Realtime Position CalculatorRisk management is the single most important factor in trading success. This indicator automates the process of position sizing in real-time based on your account risk and a dynamic technical Stop Loss. It eliminates the need for manual calculations and helps you execute trades faster while adhering to strict risk management rules.

How it Works

The indicator visually places a Stop Loss line based on recent market structure (Highs/Lows) and instantly calculates the required position size (Contracts/Lots) to match your defined monetary risk.

1. Dynamic Stop Loss : It identifies the highest high (for Shorts) or lowest low (for Longs) over a user-defined lookback period.

2. Position Calculation : It calculates the distance between the current price and the Stop Loss level.

3. Formula : Contract Size = Risk Amount / (Distance * Point Value)

4. Actual vs. Target Risk : Because of the rounding, the script calculates and displays the Actual Risk (e.g., $95) alongside your Target Risk (e.g., $100), so you know exactly what is at stake.

Key Features

Real-time Calculation : Updates instantly as price moves.

Copy Trading Support : Includes an "Account Multiplier" setting. If you trade 10 accounts via a copy trader, set the multiplier to 10. The indicator will show the total contract size needed across all accounts.

Point Value Support : Works for Stocks/Crypto (Point Value = 1) and Futures (e.g., ES = 50, NQ = 20).

Customizable UI : Toggle specific data on/off in the label (e.g., hide price, show only contracts). Adjustable label offset to keep the chart clean.

Settings Guide

Trade Direction : Toggle between Long and Short setups. Add the indicator two times and set another for Longs and another for Shorts so you can see both direction at the same time.

Risk Amount : Your max risk in currency (e.g., $100).

Lookback : How many bars back to look for the SL pivot (e.g., 10 bars).

Point Value : Crucial for Futures. Use 1.0 for Crypto/Stocks. Use tick value/point value for futures (e.g., 50 for ES).

Account Multiplier : Multiply the position size for multiple accounts.

Label Offset : Move the information label to the right to avoid overlapping with price action.

Disclaimer

This tool is for informational and educational purposes only. Always verify calculations manually before executing trades. Past performance is not indicative of future results.

Riskmangement

Adaptive Risk Management [sgbpulse]1. Introduction:

Adaptive Risk Management is an advanced indicator designed to provide traders with a comprehensive risk management tool directly on the chart. Instead of relying on complex manual calculations, the indicator automates all critical steps of trade planning. It dynamically calculates the estimated Entry Price , the Stop Loss location, the required Position Size (Quantity) based on your capital and risk limits, and the three Take Profit targets based on your defined Reward/Risk ratios. The indicator displays all these essential data points clearly and visually on the chart, ensuring you always know the potential risk-reward profile of every trade.

ARM : The A daptive R isk M anagement every trader needs to ARM themselves with.

2. The Critical Importance of Risk Management

Proper risk management is the cornerstone of successful trading. Consistent profitability in the market is impossible without rigorously defining risk limits.

Risk Control: This starts by setting the maximum risk amount you are willing to lose in a single trade (Risk per Trade), and limiting the total capital allocated to the position (Max Capital per Trade).

Defining Boundaries (Stop Loss & Take Profit): It is mandatory to define a technical Stop Loss and a Take Profit target. A fundamental rule of risk management is that the Reward/Risk Ratio (R/R) must be a minimum of 1:1.

3. Core Features, Adaptivity, and Customization

The Adaptive Risk Management indicator is engineered for use across all major trading styles, including Swing Trading, Intraday Trading, and Scalping, providing consistent risk control regardless of the chosen timeframe.

Real-Time Dynamic Adaptivity: The indicator calculates all risk management parameters (Entry, Stop Loss, Quantity) dynamically with every new bar, thus adapting instantly to changing market conditions.

Trend Direction Adjustment: Define the analysis direction (Long/Uptrend or Short/Downtrend).

Intraday Session Data Control: Full control over whether lookback calculations will include data from Extended Trading Hours (ETH), or if the daily calculations will start actively only from the first bar of Regular Trading Hours (RTH).

Status Validation: The indicator performs critical status checks and displays clear Warning Messages if risk conditions are not met.

4. Intuitive Visualization and Real-Time Data

Dynamic Tracking Lines: The Entry Price and Stop Loss lines are updated with every new bar. Crucially, the length of these lines dynamically reflects the calculation's lookback range (e.g., the extent of Lookback Bars or the location of the confirmed Pivot Point), providing a visual anchor for the calculated price.

Risk and Reward Zones: The indicator creates a graphical background fill between Entry and Stop Loss (marked with the risk color) and between Entry and the Reward Targets (marked with the reward color).

Essential Information Labels: Labels are placed at the end of each line, providing critical data: Estimated Entry Price, Stock/Contract Quantity (Quantity), Total Entry Amount, Estimated Stop Loss, Risk per Share, Total Financial Risk (Risk Amount), Exit Amount, Estimated Take Profit 1/2/3, Reward/Risk Ratio 1/2/3, Total Reward 1/2/3, TP Exit Amount 1/2/3.

4.1. Data Window Metrics (16 Full Series)

The indicator displays 16 full data series in the TradingView Data Window, allowing precise tracking of every calculation parameter:

Entry Data: Estimated Entry, Quantity, Entry Amount.

Risk Data (Stop Loss): Estimated Stop Loss, Risk per Share, Risk Amount, Exit Amount.

Reward Data (Take Profit): Estimated Take Profit 1/2/3, Reward/Risk Ratio 1/2/3, Total Reward 1/2/3, TP Exit Amount 1/2/3.

4.2. Instant Tracking in the Status Line

The indicator displays 6 critical parameters continuously in the indicator's Status Line: Estimated Entry, Quantity, Estimated Stop Loss, Estimated Take Profit 1/2/3.

5. Detailed Indicator Inputs

5.1 General

Focused Trend: Defines the analysis direction (Uptrend / Downtrend).

Max Capital per Trade: The maximum amount allocated to purchasing stocks/contracts (in account currency).

Risk per Trade: The maximum amount the user is willing to risk in this single trade (in account currency).

ATR Length: The lookback period for the Average True Range (ATR) calculation.

5.2 Intraday Session Data Control

Regular Hours Limitation : If enabled, all daily lookback calculations (for Entry/Stop Loss anchor points) will begin strictly from the first Regular Trading Hours (RTH) bar. This limits the lookback range to the current RTH session, excluding preceding Extended Trading Hours (ETH) data. Only relevant for Intraday charts. Default: False (Off)

5.3 Entry Inputs

Entry Method: Selects the entry price calculation method:

Current Price: Uses the closing price of the current bar as the estimated entry point (Market Entry).

ATR Real Bodies Margin :

- Uptrend: Calculates the Maximum Real Body over the lookback period + the calculated safety margin.

- Downtrend: Calculates the Minimum Real Body over the lookback period - the calculated safety margin.

ATR Bars Margin :

- Uptrend: Calculates the Maximum High price over the lookback period + the calculated safety margin.

- Downtrend: Calculates the Minimum Low price over the lookback period - the calculated safety margin.

Lookback Bars: The number of bars used to calculate the extremes in the ATR-based entry methods (Relevant only for ATR Real Bodies Margin and ATR Bars Margin methods).

ATR Multiplier (Entry): The multiplier applied to the ATR value. The result of the multiplication is the calculated safety margin used to determine the estimated Entry Price.

5.4 Risk Inputs (Stop Loss)

Risk Method: Selects the Stop Loss price calculation method.

ATR Current Price Margin :

- Uptrend: Entry Price - the calculated safety margin.

- Downtrend: Entry Price + the calculated safety margin.

ATR Current Bar Margin :

- Uptrend: Current Bar's Low price - the calculated safety margin.

- Downtrend: Current Bar's High price + the calculated safety margin.

ATR Bars Margin :

- Uptrend: Lowest Low over lookback period - the calculated safety margin.

- Downtrend: Highest High over lookback period + the calculated safety margin.

ATR Pivot Margin :

- Uptrend: The first confirmed Pivot Low point - the calculated safety margin.

- Downtrend: The first confirmed Pivot High point + the calculated safety margin.

Lookback Bars: The lookback period for finding the extreme price used in the 'ATR Bars Margin' calculation.

ATR Multiplier (Risk): The multiplier applied to the ATR value. The result of the multiplication is the calculated safety margin used to place the estimated Stop Loss. Note: If set to 0, the Stop Loss will be placed exactly at the technical anchor point, provided the Minimum Margin Value is also 0.

Minimum Margin Value: The minimum price value (e.g., $0.01) the Stop Loss margin buffer must be.

Pivot (Left / Right): The number of bars required on either side of the pivot bar for confirmation (relevant only for the ATR Pivot Margin method).

5.5 Reward Inputs (Take Profit)

Show Take Profit 1/2/3: ON/OFF switch to control the visibility of each Take Profit target.

