Ripster Labels + Air Gaps (v6)What it shows (on one chart)

EMA Clouds (current timeframe)

Plots EMA 8/12/21/34/50/200 with three cloud fills:

12–21 = “fast” cloud

34–50 = “mid” cloud

50–200 = “base” cloud

Cloud color: green when the faster EMA is above the slower (bullish), red/maroon/orange when below (bearish).

Toggle lines vs. clouds via A) EMA Clouds settings.

MTF Rails (higher-TF EMAs)

For three higher timeframes (defaults 30m / 60m / 240m), draws two EMAs each (defaults 34 & 50).

These are stepline-like rails you can visually use as higher-TF supports/resistances.

Configure in B) MTF Rails (turn on/off, change TFs/lengths/colors).

Relative Volume Box (RVol)

Small table (top-center) showing:

Candle Vol (formatted K/M/B if enabled)

RVol = current bar volume / SMA 20 of volume (as a %)

Color scale: blue (<100%), yellow (100–150%), red (>150%).

Settings in C) RVol Box.

DTR vs ATR Box

Daily True Range (DTR = day high − day low) vs ATR(14) on the daily timeframe, with DTR as % of ATR.

Placed at top-right; toggle in D) DTR/ATR Box.

Ripster Trend Label (10m 12/50)

Looks at a separate timeframe (default 10m): EMA 12 vs EMA 50.

Bottom-right table cell shows “10m Trend ↑/↓/Sideways” (green/red/gray).

Configure in E) Ripster Trend Labels (TF and lengths).

Air Gaps (single EMA per TF)

Three horizontal, auto-extending lines showing an EMA from 30m / 60m / 240m (default length 12).

“Air gaps” are the price spaces between these lines—often lighter-resistance zones for price.

Start point logic:

All Bars = draw from the chart’s left

Start of Day = draw from today’s first bar

Bars Offset = draw from N bars back (default 100)

Settings in F) Air Gaps (TFs, length, draw-from, bars-back).

Inputs & where to tweak

A) EMA Clouds

Show EMA Clouds: master toggle

Source: close (default)

Lengths: 8/12/21/34/50/200

Show EMA lines: toggle plotted lines (clouds remain)

B) MTF Rails

Show MTF Rails

TF1/TF2/TF3 (defaults 30/60/240)

EMA A/B (defaults 34/50)

C) RVol Box

Show box

Format as K/M/B: K=1e3, M=1e6, B=1e9

D) DTR/ATR Box

Show DTR/ATR

ATR len: default 14 (daily)

E) Ripster Trend Labels

Show labels

Trend TF: default 10 (10-minute)

Trend EMA Fast/Slow: default 12/50

F) Air Gaps

Show Air Gap lines

TF1/TF2/TF3 (30/60/240)

EMA length: default 12

Draw from: All Bars | Start of Day | Bars Offset

Bars back: used if Draw from = Bars Offset

How it makes decisions

Cloud bias = sign of (faster EMA − slower EMA) for each cloud pair.

Example: 12>21 → fast cloud is bullish (green); 34>50 → mid cloud bullish (teal).

10m trend label = sign of (EMA12−EMA50) on the Trend TF (default 10m).

RVol = volume / sma(volume, 20); formatted as a percent and color-coded.

Practical read of the screen

Fast cloud flips (12/21) often mark short-term momentum changes; mid cloud flips (34/50) reflect swing bias.

Air Gap lines from higher TFs frequently act as support/resistance. Larger spaces between lines = “air gaps” where price can move with less friction.

RVol color tells you how “real” a move is: red/yellow often confirms momentum; blue warns of thin/liquidy bars.

DTR vs ATR shows if today’s range is stretched vs recent norm.

Design choices (why your prior errors are gone)

Removed multiline ?: chains → replaced by if/else (Pine v6 is picky about line continuations).

Moved fill() calls outside of local if blocks (Pine limitation).

ta.change(time("D")) != 0 makes the if condition boolean.

Declared G_drawFrom / G_barsBack before startX() so identifiers exist.

Cerca negli script per "12月4号是什么星座"

Quarterly Cycle Theory with DST time AdjustedThe Quarterly Theory removes ambiguity, as it gives specific time-based reference points to look for when entering trades. Before being able to apply this theory to trading, one must first understand that time is fractal:

Yearly Quarters = 4 quarters of three months each.

Monthly Quarters = 4 quarters of one week each.

Weekly Quarters = 4 quarters of one day each (Monday - Thursday). Friday has its own specific function.

Daily Quarters = 4 quarters of 6 hours each = 4 trading sessions of a trading day.

Sessions Quarters = 4 quarters of 90 minutes each.

90 Minute Quarters = 4 quarters of 22.5 minutes each.

Yearly Cycle: Analogously to financial quarters, the year is divided in four sections of three months each:

Q1 - January, February, March.

Q2 - April, May, June (True Open, April Open).

Q3 - July, August, September.

Q4 - October, November, December.

S&P 500 E-mini Futures (daily candles) — Monthly Cycle.

Monthly Cycle: Considering that we have four weeks in a month, we start the cycle on the first month’s Monday (regardless of the calendar Day):

Q1 - Week 1: first Monday of the month.

Q2 - Week 2: second Monday of the month (True Open, Daily Candle Open Price).

Q3 - Week 3: third Monday of the month.

Q4 - Week 4: fourth Monday of the month.

S&P 500 E-mini Futures (4 hour candles) — Weekly Cycle.

Weekly Cycle: Daye determined that although the trading week is composed by 5 trading days, we should ignore Friday, and the small portion of Sunday’s price action:

Q1 - Monday.

Q2 - Tuesday (True Open, Daily Candle Open Price).

Q3 - Wednesday.

Q4 - Thursday.

S&P 500 E-mini Futures (1 hour candles) — Daily Cycle.

Daily Cycle: The Day can be broken down into 6 hour quarters. These times roughly define the sessions of the trading day, reinforcing the theory’s validity:

Q1 - 18:00 - 00:00 Asia.

Q2 - 00:00 - 06:00 London (True Open).

Q3 - 06:00 - 12:00 NY AM.

Q4 - 12:00 - 18:00 NY PM.

S&P 500 E-mini Futures (15 minute candles) — 6 Hour Cycle.

6 Hour Quarters or 90 Minute Cycle / Sessions divided into four sections of 90 minutes each (EST/EDT):

Asian Session

Q1 - 18:00 - 19:30

Q2 - 19:30 - 21:00 (True Open)

Q3 - 21:00 - 22:30

Q4 - 22:30 - 00:00

London Session

Q1 - 00:00 - 01:30

Q2 - 01:30 - 03:00 (True Open)

Q3 - 03:00 - 04:30

Q4 - 04:30 - 06:00

NY AM Session

Q1 - 06:00 - 07:30

Q2 - 07:30 - 09:00 (True Open)

Q3 - 09:00 - 10:30

Q4 - 10:30 - 12:00

NY PM Session

Q1 - 12:00 - 13:30

Q2 - 13:30 - 15:00 (True Open)

Q3 - 15:00 - 16:30

Q4 - 16:30 - 18:00

S&P 500 E-mini Futures (5 minute candles) — 90 Minute Cycle.

Micro Cycles: Dividing the 90 Minute Cycle yields 22.5 Minute Quarters, also known as Micro Sessions or Micro Quarters:

Asian Session

Q1/1 18:00:00 - 18:22:30

Q2 18:22:30 - 18:45:00

Q3 18:45:00 - 19:07:30

Q4 19:07:30 - 19:30:00

Q2/1 19:30:00 - 19:52:30 (True Session Open)

Q2/2 19:52:30 - 20:15:00

Q2/3 20:15:00 - 20:37:30

Q2/4 20:37:30 - 21:00:00

Q3/1 21:00:00 - 21:23:30

etc. 21:23:30 - 21:45:00

London Session

00:00:00 - 00:22:30 (True Daily Open)

00:22:30 - 00:45:00

00:45:00 - 01:07:30

01:07:30 - 01:30:00

01:30:00 - 01:52:30 (True Session Open)

01:52:30 - 02:15:00

02:15:00 - 02:37:30

02:37:30 - 03:00:00

03:00:00 - 03:22:30

03:22:30 - 03:45:00

03:45:00 - 04:07:30

04:07:30 - 04:30:00

04:30:00 - 04:52:30

04:52:30 - 05:15:00

05:15:00 - 05:37:30

05:37:30 - 06:00:00

New York AM Session

06:00:00 - 06:22:30

06:22:30 - 06:45:00

06:45:00 - 07:07:30

07:07:30 - 07:30:00

07:30:00 - 07:52:30 (True Session Open)

07:52:30 - 08:15:00

08:15:00 - 08:37:30

08:37:30 - 09:00:00

09:00:00 - 09:22:30

09:22:30 - 09:45:00

09:45:00 - 10:07:30

10:07:30 - 10:30:00

10:30:00 - 10:52:30

10:52:30 - 11:15:00

11:15:00 - 11:37:30

11:37:30 - 12:00:00

New York PM Session

12:00:00 - 12:22:30

12:22:30 - 12:45:00

12:45:00 - 13:07:30

13:07:30 - 13:30:00

13:30:00 - 13:52:30 (True Session Open)

13:52:30 - 14:15:00

14:15:00 - 14:37:30

14:37:30 - 15:00:00

15:00:00 - 15:22:30

15:22:30 - 15:45:00

15:45:00 - 15:37:30

15:37:30 - 16:00:00

16:00:00 - 16:22:30

16:22:30 - 16:45:00

16:45:00 - 17:07:30

17:07:30 - 18:00:00

S&P 500 E-mini Futures (30 second candles) — 22.5 Minute Cycle.

