Equity Trade Risk ManagerEquity Trade Risk Manager is a simple indicator that helps you protect your portfolio by going into each trade risk first !

Equity Trade Risk Manager does this by calculating your ideal position size or ideal stop loss based on your account size, purchase price and risk tolerance. This ensures you are never risking more than your predetermined amount on each trade.

Unlike most position size calculators, that will only tell traders how many shares to purchase, Equity Trade Risk Manger allows the trader to choose whether they want to calculate the ideal number of shares to purchase or where to set the trades stop loss based on the number of shares owned. Not only that, but knowing traders need to act fast, the indicator also gives the option to quickly use the current price and low of the day as an entry and stop. Lastly, your stop loss will be plotted onto the chart for a visual aid.

Features:

Dynamic Risk Settings:

Account Customization: Input your account size to get metrics tailored to you.

Calculation Choices: Decide if you want the tool to calculate the number of shares you should buy or where to set your stop-loss.

Custom Risk Parameters: Use preset risk percentages or set your own to match your comfort level.

Price Point Flexibility:

Enter your entry and stop price or opt to use the current price and the low of the day.

Interactive Display Settings:

Customizable Interface: Adjust table positions, text size, and color schemes to match your trading dashboard aesthetic.

On-Chart Stop-Loss Indication: Visualize your stop loss on the chart itself.

Get a snapshot of your dollar risk, position size, shares to buy, and stop-loss.

Risk

Position and Risk Calculator (for Indices) [dR-Algo]Position and Risk Calculator : Your Ultimate Risk Management Tool for Indices

The difference between a novice and a seasoned trader often comes down to one essential element: risk management. While trading indices, the challenges are even more intense due to market volatility and leverage. The Position and Risk Calculator steps in here to bridge the gap, providing you with an efficient tool designed exclusively for indices trading.

Key Features:

User-Friendly Interface: Designed to integrate effortlessly with your TradingView chart, this tool's interface is intuitive and clutter-free.

Dynamic Price Level Adjustment: Move your Entry, Stop Loss, and Take Profit levels directly on the chart for an interactive experience.

Account Balance Input: Customize the tool to understand your unique financial situation by inputting your current account balance.

Trade Risk Customization: Define how much you're willing to risk per trade, and the tool will do the rest.

Automated Calculations: The indicator calculates the maximum monetary risk and translates it into the maximum lot size you can afford. It delivers a full-integer lot size to make your trading decisions easier.

Comprehensive Risk Evaluation: Beyond lot sizes, it provides you with the Cost-to-Reward Ratio (CRV) of your trade, the actual monetary risk according to the calculated lot size, and the potential profit.

How To Use:

Once you add the Position and Risk Calculator to your TradingView chart, a new interactive panel appears. Here’s how it works:

Set Price Levels: Using draggable lines on the chart, set your Entry Price, Stop Loss, and Take Profit levels.

Account Details: Go to settings and enter your Account Balance and your desired risk percentage per trade.

Automatic Calculations: As soon as the above details are set, the indicator goes to work. It first calculates your maximum risk in monetary terms and then translates that into the maximum lot size you can take for the trade.

Review and Trade: The indicator shows you all the vital statistics - CRV of the trade, the money at risk according to the calculated lot size, and the possible profit.

Why Choose This Tool?

Informed Decisions: Your trading decisions will be based on concrete numbers, removing guesswork.

Time-saving: No need for manual calculations or using separate tools; everything is in one place.

Focus on Trading: By automating the risk management aspect, this tool allows you to focus more on your trading strategy and market analysis.

Tailor-Made for Indices: Unlike many other tools that try to serve all markets, the Position and Risk Calculator is designed specifically for indices trading.

Remember, effective risk management is what separates successful traders from those who burn out. The Position and Risk Calculator not only helps you define your risk but also helps you understand it, empowering you to trade with confidence.

So why not give yourself the best chance of success? Add the Position and Risk Calculator to your TradingView setup and experience the difference it can make.

Pinescript Risk Reward boxes + Custom 'Time Elapsed' MarkersUsing Pinescript to create custom Risk Reward Ratio (RRR) boxes with custom vertical time markers to help traders stay mindful of how long they've been in a trade.

//Usage:

-Add indicator to chart and you'll be prompted to click three times:

-- 1: Choose time (clicking last bar will mark entry as current candle's open).

-- 2: Click BOX TOP of RRR box on chart (long or short is toggled later).

-- 3: Click BOX BOTTOM of RRR box on chart (long or short is toggled later).

- then toggle Long or short in the dialog box.

-toggle on/off vertical time line markers (as reminder of how long you've been sat in your trade).

-User input choice of time line marker spacings (in minutes).

//Notes:

-Percentage reward and percentage risk are displayed in each of the risk reward boxes. Risk-Reward ratio is also displayed in the upper box.