Reward/Risk Ratio 1/ 2/ 3: Defines the R/R ratio for the profit target. Must be ≥1.0.

6. Indicator Status/Warning Messages

In situations where the Stop Loss location cannot be calculated logically and validly, often caused by a mismatch between the configured Focused Trend (Uptrend/Downtrend) and the actual price action, the indicator will display a warning message, explaining the reason and suggesting corrective action.

Status Message 1: Pivot reference unavailable

Condition: The Stop Loss is set to the "ATR Pivot Margin" method, but the anchor point (Pivot) is missing or inaccessible.

Message Displayed: "Pivot reference unavailable. Wait for valid price action, or adjust the Regular Hours Limitation setting or Pivot Left/Right inputs."

Status Message 2: Calculated Stop Loss is unsafe

Condition: The calculated Stop Loss is placed illogically or unsafely relative to the trend direction and the Entry price.

Message Displayed: "Calculated Stop Loss is unsafe for current trend. Wait for valid price action or adjust SL Lookback/Multiplier."

7. Summary

The Adaptive Risk Management (ARM) indicator provides a seamless and systematic approach to trade execution and risk control. By dynamically automating all critical trade parameters—from Entry Price and Stop Loss placement to Position Sizing and Take Profit targets—ARM removes emotional bias and ensures every trade adheres strictly to your predefined risk profile.

Key Benefits:

Systematic Risk Control: Strict enforcement of maximum capital allocation and risk per trade limits.

Adaptivity: Dynamic calculation of prices and quantities based on real-time market data (ATR and Lookback).

Clarity and Trust: Clear on-chart visualization, precise data metrics (16 series), and unambiguous Status/Warning Messages ensure transparency and reliability.

ARM allows traders to focus on strategy and analysis, confident that their execution complies with the core principles of professional risk management.

Important Note: Trading Risk

This indicator is intended for educational and informational purposes only and does not constitute investment advice or a recommendation for trading in any form whatsoever.

Trading in financial markets involves significant risk of capital loss. It is important to remember that past performance is not indicative of future results. All trading decisions are your sole responsibility. Never trade with money you cannot afford to lose.

Gyspy Bot Trade Engine - V1.2B - Alerts - 12-7-25 - SignalLynxGypsy Bot Trade Engine (MK6 V1.2B) - Alerts & Visualization

Brought to you by Signal Lynx | Automation for the Night-Shift Nation 🌙

1. Executive Summary & Architecture

Gypsy Bot (MK6 V1.2B) is not merely a strategy; it is a massive, modular Trade Engine built specifically for the TradingView Pine Script V6 environment. While most tools rely on a single dominant indicator to generate signals, Gypsy Bot functions as a sophisticated Consensus Algorithm.

Note: This is the Indicator / Alerts version of the engine. It is designed for visual analysis and generating live alert signals for automation. If you wish to see Backtest data (Equity Curves, Drawdown, Profit Factors), please use the Strategy version of this script.

The engine calculates data from up to 12 distinct Technical Analysis Modules simultaneously on every bar closing. It aggregates these signals into a "Vote Count" and only fires a signal plot when a user-defined threshold of concurring signals is met. This "Voting System" acts as a noise filter, requiring multiple independent mathematical models—ranging from volume flow and momentum to cyclical harmonics and trend strength—to agree on market direction.

Beyond entries, Gypsy Bot features a proprietary Risk Management suite called the Dump Protection Team (DPT). This logic layer operates independently of the entry modules, specifically scanning for "Moon" (Parabolic) or "Nuke" (Crash) volatility events to signal forced exits, preserving capital during Black Swan events.

2. ⚠️ The Philosophy of "Curve Fitting" (Must Read)

One must be careful when applying Gypsy Bot to new pairs or charts.

To be fully transparent: Gypsy Bot is, by definition, a very advanced curve-fitting engine. Because it grants the user granular control over 12 modules, dozens of thresholds, and specific voting requirements, it is extremely easy to "over-fit" the data. You can easily toggle switches until the charts look perfect in hindsight, only to have the signals fail in live markets because they were tuned to historical noise rather than market structure.

To use this engine successfully:

Visual Verification: Do not just look for "green arrows." Look for signals that occur at logical market structure points.

Stability: Ensure signals are not flickering. This script uses closed-candle logic for key decisions to ensure that once a signal plots, it remains painted.

Regular Maintenance is Mandatory: Markets shift regimes (e.g., from Bull Trend to Crab Range). Gypsy Bot settings should be reviewed and adjusted at regular intervals to ensure the voting logic remains aligned with current market volatility.

Timeframe Recommendations:

Gypsy Bot is optimized for High Time Frame (HTF) trend following. It generally produces the most reliable results on charts ranging from 1-Hour to 12-Hours, with the 4-Hour timeframe historically serving as the "sweet spot" for most major cryptocurrency assets.

3. The Voting Mechanism: How Entries Are Generated

The heart of the Gypsy Bot engine is the ActivateOrders input (found in the "Order Signal Modifier" settings).

The engine constantly monitors the output of all enabled Modules.

Long Votes: GoLongCount

Short Votes: GoShortCount

If you have 10 Modules enabled, and you set ActivateOrders to 7:

The engine will ONLY plot a Buy Signal if 7 or more modules return a valid "Buy" signal on the same closed candle.

If only 6 modules agree, the signal is rejected.

4. Technical Deep Dive: The 12 Modules

Gypsy Bot allows you to toggle the following modules On/Off individually to suit the asset you are trading.

Module 1: Modified Slope Angle (MSA)

Logic: Calculates the geometric angle of a moving average relative to the timeline.

Function: Filters out "lazy" trends. A trend is only considered valid if the slope exceeds a specific steepness threshold.

Module 2: Correlation Trend Indicator (CTI)

Logic: Measures how closely the current price action correlates to a straight line (a perfect trend).

Function: Ensures that we are moving up with high statistical correlation, reducing fake-outs.

Module 3: Ehlers Roofing Filter

Logic: A spectral filter combining High-Pass (trend removal) and Super Smoother (noise removal).

Function: Isolates the "Roof" of price action to catch cyclical turning points before standard moving averages.

Module 4: Forecast Oscillator

Logic: Uses Linear Regression forecasting to predict where price "should" be relative to where it is.

Function: Signals when the regression trend flips. Offers "Aggressive" and "Conservative" calculation modes.

Module 5: Chandelier ATR Stop

Logic: A volatility-based trend follower that hangs a "leash" (ATR multiple) from extremes.

Function: Used as an entry filter. If price is above the Chandelier line, the trend is Bullish.

Module 6: Crypto Market Breadth (CMB)

Logic: Pulls data from multiple major tickers (BTC, ETH, and Perpetual Contracts).

Function: Calculates "Market Health." If Bitcoin is rising but the rest of the market is dumping, this module can veto a trade.

Module 7: Directional Index Convergence (DIC)

Logic: Analyzes the convergence/divergence between Fast and Slow Directional Movement indices.

Function: Identifies when trend strength is expanding.

Module 8: Market Thrust Indicator (MTI)

Logic: A volume-weighted breadth indicator using Advance/Decline and Volume data.

Function: One of the most powerful modules. Confirms that price movement is supported by actual volume flow. Recommended setting: "SSMA" (Super Smoother).

Module 9: Simple Ichimoku Cloud

Logic: Traditional Japanese trend analysis.

Function: Checks for a "Kumo Breakout." Price must be fully above/below the Cloud to confirm entry.

Module 10: Simple Harmonic Oscillator

Logic: Analyzes harmonic wave properties to detect cyclical tops and bottoms.

Function: Serves as a counter-trend or early-reversal detector.

Module 11: HSRS Compression / Super AO

Logic: Detects volatility compression (HSRS) or Momentum/Trend confluence (Super AO).

Function: Great for catching explosive moves resulting from consolidation.

Module 12: Fisher Transform (MTF)

Logic: Converts price data into a Gaussian normal distribution.

Function: Identifies extreme price deviations. Uses Multi-Timeframe (MTF) logic to ensure you aren't trading against the major trend.

5. Global Inhibitors (The Veto Power)

Even if 12 out of 12 modules vote "Buy," Gypsy Bot performs a final safety check using Global Inhibitors.

Bitcoin Halving Logic: Prevents trading during chaotic weeks surrounding Halving events (dates projected through 2040).

Miner Capitulation: Uses Hash Rate Ribbons to identify bearish regimes when miners are shutting down.

ADX Filter: Prevents trading in "Flat/Choppy" markets (Low ADX).

CryptoCap Trend: Checks the total Crypto Market Cap chart for broad market alignment.

6. Risk Management & The Dump Protection Team (DPT)

Even in this Indicator version, the RM logic runs to generate Exit Signals.

