GMMA + RVOL Hariss 369GMMA + RVOL Trend Strategy

This indicator combines Guppy Multiple Moving Averages (GMMA) with Relative Volume (RVOL) to identify high-probability trend continuation entries.

GMMA uses two groups of EMAs—short-term (3–15) and long-term (30–60).

When the short-term group stays above the long-term group, it indicates a bullish trend.

When short-term EMAs stay below the long-term group, the market is in a bearish trend.

To avoid weak and low-volume signals, the strategy uses RVOL. A trade signal only appears when volume is stronger than average, confirming participation from market players.

✔ Buy Signal

Short-term GMMA above long-term GMMA (bull trend)

RVOL > threshold

Price above short GMMA average

Shows only long SL and TP based on ATR

✔ Sell Signal

Short GMMA below long GMMA (bear trend)

RVOL > threshold

Price below short GMMA average

Shows only short SL and TP based on ATR

ATR-based stop-loss and take-profit levels help identify realistic volatility-adjusted exit zones while keeping the chart clean by displaying only the relevant SL/TP depending on market direction.

Further, background color has been given for clear visibility of market trend. One can use this indicator for any class of asset and in any time frame.

This indicator is for education purpose.

Educational

Trading Session IL7 Session-Based Intraday Momentum IndicatorOverview

This indicator is designed to support discretionary traders by highlighting intraday momentum phases based on price behavior and trading session context.

It is intended as a confirmation tool and not as a standalone trading system or automated strategy.

Core Concept

The script combines multiple market observations, including:

- Directional price behavior within the current timeframe

- Structural consistency in recent price movement

- Session-based filtering to focus on periods with higher activity and liquidity

Signals are only displayed when internal conditions align, helping traders avoid low-quality setups during sideways or low-momentum market phases.

How to Use

This indicator should be used to confirm existing trade ideas rather than generate trades on its own.

It can help traders:

- Identify periods where momentum is more likely to continue

- Filter out trades during unfavorable market conditions

- Align intraday execution with higher-timeframe bias

Best results are achieved when used alongside key price levels, higher-timeframe structure and proper risk management.

Limitations

This indicator does not predict future price movements.

Signals may change during active candles.

Market conditions may reduce effectiveness during extremely low volatility periods.

Language Notice

The indicator’s user interface labels are displayed in German.

This English description is provided first to comply with TradingView community script publishing rules.

n-Day Stock Return with MAs and SlopesThis indicator calculates the n-day percentage return of a stock and visualizes it either as a histogram or line, with optional moving averages (MA1 and MA2) of the return and their slopes. The script highlights trend changes in the slopes of these moving averages by drawing colored horizontal markers at each reversal point—green for upward slope shifts, red for downward shifts, and gray when the slope turns flat—allowing users to quickly identify strengthening, weakening, or neutral return trends over time. It also includes optional slope plots for additional trend context and a zero reference line for distinguishing positive and negative performance.

EMA Market Structure [BOSWaves]// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at mozilla.org

// Join our channel for more free tools: t.me

// This Pine Script® code is subject to the terms of the Mozilla Public License 2.0 at mozilla.org

// © BOSWaves

//@version=6

indicator("EMA Market Structure ", overlay=true, max_lines_count=500, max_labels_count=500, max_boxes_count=500)

// ============================================================================

// Inputs

// ============================================================================

// Ema settings

emaLength = input.int(50, "EMA Length", minval=1, tooltip="Period for the Exponential Moving Average calculation")

emaSource = input.source(close, "EMA Source", tooltip="Price source for EMA calculation (close, open, high, low, etc.)")

colorSmooth = input.int(3, "Color Smoothing", minval=1, group="EMA Style", tooltip="Smoothing period for the EMA color gradient transition")

showEmaGlow = input.bool(true, "EMA Glow Effect", group="EMA Style", tooltip="Display glowing halo effect around the EMA line for enhanced visibility")

// Structure settings

swingLength = input.int(5, "Swing Detection Length", minval=2, group="Structure", tooltip="Number of bars to the left and right to identify swing highs and lows")

swingCooloff = input.int(10, "Swing Marker Cooloff (Bars)", minval=1, group="Structure", tooltip="Minimum number of bars between consecutive swing point markers to reduce visual clutter")

showSwingLines = input.bool(true, "Show Structure Lines", group="Structure", tooltip="Display lines connecting swing highs and swing lows")

showSwingZones = input.bool(true, "Show Structure Zones", group="Structure", tooltip="Display shaded zones between consecutive swing points")

showBOS = input.bool(true, "Show Break of Structure", group="Structure", tooltip="Display BOS labels and stop loss levels when price breaks structure")

bosCooloff = input.int(15, "BOS Cooloff (Bars)", minval=5, maxval=50, group="Structure", tooltip="Minimum number of bars required between consecutive BOS signals to avoid signal spam")

slExtension = input.int(20, "SL Line Extension (Bars)", minval=5, maxval=100, group="Structure", tooltip="Number of bars to extend the stop loss line into the future for visibility")

slBuffer = input.float(0.1, "SL Buffer %", minval=0, maxval=2, step=0.05, group="Structure", tooltip="Additional buffer percentage to add to stop loss level for safety margin")

// Background settings

showBG = input.bool(true, "Show Trend Background", group="EMA Style", tooltip="Display background color based on EMA trend direction")

bgBullColor = input.color(color.new(#00ff88, 96), "Bullish BG", group="EMA Style", tooltip="Background color when EMA is in bullish trend")

bgBearColor = input.color(color.new(#ff3366, 96), "Bearish BG", group="EMA Style", tooltip="Background color when EMA is in bearish trend")

// ============================================================================

// Ema trend filter with gradient color

// ============================================================================

ema = ta.ema(emaSource, emaLength)

// Calculate EMA acceleration for gradient color

emaChange = ema - ema

emaAccel = ta.ema(emaChange, colorSmooth)

// Manual tanh function for normalization

tanh(x) =>

ex = math.exp(2 * x)

(ex - 1) / (ex + 1)

accelNorm = tanh(emaAccel / (ta.atr(14) * 0.01))

// Map normalized accel to hue (60 = green, 120 = yellow/red)

hueRaw = 60 + accelNorm * 60

hue = na(hueRaw ) ? hueRaw : (hueRaw + hueRaw ) / 2

sat = 1.0

val = 1.0

// HSV to RGB conversion

hsv_to_rgb(h, s, v) =>

c = v * s

x = c * (1 - math.abs((h / 60) % 2 - 1))

m = v - c

r = 0.0

g = 0.0

b = 0.0

if (h < 60)

r := c

g := x

b := 0

else if (h < 120)

r := x

g := c

b := 0

else if (h < 180)

r := 0

g := c

b := x

else if (h < 240)

r := 0

g := x

b := c

else if (h < 300)

r := x

g := 0

b := c

else

r := c

g := 0

b := x

color.rgb(int((r + m) * 255), int((g + m) * 255), int((b + m) * 255))

emaColor = hsv_to_rgb(hue, sat, val)

emaTrend = ema > ema ? 1 : ema < ema ? -1 : 0

// EMA with enhanced glow effect using fills

glowOffset = ta.atr(14) * 0.25

emaGlow8 = plot(showEmaGlow ? ema + glowOffset * 8 : na, "EMA Glow 8", color.new(emaColor, 100), 1, display=display.none)

emaGlow7 = plot(showEmaGlow ? ema + glowOffset * 7 : na, "EMA Glow 7", color.new(emaColor, 100), 1, display=display.none)

emaGlow6 = plot(showEmaGlow ? ema + glowOffset * 6 : na, "EMA Glow 6", color.new(emaColor, 100), 1, display=display.none)

emaGlow5 = plot(showEmaGlow ? ema + glowOffset * 5 : na, "EMA Glow 5", color.new(emaColor, 100), 1, display=display.none)

emaGlow4 = plot(showEmaGlow ? ema + glowOffset * 4 : na, "EMA Glow 4", color.new(emaColor, 100), 1, display=display.none)

emaGlow3 = plot(showEmaGlow ? ema + glowOffset * 3 : na, "EMA Glow 3", color.new(emaColor, 100), 1, display=display.none)

emaGlow2 = plot(showEmaGlow ? ema + glowOffset * 2 : na, "EMA Glow 2", color.new(emaColor, 100), 1, display=display.none)

emaGlow1 = plot(showEmaGlow ? ema + glowOffset * 1 : na, "EMA Glow 1", color.new(emaColor, 100), 1, display=display.none)

emaCore = plot(ema, "EMA Core", emaColor, 3)

emaGlow1b = plot(showEmaGlow ? ema - glowOffset * 1 : na, "EMA Glow 1b", color.new(emaColor, 100), 1, display=display.none)

emaGlow2b = plot(showEmaGlow ? ema - glowOffset * 2 : na, "EMA Glow 2b", color.new(emaColor, 100), 1, display=display.none)

emaGlow3b = plot(showEmaGlow ? ema - glowOffset * 3 : na, "EMA Glow 3b", color.new(emaColor, 100), 1, display=display.none)

emaGlow4b = plot(showEmaGlow ? ema - glowOffset * 4 : na, "EMA Glow 4b", color.new(emaColor, 100), 1, display=display.none)

emaGlow5b = plot(showEmaGlow ? ema - glowOffset * 5 : na, "EMA Glow 5b", color.new(emaColor, 100), 1, display=display.none)

emaGlow6b = plot(showEmaGlow ? ema - glowOffset * 6 : na, "EMA Glow 6b", color.new(emaColor, 100), 1, display=display.none)

emaGlow7b = plot(showEmaGlow ? ema - glowOffset * 7 : na, "EMA Glow 7b", color.new(emaColor, 100), 1, display=display.none)

emaGlow8b = plot(showEmaGlow ? ema - glowOffset * 8 : na, "EMA Glow 8b", color.new(emaColor, 100), 1, display=display.none)

