Exhaustion Zone [by rukich]🟠 OVERVIEW

The indicator shows asset exhaustion — an area of interest where potential buying opportunities can be considered.

🟠 COMPONENTS

The indicator is based on a combination of fundamental tools designed to properly react to price movement and volatility.

It is displayed on the chart as a green line. When the price touches the indicator line, the candle lights up and is highlighted in green.

🟠 HOW TO USE

The best timeframes for using the indicator: 1D and 3D.

Since the indicator is used on higher timeframes, the price rarely reaches the indicator line, but it often shows a strong reaction when it does, which suggests that the indicator can be used for investment purposes.

Since the zone suggests potential buying opportunities, it’s best to act from the zone only when a reaction is confirmed. Confirmation may include a candle close beyond nearby fractals or the invalidation of the nearest resistance zone.

🟠 CONCLUSION

The indicator highlights an area of interest where, upon confirmation of a reaction, buying opportunities may be considered.

Investment

DCA with the Money Supply Index DCA with the Money Supply Index (MSI) by zdmre

This strategy is based on the Money Supply Index (MSI) by zdmre and enhances it with two functional options for users: a DCA (Dollar-Cost Averaging) approach and a signal-based buy/sell mode. It’s designed to help traders and investors make data-driven, disciplined entry decisions based on monetary supply trends.

🧠 Concept Overview

The Money Supply Index (MSI) provides insight into how liquidity (money supply) influences market movements. This strategy builds upon that foundation by allowing users to either:

Accumulate positions over time using DCA, based on favorable MSI conditions.

Execute a single buy and sell trade, optimized for bull market conditions.

⚙️ Inputs Explained

General Parameters

Start Bar Index / Stop Bar Index

Defines the range of bars (historical data) for backtesting or strategy visualization.

Long DCA

Activates the DCA mode. If unchecked, the strategy operates in single-entry/single-exit signal mode.

Trading Signal

Enables signal-based entries and exits when the MSI reaches predefined thresholds.

DCA Parameters

Entry Value

The MSI value that triggers a DCA buy event. When the MSI crosses below this value, the strategy considers it a favorable moment to deploy the saved capital.

Saved Amount

The amount of money set aside regularly (e.g., monthly) for investment. This simulates the DCA effect by accumulating capital and deploying it when conditions are optimal.

Data Inputs

Money Supply

The data source for the Money Supply Index (default: ECONOMICS:USM2).

Relational Symbol

The market instrument to compare against the money supply (default: NASDAQ_DLY:NDX). This allows the strategy to measure liquidity impact on a specific market.

Chart Display Options

You can toggle these metrics on the chart for better visualization:

Entry Price (green) – The price level of executed buys.

Cash Balance (yellow) – Remaining uninvested capital.

Invested Capital (red) – Total amount currently invested.

Current Value (blue) – The current valuation of the investment.

Profit (purple) – The total realized and unrealized profit.

Trades on Chart / Signal Labels / Quantity – Enables trade markers, signal text, and position size visualization.

📈 How the Strategy Works

1️⃣ DCA Mode

In DCA mode, the strategy simulates periodic savings and only invests when the MSI indicates favorable liquidity conditions (based on the Entry Value).

This approach aims to achieve the best possible average entry price over time — a powerful strategy for long-term investors seeking stable accumulation with reduced emotional bias.

2️⃣ Signal-Based Mode

In signal mode (with DCA disabled), the strategy performs one buy and one sell trade based on MSI turning points.

It’s most effective during bull markets, where liquidity expansion supports upward momentum.

This mode helps identify high-probability entry and exit zones rather than averaging in continuously.

💡 Additional Notes

This strategy includes helpful metrics to monitor your personal investment performance — showing invested capital, cash reserves, and profit in real-time.

The goal is to combine macroeconomic insight (money supply) with disciplined execution and capital management.

⚠️ Disclaimer

This strategy is for educational and research purposes only. It does not constitute financial advice. Always conduct your own analysis before making investment decisions.

Early Bird 9.4 – The No-Loss, Spot-Only BTC Trading StrategyDiscover Early Bird 9.4, your ultimate ally in the crypto markets. Designed to trade Bitcoin in spot only, with zero leverage, Early Bird offers a unique and proven approach: 90% to 100% of trades are closed in profit, and the few remaining positions are simply held as BTC until they recover.

In other words: you either win, or you own more Bitcoin — but you never lose. Not a single cent of your money will ever end up in the broker’s pocket.

Ideal for investors looking to eliminate the risk of loss, as long as they’re happy to own BTC, Early Bird is more than a strategy — it’s a new way to grow and secure your Bitcoin holdings while fully embracing the power of market volatility.

DCA Investment Tracker Pro [tradeviZion]DCA Investment Tracker Pro: Educational DCA Analysis Tool

An educational indicator that helps analyze Dollar-Cost Averaging strategies by comparing actual performance with historical data calculations.

---

💡 Why I Created This Indicator

As someone who practices Dollar-Cost Averaging, I was frustrated with constantly switching between spreadsheets, calculators, and charts just to understand how my investments were really performing. I wanted to see everything in one place - my actual performance, what I should expect based on historical data, and most importantly, visualize where my strategy could take me over the long term .

What really motivated me was watching friends and family underestimate the incredible power of consistent investing. When Napoleon Bonaparte first learned about compound interest, he reportedly exclaimed "I wonder it has not swallowed the world" - and he was right! Yet most people can't visualize how their $500 monthly contributions today could become substantial wealth decades later.

Traditional DCA tracking tools exist, but they share similar limitations:

Require manual data entry and complex spreadsheets

Use fixed assumptions that don't reflect real market behavior

Can't show future projections overlaid on actual price charts

Lose the visual context of what's happening in the market

Make compound growth feel abstract rather than tangible

I wanted to create something different - a tool that automatically analyzes real market history, detects volatility periods, and shows you both current performance AND educational projections based on historical patterns right on your TradingView charts. As Warren Buffett said: "Someone's sitting in the shade today because someone planted a tree a long time ago." This tool helps you visualize your financial tree growing over time.

This isn't just another calculator - it's a visualization tool that makes the magic of compound growth impossible to ignore.

---

🎯 What This Indicator Does

This educational indicator provides DCA analysis tools. Users can input investment scenarios to study:

Theoretical Performance: Educational calculations based on historical return data

Comparative Analysis: Study differences between actual and theoretical scenarios

Historical Projections: Theoretical projections for educational analysis (not predictions)

Performance Metrics: CAGR, ROI, and other analytical metrics for study

Historical Analysis: Calculates historical return data for reference purposes

---

🚀 Key Features

Volatility-Adjusted Historical Return Calculation

Analyzes 3-20 years of actual price data for any symbol

Automatically detects high-volatility stocks (meme stocks, growth stocks)

Uses median returns for volatile stocks, standard CAGR for stable stocks

Provides conservative estimates when extreme outlier years are detected

Smart fallback to manual percentages when data insufficient

Customizable Performance Dashboard

Educational DCA performance analysis with compound growth calculations

Customizable table sizing (Tiny to Huge text options)

9 positioning options (Top/Middle/Bottom + Left/Center/Right)

Theme-adaptive colors (automatically adjusts to dark/light mode)

Multiple display layout options

Future Projection System

Visual future growth projections

Timeframe-aware calculations (Daily/Weekly/Monthly charts)

1-30 year projection options

Shows projected portfolio value and total investment amounts

Investment Insights

Performance vs benchmark comparison

ROI from initial investment tracking

Monthly average return analysis

Investment milestone alerts (25%, 50%, 100% gains)

Contribution tracking and next milestone indicators

---

📊 Step-by-Step Setup Guide

1. Investment Settings 💰

Initial Investment: Enter your starting lump sum (e.g., $60,000)

Monthly Contribution: Set your regular DCA amount (e.g., $500/month)

Return Calculation: Choose "Auto (Stock History)" for real data or "Manual" for fixed %

Historical Period: Select 3-20 years for auto calculations (default: 10 years)

Start Year: When you began investing (e.g., 2020)

Current Portfolio Value: Your actual portfolio worth today (e.g., $150,000)

2. Display Settings 📊

Table Sizes: Choose from Tiny, Small, Normal, Large, or Huge

Table Positions: 9 options - Top/Middle/Bottom + Left/Center/Right

Visibility Toggles: Show/hide Main Table and Stats Table independently

3. Future Projection 🔮

Enable Projections: Toggle on to see future growth visualization

Projection Years: Set 1-30 years ahead for analysis

Live Example - NASDAQ:META Analysis:

Settings shown: $60K initial + $500/month + Auto calculation + 10-year history + 2020 start + $150K current value

---

🔬 Pine Script Code Examples

Core DCA Calculations:

// Calculate total invested over time

months_elapsed = (year - start_year) * 12 + month - 1

total_invested = initial_investment + (monthly_contribution * months_elapsed)

// Compound growth formula for initial investment

theoretical_initial_growth = initial_investment * math.pow(1 + annual_return, years_elapsed)

// Future Value of Annuity for monthly contributions

monthly_rate = annual_return / 12

fv_contributions = monthly_contribution * ((math.pow(1 + monthly_rate, months_elapsed) - 1) / monthly_rate)

// Total expected value

theoretical_total = theoretical_initial_growth + fv_contributions

Volatility Detection Logic:

// Detect extreme years for volatility adjustment

extreme_years = 0

for i = 1 to historical_years

yearly_return = ((price_current / price_i_years_ago) - 1) * 100

if yearly_return > 100 or yearly_return < -50

extreme_years += 1

// Use median approach for high volatility stocks

high_volatility = (extreme_years / historical_years) > 0.2

calculated_return = high_volatility ? median_of_returns : standard_cagr

Performance Metrics:

// Calculate key performance indicators

absolute_gain = actual_value - total_invested

total_return_pct = (absolute_gain / total_invested) * 100

roi_initial = ((actual_value - initial_investment) / initial_investment) * 100

cagr = (math.pow(actual_value / initial_investment, 1 / years_elapsed) - 1) * 100

---

📊 Real-World Examples

See the indicator in action across different investment types:

Stable Index Investments:

AMEX:SPY (SPDR S&P 500) - Shows steady compound growth with standard CAGR calculations

Classic DCA success story: $60K initial + $500/month starting 2020. The indicator shows SPY's historical 10%+ returns, demonstrating how consistent broad market investing builds wealth over time. Notice the smooth theoretical growth line vs actual performance tracking.

MIL:VUAA (Vanguard S&P 500 UCITS) - Shows both data limitation and solution approaches

Data limitation example: VUAA shows "Manual (Auto Failed)" and "No Data" when default 10-year historical setting exceeds available data. The indicator gracefully falls back to manual percentage input while maintaining all DCA calculations and projections.

MIL:VUAA (Vanguard S&P 500 UCITS) - European ETF with successful 5-year auto calculation

Solution demonstration: By adjusting historical period to 5 years (matching available data), VUAA auto calculation works perfectly. Shows how users can optimize settings for newer assets. European market exposure with EUR denomination, demonstrating DCA effectiveness across different markets and currencies.

NYSE:BRK.B (Berkshire Hathaway) - Quality value investment with Warren Buffett's proven track record

Value investing approach: Berkshire Hathaway's legendary performance through DCA lens. The indicator demonstrates how quality companies compound wealth over decades. Lower volatility than tech stocks = standard CAGR calculations used.

High-Volatility Growth Stocks:

NASDAQ:NVDA (NVIDIA Corporation) - Demonstrates volatility-adjusted calculations for extreme price swings

High-volatility example: NVIDIA's explosive AI boom creates extreme years that trigger volatility detection. The indicator automatically switches to "Median (High Vol): 50%" calculations for conservative projections, protecting against unrealistic future estimates based on outlier performance periods.

NASDAQ:TSLA (Tesla) - Shows how 10-year analysis can stabilize volatile tech stocks

Stable long-term growth: Despite Tesla's reputation for volatility, the 10-year historical analysis (34.8% CAGR) shows consistent enough performance that volatility detection doesn't trigger. Demonstrates how longer timeframes can smooth out extreme periods for more reliable projections.

NASDAQ:META (Meta Platforms) - Shows stable tech stock analysis using standard CAGR calculations

Tech stock with stable growth: Despite being a tech stock and experiencing the 2022 crash, META's 10-year history shows consistent enough performance (23.98% CAGR) that volatility detection doesn't trigger. The indicator uses standard CAGR calculations, demonstrating how not all tech stocks require conservative median adjustments.

Notice how the indicator automatically detects high-volatility periods and switches to median-based calculations for more conservative projections, while stable investments use standard CAGR methods.

---

📈 Performance Metrics Explained

Current Portfolio Value: Your actual investment worth today

Expected Value: What you should have based on historical returns (Auto) or your target return (Manual)

Total Invested: Your actual money invested (initial + all monthly contributions)

Total Gains/Loss: Absolute dollar difference between current value and total invested

Total Return %: Percentage gain/loss on your total invested amount

ROI from Initial Investment: How your starting lump sum has performed

CAGR: Compound Annual Growth Rate of your initial investment (Note: This shows initial investment performance, not full DCA strategy)

vs Benchmark: How you're performing compared to the expected returns

---

⚠️ Important Notes & Limitations

Data Requirements: Auto mode requires sufficient historical data (minimum 3 years recommended)

CAGR Limitation: CAGR calculation is based on initial investment growth only, not the complete DCA strategy

Projection Accuracy: Future projections are theoretical and based on historical returns - actual results may vary

Timeframe Support: Works ONLY on Daily (1D), Weekly (1W), and Monthly (1M) charts - no other timeframes supported

Update Frequency: Update "Current Portfolio Value" regularly for accurate tracking

---

📚 Educational Use & Disclaimer

This analysis tool can be applied to various stock and ETF charts for educational study of DCA mathematical concepts and historical performance patterns.

Study Examples: Can be used with symbols like AMEX:SPY , NASDAQ:QQQ , AMEX:VTI , NASDAQ:AAPL , NASDAQ:MSFT , NASDAQ:GOOGL , NASDAQ:AMZN , NASDAQ:TSLA , NASDAQ:NVDA for learning purposes.

EDUCATIONAL DISCLAIMER: This indicator is a study tool for analyzing Dollar-Cost Averaging strategies. It does not provide investment advice, trading signals, or guarantees. All calculations are theoretical examples for educational purposes only. Past performance does not predict future results. Users should conduct their own research and consult qualified financial professionals before making any investment decisions.

---

© 2025 TradeVizion. All rights reserved.

Employee Portfolio Generator [By MUQWISHI]▋ INTRODUCTION :

The “Employee Portfolio Generator” simplifies the process of building a long-term investment portfolio tailored for employees seeking to build wealth through investments rather than traditional bank savings. The tool empowers employees to set up recurring deposits at customizable intervals, enabling to make additional purchases in a list of preferred holdings, with the ability to define the purchasing investment weight for each security. The tool serves as a comprehensive solution for tracking portfolio performance, conducting research, and analyzing specific aspects of portfolio investments. The output includes an index value, a table of holdings, and chart plots, providing a deeper understanding of the portfolio's historical movements.

_______________________

▋ OVERVIEW:

● Scenario (The chart above can be taken as an example) :

Let say, in 2010, a newly employed individual committed to saving $1,000 each month. Rather than relying on a traditional savings account, chose to invest the majority of monthly savings in stable well-established stocks. Allocating 30% of monthly saving to AMEX:SPY and another 30% to NASDAQ:QQQ , recognizing these as reliable options for steady growth. Additionally, there was an admired toward innovative business models of NASDAQ:AAPL , NASDAQ:MSFT , NASDAQ:AMZN , and NASDAQ:EBAY , leading to invest 10% in each of those companies. By the end of 2024, after 15 years, the total monthly deposits amounted to $179,000, which would have been the result of traditional saving alone. However, by sticking into long term invest, the value of the portfolio assets grew, reaching nearly $900,000.

_______________________

▋ OUTPUTS:

The table can be displayed in three formats:

1. Portfolio Index Title: displays the index name at the top, and at the bottom, it shows the index value, along with the chart timeframe, e.g., daily change in points and percentage.

2. Specifications: displays the essential information on portfolio performance, including the investment date range, total deposits, free cash, returns, and assets.

3. Holdings: a list of the holding securities inside a table that contains the ticker, last price, entry price, return percentage of the portfolio's total deposits, and latest weighted percentage of the portfolio. Additionally, a tooltip appears when the user passes the cursor over a ticker's cell, showing brief information about the company, such as the company's name, exchange market, country, sector, and industry.

4. Indication of New Deposit: An indication of a new deposit added to the portfolio for additional purchasing.

5. Chart: The portfolio's historical movements can be visualized in a plot, displayed as a bar chart, candlestick chart, or line chart, depending on the preferred format, as shown below.