-Bars to extend the RRR box to the right is also a custom user input.

-Note the 'entry' of the trade will always be the open of the candle you click on (the first click on loading the indicator).

-You can drag the vertical entry time and the horizontal box-top and box-bottom times dynamically, as you like, as trade progresses.

//Use-Case:

-I wanted a RRR box which gave me custom vertical time markers to keep me mindful of overstaying my welcome in a trade that likely was running out of steam and wasn't likely to go my way. Forcing me to stay nimble. I have found in daytrading that if a trade doesn't go your way promptly, it's often not a good one to hold.

Risk Reward Calculator [lovealgotrading]

OVERVIEW:

This Risk Reward Calculator strategy can help you maximize your RR value with help of algorithmic trading.

INDICATOR:

I wanted to setup my trades more easier with this indicator, I didn't want to calculate everytime before orders, with help this indicator we can calculate R:R value, avarage price, stoploss price, take-profit price, order prices, all position cost and more ...

Our strategy is a risk revard calculation indicator that is made easy to use by using visualized lines and panels, and also has algorithmic trading support.

With the help of this indicator, we can quickly and easily calculate our risk reward values and enter the positions.

If we want to ensure that our balance grows regularly while trading in the stock market, we need to manage the risks and rewards otherwise we may fall below our initial balance at the end of the day, even if we seem to be winning.

What is the Risk-Reward value ?

This value is a value that shows how many times the amount of risk we take when entering the position is successful, we will earn.

- For example, you risked $100 while entering the trade, so if your trade stops, you will lose 100 $.

Your Risk-Reward(RR) value is 2 means that if your position is successful, you will have 200 $ in your pocket.

A trader's success is determined by the amount of R he earns monthly or yearly, not how much money he makes.

What is different in this indicator ?

I want to say thank you to © EvoCrypto. His Calculator (weighted) – evo indicator helped me when I was developed my indicator.

I want to explain what I have improved:

1-In this strategy, we can determine the time period in which we want to open our positions.

2-We can open a maximum of 4 positions in the same direction and close our positions at a single level. StopLoss or TakeProfit

3-This indicator, which works in the form of a strategy, shows where our positions have been opened or closed. With the help of this, it helps us to determine our strategy in our future positions more accurately.

4-The most important improvement is that we do not miss our positions with the help of alarms (WEB HOOK). if we want, we receive by quickly connecting all these positions to our robot, the software can enter and exit the position while we are busy.

IMPLEMENTATION DETAILS – SETTINGS:

1 - We can set the start and end dates of the positions we will take.

2- We can set our take profit, stoploss levels.

3- If your trade is stopped, we can determine the amount of the trade that we will lose.

4- We can adjust our entry levels to positions and our position sizes at entry levels.

(Sum of positions weight must be 100%)

5- We can receive our positions even if we are busy with the help of algorithmic trading. For this, we must paste our Jshon codes into the fields specified in the settings panel.

6- Finally, we can change the settings we want and don't want to have in our visual elements.

Let's make a LONG side example together

We have determined our positions to enter stoploss, take profit and long positions. We did not forget to set the start time of our strategy

Our strategy appear on the graph as follows.

Our strategy has calculated the total position size, our R-R value, the distance of the current price to the stop and take profit levels, in short, a lot of things we could look visually.

Notes:

If you're going to connect this bot to an automatic Long or Short direction,

Don’t forget! you need to Webhook URL,

Don’t miss paste this code to your message window {{strategy.order.alert_message}}

ALSO:

If you have any ideas what to add to my work to add more sources or make calculations cooler, feel free to write me.

Mason’s Line IndicatorThe Macon Strategy is an idea conceived by Didier Darcet , co-founder of Gavekal Intelligence Software. Inspired by the Water Level, an instrument used by masons to check the horizontality or verticality of a wall. This method aims to measure the psychology of financial markets and determine if the market is balanced or tilting towards an unfavorable side, focusing on the behavioral risk of markets rather than economic or political factors.

The strategy examines the satisfaction and frustration of investors based on the distance between the low and high points of the market over a period of one year. Investor satisfaction is influenced by the current price of the index and the path taken to reach that price. The distance to the low point provides satisfaction, while the distance to the high point generates frustration. The balance between the two dictates investors’ desire to hold or sell their positions.

To refine the strategy, it is important to consider the opinion of a group of investors rather than just one individual. The members of a hypothetical investor club invest successively throughout the past year. The overall satisfaction of the market on a given day is a democratic expression of all participants.

If the overall satisfaction is below 50%, investors are frustrated and sell their positions. If it is above, they are satisfied and hold their positions. The position of the group of investors relative to the high and low points represents the position of the air bubble in the water level. Market performance is measured day by day based on participant satisfaction or dissatisfaction.

