Advanced Confluence DashboardAdvanced Confluence Dashboard - Multi-Indicator Technical Analysis Tool

OVERVIEW

The Advanced Confluence Dashboard is a comprehensive technical analysis tool designed to help traders identify high-probability trade setups by tracking multiple technical indicators simultaneously. The indicator displays up to 13 different technical confluences in an easy-to-read dashboard format, providing both individual signals and an overall market bias percentage. Switch between full table view and condensed view for maximum chart flexibility.

FEATURES

- 13 Technical Confluences: RSI, VWAP, EMA Cross (9/21), MACD, Stochastic, Trend (50 EMA), Bollinger Bands, ADX Strength, Price Momentum, Volume Breakout, VWAP Bands, 200 EMA, and Price Action (Higher Highs/Lower Lows)

- Real-time Confluence Scoring: Automatically calculates bullish vs bearish signal strength

- Multi-Timeframe Support: Analyze indicators on any timeframe while viewing your chart on another

- Customizable Display: Toggle individual indicators on/off, adjust table position, size, and transparency

- ATR Information: Optional ATR display for volatility-based position sizing

- Condensed View Mode: Ultra-minimal display showing only confluence score and ATR (perfect for scalpers who want maximum chart visibility)

- Full Table View: Detailed breakdown of each indicator's value and signal

- Color-Coded Signals: Green (bullish), red (bearish), white (neutral) for instant visual clarity

HOW IT WORKS

The indicator evaluates each enabled technical indicator and assigns it either a bullish or bearish signal based on its current state. The confluence score shows how many indicators are aligned in each direction, giving you a clear percentage-based view of market bias. For example, if 8 out of 13 indicators are bullish, you'll see a 62% LONG BIAS signal.

DISPLAY MODES

Full View: Shows all enabled indicators with their current values and signals in a detailed table format. Perfect for understanding exactly which indicators are bullish or bearish and why.

Condensed View: Shows only the confluence score (e.g., "4/13 LONG | 9/13 SHORT - SHORT BIAS 69%") and optional ATR information. This minimal display keeps your chart clean while still providing the essential confluence data you need for quick trading decisions. Ideal for scalpers and traders who want maximum chart space.

CONFLUENCES EXPLAINED

- RSI: Momentum oscillator (>50 bullish, <50 bearish, shows overbought/oversold)

- VWAP: Volume-weighted average price (above = bullish, below = bearish)

- EMA Cross: Fast EMA (9) vs Slow EMA (21) with price position

- MACD: Trend-following momentum (line above signal = bullish)

- Stochastic: Momentum oscillator (>50 bullish, <50 bearish)

- Trend (50 EMA): Price position relative to 50-period EMA

- Bollinger Bands: Volatility and mean reversion (above middle = bullish)

- ADX Strength: Trend strength indicator (shows strong trends)

- Price Momentum: Rate of price change over specified period

- Volume Breakout: Detects unusual volume with directional bias

- VWAP Bands: Standard deviation bands around VWAP

- 200 EMA: Long-term trend indicator

- Price Action: Higher Highs and Lower Lows pattern detection

SETTINGS

Timeframe Settings:

- Indicator Timeframe: Analyze indicators on a different timeframe than your chart

Display Options:

- Condensed View: Toggle between full table and minimal display

- Show ATR Info: Display/hide ATR information

- Table Position: 9 positions (top/middle/bottom + left/center/right)

- Text Size: Auto, tiny, small, normal, large, huge

- Table Transparency: 0-100%

- Border Width: 1-5 pixels

Confluence Toggles:

- Enable/disable any of the 13 confluences individually

- Confluence score automatically adjusts based on enabled indicators

Indicator Settings:

- RSI Length (default: 14)

- ATR Length (default: 14)

- Fast/Slow EMA (default: 9/21)

- Trend EMA (default: 50)

- Volume SMA Length (default: 20)

- Volume Breakout Multiplier (default: 2.0x)

- Bollinger Bands Length/StdDev (default: 20/2.0)

- ADX Length (default: 14)

- ADX Strength Threshold (default: 25)

- Momentum Length (default: 10)

IDEAL USE CASES

- Scalping: Quick identification of confluence for fast entries/exits - use condensed view for clean charts

- Day Trading: Multi-timeframe analysis for intraday setups

- Swing Trading: Confirmation of longer-term bias

- Risk Management: Higher confluence = higher probability trades

- Trade Filtering: Only take trades when confluence reaches your threshold

- Multi-Monitor Setups: Use condensed view on execution charts, full view on analysis charts

HOW TO USE

1. Add the indicator to your chart

2. Toggle on/off the confluences you prefer to use

3. Choose between Full View (detailed) or Condensed View (minimal)

4. Adjust the table position and size to your preference

5. Look for high confluence percentages (70%+ is strong bias)

6. Use the individual indicator signals (full view) to understand market structure

7. Combine with your trading strategy for entry/exit confirmation

TIPS

- Use Condensed View when scalping to keep your chart clean and uncluttered

- Switch to Full View when you need to analyze which specific indicators are conflicting

- Higher confluence doesn't guarantee success - always use proper risk management

- Consider using 60%+ confluence as a minimum threshold for trades

- Pay attention to which specific indicators are aligned vs conflicting

- Use the ATR display for quick reference on position sizing

- Experiment with different timeframes to find what works for your style

- Disable indicators you don't use to simplify your confluence scoring

DISCLAIMER

This indicator is for educational and informational purposes only. It does not constitute financial advice, investment advice, trading advice, or any other type of advice. Trading and investing in financial markets involves substantial risk of loss and is not suitable for every investor. Past performance is not indicative of future results. Always do your own research and consult with a qualified financial advisor before making any investment decisions.

QQQ

QQQ Quant Power STRATEGY v13.3 (Ribbon + TQQQ Specs)1. The Quant Engine (Data Processing)

Weighted Scoring: It assigns specific weights to stocks (e.g., NVDA gets 8.5% weight, TXN gets 1.0%).

Z-Score Pressure: It calculates how "unusual" the current buying/selling pressure is compared to the average (Standard Deviation).

Alignment Bonus: It boosts the "Conviction Score" if Mega Caps (Top 8) and Large Caps (Next 12) are moving in the same direction.

2. The Dashboard (Mission Control)

The dashboard gives you an X-Ray view of the market:

Main Status: Tells you if the market is BULLISH, BEARISH, or CHOP (Sit Out).

Conviction %: A probability score (0-99%). Higher = Safer trade.

Breadth: Counts how many of the top 20 stocks are above their EMA.

Chop Logic: If Breadth is mixed (between 6 and 14 stocks above EMA), it declares "CHOP" and blocks trades.

Mega/Large Net: Shows the net buying/selling pressure for each group.

3. Visuals

Pressure Line: The line on the chart isn't just a Moving Average; it's the Net Pressure of the 20 stocks pushing price up or down.

Conviction Ribbon: The squares at the bottom of the screen.

🟩 Green: High Probability Long (>77%).

🟥 Red: High Probability Short (>77%).

⬜ Gray: Low Conviction / Holding.

4. Strategy Logic (Automated Trading)

Entry: Enters when the "Basket" of stocks is aligned (Bull/Bear Pressure) AND the Conviction Score is high (>77%).

Exit: Closes the trade if Conviction drops (Signal fades) or hits a Hard Stop Loss.

Time Filters: Includes strict trading windows (e.g., No trading during lunch 12-1pm, closes all positions on Friday).

Summary

This is a Market Breadth & Momentum Strategy. It assumes that QQQ cannot sustain a trend unless its underlying components (NVDA, AAPL, etc.) are pushing it. It filters out "fake moves" where QQQ moves but the components don't support it.

SPY/QQQ Customizable Price ConverterThis is a minimalist utility tool designed for Index traders (SPX, NDX, RUT). It allows you to monitor the price of a reference asset (like SPY, QQQ) directly on your main chart without cluttering your screen.

Key Features:

1.🖱️ Crosshair Sync for Historical Data (Highlight): Unlike simple info tables that only show the latest price, this script allows for historical inspection.

· How it works: Simply move your mouse crosshair over ANY historical candle on your chart.

· The script will instantly display the closing price of the reference asset (e.g., SPY) for that specific time in the Status Line (top-left) or the Data Window. Perfect for backtesting and reviewing price action.

2.🔄 Fully Customizable Ticker: Default is set to SPY, but you can change it to anything in the settings.

e.g.

· Trading NDX Change it to QQQ.

