粽子趋势波段策略应用在一小时图表上,提示做多或做空信号,注意⚠️每个信号只作为独立的进场信号,止盈止损自己把握,如做多信号出来之后,可进场做多,止盈止损自己把握,当做空信号出来后并不是前面做多信号的止盈信号,而是独立的新的做空信号,所以止盈止损需自己把握。

本策略适用于加密货币,外汇黄金,股票,期货,指数,作为运用在一小时图表上的做多做空进场信号提示。

联系作者,微:bbm_im7

Applied on the one-hour chart, prompting the long or short signal, note ⚠️ Each signal is only used as an independent entry signal, and the take-profit stop loss is grasped by yourself. For example, after the long signal comes out, you can enter the market and make a long, and the take-profit stop loss is grasped by yourself. When the short signal comes out, it is not the take-profit signal of the previous long signal, but independent The new short-sal signal, so you need to grasp the take-profit and stop-loss by yourself.

This strategy is applicable to cryptocurrencies, foreign exchange gold, stocks, futures, indexes, and is used as a signal prompt to enter the market on the one-hour chart.

Medie mobili

AurumFx ATR with EMAThis strategy combines the strength of breakout momentum with trend confirmation for precision entries. It uses a 9-period EMA to define short-term trend bias, while identifying key breakout points using 20-bar highs and lows. Long trades trigger on bullish breakouts above the previous high when price is above the EMA, while shorts trigger on bearish breakdowns below the prior low when price is below the EMA. Designed for traders seeking a simple yet effective trend-following system with clear visual signals and dynamic market adaptation.

MVO - MA Signal StrategyStrategy Description: MA Signal Strategy with Heikin Ashi, Break-even and Trailing Stop

⸻

🔍 Core Concept

This strategy enters long or short trades based on Heikin Ashi candles crossing above or below a moving average (MA), with optional confirmation from the Money Flow Index (MFI). It includes:

• Dynamic stop loss and take profit levels based on ATR

• Optional break-even stop adjustment

• Optional trailing stop activation after breakeven

• Full visual feedback for trades and zones

⸻

⚙️ Indicators Used

• Heikin Ashi Candles: Smooth price action to reduce noise.

• Simple Moving Average (MA): Determines trend direction.

• Average True Range (ATR): Sets volatility-based SL/TP.

• Money Flow Index (MFI): Optional momentum filter for entries.

⸻

📈 Trade Entry Logic

✅ Long Entry:

Triggered if:

• Heikin Ashi close crosses above the MA

or

• MFI is below 20 and Heikin Ashi close is above the MA

❌ Short Entry:

Triggered if:

• Heikin Ashi close crosses below the MA

or

• MFI is above 90 and Heikin Ashi close is below the MA

⸻

🛑 Stop Loss & Take Profit

• SL is set using riskMult * ATR

• TP is set using rewardMult * ATR

Example:

• If ATR = 10, riskMult = 1, rewardMult = 5

→ SL = 10 points, TP = 50 points from entry

⸻

⚖️ Break-even Logic (Optional)

• If price moves in your favor by breakevenTicks * ATR, SL is moved to entry price.

• Enabled via checkbox Enable Break Even.

⸻

📉 Trailing Stop Logic (Optional)

• Once break-even is hit, a trailing stop starts moving behind price by trailATRmult * ATR.

• Trailing stop only activates after break-even is reached.

• Enabled via checkbox Enable Trailing Stop.

📊 Visual Elements

• Heikin Ashi candles are drawn on the main chart.

• Trade zones are shaded between SL and TP during open trades.

• Lines mark Entry, SL, TP, Break-even trigger.

• Markers show entries and exits:

• Green/red triangles = long/short entries

• ✅ = Take profit hit

• ❌ = Stop loss hit

✅ Best Use Case

• Trending markets with strong pullbacks

• Works on multiple timeframes

• Better suited for assets with consistent volatility (ATR behavior)

PHANTOM STRIKE Z-4 [ApexLegion]Phantom Strike Z-4

STRATEGY OVERVIEW

This strategy represents an analytical framework using 6 detection systems that analyze distinct market dimensions through adaptive timeframe optimization. Each system targets specific market inefficiencies - automated parameter adjustment, market condition filtering, phantom strike pattern detection, SR exit management, order block identification, and volatility-aware risk management - with results processed through a multi-component scoring calculation that determines signal generation and position management decisions.

SYSTEM ARCHITECTURE PHILOSOPHY

Phantom Strike Z-4 operates through 12 distinct parameter groups encompassing individual settings that allow detailed customization for different trading environments. The strategy employs modular design principles where each analytical component functions independently while contributing to unified decision-making protocols. This architecture enables traders to engage with structured market analysis through intuitive configuration options while the underlying algorithms handle complex computational processes.

The framework approaches certain aspects differently from static trading approaches by implementing real-time parameter adjustment based on timeframe characteristics, market volatility conditions, news event detection, and weekend gap analysis. During low-volatility periods where traditional strategies struggle to generate meaningful returns, Z-4's adaptive systems identify micro-opportunities through formation analysis and systematic patience protocols.

🔍WHY THESE CUSTOM SYSTEMS WERE INDEPENDENTLY DEVELOPED

The strategy approaches certain aspects differently from traditional indicator combinations through systematic development of original analytical approaches:

# 1. Auto Timeframe Optimization Module (ATOM)

Problem Identification: Standard strategies use fixed parameters regardless of timeframe characteristics, leading to over-optimization on specific timeframes and reduced effectiveness when market conditions change between different time intervals. Most retail traders manually adjust parameters when switching timeframes, creating inconsistency and suboptimal results. Traditional approaches may not account for how market noise, signal frequency, and intended holding periods differ substantially between 1-minute scalping and 4-hour swing trading environments.

Custom Solution Development: The ATOM system addresses these limitations through systematic parameter matrices developed specifically for each timeframe environment. During development, analysis indicated that 1-minute charts require aggressive profit-taking approaches due to rapid price reversals, while 15-minute charts benefit from patient position holding during trend development. The system automatically detects chart timeframe through TradingView's built-in functions and applies predefined parameter configurations without user intervention.

Timeframe-Specific Adaptations:

For ultra-short timeframe trading (1-minute charts), the system recognizes that market noise dominates price action, requiring tight stop losses (1.0%) and rapid profit realization (25% at TP1, 35% at TP2, 40% at TP3). Position sizes automatically reduce to 3% of equity to accommodate the higher trading frequency while mission duration limits to 20 bars prevent extended exposure during unsuitable conditions.

Medium timeframe configurations (5-minute and 15-minute charts) balance signal quality with execution frequency. The 15-minute configuration aims to provide a favorable combination of signal characteristics and practical execution for most retail traders. Formation thresholds increase to 2.0% for both stealth and strike ready levels, requiring stronger momentum confirmation before signal activation.

Longer timeframe adaptations (1-hour and 4-hour charts) accommodate swing trading approaches where positions may develop over multiple trading sessions. Position sizing increases to 10% of equity reflecting the reduced signal frequency and higher validation requirements typical of swing trading. Take profit targets extend considerably (TP1: 2.0%, TP2: 4.0%, TP3: 8.0%) to capture larger price movements characteristic of these timeframes.

# 2. Market Condition Filtering System (MCFS)

Problem Identification: Existing volatility filters use simple ATR calculations that may not distinguish between trending volatility and chaotic noise, potentially affecting signal quality during news events, market transitions, and unusual trading sessions. Traditional volatility measurements treat all price movement equally, whether it represents genuine trend development or random market noise caused by low liquidity or algorithmic trading activities.

Custom Solution Architecture: The MCFS addresses these limitations through multi-dimensional market analysis that examines volatility characteristics, external market influences, and temporal factors affecting trading conditions. Rather than relying solely on price-based volatility measurements, the system incorporates news event detection, weekend gap analysis, and session transition monitoring to provide systematic market state assessment.

Volatility Classification and Response Framework:

• EXTREME Volatility Conditions (>2.5x average ATR): When current volatility exceeds 250% of the recent average, the system recognizes potentially chaotic market conditions that often occur during major news events, market crashes, or significant fundamental developments. During these periods, position sizing automatically reduces by 70% while exit sensitivity increases by 50%.

• HIGH Volatility Conditions (1.8-2.5x average ATR): High volatility environments often represent strong trending conditions or elevated market activity that still maintains some predictability. Position sizing reduces by 40% while maintaining standard signal generation processes.