Dump Protection Team (DPT): Detects "Nuke" (Crash) or "Moon" (Pump) volatility signatures. If triggered, it plots an immediate Exit Signal (Yellow Plot).

Advanced Adaptive Trailing Stop (AATS): Dynamically tightens stops in low volatility ("Dungeon") and loosens them in high volatility ("Penthouse").

Staged Take Profits: Plots TP1, TP2, and TP3 events on the chart for visual confirmation or partial exit alerts.

7. Recommended Setup Guide

When applying Gypsy Bot to a new chart, follow this sequence:

Set Timeframe: 4 Hours (4H).

Tune DPT: Adjust "Dump/Moon Protection" inputs first. These filter out bad signals during high volatility.

Tune Module 8 (MTI): Experiment with the MA Type (SSMA is recommended).

Select Modules: Enable/Disable modules based on the asset's personality (Trending vs. Ranging).

Voting Threshold: Adjust ActivateOrders to filter out noise.

Alert Setup: Once visually satisfied, use the "Any Alert Function Call" option when creating an alert in TradingView to capture all Buy/Sell/Close events generated by the engine.

8. Technical Specs

Engine Version: Pine Script V6

Repainting: This indicator uses Closed Candle data for all Risk Management and Entry decisions. This ensures that signals do not vanish after the candle closes.

Visuals:

Blue Plot: Buy/Sell Signal.

Yellow Plot: Risk Management (RM) / DPT Close Signal.

Green/Lime/Olive Plots: Take Profit hits.

Disclaimer:

This script is a complex algorithmic tool for market analysis. Past performance is not indicative of future results. Cryptocurrency trading involves substantial risk of loss. Use this tool to assist your own decision-making, not to replace it.

9. About Signal Lynx

Automation for the Night-Shift Nation 🌙

Signal Lynx focuses on helping traders and developers bridge the gap between indicator logic and real-world automation. The same RM engine you see here powers multiple internal systems and templates, including other public scripts like the Super-AO Strategy with Advanced Risk Management.

We provide this code open source under the Mozilla Public License 2.0 (MPL-2.0) to:

Demonstrate how Adaptive Logic and structured Risk Management can outperform static, one-layer indicators

Give Pine Script users a battle-tested RM backbone they can reuse, remix, and extend

If you are looking to automate your TradingView strategies, route signals to exchanges, or simply want safer, smarter strategy structures, please keep Signal Lynx in your search.

License: Mozilla Public License 2.0 (Open Source).

If you make beneficial modifications, please consider releasing them back to the community so everyone can benefit.

RiskCraft - Advanced Risk Management SystemRiskCraft – Risk Intelligence Dashboard

Trade like you actually respect risk

"I know the setup looks good… but how much am I actually risking right now?"

RiskCraft is an open-source Pine Script v6 indicator that keeps risk transparent directly on the chart. It is not a signal generator; it is a risk desk that calculates size, frames volatility, and reminds you when your behaviour drifts away from the plan.

Core utilities

Calculates professional-style position sizing in real time.

Reads volatility and market regime before position size is confirmed.

Adjusts risk based on the trader’s emotional state and confidence inputs.

Maps session risk across Asian, London, and New York hours.

Draws exactly one stop line and one target line in the preferred direction.

Provides rotating education tips plus contextual warnings when risk escalates.

It is intentionally conservative and keeps you in the game long enough for any separate entry logic to matter.

---

Chart layout checklist

Use a clean chart on a liquid symbol (e.g., AMEX:SPY or major FX pairs).

Main RiskCraft dashboard placed on the right edge.

Session Risk box on the left with UTC time visible.

Floating risk badge above price.

Stop/target guide lines enabled.

Education panel visible in the bottom-right corner.

---

1. On-chart components

Right-side dashboard : account risk %, position size/value, stop, target, risk/reward, regime, trend strength, emotional state, behavioural score, correlation, and preferred trade direction.

Session Risk box : highlights active session (Asian, London, NY), current UTC time, and risk label (High/Med/Low) per session.

Floating risk badge : keeps actual account risk percent visible with colour-coded wording from Ultra Cautious to Very Aggressive.

Stop/target lines : exactly one dashed stop and one dashed target aligned with the preferred bias.

Education panel : rotates core principles and AI-style warnings tied to volatility, risk %, and behaviour flags.

---

2. Volatility engine – ATR with context 📈

atr = ta.atr(atrLength)

atrPercent = (atr / close) * 100

atrSMA = ta.sma(atr, atrLength)

volatilityRatio = atr / atrSMA

isHighVol = volatilityRatio > volThreshold

ATR vs ATR SMA shows how wild price is relative to recent history.

Volatility ratio above the threshold flips isHighVol , which immediately trims risk.

An ATR percentile rank over the last 100 bars indicates calm versus chaotic regimes.

Daily ATR sampling via request.security() gives higher time-frame context for intraday sessions.

When volatility spikes the script dials position size down automatically instead of cheering for maximum exposure.

---

3. Market regime radar – Danger or Drift 🌊

ema20 = ta.ema(close, 20)

ema50 = ta.ema(close, 50)

ema200 = ta.ema(close, 200)

trendScore = (close > ema20 ? 1 : -1) +

(ema20 > ema50 ? 1 : -1) +

(ema50 > ema200 ? 1 : -1)

= ta.dmi(14, 14)

Regimes covered:

Danger : high volatility with weak trend.

Volatile : volatility elevated but structure still directional.

Choppy : low ADX and noisy action.

Trending : directional flows without extreme volatility.

Mixed : anything between.

Each regime maps to a 1–10 risk score and a multiplier that feeds the final position size. Danger and Choppy clamp size; Trending restores normal risk.

---

4. Behaviour engine – trader inputs matter 🧠

You provide:

Emotional state : Confident, Neutral, FOMO, Revenge, Fearful.

Confidence : slider from 1 to 10.

Toggle for behavioural adjustment on/off.

Behind the scenes:

Each state triggers an emotional multiplier .

Confidence produces a confidence multiplier .

Combined they form behavioralFactor and a 0–100 Behavioural Score .

High-risk emotions or low conviction clamp the final risk. Calm inputs allow normal size. The dashboard prints both fields to keep accountability on-screen.

---

5. Correlation guardrail – avoid stacking identical risk 📊

Optional correlation mode compares the active symbol to a reference (default AMEX:SPY ):

corrClose = request.security(correlationSymbol, timeframe.period, close)

priceReturn = ta.change(close) / close

corrReturn = ta.change(corrClose) / corrClose

correlation = calcCorrelation()

Absolute correlation above the threshold applies a correlation multiplier (< 1) to reduce size.

Dashboard row shows the live correlation and reference ticker.

When disabled, the row simply echoes the current symbol, keeping the table readable.

---

6. Position sizing engine – heart of the script 💰

baseRiskAmount = accountSize * (baseRiskPercent / 100)

adjustedRisk = baseRiskAmount * behavioralFactor *

regimeAdjustment * volAdjustment *

correlationAdjustment

finalRiskAmount = math.min(adjustedRisk,

accountSize * (maxRiskCap / 100))

stopDistance = atr * atrStopMultiplier

takeProfit = atr * atrTargetMultiplier

positionSize = stopDistance > 0 ? finalRiskAmount / stopDistance : 0

positionValue = positionSize * close

Outputs shown on the dashboard:

Position size in units and value in currency.

Actual risk % back on account after adjustments.

Risk/Reward derived from ATR-based stop and target.

---

7. Intelligent trade direction – bias without signals 🎯

Direction score ingredients:

EMA stack alignment.

Price versus EMA20.

RSI momentum relative to 50.

MACD line vs signal.

Directional Movement (DI+/DI–).

The resulting Trade Direction row prints LONG, SHORT, or NEUTRAL. No orders are generated—this is guidance so you only risk capital when the structure supports it.

---

8. Stop/target guide lines – two lines only ✂️

if showStopLines

if preferLong

// long stop below, target above

else if preferShort

// short stop above, target below

Lines refresh each bar to keep clutter low.

When the direction score is neutral, no lines appear.

Use them as visual anchors, not auto-orders.

---

9. Session Risk map – global volatility clock 🌍

Tracks Asian, London, and New York windows via UTC.

Computes average ATR per session versus global ATR SMA.

Labels each session High/Med/Low and colours the cells accordingly.

Top row shows the active session plus current UTC time so you always know the regime you are trading.

One glance tells you whether you are trading quiet drift or the part of the day that hunts stops.

---

10. Floating risk badge – honesty above price 🪪

Text ranges from Ultra Cautious through Very Aggressive.

Colour matches the risk palette inputs (High/Med/Low).

Updates on the last bar only, keeping historical clutter off the chart.

Account risk becomes impossible to ignore while you stare at price.