// Create glow layers with fills (from outermost to innermost)

fill(emaGlow8, emaGlow7, showEmaGlow ? color.new(emaColor, 97) : na)

fill(emaGlow7, emaGlow6, showEmaGlow ? color.new(emaColor, 95) : na)

fill(emaGlow6, emaGlow5, showEmaGlow ? color.new(emaColor, 93) : na)

fill(emaGlow5, emaGlow4, showEmaGlow ? color.new(emaColor, 90) : na)

fill(emaGlow4, emaGlow3, showEmaGlow ? color.new(emaColor, 87) : na)

fill(emaGlow3, emaGlow2, showEmaGlow ? color.new(emaColor, 83) : na)

fill(emaGlow2, emaGlow1, showEmaGlow ? color.new(emaColor, 78) : na)

fill(emaGlow1, emaCore, showEmaGlow ? color.new(emaColor, 70) : na)

fill(emaCore, emaGlow1b, showEmaGlow ? color.new(emaColor, 70) : na)

fill(emaGlow1b, emaGlow2b, showEmaGlow ? color.new(emaColor, 78) : na)

fill(emaGlow2b, emaGlow3b, showEmaGlow ? color.new(emaColor, 83) : na)

fill(emaGlow3b, emaGlow4b, showEmaGlow ? color.new(emaColor, 87) : na)

fill(emaGlow4b, emaGlow5b, showEmaGlow ? color.new(emaColor, 90) : na)

fill(emaGlow5b, emaGlow6b, showEmaGlow ? color.new(emaColor, 93) : na)

fill(emaGlow6b, emaGlow7b, showEmaGlow ? color.new(emaColor, 95) : na)

fill(emaGlow7b, emaGlow8b, showEmaGlow ? color.new(emaColor, 97) : na)

// ============================================================================

// Swing high/low detection

// ============================================================================

// Swing High/Low Detection

swingHigh = ta.pivothigh(high, swingLength, swingLength)

swingLow = ta.pivotlow(low, swingLength, swingLength)

// Cooloff tracking

var int lastSwingHighPlot = na

var int lastSwingLowPlot = na

// Check if cooloff period has passed

canPlotHigh = na(lastSwingHighPlot) or (bar_index - lastSwingHighPlot) >= swingCooloff

canPlotLow = na(lastSwingLowPlot) or (bar_index - lastSwingLowPlot) >= swingCooloff

// Store swing points

var float lastSwingHigh = na

var int lastSwingHighBar = na

var float lastSwingLow = na

var int lastSwingLowBar = na

// Track previous swing for BOS detection

var float prevSwingHigh = na

var float prevSwingLow = na

// Update swing highs with cooloff

if not na(swingHigh) and canPlotHigh

prevSwingHigh := lastSwingHigh

lastSwingHigh := swingHigh

lastSwingHighBar := bar_index - swingLength

lastSwingHighPlot := bar_index

// Update swing lows with cooloff

if not na(swingLow) and canPlotLow

prevSwingLow := lastSwingLow

lastSwingLow := swingLow

lastSwingLowBar := bar_index - swingLength

lastSwingLowPlot := bar_index

// ============================================================================

// Structure lines & zones

// ============================================================================

var line swingHighLine = na

var line swingLowLine = na

var box swingHighZone = na

var box swingLowZone = na

if showSwingLines

// Draw line connecting swing highs with zones

if not na(swingHigh) and canPlotHigh and not na(prevSwingHigh)

if not na(lastSwingHighBar)

line.delete(swingHighLine)

swingHighLine := line.new(lastSwingHighBar, lastSwingHigh, bar_index - swingLength, swingHigh, color=color.new(#ff3366, 0), width=2, style=line.style_solid)

// Create resistance zone

if showSwingZones

box.delete(swingHighZone)

zoneTop = math.max(lastSwingHigh, swingHigh)

zoneBottom = math.min(lastSwingHigh, swingHigh)

swingHighZone := box.new(lastSwingHighBar, zoneTop, bar_index - swingLength, zoneBottom, border_color=color.new(#ff3366, 80), bgcolor=color.new(#ff3366, 92))

// Draw line connecting swing lows with zones

if not na(swingLow) and canPlotLow and not na(prevSwingLow)

if not na(lastSwingLowBar)

line.delete(swingLowLine)

swingLowLine := line.new(lastSwingLowBar, lastSwingLow, bar_index - swingLength, swingLow, color=color.new(#00ff88, 0), width=2, style=line.style_solid)

// Create support zone

if showSwingZones

box.delete(swingLowZone)

zoneTop = math.max(lastSwingLow, swingLow)

zoneBottom = math.min(lastSwingLow, swingLow)

swingLowZone := box.new(lastSwingLowBar, zoneTop, bar_index - swingLength, zoneBottom, border_color=color.new(#00ff88, 80), bgcolor=color.new(#00ff88, 92))

// ============================================================================

// Break of structure (bos)

// ============================================================================

// Track last BOS bar for cooloff

var int lastBullishBOS = na

var int lastBearishBOS = na

// Check if cooloff period has passed

canPlotBullishBOS = na(lastBullishBOS) or (bar_index - lastBullishBOS) >= bosCooloff

canPlotBearishBOS = na(lastBearishBOS) or (bar_index - lastBearishBOS) >= bosCooloff

// Bullish BOS: Price breaks above previous swing high while EMA is bullish

bullishBOS = showBOS and canPlotBullishBOS and emaTrend == 1 and not na(prevSwingHigh) and close > prevSwingHigh and close <= prevSwingHigh

// Bearish BOS: Price breaks below previous swing low while EMA is bearish

bearishBOS = showBOS and canPlotBearishBOS and emaTrend == -1 and not na(prevSwingLow) and close < prevSwingLow and close >= prevSwingLow

// Update last BOS bars

if bullishBOS

lastBullishBOS := bar_index

if bearishBOS

lastBearishBOS := bar_index

// Plot BOS with enhanced visuals and SL at the candle wick

if bullishBOS

// Calculate SL at the low of the current candle (bottom of wick) with buffer

slLevel = low * (1 - slBuffer/100)

// BOS Label with shadow effect

label.new(bar_index, low, "BOS", style=label.style_label_up, color=color.new(#00ff88, 0), textcolor=color.black, size=size.normal, tooltip="Bullish Break of Structure SL: " + str.tostring(slLevel))

// Main SL line at candle low

line.new(bar_index, slLevel, bar_index + slExtension, slLevel, color=color.new(#00ff88, 0), width=2, style=line.style_dashed, extend=extend.none)

// SL zone box for visual emphasis

box.new(bar_index, slLevel + (slLevel * 0.002), bar_index + slExtension, slLevel - (slLevel * 0.002), border_color=color.new(#00ff88, 60), bgcolor=color.new(#00ff88, 85))

// S/R label

label.new(bar_index + slExtension, slLevel, "S/R", style=label.style_label_left, color=color.new(#00ff88, 0), textcolor=color.black, size=size.tiny)

if bearishBOS

// Calculate SL at the high of the current candle (top of wick) with buffer

slLevel = high * (1 + slBuffer/100)

// BOS Label with shadow effect

label.new(bar_index, high, "BOS", style=label.style_label_down, color=color.new(#ff3366, 0), textcolor=color.white, size=size.normal, tooltip="Bearish Break of Structure SL: " + str.tostring(slLevel))

// Main SL line at candle high

line.new(bar_index, slLevel, bar_index + slExtension, slLevel, color=color.new(#ff3366, 0), width=2, style=line.style_dashed, extend=extend.none)

// SL zone box for visual emphasis

box.new(bar_index, slLevel + (slLevel * 0.002), bar_index + slExtension, slLevel - (slLevel * 0.002), border_color=color.new(#ff3366, 60), bgcolor=color.new(#ff3366, 85))

// S/R label

label.new(bar_index + slExtension, slLevel, "S/R", style=label.style_label_left, color=color.new(#ff3366, 0), textcolor=color.white, size=size.tiny)

// ============================================================================

// Dynamic background zones

// ============================================================================

bgcolor(showBG and emaTrend == 1 ? bgBullColor : showBG and emaTrend == -1 ? bgBearColor : na)

// ============================================================================

// Alerts

// ============================================================================

alertcondition(bullishBOS, "Bullish BOS", "Bullish Break of Structure detected!")

alertcondition(bearishBOS, "Bearish BOS", "Bearish Break of Structure detected!")

alertcondition(emaTrend == 1 and emaTrend != 1, "EMA Bullish", "EMA turned bullish")

alertcondition(emaTrend == -1 and emaTrend != -1, "EMA Bearish", "EMA turned bearish")

// ╔════════════════════════════════╗

// ║ Download at ║

// ╚════════════════════════════════╝

// ███████╗██╗███╗ ███╗██████╗ ██╗ ███████╗

// ██╔════╝██║████╗ ████║██╔══██╗██║ ██╔════╝

// ███████╗██║██╔████╔██║██████╔╝██║ █████╗

// ╚════██║██║██║╚██╔╝██║██╔═══╝ ██║ ██╔══╝

// ███████║██║██║ ╚═╝ ██║██║ ███████╗███████╗

// ╚══════╝╚═╝╚═╝ ╚═╝╚═╝ ╚══════╝╚══════╝

// ███████╗ ██████╗ ██████╗ ███████╗██╗ ██╗

// ██╔════╝██╔═══██╗██╔══██╗██╔════╝╚██╗██╔╝

// █████╗ ██║ ██║██████╔╝█████╗ ╚███╔╝

// ██╔══╝ ██║ ██║██╔══██╗██╔══╝ ██╔██╗

// ██║ ╚██████╔╝██║ ██║███████╗██╔╝ ██╗

// ╚═╝ ╚═════╝ ╚═╝ ╚═╝╚══════╝╚═╝ ╚═╝

// ████████╗ ██████╗ ██████╗ ██╗ ███████╗

// ╚══██╔══╝██╔═══██╗██╔═══██╗██║ ██╔════╝

// ██║ ██║ ██║██║ ██║██║ ███████╗

// ██║ ██║ ██║██║ ██║██║ ╚════██║

// ██║ ╚██████╔╝╚██████╔╝███████╗███████║

// ╚═╝ ╚═════╝ ╚═════╝ ╚══════╝╚══════╝

// ==========================================================================================