· Trading RUT Change it to IWM.

3.📊 Clean Real-Time Dashboard:

· A floating table displays the current real-time price of your reference asset.

· Color-coded text (Green/Red) indicates price movement.

· Fully customizable size, position, and colors to fit your layout.

Mir Khans QQQThis strategy is built around how I actually trade QQQ intraday: Opening-Range continuation, VWAP trend reads, OI magnets, and a simple but strict risk framework. It’s designed to keep you on the right side of the session theme (trend vs fade), then only take trades when multiple pieces of confluence line up.

The strategy is tuned for QQQ on intraday timeframes, but the logic is generic enough to experiment with other liquid index products. It’s not financial advice—use it as a structured framework for reading OR, VWAP, and trend strength, and then layer your own execution rules and risk management on top.

QQQ TimingThis is a trend-following position trading strategy designed for the QQQ and the leveraged ETF QLD (ProShares Ultra QQQ). The primary goal is to capture multi-month holds for maximal profit.

Key Instruments & Performance

The strategy performs best with QLD, which yields far superior results compared to QQQ.

TQQQ (triple-leveraged) results in higher drawdowns and is not the optimal choice.

Important: The system is not intended for use with other indexes, individual stocks, or investments (like crypto or gold), as performance can vary widely.

Buy Signals

The strategy's signals are rooted in the S&P 500 Index (SPX), as testing showed it provides more reliable triggers than using QQQ itself.

Primary Buy Signal (Credit to IBD/Mike Webster): The SPX triggers a buy when its low closes above the 21-day Exponential Moving Average (EMA) for three consecutive days.

Refinement with Downtrend Lines: During corrective or bear periods, results and drawdowns can be significantly improved by incorporating downtrend lines. These lines connect lower highs. The strategy waits for the price to close above a drawn downtrend line before executing a buy. This refinement can modify the primary signal, either by allowing for an earlier entry or, in some cases, completely nullifying a false signal until the trend change proves itself.

Risk Management & Exit Strategy

Initial Buy Risk: A 3.7% stop loss is applied immediately upon the initial entry.

Initial Exit Rule: An exit is required if the QQQ's low drops below the 50-day Simple Moving Average (SMA).

Note: The 3.7% stop often provides protection when the initial buy occurs below the 50-day SMA. However, if QQQ is already trading above its 50-day SMA at the time of the SPX signal (indicating relative strength), historically, it has been better to use the 50-day SMA rule to give the position more room to run.

Trend Exit (Profit-Taking): To stay in a strong trend for the optimal amount of time, the long position is exited when a moving average crossover to the downside is triggered, based around the 107-day Simple Moving Average (SMA).

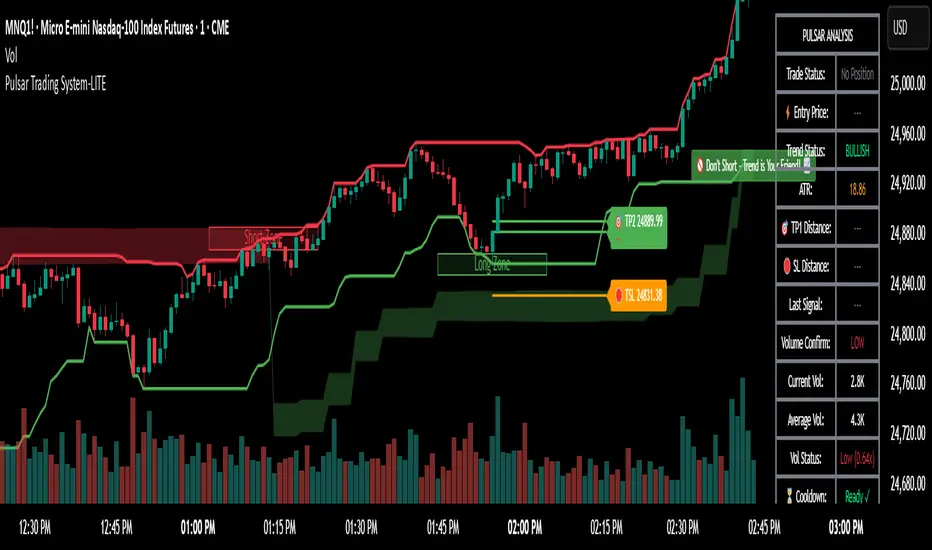

Pulsar Trading System-LITE📡 Pulsar Trading System

OVERVIEW

Pulsar is a comprehensive breakout trading system that combines dynamic support/resistance detection, trend filtering, and volume confirmation to identify high-probability entry opportunities. Unlike simple breakout indicators, Pulsar uses multi-timeframe analysis and adaptive ATR-based calculations to filter false signals and provide complete trade management from entry to exit.

WHAT MAKES THIS ORIGINAL

This indicator is unique in its integration of multiple complementary systems:

-Adaptive ATR Zones: Support and resistance levels are not static—they dynamically adjust based on current market volatility (ATR), creating entry zones that expand and contract with market conditions rather than using fixed price levels.

-Multi-Timeframe SuperTrend Filter: The trend filter operates on a higher timeframe than the chart (e.g., 5-minute SuperTrend on a 1-minute chart) to prevent counter-trend trades while maintaining granular entry precision. The visual ribbon with humorous warning text ("🚫 Don't Short - Trend is Your Friend! 📈") provides immediate trend awareness.

-Intelligent Cooldown System: After any trade exit (stop loss or take profit), the system enters a configurable cooldown period, preventing overtrading during choppy or consolidating market conditions—a critical feature often missing in breakout systems.

-Dynamic Trailing Stops: The trailing stop uses ATR multipliers to lock in profits while adapting to volatility, moving only in the favorable direction and never loosening.

-Comprehensive Dashboard: Real-time analysis displays trade status, entry prices, distances to targets in both points and ATR multiples, volume confirmation status, and cooldown countdown.

HOW IT WORKS

Core Detection Logic:

Pulsar identifies breakout opportunities by monitoring price interaction with dynamically calculated support and resistance levels:

Support/Resistance Calculation: Uses ta.lowest() and ta.highest() over a configurable lookback period to identify key levels, then adds ATR-based buffers (0.5 × ATR) to create entry zones.

Breakout Conditions:

Long Entry: Price closes above support buffer AND recent low touched support AND volume exceeds threshold

Short Entry: Price closes below resistance buffer AND recent high touched resistance AND volume exceeds threshold

SuperTrend Filter: A separate higher-timeframe SuperTrend calculation determines overall trend direction. Entries only trigger when breakout direction aligns with SuperTrend (bullish breakout + bullish trend, or bearish breakout + bearish trend).

Volume Confirmation: Current volume must exceed a configurable multiple of the 14-period SMA (default 1.0×) to confirm genuine interest in the breakout.

Cooldown Mechanism: After exit, the system tracks bars elapsed and blocks new signals until the cooldown period completes, preventing rapid-fire entries in ranging markets.

Trade Management:

Stop Loss: Calculated as entry zone ± (ATR × SL Multiplier)

Take Profit 1: Entry zone ± (ATR × TP1 Multiplier)

Take Profit 2: Entry zone ± (ATR × TP2 Multiplier)

Trailing Stop (optional): Updates every bar, moving the stop closer by maintaining distance of (ATR × Trailing Multiplier) from current price, but only in favorable direction

SuperTrend Calculation:

The SuperTrend uses standard methodology:

Upper Band = (High + Low) / 2 + (Multiplier × ATR)

Lower Band = (High + Low) / 2 - (Multiplier × ATR)

Direction changes when price crosses opposite band

The ribbon visualization adds a width offset (ATR × Ribbon Width) to create a filled zone rather than a single line.