---

11. Education engine & warnings 📚

Rotates evergreen principles (risk 1–2%, journal trades, respect plan).

Triggers contextual warnings when volatility and risk % conflict.

Flags when emotional state = FOMO or Revenge.

Highlights sub-standard risk/reward setups.

When multiple danger flags stack, an AI-style warning overrides the tip text so you can course-correct before capital is exposed.

---

12. Alerts – hard guard rails 🚨

Excessive Risk Alert : actual risk % crosses custom threshold.

High Volatility Alert : ATR behaviour signals danger regime.

Emotional State Warning : FOMO or Revenge selected.

Poor Risk/Reward Alert : risk/reward drops below your standard.

All alerts reinforce discipline; none suggest entries or exits.

---

13. Multi-market behaviour 🕒

Intraday (1m–1h): session box and badge react quickly; ideal for scalpers needing constant risk context.

Higher time frames (1D–1W): dashboard shifts slowly, supporting swing planning.

Asset classes confirmed in validation: crypto majors, large-cap equities, indices, major FX pairs, and liquid commodities.

Risk logic is price-based, so it adapts across markets without bespoke tuning.

15. Key inputs & recommended defaults

Account Size : 10,000 (modify to match actual account; min 100).

Base Risk % : 1.0 with a Maximum Risk Cap of 2.5%.

ATR Period : 14, Stop Multiplier 2.0, Target Multiplier 3.0.

High Vol Threshold : 1.5 for ATR ratio.

Behavioural Adjustment : enabled by default; disable for fixed risk.

Correlation Check : optional; default symbol AMEX:SPY , threshold 0.7.

Display toggles : main dashboard, risk badge, session map, education panel, and stop lines can be individually disabled to reduce clutter.

16. Usage notes & limits

Indicator mode only; no automated entries or exits.

Trade history panel intentionally disabled (requires strategy context).

Correlation analysis depends on additional data requests and may lag slightly on illiquid symbols.

Session timing uses UTC; adjust expectations if you trade localized instruments.

HTF ATR sampling uses daily data, so bar replay on lower charts may show brief data gaps while HTF loads.

What does everyone think RISK really means?

DCA Ladder CalculatorThis script is a DCA (Dollar-Cost Averaging) Ladder Calculator with Risk & Leverage Management baked in.

It’s designed for both LONG and SHORT positions, and helps you:

🎯 Strategically scale into positions across multiple entry points

🔐 Control risk exposure via defined capital allocation

⚖️ Utilize leverage responsibly — for efficiency, not destruction

🧮 Visualize risk, stop loss level, and entry distribution

🔁 Adapt to trend reversals or key zones, especially when combined with reversal indicators or higher timeframe signals

🧠 How It Works

This tool takes a capital allocation approach to building a ladder of positions:

1. You define:

- Portfolio value

- Risk per trade (as %)

- Leverage

- Number of DCA levels

- Entry multiplier (e.g. 1x, 2x, 4x...)

2. The script then:

- Calculates total margin to risk = Portfolio × Risk %

- Calculates total leveraged position size = Margin × Leverage

- Distributes entries according to exponential weights (1x, 2x, 4x...), totaling 7 for 3 levels

- Calculates per-entry:

- Entry price (based on price zone spacing)

- Multiplier

- Exact margin per entry

- Leverage per entry (margin × leverage)

- Computes:

- Average entry price (margin-weighted)

- Approximate stop loss level based on recent ATR and price structure

- % drawdown to SL

- Total margin and position size

3. Displays all this in a clean on-chart table.

📈 How to Use It

1. Apply the indicator to a chart (default: 1D — ideal for clean zones).

2. Configure your:

- Portfolio Value (total trading capital)

- Risk per Trade (%) (your acceptable loss)

- Leverage (exchange or strategy-based)

- DCA Levels (e.g. 3 = anchor + 2 entries)

- Multiplier (typically 2.0 for doubling)

3. Choose LONG or SHORT mode depending on direction.

4. The table will show:

- Entry price ladder

- Margin used per entry

- Total position size

- Approx. stop loss (where your full risk is defined)

Use in conjunction with price action, S/R zones, trendline breaks, volume divergence, or reversal indicators.

✅ Best Practices for Using This Tool

- Leverage is a tool, not a weapon. Use it to scale smartly — not recklessly.

- Use fewer, higher-conviction entries. Don’t blindly ladder; combine with price structure and signals.

- Stick to your risk percent. Never risk more than you can afford to lose. Let this calculator enforce discipline.

- Combine with other confirmation tools, like RSI divergence, momentum shifts, OB zones, etc.

- Avoid martingale-style over-exposure. This is not a gambling tool — it’s for capital efficiency.

🛡️ What This Tool Does NOT Do

- This is not a trade signal indicator.

- It does not place trades or auto-manage positions.

- It does not replace personal responsibility or strategy — it's a tool to help apply structure.

⚠️ Disclaimer

This script is for educational and informational purposes only.

It does not constitute financial advice, nor is it a recommendation to buy or sell any financial instrument.

Always consult a licensed financial advisor before making investment decisions.

Use of leverage involves high risk and can lead to substantial losses.

The author and publisher assume no liability for any trading losses resulting from use of this script.

SMC Statistical Liquidity Walls [PhenLabs]📊 SMC Statistical Liquidity Walls

Version: PineScript™ v6

📌 Description

The SMC Statistical Liquidity Walls indicator is designed to visualize market volatility and potential reversal zones using advanced statistical modeling. Unlike traditional Bollinger Bands that use simple lines, this script utilizes an “Inverted Sigmoid” opacity function to create a “fog of war” effect. This visualizes the density of liquidity: the further price moves from the equilibrium (mean), the “harder” the liquidity wall becomes.

This tool solves the problem of over-trading in low-probability areas. By automatically mapping “Premium” (Resistance) and “Discount” (Support) zones based on Standard Deviation (SD), traders can instantly see when price is overextended. The result is a clean, intuitive overlay that helps you identify high-probability mean reversion setups without cluttering your chart with manual drawings.

🚀 Points of Innovation

Inverted Sigmoid Logic: A custom mathematical function maps Standard Deviation to opacity, creating a realistic “wall” density effect rather than linear gradients.

Dynamic “Solidity”: The indicator is transparent at the center (Equilibrium) and becomes visually solid at the edges, mimicking physical resistance.

Separated Directional Bias: distinct Red (Premium) and Green (Discount) coding helps SMC traders instantly recognize expensive vs. cheap pricing.

Smart “Safe” Deviation: Includes fallback logic to handle calculation errors if deviation hits zero, ensuring the indicator never crashes during data gaps.

🔧 Core Components

Basis Calculation: Uses a Simple Moving Average (SMA) to determine the market’s equilibrium point.

Standard Deviation Zones: Calculates 1SD, 2SD, and 3SD levels to define the statistical extremes of price action.

Sigmoid Alpha Calculation: Converts the SD distance into a transparency value (0-100) to drive the visual gradient.

🔥 Key Features

Automated Premium/Discount Zones: Red zones indicate overbought (Premium) areas; Green zones indicate oversold (Discount) areas.

Customizable Density: Users can adjust the “Steepness” and “Midpoint” of the sigmoid curve to control how fast the walls become solid.

Integrated Alerts: Built-in alert conditions trigger when price hits the “Solid” wall (2SD or higher), perfect for automated trading or notifications.

Visual Clarity: The center of the chart remains clear (high transparency) to keep focus on price action where it matters most.

🎨 Visualization

Equilibrium Line: A gray line representing the mean price.

Gradient Fills: The space between bands fills with color that increases in opacity as it moves outward.

Premium Wall: Upper zones fade from transparent red to solid red.

Discount Wall: Lower zones fade from transparent green to solid green.

📖 Usage Guidelines

Range Period: Default 20. Controls the lookback period for the SMA and Standard Deviation calculation.

Source: Default Close. The price data used for calculations.

Center Transparency: Default 100 (Clear). Controls how transparent the middle of the chart is.

Edge Transparency: Default 45 (Solid). Controls the opacity of the outermost liquidity wall.

Wall Steepness: Default 2.5. Adjusts how aggressively the gradient transitions from clear to solid.

Wall Start Point: Default 1.5 SD. The deviation level where the gradient shift begins to accelerate.

✅ Best Use Cases

Mean Reversion Trading: Enter trades when price hits the solid 2SD or 3SD wall and shows rejection wicks.

Take Profit Targets: Use the Equilibrium (Gray Line) as a logical first target for reversal trades.

Trend Filtering: Do not initiate new long positions when price is deep inside the Red (Premium) wall.

⚠️ Limitations

Lagging Nature: As a statistical tool based on Moving Averages, the walls react to past price data and may lag during sudden volatility spikes.