Multi-Condition Alert System d//@version=5

indicator("Multi-Condition Alert System", shorttitle="MC Alert", overlay=false)

// Timeframe check - Set to 10 minutes

isCorrectTF = timeframe.isintraday and timeframe.multiplier == 10

// EMA Calculations

ema9 = ta.ema(close, 9)

ema21 = ta.ema(close, 21)

ema50 = ta.ema(close, 50)

// MACD Calculations

= ta.macd(close, 12, 26, 9)

// RSI Calculations

rsiValue = ta.rsi(close, 14)

// Define RSI levels (you can adjust these based on your violet/yellow lines)

// Assuming violet is above 50 and yellow is below 50

rsiVioletLevel = 50 // Adjust based on your actual levels

rsiYellowLevel = 50 // Adjust based on your actual levels

// Conditions

emaCondition = ema9 > ema21 and ema9 > ema50

macdCondition = macdLine > signalLine

rsiCondition = rsiValue > rsiVioletLevel and rsiValue > rsiYellowLevel

// All conditions must be true

buySignal = emaCondition and macdCondition and rsiCondition and isCorrectTF

// Plotting for visualization

plot(ema9, color=color.blue, title="EMA 9")

plot(ema21, color=color.orange, title="EMA 21")

plot(ema50, color=color.red, title="EMA 50")

plot(macdLine, color=color.blue, title="MACD Line", style=plot.style_line)

plot(signalLine, color=color.orange, title="Signal Line", style=plot.style_line)

hline(rsiVioletLevel, "RSI Violet Level", color=color.purple)

hline(rsiYellowLevel, "RSI Yellow Level", color=color.yellow)

plot(rsiValue, color=color.white, title="RSI")

// Plot buy signals

plotshape(buySignal ? 1 : na, title="Buy Signal", location=location.bottom,

color=color.green, style=shape.triangleup, size=size.small)

// Alert condition

if buySignal

alert("BUY SIGNAL: EMA 9 > EMA 21 & 50, MACD blue > orange, RSI above levels", alert.freq_once_per_bar)

// Table display

var table signalTable = table.new(position.top_right, 1, 5, bgcolor=color.black,

border_width=1)

if barstate.islast

table.cell(signalTable, 0, 0, "10min TF Check:",

text_color=isCorrectTF ? color.green : color.red)

table.cell(signalTable, 0, 1, "EMA 9 > 21 & 50:",

text_color=emaCondition ? color.green : color.red)

table.cell(signalTable, 0, 2, "MACD Blue > Orange:",

text_color=macdCondition ? color.green : color.red)

table.cell(signalTable, 0, 3, "RSI Condition:",

text_color=rsiCondition ? color.green : color.red)

table.cell(signalTable, 0, 4, "BUY SIGNAL:",

text_color=buySignal ? color.green : color.red)

Bayesian Liquidity Pain & Gain [Instit. Vol Weighted]Bayesian Liquidity Pain & Gain Indicator

Stop guessing where support and resistance are.

The Bayesian Liquidity Pain & Gain indicator moves beyond arbitrary lines and raw price action. It quantifies Institutional Intent by calculating the exact price levels where large volume has been accumulated and visualizes the "Pain" (stress) those participants feel when the market moves against them.

The Logic: Quantified Institutional Stress

Institutions don't trade single candles; they accumulate positions over time. This indicator tracks their Volume-Weighted Average Cost Basis to answer two critical questions:

Where did they enter? (The Cost Basis Lines)

Are they underwater? (The Pain Clouds)

By normalizing price distance using volatility (ATR) and statistical deviation (Z-Score), we filter out noise and only highlight zones where "Smart Money" is statistically forced to defend their positions or capitulate.

How to Read the Chart

1. The Cost Basis Lines (Anchors)

• 🟢 Green Line (Buyer Cost Basis): The average price where institutions accumulated long positions. This acts as dynamic Support.

• 🔴 Red Line (Seller Cost Basis): The average price where institutions accumulated short positions. This acts as dynamic Resistance.

2. The Pain Clouds (Signals)

When price moves significantly away from the cost basis (Z-Score > 2.0), "Clouds" appear to visualize the PnL status of the participants:

• 🔴 Red Cloud (Buyer Pain): Price is below the buyer's entry. Buyers are losing money (in the red). This creates a "Discount" zone where they may defend support.

• 🟢 Green Cloud (Seller Pain): Price is above the seller's entry. Sellers are losing money (shorts are squeezed). This indicates strong bullish momentum.

3. The Multi-Timeframe Dashboard

A real-time HUD showing the Z-Score status across 4 timeframes (1m, 5m, 15m, 1h):

• 🟢 Green: Profitable/Neutral (Trend Continuation)

• 🟠 Orange: Warning (Pressure Building)

• 🔴 Red: Critical Pain (High Probability Reversal)

Trading Strategies

Setup 1: The Defensive Bounce (Long)

• Context: Price drops into a 🔴 Red Cloud (Buyer Pain).

• Trigger: Price touches the 🟢 Green Line (Buyer Cost Basis) and shows a rejection wick.

• Logic: Institutional buyers defend their cost basis to avoid realizing losses.

Setup 2: The Short Squeeze (Momentum)

• Context: Price rallies into a 🟢 Green Cloud (Seller Pain).

• Trigger: Price holds above the 🔴 Red Line (Seller Cost Basis).

• Logic: Short sellers are trapped and forced to buy back (cover), fueling the rally.

Fractal Alignment:

For high-conviction trades, wait for the Dashboard to show "Pain" signals on both the 1h (Anchor) and 5m (Trigger) timeframes simultaneously.

Settings

• Memory Length (Default 144): The lookback period for the institutional cost basis. Increase for swing trading, decrease for scalping.

• Sigma Threshold (Default 2.0): The statistical confidence level for "Pain". Higher values = fewer, stronger signals.

• Volume Amp: When enabled, high volume amplifies the pain signal, giving more weight to institutional footprints.

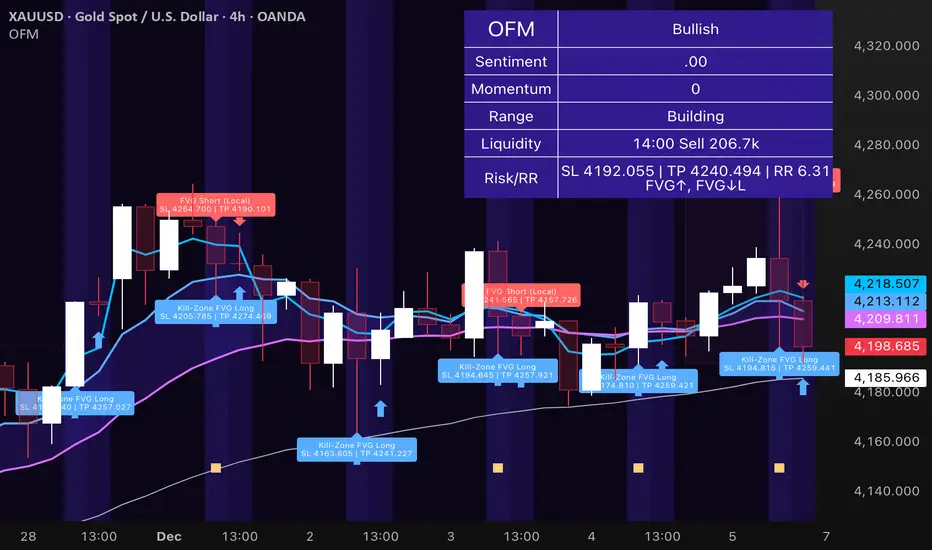

Obsidian Flux Matrix# Obsidian Flux Matrix | JackOfAllTrades

Made with my Senior Level AI Pine Script v6 coding bot for the community!

Narrative Overview

Obsidian Flux Matrix (OFM) is an open-source Pine Script v6 study that fuses social sentiment, higher timeframe trend bias, fair-value-gap detection, liquidity raids, VWAP gravitation, session profiling, and a diagnostic HUD. The layout keeps the obsidian palette so critical overlays stay readable without overwhelming a price chart.

Purpose & Scope

OFM focuses on actionable structure rather than marketing claims. It documents every driver that powers its confluence engine so reviewers understand what triggers each visual.

Core Analytical Pillars

1. Social Pulse Engine

Sentiment Webhook Feed: Accepts normalized scores (-1 to +1). Signals only arm when the EMA-smoothed value exceeds the `sentimentMin` input (0.35 by default).

Volume Confirmation: Requires local volume > 30-bar average × `volSpikeMult` (default 2.0) before sentiment flags.

EMA Cross Validation: Fast EMA 8 crossing above/below slow EMA 21 keeps momentum aligned with flow.

Momentum Alignment: Multi-timeframe momentum composite must agree (positive for longs, negative for shorts).

2. Peer Momentum Heatmap

Multi-Timeframe Blend: RSI + Stoch RSI fetched via request.security() on 1H/4H/1D by default.

Composite Scoring: Each timeframe votes +1/-1/0; totals are clamped between -3 and +3.