In conclusion, memory, emotions, and decision-making ability are closely linked, and their interaction influences investment decisions. The Macon Strategy highlights the importance of the behavioral dimension in understanding financial market dynamics. By studying investor behavior through this strategy, it is possible to better anticipate market trends and make more informed investment decisions.

Presentation of the Mason’s Line Indicator:

The main strategy of this indicator is to measure the average satisfaction of investors based on the position of an imaginary air bubble in a tube delimited by the market’s highs and lows over a given period. After calculating the satisfaction level, it is then normalized between 0 and 1, and a moving average can be used to visualize trends.

Key features:

Calculation of highs and lows over a user-defined period.

Determination of the position of the air bubble in the tube based on the closing price.

Calculation of the average satisfaction of investors over a selected period.

Normalization of the average satisfaction between 0 and 1.

Visualization of normalized or non-normalized average satisfaction levels, as well as their corresponding moving averages.

User parameters:

Period for min and max (days) : Sets the period over which highs and lows will be calculated (1 to 365 days).

Period for average satisfaction (days) : Determines the period over which the average satisfaction of investors will be calculated (1 to 365 days).

Period for SMA : Sets the period of the simple moving average used to smooth the data (1 to 1000 days).

Bubble_value : Adjustment of the air bubble value, ranging from 0 to 1, in increments of 0.025.

Normalized average satisfaction : Option to choose whether to display the normalized or non-normalized average satisfaction.

Please note that the Mason’s Line Indicator is not a guarantee of future market performance and should be used in conjunction with proper risk management. Always ensure that you have a thorough understanding of the indicator’s methodology and its limitations before making any investment decisions. Additionally, past performance is not indicative of future results.

Modified Mannarino Market Risk Indicator MMMRI MMRIModified Mannarino Market Risk Indicator MMMRI was developed by "Nobody Special Finance" as an enhancement to the original MMRI developed by Gregory Mannarino. The original and modified version were created as a way to gauge current level of risk in the market. This published indicator includes both versions along with ability to customize the symbols, denominators, and ratio factors that are used within their formulas. Additional options have been included to colorize the candles, plot, and level fills, as well as the option to show or hide a table containing the realtime values for both versions, along with the current dollar strength and 10Y yield.

Levels of market risk are denoted by dashed lines which represent the following levels: 0-50 slight risk, 50-100 low risk, 100-200 moderate risk, 200-300 high risk, 300+ extreme risk. The plot displays whichever of the following two formulas has been selected in the indicator settings, the default choice has been set to MMMRI:

MMRI = (USD Strength * USD Interest Rate) / 1.61

MMMRI = (Debt / GDP) * (USD Strength * USD Interest Rate) / 1.61

NOTICE: This is an example script and not meant to be used as an actual strategy. By using this script or any portion thereof, you acknowledge that you have read and understood that this is for research purposes only and I am not responsible for any financial losses you may incur by using this script!

Short Term Bubble RiskThis risk indicator uses the extension of the closing price to the 20W SMA and displays a color-coded risk oscillator. The higher the oscillator is, the greater the short-term risk and vice-versa. This indicator has historically worked well for estimating the short-term risk of Bitcoin and Ethereum on a weekly timeframe.

TSG 5% Daily CalculatorThis is a calculator I've created to help visualize Target and Risk Levels based on leverage use to trade crypto.

How to use it ?

Basic Use:

- Set the Direction of your trade - either Long or Short

- Set the Leverage you use in your trade - it is crutial to define the risk and target levels

- Set the Risk Amount you want to risk (in %) of your total balance ( Advised 2-3% )

- Set the Target Amount you want to profit at the target (the idea of this is 5% daily, so 5%).

- Set Entry Price if you have opened a position, and you will visually see your progress. Otherwise the levels will be adjusted to the Close of the candle.

Additions:

- Set your Initial Balance - to help you visualize on the Table your progress

- Set your Current Balance - for visualization purposes on ongoing trades and on the Table

- Entry Date - Advised to set it when you open a trade - you will be tracking the progress of your trade since the candle on which you opened it

- Show Table - to show the table of 5% daily and the target it is set on per day

- Table Size - Set table to be small or normal

- Together with the Table you have a big blue area behind that ends on the day you will become a Millionaire based on the Initial Balance, Current balance and Target % in your inputs

RISK MANAGEMENTHi dear Traders,

Here I would present you my 'Risk Management' tool which is based on your buy orders, trading fees and your desired benefit.

Easily, fulfill the price and volume of each entries. Add to this, you can prepare the info about your next proposed entries, just let them not check at first and by meeting the prices then active the check-box beside it.

Two line will be presented on your candle-plot, one of the indicate the place that without any lose/win you can exit and also the desired exit position by considering user defined benefit.

Use it for free but please do not forget to boost the script.

Best regards and happy trading.