• NORMAL Volatility Conditions (1.2-1.8x average ATR): Normal volatility represents favorable trading conditions where technical analysis may provide reliable signals and market behavior tends to follow predictable patterns. All strategy parameters operate at standard settings.

• LOW Volatility Conditions (0.8-1.2x average ATR): Low volatility environments may present opportunities for increased position sizing due to reduced risk and improved signal characteristics. Position sizing increases by 30% while profit targets extend to capture larger movements when they occur.

• DEAD Volatility Conditions (<0.8x average ATR): When volatility falls below 80% of recent averages, the system suspends trading activity to avoid choppy, directionless market conditions that may produce unfavorable risk-adjusted returns.

# 3. Phantom Strike Detection Engine (PSDE)

Problem Identification: Traditional momentum indicators may lag market reversals by 2-4 bars and can generate signals during consolidation periods. Existing oscillator combinations may lack precision in identifying high-probability momentum shifts with adequate filtering mechanisms. Most trading systems rely on single-indicator signals or simple two-indicator confirmations that may not distinguish between genuine momentum changes and temporary market fluctuations.

Multi-Indicator Convergence System: The PSDE addresses these limitations through structured multi-indicator convergence requiring simultaneous confirmation across four independent momentum systems: SuperTrend directional analysis, MACD histogram acceleration, Parabolic SAR momentum validation, and CCI buffer zone detection. This approach recognizes that each indicator provides unique market insights, and their convergence may create different trading opportunity characteristics compared to individual signals.

Enhanced vs Phantom Mode Operation:

Enhanced mode activates when at least three of the four primary indicators align with directional bias while meeting minimum validation criteria. Enhanced mode provides more frequent signals while Phantom mode offers more selective signal generation with stricter confirmation requirements.

Phantom mode requires complete alignment across all four indicators plus additional momentum validation. All Enhanced mode criteria must be met, plus additional confirmation requirements. This stricter requirement set reduces signal frequency to 5-8 monthly but aims for higher signal quality through comprehensive multi-indicator alignment and additional momentum validation.

# 4. Smart Resistance Exit Grid (SR Exit Grid)

Problem Identification: Static take-profit levels may not account for changing market conditions and momentum strength. Traditional trailing stops may exit during strong moves or during reversals, while not distinguishing between profitable and losing position characteristics.

Systematic Holding Evaluation Framework: The SR Exit Grid operates through continuous evaluation of position viability rather than predetermined price targets through a structured 4-stage priority hierarchy:

🎯 1st Priority: Standard Take Profit processing (Highest Priority)

🔄 2nd Priority: SMART EXIT (Only when TP not executed)

⛔ 3rd Priority: SL/Emergency/Timeout Exit

🛡️ 4th Priority: Smart Low Logic (Separate Safety Safeguard)

The system employs a tpExecuted flag mechanism ensuring that only one exit type activates per bar, preventing conflicting orders and maintaining execution priority. Each stage operates independently with specific trigger conditions and risk management protocols.

Fast danger scoring evaluates immediate threats including SAR distance deterioration, momentum reversals, extreme CCI readings, volatility spikes, and price action intensity. When combined scores exceed specified thresholds (8.0+ danger with <2.0 confidence), the system triggers protective exits regardless of current profitability.

# 5. Order Block Tracking System (OBTS)

Problem Identification: Standard support/resistance levels are static and may not account for institutional order flow patterns. Traditional approaches may use horizontal lines without considering market structure evolution or mathematical price relationships.

Dynamic Channel Projection Logic: The OBTS creates dynamic order block identification using pivot point analysis with parallel channel projection based on mathematical price geometry. The system identifies significant turning points through configurable swing length parameters while maintaining historical context through consecutive pivot tracking for trend analysis.

Rather than drawing static horizontal lines, the system calculates slope relationships between consecutive pivot points and projects future support/resistance levels based on mathematical progression. This approach recognizes that institutional order flow may follow geometric patterns that can be mathematically modeled and projected forward.

# 6. Volatility-Aware Risk Management (VARM)

Problem Identification: Fixed percentage risk management may not adapt optimally during varying market volatility regimes, potentially creating conservative exits in low volatility and limited protection during high volatility periods. Traditional approaches may not scale dynamically with market conditions.

Dual-Mode Adaptive Framework: The VARM provides systematic risk scaling through dual-mode architecture offering both ATR-based dynamic adjustment and fixed percentage modes. Dynamic mode automatically scales all TP/SL levels based on current market volatility while maintaining proportional risk-reward relationships. Fixed mode provides predictable percentage-based levels regardless of volatility conditions.

Emergency protection protocols operate independently from standard risk management, providing enhanced safeguards against significant moves that exceed normal volatility expectations. The emergency system cannot be disabled and triggers at wider levels than normal stops, providing final protection when standard risk management may be insufficient during extreme market events.

## Technical Formation Analysis System

The foundation of Z-4's analytical framework rests on a structured EMA system utilizing 8, 21, and 50-period exponential moving averages that create formation structure analysis. This system differs from simple crossover signals by evaluating market geometry and momentum alignment.

Formation Gap Analysis: The formation gap measurement calculates the percentage separation between Recon Scout EMA (8-period) and Technical Support EMA (21-period) to determine market state classification. When gap percentage falls below the Stealth Mode Threshold (default 1.5%), the market enters consolidation phase requiring enhanced patience. When gap exceeds Strike Ready Threshold (1.5%), conditions become favorable for momentum-based entries.

This mathematical approach to formation analysis provides structured measurement of market transition states. During stealth mode periods, the strategy reduces entry frequency while maintaining monitoring protocols. Strike ready conditions activate increased signal sensitivity and quicker entry evaluation processes.

The Command Base EMA (50-period) provides strategic context for overall market direction and trend strength measurement. Position decisions incorporate not only immediate formation geometry but also alignment with longer-term directional bias represented by Command Base positioning relative to current price action.

🎯CORE SYSTEMS TECHNICAL IMPLEMENTATION

# SuperTrend Foundation Analysis Implementation

SuperTrend calculation provides the directional foundation through volatility-adjusted bands that adapt to current market conditions rather than using fixed parameters. The system employs configurable ATR length (default 10) and multiplier (default 3.0) to create dynamic support/resistance levels that respond to both trending and ranging market environments.

Volatility-Adjusted Band Calculation:

st_atr = ta.atr(stal)

st_hl2 = (high + low) / 2

st_ub = st_hl2 + stm * st_atr

st_lb = st_hl2 - stm * st_atr

stb = close > st and ta.rising(st, 3)

The HL2 methodology (high+low)/2 aims to provide stable price reference compared to closing prices alone, reducing sensitivity to intraday price spikes that can distort traditional SuperTrend calculations. ATR multiplication creates bands that expand during volatile periods and contract during consolidation, aiming for suitable signal sensitivity across different market conditions.

Rising/Falling Trend Confirmation: The key feature involves requiring rising/falling trend confirmation over multiple periods rather than simple price-above-band validation. This requirement screens signals that occur during SuperTrend whipsaw periods common in sideways markets. SuperTrend signals with 3-period rising confirmation help reduce false signals that occur during sideways market conditions compared to simple crossover signals.

Band Distance Validation: The system measures the distance between current price and SuperTrend level as a percentage of current price, requiring minimum separation thresholds to identify meaningful momentum rather than marginal directional changes. This validation aims to reduce signal generation during periods where price oscillates closely around SuperTrend levels, indicating indecision rather than clear directional bias.

# MACD Histogram Acceleration System - Momentum Detection

MACD analysis focuses exclusively on histogram acceleration rather than traditional line crossovers, aiming to provide earlier momentum detection. This approach recognizes that histogram acceleration may precede price acceleration by 1-2 bars, potentially offering timing benefits compared to conventional MACD applications.

Acceleration-Based Signal Generation:

mf = ta.ema(close, mfl)

ms = ta.ema(close, msl)

ml = mf - ms

msg = ta.ema(ml, msgl)

mh = ml - msg

mb = mh > 0 and mh > mh and mh > mh

The requirement for positive histogram values that increase over two consecutive periods aims to identify genuine momentum expansion rather than temporary fluctuations. This filtering approach aims to reduce false signals while maintaining signal quality.

Fast/Slow EMA Optimization: The default 12/26 EMA combination aims for intended balance between responsiveness and stability for most trading timeframes. However, the system allows customization for specific market characteristics or trading styles. Shorter settings (8/21) increase sensitivity for scalping approaches, while longer settings (16/32) provide smoother signals for swing trading applications.