Intraday Readability: Configurable band thickness (1-5) so scalpers see context without losing space.

Dynamic Opacity: Stronger agreement boosts column opacity for quick bias checks.

3. Trend & Displacement Framework

Dual EMA Ribbon: Cyan/magenta ribbon highlights immediate posture.

HTF Bias: A higher-timeframe EMA (default 55 on 4H) sets macro direction.

Displacement Score: Body-to-ATR ratio (>1.4 default) detects impulses that seed FVGs or VWAP raids.

ATR Normalization: All thresholds float with volatility so the study adapts to assets and regimes.

4. Intelligent Fair Value Gap (FVG) System

Gap Detection: Three-candle logic (bullish: low > high ; bearish: high < low ) with ATR-sized minimums (0.15 × ATR default).

Overlap Prevention: Price-range checks stop redundant boxes.

Spacing Control: `fvgMinSpacing` (default 5) avoids stacking from the same impulse.

Storage Caps: Max three FVGs per side unless the user widens the limit.

Session Awareness: Kill zone filters keep taps focused on London/NY if desired.

Auto Cleanup: Boxes delete when price closes beyond their invalidation level.

5. VWAP Magnet + Liquidity Raid Engine

Session or Rolling VWAP: Toggle resets to match intraday or rolling preferences.

Equal High/Low Scanner: Looks back 20 bars by default for liquidity pools.

Displacement Filter: ATR multiplier ensures raids represent genuine liquidity sweeps.

Mean Reversion Focus: Signals fire when price displaces back toward VWAP following a raid.

6. Session Range Breakout System

Initial Balance Tracking: First N bars (15 default) define the session box.

Breakout Logic: Requires simultaneous liquidity spikes, nearby FVG activity, and supportive momentum.

Z-Score Volume Filter: >1.5σ by default to filter noisy moves.

7. Lifestyle Liquidity Scanner

Volume Z-Scores: 50-bar baseline highlights statistically significant spikes.

Smart Money Footprints: Bottom-of-chart squares color-code buy vs sell participation.

Panel Memory: HUD logs the last five raid timestamps, direction, and normalized size.

8. Risk Matrix & Diagnostic HUD

HUD Structure: Table in the top-right summarizes HTF bias, sentiment, momentum, range state, liquidity memory, and current risk references.

Signal Tags: Aggregates SPS, FVG, VWAP, Range, and Liquidity states into a compact string.

Risk Metrics: Swing-based stops (5-bar lookback) + ATR targets (1.5× default) keep risk transparent.

Signal Families & Alerts

Social Pulse (SPS): Volume-confirmed sentiment alignment; triangle markers with “SPS”.

Kill-Zone FVG: Session + HTF alignment + FVG tap; arrow markers plus SL/TP labels.

Local FVG: Captures local reversals when HTF bias has not flipped yet.

VWAP Raid: Equal-high/low raids that snap toward VWAP; “VWAP” label markers.

Range Breakout: Initial balance violations with liquidity and imbalance confirmation; circle markers.

Liquidity Spike: Z-score spikes ≥ threshold; square markers along the baseline.

Visual Design & Customization

Theme Palette: Primary background RGB (12,6,24). Accent shading RGB (26,10,48). Long accents RGB (88,174,255). Short accents RGB (219,109,255).

Stylized Candles: Optional overlay using theme colors.

Signal Toggles: Independently enable markers, heatmap, and diagnostics.

Label Spacing: Auto-spacing enforces ≥4-bar gaps to prevent text overlap.

Customization & Workflow Notes

Adjust ATR/FVG thresholds when volatility shifts.

Re-anchor sentiment to your webhook cadence; EMA smoothing (default 5) dampens noise.

Reposition the HUD by editing the `table.new` coordinates.

Use multiples of the chart timeframe for HTF requests to minimize load.

Session inputs accept exchange-local time; align them to your market.

Performance & Compliance

Pure Pine v6: Single-line statements, no `lookahead_on`.

Resource Safe: Arrays trimmed, boxes limited, `request.security` cached.

Repaint Awareness: Signals confirm on close; alerts mirror on-chart logic.

Runtime Safety: Arrays/loops guard against `na`.

Use Cases

Measure when social sentiment aligns with structure.

Plan ICT-style intraday rebalances around session-specific FVG taps.

Fade VWAP raids when displacement shows exhaustion.

Watch initial balance breaks backed by statistical volume.

Keep risk/target references anchored in ATR logic.

Signal Logic Snapshot

Social Pulse Long/Short: `sentimentEMA` gated by `sentimentMin`, `volSpike`, EMA 8/21 cross, and `momoComposite` sign agreement. Keeps hype tied to structural follow-through.

Kill-Zone FVG Long/Short: Requires session filter, HTF EMA bias alignment, and an active FVG tap (`bullFvgTap` / `bearFvgTap`). Labels include swing stops + ATR targets pulled from `swingLookback` and `liqTargetMultiple`.

Local FVG Long/Short: Uses `localBullish` / `localBearish` heuristics (EMA slope, displacement, sequential closes) to surface intraday reversals even when HTF bias has not flipped.

VWAP Raids: Detect equal-high/equal-low sweeps (`raidHigh`, `raidLow`) that revert toward `sessionVwap` or rolling VWAP when displacement exceeds `vwapAlertDisplace`.

Range Breakouts: Combine `rangeComplete`, breakout confirmation, liquidity spikes, and nearby FVG activity for statistically backed initial balance breaks.

Liquidity Spikes: Volume Z-score > `zScoreThreshold` logs direction, size, and timestamp for the HUD and optional review workflows.

Session Logic & VWAP Handling

Kill zone + NY session inputs use TradingView’s session strings; `f_inSession()` drives both visual shading and whether FVG taps are tradeable when `killZoneOnly` is true.

Session VWAP resets using cumulative price × volume sums that restart when the daily timestamp changes; rolling VWAP falls back to `ta.vwap(hlc3)` for instruments where daily resets are less relevant.

Initial balance box (`rangeBars` input) locks once complete, extends forward, and stays on chart to contextualize later liquidity raids or breakouts.

Parameter Reference

Trend: `emaFastLen`, `emaSlowLen`, `htfResolution`, `htfEmaLen`, `showEmaRibbon`, `showHtfBiasLine`.

Momentum: `tf1`, `tf2`, `tf3`, `rsiLen`, `stochLen`, `stochSmooth`, `heatmapHeight`.

Volume/Liquidity: `volLookback`, `volSpikeMult`, `zScoreLen`, `zScoreThreshold`, `equalLookback`.

VWAP & Sessions: `vwapMode`, `showVwapLine`, `vwapAlertDisplace`, `killSession`, `nySession`, `showSessionShade`, `rangeBars`.

FVG/Risk: `fvgMinTicks`, `fvgLookback`, `fvgMinSpacing`, `killZoneOnly`, `liqTargetMultiple`, `swingLookback`.

Visualization Toggles: `showSignalMarkers`, `showHeatmapBand`, `showInfoPanel`, `showStylizedCandles`.

Workflow Recipes

Kill-Zone Continuation: During the defined kill session, look for `killFvgLong` or `killFvgShort` arrows that line up with `sentimentValid` and positive `momoComposite`. Use the HUD’s risk readout to confirm SL/TP distances before entering.

VWAP Raid Fade: Outside kill zone, track `raidToVwapLong/Short`. Confirm the candle body exceeds the displacement multiplier, and price crosses back toward VWAP before considering reversions.

Range Break Monitor: After the initial balance locks, mark `rangeBreakLong/Short` circles only when the momentum band is >0 or <0 respectively and a fresh FVG box sits near price.

Liquidity Spike Review: When the HUD shows “Liquidity” timestamps, hover the plotted squares at chart bottom to see whether spikes were buy/sell oriented and if local FVGs formed immediately after.

Metadata

Author: officialjackofalltrades

Platform: TradingView (Pine Script v6)

Category: Sentiment + Liquidity Intelligence

Hope you Enjoy!

FCPO MASTER v6 – Sideway + Breakout + OB + FVG (TUPLE SAFE)TL;DR cepat

1. Gunakan M5 untuk entry & OB/FVG confirmation.

2. Gunakan M15 untuk confirm trend/false breakout.

3. Gunakan H1 untuk bias arah (overall market).

4. Entry hanya bila signal + OB/FVG/candle rejection (script buatkan).

5. SL 5–8 tick, TP 10–25 tick ikut setup (sideway vs breakout).

6. Follow checklist setiap trade — jangan lompat.

________________________________________

Setup awal (1–2 min)

1. Pasang script FCPO Sideway MASTER – OB + Imbalance + Confirmation di TradingView.

2. Timeframes: buka M5, M15, H1 (susun 3 chart atau 1 chart multi-timeframe).

3. Input default: ATR14, Breakout Buffer 5 tick, RangeLen 20, ADX14, TP12, SL8. (Kau boleh tweak nanti).

4. Aktifkan alerts pada BUY Confirm / SELL Confirm / Sideway Buy / Sideway Sell.

________________________________________

Step-by-step trading process

1) Mulakan dengan H1 — tentukan bias HTF

• Lihat H1 untuk jawapan: Trend Up / Down / Sideway.

• Rule ringkas:

o ADX H1 > 20 + price above H1 EMA → bias Bull

o ADX H1 > 20 + price below H1 EMA → bias Bear

o ADX H1 < 20 → market HTF sideway (no strong bias)

Kenapa: H1 bagi kau idea “kalau breakout pada M5, patut follow atau tolak”.

________________________________________

2) Pergi ke M15 — confirm trend & valid breakout

• M15 kena setuju dengan idea breakout.

o Untuk strong breakout: M15 kena tunjuk candle close di atas/bawah range + volume naik.

o Kalau M5 breakout tapi M15 tak setuju (M15 masih sideway) → treat as fakeout. Jangan masuk.