Shakib

Basic Position Calculator (BPC)In trading, proper position sizing is essential to managing risk and maximizing returns. The script provided is a Basic Position Calculator that allows traders to quickly and easily calculate their position size, stop loss, take profit, and risk reward ratio for a given trade.

The script starts by defining several inputs for the user to customize the calculations. The first input is the "Account Size", which specifies the total amount of funds available for the trade. The next input is "Risk Amount %", which is the percentage of the account size that the trader is willing to risk per trade. The "Stop Loss" input specifies the maximum amount of loss that the trader is willing to accept, while the "Reward" input is the desired profit target for the trade. Finally, there is a "Position" input that allows the user to specify where on the chart the table of calculations will be displayed.

The script then calculates the position size, stop loss, take profit and risk reward ratio using the user-specified inputs. The position size is calculated by dividing the risk amount by the stop loss. The stop loss is calculated by multiplying the stop loss percentage by the close price, and the take profit is calculated by multiplying the stop loss percentage by the close price and the reward. Risk-reward ratio is the ratio of amount of profit potential to the amount of risk in a trade.

The script then creates a table and displays the calculated values on the chart at the specified location. The table includes the following information: account size, position size, account risk %, stop loss, stop loss %, take profit, take profit % and risk reward ratio. This allows the trader to quickly and easily see all the key calculations for their trade in one place.

Overall, the Basic Position Calculator script is a valuable tool for any trader looking to quickly and easily calculate their position size, stop loss, take profit, and risk reward ratio for a given trade. The ability to customize the inputs and display the calculations on the chart makes it a useful and user-friendly tool for managing risk and maximizing returns.

Super 8 - 30M BTCWelcome to Super 8, the ultimate automatic trading script for Pine!

This bad boy is designed to go both long and short, and it's equipped with all the tools you need to maximize your profits. Whether you're looking to take profit, set a trailing stop, or protect yourself with a stop loss, Super 8 has you covered.

But that's not all! Super 8 is also loaded with 8 powerful indicators to help you make informed decisions. We've got the EMA, ADX, SAR, MACD, VOLUME, BOLLINGER BANDS, DONCHIAN, and ATR all working together to give you the best possible trading experience.

And if you want to take it to the next level, Super 8 also has a feature that lets you use stepped entries in normal mode or incremental 1,2,3,... to improve your average price. Plus, if you're using trailing stop, you can activate the Backtest precision to use lower timeframes.

But what's in a name? Super 8 is called that because it's just that... super! It's tailored specifically for the OKX:BTCUSDT.P pair, so you know you're getting the best possible results. it's highly adjustable and can be used with any other pair. So no matter what market you're trading in, Super 8 has got you covered.

So if you want to level up your trading game, give Super 8 a try. You won't be disappointed.

Certain Risks of Live Algorithmic Trading:

Backtesting Cannot Assure Actual Results.

The relevant market might fail or behave unexpectedly.

Your broker may experience failures in its infrastructure, fail to execute your orders in a correct or timely fashion or reject your orders.

The system you use for generating trading orders, communicating those orders to your broker, and receiving queries and trading results from your broker may fail.

Time lag at various point in live trading might cause unexpected behavior.

The systems of third parties in addition to those of the provider from which we obtain various services, your broker, and the applicable securities market may fail or malfunction.

Position Size ToolUpdated - Version 2

This tool is used to calculate the size of a trade.

Settings - Type in total account size and % of capital that can be risked on each trade.

The table will display:

Column 1 - Stop placement based on low, mid or high value of the current candle.

Column 2 - Percent risk on the trade.

Column 3 - Amount of shares that can be traded (calculated from account size, risk and selected stop placement).

Green color is intended for long position, stop at the low of the candle.

Red color is intended for short position, stop at the high of the candle.

Middle value can shift between either color since its measured from open to close.

FBMAEN:

TradingView indicator for FBMA strategy

People oftem ask: “Dmitry, BABA, TSLA, AAPL flies like a rocket! Well, what are we buying!?” - And I say no, the price does not act like a straight rocket upwards or downwards, instead it breathes, inhales moving away from the moving average and exhales returning to it, so we will wait for the first pullback and buy exactly at the value of the moving average.

Your new paradigm: wait for the stock to pull back to the moving average rather than chasing the price

And one more thing... Remember, you don't want to buy a stock when it's going down, you'll start to have doubts. it's against human nature to go long when the price is falling, but that's why this strategy works so well. We buy on the price rollback (pullback to the moving average), but we DO IT WHILE FOLLOWING THE TREND.

The biggest consequence of this strategy, my author's FBMA strategy and this is a game changer (results are in the comments).