Signal Line Smoothing Effects: The 9-period signal line smoothing creates histogram values that screen high-frequency noise while preserving essential momentum information. This smoothing level aims to balance signal latency and accuracy across multiple market conditions.

# Parabolic SAR Validation Framework - Momentum Verification

Parabolic SAR provides momentum validation through price separation analysis and inflection detection that may precede significant trend changes. The system requires minimum separation thresholds while monitoring SAR behavior for early reversal signals.

Separation-Based Validation:

sar = ta.sar(ss, si, sm)

sarb = close > sar and (close - sar) / close > 0.005

sardp = math.abs(close - sar) / close * 100

sariu = sarm > 0 and sarm < 0 and math.abs(sarmc) > saris

The 0.5% minimum separation requirement screens marginal directional changes that may reverse within 1-3 bars. The 0.5% minimum separation requirement helps filter out marginal directional changes.

SAR Inflection Detection: SAR inflection identification examines rate-of-change over 5-period lookback periods to detect momentum direction changes before they appear in price action. Inflection sensitivity (default 1.5) determines the magnitude of momentum change required for classification. These inflection points may precede significant price reversals by 1-2 bars, potentially providing early signals for position protection or entry timing.

Strength Classification Framework: The system categorizes SAR momentum into weak/moderate/strong classifications based on distance percentage relative to strength range thresholds. Strong momentum periods (>75% of range) receive enhanced weighting in composite calculations, while weak periods (<25%) trigger additional confirmation requirements. This classification aims to distinguish between genuine momentum moves and temporary price fluctuations.

# CCI SMART Buffer Zone System - Oscillator Analysis

The CCI SMART system represents a detailed component of the PSDE, combining multiple mathematical techniques to create modified momentum detection compared to conventional CCI applications. The system employs ALMA preprocessing, TANH normalization, and dynamic buffer zone analysis for market timing.

ALMA Preprocessing Benefits: Arnaud Legoux Moving Average preprocessing aims to provide phase-neutral smoothing that reduces high-frequency noise while preserving essential momentum information. The configurable offset (0.85) and sigma (6.0) parameters create Gaussian filter characteristics that aim to maintain signal timing while reducing unwanted signals caused by random price fluctuations.

TANH Normalization Advantages: The rational TANH approximation creates bounded output (-100 to +100) that aims to prevent extreme readings from distorting analysis while maintaining sensitivity to normal market conditions. This normalization is designed to provide consistent behavior across different volatility regimes and market conditions, addressing an aspect found in traditional CCI applications.

Rational TANH Approximation Implementation:

rational_tanh(x) =>

abs_x = math.abs(x)

if abs_x >= 4.0

x >= 0 ? 1.0 : -1.0

else

x2 = x * x

numerator = x * (135135 + x2 * (17325 + x2 * (378 + x2)))

denominator = 135135 + x2 * (62370 + x2 * (3150 + x2 * 28))

numerator / denominator

cci_smart = rational_tanh(cci / 150) * 100

The rational approximation uses polynomial coefficients that provide mathematical precision equivalent to native TANH functions while maintaining computational efficiency. The 4.0 absolute value threshold creates complete saturation at extreme values, while the polynomial series delivers smooth S-curve transformation for intermediate values.

Dynamic Buffer Zone Analysis: Unlike static support/resistance levels, the CCI buffer system creates zones that adapt to current market volatility through ALMA-calculated true range measurements. Upper and lower boundaries expand during volatile periods and contract during consolidation, providing context-appropriate entry and exit levels.

CCI Buffer System Implementation:

cci = ta.cci(close, ccil)

cci_atr = ta.alma(ta.tr, al, ao, asig)

cci_bu = low - ccim * cci_atr

cci_bd = high + ccim * cci_atr

ccitu = cci > 50 and cci > cci

CCI buffer analysis creates dynamic support/resistance zones using ALMA-smoothed true range calculations rather than fixed levels. Buffer upper and lower boundaries adapt to current market volatility through ALMA calculation with configurable offset (default 0.85) and sigma (default 6.0) parameters.

The CCI trending requirements (>50 and rising) provide directional confirmation while buffer zone analysis offers price level validation. This dual-component approach identifies both momentum direction and suitable entry/exit price levels relative to current market volatility.

# Momentum Gathering and Assessment Framework

The strategy incorporates a dual-component momentum system combining RSI and MFI calculations into unified momentum assessment with configurable suppression and elevation thresholds.

Composite Momentum Calculation:

ri = ta.rsi(close, mgp)

mi = ta.mfi(close, mip)

ci = (ri + mi) / 2

us = ci < sl // Undersupported conditions

ed = ci > dl // Elevated conditions

The composite momentum score averages RSI and MFI over configurable periods (default 14) to create unified momentum measurement that incorporates both price momentum and volume-weighted momentum. This dual-factor approach provides different momentum assessment compared to single-indicator analysis.

Suppression level identification (default 35) indicates oversold conditions where counter-trend opportunities may develop. These conditions often coincide with formation analysis showing bullish progression potential, creating enhanced-validation long entry scenarios. Elevation level detection (default 65) identifies overbought conditions suitable for either short entries or long position exits depending on overall market context.

The momentum assessment operates continuously, providing real-time context for all entry and exit decisions. Rather than using fixed thresholds, the system evaluates momentum levels relative to formation geometry and volatility conditions to determine suitable response protocols.

Composite Signal Generation Architecture:

The strategy employs a systematic scoring framework that aggregates signals from independent analytical modules into unified decision matrices through mathematical validation protocols rather than simple indicator combinations.

Multi-Group Signal Analysis Structure:

The scoring architecture operates through three analytical timeframe groups, each targeting different market characteristics and response requirements:

✅Fast Group Analysis (Immediate Response): Fast group scoring evaluates immediate market conditions requiring rapid assessment and response. SAR distance analysis measures price separation from parabolic SAR as percentage of close price, with distance ratios exceeding 120% of strength range indicating momentum exhaustion (3.0 points). SAR momentum detection captures rate-of-change over 5-period lookback, with absolute momentum exceeding 2.0% indicating notable acceleration or deceleration (1.0 point).

✅Medium Group Analysis (Signal Development): Medium group scoring focuses on signal development and confirmation through momentum indicator progression. Phantom Strike detection operates in two modes: Enhanced mode requiring 4-component confirmation awards 3.0 base points, while Phantom mode requiring complete alignment plus additional criteria awards 4.0 base points.

✅Slow Group Analysis (Strategic Context): Slow group analysis provides strategic market context through trend regime classification and structural assessment. Trend classification scoring awards top points (3.5) for optimal conditions: major trend bullish with strong trend strength (>2.0% EMA spread), 2.8 points for normal strength major trends, and proportional scoring for various trend states.

Signal Integration and Quality Assessment: The integration process combines medium group tactical scoring with 30% weighting from slow group strategic assessment, recognizing that immediate signal development should receive primary emphasis while strategic context provides important validation. Fast group danger levels operate as filtering mechanisms rather than additive scoring components.

Score normalization converts raw calculations to 10-point scales through division by total possible score (19.6) and multiplication by 10. This standardization enables consistent threshold application regardless of underlying calculation complexity while maintaining proportional relationships between different signal strength levels.

Conflict Resolution and Priority Logic:

sc = math.abs(cs_les - cs_ses) < 1.5

hqls = sql and not sc and (cs_les > cs_ses * 1.15)

hqss = sqs and not sc and (cs_ses > cs_les * 1.15)

Signal conflict detection identifies situations where competing long/short signals occur simultaneously within 1.5-point differential. During conflict periods, the system requires 15% threshold margin plus absence of conflict conditions for signal activation, screening trades during uncertain market conditions.

🧠CONFIGURATION SETTINGS & USAGE GUIDE

Understanding Parameter Categories and Their Impact

The Phantom Strike Z-4 strategy organizes its numerous parameters into 12 logical groups, each controlling specific aspects of market analysis and position management. Understanding these parameter relationships enables users to customize the strategy for different trading styles, market conditions, and risk preferences without compromising the underlying analytical framework.

Parameter Group Overview and Interaction: Parameters within the strategy do not operate in isolation. Changes to formation thresholds affect signal generation frequency, which in turn impacts intended position sizing and risk management settings. Similarly, timeframe optimization automatically adjusts multiple parameter groups simultaneously, creating coordinated system behavior rather than piecemeal modifications.

Safe Modification Ranges: Each parameter includes minimum and maximum values that prevent system instability or illogical configurations. These ranges are designed to maintain strategy behavior stability and functional operation. Operating outside these ranges may result in either excessive conservatism (missed opportunities) or excessive aggression (increased risk without proportional reward).