Trending Markets: In strong parabolic trends, price can “ride” the bands for extended periods; mean reversion should be used with caution in these conditions.

💡 What Makes This Unique

Physics-Based Visualization: We treat liquidity as a physical barrier that gets denser the deeper you push, rather than just a static line on a chart.

🔬 How It Works

Step 1: The script calculates the mean (SMA) and the Standard Deviation (SD) of the source price.

Step 2: It defines three zones above and below the mean (1SD, 2SD, 3SD).

Step 3: The custom `get_inverted_sigmoid` function calculates an Alpha (transparency) value based on the SD distance.

Step 4: Plot fills are colored dynamically, creating a seamless gradient that hardens at the extremes to visualize the “Liquidity Wall.”

💡 Note

For best results, combine this indicator with Price Action confirmation (such as pin bars or engulfing candles) when price touches the solid walls.

Super-AO with Risk Management Alerts Template - 11-29-25Super-AO with Risk Management: ALERTS & AUTOMATION Edition

Signal Lynx | Free Scripts supporting Automation for the Night-Shift Nation 🌙

1. Overview

This is the Indicator / Alerts companion to the Super-AO Strategy.

While the Strategy version is built for backtesting (verifying profitability and checking historical performance), this Indicator version is built for Live Execution.

We understand the frustration of finding a great strategy, only to realize you can't easily hook it up to your trading bot. This script solves that. It contains the exact same "Super-AO" logic and "Risk Management Engine" as the strategy version, but it is optimized to send signals to automation platforms like Signal Lynx, 3Commas, or any Webhook listener.

2. Quick Action Guide (TL;DR)

Purpose: Live Signal Generation & Automation.

Workflow:

Use the Strategy Version to find profitable settings.

Copy those settings into this Indicator Version.

Set a TradingView Alert using the "Any Alert() function call" condition.

Best Timeframe: 4 Hours (H4) and above.

Compatibility: Works with any webhook-based automation service.

3. Why Two Scripts?

Pine Script operates in two distinct modes:

Strategy Mode: Calculates equity, drawdowns, and simulates orders. Great for research, but sometimes complex to automate.

Indicator Mode: Plots visual data on the chart. This is the preferred method for setting up robust alerts because it is lighter weight and plots specific values that automation services can read easily.

The Golden Rule: Always backtest on the Strategy, but trade on the Indicator. This ensures that what you see in your history matches what you execute in real-time.

4. How to Automate This Script

This script uses a "Visual Spike" method to trigger alerts. Instead of drawing equity curves, it plots numerical values at the bottom of your chart when a trade event occurs.

The Signal Map:

Blue Spike (2 / -2): Entry Signal (Long / Short).

Yellow Spike (1 / -1): Risk Management Close (Stop Loss / Trend Reversal).

Green Spikes (1, 2, 3): Take Profit Levels 1, 2, and 3.

Setup Instructions:

Add this indicator to your chart.

Open your TradingView "Alerts" tab.

Create a new Alert.

Condition: Select SAO - RM Alerts Template.

Trigger: Select Any Alert() function call.

Message: Paste your JSON webhook message (provided by your bot service).

5. The Logic Under the Hood

Just like the Strategy version, this indicator utilizes:

SuperTrend + Awesome Oscillator: High-probability swing trading logic.

Non-Repainting Engine: Calculates signals based on confirmed candle closes to ensure the alert you get matches the chart reality.

Advanced Adaptive Trailing Stop (AATS): Internally calculates volatility to determine when to send a "Close" signal.

6. About Signal Lynx

Automation for the Night-Shift Nation 🌙

We are providing this code open source to help traders bridge the gap between manual backtesting and live automation. This code has been in action since 2022.

If you are looking to automate your strategies, please take a look at Signal Lynx in your search.

License: Mozilla Public License 2.0 (Open Source). If you make beneficial modifications, please release them back to the community!

Position Sizing Calculator (Real-Time) - Futures Edition█ SUMMARY

The following indicator is a Position Sizing Calculator based on Average True Range (ATR), originally developed by market technician J. Welles Wilder Jr., intended for real-time trading.

This script utilizes the user's account size, acceptable risk percentage, and a stop-loss distance based on ATR to dynamically calculate the appropriate position size for each trade in real time.

█ BACKGROUND

Developed for use on the Micro E-mini Nasdaq-100 futures (MNQ), this script provides traders with continuously updated dynamic position sizes. It enables traders to instantly determine the exact number of contracts to use when entering a trade while staying within their acceptable risk tolerance.

This real-time position sizing tool helps traders make well-informed decisions when planning trade entries and calculating maximum stop-loss levels, ultimately enhancing risk management.

█ USER INPUTS

Trading Account Size: Total dollar value of the user's trading account.

Acceptable Risk (%): Maximum percentage of the trading account that the user is willing to risk per trade.

ATR Multiplier for Stop-Loss: Multiplier used to determine the distance of the stop-loss from the current price, based on the ATR value.

ATR Length: The length of the lookback period used to calculate the ATR value.

Show Target Risk Row: Toggle to hide/show the Target Risk Row

SL Levels Display: Option to see Both, Long Only, Short Only, or None of the Stop Loss Level Values.

Contract Point Value ($): Point value per contract. Tooltip highlights common values.

Tick Size: Minimum Price Movement (Default set to 0.25)

Minimum Contracts: Override the Minimum Contracts per trade to a user selected value.

(May Exceed User's Target Risk)

Auto Position CalculatorA position sizing tool that automatically detects the instrument you're trading and calculates the correct position size based on your risk parameters.

What It Does

This indicator calculates how many contracts, lots, or shares to trade based on your account size, risk percentage, and stop loss distance. It auto-detects the instrument type and adjusts the point/pip value accordingly.

Supported Instruments

Futures: NQ, MNQ, ES, MES, YM, MYM, RTY, M2K, CL, MCL, GC, MGC

Forex: All major pairs (USD, EUR, GBP, JPY, etc.)

Index CFDs: NAS100, US500, US30, GER40, UK100

Metals: XAU, XAG

Crypto and Stocks: Automatic detection

How to Use

Set your account size and risk % in settings

Click the settings icon and place Entry, Stop Loss, and Take Profit on the chart

The position size and risk calculations appear automatically

Levels auto-reset at your chosen session (Asia, London, or New York open)

Limitations

CFD and forex pip values assume standard lot sizing - your broker may differ

Auto-detection relies on ticker naming conventions, which vary by broker/data feed

Session reset times are based on ET (Eastern Time)

Micro/Mini P&L [LDT]Overview

Micro/Mini P&L is a risk and P&L visualization tool built primarily for futures traders.

It provides accurate dollar-based calculations for either micros or minis, regardless of which contract type you are currently charting.

The indicator automatically detects your instrument (NQ, MNQ, ES, MES, YM, RTY, CL, GC, etc.) and adjusts point-value data accordingly, allowing you to chart one contract while evaluating risk for another.

This removes the need for manual conversions and keeps your position data consistent at all times.

Although optimized for futures, the tool also works on any other asset for general trade-level visualization.

Features

• Automatic instrument detection for major futures markets including NQ/MNQ, ES/MES, YM/MYM, RTY/M2K, CL/MCL, GC/MGC and others.

Point-value logic adjusts instantly based on the detected symbol ensuring accurate calculations without manual configuration.

• Micro/Mini display toggle, allowing you to calculate dollar values for either contract type regardless of which contract is on your chart.

Useful for traders who prefer charting minis whilst trading micros or the opposite.

• Trade-level visualization, including Entry, Take Profit and Stop Loss levels with automatically drawn lines and optional TP/SL zone shading for clear and structured display on the chart.

• Dynamic P/L calculations, showing both point-based and dollar-based metrics in real time.

This includes TP/SL dollar values, points to target/stop, real-time P/L and an optional risk-reward ratio.

• Adaptive risk table, displaying contract counts from 1 up to your selected maximum, total dollar risk for each row and highlighting your chosen contract size.

This provides a straightforward method for evaluating risk, scaling and position sizing.

• Customizable display options, including color settings, label visibility, extension length, bar offsets and table positioning.

This allows the tool to remain clean, unobtrusive and easy to integrate into any chart layout.

Purpose

This tool is designed to give futures traders a clear, consistent and reliable way to view dollar-accurate risk per contract without performing manual conversions.

Whether you trade micros or minis, the displayed values always align with your selected contract type, even when charting the opposite market.

Luxy BIG beautiful Dynamic ORBThis is an advanced Opening Range Breakout (ORB) indicator that tracks price breakouts from the first 5, 15, 30, and 60 minutes of the trading session. It provides complete trade management including entry signals, stop-loss placement, take-profit targets, and position sizing calculations.

The ORB strategy is based on the concept that the opening range of a trading session often acts as support/resistance, and breakouts from this range tend to lead to significant moves.

What Makes This Different?