WASDE Dates V2WASDE Dates V2 – USDA Release Calendar with Alerts, Countdown & Event Markers

By cot-trader.com

WASDE Dates V2 is a complete and reliable visualization tool for all scheduled WASDE (World Agricultural Supply and Demand Estimates) releases for 2025 and 2026.

The USDA’s WASDE report is one of the most market-moving fundamental catalysts in agricultural futures—affecting Corn (ZC), Wheat (ZW), Soybeans (ZS), Soymeal (ZM), Soybean Oil (ZL), and many related CFD products.

This script gives traders a precise timing layer directly inside their TradingView charts.

🔍 What this script does

WASDE Dates V2 automatically:

Marks each WASDE release day with a vertical line and label.

Shows an automated countdown to the next WASDE release:

In days (>24h)

In hours & minutes (<24h)

Displays an optional table of upcoming WASDE dates for quick reference.

Provides two alert conditions:

WASDE Day Alert – triggers exactly on the event

WASDE 24h Reminder – pre-alert when less than 24 hours remain

Handles both 2025 and 2026 confirmed dates.

Works on any symbol and timeframe.

📌 Why WASDE matters

The WASDE report updates global supply and demand estimates for:

Corn

Soybeans

Wheat

Other major agricultural commodities

Changes in yield, acres, production, imports/exports, and ending stocks can cause immediate and significant volatility.

Many traders combine WASDE awareness with seasonality, COT positioning, volatility filters, or fundamental models.

This script ensures you never miss the timing of these key releases.

⚙️ How the script works

The script stores official USDA WASDE release dates for 2025 and 2026 in two dedicated arrays.

On every bar, it compares the bar’s timestamp with known WASDE timestamps to detect an event day.

When an event occurs:

A red “WASDE” label is plotted above the candle

A dotted vertical line is drawn through the bar

It finds the next upcoming WASDE by scanning forward through both arrays.

A live-updating countdown label is displayed, showing days or hours/minutes until release.

If the event is less than 24 hours away:

A yellow “WASDE soon” warning appears near price

The 24h alert condition becomes active

An optional table lists upcoming events for 2025 & 2026.

This script does not generate trading signals.

It provides a time-based event layer designed to complement any discretionary or algorithmic trading approach.

🧭 How to use

Add the script to your chart.

Enable alerts for:

“WASDE Day Alert”

“WASDE 24h Reminder”

Follow the countdown to prepare for upcoming volatility.

Use together with other agricultural tools such as:

Seasonality indicators

COT (Commitment of Traders) analysis

Trend / VWAP / Volume signals

Pre- and post-WASDE trading strategies

Works on all chart types, all symbols, and all timeframes.

📅 Included WASDE Dates (Confirmed)

2025:

Jan 12, Feb 11, Mar 11, Apr 10, May 12, Jun 12, Jul 11, Aug 12, Sep 12, Oct 9, Nov 10, Dec 9

2026:

Jan 12, Feb 10, Mar 10, Apr 9, May 12, Jun 11, Jul 10, Aug 12, Sep 11, Oct 9, Nov 10, Dec 10

(All dates based on USDA’s official 12:00pm ET schedule.)

💡 What makes this script original

Fully updated 2025 + 2026 calendar

Uses a robust time-comparison method for accurate marking

Unique dual alert system (event + 24h pre-alert)

Clean, readable layout with countdown + upcoming dates table

Tailored specifically for grain & agricultural traders

Built entirely in Pine Script v6 with careful attention to performance

Range Bar Gaps DetectorRange Bar Gaps Detector

Overview

The Range Bar Gaps Detector identifies price gaps across multiple range bar sizes (12, 24, 60, and 120) on any trading instrument, helping traders spot potential support/resistance zones or breakout opportunities. Designed for Pine Script v6, this indicator detects gaps on range bars and exports data for use in companion scripts like Range Bar Gaps Overlap, making it ideal for multi-timeframe gap analysis.

Key Features

Multi-Range Gap Detection: Identifies gaps on 12, 24, 60, and 120-range bars, capturing both bullish (gap up) and bearish (gap down) price movements.

Customizable Sensitivity: Includes a user-defined minimum deviation (default: 10% of 14-period SMA) for 12-range gaps to filter out noise.

7-Day Lookback: Automatically prunes gaps older than 7 days to focus on recent, relevant price levels.

Data Export: Serializes up to 10 gaps per range (tops, bottoms, start bars, highest/lowest prices, and age) for seamless integration with overlap analysis scripts.

Debugging Support: Plots gap counts and aggregation data in the Data Window for easy verification of detected gaps.

How It Works

The indicator aggregates price movements to simulate higher range bars (24, 60, 120) from a base range bar chart. It detects gaps when the price jumps significantly between bars, ensuring gaps meet the minimum deviation threshold for 12-range bars. Gaps are stored in arrays, serialized for external use, and pruned after 7 days to maintain efficiency.

Usage

Add to your range bar chart (e.g., 12-range) to detect gaps across multiple ranges.

Use alongside the Range Bar Gaps Overlap indicator to visualize gaps and their overlaps as boxes on the chart.

Check the Data Window to confirm gap counts and sizes for each range (12, 24, 60, 120).

Adjust the "Minimal Deviation (%) for 12-Range" input to control gap detection sensitivity.

Settings

Minimal Deviation (%) for 12-Range: Set the minimum gap size for 12-range bars (default: 10% of 14-period SMA).

Range Sizes: Fixed at 24, 60, and 120 for higher range bar aggregation.

Notes

Ensure the script is published under your TradingView username (e.g., GreenArrow2005) for use with companion scripts.

Best used on range bar charts to maintain consistent gap detection.

For advanced overlap analysis, pair with the Range Bar Gaps Overlap indicator to highlight zones where gaps from different ranges align.

Ideal For

Traders seeking to identify key price levels for support/resistance or breakout strategies.

Multi-timeframe analysts combining gap data across various range bar sizes.

Developers building custom indicators that leverage gap data for advanced charting.

2:30 [LuciTech]this is a technical analysis tool designed to highlight key price levels and patterns during a specific trading window, based on UK time (Europe/London). It overlays visual elements on the chart, including a 12 PM reference line, Buy Side Liquidity (BSL) and Sell Side Liquidity (SSL) levels, a highlighted 2:30 PM candle, and Engulfing Fair Value Gaps (FVGs). This indicator is intended for traders who focus on intraday price action and liquidity zones.

Features

The 12 PM Line displays a vertical line at 12:00 PM (UK time) to mark the start of the session. It’s customizable, allowing you to enable or disable it and adjust its color.

BSL/SSL Lines track the highest high (BSL) and lowest low (SSL) from 12:00 PM to 2:00 PM (UK time). These lines extend horizontally until 3:30 PM, after which they remain static at their last recorded levels. You can customize them by enabling or disabling visibility, adjusting colors, choosing a line style (solid, dashed, or dotted), and setting the width.

The 2:30 PM Candle highlights the candle at 2:30 PM (UK time) with a distinct color. It’s customizable, with options to enable or disable it and change its color.

Engulfing FVG (Fair Value Gap) identifies bullish and bearish engulfing patterns with a gap from the prior candle’s range. It draws a shaded box over the FVG area, and you can customize it by enabling or disabling it and adjusting the box color.

How It Works

The indicator operates within a session starting at 12:00 PM (UK time). BSL/SSL levels update between 12:00 PM and 2:00 PM, with lines extending until 3:30 PM. After 3:30 PM, these lines freeze.

BSL/SSL lines show the highest price (BSL) and lowest price (SSL) reached during the 12:00 PM to 2:00 PM window. After 3:30 PM, they remain static, marking the final range boundaries.

The 2:30 PM candle emphasizes a key timestamp, often of interest to intraday traders.

Engulfing FVGs detect significant price gaps created by engulfing candles, which may indicate potential reversal or continuation zones.

Settings

12 PM Line Settings let you toggle visibility and set the line color.

BSL/SSL Line Settings allow you to toggle visibility, set BSL and SSL colors, choose a line style (Solid, Dashed, Dotted), and adjust width (1-4).

2:30 Candle Settings let you toggle visibility and set the candle color.

Engulfing FVG Settings allow you to toggle visibility and set the box color.

Interpretation

The 12 PM Line serves as a reference for the session start.

BSL/SSL Lines may act as potential support or resistance zones or highlight liquidity areas. After 3:30 PM, they remain static, showing the session’s final range.

The 2:30 PM Candle can be monitored for price action signals, such as reversals or breakouts.

Engulfing FVGs shaded areas may indicate imbalances in supply and demand, useful for identifying trade opportunities or stop-loss placement.

Notes

The timezone is set to Europe/London (UK time). Ensure your chart’s timezone aligns for accurate results.

This indicator is best used on intraday timeframes, such as 1-minute or 5-minute charts.

It provides visual aids for analysis and does not generate buy or sell signals on its own.