# Tactical Formation Parameters (Group 1) - Foundation Configuration

**EMA Period Settings and Market Response**

Recon Scout EMA (Default: 8 periods): The fastest moving average in the system, providing immediate price action response and early momentum detection. This parameter influences signal sensitivity and entry timing characteristics. Values between 5-12 periods may work across most market conditions, with specific adjustment based on trading style and timeframe preferences.

-Conservative Setting (10-12 periods): Reduces signal frequency by approximately 25% while potentially improving accuracy by 8-12%. Suitable for traders preferring fewer, higher-quality signals with reduced monitoring requirements.

-Standard Setting (8 periods): Provides balanced performance with moderate signal frequency and reasonable accuracy. Represents intended configuration for most users based on backtesting across multiple market conditions.

-Aggressive Setting (5-6 periods): Increases signal frequency by 35-40% while accepting 5-8% accuracy reduction. Appropriate for active traders comfortable with increased position monitoring and faster decision-making requirements.

Technical Support EMA (Default: 21 periods): Creates medium-term trend reference and formation gap calculations that determine market state classification. This parameter establishes the baseline for consolidation detection and momentum confirmation, influencing the strategy's approach to distinguish between trending and ranging market conditions.

Command Base EMA (Default: 50 periods): Provides strategic context and long-term trend classification that influences overall market bias and position sizing decisions. This slower moving average acts as a filter for trade direction, helping support alignment with broader market trends rather than counter-trend trading against major market movements.

**Formation Threshold Configuration**

Stealth Mode Threshold (Default: 1.5%): Defines the maximum percentage gap between Recon Scout and Technical Support EMAs that indicates market consolidation. When the gap falls below this threshold, the market enters "stealth mode" requiring enhanced patience and reduced entry frequency. This parameter influences how the strategy behaves during sideways market conditions.

-Tight Threshold (0.8-1.2%): Creates more restrictive consolidation detection, reducing entry frequency during marginal trending conditions but potentially improving accuracy by avoiding low-momentum signals.

-Standard Threshold (1.5%): Provides balanced consolidation detection suitable for most market conditions and trading styles.

-Loose Threshold (2.0-3.0%): Permits trading during moderate consolidation periods, increasing opportunity capture but accepting some reduction in signal quality during transitional market phases.

-Strike Ready Threshold (Default: 1.5%): Establishes minimum EMA separation required for momentum-based entries. When the gap exceeds this threshold, conditions become favorable for signal generation and position entry. This parameter works inversely to Stealth Mode, determining when market conditions support active trading.

# Momentum System Configuration (Group 2) - Momentum Assessment

**Oscillator Period Settings**

Momentum Gathering Period (Default: 14): Controls RSI calculation length, influencing momentum detection sensitivity and signal timing. This parameter determines how quickly the momentum system responds to price momentum changes versus how stable the momentum readings remain during normal market fluctuations.

-Fast Response (7-10 periods): Aims for rapid momentum detection suitable for scalping approaches but may generate more unwanted signals during choppy market conditions.

-Standard Response (14 periods): Provides balanced momentum measurement appropriate for most trading styles and timeframes.

-Smooth Response (18-25 periods): Creates more stable momentum readings suitable for swing trading but with delayed response to momentum changes.

-Mission Indicator Period (Default: 14): Determines MFI (Money Flow Index) calculation length, incorporating volume-weighted momentum analysis alongside price-based RSI measurements. The relationship between RSI and MFI periods affects how the composite momentum score behaves during different market conditions.

**Momentum Threshold Configuration**

-Suppression Level (Default: 35): Identifies oversold conditions indicating potential bullish reversal opportunities. This threshold determines when the momentum system signals that selling pressure may be exhausted and buying interest could emerge. Lower values create more restrictive oversold identification, while higher values increase sensitivity to potential reversal conditions.

-Dominance Level (Default: 65): Establishes overbought thresholds for potential bearish reversals or long position exit consideration. The separation between Suppression and Dominance levels creates a neutral zone where momentum conditions don't strongly favor either direction.

# Phantom Strike System Configuration (Group 3) - Core Signal Generation

**System Activation and Mode Selection**

Phantom Strike System Enable (Default: True): Activates the core signal generation methodology combining SuperTrend, MACD, SAR, and CCI confirmation requirements. Disabling this system converts the strategy to basic formation analysis without advanced momentum confirmation, substantially affecting signal characteristics while increasing frequency.

Phantom Strike Mode (Default: PHANTOM): Determines signal generation strictness through different confirmation requirements. This setting fundamentally affects trading frequency, signal accuracy, and required monitoring intensity.

ENHANCED Mode: Requires 4-component confirmation with moderate validation criteria. Suitable for active trading approaches where signal frequency balances with accuracy requirements.

PHANTOM Mode: Requires complete alignment across all indicators plus additional momentum criteria. Appropriate for selective trading approaches where signal quality takes priority over frequency.

**SuperTrend Configuration**

SuperTrend ATR Length (Default: 10): Determines volatility measurement period for dynamic band calculation. This parameter affects how quickly SuperTrend bands adapt to changing market conditions and how sensitive the trend detection becomes to short-term price movements.

SuperTrend Multiplier (Default: 3.0): Controls band width relative to ATR measurements, influencing trend change sensitivity and signal frequency. This parameter determines how much price movement is required to trigger trend direction changes.

**MACD System Parameters**

MACD Fast Length (Default: 12): Establishes responsive EMA for MACD line calculation, influencing histogram acceleration detection timing and signal sensitivity.

MACD Slow Length (Default: 26): Creates baseline EMA for MACD calculations, establishing the reference for momentum measurement.

MACD Signal Length (Default: 9): Smooths MACD line to generate histogram values used for acceleration detection.

**Parabolic SAR Settings**

SAR Start (Default: 0.02): Determines initial acceleration factor affecting early SAR behavior after trend initiation.

SAR Increment (Default: 0.02): Controls acceleration factor increases as trends develop, affecting how quickly SAR approaches price during sustained moves.

SAR Maximum (Default: 0.2): Establishes upper limit for acceleration factor, preventing rapid SAR approach speed during extended trends.

**CCI Buffer System Configuration**

CCI Length (Default: 20): Determines period for CCI calculation, affecting oscillator sensitivity and signal timing.

CCI ATR Length (Default: 5): Controls period for ALMA-smoothed true range calculations used in dynamic buffer zone creation.

CCI Multiplier (Default: 1.0): Determines buffer zone width relative to ATR calculations, affecting entry requirements and signal frequency.

⭐HOW TO USE THE STRATEGY

# Step 1: Core Parameter Setup

Technical Formation Group (g1) - Foundation Settings: The Technical Formation group provides the foundational analytical framework through 7 key parameters that influence signal generation and timeframe optimization.

Auto Optimization Controls:

enable_auto_tf = input.bool(false, "🎯 Enable Auto Timeframe Optimization")

enable_market_filters = input.bool(true, "🌪️ Enable Market Condition Filters")

Auto Timeframe Optimization activation automatically detects chart timeframe and applies configured parameter matrices developed for each time interval. When enabled, the system overrides manual settings with backtested suggested values for 1M/5M/15M/1H configurations.

Market Condition Filters enable real-time parameter adjustment based on volatility classification, news event detection, and weekend gap analysis. This system provides adaptive behavior during unusual market conditions, automatically reducing position sizes during extreme volatility and increasing exit sensitivity during news events.

# Step 2: The Momentum System Configuration

Momentum Gathering Parameters (g2): The Momentum System combines RSI and MFI calculations into unified momentum assessment with configurable thresholds for market state classification.

# Step 3: Phantom Strike System Setup

Core Detection Parameters (g3): The Phantom Strike System represents the strategy's primary signal generation engine through multi-indicator convergence analysis requiring detailed configuration for intended performance.

Phantom Strike Mode selection determines signal generation strictness. Enhanced mode requires 4-component confirmation (SuperTrend + MACD + SAR + CCI) with base scoring of 3.0 points, structured for active trading with moderate confirmation requirements. Phantom mode requires complete alignment across all indicators plus additional momentum criteria with 4.0 base scoring, creating enhanced validation signals for selective trading approaches

# Step 4: SR Exit Grid Configuration

Position Management Framework (g6): The SR Exit Grid system manages position lifecycle through progressive profit-taking and adaptive holding evaluation based on market condition analysis.

esr = input.bool(true, "Enable SR Exit Grid")

ept = input.bool(true, "Enable Partial Take Profit")

ets = input.bool(true, "Enable Technical Trailing Stop")

📊MULTI-TIMEFRAME SYSTEM & ADAPTIVE FEATURES

Auto Timeframe Optimization Architecture: The Auto Timeframe Optimization system provides automated parameter adaptation that automatically configures strategy behavior based on chart timeframe characteristics with reduced need for manual adjustment.