_______________________

▋ INDICATOR SETTINGS:

Section(1): Table Settings

(1) Naming the index.

(2) Table location on the chart and cell size.

(3) Sorting Holdings Table. By securities’ {Return(%) Portfolio, Weight(%) Portfolio, or Ticker Alphabetical} order.

(4) Choose the type of index: {Assets, Return, or Return (%)}, and the plot type for the portfolio index: {Candle, Bar, or Line}.

(5) Positive/Negative colors.

(6) Table Colors (Title, Cell, and Text).

(7) To show/hide any of selected indicator’s components.

Section(2): Recurring Deposit Settings

(1) From DateTime of starting the investment.

(2) To DateTime of ending the investment

(3) The amount of recurring deposit into portfolio and currency.

(4) The frequency of recurring deposits into the portfolio {Weekly, 2-Weeks, Monthly, Quarterly, Yearly}

(5) The Depositing Model:

● Fixed: The amount for recurring deposits remains constant throughout the entire investment period.

● Increased %: The recurring deposit amount increases at the selected frequency and percentage throughout the entire investment period.

(5B) If the user selects “ Depositing Model: Increased % ”, specify the growth model (linear or exponential) and define the rate of increase.

Section(3): Portfolio Holdings

(1) Enable a ticker in the investment portfolio.

(2) The selected deposit frequency weight for a ticker. For example, if the monthly deposit is $1,000 and the selected weight for XYZ stock is 30%, $300 will be used to purchase shares of XYZ stock.

(3) Select up to 6 tickers that the investor is interested in for long-term investment.

Please let me know if you have any questions

ROI Levels IndicatorROI Levels Indicator 📈💰

Description: The "ROI Levels Indicator" helps you visualize key Return on Investment (ROI) levels directly on your chart, making it easier to track your profit milestones! 🚀 This tool allows you to enter your entry price, and it calculates levels from 100% up to 1000% ROI, each with a spread to represent potential support and resistance zones. The levels are visually represented by red rectangles to help identify zones where the market might react. This is a great way for traders to easily understand profit-taking points and psychological price levels!

Features:

🛠️ Custom Entry Price: Set your own entry price to start calculating ROI levels.

📊 Multiple ROI Levels: Levels from 100% to 1000%, with a customizable spread for visual clarity.

🔴 Visual Representation: Each level is marked with a full-screen-width rectangle and label, making it easy to track.

🚨 Entry Price Plot: A red dashed line marks your entry price for easy reference.

How to Use:

Enter Your Price: Use the "Entry Price" input field to specify the entry price of your trade.

Spread Adjustment: Adjust the spread percentage if you want more or less tolerance around each ROI level.

View the Levels: The script automatically plots 100% to 1000% ROI levels. Each level is represented by a red rectangle and labeled on the right side for quick identification.

Track Profit Zones: Use the plotted ROI levels to identify key profit-taking areas or potential zones of support and resistance.

Pro Tip: Use these levels as reference points to decide when to scale out of positions or manage risk effectively! 🎯

Happy trading, and may your ROI always be on the rise! 📈🔥

QuantBuilder | FractalystWhat's the strategy's purpose and functionality?

QuantBuilder is designed for both traders and investors who want to utilize mathematical techniques to develop profitable strategies through backtesting on historical data.

The primary goal is to develop profitable quantitive strategies that not only outperform the underlying asset in terms of returns but also minimize drawdown.

For instance, consider Bitcoin (BTC), which has experienced significant volatility, averaging an estimated 200% annual return over the past decade, with maximum drawdowns exceeding -80%. By employing this strategy with diverse entry and exit techniques, users can potentially seek to enhance their Compound Annual Growth Rate (CAGR) while managing risk to maintain a lower maximum drawdown.

While this strategy employs quantitative techniques, including mathematical methods such as probabilities and positive expected values, it demonstrates exceptional efficacy across all markets. It particularly excels in futures, indices, stocks, cryptocurrencies, and commodities, leveraging their inherent trending behaviors for optimized performance.

In both trending and consolidating market conditions, QuantBuilder employs a combination of multi-timeframe probabilities, expected values, directional biases, moving averages and diverse entry models to identify and capitalize on bullish market movements.

How does the strategy perform for both investors and traders?

The strategy has two main modes, tailored for different market participants: Traders and Investors.

1. Trading:

- Designed for traders looking to capitalize on bullish markets.

- Utilizes a percentage risk per trade to manage risk and optimize returns.

- Suitable for both swing and intraday trading with a focus on probabilities and risk per trade approach.

2. Investing:

- Geared towards investors who aim to capitalize on bullish trending markets without using leverage while mitigating the asset's maximum drawdown.

- Utilizes pre-define percentage of the equity to buy, hold, and manage the asset.

- Focuses on long-term growth and capital appreciation by fully/partially investing in the asset during bullish conditions.

How does the strategy identify market structure? What are the underlying calculations?

The strategy utilizes an efficient logic with for loops to pinpoint the first swing candle featuring a pivot of 2, establishing the point at which the break of structure begins.

What entry criteria are used in this script? What are the underlying calculations?

The script utilizes two entry models: BreakOut and fractal.

Underlying Calculations:

Breakout: The script assigns the most recent swing high to a variable. When the price closes above this level and all other conditions are met, the script executes a breakout entry (conservative approach).

Fractal: The script identifies a swing low with a period of 2. Once this condition is met, the script executes the trade (aggressive approach).

How does the script calculate probabilities? What are the underlying calculations?

The script calculates probabilities by monitoring price interactions with liquidity levels. Here’s how the underlying calculations work:

Tracking Price Hits: The script counts the number of times the price taps into each liquidity side after the EQM level is activated. This data is stored in an array for further analysis.

Sample Size Consideration: The total number of price interactions serves as the sample size for calculating probabilities.

Probability Calculation: For each liquidity side, the script calculates the probability by taking the average of the recorded hits. This allows for a dynamic assessment of the likelihood that a particular side will be hit next, based on historical performance.

Dynamic Adjustment: As new price data comes in, the probabilities are recalculated, providing real-time aduptive insights into market behavior.

Note: The calculations are performed independently for each directional range. A range is considered bearish if the previous breakout was through a sellside liquidity. Conversely, a range is considered bullish if the most recent breakout was through a buyside liquidity.

How does the script calculate expected values? What are the underlying calculations?

The script calculates expected values by leveraging the probabilities of winning and losing trades, along with their respective returns. The process involves the following steps:

This quantitative methodology provides a robust framework for assessing the expected performance of trading strategies based on historical data and backtesting results.

How is the contextual bias calculated? What are the underlying calculations?

The contextual bias in the QuantBuilder script is calculated through a structured approach that assesses market structure based on swing highs and lows. Here’s how it works:

Identification of Swing Points: The script identifies significant swing points using a defined pivot logic, focusing on the first swing high and swing low. This helps establish critical levels for determining market structure.

Break of Structure (BOS) Assessment:

Bullish BOS: The script recognizes a bullish break of structure when a candle closes above the first swing high, followed by at least one swing low.

Bearish BOS: Conversely, a bearish break of structure is identified when a candle closes below the first swing low, followed by at least one swing high.

Bias Assignment: Based on the identified break of structure, the script assigns directional biases:

A bullish bias is assigned if a bullish BOS is confirmed.

A bearish bias is assigned if a bearish BOS is confirmed.

Quantitative Evaluation: Each identified bias is quantitatively evaluated, allowing the script to assign numerical values representing the strength of each bias. This quantification aids in assessing the reliability of market sentiment across multiple timeframes.

What's the purpose of using moving averages in this strategy? What are the underlying calculations?

Using moving averages is a widely-used technique to trade with the trend.

The main purpose of using moving averages in this strategy is to filter out bearish price action and to only take trades when the price is trading ABOVE specified moving averages.

The script uses different types of moving averages with user-adjustable timeframes and periods/lengths, allowing traders to try out different variations to maximize strategy performance and minimize drawdowns.

By applying these calculations, the strategy effectively identifies bullish trends and avoids market conditions that are not conducive to profitable trades.

The MA filter allows traders to choose whether they want a specific moving average above or below another one as their entry condition.

What type of stop-loss identification method are used in this strategy? What are the underlying calculations?

- Initial Stop-loss:

1. ATR Based:

The Average True Range (ATR) is a method used in technical analysis to measure volatility. It is not used to indicate the direction of price but to measure volatility, especially volatility caused by price gaps or limit moves.

