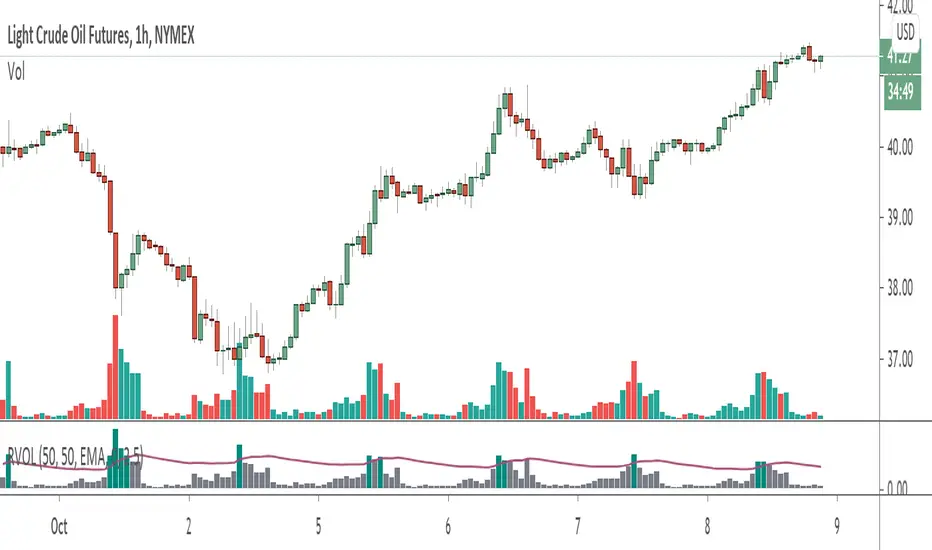

RVOL - R4RocketRelative volume or RVOL for short is an indicator that is used to measure how 'In Play' the stock is. Simply put, it helps to quantify how interested everybody is in the given stock - higher the value, higher the interest and hence higher is the probability for movement in the stock.

I have tried to create RVOL (Relative Volume ) Indicator as per the description that I read on SMB Capital blog. The blog is a great resource.

...................................................................................................................................................................................

How to use the indicator - The indicator is meant for INTRADAY ONLY.

The indicator has following inputs -

1. RVOL Period - Value from 3 to 14 (Default Value = 4)

This is used to calculate the average volume over the given period of days. e.g. average volume for the last 5 days, last 3 days, last 10 days etc. NOTE - If you use higher RVOL Period on smaller timeframes, the code will give an error. So I recommend using 4 or lower for 5 min timeframe. (Nothing will work on 1 min chart and you can experiment for other timeframes.)

2. RVOL Sectional - True / False (Default Value = False)

If you check this box then you will be able to calculate the RVOL for a particular session (or between particular sessions) in that trading day.

What do I mean by session?

Well I have divided the trading day into 6 (almost) equally spaced sessions in time, i.e. 6 hours and 15 mins (for NSE - India) of trading day is divided into 1 hr - 1st session, 1 hr - 2nd session, 1 hr - 3rd session, 1 hr - 4th session, 1 hr - 5th session, 1 hr and 15 min - 6th session.

Before using 3rd and 4th inputs of indicator, RVOL Sectional box MUST BE CHECKED FIRST.

3. RVOL From Session - 1 to 6 (Default Value = 1)

4. RVOL To Session - 1 to 6 (Default Value = 2)

Now if you select 2 in "RVOL From Session" input and 3 in "RVOL To Session" input, the indicator will calculate RVOL for the 2nd and 3rd hour of the trading day. If you select 3 in both the inputs, then the indicator will give RVOL for the 3rd hour of the trading day.

5. RVOL Trigger - 0.2 to 10 (Default Value = 2)

Filter to find days having RVOL above that value. The indicator turns green (or colour of your choice) when RVOL is more than "RVOL Trigger".

...................................................................................................................................................................................

Hope this indicator will add some value in your trading endeavor.

“Only The Game, Can Teach You The Game” – Jesse Livermore

Yours sincerely,

R4Rocket

**If you have some awesome idea for improvement of the indicator - request you to update the code and share the same.

Relative

Volume Columns w. Alerts (V) [LucF]These are volume columns on steroids, for serious volume users. You can use the indicator to show volume columns or relative volume. You can define alerts using numerous conditions in both column and relative modes simultaneously. Multiple coloring schemes allow you to reveal volume columns in a much more useful light than the two-color standard.