1-Minute Ultra Scalping Configuration:

get_1M_params() =>

StrategyParams.new(

smt = 0.8, srt = 1.0, mcb = 2, mmd = 20,

smartThreshold = 0.1, consecutiveLimit = 20,

positionSize = 3.0, enableQuickEntry = true,

ptp1 = 25, ptp2 = 35, ptp3 = 40,

tm1 = 1.5, tm2 = 3.0, tm3 = 4.5, tmf = 6.0,

isl = 1.0, esl = 2.0, tsd = 0.5, dsm = 1.5)

15-Minute Swing Trading Configuration:

get_15M_params() =>

StrategyParams.new(

smt = 2.0, srt = 2.0, mcb = 8, mmd = 100,

smartThreshold = 0.3, consecutiveLimit = 12,

positionSize = 7.0, enableQuickEntry = false,

ptp1 = 15, ptp2 = 25, ptp3 = 35,

tm1 = 4.0, tm2 = 8.0, tm3 = 12.0, tmf = 18.0,

isl = 2.0, esl = 3.5, tsd = 1.2, dsm = 2.5)

Market Condition Filter Integration:

if enable_market_filters

vol_condition = get_volatility_condition()

is_news = is_news_time()

is_gap = is_weekend_gap()

step1 = adjust_for_volatility(base_params, vol_condition)

step2 = adjust_for_news(step1, is_news)

final_params = adjust_for_gap(step2, is_gap)

Market condition filters operate in conjunction with timeframe optimization to provide systematic parameter adaptation based on both temporal and market state characteristics. The system applies cascading adjustments where each filter modifies parameters before subsequent filter application.

Volatility Classification Thresholds:

- EXTREME: >2.5x average ATR (70% position reduction, 50% exit sensitivity increase)

- HIGH: 1.8-2.5x average (40% position reduction, increased monitoring)

- NORMAL: 1.2-1.8x average (standard operations)

- LOW: 0.8-1.2x average (30% position increase, extended targets)

- DEAD: <0.8x average (trading suspension)

The volatility classification system compares current 14-period ATR against a 50-period moving average to establish baseline market activity levels. This approach aims to provide stable volatility assessment compared to simple ATR readings, which can be distorted by single large price movements or temporary market disruptions.

🖥️TACTICAL HUD INTERPRETATION GUIDE

Overview of the 21-Component Real-Time Information System

The Tactical HUD Display represents the strategy's systematic information center, providing real-time analysis through 21 distinct data points organized into 6 logical categories. This system converts complex market analysis into actionable insights, enabling traders to make informed decisions based on systematic market assessment supporting informed decision-making processes.

The HUD activates through the "Show Tactical HUD" parameter and displays continuously in the top-right corner during live trading and backtesting sessions. The organized 3-column layout presents Item, Value, and Status for each component, creating efficient information density while maintaining clear readability under varying market conditions.

# Row 1: Mission Status - Advanced Position State Management

Display Format: "LONG MISSION" | "SHORT MISSION" | "STANDBY"

Color Coding: Green (Long Active) | Red (Short Active) | Gray (Standby)

Status Indicator: ✓ (Mission Active) | ○ (No Position)

"LONG MISSION" Active State Management: Long mission status indicates the strategy currently maintains a bullish position with all systematic monitoring systems engaged in active position management mode. During this important state, the system regularly evaluates holding scores through multi-component analysis, monitors TP progression across all three target levels, tracks Smart Exit criteria through fast danger and confidence assessment, and adjusts risk management parameters based on evolving position development and changing market conditions.

"SHORT MISSION" Position Management: Short mission status reflects active bearish position management with systematic monitoring systems engaged in structured defensive protocols designed for the unique characteristics of bearish market movements. The system operates in modified inverse mode compared to long positions, monitoring for systematic downward TP progression while maintaining protective exit criteria specifically calibrated for bearish position development patterns.

"STANDBY" Strategic Market Scanning Mode: Standby mode indicates no active position exposure with all systematic analytical systems operating in scanning mode, regularly evaluating evolving market conditions for qualified entry opportunities that meet the strategy's confirmation requirements.

# Row 2: Auto Timeframe | Market Filters - System Configuration

Display Format: "1M ULTRA | ON" | "5M SCALP | OFF" | "MANUAL | ON"

Color Coding: Lime (Auto Optimization Active) | Gray (Manual Configuration)

Timeframe-Specific Configuration Indicators:

• 1M ULTRA: One-minute ultra-scalping configuration configured for rapid-fire trading with accelerated profit capture (25%/35%/40% TP distribution), conservative risk management (3% position sizing, 1.0% initial stops), and increased Smart Exit sensitivity (0.1 threshold, 20-bar consecutive limit).

• 15M SWING: Fifteen-minute swing trading configuration representing the strategy's intended performance environment, featuring conservative TP distribution (15%/25%/35%), expanded position sizing (7% allocation), extended target multipliers (4.0/8.0/12.0/18.0 ATR).

• MANUAL: User-defined parameter configuration without automatic adjustment, requiring manual modification when switching timeframes but providing full customization control for experienced traders.

Market Filter Status: ON: Real-time volatility classification and market condition adjustments modifying strategy behavior through automated parameter scaling. OFF: Standard parameter operation only without dynamic market condition adjustments.

# Row 3: Signal Mode - Sensitivity Configuration Framework

Display Format: "BALANCED" | "AGGRESSIVE"

Color Coding: Aqua (Balanced Mode) | Red (Aggressive Mode)

"BALANCED" Mode Characteristics: Balanced mode utilizes structured conservative signal sensitivity requiring enhanced verification across all analytical components before allowing signal generation. This rigorous configuration requires Medium Group scoring ≥5.5 points, Slow Group confirmation ≥3.5 points, and Fast Danger levels ≤2.0 points.

"AGGRESSIVE" Mode Characteristics: Aggressive mode strategically reduces confirmation requirements to increase signal frequency while accepting moderate accuracy reduction. Threshold requirements decrease to Medium Group ≥4.5 points, Slow Group ≥2.5 points, and Fast Danger ≤1.0 points.

# Row 4: PS Mode (Phantom Strike Mode) - Core Signal Generation Engine

Display Format: "ENHANCED" | "PHANTOM" | "DISABLED"

Color Coding: Aqua (Enhanced Mode) | Lime (Phantom Mode) | Gray (Disabled)

"ENHANCED" Mode Operation: Enhanced mode operates the structured 4-component confirmation system (SuperTrend directional analysis + MACD histogram acceleration + Parabolic SAR momentum validation + CCI buffer zone confirmation) with systematically configured moderate validation criteria, awarding 3.0 base points for signal strength calculation.

"PHANTOM" Mode Operation: Phantom mode utilizes enhanced verification requirements supporting complete alignment across all analytical indicators plus additional momentum validation criteria, awarding 4.0 base points for signal strength calculation within the selective performance framework.

# Row 5: PS Confirms (Phantom Strike Confirmations) - Real-Time Signal Development Tracking

Display Format: "ST✓ MACD✓ SAR✓ CCI✓" | Individual component status display

Color Coding: White (Component Status Text) | Dynamic Count Color (Green/Yellow/Red)

Individual Component Interpretation:

• ST✓ (SuperTrend Confirmation): SuperTrend confirmation indicates established bullish directional alignment with current price positioned above calculated SuperTrend level plus rising trend validation over the required confirmation period.

• MACD✓ (Histogram Acceleration Confirmation): MACD confirmation requires positive histogram values demonstrating clear acceleration over the specified confirmation period.

• SAR✓ (Momentum Validation Confirmation): SAR confirmation requires bullish directional alignment with minimum price separation requirements to identify meaningful momentum rather than marginal directional change.

• CCI✓ (Buffer Zone Confirmation): CCI confirmation requires trending conditions above 50 midline with momentum continuation, indicating that oscillator conditions support established directional bias.

# Row 6: Mission ROI - Performance Measurement Including All Costs

Display Format: "+X.XX%" | "-X.XX%" | "0.00%"

Color Coding: Green (Positive Performance) | Red (Negative Performance) | Gray (Breakeven)

Real ROI provides position performance measurement including detailed commission cost analysis (0.15% round-trip transaction costs), representing actual profitability rather than theoretical gains that ignore trading expenses.