So, let's dive into FBMA indicator settings:

Main settings

ATR Period — Period of intergrated ATR Indicator(shows ATR in a small dashboard);

Settings of Moving Averages

Sign Moving Averages? — shows values of moving averages near their lines on the chart;

Fix MAs' signatures overlapping? — automatically MAs' signatures overlapping (specifically for SMAs and EMAs!) ;

Fix MAs' signatures overlapping between SMAs and EMAs? — automatically group overlapping between EMAs' and SMAs' signatures;

Min distance between MAs' signatures (in % of ATR) — minimal distance between MAs' signatures that indicator will push away MAs' signatures from each other if they are overlapped;

Dashboard

Dashboard position — position of dashboard on the chart ( 9 options ).

Settings of MAs

Source;

Period;

Option for showing EMA and/or SMA of chosen period and source;

Line colour ;

Signature colour .

Addons

Show data by selected timeframe? — shows difference of current price opening and opening a "timeframe" time ago;

Shows MAs only if asset has grown by selected growth % in selected timeframe?

Growth, % — percent, which asset has to gain in order for MAs to be plotted;

Timeframe — frequency with which price's current and previous opening are being will be compared;

Show analog MAs' signatures? — shows MAs' value in a small table;

Show cloud between 1st and 2nd MAs? — shows cloud for both EMAs and SMAs simultaneously).

Price Action

This settings are intuitively understandable

Feel free to leave your questions or suggestions in the comments!

* Price Action-section was taken from ChrisMoody's CM_Price_Action and rebuilt.

RU:

Индикатор TradingView для стратегии ПООС

Мне часто пишут в личку: “Дмитрий, BABA, TSLA , AAPL летит ракетой! Ну что покупаем!?”- А я говорю нет, цена не летит по прямой ракетой вверх, она дышит, делает вдохи отдаляясь от скользящей и выдохи возвращаясь к ней, поэтому мы дождёмся первого пуллбэка и купим точно на значении скользящей

Ваша новая парадигма: ждать акцию на пуллбэке к скользящей по тренду, а не гнаться за ценой

И ещё… Помните, вы не захотите покупать акцию в момент, когда она падает, вы начнете сомневаться т.к. это против человеческой природы заходить в лонг при падении цены, но именно поэтому эта стратегия работает так эффективно, т.к. мы покупаем на откате цены (пуллбэке к скользящей), но ПО ТРЕНДУ

Самое большее следствие из этой стратегии, моя авторская стратегия ПООС и это гейм-чейнджер (результаты в комментариях).

Итак, давайте посмотрим сами настройки индикатора:

Основные настройки

ATR Period — период интегрированного индикатора ATR (показывает ATR на небольшой панели);

Настройки скользящих средних

Sign Moving Averages? — показывает значения скользящих средних рядом с их линиями на графике;

Исправить перекрытие сигнатур МА? — автоматически сигнатуры СС перекрываются (специально для SMA и EMA!) ;

Исправить перекрытие сигнатур МА между SMA и EMA? — автоматически группировать перекрытие между сигнатурами EMA и SMA;

Минимальное расстояние между сигнатурами скользящих средних (в % от ATR) — минимальное расстояние между сигнатурами скользящих средних, при котором индикатор будет отталкивать сигнатуры скользящих средних друг от друга, если они перекрываются;

Панель управления

Dashboard position — положение таблицы на графике ( 9 вариантов ).

Настройки МА

Source;

Период;

Опция отображения EMA и/или SMA выбранного периода и source;

Цвет линии ;

Цвет подписи .

Дополнения

Показать данные по выбранному таймфрейму? — показывает разницу текущей цены открытия и цены открытия в прошлом, по времени равному величины параметра "Таймфрейм";

Показывает MA только в том случае, если актив вырос на выбранный % роста за выбранный период времени?

Прирост, % — процент, на который актив должен набраться, чтобы скользящие средние были построены;

Таймфрейм — частота, с которой будет сравниваться текущее и предыдущее открытие цены;

Показать сигнатуры аналоговых МА? — показывает значение МА в небольшой таблице;

Показать облако между 1-й и 2-й скользящими средними? — показывает облако для EMA и SMA одновременно).

Price Action

Эти настройки будут интуитивно понятны

Оставляете свои вопросы и предложения в комментариях, всё учтём!

* Price Action-section was taken from ChrisMoody's CM_Price_Action and rebuilt.

Turtle Money ManagementThe Turtle Trading approach* is a trend following system that uses volatility for position size. *(Richard Dennis & William Eckhardt )

Turtle traders use the N unit system for risk management, which has its own advantages. This indicator offers beginners a simple interface that uses the same logic. Using ATR (Average True Range) to measure volatility.

The indicator shows the suggested position size and stop-loss price. You need to activate position line to see how it behaved in the past. Information about the Turtle system shows that it works in a daily candle. Intraday candles can be misleading (for ATR) because of this indicator use daily ATR by default. I leave the choice to you.