Features

Seven Color Schemes

Plain gray.

Different color for columns above average MA.

Standard green and red.

Color gradient using the relative position of MA (default mode).

The first 3 schemes allow for highlighting increasing volume columns.

A gray column in an otherwise colored scheme indicates no change in price.

Two Modes

Column Mode: In this mode you can show the volume MA and mask the columns under it. The standard is an EMA because I think it better suits volume’s quick changes, but you can change it to the usual simple MA, as well as define its length.

Relative Volume: Calculations have been kept rudimentary. Current volume is simply compared to the previous bar’s volume. In order to compensate for this, a multiple area mode also compares current volume to 5, 15, 50 and 200 periods MAs. You can choose to view only the main relative volume value. Relative volume is capped in order to prevent the loss of detail caused by wild increases. The default cap is 10, but you can define your own. Spikes that are capped show a dot at their top. A separate threshold (its default value is the standard 2) is included for relative volume; it is used to generate relative volume markers.

Four Markers

Bumps (marker 1): A bump occurs when an increasing volume column is above its MA and the candle’s close is above/below the previous close.

Double Bumps (marker 2): A double bump occurs when 2 bumps are present in the last 3 bars.

Volume Over MA (marker 3): Triggers whenever volume is above MA. This is the noisiest of the markers.

Relative Volume (marker 4): This event occurs when relative volume crosses the pre-defined threshold.

You can choose to only show long or short markers.

Two Backgrounds

You can choose to highlight the background on bumps and double bumps.

Alerts

You can define alerts on any combination of markers you configure. After defining the markers you want the alert to trigger on, make sure you are on the interval you want the alert to be monitoring at, then create the alert, select V, use the default “Configured Markers” alert condition and choose your triggering window (usually “Once Per Bar Close”). Once the alert is created, you can change the indicator's inputs with no effect on the alert.

No worthwhile price movement exists without volume. It thus makes sense to define alerts on volume if you want to monitor markets. I use the markers to define two types of alerts. For general market scanning, I use markers 2 and 4 on high time frames. When I have identified a good opportunity for entry and am waiting for confirmation, I will often setup a custom alert for that market at a shorter time interval using markers 1 and 4.

Notes

Until we have access to delta volume information on TradingView, this indicator tries to get the most out of volume columns without using security calls at inside intervals to get more resolution on volume, because it slows things down considerably.

The chart shows different combinations of color schemes and markers, along with my TLD indicator on the chart.

Volume+ (RVOL/Alerts)This indicator colors the volume bars based on any of the three follow criteria:

- Volume Amount

- RVOL (Relative Volume)

- Lookback (Highest Over Period)

You can use one, two or all three of these settings at the same time.

You can also set alerts with this indicator. The script will trigger an alert whenever any of the three specified flags are triggered.

RVOL is calculated as: Volume divided by Moving Average value. You can change the moving average period (and type) in the settings.

Dorsey InertiaThis indicator was originally developed by Donald Dorsey (Stocks & Commodities, V.13:9 (September, 1995): "Refining the Relative Volatility Index").

Inertia is based on Relative Volatility Index (RVI) smoothed using linear regression.

In physics, inertia is the tendency of an object to resist to acceleration. Dorsey chose this name because he believes that trend and inertia are related and that it takes more effort and energy to reverse the direction of a stock or market than to keep it in the same direction. He argues that the volatility is the simplest and most accurate measure of inertia.

When the indicator is below 50, it signals bearish market sentiment and when the indicator is above 50 it signals a bullish trend.

Good luck!

Weekly & Daily Percantage Price OscillatorMy first script.

By Vitali Apirine. Technical Analysis of Stocks & Commodities ( February 2018, Vol.36 Issue 2). Thank you.

Mansfield Relative Strength indicatorUse this indicator to compare how security is performing in compare with preferred index (SPX by default).

> 0 outperforming

< 0 underperforming

Works best for weekly, but can be applied to monthly and daily charts. It will be rather useless to use it in smaller timeframes

Apply it to SPX, industry index, sector index or other security in similar sector

Normalized Average True Range (NATR) (Volatility) [cI8DH]As you can see in the chart below, regular ATR is not useful for long term analysis. Normalizing it, fixes the issue. This indicator can be used to measure absolute volatility. It has a built-in stochastic as well for relative volatility. ATR counts high and low in the equation unlike Bolinger Band Width.