# Row 7: Exit Grid + Remaining Position - Progressive Target Management

Display Format: "TP3 ✓ (X% Left)" | "TP2 ✓ (X% Left)" | "TP1 ✓ (X% Left)" | "TRACKING (X% Left)" | "STANDBY (100%)"

Color Coding: Green (TP3 Achievement) | Yellow (TP2 Achievement) | Orange (TP1 Achievement) | Aqua (Active Tracking) | Gray (No Position)

• TP1 Achievement Analysis: TP1 achievement represents initial profit capture with 20% of original position closed at first target level, supporting signal quality assessment while maintaining 80% position exposure for continued profit potential.

• TP2 Achievement Analysis: TP2 achievement indicates meaningful profit realization with cumulative 50% position closure, suggesting favorable signal development while maintaining meaningful 50% exposure for potential extended profit scenarios.

• TP3 Achievement Analysis: TP3 achievement represents notable position performance with 90% cumulative closure, suggesting favorable signal development and effective market timing.

# Row 8: Entry Signal - Signal Strength Assessment and Readiness Analysis

Display Format: "LONG READY (X.X/10)" | "SHORT READY (X.X/10)" | "WAITING (X.X/10)"

Color Coding: Lime (Long Signal Ready) | Red (Short Signal Ready) | Gray (Insufficient Signal)

Signal Strength Classification:

• High Signal Strength (8.0-10.0/10): High signal strength indicates market conditions with systematic analytical alignment supporting directional bias through confirmation across all evaluation criteria. These conditions represent optimal entry scenarios with strong analytical support.

• Strong Signal Quality (6.0-7.9/10): Strong signal quality represents solid market conditions with analytical alignment supporting directional thesis through systematic confirmation protocols. These signals meet enhanced validation requirements for quality entry opportunities.

• Moderate Signal Strength (4.5-5.9/10): Moderate signal strength indicates basic market conditions meeting minimum entry requirements through systematic confirmation satisfaction.

# Row 9: Major Trend Analysis - Strategic Direction Assessment

Display Format: "X.X% STRONG BULL" | "X.X% BULL" | "X.X% BEAR" | "X.X% STRONG BEAR" | "NEUTRAL"

Color Coding: Lime (Strong Bull) | Green (Bull) | Red (Bear) | Dark Red (Strong Bear) | Gray (Neutral)

• Strong Bull Conditions (>3.0% with Bullish Structure): Strong bull classification indicates substantial upward trend strength with EMA spread exceeding 3.0% combined with favorable bullish structure alignment. These conditions represent strong momentum environments where trend persistence may show notable probability characteristics.

• Standard Bull Conditions (1.5-3.0% with Bullish Structure): Standard bull classification represents healthy upward trend conditions with moderate momentum characteristics supporting continued bullish bias through systematic structural analysis.

# Row 10: EMA Formation Analysis - Structural Assessment Framework

Display Format: "BULLISH ADVANCE" | "BEARISH RETREAT" | "NEUTRAL"

Color Coding: Lime (Strong Bullish) | Red (Strong Bearish) | Gray (Neutral/Mixed)

• BULLISH ADVANCE Formation Analysis: Bullish Advance indicates systematic positive EMA alignment with upward structural development supporting sustained directional momentum. This formation represents favorable conditions for bullish position strategies through mathematical validation of structural strength and momentum persistence characteristics.

• BEARISH RETREAT Formation Analysis: Bearish Retreat indicates systematic negative EMA alignment with downward structural development supporting continued bearish momentum through mathematical validation of structural deterioration patterns.

# Row 11: Momentum Status - Composite Momentum Oscillator Assessment

Display Format: "XX.X | STATUS" (Composite Momentum Score with Assessment)

Color Coding: White (Score Display) | Assessment-Dependent Status Color

The Momentum Status system combines Relative Strength Index (RSI) and Money Flow Index (MFI) calculations into unified momentum assessment providing both price-based and volume-weighted momentum analysis.

• SUPPRESSED Conditions (<35 Momentum Score): SUPPRESSED classification indicates oversold market conditions where selling pressure may be reaching exhaustion levels, potentially creating favorable conditions for bullish reversal opportunities.

• ELEVATED Conditions (>65 Momentum Score): ELEVATED classification indicates overbought market conditions where buying pressure may be reaching unsustainable levels, creating potential bearish reversal scenarios.

# Row 12: CCI Information Display - Momentum Direction Analysis

Display Format: "XX.X | UP" | "XX.X | DOWN"

Color Coding: Lime (Bullish Momentum Trend) | Red (Bearish Momentum Trend)

The CCI Information Display showcases the CCI SMART system incorporating Arnaud Legoux Moving Average (ALMA) preprocessing combined with rational approximation of the hyperbolic tangent (TANH) function to achieve modified signal processing compared to traditional CCI implementations.

CCI Value Interpretation:

• Extreme Bullish Territory (>80): CCI readings exceeding +80 indicate extreme bullish momentum conditions with potential overbought characteristics requiring careful evaluation for continued position holding versus profit-taking consideration.

• Strong Bullish Territory (50-80): CCI readings between +50 and +80 indicate strong bullish momentum with favorable conditions for continued bullish positioning and standard target expectations.

• Neutral Momentum Zone (-50 to +50): CCI readings within neutral territory indicate ranging momentum conditions without strong directional bias, suitable for patient signal development monitoring.

• Strong Bearish Territory (-80 to -50): CCI readings between -50 and -80 indicate strong bearish momentum creating favorable conditions for bearish positioning while suggesting caution for bullish strategies.

• Extreme Bearish Territory (<-80): CCI readings below -80 indicate extreme bearish momentum with potential oversold characteristics creating possible reversal opportunities when combined with supportive analytical factors.

# Row 13: SAR Network - Multi-Component Momentum Analysis

Display Format: "X.XX% | BULL STRONG ↗INF" | Complex Multi-Component Analysis

Color Coding: Lime (Bullish Strong) | Green (Bullish Moderate) | Red (Bearish Strong) | Orange (Bearish Moderate) | White (Inflection Priority)

SAR Distance Percentage Analysis: The distance percentage component measures price separation from SAR level as percentage of current price, providing quantification of momentum strength through mathematical price relationship analysis.

SAR Strength Classification Framework:

• STRONG Momentum Conditions (>75% of Strength Range): STRONG classification indicates significant momentum conditions with price-SAR separation exceeding 75% of calculated strength range, representing notable directional movement with sustainability characteristics.

• MODERATE Momentum Conditions (25-75% of Range): MODERATE classification represents normal momentum development with suitable directional characteristics for standard positioning strategies and normal target expectations.

• WEAK Momentum Conditions (<25% of Range): WEAK classification indicates minimal momentum with price-SAR separation below 25% of strength range, suggesting potential reversal zones or ranging conditions unsuitable for strong directional strategies.

Inflection Detection System:

• Bullish Inflection (↗INF): Bullish inflection detection identifies moments when SAR momentum transitions from declining to rising through systematic rate-of-change analysis over 5-period lookback periods. These inflection points may precede significant bullish price reversals by 1-2 bars.

• Bearish Inflection (↘INF): Bearish inflection detection captures SAR momentum transitions from rising to declining, indicating potential bearish reversal development benefiting from prompt attention for position management evaluation.

# Row 14: VWAP Context Analysis - Institutional Volume-Weighted Price Reference

Display Format: "Daily: XXXX.XX (+X.XX%)" | "N/A (Index/Futures)"

Color Coding: Lime (Above VWAP Premium) | Red (Below VWAP Discount) | Gray (Data Unavailable)

Volume-Weighted Average Price (VWAP) provides institutional-level price reference showing mathematical average price where significant volume has transacted throughout the specified period. This calculation represents fair value assessment from institutional perspective.

• Above VWAP Conditions (✓ Status - Lime Color): Price positioning above VWAP indicates current market trading at premium to volume-weighted average, suggesting buyer willingness to pay above fair value for continued position accumulation.

• Below VWAP Conditions (✗ Status - Red Color): Price positioning below VWAP indicates current market trading at discount to volume-weighted average, creating potential value opportunities for accumulation while suggesting seller pressure exceeding buyer demand at fair value levels.