Calculation:

- To calculate the ATR, the True Range (TR) first needs to be identified. The TR takes into account the most current period high/low range as well as the previous period close.

The True Range is the largest of the following:

- Current Period High minus Current Period Low

- Absolute Value of Current Period High minus Previous Period Close

- Absolute Value of Current Period Low minus Previous Period Close

- The ATR is then calculated as the moving average of the TR over a specified period. (The default period is 14)

2. ADR Based:

The Average Day Range (ADR) is an indicator that measures the volatility of an asset by showing the average movement of the price between the high and the low over the last several days.

Calculation:

- To calculate the ADR for a particular day:

- Calculate the average of the high prices over a specified number of days.

- Calculate the average of the low prices over the same number of days.

- Find the difference between these average values.

- The default period for calculating the ADR is 14 days. A shorter period may introduce more noise, while a longer period may be slower to react to new market movements.

3. PL Based:

This method places the stop-loss at the low of the previous candle.

If the current entry is based on the hunt entry strategy, the stop-loss will be placed at the low of the candle that wicks through the lower FRMA band.

Example:

If the previous candle's low is 100, then the stop-loss will be set at 100.

This method ensures the stop-loss is placed just below the most recent significant low, providing a logical and immediate level for risk management.

- Trailing Stop-Loss:

One of the key elements of this strategy is its ability to detect structural liquidity and structural invalidation levels across multiple timeframes to trail the stop-loss once the trade is in running profits.

By utilizing this approach, the strategy allows enough room for price to run.

By using these methods, the strategy dynamically adjusts the initial stop-loss based on market volatility, helping to protect against adverse price movements while allowing for enough room for trades to develop.

Each market behaves differently across various timeframes, and it is essential to test different parameters and optimizations to find out which trailing stop-loss method gives you the desired results and performance.

What type of break-even and take profit identification methods are used in this strategy? What are the underlying calculations?

For Break-Even:

Percentage (%) Based:

Moves the initial stop-loss to the entry price when the price reaches a certain percentage above the entry.

Calculation:

Break-even level = Entry Price * (1 + Percentage / 100)

Example:

If the entry price is $100 and the break-even percentage is 5%, the break-even level is $100 * 1.05 = $105.

Risk-to-Reward (RR) Based:

Moves the initial stop-loss to the entry price when the price reaches a certain RR ratio.

Calculation:

Break-even level = Entry Price + (Initial Risk * RR Ratio)

For TP1 (Take Profit 1):

- You can choose to set a take profit level at which your position gets fully closed or 50% if the TP2 boolean is enabled.

- Similar to break-even, you can select either a percentage (%) or risk-to-reward (RR) based take profit level, allowing you to set your TP1 level as a percentage amount above the entry price or based on RR.

For TP2 (Take Profit 2):

- You can choose to set a take profit level at which your position gets fully closed.

- As with break-even and TP1, you can select either a percentage (%) or risk-to-reward (RR) based take profit level, allowing you to set your TP2 level as a percentage amount above the entry price or based on RR.

What's the day filter Filter, what does it do?

The day filter allows users to customize the session time and choose the specific days they want to include in the strategy session. This helps traders tailor their strategies to particular trading sessions or days of the week when they believe the market conditions are more favorable for their trading style.

Customize Session Time:

Users can define the start and end times for the trading session.

This allows the strategy to only consider trades within the specified time window, focusing on periods of higher market activity or preferred trading hours.

Select Days:

Users can select which days of the week to include in the strategy.

This feature is useful for excluding days with historically lower volatility or unfavorable trading conditions (e.g., Mondays or Fridays).

Benefits:

Focus on Optimal Trading Periods:

By customizing session times and days, traders can focus on periods when the market is more likely to present profitable opportunities.

Avoid Unfavorable Conditions:

Excluding specific days or times can help avoid trading during periods of low liquidity or high unpredictability, such as major news events or holidays.

What tables are available in this script?

- Summary: Provides a general overview, displaying key performance parameters such as Net Profit, Profit Factor, Max Drawdown, Average Trade, Closed Trades and more.

Total Commission: Displays the cumulative commissions incurred from all trades executed within the selected backtesting window. This value is derived by summing the commission fees for each trade on your chart.

Average Commission: Represents the average commission per trade, calculated by dividing the Total Commission by the total number of closed trades. This metric is crucial for assessing the impact of trading costs on overall profitability.

Avg Trade: The sum of money gained or lost by the average trade generated by a strategy. Calculated by dividing the Net Profit by the overall number of closed trades. An important value since it must be large enough to cover the commission and slippage costs of trading the strategy and still bring a profit.

MaxDD: Displays the largest drawdown of losses, i.e., the maximum possible loss that the strategy could have incurred among all of the trades it has made. This value is calculated separately for every bar that the strategy spends with an open position.

Profit Factor: The amount of money a trading strategy made for every unit of money it lost (in the selected currency). This value is calculated by dividing gross profits by gross losses.

Avg RR: This is calculated by dividing the average winning trade by the average losing trade. This field is not a very meaningful value by itself because it does not take into account the ratio of the number of winning vs losing trades, and strategies can have different approaches to profitability. A strategy may trade at every possibility in order to capture many small profits, yet have an average losing trade greater than the average winning trade. The higher this value is, the better, but it should be considered together with the percentage of winning trades and the net profit.

Winrate: The percentage of winning trades generated by a strategy. Calculated by dividing the number of winning trades by the total number of closed trades generated by a strategy. Percent profitable is not a very reliable measure by itself. A strategy could have many small winning trades, making the percent profitable high with a small average winning trade, or a few big winning trades accounting for a low percent profitable and a big average winning trade. Most mean-reversion successful strategies have a percent profitability of 40-80% but are profitable due to risk management control.

BE Trades: Number of break-even trades, excluding commission/slippage.

Losing Trades: The total number of losing trades generated by the strategy.

Winning Trades: The total number of winning trades generated by the strategy.

Total Trades: Total number of taken traders visible your charts.

Net Profit: The overall profit or loss (in the selected currency) achieved by the trading strategy in the test period. The value is the sum of all values from the Profit column (on the List of Trades tab), taking into account the sign.

- Monthly: Displays performance data on a month-by-month basis, allowing users to analyze performance trends over each month and year.

- Weekly: Displays performance data on a week-by-week basis, helping users to understand weekly performance variations.

- UI Table: A user-friendly table that allows users to view and save the selected strategy parameters from user inputs. This table enables easy access to key settings and configurations, providing a straightforward solution for saving strategy parameters by simply taking a screenshot with Alt + S or ⌥ + S.

User-input styles and customizations:

To facilitate studying historical data, all conditions and filters can be applied to your charts. By plotting background colors on your charts, you'll be able to identify what worked and what didn't in certain market conditions.

Please note that all background colors in the style are disabled by default to enhance visualization.

How to Use This Quantitive Strategy Builder to Create a Profitable Edge and System?

Choose Your Strategy mode:

- Decide whether you are creating an investing strategy or a trading strategy.

Select a Market:

- Choose a one-sided market such as stocks, indices, or cryptocurrencies.

Historical Data:

- Ensure the historical data covers at least 10 years of price action for robust backtesting.

Timeframe Selection:

- Choose the timeframe you are comfortable trading with. It is strongly recommended to use a timeframe above 15 minutes to minimize the impact of commissions/slippage on your profits.

Set Commission and Slippage:

- Properly set the commission and slippage in the strategy properties according to your broker/prop firm specifications.

Parameter Optimization:

- Use trial and error to test different parameters until you find the performance results you are looking for in the summary table or, preferably, through deep backtesting using the strategy tester.

Trade Count:

- Ensure the number of trades is 200 or more; the higher, the better for statistical significance.

Positive Average Trade:

- Make sure the average trade is above zero.

(An important value since it must be large enough to cover the commission and slippage costs of trading the strategy and still bring a profit.)

Performance Metrics:

- Look for a high profit factor, and net profit with minimum drawdown.

- Ideally, aim for a drawdown under 20-30%, depending on your risk tolerance.

Refinement and Optimization:

- Try out different markets and timeframes.

- Continue working on refining your edge using the available filters and components to further optimize your strategy.

What makes this strategy original?

QuantBuilder stands out due to its unique combination of quantitative techniques and innovative algorithms that leverage historical data for real-time trading decisions. Unlike most algorithmic strategies that work based on predefined rules, this strategy adapts to real-time market probabilities and expected values, enhancing its reliability. Key features include:

Mathematical Framework: The strategy integrates advanced mathematical concepts, such as probabilities and expected values, to assess trade viability and optimize decision-making.