Most ORB indicators simply draw horizontal lines and leave you to figure out the rest. This indicator goes several steps further:

Multi-Stage Tracking

Instead of just one ORB timeframe, this tracks FOUR simultaneously (5min, 15min, 30min, 60min). Each stage builds on the previous one, giving you multiple trading opportunities throughout the session.

Active Trade Management

When a breakout occurs, the indicator automatically calculates and displays entry price, stop-loss, and multiple take-profit targets. These lines extend forward and update in real-time until the trade completes.

Cycle Detection

Unlike indicators that only show the first breakout, this tracks the complete cycle: Breakout → Retest → Re-breakout. You can see when price returns to test the ORB level after breaking out (potential re-entry).

Failed Breakout Warning

If price breaks out but quickly returns inside the range (within a few bars), the label changes to "FAILED BREAK" - warning you to exit or avoid the trade.

Position Sizing Calculator

Built-in risk management that tells you exactly how many shares to buy based on your account size and risk tolerance. No more guessing or manual calculations.

Advanced Filtering

Optional filters for volume confirmation, trend alignment, and Fair Value Gaps (FVG) to reduce false signals and improve win rate.

Core Features Explained

### 1. Multi-Stage ORB Levels

The indicator builds four separate Opening Range levels:

ORB 5 - First 5 minutes (fastest signals, most volatile)

ORB 15 - First 15 minutes (balanced, most popular)

ORB 30 - First 30 minutes (slower, more reliable)

ORB 60 - First 60 minutes (slowest, most confirmed)

Each level is drawn as a horizontal range on your chart. As time progresses, the ranges expand to include more price action. You can enable or disable any stage and assign custom colors to each.

How it works: During the opening minutes, the indicator tracks the highest high and lowest low. Once the time period completes, those levels become your ORB high and low for that stage.

### 2. Breakout Detection

When price closes outside the ORB range, a label appears:

BREAK UP (green label above price) - Price closed above ORB High

BREAK DOWN (red label below price) - Price closed below ORB Low

The label shows which ORB stage triggered (ORB5, ORB15, etc.) and the cycle number if tracking multiple breakouts.

Important: Signals appear on bar close only - no repainting. What you see is what you get.

### 3. Retest Detection

After price breaks out and moves away, if it returns to test the ORB level, a "RETEST" label appears (orange). This indicates:

The original breakout level is now acting as support/resistance

Potential re-entry opportunity if you missed the first breakout

Confirmation that the level is significant

The indicator requires price to move a minimum distance away before considering it a valid retest (configurable in settings).

### 4. Failed Breakout Detection

If price breaks out but returns inside the ORB range within a few bars (before the breakout is "committed"), the original label changes to "FAILED BREAK" in orange.

This warns you:

The breakout lacked conviction

Consider exiting if already in the trade

Wait for better setup

Committed Breakout: The indicator tracks how many bars price stays outside the range. Only after staying outside for the minimum number of bars does it become a committed breakout that can be retested.

### 5. TP/SL Lines (Trade Management)

When a breakout occurs, colored horizontal lines appear showing:

Entry Line (cyan for long, orange for short) - Your entry price (the ORB level)

Stop Loss Line (red) - Where to exit if trade goes against you

TP1, TP2, TP3 Lines (same color as entry) - Profit targets at 1R, 2R, 3R

These lines extend forward as new bars form, making it easy to track your trade. When a target is hit, the line turns green and the label shows a checkmark.

Lines freeze (stop updating) when:

Stop loss is hit

The final enabled take-profit is hit

End of trading session (optional setting)

### 6. Position Sizing Dashboard

The dashboard (bottom-left corner by default) shows real-time information:

Current ORB stage and range size

Breakout status (Inside Range / Break Up / Break Down)

Volume confirmation (if filter enabled)

Trend alignment (if filter enabled)

Entry and Stop Loss prices

All enabled Take Profit levels with percentages

Risk/Reward ratio

Position sizing: Max shares to buy and total risk amount

Position Sizing Example:

If your account is $25,000 and you risk 1% per trade ($250), and the distance from entry to stop loss is $0.50, the calculator shows you can buy 500 shares (250 / 0.50 = 500).

### 7. FVG Filter (Fair Value Gap)

Fair Value Gaps are price inefficiencies - gaps left by strong momentum where one candle's high doesn't overlap with a previous candle's low (or vice versa).

When enabled, this filter:

Detects bullish and bearish FVGs

Draws semi-transparent boxes around these gaps

Only allows breakout signals if there's an FVG near the breakout level

Why this helps: FVGs indicate institutional activity. Breakouts through FVGs tend to be stronger and more reliable.

Proximity setting: Controls how close the FVG must be to the ORB level. 2.0x means the breakout can be within 2 times the FVG size - a reasonable default.

### 8. Volume & Trend Filters

Volume Filter:

Requires current volume to be above average (customizable multiplier). High volume breakouts are more likely to sustain.

Set minimum multiplier (e.g., 1.5x = 50% above average)

Set "strong volume" multiplier (e.g., 2.5x) that bypasses other filters

Dashboard shows current volume ratio

Trend Filter:

Only shows breakouts aligned with a higher timeframe trend. Choose from:

VWAP - Price above/below volume-weighted average

EMA - Price above/below exponential moving average

SuperTrend - ATR-based trend indicator

Combined modes (VWAP+EMA, VWAP+SuperTrend) for stricter filtering

### 9. Pullback Filter (Advanced)

Purpose:

Waits for price to pull back slightly after initial breakout before confirming the signal.

This reduces false breakouts from immediate reversals.

How it works:

- After breakout is detected, indicator waits for a small pullback (default 2%)

- Once pullback occurs AND price breaks out again, signal is confirmed

- If no pullback within timeout period (5 bars), signal is issued anyway

Settings:

Enable Pullback Filter: Turn this filter on/off

Pullback %: How much price must pull back (2% is balanced)

Timeout (bars): Max bars to wait for pullback (5 is standard)

When to use:

- Choppy markets with many fake breakouts

- When you want higher quality signals

- Combine with Volume filter for maximum confirmation

Trade-off:

- Better signal quality

- May miss some valid fast moves

- Slight entry delay

How to Use This Indicator

### For Beginners - Simple Setup

Add the indicator to your chart (5-minute or 15-minute timeframe recommended)

Leave all default settings - they work well for most stocks

Watch for BREAK UP or BREAK DOWN labels to appear

Check the dashboard for entry, stop loss, and targets

Use the position sizing to determine how many shares to buy

Basic Trading Plan:

Wait for a clear breakout label

Enter at the ORB level (or next candle open if you're late)

Place stop loss where the red line indicates

Take profit at TP1 (50% of position) and TP2 (remaining 50%)

### For Advanced Traders - Customized Setup

Choose which ORB stages to track (you might only want ORB15 and ORB30)

Enable filters: Volume (stocks) or Trend (trending markets)

Enable FVG filter for institutional confirmation

Set "Track Cycles" mode to catch retests and re-breakouts

Customize stop loss method (ATR for volatile stocks, ORB% for stable ones)

Adjust risk per trade and account size for accurate position sizing

Advanced Strategy Example:

Enable ORB15 only (disable others for cleaner chart)

Turn on Volume filter at 1.5x with Strong at 2.5x

Enable Trend filter using VWAP

Set Signal Mode to "Track Cycles" with Max 3 cycles

Wait for aligned breakouts (Volume + Trend + Direction)

Enter on retest if you missed the initial break

### Timeframe Recommendations

5-minute chart: Scalping, very active trading, crypto

15-minute chart: Day trading, balanced approach (most popular)

30-minute chart: Swing entries, less screen time

60-minute chart: Position trading, longer holds

The indicator works on any intraday timeframe, but ORB is fundamentally a day trading strategy. Daily charts don't make sense for ORB.

DEFAULT CONFIGURATION

ON by Default:

• All 4 ORB stages (5/15/30/60)

• Breakout Detection

• Retest Labels

• All TP levels (1/1.5/2/3)

• TP/SL Lines (Detailed mode)

• Dashboard (Bottom Left, Dark theme)

• Position Size Calculator

OFF by Default (Optional Filters):

• FVG Filter

• Pullback Filter

• Volume Filter

• Trend Filter

• HTF Bias Check

• Alerts

Recommended for Beginners:

• Leave all defaults

• Session Mode: Auto-Detect

• Signal Mode: Track Cycles

• Stop Method: ATR

• Add Volume Filter if trading stocks

Recommended for Advanced:

• Enable ORB15 + ORB30 only (disable 5 & 60)

• Enable: Volume + Trend + FVG

• Signal Mode: Track Cycles, Max 3

• Stop Method: ATR or Safer

• Enable HTF Daily bias check

## Settings Guide

The settings are organized into logical groups. Here's what each section controls:

### ORB COLORS Section

Show Edge Labels: Display "ORB 5", "ORB 15" labels at the right edge of the levels

Background: Fill the area between ORB high/low with color

Transparency: How see-through the background is (95% is nearly invisible)

Enable ORB 5/15/30/60: Turn each stage on or off individually

Colors: Assign colors to each ORB stage for easy identification

### SESSION SETTINGS Section

Session Mode: Choose trading session (Auto-Detect works for most instruments)

Custom Session Hours: Define your own hours if needed (format: HHMM-HHMM)

Auto-Detect uses the instrument's natural hours (stocks use exchange hours, crypto uses 24/7).