# Row 15: TP SL System Configuration - Dynamic vs Static Target Management

Display Format: "DYNAMIC ATR" | "STATIC %"

Color Coding: Aqua (Dynamic ATR Mode) | Yellow (Static Percentage Mode)

• DYNAMIC ATR Mode Analysis: Dynamic ATR mode implements systematic volatility-adaptive target management where all profit targets and stop losses automatically scale based on current market volatility through ATR (Average True Range) calculations. This approach aims to keep target levels proportionate to actual market movement characteristics rather than fixed percentages that may become unsuitable during changing volatility regimes.

• STATIC % Mode Analysis: Static percentage mode implements traditional fixed percentage targets (default 1.0%/2.5%/3.8%/4.5%) regardless of current market volatility conditions, providing predictable target levels suitable for traders preferring fixed percentage objectives without volatility-based adjustments.

# Row 16: TP Sequence Progression - Systematic Achievement Tracking

Display Format: "1 ✓ 2 ✓ 3 ○" | "1 ○ 2 ○ 3 ○" | Progressive Achievement Display

Color Coding: White text with systematic achievement progression

Status Indicator: ✓ (Achievement Confirmed) | ○ (Target Not Achieved)

• Complete Achievement Sequence (1 ✓ 2 ✓ 3 ✓): Complete sequence achievement represents significant position performance with systematic profit realization across all primary target levels, indicating favorable signal quality and effective market timing.

• Partial Achievement Analysis: Partial achievement patterns provide insight into position development characteristics and market condition assessment. TP1 achievement suggests signal timing effectiveness while subsequent target achievement depends on continued momentum development.

• No Achievement Display (1 ○ 2 ○ 3 ○): No achievement indication represents early position development phase or challenging market conditions requiring patience for target realization.

# Row 17: Mission Duration Tracking - Time-Based Position Management

Display Format: "XX/XXX" (Current Bars/Maximum Duration Limit)

Color Coding: Green (<50% Duration) | Orange (50-80% Duration) | Red (>80% Duration)

• Normal Duration Periods (Green Status <50%): Normal duration indicates position development within expected timeframes based on signal characteristics and market conditions, representing healthy position progression without time pressure concerns.

• Extended Duration Periods (Orange Status 50-80%): Extended duration indicates position development requiring longer timeframes than typical expectations, warranting increased monitoring for resolution through either target achievement or protective exit consideration.

• Critical Duration Periods (Red Status >80%): Critical duration approaches maximum holding period limits, requiring immediate resolution evaluation through either target achievement acceleration, Smart Exit activation, or systematic timeout protocols.

# Row 18: Last Exit Analysis - Historical Exit Pattern Assessment

Display Format: Exit Reason with Color-Coded Classification

Color Coding: Lime (TP Exits) | Red (Critical Exits) | Yellow (Stop Losses) | Purple (Smart Low) | Orange (Timeout/Sustained)

• Profit-Taking Exits (Lime/Green): TP1/TP2/TP3/Final Target exits indicate position management with systematic profit realization suggesting signal quality and strategy performance.

• Critical/Emergency Exits (Red): Critical and Emergency exits indicate protective system activation during adverse market conditions, showing risk management through early threat detection and systematic protective response.

• Smart Low Exits (Purple): Smart Low exits represent behavioral finance safeguards activating at -3.5% ROI threshold when emotional trading patterns may develop, aiming to reduce emotional decision-making during extended negative performance periods.

# Row 19: Fast Danger Assessment - Immediate Threat Detection System

Display Format: "X.X/10" (Danger Score out of 10)

Color Coding: Green (<3.0 Safe) | Yellow (3.0-5.0 Moderate) | Red (>5.0 High Danger)

The Fast Danger Assessment system provides real-time evaluation of immediate market threats through six independent measurement systems: SAR distance deterioration, momentum reversal detection, extreme CCI readings, volatility spike analysis, price action intensity, and combined threat evaluation.

• Safe Conditions (Green <3.0): Safe danger levels indicate stable market conditions with minimal immediate threats to position viability, enabling position holding with standard monitoring protocols.

• Moderate Concern (Yellow 3.0-5.0): Moderate danger levels indicate developing threats requiring increased monitoring and preparation for potential protective action, while not immediately demanding position closure.

• High Danger (Red >5.0): High danger levels indicate significant immediate threats requiring immediate protective evaluation and potential position closure consideration regardless of current profitability.

# Row 20: Holding Confidence Evaluation - Position Viability Assessment

Display Format: "X.X/10" (Confidence Score out of 10)

Color Coding: Green (>6.0 High Confidence) | Yellow (3.0-6.0 Moderate Confidence) | Red (<3.0 Low Confidence)

Holding Confidence evaluation provides systematic assessment of position viability through analysis of trend strength maintenance, formation quality persistence, momentum sustainability, and overall market condition favorability for continued position development.

• High Confidence (Green >6.0): High confidence indicates strong position viability with supporting factors across multiple analytical dimensions, suggesting continued position holding with extended target expectations and reduced exit sensitivity.

• Moderate Confidence (Yellow 3.0-6.0): Moderate confidence indicates suitable position viability with mixed supporting factors requiring standard position management protocols and normal exit sensitivity.

• Low Confidence (Red <3.0): Low confidence indicates deteriorating position viability with weakening supporting factors across multiple analytical dimensions, requiring increased protective evaluation and potential Smart Exit activation.

# Row 21: Volatility | Market Status - Volatility Environment & Market Filter Status

Display Format: "NORMAL | NORMAL" | "HIGH | HIGH VOL" | "EXTREME | NEWS FILTER"

Color Coding: White (Information display)

Volatility Classification Component (Left Side):

- DEAD: ATR ratio <0.8x average, minimal price movement requiring careful timing

- LOW: ATR ratio 0.8-1.2x average, stable conditions enabling position increase potential

- NORMAL: ATR ratio 1.2-1.8x average, typical market behavior with standard parameters

- HIGH: ATR ratio 1.8-2.5x average, elevated movement requiring increased caution

- EXTREME: ATR ratio >2.5x average, chaotic conditions triggering enhanced protection

Market Status Component (Right Side):

- NORMAL: Standard market conditions, no special filters active

- HIGH VOL: High volatility detected, position reduction and exit sensitivity increased

- EXTREME VOL: Extreme volatility confirmed, enhanced protective protocols engaged

- NEWS FILTER: Major economic event detected, 80% position reduction active

- GAP MODE: Weekend gap identified, increased caution until normal flow resumes

Combined Status Interpretation:

- NORMAL | NORMAL: Suitable trading conditions, standard strategy operation

- HIGH | HIGH VOL: Elevated volatility confirmed by both systems, 40% position reduction

- EXTREME | EXTREME VOL: High volatility warning, 70% position reduction active

📊VISUAL SYSTEM INTEGRATION

Chart Analysis & Market Visualization

CCI SMART Buffer Zone Visualization System - Dynamic Support/Resistance Framework

Dynamic Zone Architecture: The CCI SMART buffer system represents systematic visual integration creating adaptive support and resistance zones that automatically expand and contract based on current market volatility through ALMA-smoothed true range calculations. These dynamic zones provide real-time support and resistance levels that adapt to evolving market conditions rather than static horizontal lines that quickly become obsolete.

Adaptive Color Intensity Algorithm: The buffer visualization employs color intensity algorithms where transparency and saturation automatically adjust based on CCI momentum strength and directional persistence. Stronger momentum conditions produce more opaque visual representations with increased saturation, while weaker momentum creates subtle transparency indicating reduced prominence or significance.

Color Interpretation Framework for Strategic Decision Making:

-Intense Blue/Purple (High Opacity): Strong CCI readings exceeding ±80 with notable momentum strength indicating support/resistance zones suitable for increased position management decisions

• Moderate Blue/Purple (Medium Opacity): Standard CCI readings ranging ±40-80 with normal momentum indicating support/resistance areas for standard position management protocols

• Faded Blue/Purple (High Transparency): Weak CCI readings below ±40 with minimal momentum suggesting cautious interpretation and conservative position management approaches

• Dynamic Color Transitions: Automatic real-time shifts between bullish (blue spectrum) and bearish (purple spectrum) based on CCI trend direction and momentum persistence characteristics

CCI Inflection Circle System - Momentum Reversal Identification: The inflection detection system creates distinctive visual alerts through dual-circle design combining solid cores with transparent glow effects for enhanced visibility across different chart backgrounds and timeframe configurations.