________________________________________

3) M5 — cari entry & confirmation (OB/FVG + candle)

• M5 adalah tempat kau buat keputusan masuk.

• Tunggu script keluarkan Sideway Buy/Sell atau Breakout Buy/Sell.

• CONFIRM entry mesti ada sekurang-kurangnya 1 dari:

o Bull/Bear Order Block searah signal (script detect).

o FVG / Imbalance zone dipenuhi & price retest.

o Candle rejection (pinbar / bearish/bullish engulfing) pada zone.

Jika tiada confirmation → no trade.

________________________________________

4) Checklist sebelum tekan Buy/Sell (MUST)

• H1 bias tidak melawan trade (prefer sama arah).

• M15 confirm breakout / trend or neutral.

• Script keluarkan signal (sideway or breakout).

• OB or FVG atau candle rejection ada.

• ATR kenaikan jika breakout (untuk breakout trade).

• Volume spike jika breakout.

• Risk:SL <= 2% akaun (position sizing).

Kalau semua ticked → boleh entry.

________________________________________

5) Setting SL / TP & position sizing

• Sideway (scalp): SL = 5–8 tick, TP = 8–12 tick.

• Breakout (trend): SL = 8–12 tick, TP = 15–25+ tick (trail later).

• Position sizing: Risk per trade 1–2%.

o Lot size = (Account Risk RM × 1 tick value) / (SL ticks × tickValue) — (kalau kau gunakan fixed tick value, adjust ikut lot).

(Script tunjuk SL & TP label — follow itu.)

________________________________________

6) Entry types

• A. Sideway Reversal (M5)

o Signal: Sideway Buy / Sideway Sell

o Confirm: OB/FVG or rejection candle at range bottom/top

o Trade: scalp target 8–12 tick, tight SL 5–8 tick

• B. Breakout (M5 entry, M15 confirm)

o Signal: Breakout Buy/Sell (Strong)

o Confirm: ATR expanding + volume spike + M15 alignment

o Trade: trend follow, TP 15–25 tick, trailing stop active

• C. Retest Entry

o Breakout happens, price returns to retest range / OB / FVG → wait for rejection candle then enter. Safer.

________________________________________

7) Trailing & exit rules

• Jika useTrail = true script plots trailing stop (ATR × multiplier).

• Exit rules:

1. Hit TP → close.

2. Hit SL → close.

3. If trailing stop hit → close.

4. If opposing confirmed signal muncul (e.g., SELL confirm while long) → consider close early.

5. If H1 bias flips strongly vs trade → tighten stop or close.

________________________________________

8) Multiple signals & scaling

• Never add to losing position (no averaging down).

• If want scale-in on confirmed trend: add 1 partial size after price moves +10–12 tick in favor and shows continuation candle + no bearish OB/FVG.

• Keep aggregated risk within your max (2–3%).

________________________________________

9) Example trade walkthrough (concrete)

• RangeHigh = 4065, RangeLow = 4035 (contoh).

• Market sideway M5.

Case A — Sideway Sell:

1. Price touches 4064–4065, script shows sidewaySell.

2. Lihat OB: ada bear OB zone di 4062–4066 → confirm.

3. Candle rejection (bearish pinbar) muncul → enter SELL M5.

4. Set SL = 5 tick above rangeHigh = 4070, TP = 10 tick → 4055.

5. Trail jika price turun > 8 tick: aktifkan trailing.

6. Close at TP or trail/SL.

Case B — Breakout Buy:

1. Price closes above 4065 + 5 tick buffer = 4070 on M5. Script shows trueBreakUp.

2. M15 shows candle close above M15 resistance + volume spike → confirm.

3. Enter BUY, SL = 8 tick below entry, TP initial 20 tick, trail with ATR×1.5.

4. Move stop to breakeven after +10 tick, scale out half at +12 tick, leave rest to trail.

________________________________________

10) Journal & review

• Semua trade: record entry time, TF, reason (which confirmations), SL/TP, result, lesson.

• Weekly review: check which confirmation worked best (OB vs FVG vs candle) and tweak settings.

________________________________________

11) Tweaks / optimisations cepat

• Jika terlalu banyak false sideway signals → kurangkan touchDist ke 2 tick.

• Kalau fakeout breakout banyak → tambah tickBuf ke 6–8.

• Nak lebih konservatif → cuma trade breakout yang juga setuju M15.

________________________________________

12) Alerts & execution (practical)

• Pasang alert pada BUY Confirm / SELL Confirm (script).

• Kalau kau guna broker yang support one-click order, siap sediakan template order (SL/TP default).

• Kalau manual, bila alert masuk: buka M5, cepat confirm OB/FVG & candle rejection → entry.

________________________________________

Quick reference table (handy)

• TF utama entry: M5

• Confirm mid-TF: M15

• Bias HTF: H1

• Sideway SL/TP: SL 5–8, TP 8–12

• Breakout SL/TP: SL 8–12, TP 15–25+

• Mandatory confirmation: (Script signal) + (OB or FVG or candle)

Pharma vs Market Monthly Returns (XLV vs SPY)A Bloomberg-style pharma momentum indicator built for TradingView.

This script recreates the “Pharma Index Monthly Returns” chart highlighted by Jordi Visser in his Youtube video — offering a clean, accessible poor man’s Bloomberg version of sector-rotation analysis for users without institutional data feeds.

Features

• XLV monthly returns (absolute mode)

• XLV vs SPY relative monthly returns (market-neutral mode)

• Top 5 strongest months ★ (momentum spikes)

• Top 5 weakest months ★ (capitulation signals)

• Optional 6-month rolling momentum line (regime trend)

• Full history from 1998 (XLV inception)

Use Cases

Ideal for tracking pharma/healthcare sector regimes, macro rotations, biotech cycles, and timing asymmetric entries in innovation themes (AI-pharma, computational drug discovery, biotech moonshots, etc.).

The Quantum Leap: Renko + ML(Note: This indicator uses the BackQuant & SuperTrend which takes a 4-5 seconds to load)

This strategy uses the following indicators (please see source code)

Synthetic Renko: Ignores time and focuses purely on price movement to detect clear trend reversals (Red-to-Green).

ATR (Average True Range): Measures volatility to calculate the Renko brick sizes and SuperTrend sensitivity.

Adaptive SuperTrend: A trend filter that uses volatility clustering to confirm if the market is currently in a "Bearish" state.

RSI (Relative Strength Index): A momentum gauge ensuring the asset is "Oversold" (exhausted) before we consider a setup.

Monthly Pivots: Horizontal support lines based on last month's data acting as price "floors" (S1, S2, S3).

SMA (Simple Moving Average): A 100-bar average ensuring we are strictly buying below the long-term mean (deep value).

BackQuant (KNN): A Machine Learning engine that compares current data to historical patterns to predict immediate momentum.

This is a sophisticated, multi-stage strategy script. It combines "Old School" price action (Renko) with "New School" Machine Learning (KNN and Clustering).

Here is the high-level summary of how we will break this down:

Topic 1: The "Bottom Hunter" Setup. How the script uses Renko bricks and aggressive filtering (SuperTrend, SMA, RSI, Pivots) to find a potential market bottom.

Topic 2: The ML Engine (BackQuant & SuperTrend). How the script uses K-Nearest Neighbors (KNN) to predict momentum and Volatility Clustering to adjust the SuperTrend.

Topic 3: The "Leap" Execution. How the script synchronizes the Setup (Topic 1) with the ML Trigger (Topic 2) using a time window.

Topic 1: The "Bottom Hunter" Setup

This script is designed as a Mean Reversion strategy (often called "catching a falling knife" or "bottom fishing"). It is trying to find the exact moment a downtrend stops and reverses.

Most strategies buy when price is above the 200 SMA or above the SuperTrend. This script does the exact opposite.

The Logic:

Renko Bricks: It simulates Renko bricks internally (without changing your chart view). It waits for a specific pattern: A Red Brick followed immediately by a Green Brick (a reversal).

The "Bearish" Filters: To generate a "WATCH" signal, the following must be true:

Price < SuperTrend: The market must officially be in a downtrend.

Price < SMA: Long-term trend is down.

Price < Monthly Pivot: Price is deeply discounted.

RSI < Threshold: The asset is oversold (exhausted).

Recommended Settings for daily signals for Stocks :

Confirmation : 10. (How many bars after Renko Buy signal the AI has to identify a bullish move).

Percentage : 2 (This is the Renko bar size. This represents 2% move.)

SMA: 100 (Signal must be found below 100 SMA)

Price must be below: PIVOT (This is the monthly Pivot levels)

Donchian 20/10 Screener + Alerts Donchian 20/10 Screener + Alerts identifies stocks breaking their 20-day high.

Includes ADX trend filter to confirm strong momentum.

Plots Donchian high/low lines and marks BUY/SELL signals on chart.

Screener output shows “PASS” for stocks meeting entry criteria.

Supports alerts for entry, exit, and screener signals for easy monitoring.

Monthly DCA & Last 10 YearsThis Pine Script indicator simulates a Monthly Dollar Cost Averaging (DCA) strategy to help long-term investors visualize historical performance. Instead of complex timing, the script automatically executes a hypothetical fixed-dollar purchase (e.g., $100) on the first trading day of every month. It visually marks entry points with green "B" labels and plots a dynamic yellow line representing your Global Break-Even Price, allowing you to instantly see if the current price is above or below your average cost basis. To provide deep insight, it generates a detailed performance table in the bottom-right corner that breaks down metrics year-by-year—including total capital invested, shares/coins accumulated, and Profit/Loss percentage—along with a grand total summary of the entire investment period.