Limits recommended by Turtle Traders

-

Single Trade % 2 Maximum risk

Single Market % 4 Maximum risk

Closely Correlated Markets % 6 Maximum risk

Loosely Correlated Markets % 10 Maximum risk

Single Direction – Long or Short % 12 Maximum risk

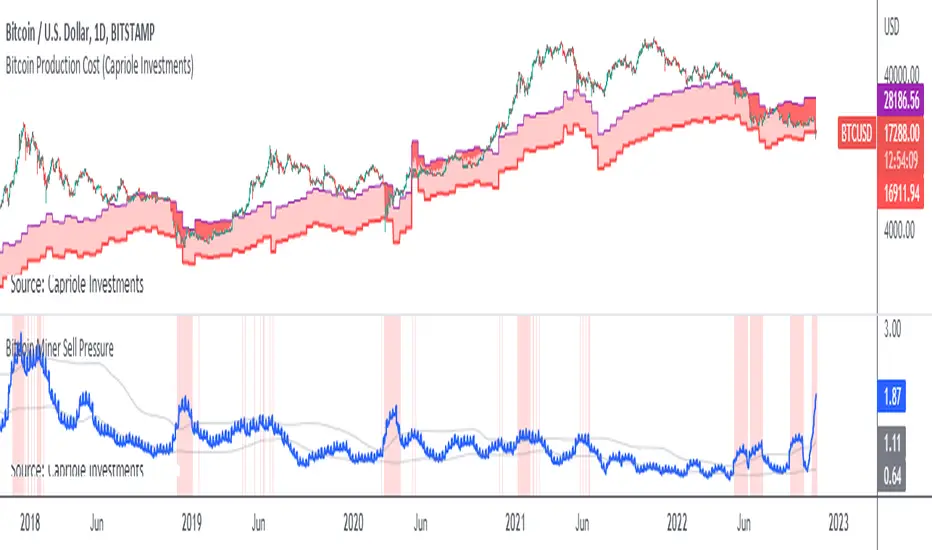

Bitcoin Miner Sell PressureBitcoin miners are in pain and now (November 2022) selling more than they have in almost 5 years!

Introducing: Bitcoin Miner Sell Pressure.

A free, open-source indicator which tracks on-chain data to highlight when Bitcoin miners are selling more of their reserves than usual.

The indicator tracks the ratio of on-chain miner Bitcoin outflows to miner Bitcoin reserves.

- Higher = more selling than usual

- Lower = less selling than usual

- Red = extraordinary sell pressure

Today , it's red.

What can we see now ?

Miners are not great at treasury management. They tend to sell most when they are losing money (like today). But there have been times when they sold well into high profit, such as into the 2017 $20K top and in early 2021 when Bitcoin breached $40K.

Bitcoin Miner Sell Pressure identifies industry stress, excess and miner capitulation.

Unsurprisingly, there is a high correlation with Bitcoin Production Cost; giving strong confluence to both.

In some instances, BMSP spots capitulation before Hash Ribbons. Such as today!

Parametric VaRValue at Risk can also be computed parametrically using a method known as variance/co-variance VaR. This method allows you to simulate a range of possibilities based on historical return distribution properties rather than actual return values. It's actually more accurate even though it assumes a normal distribution especially when not much data is available

Trend & atr day & calcHi!

Why for what and how in this script?

At the time of publication the script consists of three modules, it may increase in the future.

1. Bottom left corner : daytime ATR module

(idea and basis of the author's script - ???)

- The size of the daily ATR based on 14 bars;

- intraday ATR progress;

- colour indication of the progress status, for easier visual perception (green < 70%, yellow 70-90 and red over 90% of ATR)

By evaluating the progress of the daily ATR, it is possible to suggest and expedient to enter/exit/hold a trade.

2. Top right: trend module

The trend is calculated based on Bill Williams' alligator indicator

- trend status on specified timeframes for the current ticker;

- colour indication for visual perception (green - growing trend, yellow - alligator is sleeping, red - downtrend)

Do not forget that the alligator is based on moving averages with the resulting consequences.

Its purpose is to assess the state of the trend on other ticker TFs, without additional actions (switching to another screen or TF)

3. In the bottom left corner - risk and position calculator

(based on an idea of the risk calculator by @andrei.bunulu)

It helps to determine the advisability of entering the trade and also what size position to enter into the trade, within money management strategy chosen.

- The calculator works in two directions: long deal and short deal (short deal calculation is enabled by check-box in settings)

- two calculation methods:

a. based on the set stop loss % (default is 0.3%), in this mode the stop and takeout level is automatically calculated (default is 1 / 3).

b. by entering the desired price levels (entry, stop and take profit points)

To make this work correctly please do not forget to choose the type of calculation (% or price) in the settings, and the currency symbol (for visual representation in the results).

The calculator can take into account the set commissions and spreads.