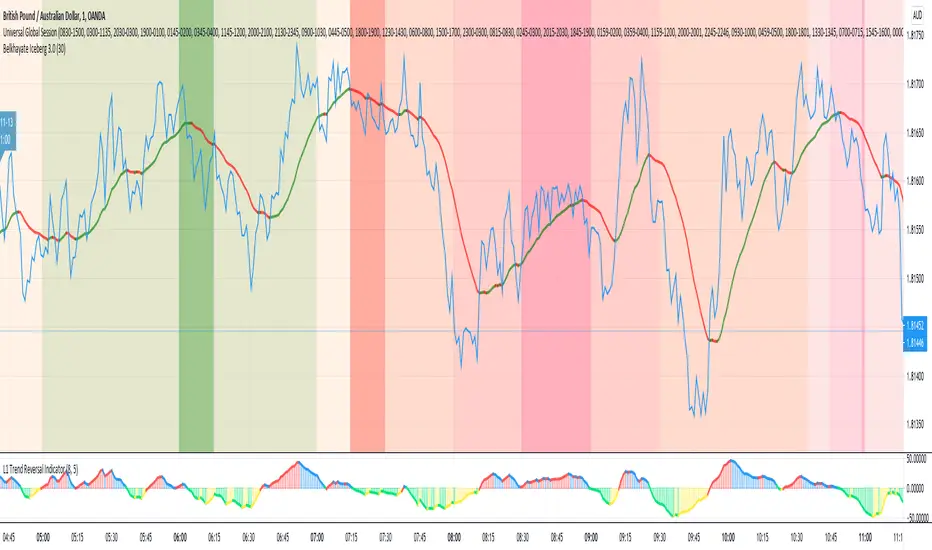

Universal Global SessionUniversal Global Session

This Script combines the world sessions of: Stocks, Forex, Bitcoin Kill Zones, strategic points, all configurable, in a single Script, to capitalize the opening and closing times of global exchanges as investment assets, becoming an Universal Global Session .

It is based on the great work of @oscarvs ( BITCOIN KILL ZONES v2 ) and the scripts of @ChrisMoody. Thank you Oscar and Chris for your excellent judgment and great work.

At the end of this writing you can find all the internet references of the extensive documentation that I present here. To maximize your benefits in the use of this Script, I recommend that you read the entire document to create an objective and practical criterion.

All the hours of the different exchanges are presented at GMT -6. In Market24hClock you can adjust it to your preferences.

After a deep investigation I have been able to show that the different world sessions reveal underlying investment cycles, where it is possible to find sustained changes in the nominal behavior of the trend before the passage from one session to another and in the natural overlaps between the sessions. These underlying movements generally occur 15 minutes before the start, close or overlap of the session, when the session properly starts and also 15 minutes after respectively. Therefore, this script is designed to highlight these particular trending behaviors. Try it, discover your own conclusions and let me know in the notes, thank you.

Foreign Exchange Market Hours

It is the schedule by which currency market participants can buy, sell, trade and speculate on currencies all over the world. It is open 24 hours a day during working days and closes on weekends, thanks to the fact that operations are carried out through a network of information systems, instead of physical exchanges that close at a certain time. It opens Monday morning at 8 am local time in Sydney —Australia— (which is equivalent to Sunday night at 7 pm, in New York City —United States—, according to Eastern Standard Time), and It closes at 5pm local time in New York City (which is equivalent to 6am Saturday morning in Sydney).

The Forex market is decentralized and driven by local sessions, where the hours of Forex trading are based on the opening range of each active country, becoming an efficient transfer mechanism for all participants. Four territories in particular stand out: Sydney, Tokyo, London and New York, where the highest volume of operations occurs when the sessions in London and New York overlap. Furthermore, Europe is complemented by major financial centers such as Paris, Frankfurt and Zurich. Each day of forex trading begins with the opening of Australia, then Asia, followed by Europe, and finally North America. As markets in one region close, another opens - or has already opened - and continues to trade in the currency market. The seven most traded currencies in the world are: the US dollar, the euro, the Japanese yen, the British pound, the Australian dollar, the Canadian dollar, and the New Zealand dollar.

Currencies are needed around the world for international trade, this means that operations are not dominated by a single exchange market, but rather involve a global network of brokers from around the world, such as banks, commercial companies, central banks, companies investment management, hedge funds, as well as retail forex brokers and global investors. Because this market operates in multiple time zones, it can be accessed at any time except during the weekend, therefore, there is continuously at least one open market and there are some hours of overlap between the closing of the market of one region and the opening of another. The international scope of currency trading means that there are always traders around the world making and satisfying demands for a particular currency.

The market involves a global network of exchanges and brokers from around the world, although time zones overlap, the generally accepted time zone for each region is as follows:

Sydney 5pm to 2am EST (10pm to 7am UTC)

London 3am to 12 noon EST (8pm to 5pm UTC)

New York 8am to 5pm EST (1pm to 10pm UTC)

Tokyo 7pm to 4am EST (12am to 9am UTC)

Trading Session

A financial asset trading session refers to a period of time that coincides with the daytime trading hours for a given location, it is a business day in the local financial market. This may vary according to the asset class and the country, therefore operators must know the hours of trading sessions for the securities and derivatives in which they are interested in trading. If investors can understand market hours and set proper targets, they will have a much greater chance of making a profit within a workable schedule.

Kill Zones

Kill zones are highly liquid events. Many different market participants often come together and perform around these events. The activity itself can be event-driven (margin calls or option exercise-related activity), portfolio management-driven (asset allocation rebalancing orders and closing buy-in), or institutionally driven (larger players needing liquidity to complete the size) or a combination of any of the three. This intense cross-current of activity at a very specific point in time often occurs near significant technical levels and the established trends emerging from these events often persist until the next Death Zone approaches or enters.

Kill Zones are evolving with time and the course of world history. Since the end of World War II, New York has slowly invaded London's place as the world center for commercial banking. So much so that during the latter part of the 20th century, New York was considered the new center of the financial universe. With the end of the cold war, that leadership appears to have shifted towards Europe and away from the United States. Furthermore, Japan has slowly lost its former dominance in the global economic landscape, while Beijing's has increased dramatically. Only time will tell how these death zones will evolve given the ever-changing political, economic, and socioeconomic influences of each region.

Financial Markets

New York

New York (NYSE Chicago, NASDAQ)

7:30 am - 2:00 pm

It is the second largest currency platform in the world, followed largely by foreign investors as it participates in 90% of all operations, where movements on the New York Stock Exchange (NYSE) can have an immediate effect (powerful) on the dollar, for example, when companies merge and acquisitions are finalized, the dollar can instantly gain or lose value.

A. Complementary Stock Exchanges

Brazil (BOVESPA - Brazilian Stock Exchange)

07:00 am - 02:55 pm

Canada (TSX - Toronto Stock Exchange)

07:30 am - 02:00 pm

New York (NYSE - New York Stock Exchange)

08:30 am - 03:00 pm

B. North American Trading Session

07:00 am - 03:00 pm

(from the beginning of the business day on NYSE and NASDAQ, until the end of the New York session)

New York, Chicago and Toronto (Canada) open the North American session. Characterized by the most aggressive trading within the markets, currency pairs show high volatility. As the US markets open, trading is still active in Europe, however trading volume generally decreases with the end of the European session and the overlap between the US and Europe.

C. Strategic Points

US main session starts in 1 hour

07:30 am

The euro tends to drop before the US session. The NYSE, CHX and TSX (Canada) trading sessions begin 1 hour after this strategic point. The North American session begins trading Forex at 07:00 am.

This constitutes the beginning of the overlap of the United States and the European market that spans from 07:00 am to 10:35 am, often called the best time to trade EUR / USD, it is the period of greatest liquidity for the main European currencies since it is where they have their widest daily ranges.

When New York opens at 07:00 am the most intense trading begins in both the US and European markets. The overlap of European and American trading sessions has 80% of the total average trading range for all currency pairs during US business hours and 70% of the total average trading range for all currency pairs during European business hours. The intersection of the US and European sessions are the most volatile overlapping hours of all.

Influential news and data for the USD are released between 07:30 am and 09:00 am and play the biggest role in the North American Session. These are the strategically most important moments of this activity period: 07:00 am, 08:00 am and 08:30 am.

The main session of operations in the United States and Canada begins

08:30 am

Start of main trading sessions in New York, Chicago and Toronto. The European session still overlaps the North American session and this is the time for large-scale unpredictable trading. The United States leads the market. It is difficult to interpret the news due to speculation. Trends develop very quickly and it is difficult to identify them, however trends (especially for the euro), which have developed during the overlap, often turn the other way when Europe exits the market.

Second hour of the US session and last hour of the European session

09:30 am

End of the European session

10:35 am

The trend of the euro will change rapidly after the end of the European session.

Last hour of the United States session

02:00 pm

Institutional clients and very large funds are very active during the first and last working hours of almost all stock exchanges, knowing this allows to better predict price movements in the opening and closing of large markets. Within the last trading hours of the secondary market session, a pullback can often be seen in the EUR / USD that continues until the opening of the Tokyo session. Generally it happens if there was an upward price movement before 04:00 pm - 05:00 pm.

End of the trade session in the United States

03:00 pm

D. Kill Zones

11:30 am - 1:30 pm

New York Kill Zone. The United States is still the world's largest economy, so by default, the New York opening carries a lot of weight and often comes with a huge injection of liquidity. In fact, most of the world's marketable assets are priced in US dollars, making political and economic activity within this region even more important. Because it is relatively late in the world's trading day, this Death Zone often sees violent price swings within its first hour, leading to the proven adage "never trust the first hour of trading in America. North.

---------------

London

London (LSE - London Stock Exchange)

02:00 am - 10:35 am

Britain dominates the currency markets around the world, and London is its main component. London, a central trading capital of the world, accounts for about 43% of world trade, many Forex trends often originate from London.