Multi-Timeframe Analysis: By utilizing multi-timeframe probabilities, QuantBuilder provides a comprehensive view of market conditions, enhancing the accuracy of entry and exit points.

Dynamic Market Structure Identification: The script employs a systematic approach to identify market structure changes, utilizing a blend of swing highs and lows to detect contextual/direction bias of the market.

Built-in Trailing Stop Loss: The strategy features a dynamic trailing stop loss based on multi-timeframe analysis of market structure. This allows traders to lock in profits while adapting to changing market conditions, ensuring that exits are executed at optimal levels without prematurely closing positions.

Robust Performance Metrics: With detailed performance tables and visualizations, users can easily evaluate strategy effectiveness and adjust parameters based on historical performance.

Adaptability: The strategy is designed to work across various markets and timeframes, making it versatile for different trading styles and objectives.

Suitability for Investors and Traders: QuantBuilder is ideal for both investors and traders looking to rely on mathematically proven data to create profitable strategies, ensuring that decisions are grounded in quantitative analysis.

These original elements combine to create a powerful tool that can help both traders and investors to build and refine profitable strategies based on algorithmic quantitative analysis.

Terms and Conditions | Disclaimer

Our charting tools are provided for informational and educational purposes only and should not be construed as financial, investment, or trading advice. They are not intended to forecast market movements or offer specific recommendations. Users should understand that past performance does not guarantee future results and should not base financial decisions solely on historical data.

Built-in components, features, and functionalities of our charting tools are the intellectual property of @Fractalyst Unauthorized use, reproduction, or distribution of these proprietary elements is prohibited.

By continuing to use our charting tools, the user acknowledges and accepts the Terms and Conditions outlined in this legal disclaimer and agrees to respect our intellectual property rights and comply with all applicable laws and regulations.

Portfolio Index Generator [By MUQWISHI]▋ INTRODUCTION:

The “Portfolio Index Generator” simplifies the process of building a custom portfolio management index, allowing investors to input a list of preferred holdings from global securities and customize the initial investment weight of each security. Furthermore, it includes an option for rebalancing by adjusting the weights of assets to maintain a desired level of asset allocation. The tool serves as a comprehensive approach for tracking portfolio performance, conducting research, and analyzing specific aspects of portfolio investment. The output includes an index value, a table of holdings, and chart plotting, providing a deeper understanding of the portfolio's historical movement.

_______________________

▋ OVERVIEW:

The image can be taken as an example of building a custom portfolio index. I created this index and named it “My Portfolio Performance”, which comprises several global companies and crypto assets.

_______________________

▋ OUTPUTS:

The output can be divided into 4 sections:

1. Portfolio Index Title (Name & Value).

2. Portfolio Specifications.

3. Portfolio Holdings.

4. Portfolio Index Chart.

1. Portfolio Index Title, displays the index name at the top, and at the bottom, it shows the index value, along with the chart timeframe, e.g., daily change in points and percentage.

2. Portfolio Specifications, displays the essential information on portfolio performance, including the investment date range, initial capital, returns, assets, and equity.

3. Portfolio Holdings, a list of the holding securities inside a table that contains the ticker, average entry price, last price, return percentage of the portfolio's initial capital, and customized weighted percentage of the portfolio. Additionally, a tooltip appears when the user passes the cursor over a ticker's cell, showing brief information about the company, such as the company's name, exchange market, country, sector, and industry.

4. Index Chart, display a plot of the historical movement of the index in the form of a bar, candle, or line chart.

_______________________

▋ INDICATOR SETTINGS:

Section(1): Style Settings

(1) Naming the index.

(2) Table location on the chart and cell size.

(3) Sorting Holdings Table. By securities’ {Return(%) Portfolio, Weight(%) Portfolio, or Ticker Alphabetical} order.

(4) Choose the type of index: {Equity or Return (%)}, and the plot type for the index: {Candle, Bar, or Line}.

(5) Positive/Negative colors.

(6) Table Colors (Title, Cell, and Text).

(7) To show/hide any indicator’s components.

Section(2): Performance Settings

(1) Calculation window period: from DateTime to DateTime.

(2) Initial Capital and specifying currency.

(3) Option to enable portfolio rebalancing in {Monthly, Quarterly, or Yearly} intervals.

Section(3): Portfolio Holdings

(1) Enable and count security in the investment portfolio.

(2) Initial weight of security. For example, if the initial capital is $100,000 and the weight of XYZ stock is 4%, the initial value of the shares would be $4,000.

(3) Select and add up to 30 symbols that interested in.

Please let me know if you have any questions.

Index Generator [By MUQWISHI]▋ INTRODUCTION :

The “Index Generator” simplifies the process of building a custom market index, allowing investors to enter a list of preferred holdings from global securities. It aims to serve as an approach for tracking performance, conducting research, and analyzing specific aspects of the global market. The output will include an index value, a table of holdings, and chart plotting, providing a deeper understanding of historical movement.

_______________________

▋ OVERVIEW:

The image can be taken as an example of building a custom index. I created this index and named it “My Oil & Gas Index”. The index comprises several global energy companies. Essentially, the indicator weights each company by collecting the number of shares and then computes the market capitalization before sorting them as seen in the table.

_______________________

▋ OUTPUTS:

The output can be divided into 3 sections:

1. Index Title (Name & Value).

2. Index Holdings.

3. Index Chart.

1. Index Title , displays the index name at the top, and at the bottom, it shows the index value, along with the daily change in points and percentage.

2. Index Holdings , displays list the holding securities inside a table that contains the ticker, price, daily change %, market cap, and weight %. Additionally, a tooltip appears when the user passes the cursor over a ticker's cell, showing brief information about the company, such as the company's name, exchange market, country, sector, and industry.

3. Index Chart , display a plot of the historical movement of the index in the form of a bar, candle, or line chart.

_______________________

▋ INDICATOR SETTINGS:

(1) Naming the index.

(2) Entering a currency. To unite all securities in one currency.

(3) Table location on the chart.

(4) Table’s cells size.

(5) Table’s colors.

(6) Sorting table. By securities’ (Market Cap, Change%, Price, or Ticker Alphabetical) order.

(7) Plotting formation (Candle, Bar, or Line)

(8) To show/hide any indicator’s components.

(9) There are 34 fields where user can fill them with symbols.

Please let me know if you have any questions.

SIP SmartlyIntroduction:

The SIP Smartly indicator is designed to mimic the behavior of a systematic investment plan, a popular investment strategy where a fixed quantity of an asset is purchased at regular intervals, typically monthly. In this case, we're applying this concept to trading by specifying a start date, a fixed purchase quantity, and certain conditions for buying.

Indicator Components:

User Inputs:

1. Start Date Inputs:

startyear, startmonth, startday: These inputs allow you to specify the year, month, and day when the SIP strategy begins.

2. buyQty:

This input allows you to specify the quantity of the security to purchase in each SIP installment.

What is Standard SIP ?

A Standard Systematic Investment Plan (SIP) is an investment strategy where individuals consistently invest a fixed amount of money at regular intervals, such as monthly or quarterly, in mutual funds or stocks. This approach promotes disciplined and long-term investing, taking advantage of rupee-cost averaging, where more shares are purchased when prices are low and fewer when prices are high. SIPs are designed for individuals seeking gradual wealth accumulation over time while mitigating the impact of market volatility through consistent, automated investments.

Logic of the Smart SIP Indicator:

Dynamic Quantity: The Smart SIP indicator allows you to invest a fixed quantity of a security at regular intervals based on technical analysis conditions. This is different from a standard SIP, where you typically invest a fixed amount of money.

Technical Analysis Driven: The Smart SIP indicator employs technical analysis indicators, such as multiple moving averages and uses the crossover of a higher MA with a lower MA which indicates a possible trend reversal, to determine Buy signals based on price trends. In contrast, a standard SIP doesn't consider technical factors but rather involves regular investments regardless of market conditions.

Adaptability: Unlike a standard SIP, which follows a predetermined investment schedule, the Smart SIP can adapt to changing market conditions. It triggers Buy actions only when specific technical conditions are met, providing a more flexible and responsive approach to investing or trading.

Market Value Tracking: The Smart SIP continuously tracks the market value of the invested quantity in real-time. This allows you to monitor the performance of your SIP investments dynamically, considering market fluctuations. In a standard SIP, you typically track the overall portfolio value without real-time adjustments.