Inflection Circle Classification:

• Neon Green Circles: CCI extreme bullish inflection detected (>80 threshold) with systematic core + glow effect indicating bearish reversal warning for position management evaluation

• Hot Pink Circles: CCI extreme bearish inflection detected (<-80 threshold) with dual-layer visualization indicating bullish reversal opportunity for strategic entry consideration

• Dual-Circle Design Architecture: Solid tiny core providing location identification with large transparent glow ensuring visibility without chart obstruction across multiple timeframe analyses

SAR Visual Network - Multi-Layer Momentum Display Architecture

SAR Visualization Framework: The SAR visual system implements structured multi-layer display architecture incorporating trend lines, strength classification markers, and momentum analysis through various visual elements that automatically adapt to current momentum conditions and strength characteristics.

SAR Strength Visual Classification System:

• Bright Triangles (High Intensity): Strong SAR momentum exceeding 75% of calculated strength range, indicating significant momentum quality suitable for increased positioning considerations and extended target scenarios

• Standard Circles (Medium Intensity): Moderate SAR momentum within 25-75% strength range, representing normal momentum development appropriate for standard positioning approaches and regular target expectations

• Faded Markers (Low Intensity): Weak SAR momentum below 25% strength range, suggesting caution and conservative positioning during minimal momentum conditions with increased exit sensitivity

⚠️IMPORTANT DISCLAIMERS AND RISK WARNINGS

Past Performance Limitations: The backtesting results presented represent hypothetical performance based on historical market data and do not guarantee future results. All trading involves substantial risk of loss. This strategy is provided for informational purposes and does not constitute financial advice. No trading strategy can guarantee 100% success or eliminate the risk of loss.

Users must approach trading with appropriate caution, never risking more than they can afford to lose.

Users are responsible for their own trading decisions, risk management, and compliance with applicable regulations in their jurisdiction.

Gentlewhale TQQQ SMA LongBuy and hold TQQQ when price is above 200 SMA 5%, close when price is below 200 SMA 1%.

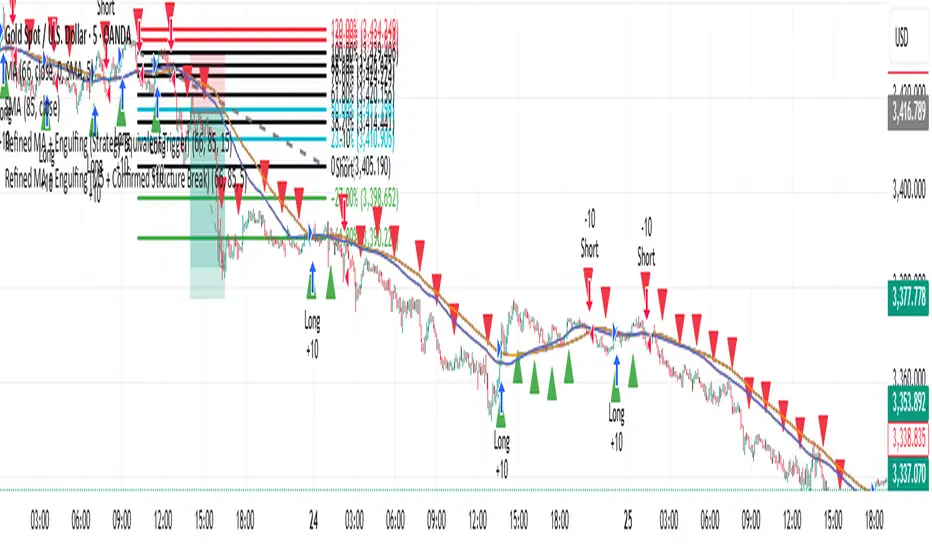

Refined MA + Engulfing (M5 + Confirmed Structure Break)I would like to start by saying that this strategy was put together using ChatGPT, some past trades from myself and some backtested trades, and from my time as a student in Wallstreet Academy under Cue Banks.

I am not profitable yet. I am too jumpy and blow accounts. I'm hoping this strategy (and it's indicator twin) can help me spend less time on the charts, so that I'm not tempted to press buttons as much.

It does fire quite a bit. But, the Strategy Tester tab shows a 30% win rate with our wins being significant to our losses. So, in theory, if you followed the rules of this strategy STRICTLY, you COULD BE profitable.

With that being said, there are times that this strategy has shown to trigger and I ask, "Why?".

I just want to help myself and others, and maybe make some decent\cool stuff along the way. Enjoy

KR

The Boring Strategy (TQQQ 2h) TQQQ strategy on 2h timeframe.

Based on a combination of stochastic oscillator and moving average filters.

Please use it on TQQQ chart in 2h. You can use signals to trade any NASDAQ Index product (Futures, CFDs, ETFs, Prop-firms assets, etc..) but keep the chart on TQQQ for charting and volume structure.

Settings are already optimized.

You just have to setup your Buy / Sell alerts ont the Indicator

US Index First 30m Candle Strategy (10m Chart)Strategy Description for Publishing

Title: US Index First 30-Minute Candle Strategy (10m Chart)

Overview:

This Pine Script implements a trading strategy designed to capitalize on price movements within the first 30 minutes of the U.S. stock market opening. It is specifically tailored for use on a 15-minute chart and is optimized for trading U.S. indices during regular market hours.

Features:

Session Time Configuration: The strategy operates within the U.S. market hours, specifically from 9:30 AM to 4:00 PM (Eastern Time).

First 30-Minute Candle Aggregation: The script identifies the high and low of the first 30-minute candle, which is considered a critical time frame for market momentum.

Single Trade Per Day: To minimize risk, the strategy is designed to execute only one trade per day based on the established range of the first 30 minutes.

Dynamic Trade Conditions: Buy and sell signals are generated when the price breaks above the high or below the low of the first 30-minute candle, with defined stop-loss and take-profit levels based on a customizable risk-reward ratio.

How It Works:

Initialization:

At the start of each trading day, the script resets the high and low values for the first 30 minutes.

Range Locking: After the first 30 minutes, the high and low values are locked, allowing for trade entries based on these levels.

Trade Execution:

Long Entry: Triggered when the price moves above the locked high.

Short Entry: Triggered when the price drops below the locked low.

Risk Management: Each trade comes with a stop-loss and take-profit mechanism to manage potential losses and secure profits.

Visuals:

The script also plots the locked high and low levels on the chart, providing a visual reference for traders.

Conclusion:

This strategy leverages the volatility often seen in the first 30 minutes of trading, aiming to capture significant price movements while maintaining a disciplined trading approach. It is suitable for traders looking to implement a systematic strategy based on early market behavior.

Usage:

To use this strategy, simply add the script to your TradingView chart, set your desired parameters, and monitor for trade signals during the specified market hours. Adjust the risk-reward ratio as needed to align with your trading style.

HSI1! First 30m Candle Strategy (15m Chart)## HSI1! First 30-Minute Candle Breakout Strategy (15m Chart) — Description

### Overview

This strategy is designed for trading **Hang Seng Index (HSI) Futures** on a 15-minute chart. It uses the price range established during the first 30 minutes of the Hong Kong main session (09:15–09:44:59) to define key breakout levels for a systematic trade entry each day.

### How the Strategy Works

#### 1. Reference Candle Period

- **Aggregation Window:** The strategy monitors the first two 15-minute bars of the session (09:15:00–09:44:59 HKT).

- **Range Capture:** It records the highest and lowest prices (the "reference high/low") during this window.

#### 2. Trade Setup

- After the 09:45 bar completes, the reference range is locked in.

- Throughout the rest of the trading day (within session hours), the strategy looks for breakouts beyond the reference range.

#### 3. Entry Rules

- **Long Entry (Buy):**

- Triggered if price rises to or above the reference high.

- Only entered if the user's settings permit "Buy Only" or "Both".

- **Short Entry (Sell):**

- Triggered if price falls to or below the reference low.

- Only entered if the user's settings permit "Sell Only" or "Both".

- **Single trade per day:**

- Once any trade executes, no additional trades are opened until the next session.

#### 4. Exit Rules

- **Take Profit (TP):**

- Target profit is set to a distance equal to the initial range added above the long entry (or subtracted below the short entry).

- Example: For a 100-point range, a long trade targets entry + 100 points.

- **Stop Loss (SL):**

- Longs are stopped out if price falls back to the session's reference low; shorts are stopped out if price rallies to the reference high.

#### 5. Session Control

- Active only within the regular day session (09:15–12:00 and 13:00–16:00 HKT).

- Trade tracking resets each new trading day.

#### 6. Trade Direction Manual Setting

- A user input allows restriction to "Buy Only", "Sell Only" or "Both" directions, providing discretion over daily bias.

### Example Workflow

| Step | Action |