A. Complementary Stock Exchange

Dubai (DFM - Dubai Financial Market)

12:00 am - 03:50 am

Moscow (MOEX - Moscow Exchange)

12:30 am - 10:00 am

Germany (FWB - Frankfurt Stock Exchange)

01:00 am - 10:30 am

Afríca (JSE - Johannesburg Stock Exchange)

01:00 am - 09:00 am

Saudi Arabia (TADAWUL - Saudi Stock Exchange)

01:00 am - 06:00 am

Switzerland (SIX - Swiss Stock Exchange)

02:00 am - 10:30 am

B. European Trading Session

02:00 am - 11:00 am

(from the opening of the Frankfurt session to the close of the Order Book on the London Stock Exchange / Euronext)

It is a very liquid trading session, where trends are set that start during the first trading hours in Europe and generally continue until the beginning of the US session.

C. Middle East Trading Session

12:00 am - 06:00 am

(from the opening of the Dubai session to the end of the Riyadh session)

D. Strategic Points

European session begins

02:00 am

London, Frankfurt and Zurich Stock Exchange enter the market, overlap between Europe and Asia begins.

End of the Singapore and Asia sessions

03:00 am

The euro rises almost immediately or an hour after Singapore exits the market.

Middle East Oil Markets Completion Process

05:00 am

Operations are ending in the European-Asian market, at which time Dubai, Qatar and in another hour in Riyadh, which constitute the Middle East oil markets, are closing. Because oil trading is done in US dollars, and the region with the trading day coming to an end no longer needs the dollar, consequently, the euro tends to grow more frequently.

End of the Middle East trading session

06:00 am

E. Kill Zones

5:00 am - 7:00 am

London Kill Zone. Considered the center of the financial universe for more than 500 years, Europe still has a lot of influence in the banking world. Many older players use the European session to establish their positions. As such, the London Open often sees the most significant trend-setting activity on any trading day. In fact, it has been suggested that 80% of all weekly trends are set through the London Kill Zone on Tuesday.

F. Kill Zones (close)

2:00 pm - 4:00 pm

London Kill Zone (close).

---------------

Tokyo

Tokyo (JPX - Tokyo Stock Exchange)

06:00 pm - 12:00 am

It is the first Asian market to open, receiving most of the Asian trade, just ahead of Hong Kong and Singapore.

A. Complementary Stock Exchange

Singapore (SGX - Singapore Exchange)

07:00 pm - 03:00 am

Hong Kong (HKEx - Hong Kong Stock Exchange)

07:30 pm - 02:00 am

Shanghai (SSE - Shanghai Stock Exchange)

07:30 pm - 01:00 am

India (NSE - India National Stock Exchange)

09:45 pm - 04:00 am

B. Asian Trading Session

06:00 pm - 03:00 am

From the opening of the Tokyo session to the end of the Singapore session

The first major Asian market to open is Tokyo which has the largest market share and is the third largest Forex trading center in the world. Singapore opens in an hour, and then the Chinese markets: Shanghai and Hong Kong open 30 minutes later. With them, the trading volume increases and begins a large-scale operation in the Asia-Pacific region, offering more liquidity for the Asian-Pacific currencies and their crosses. When European countries open their doors, more liquidity will be offered to Asian and European crossings.

C. Strategic Points

Second hour of the Tokyo session

07:00 pm

This session also opens the Singapore market. The commercial dynamics grows in anticipation of the opening of the two largest Chinese markets in 30 minutes: Shanghai and Hong Kong, within these 30 minutes or just before the China session begins, the euro usually falls until the same moment of the opening of Shanghai and Hong Kong.

Second hour of the China session

08:30 pm

Hong Kong and Shanghai start trading and the euro usually grows for more than an hour. The EUR / USD pair mixes up as Asian exporters convert part of their earnings into both US dollars and euros.

Last hour of the Tokyo session

11:00 pm

End of the Tokyo session

12:00 am

If the euro has been actively declining up to this time, China will raise the euro after the Tokyo shutdown. Hong Kong, Shanghai and Singapore remain open and take matters into their own hands causing the growth of the euro. Asia is a huge commercial and industrial region with a large number of high-quality economic products and gigantic financial turnover, making the number of transactions on the stock exchanges huge during the Asian session. That is why traders, who entered the trade at the opening of the London session, should pay attention to their terminals when Asia exits the market.

End of the Shanghai session

01:00 am

The trade ends in Shanghai. This is the last trading hour of the Hong Kong session, during which market activity peaks.

D. Kill Zones

10:00 pm - 2:00 am

Asian Kill Zone. Considered the "Institutional" Zone, this zone represents both the launch pad for new trends as well as a recharge area for the post-American session. It is the beginning of a new day (or week) for the world and as such it makes sense that this zone often sets the tone for the remainder of the global business day. It is ideal to pay attention to the opening of Tokyo, Beijing and Sydney.

--------------

Sidney

Sydney (ASX - Australia Stock Exchange)

06:00 pm - 12:00 am

A. Complementary Stock Exchange

New Zealand (NZX - New Zealand Stock Exchange)

04:00 pm - 10:45 pm

It's where the global trading day officially begins. While it is the smallest of the megamarkets, it sees a lot of initial action when markets reopen Sunday afternoon as individual traders and financial institutions are trying to regroup after the long hiatus since Friday afternoon. On weekdays it constitutes the end of the current trading day where the change in the settlement date occurs.

B. Pacific Trading Session

04:00 pm - 12:00 am

(from the opening of the Wellington session to the end of the Sydney session)

Forex begins its business hours when Wellington (New Zealand Exchange) opens local time on Monday. Sydney (Australian Stock Exchange) opens in 2 hours. It is a session with a fairly low volatility, configuring itself as the calmest session of all. Strong movements appear when influential news is published and when the Pacific session overlaps the Asian Session.

C. Strategic Points

End of the Sydney session

12:00 am

---------------

Conclusions

The best time to trade is during overlaps in trading times between open markets. Overlaps equate to higher price ranges, creating greater opportunities.

Regarding press releases (news), it should be noted that these in the currency markets have the power to improve a normally slow trading period. When a major announcement is made regarding economic data, especially when it goes against the predicted forecast, the coin can lose or gain value in a matter of seconds. In general, the more economic growth a country produces, the more positive the economy is for international investors. Investment capital tends to flow to countries that are believed to have good growth prospects and subsequently good investment opportunities, leading to the strengthening of the country's exchange rate. Also, a country that has higher interest rates through its government bonds tends to attract investment capital as foreign investors seek high-yield opportunities. However, stable economic growth and attractive yields or interest rates are inextricably intertwined. It's important to take advantage of market overlaps and keep an eye out for press releases when setting up a trading schedule.

References:

www.investopedia.com

www.investopedia.com

www.investopedia.com

www.investopedia.com

market24hclock.com

market24hclock.com

ORB Fusion🎯 CORE INNOVATION: INSTITUTIONAL ORB FRAMEWORK WITH FAILED BREAKOUT INTELLIGENCE

ORB Fusion represents a complete institutional-grade Opening Range Breakout system combining classic Market Profile concepts (Initial Balance, day type classification) with modern algorithmic breakout detection, failed breakout reversal logic, and comprehensive statistical tracking. Rather than simply drawing lines at opening range extremes, this system implements the full trading methodology used by professional floor traders and market makers—including the critical concept that failed breakouts are often higher-probability setups than successful breakouts .

The Opening Range Hypothesis:

The first 30-60 minutes of trading establishes the day's value area —the price range where the majority of participants agree on fair value. This range is formed during peak information flow (overnight news digestion, gap reactions, early institutional positioning). Breakouts from this range signal directional conviction; failures to hold breakouts signal trapped participants and create exploitable reversals.

Why Opening Range Matters:

1. Information Aggregation : Opening range reflects overnight news, pre-market sentiment, and early institutional orders. It's the market's initial "consensus" on value.

2. Liquidity Concentration : Stop losses cluster just outside opening range. Breakouts trigger these stops, creating momentum. Failed breakouts trap traders, forcing reversals.

3. Statistical Persistence : Markets exhibit range expansion tendency —when price accepts above/below opening range with volume, it often extends 1.0-2.0x the opening range size before mean reversion.

4. Institutional Behavior : Large players (market makers, institutions) use opening range as reference for the day's trading plan. They fade extremes in rotation days and follow breakouts in trend days.

Historical Context:

Opening Range Breakout methodology originated in commodity futures pits (1970s-80s) where floor traders noticed consistent patterns: the first 30-60 minutes established a "fair value zone," and directional moves occurred when this zone was violated with conviction. J. Peter Steidlmayer formalized this observation in Market Profile theory, introducing the "Initial Balance" concept—the first hour (two 30-minute periods) defining market structure.

📊 OPENING RANGE CONSTRUCTION

Four ORB Timeframe Options:

1. 5-Minute ORB (0930-0935 ET):

Captures immediate market direction during "opening drive"—the explosive first few minutes when overnight orders hit the tape.

Use Case:

• Scalping strategies

• High-frequency breakout trading

• Extremely liquid instruments (ES, NQ, SPY)

Characteristics:

• Very tight range (often 0.2-0.5% of price)

• Early breakouts common (7 of 10 days break within first hour)

• Higher false breakout rate (50-60%)

• Requires sub-minute chart monitoring

Psychology: Captures panic buyers/sellers reacting to overnight news. Range is small because sample size is minimal—only 5 minutes of price discovery. Early breakouts often fail because they're driven by retail FOMO rather than institutional conviction.