HOW TO USE

Setup:

Add Pulsar to your chart (works best on liquid instruments like NQ, ES, CL)

Configure timeframe-specific settings (see recommendations below)

Enable SuperTrend Filter for trend-following mode, or disable for pure breakout mode

Set up alerts for Entry, TP1, TP2, and Stop Loss events

Recommended Settings by Timeframe:

1-Minute Charts:

Lookback Period: 10-15

SuperTrend Timeframe: 5 min

ATR Timeframe: 5 min (for stability)

Cooldown: 8-12 bars

Trailing Stop: Enabled with 0.8-1.0 multiplier

5-Minute Charts:

Lookback Period: 15-20

SuperTrend Timeframe: 15 min

ATR Timeframe: current chart

Cooldown: 5-8 bars

Trailing Stop: Optional

15-Minute+ Charts:

Lookback Period: 20-30

SuperTrend Timeframe: 1 hour

ATR Timeframe: current chart

Cooldown: 3-5 bars

Trailing Stop: Optional

Interpreting Signals:

Long/Short Zone Box: Green (long) or red (short) box appears when breakout conditions are met

Blue Entry Line: Shows your entry price

Red/Orange SL Line: Red = fixed stop, Orange = trailing stop (moves in real-time)

Green TP Lines: TP1 (closer) and TP2 (further) targets

SuperTrend Ribbon: Green = bullish trend (favor longs), Red = bearish trend (favor shorts)

Dashboard Status: Monitor trade state, distances, volume confirmation, and cooldown

Best Practices:

Use SuperTrend Filter: Significantly reduces false signals by avoiding counter-trend trades

Enable Cooldown on Fast Timeframes: Prevents overtrading on 1-5 minute charts

Volume Confirmation is Critical: Don't lower volume multiplier below 0.9 on futures

Use Higher Timeframe ATR: On 1-minute charts, use 5-minute ATR for stability

Avoid Major News Events: Disable during FOMC, NFP, CPI releases

Scale Out Strategy: Consider taking partial profits at TP1, letting remainder run to TP2

Parameter Optimization:

Start conservative and adjust based on results:

Too many stop-outs: Increase SL multiplier or SuperTrend multiplier

Missing good trades: Decrease volume multiplier or cooldown period

Too many false signals: Increase volume multiplier, lookback period, or cooldown

Profits not protected: Enable trailing stop or reduce trailing multiplier

KEY FEATURES

✅ Dynamic ATR-Based Zones: Entry, stop loss, and take profit levels automatically adjust to market volatility

✅ Multi-Timeframe Trend Filter: Uses higher timeframe SuperTrend to eliminate counter-trend trades

✅ Volume Confirmation: Filters low-volume false breakouts

✅ Intelligent Cooldown: Prevents overtrading with configurable post-trade waiting period

✅ Trailing Stop System: Optional dynamic stops that lock in profits using ATR distance

✅ Real-Time Dashboard: 13-row analysis showing trade status, targets, distances, volume, and cooldown

✅ Visual Ribbon Warnings: Humorous trend-following reminders on SuperTrend ribbon

✅ Complete Alert System: Notifications for entries, TP1, TP2, fixed stops, and trailing stops

✅ Customizable Visuals: Adjustable colors, dashboard position, text size, and line lengths

✅ Non-Repainting: Uses lookahead = barmerge.lookahead_off for all multi-timeframe calculations

SETTINGS EXPLAINED

SuperTrend Filter:

Enable: Toggle trend filtering on/off

Timeframe: Higher timeframe for trend analysis (recommended 3-5x chart timeframe)

ATR Period: Period for ATR calculation in SuperTrend (10-14 standard)

Multiplier: Distance from center band (2.5-3.5 for most markets)

Ribbon Width: Visual thickness of trend ribbon (0.2-0.5)

Core Parameters:

Lookback Period: Bars used to identify support/resistance (lower = more sensitive)

ATR Period: Bars for Average True Range calculation (14 is standard)

ATR Timeframe: Use higher timeframe ATR for smoother calculations on fast charts

Volume Multiplier: Required volume vs average (1.0 = average, 1.5 = 50% above average)

TP/SL:

SL Multiplier: Stop loss distance in ATR units (1.0-2.0 typical)

TP1 Multiplier: First target in ATR units (1.5-2.5 typical)

TP2 Multiplier: Second target in ATR units (2.0-3.5 typical)

Trailing Stop:

Enable: Activate dynamic trailing stop

Multiplier: Distance from current price in ATR units (0.8-1.5 typical)

Cooldown:

Enable: Prevent new signals after trade exit

Bars: Number of bars to wait before allowing next trade (higher on fast timeframes)

IMPORTANT NOTES

⚠️ Not a Holy Grail: No indicator is perfect. Pulsar is a tool that requires proper risk management, position sizing, and trading discipline.

⚠️ Backtest First: Test settings on historical data before live trading. Results vary by instrument, timeframe, and market conditions.

⚠️ Market Conditions Matter: Breakout systems perform best in trending markets. Consider reducing size or disabling during known choppy periods.

⚠️ Stop Loss is Mandatory: Always use the provided stop loss levels. Markets can move against you rapidly.

⚠️ Volume Data Required: This indicator requires volume data to function properly. It will display a warning if volume is unavailable.

⚠️ No Repainting: All multi-timeframe calls use non-repainting settings. What you see in real-time is what will be plotted historically.

TECHNICAL SPECIFICATIONS

Version: Pine Script v6

Type: Indicator (overlay = true)

Max Boxes: 500 (for zone visualization)

Max Lines: 500 (for TP/SL levels)

Max Labels: Unlimited (for annotations)

Repainting: None (uses lookahead = barmerge.lookahead_off)

COMPATIBLE INSTRUMENTS

Works best on liquid instruments with reliable volume data:

✅ Futures: NQ, MNQ, ES, MES, YM, MYM, RTY, M2K, CL, GC

✅ Forex: Major pairs (EUR/USD, GBP/USD, etc.)

✅ Stocks: Large-cap stocks with high volume

⚠️ Crypto: Works but requires higher ATR multipliers

❌ Low Volume Stocks: May produce unreliable signals

SUPPORT

For questions, suggestions, or to report issues, please comment below. I actively maintain this indicator and appreciate feedback from the community.

Enjoy trading with Pulsar! 🌟

GB · Set upUp & Confirmation (Lower Pane)The GB Set-Up & Confirmation Indicator transforms raw momentum into a clear, color-coded decision framework for intraday scalping.

It’s the heartbeat monitor of 0DTE trading — revealing when momentum quietly shifts and when it explodes into confirmation.

Milliseconds Ahead: Confirm-on-Prior mode mimics predictive confirmation, letting traders catch reversals before the lag candle.

Noise-Adaptive: Near-zero band filtering reduces false breaks from micro volatility.

Visual Precision: Dual markers and labeled confirmations remove hesitation in execution.

Configurable Latency: Sensitivity presets + fine-tune ensure adaptability from SPX 1-min charts to QQQ 5-min momentum waves.

Platform: Designed for lower-pane deployment beneath the main price chart.

Primary Use: Time-sensitive momentum confirmation for 0DTE SPX/SPY/QQQ scalps.

Typical Workflow:

Wait for Early (Set-Up) triangle near the zero band → signals momentum shift.

Enter on the Confirmed triangle (or one candle prior if using “Confirm on Prior”).

Exit when opposite signal fires or wave color fades (momentum exhaustion).

Complementary Indicators: Pairs seamlessly with GB TMA Overlay, GB ORB Shading, or Phoenix Fire Confluence for full-stack entry validation.

Adaptive Sensitivity Presets

- Aggressive: reacts early to momentum pulses (scalp mode).

- Balanced: optimized for intraday consistency.

- Strict: waits for full trend maturity (swing mode).

US/SPY- Financial Regime Index Swing Strategy Credits: concept inspired by EdgeTools Bloomberg Financial Conditions Index (Proxy)

Improvements: eight component basket, inverse volatility weights, winsorization option( statistical technique used to limit the influence of outliers in a dataset by replacing extreme values with less extreme ones, rather than removing them entirely), slope and price gates, exit guards, table and gradients.

Summary in one paragraph

A macro regime swing strategy for index ETFs, futures, FX majors, and large cap equities on daily calculation with optional lower time execution. It acts only when a composite Financial Conditions proxy plus slope and an optional price filter align. Originality comes from an eight component macro basket with inverse volatility weights and winsorized return z scores that produce a portable yardstick.

Scope and intent

Markets: SPY and peers, ES futures, ACWI, liquid FX majors, BTC, large cap equities.

Timeframes: calculation daily by default, trade on any chart.

Default demo: SPY on Daily.

Purpose: convert broad financial conditions into clear swing bias and exits.

Originality and usefulness

Unique fusion: return z scores for eight liquid proxies with inverse volatility weighting and optional winsorization, then slope and price gates.

Failure mode addressed: false starts in chop and early shorts during easy liquidity.

Testability: all knobs are inputs and the table shows components and weights.

Portable yardstick: z scores center at zero so thresholds transfer across symbols.

Method overview in plain language

Base measures

Return basis: natural log return over a configurable window, standardized to a z score. Winsorization optional to cap extremes.

Components

EQ US and EQ GLB measure equity tone.

