly than a raw price-change measure.

MACD Crossover with Price Action and AlertsThe MACD should use the default parameters (12, 26, 9) for fast EMA, slow EMA, and signal EMA, respectively, applied to the Close price. Instead of simple MACD crossovers, the indicator should analyze price action in relation to the MACD histogram to generate signals. Specifically: 1. BUY signal: Generate a buy signal (an up arrow displayed below the low of the signal bar in green color) when the MACD histogram crosses above zero AND the price action shows a bullish engulfing pattern (the current candle's body completely engulfs the previous candle's body). 2. SELL signal: Generate a sell signal (a down arrow displayed above the high of the signal bar in red color) when the MACD histogram crosses below zero AND the price action shows a bearish engulfing pattern (the current candle's body completely engulfs the previous candle's body). The arrows should be non-repainting, meaning that once an arrow is plotted on a bar, it should not disappear or change position as the chart updates. The indicator should also plot the MACD line, signal line, and histogram using their default calculations. The MACD line should be blue, the signal line should be orange, and the histogram should be displayed using green bars for positive values and red bars for negative values. The indicator should also have customizable inputs for the MACD fast EMA period, slow EMA period, signal EMA period and engulfing pattern check enabled/disabled. If engulfing pattern check disabled, the indicator will generate signals based only on MACD histogram crossing zero.

Adaptive Momentum Flow (AMF)Overview

The Adaptive Momentum Flow (AMF) indicator is a powerful, multi-faceted tool designed to provide a comprehensive and adaptive view of market momentum and trend strength. Unlike traditional oscillators with fixed settings, AMF dynamically adjusts its calculations based on market volatility , ensuring its signals remain relevant across varying market conditions. By combining advanced Double Exponential Moving Averages (DEMA) with a powerful volume analysis component and a customizable scoring system, AMF offers a unique perspective on price action and underlying buying/selling pressure.

Key Features & How It Works

1. Adaptive DEMA Trend Strength:

At its core, AMF utilizes three DEMA lines (Fast, Medium, Slow) to assess the current trend's alignment and strength.

The indicator dynamically adjusts the lengths of these DEMA lines based on real-time market volatility, measured by Average True Range (ATR). This means AMF becomes more responsive in volatile markets and smoother in calmer periods.

A "Volatility Sensitivity" input allows you to fine-tune how aggressively the indicator adapts to these changes.

2. Volume Analysis (Buying/Selling Pressure):

AMF incorporates a dedicated volume analysis module to gauge whether volume is predominantly supporting upward or downward price movements. This helps identify periods of significant buying or selling pressure.

This volume analysis component is smoothed with an adjustable Moving Average (SMA, EMA, WMA, or DEMA) and contributes to the overall momentum score, adding a crucial layer of volume-driven confirmation to the analysis.

3. Comprehensive Scoring System:

The indicator generates a normalized "Oscillator Score" that ranges from -100 to 100. This score is a weighted sum of:

Price's relationship to the Fast DEMA.

The Fast DEMA's relationship to the Medium DEMA.

The Medium DEMA's relationship to the Slow DEMA.

The smoothed value from the volume analysis.

Each component's influence on the final score can be individually adjusted via input weights, allowing for deep customization.

Signal Line & Crossovers:

A smoothed "Signal Line" provides additional confirmation for momentum shifts. Crossovers between the main AMF line and its Signal Line can indicate potential changes in market direction.

Overbought/Oversold Levels:

Adjustable Overbought (default 70) and Oversold (default -70) levels visually highlight extreme momentum conditions.

These zones are enhanced with a color fill effect (bright red for overbought, bright cyan for oversold), making it easy to spot when the market is entering potentially exhausted states.

Crucially, these extreme zones can often be further validated by combining them with volatility bands (like Bollinger Bands or Keltner Channels as shown in the chart above) or other confluence indicators, offering stronger signals for potential reversals or exhaustion.

Benefits for Traders

Reduced Lag: DEMA's inherent design helps minimize lag compared to traditional moving averages, providing more timely signals.