2. 15-Minute ORB (0930-0945 ET):

Balances responsiveness with statistical validity. Captures opening drive plus initial reaction to that drive.

Use Case:

• Day trading strategies

• Balanced scalping/swing hybrid

• Most liquid instruments

Characteristics:

• Moderate range (0.4-0.8% of price typically)

• Breakout rate ~60% of days

• False breakout rate ~40-45%

• Good balance of opportunity and reliability

Psychology: Includes opening panic AND the first retest/consolidation. Sophisticated traders (institutions, algos) start expressing directional bias. This is the "Goldilocks" timeframe—not too reactive, not too slow.

3. 30-Minute ORB (0930-1000 ET):

Classic ORB timeframe. Default for most professional implementations.

Use Case:

• Standard intraday trading

• Position sizing for full-day trades

• All liquid instruments (equities, indices, futures)

Characteristics:

• Substantial range (0.6-1.2% of price)

• Breakout rate ~55% of days

• False breakout rate ~35-40%

• Statistical sweet spot for extensions

Psychology: Full opening auction + first institutional repositioning complete. By 10:00 AM ET, headlines are digested, early stops are hit, and "real" directional players reveal themselves. This is when institutional programs typically finish their opening positioning.

Statistical Advantage: 30-minute ORB shows highest correlation with daily range. When price breaks and holds outside 30m ORB, probability of reaching 1.0x extension (doubling the opening range) exceeds 60% historically.

4. 60-Minute ORB (0930-1030 ET) - Initial Balance:

Steidlmayer's "Initial Balance"—the foundation of Market Profile theory.

Use Case:

• Swing trading entries

• Day type classification

• Low-frequency institutional setups

Characteristics:

• Wide range (0.8-1.5% of price)

• Breakout rate ~45% of days

• False breakout rate ~25-30% (lowest)

• Best for trend day identification

Psychology: Full first hour captures A-period (0930-1000) and B-period (1000-1030). By 10:30 AM ET, all early positioning is complete. Market has "voted" on value. Subsequent price action confirms (trend day) or rejects (rotation day) this value assessment.

Initial Balance Theory:

IB represents the market's accepted value area . When price extends significantly beyond IB (>1.5x IB range), it signals a Trend Day —strong directional conviction. When price remains within 1.0x IB, it signals a Rotation Day —mean reversion environment. This classification completely changes trading strategy.

🔬 LTF PRECISION TECHNOLOGY

The Chart Timeframe Problem:

Traditional ORB indicators calculate range using the chart's current timeframe. This creates critical inaccuracies:

Example:

• You're on a 5-minute chart

• ORB period is 30 minutes (0930-1000 ET)

• Indicator sees only 6 bars (30min ÷ 5min/bar = 6 bars)

• If any 5-minute bar has extreme wick, entire ORB is distorted

The Problem Amplifies:

• On 15-minute chart with 30-minute ORB: Only 2 bars sampled

• On 30-minute chart with 30-minute ORB: Only 1 bar sampled

• Opening spike or single large wick defines entire range (invalid)

Solution: Lower Timeframe (LTF) Precision:

ORB Fusion uses `request.security_lower_tf()` to sample 1-minute bars regardless of chart timeframe:

```

For 30-minute ORB on 15-minute chart:

- Traditional method: Uses 2 bars (15min × 2 = 30min)

- LTF Precision: Requests thirty 1-minute bars, calculates true high/low

```

Why This Matters:

Scenario: ES futures, 15-minute chart, 30-minute ORB

• Traditional ORB: High = 5850.00, Low = 5842.00 (range = 8 points)

• LTF Precision ORB: High = 5848.50, Low = 5843.25 (range = 5.25 points)

Difference: 2.75 points distortion from single 15-minute wick hitting 5850.00 at 9:31 AM then immediately reversing. LTF precision filters this out by seeing it was a fleeting wick, not a sustained high.

Impact on Extensions:

With inflated range (8 points vs 5.25 points):

• 1.5x extension projects +12 points instead of +7.875 points

• Difference: 4.125 points (nearly $200 per ES contract)

• Breakout signals trigger late; extension targets unreachable

Implementation:

```pinescript

getLtfHighLow() =>

float ha = request.security_lower_tf(syminfo.tickerid, "1", high)

float la = request.security_lower_tf(syminfo.tickerid, "1", low)

```

Function returns arrays of 1-minute high/low values, then finds true maximum and minimum across all samples.

When LTF Precision Activates:

Only when chart timeframe exceeds ORB session window:

• 5-minute chart + 30-minute ORB: LTF used (chart TF > session bars needed)

• 1-minute chart + 30-minute ORB: LTF not needed (direct sampling sufficient)

Recommendation: Always enable LTF Precision unless you're on 1-minute charts. The computational overhead is negligible, and accuracy improvement is substantial.

⚖️ INITIAL BALANCE (IB) FRAMEWORK

Steidlmayer's Market Profile Innovation:

J. Peter Steidlmayer developed Market Profile in the 1980s for the Chicago Board of Trade. His key insight: market structure is best understood through time-at-price (value area) rather than just price-over-time (traditional charts).

Initial Balance Definition:

IB is the price range established during the first hour of trading, subdivided into:

• A-Period : First 30 minutes (0930-1000 ET for US equities)

• B-Period : Second 30 minutes (1000-1030 ET)

A-Period vs B-Period Comparison:

The relationship between A and B periods forecasts the day:

B-Period Expansion (Bullish):

• B-period high > A-period high

• B-period low ≥ A-period low

• Interpretation: Buyers stepping in after opening assessed

• Implication: Bullish continuation likely

• Strategy: Buy pullbacks to A-period high (now support)

B-Period Expansion (Bearish):

• B-period low < A-period low

• B-period high ≤ A-period high

• Interpretation: Sellers stepping in after opening assessed

• Implication: Bearish continuation likely

• Strategy: Sell rallies to A-period low (now resistance)

B-Period Contraction:

• B-period stays within A-period range

• Interpretation: Market indecisive, digesting A-period information

• Implication: Rotation day likely, stay range-bound

• Strategy: Fade extremes, sell high/buy low within IB

IB Extensions:

Professional traders use IB as a ruler to project price targets:

Extension Levels:

• 0.5x IB : Initial probe outside value (minor target)

• 1.0x IB : Full extension (major target for normal days)

• 1.5x IB : Trend day threshold (classifies as trending)

• 2.0x IB : Strong trend day (rare, ~10-15% of days)

Calculation:

```

IB Range = IB High - IB Low

Bull Extension 1.0x = IB High + (IB Range × 1.0)

Bear Extension 1.0x = IB Low - (IB Range × 1.0)

```

Example:

ES futures:

• IB High: 5850.00

• IB Low: 5842.00

• IB Range: 8.00 points

Extensions:

• 1.0x Bull Target: 5850 + 8 = 5858.00

• 1.5x Bull Target: 5850 + 12 = 5862.00

• 2.0x Bull Target: 5850 + 16 = 5866.00

If price reaches 5862.00 (1.5x), day is classified as Trend Day —strategy shifts from mean reversion to trend following.

📈 DAY TYPE CLASSIFICATION SYSTEM

Four Day Types (Market Profile Framework):

1. TREND DAY:

Definition: Price extends ≥1.5x IB range in one direction and stays there.

Characteristics:

• Opens and never returns to IB

• Persistent directional movement

• Volume increases as day progresses (conviction building)

• News-driven or strong institutional flow

Frequency: ~20-25% of trading days

Trading Strategy:

• DO: Follow the trend, trail stops, let winners run

• DON'T: Fade extremes, take early profits

• Key: Add to position on pullbacks to previous extension level

• Risk: Getting chopped in false trend (see Failed Breakout section)

Example: FOMC decision, payroll report, earnings surprise—anything creating one-sided conviction.

2. NORMAL DAY:

Definition: Price extends 0.5-1.5x IB, tests both sides, returns to IB.

Characteristics:

• Two-sided trading

• Extensions occur but don't persist

• Volume balanced throughout day

• Most common day type

Frequency: ~45-50% of trading days

Trading Strategy:

• DO: Take profits at extension levels, expect reversals

• DON'T: Hold for massive moves

• Key: Treat each extension as a profit-taking opportunity

• Risk: Holding too long when momentum shifts

Example: Typical day with no major catalysts—market balancing supply and demand.

3. ROTATION DAY:

Definition: Price stays within IB all day, rotating between high and low.

Characteristics:

• Never accepts outside IB

• Multiple tests of IB high/low

• Decreasing volume (no conviction)

• Classic range-bound action

Frequency: ~25-30% of trading days

Trading Strategy:

• DO: Fade extremes (sell IB high, buy IB low)

• DON'T: Chase breakouts

• Key: Enter at extremes with tight stops just outside IB

• Risk: Breakout finally occurs after multiple failures

Example: [/b> Pre-holiday trading, summer doldrums, consolidation after big move.

4. DEVELOPING:

Definition: Day type not yet determined (early in session).

Usage: Classification before 12:00 PM ET when IB extension pattern unclear.