### BREAKOUT DETECTION Section

Enable Breakout Detection: Master switch for signals

Show Retest Labels: Display retest signals

Label Size: Visual size for all labels (Small recommended)

Enable FVG Filter: Require Fair Value Gap confirmation

Show FVG Boxes: Display the gap boxes on chart

Signal Mode: "First Only" = one signal per direction per day, "Track Cycles" = multiple signals

Max Cycles: How many breakout-retest cycles to track (6 is balanced)

Breakout Buffer: Extra distance required beyond ORB level (0.1-0.2% recommended)

Min Distance for Retest: How far price must move away before retest is valid (2% recommended)

Min Bars Outside ORB: Bars price must stay outside for committed breakout (2 is balanced)

### TARGETS & RISK Section

Enable Targets & Stop-Loss: Calculate and show trade management

TP1/TP2/TP3 checkboxes: Select which profit targets to display

Stop Method: How to calculate stop loss placement

- ATR: Based on volatility (best for most cases)

- ORB %: Fixed % of ORB range

- Swing: Recent swing high/low

- Safer: Widest of all methods

ATR Length & Multiplier: Controls ATR stop distance (14 period, 1.5x is standard)

ORB Stop %: Percentage beyond ORB for stop (20% is balanced)

Swing Bars: Lookback period for swing high/low (3 is recent)

### TP/SL LINES Section

Show TP/SL Lines: Display horizontal lines on chart

Label Format: "Short" = minimal text, "Detailed" = shows prices

Freeze Lines at EOD: Stop extending lines at session close

### DASHBOARD Section

Show Info Panel: Display the metrics dashboard

Theme: Dark or Light colors

Position: Where to place dashboard on chart

Toggle rows: Show/hide specific information rows

Calculate Position Size: Enable the position sizing calculator

Risk Mode: Risk fixed $ amount or % of account

Account Size: Your total trading capital

Risk %: Percentage to risk per trade (0.5-1% recommended)

### VOLUME FILTER Section

Enable Volume Filter: Require volume confirmation

MA Length: Average period (20 is standard)

Min Volume: Required multiplier (1.5x = 50% above average)

Strong Volume: Multiplier that bypasses other filters (2.5x)

### TREND FILTER Section

Enable Trend Filter: Require trend alignment

Trend Mode: Method to determine trend (VWAP is simple and effective)

Custom EMA Length: If using EMA mode (50 for swing, 20 for day trading)

SuperTrend settings: Period and Multiplier if using SuperTrend mode

### HIGHER TIMEFRAME Section

Check Daily Trend: Display higher timeframe bias in dashboard

Timeframe: What TF to check (D = daily, recommended)

Method: Price vs MA (stable) or Candle Direction (reactive)

MA Period: EMA length for Price vs MA method (20 is balanced)

Min Strength %: Minimum strength threshold for HTF bias to be considered

- For "Price vs MA": Minimum distance (%) from moving average

- For "Candle Direction": Minimum candle body size (%)

- 0.5% is balanced - increase for stricter filtering

- Lower values = more signals, higher values = only strong trends

### ALERTS Section

Enable Alerts: Master switch (must be ON to use any alerts)

Breakout Alerts: Notify on ORB breakouts

Retest Alerts: Notify when price retests after breakout

Failed Break Alerts: Notify on failed breakouts

Stage Complete Alerts: Notify when each ORB stage finishes forming

After enabling desired alert types, click "Create Alert" button, select this indicator, choose "Any alert() function call".

## Tips & Best Practices

### General Trading Tips

ORB works best on liquid instruments (stocks with good volume, major crypto pairs)

First hour of the session is most important - that's when ORB is forming

Breakouts WITH the trend have higher success rates - use the trend filter

Failed breakouts are common - use the "Min Bars Outside" setting to filter weak moves

Not every day produces good ORB setups - be patient and selective

### Position Sizing Best Practices

Never risk more than 1-2% of your account on a single trade

Use the built-in calculator - don't guess your position size

Update your account size monthly as it grows

Smaller accounts: use $ Amount mode for simplicity

Larger accounts: use % of Account mode for scaling

### Take Profit Strategy

Most traders use: 50% at TP1, 50% at TP2

Aggressive: Hold through TP1 for TP2 or TP3

Conservative: Full exit at TP1 (1:1 risk/reward)

After TP1 hits, consider moving stop to breakeven

TP3 rarely hits - only on strong trending days

### Filter Combinations

Maximum Quality: Volume + Trend + FVG (fewest signals, highest quality)

Balanced: Volume + Trend (good quality, reasonable frequency)

Active Trading: No filters or Volume only (many signals, lower quality)

Trending Markets: Trend filter essential (indices, crypto)

Range-Bound: Volume + FVG (avoid trend filter)

### Common Mistakes to Avoid

Chasing breakouts - wait for the bar to close, don't FOMO into wicks

Ignoring the stop loss - always use it, move it manually if needed

Over-leveraging - the calculator shows MAX shares, you can buy less

Trading every signal - quality > quantity, use filters

Not tracking results - keep a journal to see what works for YOU

## Pros and Cons

### Advantages

Complete all-in-one solution - from signal to position sizing

Multiple timeframes tracked simultaneously

Visual clarity - easy to see what's happening

Cycle tracking catches opportunities others miss

Built-in risk management eliminates guesswork

Customizable filters for different trading styles

No repainting - what you see is locked in

Works across multiple markets (stocks, forex, crypto)

### Limitations

Intraday strategy only - doesn't work on daily charts

Requires active monitoring during first 1-2 hours of session

Not suitable for after-hours or extended sessions by default

Can produce many signals in choppy markets (use filters)

Dashboard can be overwhelming for complete beginners

Performance depends on market conditions (trends vs ranges)

Requires understanding of risk management concepts

### Best For

Day traders who can watch the first 1-2 hours of market open

Traders who want systematic entry/exit rules

Those learning proper position sizing and risk management

Active traders comfortable with multiple signals per day

Anyone trading liquid instruments with clear sessions

### Not Ideal For

Swing traders holding multi-day positions

Set-and-forget / passive investors

Traders who can't watch market open

Complete beginners unfamiliar with trading concepts

Low volume / illiquid instruments

## Frequently Asked Questions

Q: Why are no signals appearing?

A: Check that you're on an intraday timeframe (5min, 15min, etc.) and that the current time is within your session hours. Also verify that "Enable Breakout Detection" is ON and at least one ORB stage is enabled. If using filters, they might be blocking signals - try disabling them temporarily.

Q: What's the best ORB stage to use?

A: ORB15 (15 minutes) is most popular and balanced. ORB5 gives faster signals but more noise. ORB30 and ORB60 are slower but more reliable. Many traders use ORB15 + ORB30 together.

Q: Should I enable all the filters?

A: Start with no filters to see all signals. If too many false signals, add Volume filter first (stocks) or Trend filter (trending markets). FVG filter is most restrictive - use for maximum quality but fewer signals.

Q: How do I know which stop loss method to use?

A: ATR works for most cases - it adapts to volatility. Use ORB% if you want predictable stop placement. Swing is for respecting chart structure. Safer gives you the most room but largest risk.

Q: Can I use this for swing trading?

A: Not really - ORB is fundamentally an intraday strategy. The ranges reset each day. For swing trading, look at weekly support/resistance or moving averages instead.

Q: Why do TP/SL lines disappear sometimes?

A: Lines freeze (stop extending) when: stop loss is hit, the last enabled take-profit is hit, or end of session arrives (if "Freeze at EOD" is enabled). This is intentional - the trade is complete.

Q: What's the difference between "First Only" and "Track Cycles"?

A: "First Only" shows one breakout UP and one DOWN per day maximum - clean but might miss opportunities. "Track Cycles" shows breakout-retest-rebreak sequences - more signals but busier chart.

Q: Is position sizing accurate for options/forex?

A: The calculator is designed for shares (stocks). For options, ignore the share count and use the risk amount. For forex, you'll need to adapt the lot size calculation manually.

Q: How much capital do I need to use this?

A: The indicator works for any account size, but practical day trading typically requires $25,000 in the US due to Pattern Day Trader rules. Adjust the "Account Size" setting to match your capital.