Stochastic:

Volume/Rsi Overbought/oversoldI present you my last indicator. A volume indicator that indicates overbought and oversold based on the rsi, I chose the rsi because the most used surment, this indicator allows you to identify the overbought and oversold areas of the rsi with the colors blue (oversold) and orange (overbought ) on the volume indicator! Hoping that you are useful

Relative StrengthRelative strength is a ratio between two assets, most often a stock and a market average (index). This implementation uses the method described here and the second method described here to calculate its value: "To calculate the relative strength of a particular stock, divide the percentage change over some time period by the percentage change of a particular index over the same time period". This indicator oscillates around zero. If the value is greater than zero, the investment has been relatively strong during the selected period; if the value is less than zero, the investment has been relatively weak. The period and the comparative symbol can be set in the settings for the indicator (the defaults are 50 and SPX), there you can also find an option to turn on a moving average.

Relative Vigor Index with Dominant Cycle Detection (RVI)Relative Vigor Index with Dominant Cycle Detection. As Ehler's mentioned, fixed length look back is inherently flawed when it is possible to extract a length from a dominant price cycle. may be less effective if signal to noise ratio is greater than 2, but that usually would not happen at >5m candles, and honestly shouldn't be looking at RV(igor)I when price is moving sideways.

Read just like an RVGI, but adjusted to the current time frame. To reduce noise, changing to heiken ashi will help with signals as well. Let me know if there are improvements!

Made for JD, the OG.

Rapid RSIRapid RSI indicator script. This indicator was originally developed by Ian Copsey (Stocks & Commodities V. 24:10 (16-23): Forex Focus).

Relative Momentum IndexRelative Momentum Index indicator script. This indicator was originally developed by Roger Altman (Stocks & Commodities V. 11:2 (57-60)).

RMI with momentum period of 1 will be equal to an RSI when they have the same period and source price.

Normalized Relative Vigor IndexThis is the Relative Vigor Index indicator just multiplied by 100 to have non-zero integer part

STAN WEINSTEIN RS INDEX WITH NIFTYThis is an indicator for Indian markets.

It shows the relative strength of particular stock to the underlying index.

The concept of this indicator is well described in Stan Weinstein's book.

AJCrows RSIRelative Strength Index with indicator lines at 20, 30, 50, 70 and 80 marks. Use settings to show/hide these lines, and to choose appropriate colors.

Currency Relative Strengths V.2 [GM]Version 2 Updates

Speed has been increased by ~7X

Highest and lowest pairs now highlighted using brighter colors

Re-ordered pairs from highest to lowest 'flight to risk' rating

I created this tool for the purpose of determining strongest and weakest currencies over different periods of time. Each major currency is compared to the field of other majors and its average change is measured over a predetermined period of time. The result is displayed as a percentage. I use it for trend following but it can also be used to fade exhaustion.

Instructions

Add indicator to chart

Select a time frame under settings

Place cursor over period of interest

Click "Data Window" on right hand side bar

View % change avg values for each currency

Relative Strength of 2 securities - Jayy This is an update of the Relative Strength to index as used by Leaf_West.. 4th from the top. my original RS script is 3rd from the top.

In this use of the term " Relative Strength" (RS) what is meant is a ratio of one security to another.

The RS can be inerpreted in a fashion similar to price action on a regual security chart.

If you follow his methods be aware of the different moving averages for the different time periods.

From Leaf_West: "on my weekly and monthly R/S charts, I include a 13 EMA of the R/S (brown dash line) and

an 8 SMA of the 13 EMA (pink solid line). The indicator on the bottom of the weekly/monthly charts is an

8 period momentum indicator of the R/S line. The red horizontal line is drawn at the zero line.

For daily or 130-minute time periods (or shorter), my R/S charts are slightly different

- the moving averages of the R/S line include a 20EMA (brown dash line), a 50 EMA (blue dash line) and

an 8 SMA of the20 EMA (pink solid line). The momentum indicator is also slightly different from the weekly/monthly

charts – here I use a 12 period calculation (vs 8 SMA period for the weekly/monthly charts)."