CREDIT uses LQD over HYG. Higher credit quality outperformance is risk off so sign is flipped after z score.

RATES2Y uses two year yield, sign flipped.

SLOPE uses ten minus two year yield spread.

USD uses DXY, sign flipped.

VOL uses VIX, sign flipped.

LIQ uses BIL over SPY, sign flipped.

Each component is smoothed by the composite EMA.

Fusion rule

Weighted sum where weights are equal or inverse volatility with exponent gamma, normalized to percent so they sum to one.

Signal rule

Long when composite crosses up the long threshold and its slope is positive and price is above the SMA filter, or when composite is above the configured always long floor.

Short when composite crosses down the short threshold and its slope is negative and price is below the SMA filter.

Long exit on cross down of the long exit line or on a fresh short signal.

Short exit on cross up of the short exit line or on a fresh long signal, or when composite falls below the force short exit guard.

What you will see on the chart

Markers on suggestion bars: L for long, S for short, LX and SX for exits.

Reference lines at zero and soft regime bands at plus one and minus one.

Optional background gradient by regime intensity.

Compact table with component z, weight percent, and composite readout.

Table fields and quick reading guide

Component: EQ US, EQ GLB, CREDIT, RATES2Y, SLOPE, USD, VOL, LIQ.

Z: current standardized value, green for positive risk tone where applicable.

Weight: contribution percent after normalization.

Composite: current index value.

Reading tip: a broadly green Z column with slope positive often precedes better long context.

Inputs with guidance

Setup

Calc timeframe: default Daily. Leave blank to inherit chart.

Lookback: 50 to 1500. Larger length stabilizes regimes and delays turns.

EMA smoothing: 1 to 200. Higher smooths noise and delays signals.

Normalization

Winsorize z at ±3: caps extremes to reduce one off shocks.

Return window for equities: 5 to 260. Shorter reacts faster.

Weighting

Weight lookback: 20 to 520.

Weight mode: Equal or InvVol.

InvVol exponent gamma: 0.1 to 3. Higher compresses noisy components more.

Signals

Trade side: Long Short or Both.

Entry threshold long and short: portable z thresholds.

Exit line long and short: soft exits that give back less.

Slope lookback bars: 1 to 20.

Always long floor bfci ≥ X: macro easy mode keep long.

Force short exit when bfci < Y: macro stress guard.

Confirm

Use price trend filter and Price SMA length.

View

Glow line and Show component table.

Symbols

SPY ACWI HYG LQD VIX DXY US02Y US10Y BIL are defaults and can be changed.

Realism and responsible publication

No performance claims. Past is not future.

Shapes can move intrabar and settle on close.

Execution is on standard candles only.

Honest limitations and failure modes

Major economic releases and illiquid sessions can break assumptions.

Very quiet regimes reduce contrast. Use longer windows or higher thresholds.

Component proxies are ETFs and indexes and cannot match a proprietary FCI exactly.

Strategy notice

Orders are simulated on standard candles. All security calls use lookahead off. Nonstandard chart types are not supported for strategies.

Entries and exits

Long rule: bfci cross above long threshold with positive slope and optional price filter OR bfci above the always long floor.

Short rule: bfci cross below short threshold with negative slope and optional price filter.

Exit rules: long exit on bfci cross below long exit or on a short signal. Short exit on bfci cross above short exit or on a long signal or on force close guard.

Position sizing

Percent of equity by default. Keep target risk per trade low. One percent is a sensible starting point. For this example we used 3% of the total capital

Commisions

We used a 0.05% comission and 5 tick slippage

Legal

Education and research only. Not investment advice. Test in simulation first. Use realistic costs.

FluxVector Liquidity Universal Trendline FluxVector Liquidity Trendline FFTL

Summary in one paragraph

FFTL is a single adaptive trendline for stocks ETFs FX crypto and indices on one minute to daily. It fires only when price action pressure and volatility curvature align. It is original because it fuses a directional liquidity pulse from candle geometry and normalized volume with realized volatility curvature and an impact efficiency term to modulate a Kalman like state without ATR VWAP or moving averages. Add it to a clean chart and use the colored line plus alerts. Shapes can move while a bar is open and settle on close. For conservative alerts select on bar close.

Scope and intent

• Markets. Major FX pairs index futures large cap equities liquid crypto top ETFs

• Timeframes. One minute to daily

• Default demo used in the publication. SPY on 30min

• Purpose. Reduce false flips and chop by gating the line reaction to noise and by using a one bar projection

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique fusion. Directional Liquidity Pulse plus Volatility Curvature plus Impact Efficiency drives an adaptive gain for a one dimensional state

• Failure mode addressed. One or two shock candles that break ordinary trendlines and saw chop in flat regimes

• Testability. All windows and gains are inputs

• Portable yardstick. Returns use natural log units and range is bar high minus low

• Protected scripts. Not used. Method disclosed plainly here

Method overview in plain language

Base measures

• Return basis. Natural log of close over prior close. Average absolute return over a window is a unit of motion

Components

• Directional Liquidity Pulse DLP. Measures signed participation from body and wick imbalance scaled by normalized volume and variance stabilized

• Volatility Curvature. Second difference of realized volatility from returns highlights expansion or compression

• Impact Efficiency. Price change per unit range and volume boosts gain during efficient moves

• Energy score. Z scores of the above form a single energy that controls the state gain

• One bar projection. Current slope extended by one bar for anticipatory checks

Fusion rule

Weighted sum inside the energy score then logistic mapping to a gain between k min and k max. The state updates toward price plus a small flow push.

Signal rule

• Long suggestion and order when close is below trend and the one bar projection is above the trend

• Short suggestion and flip when close is above trend and the one bar projection is below the trend

• WAIT is implicit when neither condition holds

• In position states end on the opposite condition

What you will see on the chart

• Colored trendline teal for rising red for falling gray for flat

• Optional projection line one bar ahead

• Optional background can be enabled in code

• Alerts on price cross and on slope flips

Inputs with guidance

Setup

• Price source. Close by default

Logic

• Flow window. Typical range 20 to 80. Higher smooths the pulse and reduces flips

• Vol window. Typical range 30 to 120. Higher calms curvature

• Energy window. Typical range 20 to 80. Higher slows regime changes

• Min gain and Max gain. Raise max to react faster. Raise min to keep momentum in chop

UI

• Show 1 bar projection. Colors for up down flat

Properties visible in this publication

• Initial capital 25000

• Base currency USD

• Commission percent 0.03

• Slippage 5

• Default order size method percent of equity value 3%

• Pyramiding 0

• Process orders on close off

• Calc on every tick off

• Recalculate after order is filled off

Realism and responsible publication

• No performance claims

• Intrabar reminder. Shapes can move while a bar forms and settle on close

• Strategy uses standard candles only

Honest limitations and failure modes

• Sudden gaps and thin liquidity can still produce fast flips

• Very quiet regimes reduce contrast. Use larger windows and lower max gain

• Session time uses the exchange time of the chart if you enable any windows later

• Past results never guarantee future outcomes

Open source reuse and credits

• None

TriAnchor Elastic Reversion US Market SPY and QQQ adaptedSummary in one paragraph

Mean-reversion strategy for liquid ETFs, index futures, large-cap equities, and major crypto on intraday to daily timeframes. It waits for three anchored VWAP stretches to become statistically extreme, aligns with bar-shape and breadth, and fades the move. Originality comes from fusing daily, weekly, and monthly AVWAP distances into a single ATR-normalized energy percentile, then gating with a robust Z-score and a session-safe gap filter.