Diganta Strangle Plot with IV This indicator prints a strangle . You can input both the ce and pe strikes as per your trade. This also plots the IV spikes as white dots and Z score spike as white arrows . This are when one should be ready to exit

ART Customizable Overbought Oversold indicatorThis toolkit will help you identify RSI levels on either extremes, you can customize them.

White Crow**White Crow — cluster reversal signals + market structure**

> Indicator that helps you read market structure (pivots, trend, last extremes) and spot potential reversals through CCI/RSI signal clusters. This is *not* a standalone trading system and does not guarantee any result — it is a tool for filtering and confirming your own market ideas.

---

## 1. Concept

White Crow combines three core blocks:

1. **Pivots & market structure**

Automatically detects **local tops/bottoms** and derives a *Bullish / Bearish / Sideways* bias from them.

In the top-right corner you see a compact panel with current trend and **Last Bottom / Last Top** prices.

2. **Momentum & overbought/oversold zones**

Inside, the indicator uses:

* **CCI** with fixed levels `+100 / -100`;

* an optional **RSI filter** with overbought/oversold levels (`80 / 20`).

These generate basic *Buy / Close* signals.

3. **Cluster signals Buy X / CloseV**

The script tracks **clusters of signals inside a 4-bar window** and highlights rarer, “amplified” events:

* **Buy X** — cluster buy signal (multiple buy conditions in a row);

* **CloseV** — cluster signal for exit/reversal.

**Buy X and CloseV are the strongest and most reliable signals in this indicator** because they are based on repeated conditions rather than a single bar. They work **best on higher timeframes (1H–4H)**, where they reflect meaningful shifts in order flow instead of noise.

> ⚠️ Important: Buy X and CloseV are *only signals*. They must be used as **one of several confirmation factors** for your own view of market structure (support/resistance, trend, price action, volume, etc.), not as standalone reasons to enter or exit trades.

---

## 2. How it works

### 2.1. Pivots and trend detection

* The indicator builds a **zigzag-like structure**:

after a local high, once price retraces down by a given percentage (`pivotSigma`), a **Top** is marked;

after a local low, once price retraces up by the same percentage, a **Bottom** is marked.

* Using the sequence of recent tops and bottoms, the script determines the trend:

* *Bullish* — the last low is higher than the previous one (HL);

* *Bearish* — the last high is lower than the previous one (LH);

* otherwise — *Sideways*.

* The info table shows:

* **Market Trend** — Bullish / Bearish / Sideways;

* **Last Bottom / Last Top** with adaptive decimal precision (works for crypto, FX, stocks, etc.).

### 2.2. Base Buy / Close signals

* **Long condition (Buy):**

* `CCI < -100` (oversold),

* if RSI filter is enabled — `RSI < 20`.

* **Short/Exit condition (Close):**

* `CCI > +100` (overbought),

* if RSI filter is enabled — `RSI > 80`.

These conditions generate the regular **Buy** and **Close** labels on the chart.

### 2.3. Clusters: Buy X and CloseV

To reduce noise, the indicator evaluates not only the current bar, but also the **last 4 bars**:

* `buy_count` — how many times the long condition was true within the last 4 bars;

* `sell_count` — how many times the short condition was true within the last 4 bars.

Then:

* **Buy X** appears when:

* `buy_count ≥ 2` (conditions for Buy were met on at least 2 of the last 4 bars),

* the time filter between two Buy X signals is satisfied (`Min Bars Between Signals`).

* **CloseV** appears when:

* `sell_count ≥ 2`,

* the required number of bars has passed since the previous CloseV.

> ✅ This is why **Buy X / CloseV are stronger and more trustworthy than single Buy/Close signals**, especially on **1H–4H** timeframes: the market confirms the same overbought/oversold condition several times in a row.

### 2.4. Order Blocks

* When `Show Order Blocks` is enabled, the indicator highlights **impulsive candles** whose body exceeds a threshold based on ATR.

* Colored rectangles mark **potential order blocks** (areas where strong buying or selling previously occurred).

## 3. Inputs and customization

Inputs are grouped in TradingView-friendly categories.

### 3.1. Pivot Settings

* `Show Pivots` — enable/disable **Top / Bottom** markers.

* `Sigma (% retracement)` — pivot sensitivity (minimum retracement in % required to confirm a pivot).

* Colors for Top/Bottom — for visual tuning.

**Tip:**

On H1–H4 you can keep near-default values.

On lower timeframes, reduce `Sigma` if you want more detailed local structure.

### 3.2. CCI / RSI Settings

* `CCI Period` — CCI length (short by default for faster reaction).

* `Enable RSI Filter` / `RSI Period` — toggle and length for RSI filter.

* RSI levels are fixed at **20 / 80** to mark strong oversold/overbought zones.

**Usage:**

* For more conservative entries — keep the RSI filter enabled.

* For more frequent signals (e.g. scalping) — you can disable the RSI filter.

### 3.3. Order Blocks

* `Show Order Blocks` — display order block zones.

* `Block Threshold (ATR multiplier)` — how large a candle must be (vs ATR) to be considered significant.

### 3.4. Signals & Filters

* `Show Buy / Show Buy X / Show Close / Show CloseV` — choose which labels you want to see.

* `Enable Time Filter` — enable minimum spacing between amplified signals.

* `Min Bars Between Signals` — how many bars must pass between two Buy X or two CloseV signals.

**Tip:**

If you see too many amplified signals, increase `Min Bars Between Signals`.

If you want more activity, decrease it.

### 3.5. Alerts

* `Buy Alerts / Buy X Alerts / Close Alerts / CloseV Alerts` — choose which signal types should trigger alerts.

* `One Alert Per Bar` — when enabled, alerts are triggered only once per bar (recommended for H1–H4).

Alerts are generated via `alert()`, with messages that include signal type, ticker, timeframe and current price.

---

## 4. How to trade with White Crow

### 4.1. Recommended timeframes

* 📌 **Main focus: 1H–4H.**

On these timeframes:

* pivots and trend are more stable;

* CCI/RSI reflect meaningful swings;

* **Buy X / CloseV clusters** filter out a lot of intrabar noise.

You can still experiment on M1–M15, but expect more signals and more sensitivity to noise.

### 4.2. Reading the signals step by step

1. **Start with context**

* Look at **Market Trend / Last Bottom / Last Top** in the info panel.

* See where price is relative to these points: near resistance, near support, inside a range, etc.

2. **Identify zones of interest**

* Use pivots and order blocks as potential support/resistance areas.

* Wait for price to approach these zones.

3. **Watch the signals**

* **Buy** — early sign of local oversold conditions.

* **Buy X** — amplified cluster signal; more weight than a single Buy.

* **Close** — early warning of potential exhaustion in the current move.

* **CloseV** — amplified cluster exit/reversal signal.

4. **Practical approach**

* In a *Bullish* trend:

* focus on **Buy / Buy X** near bottoms and demand blocks;

* use **Close / CloseV** for partial profit-taking or tightening stops.

* In a *Bearish* trend:

* focus on **Close / CloseV** near tops and supply blocks;

* use **Buy / Buy X** mainly for countertrend scalps with strict risk control.

---

## 5. Important notes and disclaimer

1. **Buy X / CloseV are stronger — but not “magic” signals.**

They are statistically more meaningful than single Buy/Close signals because:

* they require multiple confirmations within a cluster;

* they are time-filtered.

However, **false signals are still possible**, especially in news spikes and low-liquidity conditions.

2. **Best performance on higher timeframes (1H–4H).**

Here, Buy X and CloseV usually reflect genuine shifts in supply/demand rather than micro noise.

3. **This is a confirmation tool, not a complete system.**

Pro Trading White Crow:

* does not manage risk;

* does not define position size or stop-loss;

* does not replace your own analysis.

Always use its signals as **one of several confluence factors** together with structure, trend, price action, volume, and your trading plan.

4. **Educational purpose only.**

This script and description are for educational and analytical purposes only.

They **do not constitute investment advice or a guarantee of profit**.

You are fully responsible for all trading decisions and risk management.

---

---

## White Crow — кластерные сигналы разворота + структура рынка

> Индикатор помогает читать рыночную структуру (пивоты, тренд, последние экстремумы) и находить потенциальные развороты через кластеры сигналов CCI/RSI. Это *не* готовая торговая система и *не* гарантия результата — а инструмент для фильтрации и подтверждения ваших собственных идей по рынку.

---

## 1. Концепция

White Crow объединяет три ключевых блока:

1. **Пивоты и структура рынка**

Автоматически находит **локальные вершины и впадины** и на их основе формирует трендовое смещение: *Bullish / Bearish / Sideways*.

В правом верхнем углу — компактная панель с текущим трендом и ценами **Last Bottom / Last Top**.

2. **Моментум и зоны перегрева**

Внутри используются:

* **CCI** с фиксированными уровнями `+100 / -100`;

* опциональный **фильтр RSI** с уровнями перепроданности/перекупленности (`20 / 80`).

По ним строятся базовые сигналы *Buy / Close*.

3. **Кластерные сигналы Buy X / CloseV**

Скрипт отслеживает **кластеры сигналов внутри окна в 4 бара** и выделяет более редкие, «усиленные» события:

* **Buy X** — кластерный сигнал покупки (несколько buy-условий подряд);

* **CloseV** — кластерный сигнал выхода/разворота.

Именно **Buy X и CloseV являются наиболее сильными и достоверными сигналами индикатора**, так как возникают при повторяющемся выполнении условий, а не на одном баре. Лучше всего они работают **на старших таймфреймах (1–4 часа)**, где отражают реальное смещение баланса спроса/предложения, а не рыночный шум.