Leaf's website has gone but I if you are interested in his methods message me.

What is different from my previous RS: The RS now displays RS candles. So if you prefer to watch price action of candles to

a line chart which only plots the ratio of closes then this will be more interesting to you.

I have also thrown in a few options to have fun with.

Jayy

Relative Strength Index on TranquilizersSome weeks ago, I had a patient in my practice who suffered from internal stability disorders.

Certainly not a case of disordered thinking or schizophrenic behaviour, because his general sense of direction wasn’t the problem.

He just couldn’t find the right overall balance, an ailment he struggled with for years.

Straight away I could diagnose that surgery wasn’t an option, so I gave him a medicine he would clearly benefit from.

I never heard from him again…. He must be doing just fine.

Cheers, Indicat...

Momentum of Relative strength to Index Leaf_West styleMomentum of Relative Strength to index as used by Leaf_West. This is to be used with the companion Relative Strength to Index indicator Leaf_West Style. Make sure you use the same index for comparison. If you follow his methods be aware of the different moving averages for the different time periods. From Leaf_West: "on my weekly and monthly R/S charts, I include a 13 EMA of the R/S (brown dash line) and an 8 SMA of the 13 EMA (pink solid line). The indicator on the bottom of the weekly/monthly charts is an 8 period momentum indicator of the R/S line. The red horizontal line is drawn at the zero line.

For daily or 130-minute time periods (or shorter), my R/S charts are slightly different - the moving averages of the R/S line include a 20EMA (brown dash line), a 50 EMA (blue dash line) and an 8 SMA of the20 EMA (pink solid line). The momentum indicator is also slightly different from the weekly/monthly charts – here I use a 12 period calculation (vs 8 SMA period for the weekly/monthly charts)." Leaf's methods do evolve and so watch for any changes to the preferred MAs etc..

Relative strength to Index set up as per Leaf_WestRelative Strength to index as used by Leaf_West. If you follow his methods be aware of the different moving averages for the different time periods. From Leaf_West: "on my weekly and monthly R/S charts, I include a 13 EMA of the R/S (brown dash line) and an 8 SMA of the 13 EMA (pink solid line). The indicator on the bottom of the weekly/monthly charts is an 8 period momentum indicator of the R/S line. The red horizontal line is drawn at the zero line.

For daily or 130-minute time periods (or shorter), my R/S charts are slightly different - the moving averages of the R/S line include a 20EMA (brown dash line), a 50 EMA (blue dash line) and an 8 SMA of the20 EMA (pink solid line). The momentum indicator is also slightly different from the weekly/monthly charts – here I use a 12 period calculation (vs 8 SMA period for the weekly/monthly charts)." Leaf's methods do evolve and so watch for any changes to the preferred MAs etc..

[RS][JR]RSI Donchian ChannelsRSI Donchian Channels

Built by Ricardo and JR

Here is a great indicator to use for strong trends. Donchian Channels react immediately to changes in the highest high and lowest low. For strong trends you want to trade when RSI is set along the upper or lower DC-RSI envelope. When the RSI releases from the DC-RSI envelope, you can take the trade off.

Multi Timeframe RSIThis will show you the RSI of the higher timeframes (up to 1D). Current Timeframe is colored red, higher timeframes are colored from light gray to darker gray (you can change that).

There are several ways to enter a trade:

1. look for rising RSI on higher timeframe (line is stepping up in indicator window), wait for current RSI to decline to oversold (with length 14 its below 30), look for a buy entry (vice versa for a sell setup)

2. look for all RSI timeframes to decline to oversold, this is a good zone to enter a buy (vice versa for a sell setup)

Keep in Mind that a Stochastic Indicator can have it's High/Low befor Price will have it.

Good Luck :)

Relative Momentum Index The Relative Momentum Index (RMI) was developed by Roger Altman. Impressed

with the Relative Strength Index's sensitivity to the number of look-back

periods, yet frustrated with it's inconsistent oscillation between defined

overbought and oversold levels, Mr. Altman added a momentum component to the RSI.

As mentioned, the RMI is a variation of the RSI indicator. Instead of counting

up and down days from close to close as the RSI does, the RMI counts up and down

days from the close relative to the close x-days ago where x is not necessarily

1 as required by the RSI). So as the name of the indicator reflects, "momentum" is

substituted for "strength".