Adaptive Intelligence: Automatically adjusts to market volatility, ensuring the indicator's sensitivity is appropriate for current conditions.

Holistic Momentum View: Combines price-based trend alignment with volume-based pressure for a more robust assessment of market flow.

Clear Visual Cues: Intuitive plots, signal line, and vibrant overbought/oversold zone fills make interpretation straightforward.

Customizable: Extensive input options allow traders to tailor the indicator to their specific trading style, asset, and timeframe.

How to Use

Trend Confirmation: Look for the AMF line and its Signal Line to align with the price trend.

Momentum Shifts: Crossovers between the AMF line and its Signal Line can indicate shifts in momentum.

Extreme Conditions: Pay attention when the AMF line enters the neon-highlighted overbought or oversold zones, signaling potential reversals or pauses in the current momentum. Always consider confirming these signals with other analysis tools, such as price action, chart patterns, support/resistance levels, or volatility indicators.

Customization: Experiment with the "Volatility Sensitivity," DEMA multipliers, and scoring weights to find the optimal settings for your trading strategy.

Dual Pwma Trends [ZORO_47]Key Features:

Dual PWMA System: Combines a fast and slow Parabolic Weighted Moving Average to identify momentum shifts and trend changes with precision.

Dynamic Color Coding: The indicator lines change color to reflect market conditions—green for bullish crossovers (potential buy signals) and red for bearish crossunders (potential sell signals), making it easy to interpret at a glance.

Customizable Parameters: Adjust the fast and slow PWMA lengths, power settings, and source data to tailor the indicator to your trading style and timeframe.

Clean Visualization: Plotted with bold, clear lines (3px width) for optimal visibility on any chart, ensuring you never miss a signal.

How It Works:

The indicator calculates two PWMAs using the imported ZOROLIBRARY by ZORO_47. When the fast PWMA crosses above the slow PWMA, both lines turn green, signaling a potential bullish trend. Conversely, when the fast PWMA crosses below the slow PWMA, the lines turn red, indicating a potential bearish trend. The color persists until the next crossover or crossunder, providing a seamless visual cue for trend direction.

Ideal For:

Trend Traders: Identify trend reversals and continuations with clear crossover signals.

Swing Traders: Use on higher timeframes to capture significant price moves.

Day Traders: Fine-tune settings for faster signals on intraday charts.

Settings:

Fast Length/Power: Control the sensitivity of the fast PWMA (default: 12/2).

Slow Length/Power: Adjust the smoother, slower PWMA (default: 21/1).

Source: Choose your preferred data input (default: close price).

Adaptive Multi-TF Indicator Table with Presets giua64📌 Script Name:

Adaptive Multi-Timeframe Indicator Table with Presets — giua64

📄 Description:

This script displays an adaptive multi-timeframe dashboard that summarizes the signals of three key technical indicators:

Moving Averages (MAs), Relative Strength Index (RSI), and MACD.

It provides a fast and visually intuitive overview of market conditions across five timeframes (5m, 15m, 30m, 1h, 4h), helping traders quickly identify potential directional biases (e.g., bullish, bearish, or neutral) based on either predefined presets or fully manual settings.

🧰 Preset Configurations:

You can choose between four trading styles, each with optimized indicator parameters:

Scalping

• MAs: 5 / 10 (Fast), 20 / 50 (Slow)

• RSI: 7 periods | Overbought: 70 | Oversold: 30

• MACD: 5 / 13 | Signal: 3

Intraday

• MAs: 9 / 21 (Fast), 50 / 100 (Slow)

• RSI: 14 periods | Overbought: 60 | Oversold: 40

• MACD: 12 / 26 | Signal: 9

Swing

• MAs: 10 / 20 (Fast), 50 / 200 (Slow)

• RSI: 14 periods | Overbought: 65 | Oversold: 35

• MACD: 12 / 26 | Signal: 9

Manual

• Full custom control over all indicator settings.

🛠️ All settings can be customized manually from the options panel, including the exact MA periods, RSI thresholds, and MACD structure.