> ⚠️ Важно: Buy X и CloseV — *это всего лишь сигналы*. Они должны использоваться **как один из факторов подтверждения** вашего видения структуры рынка (уровни, тренд, price action, объём и т.д.), а не как единственная причина для входа или выхода.

---

## 2. Как это работает

### 2.1. Пивоты и определение тренда

* Индикатор строит **структуру в стиле зигзага**:

после локального максимума, когда цена откатывает вниз на заданный процент (`pivotSigma`), отмечается **Top**;

после локального минимума, когда цена откатывает вверх на тот же процент, отмечается **Bottom**.

* По последовательности последних вершин и впадин определяется тренд:

* *Bullish* — последний минимум выше предыдущего (HL);

* *Bearish* — последний максимум ниже предыдущего (LH);

* иначе — *Sideways*.

* В информационной таблице отображаются:

* **Market Trend** — Bullish / Bearish / Sideways;

* **Last Bottom / Last Top** с адаптивным количеством знаков (подходит под крипту, форекс, акции и т.д.).

### 2.2. Базовые сигналы Buy / Close

* **Условие для Buy (лонг):**

* `CCI < -100` (зона перепроданности),

* при включённом фильтре — `RSI < 20`.

* **Условие для Close (шорт/выход):**

* `CCI > +100` (зона перекупленности),

* при включённом фильтре — `RSI > 80`.

По этим условиям индикатор рисует обычные метки **Buy** и **Close**.

### 2.3. Кластеры: Buy X и CloseV

Чтобы отсеять лишний шум, индикатор оценивает не только текущий бар, но и **4 последних бара**:

* `buy_count` — сколько раз условие на покупку выполнялось за последние 4 бара;

* `sell_count` — сколько раз условие на продажу/выход выполнялось за последние 4 бара.

Далее:

* **Buy X** появляется, когда:

* `buy_count ≥ 2` (минимум на 2 из 4 баров были условия для покупки),

* соблюдён фильтр по времени между усиленными сигналами (`Min Bars Between Signals`).

* **CloseV** появляется, когда:

* `sell_count ≥ 2`,

* прошло достаточно баров с момента предыдущего CloseV.

> ✅ Поэтому **Buy X и CloseV заметно сильнее и надёжнее одиночных Buy/Close**, особенно на **таймфреймах 1–4 часа**: рынок несколько раз подряд подтверждает один и тот же перегрев/разрядку момента.

### 2.4. Order Blocks

* При включённом `Show Order Blocks` индикатор выделяет **импульсные свечи**, чьё тело больше заданного множителя ATR.

* По таким свечам строятся цветные прямоугольники — **потенциальные блоки ордеров** (области поддержек/сопротивлений, где ранее проходил крупный объём).

---

## 3. Настройки и кастомизация

Настройки сгруппированы в привычные разделы TradingView.

### 3.1. Pivot Settings

* `Show Pivots` — включить/выключить метки **Top / Bottom**.

* `Sigma (% retracement)` — чувствительность к пивотам (минимальная глубина отката в процентах).

* Цвета Top/Bottom — визуальная настройка.

**Совет:**

На H1–H4 можно оставить значения близкие к стандартным.

На младших ТФ уменьшайте `Sigma`, если нужна более детальная структура.

### 3.2. CCI / RSI Settings

* `CCI Period` — период CCI (по умолчанию короткий, для более быстрой реакции).

* `Enable RSI Filter` / `RSI Period` — включение и длина RSI-фильтра.

* Уровни RSI фиксированы: **20 / 80**, выделяя сильную перепроданность/перекупленность.

**Использование:**

* Для более консервативной торговли — держите фильтр RSI включённым.

* Для более частых сигналов (скальпинг и т.п.) — можно фильтр отключить.

### 3.3. Order Blocks

* `Show Order Blocks` — отображение блоков ордеров.

* `Block Threshold (ATR multiplier)` — насколько большой должна быть свеча относительно ATR, чтобы считаться значимой.

### 3.4. Signals & Filters

* `Show Buy / Show Buy X / Show Close / Show CloseV` — выбор типов отображаемых меток.

* `Enable Time Filter` — включение минимального интервала между усиленными сигналами.

* `Min Bars Between Signals` — сколько баров должно пройти между двумя Buy X или двумя CloseV.

**Совет:**

Если усиленных сигналов слишком много — увеличьте `Min Bars Between Signals`.

Если хотите больше активности — уменьшите это значение.

### 3.5. Alerts

* `Buy Alerts / Buy X Alerts / Close Alerts / CloseV Alerts` — выбор типов сигналов для алертов.

* `One Alert Per Bar` — при включении алерты отправляются один раз на бар (рекомендуется для H1–H4).

Алерты формируются через `alert()` с сообщением, включающим тип сигнала, тикер, таймфрейм и текущую цену.

---

## 4. Как использовать White Crow в торговле

### 4.1. Рекомендуемые таймфреймы

* 📌 **Основной фокус: 1–4 часа.**

На этих ТФ:

* структура по пивотам и тренд более стабильны;

* CCI/RSI отражают существенные ценовые колебания;

* кластеры **Buy X / CloseV** лучше отсеивают шум.

На M1–M15 индикатор тоже можно применять, но нужно быть готовым к большему количеству сигналов и чувствительности к микродвижениям.

### 4.2. Пошаговое чтение сигналов

1. **Начните с контекста**

* Посмотрите на **Market Trend / Last Bottom / Last Top** в панели.

* Определите, где находитесь относительно этих уровней: у сопротивления, у поддержки, внутри диапазона и т.п.

2. **Найдите зоны интереса**

* Используйте пивоты и order blocks как потенциальные области спроса/предложения.

* Ждите подхода цены к этим зонам.

3. **Отслеживайте сигналы**

* **Buy** — ранний признак локальной перепроданности.

* **Buy X** — усиленный кластерный сигнал, более значимый, чем одиночный Buy.

* **Close** — ранний сигнал возможного ослабления текущего движения.

* **CloseV** — усиленный кластерный сигнал выхода/разворота.

4. **Практическое применение**

* В *бычьем* тренде:

* фокус на **Buy / Buy X** возле впадин и зон спроса;

* **Close / CloseV** использовать для частичной фиксации и подтягивания стопа.

* В *медвежьем* тренде:

* фокус на **Close / CloseV** возле вершин и зон предложения;

* **Buy / Buy X** — для аккуратных контртрендовых входов с жестким риском.

---

## 5. Важные замечания и дисклеймер

1. **Buy X / CloseV сильнее, но не «волшебные» сигналы.**

Они статистически более значимы, чем одиночные Buy/Close, потому что:

* требуют нескольких подтверждений в кластере;

* фильтруются по времени.

Однако **ложные срабатывания всё равно возможны**, особенно на новостях и в условиях низкой ликвидности.

2. **Оптимальная область применения — старшие ТФ (1–4 часа).**

Здесь Buy X и CloseV обычно отражают реальное изменение баланса спроса/предложения, а не шум.

3. **Это инструмент подтверждения, а не полноценная система.**

Pro Trading White Crow:

* не управляет рисками;

* не считает размер позиции и уровень стоп-лосса;

* не заменяет ваше собственное видение рынка.

Всегда используйте его сигналы **как один из факторов согласованности** вместе со структурой, трендом, price action, объёмом и персональным торговым планом.

4. **Образовательный характер.**

Скрипт и описание предназначены для обучения и анализа графиков.

Они **не являются инвестиционной рекомендацией и не гарантируют прибыль**.

Вы самостоятельно принимаете все торговые решения и несёте полную ответственность за риск.

---

SMC Fib Range Signals [@gyanapravah]SMC Fib Range Signals

This indicator blends Smart Money Concepts (SMC) with a Range Filter Trend System and Fibonacci Retracement & Extensions to generate high-probability automated Buy/Sell signals.

Designed to avoid noise and focus on market structure + trend + price confluence, this tool is ideal for:

1. Intraday traders

2. Swing traders

3. Index & stock traders

4. Crypto & Forex traders

CORE FEATURES

Range Filter Trend Detection

Smooth adaptive filter identifies true trend direction

Visual confirmation:

🟢 Green filter = bullish pressure

🔴 Red filter = bearish pressure

🟡 Yellow filter = neutral

Upper & Lower Bands act as dynamic support/resistance zones

Smart Money Order Blocks (SMC)

Automatically detects important pivot highs & lows

Marks:

OB High → supply / resistance zone

OB Low → demand / support zone

Continuously tracks latest OB levels for live price interaction

Fibonacci Engine

Detects the current swing zone and plots:

Retracement levels

0.236 – 0.382 – 0.500 – 0.618 – 0.786 (editable)

Extension targets

1.272 – 1.618

All levels update dynamically on new market structure and pivots.

SIGNAL ENGINE

This indicator generates signals from three independent confirmation systems:

BUY SIGNALS trigger when:

1. Trend flips bullish (price crosses above the Filter)

2.Bullish trend + price reacts near:

Order Block support

Fibonacci 0.382 / 0.618 levels

Bounce from the Lower Band with trend support

All setups require volume confirmation to filter fake breakouts.

SELL SIGNALS trigger when:

1. Trend flips bearish (price crosses below the Filter)

2. Bearish trend + price reacts near:

Order Block resistance

Fibonacci 0.382 / 0.618 levels

Rejection from the Upper Band with trend support

ALERTS READY

Two built-in alerts:

BUY Alert — fires on bullish signal

SELL Alert — fires on bearish signal

INPUT SETTINGS

Trend Engine

1.Source

2.Sampling Period

3.Range Multiplier

Smart Money

Pivot detection sensitivity (Left / Right bars)

Fibonacci

1.Swing lookback length

2.Editable Fib retracement and extension values

3.Toggle show/hide Fib levels

BEST USE CASE

Works extremely well on:

⏱️ 3M – 15M Intraday scalping

⏱️ 30M – 1H positional entries

⏱️ 4H – D1 swing trading

Tested on:

NIFTY / BANKNIFTY / FINNIFTY

Stocks

Crypto

Forex

DISCLAIMER

This indicator is for educational purposes only.