Alert Notifications: The Smart SIP can send alert notifications when Buy conditions are met. This feature ensures timely execution of trades when favorable market conditions align with the technical criteria. In a standard SIP, you usually follow a fixed investment schedule without real-time alerting.

In summary, the unique logic of the Smart SIP indicator lies in its adaptability, technical analysis-driven approach, and real-time tracking and alerting features, making it well-suited for trading in financial markets while still following the concept of a systematic investment plan.

How to Use the SIP Smartly Indicator:

Start Date Selection:

Input your desired start date using the startyear, startmonth, and startday parameters. This is the date when your SIP strategy will begin.

Buy Quantity Setting:

Set the buyQty input to the quantity of the security you want to purchase in each SIP installment.

Alerts:

The indicator can trigger alerts when Buy conditions are met. These alerts can be configured to notify you when it's time to make a SIP installment.

Risk Management and Considerations:

Confirmation: While the SIP Smartly indicator provides insights, use it alongside other technical and fundamental analysis tools for confirmation before making trading decisions.

Backtesting: Before using this indicator in live trading, conduct thorough backtesting on historical data to evaluate its performance under different market conditions.

Position Sizing: Determine your position size and risk management rules based on the quantity purchased in each SIP installment.

Market Awareness: Stay informed about market conditions and news events that could impact price movements. This indicator is a tool to aid your trading strategy, not a standalone solution.

Conclusion:

The SIP Smartly Indicator offers a systematic approach to trading by simulating a SIP strategy. By inputting your start date and desired buy quantity, you can follow a disciplined investment approach in your trading. Remember to customize the inputs to match your trading preferences and risk tolerance.

Disclaimer: This indicator is provided for educational purposes and should be used with caution. Trading involves risks, and you should thoroughly test any strategy before applying it in live trading.

EURUSD COT Trend StrategyThis is a long term/investment type of strategy designed to have a good idea about where the big trend direction is headed.

Its logic, its made entirely on the COT report, mainly from looking into the net non comercial positions aka the speculators.

For bullish trend we look that the difference between long non comercial vs short non comercial is higher than 0

For bearish trend we look that the difference between long non comercial vs short non comercial is lower than 0.

This is mainly as an educational tool, for a full strategy, I recommend implement other things into it, like technical analysis or risk management.

If you have any questions, please let me know !

Invest-Long : Script for quick checks before investingA simple script to verify RSI, SMAs, VWMA, and Pivots on Daily, Weekly, and Monthly time frames.

In case if you are not interested in SMA's or want to add different cheks -- simply copy the script to local and edit.

Happy investing.

Add the script to any chart and table values remain the same irrespective of current chart resolution, as it checks on Daily, Weekly, and Monthly time frames.

The table has multiple columns.

1st column checks on RSI value on all 3 timeframes. Ideally, look for all green and D>W>M

2nd Column: Check current Close is above 20 SMA and 50 SMA on Daily / Weekly / Monthly time frames

3rd Column: Check SMA 13> SMA 34, SMA 34 > SMA 55 and SMA 20 > SMA 50 on Daily / Weekly time frames

4th Column: Check Current close is above Weekly Pivot and Monthly Pivot. And also verify Close is above 4 Week High.

5th Column: Verify Close is above Daily VWMA. Also Daily VWMA is > Weekly VWMA and Weekly > Monthly.

// Similarly you can add more checks based on different time frames

Feel free to trouble me incase if need help.

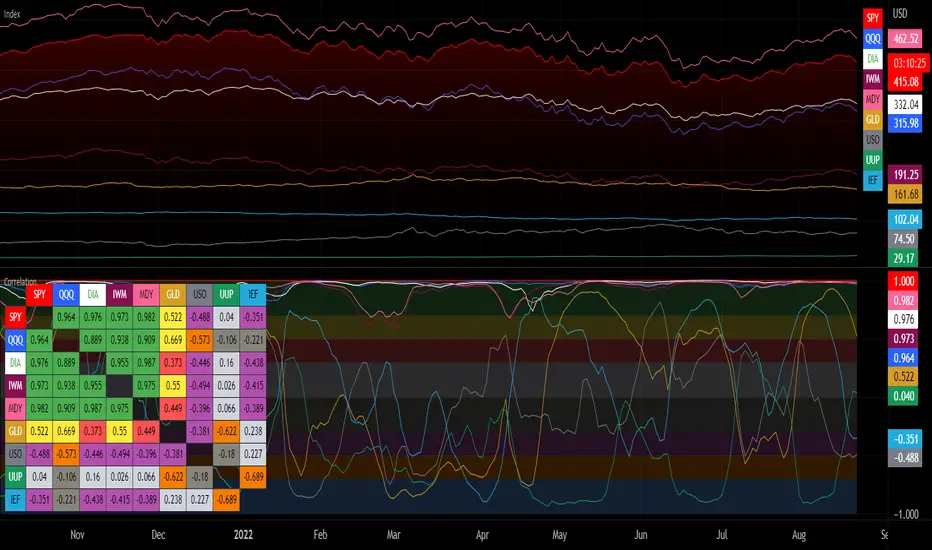

Correlation with Matrix TableCorrelation coefficient is a measure of the strength of the relationship between two values. It can be useful for market analysis, cryptocurrencies, forex and much more.

Since it "describes the degree to which two series tend to deviate from their moving average values" (1), first of all you have to set the length of these moving averages. You can also retrieve the values from another timeframe, and choose whether or not to ignore the gaps.

After selecting the reference ticker, which is not dependent from the chart you are on, you can choose up to eight other tickers to relate to it. The provided matrix table will then give you a deeper insight through all of the correlations between the chosen symbols.

Correlation values are scored on a scale from 1 to -1

A value of 1 means the correlation between the values is perfect.

A value of 0 means that there is no correlation at all.

A value of -1 indicates that the correlation is perfectly opposite.

For a better view at a glance, eight level colors are available and it is possible to modify them at will. You can even change level ranges by setting their threshold values. The background color of the matrix's cells will change accordingly to all of these choices.

The default threshold values, commonly used in statistics, are as follows:

None to weak correlation: 0 - 0.3

Weak to moderate correlation: 0.3 - 0.5

Moderate to high correlation: 0.5 - 0.7

High to perfect correlation: 0.7 - 1

Remember to be careful about spurious correlations, which are strong correlations without a real causal relationship.

(1) www.tradingview.com

Diversified Investment EMA Cross Strategy SimulatorThis simulating indicator proves that even if you use a simple strategy, you can reduce your risk by diversifying your investments.

The strategy itself is simple.(only long)

Buy when 50 days EMA crosses over 200 days EMA.

Sell when 50 days EMA crosses under 200 days EMA.

Or, stop loss when the asset falls by 2% (eg).

Using this simple strategy on an asset is just a test of your luck.

However, this capital change graph shows that risk can be reduced by diversifying investment into eight assets rather than one asset.

Options

Total Assets Capital Change represents the sum of capital changes for 8 assets. The gray line is the initial capital.

Each Asset Capital Change represents all eight asset capital changes. In this case, the gray line is displayed as the initial capital divided by 8.

The rest of the options show a graph of capital change for each asset, showing when buys and sells occurred.

And set the start date, initial capital, stop loss %, and commission.

And select the 8 assets you want to invest in and you are ready to go. To effectively reduce risk, uncoupled assets would be better if possible.

The table in the lower right shows the selected asset and color.

Please enjoy the simulation.

TrendTracers Bitcoin Stock to Flow ModelFor the best results, make sure to view this indicator on a bitcoin chart with a very long history (e.g. BNC:BLX)!

This model treats Bitcoin as being comparable to commodities such as gold, silver or platinum. These are known as ‘store of value’ commodities because they retain value over long time frames due to their relative scarcity. It is difficult to significantly increase their supply i.e. the process of searching for gold and then mining it is expensive and takes time. Bitcoin is similar because it is also scarce. In fact, it is the first-ever scarce digital object to exist. There are a limited number of coins in existence and it will take a lot of electricity and computing effort to mine the remaining coins still to be mined, therefore the supply rate is consistently low.

The stock-to-flow model predicts value changes in a straightforward manner. It compares an asset’s current stock to the rate of new production, or how much is produced in a year.