🧠 How It Works:

For each timeframe, the script evaluates:

MA crossover status (two levels):

The first symbol refers to the crossover of the fast MAs

The second symbol refers to the crossover of the slow MAs

🟢 = Bullish crossover

🔴 = Bearish crossover

➖ = Flat or no clear signal

RSI Direction:

↑ = RSI above upper threshold (potential overbought)

↓ = RSI below lower threshold (potential oversold)

→ = RSI in neutral range

MACD Line vs Signal Line:

↑ = MACD line is above signal line (bullish)

↓ = MACD line is below signal line (bearish)

→ = Flat or neutral signal

Each signal is assigned a numerical score. These are aggregated per timeframe to compute a combined score that reflects the directional bias for that specific time window.

🧠 Adaptive Logic by Asset:

This script is designed to be universally compatible across all asset types — including forex, crypto, stocks, indices, and commodities.

Thanks to its multi-timeframe nature and flexible indicator presets, the script automatically adjusts its behavior based on the asset selected, ensuring relevant analysis without requiring manual recalibration.

🧾 Summary Table Output:

At the bottom of the dashboard, a combined sentiment is displayed for:

3TF → 5m, 15m, 30m

4TF → Adds 1h

5TF → Adds 4h

Each row shows:

Signal → LONG / SHORT / NEUTRAL

Confidence (%) → Based on score aggregation and signal consistency

📌 Customization Options:

Table Position: Left, Right, or Center

Text Size: Small, Normal, or Large

Full Manual Configuration: All MA, RSI, and MACD parameters can be adjusted as needed

⚠️ Disclaimer:

This script is for educational and analytical purposes only.

It does not constitute financial advice or guarantee any trading results.

Always do your own research and apply responsible risk management.

Linear Volume MACD | Lyro RS📊 Linear Volume MACD | Lyro RS is an advanced momentum and trend detection tool that fuses price action with volume-weighted MACD logic and linear regression analysis . Designed for traders seeking deeper insights into market strength and directional conviction, this indicator highlights trend shifts, volume anomalies, and potential reversal zones with precision.

✨ Key Features :

🔁 Multi-Mode Analysis: Switch between Linear Regression , Strong/Weak Trend , or Volume MACD logic.

📐 Volume-Adjusted MACD: Incorporates volume for a more realistic momentum view.

📊 Linear Regression Signal: Smoother and more reactive trend analysis.

🎯 Dynamic Stdev Bands: Visualize ±1 and ±2 standard deviation thresholds for anomaly detection.

🌈 Custom Color Themes: Choose from built-in palettes or define your own bullish/bearish signal colors.

⚠️ Alert Conditions: Built-in alerts notify you of potential trend shifts across all signal modes.

📈 How It Works :

🧮 MACD Core: Uses volume-weighted price to generate fast and slow EMAs, forming the MACD and signal lines.

📉 Histogram Logic: Histogram is either the traditional MACD histogram or its linear regression version.

📊 Signal Modes:

• Linear Regression: Detect trend based on smoothed MACD behavior.

• Strong/Weak Trend: Identifies accelerating/decelerating trend strength.

• Volume MACD: Classic volume MACD behavior for divergence spotting.

📏 Stdev Bands: Calculated over a long period (default 200) to highlight statistically significant moves.

🎨 Color-coded Feedback: Bar and background colors adjust dynamically with market condition.

⚙️ Customization Options :

🔄 Choose your Signal Type from three unique analysis modes.

📏 Modify Fast/Slow/Signal lengths and Regression parameters to suit your strategy.

📈 Enable or disable Stdev Bands and adjust multiplier.

🎨 Select from Classic, Mystic, Accented, or Royal color palettes — or create your own.

📌 Use Cases :

🟢 Identify trend continuation or reversal zones with volume-adjusted signals.

🔴 Detect volatility breakouts using standard deviation bands.

🧭 Use in confluence with price structure, RSI, or market sentiment.

⚠️ Disclaimer :

This indicator is for educational purposes only. It is not financial advice. Always use in conjunction with your own research and risk management strategy.