It does NOT guarantee profits.

Always use:

Proper risk management

Stop-loss rules

Your own confirmation before entering trades.

AUTHOR

Built & shared by @gyanapravah (Odisha, India)

Open-source for learning and community improvement.

World Markets Table

🌍 World Markets Session Table - Track Global Exchanges in Real-Time

Monitor 10 major stock exchanges worldwide with live market status, countdown timers, and customizable themes. Perfect for multi-market traders, global portfolio managers, and anyone trading across time zones.

✨ Key Features

10 Global Exchanges Tracked:

🇺🇸 NYSE & NASDAQ (New York)

🇨🇳 Shanghai Stock Exchange

🇯🇵 Tokyo Stock Exchange

🇭🇰 Hong Kong Stock Exchange

🇬🇧 London Stock Exchange

🇪🇺 Euronext

🇩🇪 Frankfurt (Xetra)

🇨🇦 Toronto Stock Exchange

🇦🇺 Australian Securities Exchange

Real-Time Market Intelligence:

✅ Live OPEN/CLOSED status with colored indicators

⏱️ Countdown timers to market open/close

🗓️ Automatic weekday/weekend detection

🕒 Optional seconds display for precision timing

🎯 Visual status badges (green for open, red for closed)

Full Customization:

📍 6 table positions (top/bottom × left/center/right)

📏 4 size options (tiny, small, normal, large)

🎨 4 professional themes: Dark, Light, Neon, Ocean

🚩 Toggle country flags on/off

💼 Clean, professional table layout

🎨 Professional Themes

Dark Theme: Sleek charcoal design for night trading

Light Theme: Bright, clean interface for daylight charts

Neon Theme: Vibrant cyberpunk aesthetic with electric colors

Ocean Theme: Calming blue palette for focused analysis

💡 Perfect For

Multi-market traders monitoring global sessions simultaneously

Identifying optimal trading windows across time zones

Planning entries/exits around market opens and closes

Portfolio managers tracking international markets

Forex, indices, and commodities traders

Pre-market and after-hours trading planning

⚙️ How It Works

All market times are calculated in UTC and automatically adjust to your local timezone. The indicator overlays your chart without interfering with price action or technical analysis. Simply add it to any chart, customize the appearance, and stay informed about global market hours.

📊 Usage Tips

Place the table in a non-intrusive position to maintain chart clarity

Use countdown timers to prepare for volatility at market open/close

Match the theme to your chart colors for a cohesive workspace

Enable seconds display when precision timing matters most

Note: This is a display-only indicator showing market hours. It does not generate trading signals or plot price data.

Bassi MACD Pro + ADX Filter + Smart Histogram TP + RSIA professional-grade MACD indicator that dramatically reduces false signals by combining four powerful filters:

Key Features

Classic MACD (12,26,9) with clean, high-visibility histogram coloring

ADX + DI filter – only takes trades when ADX > user-defined threshold (default 25) ensuring you trade only in strong trending markets

Smart Histogram Take-Profit logic – automatically detects the exact moment bullish/bearish momentum starts to weaken after a strong move and marks a precise TP level (one TP per trade – no repainting, no multiple signals)

Zero-line crossover confirmation + histogram direction filter – eliminates many whipsaw signals common in regular MACD

Separate RSI pane with overbought/oversold levels and visual markers (for additional confluence – does not interfere with main logic)

Visual Signals

Green “MACD BUY” label + lime triangle = confirmed long entry in strong trend

Red “MACD SELL” label + red triangle = confirmed short entry in strong trend

Small lime/red “TP” triangles = Smart Histogram Take-Profit triggered (perfect exit timing based on momentum fade)

Alert Conditions Included

MACD BUY

MACD SELL

TP Long Hit

TP Short Hit

Combined “Any Signal” alert

Why this version outperforms standard MACD

Most MACD crossovers fail in ranging markets. This script solves that by:

Requiring strong trend (ADX filter)

Confirming histogram is actually growing in the new direction

Waiting for the true zero-line cross with momentum

Giving you an intelligent, non-fixed % take-profit based on real histogram exhaustion

Excellent for swing trading, day trading, crypto, forex, and stocks on any timeframe (works especially well on 1H–4H–Daily).

Clean, fast, no repainting, fully alert-ready.

Add to chart → set your alerts → trade only the highest-probability MACD signals.

Crypto Trading with Gaussian Channel Hariss 369This indicator uses a Gaussian Channel to identify volatility-based breakouts and a custom Relative Volume (RVOL) filter to confirm momentum. The Gaussian Channel smooths price using a multi-stage EMA process, creating adaptive upper and lower bands. When price closes above the upper band with strong volume (RVOL > 1.5), it signals bullish expansion. When price closes below the lower band with high RVOL, it indicates bearish momentum.

The tool also plots buy and sell labels based on these breakouts, helping traders visually track trend acceleration. This indicator works well in trending markets, breakout conditions and intraday crypto pairs where volume is a key driver.

In the input section choose current time frame to "Chart" and Higher Time Frame eg. 15m/1h etc. This indicator works well in higher time frame eg. Current Time Frame "1h" and Higher Time Frame "4H".

The middle band can be used as stop loss/to exit trade. However, one can exit the trade with suitable profit.

One can use it for any class of asset and any time frame. If you do not want higher time frame to be considered, choose both current and higher time frame to "Chart" only.

This tool is designed for educational/trading-assist purposes and does not guarantee profits

Previous 5 Days OHLC + Dates + PricesTitle: Previous 5 Days OHLC Levels (Extended Lines + Labels)

Description:

This indicator automatically plots the Open, High, Low, and Close (OHLC) levels for the previous 5 trading days. Unlike standard daily separators, this tool extends the lines from their historical origin all the way to the current price bar, allowing traders to instantly see how current price action interacts with recent support and resistance levels.

Key Features:

5-Day Lookback: Automatically fetches and plots OHLC data for the last 5 trading sessions.

Extended Lines: Lines extend to the current bar (Right) to visualize immediate Support/Resistance zones.

Smart Labels: Each line is marked with the Day Name, Date, Type (O/H/L/C), and the Exact Price.

Customizable Positioning: Choose to display labels on the Left (start of the day) or the Right (next to current price) to keep your chart clean.

Toggle Visibility: Individually turn on/off Opens, Closes, Highs, or Lows to focus on the data that matters to your strategy.

How to Use:

Trend Analysis: Use previous Highs and Lows to identify potential breakout or breakdown levels.

Range Trading: Identify where price previously opened or closed to find intraday pivots.

Clean Charting: Use the settings to hide labels or specific lines (e.g., hide Opens/Closes to see only the Daily Range).

Settings:

Label Position: Switch between "Left" (historical origin) and "Right" (current price).

Visibility: Checkboxes to show/hide Open, High, Low, Close, and Text Labels.

Style: Fully customizable colors for each level type.

Technical Note: This script is optimized for performance (Pine Script v6). It uses array management and executes drawing logic only on the last bar to minimize resource usage while maintaining real-time accuracy.

SuperTrend Fusion — Trend + Momentum + Volatility FilterSuperTrend Fusion — Trend + Momentum + Volatility Filter

SuperTrend Fusion — ATP is an original, multi-factor trend-filtering tool that enhances the classic SuperTrend by combining three market dimensions in one unified model:

1. Trend direction (SuperTrend)

Provides the base trend structure using ATR-based volatility bands.

2. Momentum confirmation (Average Force – adapted)

An adapted version of an open-source “Average Force” concept published on TradingView by racer8.

This component measures where closing price sits relative to recent highs/lows, smoothed to capture directional pressure.

3. Market condition filtering (Choppiness Index)

Filters out sideways, non-trending zones where SuperTrend alone typically produces false flips.

Together, these components create a cleaner, more selective system that focuses on higher-quality SuperTrend reversals, avoiding the most common whipsaws that occur during low-momentum or high-choppiness periods.

🔍 How it Works

A long signal occurs when:

- SuperTrend flips from downtrend to uptrend

- Momentum (AF) is positive (optional filter)

- The market is trending and not excessively choppy (optional filter)

A short signal triggers under the symmetrical conditions.

Filtered signals are visually marked with subtle “X” markers so traders can understand when a raw SuperTrend flip was rejected by the filters.

The indicator also includes:

Enhanced styling for better visibility

Colored bars during valid signals

Optional background highlight during choppy periods

🎯 What This Indicator Is Designed For

This tool aims to:

- Improve the quality of SuperTrend entries

- Remove many low-probability signals

- Help traders visually identify when the market has the momentum and structure required for cleaner trend continuation

It is not intended to predict markets or guarantee accuracy; rather, it provides structure and clarity for decision-making based on technical rules.

⚙️ Inputs

- ATR Length & Factor (SuperTrend)

- Average Force Period & Smoothing

- Choppiness Length & Threshold

- Option to enable/disable each filter individually

📘 Credits

This script includes an adapted version of an open-source “Average Force” function originally published on TradingView by its author, racer8.

SuperTrend and Choppiness Index components are derived from classical, public-domain formulas.

📌 Important Notes

This indicator is not a strategy and does not guarantee performance.

Signals are based on historical calculations only and do not use lookahead.

Past performance does not guarantee future results.

Always test different assets and timeframes before using in live conditions.

👍 Recommended Usage

For a clean experience:

- Use on standard candlestick charts

- Avoid non-standard chart types (Renko, Heikin Ashi, Kagi, Range)

- Combine with your own risk management and trade planning