ORB Fusion's Classification Algorithm:

```pinescript

if close > ibHigh:

ibExtension = (close - ibHigh) / ibRange

direction = "BULLISH"

else if close < ibLow:

ibExtension = (ibLow - close) / ibRange

direction = "BEARISH"

if ibExtension >= 1.5:

dayType = "TREND DAY"

else if ibExtension >= 0.5:

dayType = "NORMAL DAY"

else if close within IB:

dayType = "ROTATION DAY"

```

Why Classification Matters:

Same setup (bullish ORB breakout) has opposite implications:

• Trend Day : Hold for 2.0x extension, trail stops aggressively

• Normal Day : Take profits at 1.0x extension, watch for reversal

• Rotation Day : Fade the breakout immediately (likely false)

Knowing day type prevents catastrophic errors like fading a trend day or holding through rotation.

🚀 BREAKOUT DETECTION & CONFIRMATION

Three Confirmation Methods:

1. Close Beyond Level (Recommended):

Logic: Candle must close above ORB high (bull) or below ORB low (bear).

Why:

• Filters out wicks (temporary liquidity grabs)

• Ensures sustained acceptance above/below range

• Reduces false breakout rate by ~20-30%

Example:

• ORB High: 5850.00

• Bar high touches 5850.50 (wick above)

• Bar closes at 5848.00 (inside range)

• Result: NO breakout signal

vs.

• Bar high touches 5850.50

• Bar closes at 5851.00 (outside range)

• Result: BREAKOUT signal confirmed

Trade-off: Slightly delayed entry (wait for close) but much higher reliability.

2. Wick Beyond Level:

Logic: [/b> Any touch of ORB high/low triggers breakout.

Why:

• Earliest possible entry

• Captures aggressive momentum moves

Risk:

• High false breakout rate (60-70%)

• Stop runs trigger signals

• Requires very tight stops (difficult to manage)

Use Case: Scalping with 1-2 point profit targets where any penetration = trade.

3. Body Beyond Level:

Logic: [/b> Candle body (close vs open) must be entirely outside range.

Why:

• Strictest confirmation

• Ensures directional conviction (not just momentum)

• Lowest false breakout rate

Example: Trade-off: [/b> Very conservative—misses some valid breakouts but rarely triggers on false ones.

Volume Confirmation Layer:

All confirmation methods can require volume validation:

Volume Multiplier Logic: Rationale: [/b> True breakouts are driven by institutional activity (large size). Volume spike confirms real conviction vs. stop-run manipulation.

Statistical Impact: [/b>

• Breakouts with volume confirmation: ~65% success rate

• Breakouts without volume: ~45% success rate

• Difference: 20 percentage points edge

Implementation Note: [/b>

Volume confirmation adds complexity—you'll miss breakouts that work but lack volume. However, when targeting 1.5x+ extensions (ambitious goals), volume confirmation becomes critical because those moves require sustained institutional participation.

Recommended Settings by Strategy: [/b>

Scalping (1-2 point targets): [/b>

• Method: Close

• Volume: OFF

• Rationale: Quick in/out doesn't need perfection

Intraday Swing (5-10 point targets): [/b>

• Method: Close

• Volume: ON (1.5x multiplier)

• Rationale: Balance reliability and opportunity

Position Trading (full-day holds): [/b>

• Method: Body

• Volume: ON (2.0x multiplier)

• Rationale: Must be certain—large stops require high win rate

🔥 FAILED BREAKOUT SYSTEM

The Core Insight: [/b>

Failed breakouts are often more profitable [/b> than successful breakouts because they create trapped traders with predictable behavior.

Failed Breakout Definition: [/b>

A breakout that:

1. Initially penetrates ORB level with confirmation

2. Attracts participants (volume spike, momentum)

3. Fails to extend (stalls or immediately reverses)

4. Returns inside ORB range within N bars

Psychology of Failure: [/b>

When breakout fails:

• Breakout buyers are trapped [/b>: Bought at ORB high, now underwater

• Early longs reduce: Take profit, fearful of reversal

• Shorts smell blood: See failed breakout as reversal signal

• Result: Cascade of selling as trapped bulls exit + new shorts enter

Mirror image for failed bearish breakouts (trapped shorts cover + new longs enter).

Failure Detection Parameters: [/b>

1. Failure Confirmation Bars (default: 3): [/b>

How many bars after breakout to confirm failure?

Logic: Settings: [/b>

• 2 bars: Aggressive failure detection (more signals, more false failures)

• 3 bars Balanced (default)

• 5-10 bars: Conservative (wait for clear reversal)

Why This Matters:

Too few bars: You call "failed breakout" when price is just consolidating before next leg.

Too many bars: You miss the reversal entry (price already back in range).

2. Failure Buffer (default: 0.1 ATR): [/b>

How far inside ORB must price return to confirm failure?

Formula: Why Buffer Matters: clear rejection [/b> (not just hovering at level).

Settings: [/b>

• 0.0 ATR: No buffer, immediate failure signal

• 0.1 ATR: Small buffer (default) - filters noise

• [b>0.2-0.3 ATR: Large buffer - only dramatic failures count

Example: Reversal Entry System: [/b>

When failure confirmed, system generates complete reversal trade:

For Failed Bull Breakout (Short Reversal): [/b>

Entry: [/b> Current close when failure confirmed

Stop Loss: [/b> Extreme high since breakout + 0.10 ATR padding

Target 1: [/b> ORB High - (ORB Range × 0.5)

Target 2: Target 3: [/b> ORB High - (ORB Range × 1.5)

Example:

• ORB High: 5850, ORB Low: 5842, Range: 8 points

• Breakout to 5853, fails, reverses to 5848 (entry)

• Stop: 5853 + 1 = 5854 (6 point risk)

• T1: 5850 - 4 = 5846 (-2 points, 1:3 R:R)

• T2: 5850 - 8 = 5842 (-6 points, 1:1 R:R)

• T3: 5850 - 12 = 5838 (-10 points, 1.67:1 R:R)

[b>Why These Targets? [/b>

• T1 (0.5x ORB below high): Trapped bulls start panic

• T2 (1.0x ORB = ORB Mid): Major retracement, momentum fully reversed

• T3 (1.5x ORB): Reversal extended, now targeting opposite side

Historical Performance: [/b>

Failed breakout reversals in ORB Fusion's tracking system show:

• Win Rate: 65-75% (significantly higher than initial breakouts)

• Average Winner: 1.2x ORB range

• Average Loser: 0.5x ORB range (protected by stop at extreme)

• Expectancy: Strongly positive even with <70% win rate

Why Failed Breakouts Outperform: [/b>

1. Information Advantage: You now know what price did (failed to extend). Initial breakout trades are speculative; reversal trades are reactive to confirmed failure.

2. Trapped Participant Pressure: Every trapped bull becomes a seller. This creates sustained pressure.

3. Stop Loss Clarity: Extreme high is obvious stop (just beyond recent high). Breakout trades have ambiguous stops (ORB mid? Recent low? Too wide or too tight).

4. Mean Reversion Edge: Failed breakouts return to value (ORB mid). Initial breakouts try to escape value (harder to sustain).

Critical Insight: [/b>

"The best trade is often the one that trapped everyone else."

Failed breakouts create asymmetric opportunity because you're trading against [/b> trapped participants rather than with [/b> them. When you see a failed breakout signal, you're seeing real-time evidence that the market rejected directional conviction—that's exploitable.

📐 FIBONACCI EXTENSION SYSTEM

Six Extension Levels: [/b>

Extensions project how far price will travel after ORB breakout. Based on Fibonacci ratios + empirical market behavior.

1. 1.272x (27.2% Extension): [/b>

Formula: [/b> ORB High/Low + (ORB Range × 0.272)

Psychology: [/b> Initial probe beyond ORB. Early momentum + trapped shorts (on bull side) covering.

Probability of Reach: [/b> ~75-80% after confirmed breakout

Trading: [/b>

• First resistance/support after breakout

• Partial profit target (take 30-50% off)

• Watch for rejection here (could signal failure in progress)

Why 1.272? [/b> Related to harmonic patterns (1.272 is √1.618). Empirically, markets often stall at 25-30% extension before deciding whether to continue or fail.

2. 1.5x (50% Extension):

Formula: [/b> ORB High/Low + (ORB Range × 0.5)

Psychology: [/b> Breakout gaining conviction. Requires sustained buying/selling (not just momentum spike).

Probability of Reach: [/b> ~60-65% after confirmed breakout

Trading: [/b>

• Major partial profit (take 50-70% off)

• Move stops to breakeven

• Trail remaining position

Why 1.5x? [/b> Classic halfway point to 2.0x. Markets often consolidate here before final push. If day type is "Normal," this is likely the high/low for the day.

3. 1.618x (Golden Ratio Extension): [/b>

Formula: [/b> ORB High/Low + (ORB Range × 0.618)

Psychology: [/b> Strong directional day. Institutional conviction + retail FOMO.

Probability of Reach: [/b> ~45-50% after confirmed breakout

Trading: [/b>

• Final partial profit (close 80-90%)

• Trail remainder with wide stop (allow breathing room)

Why 1.618? [/b> Fibonacci golden ratio. Appears consistently in market geometry. When price reaches 1.618x extension, move is "mature" and reversal risk increases.

4. 2.0x (100% Extension): [/b>

Formula: ORB High/Low + (ORB Range × 1.0)

Psychology: [/b> Trend day confirmed. Opening range completely duplicated.

Probability of Reach: [/b> ~30-35% after confirmed breakout

Trading: Why 2.0x? [/b> Psychological level—range doubled. Also corresponds to typical daily ATR in many instruments (opening range ~ 0.5 ATR, daily range ~ 1.0 ATR).