Calculation:

Take bitcoin production in a period, divide it by that period and then multiply by 365 to get the estimated yearly production and then calculate the stock to flow.

yearlyFlow = ((stockChange) / period ) * 365

stockToFlow = (stock - missingBitcoins) / yearlyFlow

Model Value = -1.84ᵉ * stockToFlow³.³⁶ (mathematical model to calculate the model price)

For more information about the calculations followed: stats.buybitcoinworldwide.com

Features:

Works on the Daily, Weekly and Monthly Timeframe.

Allows you to adjust between a 10-day period and a 463-day period.

Has the option to account for missing bitcoins, lets you adjust the amount of missing bitcoins.

The ability to toggle a standard deviation of the Model Value with a multiplier of 1, 2 or 3

Displays a Stock to Flow Deviation Ratio: If the Deviation Ratio is close to 0 it means the price of Bitcoin is close to the Model Value Line(or Stock to Flow Ratio). If the Deviation Ratio is close to 1 or -1, it means the price of bitcoin is near the selected deviation levels.

You can toggle between the Overlay version and the Oscillator version, default is on Oscillator version. If you want to switch: Untick Oscillator mode in the indicator settings, click on the three dots and select "move to existing pane above". Then click on the three dots again and select Pin to scale A. Done!

As a bonus: Now you can toggle a "1-year Realized Price" graph, while it's not officially part of the Stock to Flow Model it does share similar technicals about supply and scarcity. The 1-year Realized Price is the realized market cap divided by total amount of generated coins.

I just noticed that, while the color gradient function is pretty cool, it does not allow for end users to customize their colors after applying this indicator to their chart. Sorry!

Period Dollar Cost Average BacktesterHere is a simple script to calculate the profits and other dollar cost average strategy statistics. This strategy was created to avoid asset price volatility, so the pump and dump scheme does not affect the portfolio. By dividing the investment amount into periods, the investor doesn’t need to analyze the market, fundamental analysis, or anything. The goal is to increase the asset holdings and avoid fast and robust price movements.

This indicator has some configurations.

Amount to buy: the amount to buy at each time

Broker fee %: the fee percentage that the broker has for spot trade

Frequency: the frequency of the investments. Example: 1 Day means that every day, it will buy an amount of the asset

Starting Date: when the indicator will start the investment simulation

Ending Date: when the indicator will end the investment simulation

InfoCell With/Height: it relates to the panel for view purposes. Change the values to fit better on your screen.

This indicator has three lines:

Total Invested (green): total amount invested at the end of the period

Total Net Profit (pink): total profit by converting the amount of the asset bought at the latest closing price

Holding Profits (yellow): the amount that would be in the portfolio if the investor had invested all the capital in a signal trade at the beginning of the period.

The statistics panel has some information to help you understand buying the asset in one or more trades. So, besides those three lines that were mentioned above, here are the other statistics:

Entry Price: The price of the asset when the first investment was made

Gross Profit: Total amount of profit, not excluding the losses

Gross Losses: Total amount of losses, not excluding the profits

Profit Factor: The Gross Profit divided by the Gross Loss. A value above 1 means it’s profitable.

Profit/Trades: Net profit per trade. This includes the broker fees.

Recovery Factor: The Net profit divided by the relative drawdown. The higher the recovery factor, the faster the recovery of a loss

Total Asset Bought: The amount of the asset that was bought at the end of the investment plan

Absolute Drawdown: The total amount of losses that made the account balance go below its initial value

Relative Drawdown: The max drawdown that occurred, no matter the account balance amount

Total Trades: number of times the investment was made in the selected period

Total Fee: total Fee that was spent on the total investment

Total Winning Trades: the total amount of winning trades. A trade is considered a winner if the net profit is up compared with the latest investment.

Total Losing Trades: the total amount of losing trades. A trade is considered a loser if the net profit is down compared to the latest investment.

Max consecutive wins: the max amount of consecutive winning trades

Max consecutive losses: the max amount of consecutive losing trades

The chart above uses the default configuration of the indicator. Placed on the BTCUSD market, taking the time range of January 1st, 2018 to January 1st, 2022, 4 years. Buying a BTC amount with 10 USDT every day in that period would generate a more than 500% profit. Compared to the profit amount by just holding the count, which was close to 350% profit, the dollar cost average by period would be much more profitable.

Volatility ContractionVolatility Contraction is a strong trading setup for Positional Traders. It works on following time frame: Daily, Weekly and Monthly.

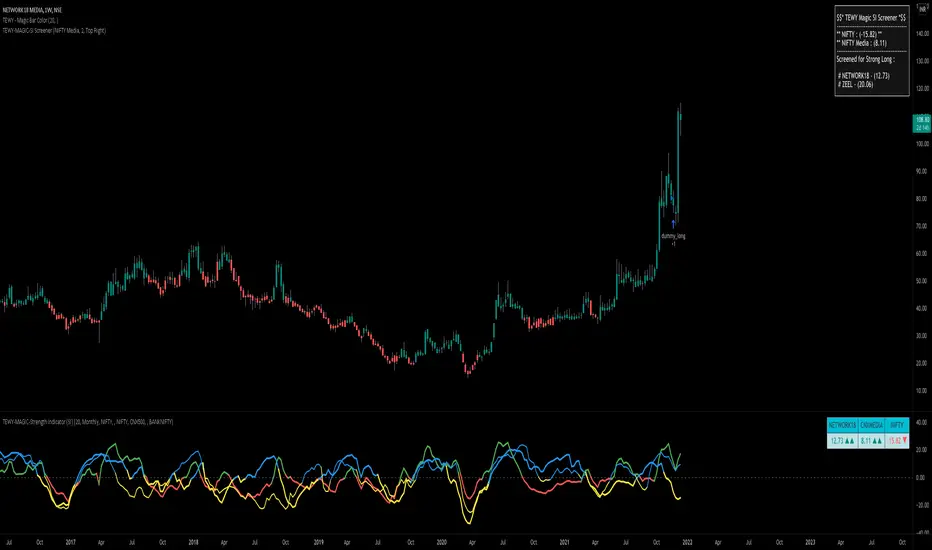

TEWY - Magic Strength Indicator (SI) ScreenerDetail about this indicator

This is screener to identify outperforming Stocks/Ticker based on the indicator "TEWY - Magic Strength Indicator (SI)" I deployed earlier. So please checkout that indicator description to understand more about this screener logic.

Below are the parameters that you may need to use to get outperforming indices/tickers.

1. Screener Set Name :

• Here you can see few of the predefined Index/Ticker sets i created, which you can use to screen Index/Ticker.

• If you select Set for 'Indices' you will get the list of Indices which are out performing NSE:NIFTY. Once you know which index is outperforming, then select the Set for that Index which I already given in the dropdown. That you will get the list of outperforming stock under that index.

• If you want to see all scripts of selected Sector Index that are outperforming NIFTY and may or may not be be outperforming Sector index, then please uncheck the box for "Outperforming Child Index Also". This will get you all the list of Stocks/Tickers which are outperforming Main Index NIFTY.

• If you want to see out-performers for specific period of time then change "How Many Outperforming Candles/Bars" as per your choice

• If you want to see under performers for Short trades then select "Find Short Trades" checkbox

• If you want to see the scripts which are just changed there signal then select "Latest Only" checkbox

Always respect RISKS and follow stop loss. In market stop loss is the only friend of yours.

I have given a sample illustrational image below, which should help you understand this indicator.

Best of luck

TEWY - Magic Strength Indicator (SI)Detail about this indicator

1. This indicator is used to identify the trend based on the momentum of the counter selected.

2. This indicator is calculated three different metrics for selected script and it's Parent/Main Index as NSE:NIFTY (default) and Sector Index. Keep in mind below point

a) Parent/Main index is set to default NSE:NIFTY, though there is option to provide your own custom parent index e.g. US30, US 100'

B) Sector Index is identified automatically for set to predefined stocks and rest ate set to default NIFTY 500. Again you have option to change it to your preference

3. I have used the rate of change and RSI of it to calculate momentum for script, it's parent index and sector index.

4. I would typically use this indicator to see momentum on the Monthly and Weekly first and daily timeframe to get proper entry.

5. Also please try to stay in the long position only unless you understand the consequences for shorting a stock . why? because the imminent nature of the market is to go upward only.

6. Please try to keep base inputs as defaults, though it allows you to change input parameters

Let's understand this indicator

• On the tor right corner you would see three different numbers. 1st number is SI of the underlying Ticker. 2nd number is SI for the Sector Index and 3rd is for Parent Index SI.