Scope and intent

• Markets: SPY QQQ IWM NDX large caps liquid futures liquid crypto

• Timeframes: 5 min to 1 day

• Default demo: SPY on 60 min

• Purpose: fade stretched moves only when multi-anchor context and breadth agree

• Limits: strategy uses standard candles for signals and orders only

Originality and usefulness

• Unique fusion: tri-anchor AVWAP energy percentile plus robust Z of close plus shape-in-range gate plus breadth Z of SPY QQQ IWM

• Failure mode addressed: chasing extended moves and fading during index-wide thrusts

• Testability: each component is an input and visible in orders list via L and S tags

• Portable yardstick: distances are ATR-normalized so thresholds transfer across symbols

• Open source: method and implementation are disclosed for community review

Method overview in plain language

Base measures

• Range basis: ATR(length = atr_len) as the normalization unit

• Return basis: not used directly; we use rank statistics for stability

Components

• Tri-Anchor Energy: squared distances of price from daily, weekly, monthly AVWAPs, each divided by ATR, then summed and ranked to a percentile over base_len

• Robust Z of Close: median and MAD based Z to avoid outliers

• Shape Gate: position of close inside bar range to require capitulation for longs and exhaustion for shorts

• Breadth Gate: average robust Z of SPY QQQ IWM to avoid fading when the tape is one-sided

• Gap Shock: skip signals after large session gaps

Fusion rule

• All required gates must be true: Energy ≥ energy_trig_prc, |Robust Z| ≥ z_trig, Shape satisfied, Breadth confirmed, Gap filter clear

Signal rule

• Long: energy extreme, Z negative beyond threshold, close near bar low, breadth Z ≤ −breadth_z_ok

• Short: energy extreme, Z positive beyond threshold, close near bar high, breadth Z ≥ +breadth_z_ok

What you will see on the chart

• Standard strategy arrows for entries and exits

• Optional short-side brackets: ATR stop and ATR take profit if enabled

Inputs with guidance

Setup

• Base length: window for percentile ranks and medians. Typical 40 to 80. Longer smooths, shorter reacts.

• ATR length: normalization unit. Typical 10 to 20. Higher reduces noise.

• VWAP band stdev: volatility bands for anchors. Typical 2.0 to 4.0.

• Robust Z window: 40 to 100. Larger for stability.

• Robust Z entry magnitude: 1.2 to 2.2. Higher means stronger extremes only.

• Energy percentile trigger: 90 to 99.5. Higher limits signals to rare stretches.

• Bar close in range gate long: 0.05 to 0.25. Larger requires deeper capitulation for longs.

Regime and Breadth

• Use breadth gate: on when trading indices or broad ETFs.

• Breadth Z confirm magnitude: 0.8 to 1.8. Higher avoids fighting thrusts.

• Gap shock percent: 1.0 to 5.0. Larger allows more gaps to trade.

Risk — Short only

• Enable short SL TP: on to bracket shorts.

• Short ATR stop mult: 1.0 to 3.0.

• Short ATR take profit mult: 1.0 to 6.0.

Properties visible in this publication

• Initial capital: 25000USD

• Default order size: Percent of total equity 3%

• Pyramiding: 0

• Commission: 0.03 percent

• Slippage: 5 ticks

• Process orders on close: OFF

• Bar magnifier: OFF

• Recalculate after order is filled: OFF

• Calc on every tick: OFF

• request.security lookahead off where used

Realism and responsible publication

• No performance claims. Past results never guarantee future outcomes

• Fills and slippage vary by venue

• Shapes can move during bar formation and settle on close

• Standard candles only for strategies

Honest limitations and failure modes

• Economic releases or very thin liquidity can overwhelm mean-reversion logic

• Heavy gap regimes may require larger gap filter or TR-based tuning

• Very quiet regimes reduce signal contrast; extend windows or raise thresholds

Open source reuse and credits

• None

Strategy notice

Orders are simulated by TradingView on standard candles. request.security uses lookahead off where applicable. Non-standard charts are not supported for execution.

Entries and exits

• Entry logic: as in Signal rule above

• Exit logic: short side optional ATR stop and ATR take profit via brackets; long side closes on opposite setup

• Risk model: ATR-based brackets on shorts when enabled

• Tie handling: stop first when both could be touched inside one bar

Dataset and sample size

• Test across your visible history. For robust inference prefer 100 plus trades.

FluxGate Daily Swing StrategySummary in one paragraph

FluxGate treats long and short as different ecosystems. It runs two independent engines so the long side can be bold when the tape rewards upside persistence while the short side can stay selective when downside is messy. The core reads three directional drivers from price geometry then removes overlap before gating with clean path checks. The complementary risk module anchors stop distance to a higher timeframe ATR so a unit means the same thing on SPY and BTC. It can add take profit breakeven and an ATR trail that only activates after the trade earns it. If a stop is hit the strategy can re enter in the same direction on the next bar with a daily retry cap that you control. Add it to a clean chart. Use defaults to see the intended behavior. For conservative workflows evaluate on bar close.

Scope and intent

• Markets. Large cap equities and liquid ETFs major FX pairs US index futures and liquid crypto pairs

• Timeframes. From one minute to daily

• Default demo in this publication. SPY on one day timeframe

• Purpose. Reduce false starts without missing sustained trends by fusing independent drivers and suppressing activity when the path is noisy

• Limits. This is a strategy. Orders are simulated on standard candles. Non standard chart types are not supported for execution

Originality and usefulness

• Unique fusion. FluxGate extracts three drivers that look at price from different angles. Direction measures slope of a smoothed guide and scales by realized volatility so a point of slope does not mean a different thing on different symbols. Persistence looks at short sign agreement to reward series of closes that keep direction. Curvature measures the second difference of a local fit to wake up during convex pushes. These three are then orthonormalized so a strong reading in one does not double count through another.

• Gates that matter. Efficiency ratio prefers direct paths over treadmills. Entropy turns up versus down frequency into an information read. Light fractal cohesion punishes wrinkly paths. Together they slow the system in chop and allow it to open up when the path is clean.

• Separate long and short engines. Threshold tilts adapt to the skew of score excursions. That lets long engage earlier when upside distribution supports it and keeps short cautious where downside surprise and venue frictions are common.

• Practical risk behavior. Stops are ATR anchored on a higher timeframe so the unit is portable. Take profit is expressed in R so two R means the same concept across symbols. Breakeven and trailing only activate after a chosen R so early noise does not squeeze a good entry. Re entry after stop lets the system try again without you babysitting the chart.

• Testability. Every major window and the aggression controls live in Inputs. There is no hidden magic number.

Method overview in plain language

Base measures

• Return basis. Natural log of close over prior close for stability and easy aggregation through time. Realized volatility is the standard deviation of returns over a moving window.

• Range basis for risk. ATR computed on a higher timeframe anchor such as day week or month. That anchor is steady across venues and avoids chasing chart specific quirks.

Components

• Directional intensity. Use an EMA of typical price as a guide. Take the day to day slope as raw direction. Divide by realized volatility to get a unit free measure. Soft clip to keep outliers from dominating.

• Persistence. Encode whether each bar closed up or down. Measure short sign agreement so a string of higher closes scores better than a jittery sequence. This favors push continuity without guessing tops or bottoms.

• Curvature. Fit a short linear regression and compute the second difference of the fitted series. Strong curvature flags acceleration that slope alone may miss.

• Efficiency gate. Compare net move to path length over a gate window. Values near one indicate direct paths. Values near zero indicate treadmill behavior.

• Entropy gate. Convert up versus down frequency into a probability of direction. High entropy means coin toss. The gate narrows there.

• Fractal cohesion. A light read of path wrinkliness relative to span. Lower cohesion reduces the urge to act.

• Phase assist. Map price inside a recent channel to a small signed bias that grows with confidence. This helps entries lean toward the right half of the channel without becoming a breakout rule.

• Shock control. Compare short volatility to long volatility. When short term volatility spikes the shock gate temporarily damps activity so the system waits for pressure to normalize.

Fusion rule

• Normalize the three drivers after removing overlap

• Blend with weights that adapt to your aggression input

• Multiply by the gates to respect path quality

• Smooth just enough to avoid jitter while keeping timing responsive

• Compute an adaptive mean and deviation of the score and set separate long and short thresholds with a small tilt informed by skew sign

• The result is one long score and one short score that can cross their thresholds at different times for the same tape which is a feature not a bug

Signal rule

• A long suggestion appears when the long score crosses above its long threshold while all gates are active

• A short suggestion appears when the short score crosses below its short threshold while all gates are active

• If any required gate is missing the state is wait

• When a position is open the status is in long or in short until the complementary risk engine exits or your entry mode closes and flips

Inputs with guidance

Setup Long

• Base length Long. Master window for the long engine. Typical range twenty four to eighty. Raising it improves selectivity and reduces trade count. Lowering it reacts faster but can increase noise

• Aggression Long. Zero to one. Higher values make thresholds more permissive and shorten smoothing

Setup Short

• Base length Short. Master window for the short engine. Typical range twenty eight to ninety six

• Aggression Short. Zero to one. Lower values keep shorts conservative which is often useful on upward drifting symbols

Entries and UI

• Entry mode. Both or Long only or Short only

Complementary risk engine

• Enable risk engine. Turns on bracket exits while keeping your signal logic untouched

• ATR anchor timeframe. Day Week or Month. This sets the structural unit of stop distance