When hovering over the module - tooltips are displayed.

Each module can be enabled / disabled in the settings.

The size and arrangement of the modules is made for joint use with the script - "Abnormal Bar".

/// а по-русски это так ///

Привет!

Зачем для чего и как в этом скрипте?

На момент публикации скрипт состоит из трех модулей, возможно в будущем увеличится.

1. В левом нижнем углу : модуль дневного ATR

(идея и основа скрипт автора - ???)

- размер дневной ATR на основании 14 баров;

- прогресс ATR внутри дня;

- цветовая индикация состояния прогресса, для более простого визуального восприятия (зеленый < 70%, желтый 70-90 и красный более 90% ATR)

Оценивая прогресс дневного ATR, можно предположить и целесообразности входа / выхода / удержания из сделки.

2. В правом верхнем углу: модуль тренда

Тренд рассчитывается на основе индикатора - аллигатор Билла Вильямса

- состояние тренда на указанных таймфреймах для текущего тикера;

- цветовая индикация для визуального восприятия (зеленый - растущий тренд, желтый - аллигатор спит, красный - нисходящий тренд)

Не забываем, что аллигатор построен на основе скользящих средних с вытекающими последствиями.

Назначение - оценить состояние тренда на других ТФ тикера, без дополнительных действий (переключения на другой экран или ТФ)

3. В нижнем левом углу - калькулятор рисков и позиции

(на основе идеи калькулятора аuthor: @andrei.bunulu)

Помогает определить целесообразность входа в сделку, а также каким размером позиции входить в сделку, в рамках выбранной стратегии мани менеджмента.

- калькулятор работает в два направления: длинная и короткая сделка (расчет по короткой включается в настройках чек-боксом)

- два варианта расчета:

а. на основании установленного % стоп лосса (по-умолчанию 0,3%), при этом режиме происходит автоматический расчет уровня стопа и тейка (по умолчанию 1 / 3).

b. путем ввода данных желаемых уровней цены (точки входа, стопа и тейк профита)

Для корректной работы не забываем в настройках выбирать тип расчета (% или цена), а также символ валюты (для визуального отображения в итогах).

Калькулятор может учитывать установленный размер комиссий и спреда.

При наведении на модуль - отображаются подсказки.

Каждый модуль можно включить / выключить в настройках.

Размер и расположение модулей сделано для совместного использования со скриптом - "Abnormal Bar"

VIX - SKEW DivergenceThe CBOE VIX is a well-known index representing market expectations for volatility over the next 30 days.

The CBOE SKEW is an index reflecting the perceived tail risk over the next 30 days.

When the SKEW rises over a certain level (~140/150), that means investors are hedging their exposure with options, because they are worried about an incoming market crash or a "black swan". If that happens when the VIX is very low and apparently there is no uncertainty, this can warn of a sudden change in direction of the market. You will see for yourself that an increasing divergence often anticipates a sharp fall of leading stock indexes, usually within two to four months.

This is probably not very relevant for the short-term trader but mid/long-term traders and market analysts may find it useful to clearly visualize the extent of the distance between the VIX and the SKEW. For that reason, I wrote this highly customizable script with which you can plot the two indexes and fill the space within them with a color gradient to highlight the maximum and minimum divergence. Additionally, you can fill the beneath VIX area with four different colors. It is also possible to plot the divergence value itself, so if you want you can draw trendlines and support/resistance levels on it.

Please note that the divergence per se doesn't predict anything and it's meant to be used synergistically with other technical analysis tools.

More informations here:

www.cboe.com

www.cboe.com

Value At Risk Channel [AstrideUnicorn]The Value at Risk Channel (VaR Channel) is a trading indicator designed to help traders control the level of risk exposure in their positions. The user can select a time period and a probability value, and the indicator will plot the upper and lower limits that the price can reach during the selected time period with the given probability.

CONCEPTS

The indicator is based on the Value at Risk (VaR) calculation. VaR is an important metric in risk management that quantifies the degree of potential financial loss within a position, portfolio or company over a specific period of time. It is widely used by financial institutions like banks and investment companies to forecast the extent and likelihood of potential losses in their portfolios.

We use the so-called “historical method” to compute VaR. The algorithm looks at the history of past returns and creates a histogram that represents the statistical distribution of past returns. Assuming that the returns follow a normal distribution, one can assign a probability to each value of return. The probability of a specific return value is determined by the distribution percentile to which it belongs.

HOW TO USE

Let’s assume you want to plot the upper and lower limits that price will reach within 4 hours with 5% probability. To do this, go to the indicator Settings tab and set the Timeframe parameter to "4 hours'' and the Probability parameter to 5.0.

You can use the indicator to set your Stop-Loss at the price level where it will trigger with low probability. And what's more, you can measure and control the probability of triggering.