Q: Can I backtest this strategy?

A: This is an indicator, not a strategy script, so it doesn't have built-in backtesting. You can visually review historical signals or code a strategy script using similar logic.

Q: Why does the dashboard show different entry price than the breakout label?

A: If you're looking at an old breakout, the ORB levels may have changed when the next stage completed. The dashboard always shows the CURRENT active range and trade setup.

Q: What's a good win rate to expect?

A: ORB strategies typically see 40-60% win rate depending on market conditions and filters used. The strategy relies on positive risk/reward ratios (2:1 or better) to be profitable even with moderate win rates.

Q: Does this work on crypto?

A: Yes, but crypto trades 24/7 so you need to define what "session start" means. Use Session Mode = Custom and set your preferred daily reset time (e.g., 0000-2359 UTC).

## Credits & Transparency

### Development

This indicator was developed with the assistance of AI technology to implement complex ORB trading logic.

The strategy concept, feature specifications, and trading logic were designed by the publisher. The implementation leverages modern development tools to ensure:

Clean, efficient, and maintainable code

Comprehensive error handling and input validation

Detailed documentation and user guidance

Performance optimization

### Trading Concepts

This indicator implements several public domain trading concepts:

Opening Range Breakout (ORB): Trading strategy popularized by Toby Crabel, Mark Fisher and many more talanted traders.

Fair Value Gap (FVG): Price imbalance concept from ICT methodology

SuperTrend: ATR-based trend indicator using public formula

Risk/Reward Ratio: Standard risk management principle

All mathematical formulas and technical concepts used are in the public domain.

### Pine Script

Uses standard TradingView built-in functions:

ta.ema(), ta.atr(), ta.vwap(), ta.highest(), ta.lowest(), request.security()

No external libraries or proprietary code from other authors.

## Disclaimer

This indicator is provided for educational and informational purposes only. It is not financial advice.

Trading involves substantial risk of loss and is not suitable for every investor. Past performance shown in examples is not indicative of future results.

The indicator provides signals and calculations, but trading decisions are solely your responsibility. Always:

Test strategies on paper before using real money

Never risk more than you can afford to lose

Understand that all trading involves risk

Consider seeking advice from a licensed financial advisor

The publisher makes no guarantees regarding accuracy, profitability, or performance. Use at your own risk.

---

Version: 3.0

Pine Script Version: v6

Last Updated: October 2024

For support, questions, or suggestions, please comment below or send a private message.

---

Happy trading, and remember: consistent risk management beats perfect entry timing every time.

Position Size calculatorOverview

This indicator automatically calculates the average candle body size (|open − close|) for the current trading day and derives a position size (quantity) based on your fixed risk per trade (default ₹1000).

For example:

If today’s average candle body = ₹3.50 and risk = ₹1000 → Quantity = 285

How It Works:

The indicator calculates the absolute difference between open and close (the candle’s body) for every bar of the current day.

It averages those body sizes to estimate the average daily volatility.

Then it divides your chosen risk per trade by the average body size to estimate an appropriate quantity.

It automatically resets at the start of each new day.

Why Use It

While risk size can be derived manually or using TradingView’s built-in Long/Short Position Tool, this indicator provides a faster, more practical alternative when you need to make quick trade decisions — especially in fast-moving intraday markets .

It keeps you focused on execution rather than calculation.

Tip

You can still verify or fine-tune the quantity using the Long/Short Position Tool or a manual calculator, but this indicator helps you react instantly when opportunities appear.

Risk ModuleThis indicator provides a visual reference for position sizing and approximate stop and target placement. It supports trade planning by calculating equalized risk per trade and maintaining consistent exposure across different markets.

For more information about the concept, see the post Position Sizing and Risk Management .

Fixed Fractional Risk

The indicator calculates the number of shares that can be traded to maintain consistent monetary risk. The formula is based on the distance between the current price and stop reference, adjusting position size proportionally. A closer stop results in a larger position size, while a wider stop results in a smaller one.

Position Size = (Account Size × Risk %) ÷ (Entry Price – Stop Price)

Stop and Target

Stop placement is derived from volatility using the Average True Range (ATR). The target is plotted as a multiple of the stop distance, defining the risk-to-reward relationship in R units.

Stop = Price ± ATR × Multiplier

Target = Price ± (R × Risk Distance)

Chart Elements

The stop and target levels are plotted above and below the current price, with the stop marked by a red dot and the target by a green dot. The information table displayed on the chart shows the number of shares to trade, stop level, and target level.

Setup and Configuration

This configuration only needs to be set once, but can be adjusted later if preferred.

1. Start by setting the account size and risk percentage per trade to define the monetary amount risked on each trade. These values form the basis for position size calculation.

2. Set the ATR multiplier to determine stop distance, common values range between 1 and 3 ATR. Lower values place stops closer to price, increasing sensitivity but risking short-term noise. Higher values widen the stop, which reduces noise impact but extends time in risk.

3. Set the R-multiple to determine target distance relative to the stop. A value of 1 represents a 1:1 risk-to-reward relationship. Lower values reduce potential reward but tend to increase win rate, whereas higher values increase potential reward but tend to reduce win rate. The selection depends on system characteristics and trade expectancy.

When the parameters are defined, the indicator displays the stop, target, and calculated position size on the chart. All that remains is to enter the trade with the number of shares shown in the table and place bracket orders at the plotted stop and target levels.

Settings Overview

Account Size / Risk %: Defines account capital and per-trade exposure.

ATR Multiplier: Adjusts stop distance relative to volatility.

R Multiple: Sets target distance relative to stop (risk-reward ratio).

Position: Choose Long or Short direction.

Table Position: Controls information table placement and scale.

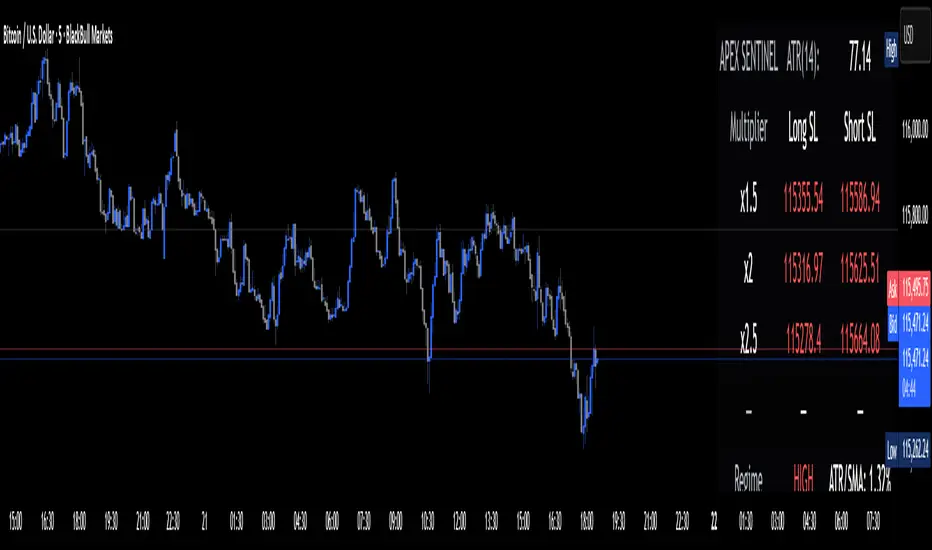

Apex Edge Sentinel - Stop Loss HUDApex Edge – ATR Sentinel Stop Loss HUD

The Apex Edge – ATR Sentinel is a complete stop-loss intelligence system built as a clean, always-on HUD.

It delivers institutional-level risk guidance by calculating and displaying live ATR-based stop levels for both long and short trades at multiple risk tolerances.

Forget cluttered charts and repainting lines — Sentinel gives you a clear stop-loss reference panel that updates dynamically with every bar.

✅ Features

• Triple ATR Multipliers

User-defined (e.g. x1.5 / x2.0 / x2.5). Compare tight, medium, and wide stops instantly.

• Dual-Side SL Levels

Both Long and Short safe stop prices displayed side by side. No more guessing trend

bias.

• ATR Transparency

HUD shows ATR(length) so you always know the calculation basis. Default = 14, adjustable

to your style.

• ATR Regime Meter

Detects volatility conditions (LOW / NORMAL / HIGH) by comparing ATR to its SMA. Helps

you avoid over-tight stops in high-volatility markets.

• Tick-Aware Rounding

Stop levels auto-rounded to the instrument’s tick size (Gold = 0.10, FX = 0.0001, indices =

whole points).

Custom HUD Design

• Location: Top/Bottom, Left/Right

• Sizes: Compact / Medium / Large (desktop or mobile)

• Opacity control (25% default Apex styling)

How to Use

1. Load Sentinel on your chart.