• ATR length. Default fourteen

• Stop multiple. Default one point five times the anchor ATR

• Use take profit. On by default

• Take profit in R. Default two R

• Breakeven trigger in R. Default one R

Usage recipes

Intraday trend focus

• Entry mode Both

• ATR anchor Week

• Aggression Long zero point five Aggression Short zero point three

• Stop multiple one point five Take profit two R

• Expect fewer trades that stick to directional pushes and skip treadmill noise

Intraday mean reversion focus

• Session windows optional if you add them in your copy

• ATR anchor Day

• Lower aggression both sides

• Breakeven later and trailing later so the first bounce has room

• This favors fade entries that still convert into trends when the path stays clean

Swing continuation

• Signal timeframe four hours or one day

• Confirm timeframe one day if you choose to include bias

• ATR anchor Week or Month

• Larger base windows and a steady two R target

• This accepts fewer entries and aims for larger holds

Properties visible in this publication

• Initial capital 25.000

• Base currency USD

• Default order size percent of equity value three - 3% of the total capital

• Pyramiding zero

• Commission zero point zero three percent - 0.03% of total capital

• Slippage five ticks

• Process orders on close off

• Recalculate after order is filled off

• Calc on every tick off

• Bar magnifier off

• Any request security calls use lookahead off everywhere

Realism and responsible publication

• No performance promises. Past results never guarantee future outcomes

• Fills and slippage vary by venue and feed

• Strategies run on standard candles only

• Shapes can update while a bar is forming and settle on close

• Keep risk per trade sensible. Around one percent is typical for study. Above five to ten percent is rarely sustainable

Honest limitations and failure modes

• Sudden news and thin liquidity can break assumptions behind entropy and cohesion reads

• Gap heavy symbols often behave better with a True Range basis for risk than a simple range

• Very quiet regimes can reduce score contrast. Consider longer windows or higher thresholds when markets sleep

• Session windows follow the exchange time of the chart if you add them

• If stop and target can both be inside a single bar this strategy prefers stop first to keep accounting conservative

Open source reuse and credits

• No reused open source beyond public domain building blocks such as ATR EMA and linear regression concepts

Legal

Education and research only. Not investment advice. You are responsible for your decisions. Test on history and in simulation with realistic costs

ProbRSI Adaptive SPY and QQQ Swing One Hour Strategy Summary in one paragraph

A probabilistic RSI engine for large cap ETFs and index names on intraday and swing timeframes. It converts ATR scaled returns into a 0 to 100 probability line, adapts its smoothing from path efficiency, and gates flips with simple percent levels. It is original because it fuses three pieces that traders rarely combine in one signal line: ATR normalized return probability, curvature compression, and per bar adaptive EMA. Add it to a clean chart, keep the default one hour signal on QQQ, and read the entry and exit markers generated by the strategy. For conservative alerts select on bar close.

Scope and intent

• Markets. Major ETFs and large cap equities. Index futures. Liquid crypto. Major FX pairs

• Timeframes. One minute to daily. Defaults to one hour for swing pace

• Default demo used in this publication. SPY/QQQ on one hour

• Purpose. Reduce false flips by adapting to path efficiency and by gating long and short separately

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique fusion. Logistic probability of ATR scaled returns with arcsine pre transform, optional curvature compression, and per bar adaptive EMA steered by an efficiency ratio

• Failure mode addressed. Fast whips in congestion and late entries after spikes

• Testability. Each component has a named input and can be tuned directly. Entry names Long and Short are visible in the list of trades

• Portable yardstick. ATR scaled return is a common unit across symbols and venues

• Protected rationale. The code stays protected to preserve implementation details of the adaptive engine and curvature assist while the method and usage are fully explained here for community review

Method overview in plain language

You convert raw returns into a probability scale, adapt the smoothing to the straightness of the path, and only allow flips when a simple gate is satisfied. The probability line crosses its own EMA to generate signals. When the cross happens below a short gate or above a long gate, the flip is allowed. Otherwise it is ignored.

Base measures

• Return basis. Close minus prior close normalized by ATR, then arcsine to damp large steps. ATR window is set by ATR length. Sensitivity is adjusted by an ATR scale input

• Probability map. A logistic function maps the normalized return to 0 to 1 which becomes 0 to 100 after scaling

Components

• Probability core. Logistic probability of ATR scaled returns. Higher values imply upside pressure. Smoothed by an adaptive EMA

• Curvature assist optional. A curvature proxy compresses extreme spikes toward neutral. Useful after news bars. Weight controls strength

• Efficiency ratio. A path efficiency score from 0 to 1 extends the smoothing length during noisy paths and shortens it during directional paths

• Signal line. An EMA of the probability line creates the reference for cross up and cross down

• Gates. Two simple percent levels define when long and short flips are allowed

Fusion rule

• The adaptive EMA length is computed as a linear map between a minimum and a maximum bound based on one minus efficiency

• If curvature assist is enabled the probability is adjusted by a small counter spike term

• Final probability is compared to its EMA

Signal rule

• Long. A long entry is suggested when probability crosses above the signal line and the current probability is above the Long gate level

• Short. A short entry is suggested when probability crosses below the signal line and the current probability is below the Short gate level

• Exit and flip. When an opposite entry condition appears the current position is closed and a new position opens in the opposite direction

What you will see on the chart

• Strategy markers on suggestion bars. Orders named Long and Short

• Exit marker when the opposite signal closes the open side

• No table by design. All tuning lives in Inputs for a clean chart

Inputs with guidance

Market TF

• Symbol. Series used for oscillator computation. Use the instrument you trade or a close proxy

• Signal timeframe. Timeframe where the oscillator is evaluated. Leave blank to follow the chart

Core

• Price source. Series used for returns. Typical choice close

• Base length. Fallback EMA length used when adaptation is off. Typical range 20 to 200. Larger smooths more

• ATR length. Window for ATR that scales returns. Typical range 10 to 30. Larger normalizes more and lowers sensitivity

• Logit sharpness. Steepness of the logistic link. Typical range 1 to 8. Raising it reacts more to the same input

• ATR scale. Extra divisor on ATR. Typical range 0.5 to 2. Smaller is more sensitive

• Signal length. EMA of the probability line. Typical range 5 to 20. Larger gives fewer flips

• Long gate. Allow long flips only above this level. Typical range 20 to 40

• Short gate. Allow short flips only below this level. Typical range 20 to 40

Adaptive

• Adaptive smoothing. If on, the efficiency ratio controls the per bar EMA length

• Min effective length. Lower bound of adaptive EMA. Typical range 5 to 50

• Max effective length. Upper bound of adaptive EMA. Typical range 50 to 300

• Efficiency window. Window for efficiency ratio. Typical range 30 to 100

Shape Assist

• Curvature influence. If on, extreme spikes are nudged toward neutral

• Curvature weight. Strength of compression. Typical range 0.1 to 0.3

Properties visible in this publication

• Initial capital. 25000

• Base currency. USD

• request.security lookahead off everywhere

• Commission. 0.03 percent

• Slippage. 5 ticks

• Default order size method percent of equity with value 3 for realistic testing

• Pyramiding 0

• Process orders on close ON

• Bar magnifier OFF

• Recalculate after order is filled OFF

• Calc on every tick OFF

Realism and responsible publication

• No performance claims. Past results never guarantee future outcomes

• Shapes can move while a bar forms and settle on close

• Strategies use standard candles for signals and orders only

Honest limitations and failure modes

• Economic releases and thin liquidity can break assumptions behind the curvature assist

• Gap heavy symbols may prefer a longer ATR window

• Very quiet regimes can reduce signal contrast. Consider higher gates or longer signal length

• Session time follows the exchange of the chart and can change symbol to symbol

• Symbol sensitivity is expected. Use the gates and length inputs to find stable settings

• Past results never guarantee future outcomes

Open source reuse and credits

• None

Mode

Public protected. Source is hidden while access is free. Implementation detail remains private. Method and use are fully disclosed here

Legal

Education and research only. Not investment advice. You are responsible for your decisions. Test on historical data and in simulation before any live use. Use realistic costs.

Quantum Flux Universal Strategy Summary in one paragraph

Quantum Flux Universal is a regime switching strategy for stocks, ETFs, index futures, major FX pairs, and liquid crypto on intraday and swing timeframes. It helps you act only when the normalized core signal and its guide agree on direction. It is original because the engine fuses three adaptive drivers into the smoothing gains itself. Directional intensity is measured with binary entropy, path efficiency shapes trend quality, and a volatility squash preserves contrast. Add it to a clean chart, watch the polarity lane and background, and trade from positive or negative alignment. For conservative workflows use on bar close in the alert settings when you add alerts in a later version.