5. 2.618x (Super Extension):

Formula: [/b> ORB High/Low + (ORB Range × 1.618)

Psychology: [/b> Parabolic move. News-driven or squeeze.

Probability of Reach: [/b> ~10-15% after confirmed breakout

[b>Trading: Why 2.618? [/b> Fibonacci ratio (1.618²). Rare to reach—when it does, move is extreme. Often precedes multi-day consolidation or reversal.

6. 3.0x (Extreme Extension): [/b>

Formula: [/b> ORB High/Low + (ORB Range × 2.0)

Psychology: [/b> Market melt-up/crash. Only in extreme events.

[b>Probability of Reach: [/b> <5% after confirmed breakout

Trading: [/b>

• Close immediately if reached

• These are outlier events (black swans, flash crashes, squeeze-outs)

• Holding for more is greed—take windfall profit

Why 3.0x? [/b> Triple opening range. So rare it's statistical noise. When it happens, it's headline news.

Visual Example:

ES futures, ORB 5842-5850 (8 point range), Bullish breakout:

• ORB High : 5850.00 (entry zone)

• 1.272x : 5850 + 2.18 = 5852.18 (first resistance)

• 1.5x : 5850 + 4.00 = 5854.00 (major target)

• 1.618x : 5850 + 4.94 = 5854.94 (strong target)

• 2.0x : 5850 + 8.00 = 5858.00 (trend day)

• 2.618x : 5850 + 12.94 = 5862.94 (extreme)

• 3.0x : 5850 + 16.00 = 5866.00 (parabolic)

Profit-Taking Strategy:

Optimal scaling out at extensions:

• Breakout entry at 5850.50

• 30% off at 1.272x (5852.18) → +1.68 points

• 40% off at 1.5x (5854.00) → +3.50 points

• 20% off at 1.618x (5854.94) → +4.44 points

• 10% off at 2.0x (5858.00) → +7.50 points

[b>Average Exit: Conclusion: [/b> Scaling out at extensions produces 40% higher expectancy than holding for home runs.

📊 GAP ANALYSIS & FILL PSYCHOLOGY

[b>Gap Definition: [/b>

Price discontinuity between previous close and current open:

• Gap Up : Open > Previous Close + noise threshold (0.1 ATR)

• Gap Down : Open < Previous Close - noise threshold

Why Gaps Matter: [/b>

Gaps represent unfilled orders [/b>. When market gaps up, all limit buy orders between yesterday's close and today's open are never filled. Those buyers are "left behind." Psychology: they wait for price to return ("fill the gap") so they can enter. This creates magnetic pull [/b> toward gap level.

Gap Fill Statistics (Empirical): [/b>

• Gaps <0.5% [/b>: 85-90% fill within same day

• Gaps 0.5-1.0% [/b>: 70-75% fill within same day, 90%+ within week

• Gaps >1.0% [/b>: 50-60% fill within same day (major news often prevents fill)

Gap Fill Strategy: [/b>

Setup 1: Gap-and-Go

Gap opens, extends away from gap (doesn't fill).

• ORB confirms direction away from gap

• Trade WITH ORB breakout direction

• Expectation: Gap won't fill today (momentum too strong)

Setup 2: Gap-Fill Fade

Gap opens, but fails to extend. Price drifts back toward gap.

• ORB breakout TOWARD gap (not away)

• Trade toward gap fill level

• Target: Previous close (gap fill complete)

Setup 3: Gap-Fill Rejection

Gap fills (touches previous close) then rejects.

• ORB breakout AWAY from gap after fill

• Trade away from gap direction

• Thesis: Gap filled (orders executed), now resume original direction

[b>Example: Scenario A (Gap-and-Go):

• ORB breaks upward to $454 (away from gap)

• Trade: LONG breakout, expect continued rally

• Gap becomes support ($452)

Scenario B (Gap-Fill):

• ORB breaks downward through $452.50 (toward gap)

• Trade: SHORT toward gap fill at $450.00

• Target: $450.00 (gap filled), close position

Scenario C (Gap-Fill Rejection):

• Price drifts to $450.00 (gap filled) early in session

• ORB establishes $450-$451 after gap fill

• ORB breaks upward to $451.50

• Trade: LONG breakout (gap is filled, now resume rally)

ORB Fusion Integration: [/b>

Dashboard shows:

• Gap type (Up/Down/None)

• Gap size (percentage)

• Gap fill status (Filled ✓ / Open)

This informs setup confidence:

• ORB breakout AWAY from unfilled gap: +10% confidence (gap becomes support/resistance)

• ORB breakout TOWARD unfilled gap: -10% confidence (gap fill may override ORB)

[b>📈 VWAP & INSTITUTIONAL BIAS [/b>

[b>Volume-Weighted Average Price (VWAP): [/b>

Average price weighted by volume at each price level. Represents true "average" cost for the day.

[b>Calculation: Institutional Benchmark [/b>: Institutions (mutual funds, pension funds) use VWAP as performance benchmark. If they buy above VWAP, they underperformed; below VWAP, they outperformed.

2. [b>Algorithmic Target [/b>: Many algos are programmed to buy below VWAP and sell above VWAP to achieve "fair" execution.

3. [b>Support/Resistance [/b>: VWAP acts as dynamic support (price above) or resistance (price below).

[b>VWAP Bands (Standard Deviations): [/b>

• [b>1σ Band [/b>: VWAP ± 1 standard deviation

- Contains ~68% of volume

- Normal trading range

- Bounces common

• [b>2σ Band [/b>: VWAP ± 2 standard deviations

- Contains ~95% of volume

- Extreme extension

- Mean reversion likely

ORB + VWAP Confluence: [/b>

Highest-probability setups occur when ORB and VWAP align:

Bullish Confluence: [/b>

• ORB breakout upward (bullish signal)

• Price above VWAP (institutional buying)

• Confidence boost: +15%

Bearish Confluence: [/b>

• ORB breakout downward (bearish signal)

• Price below VWAP (institutional selling)

• Confidence boost: +15%

[b>Divergence Warning:

• ORB breakout upward BUT price below VWAP

• Conflict: Breakout says "buy," VWAP says "sell"

• Confidence penalty: -10%

• Interpretation: Retail buying but institutions not participating (lower quality breakout)

📊 MOMENTUM CONTEXT SYSTEM

[b>Innovation: Candle Coloring by Position

Rather than fixed support/resistance lines, ORB Fusion colors candles based on their [b>relationship to ORB :

[b>Three Zones: [/b>

1. Inside ORB (Blue Boxes): [/b>

[b>Calculation:

• Darker blue: Near extremes of ORB (potential breakout imminent)

• Lighter blue: Near ORB mid (consolidation)

[b>Trading: [/b> Coiled spring—await breakout.

[b>2. Above ORB (Green Boxes):

[b>Calculation: 3. Below ORB (Red Boxes):

Mirror of above ORB logic.

[b>Special Contexts: [/b>

[b>Breakout Bar (Darkest Green/Red): [/b>

The specific bar where breakout occurs gets maximum color intensity regardless of distance. This highlights the pivotal moment.

[b>Failed Breakout Bar (Orange/Warning): [/b>

When failed breakout is confirmed, that bar gets orange/warning color. Visual alert: "reversal opportunity here."

[b>Near Extension (Cyan/Magenta Tint): [/b>

When price is within 0.5 ATR of an extension level, candle gets tinted cyan (bull) or magenta (bear). Indicates "target approaching—prepare to take profit."

[b>Why Visual Context? [/b>

Traditional indicators show lines. ORB Fusion shows [b>context-aware momentum [/b>. Glance at chart:

• Lots of blue? Consolidation day (fade extremes).

• Progressive green? Trend day (follow).

• Green then orange? Failed breakout (reversal setup).

This visual language communicates market state instantly—no interpretation needed.

🎯 TRADE SETUP GENERATION & GRADING [/b>

[b>Algorithmic Setup Detection: [/b>

ORB Fusion continuously evaluates market state and generates current best trade setup with:

• Action (LONG / SHORT / FADE HIGH / FADE LOW / WAIT)

• Entry price

• Stop loss

• Three targets

• Risk:Reward ratio

• Confidence score (0-100)

• Grade (A+ to D)

[b>Setup Types: [/b>

[b>1. ORB LONG (Bullish Breakout): [/b>

[b>Trigger: [/b>

• Bullish ORB breakout confirmed

• Not failed

[b>Parameters:

• Entry: Current close

• Stop: ORB mid (protects against failure)

• T1: ORB High + 0.5x range (1.5x extension)

• T2: ORB High + 1.0x range (2.0x extension)

• T3: ORB High + 1.618x range (2.618x extension)

[b>Confidence Scoring:

[b>Trigger: [/b>

• Bearish breakout occurred

• Failed (returned inside ORB)

[b>Parameters: [/b>

• Entry: Close when failure confirmed

• Stop: Extreme low since breakout + 0.10 ATR

• T1: ORB Low + 0.5x range

• T2: ORB Low + 1.0x range (ORB mid)

• T3: ORB Low + 1.5x range

[b>Confidence Scoring:

[b>Trigger:

• Inside ORB

• Close > ORB mid (near high)

[b>Parameters: [/b>

• Entry: ORB High (limit order)

• Stop: ORB High + 0.2x range

• T1: ORB Mid

• T2: ORB Low

[b>Confidence Scoring: [/b>

Base: 40 points (lower base—range fading is lower probability than breakout/reversal)

[b>Use Case: [/b> Rotation days. Not recommended on normal/trend days.