• If selected ticker is outperforming it's parent index the you see one green "▲" and if ticker is also outperforming it's sector index then you would see two green "▲▲". Same on the downside.

• I would only take long position if selected ticker is at least outperforming Parent index, that means at least one green "▲".

• I would take exit from the position if I see no more green "▲".

Always respect RISKS and follow stop loss. In market stop loss is the only friend of yours.

I have given a sample illustrational image below, which should help you understand this indicator.

Best of luck

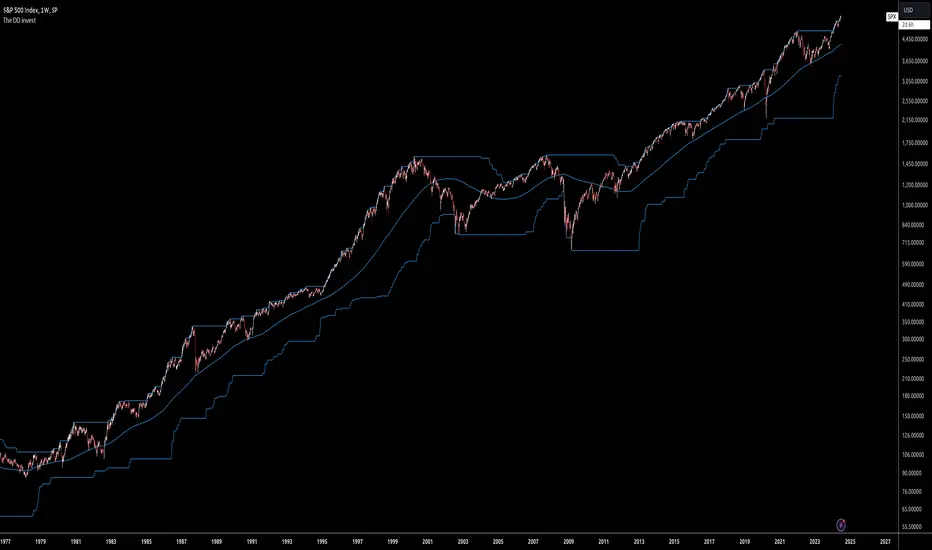

The DD investThe script tells me when to invest in the stock.

Split ur money into 3 piles. Each must be bigger than the previous one.

Buy with the first pile when the chart touches the middle line (SMA200).

Buy with the second pile when the chart touches the bottom line (lowest price of 200 weeks).

Buy with the third pile when the chart goes significantly below the bottom line (lowest price of 200 weeks).

Watch only the W1 chart (!!!).

Circles on the chart indicate places where you should buy (examples).

Consider selling half of the holding when the chart touches the top line (the highest price of 200 weeks).

Hold the rest much longer then you plan to ;)

FCMS - Time in x Timing - The Market - StudyTime in x Timing - The Market

█ DISCLAIMER

THIS IS NOT AN INVESTMENT ADVICE

The use of strategy functions doesn't compile recurring investments/contributions as used in this study, so disregard the results of the strategy tester.

As seen in the style/plots lists, I calculate the results in internal variables to analyze historical results.

prnt.sc

Anyway, this is only a historical study and past performance is no guarantee of future results

█ CONCEPTS

There is a discussion about Timing x Time in the market.

The point of this discussion is between buying in the better moment, against exposing yourself to the market as soon as possible.

Anyone who argues that the most important factor is the time exposed to the asset, no matter when, is usually based on the SP500 asset.

As shown in the image above, a hypothetical investor who made a single investment of US $ 1500.00 in December 1999, was trapped by a volatility of approximately 10% in the period, followed by a loss of around 50% in the following years. In December 2012, this investment was finally positive, and after 20 years it accumulated a gain of 180% - without reducing inflation in the period.

█ Timing the news

When an asset reaches a new historic high, the idea of "time in the market is the best strategy" gains momentum, after all, at this "moment" everyone previously exposed to the asset is making a profit, regardless of inflation or any benchmark.

█ Time in the market

Considering using this strategy, we can define 3 points for a brief analysis:

1. Asset

SPX is used as a reference for this type of statement due to the difficulty of finding another one with such consistency, liquidity, ease of access and time of history.

2. Long Term

We cannot consider it a long term strategy, as it never has a predetermined term

3. Recurring contributions.

To generate an average cost spread over periods of high and low, opening the possibility to realize positions with profit in eventual needs.

As shown in the image below, if this hypothetical investor made monthly contributions since the date of the first contributions, he would have the possibility of making profits between the period from October 2004 to September 2008, returning to the loss until October 2010, and then with a profit of 100% over the total amount invested.

Below, an example of an asset in a downtrend with the final balance returning below the total volume invested.

█ First Conclusion

> Recurring contributions (3) to an asset (1) during a downtrend will increase the loss for an indefinite period (2).

> Recurring contributions (3) to an asset (1) during an uptrend are more important than immediate exposure to the asset, regardless of the term (2).

> Recurring contributions (3) in an asset (1) in a region of possible long-term top (2), will negatively affect profitability even considering the resumption of the upward trend in an indefinite period.

█ Timing the market

As shown in the image below, following the strategy above: a single contribution in the amount of US$ 1000.00 at the worst moment (Dec / 2017), the hypothetical investor would have hold a loss of over 80%. At the moment it accumulates 89% of profit, having reached the maximum of 200% at the beginning of the year.

By making monthly contributions since the date of the first contribution, this investor would have the possibility to make profits from May 2019, accumulating 335% profit at the moment.

Adding the condition of buying the maximum cost of 10% above the average price of the last 200 days, the final result is little affected, and reduces losses in the initial investment period.

Adding the condition of taking profit of 50% of the position when the price is above the average of the last 200 days, and reinvesting 50% of the cash obtained in the next purchase opportunity (paying a maximum of 10% above the average of the last 200 days), the profit cumulative final price drops to 270%, but the realized profit already exceeds the total amount invested, which eliminates future risk of the operation. (favorable risk-return ratio)

Adding the condition to reinvest 50% of the cash flow, with the condition to buy when the price is below 20% away from the average of the last 200 days, the final result would be more than 400% of retained earnings, and realized profit in cash greater than the total amount invested.

█ Other Assets

It's possible to analyze other assets, including dividend yield and earnings for the equity formula. This way we can analyse assets more fairly.

ITSA4

BOVA11

█ Final Conclusion

> Exposing yourself early to a good opportunity may be good, but the risk of doing so at the wrong time could delay your projects indefinitely.

> Investment recurrence is the main driver for your future results.

> Setting a maximum value for making entries reduces short-term fluctuation but, in the long run, the effect is almost imperceptible.

> The realization of profits at favorable times considerably reduces the risk and volatility of the balance, in addition to providing cash for better opportunities in the short and medium term.

> Taking advantage of part of this cash flow for purchases in moments of opportunity, enhances future earnings.

Even an extremely simple strategy like the one used in the examples above, offers a better risk return for the investor compared to the immediate exposure to an asset.

Thus arises the desire to study more sophisticated strategies, as we will see in the future

█ Challenges

Time in the market

- Find good assets (1) to make recurring contributions (3) for an indeterminate period (2).

Timing the market

- Reading the markets to position yourself in favor of the more probable trends at certain times with predetermined terms.

Multi ROIThis is really, really, really basic.

Its just 10 ROIs - Return On Investment- plots for the following periods:

1 week

1 month

1/2 year

1 year

2 year

3 year

4 year

5 year

6 year

7 year

It is meant for 1 day bars. Of course it will work anywhere and you can change the settings to fit your purposes but I thought these were the most useful periods.

TM24_INVESTMENT_TOOLTM24_INVESTMENT_TOOL helps to identify following Things for Intraday Position on 60 Minutes + timeframe along with Buy or sell signal.

1. Market Trend (Different Timeframe)

2. Price Direction

3. Area of Support & Resistance

4. Price Momentum

Terminology Use ==> Black from Bottom for - Buy, Red from Top for - Sale Signal, and Numbers are to show time frame indication there is presence of buyer or seller like 30 for buy signal on 30 minute time frame etc.

Display and Interpretation ==> Buy Sale Signal in Digit with 15-30-60-D-W-M for different time frames.

any value signal ending with * shows breakout of support/ resistance and value signal starting with * shows entry to a momentum zone.

Green Mark with Triangle Up shows trend of that timeframe in positive and value shows upside possible direction on that timeframe vice versa for red signal with down triangle

Use market structure, chart pattern, trend lines for more support..