Scope and intent

• Markets. Large cap equities and ETFs. Index futures. Major FX pairs. Liquid crypto

• Timeframes. One minute to daily

• Default demo used in the publication. QQQ on one hour

• Purpose. Provide a robust and portable way to detect when momentum and confirmation align, while dampening chop and preserving turns

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique concept or fusion. The novelty sits in the gain map. Instead of gating separate indicators, the model mixes three drivers into the adaptive gains that power two one pole filters. Directional entropy measures how one sided recent movement has been. Kaufman style path efficiency scores how direct the path has been. A volatility squash stabilizes step size. The drivers are blended into the gains with visible inputs for strength, windows, and clamps.

• What failure mode it addresses. False starts in chop and whipsaw after fast spikes. Efficiency and the squash reduce over reaction in noise.

• Testability. Every component has an input. You can lengthen or shorten each window and change the normalization mode. The polarity plot and background provide a direct readout of state.

• Portable yardstick. The core is normalized with three options. Z score, percent rank mapped to a symmetric range, and MAD based Z score. Clamp bounds define the effective unit so context transfers across symbols.

Method overview in plain language

The strategy computes two smoothed tracks from the chart price source. The fast track and the slow track use gains that are not fixed. Each gain is modulated by three drivers. A driver for directional intensity, a driver for path efficiency, and a driver for volatility. The difference between the fast and the slow tracks forms the raw flux. A small phase assist reduces lag by subtracting a portion of the delayed value. The flux is then normalized. A guide line is an EMA of a small lead on the flux. When the flux and its guide are both above zero, the polarity is positive. When both are below zero, the polarity is negative. Polarity changes create the trade direction.

Base measures

• Return basis. The step is the change in the chosen price source. Its absolute value feeds the volatility estimate. Mean absolute step over the window gives a stable scale.

• Efficiency basis. The ratio of net move to the sum of absolute step over the window gives a value between zero and one. High values mean trend quality. Low values mean chop.

• Intensity basis. The fraction of up moves over the window plugs into binary entropy. Intensity is one minus entropy, which maps to zero in uncertainty and one in very one sided moves.

Components

• Directional Intensity. Measures how one sided recent bars have been. Smoothed with RMA. More intensity increases the gain and makes the fast and slow tracks react sooner.

• Path Efficiency. Measures the straightness of the price path. A gamma input shapes the curve so you can make trend quality count more or less. Higher efficiency lifts the gain in clean trends.

• Volatility Squash. Normalizes the absolute step with Z score then pushes it through an arctangent squash. This caps the effect of spikes so they do not dominate the response.

• Normalizer. Three modes. Z score for familiar units, percent rank for a robust monotone map to a symmetric range, and MAD based Z for outlier resistance.

• Guide Line. EMA of the flux with a small lead term that counteracts lag without heavy overshoot.

Fusion rule

• Weighted sum of the three drivers with fixed weights visible in the code comments. Intensity has fifty percent weight. Efficiency thirty percent. Volatility twenty percent.

• The blend power input scales the driver mix. Zero means fixed spans. One means full driver control.

• Minimum and maximum gain clamps bound the adaptive gain. This protects stability in quiet or violent regimes.

Signal rule

• Long suggestion appears when flux and guide are both above zero. That sets polarity to plus one.

• Short suggestion appears when flux and guide are both below zero. That sets polarity to minus one.

• When polarity flips from plus to minus, the strategy closes any long and enters a short.

• When flux crosses above the guide, the strategy closes any short.

What you will see on the chart

• White polarity plot around the zero line

• A dotted reference line at zero named Zen

• Green background tint for positive polarity and red background tint for negative polarity

• Strategy long and short markers placed by the TradingView engine at entry and at close conditions

• No table in this version to keep the visual clean and portable

Inputs with guidance

Setup

• Price source. Default ohlc4. Stable for noisy symbols.

• Fast span. Typical range 6 to 24. Raising it slows the fast track and can reduce churn. Lowering it makes entries more reactive.

• Slow span. Typical range 20 to 60. Raising it lengthens the baseline horizon. Lowering it brings the slow track closer to price.

Logic

• Guide span. Typical range 4 to 12. A small guide smooths without eating turns.

• Blend power. Typical range 0.25 to 0.85. Raising it lets the drivers modulate gains more. Lowering it pushes behavior toward fixed EMA style smoothing.

• Vol window. Typical range 20 to 80. Larger values calm the volatility driver. Smaller values adapt faster in intraday work.

• Efficiency window. Typical range 10 to 60. Larger values focus on smoother trends. Smaller values react faster but accept more noise.

• Efficiency gamma. Typical range 0.8 to 2.0. Above one increases contrast between clean trends and chop. Below one flattens the curve.

• Min alpha multiplier. Typical range 0.30 to 0.80. Lower values increase smoothing when the mix is weak.

• Max alpha multiplier. Typical range 1.2 to 3.0. Higher values shorten smoothing when the mix is strong.

• Normalization window. Typical range 100 to 300. Larger values reduce drift in the baseline.

• Normalization mode. Z score, percent rank, or MAD Z. Use MAD Z for outlier heavy symbols.

• Clamp level. Typical range 2.0 to 4.0. Lower clamps reduce the influence of extreme runs.

Filters

• Efficiency filter is implicit in the gain map. Raising efficiency gamma and the efficiency window increases the preference for clean trends.

• Micro versus macro relation is handled by the fast and slow spans. Increase separation for swing, reduce for scalping.

• Location filter is not included in v1.0. If you need distance gates from a reference such as VWAP or a moving mean, add them before publication of a new version.

Alerts

• This version does not include alertcondition lines to keep the core minimal. If you prefer alerts, add names Long Polarity Up, Short Polarity Down, Exit Short on Flux Cross Up in a later version and select on bar close for conservative workflows.

Strategy has been currently adapted for the QQQ asset with 30/60min timeframe.

For other assets may require new optimization

Properties visible in this publication

• Initial capital 25000

• Base currency Default

• Default order size method percent of equity with value 5

• Pyramiding 1

• Commission 0.05 percent

• Slippage 10 ticks

• Process orders on close ON

• Bar magnifier ON

• Recalculate after order is filled OFF

• Calc on every tick OFF

Honest limitations and failure modes

• Past results do not guarantee future outcomes

• Economic releases, circuit breakers, and thin books can break the assumptions behind intensity and efficiency

• Gap heavy symbols may benefit from the MAD Z normalization

• Very quiet regimes can reduce signal contrast. Use longer windows or higher guide span to stabilize context

• Session time is the exchange time of the chart

• If both stop and target can be hit in one bar, tie handling would matter. This strategy has no fixed stops or targets. It uses polarity flips for exits. If you add stops later, declare the preference

Open source reuse and credits

• None beyond public domain building blocks and Pine built ins such as EMA, SMA, standard deviation, RMA, and percent rank

• Method and fusion are original in construction and disclosure

Legal

Education and research only. Not investment advice. You are responsible for your decisions. Test on historical data and in simulation before any live use. Use realistic costs.

Strategy add on block

Strategy notice

Orders are simulated by the TradingView engine on standard candles. No request.security() calls are used.

Entries and exits

• Entry logic. Enter long when both the normalized flux and its guide line are above zero. Enter short when both are below zero

• Exit logic. When polarity flips from plus to minus, close any long and open a short. When the flux crosses above the guide line, close any short

• Risk model. No initial stop or target in v1.0. The model is a regime flipper. You can add a stop or trail in later versions if needed

• Tie handling. Not applicable in this version because there are no fixed stops or targets

Position sizing

• Percent of equity in the Properties panel. Five percent is the default for examples. Risk per trade should not exceed five to ten percent of equity. One to two percent is a common choice

Properties used on the published chart

• Initial capital 25000

• Base currency Default

• Default order size percent of equity with value 5

• Pyramiding 1

• Commission 0.05 percent

• Slippage 10 ticks

• Process orders on close ON

• Bar magnifier ON

• Recalculate after order is filled OFF

• Calc on every tick OFF

Dataset and sample size

• Test window Jan 2, 2014 to Oct 16, 2025 on QQQ one hour

• Trade count in sample 324 on the example chart

Release notes template for future updates

Version 1.1.