[b>6. FADE LOW (Range Trade):

Mirror of FADE HIGH.

[b>7. WAIT:

[b>Trigger: [/b>

• ORB not complete yet OR

• No clear setup (price in no-man's-land)

[b>Action: [/b> Observe, don't trade.

[b>Confidence: [/b> 0 points

[b>Grading System:

```

Confidence → Grade

85-100 → A+

75-84 → A

65-74 → B+

55-64 → B

45-54 → C

0-44 → D

```

[b>Grade Interpretation: [/b>

• [b>A+ / A: High probability setup. Take these trades.

• [b>B+ / B [/b>: Decent setup. Trade if fits system rules.

• [b>C [/b>: Marginal setup. Only if very experienced.

• [b>D [/b>: Poor setup or no setup. Don't trade.

[b>Example Scenario: [/b>

ES futures:

• ORB: 5842-5850 (8 point range)

• Bullish breakout to 5851 confirmed

• Volume: 2.0x average (confirmed)

• VWAP: 5845 (price above VWAP ✓)

• Day type: Developing (too early, no bonus)

• Gap: None

[b>Setup: [/b>

• Action: LONG

• Entry: 5851

• Stop: 5846 (ORB mid, -5 point risk)

• T1: 5854 (+3 points, 1:0.6 R:R)

• T2: 5858 (+7 points, 1:1.4 R:R)

• T3: 5862.94 (+11.94 points, 1:2.4 R:R)

[b>Confidence: LONG with 55% confidence.

Interpretation: Solid setup, not perfect. Trade it if your system allows B-grade signals.

[b>📊 STATISTICS TRACKING & PERFORMANCE ANALYSIS [/b>

[b>Real-Time Performance Metrics: [/b>

ORB Fusion tracks comprehensive statistics over user-defined lookback (default 50 days):

[b>Breakout Performance: [/b>

• [b>Bull Breakouts: [/b> Total count, wins, losses, win rate

• [b>Bear Breakouts: [/b> Total count, wins, losses, win rate

[b>Win Definition: [/b> Breakout reaches ≥1.0x extension (doubles the opening range) before end of day.

[b>Example: [/b>

• ORB: 5842-5850 (8 points)

• Bull breakout at 5851

• Reaches 5858 (1.0x extension) by close

• Result: WIN

[b>Failed Breakout Performance: [/b>

• [b>Total Failed Breakouts [/b>: Count of breakouts that failed

• [b>Reversal Wins [/b>: Count where reversal trade reached target

• [b>Failed Reversal Win Rate [/b>: Wins / Total Failed

[b>Win Definition for Reversals: [/b>

• Failed bull → reversal short reaches ORB mid

• Failed bear → reversal long reaches ORB mid

[b>Extension Tracking: [/b>

• [b>Average Extension Reached [/b>: Mean of maximum extension achieved across all breakout days

• [b>Max Extension Overall [/b>: Largest extension ever achieved in lookback period

[b>Example: 🎨 THREE DISPLAY MODES

[b>Design Philosophy: [/b>

Not all traders need all features. Beginners want simplicity. Professionals want everything. ORB Fusion adapts.

[b>SIMPLE MODE: [/b>

[b>Shows: [/b>

• Primary ORB levels (High, Mid, Low)

• ORB box

• Breakout signals (triangles)

• Failed breakout signals (crosses)

• Basic dashboard (ORB status, breakout status, setup)

• VWAP

[b>Hides: [/b>

• Session ORBs (Asian, London, NY)

• IB levels and extensions

• ORB extensions beyond basic levels

• Gap analysis visuals

• Statistics dashboard

• Momentum candle coloring

• Narrative dashboard

[b>Use Case: [/b>

• Traders who want clean chart

• Focus on core ORB concept only

• Mobile trading (less screen space)

[b>STANDARD MODE:

[b>Shows Everything in Simple Plus: [/b>

• Session ORBs (Asian, London, NY)

• IB levels (high, low, mid)

• IB extensions

• ORB extensions (1.272x, 1.5x, 1.618x, 2.0x)

• Gap analysis and fill targets

• VWAP bands (1σ and 2σ)

• Momentum candle coloring

• Context section in dashboard

• Narrative dashboard

[b>Hides: [/b>

• Advanced extensions (2.618x, 3.0x)

• Detailed statistics dashboard

[b>Use Case: [/b>

• Most traders

• Balance between information and clarity

• Covers 90% of use cases

[b>ADVANCED MODE:

[b>Shows Everything:

• All session ORBs

• All IB levels and extensions

• All ORB extensions (including 2.618x and 3.0x)

• Full gap analysis

• VWAP with both 1σ and 2σ bands

• Momentum candle coloring

• Complete statistics dashboard

• Narrative dashboard

• All context metrics

[b>Use Case: [/b>

• Professional traders

• System developers

• Those who want maximum information density

[b>Switching Modes: [/b>

Single dropdown input: "Display Mode" → Simple / Standard / Advanced

Entire indicator adapts instantly. No need to toggle 20 individual settings.

📖 NARRATIVE DASHBOARD

[b>Innovation: Plain-English Market State [/b>

Most indicators show data. ORB Fusion explains what the data [b>means [/b>.

[b>Narrative Components: [/b>

[b>1. Phase: [/b>

• "📍 Building ORB..." (during ORB session)

• "📊 Trading Phase" (after ORB complete)

• "⏳ Pre-Market" (before ORB session)

[b>2. Status (Current Observation): [/b>

• "⚠️ Failed breakout - reversal likely"

• "🚀 Bullish momentum in play"

• "📉 Bearish momentum in play"

• "⚖️ Consolidating in range"

• "👀 Monitoring for setup"

[b>3. Next Level:

Tells you what to watch for:

• "🎯 1.5x @ 5854.00" (next extension target)

• "Watch ORB levels" (inside range, await breakout)

[b>4. Setup: [/b>

Current trade setup + grade:

• "LONG " (bullish breakout, A-grade)

• "🔥 SHORT REVERSAL " (failed bull breakout, A+-grade)

• "WAIT " (no setup)

[b>5. Reason: [/b>

Why this setup exists:

• "ORB Bullish Breakout"

• "Failed Bear Breakout - High Probability Reversal"

• "Range Fade - Near High"

[b>6. Tip (Market Insight):

Contextual advice:

• "🔥 TREND DAY - Trail stops" (day type is trending)

• "🔄 ROTATION - Fade extremes" (day type is rotating)

• "📊 Gap unfilled - magnet level" (gap creates target)

• "📈 Normal conditions" (no special context)

[b>Example Narrative:

```

📖 ORB Narrative

━━━━━━━━━━━━━━━━

Phase | 📊 Trading Phase

Status | 🚀 Bullish momentum in play

Next | 🎯 1.5x @ 5854.00

📈 Setup | LONG

Reason | ORB Bullish Breakout

💡 Tip | 🔥 TREND DAY - Trail stops

```

[b>Glance Interpretation: [/b>

"We're in trading phase. Bullish breakout happened (momentum in play). Next target is 1.5x extension at 5854. Current setup is LONG with A-grade. It's a trend day, so trail stops (don't take early profits)."

Complete market state communicated in 6 lines. No interpretation needed.

[b>Why This Matters:

Beginner traders struggle with "So what?" question. Indicators show lines and signals, but what does it mean [/b>? Narrative dashboard bridges this gap.

Professional traders benefit too—rapid context assessment during fast-moving markets. No time to analyze; glance at narrative, get action plan.

🔔 INTELLIGENT ALERT SYSTEM

[b>Four Alert Types: [/b>

[b>1. Breakout Alert: [/b>

[b>Trigger: [/b> ORB breakout confirmed (bull or bear)

[b>Message: [/b>

```

🚀 ORB BULLISH BREAKOUT

Price: 5851.00

Volume Confirmed

Grade: A

```

[b>Frequency: [/b> Once per bar (prevents spam)

[b>2. Failed Breakout Alert: [/b>

[b>Trigger: [/b> Breakout fails, reversal setup generated

[b>Message: [/b>

```

🔥 FAILED BULLISH BREAKOUT!

HIGH PROBABILITY SHORT REVERSAL

Entry: 5848.00

Stop: 5854.00

T1: 5846.00

T2: 5842.00

Historical Win Rate: 73%

```

[b>Why Comprehensive? [/b> Failed breakout alerts include complete trade plan. You can execute immediately from alert—no need to check chart.

[b>3. Extension Alert:

[b>Trigger: [/b> Price reaches extension level for first time

[b>Message: [/b>

```

🎯 Bull Extension 1.5x reached @ 5854.00

```

[b>Use: [/b> Profit-taking reminder. When extension hit, consider scaling out.

[b>4. IB Break Alert: [/b>

[b>Trigger: [/b> Price breaks above IB high or below IB low

[b>Message: [/b>

```

📊 IB HIGH BROKEN - Potential Trend Day

```

[b>Use: [/b> Day type classification. IB break suggests trend day developing—adjust strategy to trend-following mode.

[b>Alert Management: [/b>

Each alert type can be enabled/disabled independently. Prevents notification overload.

[b>Cooldown Logic: [/b>

Alerts won't fire if same alert type triggered within last bar. Prevents:

• "Breakout" alert every tick during choppy breakout

• Multiple "extension" alerts if price oscillates at level

Ensures: One clean alert per event.

⚙️ KEY PARAMETERS EXPLAINED

[b>Opening Range Settings: [/b>

• [b>ORB Timeframe [/b> (5/15/30/60 min): Duration of opening range window