You can also see how likely it is that the price will reach your Take-Profit within a specific period of time. For example, you expect your target level to be reached within a week. To determine this probability, set the Timeframe parameter to "1 week" and adjust the Probability parameter so that the upper or lower limit of your VaR channel is close to your Take-Profit level. The resulting Probability parameter value will show the probability of reaching your target in the expected time.

The indicator can be a useful tool for measuring and managing risk, as well as for developing and fine-tuning trading strategies. If you find other uses for the indicator, feel free to share them in the comments!

SETTINGS

Timeframe - sets the time period, during which the price can reach the upper or lower bound of the VaR channel with the probability, set by the Probability parameter.

Probability - specifies the probability with which the price can reach the upper or lower bound of the VaR channel during the time period specified by the Timeframe parameter.

Window - specifies the length of history (number of historical bars) used for VaR calculation.

Position Size Calc. (Minimalist)This is a simplified position size calculator in the form of a table.

The reason I published this script is because all other position size calculator scripts try to provide way too much when it should be much simpler, position in strange areas of the chart and leave unwanted chart pollution.

This is a bare-bones functional table that takes your risk level, entry, stop and take profit as inputs, and calculates your loss, profit and required position size for your chosen risk level as a result.

Inspired by a table type position size calculator made by DojiEmoji design/color-wise. Functionally different however.

I hope you find this script useful and include it on your trading journey.

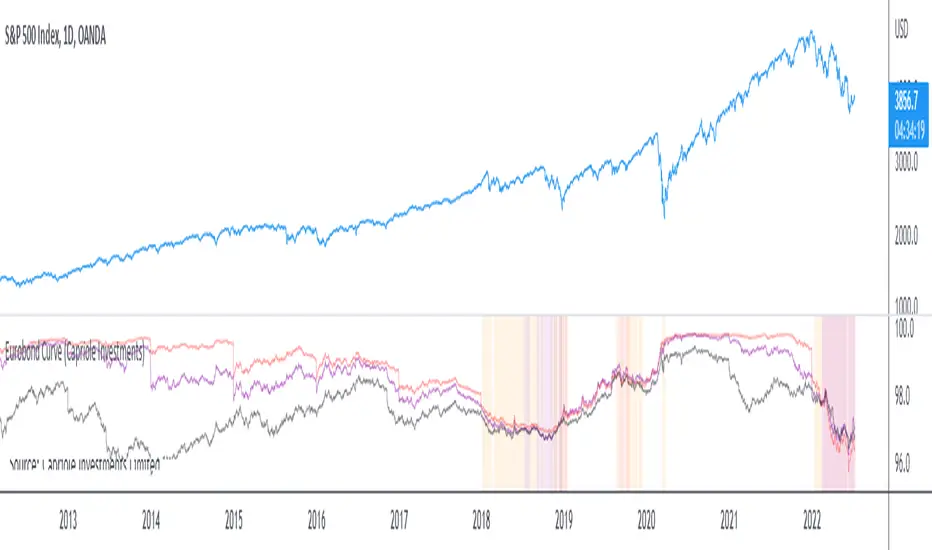

Eurobond CurveABOUT

Dynamically plots 3 no. forward EUROBOND curves. When the curves converge (or worse crossover) there is higher risk of financial uncertainty and potential market correction.

The Eurobond Curves work in a similar way to treasury "yield curve inversion"; except the EUROBOND curves can signal much earlier than Treasuries therefore providing a leading indicator.

The indicator looks the the "near" (next year EUROBOND), "mid" (EUROBOND 2 years out) and "far" (EUROBOND 5 years out) to assess for crossovers.

When the "near" and "mid" curves crossover the "far" curve, concerning economic conditions are developing and it may be a good idea to reduce risk exposure to markets.

LIMITATIONS

The EUROBOND curve crossover events are rare, and this indicator uses data back to 2005 (using approximately 25 TradingView security functions). Given there are relatively few crossover events, the reliability of this indicator should be considered low. Nonetheless, there is decent alignment with treasury yield curve inversions in the 20 year period assessed. Given treasury yield curve inversions have predicted every recession for the last 70 years, we still think the EUROBOND Curves are a useful datapoint to monitor into the future and provide confluence to other risk management strategies.

Koalafied Risk ManagementTables and labels/lines showing trade levels and risk/reward. Use to manage trade risk compared to portfolio size.

Initial design optimised for tickers denominated against USD.

trailing_drawdown

Description:

Drawdown was a tool to measure historical risk, derived from measuring current wealth from its previous peak, casually from portfolio construction (weights allocation), will consider to having a minimum drawdown. In this indicator, the drawdown for individual assets is utilized to measure its value or percentage from its trailing peak (default to 1-yr period).

Drawdown:

drawdown = (price/peaks)-1

Feature:

Static: display drawdown as percentage

Dynamic: display drawdown as value