• Add alertcondition lines for long, short, and exit short

• Add optional table with component readouts

• Add optional stop model with a distance unit expressed as ATR or a percent of price

Notes. Backward compatibility Yes. Inputs migrated Yes.

PulseGrid Universal Scalper - Adaptive Pulse and Symmetric SpansInstrument agnostic. Works on any symbol and timeframe supported by TradingView.

Message or hit me up in chat for full access .

Purpose and scope

PulseGrid is a short timeframe strategy designed to read intrabar structure and recent path so that entries align with actionable momentum and context. The strategy is private. The description below provides all the information needed to understand how it behaves, how it sizes risk, how to tune it responsibly, and how to evaluate results without making unrealistic claims. The design is instrument agnostic. It runs on any asset class that prints open high low close bars on TradingView. That includes commodities such as Gold and WTI, currencies, crypto, equity indices, and single stocks. Performance will always depend on the symbol’s liquidity, spread, slippage, and session structure, which is why the description focuses on principles and safe parameter ranges instead of hard promises.

What the strategy does at a glance

It builds a composite entry signal named Pulse from five normalized bar features that reflect short term pressure and follow through.

It applies regime guards that keep the strategy inactive when the tape is either too quiet, too bursty, or too directionally random.

It optionally uses a directional filter where a fast and a slow exponential average must agree and their gap must be material relative to recent true range.

When a signal is allowed, risk is sized using symmetric spans that come from nearby untraded price distances above and below the market. The strategy sets a single stop and a single take profit from those spans.

Lines for entry, stop, and take profit are drawn on the chart. A compact on chart table shows trade counts, win rate, average R per trade, and profit factor for all trades, longs only, and shorts only.

This combination yields entries that are reactive but not chaotic, and risk lines that respect the market’s recent path instead of generic pip or point targets.

Why the design is original and useful

The core originality is the union of a composite entry that adapts to volatility and a geometry based risk model. The entry uses five different viewpoints on the same bar space instead of relying on a single technical indicator. The risk model uses spans that come from actual untraded distance rather than fixed multipliers of a generic volatility measure. The result is a framework that is simple to read on a chart and simple to evaluate, yet it avoids the traps of curve fitting to one symbol or one month of data. Because everything is normalized locally, the same logic translates across asset classes with only modest tuning.

The Pulse composite in detail

Pulse is a weighted blend of the following normalized features.

Impulse imbalance. The script sums upward and downward impulses over a short window. An upward impulse is the extension of highs relative to the prior bar. A downward impulse is the extension of lows relative to the prior bar. The net imbalance, scaled by the local range, captures whether extension pressure is building or fading.

Wick and close location. Inside each bar, the distance between the close and the extremes carries information about rejection or acceptance. A bar that closes near the high with relatively heavier lower wick suggests upward acceptance. A bar that closes near the low with heavier upper wick suggests downward acceptance. A weight controls the contribution of wick skew versus close location so that users can favor reversal or momentum behaviour.

Shock touches. Within the recent range window, touches that occur very near the top decile or bottom decile are marked. A short sliding window counts recent shocks. Frequent top shocks in a rising context suggest supply tests. Frequent bottom shocks in a declining context suggest demand tests. The count is normalized by window length.

Breakout ledger. The script compares current extremes to lagged extremes and keeps a simple count of recent upside and downside breakouts. The difference behaves as a short term polarity meter.

Curvature. A simple second difference in closing price acts as a curvature term. It is normalized by the recent maximum of absolute one bar returns so that the value remains bounded and comparable to other terms.

Pulse is smoothed over a fraction of the main signal length. Smoothing removes impulse spikes without destroying the quick reaction that scalpers need. The absolute value of smoothed Pulse can be used with an adaptive gate so that only the top percentile of energy for the recent environment is eligible for entries. A small floor prevents accidental entries during very quiet periods.

Regime guards that keep the strategy selective

Three guards must all pass before any entry can occur.

Auction Balance Factor. This is the proportion of closes that land inside a mid band of the prior bar’s high to low range. High values indicate balanced chop where breakouts tend to fail. Low values indicate directional conditions. The strategy requires ABF to sit below a user chosen maximum.

Dispersion via a Gini style measure on absolute returns. Very low dispersion means bars are small and uniform. Very high dispersion means a few outsized bars dominate and slippage risk can be elevated. The strategy allows the user to require the dispersion measure to remain inside a band that reflects healthy activity.

Binary entropy of direction. Over the core window, the proportion of up closes is used to compute a simple entropy. Values near one indicate coin flip behaviour. Values near zero indicate one sided sequences. The guard requires entropy below a ceiling so that random directionality does not produce noise entries.

An optional directional filter asks that a fast and a slow exponential average agree on direction and that their gap, when divided by an average true range, exceed a threshold. This filter can be enabled on symbols that trend cleanly and disabled when the composite entry is already selective enough.

Risk sizing with symmetric spans

Instead of fixed points or a pure ATR multiplier, the strategy sizes stops and targets from a pair of spans. The upward span reflects recent untraded distance above the market. The downward span reflects recent untraded distance below the market. Each span is floored by a fallback that comes from the maximum of a short simple range average and a standard average true range. A tick based floor prevents microscopic stops on instruments with high tick precision. An asymmetry cap prevents one span from becoming many times larger than the other. For long entries the stop is a multiple of the downward span and the target is a multiple of the upward span. For short entries the stop is a multiple of the upward span and the target is a multiple of the downward span. This creates a risk box that is symmetric by construction yet adaptive to recent voids and gaps.

Execution, ties, and housekeeping

Entries evaluate at bar close. Exits are tested from the next bar forward. If both stop and target are hit within the same bar, the outcome can be resolved in a consistent way that favors the stop or the target according to a single user setting. A short cooldown in bars prevents flip flops. Users can restrict entries to specific sessions such as London and New York. The chart renders entry, stop, and target lines for each trade so that every action is visible. The table in the top right shows trade counts, take profit and stop counts, win rate, average R per trade, and profit factor for the whole set and by direction.

Defaults and responsible backtesting

The default properties in the script use a realistic initial capital and commission value. Users should also set slippage in the strategy properties to reflect their broker and symbol. Small timeframe trading is sensitive to friction and the strategy description does not claim immunity to that reality. The strategy is intended to be tested on a dataset that produces a meaningful sample of trades. A sample in the range of a hundred trades or more is preferred because variance in short samples can be large. On thin symbols or periods with little regular trading, users should either change timeframe, change sessions, or use more selective thresholds so that the sample contains only liquid scenarios.

Universal usage across markets

The strategy is universal by design. It will run and produce lines on any open high low close series on TradingView. The composite entry is made of normalized parts. The regime guards use proportions and bounded measures. The spans use untraded distance and range floors measured in the local price scale. This allows the same logic to function on a currency pair, a commodity, an index future, a stock, or a crypto pair. What changes is calibration.

A safe approach for universal use is as follows.

Start with the default signal length and wick weight.

If the chart prints many weak signals, enable the directional filter and raise the normalized gap threshold slightly.

If the chart is too quiet, lower the adaptive percentile or, with adaptive off, lower the fixed pulse threshold by a small amount.

If stops are too tight in quiet regimes, raise the fallback span multiplier or raise the minimum tick floor in ticks.

If you observe long one sided days, lower the maximum entropy slightly so that entries only occur when directionality is genuine rather than alternating.

Because the logic is bounded and local, these simple steps carry over across symbols. That is why the strategy can be used literally on any asset that you can load on a TradingView chart. The code does not depend on a specific tick size or a specific exchange calendar. It will still remain true that symbols with higher spread or fewer regular trading hours demand stricter thresholds and larger floors.

Suggested parameter ranges for common cases

These ranges are guidelines for one to five minute bars. They are not promises of performance. They reflect the balance between having enough signals to learn from and keeping noise controlled.

Signal length between 18 and 34 for liquid commodities and large capitalization equities.

Wick weight between 0.30 and 0.50 depending on whether you want reversal recognition or close momentum.

Adaptive gate percentile between 85 and 93 when adaptive is enabled. Fixed threshold between 0.10 and 0.18 when adaptive is disabled. Use a non zero floor so very quiet periods still require some energy.

Auction Balance Factor maximum near 0.70 for symbols with clear session bursts. Slightly higher if you prefer to include more balanced prints.

Dispersion band with a lower bound near 0.18 and an upper bound near 0.68 for most session instruments. Tighten the band if you want to skip very bursty days or very flat days.